Kuwait Insurance Company S.A.K.P Kuwait Annual … · Kuwait Insurance Company S.A.K.P Kuwait...

27

Kuwait Insurance Company S.A.K.P Kuwait Annual Financial Statements and Independent Auditors' Report 31 December 2014

Transcript of Kuwait Insurance Company S.A.K.P Kuwait Annual … · Kuwait Insurance Company S.A.K.P Kuwait...

Kuwait Insurance Company S.A.K.P

Kuwait

Annual Financial Statements and

Independent Auditors' Report

31 December 2014

Kuwait Insurance Company S.A.K.P

Kuwait

Annual Financial Statements and

Independent Auditors' Report

31 December 2014

C o n t e n t s

Page

Independent Auditors' Report 1 - 2

Statement of Financial Position 3

Statement of Income 4

Statement of Comprehensive Income 5

Statement of Changes in Equity 6

Statement of Cash Flows 7

Notes to the Financial Statements 8 – 25

Deloitte & Touche

Al-Wazzan & Co.

Ahmed Al-Jaber Street, Sharq

Dar Al-Awadi Complex, Floors 7 & 9

P.O. Box 20174 Safat 13062 or

P.O. Box 23049 Safat 13091

Kuwait

Tel : + 965 22408844, 22438060

Fax: + 965 22408855, 22452080

www.deloitte.com

Kuwait Insurance Company S.A.K.P

Kuwait

Independent Auditors’ Report to the Shareholders

Report on the financial statements

We have audited the accompanying financial statements of Kuwait Insurance Company S.A.K.P (“the Company”),

which comprise the statement of financial position as at 31 December 2014, and the statements of income,

comprehensive income, changes in equity and cash flows for the year then ended, and a summary of significant

accounting policies and other explanatory information.

Management’s Responsibility for the Financial Statements

Management is responsible for the preparation and fair presentation of these financial statements in accordance

with International Financial Reporting Standards, and for such internal control as management determines is

necessary to enable the preparation of the financial statements that are free from material misstatements, whether

due to fraud or error.

Auditors’ Responsibility

Our responsibility is to express an opinion on these financial statements based on our audit. We conducted our

audit in accordance with International Standards on Auditing. Those Standards require that we comply with ethical

requirements and plan and perform the audit to obtain reasonable assurance whether the financial statements are

free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the

financial statements. The procedures selected depend on the auditors’ judgment, including the assessment of the

risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk

assessments, the auditors consider internal control relevant to the entity's preparation and fair presentation of the

financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the

purpose of expressing an opinion on the effectiveness of the entity's internal control. An audit also includes

evaluating the appropriateness of accounting policies used and the reasonableness of accounting estimates made

by management, as well as evaluating the overall presentation of the financial statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit

opinion.

Opinion

In our opinion, the financial statements present fairly, in all material respects, the financial position of the Company

as at 31 December 2014, and of its financial performance and cash flows for the year then ended in accordance

with International Financial Reporting Standards.

2

Kuwait Insurance Company S.A.K.P

Kuwait

Independent Auditors’ Report to the Shareholders (Continued)

Report on other Legal and Regulatory Requirements

Furthermore, in our opinion, proper books of account have been kept by the Company and the financial statements,

together with the contents of the report of the Board of Directors relating to these financial statements, are in

accordance therewith. We further report that we obtained all the information and explanations that we required for

the purpose of our audit and that the financial statements incorporate all information that is required by the

Companies Law No 25 of 2012; as amended, and its executive regulations and of Law No. 24 of 1961, as amended,

concerning insurance companies and insurance agents and its related regulations; and by the Company's

Memorandum of Incorporation and Articles of Association; as amended, that an inventory was duly carried out and

that, to the best of our knowledge and belief, no material violation of Companies Law No 25 of 2012, as amended,

and its executive regulations or of Law No. 24 of 1961, as amended or of the Memorandum of Incorporation and

Articles of Association, as amended, have occurred during the financial year ended 31 December 2014 that might

have had a material effect on the business of the Company or on its financial position.

Bader A. Al-Wazzan

Licence No. 62A

Deloitte & Touche

Al-Wazzan & Co.

Rabea Saad Al-Muhanna

Licence No. 152A

Horwath Al-Muhanna & Co.

Kuwait, 10 February 2015

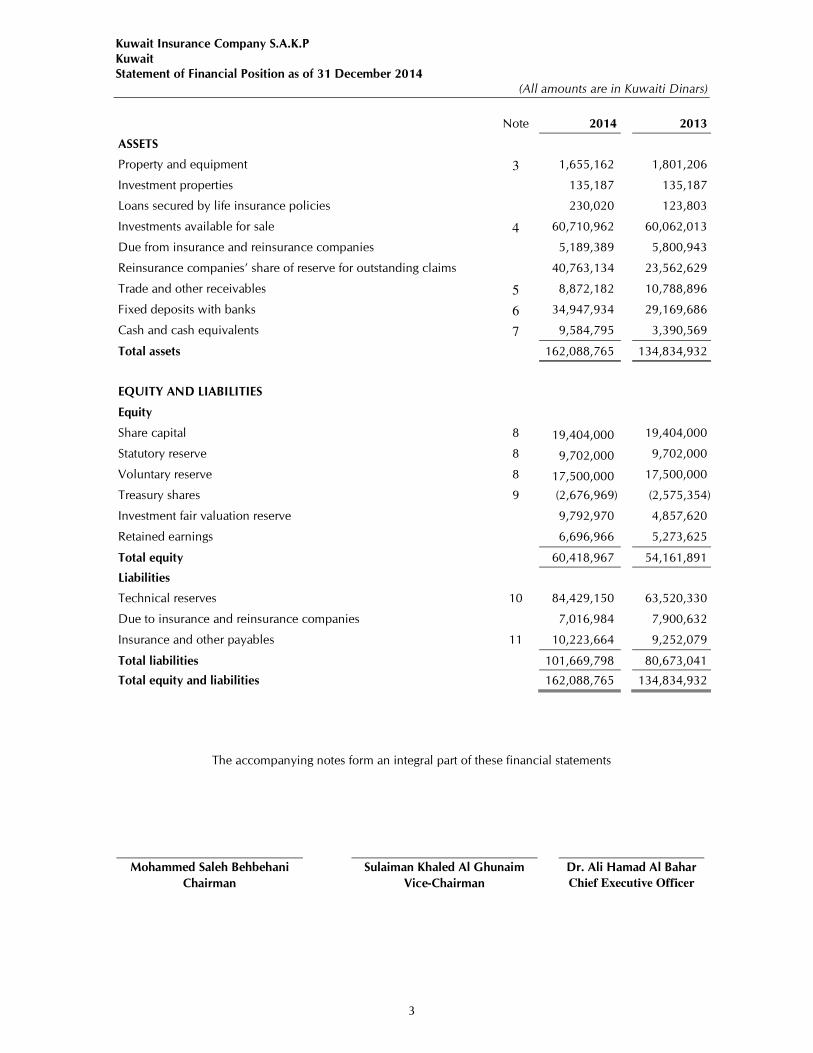

Kuwait Insurance Company S.A.K.P

Kuwait

Statement of Financial Position as of 31 December 2014

(All amounts are in Kuwaiti Dinars)

3

Note 2014 2013

ASSETS

Property and equipment 3 1,655,162 1,801,206

Investment properties 135,187 135,187

Loans secured by life insurance policies 230,020 123,803

Investments available for sale 4 60,710,962 60,062,013

Due from insurance and reinsurance companies 5,189,389 5,800,943

Reinsurance companies’ share of reserve for outstanding claims 40,763,134 23,562,629

Trade and other receivables 5 8,872,182 10,788,896

Fixed deposits with banks 6 34,947,934 29,169,686

Cash and cash equivalents 7 9,584,795 3,390,569

Total assets 162,088,765 134,834,932

EQUITY AND LIABILITIES

Equity

Share capital 8 19,404,000 19,404,000

Statutory reserve 8 9,702,000 9,702,000

Voluntary reserve 8 17,500,000 17,500,000

Treasury shares 9 (2,676,969) (2,575,354)

Investment fair valuation reserve 9,792,970 4,857,620

Retained earnings 6,696,966 5,273,625

Total equity 60,418,967 54,161,891

Liabilities

Technical reserves 10 84,429,150 63,520,330

Due to insurance and reinsurance companies 7,016,984 7,900,632

Insurance and other payables 11 10,223,664 9,252,079

Total liabilities 101,669,798 80,673,041

Total equity and liabilities 162,088,765 134,834,932

The accompanying notes form an integral part of these financial statements

Mohammed Saleh Behbehani Sulaiman Khaled Al Ghunaim Dr. Ali Hamad Al Bahar

Chairman Vice-Chairman Chief Executive Officer

Kuwait Insurance Company S.A.K.P

Kuwait

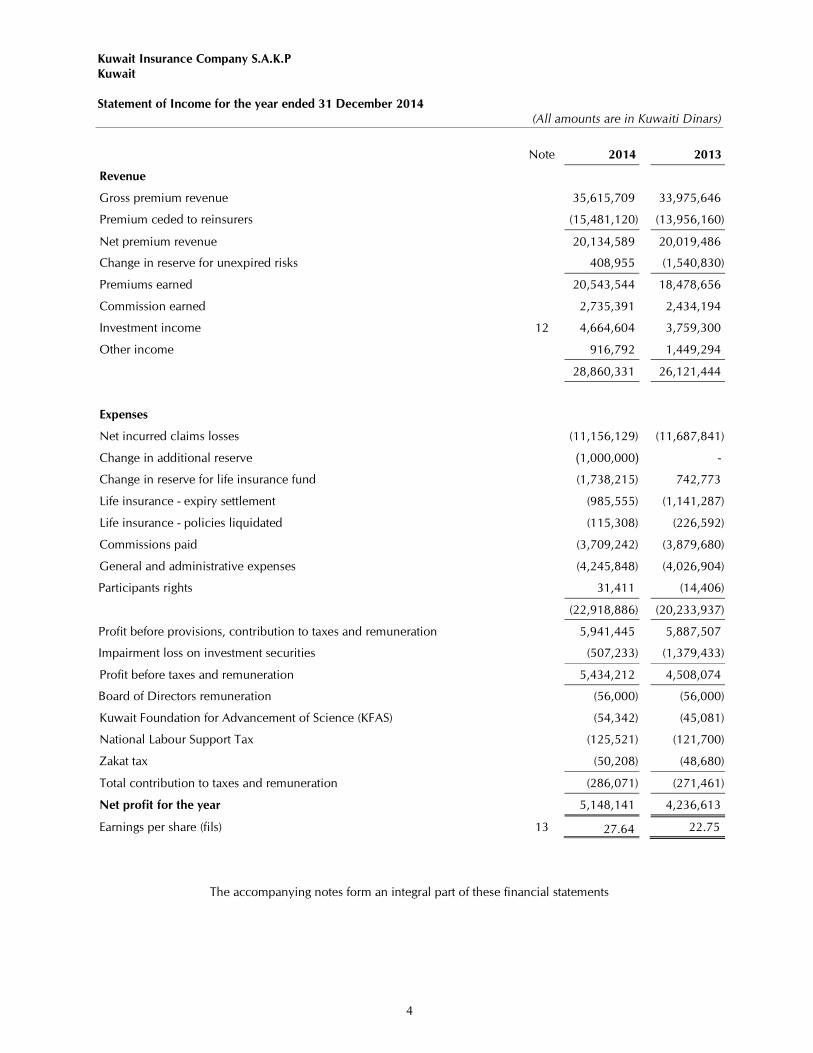

Statement of Income for the year ended 31 December 2014

(All amounts are in Kuwaiti Dinars)

4

Note 2014 2013

Revenue

Gross premium revenue 35,615,709 33,975,646

Premium ceded to reinsurers (15,481,120) (13,956,160)

Net premium revenue 20,134,589 20,019,486

Change in reserve for unexpired risks 408,955 (1,540,830)

Premiums earned 20,543,544 18,478,656

Commission earned 2,735,391 2,434,194

Investment income 12 4,664,604 3,759,300

Other income 916,792 1,449,294

28,860,331 26,121,444

Expenses

Net incurred claims losses (11,156,129) (11,687,841)

Change in additional reserve (1,000,000) -

Change in reserve for life insurance fund (1,738,215) 742,773

Life insurance - expiry settlement (985,555) (1,141,287)

Life insurance - policies liquidated (115,308) (226,592)

Commissions paid (3,709,242) (3,879,680)

General and administrative expenses (4,245,848) (4,026,904)

Participants rights 31,411 (14,406)

(22,918,886) (20,233,937)

Profit before provisions, contribution to taxes and remuneration 5,941,445 5,887,507

Impairment loss on investment securities (507,233) (1,379,433)

Profit before taxes and remuneration 5,434,212 4,508,074

Board of Directors remuneration (56,000) (56,000)

Kuwait Foundation for Advancement of Science (KFAS) (54,342) (45,081)

National Labour Support Tax (125,521) (121,700)

Zakat tax (50,208) (48,680)

Total contribution to taxes and remuneration (286,071) (271,461)

Net profit for the year 5,148,141 4,236,613

Earnings per share (fils) 13 27.64 22.75

The accompanying notes form an integral part of these financial statements

Kuwait Insurance Company S.A.K.P

Kuwait

Statement of Comprehensive Income for the year ended 31 December 2014

(All amounts are in Kuwaiti Dinars)

5

2014 2013

Net profit for the year 5,148,141 4,236,613

Other comprehensive income items:

Items that may be reclassified subsequently to statement of income

Changes in fair value of investments available for Sale 5,956,142 7,055,581

Transferred to statement of income on sale of investments available for sale (1,528,025) (747,815)

Impairment of available for sale investments 507,233 1,379,433

Other comprehensive income for the year 4,935,350 7,687,199

Total comprehensive income for the year 10,083,491 11,923,812

The accompanying notes are an integral part of these financial statements

Kuwait Insurance Company S.A.K.P

Kuwait

Statement of Changes in Shareholders’ Equity for the year ended 31 December 2014

(All amounts are in Kuwaiti Dinars)

6

Share

Capital

Statutory

reserve

Voluntary

Reserve

Treasury

Shares

Change in

fair value

reserve

Retained

Earnings s

Total

Balance as at 1 January 2014 19,404,000 9,702,000 17,500,000 (2,575,354) 4,857,620 5,273,625 54,161,891

Total comprehensive income for the year - - - - 4,935,350 5,148,141 10,083,491

Treasury shares purchased - - - (101,615) - - (101,615)

Dividend paid for 2013 - - - - - (3,724,800) (3,724,800)

Balance as at 31 December 2014 19,404,000 9,702,000 17,500,000 (2,676,969) 9,792,970 6,696,966 60,418,967

Balance as at 1 January 2013 19,404,000 9,702,000 17,500,000 (2,345,235) (2,829,579) 4,761,812 46,192,998

Total comprehensive income for the year - - - - 7,687,199 4,236,613 11,923,812

Treasury shares purchased - - - (230,119) - - (230,119)

Dividend paid for 2012 - - - - - (3,724,800) (3,724,800)

Balance as at 31 December 2013 19,404,000 9,702,000 17,500,000 (2,575,354) 4,857,620 5,273,625 54,161,891

The accompanying notes form an integral part of these financial statements

Kuwait Insurance Company S.A.K.P

Kuwait

Statement of Cash Flows for the year ended 31 December 2014

(All amounts are in Kuwaiti Dinars)

7

Note 2014 2013

Cash flows from operating activities

Net profit for the year 5,148,141 4,236,613

Adjustments for:

Investment income 12 (4,664,604) (3,759,300)

Depreciation 182,579 159,206

Impairment loss on investment securities 507,233 1,379,433

Staff terminal benefits 245,485 155,791

Finance expenses 69 25,020

Operating profit before working capital changes 1,418,903 2,196,763

Decrease in due from insurance and reinsurance companies 611,554 1,116,918

Decrease in trade and other receivables 1,916,714 3,357,209

Increase in technical reserves 3,708,316 2,929,493

Decrease in due to insurance and reinsurance companies (883,648) (4,864,637)

Increase in Insurance and other payables 987,577 1,503,402

Cash from operating activities 7,759,416 6,239,148

Payment of staff terminal benefits (20,857) (56,791)

Payment of KFAS (45,081) (41,469)

Payment of National Labour Support Tax (121,700) (98,846)

Payment of Zakat tax (48,680) (39,538)

Payment of Board of Directors remuneration (56,000) (56,000)

Net cash from operating activities 7,467,098 5,946,504

Cash flows from investing activities

Purchase of property and equipment (36,535) (13,162)

Net movement of loans secured by life insurance policies (106,217) 12,346

Purchase of investments available for sale (1,468,872) (256,416)

Proceeds from sale of investments available for sale 6,787,023 2,313,479

Net movement in fixed deposits with banks (5,778,248) (6,047,491)

Dividend received 2,523,505 2,167,972

Interest received 602,116 453,428

Net cash generated from/(used in) investing activities 2,522,772 (1,369,844)

Cash flows from financing activities

Purchase of treasury shares (101,615) (230,119)

Payment of finance expenses (69) (25,021)

Dividends paid to shareholders (3,693,960) (3,729,449)

Net cash used in financing activities (3,795,644) (3,984,589)

Net increase in cash and cash equivalents 6,194,226 592,071

Cash and cash equivalents at beginning of the year 3,390,569 2,798,498

Cash and cash equivalents at end of the year 7 9,584,795 3,390,569

The accompanying notes form an integral part of these financial statements

Kuwait Insurance Company S.A.K.P

Kuwait

Notes to the Financial Statements for the year ended 31 December 2014 (All amounts are in Kuwaiti Dinars unless otherwise stated)

8

1. Incorporation and objectives

Kuwait Insurance Company S.A.K.P, (the Company) is a Kuwaiti Public Shareholding Company established in

Kuwait in 1960 by Amiri Decree No. 7 of 1960, and registered with the Ministry of Commerce in accordance

with the Insurance Companies and Agent Law No. 24 of 1961 under Insurance license No. 1.

The objects of the Company are to underwrite life and non-life insurance risks such as fire, general accidents,

marine and aviation, lend funds against life insurance policies; and to invest in permitted securities and real

estate properties. The Company also engages in underwriting all types of risks under the Takaful insurance law.

The registered office of the Company is located at Kuwait Insurance Building, Abdullah Al-Salem Street, Kuwait.

P.O. Box 769 Safat 13008, Kuwait. The Company has 13 branches in the State of Kuwait.

These financial statements have been approved for issue by the Board of Directors on 10 February 2015, and

are subject to shareholders’ approval at the annual general meeting.

The extra-ordinary general assembly meeting was held on 7 April 2014 to approve the amendments to the

company’s Memorandum of Incorporation and Articles of Association to be in compliance with companies

law, as amended, and CMA’s related resolutions.

These amendments have been authenticated in the commercial register on 23 June 2014.

2. Basis of preparation and significant accounting policies

2.1 Basis of preparation

These financial statements have been prepared in accordance with the International Financial Reporting

Standards (IFRS) issued by International Accounting Standards Board (IASB). These financial statements are

prepared under the historical cost basis of measurement as modified by the revaluation of financial instruments

classified as “available for sale”. The financial statements have been presented in Kuwaiti Dinar.

The preparation of financial statements in conformity with International Financial Reporting Standards requires

management to make estimates and assumptions that may affect amounts reported in these financial statements,

as actual results could differ from those estimates. It also requires management to exercise its judgment in the

process of applying the Company’s accounting policies. The areas where estimates and assumptions are

significant to the financial statements, or areas involving a higher degree of judgment, are disclosed in Note 20.

New and revised standards

New and revised IFRSs issued and effective

In the current year, the Company has applied a number of new and revised IFRSs that are issued and effective

for accounting periods that begin on or after 1 January 2014.

Amendments to IFRS 10, IFRS 12 and IAS 27 Investment Entities

The Company has applied the amendments to IFRS 10, IFRS 12 and IAS 27 Investment Entities for the first time

in the current year. The amendments to IFRS 10 define an investment entity and require a reporting entity that

meets the definition of an investment entity not to consolidate its subsidiaries but instead to measure its

subsidiaries at fair value through profit or loss in its consolidated and separate financial statements.

Consequential amendments have been made to IFRS 12 and IAS 27 to introduce new disclosure requirements

for investment entities. The application of the amendments has had no impact on the disclosures or the

amounts recognized in the Company’s financial statements.

Amendments to IAS 32 Offsetting Financial Assets and Financial Liabilities

The Company has applied the amendments to IAS 32 Offsetting Financial Assets and Financial Liabilities for

the first time in the current year. The amendments to IAS 32 clarify the requirements relating to the offset of

financial assets and financial liabilities.

The amendments have been applied retrospectively. The Company has assessed whether certain of its financial

assets and financial liabilities qualify for offset based on the criteria set out in the amendments and concluded

that the application of the amendments has had no impact on the amounts recognised in the Company’s

financial statements.

Kuwait Insurance Company S.A.K.P

Kuwait

Notes to the Financial Statements for the year ended 31 December 2014 (All amounts are in Kuwaiti Dinars unless otherwise stated)

9

Amendments to IAS 36 Recoverable Amount Disclosures for Non-Financial Assets

The Company has applied the amendments to IAS 36 Recoverable Amount Disclosures for Non-Financial

Assets for the first time in the current year. The amendments to IAS 36 remove the requirement to disclose the

recoverable amount of a cash-generating unit (CGU) to which goodwill or other intangible assets with

indefinite useful lives had been allocated when there has been no impairment or reversal of impairment of the

related CGU.

Furthermore, the amendments introduce additional disclosure requirements applicable to when the

recoverable amount of an asset or a CGU is measured at fair value less costs of disposal.

The application of these amendments has had no material impact on the disclosures in the Company’s financial

statements.

New and revised IFRSs in issue but not yet effective

The Company has not applied the followings new and revised IFRS that have been issued and not yet effective

For annual periods beginning on or after 1 July 2014

Amendments to IAS 19 Defined Benefit Plans: Employee Contributions

The Annual Improvements to IFRSs 2010-2012 Cycle:

• IFRS 2 Share-based Payment

• IFRS 3 Business Combinations

• IFRS 8 Operating Segments

• IAS 16 Property, Plant and Equipment and IAS 38 Intangible Assets

• IAS 24 Related Party Disclosures

The Annual Improvements to IFRSs 2011-2013 Cycle:.

• IFRS 3 Business Combinations

• IFRS 13 Fair Value Measurement

• IAS 40 Investment Property

The directors of the Company do not anticipate that the application of these amendments will have

a material impact on the Company’s financial statements.

For annual periods beginning on or after 1 January 2016

Amendments to IFRS 11 Accounting for Acquisitions of Interests in Joint Operations

Amendments to IAS 16 & IAS 38 Clarification of Acceptable Methods of Depreciation & Amortisation

Amendments to IAS 16 and IAS 41 Agriculture: Bearer Plants

The directors of the Company do not anticipate that the application of these amendments will have

a material impact on the Company’s financial statements.

Effective for annual periods beginning on or after 1 January 2017

IFRS 15 Revenue from Contracts with Customers

The directors of the Company anticipate that the application of these IFRS 15 in the future may have a material

impact on amounts reported in respect of the Company’s financial assets and financial liabilities. However, it

is not practicable to provide a reasonable estimate of the effect until the Company undertakes a detailed review.

Effective for annual periods beginning on or after 1 January 2018

IFRS 9 Financial Instruments

The directors of the Company anticipate that the application of IFRS 9 in the future may have a material impact

on amounts reported in respect of the Company’s financial assets and financial liabilities. However, it is not

practicable to provide a reasonable estimate of the effect until the Company undertakes a detailed review.

2.2 Significant Accounting Policies

2.2.1 Financial Instruments

Classification and measurement

The Company classifies financial assets as ‘loans and receivables’ and ‘available for sale’. Financial liabilities

are classified as ‘other than at fair value through profit or loss’.

Kuwait Insurance Company S.A.K.P

Kuwait

Notes to the Financial Statements for the year ended 31 December 2014 (All amounts are in Kuwaiti Dinars unless otherwise stated)

10

All financial instruments are initially recognized at fair value. Transaction costs are included only for those

financial instruments not classified as ‘at fair value through profit or loss’.

Loans and receivables

These are non-derivative financial assets with fixed or determinable payments that are not quoted in an active

market. These are subsequently measured and carried at amortized cost using the effective interest rate, less

any provision for impairment. Loans and receivables include loans secured by life insurance policies, due from

insurance and reinsurance companies, trade and other receivables, fixed deposits, cash and cash equivalents.

Available for sale

These are non-derivative financial assets not included in any of the above classifications and are principally

those intended to be held for an indefinite period of time, which may be sold in response to needs for liquidity,

changes in interest rates or prices. These are subsequently measured and carried at fair value. Any resultant

unrealized gains and losses arising from changes in fair value are recognized in other comprehensive income

and accumulated in change in fair value reserve in equity. When an available for sale asset is disposed off or

is impaired, the related cumulative fair valuation changes earlier reported in other comprehensive income and

accumulated in equity are transferred to the statement of income.

Financial liabilities

Financial liabilities are subsequently measured at amortized cost using the effective interest rate.

Recognition and de-recognition

A financial asset or a financial liability is recognized when the Company becomes a party to the contractual

provisions of the instrument. A financial asset is derecognized when the contractual rights to the cash flows

from the financial asset expire or when the Company has transferred substantially all the risks and rewards of

ownership or when it has neither transferred nor retained substantially all risks and rewards of ownership and

it no longer has control over the asset or portion of the asset. If the Company has retained control, it shall

continue to recognize the financial asset to the extent of its continuing involvement in the financial asset. A

financial liability is derecognized when the obligation specified in the contract is discharged/ cancelled or

expired.

All 'regular way' purchase and sale of financial assets are recognized using trade date accounting. Regular way

purchases or sales are purchases or sales of financial assets that require delivery of assets within the time frame

generally established by regulations or conventions in the market place.

Fair values

Fair value is the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction

between market participants at the measurement date.

Impairment

A financial asset is impaired if its carrying amount is greater than its estimated recoverable amount. An

assessment is made at each date of financial position to determine whether there is objective evidence that a

specified financial asset, or a group of similar financial assets, may be impaired.

In the case of financial assets classified as ‘available for sale’, a significant or prolonged decline in the fair value

of assets below its cost is considered in determining whether the assets are impaired. If any such evidence exists

for available for sale financial assets, the cumulative loss measured as the difference between the acquisition

cost and the current fair value, less any impairment loss on that financial asset previously recognized in the

statement of income, is removed from shareholder’s equity and recognized in the statement of income.

Impairment loss recognized in the statement of income on available for sale financial assets that are equity

instruments are not subsequently reversed through the statement of income.

Kuwait Insurance Company S.A.K.P

Kuwait

Notes to the Financial Statements for the year ended 31 December 2014 (All amounts are in Kuwaiti Dinars unless otherwise stated)

11

A credit risk provision for impairment of loans and receivables is established if there is objective evidence that

the Company will not be able to collect all amounts due. The amount of the provision is the difference between

the carrying amount and the recoverable amount, being the present value of expected future cash flows,

discounted at the original effective rate of interest and the current contractual interest rate, for fixed and floating

rate loans respectively.

2.2.2 Offsetting financial instruments

Financial assets and liabilities are setoff and the net amount reported in the statement of financial position when

there is a legally enforceable right to set off the recognized amounts and there is an intention to settle on a net

basis, or realize the asset or settle the liability simultaneously.

2.2.3 Property and equipment

Property and equipment are stated at cost less accumulated depreciation and accumulated impairment losses.

These are depreciated on a straight line basis over their useful lives as follows:

Buildings 20 years

Equipment, Furniture and fixtures up to 3 years

Land is not depreciated. The carrying amount of property and equipment is reviewed periodically to determine

whether there is any indication of impairment in its carrying value. If any such indication exists, an impairment

loss, is recognised in the statement of income, being the difference between carrying value and the asset’s

recoverable amount. For the purposes of assessing impairment, assets are grouped at the lowest levels for which

there are separately identifiable cash flows.

2.2.4 Investment properties

Investment properties held by the Company are the properties held for capital appreciation or to earn rental

income. Investment properties are measured initially at cost, including transaction costs. Subsequent to initial

recognition, investments properties are carried out at historical cost less accumulated impairment losses.

Freehold land is not depreciated.

Investment properties are derecognized when either they have been disposed of or when the investment

property is permanently withdrawn from use and no future economic benefit is expected from its disposal. The

difference between the net disposal proceeds and the carrying amount of the asset is recognised in the statement

of income in the year of derecognition.

2.2.5 Cash and cash equivalents

Cash and cash equivalents comprise of cash in hand, current account with banks and fixed deposits with banks

with maturities not exceeding three months from acquisition date.

2.2.6 Provisions for liabilities

Provisions are recognized when the Company has a present legal or constructive obligation as a result of past

events; and it is probable that an outflow of resources embodying economic benefits will be required to settle

the obligation, and a reliable estimate of the amount of the obligation can be made.

2.2.7 Employees terminal benefits

Provision is made for amounts payable under Kuwaiti labour law. This liability, which is unfunded, represents

the amount payable to each employee as a result of involuntary termination on the date of statement of financial

position, and approximates the present value of this obligation.

Kuwait Insurance Company S.A.K.P

Kuwait

Notes to the Financial Statements for the year ended 31 December 2014 (All amounts are in Kuwaiti Dinars unless otherwise stated)

12

2.2.8 Insurance payables

Reserve for outstanding claims

Provisions are recognized for reported claims, which are not settled on the date of statement of financial

position based on internal and independent loss assessments, after deduction of expected salvage values and

other recoveries.

Reserve for unexpired risks

General Insurance

This is computed at the rate of 40% of the net retained premiums for the Fire and General Accidents

departments and 25% of the net retained premiums for the Marine and Aviation departments.

Life Insurance

Provisions for life insurance liabilities are recognised based on independent actuarial valuation.

Additional reserves

The Company estimates additional provisions for claims incurred but not reported at the date of statement of

financial position based on historical loss ratios.

2.2.9 Treasury shares

The Company’s holding in its own shares is stated at the acquisition cost. These shares are not entitled to any

cash dividend that the Board of Directors may propose.

2.2.10 Revenue recognition

Premiums are recognized as revenue annually and over the period of the cover. The portion of premiums that

relates to unexpired risks at the date of statement of financial position is reported as reserve for unexpired risks

or as unearned premium.

Dividend income is recognized when the right to receive payment is established and interest on fixed deposits

are recognized on time proportion basis using effective interest rate.

Commission earned is recognized at the time insurance policies are ceded to other insurers.

2.2.11 Contribution to taxes

Contribution to Kuwait Foundation for the Advancement of Sciences (KFAS)

The Company calculates KFAS at 1% of taxable profit for the year, in accordance with the calculation based on

the Foundation’s Board of Directors resolution.

National Labour Support Tax (NLST)

The Company calculates NLST in accordance with Law No 19 of 2000 and the Ministry of Finance Resolution

No. 24 of 2006 at 2.5% of taxable profit for the year.

Zakat

The Company calculates Zakat in accordance with Law No. 46 of 2006 and the Ministry of Finance resolution

No 58 of 2007 at 1% of the taxable profit of the Company.

2.2.12 Foreign currency translation

The Company's functional currency is the Kuwaiti Dinar. Transactions in foreign currencies are converted into

Kuwaiti Dinars at the rates prevailing at the date of the transaction. Monetary assets and liabilities denominated

in foreign currencies outstanding at the date of statement of financial position are converted into Kuwaiti Dinar

at the rates prevailing at the date of statement of financial position. Resulting gains or losses are taken to the

statement of income.

Kuwait Insurance Company S.A.K.P

Kuwait

Notes to the Financial Statements for the year ended 31 December 2014 (All amounts are in Kuwaiti Dinars unless otherwise stated)

13

Non-monetary items carried at fair value that are denominated in foreign currencies are translated at the rates

prevailing on the date when the fair value was determined. Translation difference on non-monetary items

classified as at fair value through statement of income are reported as part of the fair value gain or loss in the

statement of income whereas the translation difference on non-monetary items classified as available for sale

financial assets are included in change in fair value reserve in the statement of comprehensive income.

2.2.13 Segment reporting

A segment is a distinguishable component of the Company that engages in business activities from which it

earns revenues and incurs costs. The operating segments are used by the management of the Company to

allocate resources and assess performance. Operating segments exhibiting similar economic characteristics,

product and services, class of customers where appropriate are aggregated and reported as reportable segments.

3. Property and equipment

Land &

buildings

Furniture &

office

equipment

Total

Cost

As at 1 January 2013 4,319,335 1,693,464 6,012,799

Additions for the year 2013 - 13,162 13,162

Disposals for the year 2013 - (1,670) (1,670)

As at 31 December 2013 4,319,335 1,704,956 6,024,291

Additions for the year 2014 - 36,535 36,535

Disposals for the year 2014 - (1,329) (1,329)

As at 31 December 2014 4,319,335 1,740,162 6,059,497

Accumulated depreciation

As at 1 January 2013 2,372,086 1,693,463 4,065,549

Charge for the year 2013 146,044 11,492 157,536

As at 31 December 2013 2,518,130 1,704,955 4,223,085

Charge for the year 2014 146,044 36,535 182,579

Disposals for the year 2014 - (1,329) (1,329)

As at 31 December 2014 2,664,174 1,740,161 4,404,335

Net book value

As at 31 December 2014 1,655,161 1 1,655,162

As at 31 December 2013 1,801,205 1 1,801,206

Depreciation is included in general and administrative expenses in the statement of income.

4. Investments available for sale

2014 2013

Quoted shares 56,091,486 50,264,900

Unquoted shares 2,955,880 3,658,292

Investment funds 1,663,596 6,138,821

60,710,962 60,062,013

Movements in investments available for sale:-

2014 2013

Opening balance 60,062,013 54,673,409

Additions 1,468,872 256,416

Disposals (6,776,065) (1,923,393)

Changes in fair value 5,956,142 7,055,581

Closing balance 60,710,962 60,062,013

Investments in quoted shares include shares with fair value of KD 5,148,000 as of 31 December 2014

(31 December 2013: KD 9,606,000) are under lien to Ministry of Commerce and Industry, Kuwait to comply

with local insurance regulations.

Kuwait Insurance Company S.A.K.P

Kuwait

Notes to the Financial Statements for the year ended 31 December 2014 (All amounts are in Kuwaiti Dinars unless otherwise stated)

14

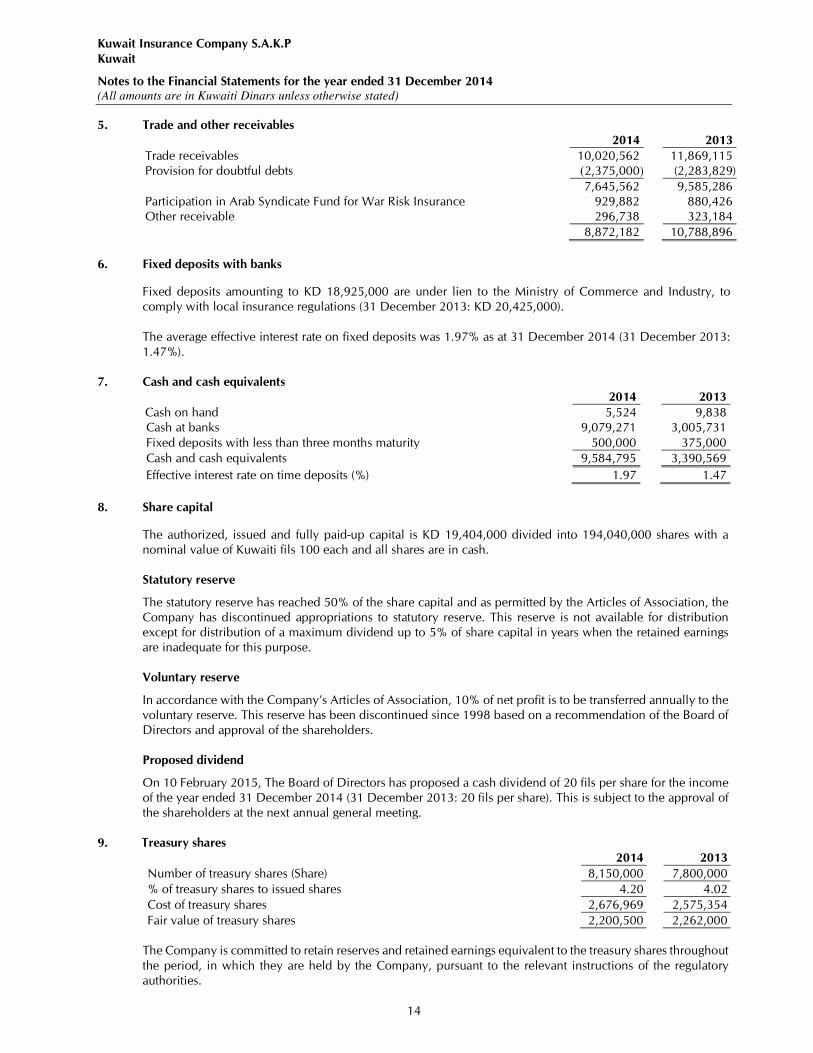

5. Trade and other receivables

2014 2013

Trade receivables 10,020,562 11,869,115

Provision for doubtful debts (2,375,000) (2,283,829)

7,645,562 9,585,286

Participation in Arab Syndicate Fund for War Risk Insurance 929,882 880,426

Other receivable 296,738 323,184

8,872,182 10,788,896

6. Fixed deposits with banks

Fixed deposits amounting to KD 18,925,000 are under lien to the Ministry of Commerce and Industry, to

comply with local insurance regulations (31 December 2013: KD 20,425,000).

The average effective interest rate on fixed deposits was 1.97% as at 31 December 2014 (31 December 2013:

1.47%).

7. Cash and cash equivalents

2014 2013

Cash on hand 5,524 9,838

Cash at banks 9,079,271 3,005,731

Fixed deposits with less than three months maturity 500,000 375,000

Cash and cash equivalents 9,584,795 3,390,569

Effective interest rate on time deposits (%) 1.97 1.47

8. Share capital

The authorized, issued and fully paid-up capital is KD 19,404,000 divided into 194,040,000 shares with a

nominal value of Kuwaiti fils 100 each and all shares are in cash.

Statutory reserve

The statutory reserve has reached 50% of the share capital and as permitted by the Articles of Association, the

Company has discontinued appropriations to statutory reserve. This reserve is not available for distribution

except for distribution of a maximum dividend up to 5% of share capital in years when the retained earnings

are inadequate for this purpose.

Voluntary reserve

In accordance with the Company’s Articles of Association, 10% of net profit is to be transferred annually to the

voluntary reserve. This reserve has been discontinued since 1998 based on a recommendation of the Board of

Directors and approval of the shareholders.

Proposed dividend

On 10 February 2015, The Board of Directors has proposed a cash dividend of 20 fils per share for the income

of the year ended 31 December 2014 (31 December 2013: 20 fils per share). This is subject to the approval of

the shareholders at the next annual general meeting.

9. Treasury shares

2014 2013

Number of treasury shares (Share) 8,150,000 7,800,000

% of treasury shares to issued shares 4.20 4.02

Cost of treasury shares 2,676,969 2,575,354

Fair value of treasury shares 2,200,500 2,262,000

The Company is committed to retain reserves and retained earnings equivalent to the treasury shares throughout

the period, in which they are held by the Company, pursuant to the relevant instructions of the regulatory

authorities.

Kuwait Insurance Company S.A.K.P

Kuwait

Notes to the Financial Statements for the year ended 31 December 2014 (All amounts are in Kuwaiti Dinars unless otherwise stated)

15

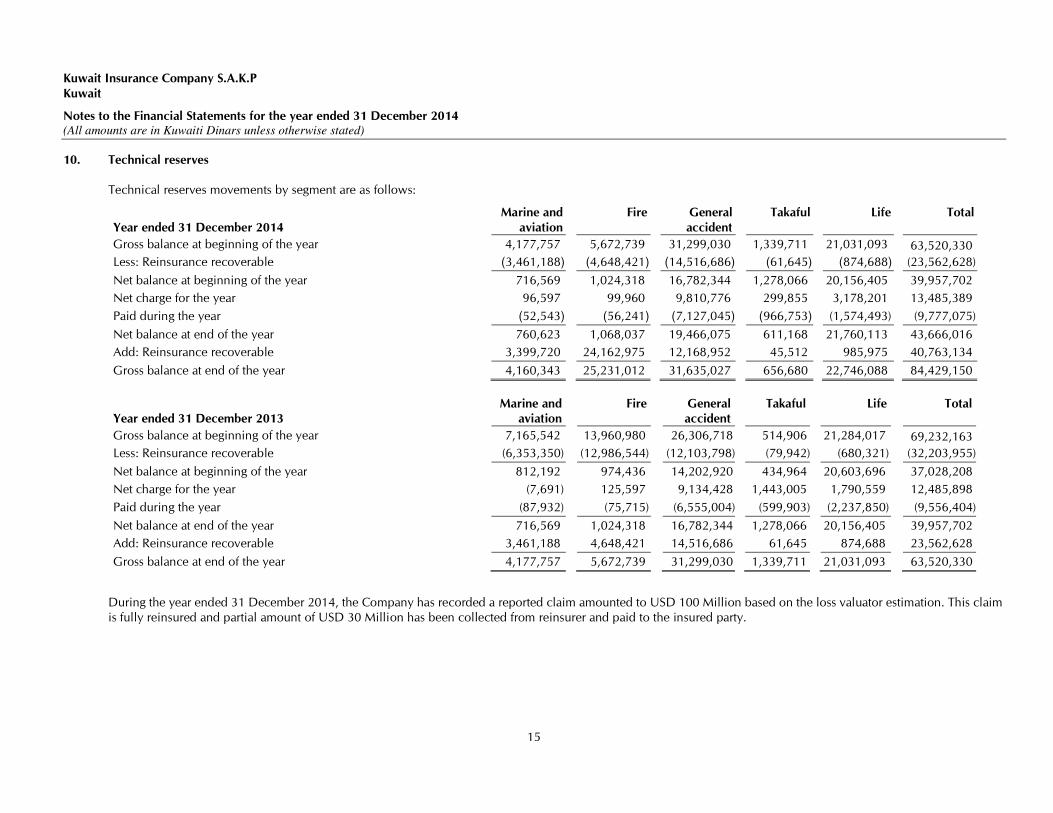

10. Technical reserves

Technical reserves movements by segment are as follows:

Year ended 31 December 2014

Marine and

aviation

Fire General

accident

Takaful Life Total

Gross balance at beginning of the year 4,177,757 5,672,739 31,299,030 1,339,711 21,031,093 63,520,330

Less: Reinsurance recoverable (3,461,188) (4,648,421) (14,516,686) (61,645) (874,688) (23,562,628)

Net balance at beginning of the year 716,569 1,024,318 16,782,344 1,278,066 20,156,405 39,957,702

Net charge for the year 96,597 99,960 9,810,776 299,855 3,178,201 13,485,389

Paid during the year (52,543) (56,241) (7,127,045) (966,753) (1,574,493) (9,777,075)

Net balance at end of the year 760,623 1,068,037 19,466,075 611,168 21,760,113 43,666,016

Add: Reinsurance recoverable 3,399,720 24,162,975 12,168,952 45,512 985,975 40,763,134

Gross balance at end of the year 4,160,343 25,231,012 31,635,027 656,680 22,746,088 84,429,150

Year ended 31 December 2013

Marine and

aviation

Fire General

accident

Takaful Life Total

Gross balance at beginning of the year 7,165,542 13,960,980 26,306,718 514,906 21,284,017 69,232,163

Less: Reinsurance recoverable (6,353,350) (12,986,544) (12,103,798) (79,942) (680,321) (32,203,955)

Net balance at beginning of the year 812,192 974,436 14,202,920 434,964 20,603,696 37,028,208

Net charge for the year (7,691) 125,597 9,134,428 1,443,005 1,790,559 12,485,898

Paid during the year (87,932) (75,715) (6,555,004) (599,903) (2,237,850) (9,556,404)

Net balance at end of the year 716,569 1,024,318 16,782,344 1,278,066 20,156,405 39,957,702

Add: Reinsurance recoverable 3,461,188 4,648,421 14,516,686 61,645 874,688 23,562,628

Gross balance at end of the year 4,177,757 5,672,739 31,299,030 1,339,711 21,031,093 63,520,330

During the year ended 31 December 2014, the Company has recorded a reported claim amounted to USD 100 Million based on the loss valuator estimation. This claim

is fully reinsured and partial amount of USD 30 Million has been collected from reinsurer and paid to the insured party.

Kuwait Insurance Company S.A.K.P

Kuwait

Notes to the Financial Statements for the year ended 31 December 2014 (All amounts are in Kuwaiti Dinars unless otherwise stated)

16

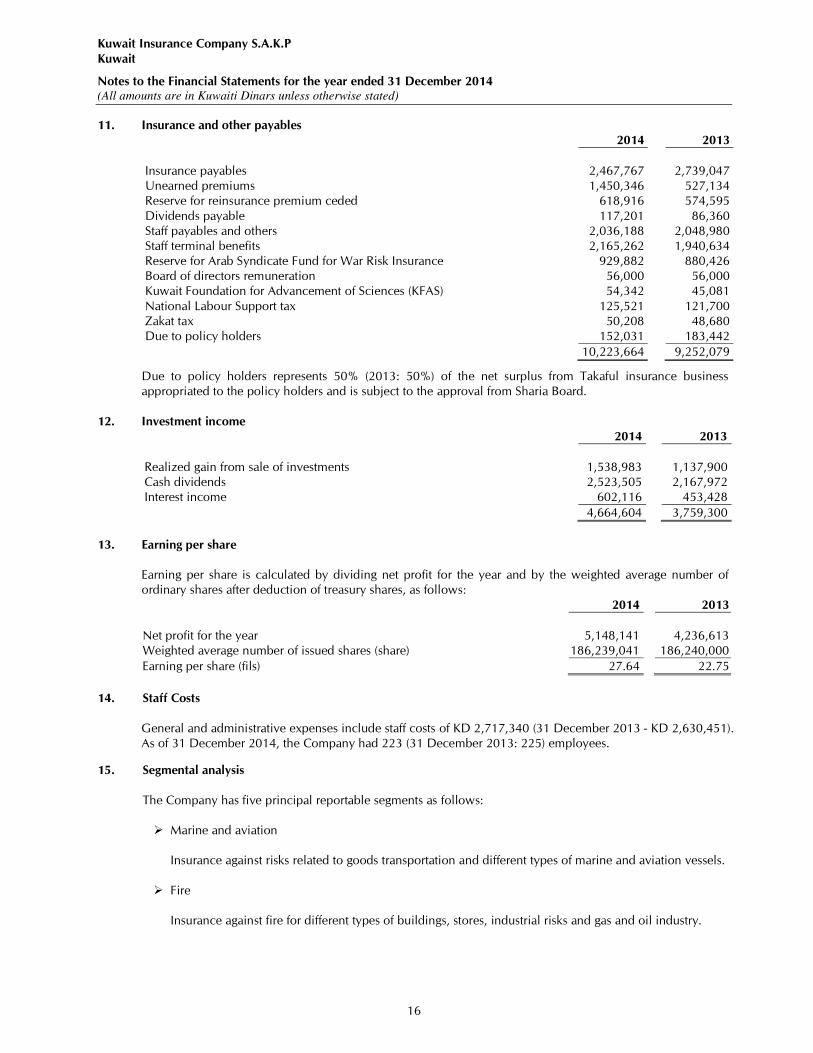

11. Insurance and other payables

2014 2013

Insurance payables 2,467,767 2,739,047

Unearned premiums 1,450,346 527,134

Reserve for reinsurance premium ceded 618,916 574,595

Dividends payable 117,201 86,360

Staff payables and others 2,036,188 2,048,980

Staff terminal benefits 2,165,262 1,940,634

Reserve for Arab Syndicate Fund for War Risk Insurance 929,882 880,426

Board of directors remuneration 56,000 56,000

Kuwait Foundation for Advancement of Sciences (KFAS) 54,342 45,081

National Labour Support tax 125,521 121,700

Zakat tax 50,208 48,680

Due to policy holders 152,031 183,442

10,223,664 9,252,079

Due to policy holders represents 50% (2013: 50%) of the net surplus from Takaful insurance business

appropriated to the policy holders and is subject to the approval from Sharia Board.

12. Investment income

2014 2013

Realized gain from sale of investments 1,538,983 1,137,900

Cash dividends 2,523,505 2,167,972

Interest income 602,116 453,428

4,664,604 3,759,300

13. Earning per share

Earning per share is calculated by dividing net profit for the year and by the weighted average number of

ordinary shares after deduction of treasury shares, as follows:

2014 2013

Net profit for the year 5,148,141 4,236,613

Weighted average number of issued shares (share) 186,239,041 186,240,000

Earning per share (fils) 27.64 22.75

14. Staff Costs

General and administrative expenses include staff costs of KD 2,717,340 (31 December 2013 - KD 2,630,451).

As of 31 December 2014, the Company had 223 (31 December 2013: 225) employees.

15. Segmental analysis

The Company has five principal reportable segments as follows:

� Marine and aviation

Insurance against risks related to goods transportation and different types of marine and aviation vessels.

� Fire

Insurance against fire for different types of buildings, stores, industrial risks and gas and oil industry.

Kuwait Insurance Company S.A.K.P

Kuwait

Notes to the Financial Statements for the year ended 31 December 2014 (All amounts are in Kuwaiti Dinars unless otherwise stated)

17

� General accident

Insurance against risks of contractors, machinery and computer damages and cessation of work; insurance

cover for cash, bonds, fidelity, professional risks, work accidents, civil responsibility and motor vehicles.

� Life insurance

Life insurance cover for individuals and groups and medical insurance cover.

� Takaful

Insurance against all type of risk under Takaful insurance law.

Investment activities are not considered as a segment by itself. Assets and liabilities are not allocated to

the Company’s segments except for those related to the life insurance and Takaful insurance segment.

Kuwait Insurance Company S.A.K.P

Kuwait

Notes to the Financial Statements for the year ended 31 December 2014 (All amounts are in Kuwaiti Dinars unless otherwise stated)

18

Information on the Company’s principal reportable segments are as follows:

Income statement

Year ended 31 December 2014

Marine &

aviation

Fire

General

accident

Life Takaful

Unallocated

items

Total

Revenue

Gross premium revenue 2,873,971 6,005,479 19,496,809 6,863,480 375,970 - 35,615,709

Premium ceded to reinsurers (2,392,026) (5,460,182) (5,713,244) (1,842,476) (73,192) - (15,481,120)

Net premiums revenue 481,945 545,297 13,783,565 5,021,004 302,778 - 20,134,589

Changes in reserve for unexpired risks 2,502 (38,544) (51,242) - 496,239 - 408,955

Premiums earned 484,447 506,753 13,732,323 5,021,004 799,017 - 20,543,544

Commissions earned 789,416 570,823 1,278,514 85,975 10,663 - 2,735,391

Investment income - - - 420,506 14,640 4,229,458 4,664,604

Other income 5,653 757 879,206 (33,230) 5,922 58,484 916,792

1,279,516 1,078,333 15,890,043 5,494,255 830,242 4,287,942 28,860,331

Expenses

Net incurred claims 99,099 11,416 8,809,534 1,439,986 796,094 - 11,156,129

Change in additional reserve - 50,000 950,000 - - - 1,000,000

Changes in reserve for life insurance fund - - - 1,738,215 - - 1,738,215

Life insurance – Expiry settlement - - - 985,555 - - 985,555

Life insurance – Policies liquidated - - - 115,308 - - 115,308

Commissions paid 134,271 240,599 3,068,769 241,946 23,657 - 3,709,242

General and administrative expenses 472,774 417,154 1,334,892 673,245 73,313 1,274,470 4,245,848

Participants rights - - - - (31,411) - (31,411)

Impairment loss on investment securities - - - - - 507,233 507,233

BOD remuneration - - - - - 56,000 56,000

Contribution to Kuwait foundation for advancement of Science share (KFAS) - - - - - 54,342 54,342

National Labour Support tax - - - - - 125,521 125,521

Zakat tax - - - - - 50,208 50,208

706,144 719,169 14,163,195 5,194,255 861,653 2,067,774 23,712,190

Net profit for the year 573,372 359,164 1,726,848 300,000 (31,411) 2,220,168 5,148,141

Kuwait Insurance Company S.A.K.P

Kuwait

Notes to the Financial Statements for the year ended 31 December 2014 (All amounts are in Kuwaiti Dinars unless otherwise stated)

19

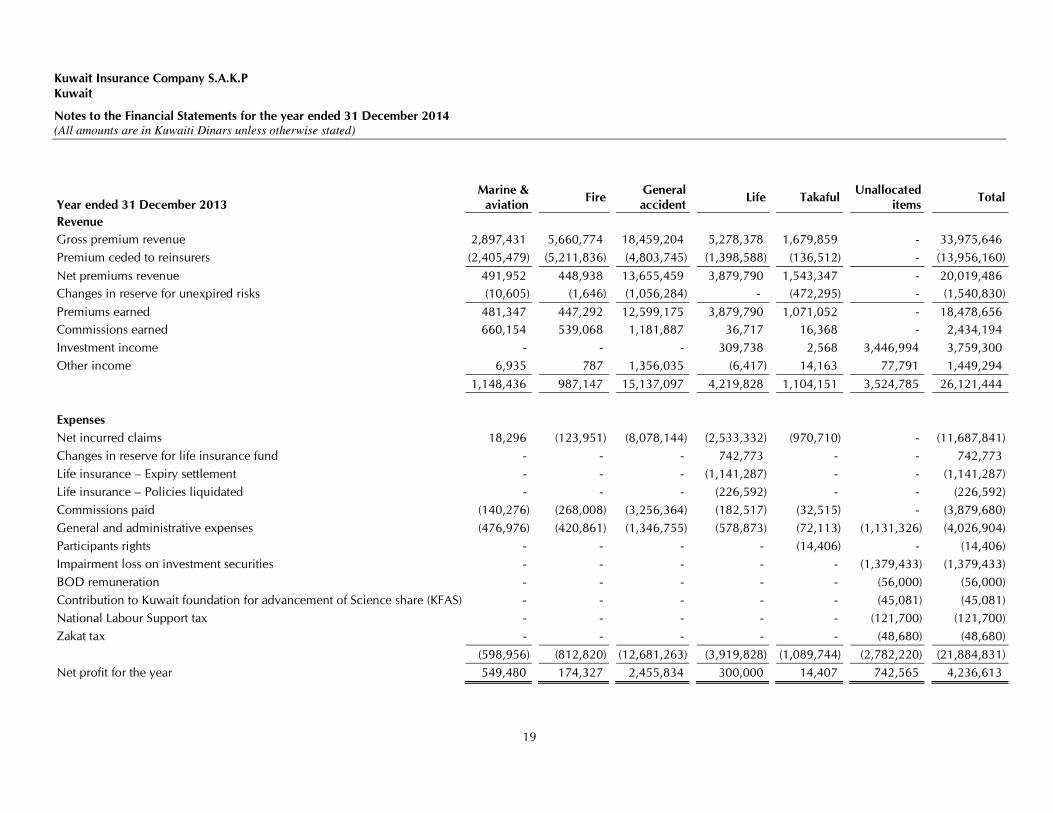

Year ended 31 December 2013

Marine &

aviation

Fire

General

accident

Life Takaful

Unallocated

items

Total

Revenue

Gross premium revenue 2,897,431 5,660,774 18,459,204 5,278,378 1,679,859 - 33,975,646

Premium ceded to reinsurers (2,405,479) (5,211,836) (4,803,745) (1,398,588) (136,512) - (13,956,160)

Net premiums revenue 491,952 448,938 13,655,459 3,879,790 1,543,347 - 20,019,486

Changes in reserve for unexpired risks (10,605) (1,646) (1,056,284) - (472,295) - (1,540,830)

Premiums earned 481,347 447,292 12,599,175 3,879,790 1,071,052 - 18,478,656

Commissions earned 660,154 539,068 1,181,887 36,717 16,368 - 2,434,194

Investment income - - - 309,738 2,568 3,446,994 3,759,300

Other income 6,935 787 1,356,035 (6,417) 14,163 77,791 1,449,294

1,148,436 987,147 15,137,097 4,219,828 1,104,151 3,524,785 26,121,444

Expenses

Net incurred claims 18,296 (123,951) (8,078,144) (2,533,332) (970,710) - (11,687,841)

Changes in reserve for life insurance fund - - - 742,773 - - 742,773

Life insurance – Expiry settlement - - - (1,141,287) - - (1,141,287)

Life insurance – Policies liquidated - - - (226,592) - - (226,592)

Commissions paid (140,276) (268,008) (3,256,364) (182,517) (32,515) - (3,879,680)

General and administrative expenses (476,976) (420,861) (1,346,755) (578,873) (72,113) (1,131,326) (4,026,904)

Participants rights - - - - (14,406) - (14,406)

Impairment loss on investment securities - - - - - (1,379,433) (1,379,433)

BOD remuneration - - - - - (56,000) (56,000)

Contribution to Kuwait foundation for advancement of Science share (KFAS) - - - - - (45,081) (45,081)

National Labour Support tax - - - - - (121,700) (121,700)

Zakat tax - - - - - (48,680) (48,680)

(598,956) (812,820) (12,681,263) (3,919,828) (1,089,744) (2,782,220) (21,884,831)

Net profit for the year 549,480 174,327 2,455,834 300,000 14,407 742,565 4,236,613

Kuwait Insurance Company S.A.K.P

Kuwait

Notes to the Financial Statements for the year ended 31 December 2014 (All amounts are in Kuwaiti Dinars unless otherwise stated)

20

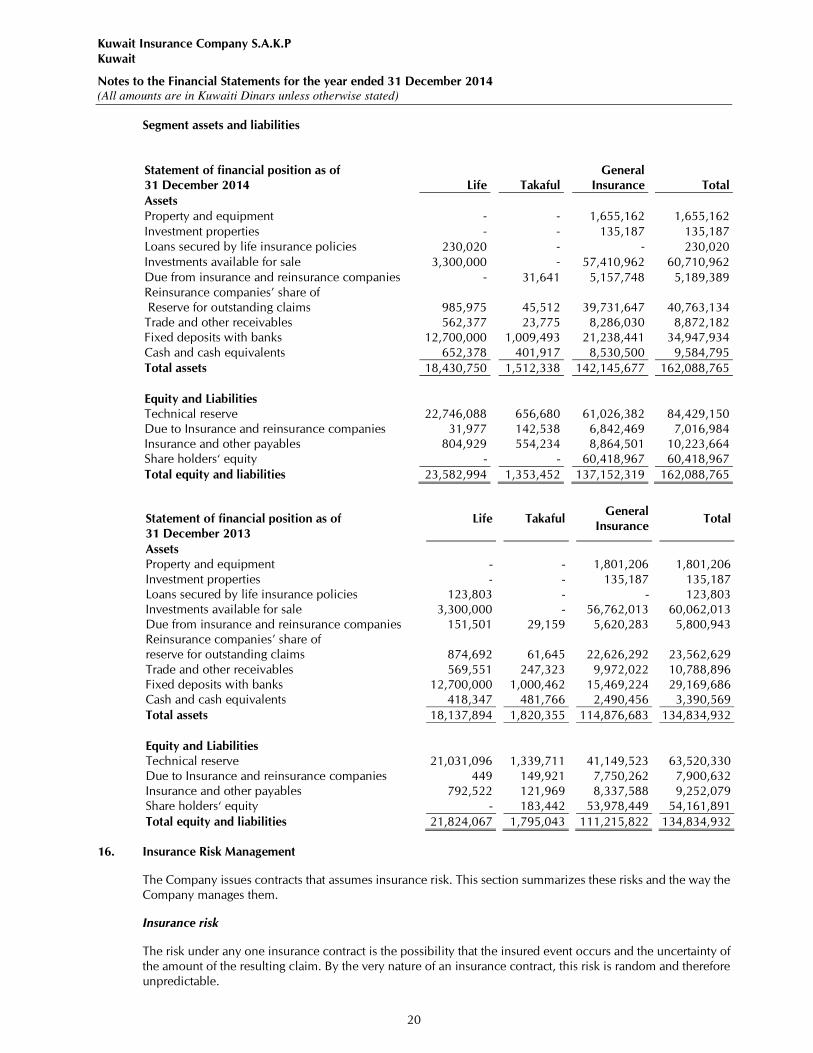

Segment assets and liabilities

Statement of financial position as of

31 December 2014 Life Takaful

General

Insurance Total

Assets

Property and equipment - - 1,655,162 1,655,162

Investment properties - - 135,187 135,187

Loans secured by life insurance policies 230,020 - - 230,020

Investments available for sale 3,300,000 - 57,410,962 60,710,962

Due from insurance and reinsurance companies - 31,641 5,157,748 5,189,389

Reinsurance companies’ share of

Reserve for outstanding claims 985,975

45,512

39,731,647

40,763,134

Trade and other receivables 562,377 23,775 8,286,030 8,872,182

Fixed deposits with banks 12,700,000 1,009,493 21,238,441 34,947,934

Cash and cash equivalents 652,378 401,917 8,530,500 9,584,795

Total assets 18,430,750 1,512,338 142,145,677 162,088,765

Equity and Liabilities

Technical reserve 22,746,088 656,680 61,026,382 84,429,150

Due to Insurance and reinsurance companies 31,977 142,538 6,842,469 7,016,984

Insurance and other payables 804,929 554,234 8,864,501 10,223,664

Share holders‘ equity - - 60,418,967 60,418,967

Total equity and liabilities 23,582,994 1,353,452 137,152,319 162,088,765

Statement of financial position as of

31 December 2013

Life Takaful General

Insurance Total

Assets

Property and equipment - - 1,801,206 1,801,206

Investment properties - - 135,187 135,187

Loans secured by life insurance policies 123,803 - - 123,803

Investments available for sale 3,300,000 - 56,762,013 60,062,013

Due from insurance and reinsurance companies 151,501 29,159 5,620,283 5,800,943

Reinsurance companies’ share of

reserve for outstanding claims

874,692

61,645

22,626,292

23,562,629

Trade and other receivables 569,551 247,323 9,972,022 10,788,896

Fixed deposits with banks 12,700,000 1,000,462 15,469,224 29,169,686

Cash and cash equivalents 418,347 481,766 2,490,456 3,390,569

Total assets 18,137,894 1,820,355 114,876,683 134,834,932

Equity and Liabilities

Technical reserve 21,031,096 1,339,711 41,149,523 63,520,330

Due to Insurance and reinsurance companies 449 149,921 7,750,262 7,900,632

Insurance and other payables 792,522 121,969 8,337,588 9,252,079

Share holders‘ equity - 183,442 53,978,449 54,161,891

Total equity and liabilities 21,824,067 1,795,043 111,215,822 134,834,932

16. Insurance Risk Management

The Company issues contracts that assumes insurance risk. This section summarizes these risks and the way the

Company manages them.

Insurance risk

The risk under any one insurance contract is the possibility that the insured event occurs and the uncertainty of

the amount of the resulting claim. By the very nature of an insurance contract, this risk is random and therefore

unpredictable.

Kuwait Insurance Company S.A.K.P

Kuwait

Notes to the Financial Statements for the year ended 31 December 2014 (All amounts are in Kuwaiti Dinars unless otherwise stated)

21

The principal risk that the Company faces under its insurance contracts is that the actual claims and benefit

payments exceed the carrying amount of the insurance liabilities. This could occur because the frequency or

severity of claims and benefits are greater than estimated. Insurance events are random and the actual number

and amount of claims and benefits will vary from year to year.

The Company manages these risks through its underwriting strategy, adequate reinsurance arrangements and

proactive claims handling.

Sources of uncertainty in the estimation of future claim payments

Non life

Claims are payable on a claims-occurrence basis. The Company is liable for all insured events that occurred

during the term of the contract, even if the loss is discovered after the end of the contract term. As a result,

liability claims are settled over a long period of time and an element of the claims provision relates to incurred

but not reported claims (IBNR). There are several variables that affect the amount and timing of cash flows from

these contracts. These mainly relate to the inherent risks of the business activities carried out by individual

contract holders and the risk management procedures they adopted.

The estimated cost of claims includes direct expenses to be incurred in settling claims, net of the expected

subrogation value and other recoveries. The Company takes all reasonable steps to ensure that it has appropriate

information regarding its claims exposures. However, given the uncertainty in establishing claims provisions, it

is likely that the final outcome will prove to be different from the original liability established. The liability for

these contracts comprise a provision for IBNR, a provision for reported claims not yet paid and a provision for

unexpired risks at the statement of financial position date.

In estimating the liability for the cost of reported claims not yet paid the Company considers any information

available from loss adjusters and information on the cost of settling claims with similar characteristics in

previous periods. Large claims are assessed on a case-by-case basis or projected separately.

Life

Uncertainty in the estimation of future benefit payments and premium receipts for life insurance contracts arises

from the unpredictability of overall levels of mortality, health and the variability in contract holder behaviour.

The Company uses an actuarial valuation to determine reserve estimate for life insurance contracts. For health

and disability insurance covers there is no need to estimate mortality rates or morbidity rates for future years

because these contracts have short duration and the claims are payable on a claims-occurrence basis. These

insurance contracts are exposed to similar risks of uncertainty in the estimation of future claim payments as non

life insurance contracts and are managed in a similar manner.

17. Fair value estimation

The fair value for the financial assets and financial liabilities are determined as follows:

• Level one: Quoted prices in active markets for identical financial instruments.

• Level two: Quoted prices in an active market for similar instruments. Quoted prices for identical assets

or liabilities in the market that is not active. Inputs other than quoted prices that is observable for assets

or liabilities.

• Level three: Inputs for the assets or liabilities that are not based on observable market data.

Kuwait Insurance Company S.A.K.P

Kuwait

Notes to the Financial Statements for the year ended 31 December 2014 (All amounts are in Kuwaiti Dinars unless otherwise stated)

22

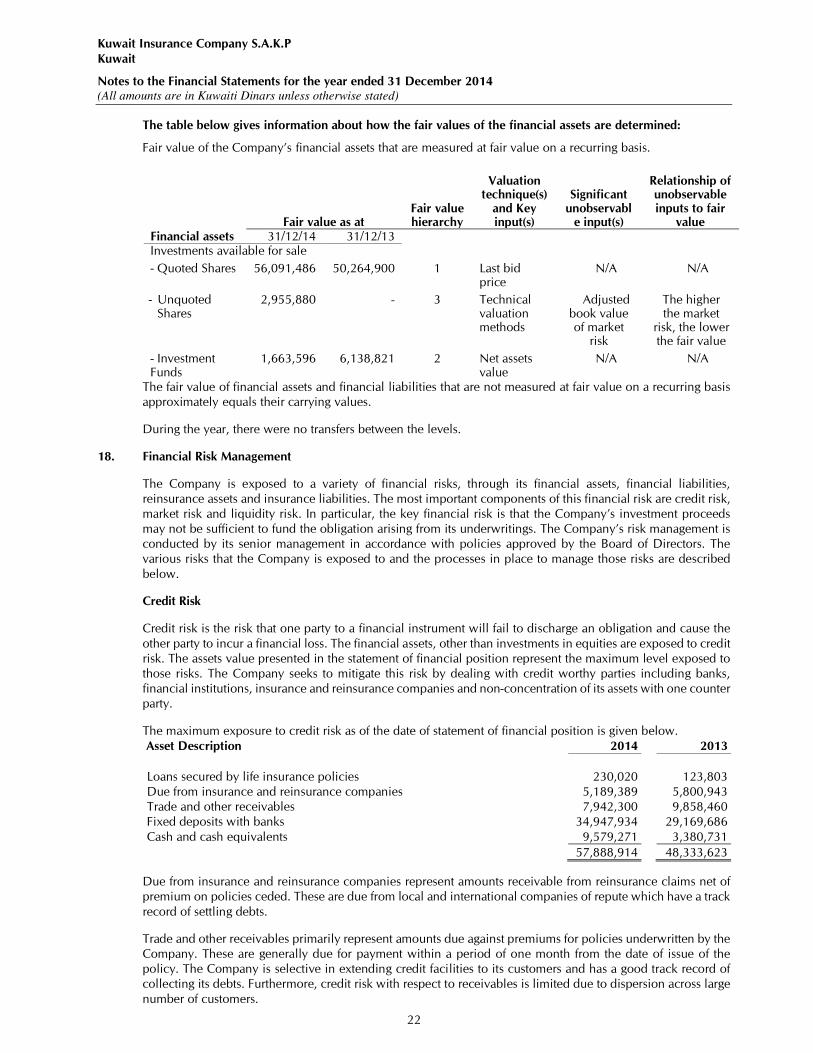

The table below gives information about how the fair values of the financial assets are determined:

Fair value of the Company’s financial assets that are measured at fair value on a recurring basis.

Fair value as at Fair value hierarchy

Valuation technique(s)

and Key input(s)

Significant unobservabl

e input(s)

Relationship of unobservable inputs to fair

value Financial assets 31/12/14 31/12/13 Investments available for sale

- Quoted Shares 56,091,486 50,264,900 1 Last bid price

N/A N/A

- Unquoted Shares

2,955,880 - 3 Technical valuation methods

Adjusted book value of market

risk

The higher the market

risk, the lower the fair value

- Investment Funds

1,663,596 6,138,821 2 Net assets value

N/A N/A

The fair value of financial assets and financial liabilities that are not measured at fair value on a recurring basis

approximately equals their carrying values.

During the year, there were no transfers between the levels.

18. Financial Risk Management

The Company is exposed to a variety of financial risks, through its financial assets, financial liabilities,

reinsurance assets and insurance liabilities. The most important components of this financial risk are credit risk,

market risk and liquidity risk. In particular, the key financial risk is that the Company’s investment proceeds

may not be sufficient to fund the obligation arising from its underwritings. The Company’s risk management is

conducted by its senior management in accordance with policies approved by the Board of Directors. The

various risks that the Company is exposed to and the processes in place to manage those risks are described

below.

Credit Risk

Credit risk is the risk that one party to a financial instrument will fail to discharge an obligation and cause the

other party to incur a financial loss. The financial assets, other than investments in equities are exposed to credit

risk. The assets value presented in the statement of financial position represent the maximum level exposed to

those risks. The Company seeks to mitigate this risk by dealing with credit worthy parties including banks,

financial institutions, insurance and reinsurance companies and non-concentration of its assets with one counter

party.

The maximum exposure to credit risk as of the date of statement of financial position is given below.

Asset Description 2014 2013

Loans secured by life insurance policies 230,020 123,803

Due from insurance and reinsurance companies 5,189,389 5,800,943

Trade and other receivables 7,942,300 9,858,460

Fixed deposits with banks 34,947,934 29,169,686

Cash and cash equivalents 9,579,271 3,380,731

57,888,914 48,333,623

Due from insurance and reinsurance companies represent amounts receivable from reinsurance claims net of

premium on policies ceded. These are due from local and international companies of repute which have a track

record of settling debts.

Trade and other receivables primarily represent amounts due against premiums for policies underwritten by the

Company. These are generally due for payment within a period of one month from the date of issue of the

policy. The Company is selective in extending credit facilities to its customers and has a good track record of

collecting its debts. Furthermore, credit risk with respect to receivables is limited due to dispersion across large

number of customers.

Kuwait Insurance Company S.A.K.P

Kuwait

Notes to the Financial Statements for the year ended 31 December 2014 (All amounts are in Kuwaiti Dinars unless otherwise stated)

23

At 31 December 2014, trade receivables of KD 1,848,191(31 December 2013 – KD 2,207,702) are neither

past due nor impaired and KD 5,797,371 (31 December 2013 – KD 7,377,584) are past due. Out of the past

due Receivables, KD 2,841,697is due for a period of one month to six months (31 December 2013 – KD

2,906,188) and KD 2,955,674 is due for a period of 6 months to one year (31 December 2013 – KD 2,527,283)

and KD 2,375,000 is due for more than one year (31 December 2013 – KD 1,944,113).

The Company made provision of KD 2,375,000 (31 December 2013 - KD 2,283,829) against past due

receivable. The Company believes that the balance amount of trade receivables can be recovered. The other

classes of financials assets are not impaired.

Deposits are placed with banks which have been given high rating by reputed international rating agencies

category (a). These deposits mature within a maximum period of 6 months from the date of this financial

statements.

Market Risk

Market risk is the risk that an enterprise may incur financial losses due to adverse movements in market price of investments or interest rates and foreign currency rates.

(a) Foreign Currency Risk

Foreign currency risk is represented in the exposure to changing currency exchange rates that may adversely

affect the Company’s cash flows or the value of assets and liabilities in foreign currencies. The Company is

exposed to foreign currency risk primarily from its foreign currency denominated investments and its dues

from/to re-insurance counterparties. The Company seeks to mitigate this risk by dealing in stable currencies

such as US Dollars, Euro and Sterling Pounds and monitoring its currency position on a regular basis.

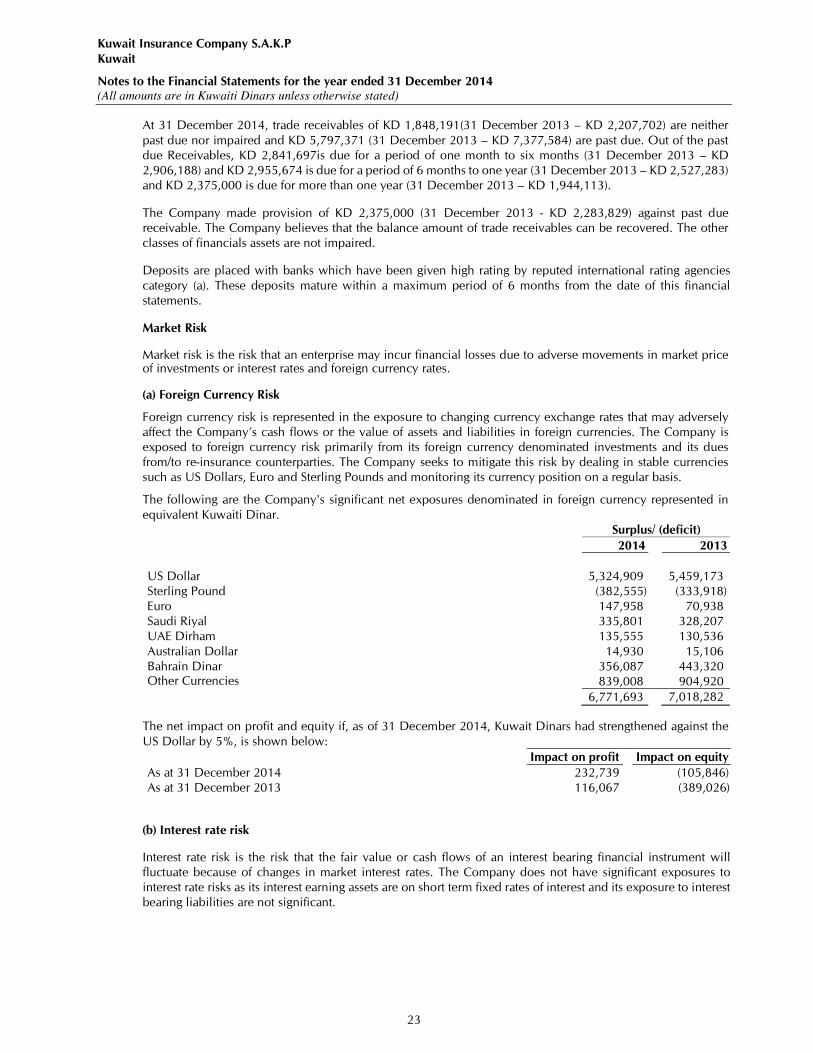

The following are the Company's significant net exposures denominated in foreign currency represented in

equivalent Kuwaiti Dinar.

Surplus/ (deficit)

2014 2013

US Dollar 5,324,909 5,459,173

Sterling Pound (382,555) (333,918)

Euro 147,958 70,938

Saudi Riyal 335,801 328,207

UAE Dirham 135,555 130,536

Australian Dollar 14,930 15,106

Bahrain Dinar 356,087 443,320 Other Currencies 839,008 904,920

6,771,693 7,018,282

The net impact on profit and equity if, as of 31 December 2014, Kuwait Dinars had strengthened against the

US Dollar by 5%, is shown below:

Impact on profit Impact on equity

As at 31 December 2014 232,739 (105,846)

As at 31 December 2013 116,067 (389,026)

(b) Interest rate risk

Interest rate risk is the risk that the fair value or cash flows of an interest bearing financial instrument will

fluctuate because of changes in market interest rates. The Company does not have significant exposures to

interest rate risks as its interest earning assets are on short term fixed rates of interest and its exposure to interest

bearing liabilities are not significant.

Kuwait Insurance Company S.A.K.P

Kuwait

Notes to the Financial Statements for the year ended 31 December 2014 (All amounts are in Kuwaiti Dinars unless otherwise stated)

24

(c) Equity Price risk

This is the risk that the value of financial instruments will fluctuate as a result of changes in market prices,

caused by factors specific to the instrument or its issuer or factors affecting all instruments traded in the market.

The Company is exposed to equity price risk from investments held by the Company and classified as “available

for sale”. The Company’s investments are primarily exposed to the Kuwait Stock Exchange index.

To manage its price risk arising from investments in equity securities, the Company invests in a diversified

portfolio of securities. Diversification of the portfolio is done in accordance with the limits set by the Company.

The Board of directors constantly monitors the exposures and provides directions to manage risks and maximize

profits.

At 31 December 2014, if the Kuwait Stock Exchange index had changed by 5%, the equity of the Company

would have changed by KD 2,387,450 (31 December 2013 - KD 2,513,245).

Liquidity Risk

It is the risk that the Company may not be able to meet its financial obligations as they fall due. The policy of

the Company is to ensure that sufficient liquidity is available at all times to meet contractual obligations,

including loss claims. To manage liquidity risk the Company maintains sufficient cash and marketable securities,

having adequate amount of credit facilities and investing in securities which can be easily closed out. The

Company also has the option to raise additional capital to meet funding requirements.

The Company’s contractual liabilities as of 31 December 2014 mature over a period of one year.

19. Capital Risk Management

The Company’s objectives when managing capital are

• To ensure adequate funds are available to underwrite risks and maintain investor, creditor and market

conditions;

• To make available funds for future development of the business;

• To safeguard the Company’s ability to continue as a going concern so that it can continue to operate;

• To provide adequate return to shareholders and benefits to its other shareholders

The Board of Directors constantly monitors the capital structure of the Company with a view to ensuring that a

balance is maintained between returns and risk. The management ensures that the Company is not geared

beyond acceptable limits. For this purpose, the Company may adjust the amount of dividend payable to its

shareholders, issue new shares or sell assets to reduce debt.

Furthermore in order to protect against the impact of large claims and catastrophes, the Company is required

under law to maintain technical reserves depending on the exposure to various types of underwriting exposures.

The details of this reserve are given in Note No. 10.

Under local regulations, the Company places some of its investments securities and bank deposits under lien

to the regulator. The amount of securities and deposits to be placed under lien is determined as a percentage

of direct premium, received during the year for all the segments other than life insurance segment. Regarding

life insurance segment, the amount to be placed under lien is determined at 100% of the liability, as ascertained

by an actuarial valuation at the end of the year. The extent of lien on deposits is given in Note No. 4 and 6.

20. Critical accounting estimates and judgments

The Company makes estimates and assumptions that may affect amounts reported in these financial statements.

Estimates are revised if changes occur in the circumstances on which the estimate was based. The areas where

estimates and assumptions are significant to the financial statements, or areas involving a higher degree of

judgment, are:

Impairment of financial assets

The Company reviews financial assets at each statement of financial position date to assess whether a provision

for impairment loss should be recognized in the Statement of Income. The process for estimating the amount

of an impairment loss involves considerable judgment by the management with respect to the estimation of

Kuwait Insurance Company S.A.K.P

Kuwait

Notes to the Financial Statements for the year ended 31 December 2014 (All amounts are in Kuwaiti Dinars unless otherwise stated)

25

future cash flows. Such estimates and assumptions are also based on several other factors involving varying

degrees of judgment and uncertainty.

Classification of financial instruments

On acquisition of a financial instrument, the Company’s management decides its classification. In making that

judgment the Company considers the primary purpose for which it is acquired and how it intends to manage

and report its performance. Such judgment determines whether it is subsequently measured at fair value or at

amortized cost.

Financial instruments carried at amortized cost

The effective yield method of calculating the amortized cost of a financial instrument involves the estimation

of future cash flows through the expected life of the instrument.

Provision for outstanding claims

Considerable judgment by management is required in the estimation of amounts due to contract holders arising

from claims made under insurance contracts. Further information on the basis of estimation and significant

assumptions, made by the Company are given in Note No. 16 of these financial statements.

21. Related party transactions

In the ordinary course of business, the company has carried some transactions with related parties. The

Company carried out transaction with related parties on term approved by management. Transactions with

related parties are included in trade and other receivables note (5) and are subject to approval of Annual

General Meeting for shareholders. The balances and transactions with related parties are as follows:

Kuwaiti Dinars

2014 2013

Transactions:

Gross premiums written 3,330,071 3,169,446

Claims paid 1,794,003 3,116,858

Balances :

Due from related parties 539,234 629,305

Key Management Remuneration 300,000 300,000