LaingBuisson Healthcare Market Review · Iain Lock LaingBuisson Healthcare Market Review Market...

21

Presented by: Iain Lock LaingBuisson Healthcare Market Review Market Activity 2017- 2018

Transcript of LaingBuisson Healthcare Market Review · Iain Lock LaingBuisson Healthcare Market Review Market...

Presented by:Iain Lock

LaingBuisson Healthcare Market Review

Market Activity 2017- 2018

Birmingham

Bristol

Manchester

Iain Lock Senior Director

Head of Healthcare

Rob HearleDirector

Charlotte Brierley Associate

Luke O’DowdAssociate

Andrew Sidwell Senior Director

Adam BurchellDirector

Cirion Plant Director

Kate DeakinAssociate

Richard TaylorSenior Director

Frank Convery Director

Tom HarrisonDirector

Clare Horrocks Associate

London

2

The core healthcare team

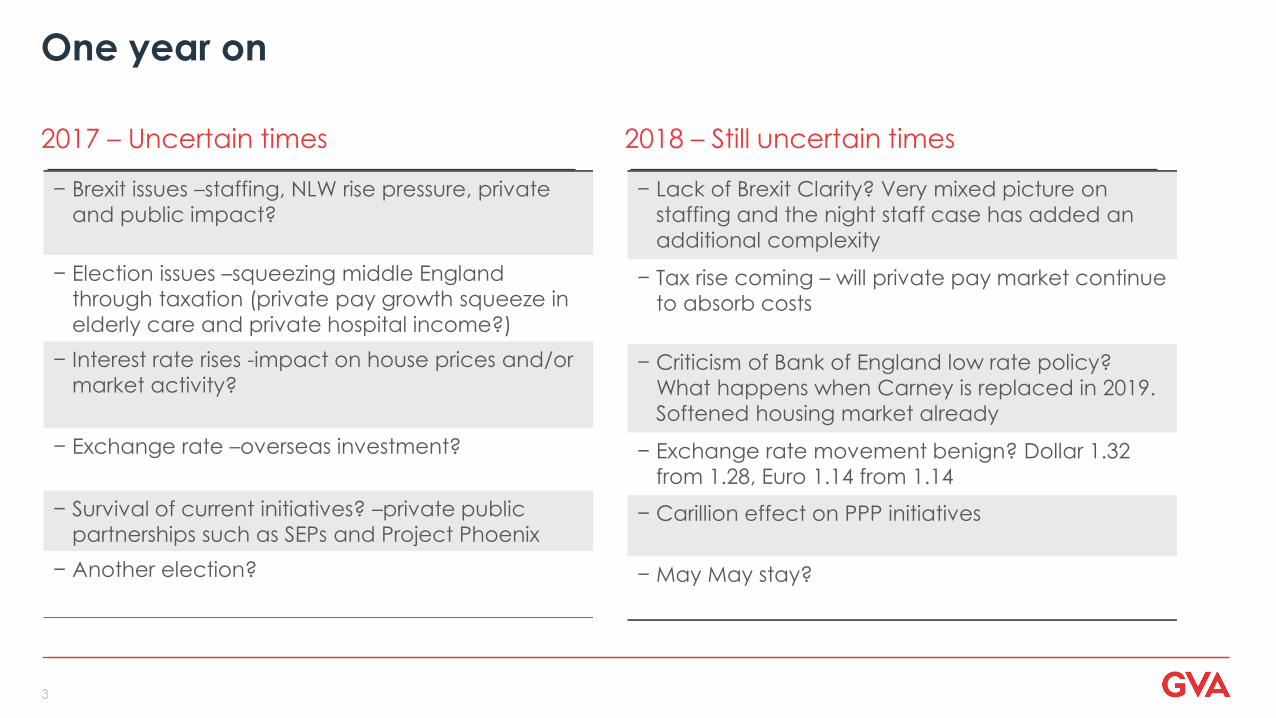

One year on

2017 – Uncertain times 2018 – Still uncertain times

3

− Brexit issues –staffing, NLW rise pressure, private

and public impact?

− Election issues –squeezing middle England

through taxation (private pay growth squeeze in

elderly care and private hospital income?)

− Interest rate rises -impact on house prices and/or

market activity?

− Exchange rate –overseas investment?

− Survival of current initiatives? –private public

partnerships such as SEPs and Project Phoenix

− Another election?

− Lack of Brexit Clarity? Very mixed picture on

staffing and the night staff case has added an

additional complexity

− Tax rise coming – will private pay market continue

to absorb costs

− Criticism of Bank of England low rate policy?

What happens when Carney is replaced in 2019.

Softened housing market already

− Exchange rate movement benign? Dollar 1.32

from 1.28, Euro 1.14 from 1.14

− Carillion effect on PPP initiatives

− May May stay?

Prediction comparison

2017 – what we might see Then and now

4

− De-risking? – Opportunity? Disposal strategies to

exit difficult assets and difficult trading

− Flight to quality –that could push prime yields

down, especially if exchange rates favour the US

REITs

− Flight to good/better value –always a strength of

the sector, could bolster good secondary values

− Scrum for covenant strength, including Govt.

backed income and not for profit operators

− Lease re-gearing to improve rent cover and

lengthen leases

− Invest to upgrade for competitive edge

− Reduce exposure to skilled nursing

− BUPA saw sales as a de-risk, Advinia and HC-One as

an opportunity

− A very active 2017/18 market has seen many deals

where quality and resilience are thought to apply.

Fund and PE entrants and merger and acquisition.

− Prime yields have, if anything, lowered a bit further.

Best healthcare covenants sub 4% NIY. Income strips

sub 3%. No depth to the market. Limited

opportunities.

− Landlords will only act when forced.

− On-going but limited examples. Much is struggling

on.

− Certainly there seems more interest in residential care

except where nursing fee levels are high.

Healthcare markets

5

Market Sector Land £

Build Cost (all in)

£

Turnkey Cost £ Value Mature £

Multiple of EBITDAR Mature

YP

NIY %

New Build Elderly

Prime55 -65k (per bed) 90 -110k (per bed)

BCIS 3.8% increase

145 -175k (per bed)

FF&E costs rising

200 -250k (per bed)

Porthaven effect?

10.0 -11.0

Possibly 12?

4.75 -5.50

Sub 4% for best

New Build Elderly

Secondary25 -35k (per bed) 80 -100k (per bed) 105 -145k (per bed) 125 -160k (per bed)

Limited evidence

9.0 -10.0 5.00 -6.00

Existing Elderly

Secondary - - - 40 -90k (per bed)

Upper end is rare

7.0 -9.0 5.50 -6.50

Specialist (LD, ABI)

Prime50k + or resi

values

80-125k (per bed) 150 –200k (per bed) 200k + (per bed) 8.0 –12.0 6.00 –7.00

Private Hospitals 1.0m -2.0m (per

acre)

2,400 -3,250

(psmGIA)

- - 8.0 –12.0 4.00 -6.00

Primary Care 200k -1.0m+ (per

acre)

2,000/2,400

(psmGIA)

2,800/3,500 (psm GIA) 3,750 (psm NIA -Regions)

6,300 (psm NIA -London)

4.25 -5.50

Retirement Housing

with Care540 -1,100

(psmGIA)

2,150 -2,700 (psm

GIA)

2,700 -3,750 (psm GIA) - - -

June 2017 – June 2018

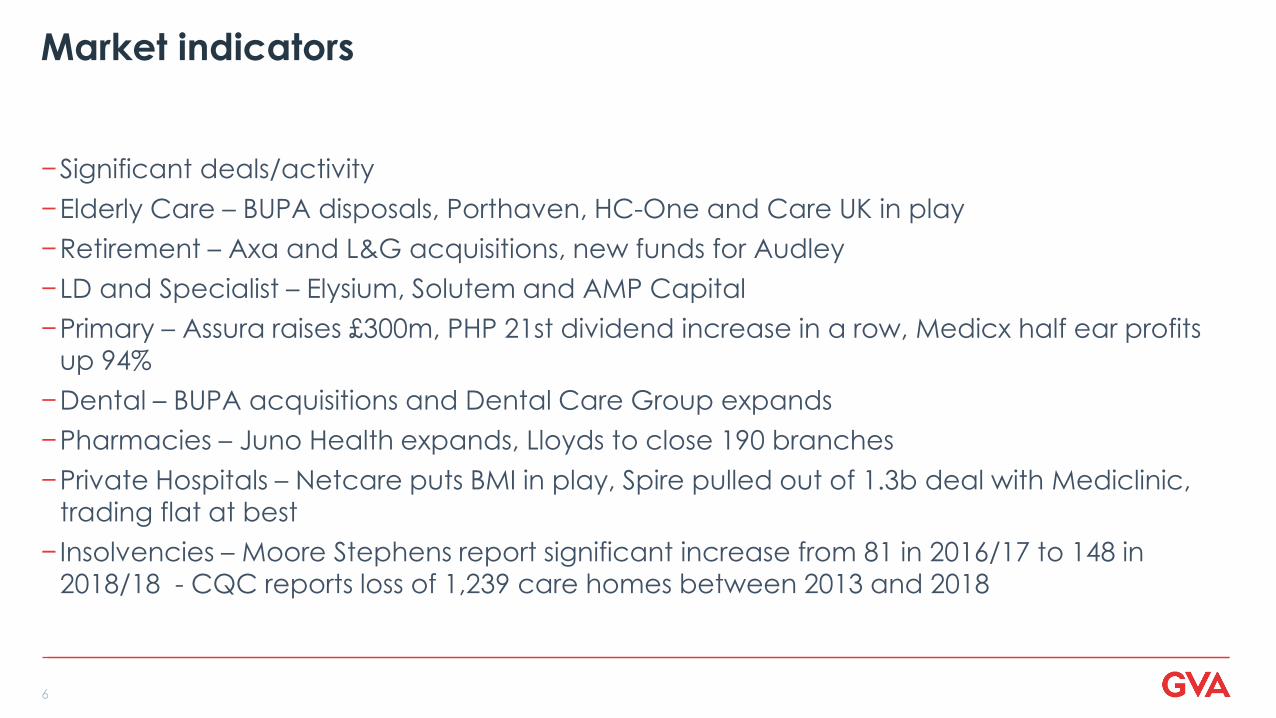

Market indicators

−Significant deals/activity

−Elderly Care – BUPA disposals, Porthaven, HC-One and Care UK in play

−Retirement – Axa and L&G acquisitions, new funds for Audley

−LD and Specialist – Elysium, Solutem and AMP Capital

−Primary – Assura raises £300m, PHP 21st dividend increase in a row, Medicx half ear profits up 94%

−Dental – BUPA acquisitions and Dental Care Group expands

−Pharmacies – Juno Health expands, Lloyds to close 190 branches

−Private Hospitals – Netcare puts BMI in play, Spire pulled out of 1.3b deal with Mediclinic,

trading flat at best

− Insolvencies – Moore Stephens report significant increase from 81 in 2016/17 to 148 in 2018/18 - CQC reports loss of 1,239 care homes between 2013 and 2018

6

2018 - 2019

−More poor stock insolvencies – and more care homes out of the system

−Serious initial interest in scale such as HC-One and Care UK – then the DD on quality?

−Growing interest in healthcare prime in line with all “alternatives” but difficult to see further

significant value growth

−PE interest to continue in highly attractive specialist care subsectors away from elderly

−Continued worries over LA funding levels and increased concern over the robustness of

private markets and fee growth

−Build costs to continue to rise – but will land pricing soften?

−Planning to remain difficult and consented sites to attract premium pricing

−Retirement village tenure and DMF structures to slowly evolve

−Continued and growing interest in dentistry

−A continued difficult trading market for private hospitals

7

What we might see

Presented by:Primary care market update Frank Convery

The Case for new surgeries

9

Small Buildings, poor layout, poor Equality Act compliance

NHS 5 year forward view – enhanced services, 7 day opening

10

Non Compliant Sinks Small Consulting Rooms

The NHS must invest in its estate and equip itself for the task

11

12

13

14

GVA primary care development projects

15

Kingsway Surgery

Glos

St Augustine’s Surgery

KeynshamMarksbury Road Surgery

Bristol

Hadwen Surgery

GlosPenzance Primary

Care Centre Trowbridge Primary Care

Centre

Prospects for rental growth

16

− New schemes showing need for rental growth

− Reviews being based on established historical evidence

− Construction cost inflation – overdue acceleration in rental growth

− Rental Growth – Greater London, South East and major Conurbations

Strong investment market

17

− GP Surgeries – a Niche Specialist Asset Class

− Strong demand but weak supply

− Lack of development pipeline

− Yield compression below 2007 peak

− Growth of Sale and Leaseback

− Over priced secondary stock

− Ireland Investment Opportunities

Sale and leaseback

18

Montgomery The Valleys Fleetwood

West Wales Taunton Somerset

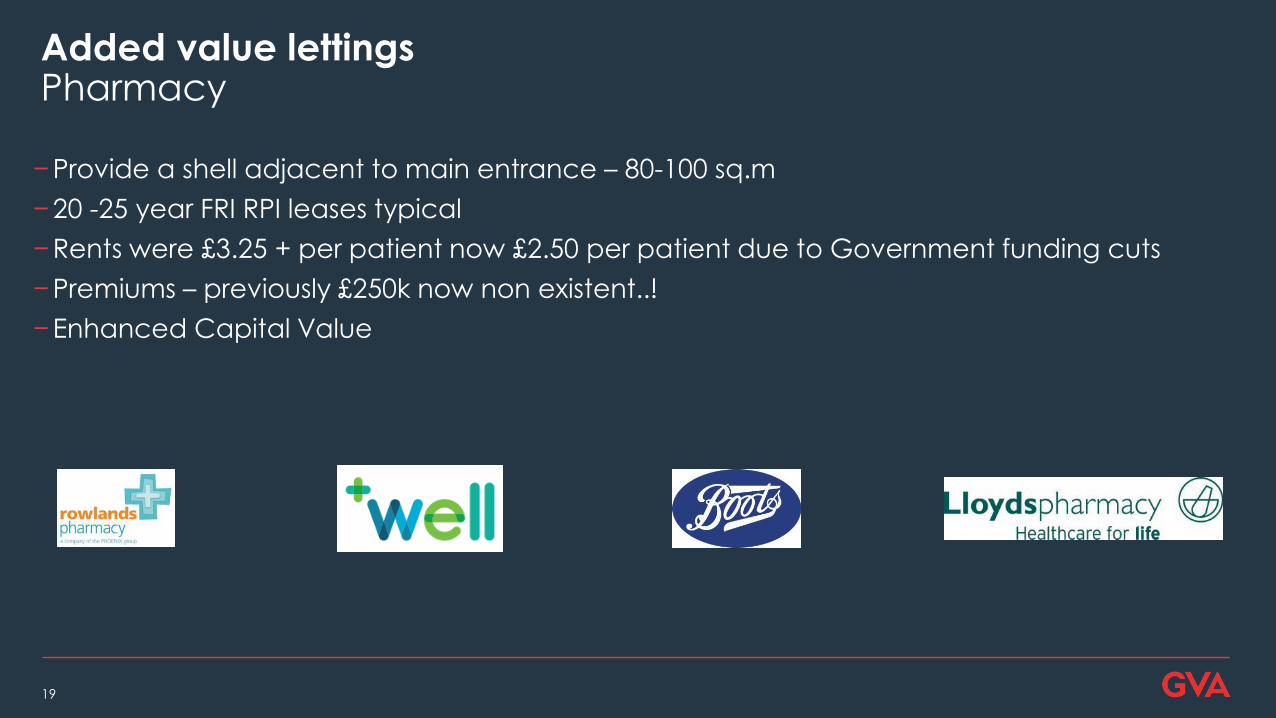

Added value lettingsPharmacy

19

−Provide a shell adjacent to main entrance – 80-100 sq.m

−20 -25 year FRI RPI leases typical

−Rents were £3.25 + per patient now £2.50 per patient due to Government funding cuts

−Premiums – previously £250k now non existent..!

−Enhanced Capital Value

Conclusions

20

−GP Surgeries now recognised as a niche specialist asset class

− Investment Returns outperforming other sectors

− Rising Values but have surgery values peaked?

−Prospects for Rental growth

−Pharmacy Rents falling

Presented by

GVA

GVA is the trading name of GVA Grimley Limited. ©2018 GVA

Iain Lock

Head of Healthcare

0207 911 2603

Thank you

Frank Convery

Director

0117 988 5255