LabourMarketInformation (LMI)’andTrainingNeeds Report’ · 2013!BC!Silviculture!!...

170

2013 BC Silviculture Labour Market Information (LMI) and Training Needs Report Funding provided through the Canada-British Columbia Labour Market Development Agreement

-

Upload

nguyenkhue -

Category

Documents

-

view

216 -

download

0

Transcript of LabourMarketInformation (LMI)’andTrainingNeeds Report’ · 2013!BC!Silviculture!!...

2013 BC Silviculture

Labour Market Information (LMI) and Training Needs

Report

Funding provided through the Canada-British Columbia Labour Market Development Agreement

Page 2 of 170

Prepared by:

Dialogue Research

#21 Dallas Rd

Victoria, British Columbia, Canada, V8V 4Z9

http://www.dialogueresearch.com/directions

March 31, 2014

Page 3 of 170

Contents List of Tables ................................................................................................................................................ 6

Acknowledgements ................................................................................................................................... 11 Background ................................................................................................................................................ 12

Executive Summary ................................................................................................................................... 13 Structure of Report .................................................................................................................................... 19 Methodology ............................................................................................................................................. 20

1. Instrumentation ......................................................................................................................... 20

2. Sampling .................................................................................................................................... 20

3. Incentives ................................................................................................................................... 23

4. Sample Management ................................................................................................................. 24

5. Data Cleaning Notes ................................................................................................................... 24

6. Data Reporting Notes ................................................................................................................. 24

Section 1 Workforce Supply and Demand ................................................................................................. 27 A. EMPLOYMENT ................................................................................................................................ 28

1. Survey Based Employment Estimates ........................................................................................ 28

2. Employment of Field Workers and Crew Bosses ....................................................................... 28

3. Field Workers By Types of Activity ............................................................................................. 29

B. EMPLOYMENT PRODUCTION STANDARDS .................................................................................... 29

1. Tree Planting .............................................................................................................................. 29

2. Brushing and Spacing ................................................................................................................. 31

3. Wildfire Fighting ......................................................................................................................... 35

C. ESTIMATED BC SILVICULTURE WORKFORCE .................................................................................. 37

1. Approach #1 – Using Provincial Production Data ...................................................................... 37

2. Approach #2 – Extrapolation Based on Coverage Rates by Size of Employer ............................ 38

D. BC SILVICULTURE WORKFORCE DEMAND DRIVERS AND OUTLOOK .............................................. 39

1. Tree Planting .............................................................................................................................. 39

2. Brushing and Spacing ................................................................................................................. 40

3. Wildfire Fighting ......................................................................................................................... 41

E. HISTORICAL WORKFORCE SUPPLY ................................................................................................. 41

Section 2 Employee Profile (Respondents) ................................................................................................ 43 F. DEMOGRAPHICS ............................................................................................................................ 44

1. Age ............................................................................................................................................. 44

2. Gender ....................................................................................................................................... 44

3. Educational Status ..................................................................................................................... 45

Page 4 of 170

4. First Nations Status .................................................................................................................... 46

G. CAREER HISTORY ............................................................................................................................ 47

1. Total Years of Experience ........................................................................................................... 47

2. Years of Experience by Type Worker ......................................................................................... 47

3. Employer History ....................................................................................................................... 48

H. 2013 EXPERIENCE ........................................................................................................................... 49

1. Roles and Responsibilities .......................................................................................................... 49

2. Subsector Activity ...................................................................................................................... 54

3. Locations Worked ...................................................................................................................... 54

4. Accommodations and Camp Services ........................................................................................ 56

5. Employer History 2013 ............................................................................................................... 58

6. Employee Injuries ...................................................................................................................... 59

7. Income ....................................................................................................................................... 60

8. Technology Access ..................................................................................................................... 65

Section 3 Employer Profile (Respondents) ................................................................................................ 67 1. Employer Population ................................................................................................................. 68

I. CORPORATE INFORMATION .......................................................................................................... 68

1. Activity by Subsector .................................................................................................................. 68

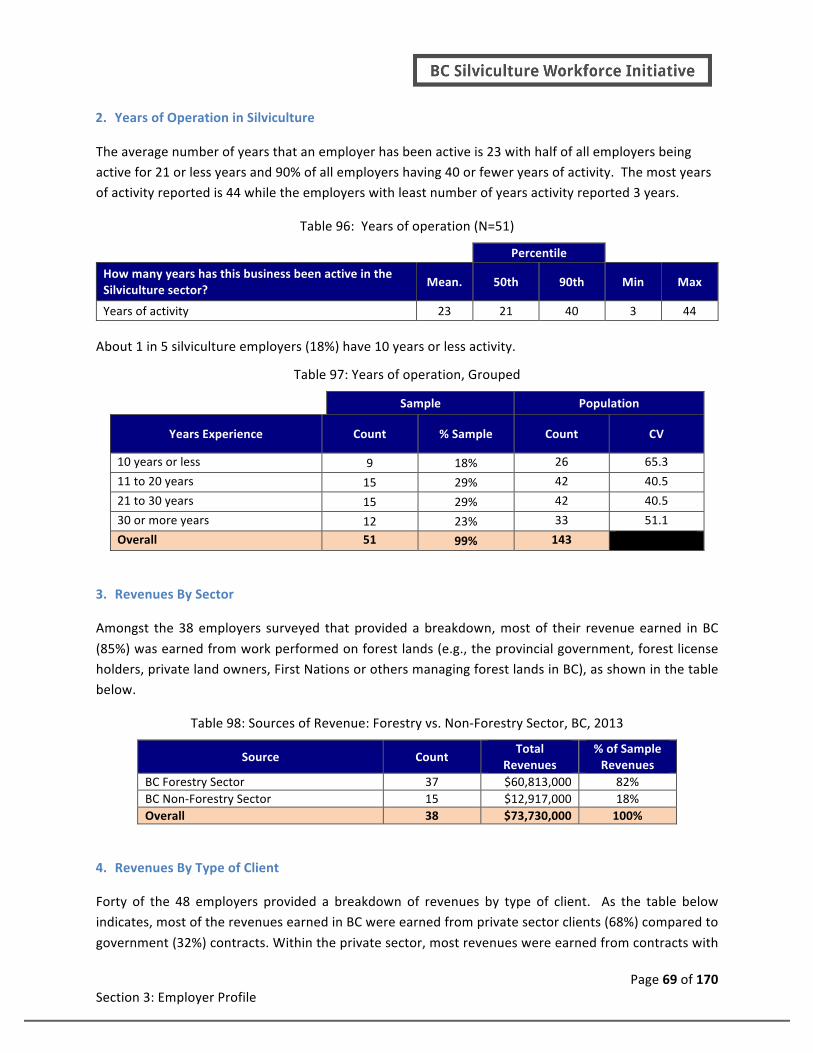

2. Years of Operation in Silviculture .............................................................................................. 69

3. Revenues By Sector .................................................................................................................... 69

4. Revenues By Type of Client ........................................................................................................ 69

5. Revenues By Activity .................................................................................................................. 71

6. Revenues By Region ................................................................................................................... 72

7. Operations -‐ BC Regions ............................................................................................................. 72

8. Incorporated versus Unincorporated ........................................................................................ 73

9. Number of Operated Businesses ............................................................................................... 74

10. Employer Years of Experience ................................................................................................ 75

11. Employer Roles and Responsibilities ...................................................................................... 75

J. WORKFORCE .................................................................................................................................. 76

1. Crew Sizes .................................................................................................................................. 76

2. Diversity of Workers .................................................................................................................. 76

K. OPINIONS AND OUTLOOK .............................................................................................................. 76

1. 2013 Revenue ............................................................................................................................ 76

2. Future Revenue .......................................................................................................................... 77

3. Future Expenditures by Customers ............................................................................................ 78

Page 5 of 170

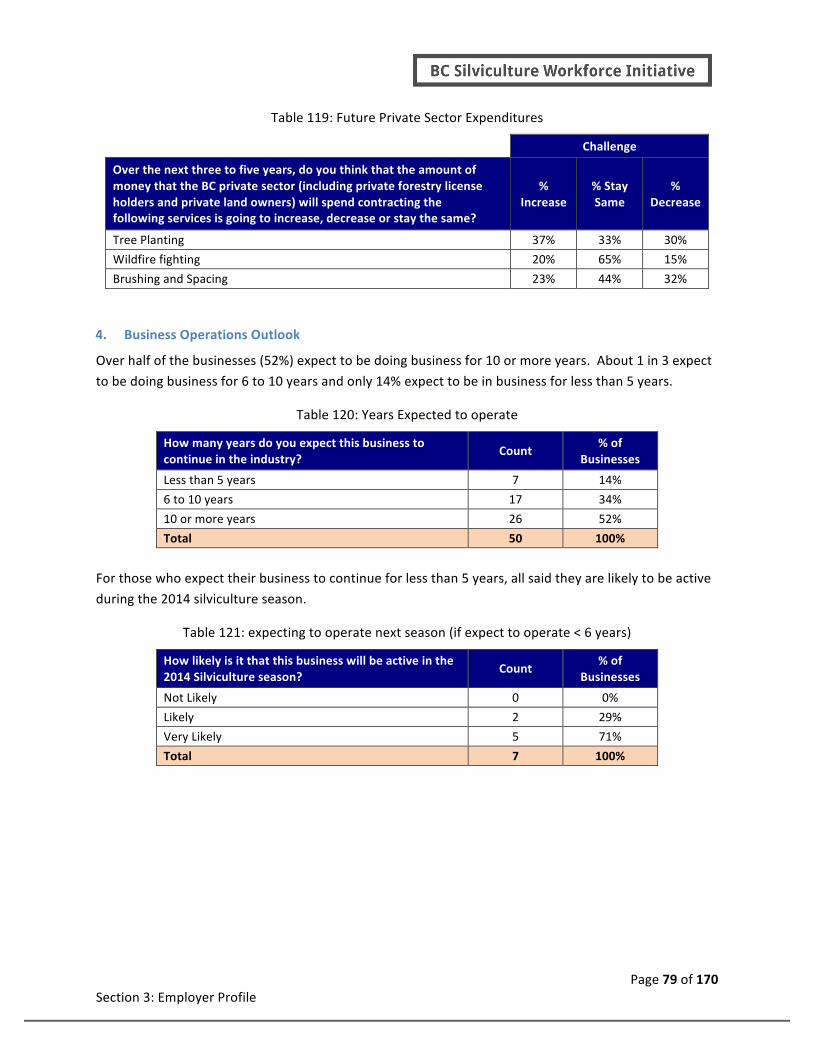

4. Business Operations Outlook ..................................................................................................... 79

5. Expansion Plans ......................................................................................................................... 80

6. Fate of Operations ..................................................................................................................... 80

7. Reasons for Exit .......................................................................................................................... 81

8. Sector Associations .................................................................................................................... 82

Section 4 Recruitment & Retention Findings ............................................................................................. 83 L. RECRUITMENT PRIORITIES ............................................................................................................. 84

M. CURRENT PRACTICES ..................................................................................................................... 85

1. Employer Recruitment and Evaluation ...................................................................................... 85

2. Employee Entrance to Sector ..................................................................................................... 89

3. Employee Exit from Sector ......................................................................................................... 90

4. Employer Support to Employees ............................................................................................... 93

N. KEY DRIVER ANALYSIS .................................................................................................................... 94

1. Key Driver Analysis – Willingness to Recommend Employer ..................................................... 98

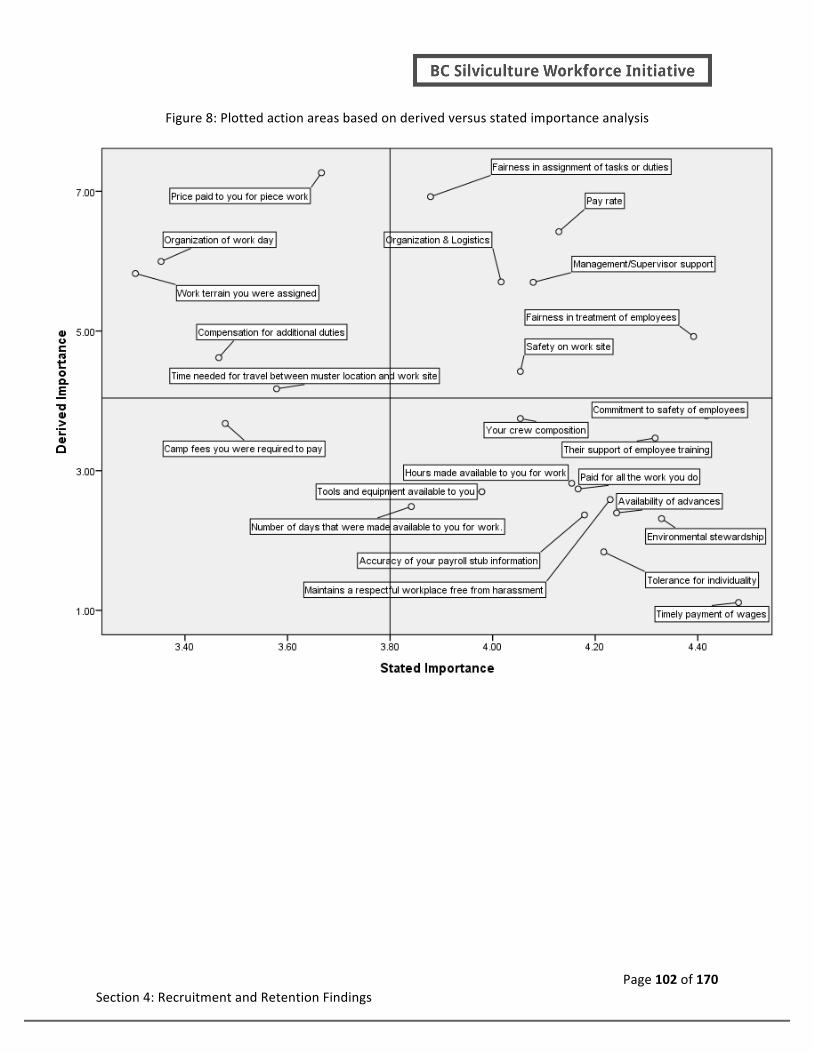

O. DERIVED VERSUS STATED IMPORTANCE ..................................................................................... 100

1. Action Areas to Improve Employee Workday Experience. ...................................................... 100

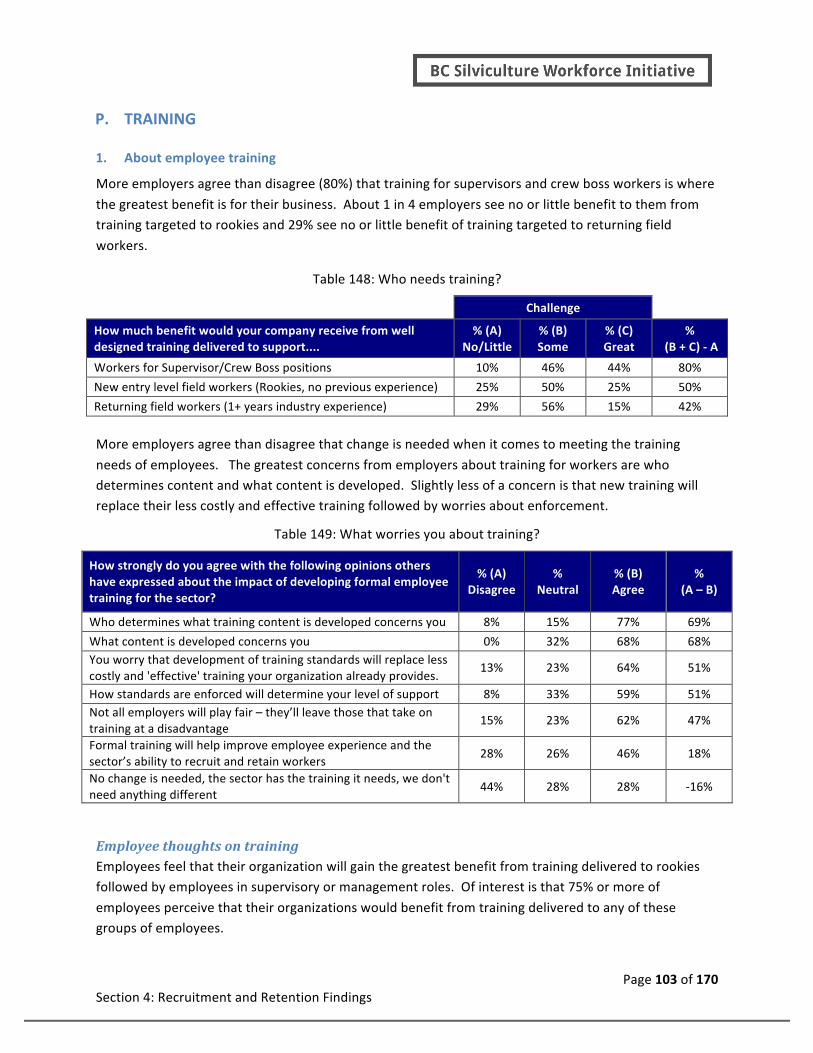

P. TRAINING ..................................................................................................................................... 103

1. About employee training ......................................................................................................... 103

Q. GENERAL FINDINGS ...................................................................................................................... 104

1. Employer’s Perspective on their Workforce ............................................................................ 104

2. Workforce Social Network ....................................................................................................... 105

Appendix 1 – Personality Assessments (GRIT) ......................................................................................... 106 Appendix 2 – Why workers enter/exit sector (summary) ........................................................................ 107 Appendix 3 – Employee Survey ................................................................................................................ 109

Appendix 4 – Employee Quality Assurance Survey .................................................................................. 133 Appendix 5 – Employer Initial Survey Invite ............................................................................................ 137 Appendix 6 – Employer Survey ................................................................................................................ 138

Appendix 7– Accuracy of BCFSC SAFE Companies Classifications ............................................................ 170

Page 6 of 170

List of Tables

TABLE 1: SAMPLE FRAME LIST COUNTS BASED ON BCFSC SAFE COMPANIES CERTIFICATION PROFILES 21 TABLE 2: SURVEY PAGE DROP OFF 23 TABLE 3: AVERAGE NUMBER OF EMPLOYEES, BC, 2013 28 TABLE 5: FIELD WORKER EFFORT BY ACTIVITY, BC, 2013 29 TABLE 6: TREE PLANTING ACTIVITIES: EMPLOYER SURVEY, BC, 2013 29 TABLE 7: TREE PLANTING ACTIVITY BY MONTHS ACTIVE, BC, 2013 30 TABLE 8: TREE PLANTING IN BC, 2008/09 TO 2012/13 30 TABLE 9: TREE PLANTING ACTIVITIES: BC INDUSTRY OVERALL, 2012/2013 31 TABLE 10: BRUSHING AND SPACING ACTIVITIES (EMPLOYER SURVEY), BC, 2013 31 TABLE 11: BRUSHING AND SPACING ACTIVITY BY MONTHS ACTIVE, BC, 2013 32 TABLE 12: BRUSHING ACTIVITIES (EMPLOYER SURVEY), BC, 2013 33 TABLE 13: BRUSHING ACTIVITIES IN BC, 2008/09 TO 2012/13 33 TABLE 14: BRUSHING ACTIVITIES: BC INDUSTRY OVERALL, 2012/13 33 TABLE 15: SPACING ACTIVITIES (EMPLOYER SURVEY), BC, 2013 34 TABLE 16: JUVENILE SPACING ACTIVITIES IN BC, 2008/09 TO 2012/13 34 TABLE 17: SPACING ACTIVITIES: BC INDUSTRY OVERALL, 2013 35 TABLE 18: WILDFIRE FIGHTING ACTIVITIES (EMPLOYER SURVEY), BC, 2013 35 TABLE 19: WILDFIRE FIGHTING ACTIVITY BY MONTHS ACTIVE, BC, 2013 36 TABLE 20: NUMBER, HECTARES, AND COST OF FOREST FIRES FOUGHT IN BC, 2005-‐2012 36 TABLE 21: APPROACH #1: BASED ON PROVINCIAL PRODUCTION DATA 37 TABLE 22: ESTIMATE COVERAGE OF THE TREE PLANTING, BRUSHING AND SPACING SUB-‐SECTORS 38 TABLE 23: APPROACH #2: PROJECTIONS BASED ON EMPLOYER POPULATION LISTS 39 TABLE 24: HISTORICAL SILVICULTURE WORKFORCE SUPPLY, 2008/09 TO 2012/13 42 TABLE 25: AGE OF WORKER 44 TABLE 26: AGE GROUPS 44 TABLE 27: GENDER 44 TABLE 28: EMPLOYEE REGISTERED IN EDUCATIONAL ACTIVITY 45 TABLE 29: ENROLLED EMPLOYEES -‐ TYPE OF EDUCATIONAL ACTIVITY 45 TABLE 30: ENROLLED EMPLOYEES – YEARS LEFT IN PROGRAM 46 TABLE 31: EMPLOYEES – FIRST NATIONS 46 TABLE 32: FIRST NATIONS – BAND MEMBERSHIP 46 TABLE 33: YEARS OF EXPERIENCE 47 TABLE 34: YEARS OF EXPERIENCE BY TYPE RESPONSIBILITY – FIELD WORKER 47 TABLE 35: YEARS OF EXPERIENCE BY TYPE RESPONSIBILITY – LEAD HAND 47 TABLE 36: YEARS OF EXPERIENCE BY TYPE RESPONSIBILITY – SUPERVISION OR CREW BOSS 47 TABLE 37: YEARS OF EXPERIENCE BY TYPE RESPONSIBILITY – PROJECT MANAGER 48 TABLE 38: NUMBER OF EMPLOYERS DURING CAREER 48 TABLE 39: TRANSIENT EMPLOYEE 48 TABLE 40: ROLES AND RESPONSIBILITIES – ALL SILVICULTURE EMPLOYEES 49 TABLE 41: COUNT OF POSITIONS -‐ ALL SILVICULTURE EMPLOYEES 49 TABLE 42: ROLES AND RESPONSIBILITIES – LEAD HAND 49 TABLE 43: COUNT OF POSITIONS – LEAD HAND 50 TABLE 44: ROLES AND RESPONSIBILITIES – LEAD HAND 50

Page 7 of 170

TABLE 45: COUNT OF POSITIONS – LEAD HAND 50 TABLE 46: ROLES AND RESPONSIBILITIES – SUPERVISOR OR CREW BOSS 51 TABLE 47: COUNT OF POSITIONS – SUPERVISOR OR CREW BOSS 51 TABLE 48: ROLES AND RESPONSIBILITIES – PROJECT MANAGER 51 TABLE 49: COUNT OF POSITIONS – PROJECT MANAGER 51 TABLE 50: TREE PLANTERS: SUBSECTORS WORKED IN 52 TABLE 51: TREE PLANTERS: POSITIONS HELD 52 TABLE 52: BRUSHING & SPACING EMPLOYEES: SUBSECTORS WORKED IN 52 TABLE 53: BRUSHING & SPACING: POSITIONS WORKED IN 53 TABLE 54: WILDFIRE FIGHTING EMPLOYEES: SUBSECTORS WORKED IN 53 TABLE 55: WILDFIRE FIGHTING: POSITIONS WORKED IN 53 TABLE 56: EMPLOYEE SUBSECTOR ACTIVITY 54 TABLE 57: NUMBER OF SUBSECTORS WORKED IN BY AN SILVICULTURE EMPLOYEE 54 TABLE 58: WORK PROVINCE -‐ ALL SILVICULTURE EMPLOYEES 54 TABLE 59: NUMBER OF BC REGIONS WORKED IN 2013 55 TABLE 60: WORK REGION -‐ BC 55 TABLE 61: NUMBER OF BC REGIONS WORKED IN 55 TABLE 62: TOTAL NUMBER OF LOCATIONS STAYED AT 56 TABLE 63: NUMBER OF LOCATIONS CORRELATION WITH… 56 TABLE 64: TYPE ACCOMMODATION 56 TABLE 65: TYPES OF ACCOMMODATIONS CORRELATION WITH… 57 TABLE 66: LENGTH OF STAY AT CAMPS 57 TABLE 67: LENGTH OF STAY AT HOTELS 57 TABLE 68: LENGTH OF STAY AT HOUSE RENTALS 57 TABLE 69: CAMP INTERNET ACCESS 58 TABLE 70: CAMP CELL PHONE COVERAGE 58 TABLE 71: NUMBER OF 2013 EMPLOYERS 58 TABLE 72: DURATION WITH EMPLOYER 2013 58 TABLE 73: NUMBER OF 2013 EMPLOYERS CORRELATION WITH YEARS LEFT IN CAREER 59 TABLE 74: DAYS MISSED DUE TO INJURY 59 TABLE 75: EMPLOYEE TYPE INJURY 59 TABLE 76: EMPLOYEE TYPE INJURY 60 TABLE 77: PAYMENT METHODS -‐ ALL SILVICULTURE EMPLOYEES 60 TABLE 78: PAYMENT METHODS BY TYPE POSITION 60 TABLE 79: SILVICULTURE INCOME 61 TABLE 80: ACTUAL DAILY WAGE AND EXPECTED SILVICULTURE INCOME 61 TABLE 81: ACTUAL DAILY WAGE AND EXPECTED SILVICULTURE INCOME 61 TABLE 82: DAILY WAGE RELATIONSHIP TO KEY OUTCOMES 62 TABLE 83: SILVICULTURE INCOME 62 TABLE 84: ACTUAL VERSUS INTERNET ACCESS 62 TABLE 85: TOTAL SILVICULTURE INCOME RELATIONSHIP TO KEY OUTCOMES 63 TABLE 86: OTHER INCOME 63 TABLE 87: SILVICULTURE INCOME AS % OF TOTAL INCOME 63 TABLE 88: INCOME DEPENDENCY RELATIONSHIP TO KEY OUTCOMES 63 TABLE 89: WHAT LIMITS YOUR SILVICULTURE INCOME (NUMBER OF EMPLOYEE WHO SELECTED EACH FACTOR) 64

Page 8 of 170

TABLE 90: WHAT LIMITS YOUR SILVICULTURE INCOME (WHEN SELECTED) 64 TABLE 91: COUNT OF PAYMENT METHODS -‐ ALL SILVICULTURE EMPLOYEES 64 TABLE 92: SATISFACTION WITH PAYROLL 65 TABLE 93: TYPE MOBILE PHONE 65 TABLE 94: SOCIAL MEDIA SITES & SERVICES 66 TABLE 95: EMPLOYER POPULATION LISTS 68 TABLE 96: SILVICULTURE SUB SECTOR ACTIVITIES, BC 2013 68 TABLE 97: YEARS OF OPERATION (N=51) 69 TABLE 98: YEARS OF OPERATION, GROUPED 69 TABLE 99: SOURCES OF REVENUE: FORESTRY VS. NON-‐FORESTRY SECTOR, BC, 2013 69 TABLE 100: SOURCES OF REVENUE: GOVERNMENT VS. PRIVATE SECTOR, BC, 2013 70 TABLE 101: OTHER REVENUE SOURCES, BC, 2013 70 TABLE 102: COMPANIES THAT HAD WORK (CONTRACTS) IN PARTNERSHIP WITH FIRST NATIONS, BC, 2013 71 TABLE 103: SOURCES OF REVENUE: ACTIVITIES AND SERVICES, BC, 2013 71 TABLE 104: SOURCES OF REVENUE: IN BC VS. OUTSIDE OF BC, 2013 72 TABLE 105: NUMBER OF BC REGIONS WORKED (N=51) 72 TABLE 106: WORK REGION -‐ BC 73 TABLE 107: TYPE OF BUSINESS, 2013 73 TABLE 108: NUMBER OF SILVICULTURE BUSINESSES OPERATED, 2013 74 TABLE 109: NUMBER OF SILVICULTURE BUSINESSES OPERATED, 2013 74 TABLE 110: EMPLOYER YEARS OF SILVICULTURE EXPERIENCE (N=54) 75 TABLE 111: EMPLOYER YEARS OF SILVICULTURE EXPERIENCE, GROUPED 75 TABLE 112: RESPONDENT ROLES AND RESPONSIBILITIES 75 TABLE 113: CREW SIZES (FIELD WORKERS), BC, 2013 76 TABLE 114: TYPES OF EMPLOYEES, BC, 2013 76 TABLE 115: 2013 BUSINESS INCOME EXPECTATIONS 77 TABLE 116: EXPECTED BUSINESS PERFORMANCE IN 2014 77 TABLE 117: YEAR OVER YEAR BUSINESS INCOME COMPARED (2012 TO 2013) 77 TABLE 118: OPTIMISTIC ABOUT SECTOR 78 TABLE 119: FUTURE GOVERNMENT EXPENDITURE 78 TABLE 120: FUTURE PRIVATE SECTOR EXPENDITURES 79 TABLE 121: YEARS EXPECTED TO OPERATE 79 TABLE 122: EXPECTING TO OPERATE NEXT SEASON (IF EXPECT TO OPERATE < 6 YEARS) 79 TABLE 123: BUSINESSES THAT WOULD PURSUE EXPANSION 80 TABLE 124: FACTORS THAT LIMIT BUSINESS EXPANSION 80 TABLE 125: BUSINESS CONTINUITY 81 TABLE 126: BUSINESS CONTINUITY BY OPERATING YEARS EXPECTED 81 TABLE 127: REASONS COMPANY CLOSES OPERATIONS -‐ TOTAL TIMES CHOSEN (1ST, 2ND OR 3RD) 81 TABLE 128: WHEN CHOSEN 82 TABLE 129: RATING INDUSTRY ASSOCIATIONS 82 TABLE 130: HIRING CHALLENGES 84 TABLE 131: HIRING OF ROOKIES 84 TABLE 132: HIRING OF FIELD WORKERS 84 TABLE 133: EMPLOYEE RECRUITMENT STRATEGY 85 TABLE 134: SECTOR PROMOTION – POPULATION PRIORITIES 85

Page 9 of 170

TABLE 135: SECTOR PROMOTION – WHO SHOULD LEAD THE WAY? 86 TABLE 136: EMPLOYEE SCREENING 87 TABLE 137: NEW HIRE EVALUATION PRACTICES 87 TABLE 138: RELATIONSHIP BETWEEN EMPLOYEE GRIT SCORE AND SELECTED KEY OUTCOMES: 88 TABLE 139: ROLE OF INFORMATION SOURCES 89 TABLE 140: WHY EMPLOYEES QUIT WORKING IN THE SECTOR 91 TABLE 147: AGE GROUPS 92 TABLE 148: RELATIONSHIP BETWEEN YEARS OF EXPERIENCE AND…: 92 TABLE 141: EMPLOYEE SUPPORT BY EMPLOYER? 93 TABLE 142: GOING THE EXTRA MILE CORRELATION WITH KEY OUTCOMES 93 TABLE 143: RELATIONSHIPS – KEY DRIVER AND ACTION AREAS 95 TABLE 144: RELATIONSHIPS – KEY DRIVERS AND ACTION AREAS 97 TABLE 145: OVERALL EMPLOYER PROFESSIONALISM SATISFACTION 99 TABLE 146: DERIVED VERSUS STATED IMPORTANCE CORRELATIONS 101 TABLE 149: WHO NEEDS TRAINING? 103 TABLE 150: WHAT WORRIES YOU ABOUT TRAINING? 103 TABLE 151: EMPLOYEE THOUGHTS ABOUT WHO TO TRAIN 104 TABLE 152: EMPLOYEE REPORTED OVERALL SATISFACTION 104 TABLE 153: EMPLOYEE ACTUAL EMPLOYEE SATISFACTION (0 TO 10) 104 TABLE 154: EMPLOYER PERCEPTION OF EMPLOYEE SATISFACTION (0 TO 10) 104 TABLE 155: SOCIAL CONNECTIONS WITH OTHER EMPLOYEES 105 TABLE 156: RELATIONSHIP BETWEEN SOCIAL CONNECTIONS AND LIKELIHOOD TO RETURN TO THE SECTOR IN 2014

105 TABLE 157: GRIT SUMMARY STATISTICS – SILVICULTURE EMPLOYEES 106 TABLE 158: GRIT QUESTIONS FOR SILVICULTURE EMPLOYEES 106 TABLE 159: SUMMARY OF WHAT ATTRACTED WORKERS TO SECTOR 107 TABLE 160: SUMMARY OF REASONS EMPLOYEE WILL LEAVE SECTOR 108

Page 10 of 170

List of Figures

FIGURE 1: SEEDLINGS PLANTED BY RESPONSIBILITY .................................................................................................. 40 FIGURE 2: TREE PLANTER WORKFORCE DEMAND ...................................................................................................... 40 FIGURE 3: SPACING VOLUMES – 2014 TO 2050 .......................................................................................................... 41 FIGURE 4: HISTORIC BC SILVICULTURE WORKFORCE SUPPLY – 2008 TO 2013 ........................................................... 42 FIGURE 5: OTHER INFORMATION SOURCES ............................................................................................................... 86 FIGURE 6: OTHER INFORMATION SOURCES ............................................................................................................... 90 FIGURE 7: REASONS WORKERS ENTERED THE SILVICULTURE SECTOR ....................................................................... 91 FIGURE 8: PLOTTED ACTION AREAS BASED ON DERIVED VERSUS STATED IMPORTANCE ANALYSIS ....................... 102

Page 11 of 170

Acknowledgements

The BC Silviculture Workforce Initiative (BCSWI) is grateful for the commitment and expertise of the Project Committee members who provided their insight and guidance to this labour market research:

• Jake Roos, Loki Tree Service

• John Lawrence, Brinkman Group of Companies

• Natalia Hautala -‐Tree planter

• Sylvia Fenwick-‐Wilson, silviculture worker and instructor

• Carly Zenzen/Crawford Young, Spectrum Resource Group Inc

• Jonathan "Scooter" Clark, Folklore Contracting, Replant.ca

• Chris Akehurst, Akehurst and Galvani Reforestation Ltd

• Sean Ardis, silviculture worker

• John Betts, Western Silvicultural Contractors' Association

• Keith Atkinson, BC First Nations Forestry Council

The BCSWI would like to thank all those employees and employers who participated in the survey. Your participation was essential in creating a better understanding of the silviculture sector labour market

and in the ongoing efforts to keep the silviculture sector a good and rewarding place to work.

The BCSWI achieved its goals through the essential leadership and contributions of its Chair, Suzanne Christensen.

This report was written by Dialogue Research, in partnership with Krista Bax and Ference Weicker and Company.

Page 12 of 170

Background

The actual number of BC silviculture sector employers and employees was unknown. Two years ago, the estimated number of employers working in BC silviculture sector was estimated to be as high as 400 and employees estimates were as much a ± 10,000, none were within ± 1,000. An understanding of the workforce has primarily been based on firsthand experience and qualitative in nature; quantitative survey based information about the workforce has been collected since 2011, but is typically based on sub-‐sets of the sector and not a representative sample. Given these factors, the current and future workforce demand and supply has been unknown.

During the fall of 2013, the BC Silviculture Workforce Initiative (BCSWI) continued and strengthened their labour market information collection efforts for the sector and undertook a multi-‐year labor market information (LMI) research project. This research provides evidence that can be used to confidently estimate the number of employer and employees; as well as, provide quantitative estimates of employer and employee characteristics used to create workforce supply and demand models and inform recruitment and retention plans

Dialogue Research was engaged to perform the labour market information research project and their efforts have been guided by the Chair and Project Committee.

Guiding the research was the goal of answering the following questions:

Research Question Related Content

What is the current size of the workforce for BC’s silviculture subsectors tree planting, wildfire fighting and brush and spacing?

Pg. 37

What has been the historical workforce for the last 5 years for BC’s silviculture subsectors; tree planting, wildfire fighting and brush and spacing?

Pg. 41

What is anticipated required workforce for the next 10 years for BC’s silviculture subsectors; tree planting, wildfire fighting and brush and spacing?

Pg. 39

What are the drivers of workforce demand for BC’s silviculture subsectors; tree planting, wildfire fighting and brush and spacing?

Pg. 39

What is the anticipated growth rate for the next 10 years for BC’s silviculture subsectors; tree planting, wildfire fighting and brush and spacing?

Pg. 39

What is the workforce outlook (difference between supply and demand) for the next 10 years for BC’s silviculture subsectors; tree planting, wildfire fighting and brush and spacing?

2014 LMI report

What is the qualitative description of the workforce of each of BC’s silviculture subsectors; tree planting, wildfire fighting and brush and spacing?

Pg. 43

What are the factors attracting workers to BC’s silviculture subsectors tree planting, wildfire fighting and brush and spacing?

Pg.89

What are the factors retaining workers to BC’s silviculture subsectors tree planting, wildfire fighting and brush and spacing?

Pg. 90, 93, 94, 98,

Can training play a positive role in better recruitment and retention to the BC’s silviculture subsectors tree planting, wildfire fighting and brush and spacing?

Pg. 103

What are factors that can increase an employer’s recruitment success to the BC’s silviculture subsectors tree planting, wildfire fighting and brush and spacing?

Pg. 98

What are the factors that can increase long term retention to BC’s silviculture sector? Pg. 93, 98 What are the current, active successful retention strategies in BC’s silviculture sector? 2014 LMI report

Page 13 of 170

Executive Summary The executive summary includes highlights from the report’s four sections: Section 1: BC Silviculture

Workforce Supply and Demand, Section 2: Employee Profile, Section 3: Employer Profile, and Section 4: Recruitment and Retention.

Section 1: BC Silviculture Workforce Supply and Demand

The BC silviculture workforce supply (2013) is estimated at 7,482 workers – 3,439 tree

planting workers, 1,205 brushing, 96 spacing, 1,634 wildfire fighting (534 industry and 1,100 government) and 1,108 other workers defined

as workers employed by silviculture firms not involved in field duties.

Sub-‐sectors # of Workers

Tree planting 3,439 Brushing 1,205 Spacing 96 Wildfire fighting (industry) 534 Wildfire fighting (gov’t) 1,100 Total Field Staff 6,374 Other Workers 1,108 Total Employment 7,482

Historically, workforce supply has fluctuated for all activities over the past 5 years where the

tree planting workforce has seen a 41% variance, brushing a 27% variance, spacing a 380% variance, and wildfire fighting a 2600%

variance.

Labour demand for tree planting work is primarily driven by the annual allowable cut (AAC) of private licensees and BC Timber Sales (BCTS) and provincial reforestation programs such as Forests for

Tomorrow (FFT) and the Forest Stand Management Fund (FSMF).

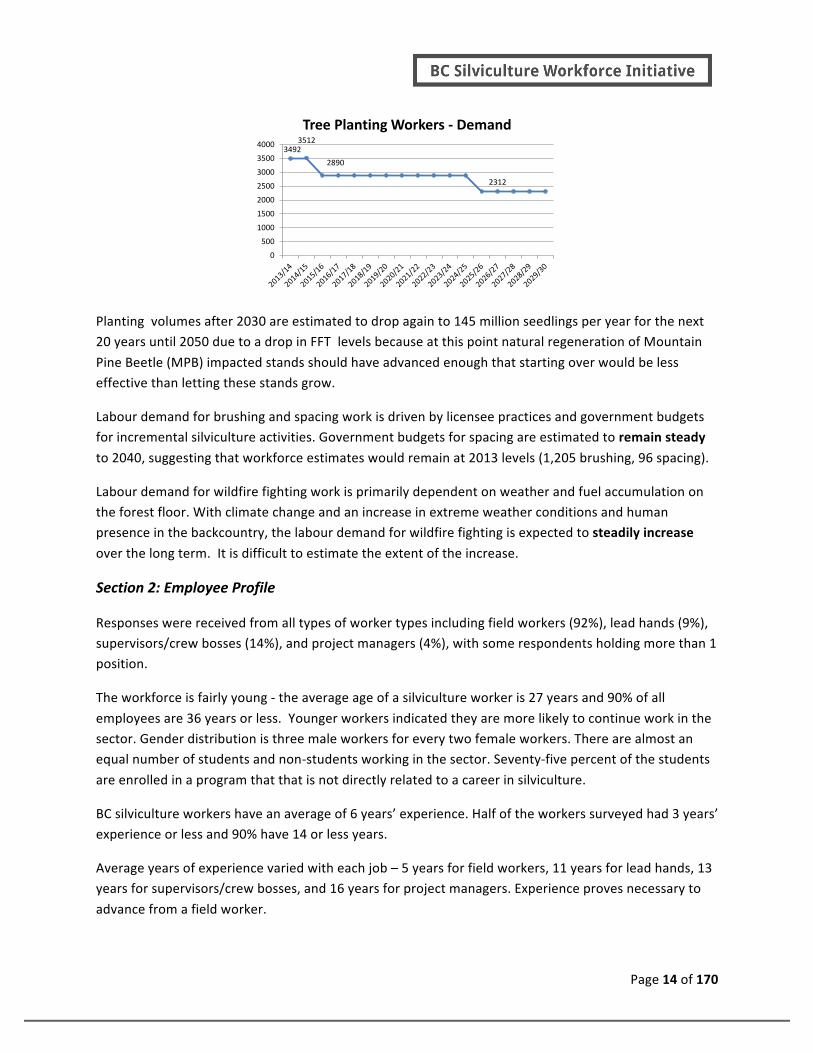

The 2013/14 tree planting estimates are at 241.7 million tree seedlings requiring 3,492 workers and the 2014/15 tree planting estimates are at 243.1 million tree seedlings requiring 3,512 workers. Thereafter,

labour demand will decrease over the long term. Sector estimates are for 200 million tree seedlings to be planted per year for the next 10 years until 2023/24, requiring 2,890 workers annually. In 2024/25, due to the reduction of AAC, planting volumes are estimated to be 160 million tree seedlings requiring

2,312 workers annually and will remain so until 2030.

Page 14 of 170

Planting volumes after 2030 are estimated to drop again to 145 million seedlings per year for the next 20 years until 2050 due to a drop in FFT levels because at this point natural regeneration of Mountain

Pine Beetle (MPB) impacted stands should have advanced enough that starting over would be less effective than letting these stands grow.

Labour demand for brushing and spacing work is driven by licensee practices and government budgets for incremental silviculture activities. Government budgets for spacing are estimated to remain steady

to 2040, suggesting that workforce estimates would remain at 2013 levels (1,205 brushing, 96 spacing).

Labour demand for wildfire fighting work is primarily dependent on weather and fuel accumulation on the forest floor. With climate change and an increase in extreme weather conditions and human presence in the backcountry, the labour demand for wildfire fighting is expected to steadily increase

over the long term. It is difficult to estimate the extent of the increase.

Section 2: Employee Profile

Responses were received from all types of worker types including field workers (92%), lead hands (9%), supervisors/crew bosses (14%), and project managers (4%), with some respondents holding more than 1 position.

The workforce is fairly young -‐ the average age of a silviculture worker is 27 years and 90% of all

employees are 36 years or less. Younger workers indicated they are more likely to continue work in the sector. Gender distribution is three male workers for every two female workers. There are almost an equal number of students and non-‐students working in the sector. Seventy-‐five percent of the students

are enrolled in a program that that is not directly related to a career in silviculture.

BC silviculture workers have an average of 6 years’ experience. Half of the workers surveyed had 3 years’ experience or less and 90% have 14 or less years.

Average years of experience varied with each job – 5 years for field workers, 11 years for lead hands, 13 years for supervisors/crew bosses, and 16 years for project managers. Experience proves necessary to

advance from a field worker.

34923512

2890

2312

0

500

1000

1500

2000

2500

3000

3500

4000

Tree Planting Workers -‐ Demand

Page 15 of 170

Employees reported working for on average 3 employers in their career and 90% reported working for no more than 7 employers during their careers, thus employers should be prepared that workers move from employer to employer.

Given that ninety percent of the workforce owns a smartphone and all have an email account,

employers should consider this medium as effective means of communications related to recruitment of new workers and retentions of existing workers during the off season.

With respects to 2013 work activities:

-‐ All of the workers surveyed said they performed tree planting activities in 2013. More than four out of five workers of were involved in two or more activities.

-‐ Piece count is the common practice of compensation. Nearly 9 out of ten workers (87%) reported being paid on piece count. Approximately 30% of lead hands, supervisor/crew bosses and project managers reported being paid on an hourly basis.

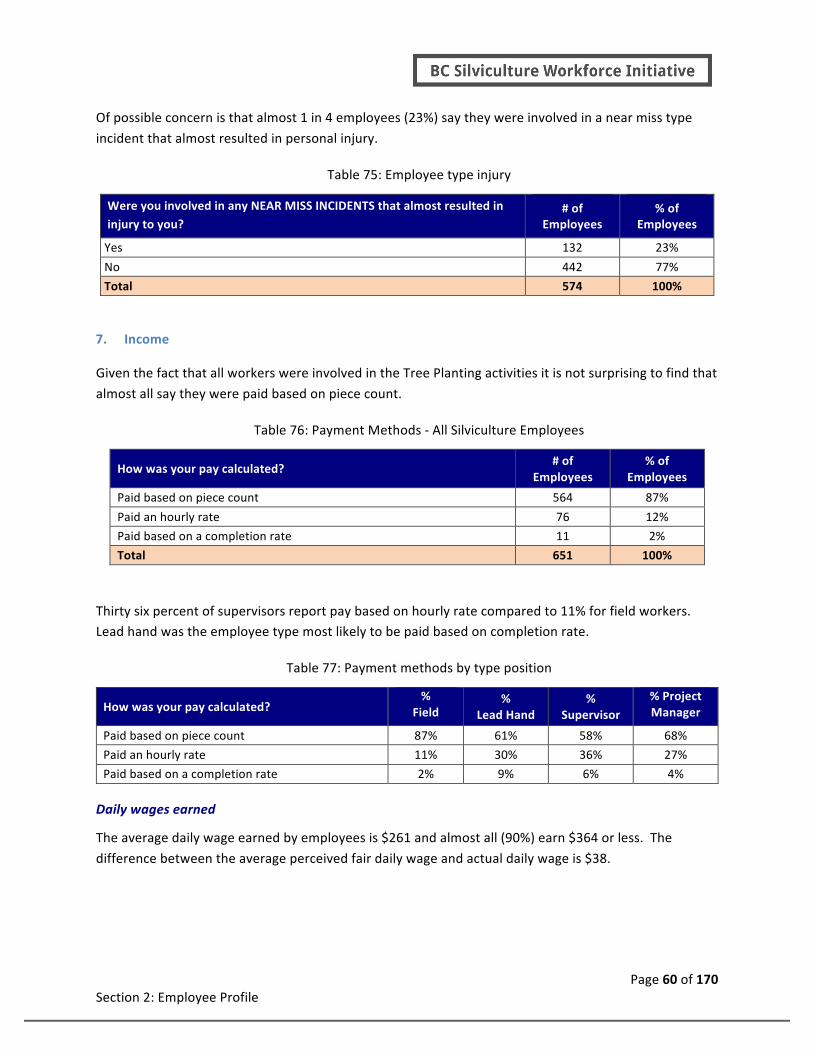

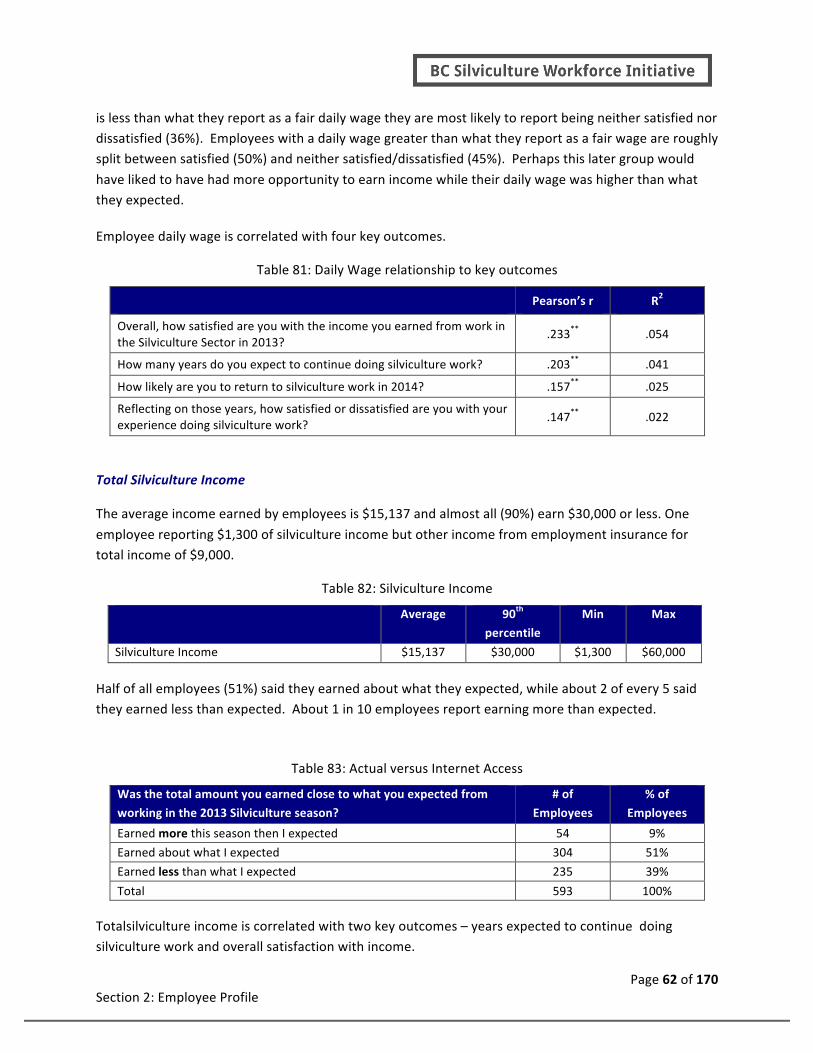

-‐ The average daily wage earned by a worker was $261, lower than their average expected fair daily wage of $299.

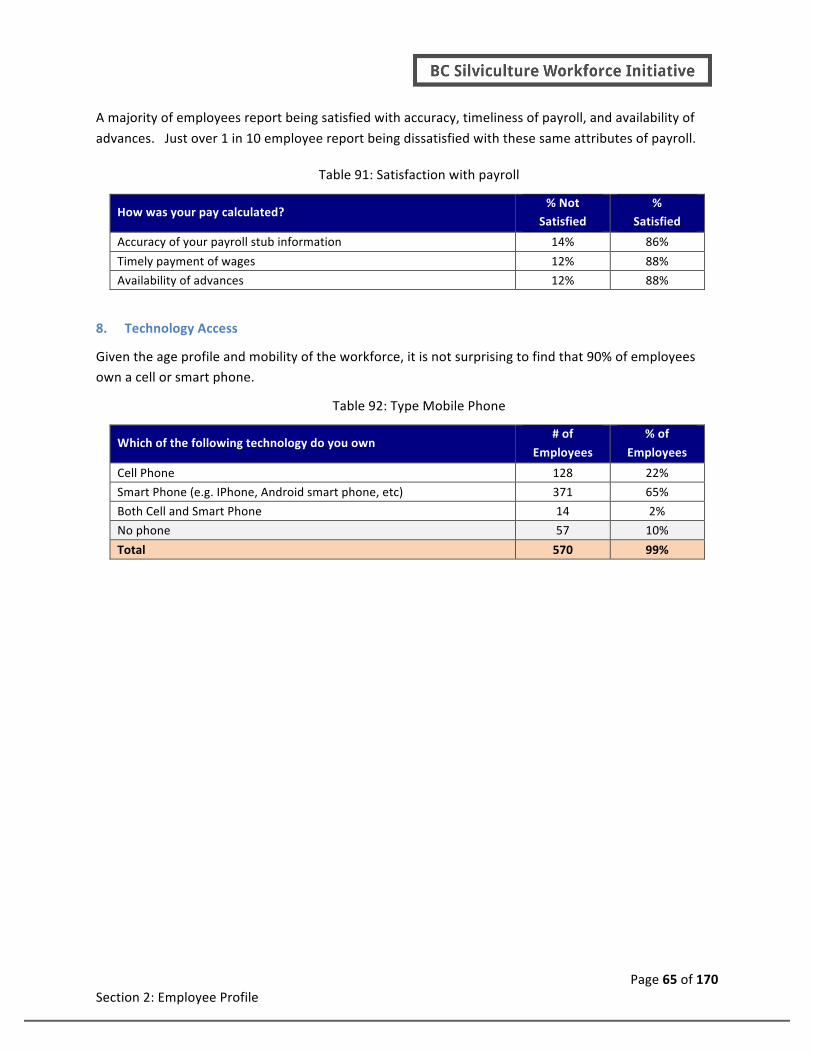

-‐ The majority of workers (86%) reported being satisfied with the accuracy of their payroll.

-‐ Nearly two out of five workers (37%) reported having at least one type of injury (overuse/exertion injury or other injury) in 2013, with the average days off work being 5 days.

-‐ One in four workers reported being involved in a “near miss” situation that could have caused

injury. -‐ Workers earned an average of $15,137 from silviculture activities and had an average gross income

of $23,939. Almost all employees (90%) earned $30,000 or less.

-‐ Four out of five workers (82%) reported that their employer went the “extra mile” to ensure workers were as happy and as productive as possible.

Section 3: Employer Profile

There are an estimated total of 188 private firms conducting silviculture work in BC -‐ 78 employers that perform tree planting activities, 80 employers that perform brushing and spacing activities, and 43

private employers that conduct wildfire fighting activities. Some firms have activities in more than on area.

Approximately 80 % of employers reported being involved in two or more activities. Employers reported working on average in 2 regions, but 50% of all employers worked only in one region.

Silviculture employers reported average annual earnings of $2.3 million and median annual earnings of

$1.5 million in 2013. As suggested by the number of activities they report, most also reported generating revenue from more than one type of activity. 20% of employers reported earnings from outside of BC. Most BC revenue (82%) was earned from work performed on forest lands and come from

private sector clients (68%) compared to government (32%) contracts. Non-‐forest sector revenue came

Page 16 of 170

from a number of different clients ranging from utilities to mining, municipalities, and oil and gas sector. Overall, 30% of employers reported work undertaken in partnership with First Nations.

Business results (revenue) for almost half of employers was below expectations in 2013. Half of employers look forward to better operations in 2014. The majority of employers (58%) reported being

optimistic about the next 3-‐5 years primary due to strong lumber prices. Employers that don’t share this bright outlook are concerned about the competition from other firms and thin profit margins.

With respect to 2013 activities and workforce composition, employers reported

-‐ The majority of their time (82%) was performing tree planting activities. -‐ They employed an average of 1 crew boss for every 7.4 field workers and 1 rookie for every 4

experienced staff employed. -‐ Crew size can range considerably and is a function of type work and company employee counts. The

average size of crew reported as small is 5 field workers. The average for larger crews is 18 field

workers. -‐ Approximately one-‐half of employers reported employing First Nations people and rarely employed

foreign workers.

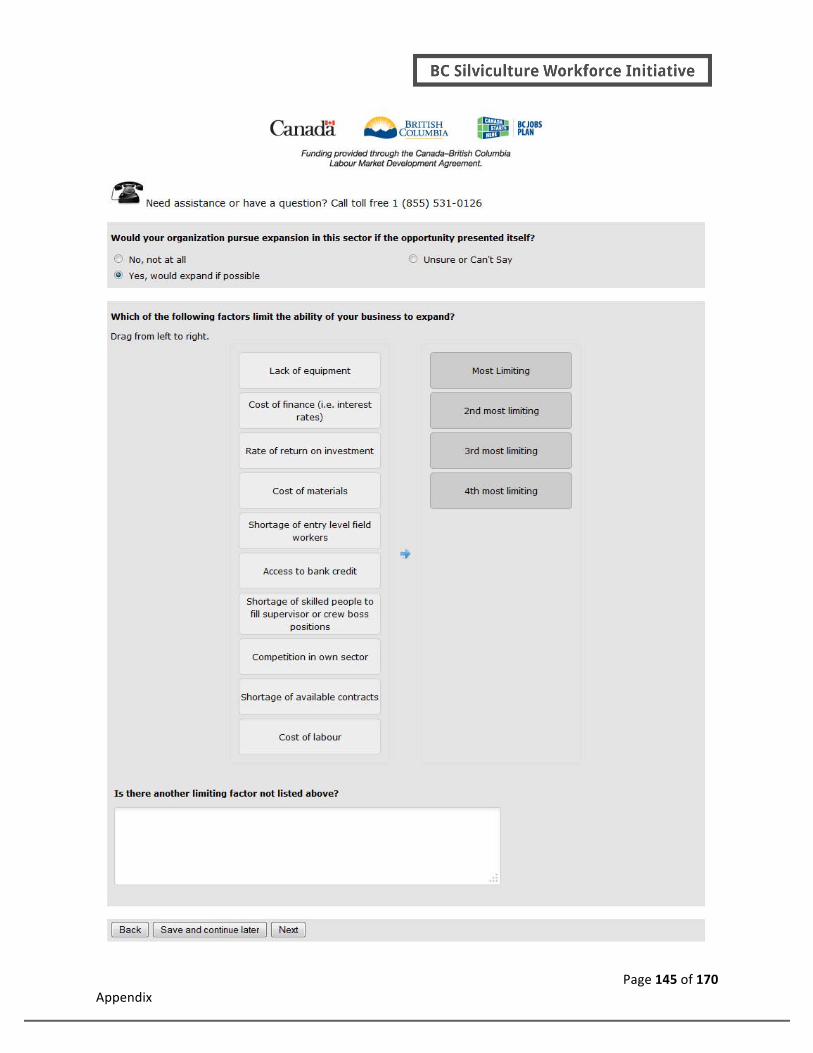

Almost 66% of employers reported they would expand if possible. Limiting factors to expansion cited

were associated with revenue (availability of contracts and competition within the sector) and ability to find skilled supervisors/crew bosses.

All employers reported plans to conduct business in 2014 and almost half (47%) expected their business to continue for 10 or more years. When an owner plans to exit the sector, 40% reported not being sure

what will happen to their business and 26% anticipate it will be taken over by an existing employee. Sixteen percent think the doors will simply shut. The two leading reasons for exiting the sector are lack of work/contracts and retirement.

A small majority of employers think industry associations are doing a good job representing their

interests. One out of three businesses would say they are doing a poor job and only 8% would say they are doing a very good job. The main area of dissatisfaction is that the associations do not represent all of the industry. Suggestions to improve include increasing membership, advocating for common standards

for business practices and improving sector wide communication.

Section 4: Recruitment and Retention

Current Practices

Supervisor and crew bosses are a recruitment priority for 33% of employer respondents. Employers have limited problems with recruiting entry level field workers, and furthermore, even if they were available only 1 in 10 employers (11%) reported they would have hired additional rookies.

Page 17 of 170

Raising awareness with high school students of the career opportunities in silviculture is a good investment for expanding the pool of potential employees according to employer respondents. A clear majority of employers (80%) think an industry association should lead the way on any effort to promote

the sector.

Almost all employers (98%) reported recruiting through existing employees but less than half (42%) agree it’s very effective. Almost 1 in 3 employers (60%) don’t use job fairs or similar events and only 7% agree that is an effective method to recruit employees. When evaluating rookies, the most common

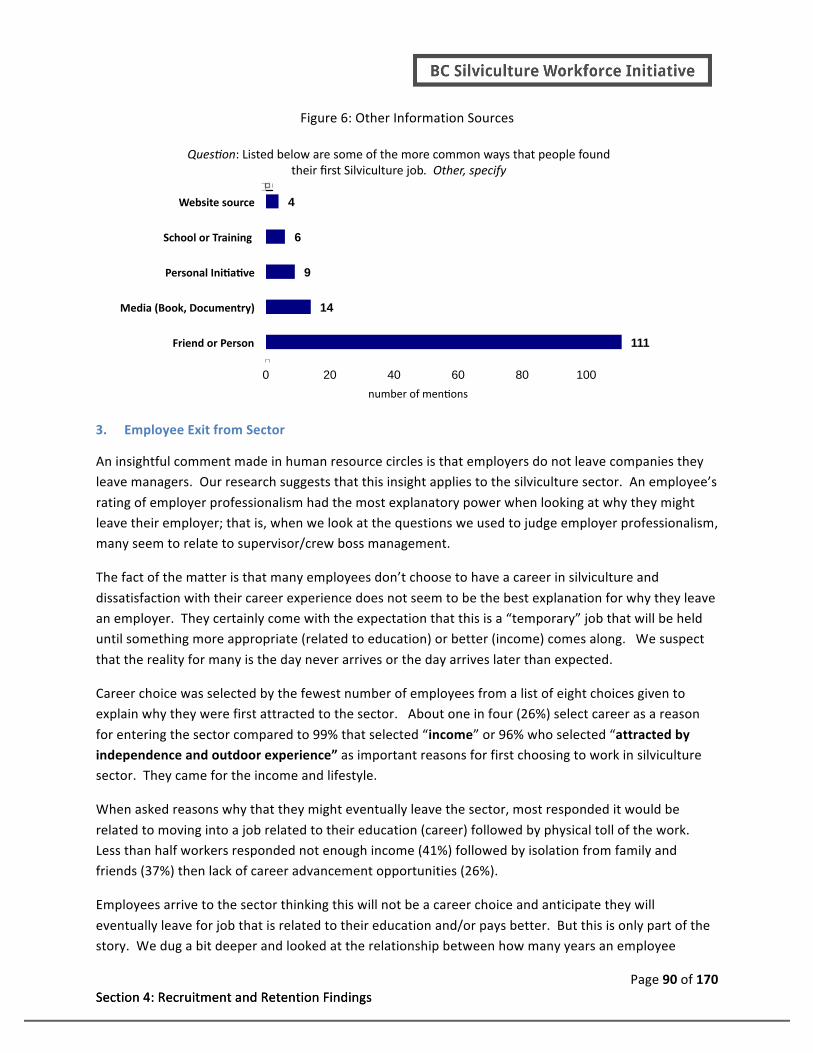

practice (55%) was an in-‐person interview. The most common evaluation tool was a reference check for evaluating experienced workers. Over half (57%) of workers said that a contact in the sector led to their first silviculture job. Information available on the internet was used by some leading up to finding a job,

but not many said this played an important role in how they looked to find work in the sector. Traditional employer recruitment methods such as newspaper job postings and career fairs were viewed by employers as inefficient in recruiting new entrants to the workforce.

Key Drivers

Each of the drivers we tested has a statistically significant correlation with an employee’s willingness to

recommend an employer. Satisfaction with employer professionalism can explain 35% of variance in how likely an employee was to recommend their employer. The next best explanatory driver is satisfaction with an employee’s overall accommodation followed by their workday experience. Overall

satisfaction with income was the least powerful predictor of how likely an employee is to recommend working for their employer

-‐ Employer professional satisfaction is mainly driven by fairness of treatment of workers by an employer.

-‐ Accommodation satisfaction is mainly driven by safety and security at camp, cleanliness, and living mates, and size of sleeping quarters (room or tent).

-‐ Workday experience satisfaction is mainly driven by fairness of assigned tasks, and supervisor/crew

boss organization. -‐ Dissatisfaction with income is associated with employees' experience with tree prices, injuries, and

available work days.

Overall, those employee that think their employer goes the extra mile to ensure employees are as happy

and as productive as possible, that are younger in age, and have more years’ experience are more likely to return to the sector to work the next season.

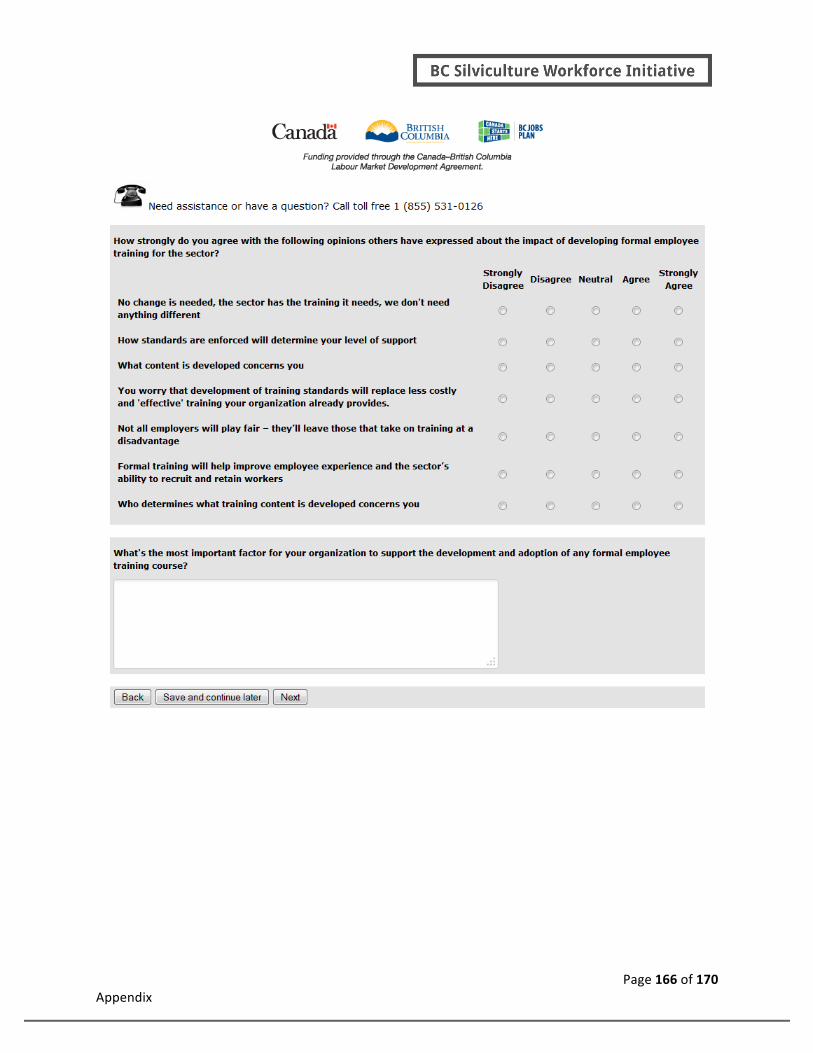

Training

Training can be a key recruitment and retention tool. Employees felt that their employers would gain the greatest benefit from training delivered to rookies followed by workers in supervisory or

management roles. Seventy five percent or more of employees perceive that their organizations would benefit from training delivered to any of these groups of employees.

Page 18 of 170

More employers agree than disagree (80%) that training for supervisors/crew bosses is where there is greatest need. More businesses agree than disagree that change is needed when it comes to meeting the training needs of employees.

The greatest concerns about training for workers are who determines content, what content is

developed, and any duplication of existing resources. Slightly less of a concern is that new training will replace their less costly and effective training followed by worries about enforcement. Employers cited training opportunities in the areas of existing training such as ATV training, resource road training,

chainsaw training, and new training in productive planting techniques, additional wildfire fighting modules, and supervisor crew and organization skills.

More detailed research findings are provided in the following sections of the report.

Page 19 of 170

Structure of Report This report provides a background to the project and an overview to the research methodology followed

by 4 main sections.

Section 1 provides findings related to BC Silviculture Workforce Supply and Demand and includes information of total employment, employment production standards, current workforce estimates,

future workforce demand projections, as well as a historical workforce supply picture.

Section 2 provides findings related to BC Silviculture Employee Profile and includes information on demographics, career history, and 2013 work experience details from the employees that responded to the survey.

Section 3 provides findings related to BC Silviculture Employer Profile and includes information on the

sector employer population, corporate information such as subsector activity, revenue, years in business, workforce composition, and opinions and outlook, such as future revenue expectations, sector optimism, and reasons for exiting the sector..

Section 4 provides research findings related to recruitment and retention in the sector and includes

information on employer recruitment priorities, current recruitment practices, key drivers of employee satisfaction, employees who are at risk to leave the sector, opinion on future training priorities, as well as additional general findings.

Appendices follow and include employer and employee surveys.

Page 20 of 170

Methodology

1. Instrumentation

The employer and employee survey question were developed based on analysis of the associated 2012 survey results and input from the BC Silviculture Workforce Committee. Ference Weicker and Company

provided content expertise for all questions required for workforce supply and demand analysis. Survey questions were pre-‐tested using a cognitive interviewing methodology. The employee survey questionnaire was structured to support Key Driver Analysis and Derived versus Stated Importance

Analysis. The employee survey also included an optional set of questions to measure personality type based on the GRIT scale1.

2. Sampling

The principle behind estimation based on survey sample is that each person in the sample "represents", besides himself or herself, several other persons not in the sample. The quality of a sample based

estimate is dependent upon how complete the list sampled from is (Sample Frame) and how representative the people providing feedback are to the total population of interest. The preferred method of ensuring representativeness is to select a “random” sample from the list to minimize

potential selection bias.

Sample Frame –Private Sector Employers The sample frame used for selecting businesses to participate contained 188 business thought to represent all BC silviculture employers. In almost all population based studies there is no such thing as a completely accurate sample frame. Most have issues associated with under and over coverage.

The sample frame used for this study contained 188 private employers. The employers identified as

working in the BC silviculture sector -‐ 78 employers that perform tree planting activities, 80 employers that perform brushing and spacing activities, and 43 employers that have wildfire fighting activity. Firms can have activity in more than one area. These firms were identified using various employer listings such

as BC Forest Safety Council SAFE Certified List, WorkSafeBC (WSBC) COR certified list2, existing BCSWI contractor database, BC Bid award notices from MOFN and BCTS, and MOFR Fire Protection Branch-‐ Standing Offer List for fire crews. Lists were cross referenced for data integrity to create our BC

silviculture employer population sample.

To estimate over coverage we tracked how many employers contacted did not meet the study requirements of having activity in BC Tree Planting, Brushing and Spacing or Wildfire fighting subsectors. Only 1% of the sample contacted employers was classified as over coverage. These were firms that

provided support and planning type service to the sector.

1 Duckworth, A.L., Peterson, C., Matthews, M.D., & Kelly, D.R. (2007). Grit: Perseverance and passion for long-‐term goals. Journal of Personality and Social Psychology, 9, 1087-‐1101. 2 See Appendix 9 for our assessment of the accuracy of business classifications.

Page 21 of 170

Sample frame under coverage is harder to determine. The fact that our model for projected number of workers that uses the estimated count of employers as part of its calculation is within 500 of the estimate based on our model based on production data suggest we have an accurate estimate of the

number of employers in the silviculture sector.

Sample Frame – Private Sector Employees There is no known complete list of silviculture employees that can be used as a sample frame. Three

strategies are used reach a representative sample of employees. Stratified random sampling; respondent driven sampling and census approaches were all attempted with employees. Our stratified random sampling uses the list of employers as the first strata, employees contacted through selected

employers is the second strata. Respondent driven sampling is a relatively new and innovative approach developed for hard to reach study populations (for instance, drug addicts) and uses non-‐random selected employees as the starting point for reaching a representative sample. Census approaches are

convenience samples in that the employees self-‐select to participate.

Sample Selection - Employer Two strategies were used to recruit employers to participate in the survey. A random selected sub-‐set of employers was selected for priority effort in recruitment. This random sample of 19 employers (10%) was selected to assist with evaluating the representativeness of our census approach. We obtained a

68% response rate to our random sample participants (n=13). These 13 employers represent 27% of all respondents in our final sample (n=48).

The total sample is n=48 represents a 25% response rate for all employers in our sample frame of 188

listed businesses.

Both the random sample response rate and the overall response rate are above the survey research industry norms. Norms for random sample based research of employers is less than 5%. It jumps to

15% when the respondent has a known and credible relationship with a respondent, such as when the respondent is a business to business customer relationship.

Table 1: Sample Frame List counts based on BCFSC SAFE Companies Certification Profiles

Whose experience is reflected in the responses to this survey? One way to answer that question is to say the feedback we report is based on employers who represent…:

3 Not all 48 employers in our sample answered all survey questions.

Sample Frame Random Sample Final Sample BCFSC Classifications Count % Count % Count % Not BCFSC Certified 55 29% 5 26% na na IOO 3 2% 1 5% 1 2% ISEBASE (2 to 5) 15 8% 2 10% 18 10% SEBASE (6 to 19) 87 46% 8 42% 87 60% BASE (20+) 28 15% 3 18% 28 19% Total 188 99% 19 101% 463 99%

Page 22 of 170

• Coverage in terms of total employment = 79% of all employees • Coverage in terms of volume of trees planted = 56% of total planted • Coverage in terms of volume of Brushing & Spacing = 25% of Hectares Brushed/Spaced

Answered from a strictly statistical inference perspective we can say that point estimates based on n=48

will be the same (± 12.24%) as we would get every 19 out of 20 times we repeated this survey.

Sample Selection -Employee Three approaches where used to reach a representative sample of BC Silviculture employees. A

stratified random sampling approach was attempted by asking the random sample of employers (Strata 1) to invite all their employees (strata 2) to participate in the employee survey. All participating employers (13 randomly selected and 35 non-‐ random selected) were asked to participate as our strata

1 list of employers. A total of 16 (33%) requested information about sending invites to their employees; only 6 (12%) of our sampled employers actually provided employee contact information. The total

count of employees contacted through this method was 1,249 with an approximate 48% response rate.

The second approach (respondent driven sampling) asked employees who completed the survey to help recruit others. While n=148 employee respondents expressed interest in recruiting other employees the final count of employees that provided emails was n=3 for total of 9 additional email invitations.

The third approach (Census) was to promote the survey using various social media tools and make the

survey publicly available for any employee to access.

A total of 796 people arrived at the surveys landing page, that explained what the survey was about and who it was directed to. Three (3) people advanced no further in the survey and a total of 55 stopped participating in the survey after viewing the first 3 pages. These first 3 pages are informational, and

asked no questions. Employees advanced through the survey after page 4 based on their profile so could legitimately visit as few as 4 pages if they were terminated as not part of the silviculture sector and the most number of pages (screens) was 37. A total of n= 576 are classified as “complete” and

viewed the appropriate number of pages based on their answers to questions in the survey.

Page 23 of 170

Table 2: Survey Page Drop Off

Survey Pages Viewed4 All Email

invite % Pubic

URL % Page Content

Responded 796 683 86% 111 14% Landing page/Greeting Page 1 only 3 2 >.5% 1 1% Landing page/Greeting Page 1 and 2 only 23 16 2% 7 6% Confidentiality Information Page 1, 2 and 3 only 29 19 3% 10 9% Incentive Information Total no questions 55 37 5% 18 16% No questions answered Viewed 4 or more pages 741 628 85% 93 84% 1 or more question answered

The public URL generated a lot more general interest type arrivals to the employee survey URL. However, once a person determined they wanted to do the survey (or determined it was appropriate to

them) they competed the survey about as often as employees who received an email invitation.

Consequently there are n=165 “partial” completed surveys. These employees have provided some information that can be used in analysis.

The final count of employee respondents is n=741.

Based on our estimate of total number of workers in the BC silviculture sector (7,298) our sample represents 1 in 10 employees (10%). See our employee profile section for full description of employee

characteristics represented in this survey.

Answered from a strictly statistical inference perspective we can say that point estimates based on n=741 will be the same (±3.4 %) as we would get every 19 out of 20 times we repeated this survey.

3. Incentives

Cash incentives in the form of lottery style prizes were used for both employer and employee incentives. Employers were entered into a draw to win one of two cash prizes of $250 dollars. Total prize dollars for

employees was $1,500 and was structured as:

• Two grand prize draws for $250

• One of ten $50 prize s

• One of twenty $25 prizes

A total of 32 employees could win a cash prize. An employee could win additional entries into the draw by providing the email addresses of another silviculture employee that did not work for the same employer as himself/herself. The incentive to earn additional entries into the draw was done to

encourage distribution of the survey.

4 A total of 111 people arrived at page one of this survey using the public URL link of survey (n=60 are classified as complete and 51 partial completes).

Page 24 of 170

Another incentive used with employees was the offer to send personalized reports, including the option to receive the results of their GRIT score. A total of 488 employees provided their email address for the purposed of sending them a personal report or notification of a prize win.

Employers were given a similar incentive for completing the survey. Employers had the option of

receiving a custom benchmark report. Half (50%) of our employer respondents (24) requested a benchmarking report. In addition, if they provided a list of employee emails to Dialogue Research they could receive additional insight in their benchmark report based on employee responses. A total of 16

employers (33%) asked to be contacted regarding this option. Only 6 employers (12% of all employer respondents) provided employee email lists.

4. Sample Management

Employers were sent an initial invite on November 13, 2013. The public version of the employer survey was available the same day. The first email invites to employees was sent December 3, 2013 and the

public version of the employee survey was available the same day. The reason for gap between sending employer employee surveys was to allow employers some time to consider having Dialogue Research send invites directly to their employees.

The employer and employee surveys were closed to new respondents on January 6, 2014. Employee

respondents had approximately 34 days (4.5 weeks) to participate in the survey. Employer respondents had approximately 53 days (7.5 weeks) to participate.

Employees received a maximum of 4 reminder emails. Likewise, an employer that was not part of the employer random selection received a maximum of 5 reminder emails. Employers in the random

sample received up to 16 email reminders. In addition, these employers also received at least one telephone call, some received up to 4 telephone calls in attempts to reach them and encourage participation.

5. Data Cleaning Notes

Once it was determined which respondents would be included in the samples, a data cleaning process

was undertaken to prepare the data for statistical analysis. The data cleaning entailed converting text responses to quantitative questions to numerical responses, as well as reviewing responses within and across questions for logic. For example, where respondents were asked to identify the percentage of

their revenues that were generated from different activities, the figures were checked if the responses added up to 100%. In cases were responses were not logical or missing, where possible, we attempted to fill in the gaps. If it was not possible to determine the logical response or if there were any doubts,

the response was identified as “missing” and excluded from the analysis of that question.

6. Data Reporting Notes

Anywhere data is reported with “*” or “**” it signifies the result is statistically significant. Statistically significant does not mean important; rather, it means the result should not be explained away as

Page 25 of 170

chance. The “*” means a one tail test of statistical significance and the “**” means a two tail test of statistical significance. One-‐tailed tests are considered more powerful than two-‐tailed tests and “*” suggest almost no coincidental result due to chance.

In order to determine the quality of an estimate using both small (employer) and large (employee) samples we have used the coefficient of variation (CV). The CV of a variable or the CV of a prediction model for a variable can be considered as a reasonable measure and is particularly useful in the interpretation of relative levels of precision, especially when widely varying quantities are being compared.

Higher values indicate higher variability and thus more potential for error.

Example: In a province there may be an estimated 50,000 people unemployed with a margin of error of 1,300 people. At the same time, that province's estimated unemployment rate is 8% with a margin of error of 0.2%. It is difficult to compare these numbers directly. However, the CV of the estimated number of unemployed is 2.6%, while the CV of the estimated unemployment rate is 2.5%. (They need not be equal.) This shows that the two estimates have essentially the same level of precision.

USA Census interpretation guidelines.

• High reliability: Coefficient of Variation (CV) of 0.0 to 15%

• Medium Reliability: CV between 15%-‐30%.

• Low Reliability: CV over 30%.

The cut-‐off depends on the application of the data – CV beyond 30% may be acceptable for very general

portraits or profiles.

Page 26 of 170

Example Report Tables Example employer table used in report

Sample All Employers3

Where did you work this year? Count Percent Count CV

A -‐ West Coast Region 21 43% 81 25.5

B -‐ Skeena Region 14 29% 54 42.2

C -‐ Omineca Region 7 14% 26 87.4

D -‐ Northeast Region 10 21% 39 58.3

E -‐ Cariboo Region 19 39% 73 31.4

F -‐ South Coast Region 6 12% 17 102.0

G -‐ Thompson/Okanagan Region 10 21% 39 58.3

H -‐ Kootenay/Boundary Region 19 39% 73 31.4

Total 48 188

Example employee table used in report

Sample All Employees3

Where did you work this year? Count Percent Count CV

Under 25 years of age 257 46% 3,268 8.6

26 to 29 years of age 179 32% 2,274 12.4

30 to 33 years of age 51 9% 640 44.0

34 to 39 years of age 37 7% 497 56.6

40 years or older 39 7% 497 56.6

Total 563 100% 7,105

Estimated count of actual

number of employers

Estimated count of actual number of employees

Page 27 of 170 Section 1: Workforce Supply and Demand

Section 1 Workforce Supply and Demand

Calculating how many workers, how many days, how much revenue

Page 28 of 170 Section 1: Workforce Supply and Demand

A. EMPLOYMENT

1. Survey Based Employment Estimates

The maximum number of private sector workers that was employed by our sample during the course of

2013 was 3,306. Our production based extrapolation model estimates total non-‐government payroll counts were 6,382 during 20135. Government employees add an additional 1,100 workers placing the total estimated number of BC silviculture workers at 7,482. A second method for calculating the

projected number or workers was also designed based on our Employer Population list and employee counts reported by employers. That estimate for BC Silviculture workers is 6,995. The estimate differs by only 487 employees.

2. Employment of Field Workers and Crew Bosses

In terms of field staff, the employers surveyed reported employing 314 crew bosses and 2,331 field

workers (a ratio of 1 per 7.4 field workers). Of these field workers, 1,881 had previously worked in the sector while 475 were rookie field workers (ratio of 1 rookie for every 4 experienced worker). Not all employers reported having rookie staff in 2013. Most employers (78% or 35 of the 45 providing a

breakdown) reported employing at least some rookies.

Table 3: Average Number of Employees, BC, 2013

Employers Employees

Type of Worker Reporting Mean Count Total % of Total

Crew Boss Employees 45 7.0 314 12% Field Workers 45 51.8 2,331 88% -‐ Rookie Field Worker 35 13.6 475 18% -‐ Experienced Field Worker 44 42.8 1,881 71% Total Crew Bosses and Filed Workers 45 59.4 2,645 100% Maximum @ Any Time (n=46) 3,306 100%-‐

5 Total of Tree Planting, Brushing, Spacing, Wildfire Fighting (Industry) and Other Workers. Wildfire Fighting (Government) is not included in this total.

Page 29 of 170 Section 1: Workforce Supply and Demand

3. Field Workers By Types of Activity

Each employer was asked to estimate the percentage of time that their silviculture field workers spent on each of the various types of silviculture activities. The percentages were then multiplied by the number of the field workers that they reported to develop an estimate of the allocation of field staff

across the activities. As indicated, silviculture field staff employed by the employers surveyed spend most of their time engaged in tree planting activities (82%).

Table 4: Field Worker Effort by Activity, BC, 2013

Sample BC Silviculture

Sector

Field Workers Count % Estimate

Tree Planting 1,917 82% 5,826

Brushing and Spacing 298 13% 924

Wildfire Fighting (private) 116 5% 355

Total Field Workers 2,331 100% 7,105

B. EMPLOYMENT PRODUCTION STANDARDS

1. Tree Planting

Overall, 29 out of the 48 employers surveyed (60%) indicated they were involved in tree planting, 26 of these reported revenues (as shown in the table below), and 23 provided estimates of the number of

trees their workers planted in 2013. These 23 employers reported that their field staff planted 120,378,298 trees in 2013. The average number of trees planted per field worker per day varied across these 23 employers from a minimum of 450 trees planted per day to a maximum of 2,700 trees planted

per day. The average across all employers reporting was 1,442 trees planted per day.

Table 5: Tree Planting Activities: Employer Survey, BC, 2013

Indicator Total Mean

Revenues (n=26) $35,984,500 $1,384,019 Trees Planted 120,379,298 5,233,883 Average Trees Planted Per Day 1,442 1,442 Tree Planting Worker Days 83,481 3,630 Number of Tree Planting Workers 1,749 76 Number of Days Planting Per Worker 48 48

An estimate of the worker days spent planting can be derived by dividing the total number of trees

planted by the 23 employers by the average of 1,442 trees per worker day; planting the 120 million trees required 83,481 worker days. On average, the 23 employers had 76 field workers active in tree planting (a total of 1,749 workers employed by the 23 employers). Dividing the total worker days by the

Page 30 of 170 Section 1: Workforce Supply and Demand

total workers active in tree planting, the average number of days worked per field staff member is equal to about 48 days. Employers were most commonly active in tree planting activities in April, May, and June, as shown in the table below.

Table 6: Tree Planting Activity By Months Active, BC, 2013

Sample

Month # of

Employers % Active

January 2 9%

February 5 22%

March 9 39%

April 18 78%

May 19 83%

June 17 74%

July 12 52%

August 7 30%

September 8 35%

October 6 26%

November 0 0%

December 0 0%

According to the BC Ministry of Forests, Lands and Natural Resource Operations, 238,000,000 trees were planted on Crown and private land in 2012/13, as indicated below. The number of trees planted on

Crown and private land per year over the past five years has varied from about 179 million in 2010/11 to 253 million in 2008/09.6

Table 7: Tree Planting in BC, 2008/09 to 2012/13

Fiscal Year Trees Planted

2008/2009 252,600,000

2009/2010 210,200,000

2010/2011 179,000,000

2011/2012 199,900,000

2012/2013 238,000,000

5-‐Year Average 215,940 ,000 Source: BC Ministry of Forests, Lands and Natural Resource Operations. Seedling Requests by Planting Year from 1994 to 2014

6 BC Ministry of Forests, Lands and Natural Resource Operations. Seedling Requests by Planting Year from 1994 to 2014. Accessed March 11, 2014 from: https://www.for.gov.bc.ca/hti/spar/statistics.htm.

Page 31 of 170 Section 1: Workforce Supply and Demand

By dividing number of trees planted on Crown and private land in BC in 2012/13 by the average number of trees planted per day from the survey findings (1,442 trees per day), we estimate that 165,049 worker planting days were required. Dividing this figure by the average number of days worked per

worker calculated from the survey (48 days), we estimate that 3,439 tree planting workers were employed in the industry in 2013.

Table 8: Tree Planting Activities: BC Industry Overall, 2012/2013

Indicator Total

Trees Planted (2012/13) 238,000,000

Tree Planting Worker Days 165,049

Number of Tree Planting Workers 3,439

According to the Ministry, there were 241,700,000 seedlings requested in 2013/14 and 243,100,000

seedlings requested in 2014/15. Using the figures obtained from the survey, this level of planting would require about 167,614 worker days and 3,492 tree planting workers in 2013/14 and 168,585 worker days and 3,512 workers in 2014/15.

2. Brushing and Spacing

In total, 37 out of the 48 employers surveyed (77%) indicated that they were involved in at least some

brushing and spacing activities. Of these 37 employers, 19 reported revenues, 31 reported number of days and workers brushing and spacing, 27 provided estimates of the number of hectares they brushed, and 6 provided estimates of the number they spaced.

On average crews were in the field for 86 days performing brushing and spacing activities (2,667 days

total). Employers reported that the average number of workers on payroll for those activities was 10 workers. Multiplying the total number of days brushing and spacing by the average number of workers per employer, we estimate that field staff worked 26,670 days brushing and spacing.

Table 9: Brushing and Spacing Activities (Employer Survey), BC, 2013

Indicator Total Mean

Revenues $7,072,500 $228,145 Days in Field Brushing and Spacing 2,667 86 Brushing and Spacing Workers 310 10

Brushing and Spacing Worker Days 26,670 860

Page 32 of 170 Section 1: Workforce Supply and Demand

Employers were most commonly active in brushing and spacing activities in June, July and September, as shown in the table below.

Table 10: Brushing and Spacing Activity By Months Active, BC, 2013

Sample

Month # of

Employers % Active

January 4 13%

February 5 16%

March 6 19%

April 9 29%

May 16 52%

June 21 68%

July 23 74%

August 18 58%

September 22 71%

October 18 58%

November 15 48%

December 7 23%

Page 33 of 170 Section 1: Workforce Supply and Demand

Brushing

The 27 employers that provided estimates of the number of hectares brushed reported brushing a total of 7,465 hectares (an average of 277 hectares per employer). Employers reported an average of 3.1 worker days per hectare brushed. Multiplying the total number of hectares brushed by the average

number of worker days per hectare, the total number of brushing worker days comes to 23,141 brushing worker days, as shown in the table below.

Table 11: Brushing Activities (Employer Survey), BC, 2013

Indicator Total Mean

Number of Hectares Brushed 7,465 277 Average Days Per Hectare Brushed 3.1 3.1 Brushing Worker Days 23,141 859

As indicated below, 33,428 hectares of Crown Land were brushed in BC in 2012/13.7

Table 12: Brushing Activities in BC, 2008/09 to 2012/13

Fiscal Year Area (ha)

2008/2009 32,220

2009/2010 28,084

2010/2011 35,635

2011/2012 33,337

2012/2013 33,428

5-‐Year Average 32,541 Source: BC Ministry of Forests and Range. 2012/13 Annual Report Silviculture Tables and Graphs (Graphs 1 to 9).

Multiplying the total number of hectares brushed in BC in 2012/13 by the average worker days per hectare brushed, the total number of brushing worker days would come to 103,627. Dividing the number of brushing worker days by the estimated number of days spent in the field brushing and spacing from

the survey results (86 days) yields an estimated 1,205 brushing workers.

Table 13: Brushing Activities: BC Industry Overall, 2012/13

Indicator Total

Hectares Brushed (2012/13) 33,428

Brushing Worker Days 103,627

Number of Brushing Workers 1,205

7 BC Ministry of Forests, Lands and Natural Resource Operations, 2012/13 Annual Report Silviculture Tables and Graphs (Graphs 1 to 9). Accessed February 12, 2014 from: http://www.for.gov.bc.ca/hfp/silviculture/statistics/2012-‐13.htm.

Page 34 of 170 Section 1: Workforce Supply and Demand

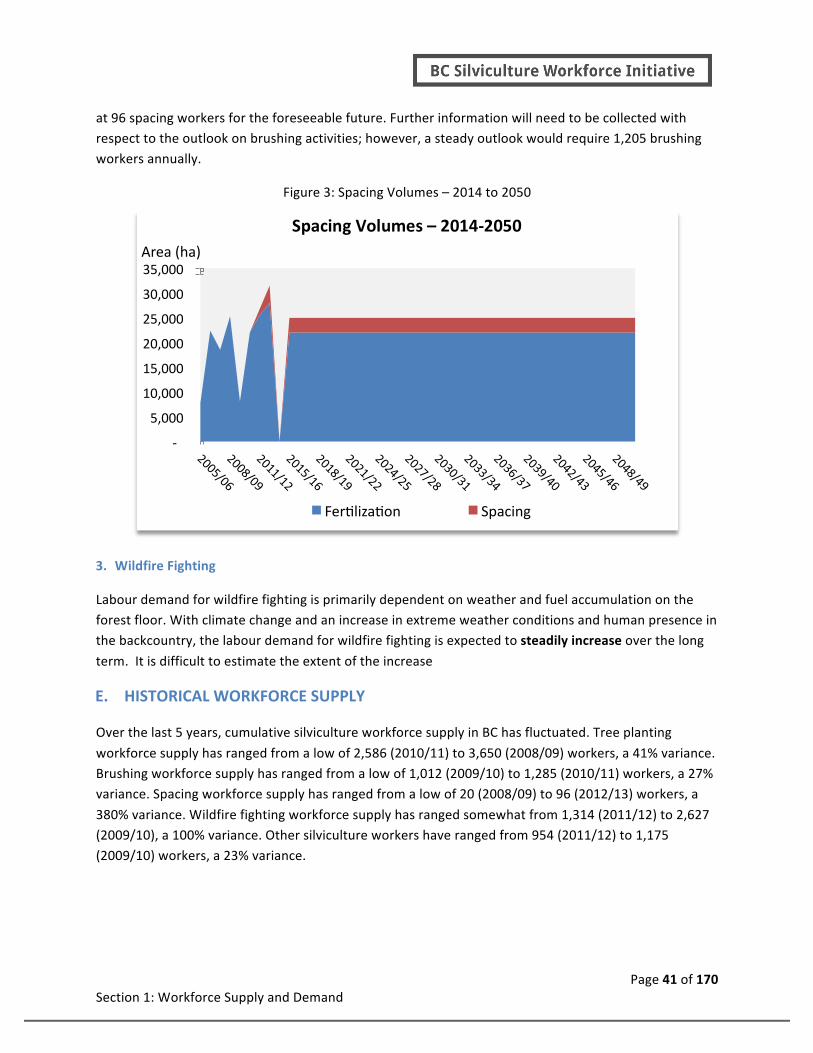

Spacing

Of the 6 employers that provided estimates of the number of hectares they spaced, employers reported spacing a total of 920 hectares (an average of 153 per employer). Employers reported an average of 2.5 worker days per hectares spaced. Multiplying the total number of hectares spaced by the average

workers days per hectare, the total number of spacing worker days comes to 2,300 spacing worker days, as indicated below.

Table 14: Spacing Activities (Employer Survey), BC, 2013

Indicator Total Mean

Number of Hectares Spaced 920 153 Average Days Per Hectare Spaced 2.5 2.5 Spacing Worker Days (Aggregate) 2,300 383

As indicated below, 3,298 hectares of Crown Land were brushed in BC in 2012/13.8

Table 15: Juvenile Spacing Activities in BC, 2008/09 to 2012/13

Fiscal Year Area (ha)

2008/2009 691

2009/2010 2,813

2010/2011 1,930

2011/2012 2,804

2012/2013 3,298

5-‐Year Average 2,307 Source: BC Ministry of Forest, Lands and Natural Resource Operations. Annual Report Silviculture Tables and Graphs (Graphs 1 to 9).

Multiplying the total number of hectares spaced in BC in 2012/13 by the average days per hectare

spaced, the total number of spacing worker days would come to 8,245 spacing worker days. Dividing the number of spacing worker days by the average estimated number of days in the field spent brushing and spacing from the survey results (86 days), comes to 96 spacing workers.

8 BC Ministry of Forests, Lands and Natural Resource Operations, 2012/13 Annual Report Silviculture Tables and Graphs (Graphs 1 to 9). Accessed February 12, 2014 from: http://www.for.gov.bc.ca/hfp/silviculture/statistics/2012-‐13.htm.

Page 35 of 170 Section 1: Workforce Supply and Demand

Table 16: Spacing Activities: BC Industry Overall, 2013

Indicator Total

Hectares Spaced (2012/13) 3,298

Spacing Worker Days 8,245

Number of Spacing Workers 96

3. Wildfire Fighting

In total, 23 out of the 48 employers9 surveyed (48%) indicated that they were involved in wildfire fighting activities. Of these 23 employers, 19 reported revenues and 20 reported number of days and

workers wildfire fighting.

On average, private crews were in the field for 23 days performing wildfire fighting activities in 2013 (452 days total). Employers reported that the average number of workers on payroll for those activities was about 9 workers (total of 183 workers across the 20 employers). Multiplying the total number of

days wildfire fighting by the average number of workers per employer, comes to about 4,068 wildfire fighting worker days.

Table 17: Wildfire Fighting Activities (Employer Survey), BC, 2013

Indicator Total Mean

Revenues $3,461,500 $182,184 Days in Field Wildfire Fighting 452 23 Wildfire Fighting Workers 183 9 Wildfire Fighting Worker Days 4,068 203

The above estimate of 183 wildfire fighting workers were based on response of 8 of the 44 employers

that indicated they were active in wildfire fighting. Based on responses to other questions in the survey, 23 out of the 48 employers responded they indicated they had some involvement in wildfire fighting activities. Based on this estimate, estimates were bumped up from the 183 wildfire fighting workers by

the average workers per firm times the number of firms that are active in wild firefighting, but were not included in the survey question (9 workers)*(36 not surveyed (44-‐8) + 3 that did not respond to the question) = (9 workers*39) = 351 + 183 = 534 wildfire fighting workers.

9 Private wildfire fighting firms supplement the government’s wildfire fighting activities when activity volumes are higher than the government workforce can handle.

Page 36 of 170 Section 1: Workforce Supply and Demand

Employers were most commonly active in wildfire fighting activities in August, as shown in the table below.

Table 18: Wildfire Fighting Activity By Months Active, BC, 2013

Sample

Month # of

Employers % Active

January 0 0%

February 0 0%

March 0 0%

April 1 5%

May 1 5%

June 1 5%

July 6 30%

August 17 85%

September 4 20%

October 6 30%

November 4 20%

December 1 5%

The reported employment in wildfire fighting activities does not include those employed by the BC Ministry of Forests, Lands and Natural Resource Operations. It is estimated that approximately 1,000 workers are employed annually, on a seasonal basis, by the Wildfire Management Branch.

The non-‐government contractors tend to be most busy in years where the level of forest fires in BC is

high. As indicated below, the level of activity can vary widely from year to year.

Table 19: Number, Hectares, and Cost of Forest Fires Fought in BC, 2005-‐2012

Year Fires Total Hectares Total Cost ($ millions)

2005 976 34,588 $47.2

2006 2,570 139,265 $159.0

2007 1,606 29,440 $98.8

2008 2,023 13,240 $82.1

2009 3,064 247.419 $382.1

2010 1,673 337.149 $212.2

2011 655 12,604 $53.5

2012 1,659 102,123 $133.6 Source: Ministry of Forest, Lands and Natural Resource Operations

Page 37 of 170 Section 1: Workforce Supply and Demand

C. ESTIMATED BC SILVICULTURE WORKFORCE

Two approaches have been taken in using the survey results to estimate the total level of employment

in the silviculture sector in BC. The first method relied primarily on using provincial production data (for tree planting, brushing and spacing) and employment production standards to estimate employment by type of activity while the second method used business size data to extrapolate from the survey results

to the known population of employers. The results vary from about 6,995 workers to 7,482 workers.

1. Approach #1 – Using Provincial Production Data

The following table utilizes the employment figures developed in the previous section for tree planning, brushing and spacing. Employment in the wildfire fighting sub-‐sector was developed by extrapolating the employment reported by wildfire fighting firms surveyed to the broader population of employers

(the survey included 8 of the 44 employers in the employer population list believed active in wildfire fighting) and includes the estimated number of seasonal workers employed by the Wildfire Management Branch. It should be noted that the number of private firm workers employed in wildfire

fighting will vary widely from year to year depending upon the level of activity. The survey results were also used to develop an estimate of the workers employed by silviculture firms who are not active in silviculture field activities (e.g. administrative staff or those active in other types of field activities). As

indicated in next table, using this methodology, the number of workers in the sector is estimated to be 7,48210.

Table 20: Approach #1: Based on Provincial Production Data

Sub-‐sector Number of Workers

Tree planting 3,439

Brushing 1,205

Spacing 96

Wildfire Fighting (Industry) 534

Wildfire Fighting (Government) 1,100

Total Field Staff 6,374

Other Workers11 1,108

Total Employment 7,482