Lbe investor presentation june 2012 v001 w4l7qz(1)

29

Nickel Production and Exploration in Timmins Chris Stewart, President & CEO Q2/ 2012 TSX: LBE

-

Upload

augustincatea -

Category

Documents

-

view

47 -

download

2

Transcript of Lbe investor presentation june 2012 v001 w4l7qz(1)

Nickel Production and Exploration in TimminsChris Stewart, President & CEO

Q2/ 2012

TSX: LBE

Forward-Looking Statement

This presentation contains “forward-looking information” and “forward-looking statements” within the meaning of applicable securities laws. This information and statements address future activities, events, plans, developments and projections. All statements, other than statements of historical fact, constitute forward-looking statements or forward-looking information. Such forward-looking information and statements are frequently identified by words such as “may”, “will”, “should”, “anticipate”, “plan”, “expect”, “believe”, “estimate”, “intend” and similar terminology and reflect assumptions, estimates, opinions and analysis made by management of Liberty in light of its experience, current conditions, expectations of future developments and other factors which it believes to be reasonable and relevant. Forward-looking information and statements involve known and unknown risks and uncertainties that may cause Liberty’s actual results, performance and achievements to differ materially from those expressed or implied by the forward-looking information and statements and accordingly, undue reliance should not be placed thereon. Risks and uncertainties that may cause actual results to vary include but are not limited to the speculative nature of mineral exploration and development, including the uncertainty of reserve and resource estimates; operational and technical difficulties; the availability of suitable financing alternatives; fluctuations in nickel and other commodity prices; changes to and compliance with applicable laws and regulations, including environmental laws and obtaining requisite permits; political, economic and other risks arising from Liberty’s activities; fluctuations in foreign exchange rates; as well as other risks and uncertainties which are more fully described in our annual and quarterly Management’s Discussion and Analysis and in other filings made by us with Canadian securities regulatory authorities and available at www.sedar.com. No invitation to purchase securities is being made. Liberty disclaims any obligation to update or revise any forward-looking information or statements except as may be required by law.

2

Investment Highlights

• New senior leadership team with turnaround strategy

• Only nickel mill/concentrator facility within the Shaw Dome

region

• Off-take agreement with Xstrata

• Strategic relationship with Jilin Jien Nickel Industry Co. (JJNICL)

• Targeted nickel production of 4.0 million lbs in 2012

• Solid pipeline of exploration projects

• Strong nickel market fundamentals

3

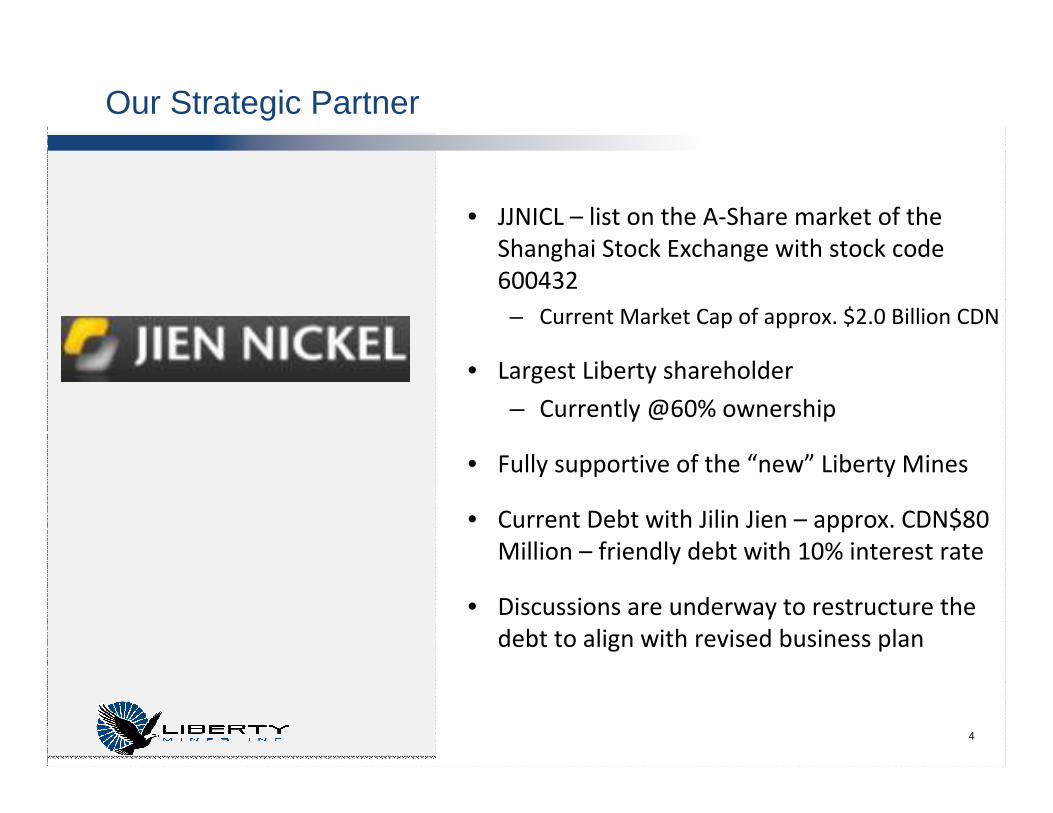

• JJNICL – list on the A-Share market of the

Shanghai Stock Exchange with stock code

600432

– Current Market Cap of approx. $2.0 Billion CDN

• Largest Liberty shareholder

– Currently @60% ownership

• Fully supportive of the “new” Liberty Mines

• Current Debt with Jilin Jien – approx. CDN$80

Million – friendly debt with 10% interest rate

• Discussions are underway to restructure the

debt to align with revised business plan

Our Strategic Partner

4

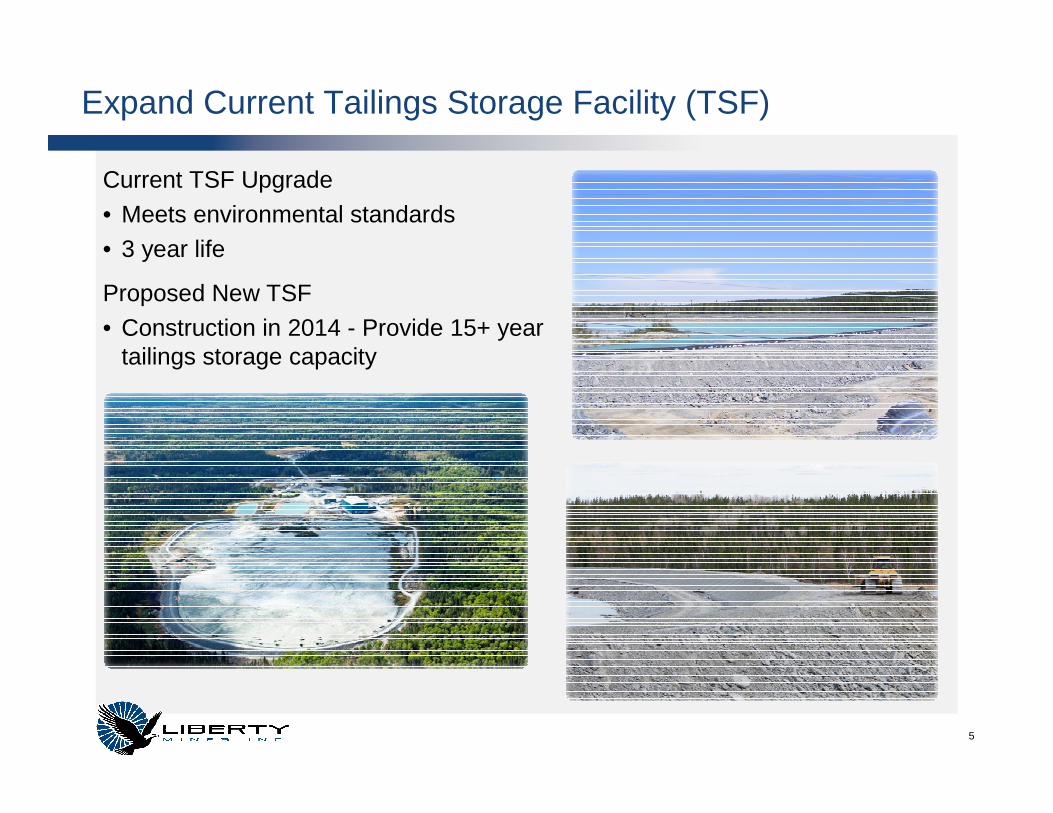

Expand Current Tailings Storage Facility (TSF)

5

Current TSF Upgrade

• Meets environmental standards

• 3 year life

Proposed New TSF

• Construction in 2014 - Provide 15+ year tailings storage capacity

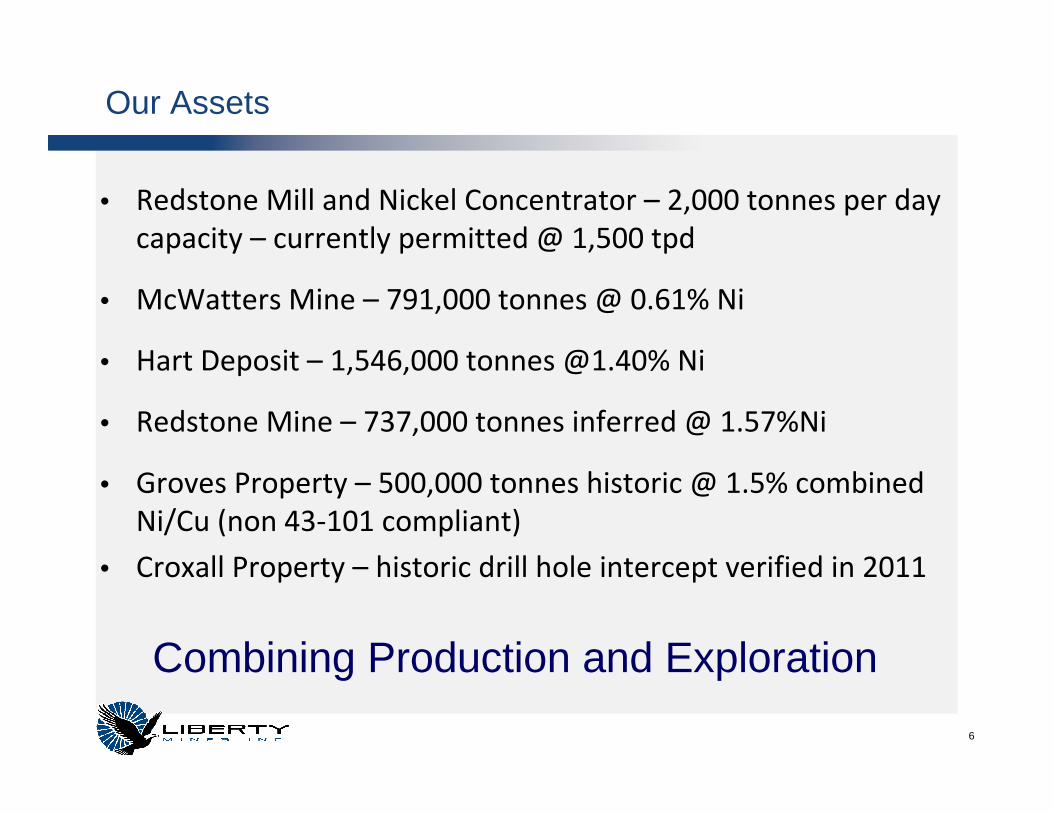

Our Assets

• Redstone Mill and Nickel Concentrator – 2,000 tonnes per day

capacity – currently permitted @ 1,500 tpd

• McWatters Mine – 791,000 tonnes @ 0.61% Ni

• Hart Deposit – 1,546,000 tonnes @1.40% Ni

• Redstone Mine – 737,000 tonnes inferred @ 1.57%Ni

• Groves Property – 500,000 tonnes historic @ 1.5% combined

Ni/Cu (non 43-101 compliant)

• Croxall Property – historic drill hole intercept verified in 2011

Combining Production and Exploration

6

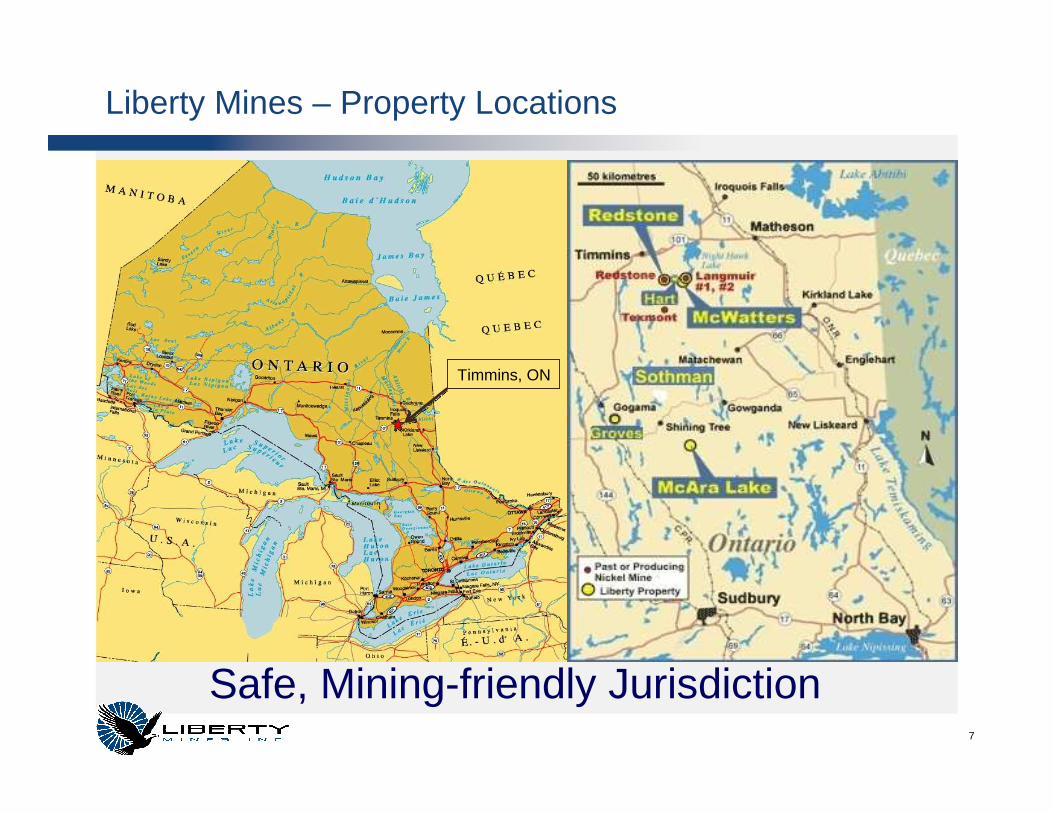

Liberty Mines – Property Locations

7

Timmins, ON

Safe, Mining-friendly Jurisdiction

Upcoming Milestones & Objectives

Short-term Long-term

Q1 2012• Restart mining and milling operations

• Expand exploration program

2013-2014• Expand Liberty beyond the ShawDome area

Q4 2012• Generate positive operating cash flow

2014•Construction of a new Tailings Pond Facility

2012• Produce 4.0 million lbs of Nickel

• Increase resources

2015•Double current resources to provide 12+ years of operating life

8

Current Operational Status

Redstone Mill• Production restarted – ramping up to full production• Concentrate shipped to Xstrata in Sudbury

9

Current Operational Status

McWatters Mine• Mine fully operational

• 1,500 tpd production

10

New 8yd Scooptram

Loading Underground Haul Truck

6yd Scooptram Mucking Drawpoint

11

Redstone Mine

Lower Zone Resource

737,000 tonnes Inferred @

1.57%– High Potential &

High Grade

Deposit is open at Depth

Production Rate

300 tpd from Q1/2014

Redstone Mine

Lower Zone Resource

737,000 tonnes Inferred @

1.57%– High Potential &

High Grade

Deposit is open at Depth

Production Rate

300 tpd from Q1/2014

McWatters Mine

791,000 tonnes @ 0.61% Ni

Production Rate

1,500 tpd Q1/2012

McWatters Mine

791,000 tonnes @ 0.61% Ni

Production Rate

1,500 tpd Q1/2012

Hart Mine

1,546,000 tonnes @ 1.40% Ni

Production Rate

250 tpd starting Q1/2014 ramping

up to 750 tpd by 2016

Deposit is open at Depth

Hart Mine

1,546,000 tonnes @ 1.40% Ni

Production Rate

250 tpd starting Q1/2014 ramping

up to 750 tpd by 2016

Deposit is open at Depth

Redstone Mill

2,000 tpd design capacity

Permitted @ 1,500 tpd now

Redstone Mill

2,000 tpd design capacity

Permitted @ 1,500 tpd now

Vision for our operations

Current Resources and Reserves

DepositResource / Reserve Category

TonnesGrade (Ni%)

Contained Ni (lbs)

Hart Resource Indicated 1,546,000 1.40% 47,716,860

Inferred 322,000 1.27% 9,015,585

McWatters Reserve

Proven &

Probable791,000 0.61% 10,637,526

Redstone Reserve

Proven &

Probable50,252 1.48% 1,644,248

Resource Inferred 737,000 1.57% 25,509,472

Grand Total 3,446,252 1.24% 94,523,692

12

Potential for resource and reserve expansion through targeted exploration program

Shallow Mine –

Ramp to Surface

Shallow Mine –

Ramp to Surface

Infrastructure in place -

multiple draw points on

multiple levels

Infrastructure in place -

multiple draw points on

multiple levels

Surface Elev.

McWatters Mine

13

Redstone Mine – Resource Drilling – At Depth Potential

1600ft level

14

Hart Mine & Hart East Deposit Potential

Gabbro D

ykeOpen

Open

15

780m

550m

650m

Hart East sits 300m away from the main Hart Deposit

16

Opportunities for new exploration

Claims in the Shaw Dome

Hart & Hart East Deposits

Redstone Mine & Mill

Croxall

McWatters Mine

Additional Drill Targets

Shaw Dome Area

17

A6

Exploration Program 2012

Primary Focus Secondary Targets

Hart & Redstone Properties Croxall, Groves and McAra

Properties

•Deep drilling on Hart, Hart

East and Redstone to

increase resources

• New drilling on prospective

targets on Hart property

•Underground drilling to

confirm ore resources at

Redstone

•Complete further geophysics

work

•Identify additional drill targets

18

19

Public markets and mining experience

Mr. Wu Shu, Director & Chairman of the Board – CEO of Jilin Jien Nickel Industry Co. Previously President of Jilin Haorong Nonferrous Metal Group Co., Ltd. and CFO and a Director of JJNICL.

Mr. John Pinsent, Lead Director - Founding partner in St. Arnaud Pinsent Steman Chartered Accountants. 10+ years of experience with Ernst & Young LLP. Significant mining industry experience.

Dr. Tao Li, Director - Specialist in geotechnical engineering and is the director and principal of an independent consulting company. 30+ years of mining and engineering experience (Mount Isa Mines, WMC Resources, Gold Fields and Newcrest Mining)

Mr. Kim Oishi, Director - 17 years of capital markets experience, serving as an officer and director of a number of public companies, and focused on China since 2004.

Dr. Shu Zhang, Director - President & COO of Jien International Investment Ltd. (JIIL). He is a mining engineer with 38+ years of mining industry experience working in China, Australia and Canada.

Board of Directors

20

Mining and operational experts

Chris Stewart, President & CEO – Professional engineer with 20+ years of mine development and mine operations experience. Bachelor of Science from Queen’s University. Successful track record in mining services and operations. Recently came from BHP Billiton where he was the Project Manager - Shafts at the Jansen Project. Former VP of Ops for Lake Shore Gold in Timmins.

David Birch, CFO – 20+ years of experience in corporate finance and accounting. Certified Public Accountant (CPA) and Certified Management Accountant (CMA) with an Economics Degree from York University. Previous Vice President of Finance & Operations for McClelland Premium Imports. He has also held various senior financial positions with Labatt Breweries and InBEV.

Heather Miree, VP Exploration – 25+ years of exploration and mining project experience in Canada and the United States. A graduate of the University of Waterloo with an Honours Bachelor of Science in Earth Science, Ms. Miree is a registered as a Professional Geologist in Ontario and Alberta. She has held senior positions for companies such as FNX Mining Company, Lake Shore Gold, St. Andrews Goldfields and most recently she was the VP Exploration at Excellon Resources.

Kevin Fearn, VP Human Resources & Communication – 28+ years of experience in the mining, construction and consumer goods industries. Mr. Fearn holds a business degree from Laurentian University, university certificates in labour relations, safety and health, alternative dispute resolution and negotiations.

Keyvan Salehi, VP Corporate Development– Professional engineer with 10+ years of experience in the mining industry. Obtained his MBA through Kellogg/Schulich program at York University. Previous positions include Chief Engineer for Lake Shore Gold at the Bell Creek Complex and Project Manager for DMC Mining on various projects in the Sudbury area.

Brendan Zuidema, General Manager – 20+ years of experience in the mining industry. He has held various senior positions including Operations General Foreman at the Montcalm Mine, Mine Manager at Lake Shore Gold’s Timmins Mine and most recently Area Manager for Dumas Contracting in Timmins.

Management team

21

Trading Symbol: LBEListing: TSX

Recent share price: $0.1052-Week Range $0.065 - $0.22Shares outstanding 214.2 million

Market Capitalization $20.65 millionFiscal year end Dec. 31

Market Data

Investment Highlights

• New senior leadership team with turnaround strategy

• Only nickel mill/concentrator facility within the Shaw Dome

region

• Off-take agreement with Xstrata

• Strategic relationship with Jilin Jien Nickel Industry Co. (JJNICL)

• Targeted nickel production of 4.0 million lbs in 2012

• Solid pipeline of exploration projects

• Strong nickel market fundamentals

22

Appendix

23

24

Nickel Ore gets

trapped in

embayments with

sources of sulphur in

footwall rocks

Nickel Ore gets

trapped in

embayments with

sources of sulphur in

footwall rocks

Footwall rock –

iron formation

(Hart) or

graphite (W4)

Footwall rock –

iron formation

(Hart) or

graphite (W4)

Typical Deposit Structure in the Shaw Dome

A6 Project – 2012 VTEM & Geochem Target

25

26

10 km road access

Historic resource (non 43-101) of 500,000 tonnes of 1.5% combined Cu/Ni.

Completed a 13 hole drill program totally 1,245 meters in 2011

Best drill hole intercept from GR-11-05 which graded 1.69% Ni, 1.66% Cu and 0.73 G/T Au over drilled width of 15.50 meters

Refer to Liberty’s press release 16-11 issued on October 25, 2011 for more details on drill results

Groves Project

2011 follow up drill hole - 25m

east of the Mustang discovery

returns with 0.92% Ni over 4.20m

Mustang Minerals 2005

nickel discovery of 0.63%

Ni over 3.34m

Croxall

27

28

Ore Sources

*Source: RBC

Nickel market trends

• Nickel demand is growing*:

– 17.1% in 2010

– 8.4% in 2011

– 9.5% in 2012

• China is main driver for growth

• Nickel consumption is dominated by the stainless steel sector

– accounts for more than half of the global consumption of nickel