KPMG Screen template · Tax Planning. Suresh R. I. Perera. Principal, Tax & Regulatory. KPMG in Sri...

39

Tax Planning Suresh R. I. Perera Principal, Tax & Regulatory KPMG in Sri Lanka CA Sri Lanka

Transcript of KPMG Screen template · Tax Planning. Suresh R. I. Perera. Principal, Tax & Regulatory. KPMG in Sri...

Tax Planning

Suresh R. I. PereraPrincipal, Tax & RegulatoryKPMG in Sri Lanka

CA Sri Lanka

1© 2015 KPMG, a Sri Lankan Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Tax planning – a definition

Considering the tax implications of individual or business decisions throughout the year, usually with the goal of minimizing the tax liability

2© 2015 KPMG, a Sri Lankan Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

What is tax planning ?

• Based on correct information, tested principles & logical statistics

• Intelligent analysis, judicious decision making, sixth sense visualization

• Tax planning is not tax evasion• Optimizing the tax liability via Judicious use of

tax provisions • Not a generalised process – depends on tax

payer’s profile

Tax planning is both a Science & an Art

Tax Planning, Tax Avoidance & Tax Evasion

4© 2015 KPMG, a Sri Lankan Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

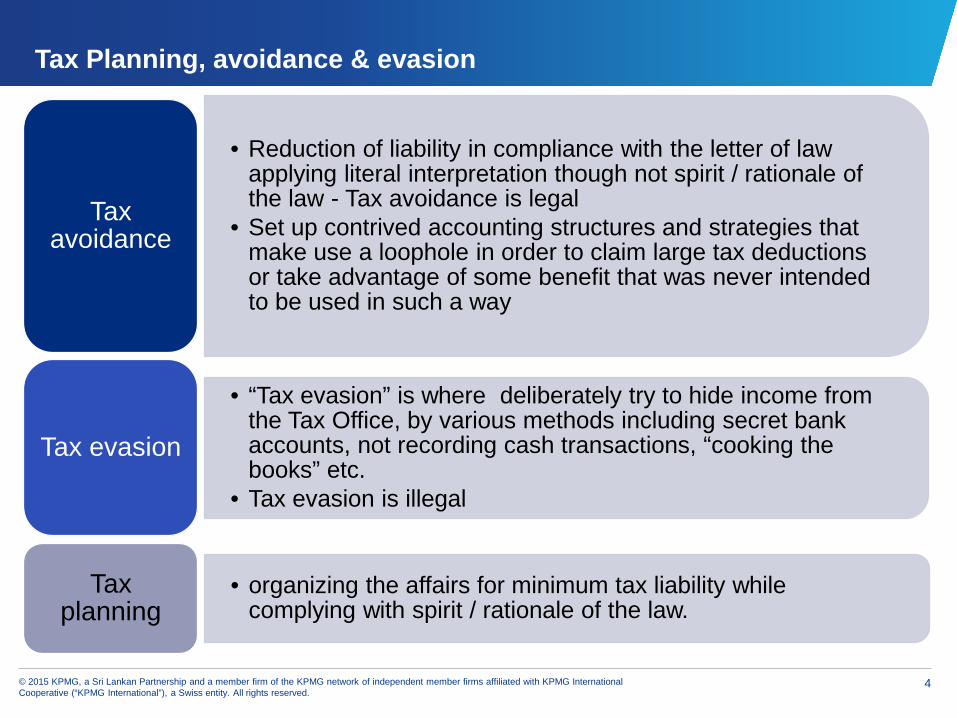

Tax Planning, avoidance & evasion

• Reduction of liability in compliance with the letter of law applying literal interpretation though not spirit / rationale of the law - Tax avoidance is legal

• Set up contrived accounting structures and strategies that make use a loophole in order to claim large tax deductions or take advantage of some benefit that was never intended to be used in such a way

Tax avoidance

• “Tax evasion” is where deliberately try to hide income from the Tax Office, by various methods including secret bank accounts, not recording cash transactions, “cooking the books” etc.

• Tax evasion is illegal

Tax evasion

• organizing the affairs for minimum tax liability while complying with spirit / rationale of the law.

Tax planning

5© 2015 KPMG, a Sri Lankan Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

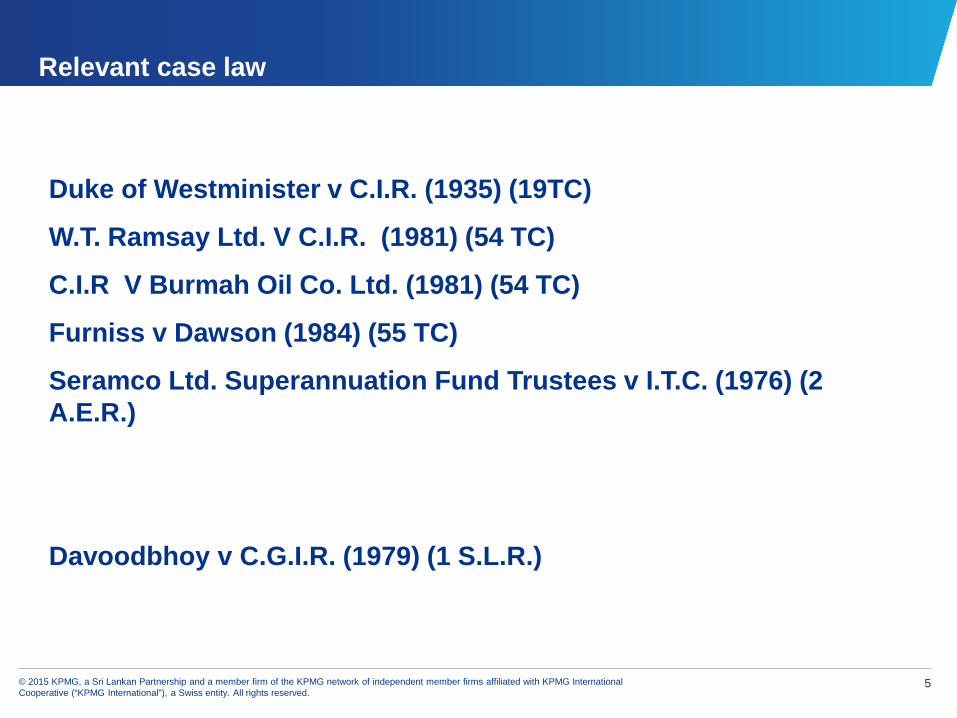

Relevant case law

Duke of Westminister v C.I.R. (1935) (19TC)

W.T. Ramsay Ltd. V C.I.R. (1981) (54 TC)

C.I.R V Burmah Oil Co. Ltd. (1981) (54 TC)

Furniss v Dawson (1984) (55 TC)

Seramco Ltd. Superannuation Fund Trustees v I.T.C. (1976) (2 A.E.R.)

Davoodbhoy v C.G.I.R. (1979) (1 S.L.R.)

6© 2015 KPMG, a Sri Lankan Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

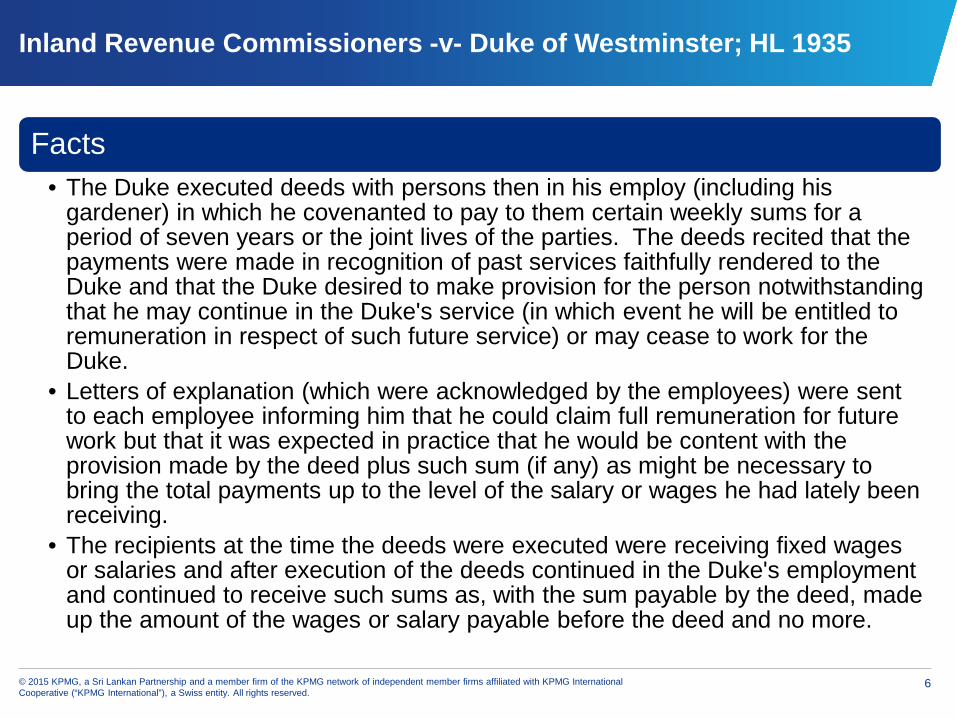

Inland Revenue Commissioners -v- Duke of Westminster; HL 1935

Facts • The Duke executed deeds with persons then in his employ (including his

gardener) in which he covenanted to pay to them certain weekly sums for a period of seven years or the joint lives of the parties. The deeds recited that the payments were made in recognition of past services faithfully rendered to the Duke and that the Duke desired to make provision for the person notwithstanding that he may continue in the Duke's service (in which event he will be entitled to remuneration in respect of such future service) or may cease to work for the Duke.

• Letters of explanation (which were acknowledged by the employees) were sent to each employee informing him that he could claim full remuneration for future work but that it was expected in practice that he would be content with the provision made by the deed plus such sum (if any) as might be necessary to bring the total payments up to the level of the salary or wages he had lately been receiving.

• The recipients at the time the deeds were executed were receiving fixed wages or salaries and after execution of the deeds continued in the Duke's employment and continued to receive such sums as, with the sum payable by the deed, made up the amount of the wages or salary payable before the deed and no more.

7© 2015 KPMG, a Sri Lankan Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

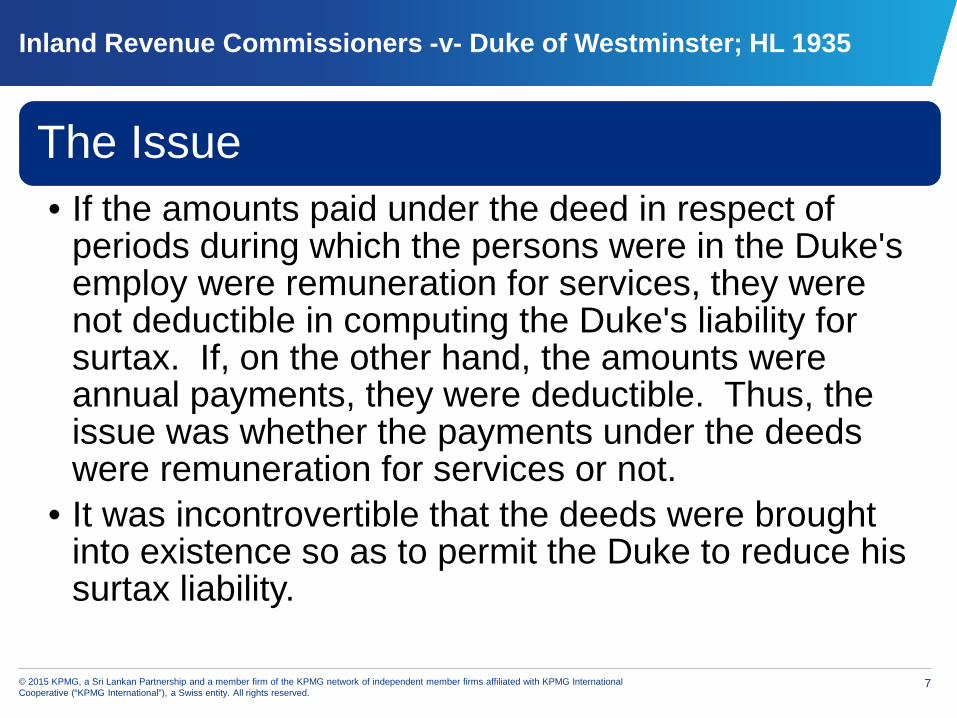

Inland Revenue Commissioners -v- Duke of Westminster; HL 1935

The Issue• If the amounts paid under the deed in respect of

periods during which the persons were in the Duke's employ were remuneration for services, they were not deductible in computing the Duke's liability for surtax. If, on the other hand, the amounts were annual payments, they were deductible. Thus, the issue was whether the payments under the deeds were remuneration for services or not.

• It was incontrovertible that the deeds were brought into existence so as to permit the Duke to reduce his surtax liability.

8© 2015 KPMG, a Sri Lankan Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

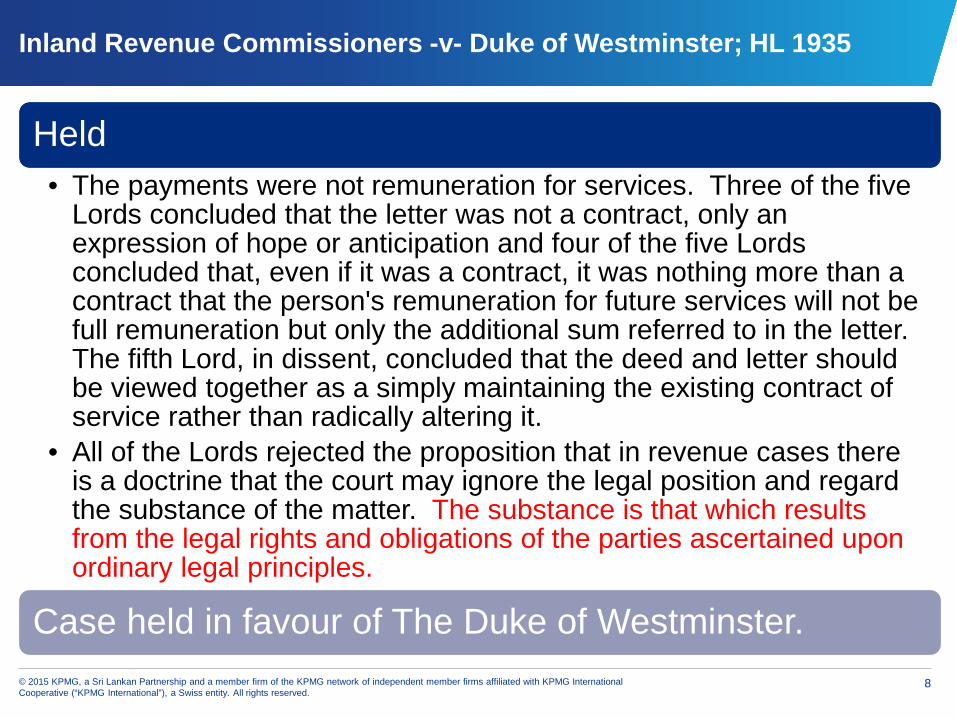

Inland Revenue Commissioners -v- Duke of Westminster; HL 1935

Held• The payments were not remuneration for services. Three of the five

Lords concluded that the letter was not a contract, only an expression of hope or anticipation and four of the five Lords concluded that, even if it was a contract, it was nothing more than a contract that the person's remuneration for future services will not be full remuneration but only the additional sum referred to in the letter. The fifth Lord, in dissent, concluded that the deed and letter should be viewed together as a simply maintaining the existing contract of service rather than radically altering it.

• All of the Lords rejected the proposition that in revenue cases there is a doctrine that the court may ignore the legal position and regard the substance of the matter. The substance is that which results from the legal rights and obligations of the parties ascertained upon ordinary legal principles.

Case held in favour of The Duke of Westminster.

9© 2015 KPMG, a Sri Lankan Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

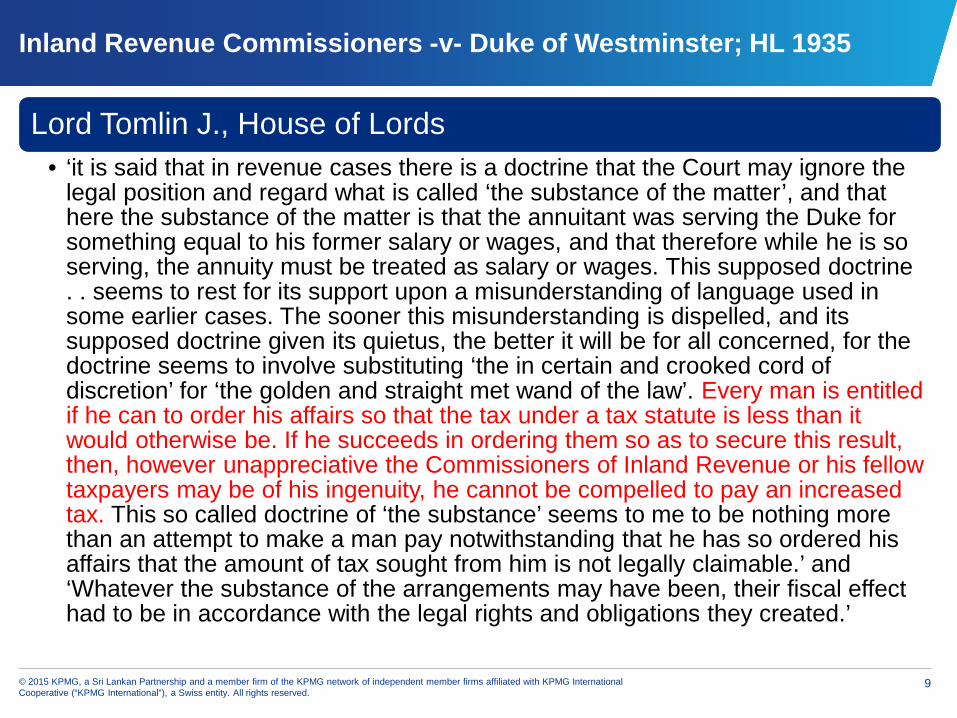

Inland Revenue Commissioners -v- Duke of Westminster; HL 1935

Lord Tomlin J., House of Lords• ‘it is said that in revenue cases there is a doctrine that the Court may ignore the

legal position and regard what is called ‘the substance of the matter’, and that here the substance of the matter is that the annuitant was serving the Duke for something equal to his former salary or wages, and that therefore while he is so serving, the annuity must be treated as salary or wages. This supposed doctrine . . seems to rest for its support upon a misunderstanding of language used in some earlier cases. The sooner this misunderstanding is dispelled, and its supposed doctrine given its quietus, the better it will be for all concerned, for the doctrine seems to involve substituting ‘the in certain and crooked cord of discretion’ for ‘the golden and straight met wand of the law’. Every man is entitled if he can to order his affairs so that the tax under a tax statute is less than it would otherwise be. If he succeeds in ordering them so as to secure this result, then, however unappreciative the Commissioners of Inland Revenue or his fellow taxpayers may be of his ingenuity, he cannot be compelled to pay an increased tax. This so called doctrine of ‘the substance’ seems to me to be nothing more than an attempt to make a man pay notwithstanding that he has so ordered his affairs that the amount of tax sought from him is not legally claimable.’ and ‘Whatever the substance of the arrangements may have been, their fiscal effect had to be in accordance with the legal rights and obligations they created.’

10© 2015 KPMG, a Sri Lankan Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

W.T. Ramsay Ltd. V C.I.R. (1981) (54 TC)

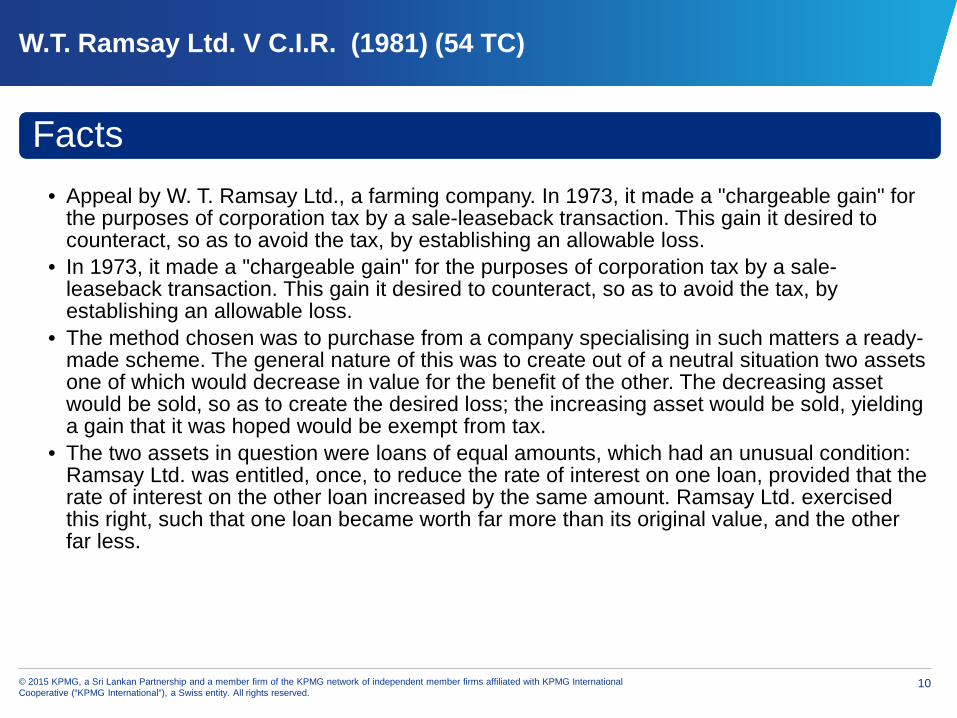

Facts• Appeal by W. T. Ramsay Ltd., a farming company. In 1973, it made a "chargeable gain" for

the purposes of corporation tax by a sale-leaseback transaction. This gain it desired to counteract, so as to avoid the tax, by establishing an allowable loss.

• In 1973, it made a "chargeable gain" for the purposes of corporation tax by a sale-leaseback transaction. This gain it desired to counteract, so as to avoid the tax, by establishing an allowable loss.

• The method chosen was to purchase from a company specialising in such matters a ready-made scheme. The general nature of this was to create out of a neutral situation two assets one of which would decrease in value for the benefit of the other. The decreasing asset would be sold, so as to create the desired loss; the increasing asset would be sold, yielding a gain that it was hoped would be exempt from tax.

• The two assets in question were loans of equal amounts, which had an unusual condition: Ramsay Ltd. was entitled, once, to reduce the rate of interest on one loan, provided that the rate of interest on the other loan increased by the same amount. Ramsay Ltd. exercised this right, such that one loan became worth far more than its original value, and the other far less.

11© 2015 KPMG, a Sri Lankan Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

W.T. Ramsay Ltd. V C.I.R. (1981) (54 TC)

Facts

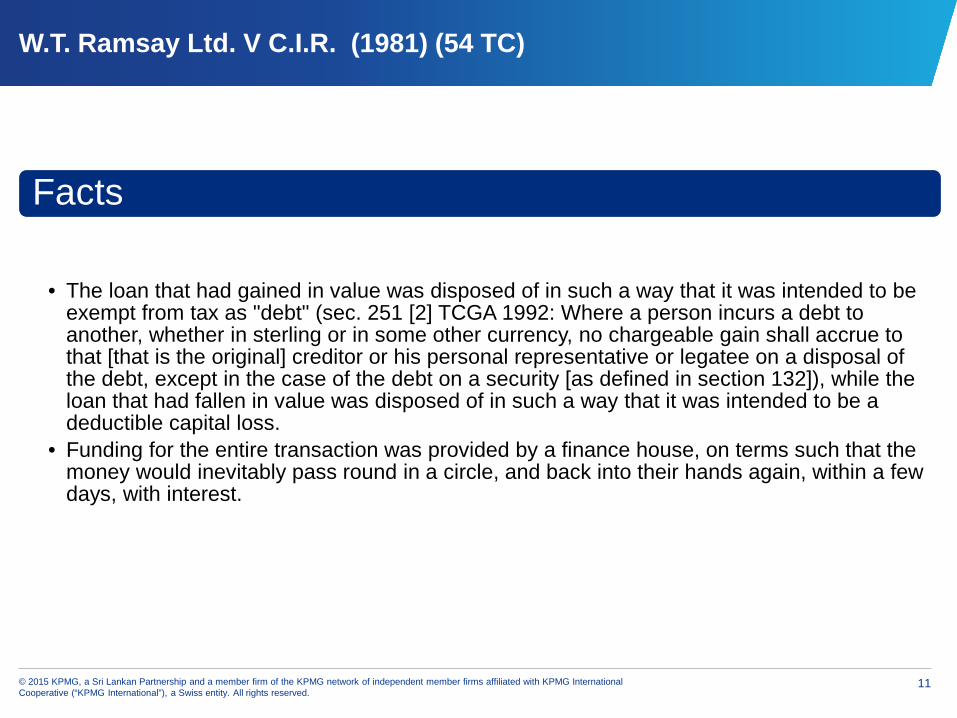

• The loan that had gained in value was disposed of in such a way that it was intended to be exempt from tax as "debt" (sec. 251 [2] TCGA 1992: Where a person incurs a debt to another, whether in sterling or in some other currency, no chargeable gain shall accrue to that [that is the original] creditor or his personal representative or legatee on a disposal of the debt, except in the case of the debt on a security [as defined in section 132]), while the loan that had fallen in value was disposed of in such a way that it was intended to be a deductible capital loss.

• Funding for the entire transaction was provided by a finance house, on terms such that the money would inevitably pass round in a circle, and back into their hands again, within a few days, with interest.

12© 2015 KPMG, a Sri Lankan Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

W.T. Ramsay Ltd. V C.I.R. (1981) (54 TC)

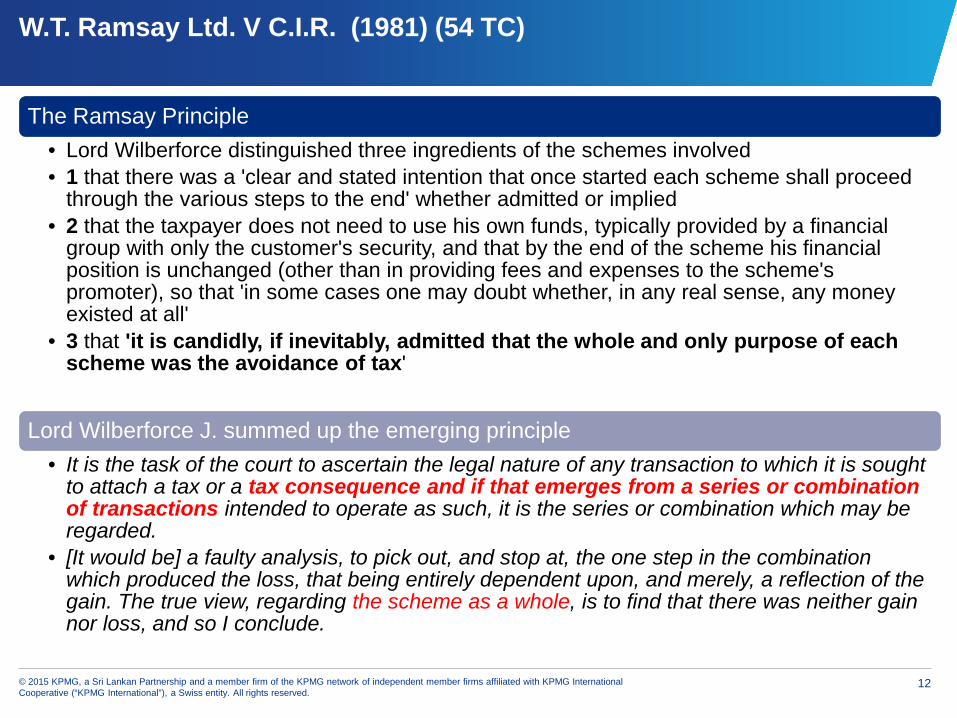

The Ramsay Principle• Lord Wilberforce distinguished three ingredients of the schemes involved• 1 that there was a 'clear and stated intention that once started each scheme shall proceed

through the various steps to the end' whether admitted or implied• 2 that the taxpayer does not need to use his own funds, typically provided by a financial

group with only the customer's security, and that by the end of the scheme his financial position is unchanged (other than in providing fees and expenses to the scheme's promoter), so that 'in some cases one may doubt whether, in any real sense, any money existed at all'

• 3 that 'it is candidly, if inevitably, admitted that the whole and only purpose of each scheme was the avoidance of tax'

Lord Wilberforce J. summed up the emerging principle• It is the task of the court to ascertain the legal nature of any transaction to which it is sought

to attach a tax or a tax consequence and if that emerges from a series or combination of transactions intended to operate as such, it is the series or combination which may be regarded.

• [It would be] a faulty analysis, to pick out, and stop at, the one step in the combination which produced the loss, that being entirely dependent upon, and merely, a reflection of the gain. The true view, regarding the scheme as a whole, is to find that there was neither gain nor loss, and so I conclude.

13© 2015 KPMG, a Sri Lankan Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

C.I.R V Burmah Oil Co. Ltd. (1981) (54 TC)

Facts • In this case, the Burmah Oil group had suffered a genuine loss on the sale

of an investment. However, the loss was not of the right kind to be deductible for tax purposes. Accordingly, the company's accountants and lawyers formulated a plan to "crystalise" that loss into a deductible form.

• They did this by entering into a series of (perfectly genuine) inter-group transactions, the overall effect of which was that the loss already incurred became a deductible capital loss on the liquidation of one of the subsidiaries in the group.

• These transactions were made using Burmah Oil's own money, and were therefore quite different from the pre-arranged, marketed "schemes" using borrowed money in the Ramsay.

Issues• Pure construction of the statutory provisions relating to capital gain tax/

corporate tax.• Implication as to whether the certain transactions which, on the face of them

and according to the taxpayer’s submission, resulted in allowable capital loss, should be disregard as artificial.

14© 2015 KPMG, a Sri Lankan Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

C.I.R V Burmah Oil Co. Ltd. (1981) (54 TC)

Held

• The judges were quite clear that they would have found in favour of BurmahOil, and against the IRC, had it not been for the decision in the Ramsay case, some months before.

• Lord Diplock said “It would be disingenuous to suggest, and dangerous on the part of those who advise on elaborate tax-avoidance schemes to assume, that Ramsay’s case did not mark a significant change in the approach adopted by this House in its judicial role to a pre-ordained series of transactions (whether or not they include the achievement of a legitimate commercial end) into which there are inserted steps that have no commercial purpose apart from the avoidance of a liability to tax which in the absence of those particular steps would have been payable. The difference is in approach.”

15© 2015 KPMG, a Sri Lankan Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

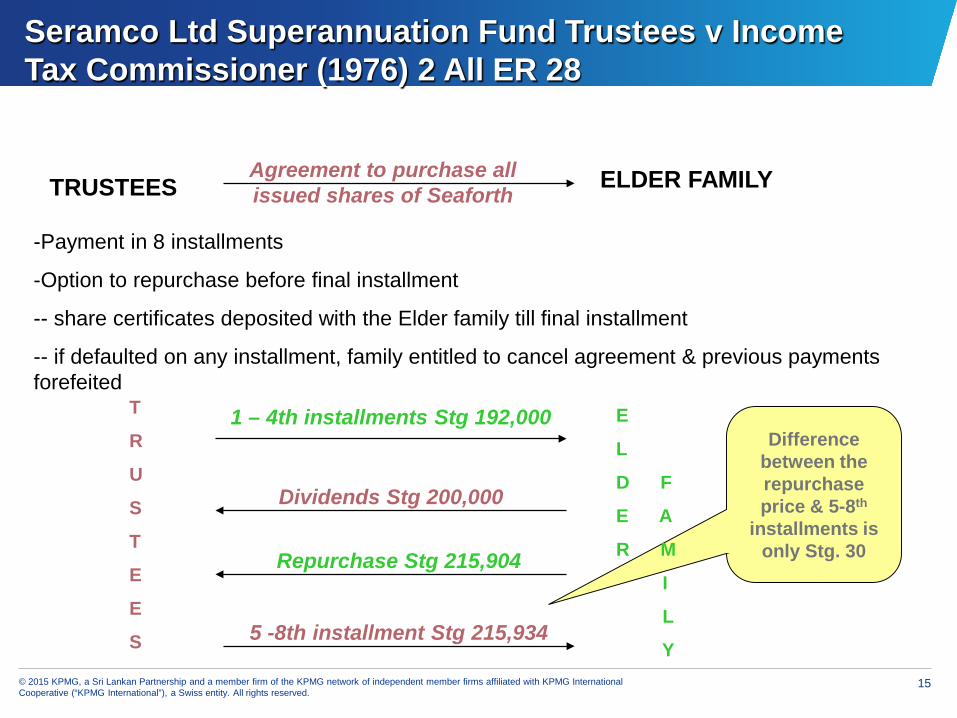

Seramco Ltd Superannuation Fund Trustees v Income Tax Commissioner (1976) 2 All ER 28

TRUSTEES ELDER FAMILY Agreement to purchase all issued shares of Seaforth

1 – 4th installments Stg 192,000

Dividends Stg 200,000

Repurchase Stg 215,904

5 -8th installment Stg 215,934

-Payment in 8 installments

-Option to repurchase before final installment

-- share certificates deposited with the Elder family till final installment

-- if defaulted on any installment, family entitled to cancel agreement & previous payments forefeited

T

R

U

S

T

E

E

S

Difference between the repurchase price & 5-8th

installments is only Stg. 30

E

L

D F

E A

R M

I

L

Y

16© 2015 KPMG, a Sri Lankan Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Seramco Ltd Superannuation Fund Trustees v Income Tax Commissioner (1976) 2 All ER)

Held • Intention of the transaction – DIVIDENDS STRIPPING

• Lord Diplock; Impossible to regard the transaction as either;• A genuine exercise by the trustees of their powers of investment of the fund or • A genuine sale of shares by the Elder family accompanied by an option to

repurchase them.• Artificial transaction within the meaning of s.10(1), but not a fictitious transaction

(one which those who are ostensibly parties to it never intended should be carried out.)

One transaction divided into two was held to be ineffective; the two transactions were regarded as one.

17© 2015 KPMG, a Sri Lankan Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Davoodbhoy v C.G.I.R. (1979) (1 S.L.R.)

Facts• The appellant Aasbhoy Davoodbhoy was one of five partners of a firm

carrying on business under the name of “Abdul Hassen Davoodbhoy” and was entitled to one fifth share of its profits. In order to provide for his children he entered in to an Agreement (A1) with them, whereby they agreed to be [partners in regard to one fifth share of the profits and losses of said the Aasbhoy Davoodbhoy.

• The agreement stated that the share of the capital and the goodwill in the said business was the property of the appellant was to remain his separate asset. The only asset of this venture therefore was the one fifth share of the profits received by the appellant.

• The agreement A1 and the rights claimed under it were rejected by the Assessor in terms of section 79(7) of the Inland Revenue Act and the whole of the one fifth share of the profits was assessed as the income of the appellant and not as the income of the partied to the agreement A1.

18© 2015 KPMG, a Sri Lankan Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Davoodbhoy v C.G.I.R. (1979) (1 S.L.R.)

Held

• The agreement A1 is not “artificial and fictitious”. It incorporates a family arrangement which is genuine and very common in our society. The accounts show that this agreement has been acted upon and profits divided accordingly. It cannot be rejected under 79(7) of the Inland Revenue Act.

• An arrangement to share profits only, can constitute in law, a partnership between the parties to the agreement, A1 created a “sub-partnership” which term is merely a convenient name used in law and commercial circles to describe a partnership which is dependent on another partnership. Such an agreement is perfectly valid in Civil Law must therefore attract the provisions of the Inland Revenue Act.

Statutory Provisions

20© 2015 KPMG, a Sri Lankan Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Artificial & fictitious transactions and dispositions not given effect to

“Where an assessor is of opinion that any transaction which reduces or would have the effect of reducing the amount of tax payable by any person is artificial or fictitious or that any disposition is not in fact given effect to, he may disregard any such transaction or disposition and the parties to the transaction or disposition shall be assessable accordingly”

Disposition includes any trust, grant, covenant, agreement or arrangement

- Sec. 103 of Inland Revenue Act No.10 of 2006-

21© 2015 KPMG, a Sri Lankan Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

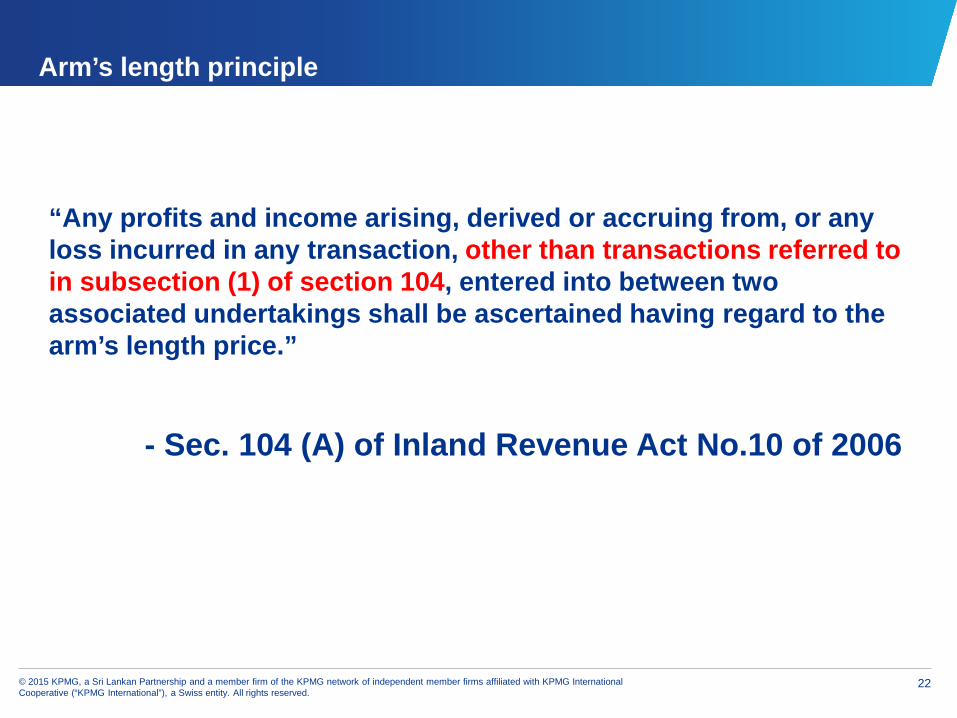

Arm’s length principle

“Any profits and income arising, derived or accruing from, or any loss incurred in any transaction entered into between two associated undertakings shall be ascertained having regard to the arm’s length price.”

“Where it appears to an Assessor or Assistant Commissioner that the profits and income or the loss, has not been as ascertained having regard to the arm’s length price, he may refer the computation of the arm’s length price in relation to such international transaction to a Transfer Pricing Officer.”

“arm’s length price” means a price which is applied in uncontrolled conditions in a transaction between persons, other than associated undertakings.

- Sec. 104 of Inland Revenue Act No.10 of 2006

22© 2015 KPMG, a Sri Lankan Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Arm’s length principle

“Any profits and income arising, derived or accruing from, or any loss incurred in any transaction, other than transactions referred to in subsection (1) of section 104, entered into between two associated undertakings shall be ascertained having regard to the arm’s length price.”

- Sec. 104 (A) of Inland Revenue Act No.10 of 2006

23© 2015 KPMG, a Sri Lankan Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

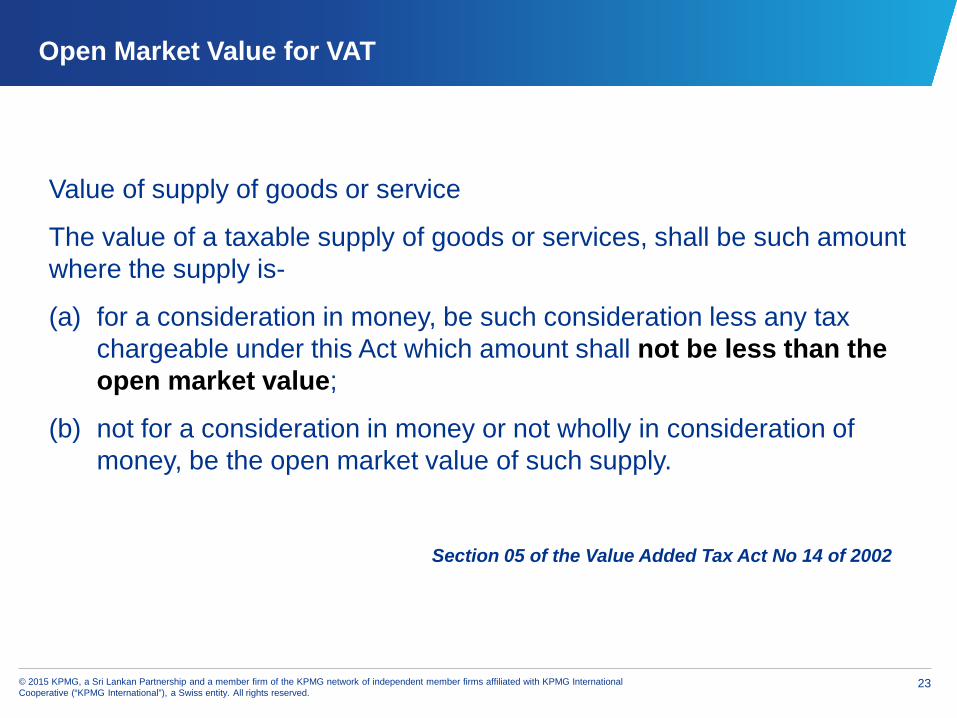

Open Market Value for VAT

Value of supply of goods or service

The value of a taxable supply of goods or services, shall be such amount where the supply is-

(a) for a consideration in money, be such consideration less any tax chargeable under this Act which amount shall not be less than the open market value;

(b) not for a consideration in money or not wholly in consideration of money, be the open market value of such supply.

Section 05 of the Value Added Tax Act No 14 of 2002

24© 2015 KPMG, a Sri Lankan Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

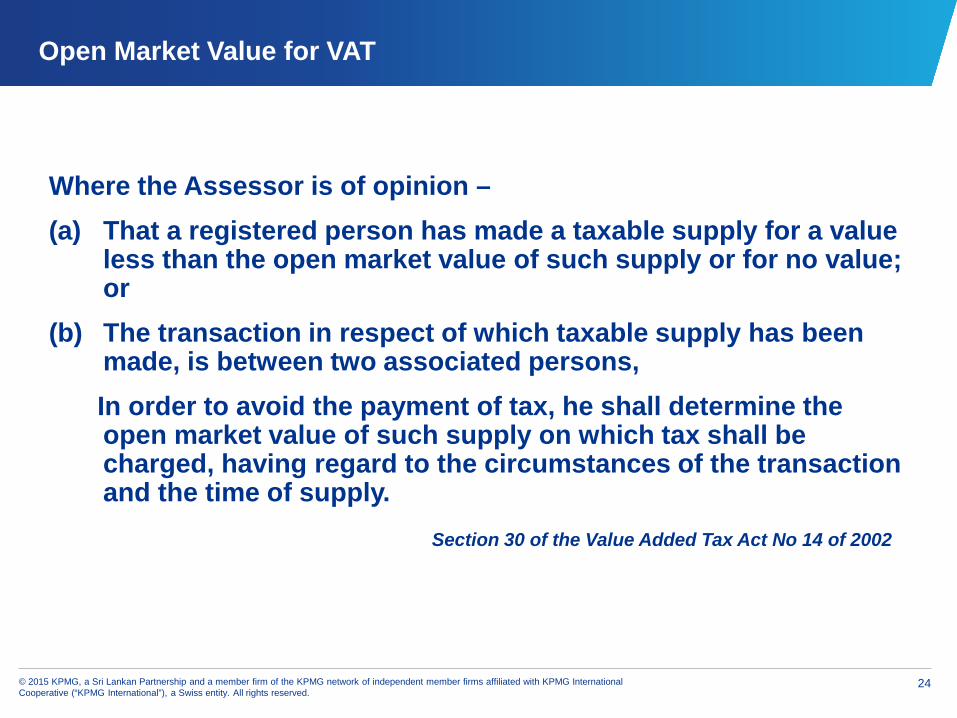

Open Market Value for VAT

Where the Assessor is of opinion –(a) That a registered person has made a taxable supply for a value

less than the open market value of such supply or for no value; or

(b) The transaction in respect of which taxable supply has been made, is between two associated persons,In order to avoid the payment of tax, he shall determine the open market value of such supply on which tax shall be charged, having regard to the circumstances of the transaction and the time of supply.

Section 30 of the Value Added Tax Act No 14 of 2002

Tax Planning points

26© 2015 KPMG, a Sri Lankan Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

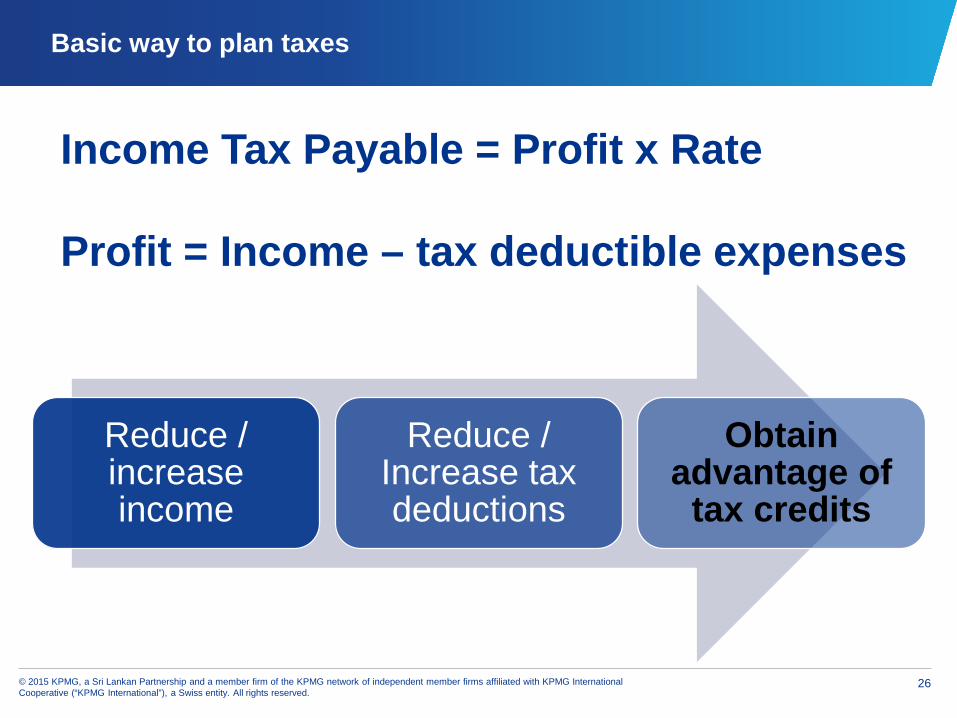

Basic way to plan taxes

Income Tax Payable = Profit x Rate

Profit = Income – tax deductible expenses

Reduce / increase income

Reduce / Increase tax deductions

Obtain advantage of

tax credits

27© 2015 KPMG, a Sri Lankan Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

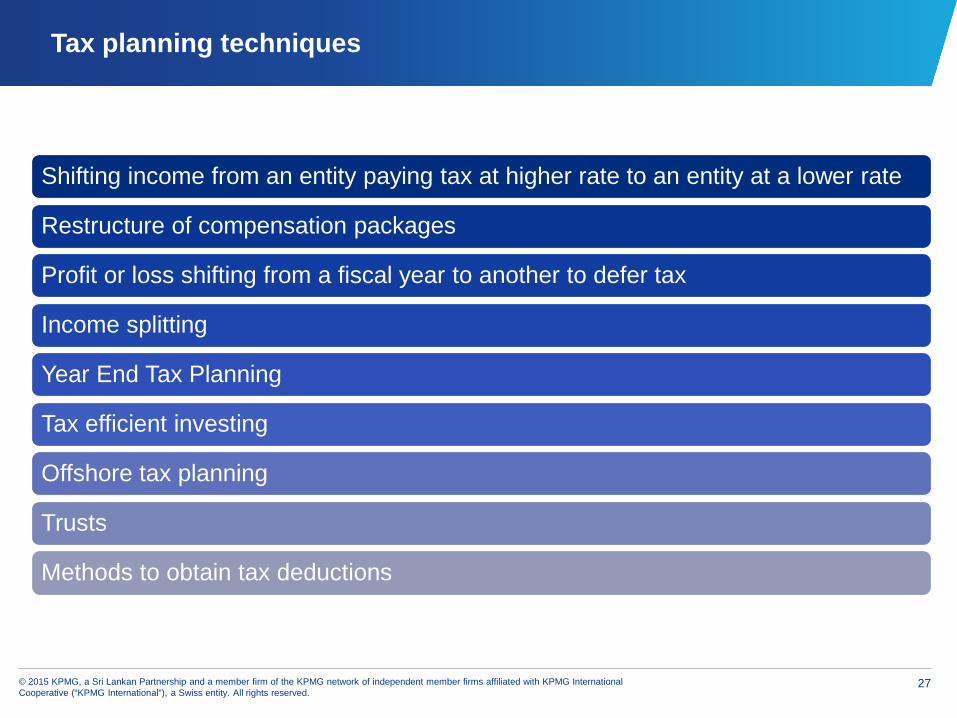

Tax planning techniques

Shifting income from an entity paying tax at higher rate to an entity at a lower rate

Restructure of compensation packages

Profit or loss shifting from a fiscal year to another to defer tax

Income splitting

Year End Tax Planning

Tax efficient investing

Offshore tax planning

Trusts

Methods to obtain tax deductions

28© 2015 KPMG, a Sri Lankan Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

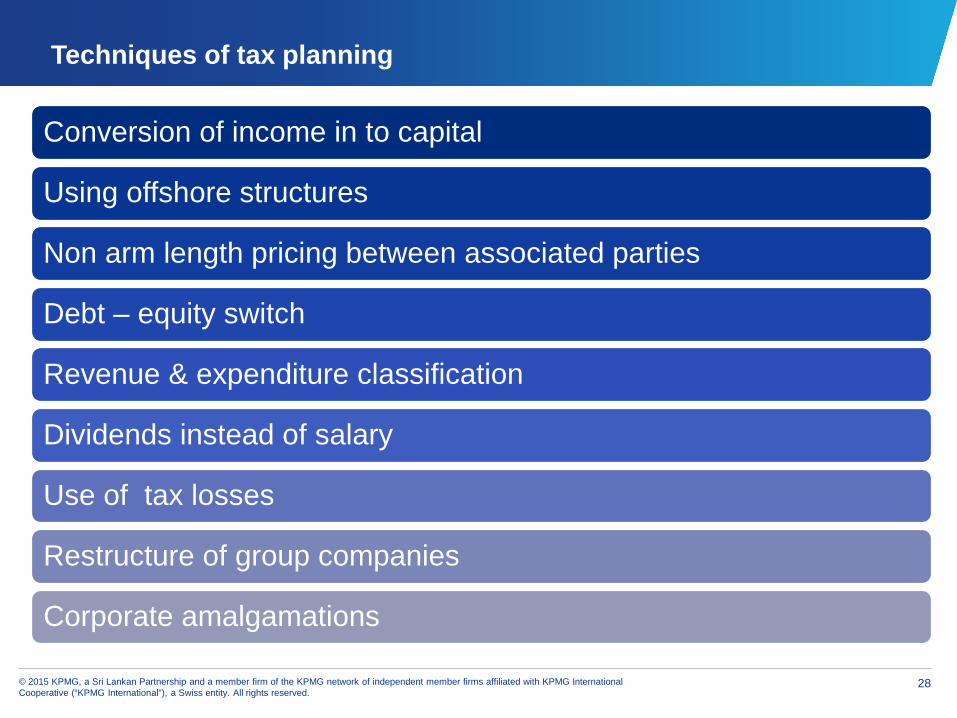

Techniques of tax planning

Conversion of income in to capital

Using offshore structures

Non arm length pricing between associated parties

Debt – equity switch

Revenue & expenditure classification

Dividends instead of salary

Use of tax losses

Restructure of group companies

Corporate amalgamations

Individual tax planning

30© 2015 KPMG, a Sri Lankan Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

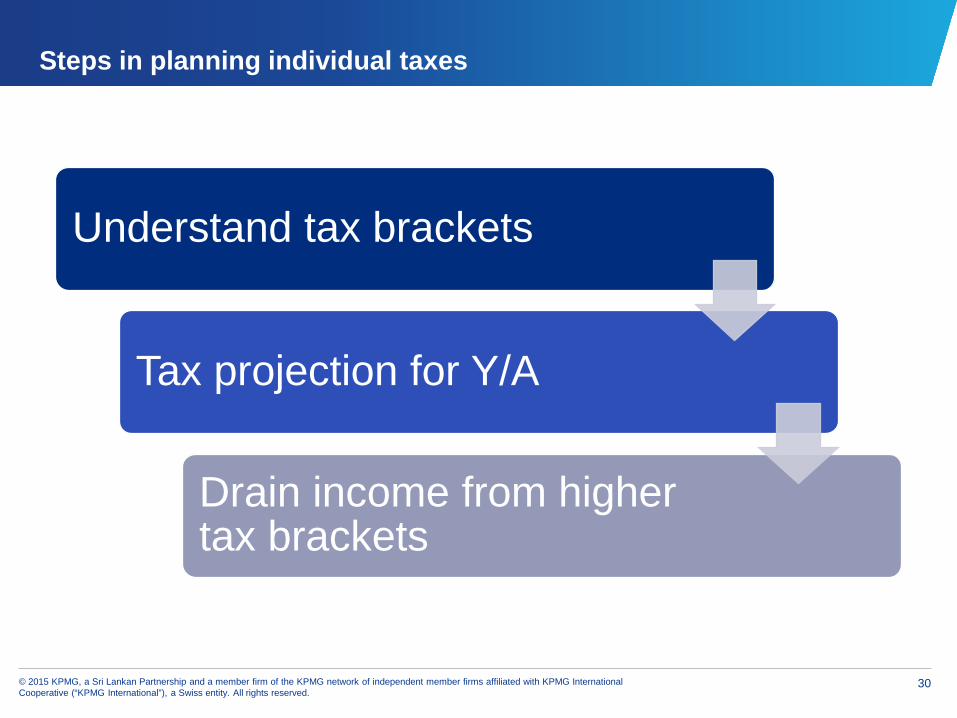

Steps in planning individual taxes

Understand tax brackets

Tax projection for Y/A

Drain income from higher tax brackets

31© 2015 KPMG, a Sri Lankan Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

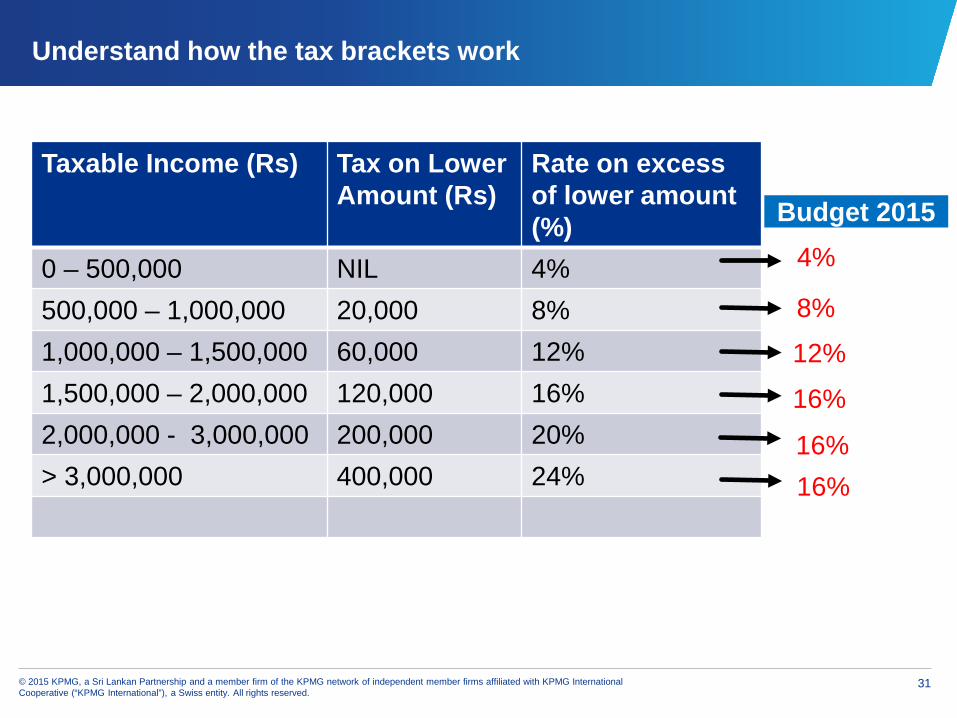

Understand how the tax brackets work

Taxable Income (Rs) Tax on Lower Amount (Rs)

Rate on excess of lower amount (%)

0 – 500,000 NIL 4%500,000 – 1,000,000 20,000 8%1,000,000 – 1,500,000 60,000 12%1,500,000 – 2,000,000 120,000 16%2,000,000 - 3,000,000 200,000 20%> 3,000,000 400,000 24%

4%

8%

12%

16%

16%16%

Budget 2015

32© 2015 KPMG, a Sri Lankan Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

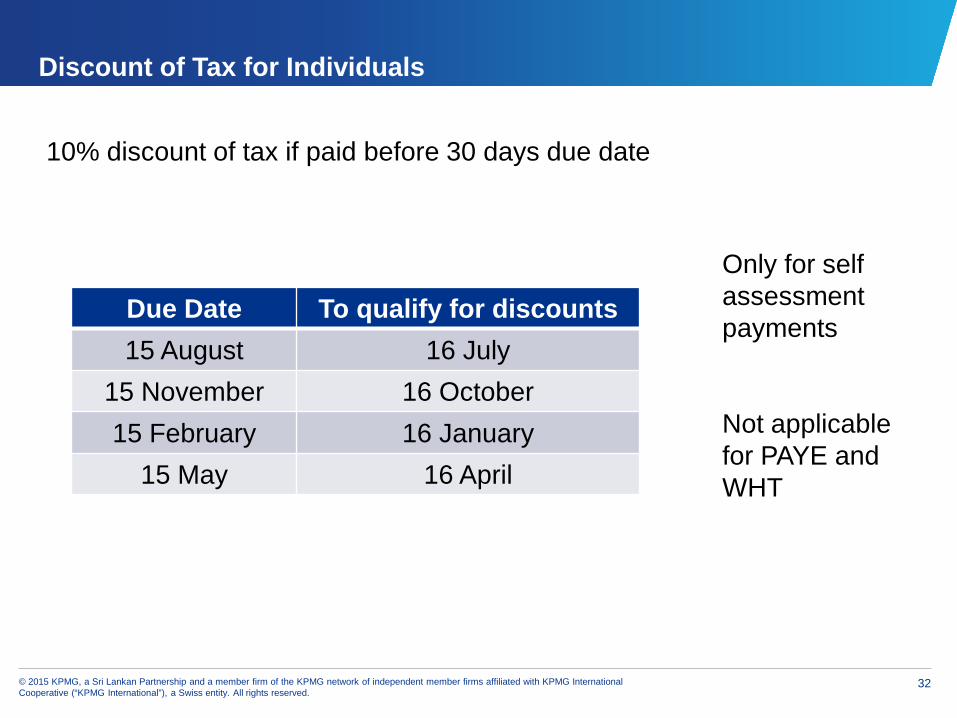

Discount of Tax for Individuals

10% discount of tax if paid before 30 days due date

Only for self assessment payments

Not applicable for PAYE and WHT

Due Date To qualify for discounts 15 August 16 July

15 November 16 October15 February 16 January

15 May 16 April

33© 2015 KPMG, a Sri Lankan Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

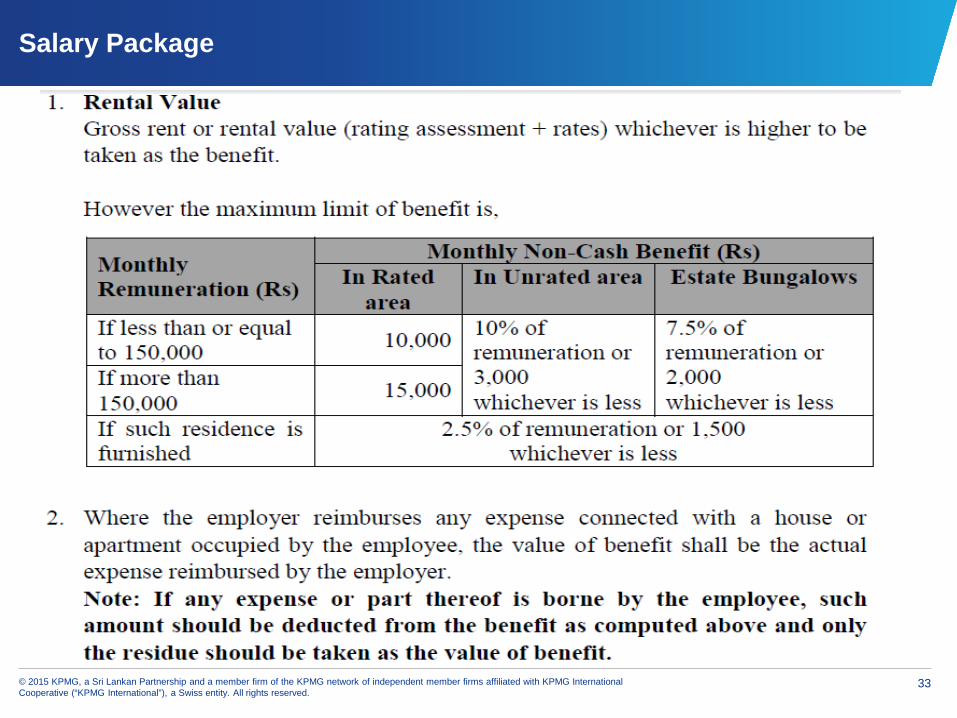

Salary Package

34© 2015 KPMG, a Sri Lankan Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

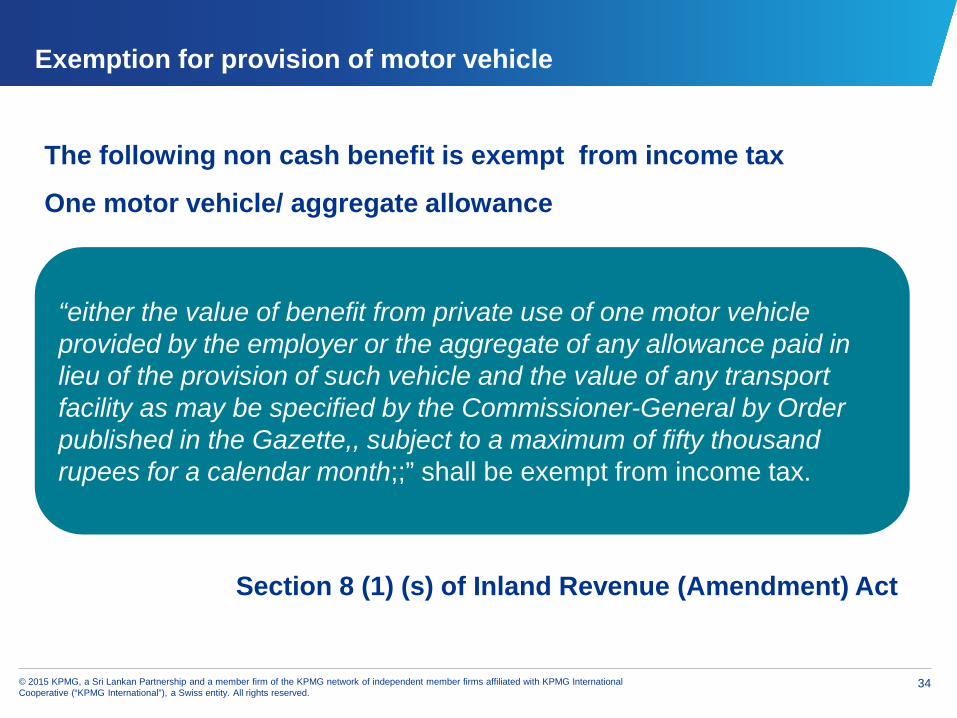

Exemption for provision of motor vehicle

The following non cash benefit is exempt from income tax

One motor vehicle/ aggregate allowance

Section 8 (1) (s) of Inland Revenue (Amendment) Act

“either the value of benefit from private use of one motor vehicle provided by the employer or the aggregate of any allowance paid in lieu of the provision of such vehicle and the value of any transport facility as may be specified by the Commissioner-General by Order published in the Gazette,, subject to a maximum of fifty thousand rupees for a calendar month;;” shall be exempt from income tax.

35© 2015 KPMG, a Sri Lankan Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

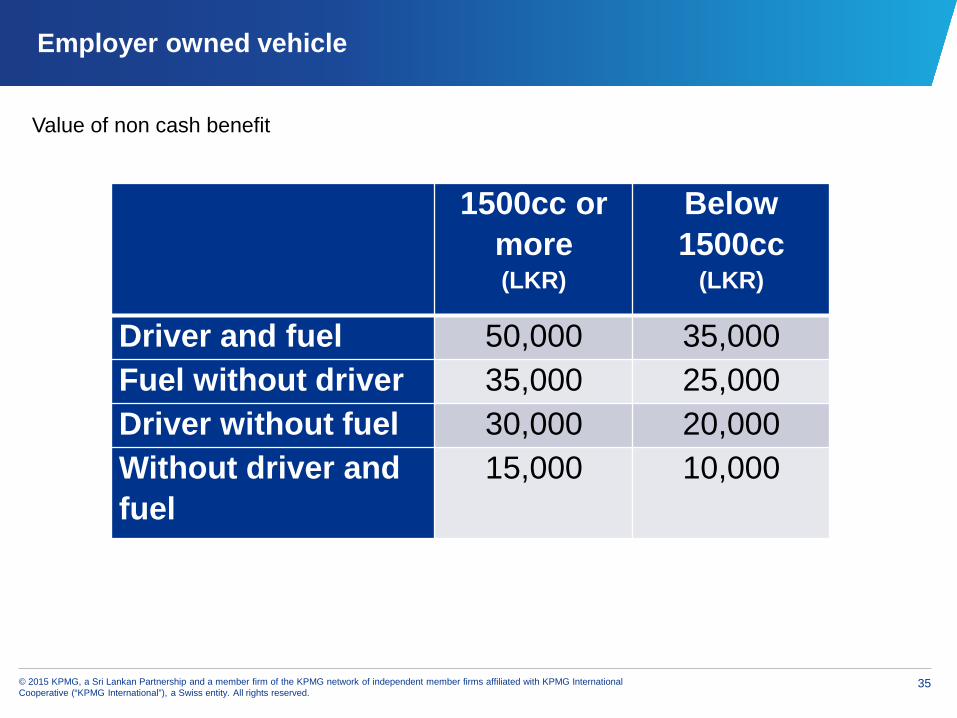

Employer owned vehicle

1500cc or more(LKR)

Below 1500cc

(LKR)

Driver and fuel 50,000 35,000Fuel without driver 35,000 25,000Driver without fuel 30,000 20,000Without driver and fuel

15,000 10,000

Value of non cash benefit

36© 2015 KPMG, a Sri Lankan Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

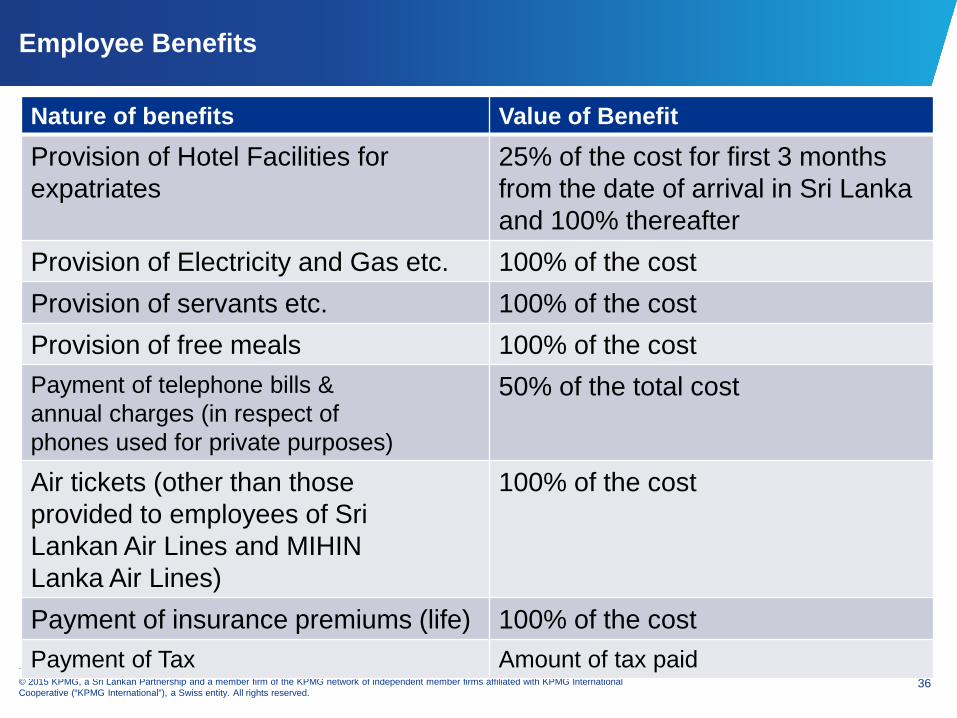

Employee Benefits

Nature of benefits Value of BenefitProvision of Hotel Facilities forexpatriates

25% of the cost for first 3 monthsfrom the date of arrival in Sri Lankaand 100% thereafter

Provision of Electricity and Gas etc. 100% of the costProvision of servants etc. 100% of the costProvision of free meals 100% of the costPayment of telephone bills &annual charges (in respect ofphones used for private purposes)

50% of the total cost

Air tickets (other than thoseprovided to employees of SriLankan Air Lines and MIHINLanka Air Lines)

100% of the cost

Payment of insurance premiums (life) 100% of the costPayment of Tax Amount of tax paid

37© 2015 KPMG, a Sri Lankan Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

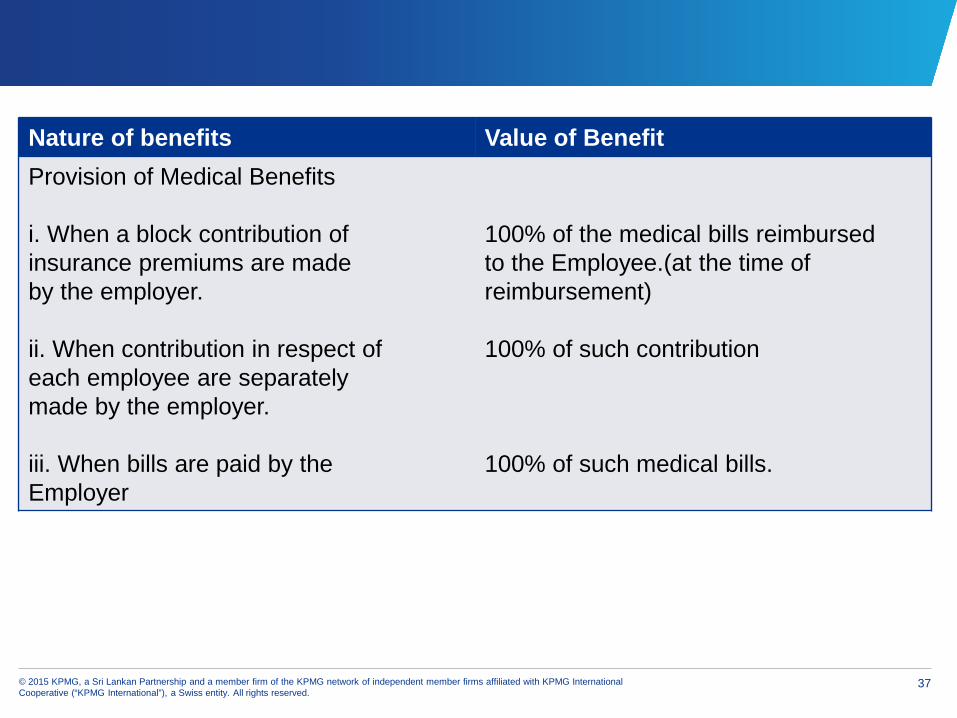

Nature of benefits Value of BenefitProvision of Medical Benefits

i. When a block contribution ofinsurance premiums are madeby the employer.

ii. When contribution in respect ofeach employee are separatelymade by the employer.

iii. When bills are paid by theEmployer

100% of the medical bills reimbursedto the Employee.(at the time ofreimbursement)

100% of such contribution

100% of such medical bills.

Thank you

Presentation by Suresh R I Perera

Principal – Tax & Regulatory

KPMG

Tel : 0115426502

Email : [email protected]