Lecture - 1 Islamic Financial System

29

-

Upload

abushahadat -

Category

Documents

-

view

645 -

download

2

Transcript of Lecture - 1 Islamic Financial System

Islamic Financial System

Introduction

Concept of Financial System

• Financial system can be defined as processes and procedures used by a firm's management to exercise financial control and accountability.

• The principal role of a financial system is to bring together economic agents with surplus financial resources and those with net financial needs.

• The parties can be brought together directly or indirectly. • The parties with excess financial resources directly finance

those with financial needs are known as direct finance. • If the parties with indirectly finance with financial needs

through intermediaries are known as indirect finance.

Structure of Financial System

The main constituents of financial system are:• 1. Money• 2. Financial Instruments• 3. Financial Market• 4. Financial Institutions• 5. Central Bank

• Financial Institutions: The modern name of Financial Intermediary (FI), because it mediates or stands between users and providers of Fund and helps transfer of funds from one to another. The financial system helps production, capital-accumulation, and growth by• Encouraging savings,• Mobilizing them, and • Allocating them among the alternative uses and users.

Structure of Financial System

• Financial Instruments:• bank deposits, life insurance policies, mutual fund unit

certificates.

• Share of bank is a secondary instrument.

• Financial Markets: • Financial markets are ones in which funds are transferred

from those who have excess funds available to those who have a shortage.

Role of Financial System in an Economy

1. The saving function provides a potentially profitable and

relatively low- risk outlet for the savings of the people;

2. liquidity aspect provides a means of raising funds by converting

securities and financial assets in the form of cash;

3. payment technique provides mechanism for making payments for

purchase of goods and services to meet the needs;

4. policy determination provides a channel for Government Policy

to achieve the goals of high employment, low inflation, economic

growth and stability;

Role of Financial System in an Economy

5. wealth creation provides means to preserve purchasing power until the resource is needed at a future date for spending on goods and services;

6. credit supply provides a continuing supply of credits for business, customers and government to support both consumption and investment;

7. risk avoidance provides means to protect business, consumers and government against risks to people, property and in come;

8. investment opportunities provides opportunities for investment of surplus funds in various profitable as well as risk- controlled sectors of the economy for equitable mobilization of economic resources and production of essential commodities to maintain a just living standard of the people of the society, etc.

Islamic Financial System

• Islamic finance is emerging as a rapidly growing part of the financial sector in the Islamic world.

• Islamic finance is not restricted to Islamic countries, but is spreading wherever there is a sizable Muslim community.

• The Islamic financial system is founded on the absolute prohibition of the payment or receipt of any predetermined, guaranteed rate of return.

• This closes the door to the concept of interest and precludes the use of debt-based instruments.

• The system encourages risk-sharing, promotes entrepreneurship, discourages speculative behavior, and emphasizes the sanctity of contracts.

Nature and Objectives of the Islamic Financial System

• Nature:• absence of interest- based financial institutions/transactions,

doubtful transactions,

• stocks of companies dealing in unlawful activities,

• unethical or immoral transactions such as market manipulations, insider trading, short- selling, etc.

• Objectives:• based on Islamic Law, Shariah, which is to be treated as an

important vehicle to transfer funds from the surplus to the deficit units.

Fundamentals of Islamic finance

• The term “Islamic Finance” refers to a system of financial activity that is consistent with Islamic law (Shariah) principles and guided by Islamic economics.

• Islamic law prohibits usury, the collection and payment of interest, also commonly called riba in Islamic discourse.

• Islamic law prohibits investing in businesses that are considered unlawful, or haraam.

Typology of Islamic financial products

Profit sharing financing products:

Musharakah ةآراشم

• Equity participation, investment and management from all partners; • profits are shared according to a pre-agreed ratio;• losses according to equity contributions.

Mudarabah ةبراضم

• A profit-sharing partnership to which one contributes the capital and the other the entrepreneurship; or

• the bank provides the capital, the customer manages the project. • Profit is shared according to a pre-agreed ratio

Qard Hasan نسح

• Charitable loans free of interest and profit-sharing margins, repayment by installments.

• A modest service charge is permissible.

Wakalah ةالآو

• An authorization to the bank to conduct some business on the customer’s behalf

Hawalah ةلاوح

• An agreement by the bank to undertake some of the liabilities of the customer for which the bank receives a fee.

• When the liabilities mature the customer pays back the bank

(1) Financing products

Typology of Islamic financial products

Advance purchase financing products:

Murabahah ةحبارم

• A sales contract between a bank and its customers, mostly for trade financing.

• The bank purchases goods ordered by the customer; • Customer pays the original price plus a profit margin agreed upon by the

two parties. • Repayment by installments within a specified period

Istithna’ ءانثتسإ

• A sales contract between bank and customer where the customer specifies goods to be made or shipped,

• Which the bank then sells to the customer according to a pre-agreed arrangement.

• Prices and installment schedules are mutually agreed upon in advance.

Mu’ajjal Bai Salam

عيب لجؤم

• Purchase with deferred delivery; • A sales contract where the price is paid in advance by the bank• the goods are delivered later by the customer to a designee

Typology of Islamic financial products

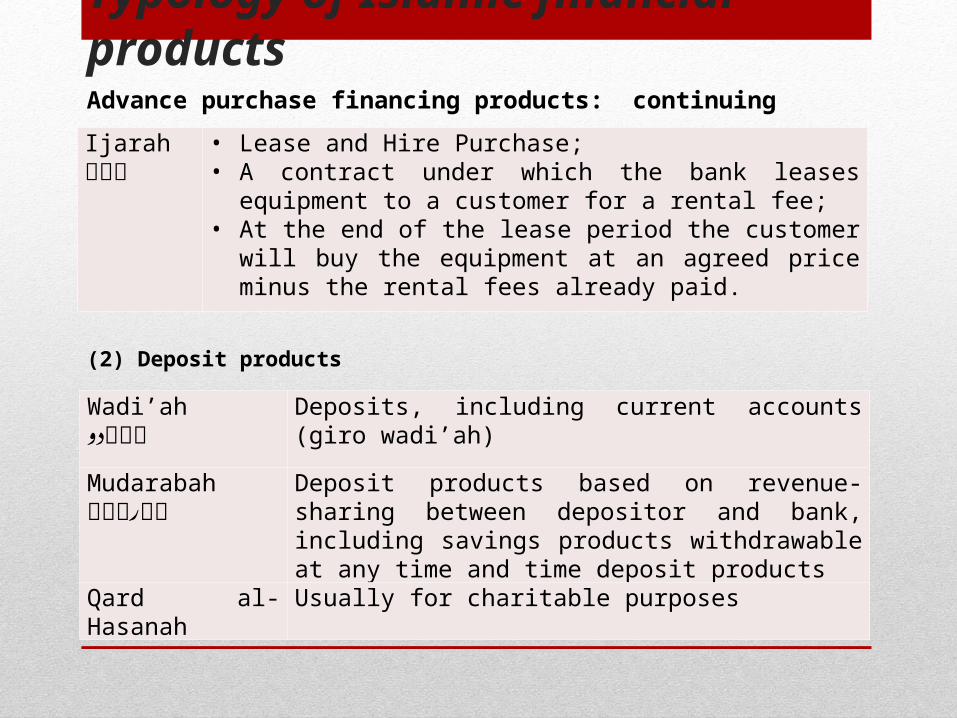

Wadi’ah ةعيدو

Deposits, including current accounts (giro wadi’ah)

Mudarabah ةبراضم

Deposit products based on revenue-sharing between depositor and bank, including savings products withdrawable at any time and time deposit products

Qard al-Hasanah Usually for charitable purposes

(2) Deposit products

Ijarah اجآ

• Lease and Hire Purchase; • A contract under which the bank leases equipment to a customer

for a rental fee; • At the end of the lease period the customer will buy the

equipment at an agreed price minus the rental fees already paid.

Advance purchase financing products: continuing

Typology of Islamic financial products

Tadamun, Takaful -لفاكت Islamic insurance with joint risk-sharing نملضت

Baitul Qirad ضارقإلا تيب

House of loans

Kafil ليفآ Guarantor

Infaq قلفنإ Expenditure

Mudharib براضم The project in a mudarabah contract

Shirkah -ةآرش Partnership ةآراشم

Rahn نهر Collateral agreement

Sadaqaat تاقدص Worship

(3) Insurance products

Tadamun, Takaful -نملضت لفاكت

Islamic insurance with joint risk-sharing

(4) Selected Islamic banking terminology

Typology of Islamic financial products

(4) Selected Islamic banking terminology (continuing)

Shar'iah ع Islamic law ةعيرش

Shirakah fi al-uqood ةآارش يف دوقعلا

Voluntary contractual agreement for joint investment and the sharing of profits and risks.

Takaful نملضت Solidarity, mutual support as the basis of insurance

Wakil ليآو Agent

Zakat ةاآز Obligatory charity, Islamic tax

Principles of an Islamic financial system

• Islamic financial system is a set of rules and laws, collectively referred to as shariah,

• Shariah originates from the rules dictated by the Quran and its practices, and explanations rendered (more commonly known as Sunnah) by the Prophet Muhammad.

• Further rules is provided by scholars in Islamic jurisprudence within the framework of the Quran and Sunnah.

Principles of an Islamic financial system

1. Prohibition of interest.

• riba, a term literally meaning "an excess" and interpreted as "any unjustifiable increase of capital whether in loans or sales".

• More precisely, any positive, fixed, predetermined rate tied to the maturity and the amount of principal is considered riba and is prohibited.

2. Risk sharing.

1. As interest is prohibited, suppliers of funds become investors instead of creditors.

2. The provider of financial capital and the entrepreneur share business risks in return for shares of the profits.

• Money as "potential" capital.

• It becomes actual capital only when it joins hands with other resources to undertake a productive activity.

• Islam recognizes the time value of money, but only when it acts as capital, not when it is "potential" capital.

Principles of an Islamic financial system

4. Prohibition of speculative behavior.

• An Islamic financial system discourages hoarding

• Prohibits transactions featuring extreme uncertainties, gambling, and risks.

5. Sanctity of contracts.

• Islam upholds contractual obligations and the disclosure of information as a sacred duty.

• This feature is intended to reduce the risk of asymmetric information and moral hazard.

6. Shariah-approved activities.

• Only those business activities that do not violate the rules of shariah qualify for investment.

• For example, any investment in businesses dealing with alcohol, gambling, and casinos would be prohibited.

Basic Islamic financial instruments

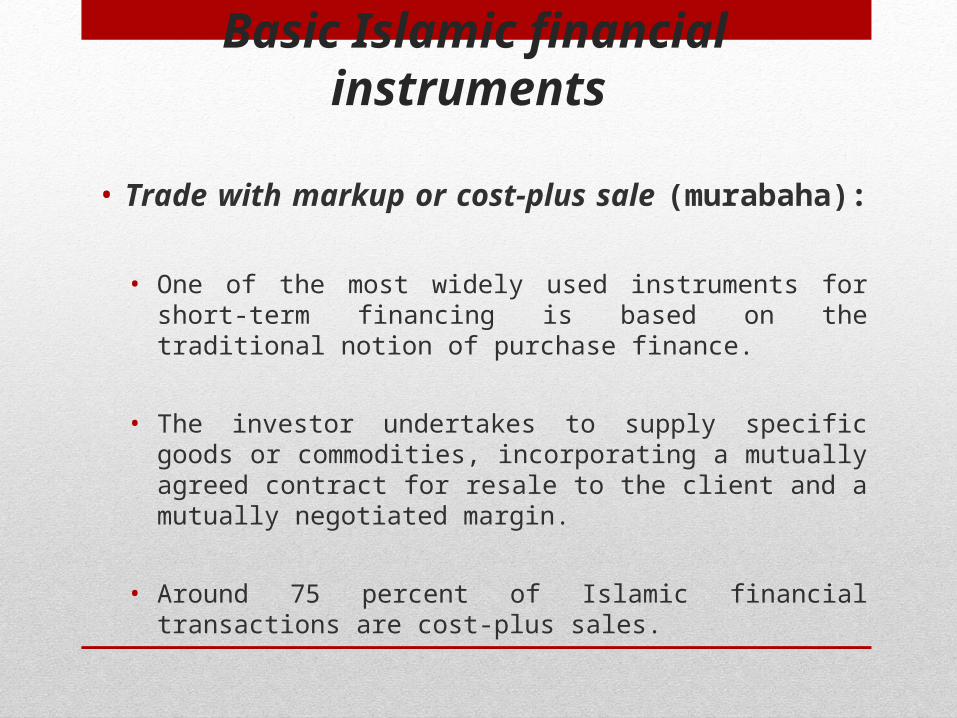

• Trade with markup or cost-plus sale (murabaha):

• One of the most widely used instruments for short-term financing is based on the traditional notion of purchase finance.

• The investor undertakes to supply specific goods or commodities, incorporating a mutually agreed contract for resale to the client and a mutually negotiated margin.

• Around 75 percent of Islamic financial transactions are cost-plus sales.

Basic Islamic financial instruments

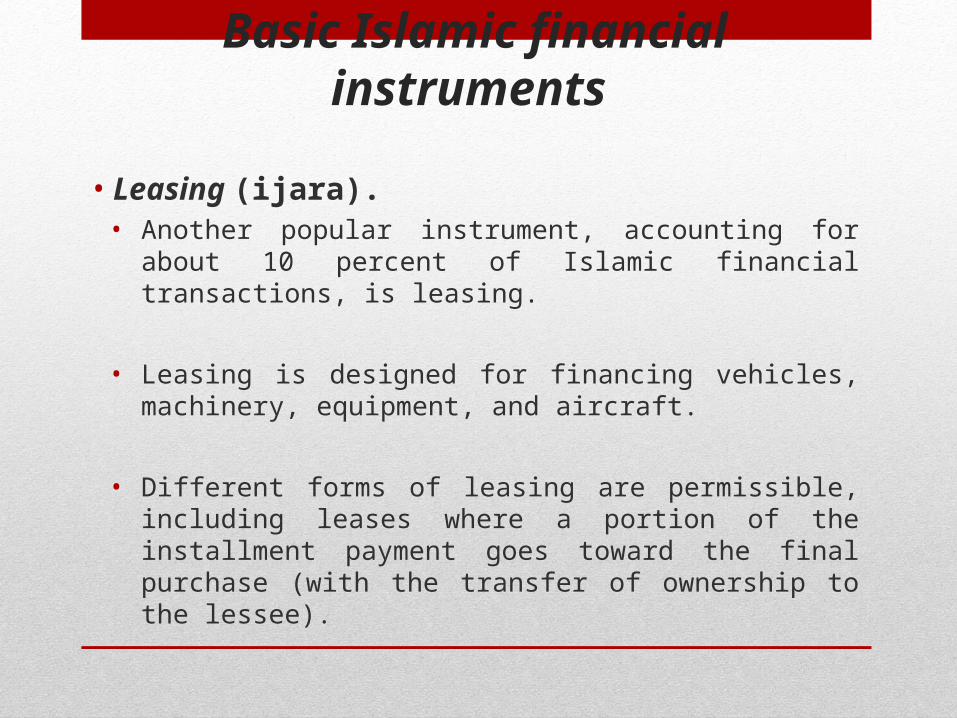

• Leasing (ijara). • Another popular instrument, accounting for about 10

percent of Islamic financial transactions, is leasing.

• Leasing is designed for financing vehicles, machinery, equipment, and aircraft.

• Different forms of leasing are permissible, including leases where a portion of the installment payment goes toward the final purchase (with the transfer of ownership to the lessee).

Basic Islamic financial instruments

• Profit-sharing agreement (mudaraba).

• This is identical to an investment fund in which managers handle a pool of funds.

• The agent-manager has relatively limited liability while having sufficient incentives to perform.

• The capital is invested in broadly defined activities, and the terms of profit and risk sharing are customized for each investment.

• The maturity structure ranges from short to medium term and is more suitable for trade activities.

Basic Islamic financial instruments

• Equity participation (musharaka).

• This is analogous to a classical joint venture.

• Both entrepreneur and investor contribute to the capital of the operation in varying degrees and agree to share the returns in proportions agreed to in advance.

• Traditionally, this form of transaction has been used for financing fixed assets and working capital of medium- and long-term duration.

Basic Islamic financial instruments

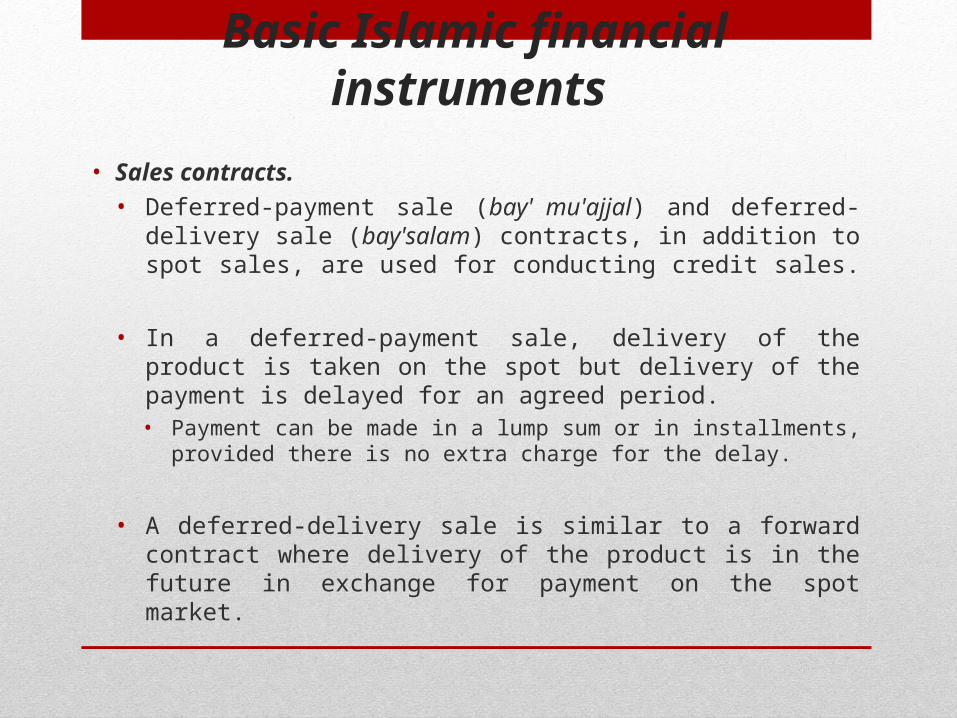

• Sales contracts.

• Deferred-payment sale (bay' mu'ajjal) and deferred-delivery sale (bay'salam) contracts, in addition to spot sales, are used for conducting credit sales.

• In a deferred-payment sale, delivery of the product is taken on the spot but delivery of the payment is delayed for an agreed period. • Payment can be made in a lump sum or in installments, provided there

is no extra charge for the delay.

• A deferred-delivery sale is similar to a forward contract where delivery of the product is in the future in exchange for payment on the spot market.

Islamic versus Conventional Financial Systems

Basis of Differences CFS IFS

Religious Belief Secular and separates religion from other parts of human life

Belief in unity of God and relates this belief to economic life of a man.

Freedom of Economic activity

• In socialism govt. enjoys economic freedom

• In capitalism individuals enjoys freedom.

Restrictive freedom is allowed in the light of Shariah both by the Govt. & / or individuals.

Ownership of means

• In Socialism - state ownership is recognized.

• In capitalism – individual ownership is recognized.

• Allah is the exclusive owner. • Man is the caretaker of the

property.

Islamic versus Conventional Financial Systems

Basis of Differences CFS IFS

Goals of financial system

• In socialism - profit of the society,

• In capitalism - Individuals profit.

• Welfare of both here and hereafter.

Competition • In socialism – No competition

• In capitalism – logical & unethical competition

• Logical competition and financial cooperation.

Basis of economic system

• Capitalism – Unequal riba or interest

• Interest free, • Zakat & • Compensation based.

Sources of the system

• Intellectual’s brain storming of the economic problems of men’s life.

• Devine book ‘Al Quran’ & prophet’s speeches.

Islamic versus Conventional Financial Systems

Basis of Differences CFS IFS

Result Capitalism concentration of income & economic power in few hands inefficiency.

Maximum & equitable distribution of economic opportunities and higher production in the society.

Social & environmental welfare

Do not consider the social & environmental welfare.

Ensure social & environmental welfare.

Owner exception in respect of investment.

Dividend or part of profit in case of equity financing.

Part of profit or loss.

Lender or bank’s expectation in terms of debt financing

Interest Profit or loss sharing.

Modes of investment Loan, overdraft & cash credit. Mudarabah, musharaka, murabaha etc.

Islamic versus Conventional Financial Systems

Basis of Differences CFS IFS

Wealth distribution Socialism – equal Equitable

Basis of economic system

Capitalism – Unequal riba or interest

Interest free, Zakat & compensation based.

Sources of the system Intellectual’s brain storming of the economic problems of men’s life.

Devine book ‘Al Quran’ & prophet’s speeches.

Result Capitalism concentration of income & economic power in few hands inefficiency.

Maximum & equitable distribution of economic opportunities and higher production in the society.

Islamic versus Conventional Financial Systems

Basis of Differences CFS IFS

Social & environmental welfare

Do not consider the social & environmental welfare.

Ensure social & environmental welfare.

Owner exception in respect of investment.

Dividend or part of profit in case of equity financing.

Part of profit or loss.

Lender or bank’s expectation in terms of debt financing

Interest Profit or loss sharing.

Modes of investment Loan, overdraft & cash credit.

Mudarabah, musharaka, murabaha etc.