KPN Investor Day: Mobile International · exhaustively) in the 2008 Annual Report. Challenger...

109

KPN Investor Day: Mobile International Doing things differently Paris, 12 June 2009

Transcript of KPN Investor Day: Mobile International · exhaustively) in the 2008 Annual Report. Challenger...

KPN Investor Day: Mobile InternationalDoing things differently

Paris, 12 June 2009

2Challenger strategy: delivering profitable growth

Safe harborNon-GAAP measures and management estimatesThis presentation contains a number of non-GAAP figures, such as EBITDA and free cash flow. These non-GAAP figures should not be viewed as a substitute for KPN’s GAAP figures. KPN defines EBITDA as operating result before depreciation and impairments of PP&E and amortization and impairments of intangible assets. Note that KPN’s definition of EBITDA deviates from the literal definition of earnings before interest, taxes, depreciation and amortization and should not be considered in isolation or as a substitute for analyses of the results as reported under IFRS. All market share information in this presentation is based on management estimates based on externally available information, unless indicated otherwise.

Forward looking statementsCertain statements contained in this presentation constitute forward-looking statements. These statements may include, without limitation, statements concerning future results of operations, the impact of regulatory initiatives on KPN’s operations, its and its joint ventures' share of new and existing markets, general industry and macro-economic trends and KPN’s performance relative thereto, and statements preceded by, followed by or including the words “believes”, “expects”, “anticipates” or similar expressions.These forward-looking statements rely on a number of assumptions concerning future events and are subject to uncertainties and other factors, many of which are outside KPN’s control that could cause actual results to differ materially from such statements. A number of these factors are described (not exhaustively) in the 2008 Annual Report.

3Challenger strategy: delivering profitable growth

Programme

Eric HagemanInternational wholesale11.30 - 11.45

Break10.45 - 11.00

Stan MillerStrategy Mobile International09.30 - 10.00

Vivienne van AstenOpening09.00 - 09.10

Marc van AsbroeckRegulation10.00 - 10.20

Stan MillerConcluding remarks11.45 - 11.50

Ad ScheepbouwerIntroduction09.10 - 09.30

Thorsten DirksE-Plus11.00 - 11.30

SpeakerTopicTime

Eric HagemanFinance

Libor Voncina, replaced by Erik HovingKPN Group Belgium10.20 - 10.45

Q&A11.50 - 12.15

Lunch12.30 - 14.00

4Challenger strategy: delivering profitable growth

Agenda

Eric Hageman, CEO International WholesaleInternational Wholesale

Stan Miller, CEO KPN Mobile InternationalConcluding remarks

Thorsten Dirks, CEO E-PlusE-Plus

Erik Hoving, CTO KPN Mobile International KPN Group Belgium

Eric Hageman, CFO KPN Mobile InternationalFinance

Stan Miller, CEO KPN Mobile InternationalStrategy

Marc van Asbroeck, Chief Legal & RegulationRegulation

Ad Scheepbouwer, Chairman and CEO KPNIntroduction

5Challenger strategy: delivering profitable growth

Historic perspective: KPN end of 20011

The Netherlands main contributor, activities all over the world

€ 10.6 bn€ 3.1 bn€ 0.9 bn

Revenues EBITDACash flow2

The Netherlands & other

€ 12.9 bn€ 3.4 bn€ 0.4 bn

Gross debtFTE

€ 23.0 bn45.7k

Revenues EBITDA Cash flow2

KPN Group

1 Pro forma figures, based on Dutch GAAP2 Cash flow defined as EBITDA -/- Capex

Footprint 2001

€ 2.3 bn€ 0.3 bn

-/-€ 0.5 bn

Revenues EBITDACash flow2

Mobile International

6Challenger strategy: delivering profitable growth

KPN strategies 2002-2010Clear strategies and execution have paved the way for growth opportunities

Time

Valu

e

‘Turnaround’2002-2004

• Turnaround BASE Belgium• ‘Line in the sand’ at KPN Mobile the Netherlands• Sale of non-core assets

• Ahead of the curve with All-IP strategy• Challenger strategy at E-Plus• Strategic M&A: Telfort, Getronics

• The Netherlands reaching inflection• Continued growth Mobile International• Additional growth from recent acquisitions

‘Attack-Defend-Exploit’

2005-2007

‘Back to growth’2008-2010

7Challenger strategy: delivering profitable growth

2002-2004: Turnaround strategyTough actions taken with focus on core activities

• Created internal sense of urgency by change of management

• Forced lay-offs through social plan for more than 5,000 FTE

• Management focus on operational excellence and customers

• Harsh refinancing actions taken to defer financial distress

• € 2.5 bn credit facility, consortium of 8 international banks in September 2001

• € 4.8 bn rights issue in December 2001, 85% dilution of outstanding shares

• Focus on core markets – The Netherlands; market leader in Fixed and Mobile

– Germany; # 3 mobile operator

– Belgium; # 3 mobile operator

• Disposal of non-core assets, total proceeds of ~€ 4.4 bn– Ireland, Indonesia, Hungary, Czech Republic: ~€ 3.0 bn

– Other non-core assets, totalling ~€ 1.4 bn

• Focus on cash flow instead of revenue growth

Focused strategy

Refinancing

Operational excellence

8Challenger strategy: delivering profitable growth

2005-2007: Attack-Defend-Exploit strategyTransforming our business model

• Proactive migration of traditional services to IP-based services, e.g. VoIP

• New IP and broadband services, extended with value-added services

• Maximize position in traditional services prior to migration to IP-based services and phase-out

• Open access model based on IP

• Unbundlers as resellers on KPN infrastructure

• Broadband access network: VDSL, HSDPA

• Rationalization of systems and processes

The NetherlandsAttack-Defend-Exploit strategy

• Handpick segments with tailored offerings

• Turn core services into great value

• Redesign pull & its economics

• Focus regionally, maximize impact of pull actions

• Launch offensive to throw rivals off-balance

• Maximize margin

Mobile InternationalChallenger Strategy

Attack

Defend

Exploit

Customer targeting

Proposition

Channels

Deployment

Regulatory

Financial model

9Challenger strategy: delivering profitable growth

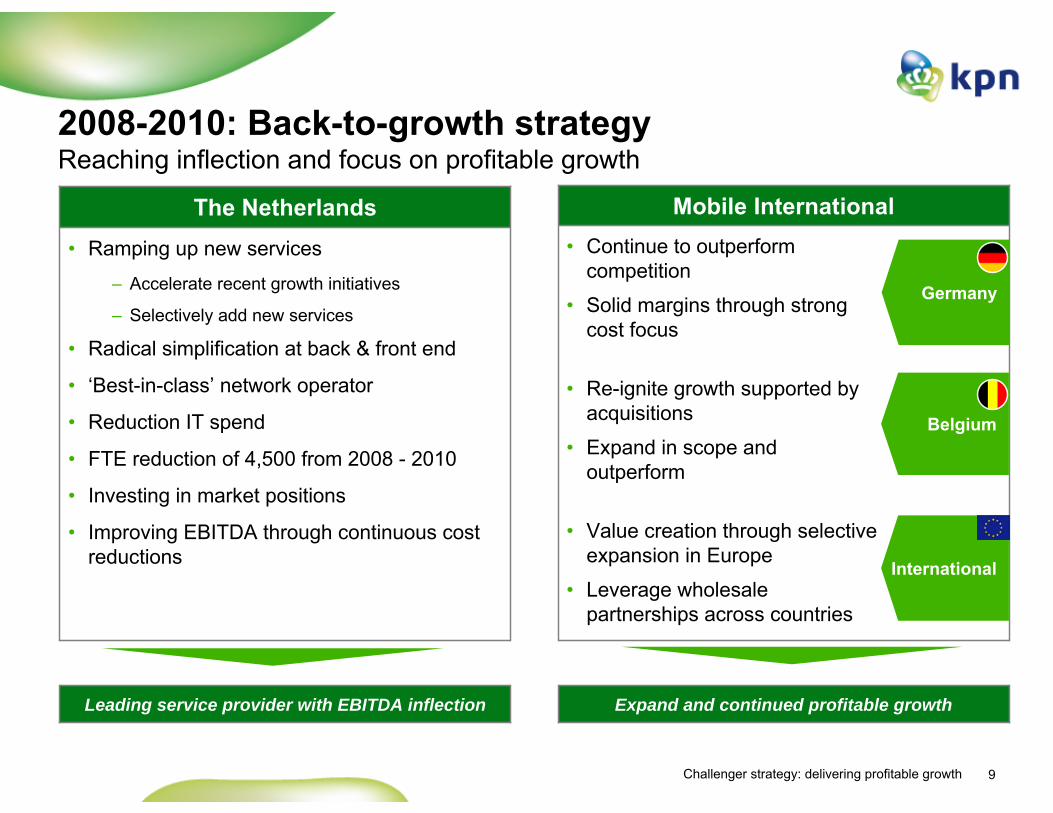

2008-2010: Back-to-growth strategyReaching inflection and focus on profitable growth

Leading service provider with EBITDA inflection

• Ramping up new services

– Accelerate recent growth initiatives

– Selectively add new services

• Radical simplification at back & front end

• ‘Best-in-class’ network operator

• Reduction IT spend

• FTE reduction of 4,500 from 2008 - 2010

• Investing in market positions

• Improving EBITDA through continuous cost reductions

The Netherlands

Expand and continued profitable growth

• Continue to outperform competition

• Solid margins through strong cost focus

• Re-ignite growth supported by acquisitions

• Expand in scope and outperform

• Value creation through selective expansion in Europe

• Leverage wholesale partnerships across countries

Mobile International

Germany

Belgium

International

10Challenger strategy: delivering profitable growth

KPN share price outperformance(1)

KPN strategies focus on value creationKPN clearly outperforming the Telco sector

0

2

4

6

8

10

12

14

1 Performances based on prices of 10 September ’01 (appointment of Ad Scheepbouwer) until 5 June ’09

+284%‘Turnaround’2002-2004

‘Attack-Defend-Exploit’2005-2007

‘Back to growth’2008-2010

€

-24%

KPN DJ Telco Index

Jun 2009Sep 2001 20042003 2005 2006 2007 2008

+193% +47% +17%

x% KPN performance vs. DJ Telco Index

11Challenger strategy: delivering profitable growth

KPN today1

Market leader in the Netherlands, mobile Challenger abroadGross debt € 13.6 bnFTE 35.6k

Revenues € 14.6 bnEBITDA € 5.1 bnCash flow2 € 3.1 bn

KPN Group

€ 10.5 bn€ 3.6 bn€ 2.3 bn

Revenues EBITDACash flow2

The Netherlands

1~50%

1>50%

144%

• Integrated market leader in telecoms• Leading business ICT service provider• Own brands and partners

WirelessPositionMarket share

WirelinePositionMarket share

Broadband PositionMarket share

Leading MVNOCustomers ~0.2m

Launched in Jan ’09

+

€ 4.1 bn

€ 1.5 bn

€ 0.8 bn

Revenues EBITDACash flow2

Mobile International

315.4%18.0m

3>16%3.5m

• ‘Challenger’ in Belgium and Germany• Leading MVNO in Spain and France• Own brands and partners

Position Market share Customers

PositionMarket shareCustomers

1 Revenues, Cash flow and EBITDA are FY 2008, other figures relate to Q1 ’092 Cash flow defined as EBITDA -/- Capex

Current footprint

+€ 0.1 bn+€ 0.5 bn+€ 1.4 bn

+€ 1.8 bn+€ 1.2 bn+€ 1.3 bn

xx Delta versus 2001

France

España

12Challenger strategy: delivering profitable growth

Agenda

Eric Hageman, CEO International WholesaleInternational Wholesale

Stan Miller, CEO KPN Mobile InternationalConcluding remarks

Thorsten Dirks, CEO E-PlusE-Plus

Erik Hoving, CTO KPN Mobile International KPN Group Belgium

Eric Hageman, CFO KPN Mobile InternationalFinance

Stan Miller, CEO KPN Mobile InternationalStrategy

Marc van Asbroeck, Chief Legal & RegulationRegulation

Ad Scheepbouwer, Chairman and CEO KPNIntroduction

13Challenger strategy: delivering profitable growth

Key messages

• We have delivered on our promises

• Challenger strategy works

• Confident that our strategy will continue to work in the future

• Management team with strong and proven track record in managing challenges

• Continue to deliver shareholder value

14Challenger strategy: delivering profitable growth

Mobile International boardExperienced team responsible for allocation of resources

KPN Mobile International

CEOStan Miller

KPN Mobile International

CFO Eric Hageman

KPN Mobile International

CHRO Bruce Humphreys

KPN Mobile International

CLOMarc van Asbroeck

E-Plus

CEOThorsten Dirks

KPN Group Belgium

CEOLibor Vončina

International Wholesale

CEOEric Hageman

Network & Operations

CEOErik Hoving

15Challenger strategy: delivering profitable growth

Strategic cornerstonesCommitted to four key pillars that deliver profitable growth

• Use choices about what segments to target to guide offers and organization

• Turn low spend customers into value

• Use MVNOs to address non-target segments

• De-average the offer

Position around customers

• Design segment-specific, highly differentiated offers that will be irresistible for finely-targeted customers

• Introduce low cost alternative channels

Create customer pull

• Break with vertical integration

• De-average by matching customer spend to SLA and cost to serve

• Manage cross-segment overlaps

Establish partnerships Introduce profit-maximizing value chains

Strategic cornerstones• Structure organization

around segment-specific end-to-end value chains

• Explore outsourcing and partnership opportunities to reduce costs & share risks

16Challenger strategy: delivering profitable growth

Strategy introduced in 2005New strategy turns weaknesses into strengths

From

To

Push

Pull

Pull

Push

Market segments

Do it in-house

Business PartnerTailor offers to

individual segmentsLeverage business partners

One market

Strategic Initiatives– Create brand preference and customer pull– Invest in network– Customer segmentation– Outsourcing partnerships– Regulatory offensive

Objectives– Attractive customer propositions– Make indoor coverage a USP– Establish multibrand strategy– Simplify operations– Rebalance playing field

Customer service & support

MarketingBack

office, billing and IT

Sales

Sales

Sales

Network ownership

and operation

Customer service & support

MarketingBack

office, billing and IT

Network ownership

and operation

Sales

Strategy update 2005

17Challenger strategy: delivering profitable growth 17

Belgian mobile market situation in 2003

Market structure • Proximus and Mobistar controlled 91% of mobile market revenues• Both had roughly three times KPN Group Belgium’s EBITDA margin

Market characteristics

• Very low usage, fourth lowest of all EU-14 countries• 35% of the market is Post Paid• Proximus and Mobistar had close to 95% business value market share

Distribution • KPN Group Belgium had 43 exclusive shops versus more than triple that number for competition

Network • KPN Group Belgium had several hundreds fewer base stations than top two players

Business model • KPN Group Belgium was a sub-scale business with high investments, leading to negative cash flow

18Challenger strategy: delivering profitable growth

German mobile market situation in 2005

• E-Plus model demanded high investment in acquiring customersBusiness model

• E-Plus had more 2G base stations than O2 but thousands less than top two playersNetwork

• E-Plus had 179 exclusive shops versus more than 500 for competitionDistribution

• Very low usage, second lowest of all EU-25 countries• 50% of the market was Post Paid• T-Mobile and Vodafone had close to 80% business market share

Market characteristics

• T-Mobile and Vodafone controlled 75% of mobile market revenues• Both had roughly two times E-Plus’ EBITDA marginMarket structure

Strategy update 2005

19Challenger strategy: delivering profitable growth

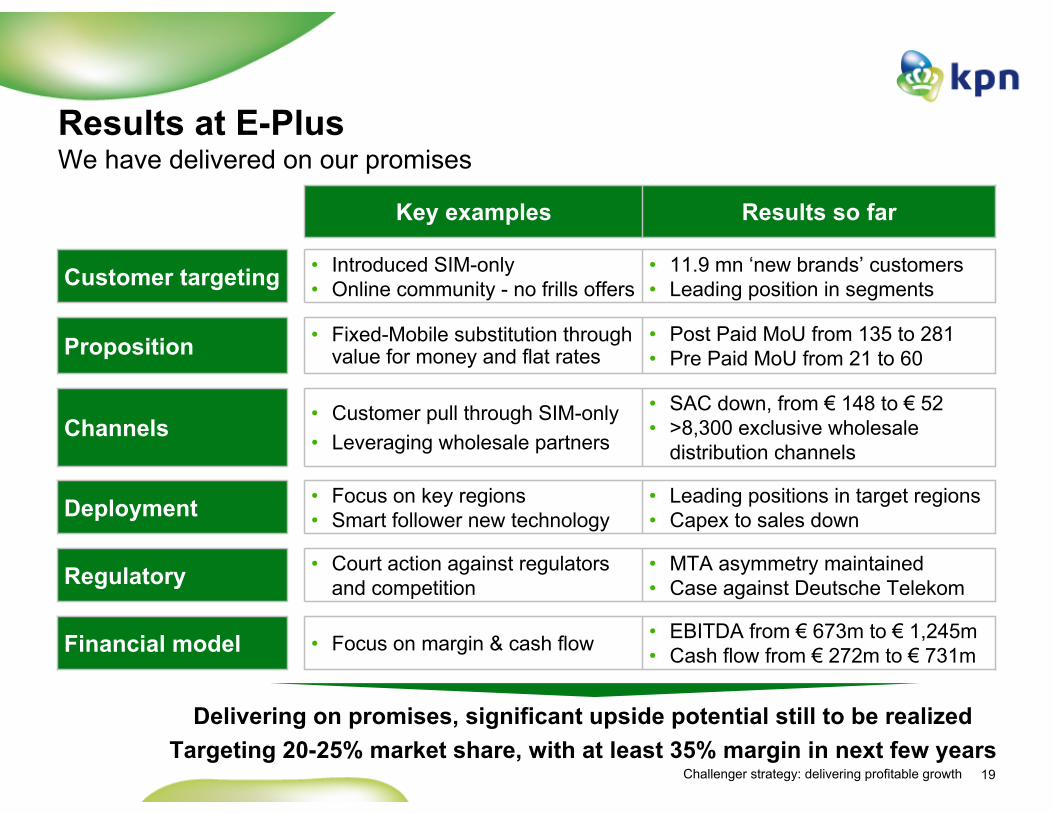

Results at E-PlusWe have delivered on our promises

• MTA asymmetry maintained• Case against Deutsche Telekom

• Court action against regulators and competitionRegulatory

• EBITDA from € 673m to € 1,245m• Cash flow from € 272m to € 731m• Focus on margin & cash flowFinancial model

• Leading positions in target regions• Capex to sales down

• Focus on key regions• Smart follower new technologyDeployment

• SAC down, from € 148 to € 52• >8,300 exclusive wholesale

distribution channels

• Customer pull through SIM-only• Leveraging wholesale partnersChannels

• Post Paid MoU from 135 to 281• Pre Paid MoU from 21 to 60

• Fixed-Mobile substitution through value for money and flat ratesProposition

• 11.9 mn ‘new brands’ customers• Leading position in segments

• Introduced SIM-only• Online community - no frills offersCustomer targeting

Results so farKey examples

Delivering on promises, significant upside potential still to be realizedTargeting 20-25% market share, with at least 35% margin in next few years

20Challenger strategy: delivering profitable growth

Mobile premiums decrease which increase mobile share of voice

Mobile market development‘Challengers’ will continue to take market share as FMS continues

New players intensify competition

Mobile share of total voice minutes

MVNOsat least20% of market

2005 >2010M

obile

pre

miu

m1

Germany ’05/’08

Belgium ’05/’08

Low HighLo

wH

igh

Increasing pressure on incumbents Germany lagging Fixed-Mobile Substitution

Finland

Denmark

Spain ’05/’08

France ’05/’08

Norway

Austria

ItalyNetherlands

Switzerland

Sweden

Greece

UK

1 Mobile cost per minute divided by fixed cost per minute Source: Equity research

Mar

ket s

hare

100%

Traditionalmobile networkoperators

No-frillsMVNOs

‘New’MVNOs

Mobile Service Providers

Today

+

-/-

21Challenger strategy: delivering profitable growth

Substitution challengers“In between”Converged services

• Ease-of-use, attractive prices• Scale and profitability• Smart follower• Partner to fixed-only players

• Customer share-of-wallet• Technology innovator

• All-in-one, quadruple play• Retention, access protection• Technology innovator

Doing things differentlyCompetitors are moving to converged services; we remain focused on mobile

Focus on converged offers

Expanding DSL footprint

Arcor integration• Competitor focus on ‘converged’ services• Untapped potential for clear FMS challenger

Fixed-Mobile organizational integration

Fixed-Mobile organizational integration

Fixed-Mobile strategies

We were the first and are market leaderWe have “carved out” segments

• Competition is copying our strategy – Low cost brands launched– More open to wholesale

General

22Challenger strategy: delivering profitable growth

Challenger strategyTactics for delivering profitable growth

Sample of some of the tactics

• Maximize return on existing assets

• Selective, low risk investments in new technology

• Expand voice target regions based on proven concept

• Monetize leading position in voice to build data position

• Leverage proven business models to new markets

• Build partnerships & business models with new entrants

• Mobile share of voice still low, significant untapped potential

• Voice remains dominant over data for the next years

Smart technology

follower

Regionalization

Wholesale & Partnerships

Fixed-Mobile Substitution

A

B

C

D

Position around

customers

Create customer pull

Establish partnerships

Introduce profit-

maximizing value chains

Strategic cornerstones

23Challenger strategy: delivering profitable growth

26%

54% 57% 52%15%

42% 38%44%

2008 2005

AFixed-Mobile SubstitutionContinued growth potential from FMS

Mobile share of voice traffic Ø 54%1

Non-voice as % of service revenues

1 Non-weighted average (2008) of Austria, Belgium, Denmark, Finland, France, Germany, Greece, Italy, Netherlands, Norway, Spain, Sweden, Switzerland, UKSource: Equity research

• Significant changes 2005-2008

− Avg. mobile voice share +16% to 54%

− Price ratio Mobile/Fixed down 25%

• Significant untapped FMS potential

− Mobile share of voice for EU top 3 >65%

• Major spread ARPM vs. MTA tariff

• Voice remains dominant part of service revenue for the next years

– Data predominantly consists of SMS at the moment

Mobile ARPM & MTA€ ct.

10.2

13.815.8

13.4

6.6 6.6 7.8 6.5

Germany FranceARPM MTA

Belgium

26%23%

17%21%20%

15% 14% 15%

Germany France4Q08 1Q06

Belgium Spain

Spain

24Challenger strategy: delivering profitable growth

WholesaleLeverage proven business models into new markets & move up the value chain

no frills / price fixed-net / utilities value / applications

Market leader

Leading

Complementary Open business model

Evolution

I

II

Wholesale growth matrix

• Expand proven business models to new markets– Footprint expanded to Spain & France: doubling addressable market– Leverage own brands & international partners

• Build partnerships & business models with new entrants – Cable / DSL, utilities – Media– Applications e.g. e-health, e-security, e-finance

I

II

B

Mar

kets

25Challenger strategy: delivering profitable growth

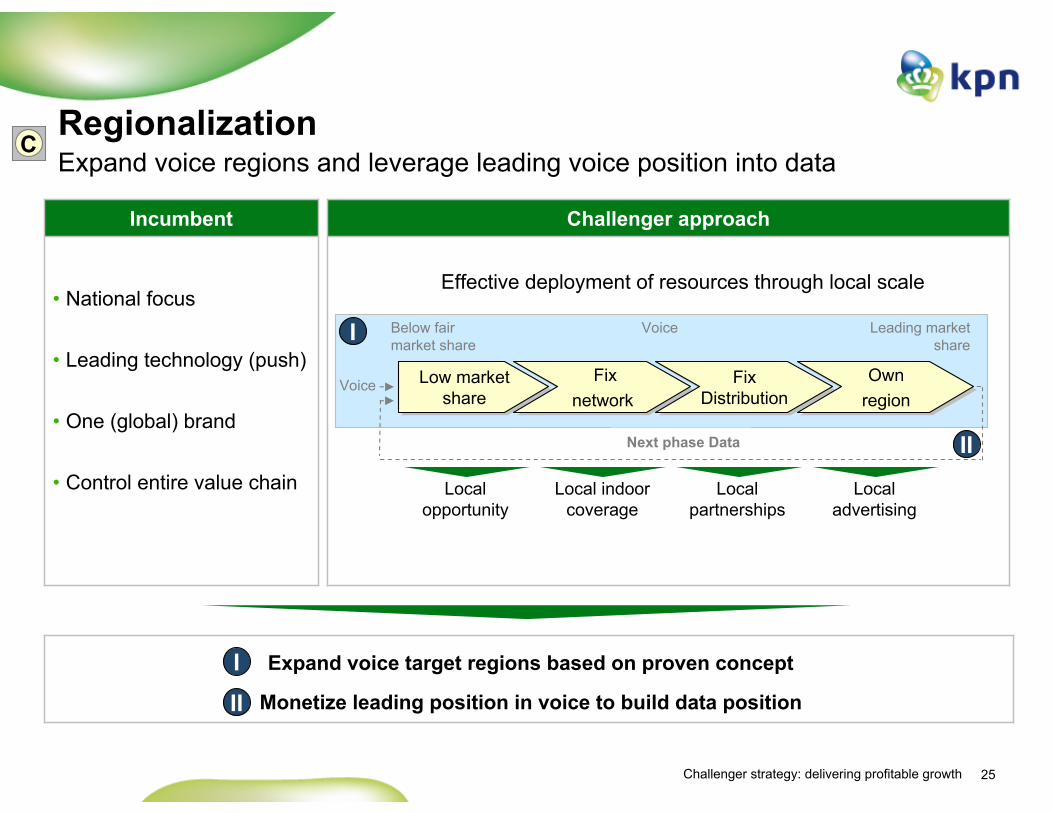

Challenger approach

RegionalizationExpand voice regions and leverage leading voice position into data

• National focus

• Leading technology (push)

• One (global) brand

• Control entire value chain

Incumbent

Voice

Next phase Data

Low market share

Low market share

Fix network

Fix network

Fix Distribution

Fix Distribution

Own regionOwn

region

Local opportunity

Local indoor coverage

Local partnerships

Local advertising

Effective deployment of resources through local scale

Below fair market share

Leading market share

Expand voice target regions based on proven concept

Monetize leading position in voice to build data position

C

I

II

I

II

Voice

26Challenger strategy: delivering profitable growth

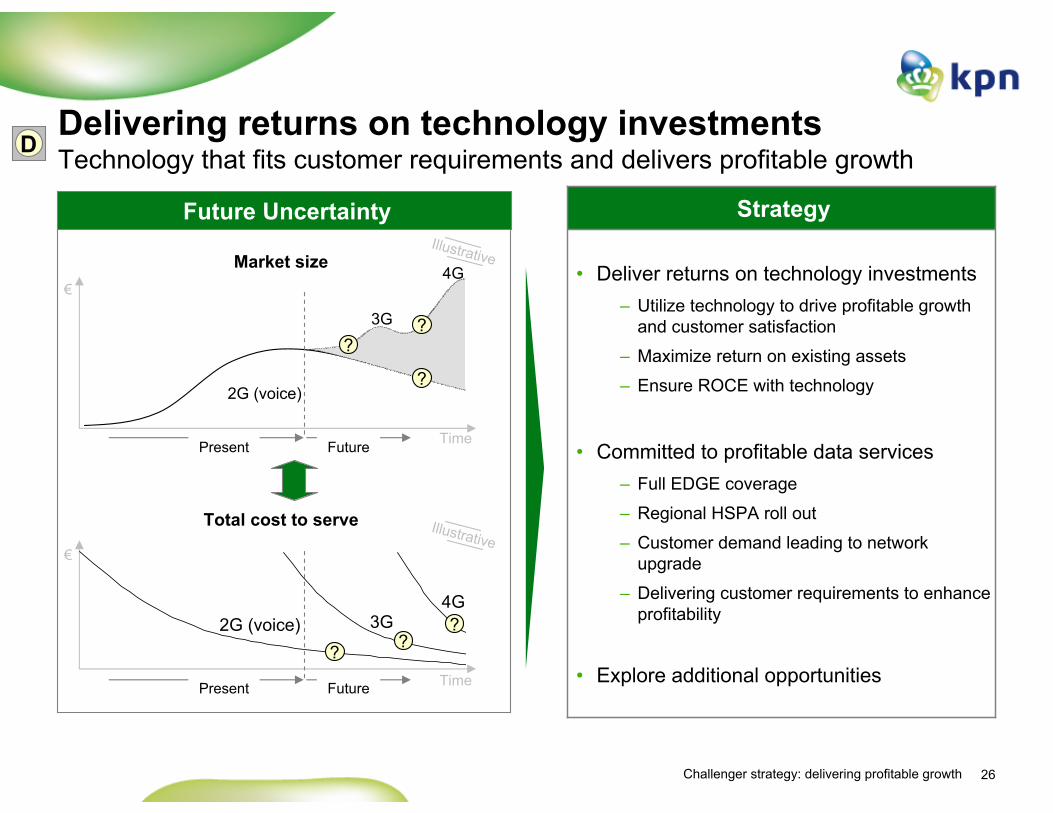

Delivering returns on technology investments Technology that fits customer requirements and delivers profitable growth

Future Uncertainty Illustrative

Total cost to serve

€

Present Future Time

Illustrative

2G (voice) 3G4G?

??

Market size€

Time

2G (voice)

4G

3G

Present Future

?

?

?

D

• Deliver returns on technology investments– Utilize technology to drive profitable growth

and customer satisfaction

– Maximize return on existing assets

– Ensure ROCE with technology

• Committed to profitable data services– Full EDGE coverage

– Regional HSPA roll out

– Customer demand leading to network upgrade

– Delivering customer requirements to enhance profitability

• Explore additional opportunities

Strategy

27Challenger strategy: delivering profitable growth

Addressable market

Enhanced segmentationCreeping up the value chain by selectively targeting SME / SoHo

• Mobile International currently playing for value for money segment of the market

• Selectively expanding addressable market through focused targeting

– Targeted offers on a selective regional basis– Seizing opportunity of increased price sensitivity

of customers due to economic slowdown– High quality voice/data (selective technologies)

• No interest in Corporate segment– Systems and processes prohibitively expensive

for Challenger– Margin / profitability for Challenger uncertain– Challenging and costly to enter

• Propositions and partners in place

Segmentation

Cus

tom

er ty

pes

Market

1

2

3

4

5

1: Pre Paid / MVNO2: Low Post Paid / MVNO3: High Post Paid

4: SME / SoHo5: Corporate

100%0%Currently addressedTarget segments/ regions

Illustrative

28Challenger strategy: delivering profitable growth

PortfolioSelectively exploring value enhancing opportunities

• Selectively exploring

• Will only do value creating investments

• No value enhancing opportunities identified

‘Asset heavy’expansion

Going forwardAchievements

• Management focus on core operations (Germany / Belgium)

• Further expansion from position of strength in Spain and France

• Exploring selective value enhancing opportunities

• Distribution strengthened– E.g. SMS Michel, Allo Telecom

• MVNO with segment focus– E.g. Ortel, blau

Core markets‘Fill-in’

acquisitions

• Successfully launched in Spain

• Successfully launched in France‘Asset light’expansion1

1 Expansion on network of foreign MNOs

29Challenger strategy: delivering profitable growth

Horizontalization

HorizontalizationLeverage successful brands, wholesale and infrastructure across markets

• International brands rolled-out across footprint based on proven business model

• Wholesale as vital intermediate to align international market trends and needs with infrastructure deployment. Long term relationship building with own brands and strategic partners

• Infrastructure (Network/IT) managed across markets to increase long term return on capital employed through optimizing scale via own brands and partners

International Wholesale

Network/IT

Current footprint

Mobile market size(€ bn)

2520224

30Challenger strategy: delivering profitable growth

Our achievements1

+68%

+124%

+ 9%-pts

+ 78%

+ 28%

Change

23.4 mn13.9 mnCustomers

€ 942 mn€ 420 mnCash flow2

36%27%EBITDA margin

€ 1.6 bn€ 0.9 bnEBITDA

€ 4.1 bn€ 3.2 bnService revenues

20082005

1 Based on old management structure, including Wholesale NL and Sympac for ’07-’082 Cash Flow defined as EBITDA minus Capex

31Challenger strategy: delivering profitable growth

Concluding remarks

• We have delivered on our promises

• Challenger strategy works

• Confident that our strategy will continue to work in the future

• Strong and proven track record in managing challenges

• Continue to deliver shareholder value

32Challenger strategy: delivering profitable growth

Agenda

Eric Hageman, CEO International WholesaleInternational Wholesale

Stan Miller, CEO KPN Mobile InternationalConcluding remarks

Thorsten Dirks, CEO E-PlusE-Plus

Erik Hoving, CTO KPN Mobile International KPN Group Belgium

Eric Hageman, CFO KPN Mobile InternationalFinance

Stan Miller, CEO KPN Mobile InternationalStrategy

Marc van Asbroeck, Chief Legal & RegulationRegulation

Ad Scheepbouwer, Chairman and CEO KPNIntroduction

33Challenger strategy: delivering profitable growth

Mobile International Key FY 2008 financials per country1

Rest of WorldGermany Belgium

Revenue € 3.2 bnEBITDA € 1.2 bnEBITDA margin 38.7%Market share2 15.4%Customers 18 mn

Revenue € 0.8 bnEBITDA € 0.3 bnEBITDA margin 32.5%Market share2 >16%Customers 3.5 mn

1 Based on the new reporting structure as per Q1’092 Market share based on wireless service revenues

Revenue € 73 mnEBITDA -/-€ 23 mnEBITDA margin -/-31.5%Leading MVNOCustomers 0.2 mn

34Challenger strategy: delivering profitable growth

Business turnaroundSignificant value creation, amongst most profitable # 3 operators

BASE E-Plus

2002

• Market underperformance• Liability instead of asset• EBITDA: € 10 mn• EBITDA margin: 3.2%• Cash flow1: -/- € 134 mn

• Market underperformance• Value of < € 5 bn• EBITDA: € 673 mn• EBITDA margin: 23.8%• Cash flow1: € 272 mn

• Market outperformance• EBITDA: € 240 mn (+€ 230 mn)• EBITDA margin: 37.1% (+34%-pts)• Cash flow1: € 131 mn (+€ 265 mn)

• Market outperformance• EBITDA: € 1,245 mn (+€ 572 mn)• EBITDA margin: 38.7% (+15%-pts)• Cash flow1: € 731 mn (+€ 459 mn)

2008 2008

Robust business model, amongst most profitable # 3 operators

2005

1 Cash flow defined as EBITDA minus Capex

Challenger strategyChallenger strategy

35Challenger strategy: delivering profitable growth

Financial performance1

Continued profitable growth with strong cash flow through Challenger model

EBIT

DA

(m

argi

n)Se

rvic

e re

venu

es

1,5981,4541,276946

27%33% 37% 36%

2005 2006 2007 2008

EBITDA margin / CF Conversion

4,1403,7863,6093,199

2005 2006 2007 2008

5%9%

19%

9%

Cas

h Fl

ow2

1 Based on old management structure, including Wholesale NL and Sympac for ’07-’082 Cash Flow defined as EBITDA minus Capex

13%

942877661

420

44%52%

60% 59%

2005 2006 2007 2008

33% 7%57%

Y-o-Y growth

31%

• Continued market outperformance

– Strong service revenue growth at 9% CAGR

• Focus on profitable growth

– Leading EBITDA growth of 19% CAGR

• Smart follower investments

– 31% average annual growth in cash flow

CAGR ’05 – ’08

14% 10%35%

36Challenger strategy: delivering profitable growth

Share price evolution1

2

4

6

8

10

12

14

Value creation Challenger model with clear focus on value creation

Challenger strategy

Jun 20092003 2005

€• Attractive customer propositions• Established multi-brand strategy and MVNOs• Distribution from push to pull• Simplified operations, outsourced where possible

BASE2003

• Differentiated offer with multi-brands• Focus on customer segments and wholesale growth• Efficient distribution e.g. SIM-only, outsourcing• Efficiency through smart follower for new technology

E-Plus2005

• First-mover to tap attractive market segment• Leveraged wholesale partners across footprint• Prepared International MVNO roll-out

Wholesale2007

KPN Dow Jones Telco Index

1 Dow Jones Telco rebased to KPN share price of € 6.08 at 1 January 2003

37Challenger strategy: delivering profitable growth

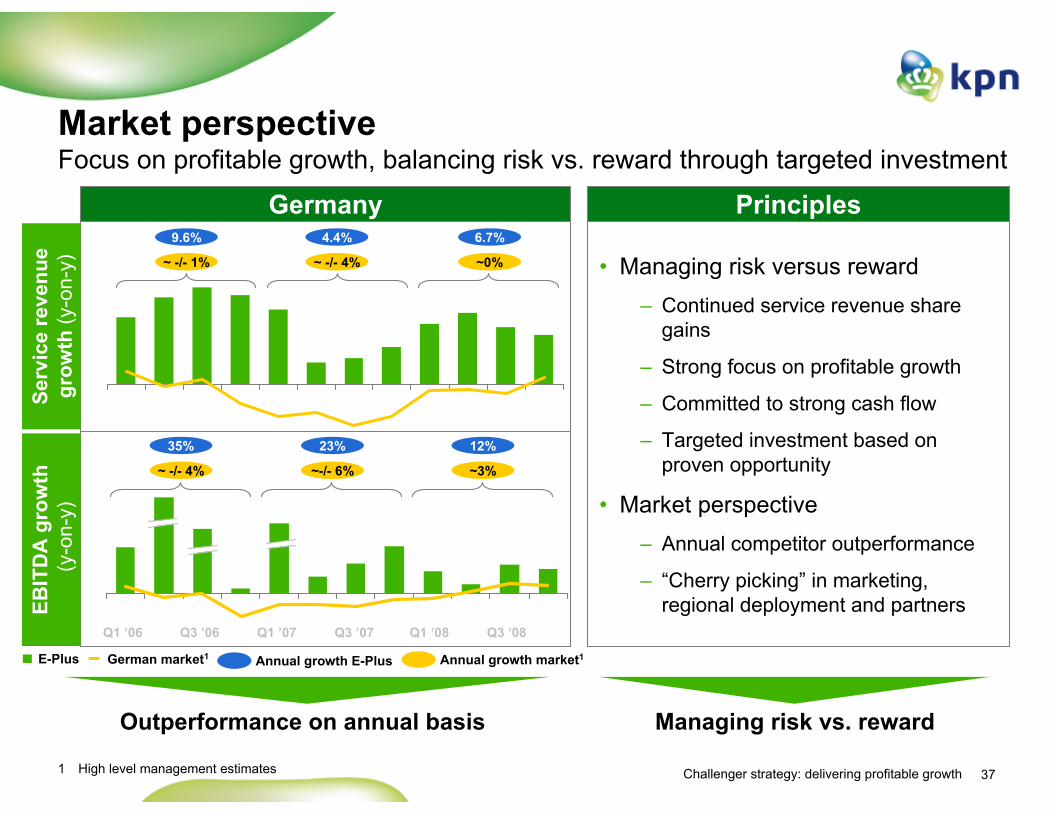

Market perspectiveFocus on profitable growth, balancing risk vs. reward through targeted investment

Germany Principles

• Managing risk versus reward– Continued service revenue share

gains

– Strong focus on profitable growth

– Committed to strong cash flow

– Targeted investment based on proven opportunity

• Market perspective– Annual competitor outperformance

– “Cherry picking” in marketing, regional deployment and partners

E-Plus German market1

Serv

ice

reve

nue

grow

th (y

-on-

y)

Q1 ’06 Q3 ’06 Q1 ’07 Q3 ’07 Q1 ’08 Q3 ’08

Managing risk vs. reward

1 High level management estimates

EBIT

DA

gro

wth

(y-o

n-y)

Outperformance on annual basis

6.7%9.6% 4.4%

12%35% 23%

Annual growth E-Plus Annual growth market1

~ -/- 4% ~-/- 6% ~3%

~ -/- 1% ~ -/- 4% ~0%

38Challenger strategy: delivering profitable growth

Macro-economic environment Various initiatives to proactively address changing economic environment

GDP % growth

Unemployment %

Source: International Monetary Fund

• Economic impact mainly on corporate market

– Little exposure for Int’l, no corporate presence

• Early signs of downturn in consumer market

– Less roaming due to less international travelling

– Customers optimizing within bundle

Limited impact

Proactive actions

• Strong positioning of value for money brands

• Propositions for ‘low income’ and unemployed

• Contingency plans for (MVNO) partnerships

• Selective marketing, low cost communication5%

10%

15%

20%

2005 2006 2007 2008 2009E 2010E

Germany Belgium Spain France

-6%

-4%

-2%

0%

2%

4%

2005 2006 2007 2008 2009E 2010EGermany Belgium Spain France

39Challenger strategy: delivering profitable growth

PrioritiesEffective execution to manage risks and maximize opportunities

• Optimizing international portfolio, focus on core assets & key strengths– Asset lifecycle management e.g. Sympac, Wholesale NL– Entry into new markets Spain and France with low cost MVNO model

• Selective “add-on” acquisitions to strengthen business profile– Strengthen distribution e.g. Allo Telecom, SMS Michel– Strengthen position in specific segments, e.g. Ortel, blau

• Clear governance structure with defined roles and responsibilities• Strengthen governance new entities, integration within Mobile International

– Right balance between entrepreneurial spirit vs. part of international organization

• Clear country focus with Germany, Belgium and Rest of the World• Ensure continuous insight available on key business metrics & aspects

• Ensure the right people are in the right place (people allocation)• Allocate investments to the right projects (capital allocation)

Portfolio

Governance

‘Reporting’

M&A

Allocation

• Manage risk versus reward– Continued service revenue share gains, with strong focus on profitability & cash flow– Targeted investment based on proven opportunity

Principles

40Challenger strategy: delivering profitable growth

Concluding remarks

• Leading Challenger & amongst most profitable # 3 operators

• Significant value created through Challenger model

• Committed to continued outperformance through profitable growth

• Proactively addressing / exploiting changing economic environment

• Effective execution to manage risks and maximize opportunities

41Challenger strategy: delivering profitable growth

Agenda

Eric Hageman, CEO International WholesaleInternational Wholesale

Stan Miller, CEO KPN Mobile InternationalConcluding remarks

Thorsten Dirks, CEO E-PlusE-Plus

Erik Hoving, CTO KPN Mobile International KPN Group Belgium

Eric Hageman, CFO KPN Mobile InternationalFinance

Stan Miller, CEO KPN Mobile InternationalStrategy

Marc van Asbroeck, Chief Legal & RegulationRegulation

Ad Scheepbouwer, Chairman and CEO KPNIntroduction

42Challenger strategy: delivering profitable growth

Key messages

• We use regulation competitively to improve our strategic position

• We strive for change because we have the flexibility and capability to use it for our good

• Regulation determines or restricts the telecoms sector, but as a Challenger we have used it to our benefit

43Challenger strategy: delivering profitable growth 43

Regulatory playing field in 2003European Challengers disadvantaged on all issues

• Abuse of dominance: not all parts of the market accessibleOverall

Regulatory strategy implemented to create level playing field

• Competitive issue at the wholesale level (alliances)Roaming

• Discrimination of 900 vs. 1800 MHzSpectrum

• Push towards symmetrical rates at high level (beneficial for incumbent)MTA

• Structural imbalance between first entrants and later entrants

• Political unwillingness to create regulatory level playing field

• Challengers have no weight in policy discussions

Regulatory playing field

Issues 2003

-/-

-/-

-/-

-/-

-/-

-/-

-/-

-/-

-/-

-/-

-/-

-/-

-/-

-/-

44Challenger strategy: delivering profitable growth 44

Market dynamics before Challenger strategyFailed implementation of the regulatory framework reinforced status quo

Market imbalance No market dynamics

• Special & exclusive rights enjoyed by first entrants

• Discrimination on frequencies

• Abuse of dominant position by first entrants

• Challengers’ aim to changing the regulatory playing field not heard

3%10% 13% 13% 13%

97%90% 87% 87% 87%

0%

20%

40%

60%

80%

100%

1999 2000 2001 2002 2003

9% 10% 12% 12% 12%

91% 90% 88% 88% 88%

0%

20%

40%

60%

80%

100%

2000 2001 2002 2003 2004M

arke

t rev

enue

shar

eM

arke

t rev

enue

shar

e

KPN Group BelgiumOther players

E-PlusOther players

Germany

Belgium

45Challenger strategy: delivering profitable growth

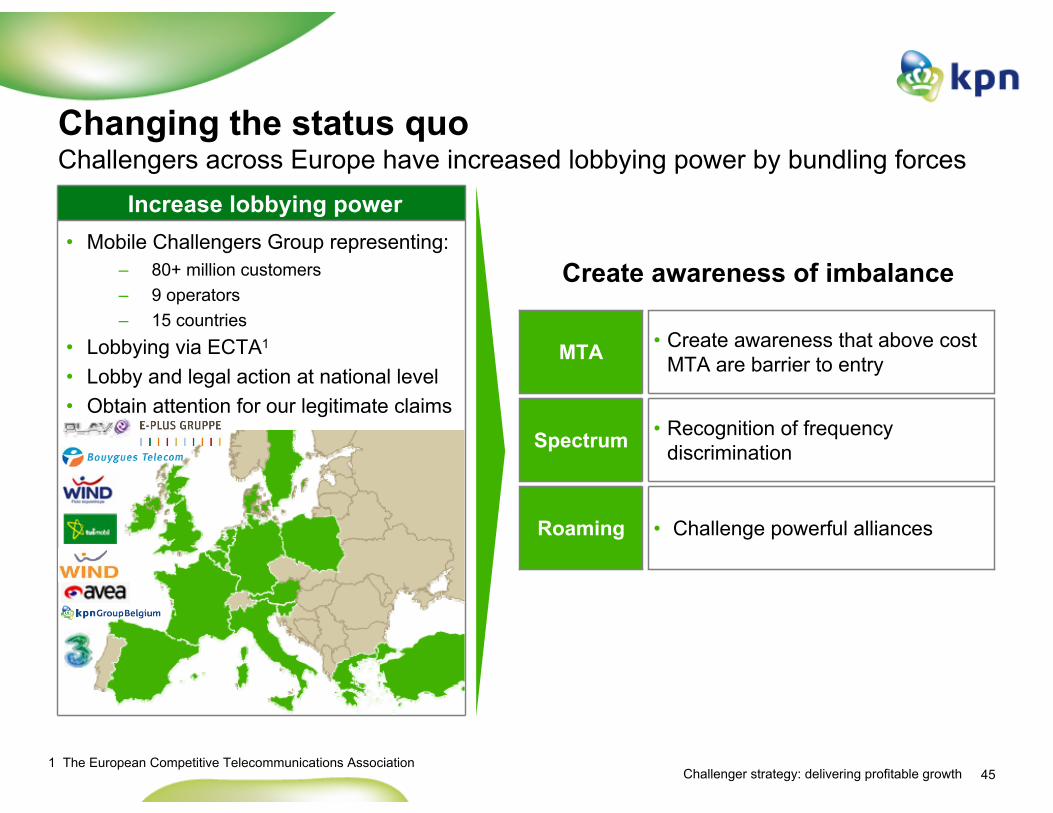

Changing the status quoChallengers across Europe have increased lobbying power by bundling forces

Increase lobbying power• Mobile Challengers Group representing:

– 80+ million customers– 9 operators – 15 countries

• Lobbying via ECTA1

• Lobby and legal action at national level• Obtain attention for our legitimate claims

1 The European Competitive Telecommunications Association

• Challenge powerful alliancesRoaming

• Recognition of frequency discriminationSpectrum

• Create awareness that above cost MTA are barrier to entryMTA

Create awareness of imbalance

46Challenger strategy: delivering profitable growth 46

MTA discussionChallengers demand asymmetry as logical outcome of scale differences

• Recognition that above cost MTAs are barriers for Challengers• Germany: some asymmetry has been maintained, while BNetZa wanted to abolish

it already in 2007• Belgium: suspension / annulment BIPT decision imposing symmetric rates

– Asymmetry increased in 2008

Status

• Asymmetrical glide path through minimizing the incumbent MTA– Removing the on-net effect– Removing the possibility of a price squeeze between MTA and (corporate) retail prices– Taking away excessive profits of large operators which they use against Challengers in

retail• Create level playing field

Goal

• Symmetry at high level as objective• Challengers not heard• German self-regulation is effectively a pseudo cartel

Issue

Commissioner Kroes on MTR recommendation: ‘The competition distortions are very real in the current situation. Smaller operators are at particular risk of being unfairly squeezed out of the market.’…. ‘The incumbents are using the termination market as a ‘cash cow’.’

47Challenger strategy: delivering profitable growth

• Enforce national asymmetric decrease during next years (via courts, incl. EU)

• Enforce Fixed-to-Mobile regulation to avoid competitive distortion

• Accepted arguments:– MTA is anti-competitive– Incumbents abuse MTA– Brussels court decision

on BIPT MTA

• New arguments:– Methodology is wrong– Discrimination– EU case law– Fixed-to-Mobile

Historic developments & going forwardProposal

0.05

0.10

0.15

0.20

0.25

47

MTA development & proposalEnforce immediate further decrease of first entrants’ MTA

0.05

0.10

0.15

0.20

BASEMobistarProximus

O2 & E-PlusT-Mobile & Vodafone€

€

Germany

Belgium2004 2010

2004 2009

Illustrative

2010

ChallengerIncumbentChallenger proposal

48Challenger strategy: delivering profitable growth

SpectrumMarket imbalance from discrimination being repaired

• Lobby for re-distribution in Germany, Belgium equal distribution of frequencies

Belgium:• 900-1800 MHz discrimination

recognized by regulator– Feb 2009: additional 900 MHz

frequencies awarded to KPN Group Belgium on a conditional basis

– Draft Royal Decree provides for more extensive frequency refarming as of 2011 or 2013

• Spectrum allocation now fairly balanced (although BASE still has fewer 900 MHz frequencies)

Germany: • 900 MHz frequencies received in 2006

– However still disadvantaged position in 900 MHz frequency band (5 MHz versus 12.5 MHz allocated to T-Mob and VOD)

• Re-distribution of 900 MHz spectrum prior to refarming of 900 MHz band

or• E-Plus and O2 get more frequencies in

800 MHz band than competitors

• Review of the GSM Directive, managed to get resolution on competitive aspects of frequency refarming (Reding)

• 900-1800 MHz discrimination between incumbents and Challengers

EU

Status

Issue

Goal

49Challenger strategy: delivering profitable growth

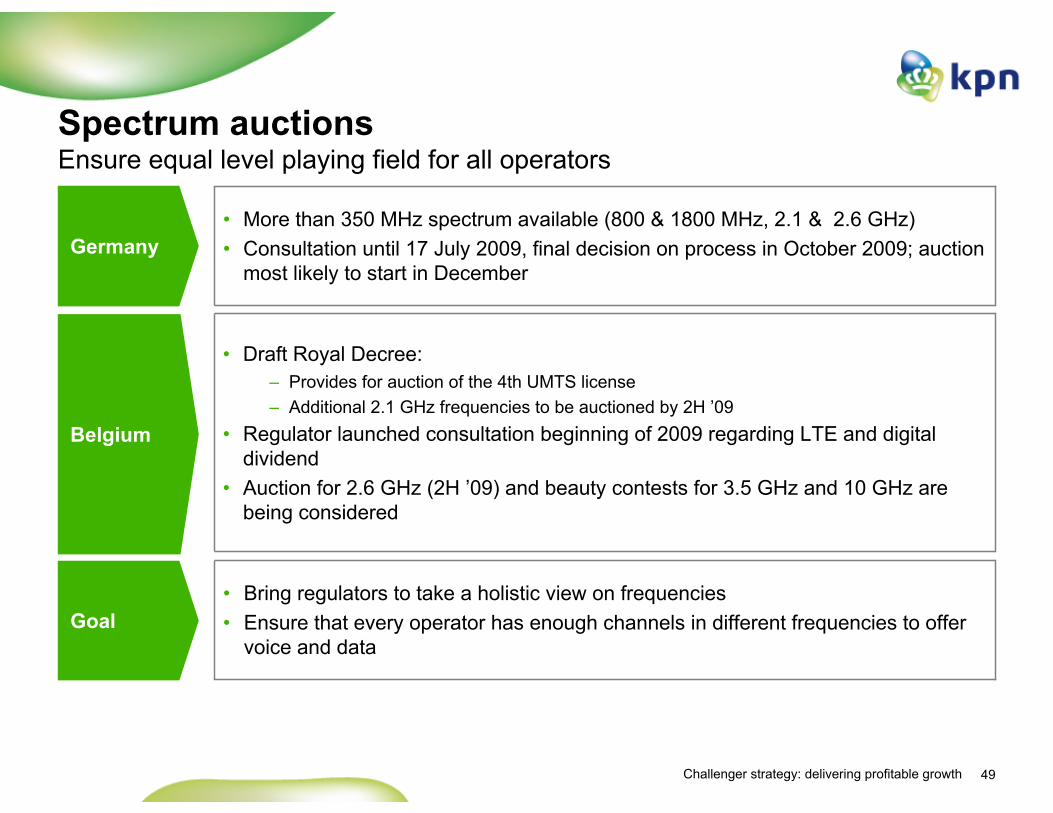

Spectrum auctionsEnsure equal level playing field for all operators

• Bring regulators to take a holistic view on frequencies • Ensure that every operator has enough channels in different frequencies to offer

voice and data

• Draft Royal Decree: – Provides for auction of the 4th UMTS license– Additional 2.1 GHz frequencies to be auctioned by 2H ’09

• Regulator launched consultation beginning of 2009 regarding LTE and digital dividend

• Auction for 2.6 GHz (2H ’09) and beauty contests for 3.5 GHz and 10 GHz are being considered

• More than 350 MHz spectrum available (800 & 1800 MHz, 2.1 & 2.6 GHz)• Consultation until 17 July 2009, final decision on process in October 2009; auction

most likely to start in DecemberGermany

Belgium

Goal

50Challenger strategy: delivering profitable growth

Roaming Different approach from incumbent operators

Roaming price caps in EU countries (€ ct / min or SMS, without VAT)

5080100n.a.n.a.Data roaming / MB

11n.a.n.a.Outgoing SMS

4n.a.n.a.SMS wholesale

1115192224Incoming calls

3539434649Outgoing calls

1822262830Wholesale rates

1 July 20111 July 20101 July 200930 August 200830 August 2007Effective as from

• Roaming alliances between large incumbents unfavourable for Challengers• KPN group companies squeezed in (corporate) retail market due to high

roaming wholesale rates • KPN not in favour of retail regulation• Ongoing lobby on the wholesale issue

51Challenger strategy: delivering profitable growth 51

Legal casesPending cases in support for Challengers

• Two complaints filed with BNetzA (no action)• Relevant market deregulated by BNetzA• Further action will be taken by E-Plus

Deutsche Telekom

F2M

• Court order against Belgacom to pass on MTA reduction• € 3 mn fine imposed by BIPT• Market still regulated with approval of Commission

BelgacomF2M

• Complaint with Commission – Bundeskartellamt• Collusion and abuse of joint dominance (on-net)• Case being investigated

T-Mobile &

Vodafone

• Price squeeze in corporate market (retail vs. MTA)• Dawn raid – prosecutor’s report: 5 indictments• € 66.3 mn fine imposed by Belgian Competition Authorities

Proximuscorporate

• € 1 bn claim for abuse of on-net• Provisional judgment (on-net & price squeeze)• Experts appointed – report expected September 2009

Proximuson-net Support for our

overall positioning as Challengers

Support for MTA case

Support for business (access to new markets)

Possible damages

52Challenger strategy: delivering profitable growth 52

Half-time score regulatory playing field in 2009European Challengers have achieved movement in the regulatory field

• Abuse of dominance: not all parts of the market accessible Overall

Regulatory strategy has started to pay-off, more is in the pipeline

• Competitive issue at the wholesale level (alliances)Roaming

• Discrimination 900 vs. 1800 MHZSpectrum

• Push towards symmetrical rates at high level (beneficial for incumbent)MTA

• Structural imbalance between first entrants and later entrants

• Political unwillingness to create regulatory level playing field

• Challengers have no weight in policy discussions

Regulatory playing field

Issues 2003+

+ +

+

+ +

+

+ +

+ +

+

+

+

+

+

+ +

+

53Challenger strategy: delivering profitable growth

Agenda

Eric Hageman, CEO International WholesaleInternational Wholesale

Stan Miller, CEO KPN Mobile InternationalConcluding remarks

Thorsten Dirks, CEO E-PlusE-Plus

Erik Hoving, CTO KPN Mobile InternationalKPN Group Belgium

Eric Hageman, CFO KPN Mobile InternationalFinance

Stan Miller, CEO KPN Mobile InternationalStrategy

Marc van Asbroeck, Chief Legal & RegulationRegulation

Ad Scheepbouwer, Chairman and CEO KPNIntroduction

54Challenger strategy: delivering profitable growth

Introduction

• KPN Group Belgium is a success story

• Delivering profitable growth ahead of the market since 2003 by doing things differently

• Values underpinning Challenger strategy are transparency, simplicity and honesty

• Confident in continued outperformance whilst delivering profitable growth

54

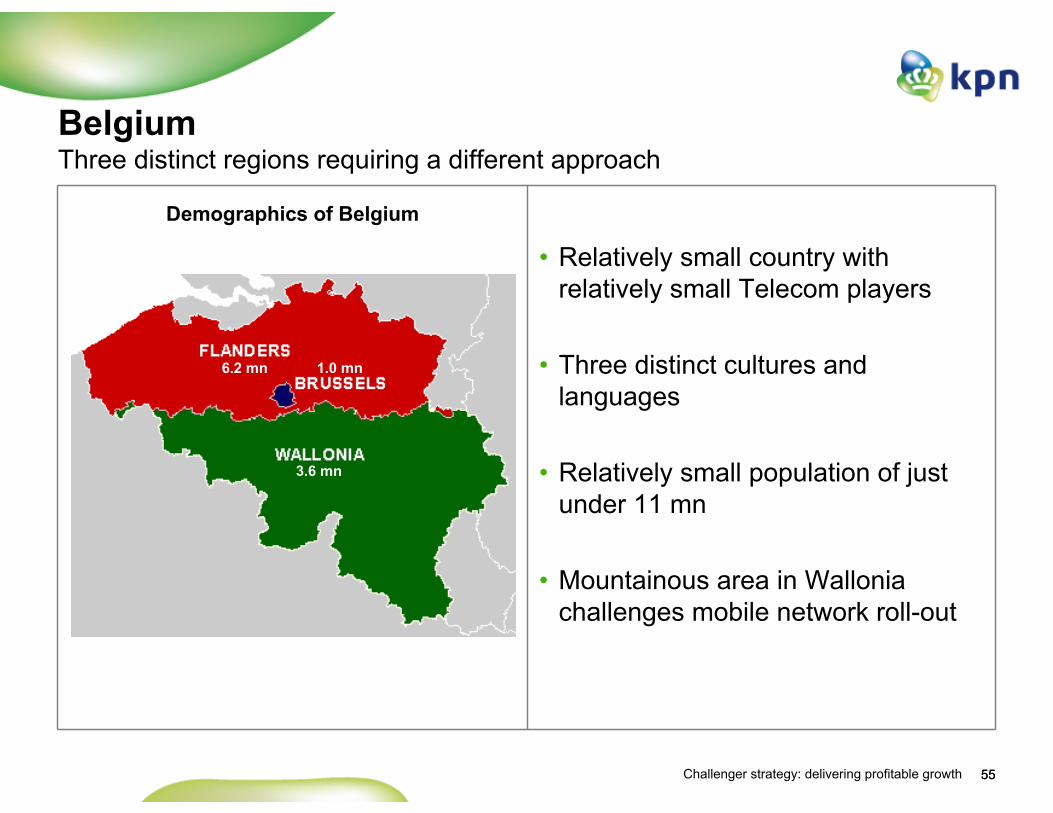

55Challenger strategy: delivering profitable growth 55

• Relatively small country with relatively small Telecom players

• Three distinct cultures and languages

• Relatively small population of just under 11 mn

• Mountainous area in Wallonia challenges mobile network roll-out

Demographics of Belgium

6.2 mn 1.0 mn

3.6 mn

BelgiumThree distinct regions requiring a different approach

56Challenger strategy: delivering profitable growth 56

Historic market trends in BelgiumRevenues stabilizing, continued growth in subscribers and minutes

• Belgium average price level is € 0.05 above European average

• Average usage at European average

• Continued growth in number of customers and minutes

– Driven by introduction of flat fees and aggressive promotions

– Increase in usage offset by regulation

Mobile Service revenues

Subscribers

€ bn

mn

3.32 3.74 3.99 4.04 3.89 3.83

2003 2004 2005 2006 2007 2008

+13%

8.2 8.8 9.2 9.8 11.0 12.1

2003 2004 2005 2006 2007 2008

Source: Equity research

MoU Belgium

147 151 153 155 157 160

2003 2004 2005 2006 2007 2008

+7% +1% -4% -2%

+7% +5% +7% +12% +10%

+3% +1% +1% +1% +2%

57Challenger strategy: delivering profitable growth

• Continued market outperformance with profitable growth

• Re-ignited growth in 2008 with positive impact of acquisitions

• Focus on Consumers, not Corporates

11.0%

33.7%29.7%

4.4% 6.5%

-2.3%

12.6%

-2% -1%

6%5%

7%

1%-4%

2003 2004 2005 2006 2007 2008 Q1 '09

KPN Group Belgium

14%

28%

37%42%

38% 37%

57

Performance KPN Group BelgiumContinued market outperformance on all key metrics

Customer growth

EBITDA and margin

mnService revenue growth (y-on-y)

204 240230264

11948

2003 2004 2005 2006 2007 2008EBITDA marginEBITDA

Belgian market

1.31.6

2.0

2.9

3.4

2.4

2003 2004 2005 2006 2007 2008

Source: Equity research and Company results

€ mn

58Challenger strategy: delivering profitable growth

Market shares 2003 Market shares 2008

58

Targeting 20-25% service revenue market share in next few yearsEBITDA margin of at least 35%

KPN Group Belgium going forwardConfident in continued outperformance in Belgium

+11%+7%+9%

KPN Group Belgium market share growth

70%60%

53%

27%31%

32%

3%9%15%

Customers Servicerevenues

EBITDA

51%49%45%

35%35%31%

14%16%24%

Customers Servicerevenues

EBITDA

59Challenger strategy: delivering profitable growth

Challenger strategyTactics for delivering profitable growth

Sample of some of the tactics

• Maximize return on existing assets

• Selective, low risk investments in new technology

• Expand voice target regions based on proven concept

• Monetize leading position in voice to build data position

• Leverage proven business models to new markets

• Build partnerships with new entrants

• Mobile share of voice on EU average, further upside

• Voice remains dominant over data for the next years

Smart technology

follower

Regionalization

Wholesale & Partnerships

Fixed-Mobile Substitution

A

B

C

D

Position around

customers

Create customer pull

Establish partnerships

Introduce profit-

maximizing value chains

Strategic cornerstones

60Challenger strategy: delivering profitable growth 60

Building BASE brand by transparent, simple and honest positioning

• BASE brand launched in 2002

• Maximizing brand awareness at lowest marketing costs

• Re-launch in April ’09 going back to values and with simplified tariff plans

• Sales force re-educated for simplification− Four simple questions to determine best

tariff plan for customer

• BASE positioning around customer− Best prices− Simple and easy comparison− Flexible options

Used mobile video booth to film ‘real’people and select new BASE faces

BASE re-launch campaign on partner TV and radio channels, using testimonials of real customers

A

61Challenger strategy: delivering profitable growth

DistributionStrong position in distribution via own channels in addition to wholesale partners

61

• Partner brands distributed via over 1,000 retail outlets in Belgium• Carrefour, Medion MobilePartners

Channels Comments

Shops• Number of shops up from 44 in 2005 to 54

shops in Q1 ’09 on AAA locations• Extending BASE experience• Focus on up-selling and servicing

• Acquisition of 63 shops on AA locations• Low-end acquisition allowing for

Pre Paid to Post Paid migration

• ~80% of shops in Wallonia• Increasing shop presence in ‘second

tier’ cities in Wallonia• Best deal / good handset prices

Chains • ThePhoneHouse / BelCompany • High-end acquisition with customers attracted by fanciest handsets

Dealers• Independent and small chains such as

local Telco or tobacco shops • Local network, cultural focus

Online• Currently only recharges• Talk plans under development

• Customers sensitive to price and convenience

A

62Challenger strategy: delivering profitable growth 62

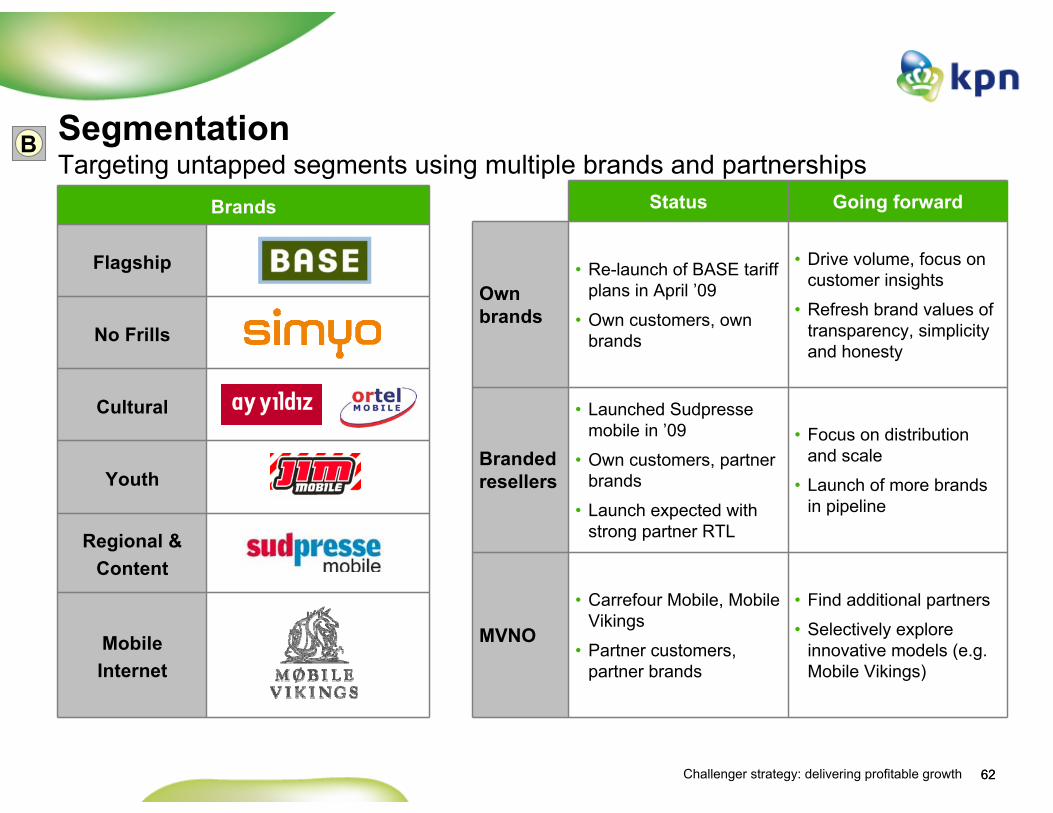

Segmentation Targeting untapped segments using multiple brands and partnerships

Status Going forward

Own brands

• Re-launch of BASE tariff plans in April ’09

• Own customers, own brands

• Drive volume, focus on customer insights

• Refresh brand values of transparency, simplicity and honesty

Branded resellers

• Launched Sudpressemobile in ’09

• Own customers, partner brands

• Launch expected with strong partner RTL

• Focus on distribution and scale

• Launch of more brands in pipeline

MVNO

• Carrefour Mobile, Mobile Vikings

• Partner customers, partner brands

• Find additional partners

• Selectively explore innovative models (e.g. Mobile Vikings)

Brands

Flagship

No Frills

Cultural

Youth

Regional & Content

Mobile Internet

B

63Challenger strategy: delivering profitable growth 63

Partnerships examples Targeting specific groups with brands familiar to the customer

• Partnership with VMMA since 2003

• Cheap SMS attracts young people, even in French (non-targeted) speaking part of country

• Solid growth: >500k customers; owned by KPN Group Belgium

• Centralised around ‘Joeri’ personality, created for brand recognition

• Leveraging on-net communities, e.g. high schools

Call for free during ‘party hours’ at weekends

• Partnership with RTL Belgium since March ’09, brand launch expected in mid 2009

• Strong partner in targeting Wallonia with trusted brand and competitive offer

• Access to mobile content of RTL TVI and Bel RTL

• Offer centered around ‘The world of RTL’

• Clear visibility of brand in own shops

B

64Challenger strategy: delivering profitable growth

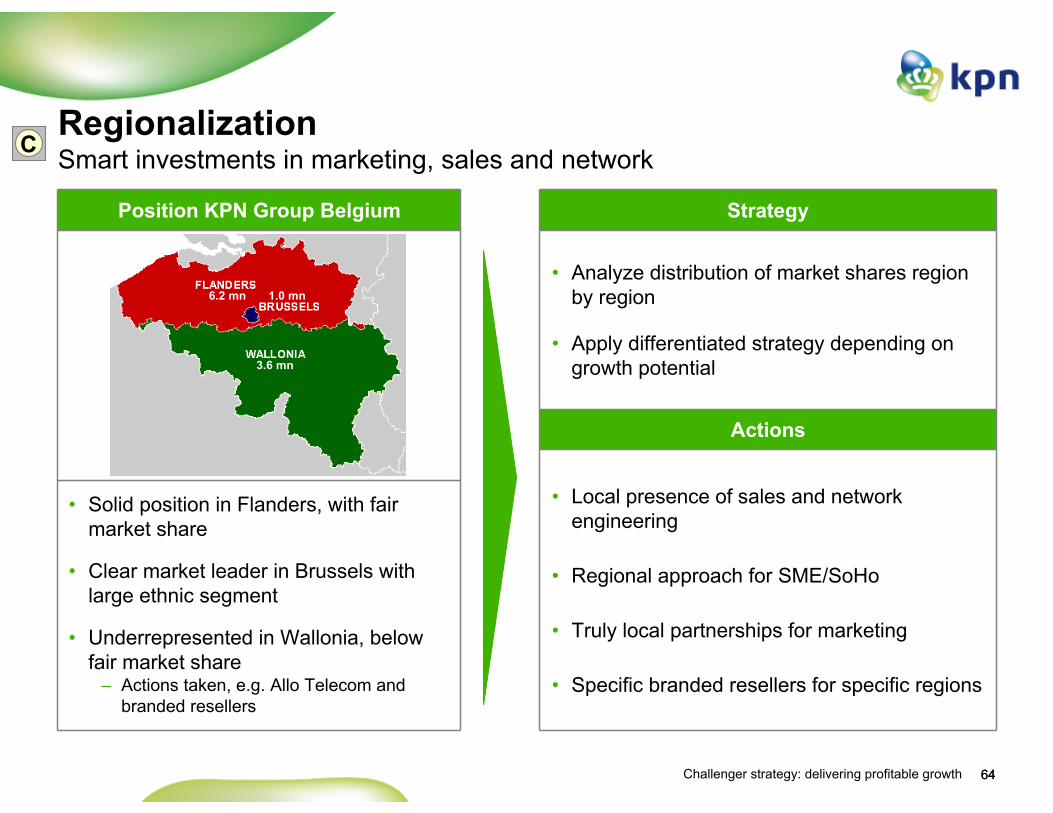

Position KPN Group Belgium

Regionalization Smart investments in marketing, sales and networkC

6.2 mn 1.0 mn

• Solid position in Flanders, with fair market share

• Clear market leader in Brussels with large ethnic segment

• Underrepresented in Wallonia, below fair market share

– Actions taken, e.g. Allo Telecom and branded resellers

3.6 mn

64

Strategy

• Analyze distribution of market shares region by region

• Apply differentiated strategy depending on growth potential

Actions

• Local presence of sales and network engineering

• Regional approach for SME/SoHo

• Truly local partnerships for marketing

• Specific branded resellers for specific regions

65Challenger strategy: delivering profitable growth

• Non-SMS data in Belgium lagging behind due to absence of handset subsidies resulting in slow uptake of expensive smart-phones

• EDGE covers large majority of consumer data need

• Network deployment EDGE / HSPA following expected handset uptake

Data development in BelgiumDelay in non-SMS data uptake and in 3G handset adaptation compared to EU

Non-SMS data as % of total market size

20082005

< 1% 6%

Handset development

0

25

50

75

100

2007 08 09 10 11 12 13

% h

ands

ets

(inst

alle

d ba

se)

HSPA

57%35%12%3G or better

UMTS

EDGE

GPRS

GSMonly

65

D

94%99%

43%65%88%EDGE or less

13E12E11E10E09E0807

Source: Industry research

66Challenger strategy: delivering profitable growth

Bandwidth needed for good mobile user experiences Comments

• Email, instant messaging, social networking account for 40 - 60% of data usage

• 10 - 20% of usage for Web-browsing, increasing due to improved devices

• KPN Group Belgium focuses on Consumers, not Corporates

66

64

256

32

512

128

512

512

2,048

3,072

E-mail (150KB attachment)

E-mail (2MB attachment)

Instant messaging

Web-browsing

Gaming

Audio streaming

Music download (track / CD)

Video clip download

Video streaming (SD / HD)

Compressed DVD download

256

1,024

8,192

EDGE UMTS HSPA LTE

Mobile data applicationsEDGE currently sufficient for majority of applications used by consumersD

Source: Industry research

EDGE bandwidth currently sufficient for majority of consumer applications

(kB)

67Challenger strategy: delivering profitable growth

Selective roll-out of data network Network roll-out based on those services that consumers want

Strategy Technology Approach

• Smart follower in wireless data– KPN Group Belgium targeting consumer and SME /

SoHo segments with value offers– Combination of EDGE and targeted HSPA sufficient

to meet demand of mass market

• Phased data network roll-out in Belgium– National EDGE coverage meets current data demand– Efficiently deploy UMTS to meet license requirements– HSPA in hot-spots with strong demand

• Regulatory development– Potential regulation on signal strength delayed– Spectrum increased with additional frequencies by

government

EDGE

• National GPRS / EDGE coverage in place

• Best coverage in 3 out of 5 regions

HSPA• Roll-out where demand

exists• Leading coverage in focus

cities and key hotspots

67

D

Smart technology follower

68Challenger strategy: delivering profitable growth

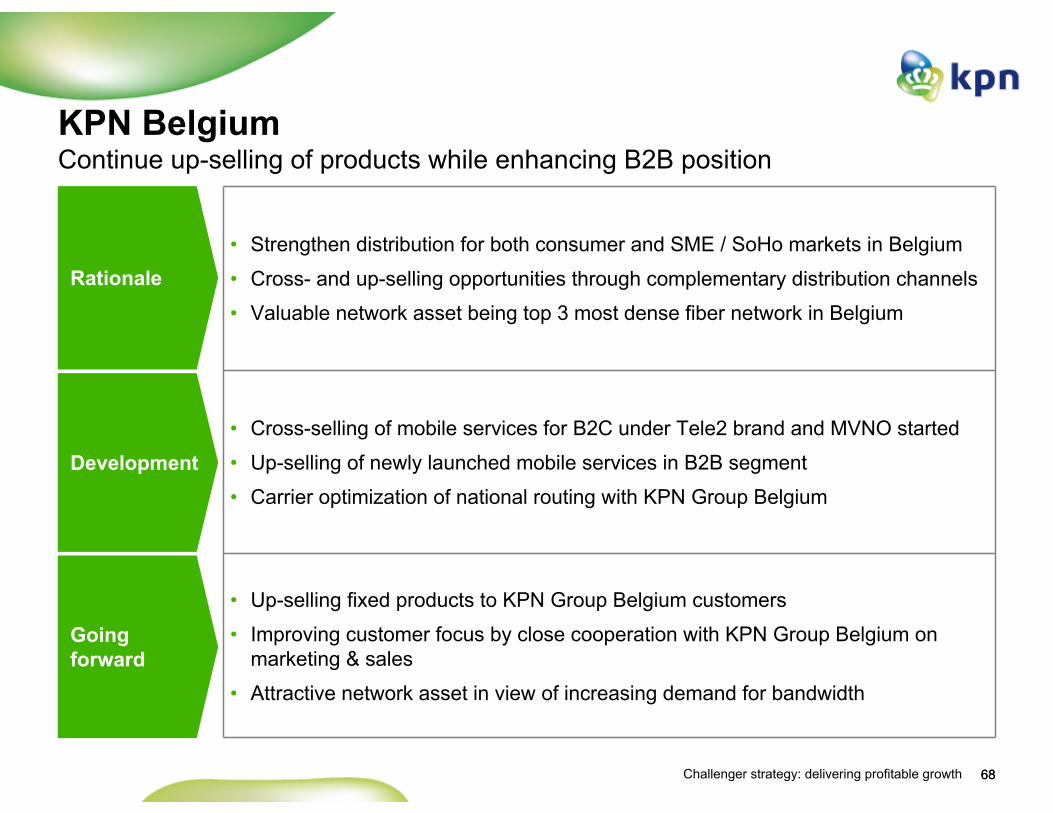

• Strengthen distribution for both consumer and SME / SoHo markets in Belgium

• Cross- and up-selling opportunities through complementary distribution channels

• Valuable network asset being top 3 most dense fiber network in Belgium

• Cross-selling of mobile services for B2C under Tele2 brand and MVNO started

• Up-selling of newly launched mobile services in B2B segment

• Carrier optimization of national routing with KPN Group Belgium

• Up-selling fixed products to KPN Group Belgium customers

• Improving customer focus by close cooperation with KPN Group Belgium on marketing & sales

• Attractive network asset in view of increasing demand for bandwidth

Rationale

Development

Going forward

KPN BelgiumContinue up-selling of products while enhancing B2B position

68

69Challenger strategy: delivering profitable growth

Concluding remarks

• Delivering profitable growth ahead of the market since 2003

• Continue to focus BASE brand on transparency, simplicity and honesty

• Targeting untapped segments using multiple brands and wholesale partnerships

• Strong position in distribution via own channels in addition to wholesale partners

• Smart technology follower, HSPA network roll-out where demand exists

• Confident in continued outperformance, clear focus on EBITDA and cash flow– Targeting 20-25% service revenue market share in next few years– EBITDA margin of at least 35%

69

70Challenger strategy: delivering profitable growth

Agenda

Eric Hageman, CEO International WholesaleInternational Wholesale

Stan Miller, CEO KPN Mobile InternationalConcluding remarks

Thorsten Dirks, CEO E-PlusE-Plus

Erik Hoving, CTO KPN Mobile International KPN Group Belgium

Eric Hageman, CFO KPN Mobile InternationalFinance

Stan Miller, CEO KPN Mobile InternationalStrategy

Marc van Asbroeck, Chief Legal & RegulationRegulation

Ad Scheepbouwer, Chairman and CEO KPNIntroduction

71Challenger strategy: delivering profitable growth

Key messages

• Delivering profitable growth ahead of the market since 2005

• Further upside potential for proven Challenger strategy

• Strong position in both wholesale and retail segments

• Leveraging potential of regional approach

• Best value-for-money proposition for mobile data

72Challenger strategy: delivering profitable growth

Historic market trends in GermanyMarket growth almost flat, continued growth in subscribers

• Continued growth in number of customers and minutes

– Driven by Fixed-Mobile substitution– Usage still below European average

• Historic market growth in Germany mid-single digit decline to flat

– Increase in usage offset by regulation

Revenues mobile telecommunications services

Total minutes

Subscribers

€ bn bn

mn

23.1 22.6 22.1 22.1

2006 2007 2008 2009

-2% -2% flat

86 97 107 110

2006 2007 2008 2009

13%10% 3%

5776 84 90

2006 2007 2008 2009

33%11%

7%

1 Management estimates for 2009

1

1

1

73Challenger strategy: delivering profitable growth

Performance E-PlusContinued market outperformance on all key metrics

SAC / SRCEBITDA and margin€ mn €

Service revenue growth

4.1%6.7%

4.4%

9.6%

4.3%

-1%-4%

0% 0%

4%

2005 2006 2007 2008 Q1 '09German market1E-Plus

1 Management estimates

18.017.814.8

12.710.7

2005 2006 2007 2008 Q1 '09

Customer basemn

Average18% growth/yr

322

1,2451,113905

673

31.3%37.6% 38.7% 41.6%

23.8%

2005 2006 2007 2008 Q1 '09

525276

90

148

2005 2006 2007 2008 Q1 '09

Down 65% since 2005

74Challenger strategy: delivering profitable growth

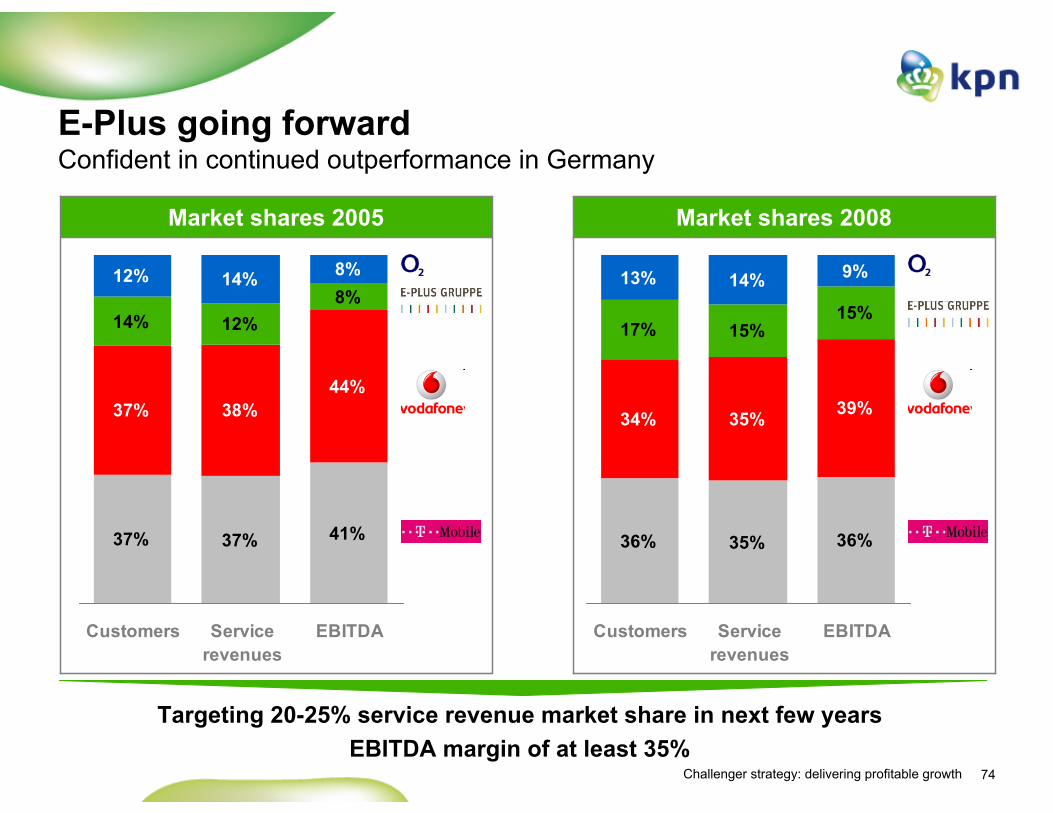

Market shares 2008Market shares 2005

E-Plus going forwardConfident in continued outperformance in Germany

37% 37% 41%

37% 38%44%

14% 12%8%

12% 14% 8%

Customers Servicerevenues

EBITDA

36% 35% 36%

34% 35% 39%

17% 15%15%

13% 14% 9%

Customers Servicerevenues

EBITDA

Targeting 20-25% service revenue market share in next few yearsEBITDA margin of at least 35%

75Challenger strategy: delivering profitable growth

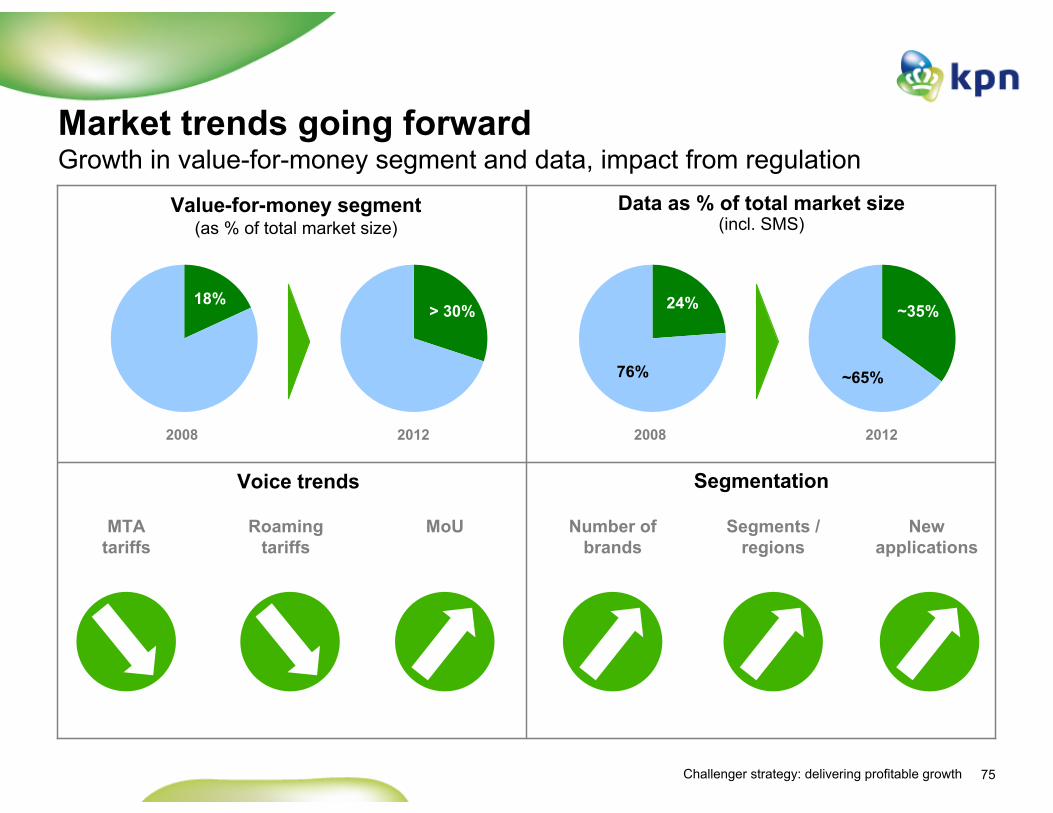

Market trends going forwardGrowth in value-for-money segment and data, impact from regulation

Data as % of total market size(incl. SMS)

Value-for-money segment(as % of total market size)

SegmentationVoice trends

2012

MTAtariffs

Roaming tariffs

MoU Number of brands

Segments / regions

New applications

2008

18%> 30%

20122008

24% ~35%

76% ~65%

76Challenger strategy: delivering profitable growth

Challenger strategyTactics for delivering profitable growth

Sample of some of the tactics

• Maximize return on existing assets

• Selective, low risk investments in new technology

• Expand voice target regions based on proven concept

• Monetize leading position in voice to build data position

• Leverage proven business models to new markets

• Build partnerships with new entrants

• Mobile share of voice still low, significant untapped potential

• Voice remains dominant over data for the next years

Smart technology

follower

Regionalization

Wholesale & Partnerships

Fixed-Mobile Substitution

A

B

C

D

Position around

customers

Create customer pull

Establish partnerships

Introduce profit-

maximizing value chains

Strategic cornerstones

77Challenger strategy: delivering profitable growth

• Rapid growth in data traffic, on top of continued growth in SMS per user

• Stimulated by flat rate offers for ‘light’data

Data

• Usage growth driven by attractive pricing and Fixed-Mobile substitution

• No-frills offers and on-net offersPre Paid

• Usage above market average• Flat rate offers, no-frills offers and on-

net offersPost Paid

Fixed-Mobile substitution Usage above market average, driven by Fixed-Mobile substitution

135 192 252 281 281

2005 2006 2007 2008 Q1 '09

Minutes of Usemin

Minutes of Usemin

Data traffic (excl. SMS)data volume

2005 2006 2007 2008 2009

+70%

+260%1100%

A

21 32 45 55 60

2005 2006 2007 2008 Q1 '09

78Challenger strategy: delivering profitable growth

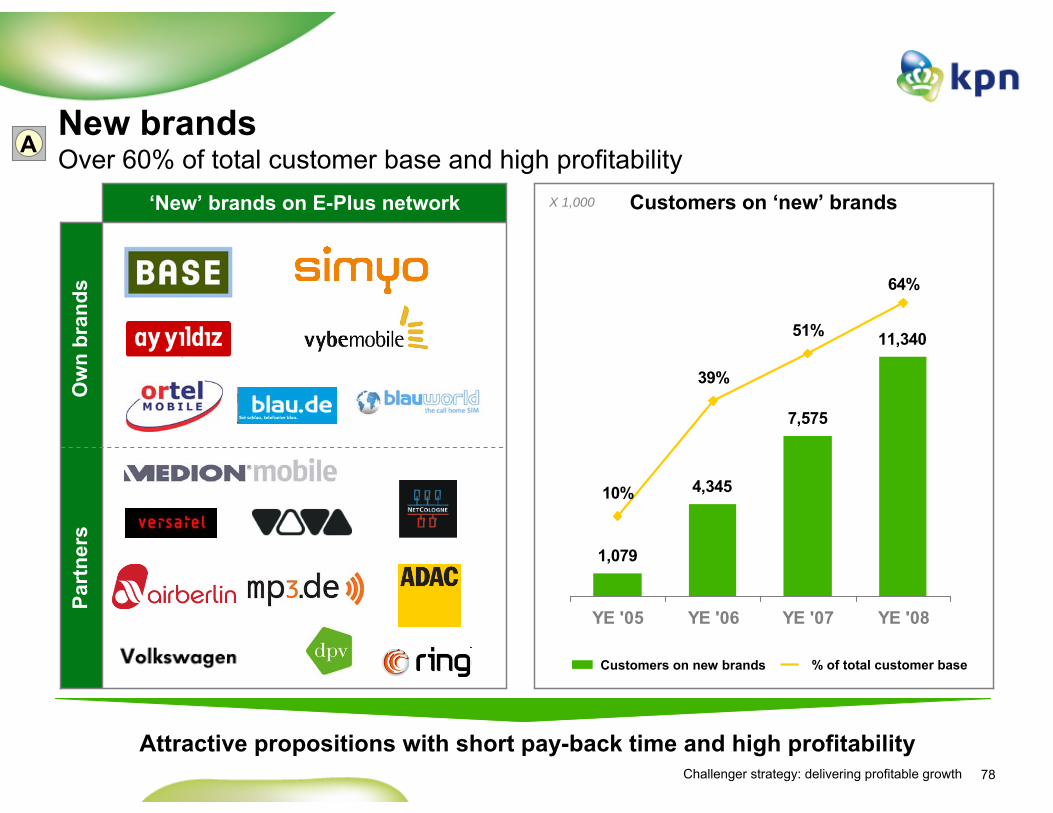

‘New’ brands on E-Plus network

New brandsOver 60% of total customer base and high profitability

Customers on ‘new’ brandsX 1,000

11,340

7,575

4,345

1,079

10%

39%

51%

64%

YE '05 YE '06 YE '07 YE '08

% of total customer baseCustomers on new brands

Attractive propositions with short pay-back time and high profitability

Ow

n br

ands

Part

ners

A

79Challenger strategy: delivering profitable growth

Leading flat rate brand in Germany

• Germany’s first mobile flat rate offer, introduced in 2005

• Still the only “flat-rate only” brand in the market

• Customer retention program “Freundeskreis”

– Community build-up via own website, special events and offers

• Point-of-sale experience

• Welcome package (BASE box)

• Premium proposition with BASE Gold

A

80Challenger strategy: delivering profitable growth

Germany’s first online no-frills brand

• Germany’s first online-only no-frills brand

– Online-only and Pre Paid only

• Best-in-class voice and data price in discount segment

• Community build-up via online platform– “Godfather” customer service idea– Viral campaign– Blog and forum communication

• High level of customer satisfaction and strong net promotor score

• Preferred brand in German online discount segment according to consumer research

A

81Challenger strategy: delivering profitable growth

• Net Promotor Score (NPS) for E-Plus brands substantially higher than competitor brands

– Customers that would recommend product to others

– Relatively few customers not satisfied with service

• Result of E-Plus offering tariffs and services that meet customer needs

• High customer satisfaction supporting community build-up

Customer satisfactionCustomer satisfaction substantially above market average A

Customer satisfaction(Net promotor score, NPS)

very satisfied not satisfied

Best Competitor

Source: E-Plus Gruppe, 2008

5460

51

44

64 3

5

82Challenger strategy: delivering profitable growth

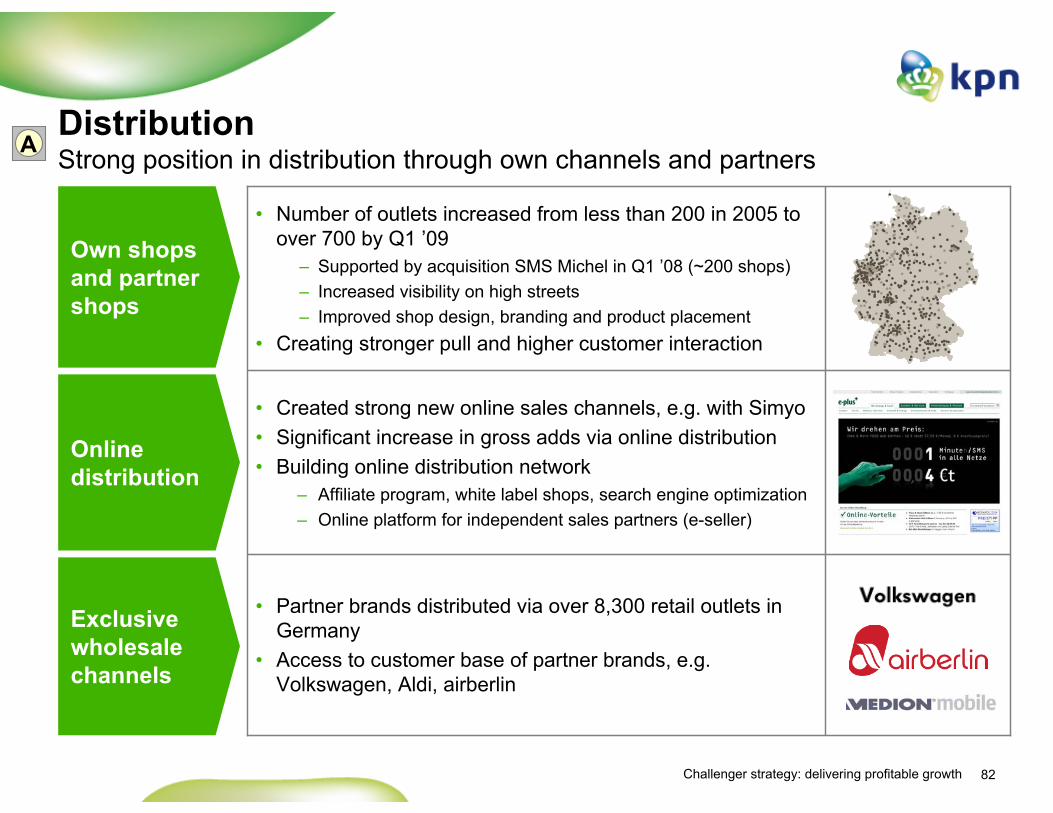

DistributionStrong position in distribution through own channels and partners

Own shops and partner shops

Online distribution

Exclusive wholesale channels

• Partner brands distributed via over 8,300 retail outlets in Germany

• Access to customer base of partner brands, e.g. Volkswagen, Aldi, airberlin

• Created strong new online sales channels, e.g. with Simyo• Significant increase in gross adds via online distribution• Building online distribution network

– Affiliate program, white label shops, search engine optimization– Online platform for independent sales partners (e-seller)

• Number of outlets increased from less than 200 in 2005 to over 700 by Q1 ’09

– Supported by acquisition SMS Michel in Q1 ’08 (~200 shops)– Increased visibility on high streets– Improved shop design, branding and product placement

• Creating stronger pull and higher customer interaction

A

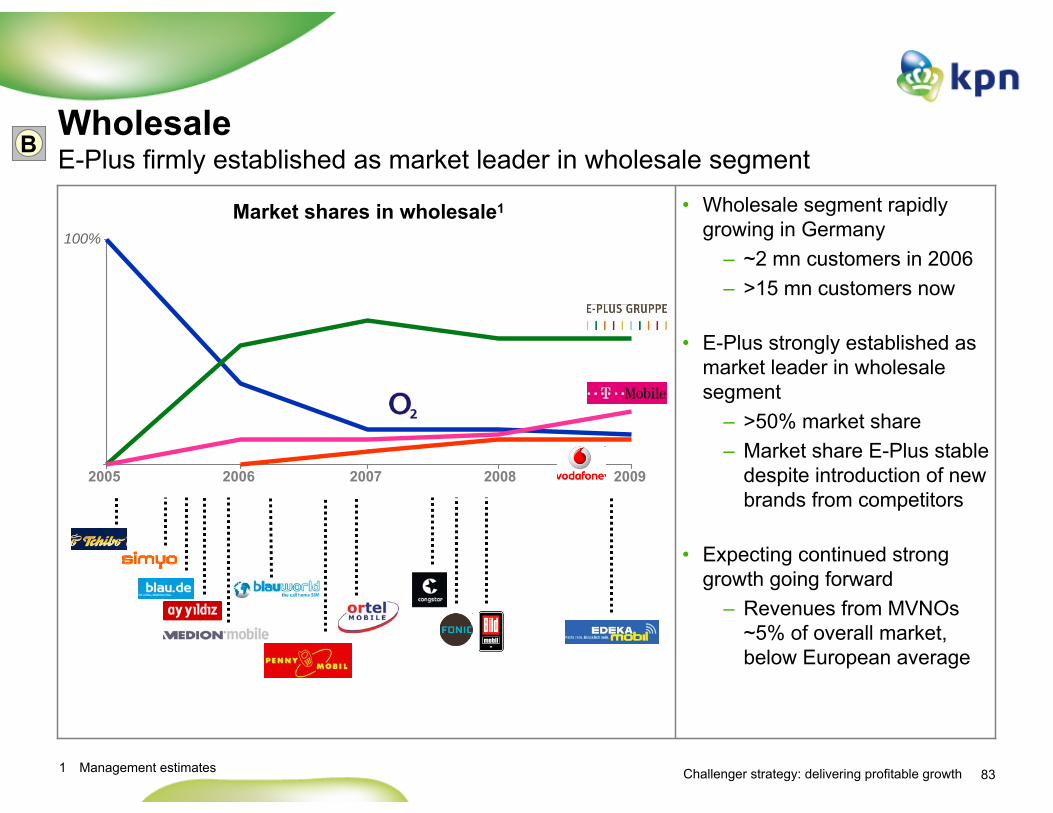

83Challenger strategy: delivering profitable growth

• Wholesale segment rapidly growing in Germany

– ~2 mn customers in 2006– >15 mn customers now

• E-Plus strongly established as market leader in wholesale segment

– >50% market share– Market share E-Plus stable

despite introduction of new brands from competitors

• Expecting continued strong growth going forward

– Revenues from MVNOs~5% of overall market, below European average

Wholesale E-Plus firmly established as market leader in wholesale segment

2005 2006 2007 2008 2009

Market shares in wholesale1

100%

1 Management estimates

B

84Challenger strategy: delivering profitable growth

Segmentation going forwardIntroducing new propositions and starting new partnerships

• Cooperation with WiFi provider FON• Access to WiFi connections shared with other users

– Over 25,000 FON WiFi hotspots in Germany

• Expanding into SME / SoHo segment• Introduction of Yes Telecom in Germany

– Value-for-money mobile services for SME / SoHo– Already successful in the Netherlands

• Partnerships with German sports clubs• Partnership with Disney targeting youth segments

• Introduction of data flat rates in new segments and new distribution channels

SME / SoHo

Data flat rates

Special interest

WiFi / Online offers

B

85Challenger strategy: delivering profitable growth

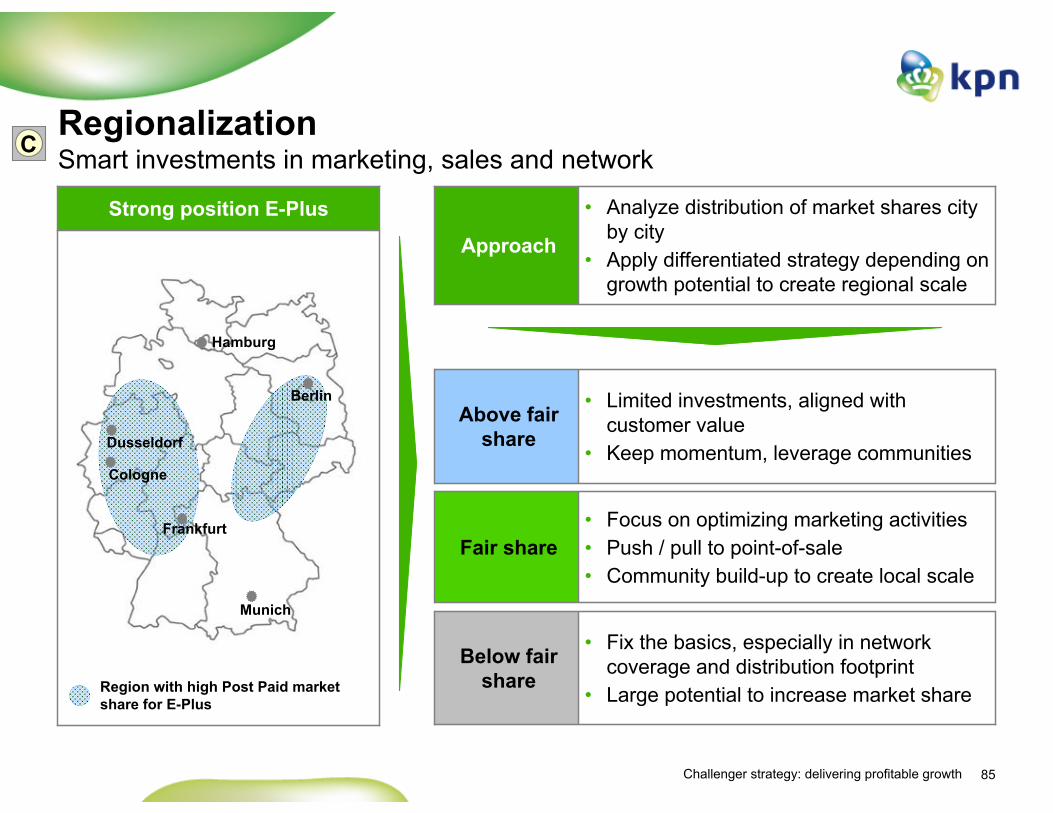

Strong position E-Plus

Regionalization Smart investments in marketing, sales and network

• Analyze distribution of market shares city by city

• Apply differentiated strategy depending on growth potential to create regional scale

Approach

• Fix the basics, especially in network coverage and distribution footprint

• Large potential to increase market share

Below fair share

• Focus on optimizing marketing activities• Push / pull to point-of-sale• Community build-up to create local scale

Fair share

• Limited investments, aligned with customer value

• Keep momentum, leverage communities

Above fair share

C

Munich

Berlin

Dusseldorf

Frankfurt

Hamburg

Cologne

Region with high Post Paid market share for E-Plus

86Challenger strategy: delivering profitable growth

• Consumers mainly use ‘light’ data applications on smartphones

• Consumers have a preference for flat fees

• Data tariffs E-Plus focus on mass market

– Flat rates and target group segmentation

– € 10 / month for wireless data on handsets

– € 1 / month for access to top-3 content

Wireless dataConsumers mainly use ‘light’ data and prefer flat rates

Preferred tariff plans

flat rate

time

uncertain

volume67%

Source: Consumer research

D

Drivers behind data usage (%)

55%

43%

36%

24%

17%

Communication

Information

Transactions

Social networks

Entertainment

87Challenger strategy: delivering profitable growth

Wireless data (cont’d)Consumers satisfied with services, data usage expected to take off

• Bandwidths offered sufficient for current ‘light’ data usage on handsets

• Different requirements and usage patterns for corporate markets

– Less relevant for E-Plus, as a result of focus on consumer and SME / SoHo segments

• Demand for wireless data taking off in German consumer market

– Substantial growth expected in near future

– Data no longer in early adopter phase, but becoming mass market proposition

Data usage patterns (% of users)

D

32%

2%

9%

8% 13%

14%

25%

10%MMS

Navigation

Internet / WAP

Today’s usage Usage near future

Satisfied

Slightly disappointed

Unsatisfied62%

*Phone users, no stationary laptop usage

Satisfaction bandwidths for handset use*

Source: Consumer research

88Challenger strategy: delivering profitable growth

Data network roll-outE-Plus network roll-out based on those services that consumers want

• Smart follower in wireless data– Investing in data networks now

demand is taking off– Benefiting from increased capabilities

for equipment and lower costs– Combination of EDGE and UMTS

sufficient to meet demand of mass market

• Phased data network roll-out in Germany

– National EDGE coverage meets current data demand

– Gradual UMTS roll-out with regionalization approach

– HSPA in regions with strong demand

Smart follower strategy ApproachTechnology

• Co-operation with provider FON for WiFi accessWiFi / WLAN

• Rolling out in focus cities and key hotspotsHSPA

• > 60% population coverage per Q1 ’09 UMTS

• EDGE roll-out in 2009 to 90% pop coverageEDGE

• National coverage in placeGPRS

D

89Challenger strategy: delivering profitable growth

Concluding remarks

• Delivering profitable growth ahead of the market since 2005

• Further upside potential for proven Challenger strategy

• Strong position in both wholesale and retail segments

• Leveraging potential of regional approach

• Best value-for-money proposition for mobile data

• Confident in continued outperformance, clear focus on EBITDA and cash flow– Targeting 20-25% service revenue market share in next few years– EBITDA margin of at least 35%

90Challenger strategy: delivering profitable growth

Agenda

Eric Hageman, CFO KPN Mobile InternationalFinance

Stan Miller, CEO KPN Mobile InternationalConcluding remarks

Eric Hageman, CEO International WholesaleInternational Wholesale

Thorsten Dirks, CEO E-PlusE-Plus

Marc van Asbroeck, Chief Legal & RegulationRegulation

Stan Miller, CEO KPN Mobile InternationalStrategy

Erik Hoving, CTO KPN Mobile International KPN Group Belgium

Ad Scheepbouwer, Chairman and CEO KPNIntroduction

91Challenger strategy: delivering profitable growth

Leverage own international brands (e.g. Simyo, Ortel, blau)

Overview Organization built across markets, leverage international partners and own brands

• Launched 2005• Leading wholesaler

Network

Own brands

Germany

Wholesale

• Launched 2003

• Leading wholesaler

Belgium

Network

Own brands

Wholesale

• Launched 2008• Leading MVNO

Spain

Wholesale

Own brands

• Launched 2009

France

Wholesale

Own brands

Netherlands

Network

Own brands

Wholesale

• Launched 2002• Leading wholesaler

Organization built across markets, international platform and know how

Leverage international wholesale partners

92Challenger strategy: delivering profitable growth

Lean operating

model

Wholesale / new

distribution

Multiple segment

marketing

Attractive propositions

Regulatory action

• Build leanest and most profitable operator in all our markets

• Wholesale, diversified distribution to drive scale at attractive economics

• Focus on value offerings with Fixed-Mobile Substitution approach

• Address individual segments directly or through wholesale partners

• Ensure level playing field between challengers and incumbents

Wholesale focus

Challenger strategy Wholesale capabilities

Financial model

Marketing

Technical complexity

Flexibility & speed

Many new entrants

• Minimize investment through Opex model, partnership, branded reselling

• Reducing commercial complexity through “single-point-of-contact”service for partners

• Quick & adequate response to new commercial / technical requirements

• Provide technological knowledge & scale through sharing platforms

• Minimize risk through synergies with own and partners’ brands

Announced

Sept ’06

Mobile wholesale strategy Wholesale as key pillar of Int’l Challenger strategy, strong wholesale capabilities

93Challenger strategy: delivering profitable growth

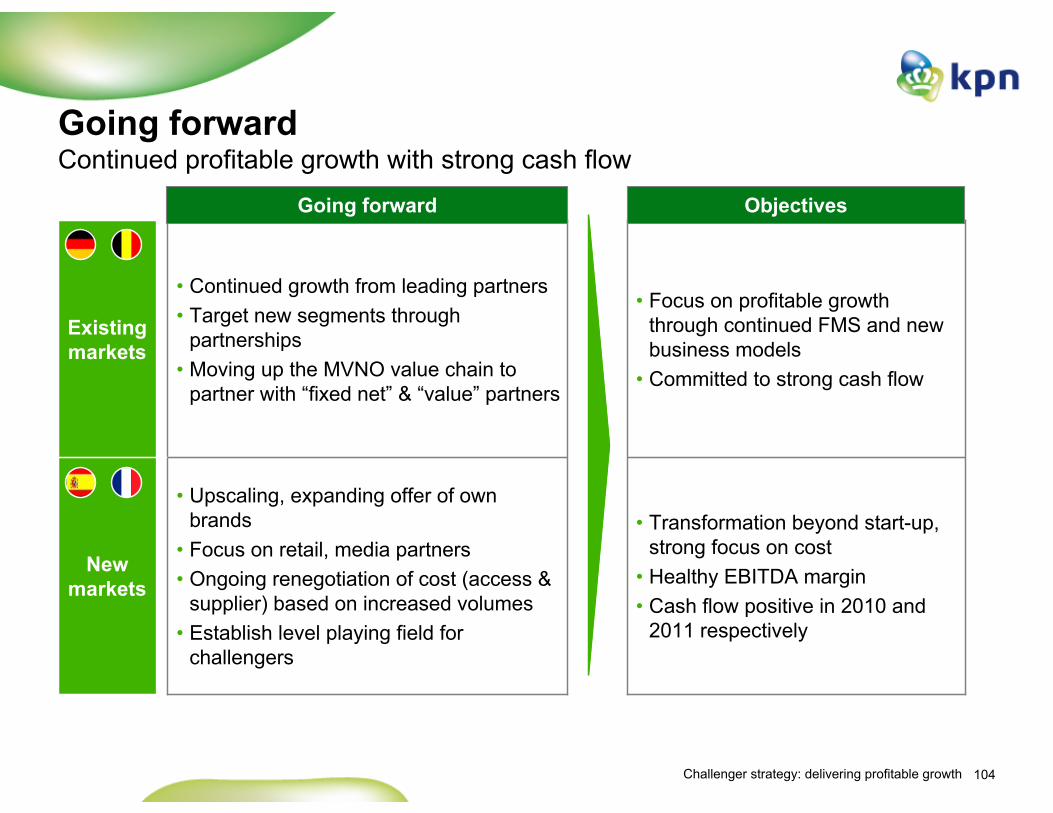

Redesigned business modelFlexible business model, successfully leveraged to new markets

Exis

ting

mar

kets

New

mar

kets

Network ownership & operation

Back office, billing & IT

Customer service & support

Marketing

Sales

Sales

Sales

Network ownership & operation

Back office, billing & IT

Customer service & support

Marketing

Sales

Sales

Sales

Leverage retail processesOwn brandsWholesale partners

Own brandsWholesale partners

Managed servicesHost outside footprint

Outsourced

Partner

Do it in-house

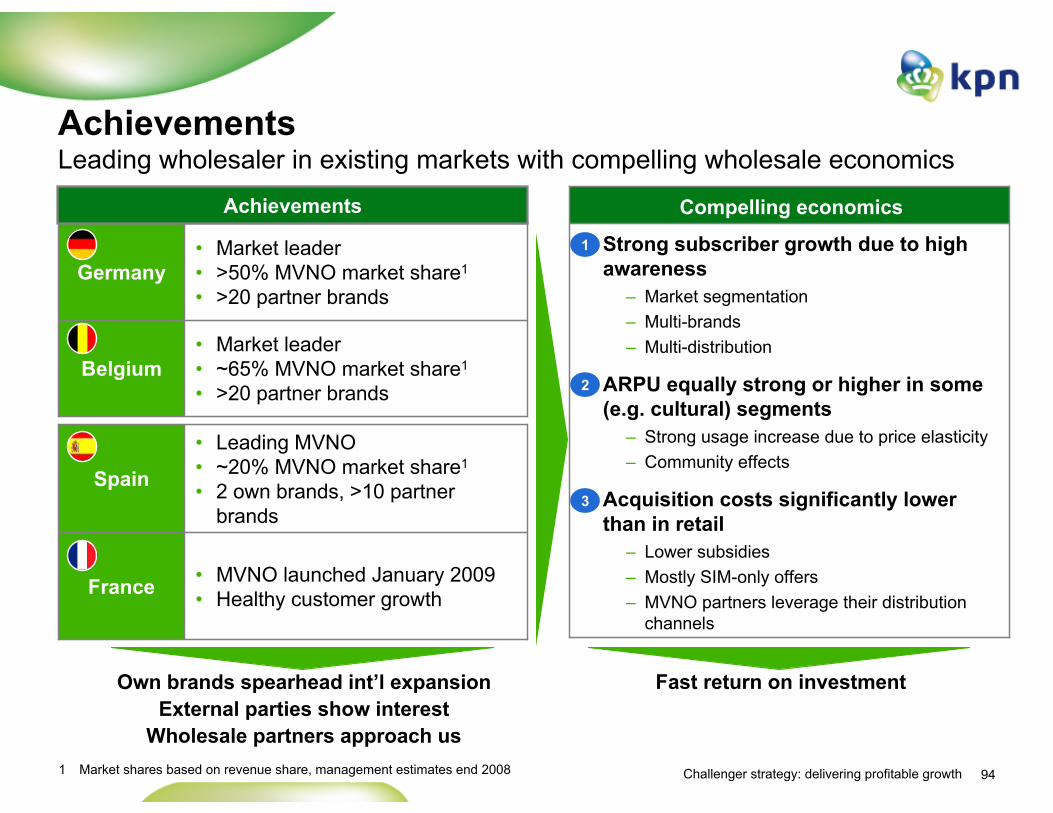

94Challenger strategy: delivering profitable growth

• Leading MVNO • ~20% MVNO market share1

• 2 own brands, >10 partner brands

Spain

• Market leader• ~65% MVNO market share1

• >20 partner brandsBelgium

• MVNO launched January 2009• Healthy customer growthFrance

• Market leader• >50% MVNO market share1

• >20 partner brandsGermany

AchievementsLeading wholesaler in existing markets with compelling wholesale economics

Achievements

Fast return on investment

1 Market shares based on revenue share, management estimates end 2008

Own brands spearhead int’l expansionExternal parties show interest

Wholesale partners approach us

Strong subscriber growth due to high awareness

– Market segmentation – Multi-brands– Multi-distribution

ARPU equally strong or higher in some (e.g. cultural) segments

– Strong usage increase due to price elasticity– Community effects

Acquisition costs significantly lower than in retail

– Lower subsidies– Mostly SIM-only offers– MVNO partners leverage their distribution

channels

Compelling economics

1

2

3

95Challenger strategy: delivering profitable growth

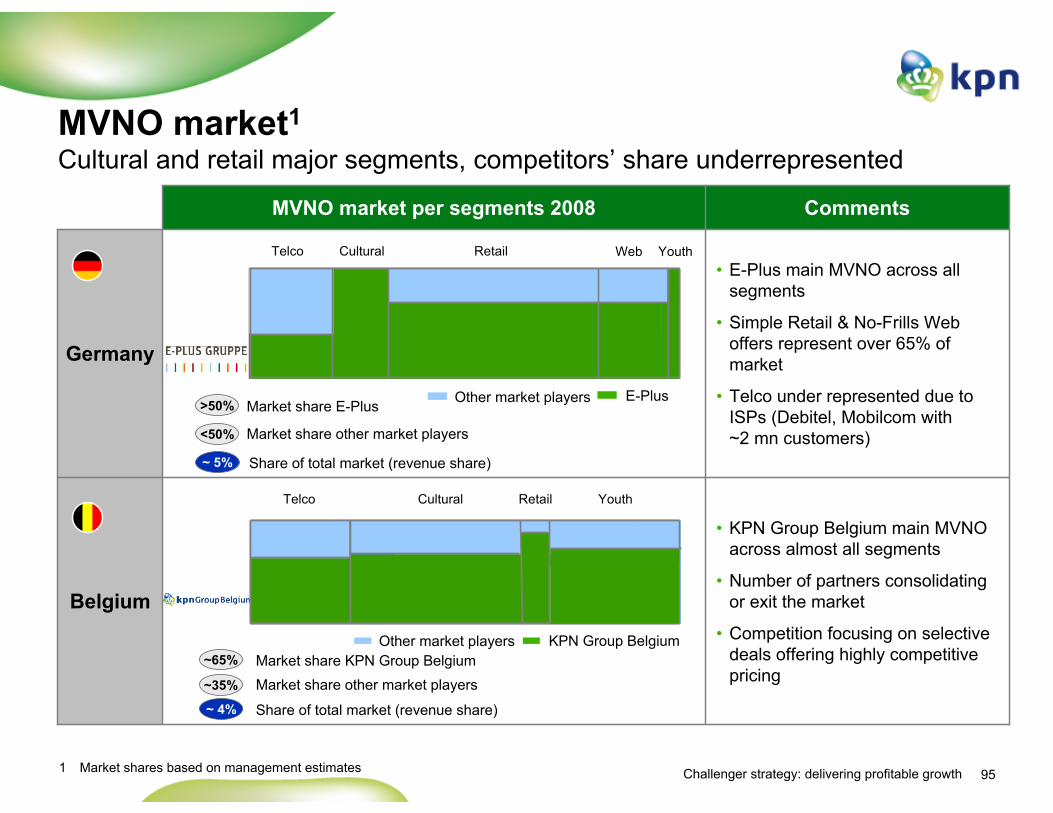

• KPN Group Belgium main MVNO across almost all segments

• Number of partners consolidating or exit the market

• Competition focusing on selective deals offering highly competitive pricing

Belgium

• E-Plus main MVNO across all segments

• Simple Retail & No-Frills Web offers represent over 65% of market

• Telco under represented due to ISPs (Debitel, Mobilcom with ~2 mn customers)

Germany

CommentsMVNO market per segments 2008

MVNO market1

Cultural and retail major segments, competitors’ share underrepresented

~ 5% Share of total market (revenue share)

>50%

<50%

Telco YouthWebRetailCultural

~35%

~65%

Market share other market players

Market share E-Plus

Market share other market playersMarket share KPN Group Belgium

Telco YouthRetailCultural

E-PlusOther market players

KPN Group BelgiumOther market players

~ 4% Share of total market (revenue share)

1 Market shares based on management estimates

96Challenger strategy: delivering profitable growth

International expansion Selective expansion to European markets through low cost business model

• Challenger strategy is very successful in home markets

– Belgium, Germany and the Netherlands

• Opportunity to expand strategy to new European markets

– Wholesale, segment-tailored propositions

– Multi-brand, no-frills

– High potential, limited risk, fast Return on Investment

Expansion rationale

• Market size: Large markets with major value creation potential

• State of competition: Relatively high price levels and limited number of MVNO / MVNEs

• Customer segments: Potential to target new and interesting segments (cultural, regional)

• Existing partners: Potential to leverage existing wholesale partners

• New partners: Potential attractive new partners with local knowledge and assets

• Regulation: Regulatory support for MVNO/MVNE

European scopeAnnounced

Sept ’06

97Challenger strategy: delivering profitable growth

• Many brands but few financially successful, lack of support and “right”conditions from MNOs

• High spread of 8 cents vs. EU average of 5.2 cents

• Continued FMS• High mobile usage close

to European average

• MVNO revenue market share only 1% of total

• Indicating growth potential, e.g. NL ~10%, Germany ~5%

Market share

Players &

segments

Pricing vs.

usage

200213

Spain EU

Spain: Market overviewAttractive MVNO landscape, showing clear upside potential

Spread

€ mn

€ cents

Source: Equity research

152

15,085MNO

MVNO

Revenue

MobileFixed

MoU

Δ 8.0

Only 4 players

> 25 players

Total minutes

Retail Telecom OtherCultural

Top 5 MVNO

Q4 '05 Q4 '08

61%

39%

44%

56%

7.8

15.8

MTA ARPM

98Challenger strategy: delivering profitable growth

Own brands

Spain: Organizational set-upLean & mean organization, large scalability at attractive economics

Management

Customer Operations Management

MVNE Platform

Operating across borders

Key activities~10 FTE

~5 FTEPartners

~5 FTE• Marketing & Sales• Web portal & community• Brand account mgmt• Project & MVNE mgmt

• Management• G&A (Finance, Legal, HR)

• Customer Care • Logistics & handsets• Product & roadmap mgmt• Roaming & inter-operator mgmt