leading Tax Department Change - Ey - United States€¦ · Excel projection ... 14 Leading tax...

41

Leading tax department change 14 May 2013

Transcript of leading Tax Department Change - Ey - United States€¦ · Excel projection ... 14 Leading tax...

Leading tax department change

14 May 2013

Leading tax department change1

Disclaimer

Ernst & Young refers to the global organization of member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young LLP is a client-serving member firm of Ernst & YoungGlobal Limited located in the US.This presentation is ©2013 Ernst & Young LLP. All rights reserved. No part of this document may be reproduced, transmitted or otherwise distributed in any form or by any means, electronic or mechanical, including by photocopying, facsimile transmission, recording, rekeying or using any information storage and retrieval system, without written permission from Ernst & Young LLP. Any reproduction, transmission or distribution of this form or any of the material herein is prohibited and is in violation of US and international law. Ernst & Young and its member firms expressly disclaim any liability in connection with use of this presentation or its contents by any third party.The views expressed by panelists in this session are not necessarily those of Ernst & Young LLP.

Leading tax department change2

Circular 230 disclaimer

Any US tax advice contained herein was not intended or written to be used, and cannot be used, for the purpose of avoiding penalties that may be imposed under the Internal Revenue Code or applicable state or local tax law provisions.These slides are for educational purposes only and are not intended, and should not be relied upon, as accounting advice.

Leading tax department change3

Today’s presenters

Gary Paice , Ernst & Young LLP – ModeratorAndrea Gronenthal, Ernst & Young LLP David Kovar, Ernst & Young LLP Brian Morris, Ernst & Young LLP Lawrence Pociask ,Vice President, US Tax - Tate & LyleSally Stiles, Director of Global Tax & Trade Operations - Caterpillar Inc.

Leading tax department change4

Agenda

► Drivers shaping tax leadership► Focus of high-performing tax

function activities:► Legislative► Business► Operational

► Conclusions

Leading tax department change5

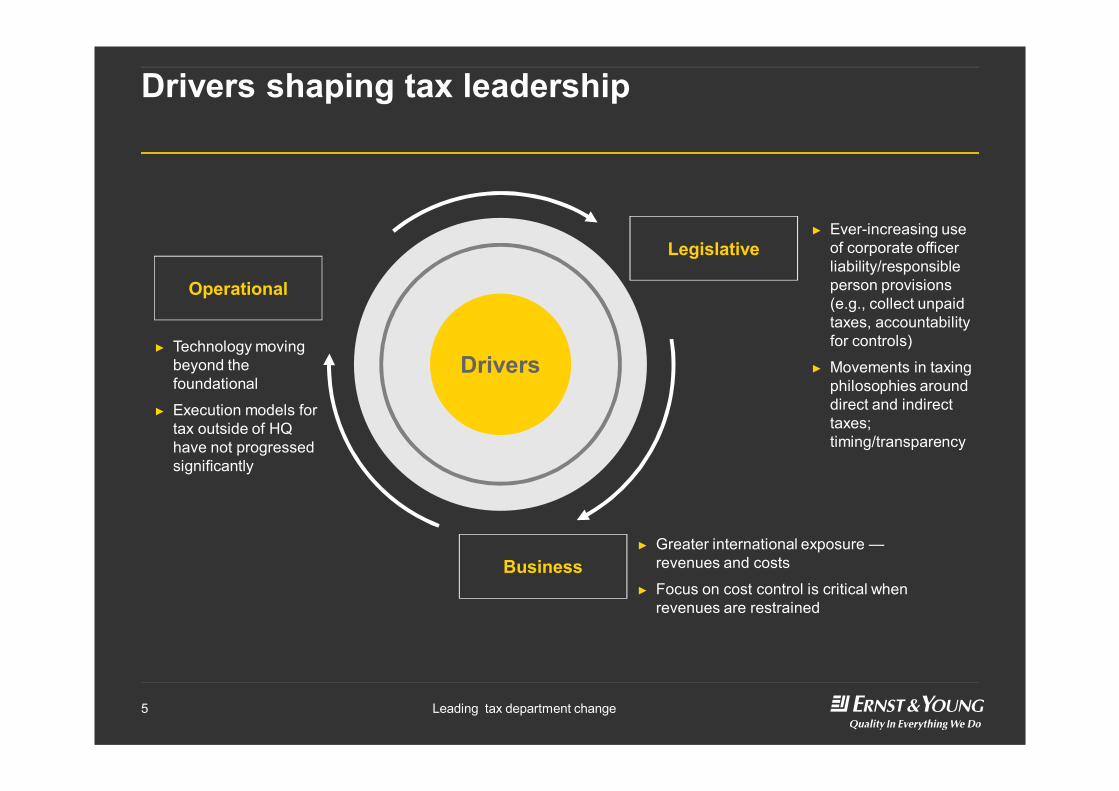

Drivers shaping tax leadership

► Ever-increasing use of corporate officer liability/responsible person provisions (e.g., collect unpaid taxes, accountability for controls)

► Movements in taxing philosophies around direct and indirect taxes; timing/transparency

► Technology moving beyond the foundational

► Execution models for tax outside of HQ have not progressed significantly

► Greater international exposure —revenues and costs

► Focus on cost control is critical when revenues are restrained

Legislative

Operational

Business

Drivers

Leading tax department change6

Legislative drivers

► Completing a tax risk profile

► Establishing responsibilities in and outside of tax

► Increased controls using technology where appropriate

► Improved monitoring

Ever-increasing use of corporate officer liability/responsible person provisions

► Indirect taxes including VAT regimes and transfer pricing changing the tax dollars to individuals with less tax experience so tax approach to bringing tax insights also changing

► Timing of reporting is increasingly shifting to contemporary reporting so companies shifting processes and technology (e.g., supply chain systems)

► Tax changes requiring significant operational support

Movements in taxing philosophies around direct and indirect taxes; timing/transparency

Driv

ers

Approaches at leading com

panies

LegislativeOperational

Business

Drivers

Leading tax department change7

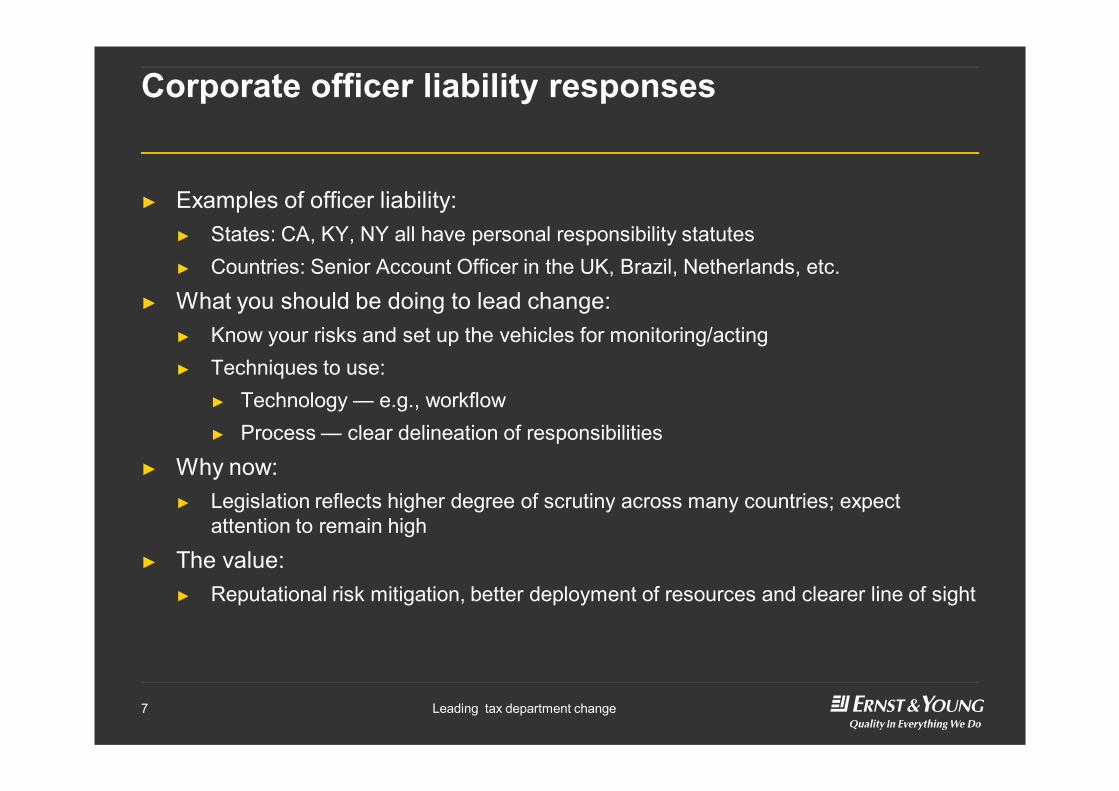

Corporate officer liability responses

► Examples of officer liability:► States: CA, KY, NY all have personal responsibility statutes► Countries: Senior Account Officer in the UK, Brazil, Netherlands, etc.

► What you should be doing to lead change:► Know your risks and set up the vehicles for monitoring/acting► Techniques to use:

► Technology — e.g., workflow► Process — clear delineation of responsibilities

► Why now:► Legislation reflects higher degree of scrutiny across many countries; expect

attention to remain high

► The value:► Reputational risk mitigation, better deployment of resources and clearer line of sight

Leading tax department change8

Simplified exampleSignificant transaction workflow

Significant transaction

identified prior to implementation

Documents collected► Excel projection► Emails► Transaction memo

Update or generate additional documents► Excel projection► Emails► Transaction memo

Update or generate additional documents► Excel projection► Emails► Transaction memo► Elections/filings

Over $$ ?Get approval from

VP of tax(SOX control)

End workflow and mark documents

final

YesNo

Planner

Taxaccounting

Taxcompliance

Provide tax accounting analysis

Provide tax compliance

analysis

Yes

Ready for broader analysis?

Leading tax department change9

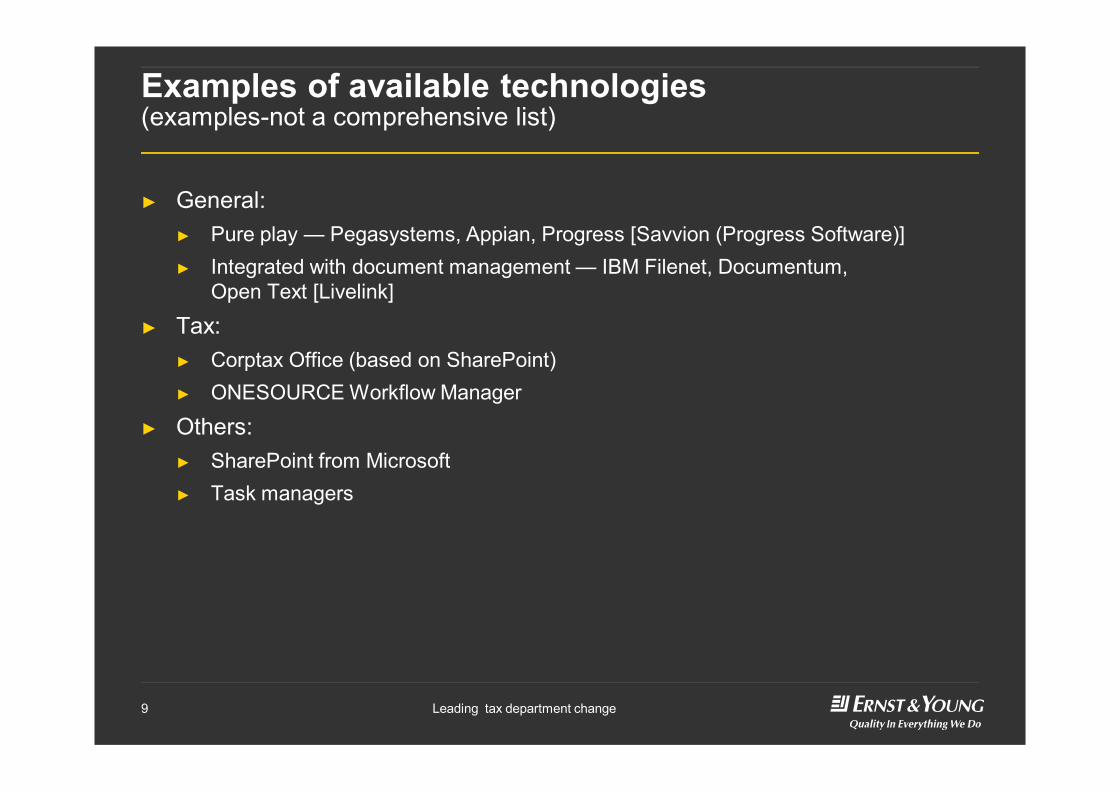

Examples of available technologies(examples-not a comprehensive list)

► General:► Pure play — Pegasystems, Appian, Progress [Savvion (Progress Software)]► Integrated with document management — IBM Filenet, Documentum,

Open Text [Livelink]

► Tax: ► Corptax Office (based on SharePoint)► ONESOURCE Workflow Manager

► Others:► SharePoint from Microsoft► Task managers

Leading tax department change10

Observations about reducing corporate officer liability

► Technology and process require a cross-functional activity especially on an international implementation.► Don’t underestimate the number of people involved.► Consider the impact of “occasional” users on the workflow design.► Is there already a finance workflow tool?

► Workflow solutions may look deceptively simple.► Consider an integrated document management and workflow solution that has

sufficient reporting and integration capabilities.► Security and user control can be very time consuming. Don’t over think this!

Leading tax department change11

Changes in taxes, timing and transparency

► Indirect taxes and taxes computed at more detailed levels (e.g., purchase order) becoming a bigger part of the overall pie yet the number of dedicated tax resources devoted is very small.► Illustration:

► Income tax — typically HQ and regional tax professionals with dedicated tax preparers doing compliance

► Transfer pricing — small number of tax professionals that set policy with the execution being primarily done with non-tax professionals

► Indirect tax — maybe a global leader but with many non-tax professionals and/or third parties doing the execution

► What should you be doing to lead change?► Partner with business to establish leadership► Implement technology/process that addresses new possibilities

Leading tax department change12

Improving timing and transparencyTransfer pricing (TP) example

TP data analytics and reportingPlanning, budgeting and forecasting Intercompany processing

Demand planning

Other

Prospective transfer pricesBudgets and forecasts are prepared at a level

needed to set and adjust transfer prices periodically to achieve target margins by end of year

Intercompany agreements and document managementIdentification of intercompany relationships and maintenance of legal agreements and transfer pricing studies

Real-time monitoringAccumulation of data into a centralized repository

to produce operating margin exception reports and determine transfer pricing adjustments

Integrated processesStandardized and automated intercompany

accounting to support statutory and consolidated financial reporting

Master data managementTransfer pricing-sensitive data definitions and governance to support data quality

Generalledger

Transaction processing

Data warehouse

Intercompany cross-charges

Profitability analysis

TP analytics

TP adjustments

TP governance and managed workflowDefined roles and responsibilities with visibility and control over all transfer pricing processes

Businessprocess

management

Consolidation

Supply chain

Financial planningand analysis (FP&A)

Leading tax department change13

Tools for operational transfer pricing

Analytics and reporting software Vendor Brief descriptionSAP Profitability and Cost Management (PCM)

SAP ► Flexible and user-driven modeling and reporting tool

► Open architecture to bring in data from multiple sources

► Create and run financial models to monitor transfer prices

► Powerful what-if analysis and simulation capabilities

ONESOURCE Operational Transfer Pricing (OOXP)

Thomson Reuters

► Provides a centralized system for all intercompany activity reviews (tangible goods, services, intangibles) to automate and enable better control over your processes and data

► Generates standard and ad hoc reporting to produce journal entries, invoices or other management reports

Transfer Pricing for Hyperion (HTP) Pebble Age (Oracle Gold Partner)

► Runs using leading Oracle Financial Management (HFM) solution as the main database and can be integrated to almost any ERP system

► Visual user interface to build computations and reporting

Longview Transfer Pricing Longview Solutions

► Prototype developed on the Longview Tax and financial reporting platform

► More information and announcement to follow

Shared Services Analyzer (SSA) Ernst & Young ► Transfer pricing analysis of complex services and intellectual property

► SSA platform automates the allocation process and can consolidate multiple services analyses into one tool

Enterprise Resource Planning (ERP) / Data warehouse (internal)

Various ► Custom reporting solutions leveraging ERP and BPM platforms from SAP, Oracle, etc.

Leading tax department change14

A SAP view

SAP NetWeaver BW, ERP, GL, DW,CRM, TRX

Application layer

SAP Profitability and Cost Management

Presentation layer

End user data entry, query & analysisWeb or LANWork management Shipped with application

Model buildersModel structure / rules

Data layerSingle open databaseOracle or MS SQL

Data BridgeFlat file or Relational

SAP Financial Information Management

Export calculated results

External Data Warehouse

Bulk Data LoaderTable to table

SAP Business Objects BI solutions

SAP BusinessObjects

UniverseCreate UniverseStatic

SAP Business Objects Analysis and other 3rd party OLAP clients

EPM add-in for Microsoft OfficeShipped with application

MDX ConnectorDynamic

SAP Financial Information Management

Other SAP EPM solutions

Leading tax department change15

Observations about changing taxes, timing and transparency

► Why now:► Technology solutions coming of age just in time for ramp up in

audit needs

► The value:► Fewer audit risks and lower overall cash taxes paid.► Be prepared for instantaneous reporting (e.g., Brazil’s SPED).

► The bottom line:► Whether it is indirect tax or transfer pricing, change is possible but these projects

take time — so, start now. If there is an issue, the fix will not be simple or fast.► Leadership means participation across functions.► Be prepared for CFO-level business case to explain and budget for change.

Leading tax department change16

Business drivers

► Starting to see movement in companies focusing specifically on improving the international data and collecting it closer to real time

► More granular forecasting, at least in key countries or operational segments

Greater international exposure —revenues and costs

► Most companies are sustaining profitability through cost control

► Finance transformations will continue to put pressure on the organizations to become increasingly efficient

► Getting tax-sensitized data out of systems controlled by finance is one of the key factors in achieving efficiencies within tax; VPs who get aggressive in this area achieve two things:► First, they capture finance

technology/transformation spend► Second, they create efficiencies

without increasing risk

Focus on cost control is critical when revenues are restrained

Driv

ers

Approaches at leading com

panies

LegislativeOperational

Business

Drivers

Leading tax department change17

Greater international exposure

► As the percentage of income/expenses outside of HQ increases and more elaborate tax planning is implemented:► Decentralized nature of non-US data becomes more problematic► Budgeting and forecasting issues with data (not the tools) drive uncertainty► Complexity and timing of calculations create risk

► Solution is to focus on areas that improve international reporting —organization, process and technology► Why now:

► Trend is to continue to increase exposure (e.g., BRIC)► The value:

► Reduce risk and provide better planning

► Example:► Company redesigned process/data so international calculations mostly known in the

first two months of the close rather than in six months, and for the acceleration of statutory filings

Leading tax department change18

Focus on long-term costs control via finance transformation

► Cost of finance, speed and accuracy is a key driver of change leading companies to make significant investments► Often huge budgets► Tax can provide an excellent business case if cash taxes, risk and value are

assessed and included in project scope

► Opportunity for change► Creates environment to reevaluate current approach► Since tax needs were often not built into current approach, this is almost all upside► More global standards help tax departments

► Change isn’t always positive► Stable resources and tasks might be replaced► Data elements might be summarized in a way that prevents good tax analysis

Leading tax department change19

Engaging in finance transformationPotential benefits for tax from finance improvement

Finance trends Tax function potential ramifications Tax function potential opportunitiesImprove use of IT systems

► Systems changes may impact current data sources and lead to more data rework and data gathering

► Customized reports for tax may no longer be available

► Leverage finance systems to generate tax-sensitive information

► Consolidate multiple sources of tax information to streamline data collection

Standardize financial and management reporting and improve forecasting

► Shorter close cycle places additional pressure on the tax-provision process

► Improved financial reports and forecasts may be optimized for management and oversight needed for legal entity reporting

► Redesign and automate tax financial close to support shorter close with increased accuracy

► Work closely with finance to “tax-sensitize” forecasting processes and systems to improve accuracy and efficiency of tax reporting and planning

Simplify finance organization structure; leverage shared services

► Fewer local finance resources available to support international tax compliance and provision reporting or manage service providers

► Functions performed by “shadow tax” resources may be altered and/or need to be assumed by the tax function

► Centralize tax activities across business units and geographies to reduce costs

► Consider how to migrate activities to achieve cost efficiencies without increased tax risk or lost tax opportunities

Leading tax department change20

Sub-projects within finance transformationsMore potential benefits to tax

Project types Potential tax benefitERP consolidation/standard chart of account (COA) implementations

► Improve tax provision and compliance accuracy through greater automation► Leverage the ability for automation in tax technology tools► Reduce manipulation of ERP data► Improve visibility into intercompany transactions and transfer pricing issues

Shared service implementation ► Improve the consistency, timing and access of key tax inputs such as statutory accounts preparation

► Reevaluate tax personnel roles and deployment and use of outside providers

Process and sub-process redesigns ► Reduce overall effort by both tax and accounting personnel by incorporating tax sensitization decisions at the source of recording

► Increase ability to automate manual tasks resulting in significant time savings

Data warehouse and archival management strategies

► Increase the availability, accessibility and standardization of data required for tax calculations and tax authority audit purposes

► Provide/create central repository for business transaction data

Business performance management initiatives, including management reporting and decision-making

► Improve the quality of the financial data available for tax forecasting and tax planning

► Enable quicker tax responses to business planning inquiries

Leading tax department change21

Tax data marts

Example of where companies can be today

Source systems Enterprisedata warehouse

Manufacturing

Job profitability

Procurement

Legal entitieshierarchies

Transfer pricing

Fixed assets

General ledger

System 1(SAP)

System 2(Oracle)

System 3 (Other)

Cons/Elims (Hyperion)

Entity profiles(shared tax and legal)

Transactionmart

Fixed assetmart

Transferpricing

mart

Other data collection tools

Interfaces

Tax provision Tax compliance Tax planning/analysis

Accountmart

Leading tax department change22

End-to-end view

► Capture► Tax sensitize — the ability for the financial system to have the means to provide

tax-level information without manual adjustments► Monitor the key accounts so what is regularly booked is of sufficient quality

► Move► Develop the reporting and interfaces to drive other systems

► Use► Utilize available mechanisms to bring data into third-party tools

(e.g., provision, compliance)► Develop reconciling mechanisms to validate against captured data

Leading tax department change23

Tax need (example: fixed assets)

Tax needs the ability to evaluate the assets that were placed in service during a given year or period of theyear and potentially change the depreciation method used to compute depreciation for that year (e.g., USmid-quarter convention, where assets that are placed in service take a half year of depreciation in the firstyear, except when more than 40% of the assets placed in service during the year occur in the last quarter of the year).

Capturing data requires multidimensional thinking (SAP Examples from Ernst & Young requirements database)

Successful data capture requires identifying the tax needs, the systems impacts and the process impacts. Each play a role in ensuring success.

Systems (example: transfer pricing)

Profitability segments will be objects used to capture costs and revenues in the CO-PA ledger. In an operating concern, a profitability segment is defined by a combination of characteristic values. Characteristics may be already available in the SAP System (customer, product, sales organization), or can be defined based upon customized data elements.

Process (example: fixed assets)

When an asset record is created in the SAP Fixed Asset system through cost settlement from the SAP Project system or direct capitalization, a user must select the appropriate asset class. While this setting is the SAP default setting, it is recommended that based on predefined rules, the asset class is auto populated for each addition.

Leading tax department change24

Transactionfacts and

factattributes

Tax data marts

Capturing data in a data warehouse

Period

DataSource

Cost center

Profit center

Currency

Fact

Dimension

Hierarchy/roll-up structure

TradingPartner

Company/AC

Responsibilitycenter

Primejob

Co/Prm Job/RC Location

Co/Wrk Ord/RC Location

Sourceaccount

WorkOrder

Document

Fact attributes

G&A tax type

DocumentItem

Line item

Billingtype

Vendor

Posting key

Transactiontype

Customer(sold to)

Subfieldcontents

Calendar/fiscal

Common Profit

Center

Common Cost

Center

Tax AcctHiers and

Attribs

AcctHiers and

Attribs

Resp Ctr to Dept to BU

Hier and Attribs

Co to Legal Entity Hier and Attribs

Transactionmart

Fixed assetmart

Transfer pricing mart

Accountmart

Leading tax department change25

Using: end result of well-engineered data

► High degree of book tax difference automation► Early sign-offs of amounts requiring no further adjustment between provision

and compliance► Reduction or elimination of most tax packages► Fewer data correction activities (e.g., finance/accounting people use the

correct codes for tax since it is monitored and reconciled regularly)► Personnel in tax or who work with tax have an understanding of the data,

where it resides and how to effectively access it

Leading tax department change26

Operational drivers

► Basics:

► Tools — compliance and provision integrated; basic indirect tax tools

► Data — G/L level feeds; monthly indirect feeds

► Next:

► Tools — budget/planning; global indirect tax tools; transfer pricing; workflow

► Data — detailed feeds expand to all major financial feeder systems; monthly reporting

Technology moving beyond the foundational

► Beyond just off-shoring — regional hubs, near-shoring

► Shifting away from quarter-only or annual-only analysis

► Career path for personnel

► Clear ownership

Execution models for tax outside of HQ have not progressed significantly

Driv

ers

Approaches at leading com

panies

LegislativeOperational

Business

Drivers

Leading tax department change27

Technology moving beyond foundational

► Early 2000s► Compliance tools with simple trial balance import► Vertex or Taxware indirect tax engine for US only► Simple storage for documents (e.g., shared directory)

► Today — tools have evolved► Integrated compliance and provision (global rollout) for income tax► Global ONESOURCE (formerly, Sabrix) or Vertex for indirect tax► Workflow and document management for multiple processes► Global tax calendars with internal and external assignments► Leverage of finance tools (entity management, finance data warehouse,

planning/forecasting, controls sign-off)

Leading tax department change28

Technology moves beyond foundationalEarly 2000s

Indirect tax

ERP system

US bolt on for mostly sales tax (some use tax)

Limited transaction

history

Order entrybilling accounts

receivable

Tax ratesTax

determinationTax calculation

Good movementfixed asset

transfer

Accounts payablePurchase order

Direct tax

Simple Excel work papers

Transaction history and audit

archive

UScompliance tool

G/L and consolidations

Multidisciplined

Shared drive

US state tax calendar

Numerous spreadsheets

Other systems

Leading tax department change29

Technology moves beyond foundationalNow

Indirect tax

ERP system

Order entrybilling accounts

receivable

Tax ratesTax

determinationTax calculation

Good movementfixed asset

transfer

Accounts payablePurchase order

ax rateTax

eterminatcalcul

Transfer pricing

Planning budgeting and

forecasting

Data analytics and reporting

Intercompany transaction processing

Direct tax

GAAP/stat/tax work papers

Audit and planning analysis

Provision and multicountrycompliance

G/L and consolidations Other systems

Multidisciplined

Global tax rates

Transaction history

Global tax logic

Multicountryreporting and

data transmission

Workflow and document

management

Global tax calendars

Entity management

tools

Fewer spreadsheets

Finance or tax data warehouse

Transaction history and

audit archive

US bolt on for mostly sales tax (some use tax)

Limited transaction

history

Simple Excel work papers

UScompliance tool

Shared drive

US state tax calendar

Numerous spreadsheets

Finance or tax data warehouse

and archive

Leading tax department change30

A look at the interfaces driving automationDirect tax examples

Interface from Description of need/benefitFixed asset module Drives high-value book-tax differences for tax depreciation, gain/loss, etc. on provision as well as

providing details for compliance activities such as fixed asset computations and state A&A determinations.

Taxes payable account detail

Automatically populates tax payments, refunds and adjustments entered in transactions at both the headquarters and local country level, providing detailed visibility to tax provision preparers and allowing for a rapidly accelerated tax account reconciliation process.

Consolidation software Ability to compare final consolidated tax results with consolidated book results at the desired level of detail. Also extraction of hierarchies and entities for meta data.

Local country trial balances

Drives automation of low-complexity, high-volume book/tax difference across the globalenterprise allowing for an accelerated close timeline and increased management attention to more material differences.

Select transaction-level detail

Drives automation of specific book/tax difference analysis and other specialized compliance information (e.g., foreign sourcing) based on detail not otherwise available at a trial balance level of detail.

Tax compliance software

Allows for tight integration of compliance and accrual process, enabling a sped-up filing and return-to-provision process.

Reports/balance checks

Various customized report interfaces used for driving detailed compliance activities, specifically for state and international compliance. Also, validations across systems.

State planning reports Allows for a tighter, more granular estimation of blended state rate leading to lower state RTAs.

Leading tax department change31

Technology moving beyond foundational

► Many companies haven’t positioned themselves to take advantage (e.g., lack of tax tech people)

► Why now:► Companies need to rethink many of the challenges for new focus points including

global control, regional centers, better data and more sophisticated solutions

► What is the value:► Speed and planning are leading to better planning and risk mitigation

Leading tax department change32

Execution model

► While finance models for execution are evolving (e.g., regional hubs, centers of excellence), tax’s models mostly have not

► Examples of disconnects:► Client moves to finance regional hub in LATAM country but no redesign of tax

processes, controls, training or instructions ► Tax not involved in hiring and no true job descriptions available► No rethinking of processes and how more of a monthly process is actually more

consistent with the regional model than a quarterly or annual process (e.g., are there activities such as account reconciliations or tax sensitive account reviews that can be formalized and adopted regionally?)

► No redesign of organization around tax audit defense and business unit planning that likely remains even with a regional hub

Leading tax department change33

Illustration of current challengesHow US multinationals manage global VAT

Undermanaged► Only about 1/3 of large

multinational corporations (MNC) have either a global or regional VAT leader

Under staffed► Most large MNCs have fewer

than 10 tax personnel worldwide dedicated to VAT

► Many have no global indirect tax resources in the tax department

Under measured► Most large MNCs do not have

clearly defined metrics to measure the effectiveness of indirect tax performance

Over-focused on EMEIA► MNCs are three times as likely

to have a regional VAT leader in EMEIA than in LATAM or Asia

► Fewer than one in seven MNCs have written indirect tax policies in place outside of EMEIA

Indirect tax

function

Leading tax department change34

VAT: a global trend with local impact

► Indirect taxes represent the largest share of global business tax outlays

► New global and regional tax functions are being created in order to manage the volume and complexities of all the new challenges

► IT departments continue to push for a reduction in the number of ERP systems and a “single source of truth”

► New/upgraded system deployments require in-depth knowledge of global supply chains, sales/use tax and VAT legislation in each individual jurisdiction

OECD business tax revenue shares (% of total business tax revenue)

Corporate Income taxes

Payroll Taxes

Property taxes

Goods and Services taxes

VAT and SUT

Most frequent reasons for tax adjustments

$

41%

23%16%

10%

10%Formal mistakes (e.g., missing or incomplete invoices, receipts)

Incorrect qualification of turnover (e.g., incorrect tax rate, exempt instead of taxableIncorrect calculation of input VAT pro-rata

Inconsistencies between declared VAT and annual financial statementsOther

Leading tax department change35

A new organization model is needed to support the new demands

► Principal accountabilities for an integrated, global indirect tax function:► Statutory compliance/right to operate► Cash and earnings planning/creation► Internal control guidance► Audit/legal dispute oversight► Business planning/advisory► Operational cost minimization

► Benefits of an integrated function:► Increased transparency► Focused accountability ► Standardization

► Principal accountabilities for a regional indirect tax function:► Lobbying/legislative analysis, planning

and advisory► Audit and legal dispute support► Data analysis and compliance support► Coordinate with global IT and finance centers

CFO

VP tax

Region tax directors

Country tax managers

Regional taxIndirect taxManagers

Global head of indirect tax

Reorganized

Leading tax department change36

Example of a changeIndirect taxes

► Execution model changes away from decentralized model due to better technology and more standardization

► Leadership► Software updates► Planning support

► Education► Data analysis► Accounting entries► Compliance support► Audit response

► Audit representation

► Leadership► Software updates► Planning support

► Education► Data analysis► Accounting entries► Compliance support► Audit response

► Audit representation

► Leadership► Software updates► Planning support

► Education► Data analysis► Accounting entries► Compliance support► Audit response

► Audit representation

LATAM

Country A

Country B

Country C

LATAM

Regional hub

Central

Local country

Support including local third parties

Leading tax department change37

Execution model

► Why now:► Whether for direct or indirect taxes, changes in models are multiyear ventures and

having an idea as to what you want and experimenting with what works cannot be underestimated

► The value:► Risk mitigation and cost containment are both key aspects to changes in the

execution models

► What functions need to be involved:► Finance, tax and key operational leaders who oversee worldwide operations

Leading tax department change38

Conclusions

► More leadership/participation by tax in finance initiatives to improve: ► Data► Ownership/monitoring► Designing the future

operating model

Positioning future tax departments

► More focus on: ► Tax significant technologies

and the resources to maintain and optimize

► Matching analysis with activity throughout the year

► Creating vehicles in the organization that can deliver complex tax change

Questions and answers

Thanks for participating