LEAR gabelli 103107

26

October 31, 2007 October 31, 2007 Lear’s Asian Strategy Lear’s Asian Strategy The 31st Annual Gabelli Automotive Aftermarket Symposium

-

Upload

finance16 -

Category

Economy & Finance

-

view

245 -

download

0

Transcript of LEAR gabelli 103107

October 31, 2007October 31, 2007

Lear’s Asian StrategyLear’s Asian Strategy

The 31st Annual Gabelli Automotive Aftermarket Symposium

2

Agenda

Company OverviewBob Rossiter, Chairman, CEO and President

Lear’s Asian StrategyLou Salvatore, Senior Vice President and President, Global Asian Operations

Q and A Session

3

Lear Profile

Lear is . . .a leading global supplier of automotive Seatingsystems, Electrical Distribution systems and Electronic products;

that serves all of the world’s major automakers;

with annual sales of $15 billion (Fortune #155);

236 facilities located in 33 countries; and

more than 90,000 employees worldwide

4

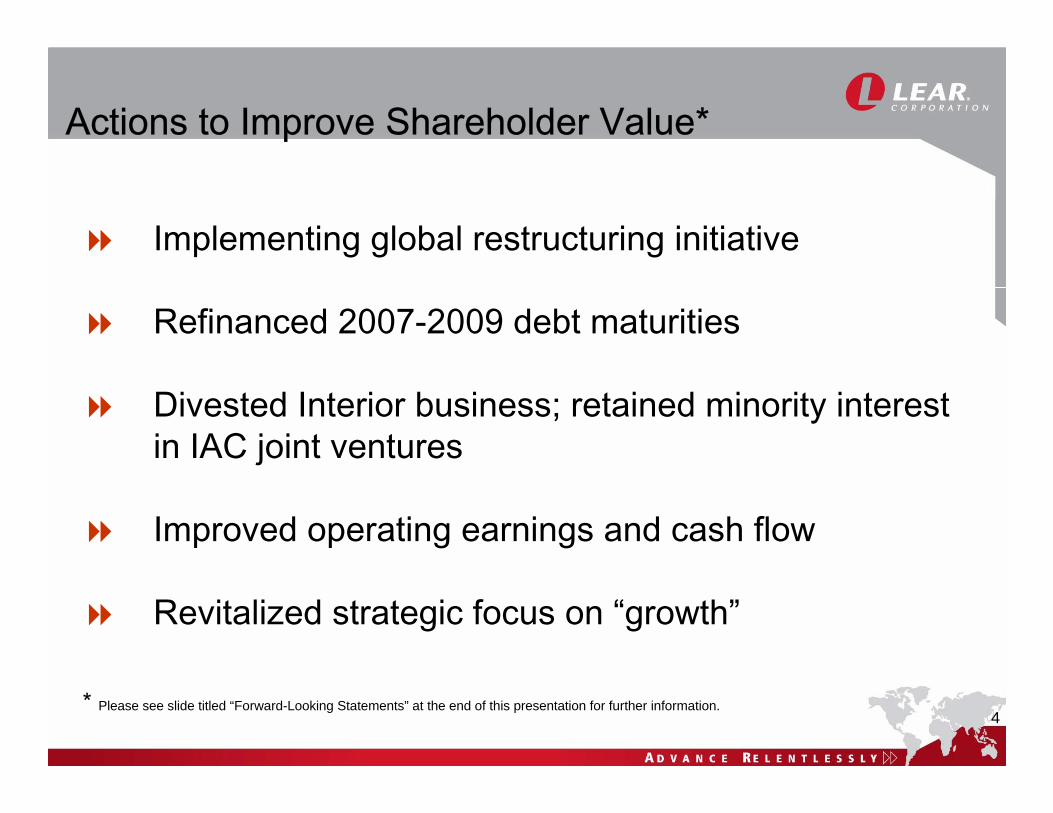

Actions to Improve Shareholder Value*

Implementing global restructuring initiative

Refinanced 2007-2009 debt maturities

Divested Interior business; retained minority interest in IAC joint ventures

Improved operating earnings and cash flow

Revitalized strategic focus on “growth”

* Please see slide titled “Forward-Looking Statements” at the end of this presentation for further information.

5

Strong Competitive Position

Seating Systems#2 position globally, in a market estimated to be about $45 to $50 billion in size:

#2 position in North America and #3 in Europe#2 position in China and #1 in India

Lear is the highest quality major seat manufacturer forthe past 6 years, according to the J.D. Power Seat Survey

Electrical Distribution Systems#3 position in North America, #4 in Europe andamong the leaders in China

Electronic ProductsNiche player in electronic modules, wireless products and audio/video applications

Lear is a true partner to all of the world’s major automakers, with strong market positions and superior quality in our core businesses:

Source: Lear Market Share Study / CSM Worldwide Survey Data

6

Lear’s Business Imperatives*

Superior quality and customer satisfaction

Global scale in core businesses

Technical competence in key components

Lowest cost global footprint

New product innovation

Sales growth and diversification* Please see slide titled “Forward-Looking Statements” at the end of this presentation for further information.

7

Lear’s Asian Strategy

8

Forward Looking Trends*Consumers Growth in vehicle ownership

Growth in micro and small cars

Exports Increased exports from Asia to N.A. / Western Europe

Domestic OEMs Government targeted domestic OEM share = 50%

Supply Chain Customer ownership of supply chain

Geographic Customers (and government) driving localization (components)

Emerging Market India -- the next China (5+ years away)

Asian Market = Continued Growth* Please see slide titled “Forward-Looking Statements” at the end of this presentation for further information.

9

INDIA∆=1.6M

THAILAND∆=0.4M

CHINA∆=2.5M

Source: CSM Worldwide, Inc., Global Light Vehicle Production Report, June 2007

Asian Market Growth*

2007 vs. 2010 Asian Market Growth = 7% CAGR

High Volume Asian Growth (China / India / Thailand) = 13%

Production Volumes

High: 2007 2010 ∆ CAGR%

China 6.8 M 9.3 M 2.5 M 11%

India 1.8 M 3.4 M 1.6 M 24%

Thailand 1.3 M 1.6 M 0.4 M 9%

Sub-total High 9.9 M 14.3 M 4.5 M 13%

Low:Japan 10.7 M 11.3 M 0.6 M 2%

Indonesia 0.3 M 0.5 M 0.2 M 17%

Taiwan 0.3 M 0.4 M 0.1 M 11%

Malaysia 0.5 M 0.6 M 0.1 M 9%

Korea 3.9 M 3.9 M 0.0 M 0%

Philippines 0.1 M 0.1 M 0.0 M 12%

Australia 0.4 M 0.4 M (0.0)M 0%

Sub-total Low 16.1 M 17.2 M 1.1 M 2%

Total Asia 25.9 M 31.5 M 5.6 M 7%

* Please see slide titled “Forward-Looking Statements” at the end of this presentation for further information.

10

Lear’s Asian Strategy*Sales Growth Aggressively grow faster than market

Focus on local OEMs

Strategic acquisitions (gain market share)

Expand seat customer relationships to other products

Profitability Lowest cost designs for customer specification

Vertical integration (components)

Manpower Emphasize local talent / leadership

Quality Operational excellence

“Best-in-class” launch execution

Lear’s Asian Strategy = Growth, Local Markets, Optimized Costs, Local Leaders* Please see slide titled “Forward-Looking Statements” at the end of this presentation for further information.

11

Aggressively Expanding Our Presence in AsiaChina • 19 manufacturing facilities, 6 new in 2007• 2 new engineering/R&D centers in Shanghai (includes CTO activities)

• 18 program launches in 2006• 26 program launches in 2007 • 20+ customers• Seats (#2), Electrical Distribution (among the leaders) and Electronic products

Korea • 2 manufacturing facilities• 1 engineering center in Seoul • Seats

ASEAN• 2 manufacturing facilities• 1 engineering/CTO center in Cebu,

Philippines • 14 program launches in 2007• Seats, Seat Trim

India• 7 manufacturing facilities, 3 new in 2007• 1 engineering center in Mumbai• 3 program launches in 2006• 4 program launches in 2007• 7 customers • Seats (#1)

Note: Includes facilities held through consolidated and non-consolidated joint ventures.

37 Manufacturing / Engineering Facilities in Asia and Growing

Japan • 1 engineering center in Atsugi (Tokyo) • 1 engineering center in Hiroshima

12

Lear China Customer Value Workshop

Opening Ceremony with Lear and Chery Executives - Wuhu, China

13

Geely Signing Ceremony

Geely Signing Ceremony

14

BAI Delegation Visit

Signing Ceremony with Lear and BAI Executives at Southfield HQ

15

New Partnership – Lear Joint Venture with JAC

LOI Signing Ceremony with Lear and JAC Executives in Hefei, China

16

Shanghai, China –Lear Engineering, Technical & Profit Improvement Center

China Engineering Center / China Technical Center / China Profit Improvement Center Co-Location

17

Asia Profit Improvement Center

Asia PIC = Lowest Cost Designs For Each Customer Specification

Foam

Trim Wiring + Tracks

Idea Generation Section

18

2007 Customer / Industry Recognition• Shanghai GM Wuling “Supplier of the Year”

(China Liuzhou plant – 2006; first time awarded to a seat supplier)

• Mazda “VA Proposal Performance Award” –for substantial contribution to cost reduction initiatives (2006 ; also received in 2004)

• Hyundai Mobis “one of outperforming suppliers in 2006”(July 2007)

• FAW-Volkswagen “Best Seat Supplier Award”(Changchun Lear - May 2007)

2007 = Continued Customer / Industry Recognition for Performance Excellence

19

2007 Customer / Industry Recognition

• Labor Ministry of Thailand – Achievement of three million man hours without injury (July 2007)

• Labor Ministry of Thailand – APC Awarded Excellence in Safety Management (May 2007)

• Auto Alliance Thailand -- Achievement of one million seat sets built and delivered (July 2007)

• Toyota – “Superior Award for Supplier Diversity 2006” – for the 3rd

consecutive year (March 2007)

2007 = Continued Customer / Industry Recognition for Performance Excellence

20

2005 2006 2007 Outlook

Consolidated Non-consolidated

Aggressively Growing Total Asian Sales*

Total Asian Sales – Core Businesses ($ in millions)

2007 Highlights• Significant market position

in China:– Total sales > $700 million **– Supply 20+ OEMs on

> 100 vehicle programs– 19 manufacturing facilities

with approximately 6,000 employees

– 2 new engineering/R&D centers in Shanghai

– Our fastest growing market

• 11 new facilities in India and China supporting Ford, Mazda, Chery, Tata, M&M, BMW and Hyundai

$1,850

~$2,850

$2,200

* Includes sales in Asia and with Asian manufacturers globally. Please see slide titled “Forward-Looking Statements” at the end of this presentation for further information.

** Includes consolidated and non-consolidated sales.

Targeting Continued Growth

21Profitable Growth = Strong Plans Will Succeed

Key Drivers For Profitable Growth*Lowest cost designs for each customer specification

Localized engineering

Localized component sourcing

Best-in-class local talent

Vertical integration (quality / cost)

Continuous improvement and lean initiatives

Operational improvements

Export low cost engineering and components to ROW

*Please see slide titled “Forward-Looking Statements” at the end of this presentation for further information.

22

Closing Comments

23

Lear’s Asian Strategy*Sales Growth Aggressively grow faster than market

Focus on local OEMs

Strategic acquisitions (gain market share)

Expand seat customer relationships to other products

Profitability Lowest cost designs for customer specification

Vertical integration (components)

Manpower Emphasize local talent / leadership

Quality Operational excellence

“Best-in-class” launch execution

Lear’s Asian Strategy = Growth, Local Markets, Optimized Costs, Local Leaders* Please see slide titled “Forward-Looking Statements” at the end of this presentation for further information.

24

Q and A Session

R

25

ADVANCE RELENTLESSLY™

www.lear.comLEA

NYSEListed

R

26

Forward-Looking Statements

This presentation contains forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995, including statements regarding anticipated financial results and liquidity. Actual results may differ materially from anticipated results as a result of certain risks and uncertainties, including but not limited to, general economic conditions in the markets in which the Company operates, including changes in interest rates or currency exchange rates, the financial condition of the Company’s customers or suppliers, fluctuations in the production of vehicles for which the Company is a supplier, disruptions in the relationships with the Company’s suppliers, labor disputes involving the Company or its significant customers or suppliers or that otherwise affect the Company, the Company's ability to achieve cost reductions that offset or exceed customer-mandated selling price reductions, the outcome of customer productivity negotiations, the impact and timing of program launch costs, the costs and timing of facility closures, business realignment or similar actions, increases in the Company's warranty or product liability costs, risks associated with conducting business in foreign countries, competitive conditions impacting the Company's key customers and suppliers, raw material costs and availability, the Company's ability to mitigate the significant impact of increases in raw material, energy and commodity costs, the outcome of legal or regulatory proceedings to which the Company is or may become a party, unanticipated changes in cash flow, including the Company’s ability to align its vendor payment terms with those of its customers, the success of the Company's restructuring initiative and other risks described from time to time in the Company's Securities and Exchange Commission filings.

The forward-looking statements in this presentation are made as of the date hereof, and the Company does not assume any obligation to update, amend or clarify them to reflect events, new information or circumstances occurring after the date hereof.

![FINAL - GenCorp - Gabelli Presentation - Sept 2012[1]](https://static.fdocuments.in/doc/165x107/55cf9a8e550346d033a253db/final-gencorp-gabelli-presentation-sept-20121.jpg)