lcbs working paperspapers volume one -...

84

volume one working papers papers lcbs ISSN 2470-6272

Transcript of lcbs working paperspapers volume one -...

volumeone

workingpaperspapers

lcbs

ISSN 2470-6272

About the Lemann Center for Brazilian Studies (LCBS)

Columbia’s Center for Brazilian Studies, was established in 2001 to offer a place for scholars and

students to pursue and share research and scholarship on Brazil. In 2015, the Center was renamed the

Lemann Center for Brazilian Studies (LCBS). In carrying out its academic mission, the LCBS stimulates

new research and debate on Brazil. The Center is committed to training future leaders for careers in

research, government, and the private sector related to Brazil. Serving as the key focal point for all

students and faculty at Columbia with interest in Brazil, the LCBS’s largest constituencies include those

affiliated with Columbia’s School of International and Public Affairs and from the numerous academic

units of the Graduate School of Arts and Sciences.

The LCBS’s rich programming includes sponsored seminars and lectures on contemporary and historical

aspects of Brazil, including culture, economics, and politics. The LCBS serves as a regular forum for

lectures and conferences by visiting Brazilian academics, government officials, business leaders,

politicians, and representatives of civil society.

In addition to public programming, the LCBS organizes courses focused on Brazil, including courses on

the economic and political development of Brazil, as well as a variety of other topics. The LCBS’s Ruth

Cardoso Visiting Faculty program brings leading Brazilian scholars to the campus for one or two

semester residencies during which they conduct collaborative research and teach courses at the LCBS

in their area of specialization.

Through its Visiting Scholars and Professional Fellows programs, the LCBS offers Brazilian academic

and policy experts the opportunity to be in residence on the Columbia campus and to interact with

members of the Columbia faculty with expertise on Brazil and Latin America.

The LCBS also helps to promote collaborations between the Columbia community and Brazilian

scholars and institutions, working closely with the Columbia University Global Center Rio de Janeiro.

The Lemann Center for Brazilian studies provides support for Columbia faculty research with a focus on

Brazil, as well as engages in original research. The LCBS, for example, has recently published a report

on “Mobile Learning in Brazil”, which examines policies and initiatives for the integration of information

and communication technologies in public schools throughout Brazil. For additional information about

the Lemann Center for Brazilian studies please visit:

http://ilas.columbia.edu/centers-and-programs/brazil-center/

2 | L e m a n n C e n t e r f o r B r a z i l i a n S t u d i e s W o r k i n g P a p e r s | M a r c h 2 0 1 6

About the Lemann Center for Brazilian Studies (LCBS) Working Papers

This Working Papers Series are coordinated by the Lemann Center for Brazilian Studies (LCBS) at

Columbia University in the City of New York. They disseminate policy reports, academic articles, and

preliminary research results encompassing relevant topics about Brazil from a variety of disciplinary

perspectives. We welcome submissions from Columbia faculty and graduate students, as well as visiting

scholars affiliated with the LCBS. Alumni students and scholars may also submit papers.

The Working Papers represents the research and the views of the authors. It does not necessarily

represent the views of the Lemann Center for Brazilian Studies.

ISSN-2470-6272

Table of Contents

1) Development Banking in Brazil: Challenges and Limits

Luiz Pinto & Marcos Reis………………………………………………………...................................Page 3

2) Fiscal policy in Brazil: from Counter-Cyclical Response to Crisis

Márcio Holland…………………………………………………………………………………………………Page 19

3) Reserve Requirements as a Macroprudential Instrument in Brazil and Colombia: Some Empirical

Evidence

Míriam O. S. Português & Antonio Luis Licha.................................................................Page 58

3 | L e m a n n C e n t e r f o r B r a z i l i a n S t u d i e s W o r k i n g P a p e r s | M a r c h 2 0 1 6

Development Banking in Brazil: Challenges and Limits

Luiz Pinto1 and Marcos Reis2

Abstract: This article examines the origins and evolution of long-term financing in Brazil. The need for government intervention in the form of a development bank is explained. Particularities of the Brazilian experience with its state-owned National Development Bank (BNDES) are described and analyzed. The final section tackles the challenges and limitations of the Brazilian system of long-term financing following the global credit crunch of 2008, when BNDES disbursements boomed because of major but unsustainable changes in its capital structure. The article concludes that the system for development finance in Brazil needs to be reformed in order to increase its efficiency and contribute to macroeconomic stability.

Keywords: development banks; long-term finance; BNDES; Brazil

1. Introduction

Global economic geography would probably be different if emerging market-based private groups and state-owned companies did not have the support of development banks. By fusing public policy with capital mobilization and investment management, development banks were crucial to boost catch-up industrialization and import substitution policies in Asia, Latin America, Africa and the Middle East. However, globalization, macroeconomic stabilization, financial market integration and capital market development forged major changes in the nature of development banks.

This paper aims to discuss the role of the Brazilian National Development Bank (BNDES) in the country’s evolving system for long-term finance. The paper is therefore structured in six sections, of which this introduction is the first. The second presents key concepts and definitions, establishing the baselines for theoretical and historical discussions on long-term finance and development banks. The third explains the origins of the BNDES and its remarkable record fostering industrial ventures and import substitution policies. BNDES support for economic modernization, market reforms and privatization during the 1990s and mid-2000s is analyzed in section four, while unorthodox policies designed to use BNDES as a post-Lehmann counter-cyclical tool are discussed in section five. Finally, section six outlines the concluding remarks.

2. Long-Term Finance and Development Banks

Development finance is the art of gathering funds to pay for multiyear payback capital-intensive undertakings. Mostly, these long-dated funds are deployed in different sorts of large-scale projects, including real estate enterprises, infrastructure, education, research, and the acquisition of capital goods, equipment and software. They are important to create jobs, expand production and increase productivity (G30, 2013).

Private sources such as commercial banks and capital markets supply most of the services for development finance demanded by developed economies. However, private sources are not able to fulfill the overall demand for funding, and especially so in emerging and developing economies, where market failures are often more relevant.

Long-term financing supply is significantly affected by the following market failures:

a) Financial markets incompleteness: because of their history of high inflation, depreciation and interest rate volatility, emerging and developing markets often suffer from so-called “original sin,” that is, a situation in which a domestic currency has a very low demand from non-residents, being unable to be used to borrow

1 Executive Director of BRICS Overseas, he holds a Ph.D. in International Political Economy and is a Visiting Scholar at the School of International and Public Affairs at Columbia University, New York. 2 Associate professor at the National Institute of High Studies (IAEN).

4 | L e m a n n C e n t e r f o r B r a z i l i a n S t u d i e s W o r k i n g P a p e r s | M a r c h 2 0 1 6

abroad or to borrow long-term (Eichengreen and Hausmann, 1999; Eichengreen et al., 2002; Céspedes et al., 2002). This fragility hits investors either through currency mismatches or maturity mismatches, preventing a thorough development of capital markets and a deepening of debt markets. Firms are therefore affected by credit constraints and capital scarcity;

b) Capital markets pro-cyclicality: financial and economic volatility tend to be intensified by the pro-cyclical character of the “price of risk” (Borio et al., 2001, Danielsson et al., 2004; Adrian and Shin, 2010; Bruno and Shin, 2014; and Borio et al., 2014). Emerging and developing markets are even more affected by monetary policy restrictions because of currency mismatches (Eichengreen and Hausmann, 1999; Eichengreen et al., 2002; Céspedes et al., 2002) and balance of payments dominance (Ocampo, 2013, 2009, 2003);

c) Higher risk aversion: future is uncertain by itself. As most prices are flexible and float, time creates additional risks to projects. The longer the projects, the higher the chances of a default. Moreover, activities related to the development of new products and technologies involve externalities grounded on high “discovery costs” (Mazzucato, 2013; Rodrik, 2004). Emerging and developing economies are often riskier because higher vulnerability to external shocks increases credit risks, market risks and liquidity risks. Banks and investors are therefore less prone to provide funding or execute complex, long-term innovation projects;

d) Coordination problems: long-term finance often faces a free-rider problem when credit markets are decentralized and dominated by private entities. Given that projects involving large sunk costs require co-financing in such credit markets, monitoring efforts tend to be left aside because of disincentives to individual investments. Insufficient monitoring, therefore, endangers project profitability, preventing funding supply (Dewatripont and Maskin, 1995). Lack of technical capacity to measure creditworthiness of long-term borrowers also affects the market (Sayers, 1957; Armendáriz de Aghion, 1999). Moreover, it is hard to coordinate complimentary investments when industries and activities are tackled by many externalities emanating from a productive structure that is specialized and heterogeneous (Rosenstein-Rodan, 1943; Prebisch, 1948; Hirschman, 1958; Rodrik, 2007; Lazzarini and Musacchio, 2014);

Thus, development finance should be enhanced by state policies. Governments have many instruments to cope with such market failures, including regulations, incentives and other indirect mechanisms. However, no policy is as direct and straightforward to foster funding as the provision of credit, equity and other financial services through development banks and development finance institutions.

Fusing public policy with investment banking, development banks are state-controlled institutions mobilizing resources from both capital markets and official sources to provide industrial, infrastructure and social enterprises with financial services. Development banks are mostly built to be lasting institutions sponsoring a large staff specialized in the preparation, appraisal, financing, implementation and evaluation of investment projects and programs. They operate through regular loans, concessional credits, equity investments, guarantees, and other special services such as funds for mergers and acquisitions, technical assistance, grants, policy dialogue, dissemination of best practices and research support.

Development banks frequently pursue a double bottom line mission. On the one side, governments are often the most important source of funds for development banks, providing resources through different mechanisms such as Treasury transfers, monetary or foreign exchange reserves, compulsory savings accounts, and special taxes. Such prevalence of official sources stress public and noncommercial goals of development banks. In the absence of good governance, this will likely favor soft budget constraints, excessive borrowing, moral hazard, adverse selection, cronyism and crowding out. On the other side, development banks “banking” mission reveals they can be self-sustaining and financially viable, carrying out prudent financial and risk management policies. Should development banks achieve good governance, they will be financially sound and push for a “crowd-in,” acting as catalysis for the development of capital markets by providing information and developing standards for long-term projects.

Development banks were first created in Continental Europe and Japan, where they emerged to help boost rapid industrialization and growth (Gershenkron, 1962; Cameron, 1961; Diamond, 1984; Yasuda, 1993; Armendáriz de

5 | L e m a n n C e n t e r f o r B r a z i l i a n S t u d i e s W o r k i n g P a p e r s | M a r c h 2 0 1 6

Aghion, 1999). In 1822, the Societé Général pour Favoriser L’Industrie Nationale was created under the sponsorship of the Dutch government. Not long thereafter, between 1848-1852, France launched relevant industrial banks such as Crédit Foncier, Comptoir D’Escompte and Crédit Mobilier. These experiences inspired the creation of the Industrial Bank of Japan in 1900.

However, development banks became part of the mainstream strategies only after the Second World War. As of 1944, financial services in both developed and developing economies were still facing great challenges posed by two “total wars” and the Great Depression. Private markets had collapsed and many countries in Europe and Asia needed long-term finance and hard currencies to recover their infrastructure and industry. This is why the “embedded liberalism compromise” (Ruggie, 1982) supported by the United States in Bretton Woods partially relied on the creation of the International Bank for Reconstruction and Development (IBRD)3 to deploy funds for projects with longer maturity. Some of the most important national development banks were created during the 1940s and 1950s supported by the IBRD and special American programs designed to halt Soviet influence through funding supply and technical and planning services (Marshall Plan, Colombo Plan and Joint Bilateral Commissions). Institutions created under these arrangements include the German Kreditanstalt fur Wiederaufbau Bankengruppe (KfW), the Development Bank of Japan (DBJ), the Korean Development Bank and the Brazilian Development Bank (BNDES).

Development banks were particularly compelling for governments and elites seeking to solidify structural transformations in their countries through catch-up industrialization or import substitution industrialization. Such elites embraced the “development” or “industrial” view in which state-owned development finance institutions are necessary to foster the creation of new capabilities and breakthroughs. State capital should nevertheless decrease in size and importance over time. Debt and equity markets tend to deepen and develop when macroeconomic stabilization is achieved and official funds prompt learning externalities, economic diversification and coordination (Hausmann and Rodrik, 2003; Musacchio and Lazzarini, 2014).

Beyond their traditional activities providing loans for long maturity projects and equity capital to national firms, development banks started a diversification process during the 1980s and 1990s, adapting themselves to liberalization and globalization. After the opening of capital accounts, macroeconomic stabilization and institutional reforms, debt and equity markets developed and state-owned banks had to engage in new arrangements with the private sector. Henceforth, development banks established new operations and offered other financial services, including working capital financing, venture capital financing, syndications, insurance, brokerage and investment banking services, advisory and consulting services, privatization, ownership restructurings and technical assistance.

According to Nicholas Bruck (1998), there are over five hundred national development banks worldwide. They concentrate in emerging and developing markets. Despite wide differences regarding size, value of financial assets, outstanding debts, capital structure, ownership structure, governance, and financial and risk management policies, development banks offer similar services.

Nowadays, according to a study benchmarking development finance institutions, conducted by the Business Development Bank of Canada (2009), the main sectors targeted by development banks are micro-enterprises/start-ups, small and medium sized enterprises (SMEs), international trade/globalization, housing, infrastructure, and rural/ agricultural sector.

3 The International Bank for Reconstruction and Development (IBRD) is the first agency of what is now known as the World Bank Group.

6 | L e m a n n C e n t e r f o r B r a z i l i a n S t u d i e s W o r k i n g P a p e r s | M a r c h 2 0 1 6

Currently, important development banks include national and multilateral entities (Table 1).

Table 1: Development Banks, USD million (2013)

Total Assets

Total Loans

Debt Ratio

D/E Ratio

NIM ROA ROE

National Development Banks

China Development Bank 1,352,844 1,181,065 0.93 13.57 0.02% 1.02% 15.07%

German Development Bank (KfW)

640,850 159,566 0.95 21.67 0.56% 0.26% 6.57%

BNDES 332,228 121,673 0.91 11.20 1.54% 1.02% 12.85%

Korean Development Bank

159,305 94,917 0.88 7.94 0.02% -0.98% -8.80%

Development Bank of Japan

158,248 147,987 0.84 5.40 0.00% 0.51% 2.86%

Multilateral Development Banks

IBRD 325,601 143,667 0.87 7.23 1.58% 0.06% 0.55%

Asian Development Bank 115,868 53,088 0.85 5.76 1.16% 0.48% 3.37%

IDB 97,007 70,782 0.77 3.11 2.03% 1.34% 5.54%

Source: Author’s elaboration based on data from Banks’ annual reports and Bloomberg

3. Brazilian National Development Bank (BNDES)

Brazil started major transformations in its productive structure just after the outbreak of the Great Depression. Manufacturing sectors such as perishable and semi-durable goods surged in the 1930s and 1940s. Bilateral agreements between Brazil and the United States created an agenda for the development of industrial projects during the Second World War. Under the so-called “Washington Accords,” the United States provided technical assistance and financing for strategic capital-intensive projects, including a big steelworks company (CSN) and a large-scale iron ore mining enterprise (Vale do Rio Doce). Moreover, the American Technical Mission (Cooke Mission) conducted the first comprehensive study diagnosing the Brazilian economy, recommending sectorial development of transport, fuel, textiles, minerals, chemicals, and education.

However, the war also imposed a scarcity of inputs for both infrastructure and industry in Brazil, causing a depreciation of fixed capital stocks. Hence, after the US released its programs to support economic reconstruction in Europe and Asia, Brazil asked for technical and financial cooperation in similar terms. Washington answered creating the Brazil-United States Technical Commission (Abbink Mission) and the Joint Brazil-United States Development Commission (CMBEU). While the Abbink Mission designed the first draft of a development plan for Brazil, outlining several investment projects, the CMBEU developed a “bottleneck” approach to prioritize investments. In addition, the CMBEU conducted feasibility studies for the projects, infusing planning, project development and project management technology in Brazil.

CMBEU and the National Plan for Economic Renovation considered infrastructure depreciation as the main bottleneck preventing industrial development. Thus, most of the 41 projects suggested by the CMBEU were either energy or transport related. Resources for project development were to be granted by the IBRD and American Export-Import Bank. In order to have access to these loans and grants, Brazil had to mobilize resources to supply projects with local currency. A modern mechanism for large-scale capital mobilization had to be developed. Industrial projects could not rely only on non-recoverable loans from the national budget, and no one would be willing to voluntarily lend long-term because of inflation and macroeconomic instability. Thus, the government opted to create compulsory savings (i.e., involuntary contribution of firms, workers, consumers and individuals for saving funds managed by public institutions). As of 1952, the Fund for Economic Renovation (FRE)

7 | L e m a n n C e n t e r f o r B r a z i l i a n S t u d i e s W o r k i n g P a p e r s | M a r c h 2 0 1 6

was established, receiving compulsory loans from a 15% extra fee to income tax, a compulsory collection of 4% of all deposits from the Federal Housing Bank and of 25% of technical reserves from insurance and capitalization companies (BNDES, 2002).

FRE was nevertheless unable to undertake infrastructure and industrial projects without additional expertise and administrative support. Therefore, the CMBEU suggested that a development bank should be founded to intermediate and manage resources mobilized for the investment projects and programs. The Brazilian Development Bank (BNDES)4 was hence created as a development finance device applying the most up-to-date technics available for project preparation, appraisal, financing, implementation and evaluation.

International funding from the IBRD and the Export Import Bank were canceled after the rise of Dwight Eisenhower to power in the US and the nationalistic path taken by president Getulio Vargas in the end of his second government (1950-54). From 1952 until 1966, funding for the BNDES mostly came from the FRE (32%) and from restricted funds created to foment specific sectors such as electricity, railways, capital goods and equipment. During this period, the BNDES focused its operations in a small number of big projects, including hydroelectric power stations, transmission lines and steelworks, being an agent for the “big push” (“50 years in 5”) conducted by the Target Plan of president Juscelino Kubitschek (1955-60).

Political instability and the lack of strong democratic institutions facilitated the implementation of a military dictatorship in 1964. Two years later, compulsory savings for the FRE ceased and the BNDES had to struggle to mobilize funds from the fiscal budget and monetary reserves. Activities were nevertheless kept and the BNDES relied on restricted funds to diversify its portfolio. During this period, support for private projects prevailed over public projects because restricted funds for infrastructure were reallocated to state-owned companies such as the Federal Railway Network S.A., the Brazilian Hydroelectric Centers S.A. (Eletrobras) and the Brazilian Steel S.A. (Siderbras). From 1964 until 1967, 43% of the USD 1.3 billion funding of the BNDES came from restricted funds, with the Fund for Industrial Plant and Machinery Financing (Finame) being the most relevant (Prochnik, 1995; BNDES, 1966-72).

Despite low annual real growth rates of GDP in 1964-67, stabilization and banking and capital market reforms conducted by finance minister Otávio Gouveia de Bulhões, planning minister Roberto Campos and central bank governor Mario Henrique Simonsen set the conditions for an economic modernization and expansion. Under these reforms, the experience of BNDES with long-term financing was important for the indexing of financial instruments. The mechanism was essential because government bond indexation allowed noninflationary financing of the budget deficit (BNDES, 2002).

Starting in 1968, Brazil underwent an economic boom known as the “Brazilian miracle” (1968-72), during which the GDP annual growth rate averaged 11.3% (Baer, 2014). Even after the oil shock of 1973 Brazil was able to push economic growth through the Second National Development Plan (IIPND) of president Ernesto Geisel. From 1973 until 1979, average annual GDP grew 6.8% (IBGE, 2003). BNDES was important for this outcome. During the “miracle,” disbursements from the BNDES reached USD 2.6 billion, a great amount compared to the USD 988 millions of total disbursements in 1952-68. In other words, annual disbursements averaged USD 520 million during the “miracle” and USD 58 million during the previous period. Annual disbursements from the BNDES averaged an increase of 48% per year in 1968-72.

By 1971, the consulting company Booz Allen Hamilton advised Brazilian authorities on administrative reform aiming to transform the BNDES’ governance and structure. In order to guarantee more independence and flexibility for the BNDES, the reform established its transition from a public agency to a state-owned company. Moreover, a new funding policy permitted the continuity of the expansion of BNDES after 1973. Instead of relying only on restricted funds, fiscal budget and monetary reserves, the BNDES gained access to compulsory savings from firms through the newly established Social Integration Program and Public Employee Savings Program

4 BNDES is the Portuguese acronym for Banco Nacional de Desenvolvimento Econômico e Social.

8 | L e m a n n C e n t e r f o r B r a z i l i a n S t u d i e s W o r k i n g P a p e r s | M a r c h 2 0 1 6

(PIS-PASEP). From 1974 until 1979, funds from PIS-PASEP accumulated USD 9.4 billion, helping to support disbursements of USD 20 billion and sustain an average increase in disbursements of 33% per year. Additionally, during this period, the BNDES created three subsidiaries—Embramec, Fibase and Ibrasa—to intervene in the capital markets, taking minority equity positions in companies deemed strategic for the national development.

BNDES was in fact the main agent behind the import substitution policies designed by president Geisel for sectors such as capital goods and basic inputs. Thus, the BNDES undertook major projects in steel, paper and pulp, petrochemicals, caustic soda, tin, zinc and aluminum, cement and fertilizer. However, everything was happening while the country’s foreign debt surged. External resources were important to fund gross capital formation, and net foreign debt increased at a yearly rate of 38.7% from USD 6.2 billion in 1973 to USD 31.6 billion in 1978. Furthermore, the share of public and publicly guaranteed debt of total medium- and long-term debt rose from 52% in 1973 to 63% in 1978 (Baer, 2014).

Two shocks led Brazilian rapid development to an abrupt end by the late 1970s and early 1980s: the second oil shock (doubling petroleum prices) and the US Federal Fund Rates hike (1000 basis points increase to 20%). Drastic movements affected the Brazilian current and capital accounts. Debt services increased from 30% of export earnings in 1974 to 83% in 1982. GDP growth rate plummeted to -4.5% in 1981. The “Lost Decade” loomed as the twilight of a long period of catch up and high GDP growth rates. From 1981 until 1990, nominal GDP growth averaged 1.6% yearly (IBGE, 2003). The Brazilian economy had to face a new age of fiscal crises, currency depreciation and high inflation. Adjustments became even more necessary in a period in which democratization and a new constitution added pressure on the fiscal budget.

BNDES had a fundamental role in this period, when most of the public agents and decision makers shortened their time horizons. Switching a sectorial approach based on individual projects to a method grounded on strategic planning, the BNDES crafted scenario analyses and changed its strategy accordingly. By 1984, the BNDES concluded that the age of state-led development was over. Under the “competitive integration” slogan, and based on a diagnostic pointing to the exhaustion of import substitution industrialization and public savings, the BNDES supported a new view about the role of the state, foreign capital and industrial policies (Mourão, 1994). Brazilian industry was no longer in “infancy.” Local entrepreneurs already had enough capacity to mobilize capital for complex projects, while state-owned companies were facing severe investment restrictions and political interferences.

By the beginning of the 1980s, dozens of companies that were originally private eventually fell under the BNDES control because of nonpayment of loans. Thus, the BNDES designed, organized and promoted the privatization of 14 companies in which it had equity majority. Moreover, the BNDES restructured its equity arm, unifying Embramec, Fibase and Ibrasa under a new subsidiary for capital market interventions called BNDES Participation (BNDESPAR).

Return on operations became the BNDES main funding source for the first time in 1981. Later on, the new Federal Constitution of 1988 established in its article number 239 that at least 40% of compulsory savings from PIS-PASEP should be channeled to BNDES for development finance, while the remaining 60% should finance the program for unemployment insurance and salary bonuses. As of 1990, with the Law Nº 7.998, savings from PIS-PASEP were unified under the Worker’s Assistance Fund (FAT).

Macroeconomic stability worsened in the end of the 1980s and the beginning of the 1990s. Hyperinflation and currency devaluation created economic chaos. The annual rate of inflation reached 2739% in 1990 and averaged 1400% between 1989 and 1994 (IBGE). Several economic plans failed one after another. Economic despair and political drama followed until the unleashing of the “Real Plan” in 1993 and 1994. Based on a de facto exchange-rate targeting regime (crawling peg), and benefiting from measures such as transparency, fiscal adjustment and a new indexing system, the Real Plan succeed in curbing hyper and very high inflation, paving the way for further economic modernization in Brazil.

9 | L e m a n n C e n t e r f o r B r a z i l i a n S t u d i e s W o r k i n g P a p e r s | M a r c h 2 0 1 6

4. Development Banking for Market Reforms

As of 1996, Brazilian yearly inflation measured by the internal general price index (IGP-DI) eased to one-digit figures for the first time since 1952 (IBGE). At first, price stability affected the so-called “inflation gains” of financial intermediaries in Brazil, demanding central bank intervention, new prudential regulations and government-sponsored devices for ownership restructuring (Studart, 2000; Baer and Nazmi, 2000). However, after the tapering of banking fragility, the Brazilian financial system was finally able to benefit from macroeconomic stabilization. Secondary capital markets developed and deepened, while investment and pension funds changed their strategy and portfolio, holding less short-term indexed bonds and estate assets and riskier positions. Under these conditions, new players loomed as potential or actual providers of long-term funds.

BNDES had an important role adapting itself and the Brazilian industry for the new economic momentum. Unlike other public agencies, the BNDES was aware of the exhaustion of the previous pattern of development financing and embraced economic reforms from the beginning. Therefore, the BNDES acted to “crowd in” private investments and develop capital markets, managing the famous National Privatization Program (PND). From 1990 to 2003, the BNDES directed 69 privatizations in sectors such as steel, chemical and petrochemical, fertilizers, electricity, rail transport, mining, ports, financial, and petroleum. Privatization included the transfer of control from government to the private sector and other operations such as concessions, leases and sales of minority stakes. Total results from the sale of companies, disposal of minority shares and concessions amounted to USD 39.7 billion (BNDES, 2003).

BNDES played three roles in the PND (Musacchio and Lazzarini, 2014):

(a) Operational agent of privatization transactions involving the sale of controlling blocks of state-owned companies;

(b) Financing provider for the buyers in some of the transactions; (c) Equity participation through its equity-holding arm, BNDESPAR.

During the 1990s and early 2000s, 86% of privatization revenues came from sales of controlling blocks, of which 53% were acquired by consortiums comprised of domestic groups, foreign investors and public entities such as the BNDESPAR and pension funds of state-owned companies. These include Previ (Banco do Brasil), Petros (Petrobras) and Funcef (Caixa Economica Federal) (Anuatti-Neto et al., 2005; Paula, 2002; Lazzarini, 2011).

Loans and equity capital from the BNDES were a sine qua non condition for a successful privatization program. Bids on controlling blocks in former state-owned companies would hardly reach minimum prices without a strong support from the BNDES and pension funds. Thus, the Brazilian state kept a strong presence in the economy even after privatization. According to Lazzarini (2011) and Musacchio and Lazzarini (2014), ownership restructurings in Brazil led to a decrease in the role of the state as a majority investor, but increased its power centrality5 and its position as a minority shareholder. Governmental entities, under the leadership of the BNDESPAR, ramped up their centrality in comparison to an average owner from 131% in 1996 to 553% in 2009. Similarly, pension funds from state-owned companies increase their centrality from 224% to 936% during the same period. In other words, the Brazilian state was able to boost its corporate influence by flexing the muscles of state-related entities holding dispersed stakes in several privatized, listed and non-listed companies.

Such arrangement also favored the development of financial services in Brazil. Few industries were as modernized as the banking industry. From 1995 to 2002, major changes affected the ownership structure of Brazilian banks. Private institutions supplied more credit than public institutions for the first time in 1999.

5 Power centrality or Bonacich centrality refers to the direct and indirect laces linking agents in a given network. In this case, the ownership networks in Brazil. Different connection degrees or centrality implies influence inequality among owners within a network. Centrality is therein the degree to which a group of owners distance themselves from the average connectivity of owners within the network.

10 | L e m a n n C e n t e r f o r B r a z i l i a n S t u d i e s W o r k i n g P a p e r s | M a r c h 2 0 1 6

Moreover, foreign banks increased their operations in this period, mostly after acquiring banks previously owned by state governments.

Figure 1: Share of Credit Operations by Bank Ownership, 1995-2002

Source: Author’s elaboration based on data from the Central Bank of Brazil

A balance of payment crises following the external shocks coming from Asia (1997) and Russia (1998) led Brazilian authorities to conduct a transition from the exchange-rate targeting regime to a inflation-targeting regime in 1999. Crawling peg to the dollar was abandoned and the new floating exchange rate required a new nominal anchor. The macroeconomic regime was thus grounded on a tripod including a (i) target inflation rate, a (ii) target primary surplus to reduce the debt-to-GDP ratio, and a (iii) floating exchange rate. Communication and accountability became vital (Bogdanski et al., 2000), and new policies enhanced credibility and favored a stronger external position. Such endeavors improved Brazilian fiscal position and helped to drastically reduce inflation volatility (Segura-Ubiergo, 2012).

The macroeconomic tripod including its inflation-targeting regime persisted even after the substitution of President Fernando Henrique Cardoso’s Social-Democratic Party (PSDB) with the left-leaning Worker’s Party (PT) of president Luiz Inacio Lula da Silva in 2003. The new macroeconomic model was indeed furthered during the first term of President Lula (2003-2006). Lower levels of inflation and inflation volatility allowed real interest rates to plunge from an average of about 20% during the exchange-rate targeting regime to an annual average of about 10% during 2000-2005 and to below 8% between 2006 and 2009 (Segura-Ubiergo, 2012). Expectations over inflation and interest rates were tamed by the central bank (Bevilaqua et al., 2007), fostering the development of capital and debt markets. Stock markets boomed, attracting new entrepreneurs, promoting better practices of corporate governance and enlarging the investor base.

Figure 2: Market Capitalization of Listed Companies in Brazil, 1995-2011

Source: Author’s elaboration based on data from the World Development Indicators

0%

20%

40%

60%

80%

0%

20%

40%

60%

80%

1995 1996 1997 1998 1999 2001 2002

Public Banks

Private Banks

0.00%

20.00%

40.00%

60.00%

80.00%

100.00%

120.00%

0

500

1000

1500

2000

Market Capitalization ofListed Companies (USDBillion)

Market Capitalization ofListed Companies (% ofGDP)

11 | L e m a n n C e n t e r f o r B r a z i l i a n S t u d i e s W o r k i n g P a p e r s | M a r c h 2 0 1 6

5. Development Banking in the Post-Crises Blues

Despite structural reforms and relevant improvements in the macroeconomic setting, the Brazilian sovereign yield curves in domestic currency are persistently volatile and high, preventing private agents from borrowing long-term and blocking the development of a free market for long-term credit at fixed interest rates in Brazilian Reais (BRL) (Sotelino, 2014).

Moreover, real interest rates are much higher in Brazil than in other emerging and developing markets. While short-term real interest rate is 5.64% in Brazil, other BRICS and MINT countries benefit from far better rates, including 4.10% for China, 3.60% for Russia, 2.75% for India, 1.06% for Indonesia, 0.51% for Turkey, 0.45% for South Africa and -1.08% for Mexico (Trading Economics).6

Figure 3: Brazilian Sovereign Yield Curve, LFT, LTN and NTN-F (Selic-based and fixed-rate bonds)

Source: Author’s elaboration based on data from the Central Bank of Brazil and National Treasury

This is a major problem for the sustainable development of capital markets in Brazil. Monetary stability and low rate risks increase the demand for long-term debts. Longer debt duration implies higher confidence and creditability, fostering the creation of benchmarks for debt markets and the widespread use of long-term commercial papers. High and volatile real interest rates express how the institutional construction of Brazilian stability is still incomplete (Lopes 2010).

Structural distortions such as the very short-term structure of debt stocks and country-specific factors related to credit market segmentation diminish the effectiveness of monetary policy. Having access to cheap funds based on compulsory savings arrangements, state-owned banks are able to supply credit at better-than-market terms, presenting less sensitivity to movements of the overnight market rate on federal debt repos (SELIC).

BNDES pays the so-called Long-Term Interest Rates (TJLP)7 for most of its funds.8 Being much lower and much less volatile than SELIC (Chart IV), the TJLP is the cornerstone of long-term financing in Brazil. Although it helps

6 February 5th, 2015. 7 A reference rate set quarterly by the Brazilian Monetary Council. 8 Debt with FAT-Constitutional is subordinated or quasi-equity. No amortizations are made while interests are paid semi-annually. Interests are limited to 6% per year for the TJLP liabilities. The excess yield is capitalized and added to the outstanding balance of FAT funds. Special Deposits FAT is comprised of additional resources channeled to the bank when

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

0 1 2 3 6 8 10

Years

12 | L e m a n n C e n t e r f o r B r a z i l i a n S t u d i e s W o r k i n g P a p e r s | M a r c h 2 0 1 6

to provide cheaper funding for entrepreneurs, it also lessens the power of monetary policy. Thus, along with the subsidized loans from Banco do Brasil and Caixa Economica Federal for housing and agriculture, the BNDES disbursements push upwards the equilibrium real interest rate in the free market (Segura-Ubiergo, 2012; Lopes, 2010; Bacha, 2010; Lara Resende, 2013).

Figure 4: Monthly rates of SELIC and TJLP (%), 2002-2015

Source: Author’s elaboration based on data from the BNDES and Central Bank of Brazil

However, the FAT—the only steady external source of funds for the BNDES—is depleting, which poses challenges for the future expansion of BNDES’ operations. The annual average of total net inflows from FAT as a share of total disbursements decreased from 14% in 2000-06 to 4.5% in 2007-14. Although net inflows from FAT-Constitutional are keeping pace with disbursements, higher minimum wages and increasing employment formalization are ramping up FAT annual expenditures with unemployment insurance, pushing FAT-Special Deposits net balance to negative levels and reducing total net inflows from FAT to the BNDES. FAT-Special Deposits net balance deteriorated quickly, plummeting from a positive amount of BRL 20 billion in 2000-06 to a negative amount of BRL 7.1 billion in 2007-14.

Figure 5: Net Inflows from FAT and Total Disbursements, 2000-2013

Source: Author’s elaboration based on data from BNDES’ annual reports

revenues from FAT exceed annual expenditures required by the legislation. BNDES’ USD-related liabilities pay USD LIBOR flat.

0.00

5.00

10.00

15.00

20.00

25.00

30.00

35.00

40.00

45.00

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

SELIC

TJLP

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

0

20

40

60

80

100

120

140

160

180

200

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

Total Disbursements, BRLBillion

Total Net Inflows fromFAT/ Disbursements

13 | L e m a n n C e n t e r f o r B r a z i l i a n S t u d i e s W o r k i n g P a p e r s | M a r c h 2 0 1 6

Net outflows from FAT-Special Deposits started amidst a surge in total disbursements. The gap was nevertheless more than fulfilled by resource mobilization from the National Treasury. From 2002 through 2014, the National Treasury funded the BNDES with BRL 426 billion. BNDES capital structure thus changed accordingly, with the participation of the National Treasury increasing from BRL 3.8 billion or 3.4% of total in 2001 to BRL 450 billion or 54% of total in 2014. FAT relative participation in the capital structure decreased from BRL 69.4 billion or 61.5% of total to BRL 192.4 billion or 23% of total during the same period.

Reasons behind government support of the BNDES include anti-cyclical policies after the subprime meltdown of 2007 and credit crunch of 2008, a renewal bet on industrial policies “picking winners” and fostering “national champions,” and progressive changes on macroeconomic policies leading to the so-called “new economic matrix” of president Dilma Rousseff. New government bonds were issued by the National Treasury to channel funds to the BNDES. Differences between government borrowing costs and subsidized TJLP imply resource mobilization from the National Treasury to the BNDES have a fiscal impact, affecting the gross national debt and crowding out private investment.

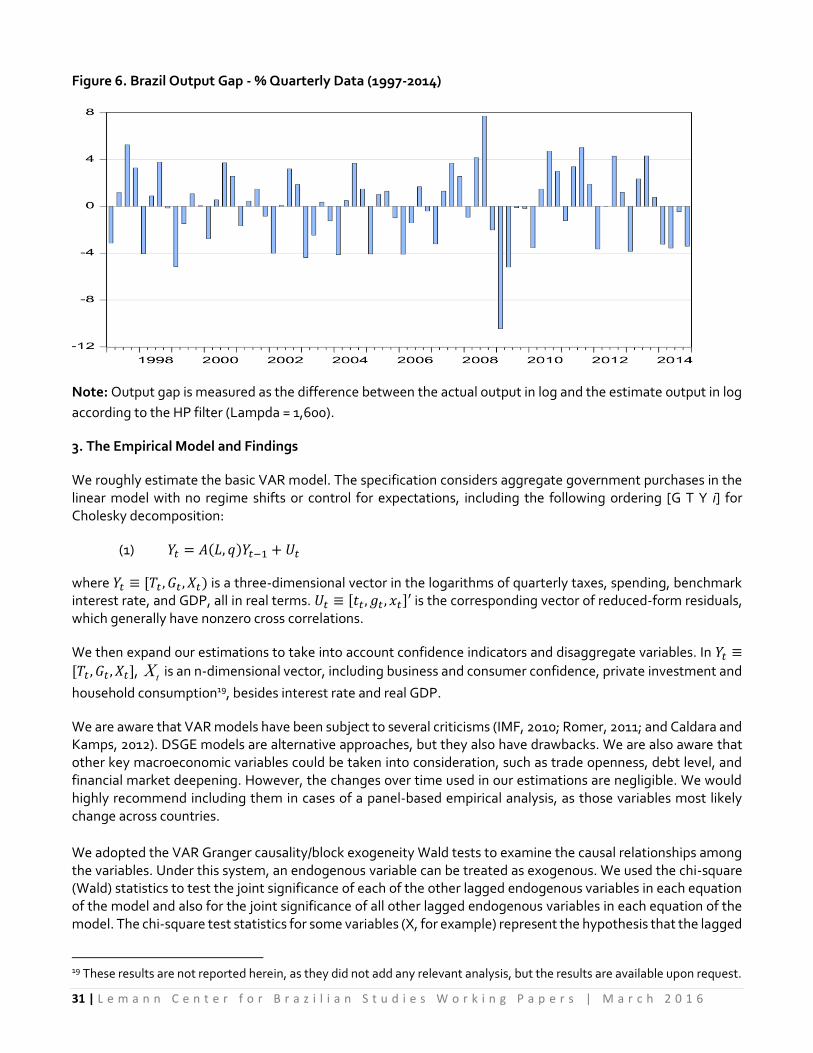

From 2004 to 2014, BNDES’ total assets increased over five-fold in BRL and over six-fold in USD to BRL 834,756 million or USD 356,733 million in 2014 (Figure 6). Similarly, BNDES disbursements ramped up over four-fold in BRL and over five fold in USD to BRL 187 billion or USD 80 billion in 2014 (Figure 7).

Figure 6: Total Assets, 2004-2014

Source: Authors’ elaboration based on BNDES and IPEA data

0

100,000

200,000

300,000

400,000

500,000

600,000

700,000

800,000

900,000

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

BRL USD

14 | L e m a n n C e n t e r f o r B r a z i l i a n S t u d i e s W o r k i n g P a p e r s | M a r c h 2 0 1 6

Figure 7: BNDES Disbursements, 2004-2014

Source: Authors’ elaboration based on BNDES and IPEA data

Expansion in earmarked loans attained remarkable success preventing a credit crunch and a recession in Brazil; however, the macro, industrial and social views prevailing in the government pushed for a continuing mobilization of funds even after the economy fully recovered. Out of the BRL 413 billion raised by the National Treasury to the BNDES since the beginning of the international financial crisis in 2007, BRL 283 billion or 66% was raised after 2009, when the Brazilian economy rebounded strongly. The new matrix of Brazilian economic policies boosted government-driven credit expansion, which ramped up participation of state-owned banks in the national credit market.

Figure 8: Share of Credit Operations by Bank Ownership, 2002-2013

Source: Authors’ elaboration based on data from the Central Bank of Brazil

0

20

40

60

80

100

120

140

160

180

200

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

BRL USD

0%

10%

20%

30%

40%

50%

60%

70%

80%

0%

10%

20%

30%

40%

50%

60%

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Public Banks

Private Banks

15 | L e m a n n C e n t e r f o r B r a z i l i a n S t u d i e s W o r k i n g P a p e r s | M a r c h 2 0 1 6

During this period, BNDES surpassed Santander and consolidated its position as the fifth largest bank by total assets and total loans in Brazil (Table 2).

Table 2: Largest Banks in Brazil, BRL million (2013)

Total Assets

Total Loans Debt Ratio

D/E Ratio NIM ROA ROE

Banco do Brasil 1,437,485 645,674 0.41 6.87 3.93% 1.20% 21.88%

Itau Unibanco 1,105,721 412,234 0.37 5.05 4.77% 1.52% 20%

Caixa Economica Federal

858,325 485,487 0.43 10.24 2.81% 0.86% 22.63%

Bradesco 838,301 323,979 0.4 4.67 4.84% 1.45% 16.92%

BNDES 784,857 287,148 0.91 11.20 1.54% 1.02% 12.85%

Santander Brasil 453,052 226,206 0.35 3.55 5.68% 1.18% 7.03%

Safra 124,399 48,662 0.59 10.34 4.21% 1.09% 19.09%

BTG Pactual 120,888 18,119 0.16 1.55 7.32% 2.29% 21.65%

Source: Author’s elaboration based on data from banks’ annual reports and Bloomberg

Holding a virtual monopolist position over long-term financing, BNDES channels subsidies from compulsory savings and Treasury transfers to its customers. BNDES’ net interest margin (NIM) was 1.54% in 2013, 325 basis points lower than the average of the eight largest banks in Brazil, 183 basis points lower than the average of the two biggest state-owned banks and 376 basis points lower than the average of the five largest private banks.

Yet, BNDES had a net income of BRL 8,150 million in 2013. However, gross income from loans registered a loss of BRL 1,649 million, being offset only by the BRL 11,271 million earned by returns on securities. It is worth noting that 72% of the BRL 160,829 million held by the BNDES in securities is state-related, including BRL 62,934 million in government and sovereign bonds and BRL 39,830 million in shares from state-owned companies. If subsidies for its funding were eliminated, BNDES’ net interest margin would drop from 1.54% to -4.37% in 2013. In other words, taxpayers spent over 4 cents for every dollar allocated by the BNDES during the year.

Subsidies are justified whenever government driven loans fulfill market failures, funding projects that cannot be funded by private markets but whose social benefits exceeds their financial costs. This includes credit to capital constrained firms and social intensive sectors.9 However, recent empirical analyses and econometric studies strongly support that BNDES’ operations do not maximize social welfare (Bonomo et al., 2014; Lazzarini et al., 2015; Mello and Garcia, 2012; Sousa, 2010). BNDES channels 67% of its total disbursements to large enterprises that can fund their projects with other sources of capital. Moreover, such trends have strengthened after the international financial crisis and the surge on government driven credit. Recently, larger, older and less risky firms benefited most from government-sponsored loans. Monopolistic firms have 18% higher chances of receiving loans from the BNDES than other firms – chances were 11% higher before 2007. Additionally, BNDES reduced its relative participation in social intensive sectors by 25% after the international crisis (Bonomo et al., 2014).

Resources allocated to large “national champions” could still be justified if loans and equity capital had a positive effect on firms’ performance, investment or productivity, funding their riskier projects and boosting innovation. But data shows no significant effect of BNDES loans and equity capital on firms’ profitability, market valuation (Lazzarini et al., 2015), productivity (Sousa, 2010), investment and capital expenditures (Bonomo et al., 2014; Lazzarini et al., 2015). There is simply no evidence that services provided by the BNDES stimulate potential output growth. Rather, evidence suggests publicly listed firms are borrowing long-term to either reduce capital costs or even benefit from interest rate arbitrage profit (Bonomo et al., 2014).

9 Social intensive sectors can include infrastructure, education, health, housing and agriculture.

16 | L e m a n n C e n t e r f o r B r a z i l i a n S t u d i e s W o r k i n g P a p e r s | M a r c h 2 0 1 6

Thus, Brazil clearly needs to reform its development banking system. The national government can indeed undermine macroeconomic stability if it keeps using BNDES to artificially expand credit or to support para-fiscal policies and accounting gimmicks. Dilma’s new economic team is willing to reinforce the inflation target regime and implement fiscal discipline. Among other measures, the new team supports a slow down on government driven credit and smaller SELIC-TJLP spreads.

However, the BNDES needs deeper changes. Funding structure and implicit subsidies imply disbursements should support projects with higher social externalities. In this sense, BNDES targeting and selecting policies may follow the trend created by leading development finance institutions, increasing the share of social intensive projects in its portfolio. Priorities may include micro-enterprises and start-ups, small and medium sized enterprises (SMEs), infrastructure, and international trade. Project monitoring and control should be enhanced, subjecting firms to performance targets conditional on their allocated capital. Finally, given the structural limits of compulsory savings and macroeconomic restrictions to further Treasury transfers, the BNDES should improve its governance and rely more on market funding and private sources of savings and widen market-based operations and off-balance sheet activities such as syndications, co-finance operations, project finance and underwritings.

6. Conclusions

Firms based in emerging markets often face capital constraints and other restrictions because of market failures such as financial incompleteness, capital markets pro-cyclicality, risk-aversion and coordination problems. Hence, emerging markets have to foster development finance through public policy. Harnessing state-owned development banks became one of the most effective ways to provide long-term finance and boost industrialization after the Second World War. However, globalization, liberalization, stabilization and privatization raised many challenges for traditional development banking in the 1990s and mid-2000s. Good governance, transparency and market-based operations turned out to be even more essential for financial sustainability thereafter. To some extent, all development banks had to adapt to the new set of best practices.

BNDES is the third largest development bank by total assets and fifth largest by total loans. One of the cornerstones of the Brazilian “developmental state,” the BNDES funded the most important infrastructure and industrial projects of the 1950s, 1960s and 1970s, nourishing a catching up process that consolidated a large base of diversified private groups. Despite its protagonist role during the “golden years” of Brazilian style state capitalism, BNDES embraced economic reforms after the international debt crisis exhausted import substitution policies and public savings in the 1980s. Crowding in private investors and developing capital markets, the BNDES operated and managed the National Privatization Program (PND).

Along with the macroeconomic stabilization, the PND created conditions for further modernization. Paradoxically, although ownership restructurings diminished state participation as a majority investor, it boosted its corporate influence as a minority shareholder. Positions were held through BNDES’ equity arm BNDESPAR and state-related entities such as pension funds of state-owned companies. Thus, the government was able to increase its power centrality while major changes increased the performance of former state-owned companies, favoring the development and deepening of capital and credit markets.

However, the subprime meltdown of 2007 and the global credit crunch of 2008 blocked the ongoing process of capital market development in Brazil. Hence, the BNDES was used to boost a credit-driven anti-cyclical program. Disbursements increased three fold, while funds were mobilized through government bond emissions. Proponents of economic interventionist policies gained momentum and pushed for a continuing mobilization of funds even after the economy fully recovered. Thus, selection problems increased and earmarked loans became less efficient.

Following these endeavors, Brazil now needs to reform its development banking system. BNDES funding structure and implicit subsidies imply disbursements should support projects with higher social externalities. In

17 | L e m a n n C e n t e r f o r B r a z i l i a n S t u d i e s W o r k i n g P a p e r s | M a r c h 2 0 1 6

this sense, targeting and selecting policies may follow the trend created by leading development finance institutions, increasing the share of social intensive projects in its portfolio. Finally, given the structural limits of compulsory savings and macroeconomic restrictions to further Treasury transfers, the BNDES should improve its governance and rely more on market funding and private sources of savings and widen market-based operations and off-balance sheet activities such as co-finance operations, project finance and underwritings.

References Cited

ARMENDÁRIZ DE AGHION, B. (1999): “Development Banking” Journal of Development Economics 58(1), pp. 83-100.

BACHA, E. (2010): “Alem da Triade: Ha como reduzir os juros?”, Working Paper Nº 17, Instituto de Estudos de Politica Economica Casa das Garças, Rio de Janeiro, Brazil.

BAER, W. (2014): The Brazilian Economy: Growth and development. Boulder, CO: Lynne Rienner Publishers. BAER, W. and NAZMI, N. (2000): “Privatization and Restructuring of Banks in Brazil” The Quarterly Review of

Economics and Finance 40(1), pp. 3-24. BNDES (2012): BNDES: Um banco de histórias e do futuro. Rio de Janeiro: BNDES. BNDES (1995/2014): Individual and Consolidated Financial Statements. Rio de Janeiro: BNDES. BNDES (1966/1994): Relatorios de Atividade. Rio de Janeiro: BNDES. BEVILAQUA, A., MESQUITA, M. and MINELLA, A. (2007): “Brazil: Taming inflation expectations”, Working Paper

Nº 129, Banco Central do Brasil, Rio de Janeiro. BOGDANSKI, J., TOMBINI, A. and WERLANG, S. (2000): “Implementing Inflation Targeting in Brazil”, Working

Paper Nº 1, Banco Central do Brasil, Rio de Janeiro. BONOMO, M., BRITO, R. and MARTINS, B. (2014): “Macroeconomic and Financial Consequences of the After

Crisis Government-Driven Credit Expansion in Brazil”, Working Paper Nº 378, Banco Central do Brasil, Rio de Janeiro.

BRUCK, N. (1998): “The Role of Development Banks in the Twentieth-First Century” Journal of Emerging Markets 3(3), pp. 61-90.

CAMERON, R. (1961): France and the Economic Development of Europe. Princeton, NJ: Princeton University Press.

CÉSPEDES, L.F., CHANG, R. and VELASCO, A. (2002): “IS-LM-BP in the Pampas”, Working Paper Nº 9337, National Bureau of Economic Research, Cambridge, MA.

DEWATRIPONT, M. and MASKIN, E. (1995): “Credit and Efficiency in Centralized and Decentralized Economies” Review of Economic Studies 62(4), pp. 541-555.

DIAMOND, D. (1984): “Financial Intermediation and Delegated Monitoring” Review of Economic Studies 51(3), pp. 393-414.

EICHENGREEN, B. and HAUSMANN, R. (1999): “Exchange Rates and Financial Fragility”, Working Paper Nº 7418, National Bureau of Economic Research, Cambridge, MA.

EICHENGREEN, B., HAUSMANN, R. and PANIZZA, U. (2002): “Original Sin: The pain, the mystery, and the road to redemption”, In Inter-American Development Bank Conference, Washington, DC, 21-22 November.

GERSCHENKRON, A. (1962): Economic Backwardness in Historical Perspective. Cambridge, MA: Harvard University Press.

HAUSMANN, R. and RODRIK, D. (2003): “Economic Development as Self-Discovery” Journal of Development Economics 72(2), pp. 603-633.

HIRSCHMAN, A. (1958): The Strategy of Economic Development. London: Oxford University Press. IBGE (2003): Estatisticas do Seculo XX. Rio de Janeiro: IBGE. LA PORTA, R., LOPEZ-DE-SILANES, F. and SHLEIFER, A. (2002): “Government Ownership of Banks” The Journal

of Finance 52(1), pp. 265-301. LAZZARINI, S., MUSACCHIO, A., MELLO, R. and MARCON, R. (2015): “What Do State-Owned Development

Banks Do? Evidence from BNDES, 2002-09” World Development 66, pp. 237-253. LAZZARINI, S. (2011): Capitalismo de Laços: Os donos do Brasil e suas conexoes. Rio de Janeiro: Elsevier.

18 | L e m a n n C e n t e r f o r B r a z i l i a n S t u d i e s W o r k i n g P a p e r s | M a r c h 2 0 1 6

LEVY-YEYATI, E., MICCO, A. and PANIZZA, U. (2004): “Should the Government Be in the Banking Business? The role of state-owned and development banks”, In Governments and Banks: Responsibilities and Limits, Inter-American Development Bank, Lima, Peru, March 28.

LOPES, F. (2010): “A Estabilização Incompleta”, Working Paper, Macrometrica, Rio de Janeiro. MAZZUCATO, M. (2013): The Entrepreneurial State. London: Anthem Press. MELLO, J., and GARCIA, M. (2012): “Bye, Bye Financial Repression, Hello Financial Deepening: The anatomy of

a financial boom” The Quarterly Review of Economics and Finance 52(2), pp. 135-153. MOURAO, J. (1994): “A Integração Competitiva e o Planejamento Estratégico no Sistema BNDES” Revista do

BNDES 1(2), pp. 3-26. MUSACCHIO, A. and LAZZARINI, S. (2014): Reinventing State Capitalism: Leviathan in business, Brazil and

beyond. Cambridge, MA: Harvard University Press. OCAMPO, J.A. (2013): “Balance of Payments Dominance: Its implications for macroeconomic policy”, Initiative

for Policy Dialogue Working Paper Series, New York, NY. OCAMPO, J.A., RADA, C. and TAYLOR, L. (2009): Growth and Policy in Developing Countries: A structuralist

approach. New York, NY: Columbia University Press. OCAMPO, J.A. (2003): Capital Account and Counter-Cyclical Prudential Regulations in Developing Countries, In

French-Davis, R. and Griffith-Jones, S. (eds.): From Capital Surges to Drought: Seeking stability for emerging markets. London: Palgrave Macmillan.

PREBISCH, R. (1948): “The Economic Development of Latin America and Its Principal Problems” Economic Survey of Latin America 11, United Nations, New York, NY.

PROCHNIK, M. and MACHADO, V. (2008): “Fontes de Recursos do BNDES” Revista do BNDES 14(29), pp. 3-34. PROCHNIK, M. (1995): “Fontes de Recursos do BNDES” Revista do BNDES 2(4), pp. 143-180. RESENDE, A. (2013): Os Limites do Possível: A economia além da conjuntura. Sao Paulo: Penguin. RODRIK, D. (2004): “Industrial Policy for the Twenty-First Century”, John F. Kennedy School of Government

Paper, Harvard University, Cambridge, MA. RODRIK, D. (2007): “Normalizing Industrial Policy”, John F. Kennedy School of Government Paper, Harvard

University, Cambridge, MA. ROSESTEIN-RODAN, P. (1943): “Problems of Industrialization of Eastern and South-Eastern Europe” The

Economic Journal 53(211), pp. 202-211. RUGGIE, J. (1982): “International Regimes, Transactions, and Change: Embedded liberalism in the postwar

economic order” International Organization 36(2), pp. 379-415. SAYERS, R. (1957): Central Banking After Bagehot. Oxford: Oxford University Press. SEGURA-UBIERGO, A. (2012): “The Puzzle of Brazil’s High Interest Rates”, Working Paper Nº 12/62, IMF,

Washington, DC. SOTELINO, F. (2014): “A Functional Financial System for Brazil, When?”, In BRICS Lab Conference: BRICS, the

road ahead, Columbia University, New York, NY, 6 March. STIGLITZ, J. (1994): “The Role of the State in Financial Markets”, In Proceedings of the World Bank Annual

Conference on Economic Development, Washington, DC. STUDART, R. (2000): “Financial Opening and Deregulation in Brazil in the 1990s: Moving towards a new pattern

of development financing?” The Quarterly Review of Economics and Finance 40(1), pp. 25-44.

19 | L e m a n n C e n t e r f o r B r a z i l i a n S t u d i e s W o r k i n g P a p e r s | M a r c h 2 0 1 6

Fiscal Policy in Brazil: from Counter-Cyclical Response to Crisis

Márcio Holland10

Abstract: The main goal of this article is to identify the dynamic effects of fiscal policy on output in Brazil from

1997 to 2014, and, more specifically, to estimate those effects when the output falls below its potential level. To

do so, we estimate VAR (vector autoregressive) models to generate impulse-response functions and

causality/endogeneity tests. Our most notable results indicate the following channel of economic policy in Brazil:

to foster output, government spending increases causing increases in both tax rates and revenue and the short-

term interest rate. A fiscal stimulus via spending seems efficient for economic performance as well as monetary

policy; however, the latter operates pro-cyclically in the way we defined here, while the former is predominantly

countercyclical. As the monetary shock had a negative effect on GDP growth and GDP growth responded

positively to the fiscal shock, it seems that the economic policy has given poise to growth with one hand and

taken it with the other one. The monetary policy is only reacting to the fiscal stimuli. We were not able to find

any statistically significant response of the output to tax changes, but vice versa seems to work in the Brazilian

case.

1. Introduction

The 2008 international financial crisis put fiscal policy at the forefront of debate, particularly its use in mitigating the painful effects of the crisis on outputs and employment. Probably because of the lack of widely recognized rules, fiscal policy is generally a controversial issue. The economic meltdown with its deep and protracted impact on both goods and labor markets presented the perfect opportunity to approach divergent views about its use. For a few years after the 2008 crash, there was no room for austerity until government debts skyrocketed. Alas, governments had to shift towards fiscal retrenchment, even under economic weakness. The results of recent fiscal policies have been mixed, and their effectiveness remains a disputed issue.

On the other hand, a stream of literature has conducted empirical studies with novel methodologies in an effort to identify the dynamic and contemporaneous effects of fiscal policy on outputs. Auerbach and Gorodnichenko (2012) estimate a government purchase multiplier for a large number of OECD countries using a specific form of the STVAR (smooth transition vector autoregressive) model and have identified a fiscal multiplier in both recession and expansion circumstances. The model might be considered a refinement of Blanchard and Perotti’s (2002) specification, who used a simplified structural VAR model. In 2014, Mineshima et al. introduced a TVAR (threshold vector autoregressive) model to use when regimes are determined by a transition variable, which is either exogenous or endogenous. More recently, Herwartz and Lütkepohl (2014) proposed a structural vector autoregression model with Markov switching that combines conventional and statistical identification of shocks, which can be useful for future studies on fiscal policy.

The main goal of this article is to identify the effect of fiscal shocks on output in Brazil from 1997 to 2014, and, more specifically, to estimate those effects when the output falls below its potential level, as observed during most of the period following the 2008 international meltdown. We pose an additional question: How low can the

10 São Paulo School of Economics at Getulio Vargas Foundation, Brazil. Corresponding author contact: [email protected]. This working paper was partially written during my mandatory cooling-off period when I spent part of this time as a visiting scholar at Columbia University in the City of New York and for this reason I am very grateful to Professors Albert Fishlow, Thomas Trebat, Gray Newman, Sidney Nakahodo, Gustavo Azenha, and Daniella Diniz, for having me and giving me all the support I needed to develop my research. However, all opinions expressed herein represent those of the author.

20 | L e m a n n C e n t e r f o r B r a z i l i a n S t u d i e s W o r k i n g P a p e r s | M a r c h 2 0 1 6

output drop when it is already below its potential level (which we call “negative initial conditions” for the fiscal consolidation program), despite the composition of the fiscal retrenchment? In other words, after the output has bottomed out, how can policymakers quickly instill confidence by cutting expenditures and increasing taxes when these measures were supposed to be implemented as an expansionary shock?

To do so, we estimate VAR (vector autoregressive) models to generate impulse-response functions and causality tests. Our most notable results indicate the following channel of economic policy in Brazil: to foster output, government spending increases, causing increases in both tax rates and revenue and the short-term interest rate. A fiscal stimulus via spending seems quite efficient for economic performance as well as monetary policy; however, the latter operates pro-cyclically, while the former is predominantly countercyclical. We were not able to find any statistically significant response of the output to tax changes, but we did find a statistically significant response of tax changes to output in the Brazilian case.

The contributions of this work are threefold: first, it identifies the response of output to fiscal and monetary policy; second, it estimates the impact of recent fiscal measures on output; and, third, in line with broader economic literature, it suggests a long-term fiscal plan for Brazil to spur its effectiveness in reducing output losses.

This work is divided in the following sections. The next section shows Brazil’s recent experience with fiscal policy and its main results. The third section reviews the literature and discussions of the effectiveness of fiscal policy. The fourth section extrapolates the impulse-response functions obtained in our research to measure the potential impact of the 2015 fiscal plan on output and confidence. Ultimately, it is the appropriate moment to present the advantages and caveats of our empirical procedures. We are aware of the many drawbacks presented in this sort of time series analysis. At the end of this section, we suggest a long-term fiscal plan for Brazil using lessons learned from both Brazil’s recent experience with fiscal policy and our empirical study.

2. The Brazilian Context

Governments across the globe responded to the 2008 crisis with unprecedented expansionary actions in recent economic history. Monetary and fiscal countercyclical actions were implemented to both stymie the contamination of the international crisis in financial systems and to resume growth as soon as possible.

From 2008 to 2010, fiscal and monetary stimuli were overwhelmingly recommended. However, since 2010, the focus has shifted to fiscal consolidation in advanced economies. Since then, fiscal results have improved over the world, even though the debt-to-GDP ratios remain high compared with those before the crisis. More recently, the United States has outperformed the euro area, where calling for austerity appears to have fallen out of fashion again, as illustrated in the 2015 Greek case.

The fiscal front has deteriorated dramatically in many advanced economies with mixed and far from outstanding achievements. However, comparing the 1929 Great Depression with the 2008 Great Recession, Eichengreen (2015:2) reflects on these crises as follows: “as a result of this different response, unemployment in the United States peaked at 10 percent in 2010. Though this was still disturbingly high, it was far below the catastrophic 25 percent scaled in the Great Depression”.

Due to this thought, the Brazilian government took a series of countercyclical policies to protect the local economy from crumbling. These policies seemed to work well, at least until 2013. The worst of the crisis was absorbed without any major disruption in the Brazilian economic system. Most importantly, the economy resumed growth in the 2nd quarter of 2009; the unemployment rate did not spike; real wages continued to grow; and consumer and business confidence recovered very quickly. Nevertheless, after a period of recovery until 2013, the overall growth remained disappointing, particularly given the very rapid deterioration in 2014, the strong contraction in 2015, and uncertainty about 2016 performance.

21 | L e m a n n C e n t e r f o r B r a z i l i a n S t u d i e s W o r k i n g P a p e r s | M a r c h 2 0 1 6

From late 2014 to early 2015, Brazil launched a tight fiscal program. The pro-cyclical biased fiscal consolidation plan is presumably considered the only plausible policy stance when solvency became the issue rather than economic activity. In Brazil, the diagnosis and prescription have been far from divergent. However, as highlighted by Frankel (2012), “a pro-cyclical fiscal policy magnifies the severity of the business cycle”. This controversy motivated this research to assess whether such fiscal consolidation policies are expected to hurt GDP growth to a greater extent because the economy is already under contraction. Alternatively, would they spur confidence so that the drag on economic activity could be avoided?

There is no doubt that fiscal stimuli were needed at that challenging time, when the Brazilian economy was severely hit by the financial crisis. As for fiscal policy, there were considerable tax exemptions in 2009. As a result of the actions taken by the government at that time, the country was able to recover very quickly from the crisis; among other things, Brazil experienced 7.6 percent and 3.9 percent growth in 2010 and 2011, respectively (see table 1).

According to the national account’s new dataset, released on March 27, 2015 by the National Bureau of Statistics (IBGE), the 2008 crises hit the economy harder and deeper, and the recovery was faster and better because investment resumed quickly and included a greater share of the GDP compared with the previous period of the crisis, regardless of its volatility (see figure 1 and 2).

In early 2011, the Federal Administration was able to start applying a fiscal consolidation plan to cool down the economy. Needless to say, solvency had not been a problem in Brazil for a long time, as international reserves have been considerable and more than enough to pay for external liabilities; in addition, the public debt-to-GDP ratio had been decreasing over the years. Thanks to Brazil’s reaction to the crash, the general gross debt-to-GDP ratio increased 3.3% from 2008 to 2009, which could be considered incredibly low in comparison with the debt dynamics in advanced economies after the crisis. However, the general gross debt-to-GDP ratio is still high in Brazil compared with that of its peers, although it had been relatively stable, even during most of the period of countercyclical fiscal policy (see table 1 and figures 2 and 3 for the fiscal results).

Table 1. Brazil: Key Macroeconomic Indicators after the 2008 Crisis (2008-2015)

2008 2009 2010 2011 2012 2013 2014 2015* 2016*

Real GDP Change (%) 5,0 -0,2 7,6 3,9 1,8 2,7 0,1 -3,7 -3,0

Unemployment Rate year average (%)

7,9 8,1 6,7 6,0 5,5 5,4 4,8 6,8 7,5

Investment Change (%), eop 12,7 -1,9 17,8 6,6 -0,6 6,1 -4,4 -12,0 -5,0

CPI Inflation - IPCA (%), eop 5,9 4,3 5,9 6,5 5,8 5,9 6,4 -10,7 -8,5

Benchmark Interest Rate (%), eop 13,75 8,75 10,75 11,0 7,25 10,0 11,75 14,25 14,25

Current Account (% of GDP) -1,7 -1,5 -2,1 -2,0 -2,3 -3,4 -4,4 -4,5 -3,5

FDI (US$ billion) 45,1 25,9 48,5 66,7 65,3 64,0 96,9 60,0 50,0

Foreign Reserves (US$ billion) 207 239 289 352 379 376 374 370 360

Exchange Rate (Real per USD) eop 2,34 1,74 1,67 1,88 2,04 2,35 2,65 4,0 4,5

Primary Result (% of GDP) 3,3 1,9 2,6 2,9 2,2 1,8 -0,6 -1,9 -0,5

Nominal Result (% of GDP) -2,0 -3,2 -2,4 -2,6 -2,3 -3,1 -6,2 -10,3 -9,5

Gross G. Govt Debt (% of GDP) 56,0 59,3 51,8 51,3 54,8 53,3 58,9 66,2 72,0

Net Public Debt (% of GDP) 37,6 40,9 38,0 34,5 32,9 31,5 34,1 36 37,0

Notes: Unemployment rate is yearly average of the Monthly Employment Survey (PME); CPI is the broad CPI (IPCA); Benchmark interest rate is the target Central Bank interest rate in the end of period; and exchange rate as in the end of period. eop = end of period. * 2015 and 2016 are author´s forecasts. Source: Ministry of Finance of Brazil, Central Bank of Brazil, and IBGE.

22 | L e m a n n C e n t e r f o r B r a z i l i a n S t u d i e s W o r k i n g P a p e r s | M a r c h 2 0 1 6

Even with such policies, the primary surplus targets were fully accomplished, at least until 201211 (see figure 2). However, by mid-2012 to 2013, the recovery appeared to be weaker than expected, and the Brazilian economic authorities returned to incentives, trying to reignite the economy12. In 2013, the economy grew again by 2.7%, and the investment grew 6.1%. A wide tax relief program and increasing government expenditures, including a broad financial subsidy for credit for capital goods via public banks, were introduced. The economy reacted reasonably, so the investment to GDP ratio remained relatively stable at approximately 20.5% until at least 2013, despite its high variability (see figure 1).

Figure 1. Brazil: Gross Formation of Fixed Capital as % of GDP) 1997-2015

Source: IBGE, updated in November 17, 2015.

Note: Investment as % of GDP measured using current values for GDP and gross formation of fixed capital. 2015

is author´s forecast.

11 Although the one-off revenues had increased in importance after the 2008 crash, responding, for instance, to 0.74% and 0.85% of GDP in 2009 and 2010, respectively, when the full primary surplus delivered was 1.9% and 2.6% of GDP, respectively, or, in 2013, when 0.68% of 1.8% of GDP was one-off revenue. In 2014, one-off revenue was 0.5% of GDP while the primary deficit was 0.6% of GDP. 2015 primary surplus is going to be plenty of on-off revenue, as well. 12 At that time, estimates of GDP growth were 2.7% for 2011, instead of 3.9% as reported in the new 2015 dataset, moving downward towards 0.9% in 2012, instead of 1.8% as reported in the new 2015 dataset. Moreover, the share of investment over GDP was sharply declining, but the new 2015 dataset unveiled very stable figures for this indicator.

19.1

18.5

17.0

18.3 18.4

17.9

16.6

17.317.1 17.2

18.0

19.4

19.1

20.5 20.6 20.7 20.9

19.7 19.7

17.8

10.0

12.0

14.0

16.0

18.0

20.0

22.0

23 | L e m a n n C e n t e r f o r B r a z i l i a n S t u d i e s W o r k i n g P a p e r s | M a r c h 2 0 1 6

Figure 2: Nominal Fiscal and Primary Results as Share of GDP (%) 1999-2018

Source: Central Bank of Brazil; 2016 - 2018 are author´s forecast.

However, from 2013 to 2014, the output was not responding at all to tax stimuli or even spending increases. After Brazil graduated to respond to the 2008 crisis using countercyclical fiscal policies (Vègh and Vulletin, 2013), it experienced a rapid deterioration on the fiscal front in 2014. Both net and gross public debt increased quickly towards a risky case scenario, so the investment grade rating was no longer assured in the medium term13. Potential output decreased at the same time as the output was well below its declining potential output level.

In late 2014 and early 2015, some social benefits were reviewed, and some tax relief was reverted (tables 5.1 and 5.2 detail these measures). The economy had actually started to adjust itself during 2014, as the Central Bank had begun a new tightening cycle from April 2013 to July 2014. The target interest rate increased 375 basis points in an interval of one year. Another 325 basis-point increase would take place between October 2014 and July 2015. A 700 basis-point monetary shock in an interval of two years is far from negligible. Its primary side effect was a considerable contraction in the domestic credit on durable and capital goods, contributing to an additional drop in consumer and business confidence.

13 In September 2015, a couple of weeks after the Government had decided to send to Congress the 2016 Budget Law with deficit, the Standard & Poor´s downgraded the Brazilian sovereign rating to speculative grade.

(5.20)

(3.30) (3.30)

(4.40)

(5.20)

(2.90)

(3.50) (3.60)

(2.70)

(2.00)

(3.20)

(2.40) (2.50) (2.30)

(3.10)

(6.20)

(10,3)

(9.50)

(7.40)

(6.00)

2.80 3.20 3.30 3.20 3.20

3.70 3.70 3.20 3.20 3.30

1.90