LARSEN & TOUBRO LIMITED - AceAnalyser Meet/100510_20100517.pdfLARSEN & TOUBRO LIMITED 17th May 2010...

36

LARSEN & TOUBRO LIMITED LARSEN & TOUBRO LIMITED 17 th May 2010

Transcript of LARSEN & TOUBRO LIMITED - AceAnalyser Meet/100510_20100517.pdfLARSEN & TOUBRO LIMITED 17th May 2010...

LARSEN & TOUBRO LIMITEDLARSEN & TOUBRO LIMITED

17th May 2010

DisclaimerThis presentation contains certain forward looking statements concerning L&T’s

future business prospects and business profitability, which are subject to a

number of risks and uncertainties and the actual results could materially differ

f h h f d l k h k dfrom those in such forward looking statements. The risks and uncertainties

relating to these statements include, but not limited to, risks and

uncertainties, regarding fluctuations in earnings, our ability to manage

growth competition (both domestic and international) economic growth in Indiagrowth, competition (both domestic and international), economic growth in India

and the target countries for exports, ability to attract and retain highly skilled

professionals, time and cost over runs on contracts, our ability to manage our

international operations, government policies and actions with respect tointernational operations, government policies and actions with respect to

investments, fiscal deficits, regulations, etc., interest and other fiscal costs

generally prevailing in the economy. The company does not undertake to make

any announcement in case any of these forward looking statements become

materially incorrect in future or update any forward looking statements made

from time to time by or on behalf of the company.

17th May 2010 2

Presentation Outline

L&T Parent Performance

Segmental Performance

Group Performance

Sectoral Opportunities

& Outlook

17th May 2010 3

Presentation Outline

L&T Parent Performance

Segmental Performance

Group Performance

Sectoral Opportunities &

Outlook

17th May 2010 4

Performance HighlightsAll figures in Rs. Billion

Key Parameters Q4 FY10 Q4 FY09 FY10 FY09

Order Inflow 238.43 125.17 90% 695.72 516.21 35%

Change Change

All figures in Rs. Billion

Order Book - 31st March 1,002.39 703.19 43%

N t S l l RMC 133 75 104 69 28% 366 75 330 41 11%Net Sales excl. RMC 133.75 104.69 28% 366.75 330.41 11%

Company level EBITDA Margins 15.1% 14.0% 1.1% 13.0% 11.6% 1.4%

PAT before Exc. & Extraord. Items 13.42 11.42 17% 31.85 27.09 18%

PAT after Exc. & Extraord. Items 14.38 9.99 44% 43.76 34.82 26%

Stellar Allround

5

Performance

Sustaining Growth

516

696

Order Inflow

on 336

367

Net Sales

on

224306

420

Rs.

Billi

o

147 176249

Rs.

Billi

o

FY 06 FY 07 FY 08 FY 09 FY 10 FY 06 FY 07 FY 08 FY 09 FY 10

O d B k R i PAT

703

1002

Order Book

n 21 027.1

31.9

Recurring PAT

n

249369

527

Rs.

Bil

lio

8.613.9

21.0R

s. B

illi

o

17th May 2010 6FY 06 FY 07 FY 08 FY 09 FY 10 FY 06 FY 07 FY 08 FY 09 FY 10

Order Inflow & Order Book

695.72

Order Inflow

35%1002.39

Order Book

43%

516.21 703.19

43%

90%

125.17

238.43 90%

Q4 FY09 Q4 FY10 FY09 FY10 FY09 FY10

717th May 2010 7All figures in Rs. Billion

Order Inflow & Order Book – FY10

Sectoral Break-up

33%

27%

30%

33%

15%

20%

16%

13%

6%

7%

Order Book: Rs 1002 39 Bn

Order Inflow: Rs. 695.72 Bn

33% 30% 15% 16% 6%

Infrastructure Power Hydrocarbons Process Others

Rs. 1002.39 Bn

InfrastructureRoads & BridgesPorts & Harbours

PowerGenerationEquipments

HydrocarbonsUpstream Mid &

ProcessMinerals & Metals

OthersShipbuildingDefense &

AirportsRailwaysBuildings & FactoriesUrban Infra

Electrification / Transmission & Distribution

DownstreamPipelinesValves

Bulk Material HandlingFertilizer

AerospaceConstruction & Mining Eqpt.Electrical & Electronic ProductsUrban Infra

WaterElectronic ProductsTechnology Services

17th May 2010 8

Order Inflow & Order Book – FY10

95% 4% 1%Order Inflow

93% 4% 3%

Domestic Middle East OthersG hi l

Order Book

Geographical Break-up

59% 38% 3%Order Inflow

53% 40% 7%Order Book

17th May 2010 9

Customer Profile

Public Private Devl. Projects - L&T

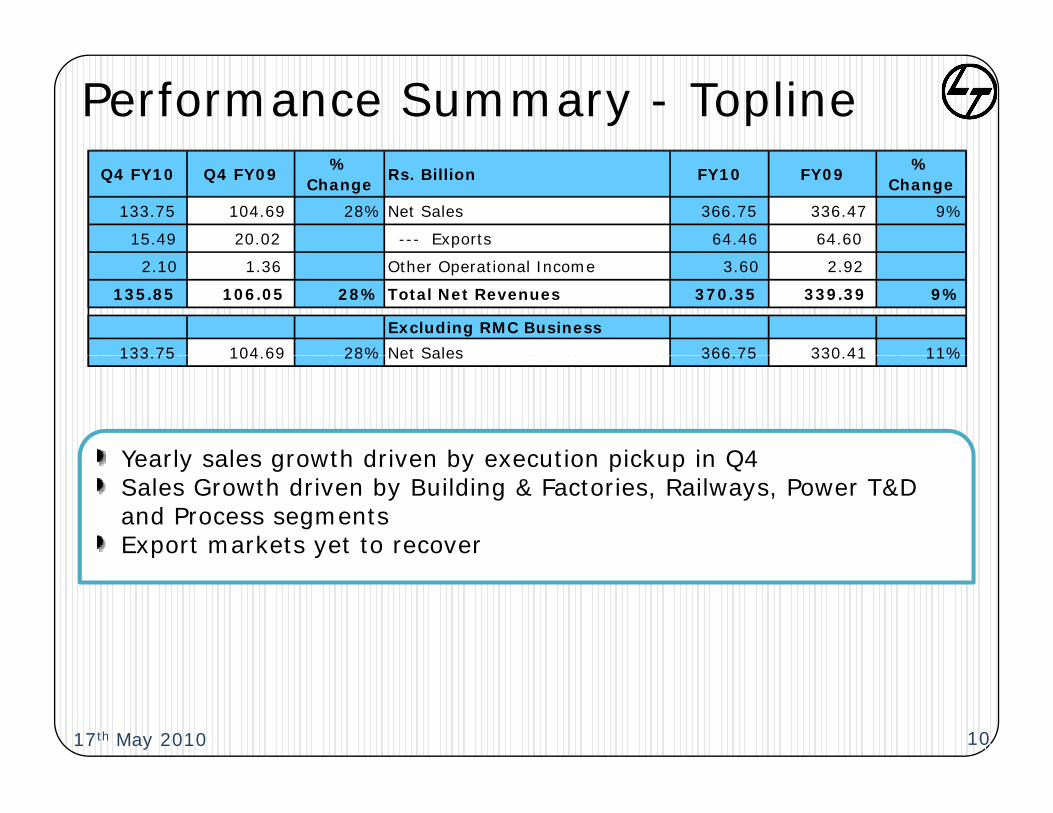

Performance Summary - ToplineQ4 FY10 Q4 FY09

% Change

Rs. Billion FY10 FY09%

Change

133.75 104.69 28% Net Sales 366.75 336.47 9%

15.49 20.02 --- Exports 64.46 64.60

2.10 1.36 Other Operational Income 3.60 2.92

135.85 106.05 28% Total Net Revenues 370.35 339.39 9%

Excluding RMC Business

133 75 104 69 28% Net Sales 366 75 330 41 11%

Yearly sales growth driven by execution pickup in Q4

133.75 104.69 28% Net Sales 366.75 330.41 11%

Yearly sales growth driven by execution pickup in Q4Sales Growth driven by Building & Factories, Railways, Power T&D and Process segmentsExport markets yet to recover

1017th May 2010 10

Performance Summary – Operational Costs

Rs Bn% to Total

Net RevenuesRs Bn

% to Total Net Revenues

Rs Bn% to Total

Net RevenuesRs Bn

% to Total Net Revenues

Q4 FY10 Q4 FY09

Particulars

FY10 FY09

104.08 76.6% 78.66 74.2% Manf., Cons. & Opex (MCO) 284.53 76.8% 262.72 77.4%

6.14 4.5% 4.89 4.6% Staff Costs 23.79 6.4% 19.74 5.8%

5.12 3.8% 7.66 7.2% Sales, adm. & other Exp. 13.87 3.8% 17.70 5.2%

115.34 84.9% 91.21 86.0% Total Operational Costs 322.19 87.0% 300.16 88.4%

Increase in MCO Expenses in Q4 led by Commodity price step-upIncrease in Staff costs on account of increase in manpower, annual rewards salary revisions and incrementsrewards, salary revisions and incrementsReduction in SGA due to effective forex hedging and expense control

1117th May 2010 11

Performance Summary – Profitability

Q4 FY10 Q4 FY09%

Change Rs. Billion FY10 FY09

% Change

20.51 14.84 38% EBITDA 48.16 39.22 23%

15.1% 14.0% EBITDA Margins 13.0% 11.6%

(1.36) (0.47) 189% Interest Expenses (5.05) (4.16) 22%

(1.16) (0.89) 31% Depreciation (4.15) (3.06) 35%

3.30 2.35 Other Income 9.10 7.40

(7.87) (4.41) Provision for Taxes (16.21) (12.31)

13.42 11.42 17% PAT before Exceptional Items 31.85 27.09 18%

0.96 (1.43)Extraordinary & Exceptional Items (Net of tax)

11.91 7.73

14.38 9.99 44% Profit after Tax 43.76 34.82 26%

Yearly Margin improvement driven by favourable commodity prices for the better part of FY10 and operational cost efficienciesIncrease in Interest cost due to higher average borrowingsDepreciation charge in line with increased capexIncrease in other income boosted by dividend from Subs. and profit on Satyam stake sale

1217th May 2010 12

on Satyam stake sale

Performance Summary – Balance Sheet

Networth and Loan funds includes proceeds from QIP and FCCB resp.

Rs. Billion Mar-10 Mar-09Increase / (Decrease)

N t W th 183 12 124 59 58 53 Q pGross D/E ratio: 37% Vs 53%Capex Outlay Rs. 15.6 Bn Segmental Net Working

Net Worth 183.12 124.59 58.53

Loan Funds 68.01 65.56 2.45

Deferred Tax Liabilities (Net)

0.77 0.49 0.28 Segmental Net Working Capital has improved from 11.7% to 7.6% driven by higher

(Net)

Total Sources 251.90 190.64 61.26

Net Fixed Asset 63.66 51.94 11.72

Current Investments 79 65 48 80 30 85 Customer advancesIncrease of Rs. 2.9 Bn in Unallocable Corporate Net Current Assets mainly

Current Investments 79.65 48.80 30.85

Invt./ICDs/Loans & Advances to S&A Cos

76.79 51.08 25.71

Other Investments 5.49 3.52 1.97 Current Assets mainly due to increase in bank balances

Net Current Assets 26.31 35.30 (8.99)

Total Applications 251.90 190.64 61.26

1317th May 2010 13

Cash Flow StatementRs. Billion FY 10 FY 09

Operating Profit 52.44 44.66

Adjustments for Working Capital Changes 17.58 (21.14)

Direct Taxes (Paid) / Refund - Net (15.19) (8.73)

Net Cash from Operations 54.83 14.79

Investments in Fixed Assets (Net) (15.60) (19.80)

(Investment) / Divestment in S&A and JVs (Net) (24.89) (11.71)

(Purchase)/Sale of Long Term & Current Investments (Net) (21.49) (4.91) ( )/ g ( ) ( ) ( )

Loans/Deposits made with S&A / Others (4.95) (12.52)

Interest & Dividend Received from Investments 4.92 4.64

Cash Received on sale of business (CY: PDP; PY: RMC) 1.29 11.21

Net Cash used in Investing Activities (60 72) (33 09) Net Cash used in Investing Activities (60.72) (33.09)

Proceeds from Issue of Share Capital 21.33 0.23

Net Borrowings (Including FCCB issue) 3.64 23.61

Dividends & Interests paid (12.51) (7.43)

h f i i i i iNet Cash from Financing Activities 12.46 16.41

Net (Dec) / Inc in Cash & Cash Equivalents 6.57 (1.89)

Cash & Cash Equivalents - Opening 7.75 9.64

Cash & Cash Equivalents - Closing 14.32 7.75

17th May 2010 14

Presentation Outline

L&T Parent Performance

Segmental Performance

Group Performance

Sectoral Opportunities &

Outlook

17th May 2010 15

Segmental Break-up – FY10

Machinery & Industrial Others

Net Revenues

Engineering &

Construction86.0% (82 5%)

Electrical & Electronics

7 3%

Industrial Products 5.7% (7.0%)

Others 1.0% (3.1%)

(82.5%)7.3% (7.4%)

Machinery & Industrial Products 8 9%

Others 1.0% (1 5%)

EBITDA

Engineering &

Construction82.1% (80.3%)

Electrical & Electronics

8.0% (7.5%)

8.9% (10.7%)

(1.5%)

Figures in the bracket indicate Previous Year’s Composition

16

Figures in the bracket indicate Previous Year s Composition

17th May 2010 16

‘Engineering & Construction’ Segment% %

Q4 FY10 Q4 FY09%

ChangeRs. Billion FY10 FY09

% Change

220.57 112.92 95% Total Order Inflows 638.99 454.18 41%

8.45 25.10 --- Exports 29.31 65.75

Total Order Book 983 86 687 53 43%Total Order Book 983.86 687.53 43%

--- Exports 71.28 100.63

119.69 91.72 30% Total Net Revenues 318.42 279.91 14%

13.19 16.81 --- Exports 56.26 51.36

19.07 14.67 30% EBITDA 43.39 36.31 19%

15.9% 16.0% EBITDA Margins 13.6% 13.0%

Net Segment Assets 62.91 64.62 -3%

Robust Growth in Order Inflow – across all sectors led by PowerInternational Business still sluggishImprovement in Execution environment in Q4Improvement in Execution environment in Q4EBITDA benefited through favourable commodity prices – leveled off in Q4Net Segment assets reduction through lower working capital

17th May 2010 17

‘Electrical & Electronics’ Segment

Q4 FY10 Q4 FY09%

ChangeRs. Billion FY10 FY09

% Change

8.63 6.94 24% Total Net Revenues 26.94 25.12 7%

0 79 1 23 E t 2 74 4 29 0.79 1.23 ---Exports 2.74 4.29

1.43 0.89 61% EBITDA 4.23 3.39 25%

16.6% 12.9% EBITDA Margins 15.7% 13.5%

Net Segment Assets 11.32 12.47 -9%g

Q4 Sales growth led by Domestic Industrial recovery; International operations still subduedSmart improvement in EBITDA margins due to:

Favourable product mixFavourable product mixCost Rationalisation

Net Segment Assets driven by improved working capital management

17th May 2010 18

‘Machinery & Industrial Products’ Segment

Q4 FY10 Q4 FY09%

ChangeRs. Billion FY10 FY09

% Change

6.53 6.07 8% Total Net Revenues 21.35 23.97 -11%

0.50 1.60 ---Exports 2.06 5.87

1.51 1.14 33% EBITDA 4.71 4.85 -3%

23.1% 18.7% EBITDA Margins 22.1% 20.2%

Net Segment Assets 2.24 4.13 -46%

Q4 Revenues indicative of sequential recoveryExport business affected by global slowdown (Mainly valves)Improvement in EBITDA margins driven by operating leverageSmart reduction in Net Segment Assets led by allround reduction in working capital

17th May 2010 19

Presentation Outline

L&T Parent Performance

Segmental Performance

Group Performance

Sectoral Opportunities &

Outlook

17th May 2010 20

Consolidated P&L Statement

L&T

FY10 FY10 FY09 % Change

370.35 Total Net Reveunes (Net Sales + Other O i l I )

439.70 405.11 9%

Rs BillionL&T Group

370.35 Operational Income)

439.70 405.11 9%

48.16 EBITDA 64.39 50.24 28%

13.0% EBITDA Margins 14.6% 12.4%

(5.05) Interest Expenses (6.92) (5.28)

(4.15) Depreciation (9.79) (7.28)

9.10 Other Income 7.60 5.76

(16.21) Provision for Taxes (18.66) (14.23)

31.85 PAT (before Exceptional Items) 36.62 29.21 31.85 PAT (before Exceptional Items) 36.62 29.21

- Share of profits in Associate Cos. 1.06 0.51

- Minority Interest 0.29 0.35

31.85 PAT after Minority Interest (before Exceptional Items)

37.97 30.07 26%Exceptional Items)

11.91 Extraordinary & Exceptional Items (Net of tax & Minortiy Interest)

16.54 7.82

43.76 Profit After Tax 54.51 37.89 44%

17th May 2010 21

Consolidated Balance SheetL&T

Mar-10 Mar-10 Mar-09 Inc/(Dec)

183.12 Net Worth 209.91 139.87 70.04

- Minority Interest 10.88 10.59 0.29

Rs. BillionL&T Group

y

Loan Funds:

- Financial Services 95.05 62.16 32.89

- Dev. Projects 55.75 43.23 12.52

68.01 Others 75.76 78.61 (2.85) 68.01 Others 75.76 78.61 (2.85)

- Deferred Payment Liabilities 19.51 19.70 (0.19)

0.77 Deferred Tax Liabilities (Net) 1.53 1.31 0.22

251.90 Total Sources 468.39 355.47 112.92

63 66 Net Fixed Asset 98 51 74 12 24 39 63.66 Net Fixed Asset 98.51 74.12 24.39

79.65 Current Investments 85.60 52.18 33.42

76.79 Invt./ICDs/Loans & Advances to S&A Cos

5.06 4.89 0.17

5.49 Other Investments 8.62 11.03 (2.41) ( )

26.31 Net Current Assets 63.62 54.76 8.86

- Dev. Business Assets 97.63 87.39 10.24

- Loans towards financing activities 109.35 71.10 38.25

17th May 2010 22

251.90 Total Applications 468.39 355.47 112.92

L&T Infotech

Revenues (Rs. Bn) PAT (Rs. Bn)

5.67 5.12

4.974.57

0.81 0.73 0.65

0.90

4.52

4.73

4.69 5.24

0.61 0.60

0.57 0.59

FY09 FY10

Q1 Q2 Q3 Q4

FY09 FY10

Q1 Q2 Q3 Q4

FY09 FY10 FY09 FY10

◊ YoY Revenue contraction due to slowdown in US and Europe markets

FY09 FY1020.40 19.11

FY09 FY102.66 2.80

17th May 2010 23

◊ o e e ue co t act o due to s o do US a d u ope a ets◊ Q4 FY10 PAT indicative of sequential improvement

Financial Services

FY10 FY09%

ChangeFY10 FY09

% Change

Total Income PAT

Rs. Billion

L&T Finance Limited 9.86 7.96 24% 1.56 0.99 58%

L&T Infrastructure Finance Limited 4.52 2.96 53% 1.11 0.77 45%

L&T Finance Revenue growth led by Rural Equipment Finance and Micro Finance PAT M i i t d i b N t I t t M i PAT Margin improvement driven by Net Interest Margin expansionBusiness Assets: Rs. 70 Bn

L&T Infra FinanceL&T Infra FinanceRevenue Growth driven by most infrastructure segments (Power, telecom, roads, etc)Business Assets: Rs. 43 Bn

17th May 2010 24

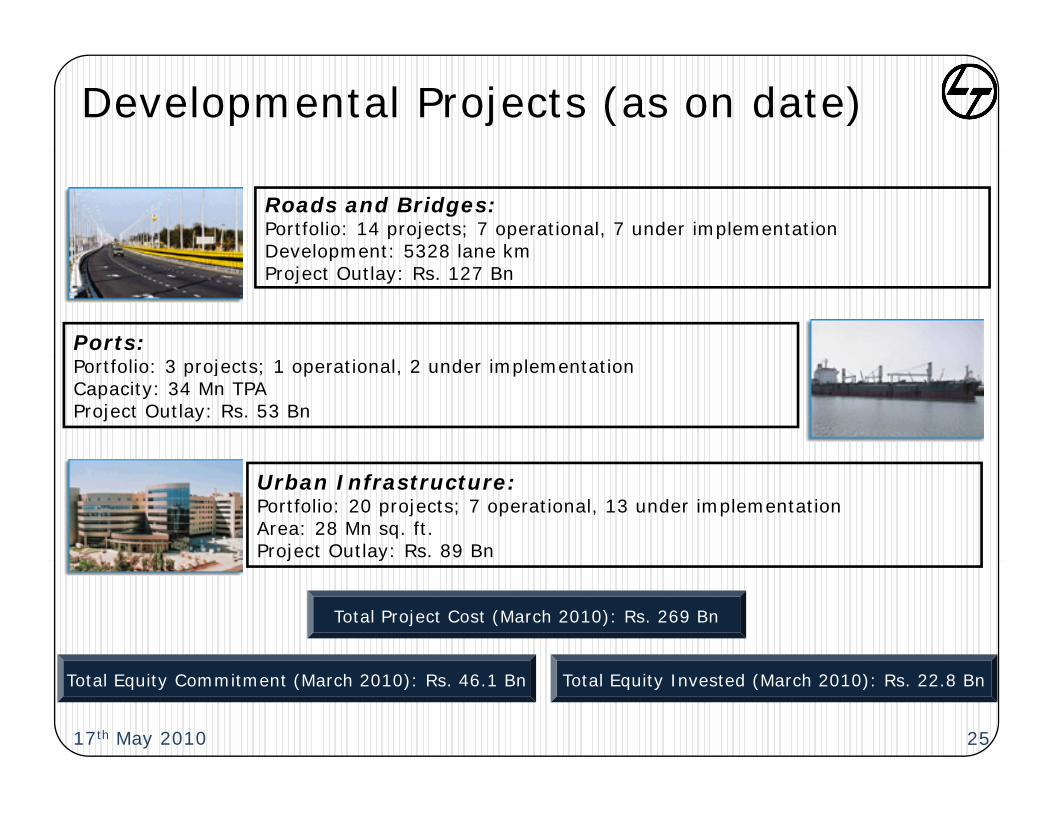

Developmental Projects (as on date)

Roads and Bridges:Portfolio: 14 projects; 7 operational, 7 under implementationDevelopment: 5328 lane kmDevelopment: 5328 lane kmProject Outlay: Rs. 127 Bn

Ports:Portfolio: 3 projects; 1 operational, 2 under implementationCapacity: 34 Mn TPAProject Outlay: Rs. 53 Bn

Urban Infrastructure:Portfolio: 20 projects; 7 operational, 13 under implementationArea: 28 Mn sq. ft.Project Outlay: Rs. 89 Bnj y

Total Project Cost (March 2010): Rs. 269 Bn

Total Equity Invested (March 2010): Rs. 22.8 BnTotal Equity Commitment (March 2010): Rs. 46.1 Bn

17th May 2010 25

Presentation Outline

L&T Parent Performance

Segmental Performance

Group Performance

Sectoral Opportunities &

Outlook

17th May 2010 26

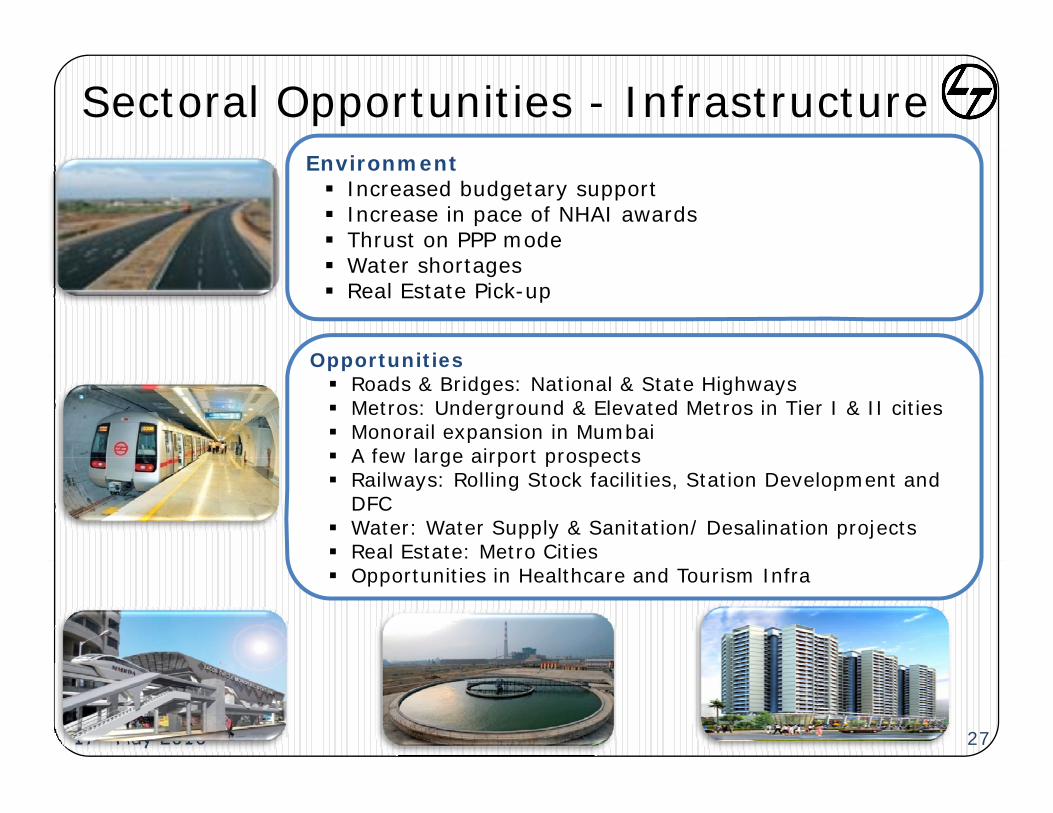

Sectoral Opportunities - InfrastructureEnvironment

Increased budgetary supportIncrease in pace of NHAI awardsThrust on PPP mode

O t iti

Water shortagesReal Estate Pick-up

OpportunitiesRoads & Bridges: National & State HighwaysMetros: Underground & Elevated Metros in Tier I & II citiesMonorail expansion in MumbaiA few large airport prospectsA few large airport prospectsRailways: Rolling Stock facilities, Station Development and DFC Water: Water Supply & Sanitation/ Desalination projects Real Estate: Metro CitiesOpportunities in Healthcare and Tourism Infra

17th May 2010 27

Sectoral Opportunities - Power

EnvironmentPower deficit and increasing energy requirementsGovernments’ plans to speed up Coal linkagesGovernments plans to speed up Coal linkagesIncreasing Private players participation (PPP)Thrust on Supercritical power plant technologyGovernment favoring domestic BTG manufacturersChinese CompetitionChinese CompetitionThrust on Nuclear Power (clean power)T&D capex to speed up

OpportunitiesEPC, BTG & BOP projects for Coal Based power plantsEPC projects for Gas Based Power plantsNuclear power plant construction and equipment supplyuc ea po e p a co s uc o a d equ p e supp yEPC projects for T&D in India and Middle East (Including PPP)

17th May 2010 28

Sectoral Opportunities - Hydrocarbon

EnvironmentCrude – Price stability and demandCrude Price stability and demandHydrocarbon Capex picking upIntense Domestic and International CompetitionMiddle East pick-upSmall signs of pick-up in FPSO and Rig market

Opportunities

S a s g s o p c up SO a d g a e

OpportunitiesEPC projects in Oil Extraction: Process Platforms, Wellhead platforms and subsea pipelinesResidue Upgradation projects in Midstream & Residue Upgradation projects in Midstream & EPC jobs for Downstream projectsConstruction and pipeline jobsRigs & FPSOs in Brazil, Middle East and Domestic

17th May 2010 29

Sectoral Opportunities - ProcessEnvironment

Minerals & MetalsIndia is net importer of steelDemand outpacing capacityp g p yPSU and Private projects still in cautious mode

FertilizersIncrease in demand for Food grains and volatility in International Urea PriceyAvailability of Natural Gas as feedstock with expected high allocation

OpportunitiesEPC projects for capacity expansion plans for both ferrous and non-ferrousDomestic investment in Power Mines Ports Domestic investment in Power, Mines, Ports, Metals industry to provide opportunities for Material Handling SystemsFertilizers: Feedstock Conversion & Expansion Projects

17th May 2010 30

Projects

E i

Outlook

Robust Growth (GDP/IIP)Worrisome Fiscal DeficitInflation is a concern

Economic

Heightened Domestic & International competition

Sectoral

Inflation is a concernAdequate liquidity but tightening policyIncreasing interest ratesEuropean ripplesNo mal monsoon

pStrong Power Gen. capexMiddle East picking upIncreasing NHAI activityT&D spends heading upWater spending likely to

Enablers&

Normal monsoon prediction

Water spending likely to increase

StrategyGrowth Drivers

Capacity expansion

Capability Building

Power (BTG) Nuclear PowerDefenseWater

p y pShipbuilding facilityOman facilitiesBTG factories due to be commissioned soonForging Unit coming up

17th May 2010

WaterRailways

Forging Unit coming upHorizontal & vertical integration

31

Thank You

Some of the largest & heaviest equipments in the world have been manufactured by L&T

India’s biggest marine equipment – an oil & gas

processing complex

manufactured by L&T

Many of the country’s prized landmarks have been built by L&T

Asia’s highest viaduct(Konkan Railway)

processing complex

The world’s longest cross-country conveyor

The world’s largest coal-gasifier (For China)

The World’s largest FCC Regenerator (Wt – 1320 MT)

3232

One of the world’s largest diesel hydro-treater project

for a refinery

88-metre bridge on the Northern Railways’ Jammu-

Udhampur line

17th May 2010

World’s First Chromium-Molybdenum-Vanadium-

Multiwall Ammonia Convertor

Bahai Temple, New Delhi

Annexure 1: Major Orders Booked in Q4 FY10

Description Rs Bn

Ammonia Feedstock Conversion Projects at Punjab & Haryana for National Fertilisers Ltd. 21.56

Aromatics Complex at Mangalore SEZ for ONGC Mangalore Petrochemicals Ltd (OMPL) 20.35

---- Domestic

Aromatics Complex at Mangalore SEZ for ONGC Mangalore Petrochemicals Ltd (OMPL) 20.35

EPC project for Steam Turbine & Generators and Auxillary Packages for 1320 MW Rajpura Thermal Power Project for Nabha Power Limited

14.33

4.17 MMTPA FCC Reactor regenerator Project of a grassroots fuel refinery for IOCL, Paradip 14.00

East Coast Offshore platform for Gujarat State Petroleum Corporation 10.60 East Coast Offshore platform for Gujarat State Petroleum Corporation 10.60

Turnkey project including engineering, procurement, fabrication and installation of 4 Well-Platforms for MHN Re-development project, ONGC

10.13

Design and construction of 36 High SpeedInterceptor Boats for Indian Coast Guard 9.77

Design & Construction of Phase I Campus at CTS SEZ Campus, Tamil Nadu for M/s. Cognizant 5 66

Technology Solutions (I) Pvt. Ltd. 5.66

Construction of Residential towers " The Address" for Wadhwa Group, Mumbai 5.01

Coal Handling Plant for 6X150 MW Mahan Captive Power Plant, Madhya Pradesh for Hindalco 4.00

Design, engineering, procurement, civil works, erection / construction, testing and i i i f th il k f 2X525 MW M ith Ri ht B k Th l P P j t

3.65 commissioning of the railway works of 2X525 MW Maithon Right Bank Thermal Power Project

Construction of 400 Bed, Women & Children Hospital Including Hostel Complex & Other facilities at Puducherry for Jawaharlal Nehru Institute of Post- Graduate Medical Education and Research

3.59

C t t f D i S l I t ll ti T ti & C i i i f MV P S t f

---- Exports

17th May 2010 33

Contract for Design, Supply, Installation, Testing & Commissioning of MV Power System for Abudhabi Ports Company at Khalifa Port and Industrial Zone at Abudhabi

3.82

Annexure 2: Details of Other IncomeRs. Billion FY10 FY09

Recovery from S&A / JV Companies 0.66 0.50

Technical Fees / IJV Profits 0 70 0 65 Technical Fees / IJV Profits 0.70 0.65

Others 2.24 1.77

Total - Other Operational Income 3.60 2.92

Interest Income 1.28 1.72

Dividend from S&A Companies 1.08 0.72

Income from Other Investments 2.79 2.63

Profit on sale of investments 1.40 0.95

Miscellaneous Income 2.55 1.38

Total - Other Income 9.10 7.40

17th May 2010 34

Annexure 3: Details of Extraordinary & Exceptional items

(Amt in Rs. Bn) FY 10 FY 09

Profit on Sale of Investment in Ultratech Cement 10.20 -

Profit on sale of stake in Associate Company 0.52 -

Exceptional Items (Net of Tax)

Profit on part buy-back of shares by Associate Co. 0.23 -

Provision for dimunition in Invst. in a Associate Co. (0.40) -

P i i t d I t t i S t (1 86)

Extraordinary Items (Net of Tax)

Provision towards Investment in Satyam - (1.86)

Profit on Sale of RMC Busines - 9.59

Profit on Sale of PDP Busines 0.73 -

Reversal of provision on part sale of Invst in Satyam 0 63 - Reversal of provision on part sale of Invst. in Satyam 0.63 -

Total 11.91 7.73

17th May 2010 35

Annexure 4: Details of Increase in support to S&A in FY10 –Investment, ICDs and Advance against Equity

Increase in Support to S&A Rs. Bn

L&T Power Development 8.19

Urban Infra SPVs 4.62

L&T Infra Finance 4.25

L&T Shipbuilding 3.74

Road Projects 2.58

IDPL 2.10

L&T Finance 1.25

Forgings 1.11

L&T International FZE 0.89

L&T Power (for MHI JVs) 0.51

L&T Capital (4.80)

Others 1.27

Total 25.71

17th May 2010 36