LAFFERTY WEST AFRICA PRESENTATION (1)

44

Managing the banking distribution mix so it is fit for purpose Presented by Sandeep Deobhakta Sub-Group Head, Chief Operating Officer Retail Banking Sub-Group May 4th, 2010 Lafferty Retail Finance Convention West Africa 2010

-

Upload

sandeep-deobhakta -

Category

Documents

-

view

274 -

download

2

Transcript of LAFFERTY WEST AFRICA PRESENTATION (1)

Managing the banking distribution mix so it is fit for purpose

Presented by Sandeep DeobhaktaSub-Group Head,Chief Operating OfficerRetail Banking Sub-Group

May 4th, 2010

Lafferty Retail FinanceConvention West Africa 2010

1

Key themes for today

# 1 We are witnessing a fundamental shift in customer behavior –The customer buying processThe way customers use banks

# 2 The Branch is important…….but, it is an expensive channelManaging cost is critical…..but not at the expense of the customer experienceUsing technology and an “assisted” customer experience

2

But first……..An introduction to Shinsei Bank

3

Background – Shinsei Bank

Shinsei Bank was formed in March 2000 when the Long Term Credit Bank (LTCB) wasprivatized.

The Old LTCB Individual Banking was a funding engine for the corporate loan business

The retail business was launched in 2001. Currently, the business has:

2.5 Million customers

Footings in excess of JPY 6.5 Trillion [USD 70 Billion]

Investment and Foreign currency AUMs of JPY 900 Billion [USD 10 Billion]

Mortgage loans of JPY 800 Billion [USD 9 Billion]

41 branches nationwide

Strong retail brand

Growing, profitable retail business

4

The CEO’s vision for the new retail bank in 2001

Yashiro-san believed it was better standards of service, and innovation in services,

that would ultimately attract customers to the bank.

5

ATM Withdrawal Fee¥ 0

Shinsei Bank ATMs, Seven Bank ATMs<Available 24 hours>

Partner ATM fees will be refunded

ATM Withdrawal Fee¥ 0

Shinsei Bank ATMs, Seven Bank ATMs<Available 24 hours>

Partner ATM fees will be refunded

A unique customer proposition – free access, 24 x 7, global ATM card

International Cash Card

Withdraw your money in local currency at overseas ATMs

International Cash Card

Withdraw your money in local currency at overseas ATMs

PowerSmart Home Mortgage

Guarantee fee ¥ 0 Auto-early repayment fee ¥ 0

Group life insurance premium ¥ 0

PowerSmart Home Mortgage

Guarantee fee ¥ 0 Auto-early repayment fee ¥ 0

Group life insurance premium ¥ 0

ATM /Call Center /Internet /Mobile24 h × 365 day

Banking Anytime, Anywhere

ATM /Call Center /Internet /Mobile24 h × 365 day

Banking Anytime, Anywhere

Internet Domestic Fund Transfer Fee ¥ 0

1, 5 or 10 times per month based on customer stage

Internet Domestic Fund Transfer Fee ¥ 0

1, 5 or 10 times per month based on customer stage

Branches are open Until 5 p.m. on weekdays

and on weekendsWe do not close at 3 p.m. as others do

Branches are open Until 5 p.m. on weekdays

and on weekendsWe do not close at 3 p.m. as others do

6

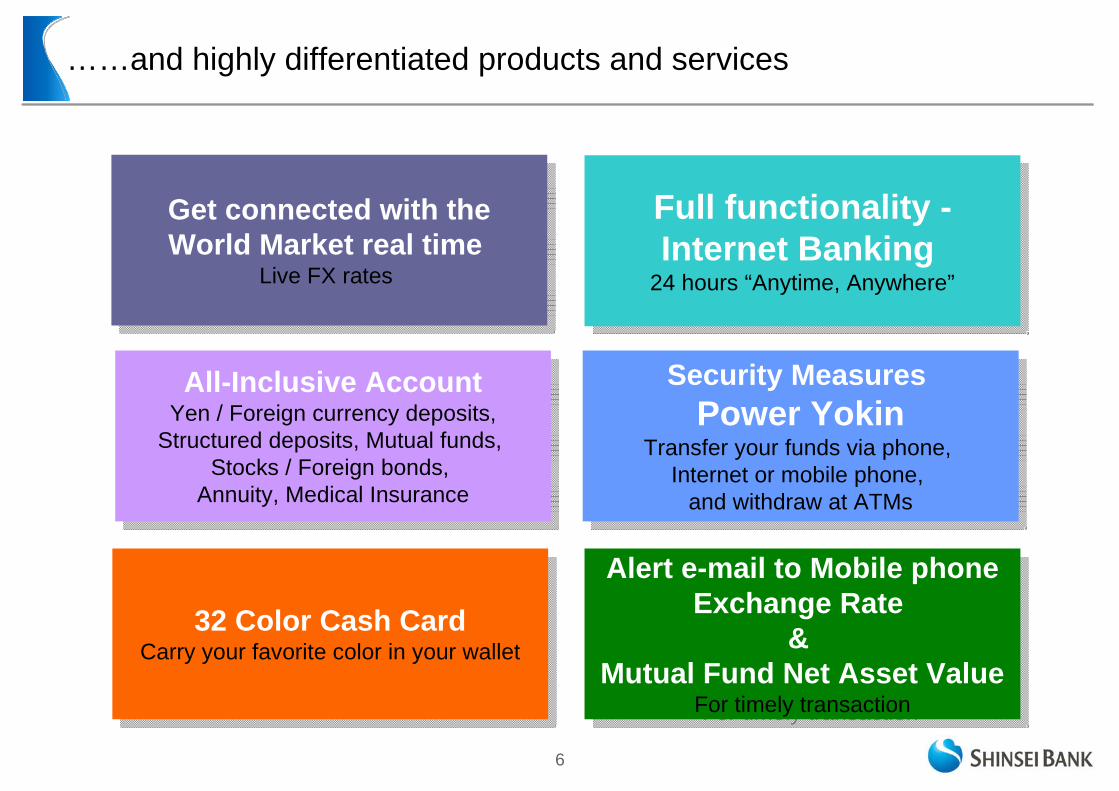

Get connected with theWorld Market real time

Live FX rates

Get connected with theWorld Market real time

Live FX rates

All-Inclusive AccountYen / Foreign currency deposits,

Structured deposits, Mutual funds, Stocks / Foreign bonds,

Annuity, Medical Insurance

All-Inclusive AccountYen / Foreign currency deposits,

Structured deposits, Mutual funds, Stocks / Foreign bonds,

Annuity, Medical Insurance

32 Color Cash CardCarry your favorite color in your wallet

32 Color Cash CardCarry your favorite color in your wallet

Full functionality -Internet Banking

24 hours “Anytime, Anywhere”

Full functionality -Internet Banking

24 hours “Anytime, Anywhere”

Security Measures Power Yokin

Transfer your funds via phone, Internet or mobile phone,

and withdraw at ATMs

Security Measures Power Yokin

Transfer your funds via phone, Internet or mobile phone,

and withdraw at ATMs

Alert e-mail to Mobile phoneExchange Rate

& Mutual Fund Net Asset Value

For timely transaction

Alert e-mail to Mobile phoneExchange Rate

& Mutual Fund Net Asset Value

For timely transaction

……and highly differentiated products and services

7

That have been acknowledged by customers and the industry.

Consistently ranked in the top tier in the Nikkei’s Annual customer satisfaction survey in Japan since 2004

Won the Asian Banker Award for the best retail bank in Japan for 4 out of the 6 years since 2004. Always ranked in the top 3

8

The Customer buying process is changing

9

The customer buying process – financial services

COMPARISON SITES11%

ONLINECOMMUNITIES

14%

OTHERS21%

COMPANY WEBSITE23%

TV / NEWSPAPER /POINT OF SALE

31%

Online media accounts for 48% of the customer information gathering process.Online communities and comparison sites account for 25%. This number is growing rapidly.

Source: Nomura Research Institute – New Trend of Innovation in the web 2.0 Era

10

Internet & Mobile media spend is on the rise

11

In a First, Web Advertising Outpaces TV in U.K.Internet Now Commands 24% of Ad Spending to TV's 22%Posted by Matthew Creamer on 09.29.09 @ 05:37 PM

12

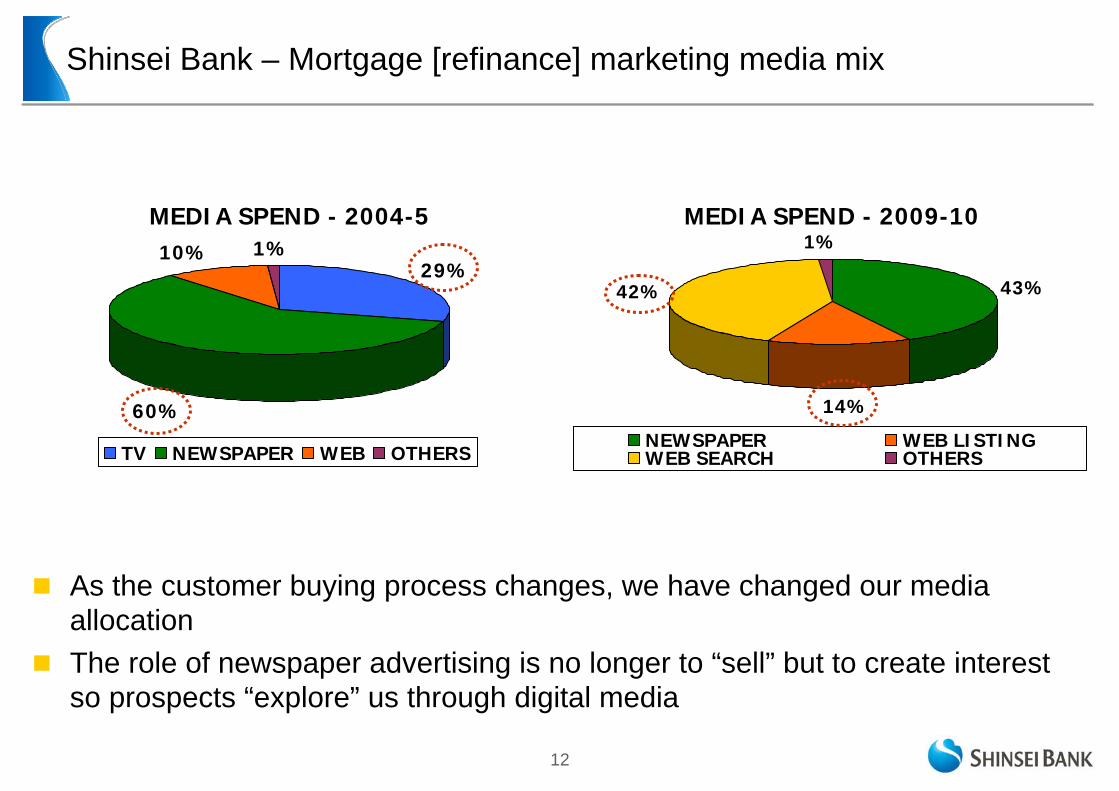

MEDIA SPEND - 2004-5

29%

60%

10% 1%

TV NEWSPAPER WEB OTHERS

As the customer buying process changes, we have changed our media allocation The role of newspaper advertising is no longer to “sell” but to create interest so prospects “explore” us through digital media

MEDIA SPEND - 2009-10

43%

14%

42%

1%

NEWSPAPER WEB LISTINGWEB SEARCH OTHERS

Shinsei Bank – Mortgage [refinance] marketing media mix

13

SOURCE - LEAD GENERATION

46%

16%

18%

20%

SEARCH / COMPARISION SITESWEB ADSSHINSEI WEBSITEOTHERS

Acquisition - mortgage

APPLICATION BY CHANNEL

83%

8% 9%

INTERNET BRANCH CALL CENTER

14

Example – “Search” engine marketing

Attention / Interest

Other banks’ AD

TV /Newspaper /

Web banner Ads

Search

Search engine( Yahoo / Google )

Action

Shinseibank.com

Starter Kit Request

Shinsei Bank’s Newspaper Advertising

15

Keyword : mortgage

Search engine directs to comparison shopping siteShinsei Bank site

We want to cover the top 3 - 4 search engine results with comparison sites and our own ads.

Example – “Search” engine marketing [contd.]

16

The way customers use

banks….

17

In the US, online banking is now the most preferred channel

18

Online channel usage at Shinsei Bank

55% of all new accounts are acquired online

75% of all deposit sales are non branch. Online alone is 45%

83% of loans originated online

72% of our new branch customers sign up for e-statements

Over 50% of mutual fund transactions are booked online

Our focus….keep improving the customer experience, especially online

19

The Branch is important…….but, it is an expensive channel

20

A large ATM and Branch network is important to Japanese customers

WHAT DID YOU CONSIDER IN CHOOSING YOUR MAIN BANK?

0 20 40 60 80 100 120 140 160

LARGE ATM NETWORK

NUMBER OF BRANCHES

SAFETY & CREDIBILITY

QUALITY OF INTERNET SERVICES

CUSTOMER ATTITUDE

INTEREST RATES

Source: Nikkei Veritas, June 2009

21

In a recent article for BAI, Dave Kerstein, explores the role and the future of branches

You don’t need as many iconic free standing branches. You need more, smaller facilities that serve tighter, more

compact trade areas. These facilities need to be built and managed differently.

22

3 ideas for downsizing the branch

1. Make it easy for customers to do business…

2. Reuse Internet functionality in the branch

3. Eliminate cash handling and processing in the branch

23

Make it easy for customers to do business

without coming to the branch

24

Q. Can customers do everything on the web, mobile and phone?Our approach is to ensure that we have full functionality across channels for all products and services

Q. Can we retain and use historical transaction data to make it easier for the customer?

For overseas funds transfers, customers can send additional funds to certain payees simply by calling, validating the payee and indicating the amount of transfer.

Q. Does it require additional paperwork / forms?The Shinsei PowerFlex Account structure is designed to provide full functionality for FX and investments - every customer has access to 10 currencies, Mutual fund and FX buy / sell

25

Reuse Internet functionality in the branch

26

Internet functionality [remote A/c opening]

Customer uses Internet a/c opening module

Starter Kit

PIN mailer

Card embossing

27

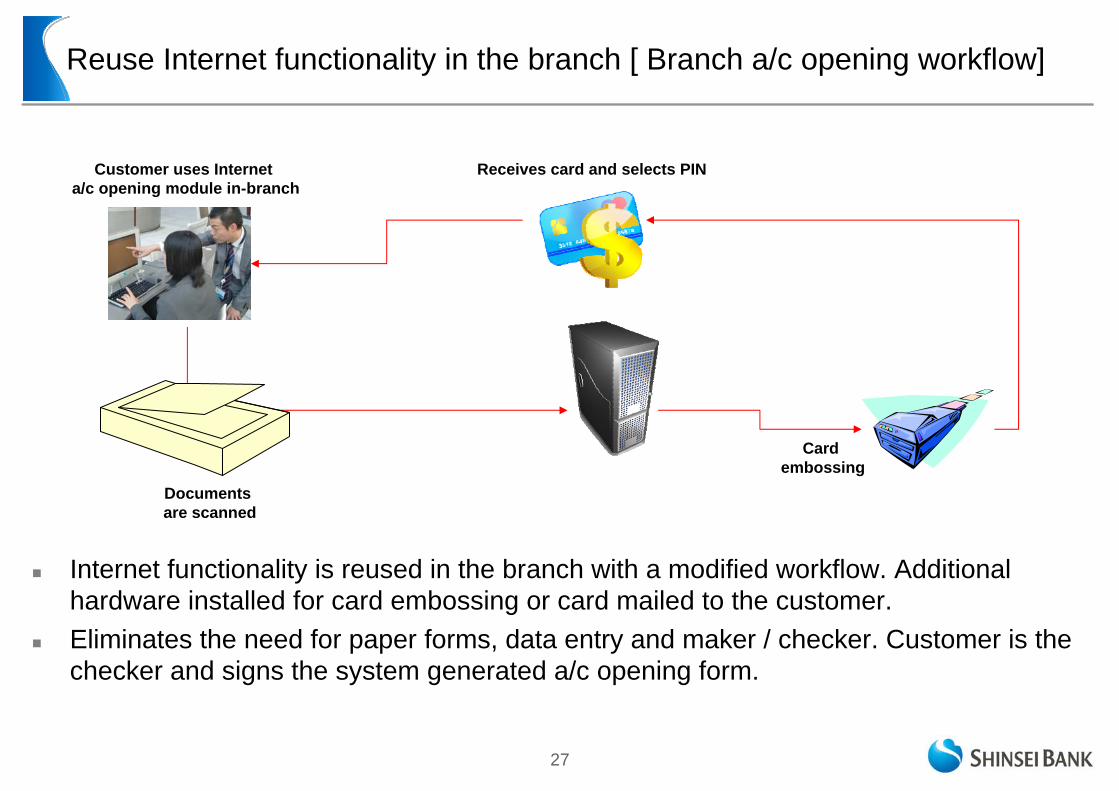

Internet functionality is reused in the branch with a modified workflow. Additional hardware installed for card embossing or card mailed to the customer.Eliminates the need for paper forms, data entry and maker / checker. Customer is the checker and signs the system generated a/c opening form.

Reuse Internet functionality in the branch [ Branch a/c opening workflow]

Card embossing

Customer uses Internet a/c opening module in-branch

Receives card and selects PIN

Documents are scanned

28

Using technology and an “assisted” customer experience

29

Some thoughts on self-service…

When you think of self-service, do you think of it as a cost savings or as customer service?

Cost savings is a primary benefit of self-service. That is a fact.

Conversely, if your idea of self-service is taken from the viewpoint of making customers’ lives easier – with faster and simpler transaction processing and customer service – then you’ve shown customers that they are important to you and that you’re thinking of them, not just the bank

Source: BAI - The Conundrum of Self-Service: Cost Savings or Customer Service? By NICOLE STURGILL

30

Airlines - before

When self check-in kiosks were first introduced, customers found them confusing and lamented the loss of the counter agent…..

31

Airlines - now

….fast forward to today when airlines have agents stationed in the kiosk area to answer questions and guide customers through the process

32

Customer experience

“Indeed, the bank’s services were entirely self-completed; the staff was present only to provide assistance as needed. Transactions took place online, at Internet portals in the branch.”David M. Upton & Virginia A. Fuller, Information Technology and Innovation at Shinsei Bank, Harvard Business School Case

STAFF COMPLETEDSELF COMPLETED WITH ASSISTANCE

33

Reuse Internet modules for all investment product sales [under development]

This will eliminate paper forms, order booking data entry and checks and will ensure version control, audit trails and improved compliance with customer protection.

Staff uses Internet Investment product module

with modified workflow

Order placement done exactly as per Internet process

Order confirmation handed over

Prospectus / solicitation documents throughprint on demand for version control & audit trails

34

Eliminate cash handling and processing in the branch

35

Cashless tellers

“Tellers were cashless. If a customer wanted to deposit or withdraw money, the teller would walk over to an ATM with the customer and execute the transaction with the customer’s participation.”David M. Upton and Bradley R. Staats, Radically Simple IT, Harvard Business Review - March 2008

STAFF ASSISTED

36

Eliminate processing in the branch

The branch receives the customer request, completes the verification and sends the work to a remote processing center.The branch also educates the customer that this can be done remote, captures the email address and signs up e-statement delivery.

Customer hands over transaction request Branch verifies the

Request and scans the form

Branch Remote processing center

37

3 additional ideas:

1. Sales process automation – is it as automated as the “best in class”collections process?

2. Video consulting – an opportunity to create staffing flexibility and reduction in branch headcount.

3. Record all branch sales interactions [audio / video] – compliance checks can be done remote.

38

RELATIONSHIPMANAGER

RELATIONSHIPMANAGER

Empowering people to succeed –Wealth Management CRM process at Shinsei Bank

CUSTOMERCUSTOMER

Customer managementBased on customer profitability and potential. Matched with RM – skill based assignmentPrioritization and coverageActivity tracking and conversion performance

Customer managementBased on customer profitability and potential. Matched with RM – skill based assignmentPrioritization and coverageActivity tracking and conversion performance

Sales & Marketing effectivenessSales activity & effectiveness dashboardsCustomized views for managementEffectiveness of marketing campaignsImmediate feedback for all functional areas

Sales & Marketing effectivenessSales activity & effectiveness dashboardsCustomized views for managementEffectiveness of marketing campaignsImmediate feedback for all functional areas

Sales contact and service request management toolCustomer contact data, preferences & history Sales opportunities developed centrallyAutomated prompts for follow ups & opportunitiesCross channel view of service requestsRM has full view of service history and resolutionstatus

Sales contact and service request management toolCustomer contact data, preferences & history Sales opportunities developed centrallyAutomated prompts for follow ups & opportunitiesCross channel view of service requestsRM has full view of service history and resolutionstatus

Customer profile, product balances and historyFull view of customer product holding [inc. 3rd party]Customer profile, goals, risk profile and experienceis recorded and product performance is reviewedHistory is captured – shows advise and actions takenHousehold linkages can be viewedReferrals are recorded and tracked

Customer profile, product balances and historyFull view of customer product holding [inc. 3rd party]Customer profile, goals, risk profile and experienceis recorded and product performance is reviewedHistory is captured – shows advise and actions takenHousehold linkages can be viewedReferrals are recorded and tracked

Product performance, research and advisoryProduct performance data available [various views]Portfolio review tools and analytics can help theRM to guide the advisory processMarket outlook, investment manager commentsand research reports available for consultative sales

Product performance, research and advisoryProduct performance data available [various views]Portfolio review tools and analytics can help theRM to guide the advisory processMarket outlook, investment manager commentsand research reports available for consultative sales

Compliance and privacy protectionAudit trails of customer interaction – audio / video recordingsReview process to ensure that customers protectionmeasures are effectively implementedException reviews of customer profile vs. product features

Compliance and privacy protectionAudit trails of customer interaction – audio / video recordingsReview process to ensure that customers protectionmeasures are effectively implementedException reviews of customer profile vs. product features

39

The Shinsei Bank Consulting Spot experience

40

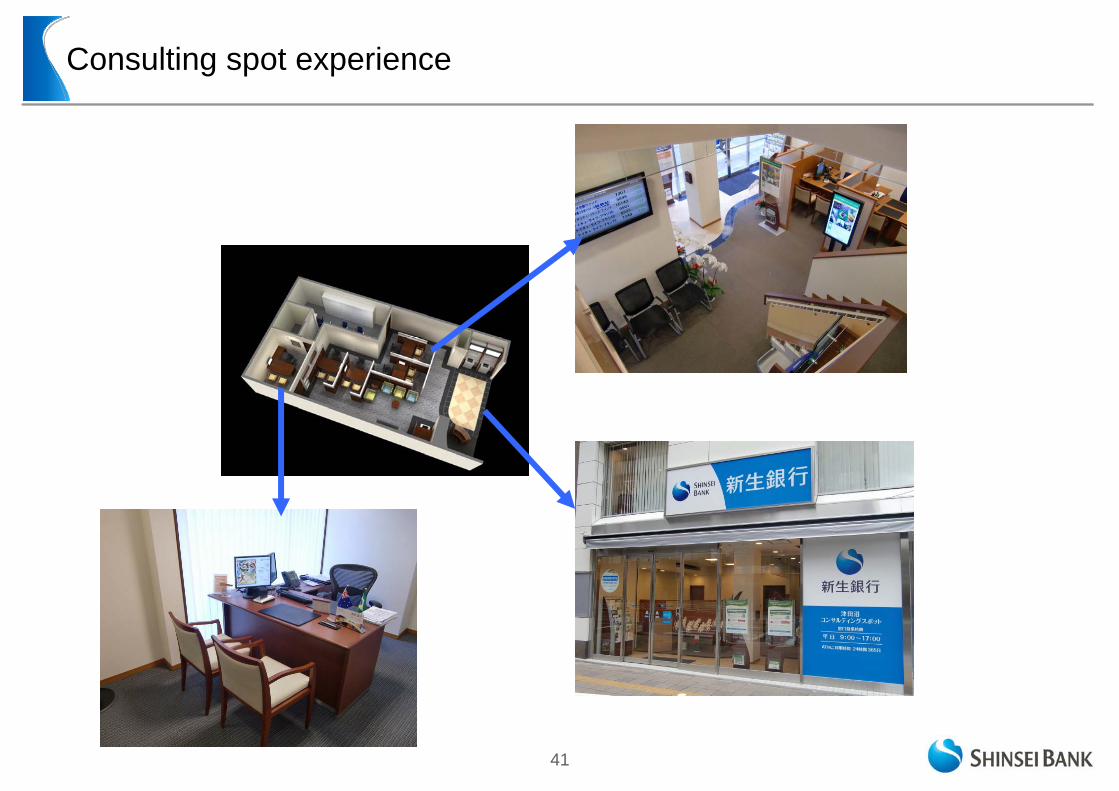

The Consulting Spot is a “sales only” mini branch

We are expanding our branch network with this model: 4-5 staff 75-100 sq. metersHub and spoke model 75 - 85% lower CAPEX & OPEX than a “hub” branchProactive sales model that targets:

1. Relationship growth with existing customers2. Acquisition of new customers

“Cashless” [ATMs only], “Paperless” [imaging], “Sales &service only” [minimal branch operations & centralized processing]

41

Consulting spot experience

42

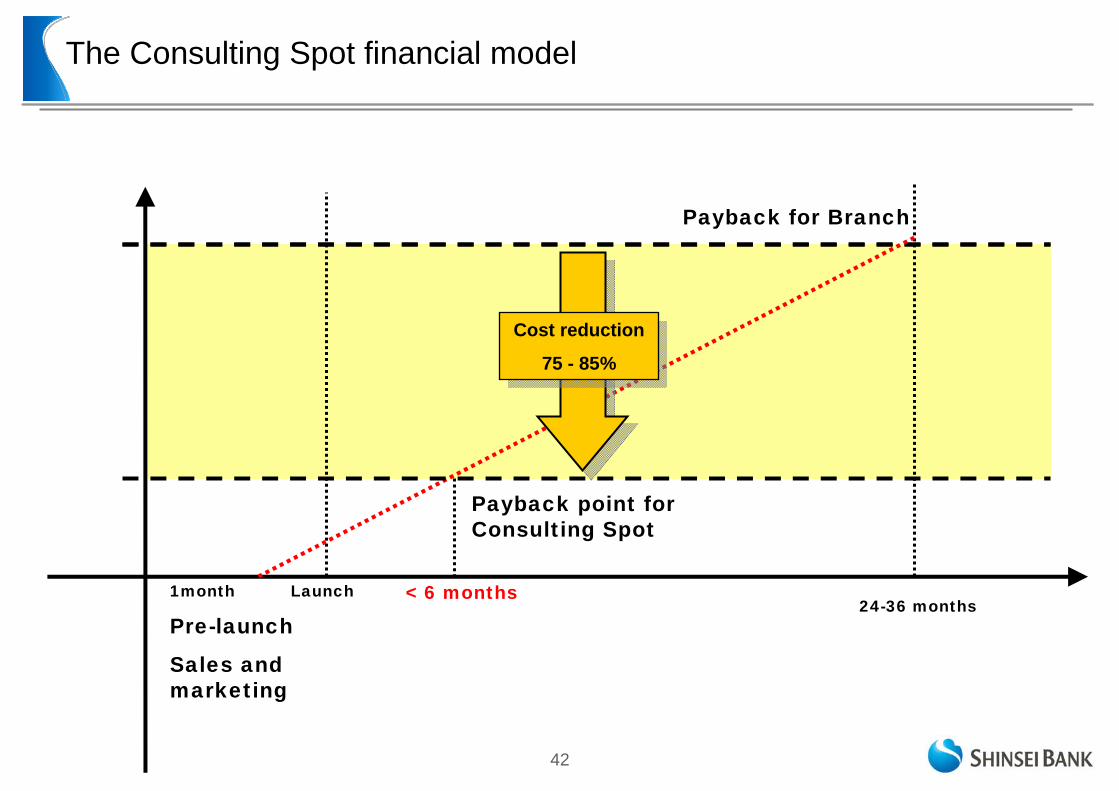

The Consulting Spot financial model

Payback for Branch

Launch24-36 months

Payback point for Consulting Spot

1month

Pre-launch

Sales and marketing

< 6 months

Cost reduction

75 - 85%

Cost reduction

75 - 85%

The f irst 7 Consult ing Spots

opened in FY 2009 achieved

Break even in the first month

o f o p e r a t i o n s a t a d i r e c t

c o n t r i b u t i o n l e v e l