LA FRANCAISE DE L’ENERGIE · LA FRANCAISE DE L’ENERGIE A public limited company (société...

40

1 LA FRANCAISE DE L’ENERGIE A public limited company (société anonyme) with share capital of € 5,065,174 Registered office: 1 avenue Saint-Remy, Espace Pierrard, 57600 Forbach Sarreguemines Trade and Companies Register no. 501 152 193 HALF YEAR FINANCIAL REPORT 31 DECEMBER 2016

-

Upload

phungkhanh -

Category

Documents

-

view

215 -

download

0

Transcript of LA FRANCAISE DE L’ENERGIE · LA FRANCAISE DE L’ENERGIE A public limited company (société...

1

LA FRANCAISE DE L’ENERGIE

A public limited company (société anonyme) with share capital of € 5,065,174

Registered office: 1 avenue Saint-Remy, Espace Pierrard, 57600 Forbach

Sarreguemines Trade and Companies Register no. 501 152 193

HALF YEAR FINANCIAL REPORT

31 DECEMBER 2016

2

1. DECLARATION BY THE PERSON RESPONSIBLE

1.1 PERSON RESPONSIBLE FOR THE INFORMATION

Mr. Julien Moulin, Chairman of the Board of Directors and Chief Executive Officer.

1.2 CERTIFICATION BY THE PERSON RESPONSIBLE

To the best of my knowledge, the financial statements for the past financial half year were

prepared in accordance with applicable accounting standards and provide a true image of the

assets, financial position and income of the Company, and all companies included in the

Group’s scope, and the management report included in this half year financial report presents

a true picture of changes in the business, income and financial position of the Company and

all the companies included in the Group’s scope as well as a description of all the main risks

and uncertainties with which they are confronted.

Forbach, France, 30 March 2017

Julien MOULIN

Chairman of the Board and CEO

3

2. HALF YEAR MANAGEMENT REPORT

The board of directors of La Française de l’Energie (the “Company”) met on 30 March 2017

and approved the accounts for the first half year of the fiscal year 2016/2017. These

consolidated half-year financial statements have been subject to a limited review by the

Statutory Auditors.

2.1 BUSINESS ACTIVITY AND DEVELOPMENT OF THE COMPANY AND

GROUP DURING THE PRECEDING FINANCIAL YEAR

In July 2016, the Company began the operational integration and tax consolidation processes

for the legal entities acquired in the 2016 financial year as described below:

On 13 October 2016, Gazonor entered into a letter of intent with the 2G Energy AG Group to

order six engines of 1.5 MW each. These engines were subsequently ordered beginning of

November for the four sites at Lens, Avion, Divion and Desiree for Gazonor to start capturing

coal mine methane and convert this gas into green electricity. The delivery for the engines and

compressors is scheduled for April and May 2017 – with the target to have all 6 engines (9

MW of installed capacity) commissioned and in operations by end of June 2017.

The half year gas sales amounted to € 1,859,671 as at 31 December 2016. The current run-rate

of the Group (SG&A and other overheads) amounted to circa € 400,000 per month, in line

with the Group forecast provided at IPO, despite of the coasts resulting by the strengthening

of the operational team. In addition, the Group is confident to improve further its operating

margin from the gas sales at Gazonor with the implementation of additional efficiency

improvements such as the replacement old engine and compressor installations by electric

drive engines. This new set up will also significantly improve the carbon footprint of the

operations with no requirement of fuel oil usage and substantial reduction in down-times due

to repeated maintenance on the old engines and compressors. These operational

improvements should be effective before the end of the year 2017.

As of the date this report, the Company is completing the drilling of the Lachambre well and

will start its production test in April. The Company is currently preparing for the drilling of

the next well at Pontpierre as part of its ongoing drilling campaign in Lorraine. The drilling

program’sobjective is to develop four production pads in Lorraine and start production of its

first local gas during the second half of the calendar year 2017. The on-going short term

drilling development program will cost a total of less than € 20 million, a significant cost

reduction of ca. 20% versus the initial budget. The Company has also increased its staffing

levels by hiring for its Lorraine operations three people, including a drilling engineer, a

drilling advisor and a chief procurement officer, to achieve these cost reduction and

operational improvements objectives.

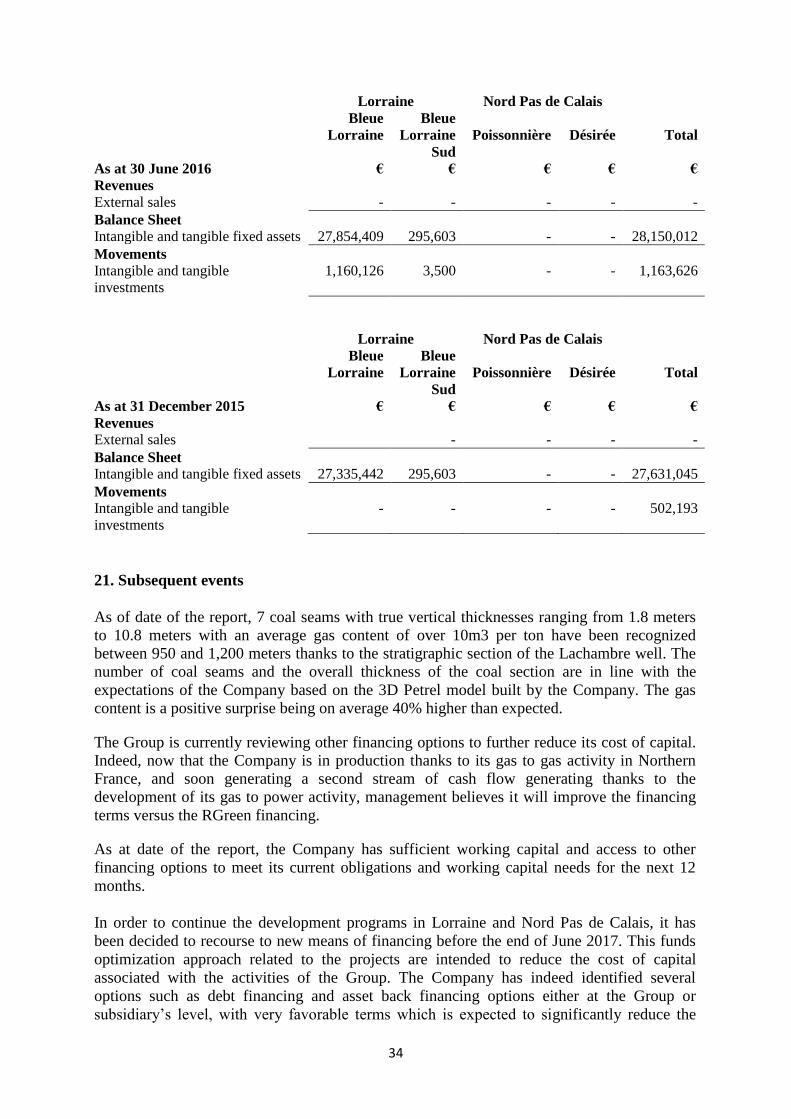

The Company spuds the first well on 7 December 2016, stopped for 10 days around

Christmas and restarted the drilling on January 2017. To date, 7 coal seams with true vertical

thicknesses ranging from 1.8 meters to 10.8 meters with an average gas content of over 10m3

per ton have been recognized between 950 and 1200 meters thanks to the stratigraphic section

of the Lachambre well. The number of coal seams and the overall thickness of the coal section

4

are in line with the expectations of the Company based on the 3D Petrel model built by the

Company. The gas content is a positive surprise being on average 40% higher than expected.

On 22 September 2016, the framework financing agreement with RGreen Invest for up to

€60,000,000 which was initially signed in May 2016, was extended until 31 December 2016.

At the date of this report, the Company has decided not to extend the RGreen facility. Given

the operational progress and the granting of the guaranteed feed in tariff, management of the

Company will decide on the best financing infrastructure before the Financial year ending 30

June 2017.

As at date of the report, the Company has sufficient working capital and access to other

financing options to meet its current obligations and working capital needs for the next 12

months.

In order to continue the development programs in Lorraine and Nord Pas de Calais, it has

been decided to recourse to new means of financing before the end of June 2017. This funds

optimization approach related to the projects are intended to reduce the cost of capital

associated with the activities of the Group. The Company has indeed identified several

options such as debt financing and asset back financing options either at the Group or

subsidiary’s level, with very favorable terms which is expected to significantly reduce the

cost of capital of the Company and allow for a full financing of its future investment needs

for 2018 onwards.

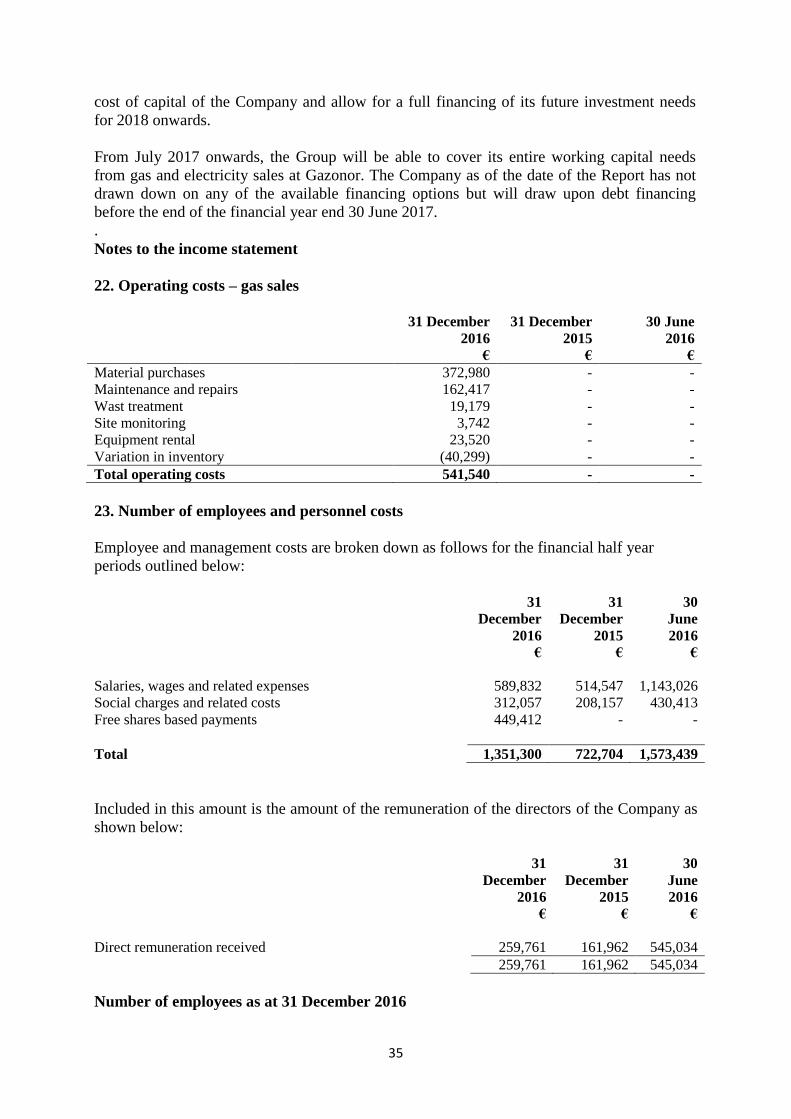

From July 2017 onwards, the Group will be able to cover its entire working capital needs

from gas and electricity sales at Gazonor.

The Company as of the date of the Report has not drawn down on any of the available

financing options but will draw upon debt financing before the end of the financial year end

30 June 2017.

In November 2016, the Company started a legal action against Société Générale, the lead

bank of the Company’s IPO on Euronext, to claim the reimbursement of part of the fees

related to this transaction. The Company indeed considers that Société Générale wrongly

retained an amount of fees exceeding the fees to which Société Générale was entitled.

5

3. FINANCIAL RESULTS FOR HALF YEAR 2016/2017

3.1 FINANCIAL RESULTS

The Group generated operating revenues of € 1,859,671 for the six-month period ending 31

December 2016, generated mainly from Gazonor (following its acquisition made through the

acquisition of its holding company Transcor Astra Luxembourg SA, since then renamed

LFDE International SA, hereinafter « LFDE International »). In the previous accounting

periods, the group did not generate any revenues.

The operating result, before interest, depreciation and amortisation (EBITDA) amounted to a

loss of € 1,069,847 for the half year to 31 December 2016 compared to a loss of € 1,512,766

for the half year to December 2015. The decrease in losses in the operating results mainly

relates to the gas sales contribution of Gazonor and to certain base cost reductions over the

last six months. The operating loss is mainly driven by the SG&A of the Group amounting to

€ 2,543,828 and inventory purchases for operations amounting to € 541,540. This SG&A

includes the wages and salaries of the Group. Furthermore, substantial expenses in relation to

legal fees and remaining payments for IPO advisory settled during the first months of the first

half year ended 31 December are included in these costs. During the first semester of the

financial year ending 2017, an amount of 449.412 € related to the share based payment

approved on 30 June 2016, have also been recorded in the SG&A costs. We expect a

significant reduction of our working capital needs in the current financial half year up to 30

June 2017.

The net financial result amounts to a loss of € 1,768,956 for the first half of the financial year

ended 31 December 2016 versus € 1,878,836 for the first half of the financial year ended

31 December 2015.

3.1.1 Revenues

During the first semester of the financial year ending 30 June 2017, the Company generated

revenues from operating activities amounting to € 1,859,671. This relates to the production

and sale of gas at Gazonor SAS in Nord Pas de Calais through an off-take contract with Total

Gas and Power, our long-term client in Northern France.

3.1.2 Other income

Other income of € 155,850 generated in the first half of the financial year ended 31 December

2016 was in relation to the penalty payment from the French government in respect of a

delayed renewal of the permits in Nord Pas des Calais and a repayment of court fees for the

cancelation of the arbitration between Trancor Astra Luxembourg and the Company as part of

the Gazonor acquisition on 27 June 2016.

6

3.1.3 Operating expenses

The detailed operating expenses are outlined in the table below:

Other operating expenses 6 months 6 months 12 months

31

December

2016

31

December

2015

30

June

2016

€ € €

Salaries and wages 1,351,300 722,704 1,573,439

Office and building rentals 51,848 42,707 86,949

Consulting, legal

& other fees

667,503 395,308 2,918,082

Marketing / PR 25,809 122,627 530,097

Taxes 56,721 9,633 13,617

Electricity, consumables and energy 2,861 1,739 6,309

Other general expenses 387,786 218,048 527,835

Total 2,543,828 1,512,766 5,656,328

On an adjusted basis, other operating expenses were 68.2% higher than last year (mainly due

to the acquisition of Gazonor). Salaries and wages amounted to € 1,351,300 and all other

SG&A amounted to € 1,192,528 as shown above. Consulting, legal and other fees amounted

to € 134,163 mainly relate to legal fees in relation to the IPO, audit fees and corporate

consulting for an amount of € 272,726 and other external services in relation to the on-going

projects amounted to € 260,160. Other general expenses include corporate insurance

payments, travelling and subsistence, costs of an ERP implementation and IT upgrades in

relation to the acquisition of Gazonor to continue to strengthen our monitoring of the

operations and continue to improve financial controls in the Company

The Group has, on consolidated basis, higher employee and management costs since the

acquisition of Gazonor. The Group, however, streamlined the management of Gazonor and

also reduced the base costs of the group on a combined level. One offs redundancy costs

amounted to € 177,784 were significant during this first half and we expect an ongoing

reduction of our overall cost base going forward.

3.1.4 Cost of financial debt and other financial expenses

Financial expenses of € 337,825 were lower for the first six months ended 31 December 2016

due to the conversion of the convertible bonds at IPO date of the Group in June 2016. As a

result, the company has no more short term financial liabilities on its balance sheet.

Financial expenses correspond to the impact of the fair value adjustment of the debt to

EGLUK for an amount of € 229,000 (see note 18 to the consolidated financial statements) and

to the decrease in value of the liquidity contract in place with Aurel for an amount of

€ 108,825 for the first six months ended December 31, 2016.

7

3.1.5 Capitalised expenses

Intangible assets

The above analysis of the Company’s income statement does not reflect amounts allocated to

exploration costs on existing permits, as these are capitalised and are therefore not included in

the Company’s income statement.

Total capitalised exploration costs relating to the Company’s exploration permits for the

Lorraine project are presented in the table below:

€

Bleue Lorraine 29,738,630

Bleue Lorraine Sud 299,103

Total costs relating to

Lorraine permits

30,037,733

The substantial amount of capitalised expenses recognised for the Bleue Lorraine permits

reflects the costs of the drilling campaigns conducted in the past and, more recently, the on-

going drilling activities at Lachambre and site preparations for the 4 wells drilling campaign.

Total exploration expenses capitalised by the Company as part of the Nord-Pas-de-Calais

exploration program mainly relate to seismic processing work, permit applications, data

processing, Petrel software modelling and DAOTMs (applications for authorisation to launch

mining works). The breakdown of these capitalised expenses is presented below:

Valenciennois (NPC)

€

229,080

Sud-Midi (NPC) 366,684

Poissonnière (NPC) 394,283

Total expenses linked to NPC permits 990,047

Capitalised exploration costs for activities at Gardanne and Lons-le-Saunier are presented

below:

Lons-le-Saunier

€

220,061

Gardanne 74,259

Total expenses for other projects 294,320

Expenses related to operations in Gardanne and Lons-le-Saunier pertain to geological studies

and other mining work conducted in the past.

Finally, an amount of €1.941.770 has been recorded as intangible assets in respect of the

exploration permit ‘’ La Folie De Paris’’, held since the acquisition of Concord Energy Inc.,

without any evolution since the financial year ended 30 June 2016.

8

Tangible assets

Work in progress in relation to the electricity project at Gazonor amounted to € 1,009,122

during the first half of 2017.

3.2 PRINCIPAL RISKS AND UNCERTAINTIES

The Company does not anticipate any substantial changes in its risks, as described in

Chapter 4 of its annual financial report for fiscal year 2015/2016 published on October 31,

2016, which may have an impact on the second semester of the financial year end 30 June

2017. The Company has not identified new risks compared to the risks already identified and

the liquidity risks are set out in Note 21 to the half year consolidated financial statements.

3.3 FUTURE OUTLOOK

The Company believes that the outlook for growth in the Group’s businesses is promising.

Firstly, France and Europe are increasingly dependent on Russian natural gas and are hoping

to reduce dependence by importing American shale gas, which is arriving in Europe in the

form of LNG.

Furthermore, France and Europe are committed to reducing their carbon footprints through

energy transition. A move away from coal and nuclear power means gas is becoming more

important in the balancing of the energy mix in Europe and with the expected implementation

of a carbon tax at some point in the near future.

Our business, which focuses on the production of local clean gas for the benefit of regional

retail and industrial consumers through the establishment of short supply chains, is a real

solution for reducing the carbon footprint of the regions in question: replacing imported

natural gas with cleaner local gas.

In Nord-Pas-de-Calais, our gas production activity has been affected by a decrease of the gas

prices and a limited availability of machinery over the summer. However the pricing

environment has picked up again and it is anticipated that gas prices will stabilise at around

€ 15/MWh of gas. In addition, the mechanical improvements made to the gas production and

compression equipment at the Avion site are intended to significantly improve machine

availability in order to boost the gas volumes injected into the network.

At the same time, Gazonor is developing a new business line dedicated to the production of

green electricity from the gas captured in the former coal mines before it goes to the

atmosphere. This activity benefits from a subsidised green feed-in tariff under the decree

published on 4 November 2016 by the French State. This decree provides for a 15 years

guaranteed feed-in tariff for any power produced from captured coal mine methane. The

Company is therefore accelerating the development of this new activity and the installation of

the first 9 MW of Jenbacher 420 engines at four different sites in Nord Pas de Calais is

expected to be completed by June 2017.

The Group is also continuing to assess growth and development opportunities in bordering

countries and notably in Belgium and Germany.

9

In Lorraine, the drilling of the Lachambre well is about to be completed with the objective to

dewater and test our initial gas production before the financial year end 30 June 2017.

Studies continue in the other areas of the Lorraine basin in order to set up next drilling sites

and to obtain the certification of new proven reserves before launching production operations

on those sites.

As at date of the report, the Company has sufficient working capital and access to other

financing options to meet its current obligations and working capital needs for the next 12

months.

In order to continue the development programs in Lorraine and Nord Pas de Calais, it has

been decided to recourse to new means of financing before the end of June 2017. This funds

optimization approach related to the projects are intended to reduce the cost of capital

associated with the activities of the Group. The Company has indeed identified several

options such as debt financing and asset back financing options either at the Group or

subsidiary’s level, with very favorable terms which is expected to significantly reduce the

cost of capital of the Company and allow for a full financing of its future investment needs

for 2018 onwards.

From July 2017 onwards, the Group will be able to cover its entire working capital needs

from gas and electricity sales at Gazonor.

The Company as of the date of the Report has not drawn down on any of the available

financing options but will draw upon debt financing before the end of the financial year end

30 June 2017.

3.4 RELATED PARTY TRANSACTIONS

The information regarding transaction with related parties is presented in Note 18 of the half-

year consolidated financial statements set forth in Chapter 4 of this report.

10

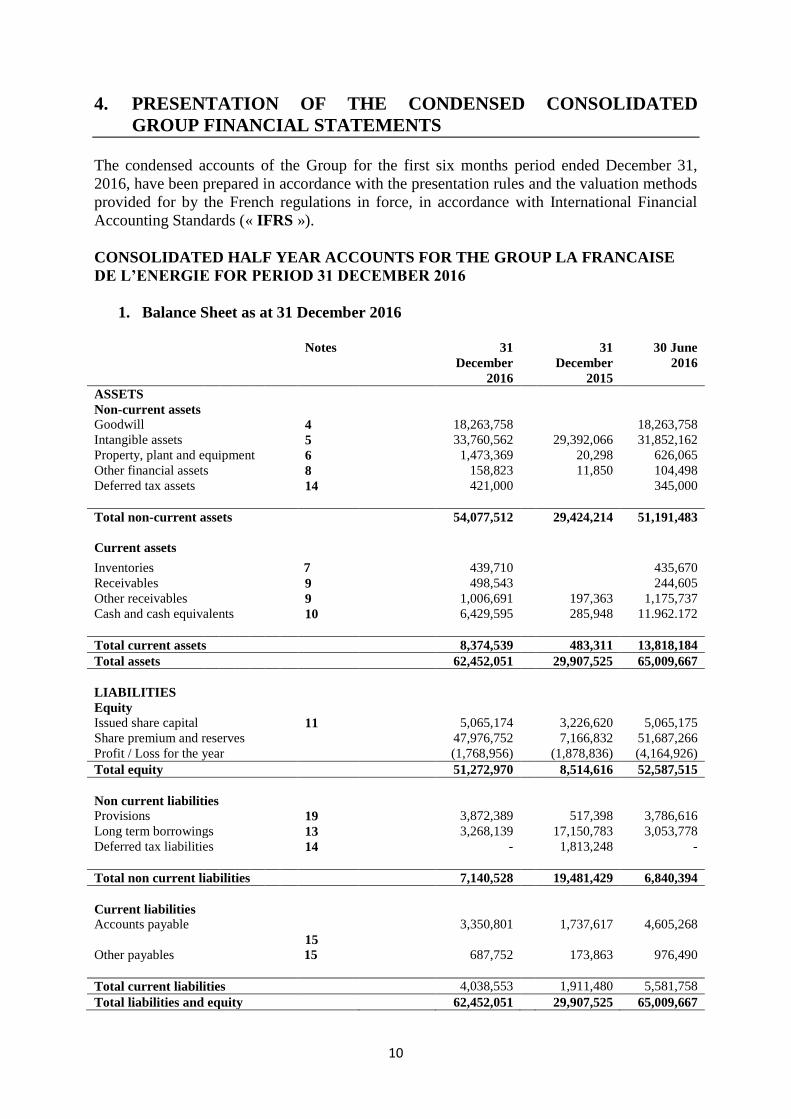

4. PRESENTATION OF THE CONDENSED CONSOLIDATED

GROUP FINANCIAL STATEMENTS

The condensed accounts of the Group for the first six months period ended December 31,

2016, have been prepared in accordance with the presentation rules and the valuation methods

provided for by the French regulations in force, in accordance with International Financial

Accounting Standards (« IFRS »).

CONSOLIDATED HALF YEAR ACCOUNTS FOR THE GROUP LA FRANCAISE

DE L’ENERGIE FOR PERIOD 31 DECEMBER 2016

1. Balance Sheet as at 31 December 2016

Notes 31

December

2016

31

December

2015

30 June

2016

ASSETS

Non-current assets

Goodwill 4 18,263,758 18,263,758

Intangible assets 5 33,760,562 29,392,066 31,852,162

Property, plant and equipment 6 1,473,369 20,298 626,065

Other financial assets 8 158,823 11,850 104,498

Deferred tax assets 14 421,000 345,000

Total non-current assets 54,077,512 29,424,214 51,191,483

Current assets

Inventories 7 439,710 435,670

Receivables 9 498,543 244,605

Other receivables 9 1,006,691 197,363 1,175,737

Cash and cash equivalents 10 6,429,595 285,948 11.962.172

Total current assets 8,374,539 483,311 13,818,184

Total assets 62,452,051 29,907,525 65,009,667

LIABILITIES

Equity

Issued share capital 11 5,065,174 3,226,620 5,065,175

Share premium and reserves 47,976,752 7,166,832 51,687,266

Profit / Loss for the year (1,768,956) (1,878,836) (4,164,926)

Total equity 51,272,970 8,514,616 52,587,515

Non current liabilities

Provisions 19 3,872,389 517,398 3,786,616

Long term borrowings 13 3,268,139 17,150,783 3,053,778

Deferred tax liabilities 14 - 1,813,248 -

Total non current liabilities 7,140,528 19,481,429 6,840,394

Current liabilities

Accounts payable

15

3,350,801 1,737,617 4,605,268

Other payables 15 687,752 173,863 976,490

Total current liabilities 4,038,553 1,911,480 5,581,758

Total liabilities and equity 62,452,051 29,907,525 65,009,667

11

2. Consolidated Income Statement

Notes

6 months

31 December

2016

6 months

31 December

2015

12 months

30 June

2016

Sales 1,859,671 - -

Other income 155,850 - -

Material purchases

General and administrative expenses 22

(541,540)

(2,543,828)

-

(1,512,766)

-

(5,656,328)

Amortisation of tangible assets and

mineral rights (168,397) (5,538) (11,816)

Provisions (96,294)

Operating Profit (1,334,538) (1,518,304) (5,668,144)

Other income - - -

Other expenses - - -

Cost of net debt - (600,000) (1,113,750)

Other financial income - - -

Other financial charges (337,825) (690,000) (1,237,000)

Net foreign exchange difference 1,488 (4,532) (2,209)

Profit before goodwill and tax (1,670,875) (2,812,836) (8,021,102)

Negative goodwill - - 1,189,556

Income taxes

14 (98,080) 934,000 2,666,622

Consolidated net loss (1,768,956) (1,878,836) (4,164,926)

Net loss – equity holder of the

parent

(1,768,956) (1,878,836) (4,164,926)

Total comprehensivce loss (1,768,956) (1,878,836) (4,164,926)

Earnings per share (0,35) (0,58) (1,26)

Fully diluted earnings per share

(0,35)

(0,58)

(1,23)

12

3. Consolidated statement of change in equity

Shares

Number

Issued

Amount

Issued share

capital

Consolidated

Retained

earnings

Total

Equity

€ € €

As at 1 July 2015 3,226,620 3,226,620 5,682,601 8,909,221

Net income/(loss) for the year 2016 (4.164.926) (4.164.926)

New issue of shares – Initial Public offering 1,388,889 1,388,889 36,111,114 37,500,003

,

Transaction costs (1.204.561) (1.204.561)

Conversion of convertible loan note 449,666 449,666 9,263,118 9,712,784

Fair value adjustment

- - (5.247.000) (5.247.000)

Forgiveness of debt - - 8,000,000 8,000,000

Income tax on loan forgiveness (2.667.253) (2.667.253)

Deferred tax on fair value adjustment - - 1,749,248 1,749,248

As at 30 June 2016 5,065,175 5,065,175 47,522,340 52,587,515

As at 1 July 2016 5,065,174 5,065,174 47,522,340 52,287,515

Net income / (loss) for the Half Year 31

December 2016

- - (1,768,956) (1,768,956)

Fair value adjustment (note 14) - - 5,000

Share based payments (note 13) - - 449,412 449,412

Forgiveness of debt (note 14) - - - -

Deferred tax on fair value adjustment

(note 15)

- -

As at 31 December 2016 5,065,174 5,065,174 46,207,796 51,272,970

13

4. Consolidated Cash Flow Statements 6 months

31 December

2016

6 months

31 December

2015

12 months

30 June

2016

Consolidated net income / (loss) (1,768,956) (1,878,836) (4,164,926)

Non-monetary

adjustments:

Elimination of Depreciation,

amortization and provisions 254,172 8,415 11,816

Income and expenses related to the

share-based payment

449,412 - -

Elimination of deferred tax assets (76,000) (934,000) (2,666,622)

Debt issuance costs - - -

Cost of financial debt - 600,000 1,100,000

Other financial costs 229,000 690,000 1,206,607

Negative goodwill - - (1.189.556)

(Increase) decrease in working capital (1,632,137) 388,195 2,292,321

Income tax paid - - -

Net cash flow from operating

activities

(2,544,509) (1,126,226) (3,410,360)

Net acquisition costs of participation - - (16,073,666)

Purchase of intangible assets

(24,000) - -

Exploration costs capitalized (1,887,721) (502,193) (1,163,626)

Purchase of Property, plant & equipment

additions

(1,012,380) - (1,508)

Other financial assets investments

(54,328) (92,648)

Net cash flow from investing

activities

(2,978,429) (502,193) (17,331,448)

Issue of new shares - - 37,500,003

Transaction costs - - (1,805,939)

Payments to EGL UK (9.639) (530,482) (5,034,933)

Payments received from EGL UK - 400,000 -

Interest paid -

Net cash flow from financing

activities

(9,639) (130.482) 30.659.131

NET INCREASE

(DECREASE) IN CASH

(5,532,577) (1,758,901) 9,917.323

Cash at the beginning of the period 11,962,172 2,044,849 2,044,849

Cash at the end of the period 6,429,595 285,948 11,962,172

14

In the consolidated cash flow statement above, net cash includes cash and cash equivalents net

of current bank borrowings. Marketable securities, in accordance with IAS 39, are shown in

the balance sheet at their market value at the balance sheet date as at 31 December 2016.

The cash flow statement does not show the following items as they were as they were non-

monetary transactions:

- The forgiveness of debt amounting to € 8,000,000 (2015: € 2,200,000) which has been

accounted for directly in equity on 30 June 2016; and

- The fair value adjustment of the loan resulting from the agreement dated December 12, 2014

whereby the existing loan was formulated into a 5 years non-bearing interest loan maturing on

12 December 2019.

5. Notes to the consolidated financial statements for the first half 2017

1. Accounting policies and general principles

The consolidated financial statements for the first half of the financial year ended 30 June

2017 have been prepared in accordance with IAS 34 "Interim financial information" on the

preparation of the interim financial statements and with the international accounting standards

and interpretations (IAS / IFRS) adopted by The European Union and put in force on

31 December 2016.

These standards and interpretations are applied consistently over the periods presented. The

half-year financial statements are prepared according to the same rules and methods as those

used for the preparation of the 2016 annual financial report filed with the AMF on 31 October

2016. They were approved by the Board of Directors on 30 March 2017.

The purpose of the interim financial statements is to provide shareholders and investors with

relevant information on significant events and transactions during the period. This

information is given, in particular, through a selection of notes explaining the significant

changes in the balance sheet between 30 June 2016 and 31 December 2016 and the main

transactions that contributed to the formation of the first half 2017 half year results. The

interim financial statements do not contain all the information required for full annual

financial statements and must be read in conjunction with the Group's financial statements for

the year ended 30 June 2016 filed with the “Autorité des Marchés Financiers” on 31 October

2016 (available on the Company's website both in English and French).

The preparation of the financial statements in accordance with IFRS requires the Group’s

executive management to make estimates and assumptions that can affect the carrying

amounts of assets, liabilities and contingent liabilities at the date of preparation of the

financial statements and reported income and expenses for the period. The executive

management reviews these estimates and assumptions on an on-going basis, by reference to

past experience and various other factors considered as reasonable for assessing in particular

the assets and liabilities carrying book value. These judgements and estimates are made on the

basis of information or circumstances existing at the date of preparation of the financial

statements, which may later differ from the actual results. The implementation of these

estimates and assumptions relates principally to the application of the successful efforts

15

method for the oil & gas activities, depreciation of fixed assets, provisions for site

rehabilitation (environmental remediation) and provisions for risks and charges linked to the

environment, valuation of financial instruments, valuation of derivatives and share based

payments and deferred taxes.

Furthermore when the accounting treatment of a specific transaction is not addressed by any

accounting standard or interpretation, the executive management applies its judgment to

define and apply accounting policies that provide information consistent with the general

IFRS concepts: true and fair view, relevance and materiality.

The interim consolidated financial statements for the year ended December 31, 2016 are not

impacted by mandatory regulations from January 1, 2017. The Group has not adopted the

latest standards, interpretations and amendments to existing standards recently published by

the IASB but not yet been adopted by the European Union or adopted at the European level,

hence not made mandatory at this stage:

IFRS 9 – Financial instruments and amendments (not adopted - applicable to

accounting periods beginning January 1st, 2018);

IFRS 15 – Revenue from contracts with customers (applicable to accounting periods

beginning January 1st, 2017);

2. General accounting principles

Intangible assets

The Group applies IFRS 6 “Exploration for and Evaluation of Mineral Resources”. Oil and

gas exploration and production properties and assets are accounted for in accordance with the

successful efforts method.

Exploration costs

Geology and geophysical costs, including seismic surveys for exploration purposes, are

recorded directly as expenses of the period when incurred.

Mineral interests are capitalized as intangible assets. They are regularly tested for impairment,

license by license, according to the results of the exploration activity and executive

management’s evaluation.

In the event of a discovery, the unproved mineral interests are transferred to proved mineral

interests, at their net book value, as soon as proved reserves are booked.

Exploratory drillings are recorded and tested for depreciation on an individual basis as

follows:

- costs of exploratory drillings which result in proved reserves are capitalized and then

depreciated using the unit of production method based on proved developed reserves;

- the cost of dry wells and drillings that have not found proved reserves are charged to

expenses;

16

- the costs of exploratory drillings are temporarily capitalized until a determination is

made as to whether the drilling has found proved reserves if both of the following

conditions are met:

- the well has found a sufficient quantity of reserves to justify, if appropriate, its

completion as a producing well, assuming that the required capital expenditures are

made,

- the Group is making sufficient progress assessing the reserves and the economic and

operating viability of the project. This progress is evaluated on the basis of indicators

such as whether additional exploratory works are under way or firmly planned (wells,

seismic or significant studies), whether costs are being incurred for development

studies and whether the Group is waiting for governmental or other third-party

authorization of a proposed project, or availability of capacity on an existing transport

or processing facility.

The costs of exploratory drillings not meeting these conditions are charged to expenses.

According to IFRS 6, cost of exploration and evaluation are initially capitalised as intangible

assets until the technical feasibility and commercial viability of extracting a mineral resource

are demonstrable. Therefore, when proved reserves of natural gas are determined and

development is approved by management, the relevant capitalised expenditures are first

assessed for impairment when facts and circumstances suggest that the net book value of the

assets of exploration and evaluation may exceed its recoverable amount and (if necessary)

considers any impairment that may result and the remaining balance is transferred to property,

plant and equipment.

Other intangible assets include patents, software, trademarks, and rights to lease.

Intangible assets are recognized in the balance sheet at acquisition or production cost, less any

depreciation and impairment losses recognized.

Other intangible assets are amortized on a straight-line basis over their useful lives between 3

and 10 years.

Property, plant and equipment

Property, plant and equipment acquired separately are initially measured at their acquisition

cost in accordance with IAS 16. The cost includes expenditures that are directly related to the

acquisition of the asset and the estimated cost of restoration of a portion of the assets if

necessary. Tangible assets acquired in a business combination are recognized and value at

their fair value separately from goodwill.

No property, plant and equipment have been pledged as security for debts and none are

subject to finance lease contracts. Property, plant and equipment are recorded at their

acquisition cost and amortized over a period corresponding to their foreseeable period of use.

Except in exceptional cases, the amortization plans are the same as those used for the parent

company financial statements (excluding an exception for tax purposes).

17

Receivables:

Receivables are valued at their nominal value. They shall be assessed individually and, where

appropriate, shall be subject to a provision for depreciation in order to take into account the

recovery difficulties to which they might be liable.

Inventories:

The inventories consist mainly of maintenance parts for the servicing of the station at Avion

and are valued at the lower of purchase cost or net realizable value. Impairment is recognized

when the net realizable value is lower than cost. No impairment has been recognised for the

financial half year ending 31 December 2016. The accounting method used for the inventories

is based on the first-in first-out basis.

Liquidity contract:

Following the IPO of the Company on the regulated market of Euronext Paris, the Company

signed a liquidity contract with Aurel BGC with a view to reduce the intra-day trading

volatility of the Company shares. This liquidity contract, in compliance with the AFEI Code

of conduct (Association Francaise des Entreprises d’Investissement), was signed on 15 June

2016. The Company has made available to Aurel BCG cash for an amount of € 350,000 to

buy or sell the shares of the Company to ensure liquidity on the stock market. This liquidity

contract resulted in a financial expense of € 108,825 for the six-month period ended 31

December 2016. The impairment loss arose from the sale of securities during the first half of

2017 and the difference between the value of the shares held as at 31 December 2016 and

their historic purchase value at date of purchase during this financial period.

At December 31, 2016, cash and cash equivalents of this liquidity contract amounted to €

95,712 and € 145,463 in other financial assets.

Provisions for pensions and other employment benefits:

In accordance with IAS 19, the Group recognizes its obligations to pay retirement

indemnities. Commitments are valued using the actuarial method of projected credit units,

taking into account actuarial assumptions such as salary increases, age of departure, mortality,

staff turnover and discount rate.

Valuation and recognition of financial liabilities:

Long-term debt consists of the corporate loan from EGLUK which has been put in place as

part of the restructuring of the Group in 2015 (share buy-back transaction in May 2015) and

the subsequent transfer of permits from EGLUK to LFDE.

The EGLUK loan as at 31 December 2016 was valued by discounting future payments at a

market rate of 15% until the maturity date of 12 December 2019. This is consistent with the

risk premium for a company such as La Française de l’Energie and in line with historic rates

used to value the fair value of the loan. Consistent with the principles implemented as part of

the reorganization of the Group as described in the consolidated financial statements at 30

June 2016, this fair value adjustment has been recognized in equity.

18

Share based payments for employees - free shares:

IFRS 2 outlines the recognition of a personnel expense corresponding to benefits granted to

employees in the form of share-based payments. The purchase price of shares and similar

securities is measured through to the fair value at the date on which the equity instruments are

allocated.

The free shares are valued on the basis of the share price of a share at the date of allocation to

the employees.

Goodwill

Goodwill relating to different consolidated subsidiaries are recorded on the consolidated

balance sheet in the ‘’goodwill’’ section.

The acquirer accounts for goodwill at the date of acquisition, evaluated as being the excess of:

The consideration transferred, the amount of any non-controlling interests and, in a

business combination achieved in stages, the fair value of any previously held equity

interest remeasured at its acquisition date, less;

The fair value, at the acquisition date, of the identifiable acquired assets and assumed

liabilities.

If the consideration transferred is lower than the aggregate fair value of the identifiable assets

acquired and liabilities recorded, the group re-assesses whether it has correctly identified all

the assets acquired and all the liabilities assumed. If the reassessment still results in an excess

of the fair value of net assets acquired over the aggregate consideration transferred, then the

negative goodwill is recognized directly in the income statement.

When transactions with non-controlling interests have no impact on control, the difference

between the consideration transferred and the book value of the acquired non–controlling

interests is accounted for directly in equity.

Goodwill is not amortized but is subject to an impairment test at least once a year. When an

impairment loss is recognized, the difference between the carrying value of the asset and its

recoverable amount is expensed through the statement of comprehensive income during the

financial year in the section operating results.

Revenue recognition:

In accordance with IAS 18, sales are measured at the fair value of the expected consideration,

net of discounts, rebates and rebates, excluding VAT and other taxes. In the case of the group,

the revenue is recorded as of the date when the Group transferred to the buyer the ownership

and risks of the products sold.

Recognition of turnover for gas sales is made in accordance with the contractual terms of the

sales contract with Total and a gas liquidity contract with GRT covering the over /

underselling of gas quantity as per the contractual T&C’s.

19

Income tax:

Income tax expense is equal to the sum of current and deferred taxes. With regard to deferred

tax, it is based on the validity period for tax losses determined by French law and using the

possibilities of losses carried forward.

The tax charge for the first half-year is determined by applying to pre-tax income the effective

tax rate of the Company estimated for the financial year 2017 (including deferred taxes). This

rate is, where appropriate, adjusted for tax implications related to unusual items for the period.

Use of estimates:

The preparation of financial statements in accordance with IFRS requires the use of estimates

and assumptions that affect the amounts reported in these financial statements, including the

following:

(ii) valuations used for value tests;

(iii) valuation of share-based payments;

(iv) recognition of deferred tax assets;

(v) the valuation of financial instruments;

These estimates are based on assumptions which are based on the information available at the

time of their establishment. Estimates may be revised if the circumstances on which they are

based change or as a result of new information. Actual results may differ from these

estimates.

Going concern:

The management of the Group regularly reviews its financing options in order to ensure

continuity of operations, in particular with regard to its various assets and liabilities an income

from its gas sales.

The Group's current working capital requirement (including direct costs of gas sales) amount

to circa € 400,000 per month and its current cash resources enable the group to finance its

current activities under AFE and support its working capital requirements until June 2017

without drawing down further funding. As a result, the Group is committed to maintaining a

very broad access to liquidity in order to meet its financial commitments and requirements. As

at December 31, 2016, the Group had cash or cash equivalents in the amount of € 6,429,595.

As at date of the report, the Company has sufficient working capital and access to other

financing options to meet its current obligations and working capital needs for the next 12

months.

In order to continue the development programs in Lorraine and Nord Pas de Calais, it has

been decided to recourse to new means of financing before the end of June 2017. This funds

optimization approach related to the projects are intended to reduce the cost of capital

associated with the activities of the Group. The Company has indeed identified several

options such as debt financing and asset back financing options either at the Group or

subsidiary’s level, with very favorable terms which is expected to significantly reduce the

cost of capital of the Company and allow for a full financing of its future investment needs

20

for 2018 onwards.

From July 2017 onwards, the Group will be able to cover its entire working capital needs

from gas and electricity sales at Gazonor.

The Company as of the date of the Report has not drawn down on any of the available

financing options but will draw upon debt financing before the end of the financial year end

30 June 2017.

Notes to the Balance Sheet

3. Scope of the first half consolidated accounts 31 December 2016:

The consolidated financial statements include the financial statements of the Company and its

direct and indirect subsidiaries, all of which are fully consolidated.

The consolidated financial statements of the Company and its subsidiaries are presented in

euros, which is also the functional currency of the company and its subsidiaries, except

Concorde Energy Inc. (US dollar).

The list of subsidiaries and shareholdings, with an indication of the share of the capital held

for the financial year ended December 31, 2016, is stated below:

Subsidiaries and shareholdings % equity held

Direct subsidiaries

EG NPC SAS 100%

EG Lorraine SAS 100%

EG Jura SAS 100%

EG Gardanne SAS 100%

LFDE International SA 100%

Concorde Energy Inc. 100%

Indirect subsidiaries

Gazonor Holding SAS 100%

Gazonor SAS 100%

European Gas Benelux 100%

Concorde Energie Paris SAS 100%

As of the date of this report, the direct and indirect subsidiaries have no operational activities,

with the exception of Gazonor SAS, a French company devoted to research, extraction,

purification, and sale of coal mine gas (CMM) and coal bed gas (CBM) recovered in the

basins of the former Nord-Pas-de-Calais mining area. Consequently, Gazonor SAS's main

activity is the exploitation and sale of coal mine gas. Following the issuance by the French

government of a decree declaring the production of electricity from coal mine methane as

green energy, Gazonor SAS will, in addition, start producing electricity from four of its sites

by June 2017 through the installation of 9 MW of gas engines.

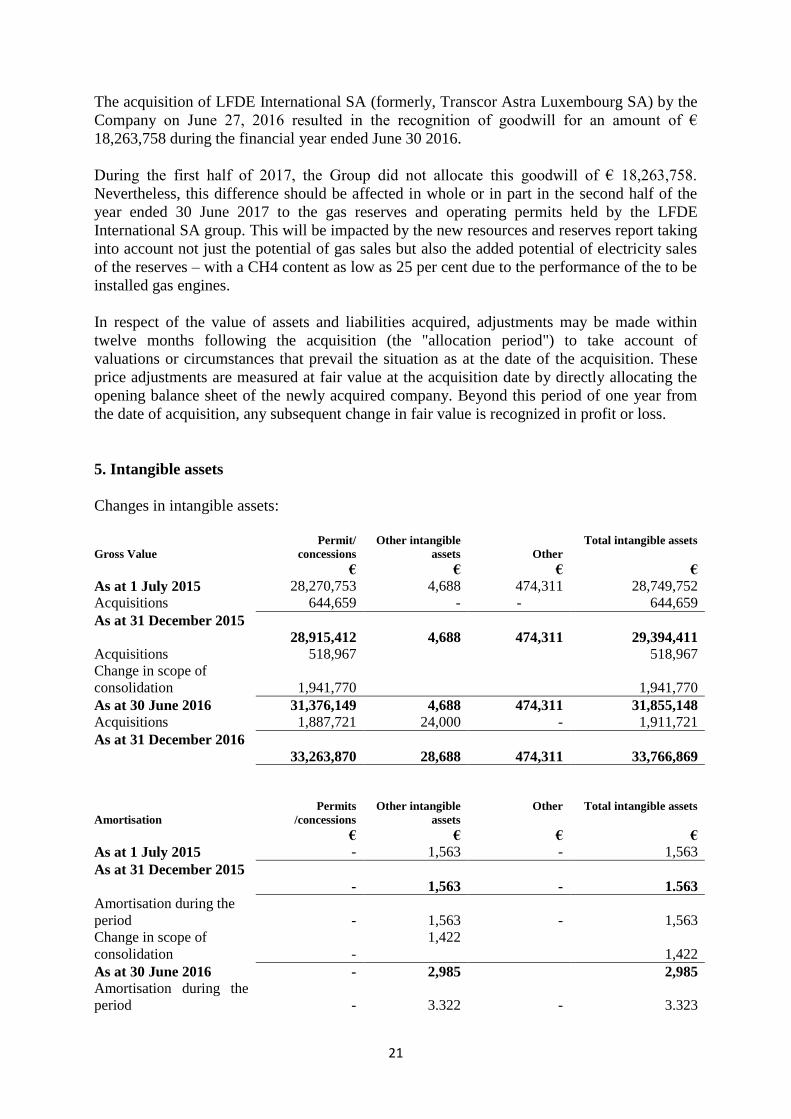

4. Goodwill

21

The acquisition of LFDE International SA (formerly, Transcor Astra Luxembourg SA) by the

Company on June 27, 2016 resulted in the recognition of goodwill for an amount of €

18,263,758 during the financial year ended June 30 2016.

During the first half of 2017, the Group did not allocate this goodwill of € 18,263,758.

Nevertheless, this difference should be affected in whole or in part in the second half of the

year ended 30 June 2017 to the gas reserves and operating permits held by the LFDE

International SA group. This will be impacted by the new resources and reserves report taking

into account not just the potential of gas sales but also the added potential of electricity sales

of the reserves – with a CH4 content as low as 25 per cent due to the performance of the to be

installed gas engines.

In respect of the value of assets and liabilities acquired, adjustments may be made within

twelve months following the acquisition (the "allocation period") to take account of

valuations or circumstances that prevail the situation as at the date of the acquisition. These

price adjustments are measured at fair value at the acquisition date by directly allocating the

opening balance sheet of the newly acquired company. Beyond this period of one year from

the date of acquisition, any subsequent change in fair value is recognized in profit or loss.

5. Intangible assets

Changes in intangible assets:

Gross Value

Permit/

concessions

Other intangible

assets

Other

Total intangible assets

€ € € €

As at 1 July 2015 28,270,753 4,688 474,311 28,749,752

Acquisitions 644,659 - - 644,659

As at 31 December 2015

28,915,412

4,688

474,311

29,394,411

Acquisitions 518,967 518,967

Change in scope of

consolidation

1,941,770

1,941,770

As at 30 June 2016 31,376,149 4,688 474,311 31,855,148

Acquisitions 1,887,721 24,000 - 1,911,721

As at 31 December 2016

33,263,870

28,688

474,311

33,766,869

Amortisation

Permits

/concessions

Other intangible

assets

Other Total intangible assets

€ € € €

As at 1 July 2015 - 1,563 - 1,563

As at 31 December 2015

-

1,563

-

1.563

Amortisation during the

period

-

1,563

-

1,563

Change in scope of

consolidation

-

1,422

1,422

As at 30 June 2016 - 2,985 2,985

Amortisation during the

period

-

3.322

-

3.323

22

As at 31 December 2016

-

6,307

6,307

NET VALUE

As at 31 December 2015

28,915,412

3,125

474,311

29,392,848

As at 30 June 2016 31,376,149 1,703 474,311 31,852,163

As at 31 December 2016

33,263,870

22,381

474,311

33,760,562

Permits / concessions primarily include exploration expenditures and exploration drilling

costs that are recognized as intangible assets and are not amortized. On the other hand, they

may be subjected, if necessary, to an impairment test on an individual basis as per the Groups

accounting policies on capitalised expenses and intangible assets.

Acquisitions in the first half of 2017 for an amount of € 1,887,721 mainly include the cost of

the drilling at the Lachambre site.

Other intangible assets mainly include software. In the first half of 2017, the acquisition of the

licenses for the new Sage X3 software for an amount of € 24,000 was recognized as other

intangible assets, which was implemented as of July 1, 2016.

"Other" includes a provision to cover the costs of abandoning wells and restoring the

Tritteling site to its original form in the event that the exploration and drilling activity is

discontinued.

As at December 31, 2016, the exploration assets break-down is outlined below by each

exclusive research license / permit or concession, excluding provisions for rehabilitation:

Exploration licences

31

December

2016

31

December

2015

30 June

2016

€

€ €

Bleue Lorraine Renewed until 30 Nov. 2018 29,738,630 27,335,442 27,854,409

Bleue Lorraine Sud Renewed until 7 Nov. 2016 299,103 295,603 295,603

Bleue Lorraine Nord Licence award in progress - - -

La Grande Garde Licence award in progress - - -

Lons-le-Saunier (Jura) Request 2nd

period applied for

(reject (1)

)

220,061

220,061

220,061

Gardanne Request 3rd

period applied for

(reject (1)

)

74,259

74,259

74,259

École supérieure Under review (implicit rejection (1)

)

-

-

-

Chéroy Under review (implicit rejection (1)

)

-

-

-

Courgivaux Under review (implicit rejection (1)

)

-

-

-

Deux-Nanteuil Under review (implicit rejection (1)

)

-

-

-

Dormans Under review (implicit rejection (1)

)

-

-

-

23

Exploration licences

31

December

2016

31

December

2015

30 June

2016

€

€ €

La Folie de Paris Renewed on 7 August 2016 (2)

1,941,770 - 1,941,770

La Sole Under review (implicit rejection (1)

)

-

-

-

Les Chollets Rejected (1)

- - -

L’Ourcq Rejected (1)

- - -

Marigny Under review (implicit rejection (1)

)

Ozoir Under review (implicit rejection (1)

)

Valenciennois (NPC) Renewed on 20 March 2017 229,080 229,080 229,080

Sud-Midi (NPC) Renewal request in progress 366,684 366,684 366,684

Poissonière (NPC) Renewed on 29 May 2015 394,283 394,283 394,283

Desiree (NPC) Renewed on 29 May 2015

Total exploration assets 33,263,870 28,915,412 31,376,149

(1) In accordance with Article 23 of Decree No. 2006-648, an implicit rejection decision occurs on the expiry of a

period of two years from the original application. This implicit rejection decision can be appealed with the Minister

and / or have recourse before the administrative courts. Given the recurrent delays of the government departments

in the processing of applications for extension or granting of mining permits in France, and with experience on

previous permit applications, the Group's management considers that it is not necessary to write down these assets

at this stage of the administrative process, as no explicit refusal decision of the application has been obtained from

the French government to date. Therefore, management believes that there is still a chance, the permit could be

granted as in practice, even after expiry of the applicable time limits and rejection situation, the administration may

take a decision to grant the permit applied for.

(2) The renewal application has been timely submitted and the company is waiting for the decision of the French

authorities.

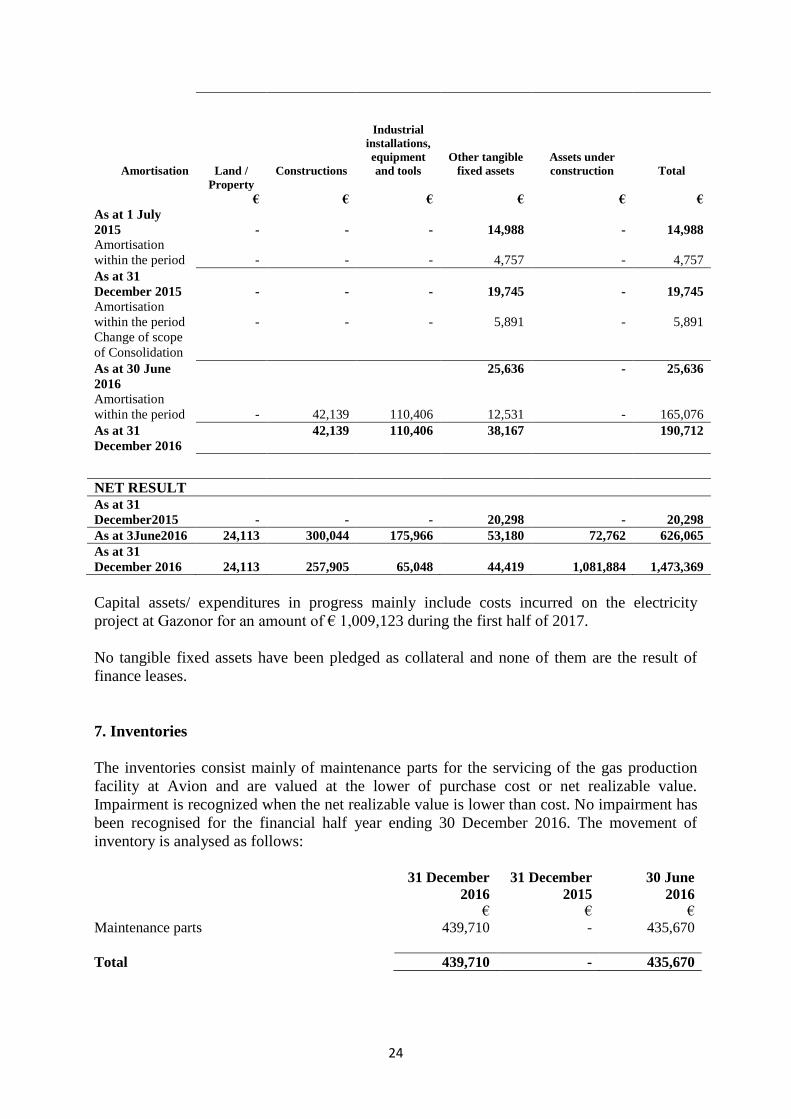

6 Property, plant & equipment

The break-down of the property, plant and equipment for the periods up to 31 December 2016

is outlined below:

Gross value

Land /

Property

Constructions

Industrial

installations,

equipment

and tools

Other tangible

fixed assets

Assets under

construction

Total

€ € € € € €

As at 1 July

2015

-

-

-

40,043

-

40,043

As at 31

December 2015

-

-

-

40,043

-

40,043

Acquisitions - - - 1,508 - 1,508

Change in scope

of consolidation

24,113

300,044

175,966

37,265

72,762

610,150

As at 30 June

2016

24,113 300,044 175,966 78,816 72,762 651,701

Acquisitions /

additions

- - - 3,258 1,009,122 1,012,380

As at 31

December 2016

24,113

300,044

175,966

82,074

1,081,884

1,664,081

24

Amortisation

Land /

Property

Constructions

Industrial

installations,

equipment

and tools

Other tangible

fixed assets

Assets under

construction

Total

€ € € € € €

As at 1 July

2015

-

-

-

14,988

-

14,988

Amortisation

within the period

-

-

-

4,757

-

4,757

As at 31

December 2015

-

-

-

19,745

-

19,745

Amortisation

within the period

-

-

-

5,891

-

5,891

Change of scope

of Consolidation

As at 30 June

2016

25,636 - 25,636

Amortisation

within the period

-

42,139

110,406

12,531

-

165,076

As at 31

December 2016

42,139 110,406 38,167 190,712

NET RESULT As at 31

December2015

-

-

-

20,298

-

20,298

As at 3June2016 24,113 300,044 175,966 53,180 72,762 626,065

As at 31

December 2016

24,113

257,905

65,048

44,419

1,081,884

1,473,369

Capital assets/ expenditures in progress mainly include costs incurred on the electricity

project at Gazonor for an amount of € 1,009,123 during the first half of 2017.

No tangible fixed assets have been pledged as collateral and none of them are the result of

finance leases.

7. Inventories

The inventories consist mainly of maintenance parts for the servicing of the gas production

facility at Avion and are valued at the lower of purchase cost or net realizable value.

Impairment is recognized when the net realizable value is lower than cost. No impairment has

been recognised for the financial half year ending 30 December 2016. The movement of

inventory is analysed as follows:

31 December

2016

31 December

2015

30 June

2016

€ € €

Maintenance parts 439,710 - 435,670

Total 439,710 - 435,670

25

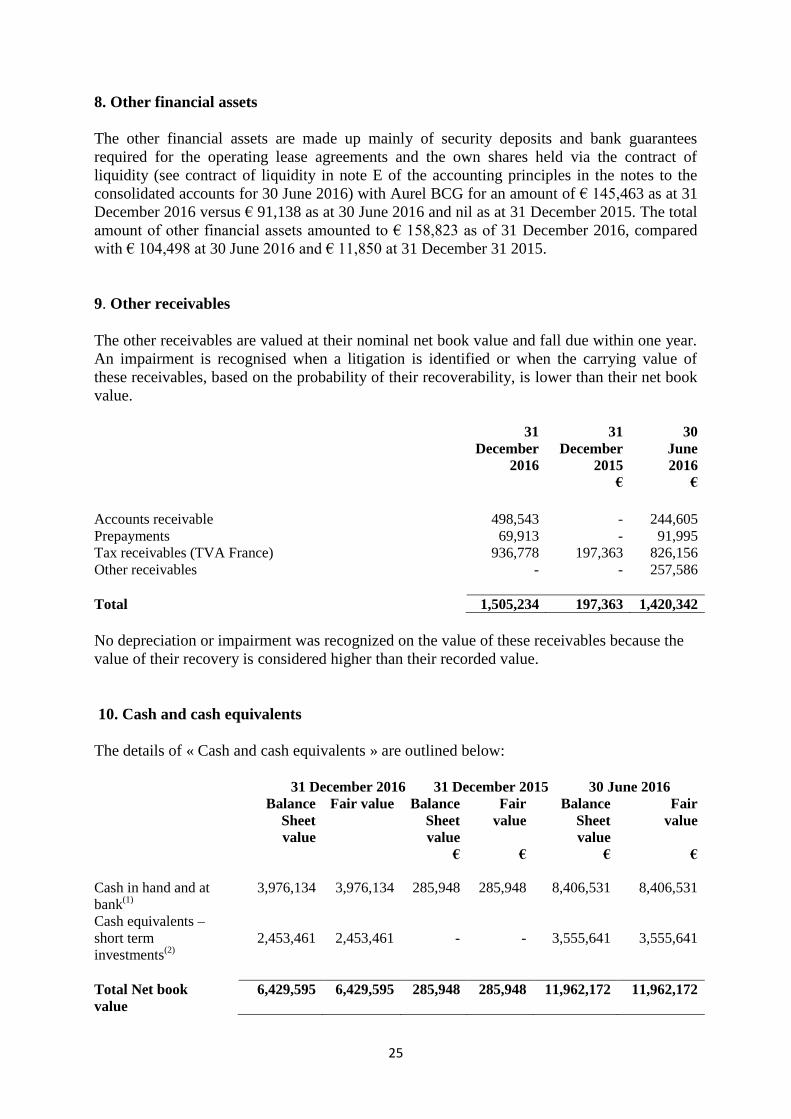

8. Other financial assets

The other financial assets are made up mainly of security deposits and bank guarantees

required for the operating lease agreements and the own shares held via the contract of

liquidity (see contract of liquidity in note E of the accounting principles in the notes to the

consolidated accounts for 30 June 2016) with Aurel BCG for an amount of € 145,463 as at 31

December 2016 versus € 91,138 as at 30 June 2016 and nil as at 31 December 2015. The total

amount of other financial assets amounted to € 158,823 as of 31 December 2016, compared

with € 104,498 at 30 June 2016 and € 11,850 at 31 December 31 2015.

9. Other receivables

The other receivables are valued at their nominal net book value and fall due within one year.

An impairment is recognised when a litigation is identified or when the carrying value of

these receivables, based on the probability of their recoverability, is lower than their net book

value.

31

December

2016

31

December

2015

30

June

2016

€ €

Accounts receivable 498,543 - 244,605

Prepayments 69,913 - 91,995

Tax receivables (TVA France) 936,778 197,363 826,156

Other receivables - - 257,586

Total 1,505,234 197,363 1,420,342

No depreciation or impairment was recognized on the value of these receivables because the

value of their recovery is considered higher than their recorded value.

10. Cash and cash equivalents

The details of « Cash and cash equivalents » are outlined below:

31 December 2016 31 December 2015 30 June 2016

Balance

Sheet

value

Fair value Balance

Sheet

value

Fair

value

Balance

Sheet

value

Fair

value

€ € € €

Cash in hand and at

bank(1)

3,976,134 3,976,134 285,948 285,948 8,406,531 8,406,531

Cash equivalents –

short term

investments(2)

2,453,461

2,453,461

-

-

3,555,641

3,555,641

Total Net book

value

6,429,595 6,429,595 285,948 285,948 11,962,172 11,962,172

26

(1) At the Balance Sheet date of 31 December 2016, Cash in hand and at bank includes a bank balance

amounting to € 3,880,422 and the closing balance of € 95,712 in relation to the liquidity contract with

Aurel BCG.

(2) At balance sheet date of 31 December 2016, the balance of cash in hand at bank of Gazonor SAS

amounted to € 2,453,461.

Cash and cash equivalents are available immediately (non-pledged), non-risky and of

negligible volatility.

11. Share capital

As at 31 December 2016, the share capital of the Company amounted to € 5,065,174 and was

divided into 5,065,174 ordinary shares of par value € 1 each and fully paid.

During the last financial periods, changes in the share capital of the Company were as

follows:

Number

Nominal

Value Amount

€ €

As at 1 July 2015 3,226,620 1 3,226,620

As at 31 December 2015 3,226,620 1 3,226,620

Shares issued through IPO in June 2016 1,388,889 1 1,388,889

Shares issued following conversion of debentures into

ordinary shares

449,665 1 449,665

As at 30 June 2016 5,065,174 1 5,065,174

As at 31 December 2016 5,065,174 1 5,065,174

12. Free shares plans for the employees

The Company’s general meeting of 23 March 2016 authorised the Board of Directors to

proceed with the award of free shares to employees and corporate officers up to 5% of the

Company’s share capital. This operation will be realised by an increase in share capital.

On 30 June 2016, the Board of Directors authorised and approved the free share attribution

plan to the executives and employees as well as agreeing the terms, allocation and the

conditions of the plan in favour of the employees and officers of the Company. The total

number of shares which may be issued under such plan is of 85,601 free shares, representing

1.64% of the share capital of the Company.

These free shares will actually be issued to the eligible beneficiaries 2 years after the date of

their grant, provide the beneficiaries are still holding their position with the Company at that

time, and subject to the other conditions set forth in this free shares plan.

Pursuant to IFRS 2, the benefits granted under this plan are recognized as personnel expenses

in return for an increase in shareholders' equity, with the rights being immediately vested at

the grant date, the plan being settled shareholders' equity.

27

For this free share plan for all employees and managers, the unit value is based on the share

price on the grant date and takes into account the evolution of the beneficiary workforce. The

expense recognized is allocated over the vesting period of the current rights from the date of

the board that approved the plan and the likelihood of being present. The grant date

corresponds to the date of the board of directors which decided on the allocation of this plan.

The following table illustrates the number, fair value and changes of these free shares during

the first half of the financial year ended 31 December 2016:

Distribution

date

Excercise

Period

Minimum

holding

period

Shares

issued

Fair value at

date of

distribution

Shares issued as

at 31 December

2015

30 June 2016 2 years 2 years 85,602 21 € n/a

13. Long-term borrowings

The Non-current financial liabilities are presented below:

31 December

2016

31 December

2015

30 June

2016

€ €

Non-current financial debt 3,268,139 7,938,000 3,053,778

Convertible loan notes 9,212,783 -

Total non-current financial liabilities 3,268,139 17,150,783 3,053,778

Non-current financial debt corresponds to the loan granted by European Gas

Limited (“EGLUK”) with a maturity date of 12 December 2019 with an interest rate of zero

percent pursuant to the loan agreement with EGLUK as at 12 December 2014. This interest-

free loan with a nominal value of € 4,970,139 as at December 31, 2016 (€ 13,885,230 at 31

December 2015) was valued by discounting future payments at a market rate of 15% until

maturity.

As part of the restructuring of the Group in 2015, EGLUK and the Company, pursuant to a

Reorganization and Cooperation Agreement dated 25 June 2015, that such loan granted by

EGLUK would be phased out over a period of five years in consideration for the Company's

undertaking to re-open a buy-back transaction for the shareholders of EGLUK and the

Company’s undertaking to fund the repayment of bonds issued by EGLUK and valued at

€ 4,668,750 as of May 31, 2016. This sum was settled on June 15, 2016.

Given the complexity to implement a new share buyback or exchange operation allowing

EGLUK shareholders to become shareholders of the Company, EGLUK and the Company

agreed to extend the duration of the EGLUK loan for the year 2017.

28

The impact of the various transactions on the loan for the six-month period ended

31 December 2016 is detailed below:

Liabilities Equity Income

Statement

Cash

flow

€ € € €

EGL UK loan

(fair value) - 30

June 2016

3,053,778 - -

Cash movements

between June

2016 and

December 2016(1)

(9,639) - - (9,639)

Repayment of the

shareholder loan

of EGLUK as at

31 December

2016(2)

(5,000) (5,000) - -

Forgiveness of

debt for the period

up to 31

December 2016(3)

229,000 - 229,000 -

Fair value

adjustment at

31December

2016(4)

3,268,139 (5,000) 229,000 (9,639)

(1) Cash flows between June 2016 and December 2016 amounting to € 9,639 correspond to the

consideration for payments made by FDE in respect of EGL UK commitments.

(2) The amount of € (5,000) corresponds to the impact on the fair value adjustment of the movements

between June 2016 and December 2016 mentioned above.

(3) The amount of € 229,000 corresponds to the effect of the unwinding of the debt with respect to EGL

UK for the year ended December 31, 2016.

14. Income taxes

31 December

2016

31 December

2015

30 June

2016

€ € €

Income tax 174,080

Deferred tax (76,000) 934,000 2,666,622

Total tax 98,080 934,000 2,666,622

Total theoretical tax 33.33% 33.33% 33.33%

Deferred taxes

The deferred taxes break-down is as follows:

29

31

December

2016

31

December

2015

30

June

2016

€ € €

Deferred tax assets on losses carried forward 345,000 154,312 984,000

Deferred tax losses on temporary adjustments - 14,362 3,092

Deferred tax losses on fair value adjustments

of the loan with EGLUK (Note 19) 76,000 (1,981,922)

-

(642,092)

-

Net Balance Sheet impact 421,000 (1,813,248) 345,000

15. Accounts payable and other current liabilities

Accounts payable and other current liabilities are comprised of the following:

31 December

2016

31 December

2015

30 June

2016

€ € €

Accounts payable 3,350,802 1,737,617 4,605,268

Social liabilities 518,486 172,863 826,490

Tax liabilities 169,265 -

Other liabilities - 1,000 150,000

Total accounts payable and other current

liabilities

4,038,553

1,911,480

5,581,758

Accounts payable and other current liabilities are due within one year as at 31 December

2016.

16. Related parties transactions

The Company has been engaged in a number of transactions with related parties for the

financial half year ended 31 December 2016 as follows:

- Interest free loan agreement with EGLUK, for a nominal value of € 4,970,139 at 31

December 2016, with an initial maturity of five years to 12 December 2019. A second

amendment in respect to the « Accord de Réorganisation et de Coopération » has been

concluded and signed by both parties on 18 December 2016, whereby EGLUK and the

Company has agreed to extend the loan till 30 June 2017.

- In the meeting of 23 March 2016, the Board of Directors of the Company had decided

to award to the Chairman and CEO an exceptional pre-tax remuneration of € 250,000

in case of a successful IPO of the company and an additional pre-tax amount of €

250,000 in the event of funds raised in excess of € 20,000,000. An accrual amounting

to € 600,000 including the charges related to the remuneration were recorded at the

end of June 2016 in the consolidated financial statements of the Company for the

benefit of the companies Nebula Resources Limited and Next Gen NRJ Limited. An

amount of € 300,000 has been paid and an equal amount has been recorded as payable

in the first half year 31 December 2016.

30

- A contract for services between the company LFDE International (formerly Transcor

Astra Luxembourg) and the company NextGen NRJ Limited, a company domiciled in

the United Kingdom and a personal holding of the Chief Executive Officer of the

Company, based on the promoting the activities, notably to the European Union

institutions and seeking potential acquisitions and sources of financing. In

consideration for these services, LFDE International pays NextGen NRJ Limited a

monthly fee of € 10,000 excluding taxes since July 1, 2016, representing an expense of

€ 60,000 over the first half of the financial year 31 December 2016.

A contract for provision of services between the company LFDE International and the

company Karlin Limited, a company domiciled in the United Kingdom and controlled

by the Financial Director of the Company for the provision of consultancy services

primarily in seeking potential acquisition opportunities on behalf of the Company. In

return for its services, LFDE International pays Karlin an annual fee of € 50,000

excluding taxes, hence expenses of € 25,000 were recorded for the first half of the

financial year 31 December 2016.

The members of the boards of directors of the Company and EGLUK are also related parties.

Transactions with these related parties primarily relate to the remuneration and benefits

granted to the CEO and other executives of EGLUK, no further agreement has been

concluded during the first half of the financial year ending 30 June 2017.

17. Contractual obligations

Purchase commitments

The purchase obligations are obligations to purchase goods or services, including the

acquisition of fixed assets, on the basis of contractual terms negotiated with the suppliers of

the Group. During the first half of the financial year ended 31 December 2016, the Group

implemented several purchase commitments and other contractual obligations related to the

Lachambre drilling project and the electricity project at Gazonor with suppliers. The first well

at Lachambre is expected to cost a maximum of € 4.6 million. At Gazonor the purchase of

equipment and site preparation for the electricity project is expected to cost the Company a

maximum of € 6.8 million.

Financial commitment on the exploration licences

The table below describes the financial commitments made by the Group in respect of two

key licenses currently operated by the company at 31 December 2016:

Exclusive licence

research (PER)

Initial financial

commitment

Realised

investments

Residual

commitment

€ € €

Bleue Lorraine 7,700,000 29,738,630 Nil

Bleue Lorraine Sud 7,250,000 299,103 6,950,897

Each exploration license awarded to the Group includes financial commitments in terms of

exploration expenditures to be incurred during the term of the license. However, in practice,

the Group may decide to spend far more in excess of its original financial commitments. On

31

the other hand, the Group may decide to delay these expenses depending on the circumstances

and exploration programs. Furthermore, it is important to clarify that the expenses recorded

on the PER of Bleue Lorraine also cover studies on well architectures, the quality and

resistance of equipment and drilling tools and the characteristics of the Lorraine coals that can

be useful for the PER of Bleue Lorraine Sud.

18. Financial instruments and risk management

The main financial assets and liabilities of the group include cash, other receivables, payables

and convertible debenture loan notes.

Fair value of financial assets and liabilities

The financial assets and liabilities can be ranked according to the following three levels of fair

value:

Level 1, prices (non-adjusted) quoted in active markets for identical assets and liabilities, for

which the company can obtain the market value at a specific date;

Level 2, other data than those regarding the quoted prices mentioned in Level 1, observable

directly or indirectly in the market;

Level 3, data related to assets or liabilities that are not observable in the market.

The fair value of financial assets and liabilities is determined as follows:

The fair value of accounts receivable, payables as well as the other current miscellaneous

receivables and payables, is deemed to be the same as their carrying value in the balance

sheet, considering their very short-payment terms;

The fair value of the non-current financial debts that concerns a loan from the Company,

EGLUK (Level 2 in the hierarchy of the fair value as per IFRS 13) is estimated by

discounting the future payments to be made at the balance sheet date, using the market

rate of 15%.

The fair value of the bonus shares is determined in accordance with IFRS 2, taking into

account the market price at the date of issue to the beneficiaries.

Derivative financial instruments are initially recognized at their fair value at the date of the

conclusion of the derivative contract and then, they are reassessed to their fair value at each

year-end closing.

There were no significant changes in financial instruments and risk management in the first

half of the financial year 31 December 2017.

The table below shows the maturity of the Group's financial assets and liabilities as at

December 31, 2016, June 30, 2016 and December 31, 2015:

32

As at 31 December 2015 Up to 1

Year

From 1 to 5

Years

More than 5

years Total

Trade payables (1,723,168) (14,449) - (1,737,617)

Other current liabilities (173,863) - (173,863)

Financial debt EGLUK - (13,885,230) - (13,885,230)

Convertible bonds - (9,212,783) - (9,212,783)

Other receivables 197,363 - 197,363

Net amount (1,699,668) (23,112,462) - (24,812,130)

As at 30 June 2016

Up to 1

Year

From 1 to 5

Years

More than 5

years

Total

Trade payables (4,605,268) - - (4,605,268)

Other current liabilities (976,490) - - (976,490)

Financial debt EGLUK - (4,979,778) - (4,979,778)

Convertible bonds 1,420,342 - -

1,420,342

Other receivables (4,161,416) (4,979,778) (9,141,194)

As at 31 December 2016 Up to 1

Year

From 1 to 5

Years

More than 5

years Total

Trade payables (3,350,802) - - (3,350,802)

Other current liabilities (687,751) - - (687,751)

Financial debt EGLUK - (4,970,139) - (4,970,139)

Convertible bonds 1,505,234 - - 1,505,234

Other receivables (2,533,319) (4,970,139) - (7,503,458)

19. Provisions for liabilities and charges

Development of the provisions 31 December

2016

31 December

2015

30

June 2016

€ € €

Provision for site refurbishments /restoration 3,855,303 474,311 474,311

Provision for pensions 17,086 43,087 9,275

Total 3,872,389 517,398 483,586

Provisions for site refurbishments/ restorations can be summarised as follows:

- an amount of € 474,311 recognized by the Company, which represents the costs of

abandoning the wells and the costs of rehabilitating the Tritteling site in the event that

the exploration activity ceases. The amount of this reclamation provision has not been

subject to a discount calculation as of December 31, 2016, as the impact of such a

discount has been considered insignificant.

33

- an amount of € 2,526,034 recorded by the subsidiary Gazonor SAS in previous years

for the shutdown and closing of the site, dismantling and final treatment of the

pipelines, for the license and concession zones of Gazonor. The consideration for this

provision has been recognized as intangible assets and is fully amortized. No provision

is made for this provision.

- a provision of € 854,957 related to Gazonor's operating activities is also recorded to

cover multi-year maintenance costs.

Provisions for restoration are capitalized and included in the value of the underlying fixed

assets, namely exploration assets recognized as fixed assets.

The actuarial assumptions used to estimate the actuarial liability for provisions for pensions

and retirement benefits as of December 31, 2016 are as follows:

i) Pension age: 65 years

ii) Salary growth YoY: 2%

iii) Discount rate: 1.5%

iv) Average staff turnover: Company specific rate: 5%

v) Surivival rate in accordance to INSEE table

20. Segmented financial information

Segmented financial information is presented in accordance with the same principles as

internal reporting, based on exploration, production and EBITDA indicators by operating

segment. These operating segments are:

- Lorraine (exploration of gas reserves), the costs of which are broken down according

to the permits and geographical areas presented in note 5 of this appendix to the

consolidated half-yearly financial statements.

- Nord Pas de Calais (gas production), which represents the exploitation and marketing

of mine gas by Gazonor SAS, whose revenues and costs are allocated according to

permits and geographical areas.

The following tables present, by geographical area, information on turnover and information

on the main exploration assets and production concessions held by the Group as at 31

December 2016. Lorraine Nord Pas de Calais

As at 31 December 2016

Bleue

Lorraine

Bleue

Lorraine

Sud

Poissonnière

Désirée

Total

€ € € € €

Revenues

Gas sales - - 1,859,671 - 1,859,671

Balance

Sheet