LAPORTE l..ih)rtc, APAc: CPA* t SUS

13

"LAPORTE CPA* t SUS<KfiSI AOVrSOAa November 14, 2017 To Whom It May Concern: l..ih)rtc, APAc: 111 Vciemns Blvd. | Stt'iie 600 Mcuiric, LA 7000S 504.835.'^522 ! Fax 304.«35,553S l^Porte.com (3 This report has been re-submitted to the Louisiana Legislative Auditor to (1) include the opinion on the schedule of expenditures of federal awards (pages 1-2 of this report) that had previously been omitted and (2) remove the financial statement section of the summary of auditor's results (page 10 of this report) that was previously reported in error. A Professional Accounting Corporation Metairie, LA Under provisions of state law, this report is a public document. A copy of the report has been subm itted to the entity and other appropriate public officials. The report is available for public inspection at the Baton Rouge office of the Legislative Auditor and, where appropriate, at the office of the parish clerk of court Release Date 1 7 ?niR LOUISIANA • TEXAS An ludcpciulcniiy Owntrd Mcmbt-r. RSM UN Alliance (tSMUS WMftccnewibw ft tepjfiUg anf a'dpperiit^frw thetere iMpcMkubfp'wUHRi (wniKU«Tdan}tk>nv*n(te4(t^(Vk*iMfM«Andtodppee(iri]i fiWA ASM IK LLP RSU IK IIJ>» Ihe U.S. mombe) «imi ol RSM 1ft(einat>o<ul « eet^.nk of woepenthmi audi, m and cofiuiitinqfttmi Mamoart'rfRSM AttrawftMactes^toRSiA tnten^tona' («>«ouKe«llwou^> RSMUStLPtMl a** no) flV>nb*<f>rn)»i^RSM tni^matxVTal

Transcript of LAPORTE l..ih)rtc, APAc: CPA* t SUS

"LAPORTE CPA* t SUS<KfiSI AOVrSOAa

November 14, 2017

To Whom It May Concern:

l..ih)rtc, APAc: 111 Vciemns Blvd. | Stt'iie 600

Mcuiric, LA 7000S 504.835.'^522 ! Fax 304.«35,553S

l^Porte.com

(3 This report has been re-submitted to the Louisiana Legislative Auditor to (1) include the opinion on the schedule of expenditures of federal awards (pages 1-2 of this report) that had previously been omitted and (2) remove the financial statement section of the summary of auditor's results (page 10 of this report) that was previously reported in error.

A Professional Accounting Corporation Metairie, LA

Under provisions of state law, this report is a public document. A copy of the report has been subm itted to the entity and other appropriate public officials. The report is available for public inspection at the Baton Rouge office of the Legislative Auditor and, where appropriate, at the office of the parish clerk of court

Release Date 1 7 ?niR

LOUISIANA • TEXAS

An ludcpciulcniiy Owntrd Mcmbt-r. RSM UN Alliance (tSMUS WMftccnewibw ft tepjfiUg anf a'dpperiit^frw thetere iMpcMkubfp'wUHRi (wniKU«Tdan}tk>nv*n(te4(t^(Vk*iMfM«Andtodppee(iri]i fiWA ASM IK LLP RSU IK IIJ>» Ihe U.S. mombe) «imi ol RSM 1ft(einat>o<ul « eet^.nk of woepenthmi audi, m and cofiuiitinqfttmi Mamoart'rfRSM AttrawftMactes^toRSiA tnten^tona' («>«ouKe«llwou^> RSMUStLPtMl a** no) flV>nb*<f>rn)»i^RSM tni^matxVTal

RENAISSANCE NEIGHBORHOOD DEVELOPMENT CORPORATION

Audit of the Schedule of Expenditure of Federal Awards

June 30, 2015

LAPORTE CPAi i SOSlfilSS ADVISOBS

Contents

Independent Auditor's Report 1-2

Report on Compliance for a Federal Program and Report on Internal Control Over Compliance When Using the Program-Specific Audit Option to Satisfy OMB Circular A-133 Requirements 3-5

Schedule of Expenditures of Federal Awards

Notes to Schedule of Expenditures of Federal Awards

Schedule of Findings and Questioned Costs 8-9

Summary Schedule of Prior Audit Findings 10

T A "T^ 1 • 1 • I-4iPoftc, APACJ LAx ORTE 111 Veteram Btv-d.! Suite 600

CPA. A BusiNEce Asvisofl* Mctairtc, LA 70005

504.^35.5522 i Fax 504.835.5535 LaPorte.com

Independent Auditor's Report

To the Board of Directors Renaissance Neighborhood Development Corporation

Report on the Schedule of Expenditures of Federal Awards We have audited the accompanying schedule of expenditures of federal awards for the Community Development Block Grant (CDBG Program) of Renaissance Neighborhood Development Corporation (RNDC) for the year ended June 30, 2015, and the related notes (the financial statement).

Management's Responsibility for the Schedule of Expenditures of Federal Awards Management is responsible for the preparation and fair presentation of this financial statement in accordance with accounting principles generally accepted in the United States of America; this includes the design, implementation, and maintenance of internal control relevant to the preparation and fair presentation of a financial statement that is free from material misstatement, whether due to fraud or error.

Auditor's Responsibility Our responsibility is to express an opinion on this financial statement based on our audit. We conducted our audit in accordance with auditing standards generally accepted in the United States of America; the standards applicable to financial audits contained in Government Auditing Standards, issued by the Comptroller General of the United States; and 0MB Circular A-133, Audits of States, Local Governments, and Non-Profit Organizations. Those standards and 0MB Circular A-133 require that we plan and perform the audit to obtain reasonable assurance about whether the financial statement is free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statement. The procedures selected depend on the auditor's judgment, including the assessment of the risks of material misstatement of the financial statement, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity's preparation and fair presentation of the financial statement in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity's internal control. Accordingly, we express no such opinion. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluating the overall presentation of the financial statement.

LOUiSiANA • TEK.AS

An Ownvd Mctnbcf, RSM liS Alliance

(hit««! ao^iion^. a Arai frem R5« US LLf RSM US ILP is ihc US, membw fmn of RSW tntPinatssiw!, a giobi! "tfwiwk liS ifKSAf*«d«w AutSt.ia*. Afui conuKi^ Srmv fApmofrio! RSM US havp »tr.9V so

- •• -X •••

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion.

Opinion In our opinion, the financial statement referred to above presents fairly, in all material respects, the expenditures of federal awards for the CDBG Program of RNDC for the year ended June 30, 2015, in accordance with accounting principles generally accepted in the United States of America.

Under Louisiana Revised Statute 24:513, this report is distributed by the Louisiana Legislative Auditor as a public document.

mL

A Professional Accounting Corporation

Metairie, LA September 29, 2017

LAPORTE I i I Vftcnins Blvd. I Suiic 600 CPA, A SUSINEM ADV.SOBS Mci.uric, l.A 70005

504.«35.S522 I Tax 504.835A435 La Porte.com

Report on Compliance for a Federal Program and Report on Internal Control Over Compliance When Using the Program-Specific Audit Option to Satisfy

0MB Circular A-133 Requirements

Independent Auditor's Report

To the Board of Directors Renaissance Neighborhood Development Corporation

Report on Compliance for the Community Development Block Grant We have audited the Renaissance Neighborhood Development Corporation's (RNDC) compliance with the types of compliance requirements described in the 0MB Compliance Supplement that could have a direct and material effect on its Community Development Block Grant (CDBG Program) for the year ended June 30, 2015.

Management's Responsibility Management is responsible for compliance with the requirements of laws, regulations, contracts, and grants applicable to the CDBG Program.

Auditor's Responsibility Our responsibility is to express an opinion on compliance for RNDC's CDBG Program based on our audit of the types of compliance requirements referred to above. We conducted our audit of compliance in accordance with auditing standards generally accepted in the United States of America: the standards applicable to financial audits contain^ in Government Auditing Standards, issued by the Comptroller General of the United States; and 0MB Circular A-133, Audits of States, Local Governments, and Non-Profit Organizations. Those standards and 0MB Circular A-133 require that we plan and perform the audit to obtain reasonable assurance about whether noncompliance with the types of compliance requirements referred to above that could have a direct and material effect on the CDBG Program occurred. An audit includes examining, on a test basis, evidence about RDNC's compliance with those requirements and performing such other procedures as we considered necessary in the circumstances.

We believe that our audit provides a reasonable basis for our opinion on compliance for the CDBG Program. However our audit does not provide a legal determination of RNDC's compliance.

Opinion on Compliance for the CDBG Program In our opinion, RNDC complied, in all material respects, with the compliance requirements referred to above that could have a direct and material effect on its CDBG Program for the year ended June 30, 2015.

LOUISIANA • TEXAS

An IndcpcnUcnily Owntd Member. RSM l.iS AlliiUicc KSM US Affiiintje m8«nbcf ftnm M aad rtiM (a owt «nd»«h r> fiwn ASM US Uf RSM US a tlw US. rncfr^ fam it RSM a '»«v»orit o( wid^ena^nt audit to* and eanjwftteg Sfmt MewiOart o< RSW u i Mv# to RSM

moMUM tiueu«^> RSM USLLI* IM «t* (rwinbo< u< RSM intc/iaiiocul

other Matters The results of our auditing procedures disclosed an instance of noncompliance, which is required to be reported in accordance with 0MB Circular A-133 and which is described in the accompanying schedule of findings and questioned costs as item 2015-001. Our opinion on its major federal program is not modified with respect to this matter.

RNDG's response to the noncompliance finding identified in our audit is described in the accompanying schedule of findings and questioned costs. RNDG's response was not subjected to the auditing procedures applied in the audit of compliance and. accordingly, we express no opinion on the response.

Report on Internal Control Over Compliance Management of RNDG is responsible for establishing and maintaining effective intemal control over compliance with the types of compliance requirements referred to above. In planning and performing our audit of compliance, we considered RNDG's internal control over compliance with the types of requirements that could have a direct and material effect on its GDBG Program to determine the auditing procedures that are appropriate in the circumstances for the purpose of expressing an opinion on compliance for its GDBG Program and to test and report on internal control over compliance in accordance with 0MB Gircular A-133, but not for the purpose of expressing an opinion on the effectiveness of internal control over compliance. Accordingly, we do not express an opinion on the effectiveness of RNDG's internal control over compliance.

A deficiency in intemal control over compliance exists when the design or operation of a control over compliance does not allow management or employees, in the normal course of performing their assigned functions, to prevent, or detect and correct, noncompliance with a type of compliance requirement of a federal program on a timely basis. A material weakness in intemal control over compliance is a deficiency, or combination of deficiencies, in Internal control over compliance, such that there is a reasonable possibility that material noncompliance with a type of compliance requirement of a federal program will not be prevented, or detected and corrected, on a timely basis. A significant deficiency in internal control over compliance is a deficiency, or a combination of deficiencies, in internal control over compliance with a type of compliance requirement of a federal program that is less severe than a material weakness in internal control over compliance, yet important enough to merit attention by those charged with governance.

Our consideration of internal control over compliance was for the limited purpose described in the first paragraph of this section and was not designed to identify alt deficiencies in internal control over compliance that might be material weaknesses or significant deficiencies and, therefore, material weaknesses or significant deficiencies may exist that were not identified. We identified a certain deficiency in internal control over compliance, described in the accompanying schedule of findings and questioned costs as item 2015-001, that we consider to be a material weakness.

RNDG's response to the internal control over the compliance finding identified in our audit is described in the accompanying schedule of findings and questioned costs. RNDG's response was not subjected to the auditing procedures applied in the audit of compliance and, accordingly, we express no opinion on the response.

The purpose of this report on internal control over compliance is solely to describe the scope of our testing of internal control over compliance and the results of that testing based on the requirements of 0MB Circular A-133. Accordingly, this report is not suitable for any other purpose.

Under Louisiana Revised Statute 24:513, this report is distributed by the Louisiana Legislative Auditor as a public document.

A Professional Accounting Corporation

Metairie, LA September 29.2017

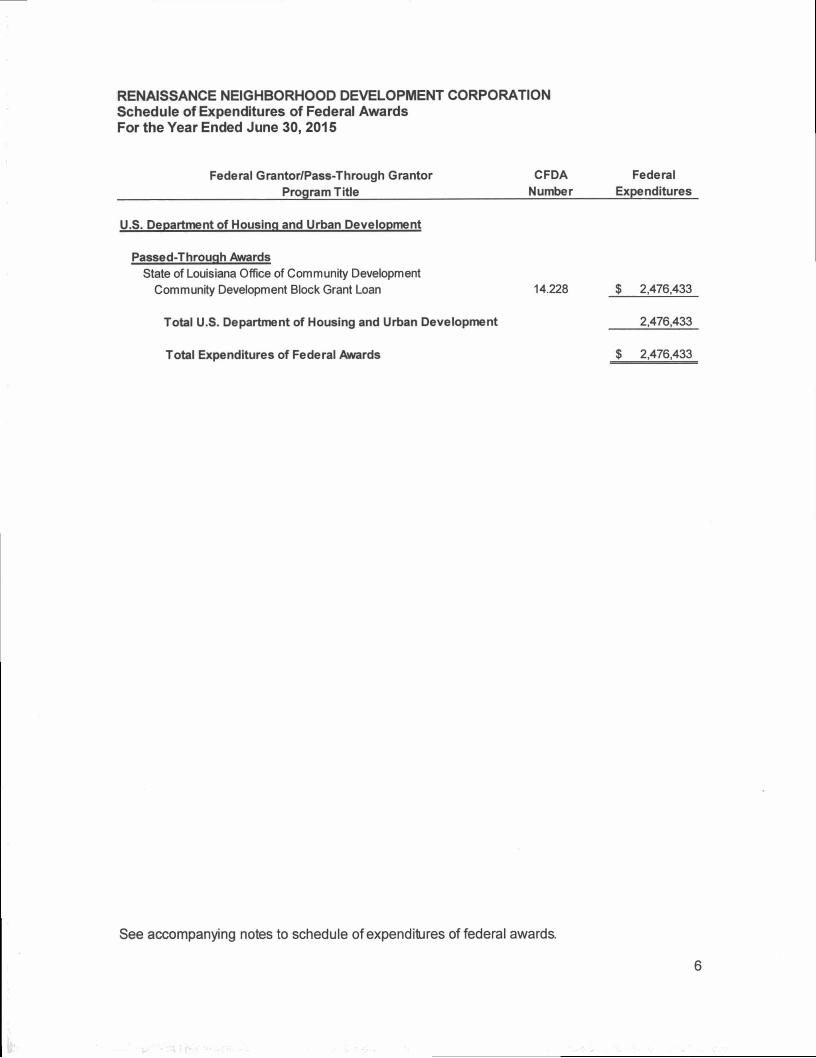

RENAISSANCE NEIGHBORHOOD DEVELOPMENT CORPORATION Schedule of Expenditures of Federal Awards For the Year Ended June 30, 2015

Federal Grantor/Pass-Through Grantor Program Title

CFDA Number

Federal Expenditures

U.S. Department of Housing and Urban Development

Passed-Throuqh Awards State of Louisiana Office of Community Development

Community Development Block Grant Loan

Total U.S. Department of Housing and Urban Development

Total Expenditures of Federal Awards

14.228 $ 2,476,433

2,476,433

$ 2,476,433

See accompanying notes to schedule of expenditures of federal awards.

RENAISSANCE NEIGHBORHOOD DEVELOPMENT CORPORATION

Notes to Schedule of Expenditures of Federal Awards

Note 1. Basis of Presentation

The accompanying schedule of expenditures of federal awards includes the federal grant activity of the Renaissance Neighborhood Development Corporation (RNDC) under programs of the federal government for the year ended June 30. 2015. The information in this schedule is presented in accordance with the requirements of the Office of Management and Budget (0MB) Circular A-133, Audits of States, Local Governments, and Non-Profit Organizations, Because the schedule presents only a selected portion of the operations of RNDC, it is not intended to and does not present the financial position, changes in net assets, or cash flows of RNDC.

Note 2. Summary of Significant Accounting Policies

Expenditures are reported on the schedule on the accrual basis of accounting and the cost accounting principles contained in 0MB Circular A-122, Cosf Principles for Nonprofit Organizations. Under these cost principles, certain types of expenditures are not allowable or are limited as to reimbursement. Expenditures for loan disbursements are recognized when paid.

Note 3. Sub-Recipients

There were no payments to sub-recipients for the fiscal year ended June 30, 2015.

Note 4. Loan Balance

In accordance with 2 CFR 200.502, the loan balance reported on the schedule of expenditures of federal awards represents the loan balance at the beginning of the year. As of June 30, 2015, the outstanding balance of this loan program is $2,382,735.

Note 5. Indirect Cost Rate

RNDC did not apply indirect costs to this program.

RENAISSANCE NEIGHBORHOOD DEVELOPMENT CORPORATION

Schedule of Findings and Questioned Costs For the Year Ended June 30, 2015

Section I - Summary of Auditor's Results

Financial Statements

Not Applicable

Federal Awards

Internal control over major programs:

• Material weaknesses identified? • Significant deficiencies identified not considered

to be material weaknesses?

Type of auditor's report issued on compliance for major program:

Audit findings disclosed that are required in accordance with Section 510(a) of 0MB Circular A-133?

Identification of major program:

CFDA Number Name of Federal Program 14.228 Community Development Block Grant (CDBG) Loan

Dollar threshold used to disti nguish between Type A and B programs:

Auditee qualified as a low-risk auditee?

Yes

None Reported

Unmodified

Yes

$500,000

No

Section II - Findings - Financial Statement Audit

None

RENAISSANCE NEIGHBORHOOD DEVELOPMENT CORPORATION

Schedule of Findings and Questioned Costs (Continued) For the Year Ended June 30, 2015

Section III - Findings and Questioned Costs - Major Federal Award Program Audit

2015-001 CDBG (CFDA 14.228)

Criteria:

Condition:

Effect:

Cause:

Recommendation:

Auditee Response:

Office of Management and Budget (0MB) Circular A-133, Audits of States, Local Governments, and Non-Profit Organizations, section .320, requires RNDC to submit its single audit reporting package to the Federal Audit Clearinghouse no later than nine months after fiscal year-end.

The federal reporting deadline for RNDC's single audit reporting package was March 31, 2016; however, RNDC did not issue its single audit reporting package by the required deadline.

RNDC was not in compliance with OMB Circular A-133, section .320.

RNDC's management was not aware of the reporting requirements. This contributed to the late submission of its single audit reporting package.

We recommend RNDC's management implement a process and internal controls to ensure submission of its single audit reporting package to the Federal Audit Clearinghouse by the reporting deadline.

RNDC was not aware of the reporting requirement related to our federal award. We have since made appropriate communication with whom we are to report to ensure timely reporting going forward and ensuring we are in compliance.

RENAISSANCE NEIGHBORHOOD DEVELOPMENT CORPORATION

Summary Schedule of Prior Audit Findings For the Year Ended June 30, 2015

Federal Award Findings and Questioned Costs

2014-001 CDBG (CFDA 14.228)

Condition: The federai reporting deadiine for RNDC's singie audit reporting package was March 31. 2015; however. RNDC did not issue its singie audit reporting package by the required deadline.

Status: Not resoived. See finding 2015-001.

10

k