LAS PALOMAS LIMITED PARTNERSHIP . (A Limited Partnership… · LAS PALOMAS LIMITED PARTNERSHIP . (A...

17

LAS PALOMAS LIMITED PARTNERSHIP . (A Limited Partnership) Financial Statements December 31,2011 and 2010

Transcript of LAS PALOMAS LIMITED PARTNERSHIP . (A Limited Partnership… · LAS PALOMAS LIMITED PARTNERSHIP . (A...

LAS PALOMAS LIMITED PARTNERSHIP . (A Limited Partnership)

Financial Statements December 31,2011 and 2010

SALMIN, CELONA, WEHRLE & FLAHERTY, LLP CERTIFIED PUBLIC ACCOUNTANTS

1170 CHILI AVENUE • ROCHESTER, NY 14624-3033 585 / 279 / 0120 • FAX 585 / 279 / 0166 • EMAil [email protected]

fNDEPENDENT AUDITOR'S REPORT

To the Partners Las Palomas Limited Partnership

We have audited the accompanying balance sheet of Las Palomas Limited Partnership as of December 31, 2011 and 2010, and the related statements of operations and partners' capital (deficit) and cash flows for the years then ended. These financial statements are the responsibility of the Partnership's management. Our responsibility is to express an opinion on these financial statements based on our audits.

We conducted our audits in accordance with auditing standards generally accepted in the United States of America. Those standards require that we plan and perform the audits to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. An audit also includes assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. We believe that our audits provide a reasonable basis for our opinion.

In our opinion, the financial statements referred to above present fairly, in all material respects, the financial position of Las Palomas Limited Partnership as of December 31, 2011 and 2010, and the results of its operations and its cash flows for the years then ended in conformity with accounting principles generally accepted in the United States of America.

Salmin, Celona, Wehrle & Flaherty, LLP Rochester, New York

February 28,2012

The ~. Never Underestimate The Value.® Members of the American Institute of Certified Public Accountants

POl-ARIS ./ ,

LAS PALOMAS LIMITED PARTNERSHIP (A Limited Partnership)

BALANCE SHEET DECEMBER 31, 2011 AND 2010

ASSETS 2011 2010

Current assets:

Cash - operating $ 56,053 $ 20,635

Accounts receivable - tenants 13,262 21,038 Accounts receivable - rent subsidy 506 7,291

Accounts receivable - other ° 2,497 Prepaid expenses 20,615 18,429

Capital contribution receivable 162,071 162,071

Total current assets 252,507 231,961

Cash - tax and insurance escrows 91,347 90,765

Cash - replacement reserve 362,614 353,238

Rental property and equipment, net of accumulated depreciation 16,158,794 16,749,415

Other assets, net 303,490 315,436

$ 17,168,752 $ 17,740,815

LIABILITIES AND PARTNERS' CAPITAL (DEFICIT)

Current liabil ities: Current portion of long-term debt $ 184,340 $ 175,366

Tenant security deposits 10,833 15,878

Accounts payable - operations 63,813 68,076

Due to managing agent 50,197 50,197

Accrued management fee payable 438 a Accrued expenses 9,970 9,670

Accrued property taxes 22,999 22,184

Prepaid rent 12,773 12,397

Investor service fee payable 57,468 48,513

Total current liabilities 412,831 402,281

Long-term debt, net of current portion 11,378,490 11,562,830

Operating deficit loans payable 410,416 361,293

Development fee payable 1,887,112 1,887,112

Total partners' capital (deficit) 3,079,903 3,527,299

$ 17,168,752 $ 17,740,815

See accompanying notes to financial statements

LAS PALOMAS LIMITED PARTNERSHIP

(A Limited Partnership) STATEMENT OF OPERATIONS AND PARTNERS' CAPITAL (D EFICIT)

FOR THE YEARS ENDED DECEMBER 31, 2011 AND 2010

2011

Revenue: Gross residential rent potential $ 2,230,107

Less: residential vacancy and allowances (450,086)

Net residential rental income 1,780,021

Laundry income 27,877

Tenant charges 68,886

Other income 20,203

Total revenue 1,896,987

Operating expenses: Administration and management:

Office payroll 135,989

Office expenses 34,646

Management fees 78,499

Advertising 36,835

Legal and accounting 12,883

Bad debts 67,519

Other 28,700

Total administration and management 395,071

Utilities:

Gas 3,288

Electricity 29,301

Water and sewer 111,146

Total utilities 143,735

Repairs and maintenance: Maintenance payroll 124,812

Supplies 56,149

Repairs 110,322

Grounds 11,815

Rubbish removal 31,615

Other 67

Total repairs and maintenance 334,780

Taxes and insurance:

Property taxes 45,998

Insurance 53,904

Payroll taxes and benefits 61,331

Total taxes and insurance 161,233

Total operating expenses 1,034,819

Continued on next page

2010

2,070,140 (230,208)

1,839,932 50,404 42,765

4,355 1,937,456

123,648

37,338 78,630 32,804 18,933 70,524 l3,553

375,430

4,194 25,566

118,395 148,155

130,312 55,020

128,830 24,817

27,629 2,204

368,812

44,368

51,335 52,026

147,729

1,040,126

LAS PALOMAS LIMITED PARTNERSHIP (A Limited Partnership)

STATEMENT OF OPERATIONS AND PARTNERS' CAPITAL (DEFICIT)

FOR THE YEARS ENDED DECEMBER 31, 2011 AND 2010 (Continued)

Operating income 862,168

Other income (expense): Interest income 1,888

Mortgage interest expense (609,063)

Tax credit monitoring fee (11,200)

Other mortgage fees and costs (54,772)

Partnership and asset management fees (8,955)

Amortization (11,946)

Depreciation (615,516)

Net income (loss) (447,396)

Partners' capital (deficit) - beginning of year 3,527,299

Partners' capital (deficit) - end of year $ 3,079,903

See accompanying notes to financial statements

897,330

2,452 (617,568)

(11,200) (55,533)

(8,694)

01,946) (612,475)

(417,634)

3,944,933

$ 3,527,299

LAS PALOMAS LIMITED PARTNERSHIP (A Limited Partnership)

STATEMENT OF CASH FLOWS FOR THE YEARS ENDED DECEMBER 31, 2011 AND 2010

Cash flows from operating activities:

Net income (loss)

Adjustments to net income (loss) to reconcile to net cash

provided by (used in) operating activities:

Depreciation and amortization

Decrease (increase) in accounts receivable - tenants

Decrease (increase) in accounts receivable - rent subsidy

Decrease (increase) in accounts receivable - other

Decrease (increase) in prepaid expense

Increase (decrease) in tenants security deposits

Increase (decrease) in accounts payable

Increase (decrease) in accrued management fee payable

Increase ( decrease) in accrued expenses

Increase (decrease) in accrued property taxes

Increase (decrease) in prepaid rent Increase (decrease) in accrued investor service fee payable

Total adjustments

Net cash provided by (used in) operating activities

Cash flows from investing activities:

Deposits to tax and insurance escrows

Withdrawals from tax and insurance escrows

Deposits to replacement reserve

Withdrawals from replacement reserve

Purchase of rental propelty and equipment

Net cash provided by (used in) investing activities

Cash flows from financing activities:

Principal repayments on long-term debt

Increase in operating deficit loans

Increase (decrease) in due to managing agent

Net cash provided by (used in) financing activities

Continued on next page

$

2011

(447,396)

627,462

7,776

6,785

2,497

(2,186)

(5,045)

(4,263)

438

300

815

376 8,955

643,910

196,514

(151,200)

150,618

(85,885)

76,509

(24,895)

(34,853)

(175,366)

49,123

o

(126,243)

$

2010

(417,634)

624,421

(15,484)

(4,669)

(2,497)

245

(19,016)

(43,931)

0

1,790 1,051

(12,583)

8,694

538,021

120,387

(156,192)

165,033 (86,446)

122,275

(39,915)

4,755

(166,862)

° 40,197

(126,665)

LAS PALOMAS LIMITED PARTNERSHIP (A Limited Partnership)

STATEMENT OF CASH FLOWS FOR THE YEARS ENDED DECEMBER 31,20 II AND 2010

(Continued)

Increase (decrease) in cash - operating 35,418

Cash - beginning of year 20,635

Cash - end of year $ 56,053

Supplemental disclosure of cash flow information:

Cash paid during the year for interest $ 609,063

See accompanying notes to financial statements

(1,523)

22,158

$ 20,635

$ 617,568

LAS PALOMAS LIMITED PARTNERSHIP (A LIMITED PARTNERSHIP)

NOTES TO FINANCIAL STATEMENTS DECEMBER 31,2011 AND 2010

1. BACKGROUND AND ORGANIZATION

The following represents certain background and organization information:

Project name:

Location of proj ect:

Number and type of residential units:

Commercial space (if any):

Type of entity:

State of formation:

Formation date:

Scheduled termination of existence:

Acquisition date

Rehabilitation completion

Significant revenue source(s):

Significant operating and regulatory agreements/restrictions:

Target occupancy:

Restricted use periods:

Las Palomas Apartments

Santa Fe, New Mexico

279 unit low income apartments

None

Limited partnership

New Mexico

March 1, 2005

1213112065 unless earlier dissolved/terminated

March 10,2005

July 31, 2006.

Tenant rental payments and rental assistance payments received from government agencies on behalf of certain tenants.

New Mexico Mortgage Finance Authority (NMMF A) 542(c) Multifamily Insurance Program Regulatory Agreement

Low income housing tax credit land use restriction agreement (LURA)

There are 11 units (The HOME units) which are restricted to tenants whose income, at initial occupancy, is 50% or less of the area median gross income (AMGI). All of the other units to be rented to tenants whose income, at initial occupancy, is 60% or less of the area median gross income (AMGI).

NMMF A regulatory agreement through March 1, 2040.

LURA regulatory agreement through 2036.

LAS PALOMAS LIMITED PARTNERSHIP (A LIMITED PARTNERSHIP)

NOTES TO FINANCIAL STATEMENTS DECEMBER3l, 2011 AND 2010

2. SIGNIFICANT ACCOUNTING POLICIES

Restatement of Prior Period - The accompanying financial statements for 2010 have been restated to correct an error made in recording accrued interest on the development fee payable. The First Amendment to Amended and Restated Agreement of Limited Partnership states that the unpaid developer fee does not accrued interest. The effect of the restatement was to increase partner's capital by $283,068 as of January 1, 2010 and to decrease the net loss for 2010 by $94,356.

Accounting Method - The Partnership has adopted the accrual method of accounting for both financial and income tax reporting purposes. The financial statements are prepared in accordance with accounting principles generally accepted in the United States of America.

Use of Estimates - The preparation of financial statements in conformity with accounting principles generally accepted in the United States of America requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenue and expenses during the reporting period. Actual results could differ from those estimates. The most significant estimate included in the preparation of the financial statements is related to asset lives.

Rental Property and Equipment - Rental property and equipment are stated at cost and include $639,606 of interest that was capitalized through 2006. Depreciation is calculated using straight-line and accelerated methods over the estimated useful lives of the related assets as follows:

Building improvements and components Land improvements Equipment, furniture and fixtures

30 years 15 years 7 years

For income tax reporting, depreciation is calculated using methods and estimated useful lives as prescribed by federal income tax regulations.

Improvements are capitalized, while expenditures for maintenance and repairs are charged to expense as incurred. Upon disposal of depreciable property, the appropriate property accounts are reduced by the related costs and accumulated depreciation. The resulting gains and losses are reflected in the statement of operations.

The Partnership reviews its investment in real estate for impairment whenever events or changes in circumstances indicate that the carrying value of such property may not be recoverable. Recoverability is measured by a comparison of the carrying amount of the real estate to the future net undiscounted cash flow expected to be generated by the rental property including the low income housing tax credits and any estimated proceeds from the eventual disposition of the real estate. Tfthe real estate is considered to be impaired, the impairment to be recognized is measured at the amount by which the carrying amount of the real estate exceeds the fair value of such property. There were no impairment losses recognized in 201101' 2010.

Other Assets - Other assets include deferred mortgage financing costs aggregating $359,745 which are being amortized using the straight-line method over the 35 year terms of the permanent loans. Other assets also include ta.x credit fees of $25,014 which are amortized using the straight-line method over a fifteen year period.

Cash - The Partnership considers all cash on hand, cash in banks and short term investments with an original maturity of three months or less to be cash for financial reporting purposes. For the purposes of reporting cash flows in the Statement of Cash Flows, cash includes only cash - operating and cashconstruction.

LAS PALOMAS LIMITED PARTNERSHIP (A LIMITED PARTNERSHIP)

NOTES TO FINANCIAL STATEMENTS DECEMBER 31, 2011 AND 2010

2. SIGNIFICANT ACCOUNTING POLICIES, Continued

Accounts Receivable - The Partnership records accounts receivable in the balance sheet at the amount invoiced to the tenant or government agency adjusted for an allowance for doubtful accounts. The allowance for doubtful accounts is periodically estimated by management and includes all tenant accounts for which it appears there will be a problem with collection. Individual tenant receivables are deemed uncollectible and written off once reasonable collection efforts have been made or when the respective tenant is deceased. The Partnership does not have a material concentration of credit risk, with respect to accounts receivable, due to the generally short payment terms (i.e. rent is due at the beginning of the service month). In addition, the allowance for doubtful accounts is not significant.

Income Taxes - The Partnership does not pay federal or state income taxes on its income. Instead, the Partnership's income, deductions and other income tax attributes are reported to each partner, based on their respective ownership, and included in their respective income tax returns. The Partnership follows the provisions of Financial Accounting Standards Board Accounting Standards Codification pertaining to accounting for uncertainty in income taxes. Federal and state tax authorities generally have the right to examine and audit the previous three years of tax returns filed. Any interest and penalties assessed to the Partnership are recorded in operating expenses ($0 for the years ended December 31, 2011 and 2010). Management is not aware of any uncertain tax positions requiring measurement or disclosure in these financial statements.

Rental Income - Rental income is recognized as rentals become due. Rental payments received in advance are deferred until earned. All leases between the Partnership and the tenants of the property are typically for one year or less and classified as operating leases.

Advertising - Advertising costs are expensed as incurred.

Account Reclassification - In addition to the restatement noted above, certain account balances at December 31,2010, were reclassified to conform to account classifications used by the Pminership at December 31,2011. The reclassifications had no effect on reported results of operations or financial position.

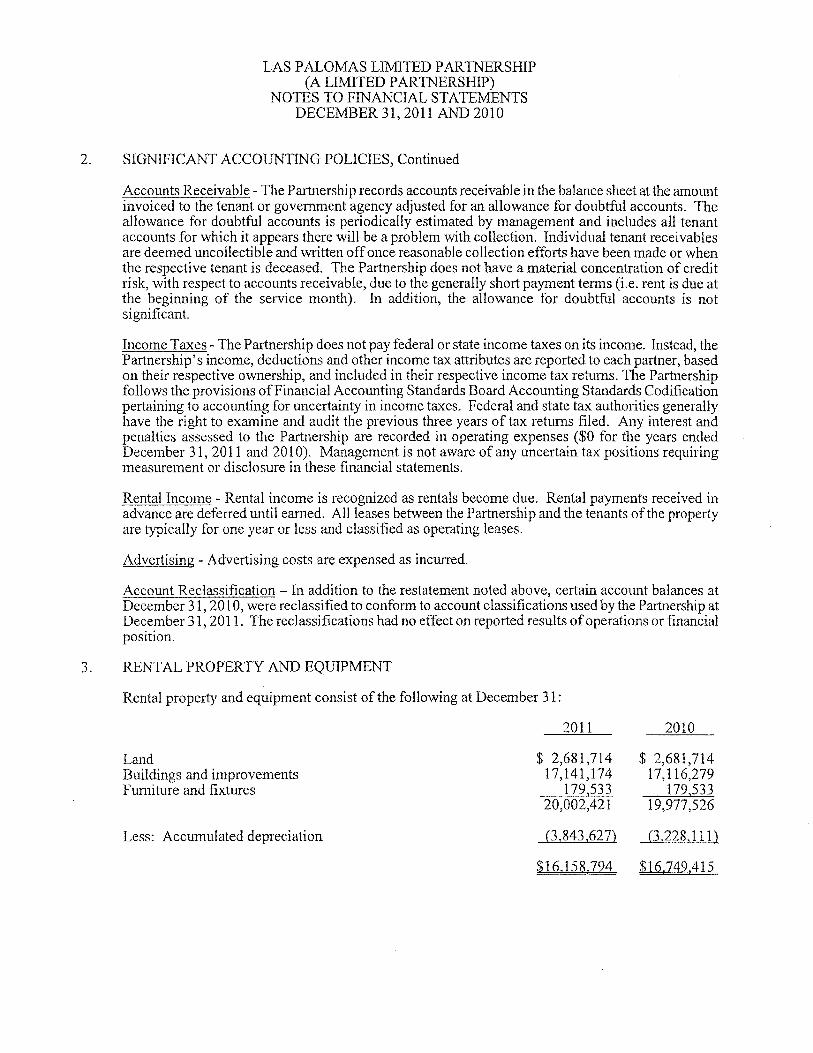

3. RENTAL PROPERTY AND EQUIPMENT

Rental property and equipment consist of the following at December 31:

Land Buildings and improvements Furniture and fixtures

Less: Accumulated depreciation

2011

$ 2,681,714 17,141,174

179,533 20,002,421

(3,843,627)

$16,158.794

2010

$ 2,681,714 17,116,279

179,533 19,977,526

(3,228,111)

$16.749.415

LAS PALOMAS LIMITED PARTNERSHIP (A LIMITED PARlNERSHIP)

NOTES TO FINANCIAL STATEMENTS DECEMBER 31,2011 AND 2010

4. MORTGAGES PAYABLE

5.

Mortgages payable consist of the following at December 31 :

New Mexico Mortgage Finance Authority (NMMF A) mortgage with monthly payments of $63,173, including principal and interest at 5.49% per annum, through March 1, 2040. The mortgage is insured by the Federal Housing Administration (FHA) and collateralized by a first mortgage lien on the

2011

Partnership property. $ 10,883,174

New Mexico Mortgage Finance Authority (NMMF A) $800,000 HOME loan with monthly payments of$2, 197, including principal and interest at 1 % per annum, through October 10,2041. The loan is secured by a second mortgage on the Partnership property. 679,656

11,562,830 Less: Current portion 184,340

2010

$ 11,039,084

699,112

11,738,196 175,366

$ 11,378.490 $ 11.562,830

The aggregate annual principal payments on the mortgages for the years subsequent to 2011 are as follows:

2012 $ 184,340 2013 193,809 2014 203,803 2015 214,351 2016 225,482 Thereafter 10,541,045

$ 11,562,830

PARTNERS' CAPITAL (DEFICIT) ACCOUNT

The following represents certain ownership information:

General partner:

Investment limited partners:

Special limited partner:

Name

Las Palomas Management, LLC

PNC Multifamily Capital Institutional Fund XXIX Limited Partnership

Columbia Housing SLP Corporation

Percent interest

.01%

99.99%

.00%

LAS PALOMAS LIMITED PAR1NERSHIP (A LIMITED PAR1NERSHIP)

NOTES TO FINANCIAL STATEMENTS DECEMBER 31,2011 AND 2010

5. PAR1NERS' CAPITAL (DEFICIT) ACCOUNT, Continued

The limited partners' capita~ contribution is estimated to be $6,066,992, calculated as follows:

Original estimate of contributions per partnership agreement Increase to contributions due to upward basis adjusters Additional capital contribution per first amendment

to partnership agreement (Special Installment) Decrease due to 2005 timing adjuster Decrease due to 2006 timing adjuster Decrease due to 2007 timing adjuster (estimated) Decrease due to 2006-2015 timing adjusters Special adjustment due to mold remediation Total estimated limited partner capital contribution

$ 4,904,410 1,298,012

250,000 (157,000) (356,255)

(5,146) (33,191) 166,162

$ 6,066,992

The above estimate is based upon the partnership realizing its revised tax credit allocation of $678,370 per year. As of December 31, 2011, $5,904,921 has been funded. The partnership agreement provides for adjustment to the capital contribution and repayment to the limited partners for any subsequent tax credit adjustments or recapture.

In general, profits and losses from operations are allocated 99.99% to the limited partners and .01 % to the general partner.

The following details the activity in the partners' capital (detlcit) accounts for 2011 and 2010:

Balance - January 1,2010-previously reported

Correction of prior period error in reporting interest on deferred developer fee - see note 2

Balance - January 1,2010 - restated Net loss - 2010 - restated

Balance - December 31, 2010 Net loss - 2011

$

General Partners

(241)

28

(213) (42)

(255) (45)

(300) Balance - December 31, 2011 $ =======

Limited Partners

$ 3,662,106

283,040

3,945,146 (417,592)

3,527,554 (447,351)

$ 3,080,203

Total

$ 3,661,865

283,068

3,944,933 (417,634)

3,527,299 (447,396)

$ 3,079,903

LAS PALOMAS LIMITED PARTNERSHIP (A Limited Partnership)

NOTES TO FINANCIAL STATEMENTS DECEMBER 31,2011 AND 2010

5. PARTNERS' CAPITAL (DEFICIT) ACCOUNT, Continued

Subject to lender and regulatory approval, cash flow for each fiscal year or portion thereof of the Partnership shall be applied as follows:

Prior to the full payment of Special Adjustment amount (as defined in the first amendment to the limited partnership agreement):

First, to the payment of the Investor Services Fee for such year; Second, to the payment of the Special Installment to the investment limited partner; Third, pro rate to the payment of any outstanding Special Adjustment amount to the investor

limited partner and the Deferred Development Fee to the developer.

After the full payment of Special Adjustment amount:

First, to the payment of the Investor Services Fee for such year; Second, to the payment of any loans due to the Investment Limited Partner; Third, to the payment of the Deferred Development Fee; Fourth, to the payment of any Operating Deficit Loans; Fifth, to the payment of any unpaid Adjustment Amounts; Sixth, to the payment of the Partnership Management Fee; Seventh, to the payment of the Incentive Management Fee; Eighth, the balance thereof, if any, shall be distributed annually 90% to the general partner

and 10% to the Investment Limited Partner.

Gains, losses and cash f10w from a sale or refinancing shall be applied according to the terms of the partnership agreement.

6. RELATED PARTY TRANSACTIONS AND BALANCES

Related party transactions were as follows for the years ended December 31 :

Management fee of 4.25% of gross rental income to an affiliate of the general partner.

Investor Services Fee ( cumulative) to the investment limited partner equal to $7,500 (2006 base year) per year payable out of available cash flow. The fee will be adjusted annually to reflect a 3% increase.

Annual partnership management fee (non cumulative) to the general partner equal to $7,500 (2006 base year) per year, payable out of available cash flow. The fee will be adjusted annually to reflect a 3% increase.

Incentive Management Fee (non cumulative) to the general partner equal to 10% of effective gross income payable out of available cash flow.

2011

$ 78,499

$ 8,955

$ 0

$ 0

2010

$ 78,630

$ 8,694

$ 0

$ 0

LAS PALOMAS LIMITED PARTNERSHIP (A Limited Partnership)

NOTES TO FINANCIAL STATEMENTS DECEMBER 31, 2011 AND 2010

6. RELATED PARTY TRANSACTIONS AND BALANCES, Continued

7.

For administrative and economic efficiency purposes, the management company maintains a centralized payroll system and employee benefit programs for all employees of the entities that it manages. The actual payroll and benefit charges ofthe Partnership's employees are charged directly to the Partnership.

Amounts due to related parties consist of the following at December 31 :

2011 2010

Management fee payable (receivable) $ 438 $ (2,497)

Loan due to managing agent $ 50,197 $ 50,197

Accounts payable due to managing agent $ 0 $ 46,137

Investor services fee payable $ 57,468 $ 48,513

Partnership management fee payable $ 0 $ 0

Incentive management fee payable $ 0 $ ° Operating deficit loans (non-interest bearing) $ 410,416 $ 361,293

Development fee payable $1,887,112 $1,887,112

Investment limited partner capital contribution receivable $ 162,071 $ 162,071

RESTRICTED RESERVES

In connection with the project's financing agreements with NMMF A, the Partnership was required to establish the following reserve accounts:

Tax and Insurance Escrow Fund - The Partnership makes monthly deposits into the tax insurance escrow fund to be used for real estate taxes and mortgage insurance. The fund is maintained by NMMFA.

Replacement Reserve - This fund is used to finance the cost of repairs or replacement of major capital improvements. The Partnership must obtain NMMF A approval prior to disbursing any funds. The Partnership is required to make monthly deposits of $7,000 to an account that is maintained by NMMFA.

8. FEDERAL LOW INCOME HOUSING TAX CREDIT

Each building ofthe project has qualified and been allocated low-income housing tax credits pursuant to Internal Revenue Code Section 42, which regulates the use of the project as to occupant eligibility and unit gross rent, among other requirements. Each building of the project must meet the provisions ofthese regulations during each of fifteen consecutive years in order to continue to qualify to receive the tax credits. Failure to comply with occupant eligibility and/or unit gross rent, or to correct noncompliance within a specified time period could result in recapture of previously taken low income housing tax credits plus interest. Such potential noncompliance may require an adjustment to the contributed capital by the limited partners.

LAS PALOMAS LIMITED PARTNERSHIP (A Limited Partnership)

NOTES TO FINANCIAL STATEMENTS DECEMBER 31,2011 AND 2010

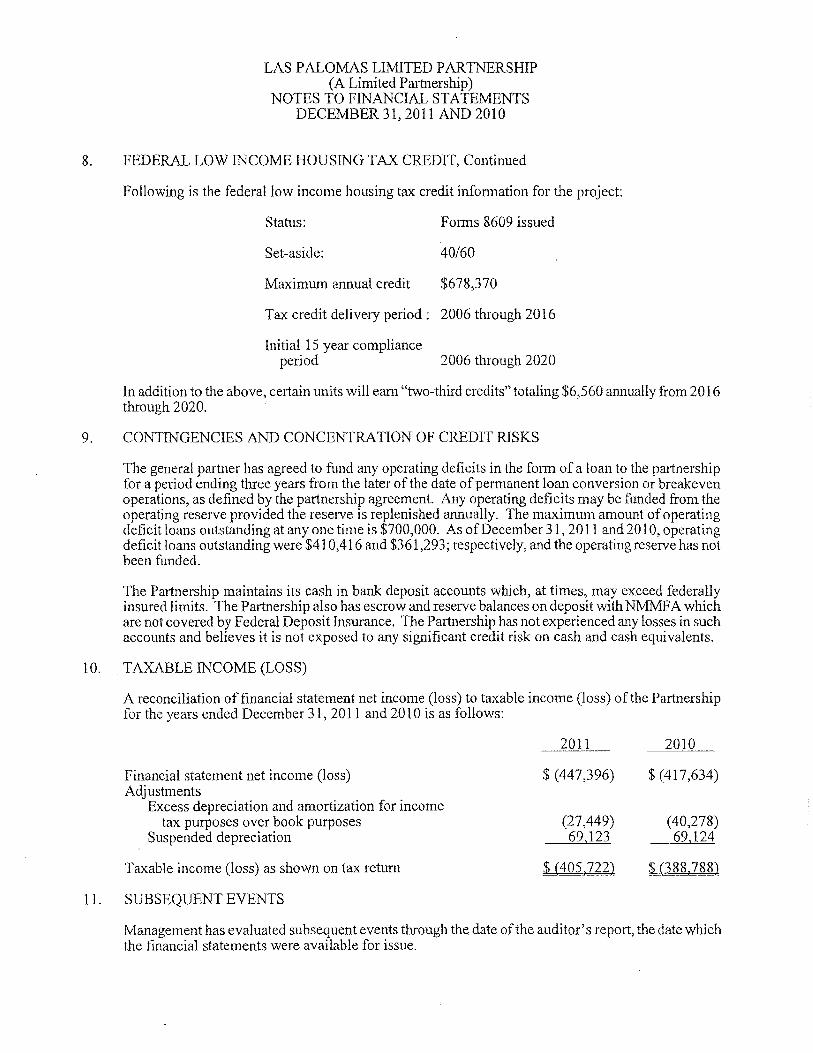

8. FEDERAL LOW INCOME HOUSING TAX CREDIT, Continued

Following is the federal low income housing tax credit information for the project:

Status:

Set-aside:

Maximum annual credit

Forms 8609 issued

40/60

$678,370

Tax credit delivery period; 2006 through 2016

Initial 15 year compliance period 2006 through 2020

In addition to the above, celiain units will earn "two-third credits" totaling $6,560 annually from 20 16 through 2020.

9. CONTINGENCIES AND CONCENTRATION OF CREDIT RISKS

The general partner has agreed to fund any operating deficits in the forn1 of a loan to the partnership for a period ending three years from the later of the date of permanent loan conversion or breakeven operations, as defined by the partnership agreement. Any operating deficits may be funded from the operating reserve provided the reserve is replenished annually. The maximum amount of operating deficit loans outstanding at anyone time is $700,000. As of December 31,2011 and 2010, operating deficit loans outstanding were $410,416 and $361,293; respectively, and the operating reserve has not been funded.

The Partnership maintains its cash in bank deposit accounts which, at times, may exceed federally insured limits. The Partnership also has escrow and reserve balances on deposit with NMMF A which are not covered by Federal Deposit Insurance. The Partnership has not experienced any losses in such accounts and believes it is not exposed to any significant credit risk on cash and cash equivalents.

10. TAXABLE INCOME (LOSS)

A reconciliation of financial statement net income (loss) to taxable income (loss) of the Partnership for the years ended December 31,2011 and 2010 is as follows:

Financial statement net income (loss) Adjustments

Excess depreciation and amortization for income tax purposes over book purposes

Suspended depreciation

Taxable income (loss) as shown on tax return

11. SUBSEQUENT EVENTS

2011

$ (447,396)

(27,449) 69,123

$ (405,722)

2010

$ (417,634)

(40,278) 69,124

$ (288,788)

Management has evaluated subsequent events through the date of the auditor's report, the date which the financial statements were available for issue.

LAS PALOMAS LIMITED PARTNERSHIP (A Limited Partnership)

NOTES TO FINANCIAL STATEMENTS DECEMBER 31, 2011 AND 2010

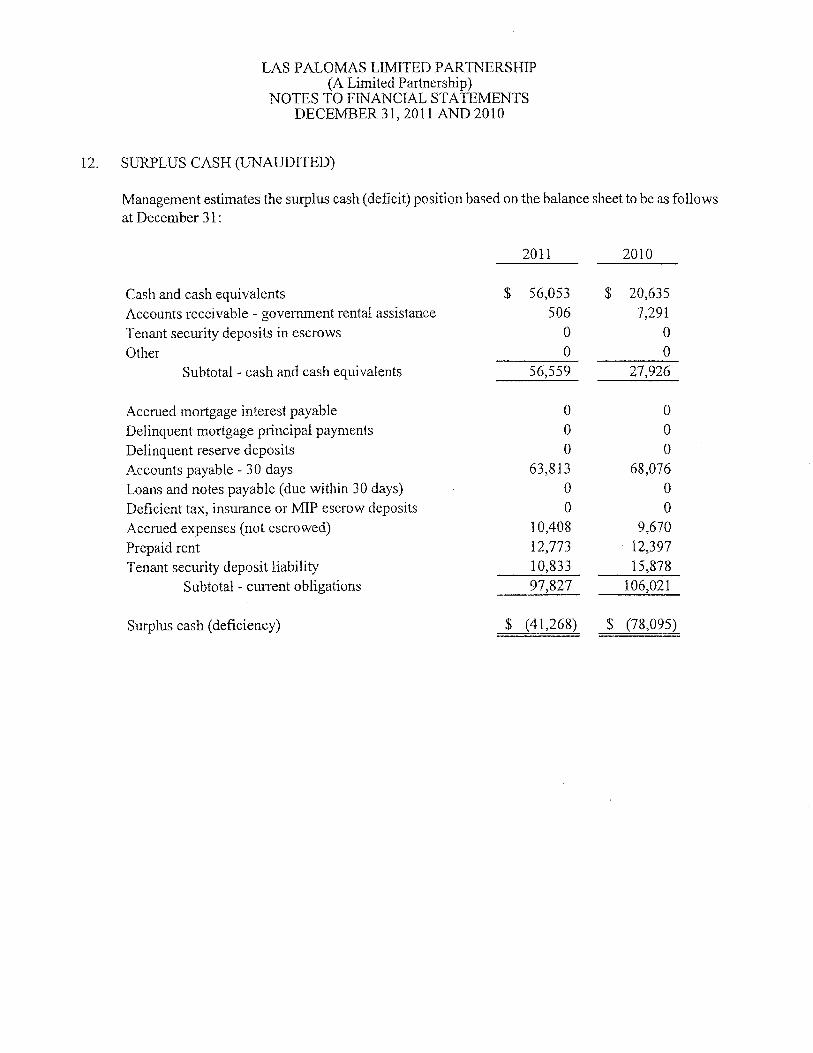

12. SURPLUS CASH (UNAUDITED)

Management estimates the surplus cash (deficit) position based on the balance sheet to be as follows at December 31:

2011 2010

Cash and cash equivalents $ 56,053 $ 20,635 Accounts receivable - government rental assistance 506 7,291 Tenant security deposits in escrows ° ° Other 0 ° Subtotal - cash and cash equivalents 56,559 27,926

Accrued mortgage interest payable ° ° Delinquent mortgage principal payments 0 0

Delinq uent reserve deposits ° ° Accounts payable - 30 days 63,813 68,076

Loans and notes payable (due within 30 days) ° 0

Deficient tax, insurance or MIP escrow deposits 0 0

Accrued expenses (not escrowed) 10,408 9,670

Prepaid rent 12,773 12,397

Tenant security deposit liability 10,833 15,878 Subtotal - current obligations 97,827 106,021

Surplus cash (deficiency) $ (41,268) $ (78,095)

Las Palomas Disclosure Report Angie Pizzolato to: [email protected] 05/09/2012 10:42 AM

"Pamela Monroe ([email protected])" Cc: , "Williamson, Asya ([email protected]}", "Foster,

David", Brenda Paradis

From: Angie Pizzolato <[email protected]>

To: "[email protected]" <[email protected]>

Cc: "Pamela Monroe ([email protected])" <[email protected]>, "Williamson, Asya ([email protected])" <[email protected]>, "Foster, David"

Hi Renea,

Please find attached both the 2011 audited financials and the Owner certification letter you requested for Las Palomas.

Should you need any additional information for the Disclosure Report, please let me know as I am happy to be of assistance.

Regards,

Angie

• THE SILVER STREET GROUp, LLC CD

Angie Pizzolato Financial Analyst THE SILVER STREET GROUP, LLC 33 Silver Street - Suite 300 Portland, Maine 04101 207-780-9800, ext. #3 (ph) 207-274-0058 (cell) 207-221-2040 (fx) [email protected] www.silverstreetcorp.com

~'~ :/~,

Las Palomas Continuing Disclosure Cert 5·8·2012.pdf