KPMG Sourcing Advisory 4Q13 Global Pulse Survey · PDF file• Human resources ... Advisory...

54

KPMG Sourcing Advisory 4Q13 Global Pulse Survey Trends in shared services, outsourcing, and third-party business and IT service markets, gleaned from KPMG’s own field advisors and leading global service providers. kpmg.com

-

Upload

hoangduong -

Category

Documents

-

view

223 -

download

3

Transcript of KPMG Sourcing Advisory 4Q13 Global Pulse Survey · PDF file• Human resources ... Advisory...

KPMG Sourcing Advisory 4Q13

Global Pulse SurveyTrends in shared services, outsourcing, and

third-party business and IT service markets, gleaned from KPMG’s own field advisors

and leading global service providers.

kpmg.com

2 Shared Services and Outsourcing Advisory / KPMG Sourcing Advisory 4Q13 Global Pulse Survey / January 2014

© 2014 KPMG International Cooperative (“KPMG International”). KPMG International provides no client services

and is a Swiss entity with which the independent member firms of the KPMG network are affiliated.

The Sourcing Advisory Pulse surveys are part of a broad family of KPMG Pulse surveys. This collective research program focuses on GBS market trending in specific geographies such as China or South Africa, functional areas such as real estate and facilities management (REFM). The Pulse research program also examines related key topics such as cloud computing, human resources (HR) transformation, and vertical industry business trends.

Since their inception in 2004, the global Sourcing Advisory Pulse surveys have yielded insightful analyses of current and ongoing market trends in the use, deployment, and delivery of business and information technology (IT) services. They capture changes in demand, usage levels, future adoption plans, and related key market indicators. They highlight the changes, and the direction of change, in the GBS market as a whole. The surveys focus on where the market is going and how that direction is changing—or not—as compared to prior quarters and years.

This edition of the global Sourcing Advisory Pulse surveys reflects GBS market activity during 4Q13 as well as projections and predictions for 2014 for GBS services as well as broader economic and market trends globally.

Topics explored include:

• GBS demand and adoption trends

• Drivers for GBS delivery improvement efforts

• Top 2014 trends and predictions

• Outsourcing deal pricing, service provider profitability, and scope

KPMG is pleased to release the findings from its KPMG 4Q13 global Sourcing Advisory Pulse surveys. The Pulse surveys provide insights into trends and projections in end-user organizations’ usage of global business services (GBS). The learnings are gleaned globally from KPMG International (KPMGI) member firms’ (KPMG firms’) advisors, who work closely with end-user organizations that are actively exploring or undertaking domestic, near and offshore shared services and outsourcing, and other service delivery initiatives, as well as from leading global business and IT service providers.

Introduction

Shared Services and Outsourcing Advisory / KPMG Sourcing Advisory 4Q13 Global Pulse Survey / January 2014 3

© 2014 KPMG International Cooperative (“KPMG International”). KPMG International provides no client services

and is a Swiss entity with which the independent member firms of the KPMG network are affiliated.

The Pulse surveys focus on end-user organizations’ global use of shared services, outsourcing, and other third-party services across the following functional areas:

• Customer care/call center• Finance and accounting (F&A)• Human resources (HR)• Information technology (IT)• Knowledge process outsourcing (KPO)• Procurement/source to pay• Real estate and facilities management (REFM)• Vertical industry business services

The following leading global business and IT service providers participated in the 4Q13 survey:

• Accenture• ADP• BT Global Services• Capgemini• CGI• CSC• Dell• EXL• Genpact

• HCL Technologies• HP• Serco• Syntel• Tech Mahindra• Wipro• WNS• Unisys• Xerox

Questions or comments regarding the Pulse surveys should be directed to Stan Lepeak, director, Global Research, KPMG Management Consulting, at [email protected] or +1 203-458-0677.

4

.

Table of Contents

IManagement Summary 6

IIHighlights 12

IIIMarket Conditions 14

IVTrends 30

VLearn More 44

KPMG Advisors: Top Approaches to Improve Service Delivery Capabilities 14

Business and IT Service Providers Market Demand Assessments 20

Current Market Deal Characteristics: Service Providers’ Perspectives 24

Outsourcing Market Macro Trends 30

Top 2014 Trends and Predictions 32

Where to Learn More about Global Sourcing Market Trends 44

Appendix 45

4Q13 Global Pulse Survey | Management SummaryManagement Summary

6 Shared Services and Outsourcing Advisory / KPMG Sourcing Advisory 4Q13 Global Pulse Survey / January 2014

© 2014 KPMG International Cooperative (“KPMG International”). KPMG International provides no client services

and is a Swiss entity with which the independent member firms of the KPMG network are affiliated.

The 4Q13 edition of the global Sourcing Advisory Pulse represents a new installment in KPMG’s quarterly deep dive into industry trends and best practices in the deployment, use, and expansion of global business services (GBS). KPMG defines global business services as an operating model and strategic governance framework that helps organizations transform end-to-end business support services to deliver more effective solutions for both the internal and external customers of the organization. GBS focuses on optimizing the mix of human capital, service delivery models, process innovation, and technology to deliver services on an enterprise-wide, cross-functional basis, to support the business strategy. GBS adoption rates continue to accelerate as found in a recent comprehensive KPMG market study on GBS trending.

GBSMATURITY

SUB-OPTIMIZED RATIONALIZED OPTIMIZED STRATEGIC INTEGRATEDDecentralized and duplicative functions ; little central control over business support services

Single function shared services with tactical onshore or offshore provider relationships

Traditional outsourcing relationships with global delivery; non-integrated internal shared services capabilities

Optimized balance of internal and external delivery capabilities, global sourcing with multifunction focus

Globally integrated services portfolio with aggressive use of alternative and mixed delivery models

Level 01

Level 02

Level 03

Level 04

Level 05

Value capture and performance sustainability

KPMG GBS Maturity Model

4Q13 Global Pulse Survey | Management Summary

Shared Services and Outsourcing Advisory / KPMG Sourcing Advisory 4Q13 Global Pulse Survey / January 2014 7

© 2014 KPMG International Cooperative (“KPMG International”). KPMG International provides no client services

and is a Swiss entity with which the independent member firms of the KPMG network are affiliated.

This edition of the Pulse survey does an annual examination of the expected top trends

for the coming year for global business services as well as broader economic, business

and geopolitical market trends. Talent shortages and talent management challenges

have supplanted negative global economic conditions and weak demand for goods and

services as the top challenge facing organizations. Despite high unemployment rates in

most Western markets, available talent often does not have the skills or ambition sought

by employers. This is a driving factor for ongoing increased adoption of global service

delivery models. While eroding cost differentials across markets is encouraging some

organizations to bring work back “onshore” the total headcount is relatively small and a

focus on increased process automation in lieu of hiring new staff is a growing trend.

Emerging market competitors to Western firms is a growing concern in the Americas

and in EMEA while in the Americas, especially the US, concern over the negative impact

of political and economic gridlock continues to grow.

2014 Trends with Biggest Negative Impact on User Organizations – Top 5

4Q13 Global Pulse Survey | Management Summary

8 Shared Services and Outsourcing Advisory / KPMG Sourcing Advisory 4Q13 Global Pulse Survey / January 2014

© 2014 KPMG International Cooperative (“KPMG International”). KPMG International provides no client services

and is a Swiss entity with which the independent member firms of the KPMG network are affiliated.

While economic conditions continue to slowly improve in many Western markets, growth

is slowing in emerging markets, creating a mixed bag of business growth opportunities

globally. There is great optimism on the potential benefits from the maturation of,

and greater access to, innovative technologies such as cloud, social media, and

virtualization, more so than hope for improving economic conditions. Despite concern

over emerging market competition, there are positive expectations for expanding

opportunities for selling goods and services in emerging markets.

As has been the case for several years, the clear top initiative cited for organizations

in 2014 remains continuing to drive down operating costs though many firms face

diminishing returns from these efforts. This being said, there is more appetite to invest in

new and improved information technology (IT), such as enterprise software systems,

business intelligence and analytics, cloud, and social media. Optimizing global service

delivery chains and excelling at global business services as well as finding, attracting

and retaining talent globally are also top priorities for 2014

2014 Trends with Biggest Positive Impact on User Organizations – Top 5

Top 2014 User Organization Initiatives – Top 5

4Q13 Global Pulse Survey | Management Summary

Shared Services and Outsourcing Advisory / KPMG Sourcing Advisory 4Q13 Global Pulse Survey / January 2014 9

© 2014 KPMG International Cooperative (“KPMG International”). KPMG International provides no client services

and is a Swiss entity with which the independent member firms of the KPMG network are affiliated.

Organizations will face many challenges in successfully undertaking these initiatives.

One clear and recurring challenge cited is the problem of dysfunctional and fragmented

organizational and operating models, designs and processes. These will prove

challenging to overcome and are often another one of the drivers behind expanded GBS

efforts. Inadequate and antiquated IT infrastructure and systems will challenge efforts,

hence the high expectations for innovative technologies and the focus on investing in new

IT. A more fundamental challenge cited is inability to innovate which will plague affected

firms globally, especially in more staid or protected markets.

There is a broad range of skills and capabilities identified as critical enablers for

successfully undertaking the initiatives outlined. One is having smart and innovative

management and management practices, a capability in too short supply in too many

organizations. One means through which to enable smart management is by investing

in reporting and analytics to make better business decisions faster. Alternative service

delivery models such as shared services and outsourcing, as part of an overall GBS

strategy and model, is another key enabler. The ability to find, attract and retain talent

globally, both for smart management and smart rank and file, will prove critical.

Top Challenges to Successfully Undertaking 2014 Initiatives – Top 5

Top Capabilities Required to Successfully Undertake 2014 Initiatives – Top 5

4Q13 Global Pulse Survey | Management Summary

10 Shared Services and Outsourcing Advisory / KPMG Sourcing Advisory 4Q13 Global Pulse Survey / January 2014

© 2014 KPMG International Cooperative (“KPMG International”). KPMG International provides no client services

and is a Swiss entity with which the independent member firms of the KPMG network are affiliated.

Major investments areas in 2014 will include cloud software and services as well as

data and analytics software and services. Data and analytics investments will span

several areas with a priority placed on analytical tools and foundational infrastructure

capabilities. Keeping with the talent theme, hiring more GBS staff with analytics skills is

also a priority.

Advisors: Investments Levels, 2014 Compared to 2013 – Top 5 Growth Areas

4Q13 Global Pulse Survey | Management Summary

Shared Services and Outsourcing Advisory / KPMG Sourcing Advisory 4Q13 Global Pulse Survey / January 2014 11

© 2014 KPMG International Cooperative (“KPMG International”). KPMG International provides no client services

and is a Swiss entity with which the independent member firms of the KPMG network are affiliated.

Finally, there is a general sense of pessimism about general market conditions at the

regional and country level. Both third party service providers and KPMG professionals

polled indicated their clients had mixed expectations on global economic growth,

especially in Asia Pacific. There are also growing concerns over inflation and the rising

cost of living in Asia Pac. The cost and quality of healthcare and its potential drag on the

economy is a major concern, especially in the US. On a more positive note, deterioration

of the level of global free trade, or de-globalization in general, is not expected to worsen in

2014. All in all it should make for an interesting year.

Advisors: Change in Market Conditions 2014-15

Highlights

12 Shared Services and Outsourcing Advisory / KPMG Sourcing Advisory 4Q13 Global Pulse Survey / January 2014

© 2014 KPMG International Cooperative (“KPMG International”). KPMG International provides no client services

and is a Swiss entity with which the independent member firms of the KPMG network are affiliated.

KPMG International Firms’ Shared Services and Outsourcing Advisory Highlights

1. Improve current SSC/outsourcing governanceprocesses/capabilities

2. Internal process improvement/reengineering efforts 3. Use/expansion of shared services

Top Means to Improve Service Delivery Performance

1. Continue to drive down operating costs 2. Invest in new/improved IT 3. Redesign/reengineer core business processes

Top 2014 Buyer Initiatives

1. Maturation of/greater access to innovative technologies 2. Expanding emerging market opportunities for selling goods

and services 3. Improving/rebounding global economic conditions

Top Positive 2014 Market Trends

1. Analytical tools – BI, BPM, EPM 2. Foundational infrastructure capabilities3. Third party advisory services

Top Areas of Data & Analytics Investments

1. IT2. F&A3. HR

Top Focus Areas for Performance Improvement Efforts

1. Dysfunctional/fragmented org./op. models, designs, and processes 2. Inadequate/antiquated IT infrastructure and systems 3. Inability to innovate

Top Challenges to 2014 Initiatives

1. Talent shortages/talent management challenges 2. Weak global/regional economies; "double-dip" recession3. Weak consumer/customer demand

Top Negative 2014 Market Trends

1. Smart/innovative management and management practices 2. Alternative service delivery models – shared services and outsourcing3. GBS-integrated/consistent global services delivery models

Top Factors and Capabilities Needed to Succeed at Initiatives

KPMG International Firms’ Shared Services and Outsourcing Advisor Highlights

Shared Services and Outsourcing Advisory / KPMG Sourcing Advisory 4Q13 Global Pulse Survey / January 2014 13

© 2014 KPMG International Cooperative (“KPMG International”). KPMG International provides no client services

and is a Swiss entity with which the independent member firms of the KPMG network are affiliated.

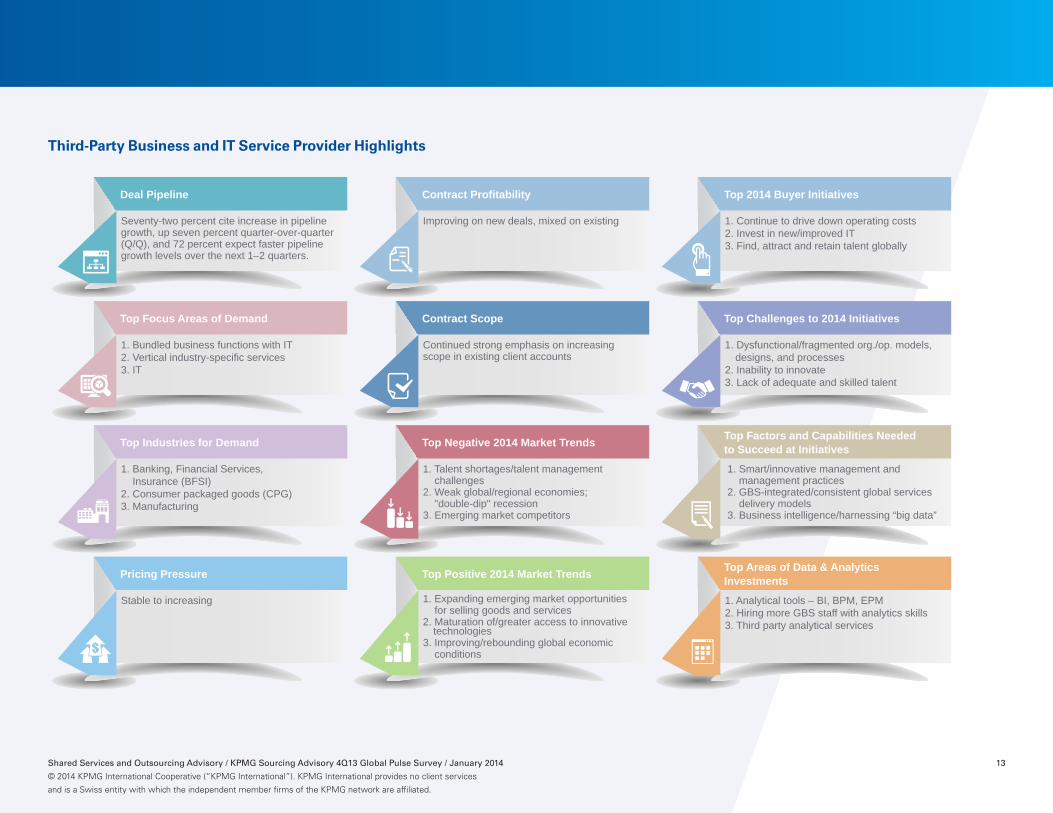

Third-Party Business and IT Service Provider HighlightsThird-Party Business and IT Service Provider HighlightsDeal Pipeline

Seventy-two percent cite increase in pipeline growth, up seven percent quarter-over-quarter (Q/Q), and 72 percent expect faster pipeline growth levels over the next 1–2 quarters.

Top Focus Areas of Demand

1. Bundled business functions with IT2. Vertical industry-specific services3. IT

Top Industries for Demand

1. Banking, Financial Services, Insurance (BFSI)2. Consumer packaged goods (CPG)3. Manufacturing

Pricing Pressure

Stable to increasing

Contract Profitability

Contract Scope

Continued strong emphasis on increasing scope in existing client accounts

Top Negative 2014 Market Trends

1. Talent shortages/talent management challenges 2. Weak global/regional economies; "double-dip" recession3. Emerging market competitors

Top Positive 2014 Market Trends

1. Expanding emerging market opportunities for selling goods and services 2. Maturation of/greater access to innovative

technologies 3. Improving/rebounding global economic conditions

Top 2014 Buyer Initiatives

1. Continue to drive down operating costs 2. Invest in new/improved IT 3. Find, attract and retain talent globally

Top Challenges to 2014 Initiatives

1. Dysfunctional/fragmented org./op. models,designs, and processes

2. Inability to innovate 3. Lack of adequate and skilled talent

Top Factors and Capabilities Neededto Succeed at Initiatives

1. Smart/innovative management and management practices 2. GBS-integrated/consistent global services delivery models 3. Business intelligence/harnessing “big data”

Top Areas of Data & Analytics Investments

1. Analytical tools – BI, BPM, EPM 2. Hiring more GBS staff with analytics skills3. Third party analytical services

Improving on new deals, mixed on existing

4Q13 Global Pulse Survey | Market Conditions

14 Shared Services and Outsourcing Advisory / KPMG Sourcing Advisory 4Q13 Global Pulse Survey / January 2014

© 2014 KPMG International Cooperative (“KPMG International”). KPMG International provides no client services

and is a Swiss entity with which the independent member firms of the KPMG network are affiliated.

Market Conditions

KPMG Firms’ Advisors: Top Approaches to Improve Service Delivery Capabilities

KPMG polled its global network of shared services and outsourcing advisors and professionals (KPMG consultants working with clients in the field) on what they are seeing in client accounts as the top approaches that end-user organizations are employing today to improve service delivery performance, as well as to help minimize or reduce service delivery costs (see Figure 1).• Sixty-two percent of advisors, up four percent from last quarter but down six percent from last year, cited improve current

shared services and outsourcing governance processes and capabilities as the most common approach undertaken to improve service delivery capabilities. This is a perennial top-rated approach over the past three years. It reflects market awareness of the importance of sourcing governance to GBS success as well as the challenges many organizations have in improving these capabilities, especially as GBS efforts become more complex. GBS governance excellence is an ever moving target that in some respects becomes harder to achieve as organizations more fully appreciate its complexity, its importance and what constitutes best in class.

• The second most commonly cited approach was internal process improvement or reengineering efforts, identified by 49 percent of advisors. Ranking third and selected by 47 percent of advisors was use and expansion of shared services. Insourcing work previously outsourced jumped to 16 percent from nine percent last quarter (though still a low number given the volume of activities outsourced) while bringing work performed offshore back onshore was selected by under five percent of respondents (highlighting that onshoring is often more urban myth than reality though where it occurs it is usually with more strategic work) . These last two answers were first added in the 2Q13 Pulse survey.

• Improving governance processes and capabilities was the top-cited approach by all classes of advisors except those operating in the Asia Pacific region where internal process improvement or re-engineering efforts was the top change mechanism cited (see Appendix for a breakout of KPMG firms’ advisors’ responses by geographic region and by functional area of focus). The expansion of shared services usage was more frequently cited by advisors that support business process services than those that focus on IT services. The interconnection between global business services efforts and underlying supporting IT services is becoming more complex as well as more often recognized as a key enabler to GBS success.

4Q13 Global Pulse Survey | Market Conditions

Shared Services and Outsourcing Advisory / KPMG Sourcing Advisory 4Q13 Global Pulse Survey / January 2014 15

© 2014 KPMG International Cooperative (“KPMG International”). KPMG International provides no client services

and is a Swiss entity with which the independent member firms of the KPMG network are affiliated.

Figure 1 | Advisors: Top Approaches to Improve Service Delivery Capabilities

* New category 2Q13

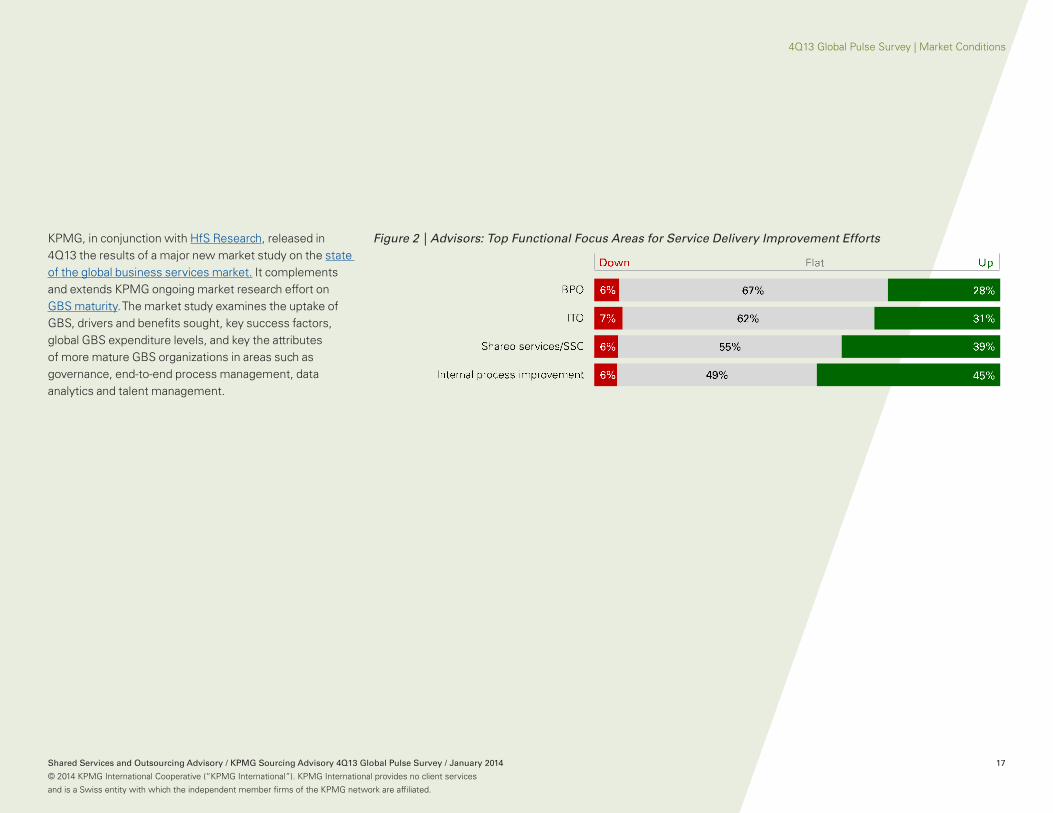

KPMG firms’ sourcing advisors were asked in which functional areas buyers are today most commonly applying the approaches outlined in Figure 1 to improve service delivery capabilities (see Figure 2). IT was the most commonly cited functional area, identified by 64 percent of advisors, down one percent from last quarter. F&A was ranked second and selected by 58 percent of advisors polled. There was general consensus on these rankings across geographies, though advisors serving the Asia-Pacific region more frequently identify BPO categories though ITO demand was exceptionally strong in Asia Pac this quarter.

Use of third parties to support F&A and procurement functions continues to benefit from the growth of more mature cloud and software as a service (SaaS) based offerings. Overall, however, market penetration into F&A and procurement is still much lower than with the IT function. For a comprehensive overview of the F&A services and the FAO market space refer to the results from KPMG’s 2013 study on F&A sourcing trends.

4Q13 Global Pulse Survey | Market Conditions

16 Shared Services and Outsourcing Advisory / KPMG Sourcing Advisory 4Q13 Global Pulse Survey / January 2014

© 2014 KPMG International Cooperative (“KPMG International”). KPMG International provides no client services

and is a Swiss entity with which the independent member firms of the KPMG network are affiliated.

GBS continues to become a more mainstream concept, framework and operating model for more progressive global organizations. As part of this there is a continued

growing interest among organizations utilizing a GBS model, especially when it comes to shared services, to deploy the model in nontraditional functional and process areas

beyond back office IT, HR, F&A and procurement. These include areas and activities such business intelligence and analytics, real estate and facilities management services, and

supplier and supply chain management.

Reducing operating costs, or at least keeping costs from rising, remains a fundamental goal for GBS efforts, though for many organizations cost levels in areas in scope are already

quite low based on reductions already achieved over the past several years. Increased process automation – and eliminating the labor component of costs - in lieu of or in conjunction with

expansion of GBS efforts, is a growing focus areas among organizations keen on further driving down operating costs while also pursuing improved service quality and accuracy.

The increased focused on process automation, often delivered via cloud services, will create growing challenges for third party services providers that have relied on high skilled yet lower

cost labor as a differentiator. It creates opportunities for providers that can help client enable this automation and have the vertical industry and business process knowledge to so. Greater use of data

analytics coupled with greater process automation will enable organizations to create more intelligent business processes that can increasingly sense and respond to changing business needs in a more real

time fashion based upon predefined rules and models, and effectively minimize certain labor components whether outsourced or internal. Collectively capabilities such as these will further drive the business value of

GBS operations but also exacerbate the under-employment challenge in many Western markets.

4Q13 Global Pulse Survey | Market Conditions

Shared Services and Outsourcing Advisory / KPMG Sourcing Advisory 4Q13 Global Pulse Survey / January 2014 17

© 2014 KPMG International Cooperative (“KPMG International”). KPMG International provides no client services

and is a Swiss entity with which the independent member firms of the KPMG network are affiliated.

KPMG, in conjunction with HfS Research, released in 4Q13 the results of a major new market study on the state of the global business services market. It complements and extends KPMG ongoing market research effort on GBS maturity. The market study examines the uptake of GBS, drivers and benefits sought, key success factors, global GBS expenditure levels, and key the attributes of more mature GBS organizations in areas such as governance, end-to-end process management, data analytics and talent management.

Figure 2 | Advisors: Top Functional Focus Areas for Service Delivery Improvement Efforts

4Q13 Global Pulse Survey | Market Conditions

18 Shared Services and Outsourcing Advisory / KPMG Sourcing Advisory 4Q13 Global Pulse Survey / January 2014

© 2014 KPMG International Cooperative (“KPMG International”). KPMG International provides no client services

and is a Swiss entity with which the independent member firms of the KPMG network are affiliated.

KPMG firms’ professionals were next polled on the change in demand or usage levels over the past one to two quarters, and expected change in usage levels over the coming one to two quarters, across four different categories of business and IT sourcing models employed in service delivery improvement efforts. These categories are shared services, internal process improvement efforts, ITO, and BPO (see Figures 3, 4, and 5)

• Internal process improvement efforts, identified by 45 percent of advisors, down 12 percent from last quarter (see Figure 3), was again the top-cited area of demand tied. Shared services was ranked second but fell over 10 percent from last quarter from 54 to 39 percent. The number of advisors citing demand growth for ITO also fell from 44 to 31 percent, while BPO demand growth citations fell eight points from last quarter to 28 percent. Just five percent of advisors, however, cited decreasing levels of demand for BPO, the lowest level scored over the life of the Pulse survey conducted by KPMG. BPO growth expectations, especially for FAO, continue stronger in more specialized areas such as industry-specific BPO over more generic horizontal BPO. These deals are smaller and more diverse and increasingly employ cloud based options that are becoming more appealing to buyers than traditional hosted BPO models, especially in functions such as HR.

Figure 3 | Advisors: Demand by Service Delivery Model, Past 1–2 Quarters

Figure 4 | Advisors: Demand by Service Delivery Model, Next 1–2 Quarters

4Q13 Global Pulse Survey | Market Conditions

Shared Services and Outsourcing Advisory / KPMG Sourcing Advisory 4Q13 Global Pulse Survey / January 2014 19

© 2014 KPMG International Cooperative (“KPMG International”). KPMG International provides no client services

and is a Swiss entity with which the independent member firms of the KPMG network are affiliated.

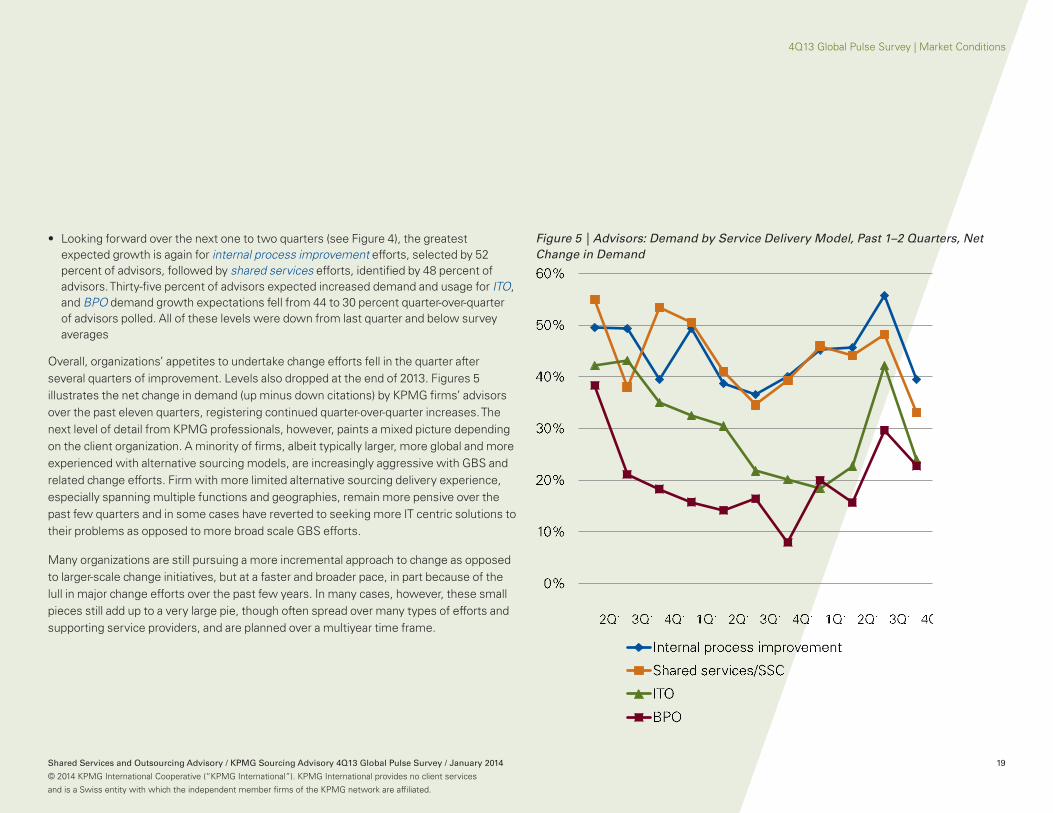

• Looking forward over the next one to two quarters (see Figure 4), the greatest expected growth is again for internal process improvement efforts, selected by 52 percent of advisors, followed by shared services efforts, identified by 48 percent of advisors. Thirty-five percent of advisors expected increased demand and usage for ITO, and BPO demand growth expectations fell from 44 to 30 percent quarter-over-quarter of advisors polled. All of these levels were down from last quarter and below survey averages

Overall, organizations’ appetites to undertake change efforts fell in the quarter after several quarters of improvement. Levels also dropped at the end of 2013. Figures 5 illustrates the net change in demand (up minus down citations) by KPMG firms’ advisors over the past eleven quarters, registering continued quarter-over-quarter increases. The next level of detail from KPMG professionals, however, paints a mixed picture depending on the client organization. A minority of firms, albeit typically larger, more global and more experienced with alternative sourcing models, are increasingly aggressive with GBS and related change efforts. Firm with more limited alternative sourcing delivery experience, especially spanning multiple functions and geographies, remain more pensive over the past few quarters and in some cases have reverted to seeking more IT centric solutions to their problems as opposed to more broad scale GBS efforts.

Many organizations are still pursuing a more incremental approach to change as opposed to larger-scale change initiatives, but at a faster and broader pace, in part because of the lull in major change efforts over the past few years. In many cases, however, these small pieces still add up to a very large pie, though often spread over many types of efforts and supporting service providers, and are planned over a multiyear time frame.

Figure 5 | Advisors: Demand by Service Delivery Model, Past 1–2 Quarters, Net Change in Demand

4Q13 Global Pulse Survey | Market Conditions

Business and IT Service Providers Market Demand Assessments

20 Shared Services and Outsourcing Advisory / KPMG Sourcing Advisory 4Q13 Global Pulse Survey / January 2014

© 2014 KPMG International Cooperative (“KPMG International”). KPMG International provides no client services

and is a Swiss entity with which the independent member firms of the KPMG network are affiliated.

KPMG polled leading global business and IT service providers on the current and expected growth levels in their pipelines for services deals. Providers polled are bullish this quarter on pipeline growth. While solid pipeline growth is cited, as always it remains to be seen how quickly this growth will result in signed deals though commentary from providers indicate that the pace of deal flow through the pipeline is quickening compared to earlier this year. The degree to which this is the case continues to vary widely, however, across individuals and classes of providers and functional areas in scope.

Figure 6 | Service Providers: Pipeline Growth Last Quarter• Seventy-two percent of service providers cited pipeline growth over the past quarter, a rise of seven percent from last quarter’s Pulse (see Figure 6) and above the average score of 65 percent over the life of the Pulse as conducted by KPMG. It is important to note that the Pulse surveys measure change in pipeline growth levels, not absolute pipeline size or revenue levels.

4Q13 Global Pulse Survey | Market Conditions

Shared Services and Outsourcing Advisory / KPMG Sourcing Advisory 4Q13 Global Pulse Survey / January 2014 21

© 2014 KPMG International Cooperative (“KPMG International”). KPMG International provides no client services

and is a Swiss entity with which the independent member firms of the KPMG network are affiliated.

• Seventy-two percent of providers expected the pace of customer demand for business and IT services to increase over the next one to two quarters (see Figure 7), up five percent from the 3Q13 poll and above the survey average of 62 percent.

Figure 7 | Service Providers: Demand Next 1–2 Quarters

4Q13 Global Pulse Survey | Market Conditions

22 Shared Services and Outsourcing Advisory / KPMG Sourcing Advisory 4Q13 Global Pulse Survey / January 2014

© 2014 KPMG International Cooperative (“KPMG International”). KPMG International provides no client services

and is a Swiss entity with which the independent member firms of the KPMG network are affiliated.

Bundled business functions with IT, cited by 60 percent of respondents, was the top ranked functional area of demand, supplanting ITO, which slipped to third place and was cited by 48 percent of advisors, as was F&A. Ranked second was vertical industry specific services selected by 56 percent of providers polled. This trending further illustrates the ongoing specialization of outsourcing demand with buyers’ preferences moving more towards bundled services and industry specific offerings. While the services are often more valuable and strategic to buyers, the deals are often smaller for providers and the skills required to deliver them more demanding. This increased required level of skill and experience for providers and is one of the drivers for buyers’ increased use of shared services as an outsourcing alternative. This is often more a response to inadequate capabilities available in the market than a marked preference to shared services over of outsourcing.

Figure 8 | Service Providers: Top Functional Areas of Demand

4Q13 Global Pulse Survey | Market Conditions

Shared Services and Outsourcing Advisory / KPMG Sourcing Advisory 4Q13 Global Pulse Survey / January 2014 23

© 2014 KPMG International Cooperative (“KPMG International”). KPMG International provides no client services

and is a Swiss entity with which the independent member firms of the KPMG network are affiliated.

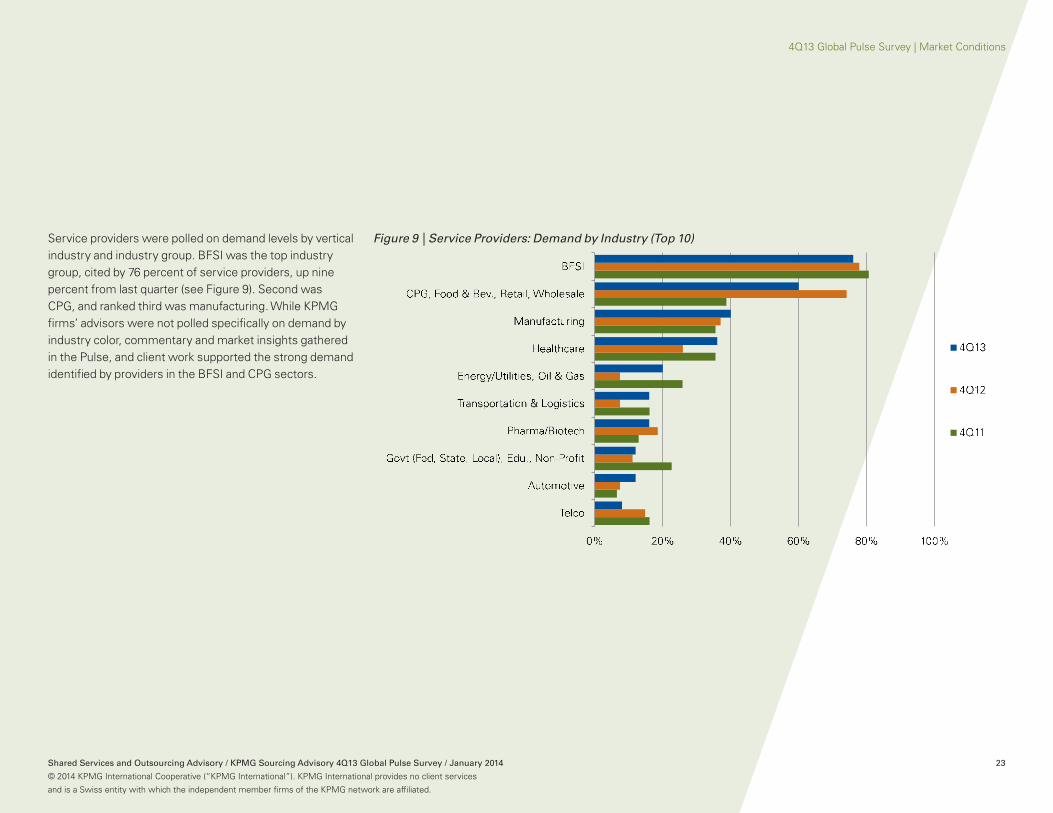

Service providers were polled on demand levels by vertical industry and industry group. BFSI was the top industry group, cited by 76 percent of service providers, up nine percent from last quarter (see Figure 9). Second was CPG, and ranked third was manufacturing. While KPMG firms’ advisors were not polled specifically on demand by industry color, commentary and market insights gathered in the Pulse, and client work supported the strong demand identified by providers in the BFSI and CPG sectors.

Figure 9 | Service Providers: Demand by Industry (Top 10)

4Q13 Global Pulse Survey | Market Conditions

24 Shared Services and Outsourcing Advisory / KPMG Sourcing Advisory 4Q13 Global Pulse Survey / January 2014

© 2014 KPMG International Cooperative (“KPMG International”). KPMG International provides no client services

and is a Swiss entity with which the independent member firms of the KPMG network are affiliated.

The next section of the quarterly Sourcing Advisory Pulse survey assesses the characteristics of current outsourcing and third-party services deals in the market from the perspective of the business and IT service providers polled.

Pricing Competitiveness

Exerting pressure on pricing on suppliers is a perennial and fundamental element of any buyer/service provider negotiation and relationship. While most buyers today recognize, at least philosophically, that major services or outsourcing efforts should embody more of a partnership or strategic relationship approach than a simple buyer/vendor transaction, this does not mean buyers will cave-in on price. While buyers are focusing more on process improvement over pure cost reduction in GBS efforts, they still want support for this improvement to come as a very good price. Providers that can illustrate how they can enable meaningful and measureable process improvement, however, are in a better position to charge a premium for their services.

Difficult economic times over the past several years have heightened the focus on price and cost of services. And despite the conceptual recognition of the need to approach major outsourcing efforts, for example, as a partnership with the service provider, in the heat of the negotiations and when cost conscious procurement organization are leading efforts, price becomes even more of a narrow focus.

This being said, realistic buyer expectations around pricing are critical to the success of services efforts. As buyers increasingly view GBS efforts as a means to drive value as much as, or more than, reducing costs, the discussion of pricing and pricing pressure takes on new dimensions. When buyers seek more lofty goals from their use of third-party services such as “innovation” or “transformation,” realistic pricing becomes even more important. Many buyers are locking in target year-over-year cost reductions for their GBS operations as a standard performance metric, and shifting the majority of focus to other goals beyond achieving this cost savings that is assumed a given.

Current Market Deal Characteristics: Service Providers’ Perspectives

4Q13 Global Pulse Survey | Market Conditions

Shared Services and Outsourcing Advisory / KPMG Sourcing Advisory 4Q13 Global Pulse Survey / January 2014 25

© 2014 KPMG International Cooperative (“KPMG International”). KPMG International provides no client services

and is a Swiss entity with which the independent member firms of the KPMG network are affiliated.

This approach extends to the use of service providers where costs savings are expected, but the focus is on what additional benefits providers can deliver. All this said, service providers polled in the Pulse survey typically cite pricing pressure as a major factor in client negotiations.

Thirty-two percent of service providers polled, down 12 percent from last quarter, indicate that pricing pressure increased in the quarter, while the 68 percent of service providers indicated they saw little or no change in pricing pressure (see Figure 10). The discussion around which class of service provider (e.g., India-based, legacy IT, regional, multifunction, multinational) is evolving, especially among India-based providers or providers with extensive operations in India. The differentiation today is more about a set of capabilities and offerings, vertical industry expertise, platform BPO capabilities, and strength of delivering strategic services. Providers weak in these areas regardless of their heritage or geographic footprint face the most pricing pressure in the market as their service offerings, as well as brands, commoditize.

Figure 10 | Service Providers: Pricing Pressure

Note: numbers may not total 100% due to rounding.

4Q13 Global Pulse Survey | Market Conditions

26 Shared Services and Outsourcing Advisory / KPMG Sourcing Advisory 4Q13 Global Pulse Survey / January 2014

© 2014 KPMG International Cooperative (“KPMG International”). KPMG International provides no client services

and is a Swiss entity with which the independent member firms of the KPMG network are affiliated.

Contract Profitability and Ability to Increase Scope

Service providers are naturally very focused on growing the business in existing clients. Success rates are higher, pursuit costs lower, and often additional services added to scope are more strategic and hence more lucrative and profitable. As such profitability is ideally higher in more mature and expansive deals and accounts, though other factors impact it such wage inflation and currency exchange rates and provider abilities to industrialize offerings and better leverage technologies over labor greatly impact profitability. Increased process automation, for example, can help provider profitability as well as reduce buyer costs. Greater use of cloud by buyers for commoditized IT services, however, as well as greater use of SaaS in lieu of traditional outsourcing, and increasingly commoditized horizontal BPO services increase margin pressure going forward on one-dimensional, technology-light and people-intensive service providers.

4Q13 Global Pulse Survey | Market Conditions

Shared Services and Outsourcing Advisory / KPMG Sourcing Advisory 4Q13 Global Pulse Survey / January 2014 27

© 2014 KPMG International Cooperative (“KPMG International”). KPMG International provides no client services

and is a Swiss entity with which the independent member firms of the KPMG network are affiliated.

Provider sentiment improved this quarter on their ability to improve contract profitability on new deals but fell back on existing deals (see Figures 11 and 12).

• Thirty-six percent of service providers polled, up 11 percent from last quarter and 21 percent from 2Q13, indicate that contract profitability is improving in new deals, with just four percent indicating a decline in new contract profitability.

Figure 11 | Service Providers: Contract Profitability, New Contracts

4Q13 Global Pulse Survey | Market Conditions

28 Shared Services and Outsourcing Advisory / KPMG Sourcing Advisory 4Q13 Global Pulse Survey / January 2014

© 2014 KPMG International Cooperative (“KPMG International”). KPMG International provides no client services

and is a Swiss entity with which the independent member firms of the KPMG network are affiliated.

• Twenty-nine percent of service providers expect to improve contract profitability in existing deals in flight for more than one year, down nine percent from last quarter and in line with the survey average, while eight percent indicate existing deal profitability is declining.

Figure 12 | Service Providers: Contract Profitability, Existing Contracts

4Q13 Global Pulse Survey | Market Conditions

Shared Services and Outsourcing Advisory / KPMG Sourcing Advisory 4Q13 Global Pulse Survey / January 2014 29

© 2014 KPMG International Cooperative (“KPMG International”). KPMG International provides no client services

and is a Swiss entity with which the independent member firms of the KPMG network are affiliated.

Deal scope is another element that impacts service provider margins and profitability. Larger deals tend to offer more room for greater profits, though this is not always the case if they involve transactional and commoditized work. Doing more and broader work with a client should—from the provider’s perspective—ideally lead to doing more strategic, value-added, and more profitable work; though this presupposes the provider has the skills and credentials to perform more strategic work. Following this logic, if providers are able to expand scope in a client account, profitability should improve, but it can depend on the provider in question. Conversely, if a provider cannot improve profitability, it should question whether to push for broader scope in the account.

Figure 13 illustrates service provider expectations about their ability to increase scope, ideally in a profitable manner, in current accounts. Providers today are highly focused on growing business in existing accounts, not only because pursuit costs are lower than competing for new business, but also because doing so protects their base as buyers rationalize suppliers and cut back on spend levels. Expectations on ability to increase scope over the past two years have been high, though they slipped a bit in 1Q13 but have rebounded to 79 percent in 4Q13.

Figure 13 | Service Providers: Ability to Increase Deal Scope

4Q13 Global Pulse Survey | Trends

30 Shared Services and Outsourcing Advisory / KPMG Sourcing Advisory 4Q13 Global Pulse Survey / January 2014

© 2014 KPMG International Cooperative (“KPMG International”). KPMG International provides no client services

and is a Swiss entity with which the independent member firms of the KPMG network are affiliated.

Trends

KPMG, on a quarterly basis, publishes an outsourcing deal tracking report. Results

from the most recent, 3Q13 edition of that report are available via this link. KPMG and

research firm HfS Research earlier this year released a global market study entitled State

of the Outsourcing Industry 2013: Executive Findings, which examines global trends, themes,

and adoptions partners of ITO and BPO as well as related shared services and global business services

efforts. Those interested in outsourcing market size and growth projection figures should check out HfS

Research’s new Market Index program.

Outsourcing Market Macro Trends

4Q13 Global Pulse Survey | Trends

Shared Services and Outsourcing Advisory / KPMG Sourcing Advisory 4Q13 Global Pulse Survey / January 2014 31

© 2014 KPMG International Cooperative (“KPMG International”). KPMG International provides no client services

and is a Swiss entity with which the independent member firms of the KPMG network are affiliated.

“““

““““

“““

KPMG firms’ advisors offered the following comments on GBS trending and service delivery improvement efforts:

Organizations are no longer viewing technology in isolation from the way in which their business operates. Executives are requiring services, which they know will be delivered and supported by IT, to run and optimize their business, but they aren’t tied in to who delivers them – internal or external – or how. Increasingly the focus is on trying to commoditize aspects of the IT landscape to drive competition and create greater overall efficiencies.

GBS is hot. Use it as a model and framework to get more value out of existing sourcing models in a globally consistent way. Also, expand its usage into areas such as data analytics.

As more organizations recognize they are getting diminishing returns from traditional cost reduction mechanisms – offshore, labor arbitrage, lift and shift – they are looking to models such as global business services to take them to the next level of cost savings, for example, via global optimization and greater process automation.

Organizations that ‘get’ GBS and can execute it well will increasingly gain meaningful competitive advantage via a higher performing, more cost effective and more flexible back office operating environment.

Progressive firms today recognize they have reached a near practical limit in driving down costs via shared services and outsourcing and are shifting focus to use a GBS model to drive process improvement and increase competitiveness. Process automation, analytics, end-to-end process ownership on a global scale and other GBS dictums will enable this.

Data and analytics, both as a GBS provided service as well as a tool to improve GBS operational performance, is very hot among more experienced GBS organizations.

Despite high unemployment levels in the West, ‘skilled’ talent shortages continue to drive globalization of shared services and outsourcing. Many GBS operations themselves, however, struggle with talent management issues and needs.

Service providers polled offered these comments on general market trends:

As more and more clients understand the linkages between business and IT more bundled offerings will be required in the space. This is especially the case with tier 2 clients which have limited exposure to global business services.

Economic growth, global expansion, and a better educated market will decrease political reluctance to outsource, as will new cloud based services models.

There is an insatiable demand for SMAC (Social, Mobile, Analytics, Cloud) which will accelerate demand for cloud and infrastructure technology services.

4Q13 Global Pulse Survey | Trends

32 Shared Services and Outsourcing Advisory / KPMG Sourcing Advisory 4Q13 Global Pulse Survey / January 2014

© 2014 KPMG International Cooperative (“KPMG International”). KPMG International provides no client services

and is a Swiss entity with which the independent member firms of the KPMG network are affiliated.

KPMG annually polls its professionals globally as well as leading business and IT service providers in each 4Q edition of the quarterly Pulse on what are their top business and IT trends and predictions for the coming year. The focus is both on trends and predictions as they relate to global business services as well as on broader market trends. Last year’s predictions can be found here.

Buyer Global Sourcing Preferences and Demand Levels

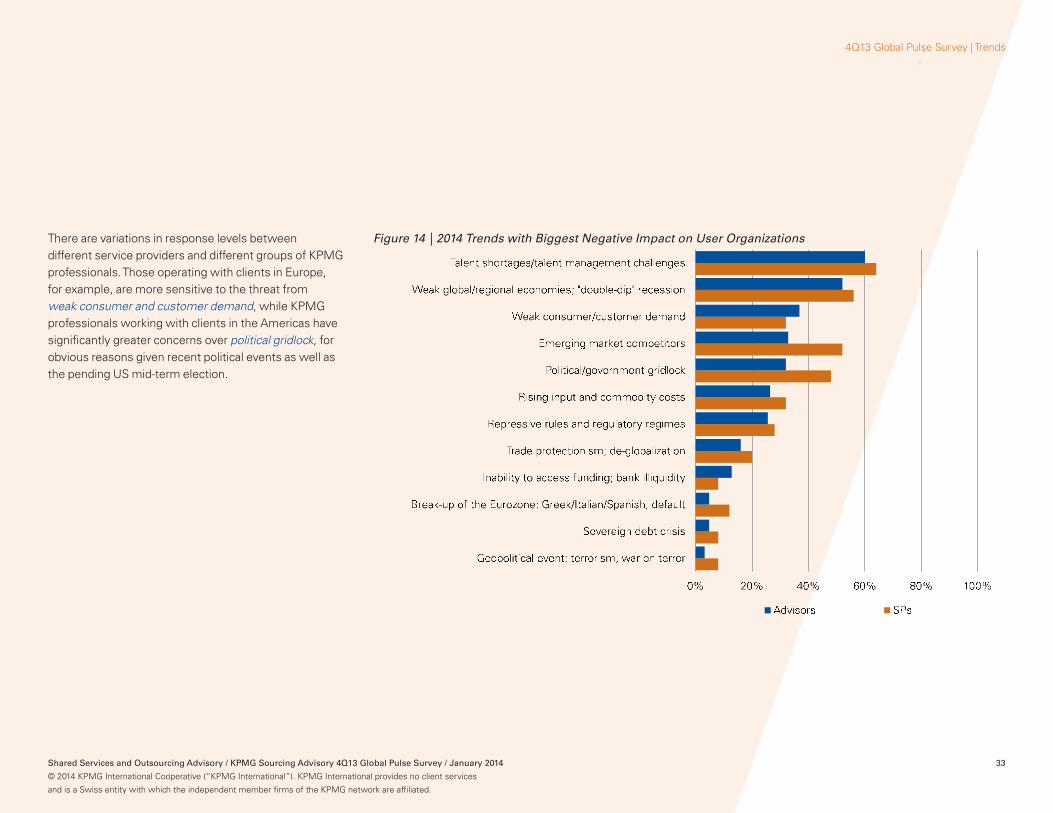

KPMG first polled third-party service providers and its professionals globally on what market events or conditions they predict will have the biggest negative impact on their clients’ and prospects’ business operations in 2014 (see Figure 14). For the first five of the trend questions, each respondent could select up to five responses.

• There was consensus between service providers and KPMG professionals on the expected top negative trends of 2014. Sixty percent of KPMG professionals and 64 percent of providers polled cited talent shortages and talent management challenges as likely having the biggest negative impact on user organizations. Talent shortages is a recurring theme across KPMG research and a key driver for increased adoption of a GBS model and framework. The converse is that organizations that can improve and excel at talent management can leverage this for meaningful competitive advantage. Recent KPMG research on the “intelligent” finance function bore this out.

• Coming in second according to both constituencies was weak global or regional economies or a “double-dip” recession which had been ranked first the past two years. Perceived economic challenges vary widely by geography and industry.

• KPMG professionals rank third weak consumer or customer demand, a by-product of, and contributor to, ongoing weak economic conditions. Thirty-two percent of service providers selected this trend. Service providers rank emerging market competitors third while advisors rank it fourth.

Top 2014 Trends and Predictions

4Q13 Global Pulse Survey | Trends

Shared Services and Outsourcing Advisory / KPMG Sourcing Advisory 4Q13 Global Pulse Survey / January 2014 33

© 2014 KPMG International Cooperative (“KPMG International”). KPMG International provides no client services

and is a Swiss entity with which the independent member firms of the KPMG network are affiliated.

There are variations in response levels between different service providers and different groups of KPMG professionals. Those operating with clients in Europe, for example, are more sensitive to the threat from weak consumer and customer demand, while KPMG professionals working with clients in the Americas have significantly greater concerns over political gridlock, for obvious reasons given recent political events as well as the pending US mid-term election.

Figure 14 | 2014 Trends with Biggest Negative Impact on User Organizations

4Q13 Global Pulse Survey | Trends

34 Shared Services and Outsourcing Advisory / KPMG Sourcing Advisory 4Q13 Global Pulse Survey / January 2014

© 2014 KPMG International Cooperative (“KPMG International”). KPMG International provides no client services

and is a Swiss entity with which the independent member firms of the KPMG network are affiliated.

Looking on the brighter side of things, service providers and KPMG professionals were polled on what market events or conditions they predict will have the biggest positive impact on their clients’ and prospects’ business operations in 2014 (see Figure 15).

• The top positive trend cited by 53 percent of KPMG professionals is maturation of and greater access to innovative technologies such as cloud, social media, and virtualization. Service providers ranked this trend second while both groups ranked this trend first in the 2013 poll. Service providers ranked expanding emerging market opportunities for selling goods and services first and KPMG professionals ranked it second in this year’s poll. This focus on expanding business emerging markets will continue to negatively impact growth in Western markets and contribute to high unemployment rates and weak tax basis, though to a lesser degree than over the past two years.

• Both advisors and providers are positive on improving consumer and customer demand and improving or rebounding global economic conditions, with providers more bullish than KPMG professionals on the latter trend. The percentage of service providers citing the ability to tap into skilled global talent pools fell by 16 percent year over year.

Figure 15 | 2014 Trends with Biggest Positive Impact on User Organizations

4Q13 Global Pulse Survey | Trends

Shared Services and Outsourcing Advisory / KPMG Sourcing Advisory 4Q13 Global Pulse Survey / January 2014 35

© 2014 KPMG International Cooperative (“KPMG International”). KPMG International provides no client services

and is a Swiss entity with which the independent member firms of the KPMG network are affiliated.

Top Client Initiatives

KPMG next polled its professionals globally and third-party service providers on the top initiatives their clients are undertaking in 2014 (see Figure 16).

• The top initiative cited by 63 percent KPMG professionals and 67 percent of service providers (down 26 percent year over year) is continue to drive down operating costs. This remains a constant theme in the market today though it is increasingly part of a bundle of key initiatives addressing both the bottom and top business lines. The challenge for organizations is how to balance the desire to drive down costs with the needs of the other top initiatives identified, most of which require making investments.

• The second most popular initiative cited by 53 percent of advisors and 63 percent of service providers is invest in new and improved information technology applications and systems. Keeping with the talent theme, 63 percent of service providers also identified find, attract and retain talent globally as a top initiative for 2014. This score was up 39 percent year over year.

Figure 16 | Top 2014 User Organization Initiatives

4Q13 Global Pulse Survey | Trends

36 Shared Services and Outsourcing Advisory / KPMG Sourcing Advisory 4Q13 Global Pulse Survey / January 2014

© 2014 KPMG International Cooperative (“KPMG International”). KPMG International provides no client services

and is a Swiss entity with which the independent member firms of the KPMG network are affiliated.

Top Challenges to and Enablers for Initiatives

Next, KPMG examined the perceived greatest challenges organizations face in successfully undertaking the initiatives outlined above. On a positive note, despite the strong emphasis cited on continuing to drive down operating costs, lack of access to capital, poor liquidity and inadequate funds to invest are not expected to present major hurdles to achieving key initiatives.

• The top challenge cited by 68 percent of KPMG professionals and 67 percent of service providers is dysfunctional or fragmented organizational and operating models, designs, and processes (see Figure 17). This has been the top challenge cited the past three years and is not an easy one to overcome, regardless of funding levels.

• The second most frequent challenge, cited by 57 percent of KPMG professionals, is inadequate or antiquated IT infrastructure and systems. Service providers ranked inability to innovate second and lack of adequate and skilled talent and an inability to attract and retain talent third.

Figure 17 | Top Challenges to Successfully Undertaking 2014 Initiatives

4Q13 Global Pulse Survey | Trends

Shared Services and Outsourcing Advisory / KPMG Sourcing Advisory 4Q13 Global Pulse Survey / January 2014 37

© 2014 KPMG International Cooperative (“KPMG International”). KPMG International provides no client services

and is a Swiss entity with which the independent member firms of the KPMG network are affiliated.

The next 2014 prediction was on the top capabilities organizations will need to possess to successfully undertake their top initiatives. Here again, a broad range of capabilities were identified.

• The top capability cited by 50 percent of KPMG professionals and 61 percent of third party service providers is the need for smart and innovative management and management practices (see Figure 18). This is a potential elixir for the challenges of dysfunctional organizational and operating models cited above.

• The importance of global business services and related alternative service delivery models were given strong support by both KPMG professionals and third party service providers. Advisors ranked alternative service delivery models such as shared services and outsourcing second while service providers rank it third. Ranked second by providers and third by advisors was GBS as manifested in the integrated and consistent global service delivery models. Service providers are also bullish on the importance of business intelligence and the harnessing “big data”.

• There was general consensus among advisors across geographies, though those in EMEA are less concerned with harnessing big data and more focused on the importance of adequate access to capital and funding. Those supporting Asia Pacific were more likely to cite the importance of information technology systems and capabilities beyond cloud.

Figure 18 | Top Capabilities Required to Successfully Undertake Top 2014 Initiatives

4Q13 Global Pulse Survey | Trends

38 Shared Services and Outsourcing Advisory / KPMG Sourcing Advisory 4Q13 Global Pulse Survey / January 2014

© 2014 KPMG International Cooperative (“KPMG International”). KPMG International provides no client services

and is a Swiss entity with which the independent member firms of the KPMG network are affiliated.

KPMG added three new additional trending questions for 2014. The first examines expected investment trending in a variety of operational areas, the second digs deeper into investments into data and analytics while the third assesses general market trending at the country, market and regional level.

KPMG professionals and third party service providers were asked whether typical clients would likely invest the more, the same, or less across 12 areas in 2014 (see Figures 19 and 20). The ordering of the results in the charts reflect top rankings for areas where clients are most likely to invest more this year, though this does not always imply that the lowest ranked areas are most likely to receive less investment.

• There was a three way tie among KPMG professionals for the area most likely to receive move investment in 2014 than in 2013. These three areas are cloud software and services, data and analytics software and services, and global business services or integrated shared services and outsourcing staff & resources. Each category was selected by 51 percent of advisors.

Figure 19 | Advisors: Investment Levels 2014 Compared to 2013

4Q13 Global Pulse Survey | Trends

Shared Services and Outsourcing Advisory / KPMG Sourcing Advisory 4Q13 Global Pulse Survey / January 2014 39

© 2014 KPMG International Cooperative (“KPMG International”). KPMG International provides no client services

and is a Swiss entity with which the independent member firms of the KPMG network are affiliated.

• While over 50 percent of service providers polled selected the top three categories identified by advisors, the overall top categories selected by third party providers are data and analytics software and services, mobility and cloud infrastructure. Over 60 percent of providers polled also selected data and analytics staff and resources.

Figure 20 | Service Providers: Investment Levels 2014 Compared to 2013

4Q13 Global Pulse Survey | Trends

40 Shared Services and Outsourcing Advisory / KPMG Sourcing Advisory 4Q13 Global Pulse Survey / January 2014

© 2014 KPMG International Cooperative (“KPMG International”). KPMG International provides no client services

and is a Swiss entity with which the independent member firms of the KPMG network are affiliated.

Next the Pulse looked specifically at investments into data and analytics to support their global business services, shared services and outsourcing efforts over the next 24 months. KPMG professionals and third party providers were asked where their typical client accounts would most heavily invest across seven dimensions of data and analytics.

• The top category identified by both advisors and providers is analytical tools such as those for business intelligence, business performance management and enterprise performance management (see Figure 21). This is the only category selected by over 50 percent of KPMG professionals globally.

• Ranked second by providers (perhaps wishful thinking) is third party analytical services along with hiring more global business services staff with analytics skills while advisors ranked foundational infrastructure capabilities second

Figure 21 | GBS Data & Analytics Investments Next 24 Months

4Q13 Global Pulse Survey | Trends

Shared Services and Outsourcing Advisory / KPMG Sourcing Advisory 4Q13 Global Pulse Survey / January 2014 41

© 2014 KPMG International Cooperative (“KPMG International”). KPMG International provides no client services

and is a Swiss entity with which the independent member firms of the KPMG network are affiliated.

The final question on 2014 trending focused on how KPMG professionals and third party service providers expect conditions to change (improve, stay the same or worsen) across 13 general socioeconomic and geopolitical issues and topics in their respective countries, markets and regions in 2014 and 2015. As with the prior question on investments, the ordering of the results in the charts (see figures 22 and 23) reflect top ranking for areas where clients are most likely to invest more this year, though this does not always imply that the lowest ranked areas are most likely to receive less investment. Overall both advisors and service providers are pessimistic regarding market trending across these topics.

• No topic was cited as improving by more than 50 percent of KPMG professionals polled (see Figure 22). The most optimism is for national economic growth where 40 percent of advisors polled expect improvement over the next two years. EMEA advisors are the most optimistic on economic growth as 55 percent did cite improvement in this area. A distant second overall was for improved quality and accessibility of healthcare. The most pessimism was around cost of healthcare and cost of living and inflation. Advisors in the Asia Pacific region are the most negative on inflation.

Figure 22 | Advisors: Change in Market Conditions 2014-15

4Q13 Global Pulse Survey | Trends

42 Shared Services and Outsourcing Advisory / KPMG Sourcing Advisory 4Q13 Global Pulse Survey / January 2014

© 2014 KPMG International Cooperative (“KPMG International”). KPMG International provides no client services

and is a Swiss entity with which the independent member firms of the KPMG network are affiliated.

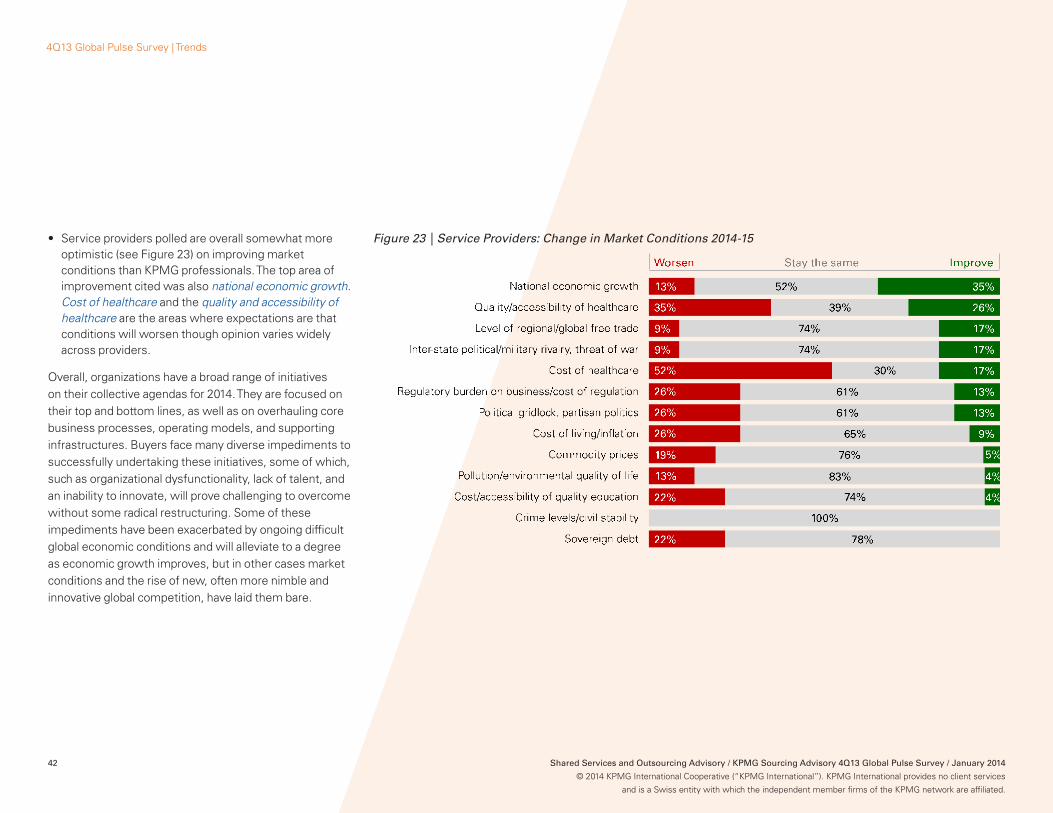

• Service providers polled are overall somewhat more optimistic (see Figure 23) on improving market conditions than KPMG professionals. The top area of improvement cited was also national economic growth. Cost of healthcare and the quality and accessibility of healthcare are the areas where expectations are that conditions will worsen though opinion varies widely across providers.

Overall, organizations have a broad range of initiatives on their collective agendas for 2014. They are focused on their top and bottom lines, as well as on overhauling core business processes, operating models, and supporting infrastructures. Buyers face many diverse impediments to successfully undertaking these initiatives, some of which, such as organizational dysfunctionality, lack of talent, and an inability to innovate, will prove challenging to overcome without some radical restructuring. Some of these impediments have been exacerbated by ongoing difficult global economic conditions and will alleviate to a degree as economic growth improves, but in other cases market conditions and the rise of new, often more nimble and innovative global competition, have laid them bare.

Figure 23 | Service Providers: Change in Market Conditions 2014-15

4Q13 Global Pulse Survey | Trends

Shared Services and Outsourcing Advisory / KPMG Sourcing Advisory 4Q13 Global Pulse Survey / January 2014 43

© 2014 KPMG International Cooperative (“KPMG International”). KPMG International provides no client services

and is a Swiss entity with which the independent member firms of the KPMG network are affiliated.

4Q13 Global Pulse Survey | Learn More

44 Shared Services and Outsourcing Advisory / KPMG Sourcing Advisory 4Q13 Global Pulse Survey / January 2014

© 2014 KPMG International Cooperative (“KPMG International”). KPMG International provides no client services

and is a Swiss entity with which the independent member firms of the KPMG network are affiliated.

KPMG Online Research Portals and Blogs

• KPMG Shared Services and Outsourcing Institute

• KPMG Advisory Institute

• KPMG Management Consulting Blog: Advice Worth Keeping

• KPMG Management Consulting Podcast Series: Advice Worth Keeping

• Directory of all KPMG Institutes

• KPMG Competitive Alternatives – global sourcing location assessment services

Where to Learn More about Global Sourcing Market Trends

Learn More

4Q13 Global Pulse Survey | Learn More

Shared Services and Outsourcing Advisory / KPMG Sourcing Advisory 4Q13 Global Pulse Survey / January 2014 45

© 2014 KPMG International Cooperative (“KPMG International”). KPMG International provides no client services

and is a Swiss entity with which the independent member firms of the KPMG network are affiliated.

All IT BP All Function Global Americas EMEA AsiaPac

Top Approaches to Change

Improve current SSC/outsourcing governance 62% 69% 61% 55% 61% 67% 68% 50%

Internal process improvement/re-engineering efforts 49% 40% 54% 52% 46% 51% 38% 55%

Investments into/improvements to enterprise software systems 21% 26% 28% 14% 20% 24% 22% 27%

Investments into cloud computing services 24% 35% 16% 19% 24% 22% 43% 36%

Use/expansion of SSCs 47% 35% 55% 52% 48% 53% 32% 50%

Use/expansion of offshore captive SSCs 17% 12% 19% 17% 24% 9% 8% 32%

Use/expansion of ITO 36% 53% 24% 38% 33% 40% 43% 36%

Use/expansion of BPO 25% 19% 37% 21% 24% 36% 11% 23%

Insourcing work previously outsourced 9% 9% 5% 17% 13% 11% 5% 9%

Bringing work performed offshore back onshore 2% 3% 5% 0% 7% 4% 0% 0%

Nothing/major improvements not required 2% 0% 0% 2% 0% 0% 5% 0%

Nothing/lack of ambition/execute support/funding 2% 2% 3% 0% 0% 0% 8% 0%

Appendix Key Questions by Advisors’ Primary Geography and Outsourcing Focus Area

4Q13 Global Pulse Survey | Learn More

46 Shared Services and Outsourcing Advisory / KPMG Sourcing Advisory 4Q13 Global Pulse Survey / January 2014

© 2014 KPMG International Cooperative (“KPMG International”). KPMG International provides no client services

and is a Swiss entity with which the independent member firms of the KPMG network are affiliated.

All IT BP All Function Global Americas EMEA AsiaPac

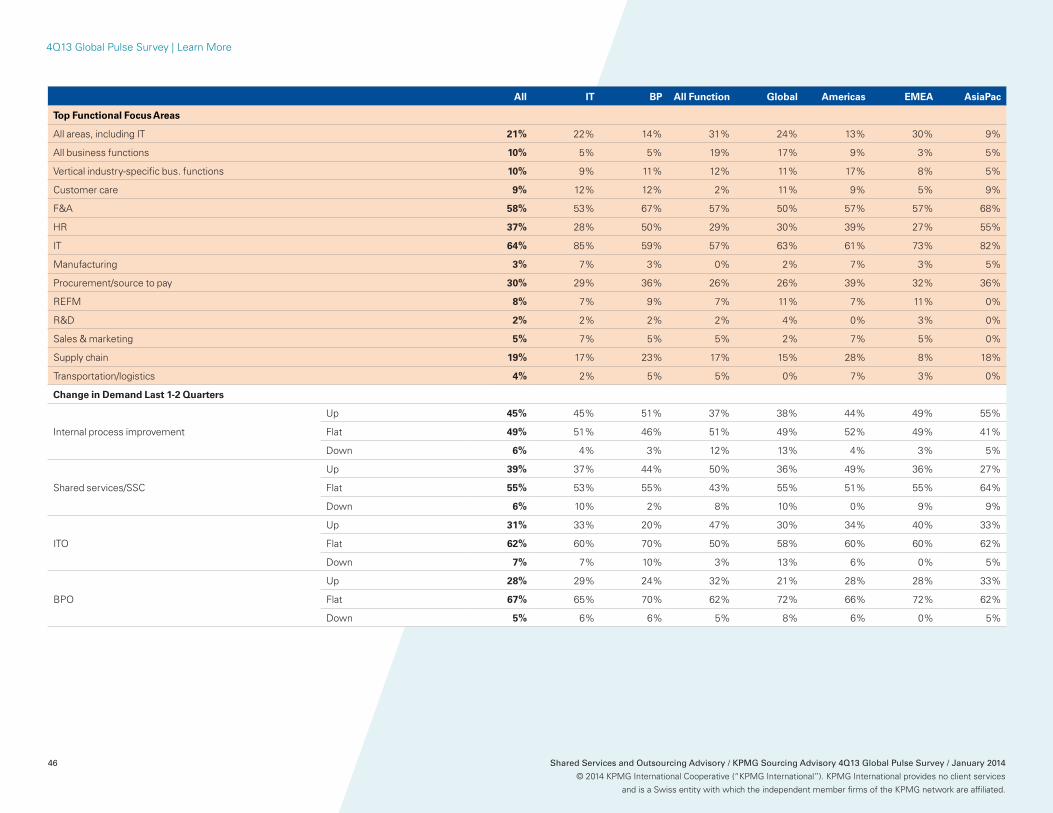

Top Functional Focus Areas

All areas, including IT 21% 22% 14% 31% 24% 13% 30% 9%

All business functions 10% 5% 5% 19% 17% 9% 3% 5%

Vertical industry-specific bus. functions 10% 9% 11% 12% 11% 17% 8% 5%

Customer care 9% 12% 12% 2% 11% 9% 5% 9%

F&A 58% 53% 67% 57% 50% 57% 57% 68%

HR 37% 28% 50% 29% 30% 39% 27% 55%

IT 64% 85% 59% 57% 63% 61% 73% 82%

Manufacturing 3% 7% 3% 0% 2% 7% 3% 5%

Procurement/source to pay 30% 29% 36% 26% 26% 39% 32% 36%

REFM 8% 7% 9% 7% 11% 7% 11% 0%

R&D 2% 2% 2% 2% 4% 0% 3% 0%

Sales & marketing 5% 7% 5% 5% 2% 7% 5% 0%

Supply chain 19% 17% 23% 17% 15% 28% 8% 18%

Transportation/logistics 4% 2% 5% 5% 0% 7% 3% 0%

Change in Demand Last 1-2 Quarters

Internal process improvement

Up 45% 45% 51% 37% 38% 44% 49% 55%

Flat 49% 51% 46% 51% 49% 52% 49% 41%

Down 6% 4% 3% 12% 13% 4% 3% 5%

Shared services/SSC

Up 39% 37% 44% 50% 36% 49% 36% 27%

Flat 55% 53% 55% 43% 55% 51% 55% 64%

Down 6% 10% 2% 8% 10% 0% 9% 9%

ITO

Up 31% 33% 20% 47% 30% 34% 40% 33%

Flat 62% 60% 70% 50% 58% 60% 60% 62%

Down 7% 7% 10% 3% 13% 6% 0% 5%

BPO

Up 28% 29% 24% 32% 21% 28% 28% 33%

Flat 67% 65% 70% 62% 72% 66% 72% 62%

Down 5% 6% 6% 5% 8% 6% 0% 5%

4Q13 Global Pulse Survey | Learn More

Shared Services and Outsourcing Advisory / KPMG Sourcing Advisory 4Q13 Global Pulse Survey / January 2014 47

© 2014 KPMG International Cooperative (“KPMG International”). KPMG International provides no client services

and is a Swiss entity with which the independent member firms of the KPMG network are affiliated.

All IT BP All Function Global Americas EMEA AsiaPac

Change in Demand Next 1-2 Quarters

Internal process improvement

Up 52% 48% 57% 46% 51% 49% 49% 59%

Flat 45% 50% 41% 46% 41% 49% 51% 36%

Down 3% 2% 2% 7% 8% 2% 0% 5%

Shared services/SSC

Up 48% 37% 48% 51% 52% 47% 34% 41%

Flat 47% 53% 48% 46% 43% 49% 56% 50%

Down 5% 10% 3% 2% 5% 4% 9% 9%

ITO

Up 35% 33% 21% 50% 35% 35% 40% 38%

Flat 61% 64% 72% 50% 63% 61% 60% 57%

Down 3% 4% 7% 0% 3% 4% 0% 5%

BPO

Up 30% 31% 23% 32% 31% 29% 35% 33%

Flat 64% 65% 71% 62% 64% 65% 58% 62%

Down 6% 4% 6% 5% 5% 6% 6% 5%

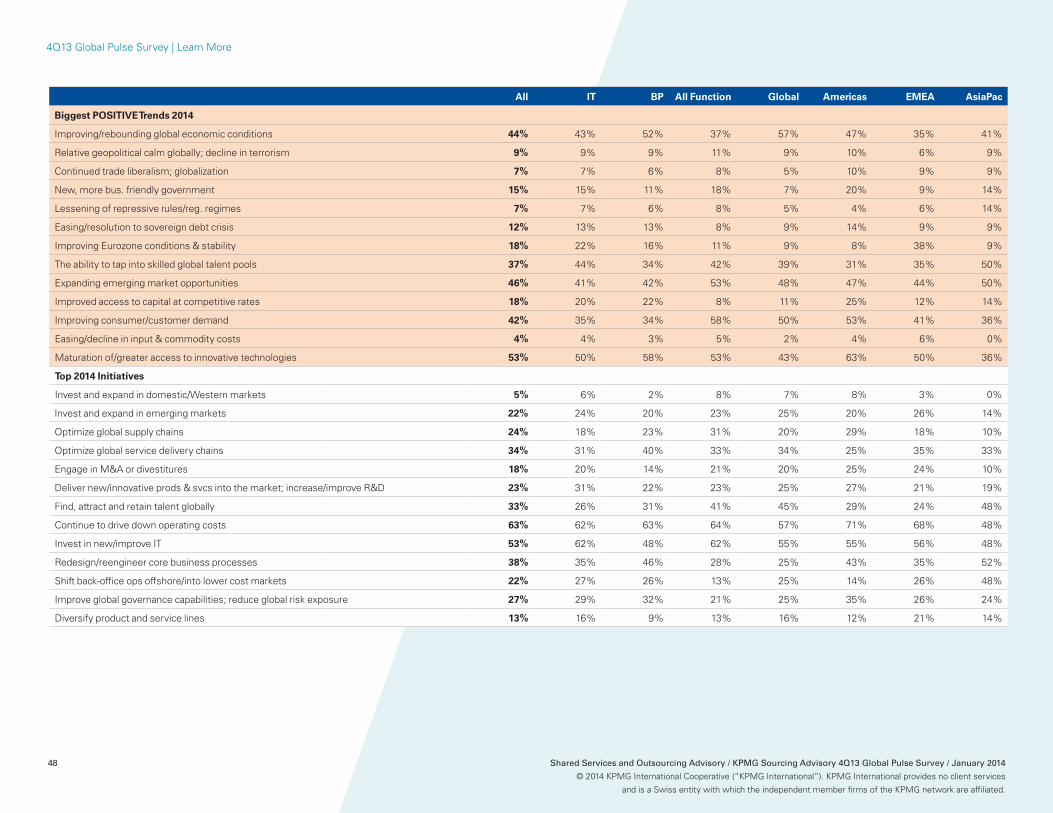

Biggest NEGATIVE Trends 2014

Weak global/regional economies; "double-dip" recession 52% 44% 53% 61% 56% 55% 47% 32%

Geopolitical event; terrorism; war on terror 3% 2% 3% 5% 2% 6% 0% 0%

Trade protectionism; de-globalization 16% 20% 16% 16% 16% 15% 21% 23%

Political/government gridlock 32% 22% 38% 42% 28% 53% 9% 18%

Repressive rules and regulatory regimes 26% 22% 25% 32% 26% 30% 29% 23%

Sovereign debt crisis 5% 9% 5% 0% 5% 2% 12% 9%

Break-up of the Eurozone; Greek/Italian/Spanish, et al default 5% 7% 5% 0% 2% 2% 12% 0%

Talent shortages/talent mgmnt challenges 60% 67% 59% 50% 65% 55% 56% 68%

Emerging market competitors 33% 29% 23% 45% 37% 30% 26% 32%

Inability to access funding; bank illiquidity 13% 13% 13% 11% 5% 13% 24% 9%

Weak consumer/customer demand 37% 40% 36% 32% 28% 30% 53% 50%

Rising input and commodity costs 26% 27% 23% 26% 9% 28% 29% 23%

4Q13 Global Pulse Survey | Learn More

48 Shared Services and Outsourcing Advisory / KPMG Sourcing Advisory 4Q13 Global Pulse Survey / January 2014

© 2014 KPMG International Cooperative (“KPMG International”). KPMG International provides no client services

and is a Swiss entity with which the independent member firms of the KPMG network are affiliated.

All IT BP All Function Global Americas EMEA AsiaPac

Biggest POSITIVE Trends 2014

Improving/rebounding global economic conditions 44% 43% 52% 37% 57% 47% 35% 41%

Relative geopolitical calm globally; decline in terrorism 9% 9% 9% 11% 9% 10% 6% 9%

Continued trade liberalism; globalization 7% 7% 6% 8% 5% 10% 9% 9%

New, more bus. friendly government 15% 15% 11% 18% 7% 20% 9% 14%

Lessening of repressive rules/reg. regimes 7% 7% 6% 8% 5% 4% 6% 14%

Easing/resolution to sovereign debt crisis 12% 13% 13% 8% 9% 14% 9% 9%

Improving Eurozone conditions & stability 18% 22% 16% 11% 9% 8% 38% 9%

The ability to tap into skilled global talent pools 37% 44% 34% 42% 39% 31% 35% 50%

Expanding emerging market opportunities 46% 41% 42% 53% 48% 47% 44% 50%

Improved access to capital at competitive rates 18% 20% 22% 8% 11% 25% 12% 14%

Improving consumer/customer demand 42% 35% 34% 58% 50% 53% 41% 36%

Easing/decline in input & commodity costs 4% 4% 3% 5% 2% 4% 6% 0%

Maturation of/greater access to innovative technologies 53% 50% 58% 53% 43% 63% 50% 36%

Top 2014 Initiatives

Invest and expand in domestic/Western markets 5% 6% 2% 8% 7% 8% 3% 0%

Invest and expand in emerging markets 22% 24% 20% 23% 25% 20% 26% 14%

Optimize global supply chains 24% 18% 23% 31% 20% 29% 18% 10%

Optimize global service delivery chains 34% 31% 40% 33% 34% 25% 35% 33%

Engage in M&A or divestitures 18% 20% 14% 21% 20% 25% 24% 10%

Deliver new/innovative prods & svcs into the market; increase/improve R&D 23% 31% 22% 23% 25% 27% 21% 19%

Find, attract and retain talent globally 33% 26% 31% 41% 45% 29% 24% 48%

Continue to drive down operating costs 63% 62% 63% 64% 57% 71% 68% 48%

Invest in new/improve IT 53% 62% 48% 62% 55% 55% 56% 48%

Redesign/reengineer core business processes 38% 35% 46% 28% 25% 43% 35% 52%

Shift back-office ops offshore/into lower cost markets 22% 27% 26% 13% 25% 14% 26% 48%

Improve global governance capabilities; reduce global risk exposure 27% 29% 32% 21% 25% 35% 26% 24%

Diversify product and service lines 13% 16% 9% 13% 16% 12% 21% 14%

4Q13 Global Pulse Survey | Learn More

Shared Services and Outsourcing Advisory / KPMG Sourcing Advisory 4Q13 Global Pulse Survey / January 2014 49

© 2014 KPMG International Cooperative (“KPMG International”). KPMG International provides no client services

and is a Swiss entity with which the independent member firms of the KPMG network are affiliated.

All IT BP All Function Global Americas EMEA AsiaPac

Biggest Challenges to 2014 Initiatives

Lack of access to capital; poor liquidity; inadequate funds to invest 10% 11% 9% 3% 0% 8% 21% 5%

Inadequate mgmnt/board skills & capabilities 40% 48% 42% 36% 35% 43% 56% 33%

Competitive pressures from traditional competitors 11% 7% 9% 21% 12% 12% 12% 24%

Competitive pressures from new/emerging market competitors 14% 6% 16% 18% 5% 18% 9% 14%

Inadequate/antiquated IT infrastructure & systems 57% 61% 61% 56% 51% 57% 62% 62%

Inadequate/fragmented global business services capabilities 32% 32% 34% 33% 40% 33% 21% 33%

Inadequate/antiquated local market physical infrastructure 13% 17% 8% 15% 14% 18% 6% 5%

Restrictive government trade policies 7% 11% 6% 5% 5% 12% 6% 10%

Restrictive government regulatory policies; hostile business environments 14% 11% 16% 10% 16% 14% 9% 5%

Lack of adequate & skilled talent; inability to attract &retain talent 40% 41% 39% 44% 35% 39% 47% 48%

Dysfunctional/fragmented org./operating models, designs & processes 68% 74% 70% 72% 72% 76% 68% 57%

Inability to innovate 40% 37% 42% 36% 35% 37% 47% 38%

Lack of global scale 18% 20% 19% 8% 16% 16% 24% 24%

Top Capabilities Required to Successfully Undertake Top 2014 Initiatives

Cloud computing 19% 26% 19% 15% 23% 24% 24% 10%

Creative use of social media 9% 13% 9% 3% 5% 6% 12% 10%

Business intelligence/harnessing "big data" 29% 20% 25% 44% 30% 39% 12% 19%

IT systems and capabilities beyond cloud 37% 48% 30% 36% 27% 35% 42% 52%

Alternative service delivery models such as shared services and outsourcing 48% 46% 55% 44% 36% 53% 48% 57%

Access to emerging market talent and skills at a low cost 19% 24% 20% 15% 27% 24% 15% 14%

The ability to find, attract and retain talent globally 36% 37% 38% 31% 34% 33% 39% 38%

Supportive local market trade policies 1% 0% 2% 0% 0% 2% 0% 0%

Supportive local market regulatory policies and regimes 8% 6% 8% 8% 7% 10% 6% 5%

Globally integrated supply chains 16% 15% 19% 18% 11% 22% 15% 10%

Global business services - globally integrated and consistent service delivery models 47% 40.7% 57.8% 49% 43% 57% 39% 38%

Adequate access to capital and funding 17% 22.2% 17.2% 8% 9% 18% 30% 19%

Smart/innovative management and management practices 50% 55.6% 50.0% 51% 50% 45% 48% 43%

Research and development capabilities 9% 11.1% 4.7% 13% 11% 10% 12% 5%

Strong global governance policies and procedures 35% 38.9% 40.6% 26% 43% 35% 39% 29%

Strong brand 9% 3.7% 10.9% 10% 11% 6% 9% 5%

4Q13 Global Pulse Survey | Learn More

50 Shared Services and Outsourcing Advisory / KPMG Sourcing Advisory 4Q13 Global Pulse Survey / January 2014

© 2014 KPMG International Cooperative (“KPMG International”). KPMG International provides no client services

and is a Swiss entity with which the independent member firms of the KPMG network are affiliated.

All IT BP All Function Global Americas EMEA AsiaPac

Investment Appetites in 2014

Talent and talent management

Invest Less 8% 8% 7% 8% 7% 10% 3% 5%

Invest Same 55% 52% 50% 57% 56% 55% 59% 53%

Invest More 38% 40% 43% 35% 37% 35% 38% 42%

Data and analytics software and services

Invest Less 6% 6% 7% 6% 6% 10% 6% 10%

Invest Same 43% 57% 52% 31% 42% 46% 41% 55%

Invest More 51% 37% 41% 63% 53% 44% 53% 35%

Data and analytics staff and resources

Invest Less 8% 9% 11% 6% 8% 12% 10% 11%

Invest Same 48% 62% 53% 39% 47% 53% 45% 47%

Invest More 44% 30% 37% 56% 45% 35% 45% 42%

Mobility

Invest Less 9% 11% 11% 11% 8% 8% 6% 11%

Invest Same 53% 47% 62% 46% 53% 63% 45% 44%

Invest More 38% 43% 27% 43% 39% 29% 48% 44%

Social media

Invest Less 8% 9% 7% 6% 8% 14% 6% 0%

Invest Same 57% 62% 62% 59% 62% 55% 48% 72%

Invest More 35% 30% 31% 35% 30% 31% 45% 28%

Cloud software and services

Invest Less 4% 4% 4% 9% 8% 6% 0% 0%

Invest Same 44% 39% 50% 44% 37% 47% 44% 50%

Invest More 51% 57% 46% 47% 55% 47% 56% 50%

Cloud infrastructure

Invest Less 7% 8% 11% 9% 8% 10% 3% 0%

Invest Same 46% 47% 54% 34% 33% 47% 42% 58%

Invest More 46% 45% 35% 57% 59% 43% 55% 42%

Non-cloud IT enterprise software

Invest Less 34% 38% 38% 31% 45% 36% 29% 33%

Invest Same 51% 43% 52% 54% 39% 48% 52% 67%

Invest More 15% 19% 11% 14% 16% 16% 19% 0%

Third party advisory services

Invest Less 17% 18% 19% 11% 15% 12% 29% 14%

Invest Same 61% 52% 59% 69% 63% 68% 48% 76%