Latest Investor Presentation - Southwestern Energy

32

March 2019 Investor Update NYSE: SWN Contact: Paige Penchas Vice President, Investor Relations [email protected] Phone: (832) 796-4068

Transcript of Latest Investor Presentation - Southwestern Energy

March 2019 Investor Update

NYSE: SWN

Contact: Paige Penchas

Vice President, Investor Relations

Phone: (832) 796-4068

1

Forward-Looking Statements

This presentation contains forward-looking statements. Forward-looking statements relate to future events and anticipated results of operations, business

strategies, and other aspects of our operations or operating results. In many cases you can identify forward-looking statements by terminology such as

“anticipate,” “intend,” “plan,” “project,” “estimate,” “continue,” “potential,” “should,” “could,” “may,” “will,” “objective,” “guidance,” “outlook,” “effort,” “expect,”

“believe,” “predict,” “budget,” “projection,” “goal,” “forecast,” “target” or similar words. Statements may be forward-looking even in the absence of these particular

words. Where, in any forward-looking statement, the Company expresses an expectation or belief as to future results, such expectation or belief is expressed in

good faith and believed to have a reasonable basis. However, there can be no assurance that such expectation or belief will result or be achieved. The actual

results of operations can and will be affected by a variety of risks and other matters including, but not limited to, changes in commodity prices (including

geographic basis differentials); changes in expected levels of natural gas and oil reserves or production; operating hazards; drilling risks; unsuccessful

exploratory activities; natural disasters; limited access to capital or significantly higher cost of capital related to illiquidity or uncertainty in the domestic or

international financial markets; international monetary conditions; unexpected cost increases in service or other costs related to drilling and completion activities;

potential liability for remedial actions under existing or future environmental regulations; failure to obtain necessary regulatory approvals; potential liability

resulting from pending or future litigation; and general domestic and international economic and political conditions; as wel l as changes in tax, environmental and

other laws, including court rulings, applicable to our business. Other factors that could cause actual results to differ materially from those described in the

forward-looking statements include other economic, business, competitive and/or regulatory factors affecting our business generally as set forth in our filings with

the Securities and Exchange Commission. Unless legally required, Southwestern Energy Company undertakes no obligation to update publicly any forward-

looking statements, whether as a result of new information, future events or otherwise.

Cautionary Note to U.S. Investors – The SEC permits oil and gas companies, in their filings with the SEC, to disclose only proved, probable and possible

reserves. We use the terms "resource" and “EUR” in this presentation that the SEC’s guidelines prohibit us from including in filings with the SEC. The quarterly

reserves data included in this release are estimates we prepared that have not been audited by our independent reserve engineers. All such estimates are

inherently more speculative than estimates of proved reserves and are subject to substantially greater risk of actually being realized. U.S. investors are urged to

consider closely the oil and gas disclosures and associated risk factors in our Form 10-K and other reports and filings with the SEC. Copies are available from

the SEC and from the SWN website.

This presentation contains non-GAAP financial measures, such as adjusted net income, adjusted EBITDA and net cash flow, including certain key statistics and

estimates. We report our financial results in accordance with accounting principles generally accepted in the United States of America (“GAAP”). However,

management believes certain non-GAAP performance measures may provide users of this financial information additional meaningful comparisons between

current results and the results of our peers and of prior periods. Please see the Appendix for definitions and reconciliations of the non-GAAP financial measures

that are based on reconcilable historical information.

The contents of this presentation are updated as of March 22, 2019 unless otherwise indicated.

2

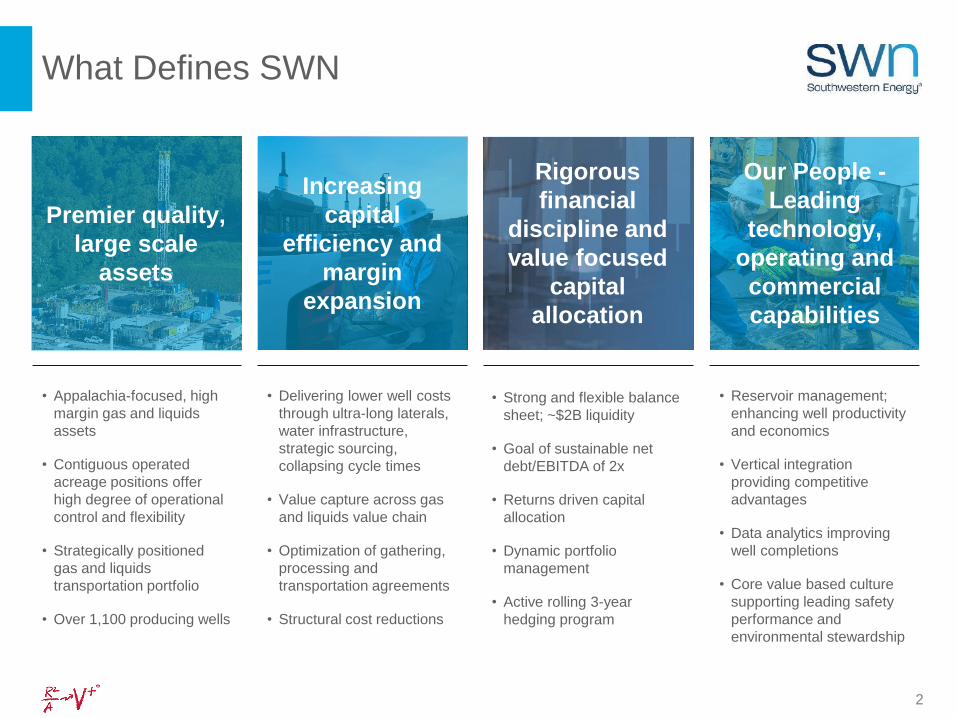

What Defines SWN

Premier quality,

large scale

assets

Rigorous

financial

discipline and

value focused

capital

allocation

Increasing

capital

efficiency and

margin

expansion

Our People -

Leading

technology,

operating and

commercial

capabilities

• Appalachia-focused, high

margin gas and liquids

assets

• Contiguous operated

acreage positions offer

high degree of operational

control and flexibility

• Strategically positioned

gas and liquids

transportation portfolio

• Over 1,100 producing wells

• Strong and flexible balance

sheet; ~$2B liquidity

• Goal of sustainable net

debt/EBITDA of 2x

• Returns driven capital

allocation

• Dynamic portfolio

management

• Active rolling 3-year

hedging program

• Delivering lower well costs

through ultra-long laterals,

water infrastructure,

strategic sourcing,

collapsing cycle times

• Value capture across gas

and liquids value chain

• Optimization of gathering,

processing and

transportation agreements

• Structural cost reductions

• Reservoir management;

enhancing well productivity

and economics

• Vertical integration

providing competitive

advantages

• Data analytics improving

well completions

• Core value based culture

supporting leading safety

performance and

environmental stewardship

3

SWN at a Glance

SWN is an independent energy company

with operations focused across 480,000

net acres in the Appalachia Basin

Northeast Appalachia

100% gas

184,024 Net Acres

2018 Proved Reserves – 4.4 Tcf

2019E Production(3) – 1,270 MMcf/d

Southwest Appalachia

45% gas, 46% NGL, 9% oil

297,445 Net Acres

2018 Proved Reserves – 7.6 Tcfe

2019E Production(3) – 833 MMcfe/d

Resource Potential 53 Tcfe

Total Drilling Locations(1) 3,200

2018 Proved Reserves 11.9 Tcfe

Natural Gas / Liquids 67% / 33%

2018 Proved Reserve PV-10 $6.5B

2018 Production(2) 702 Bcfe

Liquids (% of production / % of revenues) 20% / 28%

Gross Producing Wells 1,100

2019E Production(3) 768 Bcfe

2018 Year-end Debt $2.3B

2018 Net Debt / EBITDA(4) 1.9x

(1) Assumes minimum 10% return at $3.00 natural gas $50.00 oil.

(2) Production excludes Fayetteville contribution of 243 Bcf in 2018.

(3) Net production based off of midpoint of guidance issued February 5, 2019.

(4) Excludes Fayetteville EBITDA of approximately $375MM generated prior to December

2018 divestiture, at year-end 2018 net debt/EBITDA was 1.4x.

4

Our Strategy in Action

Driving

Shareholder

Value

Organic Growth,

Liquids-rich

Enhanced Well

Performance, Diligent

Cost Management

Sustainable 2X

Leverage

Rigorous Financial

Discipline,

Returns-focused

Transition to Free Cash

Flow Neutral by

Year-end 2020

Opportunistic

Growth

5

Recent Performance Catalysts

• Closed sale of Fayetteville Shale receiving $1.65 billion after closing price

adjustments

• Reduced senior notes and bank debt by $2.1 billion

• Completed $200 million share repurchase program, reducing shares

outstanding by 8% at an average price of $4.53

• Implemented cost savings initiatives resulting in estimated annual G&A and

interest savings of $150 million beginning in 2019

• Generated over $100 million in net cash flow above capital

• Reported total Company proved reserves of 11.9 Tcfe, with a pre-tax PV-10

value of $6.5 billion

• Longer laterals driving capital efficiency, including the drilling of 3 ultra-long

laterals in excess of 15,000 ft

6

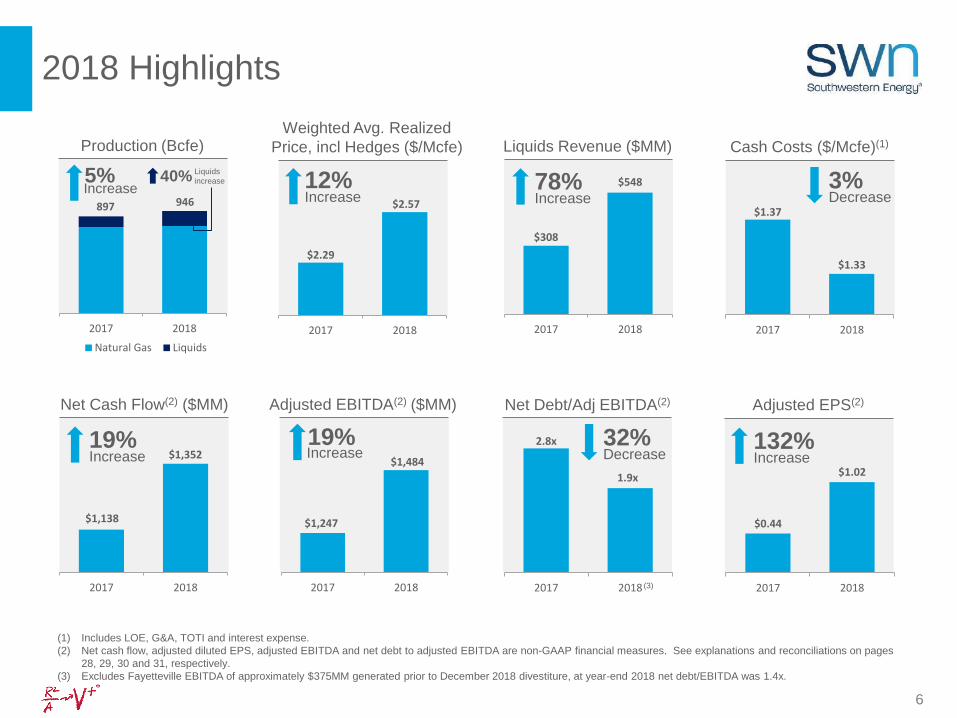

2018 Highlights

$0.44

$1.02

2017 2018

132%Increase

Adjusted EPS(2)

$1,138

$1,352

2017 2018

19%Increase

Net Cash Flow(2) ($MM)

2.8x

1.9x

2017 2018

32%Decrease

Net Debt/Adj EBITDA(2)

897 946

2017 2018

Natural Gas Liquids

5%Increase

Production (Bcfe)

$308

$548

2017 2018

78%Increase

Liquids Revenue ($MM)

$1.37

$1.33

2017 2018

3%Decrease

Cash Costs ($/Mcfe)(1)

(1) Includes LOE, G&A, TOTI and interest expense.

(2) Net cash flow, adjusted diluted EPS, adjusted EBITDA and net debt to adjusted EBITDA are non-GAAP financial measures. See explanations and reconciliations on pages

28, 29, 30 and 31, respectively.

(3) Excludes Fayetteville EBITDA of approximately $375MM generated prior to December 2018 divestiture, at year-end 2018 net debt/EBITDA was 1.4x.

$1,247

$1,484

2017 2018

19%Increase

Adjusted EBITDA(2) ($MM)

$2.29

$2.57

2017 2018

12%Increase

Weighted Avg. Realized

Price, incl Hedges ($/Mcfe)

Liquids

increase40%

(3)

7

4.5x

2.8x

1.9x 2.0x

2016 2017 Q3 2018 ProForma without

Fayetteville

Target

Strong and Flexible Balance Sheet

• Improved liquidity

– $2 billion bank revolver, 2023

maturity

– BB/Ba2 credit ratings

• No significant bond maturities until

2025

Net Debt / Adjusted EBITDA Debt Maturity Schedule ($MM)

(1) Excludes Fayetteville EBITDA of approximately $375MM generated prior to December 2018 divestiture, at year-end 2018 net debt/EBITDA was 1.4x.

(2) Based on Form 10-K filed on February 28, 2019.

0

500

1,000

1,500

2,000

2019 2020 2021 2022 2023 2024 2025 2026 2027

Bonds Revolver - Capacity

Sr Notes Wtd Avg YTM: 6.3 years(2)

Sr Notes Wtd Avg Interest: 6.7%(2)

Sr Notes Outstanding: $2.3B(2)

No significant maturities until 2025

• Continuous net debt/EBITDA

improvement

– Goal of 2X sustainable net

debt/EBITDA

– Reduced debt by $2.1 billion in 2018

– Interest expense reduced by ~$80

million annually

2018(1)

8

• Diversifying commodity mix, growing liquids portfolio

– Southwest Appalachia liquids production increasing to 75,600 barrels per

day,(1) 20% higher than record levels of 2018

– Northeast Appalachia production held flat with maintenance capital of

$280 - $310 million

• Fully funded, flexible capital program

NE Appalachia60%

SW Appalachia40%

2019 Guidance

Gas78%

NGLs 18%

Oil 4%

2019E

Production750 – 785 Bcfe

Appalachia78%

Other4%

CI&E18%

2019E

Capital$1.08B – $1.18B

2019E

Production by

Commodity

(1) The Company issued annual guidance on February 5, 2019. All figures assume midpoint of guidance.

9

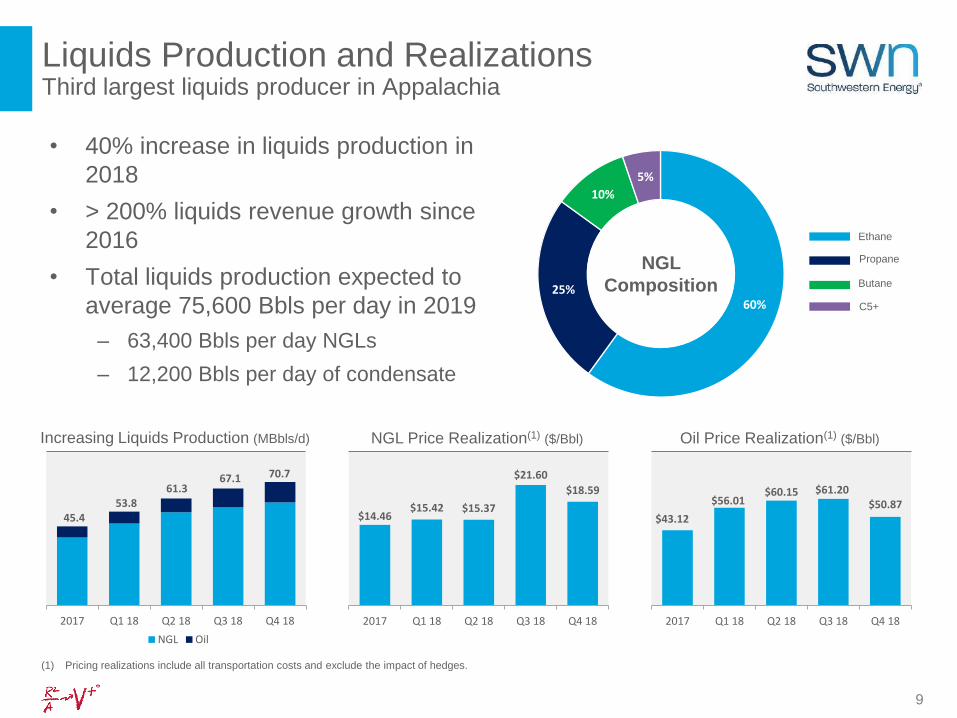

Liquids Production and RealizationsThird largest liquids producer in Appalachia

• 40% increase in liquids production in

2018

• > 200% liquids revenue growth since

2016

• Total liquids production expected to

average 75,600 Bbls per day in 2019

– 63,400 Bbls per day NGLs

– 12,200 Bbls per day of condensate

NGL

Composition

Ethane

Propane

Butane

C5+

(1) Pricing realizations include all transportation costs and exclude the impact of hedges.

45.453.8

61.367.1 70.7

2017 Q1 18 Q2 18 Q3 18 Q4 18

NGL Oil

Increasing Liquids Production (MBbls/d)

$14.46$15.42 $15.37

$21.60

$18.59

2017 Q1 18 Q2 18 Q3 18 Q4 18

NGL Price Realization(1) ($/Bbl)

$43.12

$56.01$60.15 $61.20

$50.87

2017 Q1 18 Q2 18 Q3 18 Q4 18

Oil Price Realization(1) ($/Bbl)

60%25%

10%

5%

10

Driving Well Costs Down

• Decreasing well costs by 25% to an average $875/ft

– Longer laterals, direct sand sourcing, water project and vertical integration

• Increasing average lateral lengths on wells to sales by 35% to over 10,000 ft

– Latest successfully drilled ultra-long lateral is 16,272 ft

– Continue testing ultra-long laterals to economic and technical limit

• Reducing drilling and completions capital while increasing drilled footage by 30%

2018 SWN Increased Lateral Frac Design Water and VerticalIntegration

Direct PurchasedSand

SWN Post Netback

$1,131

$875

2018(1) 2019(2)Increased

Lateral LengthCompletion

Design

Water Systems

and Vertical

Integration

Directly

Sourced Sand

Well Costs per Lateral Foot ($)

(1) 2018 includes only Marcellus wells.

(2) Improvement assumes $2.85 per Mcf gas and $50 per barrel oil.

11

4.65.2

6.3

7.7

4.0

5.56.4

8.4

2017 2018 2019E SWN Record

Southwest Appalachia Northeast Appalachia

7,451 7,267

10,600

15,559

6,185

7,584 9,400

16,272

2017 2018 2019E SWN Record

Southwest Appalachia Northeast Appalachia

65

27

19

710

6 41

2017 2018 2019E SWN Record

Southwest Appalachia Northeast Appalachia

1,1651,248 1,246

1,787

1,102 1,0451,219

1,700

2017 2018 2019E SWN Record

Southwest Appalachia Northeast Appalachia

Delivering Leading Operational Execution

37%Increase Increase

60%7%Increase Increase

11%

71%Decrease Decrease

60%42%Increase Increase

52%

Footage Drilled (ft/day) Completed Stages (stages/day)

Facilities Installation (days)Lateral Length (ft)

12

Vertical IntegrationCompetitive advantages increase capital efficiency

• Own and operate 7 super-spec

drilling rigs and 1 frac fleet

• Strategic and economic benefit

• Improves operating efficiency and

flexibility

• Mitigates service cost inflation

• Realizing full cost savings from

Southwest Appalachia water project

– $500,000 per well savings

– Improves logistics and reduces

trucking traffic and costs

13

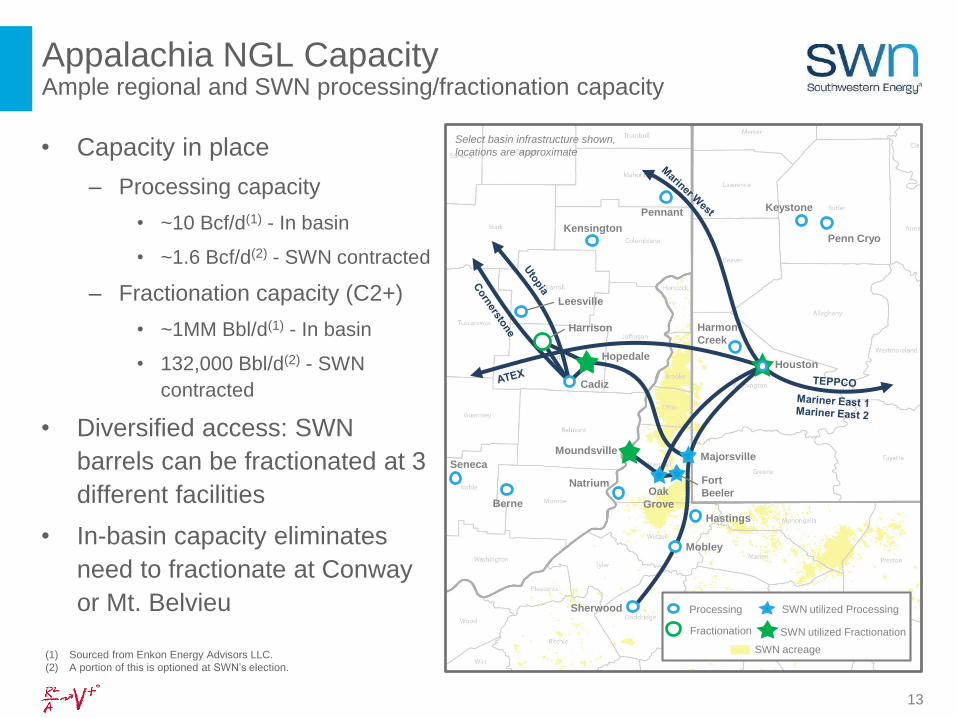

Appalachia NGL Capacity Ample regional and SWN processing/fractionation capacity

• Capacity in place

– Processing capacity

• ~10 Bcf/d(1) - In basin

• ~1.6 Bcf/d(2) - SWN contracted

– Fractionation capacity (C2+)

• ~1MM Bbl/d(1) - In basin

• 132,000 Bbl/d(2) - SWN

contracted

• Diversified access: SWN

barrels can be fractionated at 3

different facilities

• In-basin capacity eliminates

need to fractionate at Conway

or Mt. Belvieu Sherwood

Mobley

Fort

Beeler

Majorsville

Houston

Harrison

Hopedale

Cadiz

Moundsville

Oak

Grove

Hastings

Natrium

Berne

Seneca

Leesville

Kensington

Pennant Keystone

Penn Cryo

Fractionation

Processing

SWN utilized Fractionation

SWN acreage

Harmon

Creek

Select basin infrastructure shown,

locations are approximate

SWN utilized Processing

(1) Sourced from Enkon Energy Advisors LLC.

(2) A portion of this is optioned at SWN’s election.

14

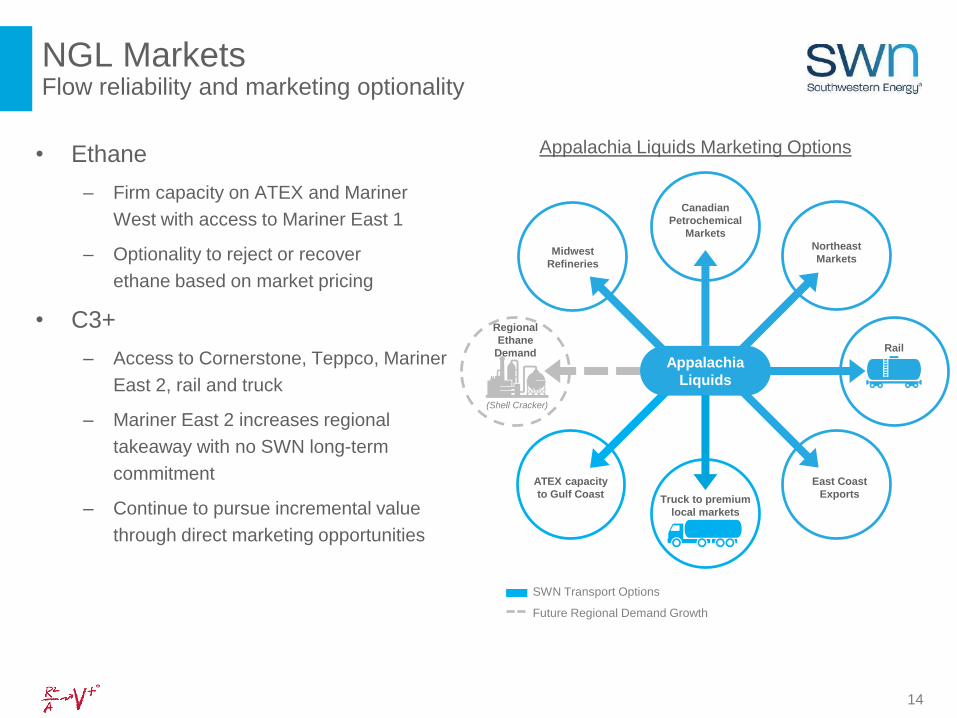

NGL MarketsFlow reliability and marketing optionality

• Ethane

– Firm capacity on ATEX and Mariner

West with access to Mariner East 1

– Optionality to reject or recover

ethane based on market pricing

• C3+

– Access to Cornerstone, Teppco, Mariner

East 2, rail and truck

– Mariner East 2 increases regional

takeaway with no SWN long-term

commitment

– Continue to pursue incremental value

through direct marketing opportunities

SWN Transport Options

Future Regional Demand Growth

Appalachia Liquids Marketing Options

Regional

Ethane

Demand

East Coast

ExportsTruck to premium

local markets

Rail

ATEX capacity

to Gulf Coast

Midwest

Refineries

Northeast

Markets

Canadian

Petrochemical

Markets

Appalachia

Liquids

(Shell Cracker)

15

($0.25)($0.29) ($0.28)

2019 2020 2021

Northeast Appalachia Gas Takeaway Access to diversified and premium markets

Year

Total Firm Takeaway

(MMBtu/d)

Annual WAVG Rate

per MMBtu

2019 1,461,000 $0.27

2020 1,379,000 $0.31

2021 1,351,000 $0.33

Transportation Cost(1,2,3)

2019: 5%

Gulf Coast

2019: 67%

Greater Appalachia

2019: 28%

City Gate

Production Areas

Sales Areas

Millennium

Tennessee Gas Pipeline

Columbia Gas

Transco Pipeline

Weighted Average Basis(4)

M3

(1) Committed volume and rate per MMBtu based on February 5, 2019 contracted takeaway. Substantially all 2019 volume commitment will be used.

(2) Ability to release capacity or buy gas to fill excess transportation capacity.

(3) Constitution in-service is assumed as of April 2020.

(4) Basis as of February 21, 2019.

16

($0.31) ($0.30) ($0.31)

2019 2020 2021

Gulf

Southwest Appalachia Gas TakeawayRight sized with access to premium markets

2019: 57%

Gulf Coast

2019: 34%

TCO - Appalachia

2019: 9%

M2 - Appalachia

Weighted Average Basis(3)

Year

Total Firm Takeaway

(MMBtu/d)

Annual WAVG Rate

per MMBtu

2019 702,000 $0.58

2020 785,000 $0.58

2021 913,000 $0.56

Transportation Cost(1,2)

Production Areas

Sales Areas

TETCO

Columbia Gas/MXP/GXP

Rover

TETCO M2

TCO

(1) Committed volume and rate per MMBtu based on February 5, 2019 contracted takeaway. Not all 2019 volume commitment will be used; however, February 5, 2019

guidance for natural gas price differentials includes all commitment costs.

(2) Ability to release capacity or buy gas to fill excess transportation capacity.

(3) Basis as of February 21, 2019.

17

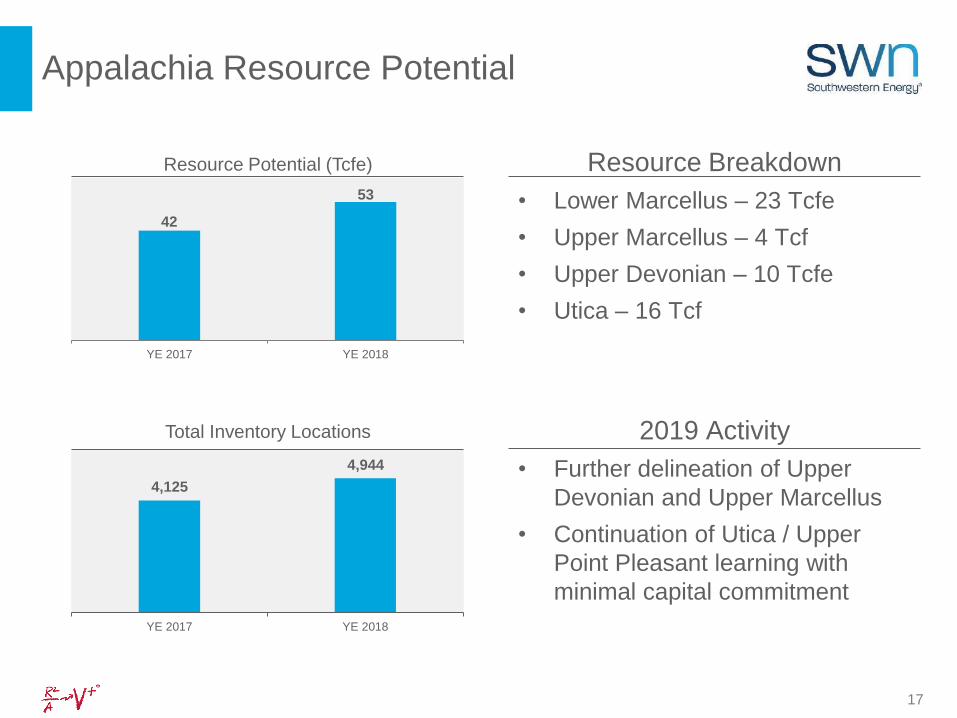

Resource Breakdown

• Lower Marcellus – 23 Tcfe

• Upper Marcellus – 4 Tcf

• Upper Devonian – 10 Tcfe

• Utica – 16 Tcf

2019 Activity

• Further delineation of Upper

Devonian and Upper Marcellus

• Continuation of Utica / Upper

Point Pleasant learning with

minimal capital commitment

YE 2017 YE 2018

YE 2017 YE 2018

Appalachia Resource Potential

Resource Potential (Tcfe)

Total Inventory Locations

4,125

4,944

42

53

18

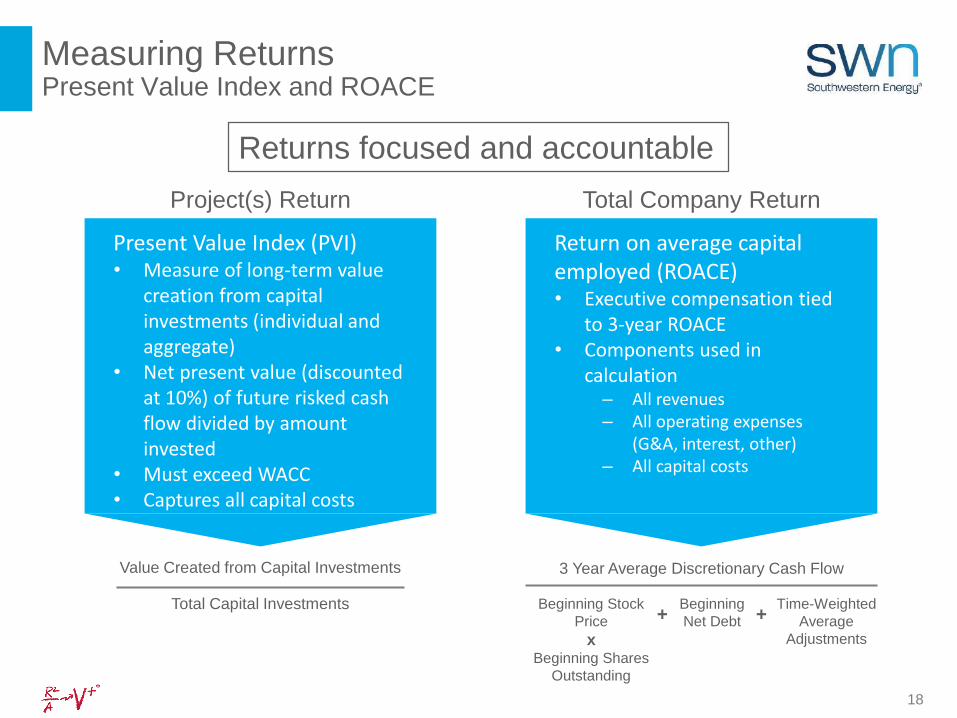

Measuring ReturnsPresent Value Index and ROACE

Project(s) Return

Value Created from Capital Investments

Total Capital Investments

Present Value Index (PVI)• Measure of long-term value

creation from capital investments (individual and aggregate)

• Net present value (discounted at 10%) of future risked cash flow divided by amount invested

• Must exceed WACC• Captures all capital costs

Total Company Return

3 Year Average Discretionary Cash Flow

Beginning

Net Debt

Beginning Stock

Price

xBeginning Shares

Outstanding

Time-Weighted

Average

Adjustments

+ +

Return on average capital employed (ROACE)• Executive compensation tied

to 3-year ROACE• Components used in

calculation‒ All revenues‒ All operating expenses

(G&A, interest, other)‒ All capital costs

Returns focused and accountable

19

Building Long-Term Shareholder Value

• Dynamic and disciplined capital

allocation

• Transition back to free cash flow

neutral by end of 2020

• Strong and flexible balance sheet

• Diversified commodity risk: gas,

NGLs, oil

• Improving capital efficiency and

operational execution

• Recognized environmental

stewardship

• Identify long-term, accretive

opportunities

2020

Appendix

21

An Industry Leader in Corporate Responsibility

Logistics

Advancing Technology to

Reduce Methane Emissions

• Freshwater neutral since December

2016

• Contractor safe driver training• $2.3 million charitable contributions

• 4,056 employee volunteer hours

• Supporting STEM education

• Eliminated 170,000 truckloads in 2019

through pipeline transport of water

• Founding member of consortium

• Targeting a less than 1%

emission rate across natural gas

industry

• Reviewed 100% of chemicals used

for operations since 2016

• API Voluntary Methane Reduction

Program

• Gold Certification by IES

(Independent Energy Standards)

• Company-wide Leak Detection

and Repair (LDAR) Programs

• Participating in scientific studies

• Facilitating new technology

22

Environmental, Social and Governance

• Board independence

8 out of 9 directors are independent

Bill Way, President and CEO, is sole non-

independent director

• Board tenure

Added 4 new directors since 2017

Average board member tenure is less than 5

years

• Board diversity

44% diverse (gender, nationality, ethnicity)

• Best practices

Annual “say on pay” vote

Majority voting in director elections

Annual election of all directors

Proxy access

Ability to call special meetings

No supermajority voting standards

Regular shareholder engagement on

compensation and other key issues

• Management compensation

Independent directors approve compensation

Mix of awards weighted heavily on long-term

equity based incentives

Relative and absolute total shareholder return

Return on Average Capital Employed metric

Stock ownership requirement

Compensation committee retains independent

consultant

• Social

24-hour community hotline in all operating areas

Employee volunteerism well established within

SWN culture

• Environmental and safety

Annual bonus metrics include environmental and

safety performance

Core values of our culture

Certified “green gas” producer

Advanced leak detection technology

Active participant in coalitions focused on reducing

methane emissions

Freshwater neutral

23

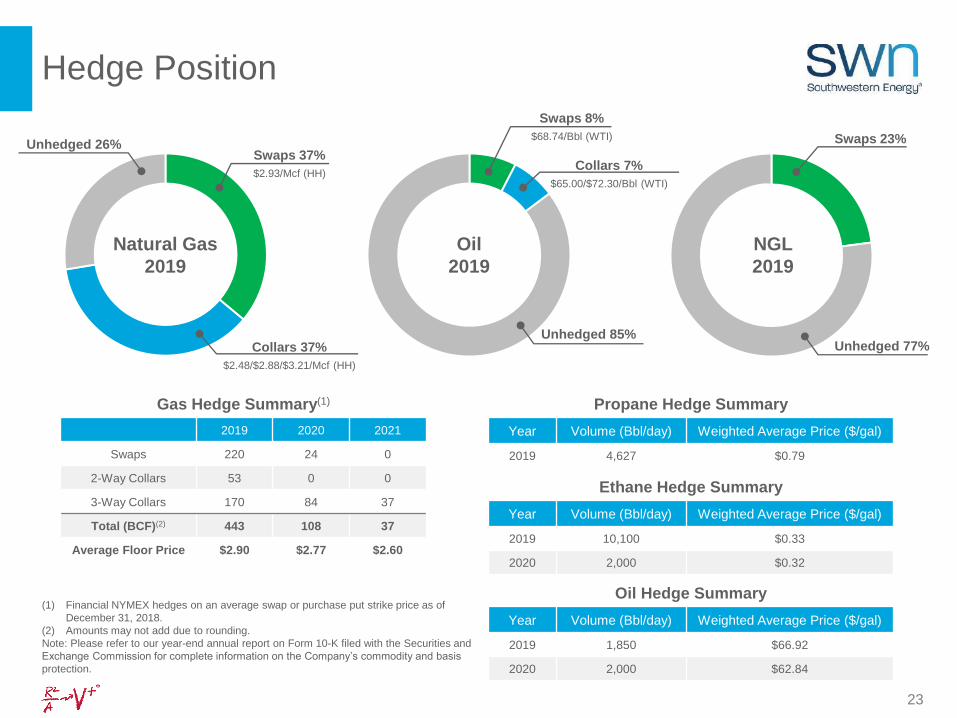

Oil

2019

Swaps 8%

$68.74/Bbl (WTI)

Hedge Position

Collars 7%

$65.00/$72.30/Bbl (WTI)

Natural Gas

2019

Swaps 37%

$2.93/Mcf (HH)

Collars 37%

$2.48/$2.88/$3.21/Mcf (HH)

NGL

2019

Swaps 23%

Ethane Hedge Summary

Year Volume (Bbl/day) Weighted Average Price ($/gal)

2019 10,100 $0.33

2020 2,000 $0.32

Propane Hedge Summary

Year Volume (Bbl/day) Weighted Average Price ($/gal)

2019 4,627 $0.79

Gas Hedge Summary(1)

2019 2020 2021

Swaps 220 24 0

2-Way Collars 53 0 0

3-Way Collars 170 84 37

Total (BCF)(2) 443 108 37

Average Floor Price $2.90 $2.77 $2.60

(1) Financial NYMEX hedges on an average swap or purchase put strike price as of

December 31, 2018.

(2) Amounts may not add due to rounding.

Note: Please refer to our year-end annual report on Form 10-K filed with the Securities and

Exchange Commission for complete information on the Company’s commodity and basis

protection.

Unhedged 85%

Unhedged 26%

Unhedged 77%

Oil Hedge Summary

Year Volume (Bbl/day) Weighted Average Price ($/gal)

2019 1,850 $66.92

2020 2,000 $62.84

24

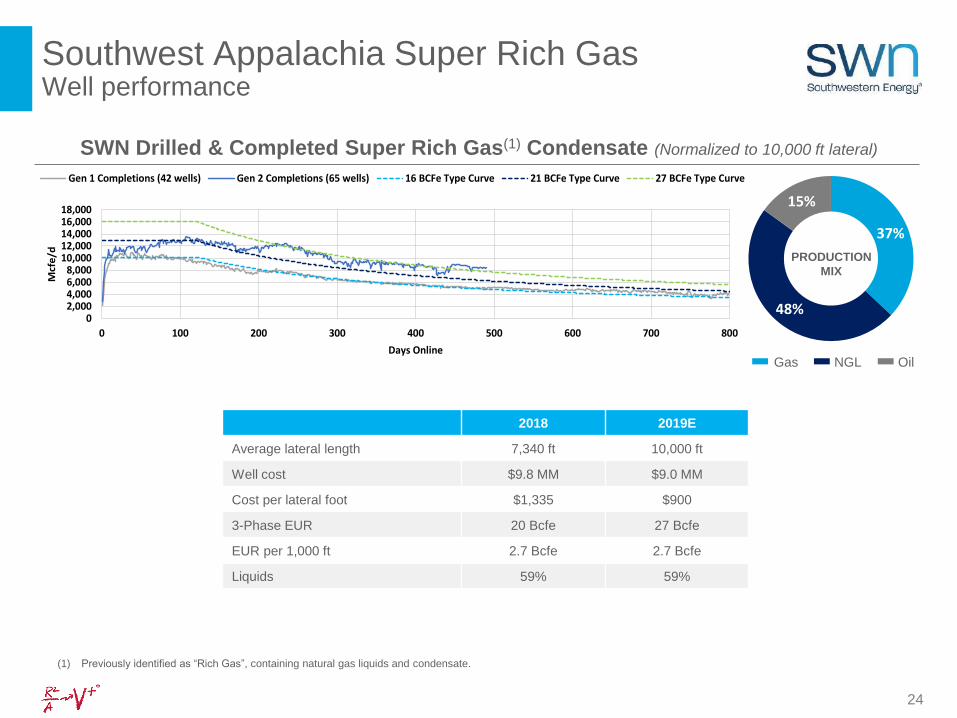

Southwest Appalachia Super Rich GasWell performance

Well Results Exceeding ExpectationsSWN Drilled & Completed Super Rich Gas(1) Condensate (Normalized to 10,000 ft lateral)

Gas NGL Oil

(1) Previously identified as “Rich Gas”, containing natural gas liquids and condensate.

37%

48%

15%

PRODUCTION

MIX

02,0004,0006,0008,000

10,00012,00014,00016,00018,000

0 100 200 300 400 500 600 700 800

Mcf

e/d

Days Online

Gen 1 Completions (42 wells) Gen 2 Completions (65 wells) 16 BCFe Type Curve 21 BCFe Type Curve 27 BCFe Type Curve

2018 2019E

Average lateral length 7,340 ft 10,000 ft

Well cost $9.8 MM $9.0 MM

Cost per lateral foot $1,335 $900

3-Phase EUR 20 Bcfe 27 Bcfe

EUR per 1,000 ft 2.7 Bcfe 2.7 Bcfe

Liquids 59% 59%

25

Southwest Appalachia Rich GasWell performance

Well Results Exceeding Expectations

Gas NGL Oil

SWN Drilled & Completed Rich Gas(1) Condensate (Normalized to 10,000 ft lateral)

(1) Previously identified as “Lean Gas”, containing natural gas liquids.

PRODUCTION

MIX 52%47%

1%

02,0004,0006,0008,000

10,00012,00014,00016,00018,00020,00022,00024,000

0 100 200 300 400 500 600 700 800

Mcf

e/d

Days Online

Gen 1 Completions (22 wells) Gen 2 Completions (15 wells) 32 BCFe Type Curve 40 BCFe Type Curve 48 BCFe Type Curve

2018 2019E

Average lateral length 6,068 ft 10,000 ft

Well cost $9.1 MM $9.6 MM

Cost per lateral foot $1,500 $960

3-Phase EUR 21 Bcfe 35 Bcfe

EUR per 1,000 ft 3.5 Bcfe 3.5 Bcfe

Liquids 42% 43%

26

Northeast AppalachiaWell performance

SWN Drilled & Completed Dry Gas (Normalized to 9,500 ft lateral)

02,0004,0006,0008,000

10,00012,00014,00016,00018,00020,00022,00024,00026,00028,00030,00032,000

0 100 200 300 400 500 600 700 800

Daily

Rate

, M

cf/

d

Days of Production

Legacy Susquehanna & Bradford (113 Wells) Tioga Area (15 Wells) 15 BCF EUR Curve 20 BCF EUR Curve 25 BCF EUR Curve

2018 Susquehanna 2019E Tioga 2019E

Average lateral length 7,584 ft 9,500 ft 9,500 ft

Well cost $7.5 MM $7.6 MM $7.9 MM

Cost per lateral foot $988 $804 $834

EUR 17 Bcf 20 Bcf 19 Bcf

EUR per 1,000 ft 2.2 Bcf 2.1 Bcf 2.0 Bcf

27

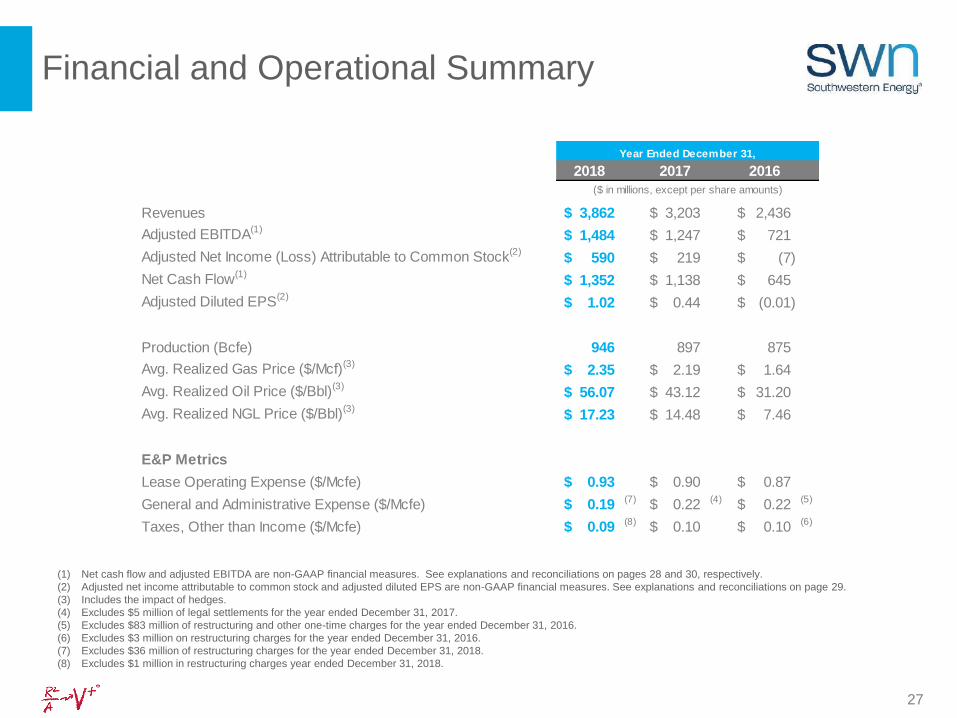

Financial and Operational Summary

(1) Net cash flow and adjusted EBITDA are non-GAAP financial measures. See explanations and reconciliations on pages 28 and 30, respectively.

(2) Adjusted net income attributable to common stock and adjusted diluted EPS are non-GAAP financial measures. See explanations and reconciliations on page 29.

(3) Includes the impact of hedges.

(4) Excludes $5 million of legal settlements for the year ended December 31, 2017.

(5) Excludes $83 million of restructuring and other one-time charges for the year ended December 31, 2016.

(6) Excludes $3 million on restructuring charges for the year ended December 31, 2016.

(7) Excludes $36 million of restructuring charges for the year ended December 31, 2018.

(8) Excludes $1 million in restructuring charges year ended December 31, 2018.

2018 2017 2016

Revenues 3,862$ 3,203$ 2,436$

Adjusted EBITDA(1)1,484$ 1,247$ 721$

Adjusted Net Income (Loss) Attributable to Common Stock(2)590$ 219$ (7)$

Net Cash Flow(1)1,352$ 1,138$ 645$

Adjusted Diluted EPS(2)1.02$ 0.44$ (0.01)$

Production (Bcfe) 946 897 875

Avg. Realized Gas Price ($/Mcf)(3)2.35$ 2.19$ 1.64$

Avg. Realized Oil Price ($/Bbl)(3)56.07$ 43.12$ 31.20$

Avg. Realized NGL Price ($/Bbl)(3)17.23$ 14.48$ 7.46$

E&P Metrics

Lease Operating Expense ($/Mcfe) 0.93$ 0.90$ 0.87$

General and Administrative Expense ($/Mcfe) 0.19$ (7) 0.22$ (4) 0.22$ (5)

Taxes, Other than Income ($/Mcfe) 0.09$ (8) 0.10$ 0.10$ (6)

Year Ended December 31,

($ in millions, except per share amounts)

28

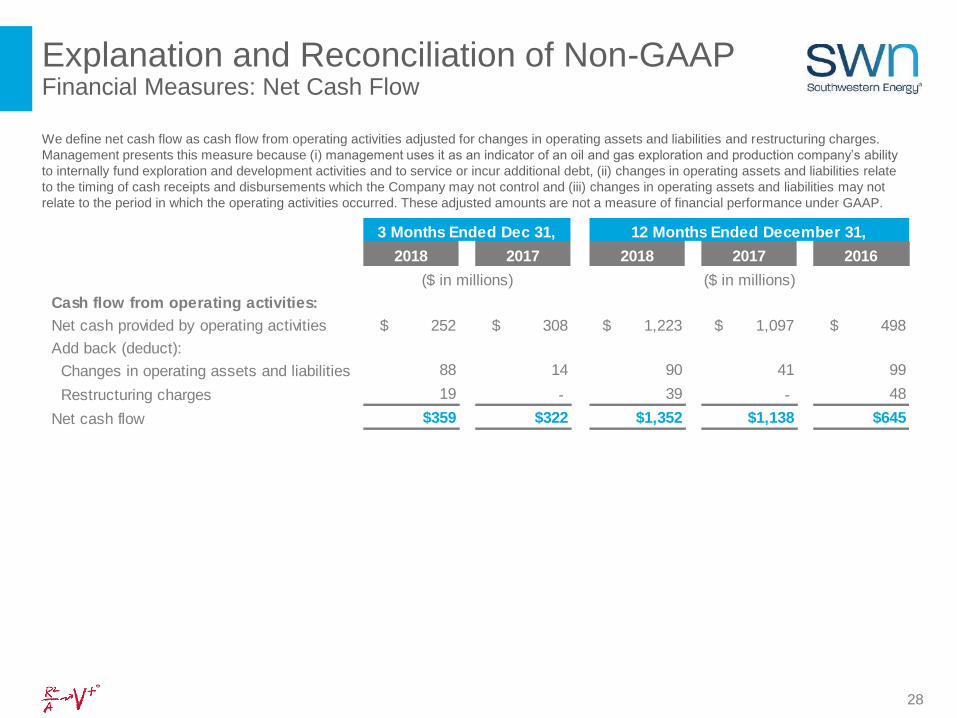

Explanation and Reconciliation of Non-GAAP Financial Measures: Net Cash Flow

We define net cash flow as cash flow from operating activities adjusted for changes in operating assets and liabilities and restructuring charges.

Management presents this measure because (i) management uses it as an indicator of an oil and gas exploration and production company’s ability

to internally fund exploration and development activities and to service or incur additional debt, (ii) changes in operating assets and liabilities relate

to the timing of cash receipts and disbursements which the Company may not control and (iii) changes in operating assets and liabilities may not

relate to the period in which the operating activities occurred. These adjusted amounts are not a measure of financial performance under GAAP.

2018 2017 2018 2017 2016

Cash flow from operating activities:

Net cash provided by operating activities $ 252 $ 308 $ 1,223 $ 1,097 $ 498

Add back (deduct):

Changes in operating assets and liabilities 88 14 90 41 99

Restructuring charges 19 - 39 - 48

Net cash flow $359 $322 $1,352 $1,138 $645

3 Months Ended Dec 31,

($ in millions)

12 Months Ended December 31,

($ in millions)

29

Explanation and Reconciliation of Non-GAAP Financial Measures: Adjusted Net Income Attributable to Common Stock

Additional non-GAAP financial measures we may present from time to time are adjusted net income attributable to common stock and adjusted

diluted earnings per share attributable to Southwestern Energy stockholders, both of which exclude certain charges or amounts shown in the

tables below. Management presents these measures because (i) they are consistent with the manner in which the Company’s performance is

measured relative to the performance of its peers, (ii) these measures are more comparable to earnings estimates provided by securities

analysts, and (iii) charges or amounts excluded cannot be reasonably estimated and guidance provided by the Company excludes information

regarding these types of items. These adjusted amounts are not a measure of financial performance under GAAP.

(1) Primarily relates to the exclusion of certain discrete tax adjustments due to an increase to the valuation allowance against the Company’s deferred tax assets

($ in millions) (per share) ($ in millions) (per share)

Net income attributable to common stock 307$ 0.54$ 267$ 0.53$

Add back (deduct):

Participating securities - mandatory convertible preferred stock - - 31 0.06

Restructuring and other one-time charges 19 0.03 - -

Gain on sale of assets, net (16) (0.03) (1) -

(Gain) loss on certain derivatives (89) (0.16) (101) (0.20)

Loss on early debt extinguishment and other 9 0.02 3 0.01

Legal settlements 1 - - -

Loss on foreign currency adjustment - - 6 0.01

Adjustments due to inventory valuation 2 0.01 (1) -

Adjustments due to discrete tax items (1) (75) (0.13) (176) (0.36)

Tax impact on adjustments 18 0.03 35 0.07

Adjusted net income attributable to common stock 176$ 0.31$ 63$ 0.12$

($ in millions) (per share) ($ in millions) (per share) ($ in millions) (per share)

Net income (loss) attributable to common stock 535$ 0.93$ 815$ 1.63$ (2,751)$ (6.32)$

Add back (deduct):

Participating securities - mandatory convertible preferred stock -$ -$ 90$ 0.18$ -$ -$

Impairments 171 0.30 - - 2,321 5.33

Restructuring and other one-time charges 39 0.06 - - 89 0.20

Gain on sale of assets, net (17) (0.03) (4) (0.01) (3) (0.00)

(Gain) Loss on certain derivatives 24 0.04 (451) (0.90) 373 0.86

Loss on early debt extinguishment and other (1) 17 0.03 73 0.15 57 0.13

Legal settlements 9 0.02 5 0.01 - -

Loss on foreign currency adjustment - - 6 0.01 - -

Adjustments due to inventory valuation 3 0.01 (2) (0.00) 3 0.01

Adjustments due to discrete tax items (1) (130) (0.23) (455) (0.91) 978 2.25

Tax impact on adjustments (61) (0.11) 142 0.28 (1,074) (2.47)

Adjusted net income (loss) 590$ 1.02$ 219$ 0.44$ (7)$ (0.01)$

2018 2017

12 Months Ended December 31,

2018 2017 2016

3 Months Ended December 31,

30

Explanation and Reconciliation of Non-GAAP Financial Measures: Adjusted EBITDA

EBITDA is defined as net income plus interest, income tax expense, depreciation, depletion and amortization. Adjusted EBITDA is defined as

EBITDA less gains (losses) on sale of assets and gains (losses) on unsettled derivatives plus write-down of inventory, non-cash stock-based

compensation, restructuring charges, loss on debt extinguishment, impairments, legal settlements and foreign currency adjustments.

Southwestern has included information concerning EBITDA and Adjusted EBITDA because they are used by certain investors as a measure of the

ability of a company to service or incur indebtedness and because it is a financial measure commonly used in the energy industry. EBITDA and

Adjusted EBITDA should not be considered in isolation or as a substitute for net income, net cash provided by operating activities or other income

or cash flow data prepared in accordance with GAAP or as a measure of the Company's profitability or liquidity. EBITDA and Adjusted EBITDA, as

defined above, may not be comparable to similarly titled measures of other companies. Net income is a financial measure calculated and

presented in accordance with generally accepted accounting principles. The table below reconciles historical net income with historical Adjusted

EBITDA.

(1) 2016 includes the impact from a full cost ceiling test impairment of our natural gas and oil properties.

(1)

2018 2017 2016

Net income (loss) 537$ 1,046$ (2,643)$

Add back (deduct):

Net interest expense 124 135 88

Provision (benefit) for income taxes 1 (93) (29)

Depreciation, depletion and amortization 560 504 436

Impairments(1) 171 - 2,321

Restructuring and other one-time charges 39 - 89

Gain on sale of assets, net (17) (4) (3)

Loss on early extinguishment of debt 17 73 51

Legal settlements 9 5 -

(Gain) loss on unsettled derivatives 24 (451) 373

Loss on foreign currency adjustment - 6 -

Adjustments due to inventory valuation and other 3 (2) 3

Stock-based compensation expense 16 28 35

Adjusted EBITDA $1,484 $1,247 $721

($ in millions)

12 Months Ended December 31,

31

Explanation and Reconciliation of Non-GAAP Financial Measures: Net debt / Adj. EBITDA

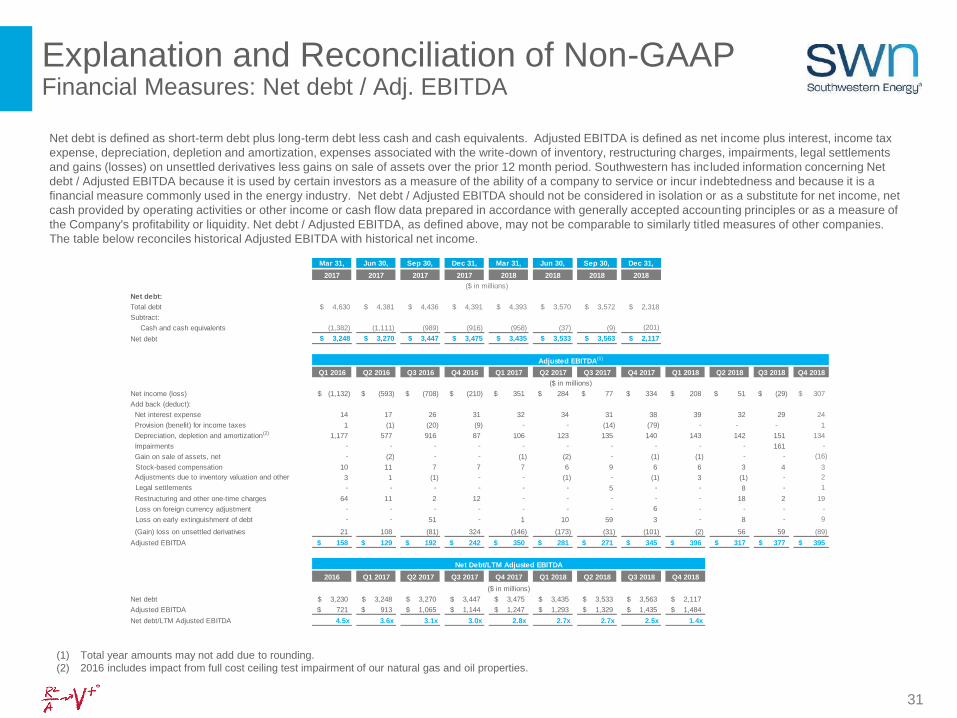

Net debt is defined as short-term debt plus long-term debt less cash and cash equivalents. Adjusted EBITDA is defined as net income plus interest, income tax

expense, depreciation, depletion and amortization, expenses associated with the write-down of inventory, restructuring charges, impairments, legal settlements

and gains (losses) on unsettled derivatives less gains on sale of assets over the prior 12 month period. Southwestern has included information concerning Net

debt / Adjusted EBITDA because it is used by certain investors as a measure of the ability of a company to service or incur indebtedness and because it is a

financial measure commonly used in the energy industry. Net debt / Adjusted EBITDA should not be considered in isolation or as a substitute for net income, net

cash provided by operating activities or other income or cash flow data prepared in accordance with generally accepted accounting principles or as a measure of

the Company's profitability or liquidity. Net debt / Adjusted EBITDA, as defined above, may not be comparable to similarly ti tled measures of other companies.

The table below reconciles historical Adjusted EBITDA with historical net income.

(1) Total year amounts may not add due to rounding.

(2) 2016 includes impact from full cost ceiling test impairment of our natural gas and oil properties.

Mar 31, Jun 30, Sep 30, Dec 31, Mar 31, Jun 30, Sep 30, Dec 31,

2017 2017 2017 2017 2018 2018 2018 2018

Net debt:

Total debt $ 4,630 $ 4,381 $ 4,436 $ 4,391 $ 4,393 $ 3,570 $ 3,572 $ 2,318

Subtract:

Cash and cash equivalents (1,382) (1,111) (989) (916) (958) (37) (9) (201)

Net debt $ 3,248 $ 3,270 $ 3,447 $ 3,475 $ 3,435 $ 3,533 $ 3,563 $ 2,117

Q1 2016 Q2 2016 Q3 2016 Q4 2016 Q1 2017 Q2 2017 Q3 2017 Q4 2017 Q1 2018 Q2 2018 Q3 2018 Q4 2018

Net income (loss) (1,132)$ (593)$ (708)$ (210)$ 351$ 284$ 77$ 334$ 208$ 51$ (29)$ 307$

Add back (deduct):

Net interest expense 14 17 26 31 32 34 31 38 39 32 29 24

Provision (benefit) for income taxes 1 (1) (20) (9) - - (14) (79) - - - 1

Depreciation, depletion and amortization(2) 1,177 577 916 87 106 123 135 140 143 142 151 134

Impairments - - - - - - - - - - 161 -

Gain on sale of assets, net - (2) - - (1) (2) - (1) (1) - - (16)

Stock-based compensation 10 11 7 7 7 6 9 6 6 3 4 3

Adjustments due to inventory valuation and other 3 1 (1) - - (1) - (1) 3 (1) - 2

Legal settlements - - - - - - 5 - - 8 - 1

Restructuring and other one-time charges 64 11 2 12 - - - - - 18 2 19

Loss on foreign currency adjustment - - - - - - - 6 - - - -

Loss on early extinguishment of debt - - 51 - 1 10 59 3 - 8 - 9

(Gain) loss on unsettled derivatives 21 108 (81) 324 (146) (173) (31) (101) (2) 56 59 (89)

Adjusted EBITDA 158$ 129$ 192$ 242$ 350$ 281$ 271$ 345$ 396$ 317$ 377$ 395$

2016 Q1 2017 Q2 2017 Q3 2017 Q4 2017 Q1 2018 Q2 2018 Q3 2018 Q4 2018

Net debt 3,230$ 3,248$ 3,270$ 3,447$ 3,475$ 3,435$ 3,533$ 3,563$ 2,117$

Adjusted EBITDA 721$ 913$ 1,065$ 1,144$ 1,247$ 1,293$ 1,329$ 1,435$ 1,484$

Net debt/LTM Adjusted EBITDA 4.5x 3.6x 3.1x 3.0x 2.8x 2.7x 2.7x 2.5x 1.4x

($ in millions)

Adjusted EBITDA(1)

($ in millions)

Net Debt/LTM Adjusted EBITDA

($ in millions)