Labour Costs and the Future of North America’s Auto · PDF fileLabour Costs and the...

24

Labour Costs and the Future of North America’s Auto Industry Jim Stanford Economist, CAW-Canada CAR Management Briefing Seminar Grand Traverse MI, August 2011

-

Upload

phungkhuong -

Category

Documents

-

view

220 -

download

3

Transcript of Labour Costs and the Future of North America’s Auto · PDF fileLabour Costs and the...

Labour Costsand the Future of

North America’s Auto Industry

Jim StanfordEconomist, CAW-Canada

CAR Management Briefing SeminarGrand Traverse MI, August 2011

Automotive Labour Costs:A Canadian Twist

• CAW founded in 1985.

• Membership up 50% since then.

• Egalitarian philosophical approach, but withcommitment to a viable, productive industry.

• Record of innovation in labour relations:

– CAMI, 3-shift, M80, Magna FFA, WCM

• Canadian productivity advantage ≈ 10%.

• More activist policy context.

– Auto Pact, higher PITs, health care ($5/hr)

• Different currency (volatile).

The Loonie Then and Now

$0.60

$0.70

$0.80

$0.90

$1.00

$1.10

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

$C

($U

.S.)

PPP Value

May 2009

25% above PPP

122%122100All Consumer

Prices (OECD)

113%$8.99$7.99Paperback Novel

(Danielle Steele)

115%$4.27$3.71Big Mac

128%$4.75$3.70Gasoline (US gal)

118%$28,875$24,495Impala LS MSRP

170%(Ont/Mich: 330%)

$338,700(Ont.: $352,500)

$198,900(Mich.: $106,800)Detached House

Canadaas %U.S.

CanadaU.S.

The 2009 Restructuring:North of the Border

• Canadian/Ontario governments contributedproportionately to the binational rescue.

– Proportional to Canadian share of output.

• GM and Chrysler avoided CCAA (“Chapter 11”).

• “Target” for labour costs: $57 (Cdn.).

• Formation of Canadian Health Care Trusts.

• Canadian “footprint” commitments.

• Canadian production & employment shares grew.

• CAW contracts expire Sept. 2012.

Canadian Assembly Share

14.5%

15.0%

15.5%

16.0%

16.5%

17.0%

17.5%

1995 2000 2005 2010

%o

fT

ota

lN

ort

hA

meri

can

Assem

bly

.

Employment Index: Assembly

50

60

70

80

90

100

110

2006 2007 2008 2009 2010 2011

Pro

du

cti

on

Wo

rke

rs,

20

06

=1

00

Jan-Apr

Canada

U.S.

Employment Index: Parts

50

60

70

80

90

100

110

2006 2007 2008 2009 2010 2011

Pro

du

cti

on

Wo

rke

rs,

20

06

=1

00

Jan-Apr

Canada

U.S.

Labour Costs in Context• Widespread assumption: Detroit 3

recovered because they cut labour costs.

• “We can’t go back to our bad old ways.”

• Misdiagnosed problem false solutions.

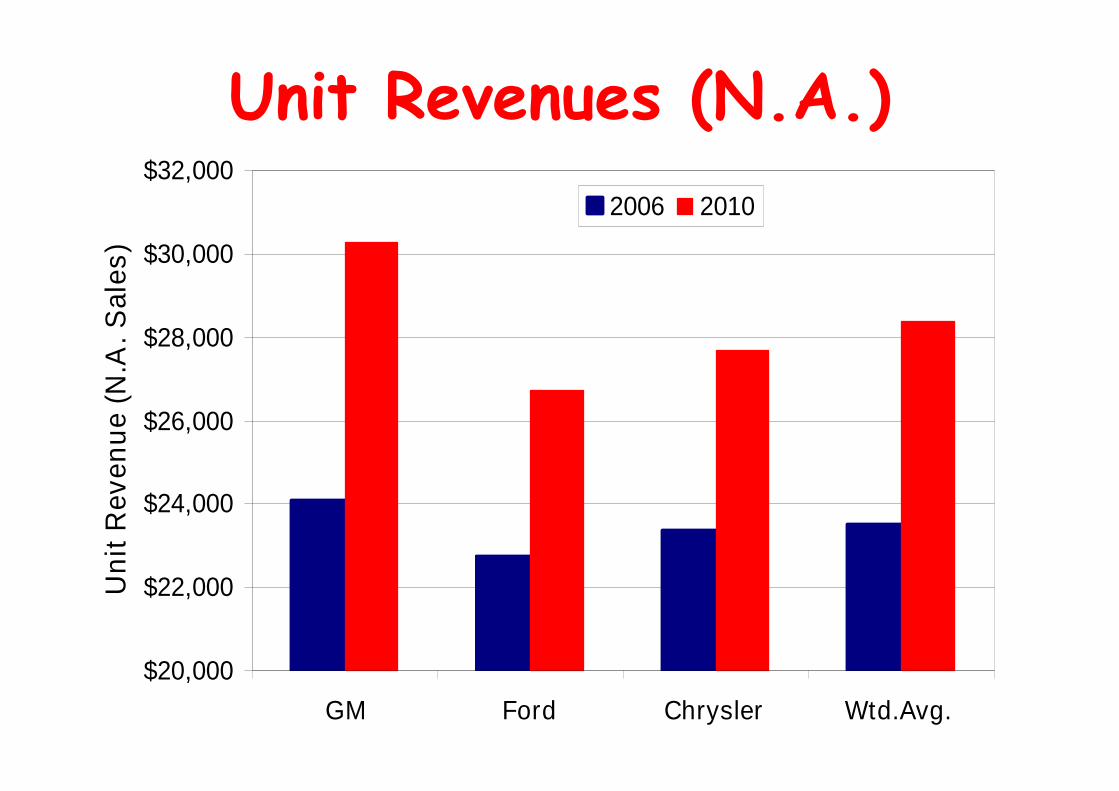

• Other things happened:– Shrinking of the overall market.

– Higher unit revenues.

– Lower interest charges.

– Capacity & overhead downsizing.

• Need to understand labour costs andcontract talks in context.

Net Income

-$20

-$15

-$10

-$5

$0

$5

$10

$15

GM Ford Chrysler Total

Ne

tIn

co

me

($b

il.

U.S

.)

2006 2010

Est

All-In Hourly Labour Costs:Use With Caution

• Subject to major methodological issues.

• Fluctuations in hours worked cause largechanges in hourly value of fixed costs.

• Inclusion of statutory costs, income securitycharges, and other elements creates a wedgebetween cost and “compensation.”

• Legacy cost categories very volatile:

– Assumptions, experience, amortization.

• See CAW publication for more discussion:

– “How Much do Autoworkers Really Make?” April 2009

Hourly Labour Cost

$0

$10

$20

$30

$40

$50

$60

$70

$80

$90

GM Ford Chrysler Unwtd.Avg.

All

-In

La

bo

ur

Co

st

inU

.S.

($/h

rw

ork

ed

)

2006 2010

Est

Est

Total Employment (N.A.)

0

50

100

150

200

250

300

350

400

GM Ford Chrysler Total

N.A

.E

mp

loy

ee

s(a

nn

.av

g.)

2006 2010

Unit Revenues (N.A.)

$20,000

$22,000

$24,000

$26,000

$28,000

$30,000

$32,000

GM Ford Chrysler Wtd.Avg.

Un

itR

ev

en

ue

(N.A

.S

ale

s)

2006 2010

Labour Cost Savings• Average (unwtd) hourly saving: $18.50.

• Heroic assumption: apply to entire NAworkforce (220,000).– Upper bound: $8 billion.

• Don’t forget the VEBAs: Cost shifting.– Amortize over 15 years.

• Net saving: $4-5 billion.– 2% of North American revenues (upper bound).

– Biggest at Chrysler, smallest at Ford.

• Labour cost savings were the leastimportant factor in the companies’ survival.

Financial Analysis• Compare income statements from 2006 and

2010.

• Combined improvement in net income:almost $30 billion.

• Identify some major sources of savingdirectly (unit revenues, interest, G&A).

• Hourly labour cost and employmentdownsizing estimated on basis of hourlycost data.

• Chrysler data incomplete.

G.M. Improvements

$0

$2

$4

$6

$8

$10

$12

$14

$16

$18

$20

Profit

Growth

Interest

Savings

G&A/Other

Savings

Labour

Dnsizing

Higher

Unit Price

Lower

Labour

Cost

$B

illi

on

(U.S

.)

Ford Improvements

$0

$5

$10

$15

$20

$25

Profit

Growth

Interest

Savings

G&A/Other

Savings

Labour

Dnsizing

Higher

Unit Price

Lower

Labour

Cost

$B

illi

on

(U.S

.)

Chrysler Improvements

$0

$1

$2

$3

$4

$5

$6

$7

Profit

Growth

Interest

Savings

G&A/Other

Savings

Labour

Dnsizing

Higher

Unit Price

Lower

Labour

Cost

$B

illi

on

(U.S

.)

Real Reasons for Recovery

• Product, product, product.

• “A revenue problem, not a cost problem.”

• Discipline on incentives, leases, fleets.

• Relaxation of international pressure.

• Restructuring of debt (esp. GM).

• Downsizing to meet capacity (both hourlyand G&A).

• All swimming against the tide of smallerscale.

Consumer Reports

Chrysler gets 3“very goods”(Durango, Charger,Town & Country).

Honda Civic nolongerrecommended.

Dollar-Yen Exchange Rate

60%

U.S. Offshore Imports

0%

5%

10%

15%

20%

25%

30%

1990 1995 2000 2005 2011

Off

sh

ore

Imp

ort

s(%

U.S

.S

ale

s)

Conclusion

• “7% of the cost, 99% of the attention.”

• Conclusion that labour cost cuts explain Detroit 3recovery is wrong, misleads strategy by bothcompanies & government.

• Equalizing labour costs to (certain) U.S.transplants does not make Detroit 3 competitive.– Certain U.S. transplants are not the key competition.

– Labour costs are not the key indicator.

• Other actions (by both business and policy) areneeded to keep the recovery going.

• Undue focus on labour costs will end indisappointment.