LARGE FORMAT RETAIL - m3property Strategists · sub groups with furniture, floor coverings, ......

10

| P1 www.m3property.com.au Key Research Contacts: m3commentary LARGE FORMAT RETAIL Autumn | 2017 Jennifer Williams National Director | NSW (02) 8234 8116 Casey Robinson Research Manager | QLD (07) 3620 7906 Erin Obliubek Research Manager | VIC (02) 9605 1075 Zoe Haskett Research Manager | SA (08) 7099 1807 m3property.com.au

Transcript of LARGE FORMAT RETAIL - m3property Strategists · sub groups with furniture, floor coverings, ......

| P1www.m3property.com.au

Key Research Contacts:

m3commentary LARGE FORMAT RETAIL

Autumn | 2017

Jennifer WilliamsNational Director | NSW

(02) 8234 8116

Casey RobinsonResearch Manager | QLD

(07) 3620 7906

Erin ObliubekResearch Manager | VIC

(02) 9605 1075

Zoe HaskettResearch Manager | SA

(08) 7099 1807

m3property.com.au

| P2www.m3property.com.au

m3property Research

Market Overview 3

Key Retail Influences 4

Occupier Demand 5

Key Indicators 7

Significant Sales 9

Outlook 10

CONTENTS

•Household goods retail turnover continued to grow

over the year to January 2017, supported by ongoing

population growth, dwelling completions and low

interest rates. The rate of growth has, however,

declined compared to the year prior.

•Consumer sentiment remains volatile.

•Due to household goods retail trade remaining

positive and low vacancy over the year to March 2017,

rents for large format retail space has risen over the

year.

• Investor demand was strong over 2016, however,

sales activity slowed, compared to the year prior. Over

the first quarter of 2017 there have already been

seven sales totalling $178,691,568.

•Yields across prime retail centres continued to tighten

over the year to March 2017, with further slight

tightening likely in the short term.

RISING RENTALS

AND TIGHTENING

YIELDS IN LARGE

FORMAT RETAIL

Large Format Retail Centres: Medium to

large shopping centres, dominated by bulky

goods retailers (furniture, electrical, outdoor

etc). Centres typically contain a small

number of specialty shops.

Freestanding stores: Large format retailer

in a stand alone store.

DEFINITIONS

m3commentary Autumn 2017

| P3www.m3property.com.au

Large format retail properties are experiencing positive tenant demand across most

States, driven by continued residential development activity, albeit slowing, and positive

household goods retail trade over the past year. Transaction activity decreased slightly

over 2016 compared to 2015 but has started strongly with seven sales reported, over the

$5,000,000 threshold, already recorded in the first quarter of 2017.

This m3property report focuses on retailer and investment

activity in large format retail properties across

Australia. Large format retail comprises multi-tenanted

centres (formerly known as bulky goods centres) and

single tenanted freestanding stores (occupied by tenants

such as Bunnings, Officeworks and Harvey Norman).

The key influences on tenant demand strengthened over

2014 and 2015, however, growth in the demand drivers

slowed in 2016. With the major banks independently

raising interest rates, residential development approvals

falling and construction set to follow, key drivers are likely

to continue to slow in the short term.

Leasing demand strengthened over the second half of

2016 for large format retail space. This positive demand,

has resulted in vacancy falling over the past six months

from 6.6% as at September 2016, to 6.2% as at March

2017.

This low vacancy rate has only translated into rental growth

in Sydney and Brisbane over the year to March 2017, with

Melbourne, Perth and Adelaide rents being fairly stable.

Investment activity was solid over 2016, but fell marginally

compared to a very strong 2015. The first three months of

2017 have seen seven large format retail sales, over the

$5,000,000 threshold. Transaction demand remains

positive due to low interest rates and good sales

performance in most markets. Yields have firmed over the

year to March 2017 across all the capital cities monitored

by m3property.

Ownership of large format retail centres has become

increasingly concentrated following the exit of many

institutional investors from the sector. Some of the larger

centre owners include Aventus (formerly BB Retail Capital),

Harvey Norman, Arkadia, LaSalle Investment

Management, Charter Hall, Telstra Super, Sentinel

Property Group, Primewest, Valad and Lancini Property &

Development.

MARKET OVERVIEW

m3property Research

m3commentary Autumn 2017

m3property Valuation

Bunnings Hastings, Victoria

| P4www.m3property.com.au

ECONOMY

Business investment continues to be restrained, although measures of business

sentiment remain above average. Labour market indicators continue to be mixed and

inflation low. While a low official interest rate is supporting domestic demand, rising

rates from the major banks and an appreciating exchange rate are reducing its

effectiveness.

CONSUMER CONFIDENCE

The Westpac-Melbourne Institute Index of Consumer Sentiment remains volatile. The

index is currently at 99.7 in March 2017, below a net balance of 100 (meaning

pessimists slightly outweigh optimists). The mixed outlook for the economy is likely to

have kept sentiment weak despite positive signs from the labour market and an overall

improvement in the Australian economy reported for the December quarter.

RETAIL BUILDING ACTIVITY

The value of retail building approvals in 2016 has for the fifth consecutive year

exceeded long-term average levels as retailers have looked to keep their offering fresh

in the changing retail environment. Retail development activity is, therefore, expected

to remain robust in the short term due to approvals from 2016 still to be actioned.

New residential building work done remains strong, having increased by 5.5% from

December quarter 2015 to December quarter 2016 (ABS February 2017). This is likely

to continue to support household goods turnover in the short term.

POPULATION

Moderate population growth continues to underpin the retail sector despite volatile

consumer sentiment and low wages growth. Australia’s Estimated Resident

Population (ERP) as at 30 September 2016 was 24,220,200 people reflecting an

annual increase of 348,700 (1.5%). The fastest population growth in the year to

September 2016 was in Victoria (2.1%), followed by ACT (1.5%) and NSW and

Queensland (both 1.4%). A consequence of population growth is residential property

demand which, in turn, generates greater pressure for new household goods.

HOUSEHOLD GOODS RETAIL TURNOVER

Household goods retail turnover continued to grow over the year to January 2017,

supported by ongoing population growth, dwelling completions and low interest rates.

The rate of growth has, however, declined compared to the year prior. Household

goods retail turnover rose 2.0% over the year to January 2017. Turnover rose for all

sub groups with furniture, floor coverings, houseware and textile goods retailing rising

by 4.1%, Electrical and electronic goods retailing increasing by 1.7% and hardware,

building and garden supplies retailing rising by 0.7%.

The weaker Australian dollar has increased import prices and pressure on profit

margins in the sector. It has, however, also dampened imports including those

purchased online.

The combination of more households and positive domestic retail spending bodes well

for the large format retail sector in the short term. Increased price competition in the

retail industry generally presents an opportunity for the large format retail sector given

the industry’s low rent/low cost business model which can enable higher savings to

consumers.

$

KEY INFLUENCES

m3property Research

m3commentary Autumn 2017

| P5www.m3property.com.au

OCCUPIER DEMAND

m3property Research

MAJOR TENANTS

There are a number of large retail

groups which have a significant

influence on demand for large format

retail space. This section looks at the

reported plans and performance of a

number of these groups.

WESFARMERS

Bunnings and Officeworks achieved

strong revenue growth of 8.3% and

5.9% respectively over the six

months ended December 2016

compared to the six months to

December 2015.

Bunnings opened nine new stores in

the second half of 2016 taking its

network to 248 large stores, 73

smaller format stores and 33 trade

centres across Australia according to

Wesfarmers. Bunnings continues to

expand and improve its store network

through ongoing investment in

existing outlets and new store

openings. With 11 stores currently

under construction, Bunnings plan to

expand the store network by 15-18

new stores over the 2017 financial

year.

Officeworks had a network of 163

stores across Australia as at

December 2016. Four stores were

opened during the second half of

2016. Officeworks’ strategy for

growth includes strong focus on

customer offer, developing and

engaging staff and continuing to

invest in all channels.

SUPER RETAIL GROUP

The Super Retail Group includes

Amart Sports, Rebel, Avanti Fitness,

BCF (Boating Camping Fishing),

Ray’s Outdoors, Supercheap Auto,

Goldcross Bicycles and Workout

World. While some of these retailer’s

stores are freestanding, many are

located within large format retail

centres.

Auto retailing division -

Supercheap Auto and Auto Trade

Direct witnessed solid sales growth

from new stores and existing stores

of 6.9% over the six months to

December 2016 compared to the six

months to December 2016 (3.7% like

–for-like sales growth). There were

312 stores as at the end of

December 2016. Over the six

months, seven new stores opened,

two were closed and 14 were

refurbished. Over the next six

months eight new stores are

planned, two are expected to close

and 39 stores are likely to be

refurbished, extended or relocated.

Leisure Division – Sales growth

increased over the six months to

December 2016 by 2.9% compared

to the same period last year, with

like-for-like growth increasing by

5.8% over the same period. There

were 133 BCF stores and 17 Ray’s

Outdoor stores as at the end of

December 2016 with two new BCF

stores and 11 Ray’s Outdoor’s stores

converted to BCF over the six

months. One new store, eight

refurbishments and one relocation is

planned for BCF in next six months

and two Ray’s Outdoors are likely to

be refurbished.

Sports Retailing - Sales

performance was strong in the sports

retailing division. Sales grew by

8.5% over the six months to

December 2016 compared to the

same period in the previous year.

Like-for-like sales growth was 6.0%

over the six-month period. Two

Rebel and one Amart Sports store

opened, two Rebel stores were

closed and three Amart Sports were

converted from Ray’s Outdoors over

the second half of 2015. This took

the total to 64 Amart Sports and 101

Rebel stores as at December 2016.

Super Retail Group plan to open

three new Amart Sports stores,

relocate one Rebel and undertake

one Amart Sports refurbishment in

the next six months.

METCASH

As at October 2016, Metcash owned

755 hardware stores across Australia

under the brands of Home Timber

and Hardware (acquired October

2016), Mitre 10, True Value and

Thrifty-link Hardware. Over the six

months to October five stores were

added, nine were closed and 381

were acquired. This now makes

them a key player in the sector.

m3commentary Autumn 2017

m3property Valuation:

Home Central Coffs Harbour, NSW

| P6www.m3property.com.au

SPOTLIGHT RETAIL GROUP

The privately owned Spotlight Retail

Group owns Spotlight and Anaconda

retail operations. As at March 2017

there were 105 Spotlight stores and

44 Anaconda stores in Australia.

Over the year to March 2017 there

was one Spotlight store (Trinity

Gardens) and three new Anaconda

stores opened in Australia.

STEINHOFF ASIA PACIFIC

LIMITED (FANTASTIC

HOLDINGS LIMITED)

In October 2016 Steinhoff Asia

Pacific announced they had executed

a Scheme Implementation Deed

(SID) under which it was proposed

that Steinhoff would acquire 100% of

the issued share capital in Fantastic

Holdings by way of a scheme of

arrangement. Steinhoff Asia Pacific

is a retailer of furniture and

homeware in Australia and New

Zealand through 157 retail stores

under the Freedom, Snooze, POCO

and Bay Leather Republic brands.

Fantastic Holdings Limited (FHL)

operated 127 stores in Australia

according to their latest financial

report, comprising the Fantastic

Furniture (71 stores), Plush (35

stores), Original Mattress Factory (18

stores) and Le Cornu brands (2

stores). The group produced strong

sales over the 2016 financial year

recording 11.8% comparative store

sales growth. During 2015-16,

Fantastic Furniture opened a store in

Rockhampton Queensland and

closed three stores, Plush opened

two stores in Queensland (Fortitude

Valley and Townsville) and Original

Mattress Factory opened one new

store in Wagga Wagga, New South

Wales. Of the Le Cornu stores open

at the end of financial year 2016,

Keswick has since closed, while

Darwin is expected to continue

operating under the Le Cornu brand

but with a hybrid product offering.

JB HI-FI LIMITED

JB Hi-Fi is an ASX listed company

which continues to see strong growth

in sales and store numbers. Like for

like sales growth was up 8.7% over

the six months to December 2016

compared to the corresponding

period in 2015. There were 183

stores as at December 2016 up from

179 stores at the end of 2015. The

stores are located in large format

retail centres, strips, shopping

centres and as freestanding stores.

Two new JB Hi-Fi stores are

expected to open in Australia in the

six months to June 2017.

JB Hi-Fi Limited took over The Good

Guys network of 103 stores on 28

November 2016. Like-for-like growth

over their period of ownership until

the end of December 2016 was

-0.7%. The Good Guys is expected

to open one new store in the six

months to June 2017.

HARVEY NORMAN

HOLDINGS LIMITED

Harvey Norman Holdings Limited

experienced strong sales growth over

the second half of 2016. The retailer

has 193 franchised complexes in

Australia and 87 company operated

stores across seven countries.

Comparable sales growth of

Australian stores was 4.7% in the

second half of 2016, compared to the

same period in 2015.

NEW ENTRANTS OR

EXPANSION OF NETWORKS

Large format retailing centres are

seeing a changing tenant mix often

including more traditional Shopping

Centre or High Street retailers such

as supermarkets, services and

restaurants. Planning law changes

across many States have facilitated

this move.

Hardware stores and Auto retailing

have the largest store networks,

although hardware expansion is likely

to slow over the short to medium

term with the excess capacity

created by the Masters closure.

In terms of expanding networks,

bedding retailers showed the

greatest growth in store numbers

over the year to March 2017 with

store growth of 9.1%. This was

followed by hardware retailers, which

expanded their store network by

5.3% over the same period.

OCCUPIER DEMAND

m3property Research

m3commentary Autumn 2017

m3property Valuation:

The Brickworks Annex, Southport

Queensland

| P7www.m3property.com.au

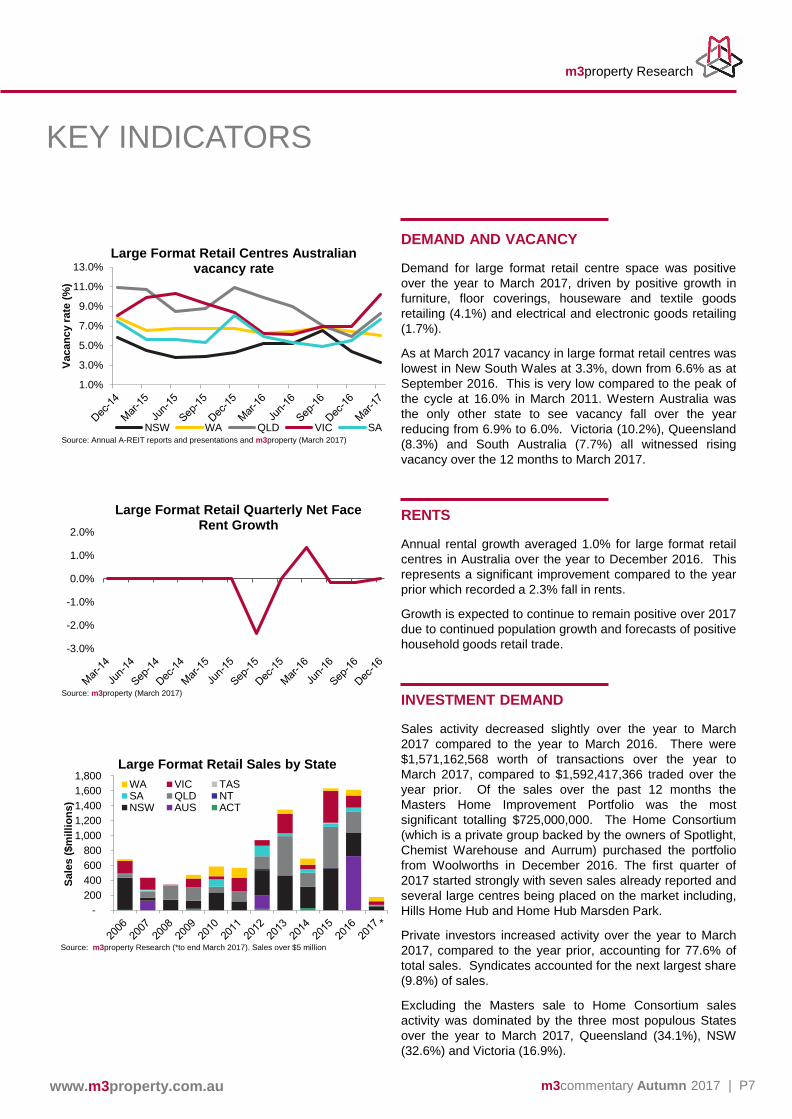

DEMAND AND VACANCY

Demand for large format retail centre space was positive

over the year to March 2017, driven by positive growth in

furniture, floor coverings, houseware and textile goods

retailing (4.1%) and electrical and electronic goods retailing

(1.7%).

As at March 2017 vacancy in large format retail centres was

lowest in New South Wales at 3.3%, down from 6.6% as at

September 2016. This is very low compared to the peak of

the cycle at 16.0% in March 2011. Western Australia was

the only other state to see vacancy fall over the year

reducing from 6.9% to 6.0%. Victoria (10.2%), Queensland

(8.3%) and South Australia (7.7%) all witnessed rising

vacancy over the 12 months to March 2017.

RENTS

Annual rental growth averaged 1.0% for large format retail

centres in Australia over the year to December 2016. This

represents a significant improvement compared to the year

prior which recorded a 2.3% fall in rents.

Growth is expected to continue to remain positive over 2017

due to continued population growth and forecasts of positive

household goods retail trade.

INVESTMENT DEMAND

Sales activity decreased slightly over the year to March

2017 compared to the year to March 2016. There were

$1,571,162,568 worth of transactions over the year to

March 2017, compared to $1,592,417,366 traded over the

year prior. Of the sales over the past 12 months the

Masters Home Improvement Portfolio was the most

significant totalling $725,000,000. The Home Consortium

(which is a private group backed by the owners of Spotlight,

Chemist Warehouse and Aurrum) purchased the portfolio

from Woolworths in December 2016. The first quarter of

2017 started strongly with seven sales already reported and

several large centres being placed on the market including,

Hills Home Hub and Home Hub Marsden Park.

Private investors increased activity over the year to March

2017, compared to the year prior, accounting for 77.6% of

total sales. Syndicates accounted for the next largest share

(9.8%) of sales.

Excluding the Masters sale to Home Consortium sales

activity was dominated by the three most populous States

over the year to March 2017, Queensland (34.1%), NSW

(32.6%) and Victoria (16.9%).

KEY INDICATORS

m3property Research

m3commentary Autumn 2017

1.0%

3.0%

5.0%

7.0%

9.0%

11.0%

13.0%

Vacan

cy r

ate

(%

)

Large Format Retail Centres Australian vacancy rate

NSW WA QLD VIC SASource: Annual A-REIT reports and presentations and m3property (March 2017)

-3.0%

-2.0%

-1.0%

0.0%

1.0%

2.0%

Large Format Retail Quarterly Net Face Rent Growth

Source: m3property (March 2017)

-

200

400

600

800

1,000

1,200

1,400

1,600

1,800

Sale

s (

$m

illi

on

s)

Large Format Retail Sales by State

WA VIC TASSA QLD NTNSW AUS ACT

Source: m3property Research (*to end March 2017). Sales over $5 million

*

| P8www.m3property.com.au

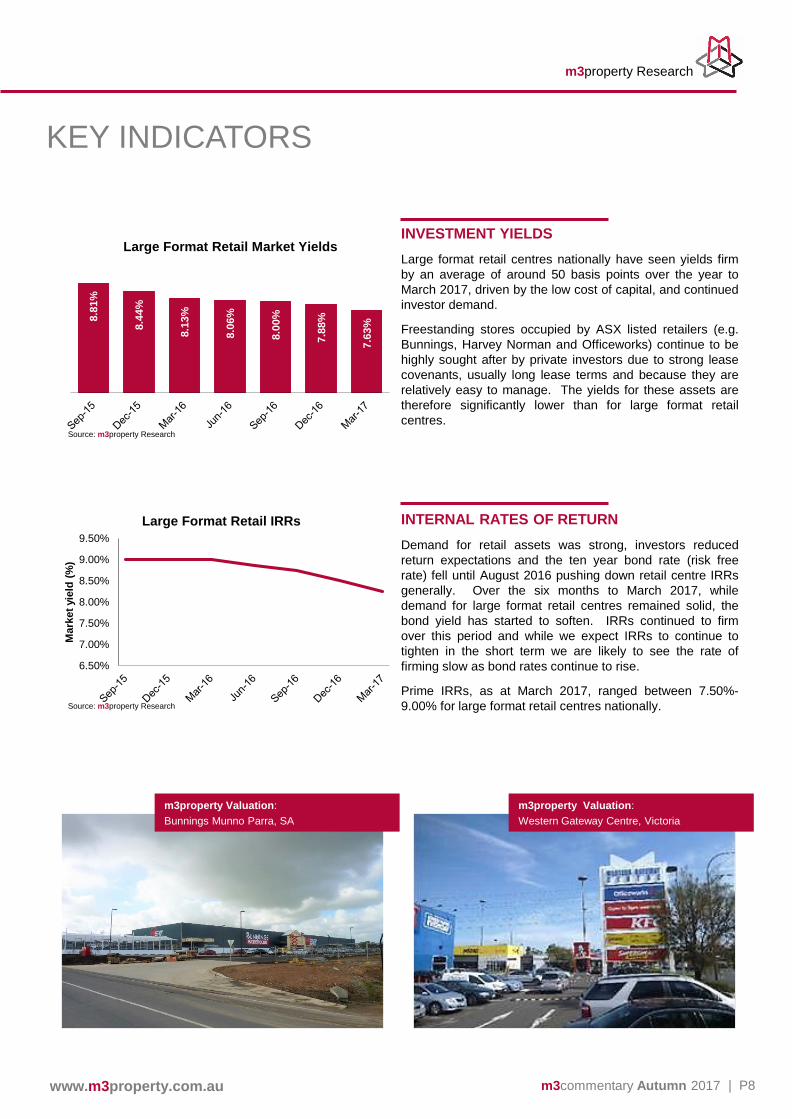

INVESTMENT YIELDS

Large format retail centres nationally have seen yields firm

by an average of around 50 basis points over the year to

March 2017, driven by the low cost of capital, and continued

investor demand.

Freestanding stores occupied by ASX listed retailers (e.g.

Bunnings, Harvey Norman and Officeworks) continue to be

highly sought after by private investors due to strong lease

covenants, usually long lease terms and because they are

relatively easy to manage. The yields for these assets are

therefore significantly lower than for large format retail

centres.

INTERNAL RATES OF RETURN

Demand for retail assets was strong, investors reduced

return expectations and the ten year bond rate (risk free

rate) fell until August 2016 pushing down retail centre IRRs

generally. Over the six months to March 2017, while

demand for large format retail centres remained solid, the

bond yield has started to soften. IRRs continued to firm

over this period and while we expect IRRs to continue to

tighten in the short term we are likely to see the rate of

firming slow as bond rates continue to rise.

Prime IRRs, as at March 2017, ranged between 7.50%-

9.00% for large format retail centres nationally.

KEY INDICATORS

m3property Research

m3commentary Autumn 2017

m3property Valuation:

Bunnings Munno Parra, SA

m3property Valuation:

Western Gateway Centre, Victoria

8.8

1%

8.4

4%

8.1

3%

8.0

6%

8.0

0%

7.8

8%

7.6

3%

Large Format Retail Market Yields

Source: m3property Research

6.50%

7.00%

7.50%

8.00%

8.50%

9.00%

9.50%

Mark

et

yie

ld (

%)

Large Format Retail IRRs

Source: m3property Research

| P9www.m3property.com.au

Property Date PriceMarket

Yield

Building

Rate (/m2)Major Tenants Purchaser

12-18 David Witton Drive, Noarlunga

Centre, SAFeb 17 $17,551,568 8.13% $2,355

Blood Doner Centre,

GodfreysPeak Equities Pty Ltd

456 Logan Road, Greenslopes, Qld Oct 16 $7,900,000 5.53% $3,776Supercheap Auto, Cash

ConvertersPrivate Investor

Bunnings, Corner Murray Valley

Highway and Frank Drive,

Yarrawonga, Vic

Aug 16 $11,590,000 4.94% $1,689 Bunnings Overseas Investor

Indooroopilly Central, 34 Coonan

Street, QldMay 16 $85,000,000 5.78% $4,344

Spotlight, Midas Carpet

Call, Kmart TyresJen Retail Properties Limited

232 Brisbane Road, Booval, Qld May 16 $8,690,000 7.24% $3,158 Snooze, Baby Bunting Syndicate

Masters Portfolio Apr 16 $219,000,000 7.26% $1,581-3,104 N/AAventus Retail Property

Fund

Bunnings, Corner Sundew Rise and

Honeybush Drive, Joondalup, WAMar-16 $43,545,454 5.5% $2,561 Bunnings Private Investor

Bunnings, Corner Tulloch Road and

Barnet Road, Evanston, SAMar 16 $13,135,400 5.9% $2,960 Bunnings Undisclosed

Harvey Norman Centre, 494-504

Gardeners Road, Alexandria, NSWFeb 16 $63,000,000 5.87% $5,220 Harvey Norman Arkadia

Please contact our Retail Valuers for further details.

SIGNIFICANT SALES TO DATE

m3property Research

m3commentary Autumn 2017

m3property Valuation:

12-18 David Witton Drive, Noarlunga

Centre, SA sold in February 2017

KEY RETAIL VALUATION

CONTACTS

.

OUTLOOKLARGE FORMAT RETAIL

DISCLAIMER

© m3property Australia. This report has been derived, in part, from sources other than m3property. In passing on this information, m3property makes no

representation that any information or assumption contained in this material is accurate or complete.

To the extent that this material contains any statement as to the future, it is simply an estimate or opinion based on information currently available to m3property

and contains assumptions which may be incorrect. m3property makes no representation that any such statements are, or will be, accurate.

Heath Crampton

National Director | NSW

(02) 8234 8113

Shaun O’Sullivan

Director | VIC

(03) 8234 8113

Basil Simitci

Director | QLD

(07) 3620 7908

Simon Hickin

Director | SA

(08) 7099 1812

m3property Research

m3property provides national

coverage in all States and

Territories.

New supply of large format retail centres is expected to

be driven by freestanding stores in 2017. Hardware

retailer Bunnings, in particular, is expected to open

between 15-18 new stores across various states over the

next year with 11 stores already under construction. A

slowing of centre supply is expected due to the reduction

in residential construction activity forecast in the short to

medium term.

The Federal Government’s 2016 Budget is forecasting

economic growth of 2.5% (2016-17) and 3.0% (2017-18),

which is well above other advanced economies and

bodes well for retail over the next two years.

Although continued global economic uncertainty and

financial market volatility has affected consumer

confidence over the past few years, it is expected to

improve over 2017 given the continuing low interest rate

environment and the slow transition towards non-mining

sectors.

Furthermore, the above-mentioned economic factors

should also support further jobs growth and business

confidence in the year ahead, particularly in New South

Wales and Victoria where population growth is expected

to be strongest.

Yield compression occurred nationally although it was

strongest within non-mining driven states in 2016.

Further yield compression, could occur over 2017 given

the continued low cost of capital, however, it is expected

to slow compared to 2016.

It is expected that investor demand will remain strong in

the short term with continued interest in the sector

coming largely from private investors and syndicates.