Learning Objectives

40

C13 - 1 Learning Objectives Power Notes 1. Corporate Income Taxes 2. Unusual Income Statement Items 3. Earnings Per Common Share 4. Reporting Stockholders’ Equity 5. Comprehensive Income 6. Accounting for Investment in Stocks 7. Business Combinations 8. Financial Analysis and Interpretation Chapter 13 C13 Corporations: Income and Taxes, Corporations: Income and Taxes, Stockholders’ Equity, Investments in Stoc Stockholders’ Equity, Investments in Stoc

-

Upload

drake-vincent -

Category

Documents

-

view

26 -

download

0

description

Power Notes. Chapter 13. Corporations: Income and Taxes, Stockholders’ Equity, Investments in Stocks. 1.Corporate Income Taxes 2.Unusual Income Statement Items 3.Earnings Per Common Share 4.Reporting Stockholders’ Equity 5.Comprehensive Income - PowerPoint PPT Presentation

Transcript of Learning Objectives

C13 - 1

Learning Objectives

Power Notes

1. Corporate Income Taxes

2. Unusual Income Statement Items

3. Earnings Per Common Share

4. Reporting Stockholders’ Equity

5. Comprehensive Income

6. Accounting for Investment in Stocks

7. Business Combinations

8. Financial Analysis and Interpretation

Chapter 13

C13

Corporations: Income and Taxes, Corporations: Income and Taxes, Stockholders’ Equity, Investments in StocksStockholders’ Equity, Investments in Stocks

C13 - 2

• Corporate Income Taxes• Unusual Income Statement Items• Earnings Per Common Share• Reporting Stockholders’ Equity• Long-Term Stock Investments• Business Combinations• Price-Earnings Ratio

Slide # Power Note Topics

31016222836

38 Note: To select a topic, type the slide # and press Enter.

Power NotesChapter 13 Corporations: Income and Taxes, Corporations: Income and Taxes, Stockholders’ Equity, Investments in StocksStockholders’ Equity, Investments in Stocks

C13 - 3

Corporate Income TaxesCorporate Income Taxes

Corporations are taxable entities that must pay income taxes.

Because income tax is often a significant amount, it is reported as a special deduction.

Taxable income is determined according to tax laws which are often different from income before income tax according to GAAP.

Differences in tax law and GAAP create some temporary differences that reverse in later years.

Temporary differences do not change or reduce the total amount of tax paid, they affect only the timing of when the taxes are paid.

C13 - 4

Temporary Differences in Reporting RevenuesTemporary Differences in Reporting Revenues

Report NowReport Now Taxable LaterTaxable Later

Report LaterReport Later Taxable NowTaxable Now

Example: Income reporting methods.

Point-of-Sale Method

Installment Method

FinancialReporting

TaxReporting

Example: Cash collected in advance.

WhenEarned

WhenCollected

RevenueReporting

C13 - 5

Temporary Differences in Reporting ExpensesTemporary Differences in Reporting Expenses

Deduct NowDeduct Now Deduct LaterDeduct Later

Deduct SlowerDeduct Slower Deduct FasterDeduct Faster

Example: Product warranty expense.

WhenEstimated

WhenPaid

FinancialReporting

TaxReporting

Example: Methodsof depreciation.

Straight-LineMethod

MACRSMethod

ExpenseDeductions

C13 - 6

DateDate DescriptionDescription DebitDebit CreditCredit

Income Tax AccountingIncome Tax Accounting

Income Tax Expense 120,000Income Tax Payable 40,000Deferred Income Tax Payable 80,000

Deferred Income Tax Payable 48,000 Income Tax Payable 48,000

1st Yr.

Income tax allocation due to timing differences.

Financial reporting and tax reporting summary:Income before tax $300,000 x 40% rate = $120,000Taxable income $100,000 x 40% rate = $40,000

Record $48,000 of deferred tax as payable.

2nd Yr.

C13 - 7

DateDate DescriptionDescription DebitDebit CreditCredit

Income Tax AccountingIncome Tax Accounting

Financial reporting and tax reporting summary:Income before tax $300,000 x 40% rate = $120,000Taxable income $100,000 x 40% rate = $40,000

Income Tax Expense 120,000Income Tax Payable 40,000Deferred Income Tax Payable 80,000

The income tax expense is deducted from the income before tax reported on the income statement.

The income tax expense is deducted from the income before tax reported on the income statement.

1st Yr.

C13 - 8

DateDate DescriptionDescription DebitDebit CreditCredit

Income Tax AccountingIncome Tax Accounting

Financial reporting and tax reporting summary:Income before tax $300,000 x 40% rate = $120,000Taxable income $100,000 x 40% rate = $40,000

Income Tax Expense 120,000Income Tax Payable 40,000Deferred Income Tax Payable 80,000

The income tax payable is based on the taxable income and is a current liability due and payable.

The income tax payable is based on the taxable income and is a current liability due and payable.

1st Yr.

C13 - 9

DateDate DescriptionDescription DebitDebit CreditCredit

Income Tax AccountingIncome Tax Accounting

Financial reporting and tax reporting summary:Income before tax $300,000 x 40% rate = $120,000Taxable income $100,000 x 40% rate = $40,000

Income Tax Expense 120,000Income Tax Payable 40,000Deferred Income Tax Payable 80,000

The deferred income tax payable is a deferred liability due later as the timing differences reverse and the taxes become due.

The deferred income tax payable is a deferred liability due later as the timing differences reverse and the taxes become due.

1st Yr.

C13 - 10

Unusual Income Statement ItemsUnusual Income Statement Items

Three types of unusual items are:

1. Results of discontinued operations.2. Extraordinary items of gain or loss.3. A change from one generally accepted

accounting principle to another.

These items and the related tax effects are reported separately in the income statement.

C13 - 11

Jones CorporationIncome Statement

For the Year Ended December 31, 2003

Net sales $9,600,000

Income from continuing operationsbefore income tax $1,310,000

Income tax 620,000

Income from continuing operations $ 690,000

Loss on discontinued operations (Note A) 100,000

Income before extraordinary items and cumulative effect of a change in accounting principle $ 590,000

Extraordinary item:Gain on condemnation of land, net ofapplicable income tax of $65,000 150,000

Cumulative effect on prior years of changing todifferent depreciation method (Note B) 92,000

Net income $832,000

C13 - 12

Jones CorporationIncome Statement

For the Year Ended December 31, 2003

Net sales $9,600,000

Income from continuing operationsbefore income tax $1,310,000

Income tax 620,000

Income from continuing operations $ 690,000

Loss on discontinued operations (Note A) 100,000

Income before extraordinary items and cumulative effect of a change in accounting principle $ 590,000

Extraordinary item:Gain on condemnation of land, net ofapplicable income tax of $65,000 150,000

Cumulative effect on prior years of changing todifferent depreciation method (Note B) 92,000

Net income $832,000

C13 - 13

Jones CorporationIncome Statement

For the Year Ended December 31, 2003

Net sales $9,600,000

Income from continuing operationsbefore income tax $1,310,000

Income tax 620,000

Income from continuing operations $ 690,000

Loss on discontinued operations (Note A) 100,000

Income before extraordinary items and cumulative effect of a change in accounting principle $ 590,000

Extraordinary item:Gain on condemnation of land, net ofapplicable income tax of $65,000 150,000

Cumulative effect on prior years of changing todifferent depreciation method (Note B) 92,000

Net income $832,000

C13 - 14

Jones CorporationIncome Statement

For the Year Ended December 31, 2003

Net sales $9,600,000

Income from continuing operationsbefore income tax $1,310,000

Income tax 620,000

Income from continuing operations $ 690,000

Loss on discontinued operations (Note A) 100,000

Income before extraordinary items and cumulative effect of a change in accounting principle $ 590,000

Extraordinary item:Gain on condemnation of land, net ofapplicable income tax of $65,000 150,000

Cumulative effect on prior years of changing todifferent depreciation method (Note B) 92,000

Net income $832,000

C13 - 15

Jones CorporationIncome Statement

For the Year Ended December 31, 2003

Net sales $9,600,000

Income from continuing operationsbefore income tax $1,310,000

Income tax 620,000

Income from continuing operationsIncome from continuing operations $ 690,000$ 690,000

Loss on discontinued operations (Note A) 100,000

Income before extraordinary items and cumulative effect of a change in accounting principle $ 590,000

Extraordinary item:Gain on condemnation of land, net ofapplicable income tax of $65,000 150,000

Cumulative effect on prior years of changing todifferent depreciation method (Note B) 92,000

Net incomeNet income $832,000$832,000

Differences created by unusual items: discontinued operations, extraordinary items, and change in methods.

Differences created by unusual items: discontinued operations, extraordinary items, and change in methods.

C13 - 16

Reporting Earnings Per Common ShareReporting Earnings Per Common Share

1. Income from continuing operations.2. Income before extraordinary items and the

cumulative effect of a change in accounting principle.

3. Extraordinary items and the cumulative effect of a change in accounting principle.

4. Net income.

Earnings per share (EPS) is the net income per share of common stock outstanding. When unusual items exist, EPS should be reported for:

C13 - 17

Jones CorporationIncome Statement

For the Year Ended December 31, 2003

Income from continuing operations $690,000

Net income $832,000

Earnings per common share:Earnings per common share:

Income from continuing operations $ 3.45

Loss on discontinued operations .50

Income before extraordinary item and cumulative effect of a change in accounting principle 2.95

Extraordinary item .75

Cumulative effect on prior years of changing to a different depreciation method .46

Net income $ 4.16

C13 - 18

Jones CorporationIncome Statement

For the Year Ended December 31, 2003

Income from continuing operations $690,000

Net income $832,000

Earnings per common share:Earnings per common share:

Income from continuing operations $ 3.45

Loss on discontinued operations .50

Income before extraordinary item and cumulative effect of a change in accounting principle 2.95

Extraordinary item .75

Cumulative effect on prior years of changing to a different depreciation method .46

Net income $ 4.16

C13 - 19

Jones CorporationIncome Statement

For the Year Ended December 31, 2003

Income from continuing operations $690,000

Net income $832,000

Earnings per common share:Earnings per common share:

Income from continuing operations $ 3.45

Loss on discontinued operations .50

Income before extraordinary item and cumulative effect of a change in accounting principle 2.95

Extraordinary item .75

Cumulative effect on prior years of changing to a different depreciation method .46

Net income $ 4.16

C13 - 20

Jones CorporationIncome Statement

For the Year Ended December 31, 2003

Income from continuing operations $690,000

Net income $832,000

Earnings per common share:Earnings per common share:

Income from continuing operations $ 3.45

Loss on discontinued operations .50

Income before extraordinary item and cumulative effect of a change in accounting principle 2.95

Extraordinary item .75

Cumulative effect on prior years of changing to a different depreciation method .46

Net income $ 4.16

C13 - 21

Jones CorporationIncome Statement

For the Year Ended December 31, 2003

Income from continuing operations $690,000

Net income $832,000

Earnings per common share:Earnings per common share:

Income from continuing operations $ 3.45

Loss on discontinued operations .50

Income before extraordinary item and cumulative effect of a change in accounting principle 2.95

Extraordinary item .75

Cumulative effect on prior years of changing to a different depreciation method .46

Net income $ 4.16

C13 - 22

Paid-in capitalPaid-in capital:Preferred $5 stock, cumulative, $50 par (2,000 shares authorized and issued) $100,000Excess of issue price over par 10,000 $ 110,000Common stock, $20 par (50,000 shares authorized, 45,000 issued) $900,000Excess of issue price over par 132,000 1,032,000From donated land 60,000 Total paid-in capital $1,202,000

Stockholders’ EquityStockholders’ Equity

C13 - 23

Stockholders’ EquityStockholders’ Equity

Paid-in capitalPaid-in capital:Preferred $5 stock, cumulative, $50 par (2,000 shares authorized and issued) $100,000Excess of issue price over par 10,000 $ 110,000Common stock, $20 par (50,000 shares authorized, 45,000 issued) $900,000Excess of issue price over par 132,000 1,032,000From donated land 60,000 Total paid-in capital $1,202,000

Contributed capitalContributed capital:Preferred 10% stock, cumulative, $50 par (2,000 shares authorized and issued) $100,000Common stock, $20 par (50,000 shares authorized, 45,000 issued) $900,000Additional paid-in capital 202,000 Total contributed capital $1,202,000

Shareholders’ EquityShareholders’ Equity

C13 - 24

Stockholders’ EquityStockholders’ Equity

Shareholders’ EquityShareholders’ Equity

Contributed capitalContributed capital:Preferred 10% stock, cumulative, $50 par (2,000 shares authorized and issued) $100,000Common stock, $20 par (50,000 shares authorized, 45,000 issued) $900,000Additional paid-in capital 202,000 Total contributed capital $1,202,000

Paid-in capitalPaid-in capital:Preferred $5 stock, cumulative, $50 par (2,000 shares authorized and issued) $100,000Excess of issue price over par 10,000 $ 110,000Common stock, $20 par (50,000 shares authorized, 45,000 issued) $900,000Excess of issue price over par 132,000 1,032,000From donated land 60,000 Total paid-in capital $1,202,000

C13 - 25

Adang CorporationRetained Earnings Statement

For the Year Ended June 30, 2003

Reporting Retained EarningsReporting Retained Earnings

Retained earnings, July 1, 2002 $350,000

Net income $280,000

Less dividends declared 75,000

Increase in retained earnings 205,000

Retained earnings, June 30, 2003 $555,000

C13 - 26

Adang CorporationRetained Earnings Statement

For the Year Ended June 30, 2003

Reporting Retained EarningsReporting Retained Earnings

Retained earnings, July 1, 2002 $350,000

Net income $280,000

Less dividends declared 75,000

Increase in retained earnings 205,000

Retained earnings, June 30, 2003 $555,000

C13 - 27

Adang CorporationRetained Earnings Statement

For the Year Ended June 30, 2003

Reporting Retained EarningsReporting Retained Earnings

Retained earnings, July 1, 2002 $350,000

Net income $280,000

Less dividends declared 75,000

Increase in retained earnings 205,000

Retained earnings, June 30, 2003 $555,000

C13 - 28

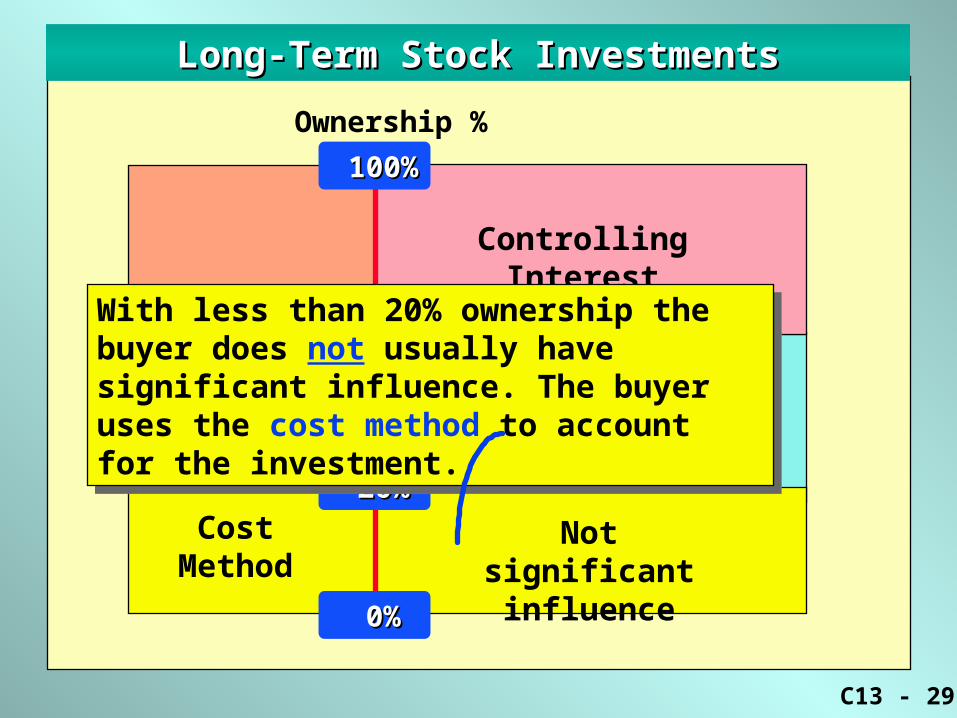

Long-Term Stock InvestmentsLong-Term Stock Investments

EquityMethod

CostMethod

Not significantinfluence

Significantinfluence

Ownership %

Controlling Interest

100%100%

20%20%

0%0%

50%50%

C13 - 29

Long-Term Stock InvestmentsLong-Term Stock Investments

EquityMethod

CostMethod

Not significantinfluence

Significantinfluence

Ownership %

Controlling Interest

100%100%

20%20%

0%0%

50%50%With less than 20% ownership the buyer does not usually have significant influence. The buyer uses the cost method to account for the investment.

With less than 20% ownership the buyer does not usually have significant influence. The buyer uses the cost method to account for the investment.

C13 - 30

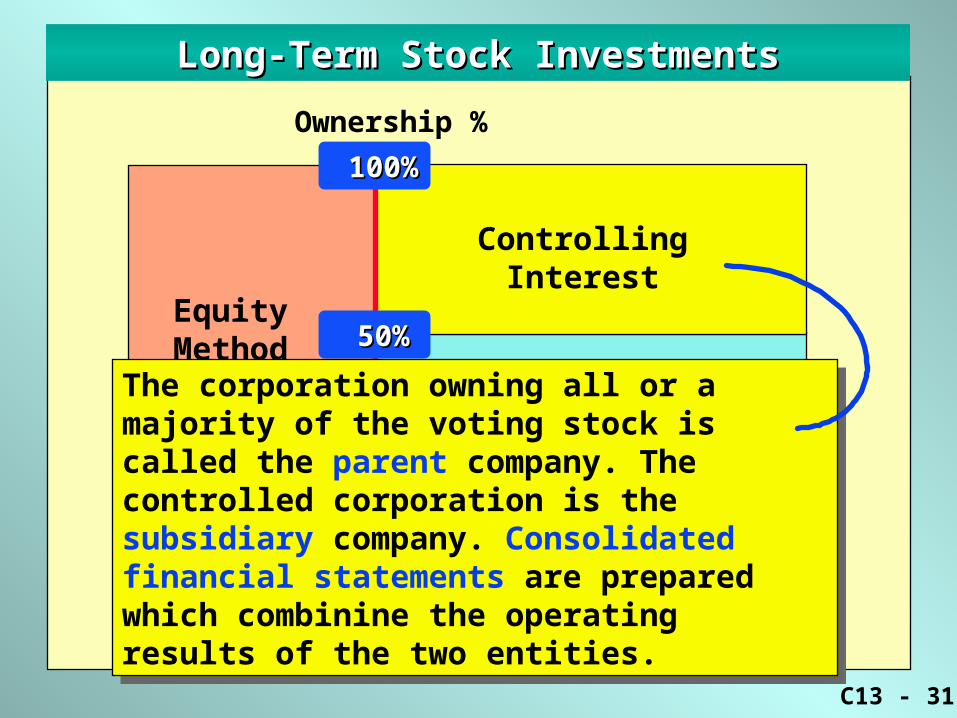

Long-Term Stock InvestmentsLong-Term Stock Investments

EquityMethod

CostMethod

Not significantinfluence

Significantinfluence

Ownership %

Controlling Interest

100%100%

20%20%

0%0%

50%50%

Ownership over 20% usually indicates significant influence.The buyer uses the equity method to account for the investment.

Ownership over 20% usually indicates significant influence.The buyer uses the equity method to account for the investment.

C13 - 31

Long-Term Stock InvestmentsLong-Term Stock Investments

EquityMethod

CostMethod

Not significantinfluence

Significantinfluence

Ownership %

Controlling Interest

100%100%

20%20%

0%0%

50%50%

The corporation owning all or a majority of the voting stock is called the parent company. The controlled corporation is the subsidiary company. Consolidated financial statements are prepared which combinine the operating results of the two entities.

The corporation owning all or a majority of the voting stock is called the parent company. The controlled corporation is the subsidiary company. Consolidated financial statements are prepared which combinine the operating results of the two entities.

C13 - 32

Long-Term Stock InvestmentsLong-Term Stock Investments

EquityMethod

CostMethod

Not significantinfluence

Significantinfluence

Ownership %

Controlling Interest

100%100%

20%20%

0%0%

50%50%

C13 - 33

DateDate DescriptionDescription DebitDebit CreditCredit

Cost MethodCost Method

Investment in Stock 5,940Cash 5,940

Cash 200Dividend Revenue 200

Mar. 1

Purchased 100 shares of Compton Corp. stock at 59 plus brokerage fee of $40.

Received $2 cash dividend from Compton Corp.

Dec. 31

The cost method is used when the buyer does not have significant influence over the operating and financing activities of the investee.

C13 - 34

DateDate DescriptionDescription DebitDebit CreditCredit

Equity MethodEquity Method

Investment in Brock Corp. Stock 350,000Cash 350,000

Investment in Brock Corp. Stock 42,000Income of Brock Corp. 42,000

Cash 18,000 Investment in Brock Corp. Stock 18,000

Jan. 2

Purchased 40% of Brock Corporation for $350,000.

Brock Corporation reports net income of $105,000.

Dec. 31

Brock Corporation reports total dividends of $45,000.

Dec. 31

C13 - 35

DateDate DescriptionDescription DebitDebit CreditCredit

Sale of Long-Term Stock InvestmentSale of Long-Term Stock Investment

Cash 17,500Investment in Stock 15,700Gain on Sale of Investments 1,800

Mar. 1

Sold stock of Drey Inc. for $17,500.Stock has a carrying value of $15,700.

When shares of stock are sold, the investment account is credited for the carrying value (book value) of the shares sold.

C13 - 36

Business CombinationsBusiness Combinations

Many businesses combine in order to produce more efficiently or to diversify product lines.

A merger combines two corporations by one acquiring the properties of another that is then dissolved.

A consolidation is the creation of a new corporation, to which the combined assets and liabilities of the old corporations are transferred.

C13 - 37

Business CombinationsBusiness Combinations

Mergers:Mergers: Company A acquires company B.The assets and liabilities of B are transferred to A and B is then dissolved.

Consolidations:Consolidations: Company A acquires company B. The assets and liabilities of both A and B are transferred to a new company C and A and B are then dissolved.

Mergers

A

B

Consolidations

CA

B

C13 - 38

Analyzing Stock InvestmentsAnalyzing Stock Investments

Accounting: Earnings Per ShareAccounting: Earnings Per Share

Net Income

Common Shares

Investing: Price - Earnings RatioInvesting: Price - Earnings Ratio

Market Price Per ShareEarnings Per Share

EarningsPer Share=

Price-Earnings

Ratio=

C13 - 39

Price – Earnings RatioPrice – Earnings Ratio

The price-earnings ratio represents how much the market is willing to pay per dollar of a company’s earnings. This indicates the market’s assessment of a firm’s growth potential and future earnings prospects.

The price-earnings ratio indicates that a share of common stock was selling for 10 times earnings for 1999 and 12.5 times for 2000.

An example: 2000 1999

Market price per share $20.50 $13.50

Earnings per share $1.64 $1.35

Price-earnings ratioPrice-earnings ratio 12.5 12.5 10.0 10.0

C13 - 40

Note: To see the topic slide, type 2 and press Enter.

This is the last slide in Chapter 13. This is the last slide in Chapter 13.

Power NotesChapter 13 Corporations: Income and Taxes, Corporations: Income and Taxes, Stockholders’ Equity, Investments in StocksStockholders’ Equity, Investments in Stocks