Lagos State Government of Nigeria - Nigeria’s No1 ... · Nigeria Local Authority Analysis |...

12

Nigeria Local Authority Analysis | Public Rating Lagos State Government of Nigeria Nigeria Local Authority Analysis August 2016 Summary rating rationale Lagos is the economic hub of Nigeria, housing a significant number of commercial establishments and manufacturing companies. The economy is the most diversified in the country, and continues to expand, with significant capital injection helping to deliver needed infrastructure, and providing opportunities for job creation. Resulting from the combined declines to both statutory receipts and Internally Generated Revenue (“IGR”), total revenue declined for the first time over the five-year review period by 6% to N384.4bn in F15 (82% of budget). While the N14.6bn decrease in statutory receipts to a six-year low of N43.8bn was attributed directly to the sustained fall in the global oil price, IGR (inclusive of VAT receipts) also dipped to N340.6bn (F14: N349.7bn) attributed to the slowing of the economy. After accounting for slightly lower expenditure of N240.3bn, and with debt service charges falling by 12% to N49.7bn, the State reported an operating surplus before debt service charge of N193.5bn, which covered debt service charges by an unchanged 3.9x. Following these charges, the operating surplus of N143.8bn equated to a reduced 37.4% operating margin (F14: 40.5%). Although, capex spend remained high in F15, it fell to a six-year low of N174bn, attributed to lower than expected surplus, which was further exacerbated by disbursement constraints, following the change in government. Capex has been facilitated by a large component of borrowings. Specifically, Lagos State reported a N38.2bn rise in debt to a new high of N619.3bn at FYE15. As a consequence, gross and net debt to total revenue increased further to 161% and 124% respectively. Nevertheless, Global Credit Rating Company Limited (“GCR”) takes note of the funds being transferred to the Sinking Fund [via the Consolidated Debt Service Account (“CDSA”) and Irrevocable Standing Payment Order (“ISPO”)] to ensure sufficient funding for the repayment of principal and interest on the existing bonds. Accordingly, gross debt is moderated by the N120.5bn in cash in the debt service account at FYE15, maintained to meet interest and principal repayment on the bonds as they fall due. With Cash holdings peaking at N144.1bn at FYE15 (FYE14: N128.4bn), days cash on hand rose to 219 days (F14: 193 days). However, if funds in the Sinking Fund Account were stripped out of cash holdings, days cash on hand would significantly decline to 36 days, well below GCR’s 90-day benchmark. The finances of many States (excluding Lagos) have been severely impacted by the decline in statutory receipts, worsened by their low levels of IGR and high expense ratio. In order to reduce the current strain on those States, the Federal government established a new N90bn credit facility to be accessed upon meeting 22 stringent conditions. Factors that could trigger a rating action may include Positive change: An upgrade is unlikely in the short term given the generally challenging economic environment and especially the reduced capacity of the federal government to support States in need. Negative change: Revenue underperformance combined with higher than expected debt could place pressure on the State’s ratings. Security class Rating scale Rating Rating outlook Expiry date Issuer rating National A+(NG) Stable July 2017 Programme 1 - Series 2: N57.5bn Fixed Rate Bond National A+(NG) Programme 2 - Series 1: N80bn Fixed Rate Bond National AA-(NG Programme 2 - Series 2: N87.5bn Fixed Rate Bond National AA-(NG Summary of bond programme: Total programme value: N275,000,000,000 (Programme 1 lapsed, 2010) N167,500,000,000 (Programme 2- lapsed, 2014) Instruments: Various – Bonds were issued at different fixed coupon rates. Coupon rate: Series specific. Maturity: Series specific. Status of bonds: Bonds are direct, unsecured & general obligations of the State i.e. ranking pari passu with other senior unsecured obligations. Key transaction counterparties: Issuer: Lagos State Government of Nigeria Joint Trustees: FBN Trustees Ltd, STL Trustees Ltd, United Capital Trustees Ltd, Union Trustees Ltd, CSL Trustees Ltd, Sterling Trustees Ltd, Radix Trustees Ltd. Registrars: First Registrars & Investors Services Limited Rating methodologies/research: Criteria for rating Public Entities, February 2016 Lagos State Government (“Lagos State”, “Lagos”, “the State”) rating reports 2011- 2015, Glossary of Terms/Ratios (February 2015) Rating history: Initial Rating (September 2011) Issuer Rating: A(NG Programme 1 - Series 1: A(NG) Programme 1 - Series 2: A(NG) Rating outlook: Stable Last Rating (July 2015) Issuer Rating: A+(NG) Programme 1 - Series 2: A+(NG) Programme 2 - Series 1: AA-(NG) Programme 2 - Series 2: AA-(NG) Rating outlook: Negative GCR contacts: Primary Analyst: Kunle Ogundijo Credit Analyst [email protected] Committee Chairperson: Dave King [email protected] Analyst Location: Lagos, Nigeria +23 41 462-2545 Website: http://www.globalratings.com.ng

Transcript of Lagos State Government of Nigeria - Nigeria’s No1 ... · Nigeria Local Authority Analysis |...

Nigeria Local Authority Analysis | Public Rating

Lagos State Government of Nigeria Nigeria Local Authority Analysis August 2016

Summary rating rationale

Lagos is the economic hub of Nigeria, housing a significant number of commercial establishments and manufacturing companies. The economy is the most diversified in the country, and continues to expand, with significant capital injection helping to deliver needed infrastructure, and providing opportunities for job creation.

Resulting from the combined declines to both statutory receipts and Internally Generated Revenue (“IGR”), total revenue declined for the first time over the five-year review period by 6% to N384.4bn in F15 (82% of budget). While the N14.6bn decrease in statutory receipts to a six-year low of N43.8bn was attributed directly to the sustained fall in the global oil price, IGR (inclusive of VAT receipts) also dipped to N340.6bn (F14: N349.7bn) attributed to the slowing of the economy.

After accounting for slightly lower expenditure of N240.3bn, and with debt service charges falling by 12% to N49.7bn, the State reported an operating surplus before debt service charge of N193.5bn, which covered debt service charges by an unchanged 3.9x. Following these charges, the operating surplus of N143.8bn equated to a reduced 37.4% operating margin (F14: 40.5%).

Although, capex spend remained high in F15, it fell to a six-year low of N174bn, attributed to lower than expected surplus, which was further exacerbated by disbursement constraints, following the change in government.

Capex has been facilitated by a large component of borrowings. Specifically, Lagos State reported a N38.2bn rise in debt to a new high of N619.3bn at FYE15. As a consequence, gross and net debt to total revenue increased further to 161% and 124% respectively.

Nevertheless, Global Credit Rating Company Limited (“GCR”) takes note of the funds being transferred to the Sinking Fund [via the Consolidated Debt Service Account (“CDSA”) and Irrevocable Standing Payment Order (“ISPO”)] to ensure sufficient funding for the repayment of principal and interest on the existing bonds. Accordingly, gross debt is moderated by the N120.5bn in cash in the debt service account at FYE15, maintained to meet interest and principal repayment on the bonds as they fall due.

With Cash holdings peaking at N144.1bn at FYE15 (FYE14: N128.4bn), days cash on hand rose to 219 days (F14: 193 days). However, if funds in the Sinking Fund Account were stripped out of cash holdings, days cash on hand would significantly decline to 36 days, well below GCR’s 90-day benchmark.

The finances of many States (excluding Lagos) have been severely impacted by the decline in statutory receipts, worsened by their low levels of IGR and high expense ratio. In order to reduce the current strain on those States, the Federal government established a new N90bn credit facility to be accessed upon meeting 22 stringent conditions.

Factors that could trigger a rating action may include

Positive change: An upgrade is unlikely in the short term given the generally challenging economic environment and especially the reduced capacity of the federal government to support States in need.

Negative change: Revenue underperformance combined with higher than expected debt could place pressure on the State’s ratings.

Security class Rating scale Rating Rating outlook Expiry date Issuer rating National A+(NG)

Stable

July 2017

Programme 1 - Series 2: N57.5bn Fixed Rate Bond National A+(NG) Programme 2 - Series 1: N80bn Fixed Rate Bond National AA-(NG Programme 2 - Series 2: N87.5bn Fixed Rate Bond National AA-(NG

Summary of bond programme: Total programme value: N275,000,000,000 (Programme 1 lapsed, 2010) N167,500,000,000 (Programme 2- lapsed, 2014) Instruments: Various – Bonds were issued at different fixed coupon rates. Coupon rate: Series specific. Maturity: Series specific. Status of bonds: Bonds are direct, unsecured & general obligations of the State i.e. ranking pari passu with other senior unsecured obligations.

Key transaction counterparties: Issuer: Lagos State Government of Nigeria Joint Trustees: FBN Trustees Ltd, STL Trustees Ltd, United Capital Trustees Ltd, Union Trustees Ltd, CSL Trustees Ltd, Sterling Trustees Ltd, Radix Trustees Ltd.

Registrars: First Registrars & Investors Services Limited Rating methodologies/research: Criteria for rating Public Entities, February 2016 Lagos State Government (“Lagos State”, “Lagos”, “the State”) rating reports 2011-2015, Glossary of Terms/Ratios (February 2015)

Rating history: Initial Rating (September 2011) Issuer Rating: A(NG Programme 1 - Series 1: A(NG) Programme 1 - Series 2: A(NG) Rating outlook: Stable Last Rating (July 2015) Issuer Rating: A+(NG) Programme 1 - Series 2: A+(NG) Programme 2 - Series 1: AA-(NG) Programme 2 - Series 2: AA-(NG)

Rating outlook: Negative GCR contacts: Primary Analyst: Kunle Ogundijo Credit Analyst [email protected]

Committee Chairperson: Dave King [email protected]

Analyst Location: Lagos, Nigeria +23 41 462-2545 Website: http://www.globalratings.com.ng

Nigeria Local Authority Analysis | Public Rating Page 2

Background on Lagos State

Lagos State was created in 1967 and consists of five administrative divisions, which are further divided into 20 local government areas and 37 local council development areas, all under 3 senatorial districts. The capital city is Ikeja, other major cities include Surulere, Lagos Island, Agege and Lekki among others. The State is located in the South-western part of Nigeria, bounded by Ogun State to the North and East, Benin Republic to the West and the Atlantic Ocean to the South. With a land mass of 3,577km2, the State is the smallest in the country but it is the most densely populated, housing around 5% of the Nigerian population. The State has witnessed significant infrastructural development in recent years, further expanding economic activities and diversifying revenue sources. Lagos is the economic hub of Nigeria, housing a significant number of commercial establishments and over 2,000 manufacturing companies. The two major sea ports; Tin-Can and Apapa port account for over half of the Nation’s revenue from port services. Lagos State’s Gross Domestic Product (“GDP”) in 2015 amounted to USD128bn (making it one of the largest economies in Africa on a standalone basis).

Programmes 1 & 2 –bond issuance programme

Lagos State has consistently relied on the Nigerian capital market to raise funds to accelerate development. Since 2009, it has successfully undertaken two bond programmes and issued four fixed rate bonds. After fully settling the initial N50bn bond upon maturity in 2014 and with another bond nearing maturity in 2017, the State is in the process of issuing new bonds into the market. A preliminary filing has been carried out at the Securities and Exchange Commission (“SEC”) to issue bonds up to a total of N60bn (in series 1), under a new N500bn programme. Details of existing bond programmes are provided in table 1;

Table 1: Lagos State Fixed Rate Bond Programmes Programme Series Rate Tenor Maturity I - N275bn* N50bn Series 1 13 5 Redeemed N57.5bn Series 2 10 7 2017

II - N167bn* N80bn Series 1 14.5 7 2019 N87.5bn Series 2 13.5 7 2020

*Lapsed

Some key features of the Programmes include: Each series issued is listed on The Nigeria Stock Exchange (“NSE”).

The bonds bear a negative pledge; whereby, as long as any of the bonds remain outstanding and unpaid (including unpaid interest where applicable), the State will not cause or permit to be created, any mortgage or other charge of security for borrowings of more than 1 year (unless the bonds under this programme rank pari passu with the new secured borrowings in regard to the secured charge).

Repayment of interest and principal on the bonds issued is funded with contributions from an ISPO1 and the Consolidated Debt Service Account2.

A Sinking Fund (as provided in the Trust Deed and managed by the Trustees) has been established to ensure that cash is sufficient for principal repayment.

Municipal bonds are exempt from taxation in Nigeria.

As the ratings accorded under the debt issuance programmes are linked to the unsecured domestic Naira rating accorded to Lagos State, the focus of this report is on the operating and economic environment in which the State functions, as well as the financial performance and profile of the State. Unique rating considerations for the existing bond issuances are detailed in the final section of this report.

Political considerations

Political and legislative framework Under the federal system, there are 3 tiers of government, namely the Federal, State and Local governments. The fiscal decentralisation model in place is aimed at empowering the lower tiers of government. Each tier is responsible for the provision of various government services and has the authority to collect and retain revenues under their respective jurisdictions. The major areas of jurisdiction and sources of revenue currently available to the Federal and State Governments, as well as their respective obligations, are tabulated below.

Table 2: Federal and State government duties and revenue sources Federal government State government

Duties Housing Local Government creation Currency & external affairs Legislature Legislature Education Security Housing Electricity supply Water & electricity supply Infrast. expansion & maintenance Road construction & maintenance Distributions to State & Local Gov. Health

Revenue sources Company tax Federal account Oil sales Personal income tax* Value Added Tax (“VAT”) VAT allocation Mineral royalties & rents Derivation income Duties Licences and fees*

*Collected by States. Other revenues collected & held in trust by the FGN.

It is noted that revenue allocations between the Federal, State and Local Governments change from time-to-time. In this regard, 15% of VAT is retained by the Federal Government of Nigeria (“FGN”), whilst State and Local Governments are apportioned the remaining 50% and 35% respectively. In terms of federally allocated revenues (excluding VAT), as it currently stands: 52.68% is allocated to the Federal Government, 26.72% to the States and 20.6% to the Local Government Areas. A further 1% each is directed towards the Federal Capital Territory and Ecological Fund. In addition, mineral producing states receive a 13% derivation from the FGN. By law, all activities

1An ISPO is issued by the Ministry of Finance and represents a first line charge on federally allocated funds. 2The Consolidated Debt Services Account is being funded through monthly transfers (around 15%) from the IGR. Such monies are administered by the CDSA Trustees in accordance with the Trust Deed.

BC

Nigeria Local Authority Analysis | Public Rating Page 3

that relate to mining/exploration of mineral resources in commercial quantity fall under the purview of the FGN, with proceeds distributed among the federating units under a sharing arrangement.

Administration and corporate governance The affairs of the State are managed by an elected governor and an executive council, which is comprised of appointed commissioners manning various ministries, departments and agencies. Other arms of government include the Legislature (i.e. the Lagos State House of Assembly), which is responsible for passing State-specific laws. The Judiciary serves as the third arm of government, interpreting and adjudicating on disputes, and is headed by the Chief Judge. Activities of the State are governed under the 1999 Constitution of the Federal Republic of Nigeria.

The financial statements of Lagos State have been prepared in accordance with the provisions of the amended Finance (Control and Management) Act 1958 Cap 144 LFN. The Accountant-General is responsible for the preparation and presentation of the financial statements, thereafter, it is the statutory responsibility of the Auditor General to form an independent opinion based on the audit of the financial statements as provided under section 125(5) of the constitution

Lagos State’s financial statements are in compliance with Nigeria’s Generally Accepted Accounting Principles and Practices, and other government-prescribed accounting regulations and principles. Further to this, GCR’s rating of the State is based on audited financials for the five years to 2015, in respect of which the Auditor-General issued an unqualified opinion.

The impact of economics The FGN is responsible for the allocation of revenue (accruing to the country) among the various tiers of government. As most States have low levels of internally generated revenue (particularly the smaller States), they remain heavily dependent on federal receipts for financial sustenance.

At the same time, the State governments have been tasked with stimulating economic activity within their jurisdictions and attending to the substantial social development requirements. This has led to high operating costs structures, which have been exacerbated by the ongoing decentralisation of responsibilities. To help meet their infrastructure requirements, about eighteen States were given approval to raise funding from capital markets to be invested in economic development projects. Most of these issuances were secured by ISPOs, providing lenders with first rights to repayment directly from transfers form the FGN.

This mechanism proved a successful means for States to access new capital, but as the fiscal position of the FGN has deteriorated due to the severe decline in oil revenues, shortfalls in the system have arisen. This has resulted in a similar decline in statutory transfers to the State Governments. While the performance of the

bonds has not been impacted, due to their priority of payment from the FGN transfers, this has left very little funding available for States to meet ongoing operational requirements. In addition, as most of the projects to which the borrowed funds have been applied are long term in nature, they have not yielded tangible benefits in terms of increased taxes and other revenue. Accordingly, many States have been unable to effectively finance recurrent expenditure over the last year, demonstrated by their inability to pay workers’ salaries and pensions and other unsecured creditors on time.

As the FGN has ultimate responsibility for the financial wellbeing of the States, in mid-2015 the FG established a financial package to support States. Key among the intervention measures to Sates have been a cash bailout and restructuring of commercial debt obligations. However, as monthly allocation from FGN remain low, due to the national fiscal constraints, the position of State governments is also very weak. Accordingly, the FGN has established a new N90bn credit facility, which will carry a concessionary interest rate of just 9%, compared to over 20% available in the market. However, for States to qualify for access they have to meet 22 stringent conditions, primarily aimed at fostering greater transparency and accountability in their financial transactions. Key conditions listed are detailed in the box below.

Notwithstanding the above, cognisance is taken that Lagos State is financially independent of the FG, given that its income is dominated by internally generated revenue sources.

Economic environment

With crude oil receipts representing c.75% of the Nigerian Federal Government budgetary revenues, the sustained decline in crude oil prices (since 3Q F14) has severely affected government finances at both Federal and State levels. Nevertheless, consistent growth reported in the non-oil sector has served to cushion the impact of reduced revenue from oil on the economy. Preliminary data released by the Statistics Bureau indicates a slower Gross Domestic Product (“GDP”)

An overview of conditions set to access new N90bn credit facility Publication of audited annual financial statements within nine

months of financial year end. Online publication of State budgets annually and quarterly

publication of budget implementation performance report. Establish a capital development fund to ring-fence capital receipts

and adopt accounting policies to ensure that capital receipts are strictly applied to capital projects.

Enact the Fiscal Responsibility Act, complying with its requirements and reporting obligations, including; No commercial bank loans to be undertaken by States and Routine submission of updated debt profile report to the Debt Management Office.

Set realistic and achievable targets to improve independently generated revenue (from all revenue generating activities of the state in addition to tax collections) and ratio of capital to recurrent expenditure.

Set limits on personnel expenditure as a share of total budgeted expenditure, and also establish an efficiency unit.

Obtaining and maintaining a credit rating; among others.

Nigeria Local Authority Analysis | Public Rating Page 4

growth of 2.8% in 2015, compared with over 5% growth reported through the last decade.

With the decline in forex receipts significantly impacting external reserves, the Central Bank of Nigeria (“CBN”) implemented a more restrictive foreign exchange policy that denied access to foreign currency (from the official CBN window) for forty-one items. The aim of this was to ensure efficient currency utilisation, conserve foreign reserves and resuscitate domestic industries. Despite these interventions, the currency remained under pressure, with the inadequate forex from the official CBN window driving much weaker exchange rates on the parallel market. More significantly, the forex restrictions further dampened economic activity as many foreign operators withdrew from the Nigerian market due to inability to source currency for imports, or to expatriate their profits.

In order to mitigate forex shortages and stimulate economic activity, CBN jettisoned the exchange rate peg to the USD in favour of a flexible exchange rate policy (June 2016), expected to facilitate a more liquid and efficient forex market. The market driven exchange rate will bridge the gap between the official and parallel market trading rates, improving efficiency in planning and resource allocation. While the new policy has resulted in further devaluation of the Naira to around USD/N290 (from USD/N197), it could lead to a resuscitation in local manufacturing (as imports have become more expensive) and higher foreign inflow from investors. The introduction of the futures market would also enable hedging against variability. Overall, while the implementation of the new policy has seen an increase in liquidity, enabling increased access to forex (albeit, at a higher rate), scarcity still persists with rates rising as high as USD/N370 at the parallel market.

Scarcity and currency devaluation has led to rising prices for goods and other consumables in recent months, as manufacturers passed on the higher production costs. Accordingly, inflation has trended above the 9% CBN benchmark, reaching a six-year high of 16.5% in June 2016, from 15.6% in April (9.6% in January 2016), further exacerbated by increased electricity rates and energy costs (resulting from the 68% increase in the pump price of petrol).

Notwithstanding the current macroeconomic challenges, prospects for growth remain mixed over the short to medium term. While the relatively stable political environment, strong investor confidence and the fast growing youthful urban population portends future growth, the impact of reduced revenue on government spending and weakness of the Naira could delay the massive infrastructural projects being planned. Furthermore, the country faces significant challenges in building a stable business environment, given the weak nature of institutions and governance structures.

Income and expenditure

A 5-year historical financial synopsis is reflected at the end of this report and brief comment follows hereafter. The financial statements are based on the Audited Financial Statement for the years 2011-2015 These statements are prepared using the cash basis of accounting and are divided into distinct operating and capital income/expenditure statements. The Auditor General of Lagos State gave an unqualified audit opinion on the results for F15.

In the face of challenges in the operating environment, occasioned by liquidity constraints and scarcity in foreign exchange, Lagos State’s economy has remained resolute, supported by an organised tax collection system, improved infrastructure and increasing efficiency across the various government institutions. The diversified stream of revenues from taxes has provided a base for accelerating development (in all facets), including critical infrastructure, thus, creating an enabling environment for businesses to thrive within the State. In this regard, while most States have struggled to effectively meet their obligations, as a result of dwindling allocations from the FGN, collections from taxes and other IGRs have been sufficient to effectively meet Lagos’ recurrent expenditure and other capex requirements. Notwithstanding this, Lagos’ financial performance could not fully withstand the economic environment, as total revenue declined by N23.7bn to N384.4bn in F15 (82% of F15 budget). Of the decline, N14.6bn was the result of lower statutory receipts, in line with the lower transfers form the FGN across all States. Lagos also saw IGR (inclusive of VAT receipts) dip to N340.6bn (F14: N349.7bn), as a result of the slowing of the economy.

Table 3: Operating cash flow (N’m) Actual Budget F15

% achieved F14 F15

Total IGR 349,739 340,643 414,013 82.3 Statutory allocation 58,383 43,768 54,000 81.1 Total recurrent inc. 408,123 384,411 468,013 82.1 Personnel costs (78,815) (91,019) (100,839) 90 Overhead costs (160,739) (146,622) (137,994) 106 Consol. rev. charges (254) (197) (259) 76 Grants & subvention (3,087) (2,801) (2,884) 97 Total recurrent exp. (242,895) (240,639) (241,977) 99.4 Operating surplus 165,228 143,772 226,036 63.6 Other capital rec. 28,298 28,986 21,677 133.7 Borrowings/bonds 104,924 150,879 90,818 166.1 Special funds 7,098 14,569 - n.a. Capital expenditure (213,140) (173,987) (247,713) 70.2 Acq./dim in assets (7,093) (14,465) - n.a. Facility repayments (89,051) (134,053) (90,818) 147.6 Cash & equiv. (3,736) 15,702 0 n.a.

Cash bal. (begin) 132,112 128,376 n.a n.a. Cash bal. (end) 128,376 144,078 n.a n.a.

As has become the trend over recent years, income tax receipts have increasingly underpinned funding, amounting to a relatively unchanged N212.2bn in F15 (compared to just N32.5bn in F05). An analysis of income tax receipts reveals some concentration risk to the oil and gas sector workers, with the top five tax payers in the industry accounting for 16% of tax receipts, while the top five tax payers in the financial

Nigeria Local Authority Analysis | Public Rating Page 5

institution industry accounted for 8%. Overall, the top ten individual contributors (six oil and gas companies and four financial institutions) accounted for 25% of tax receipts/15% of total IGR. Contribution from other sectors, including telecommunications, construction, public service and the expanding informal sector remain sizeable, with growth prospects expected following ongoing diversification efforts.

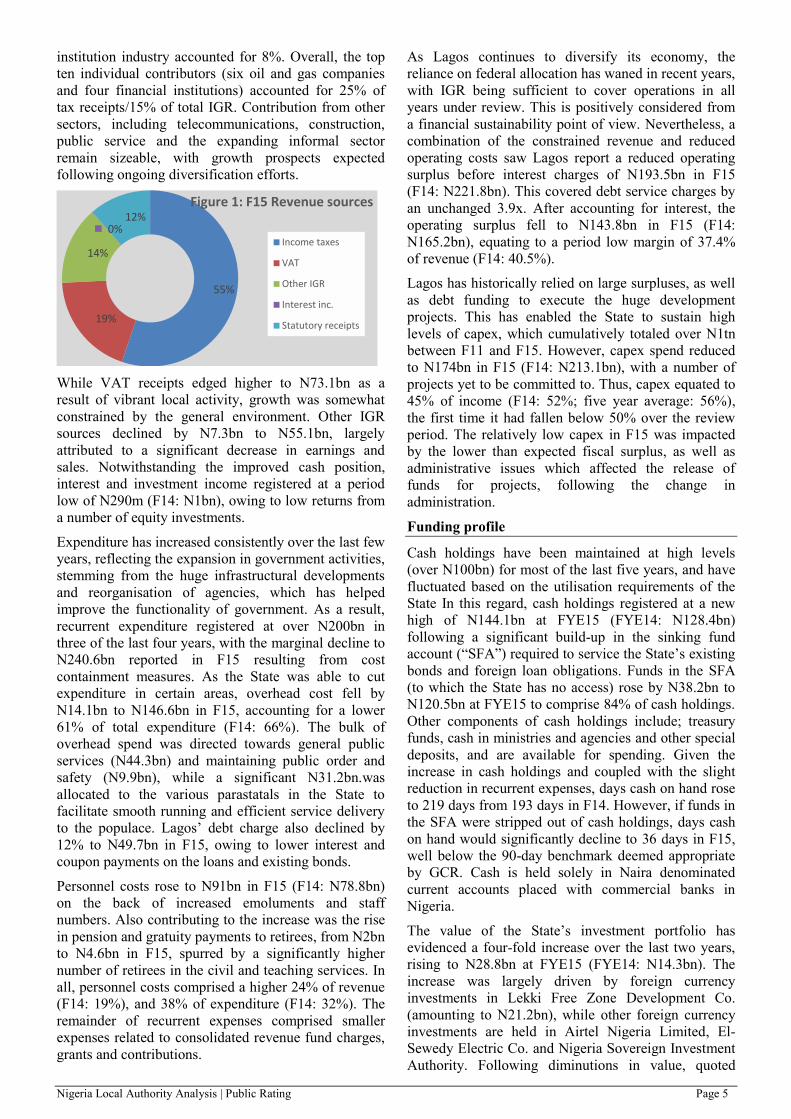

While VAT receipts edged higher to N73.1bn as a result of vibrant local activity, growth was somewhat constrained by the general environment. Other IGR sources declined by N7.3bn to N55.1bn, largely attributed to a significant decrease in earnings and sales. Notwithstanding the improved cash position, interest and investment income registered at a period low of N290m (F14: N1bn), owing to low returns from a number of equity investments.

Expenditure has increased consistently over the last few years, reflecting the expansion in government activities, stemming from the huge infrastructural developments and reorganisation of agencies, which has helped improve the functionality of government. As a result, recurrent expenditure registered at over N200bn in three of the last four years, with the marginal decline to N240.6bn reported in F15 resulting from cost containment measures. As the State was able to cut expenditure in certain areas, overhead cost fell by N14.1bn to N146.6bn in F15, accounting for a lower 61% of total expenditure (F14: 66%). The bulk of overhead spend was directed towards general public services (N44.3bn) and maintaining public order and safety (N9.9bn), while a significant N31.2bn.was allocated to the various parastatals in the State to facilitate smooth running and efficient service delivery to the populace. Lagos’ debt charge also declined by 12% to N49.7bn in F15, owing to lower interest and coupon payments on the loans and existing bonds.

Personnel costs rose to N91bn in F15 (F14: N78.8bn) on the back of increased emoluments and staff numbers. Also contributing to the increase was the rise in pension and gratuity payments to retirees, from N2bn to N4.6bn in F15, spurred by a significantly higher number of retirees in the civil and teaching services. In all, personnel costs comprised a higher 24% of revenue (F14: 19%), and 38% of expenditure (F14: 32%). The remainder of recurrent expenses comprised smaller expenses related to consolidated revenue fund charges, grants and contributions.

As Lagos continues to diversify its economy, the reliance on federal allocation has waned in recent years, with IGR being sufficient to cover operations in all years under review. This is positively considered from a financial sustainability point of view. Nevertheless, a combination of the constrained revenue and reduced operating costs saw Lagos report a reduced operating surplus before interest charges of N193.5bn in F15 (F14: N221.8bn). This covered debt service charges by an unchanged 3.9x. After accounting for interest, the operating surplus fell to N143.8bn in F15 (F14: N165.2bn), equating to a period low margin of 37.4% of revenue (F14: 40.5%).

Lagos has historically relied on large surpluses, as well as debt funding to execute the huge development projects. This has enabled the State to sustain high levels of capex, which cumulatively totaled over N1tn between F11 and F15. However, capex spend reduced to N174bn in F15 (F14: N213.1bn), with a number of projects yet to be committed to. Thus, capex equated to 45% of income (F14: 52%; five year average: 56%), the first time it had fallen below 50% over the review period. The relatively low capex in F15 was impacted by the lower than expected fiscal surplus, as well as administrative issues which affected the release of funds for projects, following the change in administration.

Funding profile

Cash holdings have been maintained at high levels (over N100bn) for most of the last five years, and have fluctuated based on the utilisation requirements of the State In this regard, cash holdings registered at a new high of N144.1bn at FYE15 (FYE14: N128.4bn) following a significant build-up in the sinking fund account (“SFA”) required to service the State’s existing bonds and foreign loan obligations. Funds in the SFA (to which the State has no access) rose by N38.2bn to N120.5bn at FYE15 to comprise 84% of cash holdings. Other components of cash holdings include; treasury funds, cash in ministries and agencies and other special deposits, and are available for spending. Given the increase in cash holdings and coupled with the slight reduction in recurrent expenses, days cash on hand rose to 219 days from 193 days in F14. However, if funds in the SFA were stripped out of cash holdings, days cash on hand would significantly decline to 36 days in F15, well below the 90-day benchmark deemed appropriate by GCR. Cash is held solely in Naira denominated current accounts placed with commercial banks in Nigeria.

The value of the State’s investment portfolio has evidenced a four-fold increase over the last two years, rising to N28.8bn at FYE15 (FYE14: N14.3bn). The increase was largely driven by foreign currency investments in Lekki Free Zone Development Co. (amounting to N21.2bn), while other foreign currency investments are held in Airtel Nigeria Limited, El-Sewedy Electric Co. and Nigeria Sovereign Investment Authority. Following diminutions in value, quoted

55%

19%

14%

0%12%

Figure 1: F15 Revenue sources

Income taxes

VAT

Other IGR

Interest inc.

Statutory receipts

Nigeria Local Authority Analysis | Public Rating Page 6

investments registered at a lower N2.3bn at FYE15 (FYE14 N2.9bn) with Skye Bank Plc and Lasaco Assurance Plc comprising a combined 89% of the portfolio. While this reflects significant concentration risk (especially as GCR recently downgraded the long term national scale rating of Skye Bank Plc. below investment grade), the total equities portfolio remains small in the context of the State. The remainder of investments comprised unquoted equities, which grew to N2.4bn (FYE14: N2bn) and investments in subsidiaries and associated companies.

In addition to the robust fiscal surpluses (totalling a cumulative N703bn in the last five years), the growth of the State’s infrastructural base has been strongly facilitated by debt funding. This State demonstrates strong access to borrowings from various sources, with debt increasing by a net N32.8bn to a new high of N619.3bn reported at FYE15. As a consequence, gross and net debt to revenue levels increased further, to 161% and 124% respectively at FYE15 (FYE14: 142% and 111%). An analysis of the loan book reveals that internal loans comprised seven loans cumulatively equalling a marginally higher N132.6bn (21% of debt). All of these were secured around November and December 2015 (at relatively lower rates), following the restructuring of previous outstanding loans (amounting to N129.7bn). Leading the credit package are Access Bank (N59.2bn/10% of debt) and Guaranty Trust Bank (N29.5bn/5% of Debt). The maturity profile of the new loans appear well spread, with maturities extending until 2025 (for most of the loans), in alignment with the various infrastructural projects they finance.

Table 4: Financing sources (N’m) FYE13 FYE14 FYE15

External 150,063 225,544 261,669 Commercial 112,524 130,533 132,609 Bond Issues 275,000 225,000 225,000

Total* 537,586 581,077 619,278 Gross debt: income (%) 142.7 142.4 161.1 Net debt: income (%) 107.6 110.9 123.6 DSC^(x) 11.6 3.9 3.9 *Total debt is moderated by funds in the SFA- N82.4bn and N120.5bn at FYE14 and FYE15 respectively. ^Debt Service Coverage

The majority of Lagos’ borrowings derive from the three bonds in issue (under two programmes), totalling N225bn (36% of debt). The bonds are serviced through semi-annual coupon payments. The initial agreement was for bullet repayment of principal upon maturity, with reserves being built up in the SFA to ensure timely repayment. However, this gave rise to some interest leakage as the interest earned on positive cash balances did not fully cover the interest paid on the bonds. Accordingly, an agreement has been reached between the State government and bondholders (and approved by the SEC) that principal repayments on the Programme II bonds (N80bn and N87.5bn) will be brought forward and made on a semi-annual basis, along with interest payments. The first set of principal repayments on the N80bn and N87.5bn bonds were

made in May 2016. The N57.5bn bond (under Programme 1) is expected to be fully settled via bullet repayment in F17, while the N80bn and N87.5bn bonds would be fully repaid by FYE19 and FYE20 respectively.

Foreign loans amounted to a higher N261.7bn at FYE15 (FYE14: N225.5bn), mainly impacted by the weakening of the Naira. during F15, Funds were however drawn from existing facilities to finance ongoing projects including; N304m for the 2nd National Urban Water project, N243m for Commercial Agricultural development Programme; N9.2bn for transportation projects (under LAMATA), and N3.1bn additional funding for Eko Secondary Education Programme. The bulk of these loans generally have concessionary interest rates of around 1% per annum, with tenors ranging between 20 and 35 years, and moratorium on principal repayment of between 5 and 10 years.

Future prospects and forecasts

The operating and capital budgets are as provided by the State and have been approved by the Lagos State Legislature under the Appropriation Act for 2016. The budget is premised on a number of assumptions, key among which is a conservative expectation on statutory receipts, with an oil price benchmark of USD38/barrel.

The budget has been christened “The People’s Budget”, with emphasis on accelerating development through massive investments in security, transport/traffic management, physical and social infrastructure and job creation. Added to this, the State plans to enhance employment and wealth creation opportunities by implementing an Employment Trust Scheme, with N25bn funding over an initial four-year period (N6.5bn has been released for F16). In the area of agriculture and food security, a food expansion programme is already in place, focused on rice production, animal rearing and root crop production. The government intends to collaborate with other States in the creation of a commodity value chain to provide a sustainable market for rice. A MOU already exists with Kebbi State on the supply of paddy rice. Furthermore, fish production would be boosted through increased investments in the Ayobo fish farm. Besides consolidating the gains under the Agric YES programme in Badagry (following the adoption of the Shongai farm settlement model), the Agric Park in Ikorodu is also thriving with the planned expansion of the rice milling facility to satisfy requirements within the Lagos area. In all, these projects are geared towards improving economic activities, while also enhancing job creation opportunities.

In view of the above, Lagos anticipates sustained growth in revenue over the medium term. Although IGR evidenced a decline in F15, it is budgeted to rise by 35% to N458bn (includes VAT) in F16, to be driven by the ongoing implementation of tax laws (with renewed emphasis on property tax), as well as the enforcements thereof. Statutory allocations are also budgeted to rise by

Nigeria Local Authority Analysis | Public Rating Page 7

around 15% to N50bn. While transfers remain dependent on global oil prices, prices seem to have steadied above USD45/barrel in recent weeks, above the budget assumption of USD38/barrel. Together, this would see total operating income rise 32% to N509bn. With budgets anticipating a further 15% reduction in expenditure, an operating surplus of N233bn has been budgeted for F16 (F15: N144bn).

Table 5: Operating budgets (Nbn)

Actual Budget F16

% achieved F15 1H F16^

Total IGR* 341 180 458 39 Statutory allocation 44 13 50 27 Total recurrent inc. 384 193 509 38 Total recurrent exp. (241) (115) (276) 42 Operating surplus 144 79 233 34 Other capital receipts 29 5 34 16 Loans/bonds 151 31 120 26 Capital expenditure (174) (110) (314) 35 Facility repayments (134) (5) (72) 7 Cash & equiv. 16 0 (0) 0 *Includes VAT receipts ^Management accounts to June 2016

Year-to-date accounts for the six months to 30 June 2016 (“1H F16”) indicate slight shortfalls relative to budget, with IGR of N180bn reported and statutory allocations of just N13bn having been received. Accordingly, total income amounted to N193bn in 1H F16, representing 38% of the full-year expectation, albeit that, this is in line with F15 revenue on an annualised basis. In contrast, expenditure of N115bn amounted to 42% of the full year budget, with the operating surplus of N79bn representing around a third of the full year projection. Nevertheless, expectation for the rest of the year is high, with improved economic activities associated with the latter part of the year and the renewed emphasis on the implementation of property tax laws.

The State has budgeted to escalate the current level of infrastructure development, with capex budgeted to almost double to N314bn in F16. Most of this would be funded through the operating surplus, with grants and counterpart expenses amounting to a relatively low N14.9bn. the remainder of funding would derive from borrowings, with foreign loans of N56.4bn and a proposed Bond Issue of N60bn. However, the relatively low capex spend of N110bn at 1H F16, was financed mainly from the surplus and foreign loan amounting to N31bn. In this vein, GCR considers the capex projections to be somewhat high as capex has generally been around N200bn and peaked at N275bn in FYE13. Moreover, securing the required funding might prove more difficult than anticipated.

With the budget providing for a loan repayment of N72.5bn, gross debt is likely to rise to N666.5bn by FYE16. This would see gross debt to revenue falling to around 131% at FYE16.

Bond rating considerations

In performing the above analysis, GCR has considered those factors impacting the general creditworthiness of Lagos State i.e. its unsecured Issuer credit rating.

However, structural and other enhancements have been (or are expected to be) utilised to improve the credit risk of a specific Issue(s) under the bond programme. In respect of the above, apart from the scenario of a full guarantee, GCR’s approach to Issue Ratings is to utilise the unsecured Issuer rating as a base from which credit enhancement is considered. Credit enhancements are considered in terms of their impact on the likelihood of repayment of that particular Issue.

Programme 1: The Series 2 N57.5bn Fixed Rate Bond is a 7-year bond, issued in 2010, bearing interest of 10% per annum, payable semi-annually. Coupon payments totalling N2.9bn are made semi-annually (N5.75bn annually), payable in arrears up to and including the maturity date (April, 2017). The aggregate principal amount and any coupon is to be paid in one bullet on the maturity date from the Series 2 SFA, managed by the independent Trustees. The State did not issue an ISPO in respect of Series 2, as such, interest and principal obligations are met solely from the CDSA. Based on the performance report received from the Trustees, N11.4bn was transferred into the Series 2 SFA (in 2015) from the CDSA to meet coupon payments, as well as the principal repayment on maturity.

Table 6: Sinking fund account- P1S2 (N'm)

Actual 1HF16*

Budget** F17 F18 F18

Op. bal. sinking fund - 57,074 60,880 71,499 Transfer from revenue 79,315 7,700 13,200 13,200 Investment income 13,526 2,002 3,432 3,432 Total before debt service 92,841 66,776 77,511 88,131 Projected debt service (34,511) (5,734) (5,734) (5,734) Professional fees/charges (1,256) (162) (278) (278) Cl. bal. sinking fund 57,074 60,880 71,499 82,118

*Total inflows and outflows up to June 2016 **GCR projections

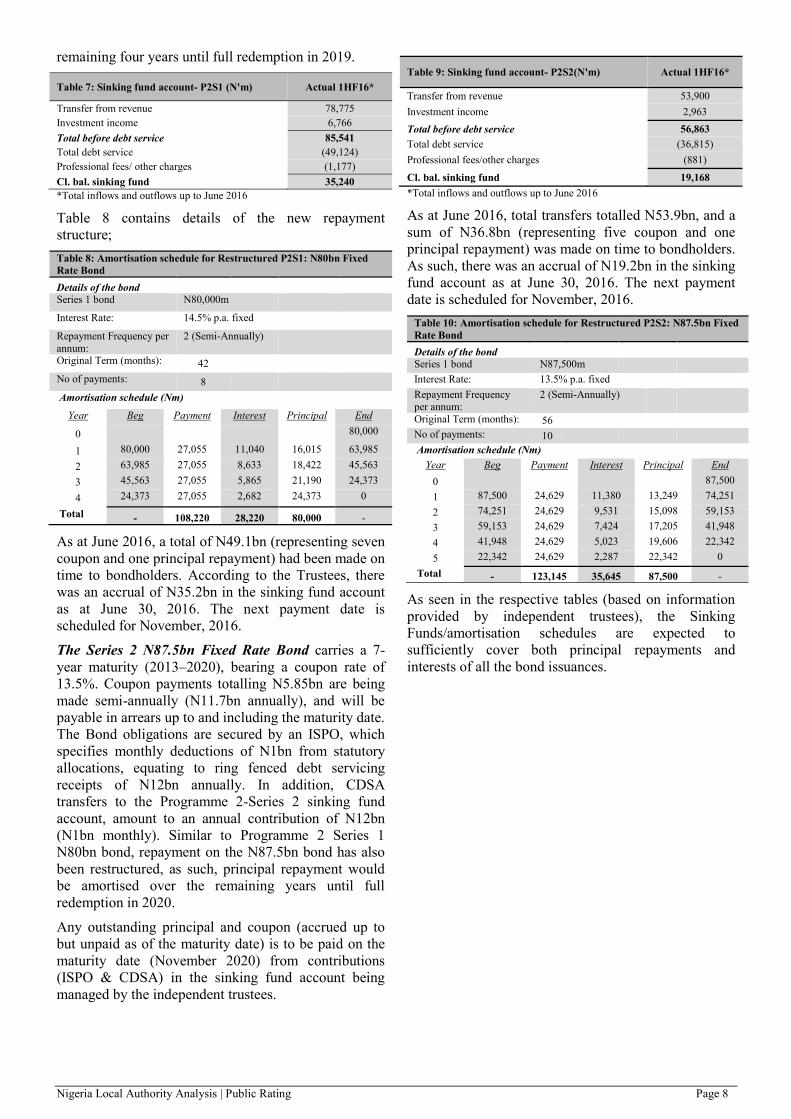

As at June 2016, a total of N34.5bn (representing thirteen semi-annual payments) had been made on time to bondholders. According to the Trustees, there was an accrual of N57.1bn in the sinking fund account as at June 30 2016. The next payment date is scheduled for October, 2016.

Programme 2: The Series 1 N80bn Fixed Rate Bond carries a 7-year maturity (2012–2019), bearing a coupon rate of 14.5%. Coupon payments totalling N5.7bn are being made semi-annually (N11.4bn annually), and will be payable in arrears up to and including the maturity date. The Bond obligations are secured by an ISPO, which specifies monthly deductions of N1bn from statutory allocations. This equates to ring fenced debt servicing receipts of around N12bn annually.

The Programme 2 - Series 1 ISPO is augmented by transfers from Lagos State’s IGR (via the CDSA), in respect of which a monthly sum of N0.9bn (N10.8bn annually) is being transferred into the sinking fund account. As previously mentioned, the State decided to advance payment on the principal, rather than the initial bullet repayment. The plan was agreed with bondholders and also sanctioned by the SEC. In this regard, principal repayment will be amortised over the

Nigeria Local Authority Analysis | Public Rating Page 8

remaining four years until full redemption in 2019.

Table 7: Sinking fund account- P2S1 (N'm) Actual 1HF16*

Transfer from revenue 78,775 Investment income 6,766 Total before debt service 85,541 Total debt service (49,124) Professional fees/ other charges (1,177) Cl. bal. sinking fund 35,240 *Total inflows and outflows up to June 2016

Table 8 contains details of the new repayment structure;

Table 8: Amortisation schedule for Restructured P2S1: N80bn Fixed Rate Bond Details of the bond Series 1 bond N80,000m Interest Rate: 14.5% p.a. fixed Repayment Frequency per annum:

2 (Semi-Annually)

Original Term (months): 42 No of payments: 8 Amortisation schedule (Nm)

Year Beg Payment Interest Principal End

0 80,000

1 80,000 27,055 11,040 16,015 63,985 2 63,985 27,055 8,633 18,422 45,563 3 45,563 27,055 5,865 21,190 24,373

4 24,373 27,055 2,682 24,373 0

Total - 108,220 28,220 80,000 -

As at June 2016, a total of N49.1bn (representing seven coupon and one principal repayment) had been made on time to bondholders. According to the Trustees, there was an accrual of N35.2bn in the sinking fund account as at June 30, 2016. The next payment date is scheduled for November, 2016.

The Series 2 N87.5bn Fixed Rate Bond carries a 7-year maturity (2013–2020), bearing a coupon rate of 13.5%. Coupon payments totalling N5.85bn are being made semi-annually (N11.7bn annually), and will be payable in arrears up to and including the maturity date. The Bond obligations are secured by an ISPO, which specifies monthly deductions of N1bn from statutory allocations, equating to ring fenced debt servicing receipts of N12bn annually. In addition, CDSA transfers to the Programme 2-Series 2 sinking fund account, amount to an annual contribution of N12bn (N1bn monthly). Similar to Programme 2 Series 1 N80bn bond, repayment on the N87.5bn bond has also been restructured, as such, principal repayment would be amortised over the remaining years until full redemption in 2020.

Any outstanding principal and coupon (accrued up to but unpaid as of the maturity date) is to be paid on the maturity date (November 2020) from contributions (ISPO & CDSA) in the sinking fund account being managed by the independent trustees.

Table 9: Sinking fund account- P2S2(N'm) Actual 1HF16*

Transfer from revenue 53,900 Investment income 2,963 Total before debt service 56,863 Total debt service (36,815) Professional fees/other charges (881)

Cl. bal. sinking fund 19,168 *Total inflows and outflows up to June 2016

As at June 2016, total transfers totalled N53.9bn, and a sum of N36.8bn (representing five coupon and one principal repayment) was made on time to bondholders. As such, there was an accrual of N19.2bn in the sinking fund account as at June 30, 2016. The next payment date is scheduled for November, 2016.

Table 10: Amortisation schedule for Restructured P2S2: N87.5bn Fixed Rate Bond Details of the bond Series 1 bond N87,500m Interest Rate: 13.5% p.a. fixed Repayment Frequency per annum:

2 (Semi-Annually)

Original Term (months): 56 No of payments: 10 Amortisation schedule (Nm)

Year Beg Payment Interest Principal End

0 87,500 1 87,500 24,629 11,380 13,249 74,251 2 74,251 24,629 9,531 15,098 59,153 3 59,153 24,629 7,424 17,205 41,948 4 41,948 24,629 5,023 19,606 22,342 5 22,342 24,629 2,287 22,342 0

Total - 123,145 35,645 87,500 -

As seen in the respective tables (based on information provided by independent trustees), the Sinking Funds/amortisation schedules are expected to sufficiently cover both principal repayments and interests of all the bond issuances.

Nigeria Local Authority Analysis | Public Rating Page 9

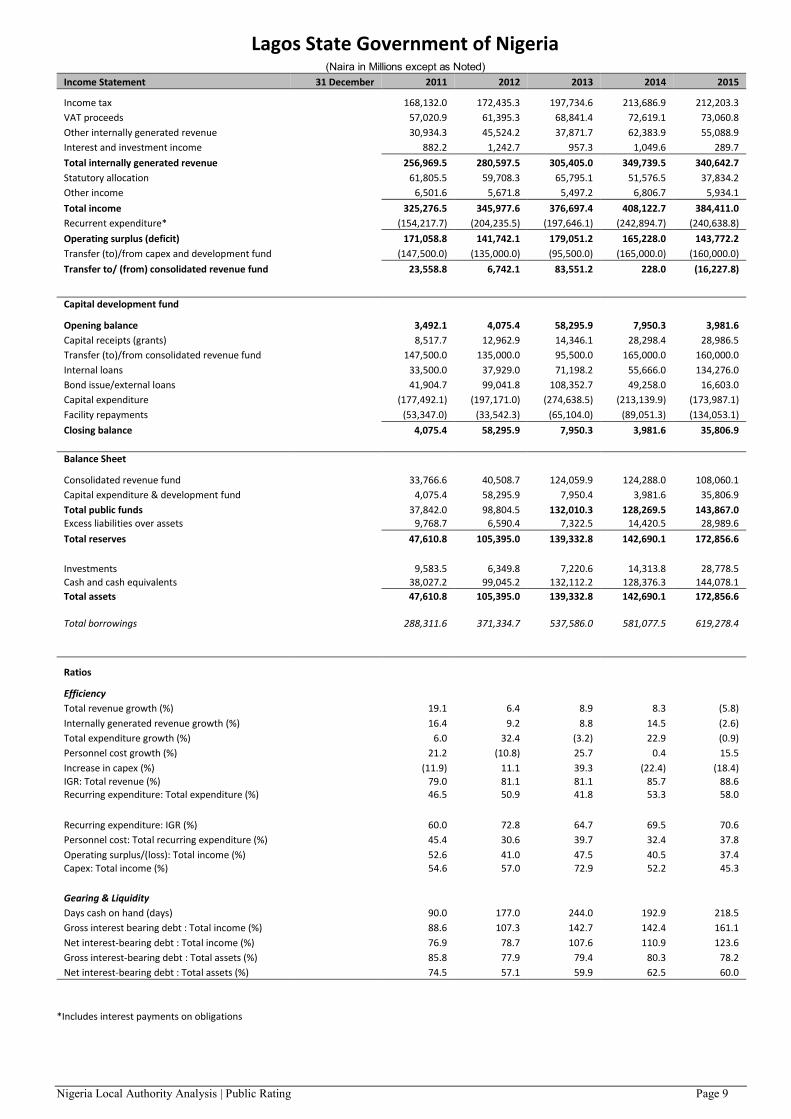

Lagos State Government of Nigeria

(Naira in Millions except as Noted) Income Statement 31 December 2011 2012 2013 2014 2015

Income tax 168,132.0 172,435.3 197,734.6 213,686.9 212,203.3 VAT proceeds 57,020.9 61,395.3 68,841.4 72,619.1 73,060.8 Other internally generated revenue 30,934.3 45,524.2 37,871.7 62,383.9 55,088.9 Interest and investment income 882.2 1,242.7 957.3 1,049.6 289.7 Total internally generated revenue 256,969.5 280,597.5 305,405.0 349,739.5 340,642.7 Statutory allocation 61,805.5 59,708.3 65,795.1 51,576.5 37,834.2 Other income 6,501.6 5,671.8 5,497.2 6,806.7 5,934.1 Total income 325,276.5 345,977.6 376,697.4 408,122.7 384,411.0 Recurrent expenditure* (154,217.7) (204,235.5) (197,646.1) (242,894.7) (240,638.8) Operating surplus (deficit) 171,058.8 141,742.1 179,051.2 165,228.0 143,772.2 Transfer (to)/from capex and development fund (147,500.0) (135,000.0) (95,500.0) (165,000.0) (160,000.0) Transfer to/ (from) consolidated revenue fund 23,558.8 6,742.1 83,551.2 228.0 (16,227.8)

Capital development fund

Opening balance 3,492.1 4,075.4 58,295.9 7,950.3 3,981.6 Capital receipts (grants) 8,517.7 12,962.9 14,346.1 28,298.4 28,986.5 Transfer (to)/from consolidated revenue fund 147,500.0 135,000.0 95,500.0 165,000.0 160,000.0 Internal loans 33,500.0 37,929.0 71,198.2 55,666.0 134,276.0 Bond issue/external loans 41,904.7 99,041.8 108,352.7 49,258.0 16,603.0 Capital expenditure (177,492.1) (197,171.0) (274,638.5) (213,139.9) (173,987.1) Facility repayments (53,347.0) (33,542.3) (65,104.0) (89,051.3) (134,053.1) Closing balance 4,075.4 58,295.9 7,950.3 3,981.6 35,806.9

Balance Sheet

Consolidated revenue fund 33,766.6 40,508.7 124,059.9 124,288.0 108,060.1 Capital expenditure & development fund 4,075.4 58,295.9 7,950.4 3,981.6 35,806.9 Total public funds 37,842.0 98,804.5 132,010.3 128,269.5 143,867.0 Excess liabilities over assets 9,768.7 6,590.4 7,322.5 14,420.5 28,989.6 Total reserves 47,610.8 105,395.0 139,332.8 142,690.1 172,856.6

Investments 9,583.5 6,349.8 7,220.6 14,313.8 28,778.5 Cash and cash equivalents 38,027.2 99,045.2 132,112.2 128,376.3 144,078.1 Total assets 47,610.8 105,395.0 139,332.8 142,690.1 172,856.6

Total borrowings 288,311.6 371,334.7 537,586.0 581,077.5 619,278.4

Ratios

Efficiency Total revenue growth (%) 19.1 6.4 8.9 8.3 (5.8)

Internally generated revenue growth (%) 16.4 9.2 8.8 14.5 (2.6) Total expenditure growth (%) 6.0 32.4 (3.2) 22.9 (0.9) Personnel cost growth (%) 21.2 (10.8) 25.7 0.4 15.5 Increase in capex (%) (11.9) 11.1 39.3 (22.4) (18.4) IGR: Total revenue (%) 79.0 81.1 81.1 85.7 88.6 Recurring expenditure: Total expenditure (%) 46.5 50.9 41.8 53.3 58.0

Recurring expenditure: IGR (%) 60.0 72.8 64.7 69.5 70.6 Personnel cost: Total recurring expenditure (%) 45.4 30.6 39.7 32.4 37.8 Operating surplus/(loss): Total income (%) 52.6 41.0 47.5 40.5 37.4 Capex: Total income (%) 54.6 57.0 72.9 52.2 45.3

Gearing & Liquidity Days cash on hand (days) 90.0 177.0 244.0 192.9 218.5

Gross interest bearing debt : Total income (%) 88.6 107.3 142.7 142.4 161.1 Net interest-bearing debt : Total income (%) 76.9 78.7 107.6 110.9 123.6 Gross interest-bearing debt : Total assets (%) 85.8 77.9 79.4 80.3 78.2 Net interest-bearing debt : Total assets (%) 74.5 57.1 59.9 62.5 60.0

*Includes interest payments on obligations

Nigeria Local Authority Analysis | Public Rating Page 10

This page is intentionally left blank

Nigeria Local Authority Analysis | Public Rating Page 11

This page is intentionally left blank

Nigeria Local Authority Analysis | Public Rating Page 12

SALIENT POINTS OF ACCORDED RATINGS

GCR affirms that a.) no part of the rating was influenced by any other business activities of the credit rating agency; b.) the rating was based solely on the merits of the rated entity, security or financial instrument being rated; c.) such rating was an independent evaluation of the risks and merits of the rated entity, security or financial instrument; and d.) the ratings are valid until 07/2017. Lagos State participated in the rating process via face-to-face meeting, teleconferences and other written correspondence. Furthermore, the quality of information received was considered adequate and has been independently verified where possible. The information received from Lagos State Government of Nigeria and other reliable third parties to accord the credit rating included -the audited accounts for the year ended 31 December 2015 (plus four years of comparative numbers); -the approved budget for 2016 -the Joint Trustees reports on the three bonds (N57.5bn, N80bn and N87.5bn bonds) for the period ended 30 June 2016 -a breakdown of facilities available and related counterparties, and -information specific to the rated entity and/or industry was also received. The ratings above were solicited by, or on behalf of, the rated client, and therefore, GCR has been compensated for the provision of the ratings.

ALL GCR CREDIT RATINGS ARE SUBJECT TO CERTAIN LIMITATIONS, TERMS OF USE OF SUCH RATINGS AND DISCLAIMERS. PLEASE READ THESE LIMITATIONS, TERMS OF USE AND DISCLAIMERS BY FOLLOWING THIS LINK:HTTP://GLOBALRATINGS.COM.NG/UNDERSTANDING-RATINGS. IN ADDITION, RATING SCALES AND DEFINITIONS ARE AVAILABLE ON GCR’S PUBLIC WEB SITE AT HTTP://GLOBALRATINGS.COM.NG/RATINGS-INFO/RATING-SCALES-DEFINITIONS. PUBLISHED RATINGS, CRITERIA, AND METHODOLOGIES ARE AVAILABLE FROM THIS SITE AT ALL TIMES. GCR'S CODE OF CONDUCT, CONFIDENTIALITY, CONFLICTS OF INTEREST, COMPLIANCE, AND OTHER RELEVANT POLICIES AND PROCEDURES ARE ALSO AVAILABLE FROM THE UNDERSTANDING RATINGS SECTION OF THIS SITE. CREDIT RATINGS ISSUED AND RESEARCH PUBLICATIONS PUBLISHED BY GCR, ARE GCR’S OPINIONS, AS AT THE DATE OF ISSUE OR PUBLICATION THEREOF, OF THE RELATIVE FUTURE CREDIT RISK OF ENTITIES, CREDIT COMMITMENTS, OR DEBT OR DEBT-LIKE SECURITIES. GCR DEFINES CREDIT RISK AS THE RISK THAT AN ENTITY MAY NOT MEET ITS CONTRACTUAL AND/OR FINANCIAL OBLIGATIONS AS THEY BECOME DUE. CREDIT RATINGS DO NOT ADDRESS ANY OTHER RISK, INCLUDING BUT NOT LIMITED TO: FRAUD, MARKET LIQUIDITY RISK, MARKET VALUE RISK, OR PRICE VOLATILITY. CREDIT RATINGS AND GCR’S OPINIONS INCLUDED IN GCR’S PUBLICATIONS ARE NOT STATEMENTS OF CURRENT OR HISTORICAL FACT. CREDIT RATINGS AND GCR’S PUBLICATIONS DO NOT CONSTITUTE OR PROVIDE INVESTMENT OR FINANCIAL ADVICE, AND CREDIT RATINGS AND GCR’S PUBLICATIONS ARE NOT AND DO NOT PROVIDE RECOMMENDATIONS TO PURCHASE, SELL OR HOLD PARTICULAR SECURITIES. NEITHER GCR’S CREDIT RATINGS, NOR ITS PUBLICATIONS, COMMENT ON THE SUITABILITY OF AN INVESTMENT FOR ANY PARTICULAR INVESTOR. GCR ISSUES ITS CREDIT RATINGS AND PUBLISHES GCR’S PUBLICATIONS WITH THE EXPECTATION AND UNDERSTANDING THAT EACH INVESTOR WILL MAKE ITS OWN STUDY AND EVALUATION OF EACH SECURITY THAT IS UNDER CONSIDERATION FOR PURCHASE, HOLDING OR SALE. Copyright © 2016 Global Credit Rating Company Ltd. THE INFORMATION CONTAINED HEREIN MAY NOT BE COPIED OR OTHERWISE REPRODUCED OR DISCLOSED , IN WHOLE OR IN PART, IN ANY FORM OR MANNER OR BY ANY MEANS WHATSOEVER, BY ANY PERSON WITHOUT GCR’S PRIOR WRITTEN CONSENT. The ratings were solicited by, or on behalf of, the issuer of the instrument in respect of which the rating is issued, and GCR has been compensated for the provision of the ratings. Information sources used to prepare the ratings are set out in each credit rating report and/or rating notification and include the following: parties involved in the ratings and public information. All information used to prepare the ratings is obtained by GCR from sources reasonably believed by it to be accurate and reliable. Although GCR will at all times use its best efforts and practices to ensure that the information it relies on is accurate at the time, GCR does not provide any warranty in respect of, nor is it otherwise responsible for, the accurateness of such information. GCR adopts all reasonable measures to ensure that the information it uses in assigning a credit rating is of sufficient quality and that such information is obtained from sources that GCR, acting reasonably, considers to be reliable, including, when appropriate, independent third-party sources. However, GCR cannot in every instance independently verify or validate information received in the rating process. Under no circumstances shall GCR have any liability to any person or entity for (a) any loss or damage suffered by such person or entity caused by, resulting from, or relating to, any error made by GCR, whether negligently (including gross negligence) or otherwise, or other circumstance or contingency outside the control of GCR or any of its directors, officers, employees or agents in connection with the procurement, collection, compilation, analysis, interpretation, communication, publication or delivery of any such information, or (b) any direct, indirect, special, consequential, compensatory or incidental damages whatsoever (including without limitation, lost profits) suffered by such person or entity, as a result of the use of or inability to use any such information. The ratings, financial reporting analysis, projections, and other observations, if any, constituting part of the information contained herein are, and must be construed solely as, statements of opinion and not statements of fact or recommendations to purchase, sell or hold any securities. Each user of the information contained herein must make its own study and evaluation of each security it may consider purchasing, holding or selling. NO WARRANTY, EXPRESS OR IMPLIED, AS TO THE ACCURACY, TIMELINESS, COMPLETENESS, MERCHANTABILITY OR FITNESS FOR ANY PARTICULAR PURPOSE OF ANY SUCH RATING OR OTHER OPINION OR INFORMATION IS GIVEN OR MADE BY GCR IN ANY FORM OR MANNER WHATSOEVER.