KPMG LLP - NOAA · KPMG LLP 2001 M Street, NW Washington, DC 20036 MANAGEMENT LETTER November 9,...

40

KPMG LLP 2001 M Street, NW Washington, DC 20036 MANAGEMENT LETTER November 9, 2004 CONFIDENTIAL Mr. Otto J. Wolff Chief Financial Officer and Assistant Secretary for Administration U.S. Department of Commerce 14 th and Constitution Avenue, N.W. Washington, D.C. 20230 Dear Mr. Wolff: We have audited the consolidated financial statements of the Department of Commerce (Department) as of and for the years ended September 30, 2004 and 2003, and have issued our report thereon dated November 9, 2004. In planning and performing our audits of the Department’s consolidated financial statements, we considered the Department’s internal control over financial reporting, in order to determine our auditing procedures for the purpose of expressing an opinion on the consolidated financial statements. An audit does not include examining the effectiveness of internal control, and does not provide assurance on internal control over financial reporting. During our fiscal year 2004 audit of the Department’s consolidated financial statements, we noted one matter involving internal control over financial reporting and its operation that we consider to be a reportable condition under standards established by the American Institute of Certified Public Accountants. In our Independent Auditors’ Report, dated November 9, 2004, we reported that we consider the Department’s financial management systems to be a reportable condition, but that we do not consider this area to be a material weakness. Details of our financial management systems findings were reported to the Department in a separate letter. Reportable conditions are matters coming to our attention relating to significant deficiencies in the design or operation of the internal controls, that in our judgment, could adversely affect the Department’s ability to record, process, summarize, and report financial data consistent with the assertions of management in the consolidated financial statements. Our consideration of internal control over financial reporting would not necessarily disclose all matters in internal control that might KPMG LLP. KPMG LLP, a U.S. limited liability partnership, is a member of KPMG International, a Swiss association.

Transcript of KPMG LLP - NOAA · KPMG LLP 2001 M Street, NW Washington, DC 20036 MANAGEMENT LETTER November 9,...

KPMG LLP2001 M Street, NWWashington, DC 20036

MANAGEMENT LETTER

November 9, 2004

CONFIDENTIAL

Mr. Otto J. WolffChief Financial Officer and Assistant Secretary for AdministrationU.S. Department of Commerce 14th and Constitution Avenue, N.W. Washington, D.C. 20230

Dear Mr. Wolff:

We have audited the consolidated financial statements of the Department of Commerce (Department)as of and for the years ended September 30, 2004 and 2003, and have issued our report thereon datedNovember 9, 2004. In planning and performing our audits of the Department’s consolidated financial statements, we considered the Department’s internal control over financial reporting, in order todetermine our auditing procedures for the purpose of expressing an opinion on the consolidated financial statements. An audit does not include examining the effectiveness of internal control, anddoes not provide assurance on internal control over financial reporting.

During our fiscal year 2004 audit of the Department’s consolidated financial statements, we noted onematter involving internal control over financial reporting and its operation that we consider to be a reportable condition under standards established by the American Institute of Certified Public Accountants. In our Independent Auditors’ Report, dated November 9, 2004, we reported that we consider the Department’s financial management systems to be a reportable condition, but that we donot consider this area to be a material weakness. Details of our financial management systems findings were reported to the Department in a separate letter.

Reportable conditions are matters coming to our attention relating to significant deficiencies in the design or operation of the internal controls, that in our judgment, could adversely affect theDepartment’s ability to record, process, summarize, and report financial data consistent with the assertions of management in the consolidated financial statements. Our consideration of internalcontrol over financial reporting would not necessarily disclose all matters in internal control that might

KPMG LLP. KPMG LLP, a U.S. limited liability partnership, isa member of KPMG International, a Swiss association.

KPMG LLP. KPMG LLP, a U.S. limited liability partnership, isa member of KPMG International, a Swiss association.

Mr. Otto J. WolffU.S. Department of Commerce November 9, 2004 Page 2

be reportable conditions. Material weaknesses are reportable conditions in which the design or operation of one or more of the internal control components does not reduce, to a relatively low level, the risk that misstatements, in amounts that would be material in relation to the consolidated financial statements being audited, may occur and not be detected within a timely period by employees in thenormal course of performing their assigned functions.

Our audit procedures were designed primarily to enable us to form an opinion, based on our audit and the reports of other auditors, on the Department’s consolidated financial statements, and therefore, maynot bring to light all weaknesses in policies or procedures that exist. However, we also take this opportunity to share our knowledge of the Department, gained during our work, to make comments andsuggestions that we hope can be useful to you.

Although not considered to be reportable conditions, we noted certain matters involving internalcontrols and other operational matters, which are presented in Exhibits A through F, attached, for yourconsideration. These comments and recommendations, all of which have been discussed with theappropriate members of management, are intended to improve the Department’s internal controls or result in other operating efficiencies. Each exhibit presents the status of prior year management lettercomments. We have not considered the Department’s internal controls since the date of our report.

We appreciate the courteous and professional assistance that the Department’s personnel extended to us to complete our audit timely. We would be pleased to discuss these comments and recommendationswith you at any time.

This report is intended solely for the information and use of the Department’s management and the Department’s Office of Inspector General and is not intended to be and should not be used by anyoneother than these specified parties.

FY 2004 Management Letter U.S. Department of Commerce

Table of Contents

i

Departmental Level Exhibit A

Certain Operational and Accounting Handbooks Should be Updated A.1

Federal Managers’ Financial Integrity Act Oversight Should be Improved A.2

Status of Prior Year Management Letter Comments A.4

National Oceanic and Atmospheric Administration (NOAA) Exhibit B

Accounting for Construction Work-in-Progress Should be Improved B.1

Controls over Personal Property Should be Improved B.1

Personal Property Lease Accounting Should be Strengthened B.3

Accounting for Grant Advances and Payables Should be Improved B.4

Procedures for Aging Receivables Should be Reviewed B.5

Controls over Physical Inventory Counts Should be Strengthened B.5

Controls over Payroll Should be Strengthened B.6

Accounting for Fund Balance with Treasury and Other Cash Should be Improved

B.6

Internal Controls and Accounting for Deferred Revenue Should be Strengthened

B.7

Internal Controls over Budgetary Resources Should be Improved B.7

Accounting for Supplementary Stewardship Reporting Should be Strengthened

B.8

Status of Prior Year Management Letter Comments B.9

National Institute of Standards and Technology (NIST) and NIST-Serviced Bureaus

Exhibit C

Controls over the Review of Time and Attendance (T&A) Reports Should be Improved

C.1

Controls over the Reconciliation of Property, Plant, and Equipment Should be Improved

C.1

FY 2004 Management Letter U.S. Department of Commerce Table of Contents, Continued

ii

National Institute of Standards and Technology (NIST) and NIST-Serviced Bureaus, Continued

Exhibit C, cont.

Controls over the Review of ELGP Loan Guarantee Liability Account Should be Improved

C.1

Corrective Action Plan for Prior Year’s Finding Should be Implemented C.2

Status of Prior Year Management Letter Comments C.3

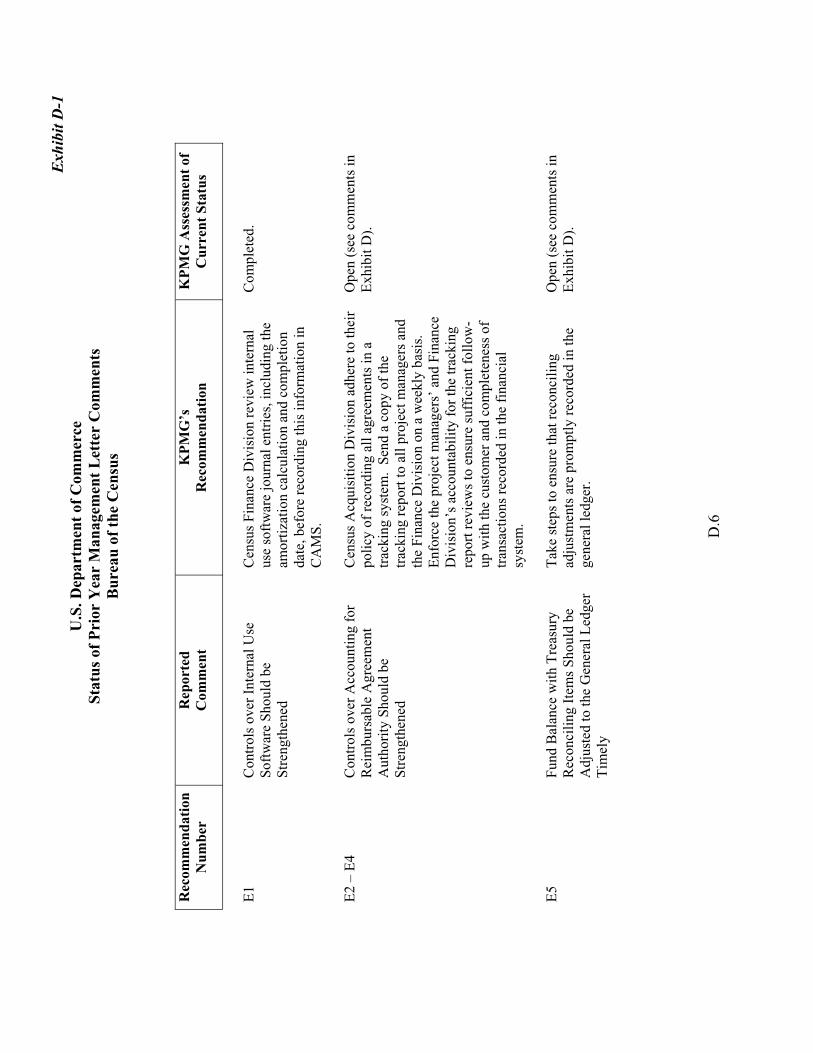

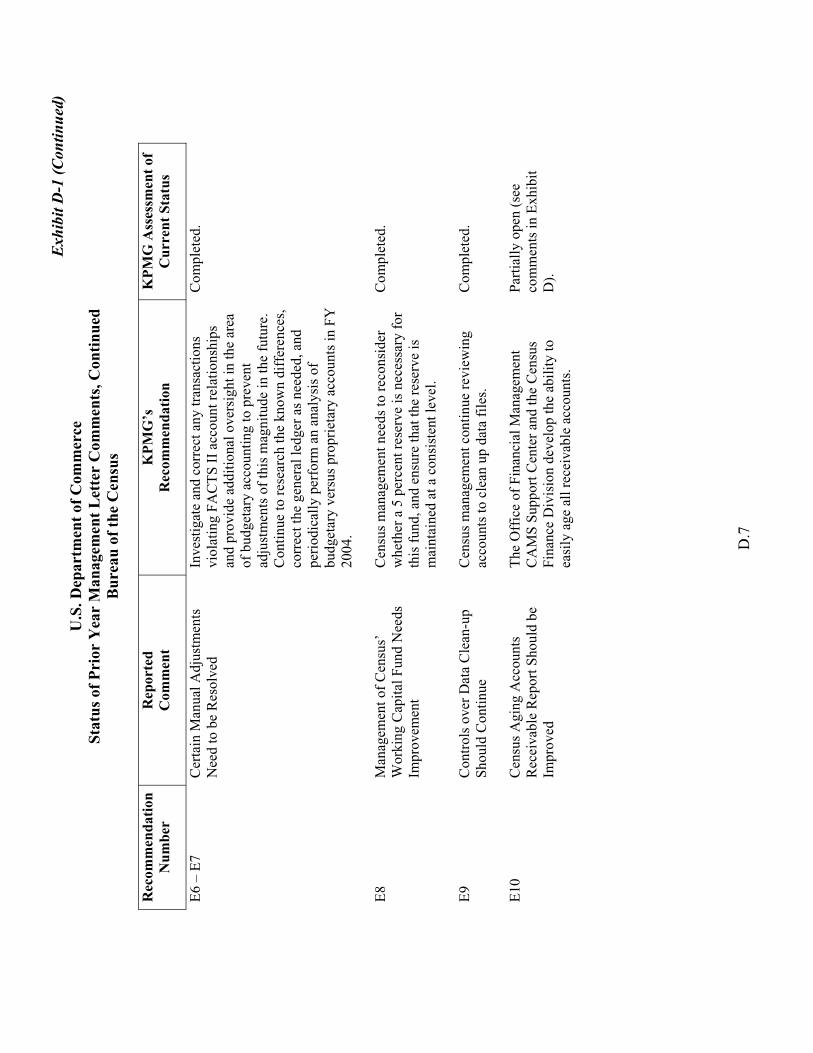

Bureau of the Census (Census) Exhibit D

Accounting for Accruals Need to be Improved D.1

Controls over Accounting for Reimbursable Agreement Authority Should be Strengthened

D.1

Accounts Receivable Aging Report Needs to be Finalized D.2

Accounting for Accounts Receivable and Deferred Revenue Needs to be Strengthened

D.3

Fund Balance with Treasury Reconciling Items Should be Adjusted to the General Ledger, Timely

D.3

Accounting for Equipment Trade-ins Should be Improved D.4

Controls over General Service Administration Leases Schedules Should be Strengthened

D.5

Receipt Dates for Electronic Transmissions Need to be Resolved D.5

Status of Prior Year Management Letter Comments D.7

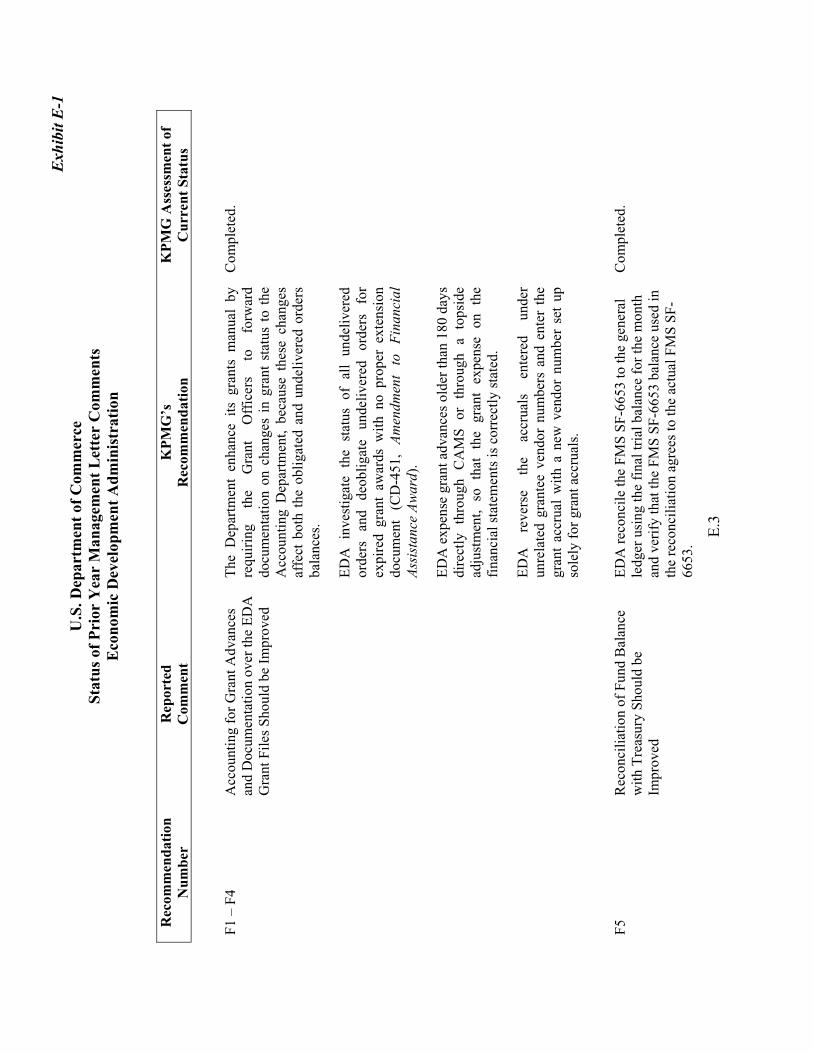

Economic Development Administration (EDA) Exhibit E

Management Review over Recorded Obligations Should be Implemented E.1

Controls over Monitoring Excess Funds Should be Strengthened E.1

Controls over Cash Receipts Should be Improved E.1

FY 2004 Management Letter U.S. Department of Commerce Table of Contents, Continued

iii

Economic Development Administration (EDA), Continued Exhibit E, cont.

Controls over the Review of FACTS II Information Should be Improved E.2

The Process of Updating Goals II Enterprise System User Information Should be Strengthened

E.2

Controls over Grant Accruals Should be Improved E.2

Status of Prior Year Management Letter Comments E.3

International Trade Administration (ITA) Exhibit F

Status of Prior Year Management Letter Comments F.2

Exhibit A U.S. Department of Commerce

FY 2004 Management Letter CommentsDepartmental Level

Certain Operational and Accounting Handbooks Should be Updated

Now that the U.S. Department of Commerce (Department or Commerce) has (1) fully implemented theDepartment-wide financial system, Commerce Administrative Management System (CAMS), and theSunflower personal property system (a subsidiary ledger for personal property); (2) transitioned to the U.S. Department of Treasury’s grant-related system, Automated Standard Application for Payments(ASAP); and (3) prepared comparative quarterly financial statements in accordance with the Office of Management and Budget (OMB); the Department should review the Department’s existing operational and accounting handbooks, to ensure that the daily activities of its employees are in line with the current,and increasing, reporting requirements.

Although some of our comments are based on the bureau-level handbooks, manuals, or directives that weobserved during our detailed test work in prior years, most manuals need to be addressed at theDepartment-wide level, to ensure that the information that is required at the Department level is providedin a consistent format and within the timeframes outlined in the Department’s Financial Statement Guidance, that is updated annually.

Specifically, some of the handbooks, manuals, or directives that we found should be updated on the Department’s Office of Financial Management (OFM) website. The Department is aware of this matterand is in the process of updating the following handbooks, which were listed on the OFM website in FY 2004.

Advances and Reimbursable Handbook;Working Capital Fund Handbook;Accounting Principles and Standards Handbook; andCredit and Debt Operating Standards and Procedures Handbook.

In the prior year, we observed that the following manuals should be updated. In addition, these manualsshould be added to the Department’s OFM website.

With the full implementation of CAMS, budget handbooks or manuals should be reviewed andupdated at the Department level, to address current procedures in place to be consistent with CAMSbudget module user manuals.

The Department’s Personal Property Management Manual requires that “Property accountabilityrecords be reconciled periodically with the financial control accounts in accordance with proceduresestablished by servicing financial accounting activities.” However, the term “periodically” is not defined in terms of time periods, such as monthly or quarterly. Thus, the individual bureaus interpretthe interval to complete property reconciliations differently. Additionally, reconciliation proceduresare not specific enough to provide for consistent control.

Clarification should be added to the grants manual for grant file review requirements. Similar to the property manual, the term “periodically” or “annually” is interpreted differently across the Department.

In the prior year, we also observed that the Department-level directive for Federal Managers’ FinancialIntegrity Act (FMFIA) is outdated and the bureaus interpreted the self-assessment requirementsdifferently. In lieu of an updated directive, the Department conducted a workshop on August 12, 2004, to

A.1

Exhibit A (Continued) U.S. Department of Commerce

Status of Prior Year Management Letter Comments Departmental Level

assist the bureaus with preparing the FMFIA report. While this workshop was necessary, it was conducted too late for bureaus to implement any new self-assessment programs for FY 2004 based on thoroughly reviewing the requirements and evaluating existing control environments. This matter isdiscussed further in the separate comment, below.

Recommendation:

1. We continue to recommend that the Department’s OFM coordinate with all bureaus to review existing operational and accounting handbooks, manuals, and directives, to ensure that the daily activities of its employees are in line with the current, and increasing, reporting requirements andDepartment-wide use of CAMS.

Federal Managers’ Financial Integrity Act (FMFIA) Oversight Should be Improved

FMFIA states that by December 31, 1983, and by December 31 of each succeeding year, the head of each executive agency [Department] shall, on the basis of an evaluation conducted in accordance withguidelines prescribed under paragraph (2) of this subsection, prepare a statement that:

The Department’s systems of internal accounting and administrative control fully comply with the requirements of paragraph (1); or

Such systems do not fully comply with such requirements.

In the prior year, we noted that the Department and its bureaus conduct a self-assessment of “systems”related to internal accounting and administrative control but the bureaus do not have a consistent interpretation of the word “systems” as it applies to the FMFIA. Congressional intent for this act was notlimited to information technology (IT) systems, but is intended for agencies to include in their self-assessments a review of the “methods” of internal accounting and administrative controls.

Based on our limited review in FY 2004, we found that the bureaus considered non-IT controls as well as IT controls. However, while each bureau has a central point for gathering information for the FMFIA report, the level of documentation and interaction among the stakeholders of the FMFIA process at the bureau-level is inconsistent across the Department. For example, the National Oceanic and AtmosphericAdministration (NOAA) has a central database for tracking all deficiencies. The Bureau of the Census (Census) and the National Institute of Standards and Technology (NIST) did not have a central database for tracking all deficiencies. However, these bureaus have not identified any material weaknesses, whichmust be tracked for FMFIA. Without a formal process for tracking deficiencies, it is not clear that alldeficiencies are being reported to a central point for consideration of findings individually and inaggregate. The inconsistency in addressing the FMFIA process may be due to outdated handbooks and manuals, which should include a schedule of the assessment programs required and evaluation timeframe,related to all accounting and control procedures. The need for updated handbooks and manuals is discussed in the previous section.

A.2

Exhibit A (Continued) U.S. Department of Commerce

Status of Prior Year Management Letter Comments Departmental Level

Recommendations:

We continue to recommend that the Department:

2. Take a more proactive role in coordinating the annual FMFIA self-assessments and ensuring that the intent of the Act is followed.

3. Review and revise the Departmental directive to assist the bureaus with the timing, extent, and performance of the self-assessments.

A.3

Exh

ibit

A-1

U

.S. D

epar

tmen

t of

Com

mer

ce

Stat

us o

f P

rior

Yea

r M

anag

emen

t L

ette

r C

omm

ents

D

epar

tmen

tal L

evel

Rec

omm

enda

tion

Num

ber

Rep

orte

dC

omm

ent

KP

MG

’sR

ecom

men

dati

onK

PM

G A

sses

smen

t of

C

urre

nt S

tatu

s

A1

Cer

tain

Ope

ratio

nal a

nd

Acc

ount

ing

Han

dboo

ks S

houl

dbe

Upd

ated

The

Dep

artm

ent’

s O

FM s

houl

d co

ordi

nate

with

all

bure

aus

to r

evie

w e

xist

ing

oper

atio

nal a

nd

acco

untin

g ha

ndbo

oks,

man

uals

, and

dir

ectiv

es, t

o en

sure

that

the

daily

act

iviti

es o

f its

em

ploy

ees

are

in li

ne w

ith th

e cu

rren

t, an

d in

crea

sing

, rep

ortin

g re

quir

emen

tsan

d D

epar

tmen

t-w

ide

impl

emen

tatio

nof

CA

MS.

Ope

n (s

ee c

omm

ents

in

Exh

ibit

A).

A2

– A

3 Fe

dera

l Man

ager

s’ F

inan

cial

Inte

grity

Act

Ove

rsig

ht S

houl

dbe

Impr

oved

The

Dep

artm

ent s

houl

d ta

ke a

mor

e pr

oact

ive

role

in

coo

rdin

atin

g th

e an

nual

FM

FIA

sel

f-as

sess

men

ts

and

ensu

ring

that

the

inte

nt o

f th

e A

ct is

fol

low

ed,

and

revi

ew a

nd r

evis

e th

e D

epar

tmen

tal d

irec

tive

to

assi

st th

e bu

reau

s w

ith th

e tim

ing,

ext

ent,

and

perf

orm

ance

of th

e se

lf-a

sses

smen

ts.

Ope

n (s

ee c

omm

ents

in

Exh

ibit

A).

A4

Rev

iew

s ov

er P

erfo

rman

ceM

easu

res

Shou

ld b

e Im

prov

edIT

A, N

IST

, and

BE

A s

houl

d w

ork

with

the

Off

ice

of M

anag

emen

t and

Org

aniz

atio

n (O

MO

) to

de

velo

p an

d im

plem

ent a

for

mal

rev

iew

pro

cess

to

ensu

re th

at th

e pe

rfor

man

cem

easu

res

resu

ltsre

port

ed to

OM

O f

or th

e Pe

rfor

man

ce a

nd

Acc

ount

abili

ty R

epor

t are

acc

urat

e.

Com

plet

ed.

A.4

Exhibit B U.S. Department of Commerce

FY 2004 Management Letter Comments for the National Oceanic and Atmospheric Administration

Accounting for Construction Work-in-Progress (CWIP) Should be Improved

The National Oceanic and Atmospheric Administration (NOAA) has made improvements in its accounting for Construction Work-in-Progress (CWIP) in FY 2004; however, we continued to identifyexceptions in this area. Specifically, we noted the following:

4 out of 38 CWIP projects tested were incorrectly listed as active projects in the June 30, 2004,CA500D, Construction Work in Progress Report. These projects were either completed prior to June30, 2004, or incorrectly classified as CWIP projects.

2 out of 6 transactions listed on the September 30, 2004, Unreconciled Procurement Request listing represented internal use software development costs incurred prior to September 30, 2004. These costs should have been classified as CWIP costs when incurred.

Recommendations:

We continue to recommend that the NOAA Finance Office and the appropriate CWIP activity managers:

1. Transfer costs of CWIP projects immediately to personal property once a constructed property item is placed into service. If the CWIP activity manager requires time to close the CWIP contracts, apreliminary Form 37-6 should be submitted to the Personal Property Office. A final Form 37-6 should be completed once all contracts are closed and finalized, and any cost adjustment should berecorded.

We recommend that the NOAA Finance Office:

2. Ensure that adjustments requested by the CWIP activity managers are recorded timely and anyfollow-up actions, such as additional information requests, are immediately communicated and taken.

We also recommend that the CWIP activity managers:

3. Ensure that all Unreconciled Procurement Request transactions relating to CWIP are timelyinvestigated and resolved. CWIP activity managers should work in conjunction with the NOAA Personal Property Office to ensure that all required information is submitted.

Controls over Personal Property Should be Improved

During our test work over personal property, we noted the following:

6 out of 23 Physical Inventory Report Certifications, used by NOAA’s Line Offices to verify theSunflower system information, reported data that differed from the Sunflower system as of June 30,2004. The data included object classification codes and useful lives, and did not impact the financialstatement data.

The Sunflower system has a limitation whereby if the acquisition cost is subsequently increased (i.e.,upward adjustment) the related accumulated depreciation balance is not properly adjusted. TheSunflower system treats the upward adjustment on a proactive basis. The accumulated depreciation

B.1

Exhibit B (Continued) U.S. Department of Commerce

FY 2004 Management Letter Comments for the National Oceanic and Atmospheric Administration, Continued

balance is manually adjusted by NOAA’s Personal Property Office (PPO) for all items with upward adjustments to the acquisition cost.

The PPO authorized a Sunflower programmer to assign useful lives to future personal propertyadditions. However, in August 2003, the programmer inadvertently changed existing property useful lives in the Sunflower system, which overstated fiscal year 2004 depreciation expense and the relatedaccumulated depreciation balance by $68,617,691. NOAA recorded an audit adjustment atSeptember 30, 2004, to correct its financial statements for this error.

The personal property roll forward as of June 15 and September 15, 2004, did not properly begin with prior year audited balances and did not reconcile to the amounts included in the NOAA FinanceOffice reconciliation to CAMS, NOAA’s general ledger system.

The PPO often receives the supporting documentation needed to enter the personal property data into Sunflower from NOAA Line Offices months, or even years, after the asset has been declaredoperational and placed into service. Although the total adjustment resulting from such delays in FY 2004 was considered immaterial for recording purposes, future delays could materially misstatefinancial statements.

In FY 2004, two supervisory positions remained vacant within the PPO: the NOAA Property BranchChief and Facilities Division Chief. The NOAA Property Branch Chief position was temporarilyfilled with two different rotations, the first of whom was the NOAA Headquarters PropertyManagement Officer, who already had a full workload. Although all transactions processed duringFY 2004 underwent review procedures, the PPO was severely constrained when working with limitedstaff knowledgeable in Sunflower and personal property accounting. Various spreadsheets and schedules received during the audit were incorrect, and could have been prevented had the properoversight and review, required by NOAA’s personal property policies and procedures, been in place.

Recommendations:

We recommend that the NOAA Personal Property Office (PPO):

4. Work with Property Custodians to ensure that those responsible for certifying the physical inventoryin their custodial areas reconcile all data included on the Physical Inventory Report Certifications to their records at least annually.

5. Ensure that the Sunflower system is adequately modified to correct the accumulated depreciationlimitation for all adjustments. The modifications should include manual computation for all personal property items with upward changes in acquisition costs and other information that is needed for thecomputation of accumulated depreciation until the system modifications are made.

6. Perform review procedures to ensure any changes in Sunflower data fields are immediatelyinvestigated and explained. These procedures can be system generated, i.e., exception reports run against data fields that should not be changed unless approved. The PPO should also performquarterly analyses of depreciation expense by comparing the present quarter or year to prior year toensure any significant or unusual fluctuations are investigated and explained.

7. Work with the respective Line Offices to ensure information is submitted to the PPO for recording, ona timely basis and in accordance with its policies and procedures. All capitalizable propertytransferred to NOAA should be recorded as an asset when title passes to NOAA.

B.2

Exhibit B (Continued) U.S. Department of Commerce

FY 2004 Management Letter Comments for the National Oceanic and Atmospheric Administration, Continued

8. Work with NOAA management to permanently fill the vacant supervisory positions within the PPO and to reanalyze the workload for all people in that office. This will enable the PPO to ensureadequate supervisory reviews are performed over all personal property transactions.

We recommend that the NOAA Personal Property Office and NOAA Finance Office:

9. Meet on a monthly basis to discuss any differences resulting from the reconciliation between theSunflower system and CAMS. This meeting will enable both parties to ensure that the data being reconciled is current and that all differences are immediately identified, investigated, and resolved.

Personal Property Lease Accounting Should be Strengthened

The NOAA Procurement Office has made numerous improvements in preparing and completing Lease Determination Worksheets (worksheets); however, we noted the following during our test work over two new operating personal property leases in FY 2004:

1 worksheet was finalized and reviewed on October 13, 2004; however, the reviewer could notanswer questions regarding the nature of the leased asset, the supporting documentation for the fair market value, and other lease questions. While a reviewer is not expected to be fully knowledgeableon all aspects of a complex lease, the reviewer should be familiar with the information used to complete the worksheet.

The fair market value used in the worksheet for one new FY 2004 lease represented the same value assigned to an identical asset leased in FY 2002. However, the value assigned to the FY 2004 leasedasset did not reflect market changes or inflation that may have occurred between the two fiscal years.We determined that the FY 2004 lease classification would not have changed had the fair marketvalue been properly adjusted.

Recommendations:

We recommend that the NOAA Procurement Office:

10. Ensure that all information entered on the Lease Determination Worksheets is supported by documentation that is retained in the respective lease folder before the worksheet is approved by thereviewer.

11. Perform periodic reviews to ensure the controls are operating and that all new leases are properlyaccounted for.

12. Ensure that all worksheet responses for values use current year dollars.

B.3

Exhibit B (Continued) U.S. Department of Commerce

FY 2004 Management Letter Comments for the National Oceanic and Atmospheric Administration, Continued

Accounting for Grant Advances and Payables Should be Improved

During our test work over NOAA’s grants management process, we noted the following:

4 of 5 expired grants selected for test work were not yet closed, although they were expired for morethan 180 days and the necessary documentation had been received from the grantees. Furtherinvestigation revealed that there is a backlog in closing out expired grants dating back to October 31, 2002. At September 30, 2004, we noted that of the 759 grants that were expired, 242 grants were expired for more than 180 days for $5,218,927 and were not yet closed.

7 of 35 active grant files reviewed did not contain the Federal Cash Transactions Report (SF-272) in the files, as required. For 5 out of the 7 grants, there was no evidence of the Grant ManagementDivision’s (GMD) attempt to obtain the missing reports.

For 1 of 35 active grant tested, the CD435 Procurement Request was not date-stamped, as required.

Recommendations:

We continue to recommend that the NOAA GMD:

13. Develop a consistent method of identifying expired grants and enforce timely administrative closeoutof these grants, to ensure that all remaining funds are deobligated.

14. Implement adequate procedures to monitor its grants to ensure that all required monitoring reports are received from grantees timely.

We also recommend that the NOAA GMD:

15. Establish an internal review process to ensure that grant documentation is systematically reviewed to ensure compliance with applicable policies and procedures.

Procedures for Aging Receivables Should be Reviewed

NOAA’s procedures for aging receivables should be reviewed to ensure that adequate reports are generated from CAMS and available for use by decision makers. During FY 2004, NOAA’s Financial Statements Branch used the GLD 171B, Accounts Receivable Aging Report, to determine the allowancefor losses against receivables for financial statement purposes. During our audit, we noted that this reportincluded several credit amounts, because collections or other credit adjustments were not recorded in thesame categories as the related receivables balances. In addition, we noted that other debit amounts were listed under the “not aged” category. As a result, the General Ledger Reporting Branch had to manuallyadjust the aging analysis to determine the proper allowance for doubtful accounts receivable as ofSeptember 30, 2004.

Recommendation:

16. We recommend that the General Ledger Branch and Accounts Receivable Branch continue to workclosely with the CAMS Office to further enhance the accounts receivable module to ensure that reported balances are aged properly.

B.4

Exhibit B (Continued) U.S. Department of Commerce

FY 2004 Management Letter Comments for the National Oceanic and Atmospheric Administration, Continued

Controls over Physical Inventory Counts Should be Strengthened

We noted that 1 of 40 items tested during our inventory count procedures at the National Logistics and Support Center (NLSC) differed from the Consolidated Logistic Support (CLS) system count. The CLS system was not updated as of the inventory observation date of June 15, 2004, for the shipment of an item that occurred on May 5, 2004.

Recommendation:

17. We recommend that the NLSC ensure all Bills of Lading received are compared to the items being shipped. All incorrect Bills of Lading should either be returned for correction, or adjusted by the NLSC warehouse immediately. Once the Bills of Lading are received, the CLS inventory systemshould be immediately updated.

Controls over Payroll Should be Strengthened

During our internal control test work over 43 payroll transactions selected for testing at NOAA, we noted the following:

In pay period 26, one employee was allowed to carry forward a balance of 242.5 hours of annualleave. However, the maximum number of hours employees are allowed to carry forward is 240 hours.

In 1 of 43 cases tested, the timekeeper initialed the time sheet of one employee and that employee was paid despite the fact that the employee’s supervisor did not sign and date the time sheet as evidence of proper approval.

Recommendations:

We recommend that:

18. The Technical Service Unit review all manual adjustments to the payroll system to ensure that accrued annual leave balances carried forward are accurately reported.

19. NOAA’s management ensure that all employees’ timesheets are properly approved by their directsupervisors before their paychecks are disbursed, and that timekeepers only initial time sheets that are signed and dated by the employee’s supervisor.

Accounting for Fund Balance with Treasury and Other Cash Should be Improved

During our test work over the financial management process, we noted the following:

Undeposited Collections (account 1110) included $543,003 which was carried forward from FY 2002. This amount does not represent an undeposited collection, but rather an amount not properlytransferred during the CAMS conversion, which occurred on October 1, 2003.

Suspense Account 13F3875 (FC 65) included an unreconciled difference of $989,202, which was carried forward for at least one year due to the CAMS conversion.

B.5

Exhibit B (Continued) U.S. Department of Commerce

FY 2004 Management Letter Comments for the National Oceanic and Atmospheric Administration, Continued

Recommendations:

We recommend that the NOAA Funds Management Branch:

20. Record all adjustments timely, and ensure all amounts included in the Other Cash account representcash held by NOAA.

21. Investigate and timely resolve the unreconciled difference identified in the Suspense Account, and adjust the general ledger accordingly.

Internal Controls and Accounting for Deferred Revenue Should be Strengthened

During our test work over deferred revenue, we noted the following:

1 of 9 projects selected for testing, with a balance of $375,326, related to an agreement that expired onSeptember 30, 1995. However, NOAA did not liquidate the deferred revenue balance until August 24, 2004.

At the end of FY 2002, the CAMS system did not automatically create the carry forward entry fordeferred revenue balances related to unobligated budgetary resources, totaling $39.6 million, forcertain projects. As recommended by the NOAA CAMS team, the Financial Reporting Divisionmanually recorded the total credit balances under one defaulted project number with a debit to Fund Balance with Treasury and, due to system limitations, manually recorded the offsetting debit using adifferent default project number with a credit to Fund Balance with Treasury. Although these twomanual entries net to zero in the deferred revenue account, it results in an improper matching at the project level.

Recommendations:

We recommend that:

22. The NOAA Line Offices should periodically review their projects with advances and deferred revenuebalances and routinely alert the Accounts Receivable Branch when projects should be closed and when to refund the sponsors for any remaining advance or deferred amounts.

23. The NOAA CAMS team ensure that the debit and credit balances for the projects identified in our test work are properly matched using the same project number.

Internal Controls over Budgetary Resources Should be Improved

During our test work, we noted a difference of $928,064 between the net transfers reported on the SF-133 and the Funds Control Document (obligations to appropriations document) for fund code 29. Thisamount was transferred from fund code 28 (Treasury Fund Symbol 1304/061460) to fund code 29 (Treasury Fund Symbol 1304/061450) during FY 2004, and was inadvertently omitted from the detailed Funds Control Document. However, we noted that the transfer was recorded properly on the FundsControl Summary Report.

B.6

Exhibit B (Continued) U.S. Department of Commerce

FY 2004 Management Letter Comments for the National Oceanic and Atmospheric Administration, Continued

Recommendation:

24. We recommend that NOAA strengthen its internal review process to ensure that a supervisorsystematically reviews the Funds Control Document to ensure that discrepancies are identified and cleared on a timely basis.

Accounting for Supplementary Stewardship Reporting Should be Strengthened

During our test work over supplementary stewardship reporting, we noted that NOAA does not report performance outcomes and measures for its stewardship investment in human capital, as required byStatements of Federal Financial Accounting Standards (SFFAS) Number 8, Supplementary Stewardship Reporting.

Recommendation:

We continue to recommend that:

25. NOAA initiate procedures to report performance outcomes and measures for its stewardshipinvestment in human capital. This includes identifying the performance outcomes and measures, andrequiring the respective departments to gather the information necessary to report this information for the FY 2005 financial statements.

B.7

Exh

ibit

B-1

U

.S. D

epar

tmen

t of

Com

mer

ce

Stat

us o

f P

rior

Yea

r M

anag

emen

t L

ette

r C

omm

ents

N

atio

nal O

cean

ic a

nd A

tmos

pher

ic A

dmin

istr

atio

n

Rec

omm

enda

tion

Num

ber

Rep

orte

dC

omm

ent

KP

MG

’sR

ecom

men

dati

onK

PM

G A

sses

smen

t of

C

urre

nt S

tatu

s

B1

– B

4 A

ccou

ntin

g fo

r C

onst

ruct

ion

Wor

k-in

-Pro

gres

s Sh

ould

be

Impr

oved

Ver

ify

the

valu

atio

n of

the

CW

IP b

alan

ces

in th

e C

A50

0D R

epor

t, by

ensu

ring

that

all

adju

stm

ents

iden

tifie

d qu

arte

rly

and

at y

ear-

end

are

post

ed ti

mel

y by

the

NO

AA

Fin

ance

Off

ice.

Tra

nsfe

r co

sts

of C

WIP

pro

ject

s im

med

iate

ly to

per

sona

l pro

pert

y on

ce a

co

nstr

ucte

d pr

oper

ty it

em is

pla

ced

into

se

rvic

e. I

f th

e C

WIP

act

ivity

man

ager

requ

ires

tim

eto

clo

se th

e C

WIP

con

trac

ts, a

pr

elim

inar

y Fo

rm 3

7-6

shou

ld b

e su

bmitt

edto

the

Pers

onal

Pro

pert

y O

ffic

e. A

fin

al

Form

37-

6 sh

ould

be

com

plet

ed o

nce

all

cont

ract

s ar

e cl

osed

and

fin

aliz

ed, a

nd a

nyco

st a

djus

tmen

t sho

uld

be r

ecor

ded.

Ens

ure

that

rec

onci

liatio

ns a

re p

repa

red

for

all C

WIP

pro

ject

s, a

nd a

djus

tmen

ts p

oste

d to

rem

ove

any

CW

IP b

alan

ces

that

are

not

rela

ted

to th

e co

nstr

uctio

n of

pro

pert

y.

Ens

ure

that

all

unca

pita

lized

neg

ativ

e co

st

bala

nces

are

iden

tifie

d an

d ad

just

ed, t

imel

y.

Com

plet

ed.

Ope

n (s

ee c

omm

ents

in

Exh

ibit

B).

Com

plet

ed.

Com

plet

ed.

B5

Con

trol

s ov

er D

efer

red

Mai

nten

ance

Sho

uld

beIm

prov

ed

The

NO

AA

Rea

l Pro

pert

y O

ffic

e pe

rfor

mpe

riod

ic r

evie

ws

of th

e de

ferr

ed

mai

nten

ance

list

ings

to e

nsur

e th

at th

e pr

ojec

t lis

tings

are

com

plet

e.

Com

plet

ed.

B.8

Exh

ibit

B-1

(C

ontin

ued)

U

.S. D

epar

tmen

t of

Com

mer

ce

Stat

us o

f P

rior

Yea

r M

anag

emen

t L

ette

r C

omm

ents

, Con

tinu

ed

Nat

iona

l Oce

anic

and

Atm

osph

eric

Adm

inis

trat

ion

Rec

omm

enda

tion

Num

ber

Rep

orte

dC

omm

ent

KP

MG

’sR

ecom

men

dati

onK

PM

G A

sses

smen

t of

C

urre

nt S

tatu

sB

6 –

B9

Con

trol

s O

ver

Pers

onal

Pr

oper

ty S

houl

d be

Im

prov

edT

he N

OA

A P

erso

nal P

rope

rty

Off

ice

and

Fina

nce

Off

ice:

Wor

k w

ith th

e re

spec

tive

line

offi

ces

to

ensu

re in

form

atio

n is

sub

mitt

ed to

the

Pers

onal

Pro

pert

y O

ffic

e fo

r re

cord

ing,

on

a tim

ely

basi

s.

Ens

ure

that

all

capi

taliz

able

pro

pert

ytr

ansf

erre

d to

NO

AA

is r

ecor

ded

as a

n as

set

whe

n tit

le p

asse

s to

NO

AA

.

Ens

ure

that

all

unre

conc

iled

proc

urem

ent

requ

ests

are

rev

iew

ed a

t fis

cal y

ear

end

for

any

capi

taliz

able

pro

pert

y ite

ms

not p

rope

rly

reco

rded

.

The

NO

AA

Per

sona

l Pro

pert

y O

ffic

e pe

rfor

mm

anua

l rev

iew

pro

cedu

res

to e

nsur

e th

at a

ll pr

ior

peri

od a

djus

tmen

ts r

epre

sent

va

lid a

djus

tmen

ts to

the

prio

r ye

ar b

alan

ces

and

that

the

prop

erty

rol

l-fo

rwar

ds a

re

subj

ecte

d to

sup

ervi

sory

rev

iew

.

Ope

n (s

ee c

omm

ents

in

Exh

ibit

B).

Ope

n (s

ee c

omm

ents

in

Exh

ibit

B).

Ope

n (s

ee c

omm

ents

in

Exh

ibit

B r

elat

ing

to

CW

IP)

Ope

n (s

ee c

omm

ents

in

Exh

ibit

B).

B10

– B

16

Pers

onal

Pro

pert

yL

ease

Acc

ount

ing

Shou

ld b

e St

reng

then

ed

The

NO

AA

Per

sona

l Pro

pert

y O

ffic

e an

dth

e Pr

ocur

emen

t Off

ice:

Wor

k w

ith th

e Fi

nanc

e O

ffic

e to

impr

ove

the

timel

y co

mm

unic

atio

n of

cha

nges

to

oper

atin

g an

d ca

pita

l lea

ses,

as

wel

l as

toen

sure

that

new

leas

es a

re e

valu

ated

and

re

cord

ed ti

mel

y. T

his

is e

spec

ially

Com

plet

ed.

B.9

Exh

ibit

B-1

(C

ontin

ued)

U

.S. D

epar

tmen

t of

Com

mer

ce

Stat

us o

f P

rior

Yea

r M

anag

emen

t L

ette

r C

omm

ents

, Con

tinu

ed

Nat

iona

l Oce

anic

and

Atm

osph

eric

Adm

inis

trat

ion

Rec

omm

enda

tion

Num

ber

Rep

orte

dC

omm

ent

KP

MG

’sR

ecom

men

dati

onK

PM

G A

sses

smen

t of

C

urre

nt S

tatu

sim

port

ant b

ecau

se th

e Su

nflo

wer

sys

tem

com

pute

s de

prec

iatio

n us

ing

the

info

rmat

ion

inpu

t int

o th

e sy

stem

.

Wor

k to

geth

er to

impr

ove

the

cont

rols

ove

r ac

coun

ting

for

pers

onal

pro

pert

yle

ases

.T

hese

con

trol

s sh

ould

incl

ude

peri

odic

re

view

s to

ens

ure

the

cont

rols

are

ope

ratin

g an

d th

at a

ll ne

w le

ases

are

prop

erly

acco

unte

d fo

r an

d th

at a

ll ch

ange

s to

leas

es

are

timel

y co

mm

unic

ated

.

Ens

ure

that

all

fina

ncia

l sta

tem

ent f

ootn

ote

disc

losu

res

are

upda

ted

to r

efle

ct c

urre

nt

futu

re p

aym

ent e

stim

ates

.

The

NO

AA

Pro

cure

men

t Off

ice:

Plac

e a

nota

tion

on th

e re

vise

d w

orks

heet

stat

ing

whe

n th

e w

orks

heet

was

rev

ised

, w

hyit

was

rev

ised

, and

atta

ch s

uppo

rtin

gdo

cum

enta

tion

for

the

chan

ge.

Ens

ure

that

the

prep

arer

of

the

wor

kshe

et

unde

rsta

nds

all a

spec

ts o

f th

e co

ntra

ct a

s w

ell a

s th

e in

form

atio

n ne

eded

to d

eter

min

e th

e pr

oper

cla

ssif

icat

ion

of th

e le

ase

asca

pita

l or

oper

atin

g.

The

NO

AA

Per

sona

l Pro

pert

y O

ffic

e:

Ens

ure

that

the

Sunf

low

er S

yste

m is

Ope

n (s

ee c

omm

ents

in

Exh

ibit

B).

Com

plet

ed.

Com

plet

ed.

Ope

n (s

ee c

omm

ents

in

Exh

ibit

B).

B.1

0

Exh

ibit

B-1

(C

ontin

ued)

U

.S. D

epar

tmen

t of

Com

mer

ce

Stat

us o

f P

rior

Yea

r M

anag

emen

t L

ette

r C

omm

ents

, Con

tinu

ed

Nat

iona

l Oce

anic

and

Atm

osph

eric

Adm

inis

trat

ion

Rec

omm

enda

tion

Num

ber

Rep

orte

dC

omm

ent

KP

MG

’sR

ecom

men

dati

onK

PM

G A

sses

smen

t of

C

urre

nt S

tatu

sad

equa

tely

mod

ifie

d to

cor

rect

the

accu

mul

ated

dep

reci

atio

n lim

itatio

n as

soo

n as

pos

sibl

e. M

anua

l com

puta

tions

will

be

need

ed f

or a

ccum

ulat

ed d

epre

ciat

ion

until

th

e sy

stem

mod

ific

atio

ns a

re im

plem

ente

d.

Prov

ide

upda

ted

capi

tal l

ease

rol

l for

war

d in

form

atio

n to

the

NO

AA

Fin

ance

Off

ice

in

a tim

ely

man

ner

to e

nsur

e th

e in

form

atio

n in

th

e ge

nera

l led

ger

is p

rope

rly

stat

ed.

Com

plet

ed.

Com

plet

ed.

B17

– B

18

Env

iron

men

tal L

iabi

lity

Con

trol

s Sh

ould

be

Impr

oved

The

NO

AA

Env

iron

men

tal C

ompl

ianc

e,H

ealth

, and

Saf

ety

Off

ice

ensu

re th

at a

ll co

sts

expe

cted

to b

e in

curr

ed to

com

plet

een

viro

nmen

tal l

iabi

litie

s ar

e pr

oper

lyid

entif

ied

and

reco

rded

in th

e fi

nanc

ial

stat

emen

ts.

Ens

ure

that

all

cost

s un

der

an

envi

ronm

enta

l pro

ject

are

iden

tifie

d an

d ca

ptur

ed, e

ven

whe

n th

e co

sts

will

be

incu

rred

by

diff

eren

t off

ices

. C

omm

uni-

catio

n sh

ould

be

mai

ntai

ned

betw

een

the

vari

ous

offi

ces

invo

lved

inth

e co

st e

stim

ate

to e

nsur

e th

at a

ll co

sts

are

capt

ured

, and

re

spon

sibi

litie

s ar

e cl

earl

y de

fine

d. A

ce

ntra

l poi

nt o

f co

ntac

t sho

uld

be a

ppoi

nted

to e

nsur

e al

l cos

ts a

re id

entif

ied

and

capt

ured

, NO

AA

-wid

e.

Com

plet

ed.

B.1

1

Exh

ibit

B-1

(C

ontin

ued)

U

.S. D

epar

tmen

t of

Com

mer

ce

Stat

us o

f P

rior

Yea

r M

anag

emen

t L

ette

r C

omm

ents

, Con

tinu

ed

Nat

iona

l Oce

anic

and

Atm

osph

eric

Adm

inis

trat

ion

Rec

omm

enda

tion

Num

ber

Rep

orte

dC

omm

ent

KP

MG

’sR

ecom

men

dati

onK

PM

G A

sses

smen

t of

C

urre

nt S

tatu

sB

19 –

B23

A

ccou

ntin

g fo

r G

rant

A

dvan

ces

and

Gra

nt P

ayab

les

Shou

ld b

e Im

prov

ed

The

NO

AA

GM

D e

stab

lish

timel

ines

for

its

staf

f to

req

uest

clo

seou

t doc

umen

tatio

n on

ex

pire

d gr

ants

.

Dev

elop

a c

onsi

sten

t met

hod

of id

entif

ying

expi

red

gran

ts a

nd e

nfor

ce ti

mel

yad

min

istr

ativ

e cl

oseo

ut o

f th

ese

gran

ts to

en

sure

that

all

rem

aini

ng f

unds

are

de

oblig

ated

.

Impl

emen

t ade

quat

e pr

oced

ures

to m

onito

rgr

ants

in o

rder

to e

nsur

e th

at a

ll re

port

s ar

e re

ceiv

ed f

rom

gra

ntee

s, ti

mel

y.

Est

ablis

h an

inte

rnal

rev

iew

pro

cess

so

that

whe

n da

ta is

ent

ered

into

NO

AA

’s G

rant

Syst

em, a

sup

ervi

sor

syst

emat

ical

ly r

evie

ws

it. Impl

emen

t pro

cedu

res

to e

nsur

e th

at

gran

tees

sub

mit

thei

r O

MB

Cir

cula

r A

-133

audi

t rep

orts

, tim

ely.

In

case

s w

here

the

Sing

le A

udit

repo

rt w

as n

ot s

ubm

itted

to th

e Fe

dera

l Aud

it C

lear

ingh

ouse

dat

abas

e,

NO

AA

’s G

MD

sho

uld

obta

in it

dir

ectly

from

the

gran

tees

. If

the

gran

tee

has

not

com

plet

ed it

s Si

ngle

Aud

it an

d G

MD

de

cide

s to

issu

e th

e gr

ant a

war

d, th

e aw

ard

docu

men

t sho

uld

incl

ude

a sp

ecia

l con

ditio

n to

info

rm th

e gr

ante

e th

at th

e re

port

mus

t be

subm

itted

with

in a

spe

cifi

ed ti

me,

or

the

fund

ing

will

be

plac

ed in

a “

hold

” st

atus

.

Com

plet

ed.

Ope

n (s

ee c

omm

ents

in

Exh

ibit

B).

Ope

n (s

ee c

omm

ents

in

Exh

ibit

B).

Com

plet

ed.

Com

plet

ed.

B.1

2

Exh

ibit

B-1

(C

ontin

ued)

U

.S. D

epar

tmen

t of

Com

mer

ce

Stat

us o

f P

rior

Yea

r M

anag

emen

t L

ette

r C

omm

ents

, Con

tinu

ed

Nat

iona

l Oce

anic

and

Atm

osph

eric

Adm

inis

trat

ion

Rec

omm

enda

tion

Num

ber

Rep

orte

dC

omm

ent

KP

MG

’sR

ecom

men

dati

onK

PM

G A

sses

smen

t of

C

urre

nt S

tatu

s

B24

– B

27

Con

trol

s ov

er R

eal P

rope

rty

Tra

nsac

tions

Sho

uld

beIm

prov

ed

The

NO

AA

Rea

l Pro

pert

y O

ffic

e en

sure

that

al

l inf

orm

atio

n is

tim

ely

com

mun

icat

ed

from

the

line

offi

ces

to th

e R

eal P

rope

rty

Adm

inis

trat

ive

Supp

ort C

ente

rs a

nd

Hea

dqua

rter

sR

eal P

rope

rty

Off

ices

to

ensu

re a

ccur

ate

acco

untin

g. C

oord

inat

eef

fort

s w

ith th

e N

OA

A F

inan

cial

Rep

ortin

g B

ranc

h to

ens

ure

that

all

upda

ted

info

rmat

ion

is a

ccur

atel

y pr

epar

ed f

or th

e re

al p

rope

rty

roll

forw

ard

and

the

info

rmat

ion

in th

e ge

nera

l led

ger

is p

rope

rly

stat

ed.

Ens

ure

that

all

cert

ific

atio

ns a

re

timel

y pe

rfor

med

on

the

Form

37-

6, a

nd th

at

all i

nfor

mat

ion

is r

ecei

ved

by th

e Fi

nanc

eO

ffic

e tim

ely,

to e

nsur

e ac

cura

te a

ccou

ntin

g fo

r co

mpl

eted

pro

pert

ypr

ojec

ts.

Perf

orm

pe

riod

ic r

evie

ws

of a

ll re

al p

rope

rty

capi

tal

and

oper

atin

g le

ases

to e

nsur

e al

l act

ivity

is

prop

erly

rec

orde

d.

Com

plet

ed.

B28

Acc

ount

ing

for

Ope

ratin

g M

ater

ials

and

Sup

plie

sA

llow

ance

Sho

uld

be

Stre

ngth

ened

NO

AA

’s N

atio

nal W

eath

er S

ervi

ce r

evie

wth

e ob

sole

scen

ce r

eser

ve m

etho

dolo

gy a

nden

sure

it is

con

sist

ently

app

lied

at th

e N

LSC

an

d N

RC

at a

“su

bsys

tem

leve

l” w

hich

re

sults

in a

mor

e pr

ecis

e es

timat

e of

the

deco

mm

issi

onin

g re

serv

e.

Com

plet

ed.

B.1

3

Exh

ibit

B-1

(C

ontin

ued)

U

.S. D

epar

tmen

t of

Com

mer

ce

Stat

us o

f P

rior

Yea

r M

anag

emen

t L

ette

r C

omm

ents

, Con

tinu

ed

Nat

iona

l Oce

anic

and

Atm

osph

eric

Adm

inis

trat

ion

Rec

omm

enda

tion

Num

ber

Rep

orte

dC

omm

ent

KP

MG

’sR

ecom

men

dati

onK

PM

G A

sses

smen

t of

C

urre

nt S

tatu

sB

29 –

B30

Pr

oced

ures

for

Agi

ng

Rec

eiva

bles

Sho

uld

be

Rev

iew

ed

The

Gen

eral

Led

ger

Bra

nch

and

Acc

ount

sR

ecei

vabl

e B

ranc

h w

ork

clos

ely

with

the

CA

MS

Off

ice

to f

urth

er e

nhan

ce th

e ac

coun

ts r

ecei

vabl

e m

odul

e to

ens

ure

that

ba

lanc

es a

reag

ed p

rope

rly.

NO

AA

’sFi

nanc

e O

ffic

e sh

ould

per

iodi

cally

rev

iew

th

e ag

ing

repo

rt, a

nd (

1) ta

ke c

orre

ctiv

e ac

tion

on d

elin

quen

t acc

ount

s, a

nd (

2) a

djus

tth

e al

low

ance

for

unc

olle

ctib

le a

ccou

nt

prov

isio

n.

Ope

n (s

ee c

omm

ents

in

Exh

ibit

B).

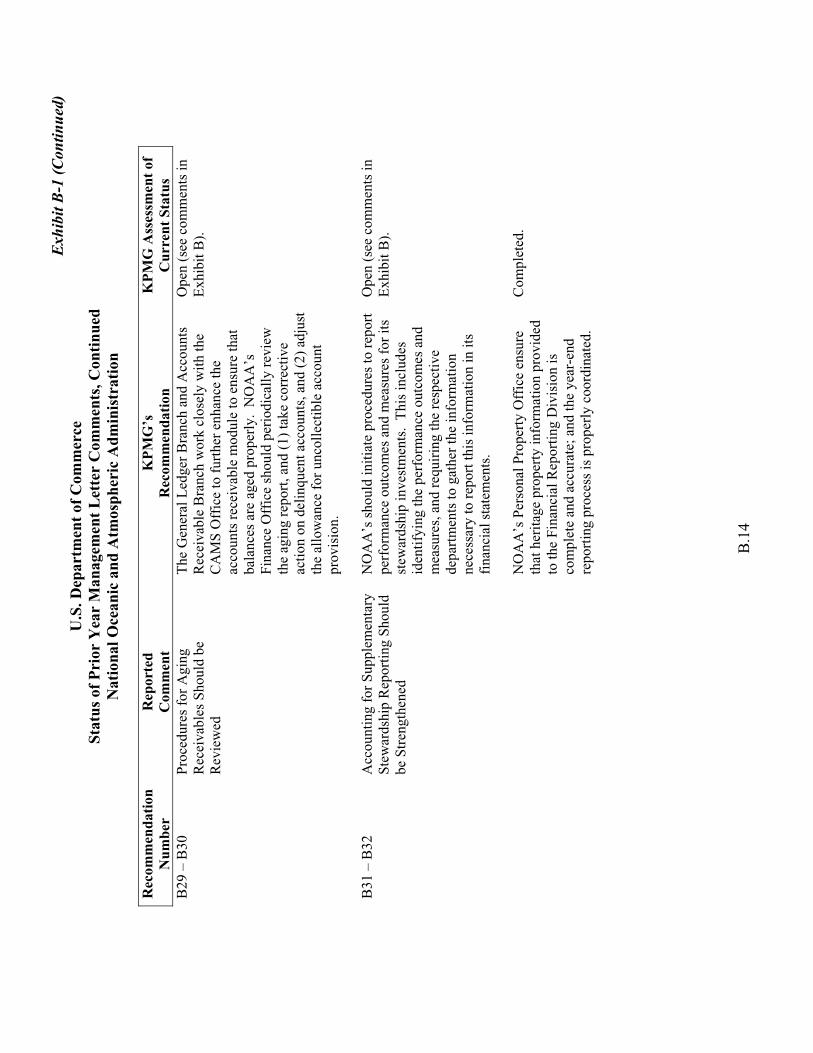

B31

– B

32

Acc

ount

ing

for

Supp

lem

enta

rySt

ewar

dshi

p R

epor

ting

Shou

ldbe

Str

engt

hene

d

NO

AA

’s s

houl

d in

itiat

e pr

oced

ures

to r

epor

t pe

rfor

man

ceou

tcom

es a

nd m

easu

res

for

its

stew

ards

hip

inve

stm

ents

. T

his

incl

udes

id

entif

ying

the

perf

orm

ance

out

com

es a

ndm

easu

res,

and

req

uiri

ng th

e re

spec

tive

depa

rtm

ents

to g

athe

r th

e in

form

atio

nne

cess

ary

to r

epor

t thi

s in

form

atio

n in

its

fina

ncia

l sta

tem

ents

.

NO

AA

’s P

erso

nal P

rope

rty

Off

ice

ensu

reth

at h

erita

ge p

rope

rty

info

rmat

ion

prov

ided

to th

e Fi

nanc

ial R

epor

ting

Div

isio

n is

co

mpl

ete

and

accu

rate

; and

the

year

-end

repo

rtin

gpr

oces

s is

pro

perl

y co

ordi

nate

d.

Ope

n (s

ee c

omm

ents

in

Exh

ibit

B).

Com

plet

ed.

B.1

4

Exhibit C Department of Commerce

FY 2004 Management Letter Comments for the National Institute of Standards and Technology and NIST-Serviced Bureaus

C.1

Controls over the Review of Time and Attendance (T&A) Reports Should be Improved

During our control test work over payroll transactions, we noted that for pay period 26, one of the National Telecommunications and Information Administration (NTIA) employees’ Time and Attendance(T&A) Report was signed but not dated by the supervisor. Therefore, we could not verify that the T&A was approved by the supervisor in a timely manner.

Recommendation:

1. We recommend that management ensure that all employees’ T&A Reports are signed and dated by the supervisor in a timely manner.

Controls over the Reconciliation of Property, Plant, and Equipment Should be Improved

During our test work over the National Institute of Standards and Technology (NIST)’s personal propertyreconciliation (Accounts 1750, 1720.02, 1720.03) for the month of June 2004, we noted that NIST did not start its process to resolve unreconciled items for FY 1999 for a total of $186,107 until February 2003,and did not complete the reconciliation until August 2004.

Recommendation:

2. We recommend that NIST ensure that differences noted in the monthly personal propertyreconciliations are resolved timely.

Controls over the Review of ELGP Loan Guarantee Liability Account Should be Improved

During our test work over subsidy estimates for the Emergency Loan Guarantee Program (ELGP), wenoted that the FY 2004 downward re-estimates were incorrectly calculated for the Oil and Gas Program.ELGP recorded an adjustment by taking the FY 2004 total re-estimate less the original re-estimate amount. However, because the Loan Guarantee Liability account is adjusted each year, the FY 2004 adjustment amount should have been calculated by taking the FY 2004 total re-estimate less the FY 2003total re-estimate.

Recommendation:

3. We recommend that the NIST Financial Statements Group ensure proper review of the Loan Guarantee Liability account and related calculations to ensure that the annual subsidy re-estimates are properly recorded.

Corrective Action Plan for Prior Year’s Finding Should be Implemented

During our reimbursable agreement internal control test work and follow-up on the prior year’s finding, we noted that NIST did not start to implement its corrective action plan for the prior year reimbursableagreement finding until October 14, 2004. Our prior year recommendation related to requiring agenciesto forward, to NIST, reimbursable agreements immediately after they are executed.

Exhibit C (Continued) Department of Commerce

FY 2004 Management Letter Comments for the National Institute of Standards and Technology and NIST-Serviced Bureaus, Continued

Recommendation:

4. We recommend that NIST ensure that its corrective action plan for obtaining reimbursable agreementdocuments is implemented timely.

C.2

Exh

ibit

C-1

U

.S. D

epar

tmen

t of

Com

mer

ce

Stat

us o

f P

rior

Yea

r M

anag

emen

t L

ette

r C

omm

ents

N

atio

nal I

nsti

tute

of

Stan

dard

s an

d T

echn

olog

y an

d N

IST

-Ser

vice

d B

urea

us

Rec

omm

enda

tion

Num

ber

Rep

orte

dC

omm

ent

KP

MG

’sR

ecom

men

dati

onK

PM

G A

sses

smen

t of

C

urre

nt S

tatu

s

C1

Rec

onci

liatio

n of

Per

sona

l Pr

oper

ty b

etw

een

the

Subs

idia

ryan

d th

e G

ener

al L

edge

rs N

eeds

to

be I

mpr

oved

NIS

T F

inan

ce D

ivis

ion

impl

emen

t a p

olic

yth

at r

equi

res

the

reco

ncili

atio

n be

twee

n th

e pe

rson

al p

rope

rty

subs

idia

ry a

nd g

ener

alle

dger

s fo

r al

l fun

ds.

Com

plet

ed.

C2

Rec

onci

liatio

n D

iffe

renc

es w

ith

the

Tec

hnol

ogy

Adm

inis

trat

ion’

sFu

nd B

alan

ce w

ith T

reas

ury

Shou

ld b

e R

esol

ved

NIS

T, i

n co

njun

ctio

n w

ith th

e D

epar

tmen

t of

Com

mer

ce O

ffic

e of

Fin

anci

al

Man

agem

ent,

cont

act t

he D

epar

tmen

t of

Tre

asur

y to

suc

cess

fully

res

olve

the

issu

e w

ith th

e T

echn

olog

y A

dmin

istr

atio

n’s

SF-

6653

, as

soon

as

poss

ible

.

Com

plet

ed.

D1

Rep

ortin

gof

Dif

fere

nces

Not

edin

the

Rec

onci

liatio

n of

Fun

dB

alan

cew

ith T

reas

ury

Nee

ds to

be

Im

prov

ed

NIS

T/C

AM

S ta

ke p

rope

r ac

tion

to e

nsur

eth

at d

iffe

renc

es a

re p

rope

rly

clas

sifi

ed o

n th

e SF

-665

2.

Com

plet

ed.

D2

Man

agem

entR

evie

wC

ontr

ols

Rel

ated

to S

igni

ng a

nd D

atin

g th

e T

reas

ury

SF-2

24 N

eeds

to b

eIm

prov

ed

NIS

T’s

Fin

anci

al S

ervi

ces

Gro

up (

FSG

) m

anag

emen

t im

plem

ent a

sup

ervi

sory

revi

ew to

ens

ure

that

the

SF-2

24 is

sig

ned

and

date

d be

fore

sub

mis

sion

to T

reas

ury.

Com

plet

ed.

D3

– D

4 R

eim

burs

able

Agr

eem

ent

Am

ount

s Sh

ould

be

Rec

orde

d as

U

nfill

ed C

usto

mer

Ord

ers,

T

imel

y

The

per

form

ing

agen

cy f

orw

ards

all

reim

burs

able

agre

emen

ts to

the

FSG

im

med

iate

lyaf

ter

they

are

exe

cute

d. T

he

FSG

sho

uld

mon

itor

perf

orm

ing

agen

cies

to

ensu

re th

at r

eim

burs

able

agr

eem

ents

are

rece

ived

and

rec

orde

d pr

oper

ly a

nd ti

mel

y.

Ope

n (s

ee c

omm

ents

in

Exh

ibit

C).

C.3

Exh

ibit

C-1

(C

ontin

ued)

U

.S. D

epar

tmen

t of

Com

mer

ce

Stat

us o

f P

rior

Yea

r M

anag

emen

t L

ette

r C

omm

ents

, Con

tinu

ed

Nat

iona

l Ins

titu

te o

f St

anda

rds

and

Tec

hnol

ogy

and

NIS

T-S

ervi

ced

Bur

eaus

Rec

omm

enda

tion

Num

ber

Rep

orte

dC

omm

ent

KP

MG

’sR

ecom

men

dati

onK

PM

G A

sses

smen

t of

C

urre

nt S

tatu

sD

5A

ccou

ntin

g fo

r th

e D

efau

lted

Loa

n G

uara

ntee

Lia

bilit

y N

eeds

to b

e Im

prov

ed

The

EL

GP

pers

onne

l rev

iew

the

guid

ance

on r

ecor

ding

def

aulte

d lo

an g

uara

ntee

s an

d en

sure

that

pro

per

amou

nts

are

tran

sfer

red

to th

e cr

edit

prog

ram

subs

idy

allo

wan

ce

acco

unt f

or f

utur

e de

faul

ts.

Com

plet

ed.

D6

Acc

ount

ing

for

Subs

idy

Est

imat

es N

eeds

to b

e Im

prov

edT

he E

LG

P pe

rson

nel d

eter

min

e th

e lo

an

disb

urse

men

t am

ount

s fo

r fu

ture

loan

gu

aran

tee

coho

rts,

and

rec

ord

a su

bsid

yon

lyon

the

amou

nts

disb

urse

d.

Com

plet

ed.

D7

Acc

ount

ing

for

Acc

rual

s N

eeds

to b

e Im

prov

edT

he p

rogr

amof

fice

che

ck a

nd s

ee if

re

cent

ly s

ubm

itted

invo

ices

hav

e be

en

proc

esse

d be

fore

pre

pari

ng th

e ac

crua

l es

timat

e. T

he p

rogr

am o

ffic

e sh

ould

in

clud

e an

y un

paid

invo

ices

in th

e ac

crua

l es

timat

e in

add

ition

to th

e in

voic

es th

eyex

pect

to r

ecei

ve r

elat

ed to

the

fisc

al y

ear

for

serv

ices

pro

vide

d.

Com

plet

ed.

Not

e th

at p

rior

yea