LATER LIFE MORTGAGE LENDING

5

Q2 2021 Update Callum Bilbe Analyst, Data & Research This new UK Finance update provides a quarterly insight into mortgage lending to borrowers over age 55, the trends in lending and demographics of borrowers accessing the market. These trends cover mainstream lending to older borrowers, as well as specialist products such as lifetime mortgages This quarter’s update highlights the vital role that later life lending plays in the wider mortgage market. The figures also highlight how the sector is set to enhance its status as a key component of the industry in the coming years, as the age of mortgage holders shifts upwards. Written by: LATER LIFE MORTGAGE LENDING KEY FINDINGS: • Later life mortgage lending (lending to borrowers over age 55) is increasing in popularity. While in part due to an ageing population, a more significant driver appears to be steadily increasing mortgage terms over the past 15 years. In 2021, the proportion of new mortgage lending to homeowners with a term ending past the main borrowers 65th birthday makes up more than 50 per cent of all homeowner loans. This is the first time this proportion has been reached since records began, and demonstrates that later life mortgage lending is set to become more significant in the future. • Mortgage lending to older borrowers has increased in popularity since 2014, returning to pre- pandemic levels in 2021. This is driven in part by increases in house purchase due to the stamp duty holiday, but also by stability in lending across different products. Older borrowers have continued to access a wide range of products as lenders have largely overcome the logistical and affordability challenges presented as a result of the Covid-19 pandemic relatively quickly. • Over the past five years, mortgage lending to over 55’s has continued to grow, even where gross lending in the wider mortgage market has remained subdued; in part due to loans to older borrowers having strong affordability. • Within the wider later life lending market, lifetime mortgages (also known as equity release products) have continued to grow in popularity over the past seven years as older homeowners look to access the equity in their homes. There has been a recent modest reduction in lifetime mortgages, due in part to the Covid-19 pandemic, however this reduction is expected to be temporary as pandemic restrictions are lifted.

Transcript of LATER LIFE MORTGAGE LENDING

Q2 2021 Update

Callum BilbeAnalyst, Data & Research

This new UK Finance update provides a quarterly insight into mortgage lending to borrowers over age 55, the trends in lending and demographics of borrowers accessing the market. These trends cover mainstream lending to older borrowers, as well as specialist products such as lifetime mortgages

This quarter’s update highlights the vital role that later life lending plays in the wider mortgage market. The figures also highlight how the sector is set to enhance its status as a key component of the industry in the coming years, as the age of mortgage holders shifts upwards.

Written by:

LATER LIFE MORTGAGE LENDING

KEY FINDINGS: • Later life mortgage lending (lending to borrowers over age 55) is increasing in popularity. While

in part due to an ageing population, a more significant driver appears to be steadily increasing mortgage terms over the past 15 years. In 2021, the proportion of new mortgage lending to homeowners with a term ending past the main borrowers 65th birthday makes up more than 50 per cent of all homeowner loans. This is the first time this proportion has been reached since records began, and demonstrates that later life mortgage lending is set to become more significant in the future.

• Mortgage lending to older borrowers has increased in popularity since 2014, returning to pre-pandemic levels in 2021. This is driven in part by increases in house purchase due to the stamp duty holiday, but also by stability in lending across different products. Older borrowers have continued to access a wide range of products as lenders have largely overcome the logistical and affordability challenges presented as a result of the Covid-19 pandemic relatively quickly.

• Over the past five years, mortgage lending to over 55’s has continued to grow, even where gross lending in the wider mortgage market has remained subdued; in part due to loans to older borrowers having strong affordability.

• Within the wider later life lending market, lifetime mortgages (also known as equity release products) have continued to grow in popularity over the past seven years as older homeowners look to access the equity in their homes. There has been a recent modest reduction in lifetime mortgages, due in part to the Covid-19 pandemic, however this reduction is expected to be temporary as pandemic restrictions are lifted.

Charles Roe, Director of Mortgages at UK Finance said:

“There’s been growing demand for mortgages from those aged over 55 and this is set to continue as more people live and work for longer.

“For the first time since records began more than half of all new mortgages are due to end after the homeowner’s 65th birthday, and lending to over 55s has grown even where mortgage lending in the wider market has remained subdued.

“Later life lending both now and in the future will be imperative as existing homeowners look to later life products for accessing equity as they get older.”

Jim Boyd, Chief Executive of the Equity Release Council said:

“UK Finance’s findings underscore the integral role that later life lending plays in consumers’ long-term security. Attitudes towards home finance in later life have changed, and homeowners are increasingly comfortable with mortgage borrowing into retirement and open to the benefits of realising some of their property wealth as they age.

“Property wealth can play an important part in a holistic approach to funding retirement and, as an industry, we must work together to ensure consumers get the information they need to weigh up increasingly complex financial decisions to do this.”

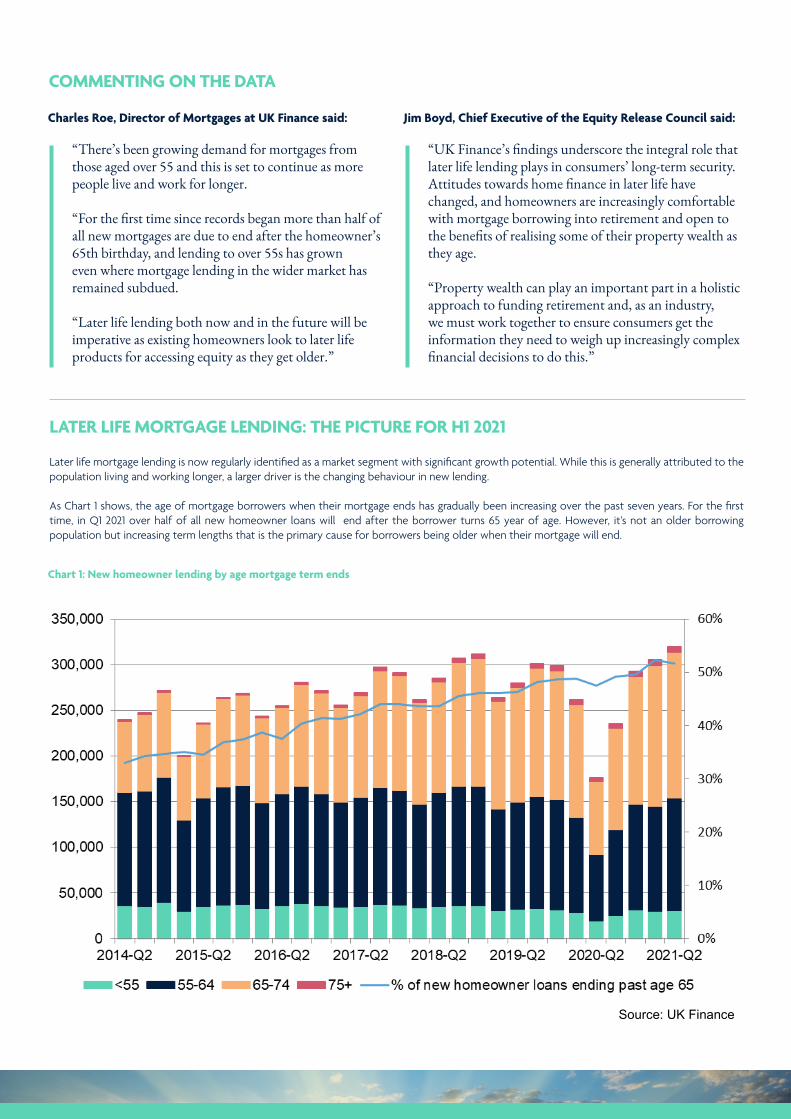

LATER LIFE MORTGAGE LENDING: THE PICTURE FOR H1 2021

Later life mortgage lending is now regularly identified as a market segment with significant growth potential. While this is generally attributed to the population living and working longer, a larger driver is the changing behaviour in new lending.

As Chart 1 shows, the age of mortgage borrowers when their mortgage ends has gradually been increasing over the past seven years. For the first time, in Q1 2021 over half of all new homeowner loans will end after the borrower turns 65 year of age. However, it’s not an older borrowing population but increasing term lengths that is the primary cause for borrowers being older when their mortgage will end.

Chart 1: New homeowner lending by age mortgage term ends

“Property wealth can play an important part in a holistic approach to funding retirement and, as an industry, we must work together to ensure consumers get the information they need to weigh up increasingly complex financial decisions to do this.”

Later life mortgage lending: The picture for H1 2021 Later life mortgage lending is now regularly identified as a market segment with significant growth potential. While this is generally attributed to the population living and working longer, a larger driver is the changing behaviour in new lending. As Chart 1 shows, the age of mortgage borrowers when their mortgage ends has gradually been increasing over the past seven years. For the first time, in Q1 2021 over half of all new homeowner loans will end after the borrower turns 65 year of age. However, it’s not an older borrowing population but increasing term lengths that is the primary cause for borrowers being older when their mortgage will end. Chart 1: New homeowner lending by age mortgage term ends

Source: UK Finance

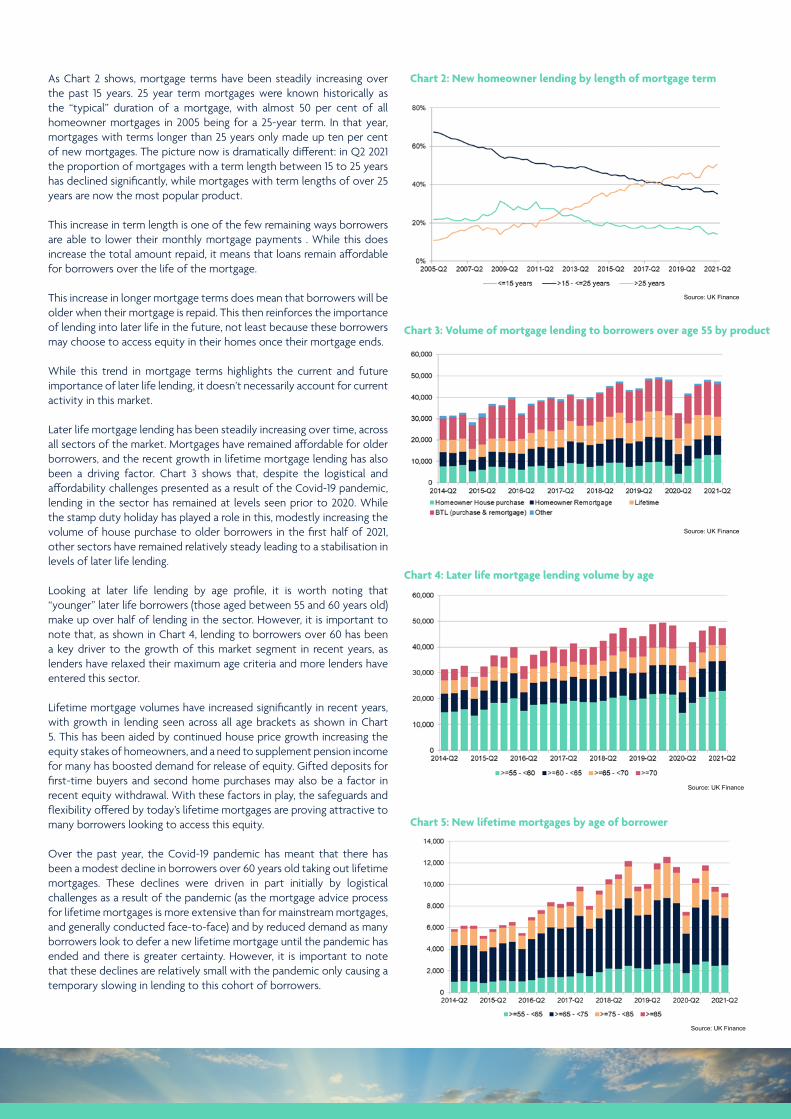

As Chart 2 shows, mortgage terms have been steadily increasing over the past 15 years. 25 year term mortgages were known historically as the “typical” duration of a mortgage, with almost 50 per cent of all homeowner mortgages in 2005 being for a 25-year term. In that year, mortgages with terms longer than 25 years only made up ten per cent of new mortgages. The picture now is dramatically different: in Q2 2021 the proportion of mortgages with a term length between 15 to 25 years has declined significantly, while mortgages with term lengths of over 25 years are now the most popular product. This increase in term length is one of the few remaining ways borrowers are able to lower their monthly mortgage payments . While this does increase the total amount repaid, it means that loans remain affordable for borrowers over the life of the mortgage. This increase in longer mortgage terms does mean that borrowers will be older when their mortgage is repaid. This then reinforces the importance of lending into later life in the future, not least because these borrowers may choose to access equity in their homes once their mortgage ends.

COMMENTING ON THE DATA

As Chart 2 shows, mortgage terms have been steadily increasing over the past 15 years. 25 year term mortgages were known historically as the “typical” duration of a mortgage, with almost 50 per cent of all homeowner mortgages in 2005 being for a 25-year term. In that year, mortgages with terms longer than 25 years only made up ten per cent of new mortgages. The picture now is dramatically different: in Q2 2021 the proportion of mortgages with a term length between 15 to 25 years has declined significantly, while mortgages with term lengths of over 25 years are now the most popular product.

This increase in term length is one of the few remaining ways borrowers are able to lower their monthly mortgage payments . While this does increase the total amount repaid, it means that loans remain affordable for borrowers over the life of the mortgage.

This increase in longer mortgage terms does mean that borrowers will be older when their mortgage is repaid. This then reinforces the importance of lending into later life in the future, not least because these borrowers may choose to access equity in their homes once their mortgage ends.

While this trend in mortgage terms highlights the current and future importance of later life lending, it doesn’t necessarily account for current activity in this market.

Later life mortgage lending has been steadily increasing over time, across all sectors of the market. Mortgages have remained affordable for older borrowers, and the recent growth in lifetime mortgage lending has also been a driving factor. Chart 3 shows that, despite the logistical and affordability challenges presented as a result of the Covid-19 pandemic, lending in the sector has remained at levels seen prior to 2020. While the stamp duty holiday has played a role in this, modestly increasing the volume of house purchase to older borrowers in the first half of 2021, other sectors have remained relatively steady leading to a stabilisation in levels of later life lending.

Looking at later life lending by age profile, it is worth noting that “younger” later life borrowers (those aged between 55 and 60 years old) make up over half of lending in the sector. However, it is important to note that, as shown in Chart 4, lending to borrowers over 60 has been a key driver to the growth of this market segment in recent years, as lenders have relaxed their maximum age criteria and more lenders have entered this sector.

Lifetime mortgage volumes have increased significantly in recent years, with growth in lending seen across all age brackets as shown in Chart 5. This has been aided by continued house price growth increasing the equity stakes of homeowners, and a need to supplement pension income for many has boosted demand for release of equity. Gifted deposits for first-time buyers and second home purchases may also be a factor in recent equity withdrawal. With these factors in play, the safeguards and flexibility offered by today’s lifetime mortgages are proving attractive to many borrowers looking to access this equity.

Over the past year, the Covid-19 pandemic has meant that there has been a modest decline in borrowers over 60 years old taking out lifetime mortgages. These declines were driven in part initially by logistical challenges as a result of the pandemic (as the mortgage advice process for lifetime mortgages is more extensive than for mainstream mortgages, and generally conducted face-to-face) and by reduced demand as many borrowers look to defer a new lifetime mortgage until the pandemic has ended and there is greater certainty. However, it is important to note that these declines are relatively small with the pandemic only causing a temporary slowing in lending to this cohort of borrowers.

Chart 2: New homeowner lending by length of mortgage term Chart 2: New homeowner lending by length of mortgage term

Source: UK Finance

While this trend in mortgage terms highlights the current and future importance of later life lending, it doesn’t necessarily account for current activity in this market. Later life mortgage lending has been steadily increasing over time, across all sectors of the market. Mortgages have remained affordable for older borrowers, and the recent growth in lifetime mortgage lending has also been a driving factor. Chart 3 shows that, despite the logistical and affordability challenges presented as a result of the Covid-19 pandemic, lending in the sector has remained at levels seen prior to 2020. While the stamp duty holiday has played a role in this, modestly increasing the volume of house purchase to older borrowers in the first half of 2021, other sectors have remained relatively steady leading to a stabilisation in levels of later life lending. Chart 3: Volume of mortgage lending to borrowers over age 55 by product

Source: UK Finance

Chart 3: Volume of mortgage lending to borrowers over age 55 by product

Chart 2: New homeowner lending by length of mortgage term

Source: UK Finance

While this trend in mortgage terms highlights the current and future importance of later life lending, it doesn’t necessarily account for current activity in this market. Later life mortgage lending has been steadily increasing over time, across all sectors of the market. Mortgages have remained affordable for older borrowers, and the recent growth in lifetime mortgage lending has also been a driving factor. Chart 3 shows that, despite the logistical and affordability challenges presented as a result of the Covid-19 pandemic, lending in the sector has remained at levels seen prior to 2020. While the stamp duty holiday has played a role in this, modestly increasing the volume of house purchase to older borrowers in the first half of 2021, other sectors have remained relatively steady leading to a stabilisation in levels of later life lending. Chart 3: Volume of mortgage lending to borrowers over age 55 by product

Source: UK Finance

Chart 4: Later life mortgage lending volume by age

Looking at later life lending by age profile, it is worth noting that “younger” later life borrowers (those aged between 55 and 60 years old) make up over half of lending in the sector. However, it is important to note that, as shown in Chart 4, lending to borrowers over 60 has been a key driver to the growth of this market segment in recent years, as lenders have relaxed their maximum age criteria and more lenders have entered this sector. Chart 4: Later life mortgage lending volume by age

Source: UK Finance

Lifetime mortgage volumes have increased significantly in recent years, with growth in lending seen across all age brackets as shown in Chart 5. This has been aided by continued house price growth increasing the equity stakes of homeowners, and a need to supplement pension income for many has boosted demand for release of equity. Gifted deposits for first-time buyers and second home purchases may also be a factor in recent equity withdrawal. With these factors in play, the safeguards and flexibility offered by today’s lifetime mortgages are proving attractive to many borrowers looking to access this equity. Over the past year, the Covid-19 pandemic has meant that there has been a modest decline in borrowers over 60 years old taking out lifetime mortgages. These declines were driven in part initially by logistical challenges as a result of the pandemic (as the mortgage advice process for lifetime mortgages is more extensive than for mainstream mortgages, and generally conducted face-to-face) and by reduced demand as many borrowers look to defer a new lifetime mortgage until the pandemic has ended and there is greater certainty. However, it is important to note that these declines are relatively small with the pandemic only causing a temporary slowing in lending to this cohort of borrowers. Chart 5: New lifetime mortgages by age of borrower

Chart 5: New lifetime mortgages by age of borrower

Source: UK Finance

Quarterly Spotlight: How does later life mortgage lending performance compare to the wider market? Each quarter we will take a more in-depth look at a specific part of the later life mortgage lending market. This quarter, we look at how later life lending has fared recently compared to the wider mortgage market. While gross mortgage lending in the wider mortgage market had been subdued in recent years, lending to over 55’s grew steadily each year up to 2020. While we might have expected this to be driven by growth in lifetime loans, residential lending to over 55s has also increased. This has led to the later life sector outperforming total market gross lending consistently from Q2 2018 to the end of 2020, where the stamp duty holiday saw demand from younger borrowers looking to buy a new home outstrip demand from older borrowers. Chart 6: Gross Mortgage Lending by market, year-on-year percentage change

QUARTERLY SPOTLIGHT: HOW DOES LATER LIFE MORTGAGE LENDING PERFORMANCE COMPARE TO THE WIDER MARKET?

Each quarter we will take a more in-depth look at a specific part of the later life mortgage lending market. This quarter, we look at how later life lending has fared recently compared to the wider mortgage market.

While gross mortgage lending in the wider mortgage market had been subdued in recent years, lending to over 55’s grew steadily each year up to 2020. While we might have expected this to be driven by growth in lifetime loans, residential lending to over 55s has also increased. This has led to the later life sector outperforming total market gross lending consistently from Q2 2018 to the end of 2020, where the stamp duty holiday saw demand from younger borrowers looking to buy a new home outstrip demand from older borrowers.

For those older borrowers, higher equity stakes increase their borrowing options and lowers the barriers to accessing mortgage credit. Chart 7 shows that, while loan to value ratios (LTVs) for younger borrowers increased over time, the opposite was true for older borrowers. We’ve seen similar trends across other measures of affordability, allowing for more transactions to take place within the older borrower cohort.

Overall, lending to older borrowers has been a vital part of the mortgage market over the past decade, with it anticipated to increase its importance in the future. Our next update for Q3 2021 data will focus on how the sector has adapted to ensure more older borrowers are able to access the market as they age and their situations become more complex.

Chart 6: Gross Mortgage Lending by market, year-on-year percentage change

Source: UK Finance

Quarterly Spotlight: How does later life mortgage lending performance compare to the wider market? Each quarter we will take a more in-depth look at a specific part of the later life mortgage lending market. This quarter, we look at how later life lending has fared recently compared to the wider mortgage market. While gross mortgage lending in the wider mortgage market had been subdued in recent years, lending to over 55’s grew steadily each year up to 2020. While we might have expected this to be driven by growth in lifetime loans, residential lending to over 55s has also increased. This has led to the later life sector outperforming total market gross lending consistently from Q2 2018 to the end of 2020, where the stamp duty holiday saw demand from younger borrowers looking to buy a new home outstrip demand from older borrowers. Chart 6: Gross Mortgage Lending by market, year-on-year percentage change

Chart 7: Average loan-to-value for homeowner mortgages, split by age of borrower

Source: Bank of England/UK Finance

For those older borrowers, higher equity stakes increase their borrowing options and lowers the barriers to accessing mortgage credit. Chart 7 shows that, while loan to value ratios (LTVs) for younger borrowers increased over time, the opposite was true for older borrowers. We’ve seen similar trends across other measures of affordability, allowing for more transactions to take place within the older borrower cohort. Chart 7: Average loan-to-value for homeowner mortgages, split by age of borrower

Source: UK Finance

Overall, lending to older borrowers has been a vital part of the mortgage market over the past decade, with it anticipated to increase its importance in the future. Our next update for Q3 2021 data will focus on how the sector has adapted to ensure more older borrowers are able to access the market as they age and their situations become more complex. New later life mortgage lending

2019-Q2 2019-Q3 2019-Q4 2020-Q1 2020-Q2 2020-Q3 2020-Q4 2021-Q1 2021-Q2

Volume 44,000 48,690 49,330 48,220 32,640 41,700 46,250 47,990 47,220

Value (£bn) 5.57 6.29 6.46 6.38 4.35 5.86 6.50 7.17 7.34 New later life mortgage lending, by product

2019-Q2

2019-Q3

2019-Q4

2020-Q1

2020-Q2

2020-Q3

2020-Q4

2021-Q1

2021-Q2

Homeowner House purchase 8,190 9,780 9,920 8,130 4,430 8,080 11,580 13,050 13,220

Homeowner remortgage 11,160 11,850 11,300 12,030 9,170 9,360 8,690 9,100 8,860

Buy-to-let (purchase & remortgage)

14,060 14,470 14,880 15,890 11,350 13,170 13,640 15,410 14,970

Lifetime Mortgage 9,990 11,900 12,510 11,580 7,430 10,530 11,740 9,740 9,150* *Lifetime mortgage figure for the most recent quarter (Q2 2021) is an estimate and is subject to revision.

2019-Q2 2019-Q3 2019-Q4 2020-Q1 2020-Q2 2020-Q3 2020-Q4 2021-Q1 2021-Q2

Volume 44,000 48,690 49,330 48,220 32,640 41,700 46,250 47,990 47,220

Value (£bn) 5.57 6.29 6.46 6.38 4.35 5.86 6.50 7.17 7.34

2019-Q2 2019-Q3 2019-Q4 2020-Q1 2020-Q2 2020-Q3 2020-Q4 2021-Q1 2021-Q2

Homeowner House purchase 8,190 9,780 9,920 8,130 4,430 8,080 11,580 13,050 13,220

Homeowner remortgage 11,160 11,850 11,300 12,030 9,170 9,360 8,690 9,100 8,860

Buy-to-let (purchase & remortgage)

14,060 14,470 14,880 15,890 11,350 13,170 13,640 15,410 14,970

Lifetime Mortgage 9,990 11,900 12,510 11,580 7,430 10,530 11,740 9,740 9,150*

*Lifetime mortgage figure for the most recent quarter (Q2 2021) is an estimate and is subject to revision.

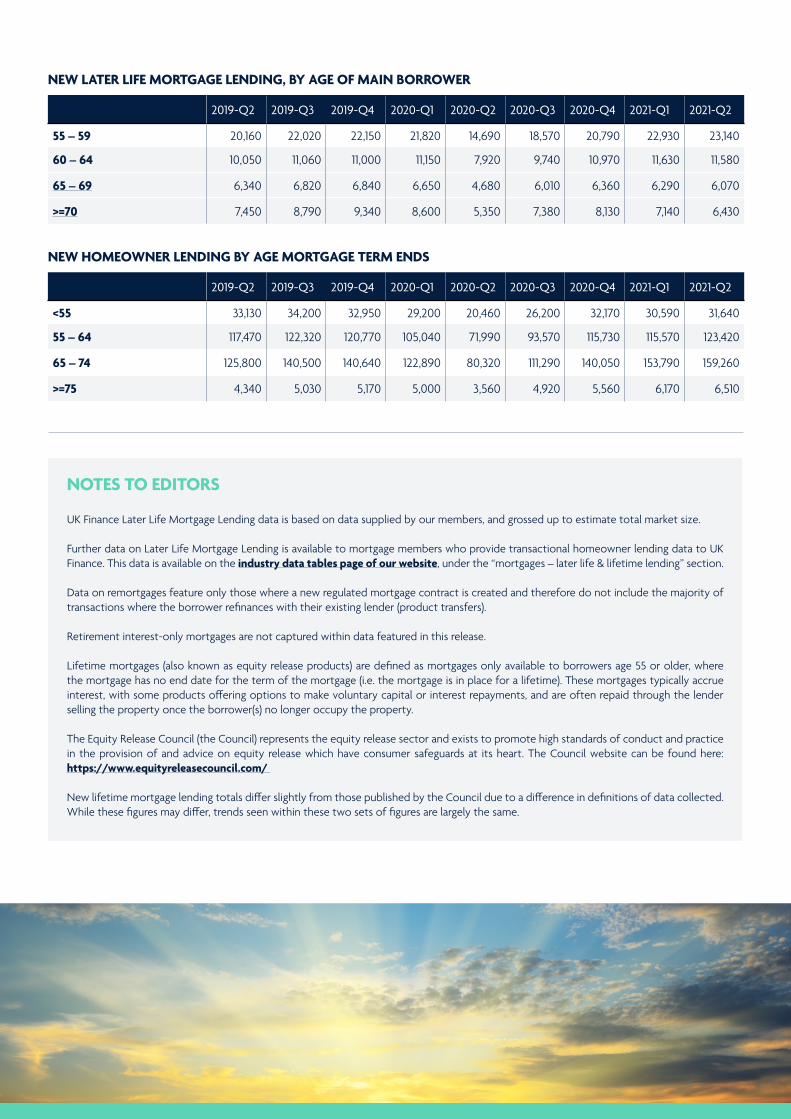

NEW LATER LIFE MORTGAGE LENDING, BY PRODUCT

NEW LATER LIFE MORTGAGE LENDING

2019-Q2 2019-Q3 2019-Q4 2020-Q1 2020-Q2 2020-Q3 2020-Q4 2021-Q1 2021-Q2

55 – 59 20,160 22,020 22,150 21,820 14,690 18,570 20,790 22,930 23,140

60 – 64 10,050 11,060 11,000 11,150 7,920 9,740 10,970 11,630 11,580

65 – 69 6,340 6,820 6,840 6,650 4,680 6,010 6,360 6,290 6,070

>=70 7,450 8,790 9,340 8,600 5,350 7,380 8,130 7,140 6,430

2019-Q2 2019-Q3 2019-Q4 2020-Q1 2020-Q2 2020-Q3 2020-Q4 2021-Q1 2021-Q2

<55 33,130 34,200 32,950 29,200 20,460 26,200 32,170 30,590 31,640

55 – 64 117,470 122,320 120,770 105,040 71,990 93,570 115,730 115,570 123,420

65 – 74 125,800 140,500 140,640 122,890 80,320 111,290 140,050 153,790 159,260

>=75 4,340 5,030 5,170 5,000 3,560 4,920 5,560 6,170 6,510

NEW HOMEOWNER LENDING BY AGE MORTGAGE TERM ENDS

NEW LATER LIFE MORTGAGE LENDING, BY AGE OF MAIN BORROWER

NOTES TO EDITORS

UK Finance Later Life Mortgage Lending data is based on data supplied by our members, and grossed up to estimate total market size.

Further data on Later Life Mortgage Lending is available to mortgage members who provide transactional homeowner lending data to UK Finance. This data is available on the industry data tables page of our website, under the “mortgages – later life & lifetime lending” section.

Data on remortgages feature only those where a new regulated mortgage contract is created and therefore do not include the majority of transactions where the borrower refinances with their existing lender (product transfers).

Retirement interest-only mortgages are not captured within data featured in this release.

Lifetime mortgages (also known as equity release products) are defined as mortgages only available to borrowers age 55 or older, where the mortgage has no end date for the term of the mortgage (i.e. the mortgage is in place for a lifetime). These mortgages typically accrue interest, with some products offering options to make voluntary capital or interest repayments, and are often repaid through the lender selling the property once the borrower(s) no longer occupy the property.

The Equity Release Council (the Council) represents the equity release sector and exists to promote high standards of conduct and practice in the provision of and advice on equity release which have consumer safeguards at its heart. The Council website can be found here: https://www.equityreleasecouncil.com/

New lifetime mortgage lending totals differ slightly from those published by the Council due to a difference in definitions of data collected. While these figures may differ, trends seen within these two sets of figures are largely the same.