KEY CONCERNS FOR THE LITHIUM INDUSTRY TO THE END OF … · 2017-06-05 · KEY CONCERNS FOR THE...

26

1 KEY CONCERNS FOR THE LITHIUM INDUSTRY TO THE END OF THE DECADE LITHIUM SUPPLY & MARKETS CONFERENCE MONTREAL, CANADA 31 MAY 2017 For personal use only

Transcript of KEY CONCERNS FOR THE LITHIUM INDUSTRY TO THE END OF … · 2017-06-05 · KEY CONCERNS FOR THE...

1

KEY CONCERNS FOR THE LITHIUM INDUSTRY TO THE END OF THE DECADELITHIUM SUPPLY & MARKETS CONFERENCE MONTREAL, CANADA

31 MAY 2017

For

per

sona

l use

onl

y

2

DEMAND

For

per

sona

l use

onl

y

3

0102030405060708090

2000 2005 2010 2015

LCE

kt

Lithium Consumption by Li-ion Battery End Use (LCE kt)

Portable Electronics Aftermarket

Power Devices & Other ESS Applications

Automotive

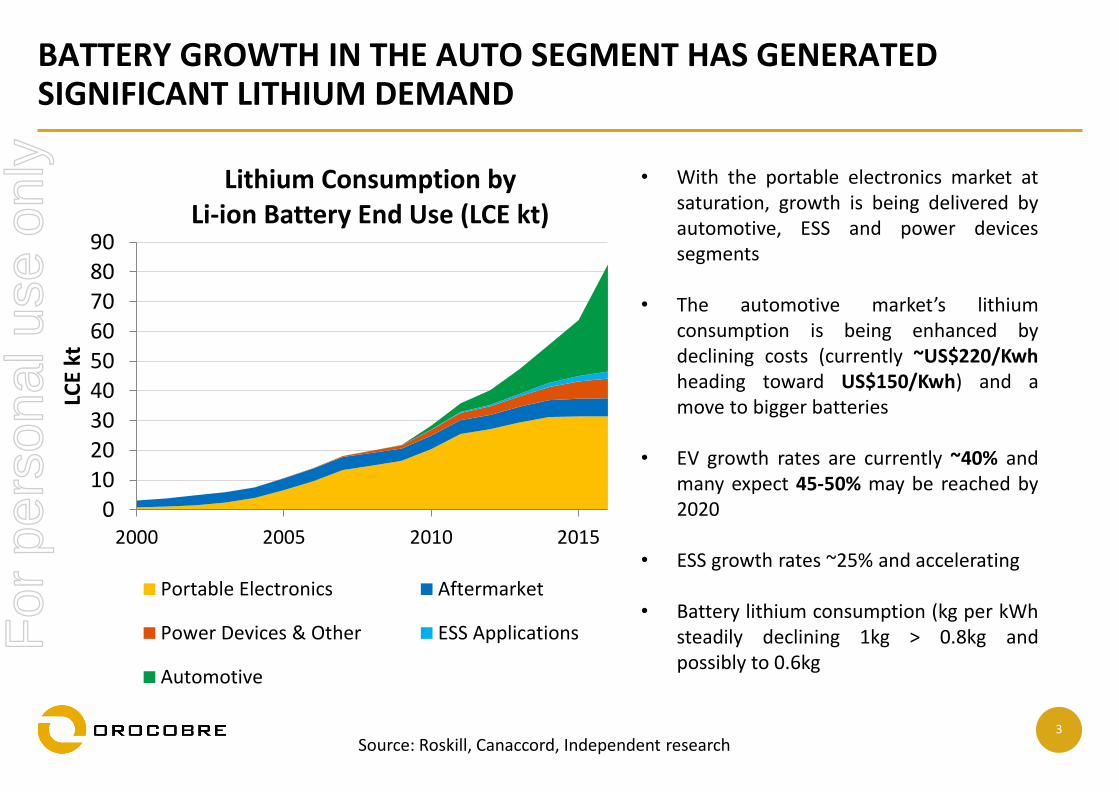

BATTERY GROWTH IN THE AUTO SEGMENT HAS GENERATED SIGNIFICANT LITHIUM DEMAND

• With the portable electronics market atsaturation, growth is being delivered byautomotive, ESS and power devicessegments

• The automotive market’s lithiumconsumption is being enhanced bydeclining costs (currently ~US$220/Kwhheading toward US$150/Kwh) and amove to bigger batteries

• EV growth rates are currently ~40% andmany expect 45-50% may be reached by2020

• ESS growth rates ~25% and accelerating

• Battery lithium consumption (kg per kWhsteadily declining 1kg > 0.8kg andpossibly to 0.6kg

Source: Roskill, Canaccord, Independent research

For

per

sona

l use

onl

y

4

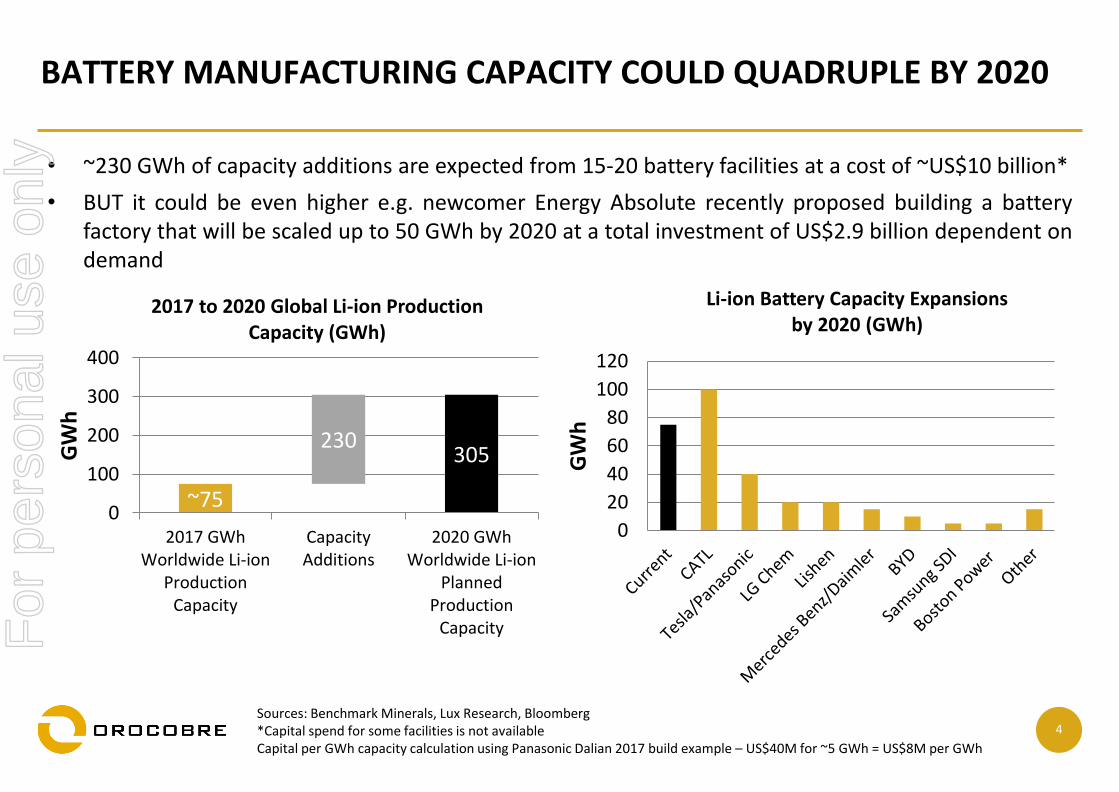

BATTERY MANUFACTURING CAPACITY COULD QUADRUPLE BY 2020

0

20

40

60

80

100

120

GW

h

Li-ion Battery Capacity Expansions by 2020 (GWh)

~75

305230

0

100

200

300

400

2017 GWhWorldwide Li-ion

ProductionCapacity

CapacityAdditions

2020 GWhWorldwide Li-ion

PlannedProduction

Capacity

GW

h

2017 to 2020 Global Li-ion Production Capacity (GWh)

• ~230 GWh of capacity additions are expected from 15-20 battery facilities at a cost of ~US$10 billion*

• BUT it could be even higher e.g. newcomer Energy Absolute recently proposed building a batteryfactory that will be scaled up to 50 GWh by 2020 at a total investment of US$2.9 billion dependent ondemand

Sources: Benchmark Minerals, Lux Research, Bloomberg *Capital spend for some facilities is not available Capital per GWh capacity calculation using Panasonic Dalian 2017 build example – US$40M for ~5 GWh = US$8M per GWh

For

per

sona

l use

onl

y

5

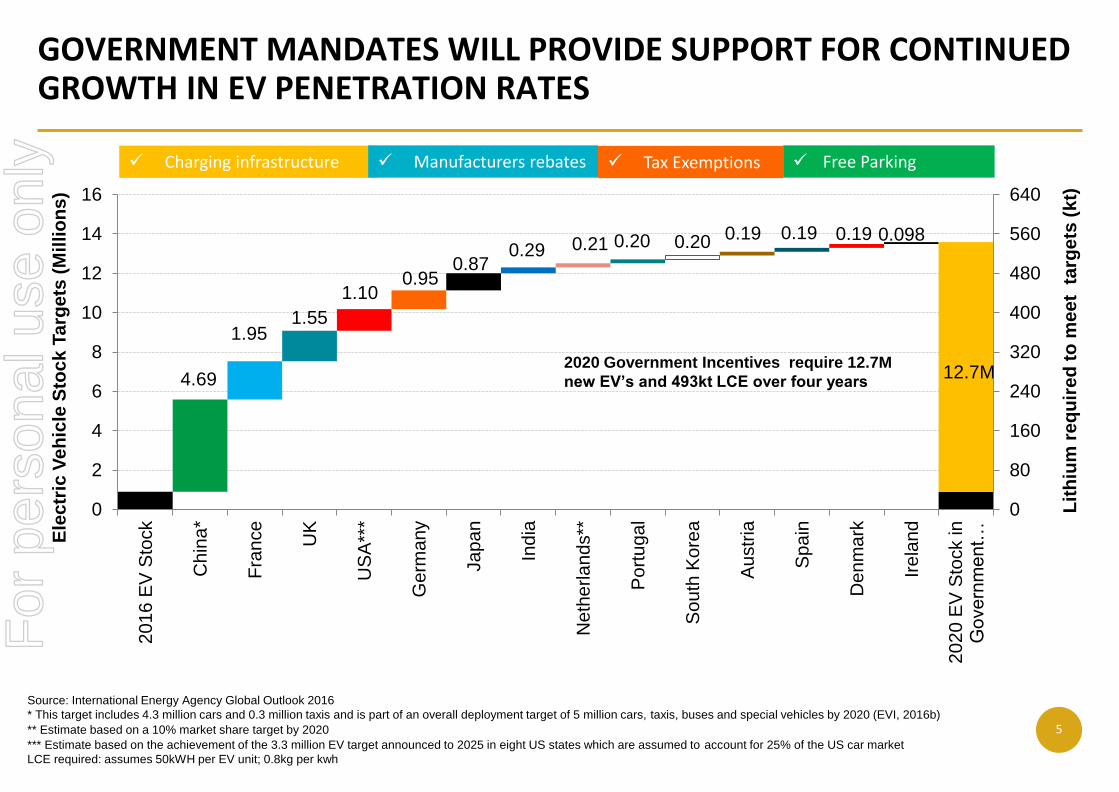

GOVERNMENT MANDATES WILL PROVIDE SUPPORT FOR CONTINUED GROWTH IN EV PENETRATION RATES

4.69

1.951.55

1.100.95

0.870.29 0.21 0.20 0.20 0.19 0.19 0.19 0.098

12.7M

0

80

160

240

320

400

480

560

640

0

2

4

6

8

10

12

14

16

20

16

EV

Sto

ck

Ch

ina

*

Fra

nce

UK

US

A**

*

Ge

rma

ny

Ja

pa

n

India

Ne

the

rla

nd

s**

Po

rtu

ga

l

So

uth

Ko

rea

Au

str

ia

Spain

De

nm

ark

Ire

lan

d

20

20

EV

Sto

ck in

Government…

Lit

hiu

m r

eq

uir

ed

to

me

et

ta

rge

ts (

kt)

Ele

ctr

ic V

eh

icle

Sto

ck

Ta

rge

ts (

Mil

lio

ns

)

2020 Government Incentives require 12.7M

new EV’s and 493kt LCE over four years

Source: International Energy Agency Global Outlook 2016

* This target includes 4.3 million cars and 0.3 million taxis and is part of an overall deployment target of 5 million cars, taxis, buses and special vehicles by 2020 (EVI, 2016b)

** Estimate based on a 10% market share target by 2020

*** Estimate based on the achievement of the 3.3 million EV target announced to 2025 in eight US states which are assumed to account for 25% of the US car market

LCE required: assumes 50kWH per EV unit; 0.8kg per kwh

✓ Charging infrastructure ✓ Manufacturers rebates ✓ Free Parking✓ Tax Exemptions

For

per

sona

l use

onl

y

6

OVER 120 DIFFERENT EV MODELS ARE EXPECTED BY 2020

Sources: Bloomberg

For

per

sona

l use

onl

y

7

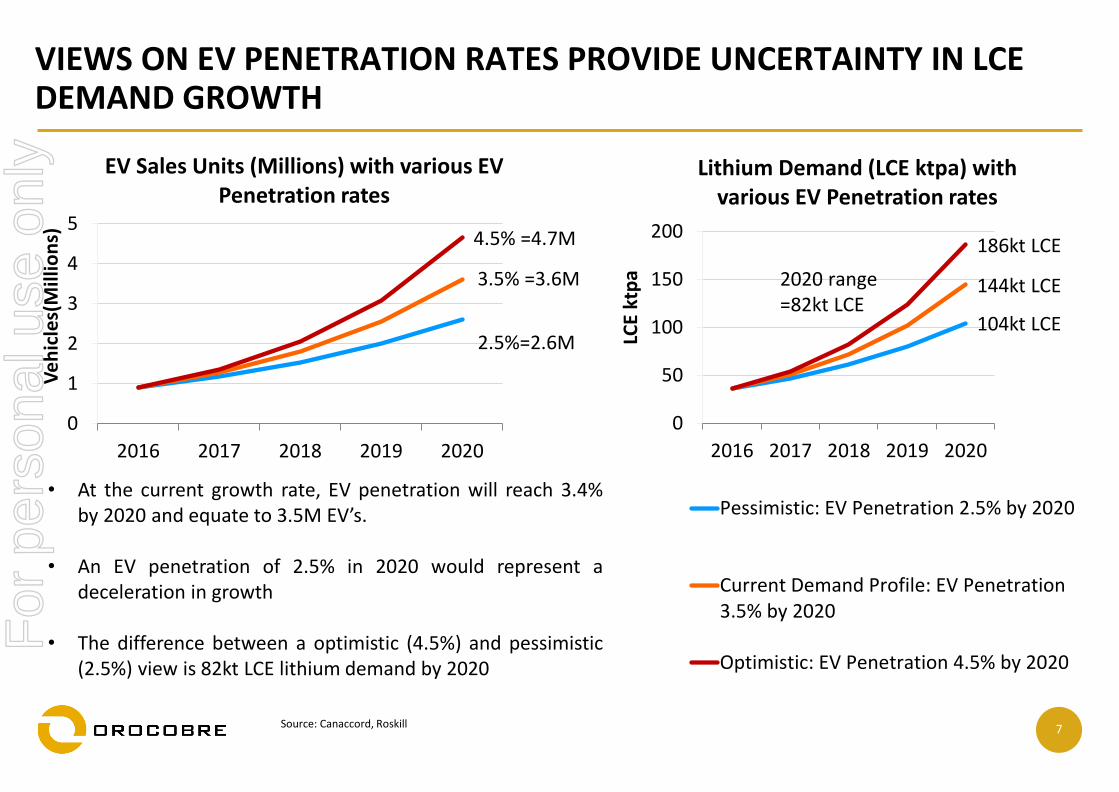

2.5%=2.6M

3.5% =3.6M

4.5% =4.7M

0

1

2

3

4

5

2016 2017 2018 2019 2020

Ve

hic

les(

Mill

ion

s)

EV Sales Units (Millions) with various EV Penetration rates

104kt LCE

144kt LCE

186kt LCE

0

50

100

150

200

2016 2017 2018 2019 2020

LCE

ktp

a

Lithium Demand (LCE ktpa) with various EV Penetration rates

Pessimistic: EV Penetration 2.5% by 2020

Current Demand Profile: EV Penetration3.5% by 2020

Optimistic: EV Penetration 4.5% by 2020

2020 range =82kt LCE

VIEWS ON EV PENETRATION RATES PROVIDE UNCERTAINTY IN LCE DEMAND GROWTH

• At the current growth rate, EV penetration will reach 3.4%by 2020 and equate to 3.5M EV’s.

• An EV penetration of 2.5% in 2020 would represent adeceleration in growth

• The difference between a optimistic (4.5%) and pessimistic(2.5%) view is 82kt LCE lithium demand by 2020

Source: Canaccord, Roskill

For

per

sona

l use

onl

y

8

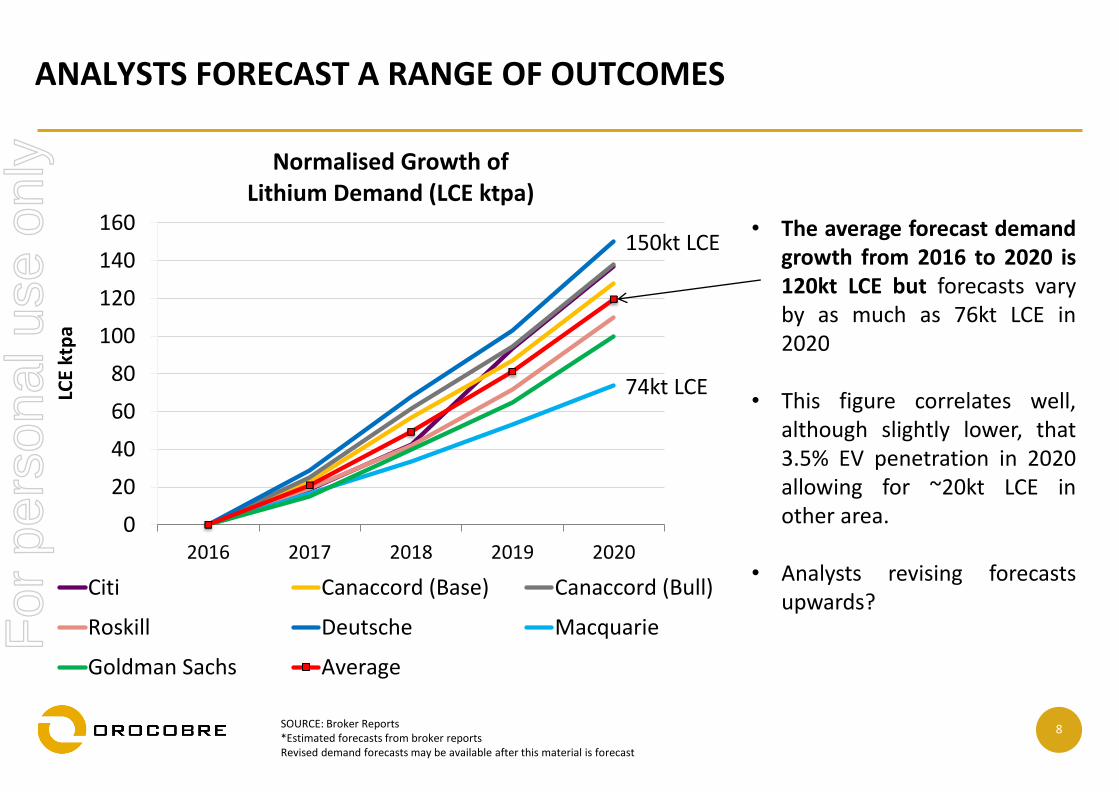

ANALYSTS FORECAST A RANGE OF OUTCOMES

150kt LCE

74kt LCE

0

20

40

60

80

100

120

140

160

2016 2017 2018 2019 2020

LCE

ktp

a

Normalised Growth of Lithium Demand (LCE ktpa)

Citi Canaccord (Base) Canaccord (Bull)

Roskill Deutsche Macquarie

Goldman Sachs Average

SOURCE: Broker Reports*Estimated forecasts from broker reportsRevised demand forecasts may be available after this material is forecast

• The average forecast demandgrowth from 2016 to 2020 is120kt LCE but forecasts varyby as much as 76kt LCE in2020

• This figure correlates well,although slightly lower, that3.5% EV penetration in 2020allowing for ~20kt LCE inother area.

• Analysts revising forecastsupwards?

For

per

sona

l use

onl

y

9

WILL WE HAVE SUFFICIENT BATTERY CAPACITY?

0

50

100

150

200

250

300

350

2017 2018 2019 2020

GW

h

Battery Capacity & Potential Demand Scenarios (GWh)

Incremental Demand: EV Penetration4.5% by 2020

Incremental Demand: EV Penetration3.5% by 2020

Pessimistic: EV Penetration 2.5% by2020

Non-Auto Battery Lithium Demand

Forecast Battery Capacity

• EV growth rates are currently ~40% which would result in a 3.4% EV penetration rate by 2020, however a growing number of industry participants believe penetration rates of at least 4.5% are possible given recent momentum and support e.g. Government subsidies and policies, lowering costs, growing range of EV models available to consumers

• However, any growth above 4.5% EV penetration OR further upside to ESS growth (>30%) would require battery capacity above the current forecasted ~305 GWh figure.

Assumes 0.8kg LCE t per kWhNon-Auto Battery Lithium Demand Assumptions: ESS 30% YoY growth (2010-2015 ~25% p.a. and growing); Power, Aftermarket and Portable battery market growth at 4% YoY

For

per

sona

l use

onl

y

10

SUPPLY

For

per

sona

l use

onl

y

11

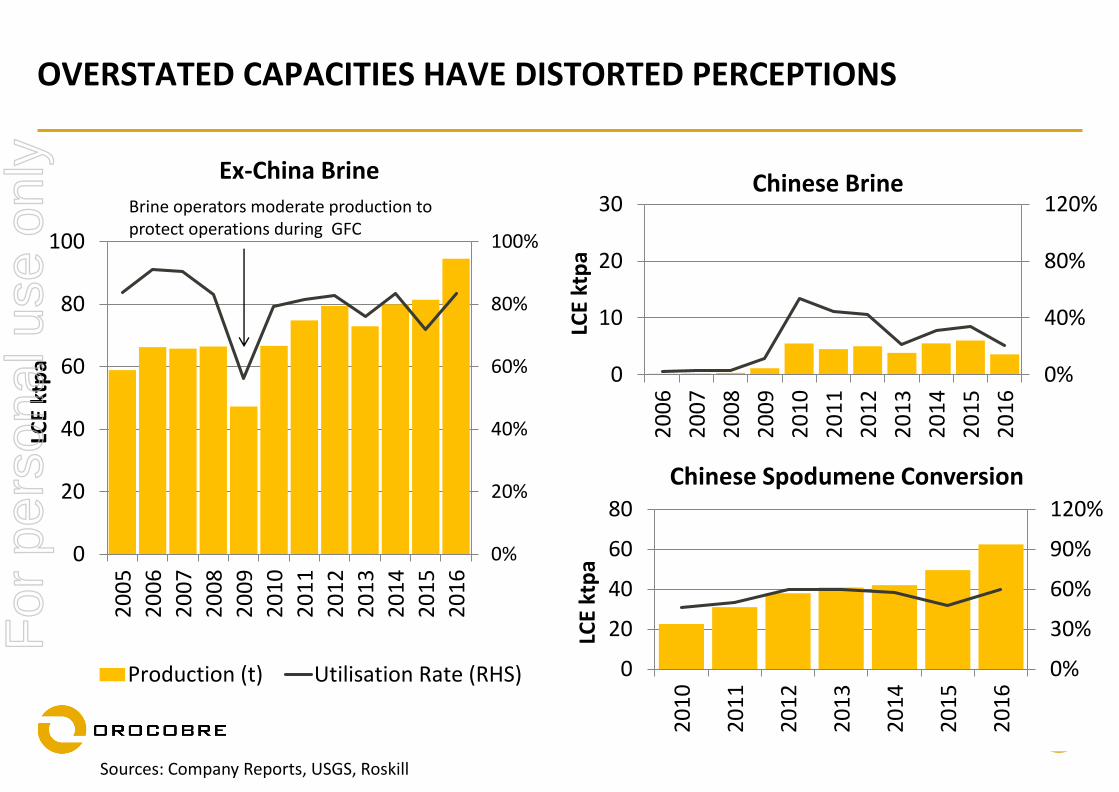

0%

40%

80%

120%

0

10

20

30

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

LCE

ktp

a

Chinese Brine

0%

20%

40%

60%

80%

100%

0

20

40

60

80

100

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

LCE

ktp

a

Ex-China Brine

Production (t) Utilisation Rate (RHS)

OVERSTATED CAPACITIES HAVE DISTORTED PERCEPTIONS

Sources: Company Reports, USGS, Roskill

Brine operators moderate production to protect operations during GFC

0%

30%

60%

90%

120%

0

20

40

60

80

20

10

20

11

20

12

20

13

20

14

20

15

20

16

LCE

ktp

a

Chinese Spodumene Conversion

For

per

sona

l use

onl

y

12

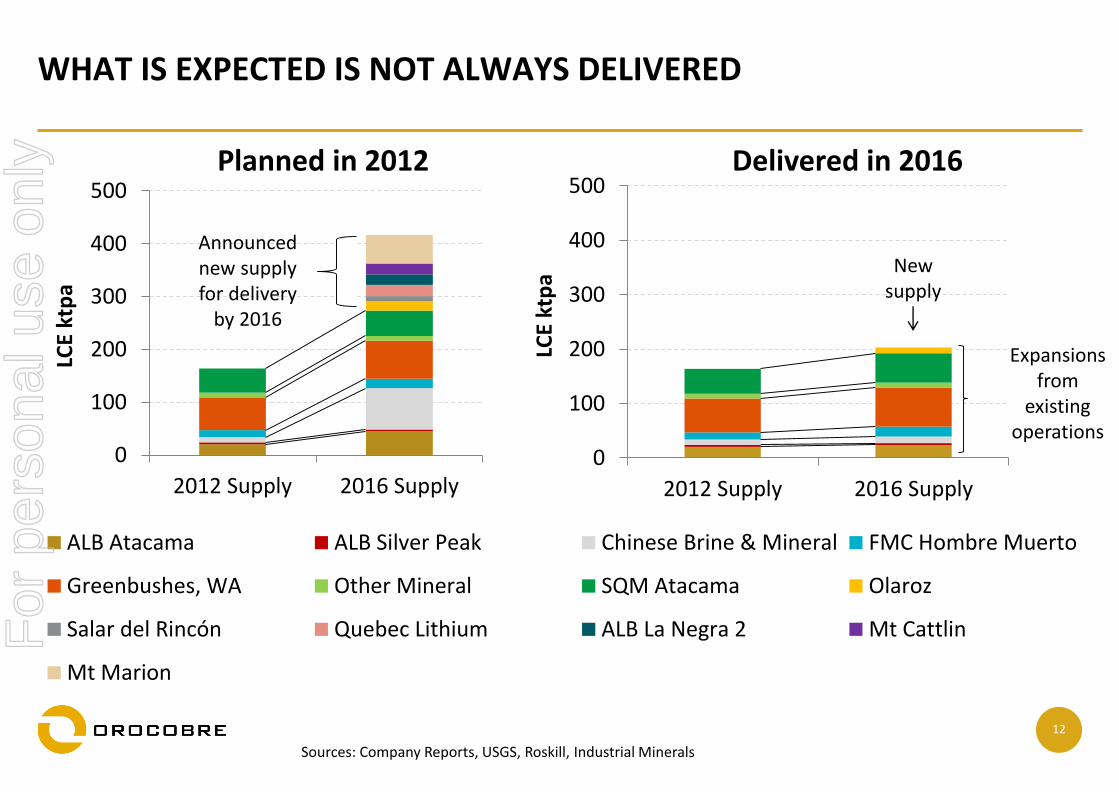

WHAT IS EXPECTED IS NOT ALWAYS DELIVERED

Sources: Company Reports, USGS, Roskill, Industrial Minerals

0

100

200

300

400

500

2012 Supply 2016 Supply

LCE

ktp

a

ALB Atacama ALB Silver Peak Chinese Brine & Mineral FMC Hombre Muerto

Greenbushes, WA Other Mineral SQM Atacama Olaroz

Salar del Rincón Quebec Lithium ALB La Negra 2 Mt Cattlin

Mt Marion

0

100

200

300

400

500

2012 Supply 2016 Supply

LCE

ktp

a

Planned in 2012 Delivered in 2016

Expansions from

existing operations

New supply

Announced new supply for delivery

by 2016

For

per

sona

l use

onl

y

13

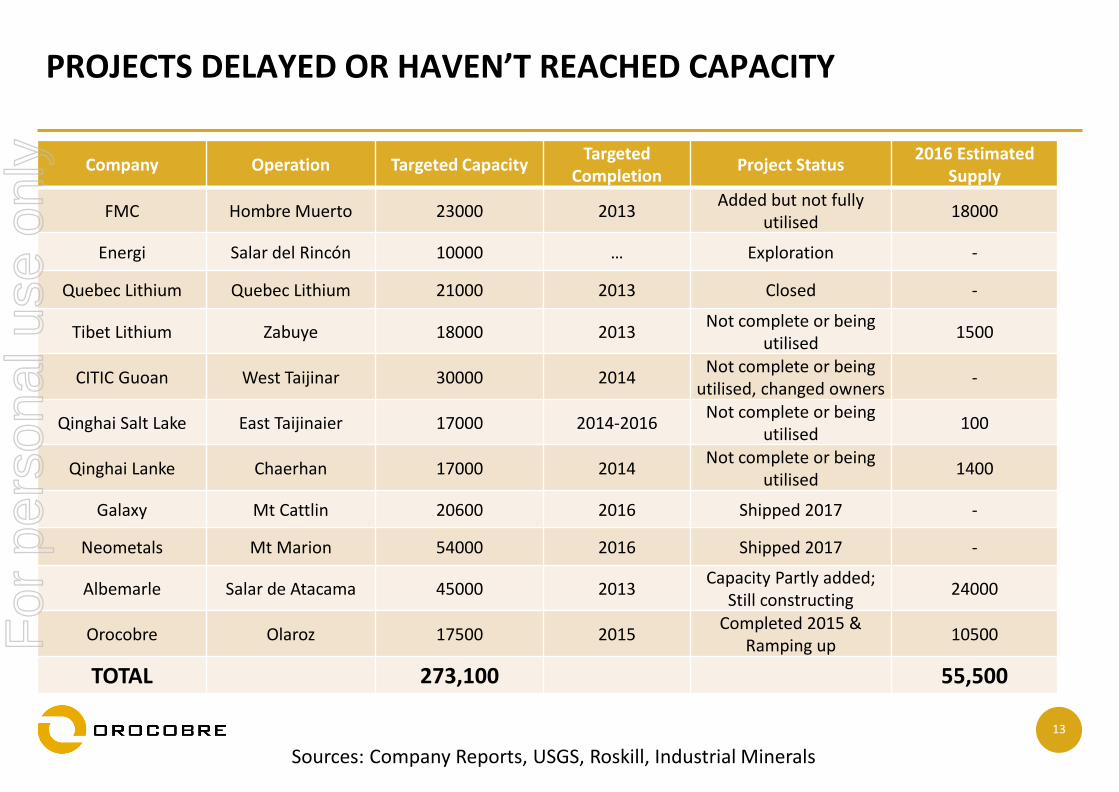

PROJECTS DELAYED OR HAVEN’T REACHED CAPACITY

Company Operation Targeted CapacityTargeted

CompletionProject Status

2016 Estimated Supply

FMC Hombre Muerto 23000 2013Added but not fully

utilised18000

Energi Salar del Rincón 10000 … Exploration -

Quebec Lithium Quebec Lithium 21000 2013 Closed -

Tibet Lithium Zabuye 18000 2013Not complete or being

utilised1500

CITIC Guoan West Taijinar 30000 2014Not complete or being

utilised, changed owners-

Qinghai Salt Lake East Taijinaier 17000 2014-2016Not complete or being

utilised100

Qinghai Lanke Chaerhan 17000 2014Not complete or being

utilised1400

Galaxy Mt Cattlin 20600 2016 Shipped 2017 -

Neometals Mt Marion 54000 2016 Shipped 2017 -

Albemarle Salar de Atacama 45000 2013Capacity Partly added;

Still constructing24000

Orocobre Olaroz 17500 2015Completed 2015 &

Ramping up10500

TOTAL 273,100 55,500

Sources: Company Reports, USGS, Roskill, Industrial Minerals

For

per

sona

l use

onl

y

14

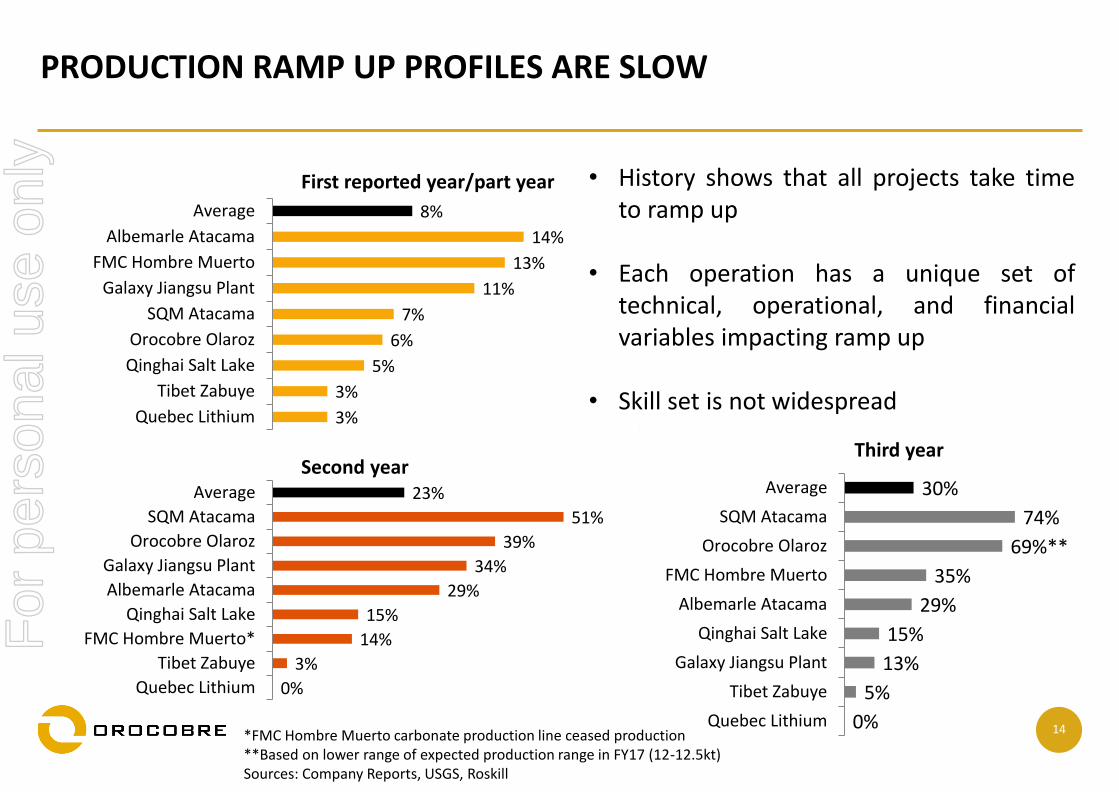

PRODUCTION RAMP UP PROFILES ARE SLOW

3%

3%

5%

6%

7%

11%

13%

14%

8%

Quebec Lithium

Tibet Zabuye

Qinghai Salt Lake

Orocobre Olaroz

SQM Atacama

Galaxy Jiangsu Plant

FMC Hombre Muerto

Albemarle Atacama

Average

*FMC Hombre Muerto carbonate production line ceased production**Based on lower range of expected production range in FY17 (12-12.5kt)Sources: Company Reports, USGS, Roskill

0%

5%

13%

15%

29%

35%

69%**

74%

30%

Quebec Lithium

Tibet Zabuye

Galaxy Jiangsu Plant

Qinghai Salt Lake

Albemarle Atacama

FMC Hombre Muerto

Orocobre Olaroz

SQM Atacama

Average

0%

3%

14%

15%

29%

34%

39%

51%

23%

Quebec Lithium

Tibet Zabuye

FMC Hombre Muerto*

Qinghai Salt Lake

Albemarle Atacama

Galaxy Jiangsu Plant

Orocobre Olaroz

SQM Atacama

Average

First reported year/part year

Second yearThird year

• History shows that all projects take timeto ramp up

• Each operation has a unique set oftechnical, operational, and financialvariables impacting ramp up

• Skill set is not widespread

For

per

sona

l use

onl

y

15

SUPPLY DEMAND BALANCE

For

per

sona

l use

onl

y

16

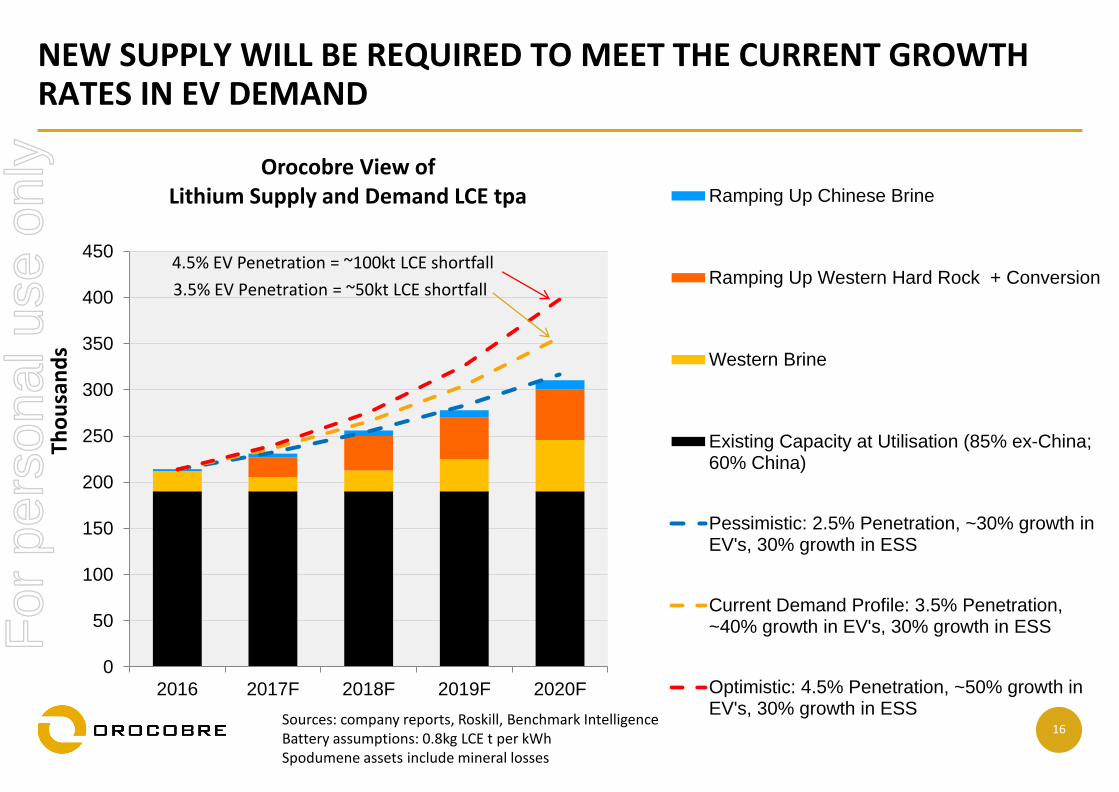

0

50

100

150

200

250

300

350

400

450

2016 2017F 2018F 2019F 2020F

Tho

usa

nd

s

Orocobre View of Lithium Supply and Demand LCE tpa Ramping Up Chinese Brine

Ramping Up Western Hard Rock + Conversion

Western Brine

Existing Capacity at Utilisation (85% ex-China;60% China)

Pessimistic: 2.5% Penetration, ~30% growth inEV's, 30% growth in ESS

Current Demand Profile: 3.5% Penetration,~40% growth in EV's, 30% growth in ESS

Optimistic: 4.5% Penetration, ~50% growth inEV's, 30% growth in ESS

3.5% EV Penetration = ~50kt LCE shortfall

NEW SUPPLY WILL BE REQUIRED TO MEET THE CURRENT GROWTH RATES IN EV DEMAND

Sources: company reports, Roskill, Benchmark Intelligence Battery assumptions: 0.8kg LCE t per kWhSpodumene assets include mineral losses

4.5% EV Penetration = ~100kt LCE shortfall

For

per

sona

l use

onl

y

17

PARTNERSHIPS & CONSOLIDATION

For

per

sona

l use

onl

y

18

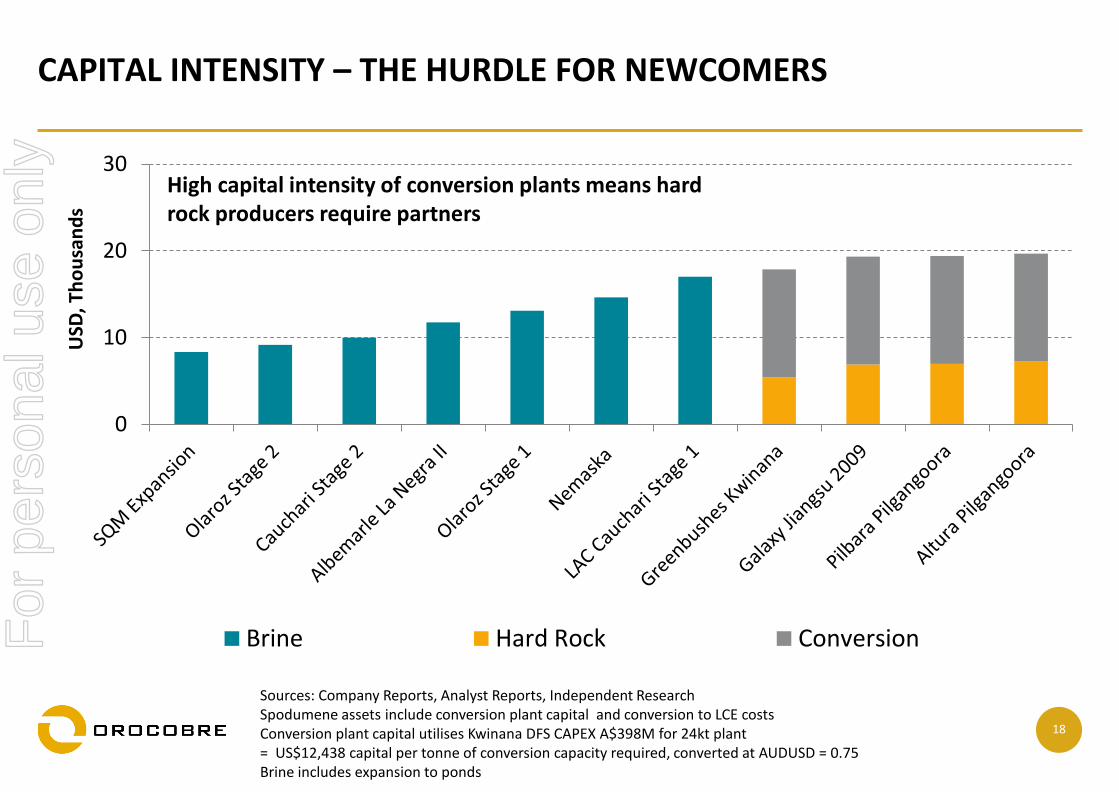

CAPITAL INTENSITY – THE HURDLE FOR NEWCOMERS

Sources: Company Reports, Analyst Reports, Independent ResearchSpodumene assets include conversion plant capital and conversion to LCE costsConversion plant capital utilises Kwinana DFS CAPEX A$398M for 24kt plant = US$12,438 capital per tonne of conversion capacity required, converted at AUDUSD = 0.75Brine includes expansion to ponds

0

10

20

30

USD

, Th

ou

san

ds

Brine Hard Rock Conversion

High capital intensity of conversion plants means hard rock producers require partners

For

per

sona

l use

onl

y

19

FUNDING CAPITAL-HUNGRY LITHIUM PROJECTS IS CHALLENGING

- Lithium is not an LME traded commodity

- Customers require qualified product

- Operations are bespoke

- Technology is held by incumbents

- Greenfield developments are inherently high risk

- Below expectation ramp-up performance experienced in brine operations, hard rock mines and conversion plants increases funding risk for debt and equity

- Technical skills required for integrated concentrate and conversion projects are beyond those normally found in either resource or conversion companies

- Brine does not naturally fit either in chemicals sector or mining experiences

Junior companies need partners or politically supported financing

For

per

sona

l use

onl

y

20

FUNDING PARTNERSHIP DEALS ARE BEING ESTABLISHED BUT SLOWLY

Well established partnerships :• Orocobre and TTC• Neometals with Mineral Resources and

Ganfeng• LAC with SQM

New partnerships developing:• LAC with Ganfeng and Bangchak• Pilbara and Ganfeng• Pilbara and General Lithium

But not all partnerships survive:• LAC with Mitsubishi and Magma Corp• Galaxy with KORES

Partnerships are part of the new norm for non-established producers

For

per

sona

l use

onl

y

21

EXPANSION ASPIRATIONS

For

per

sona

l use

onl

y

22

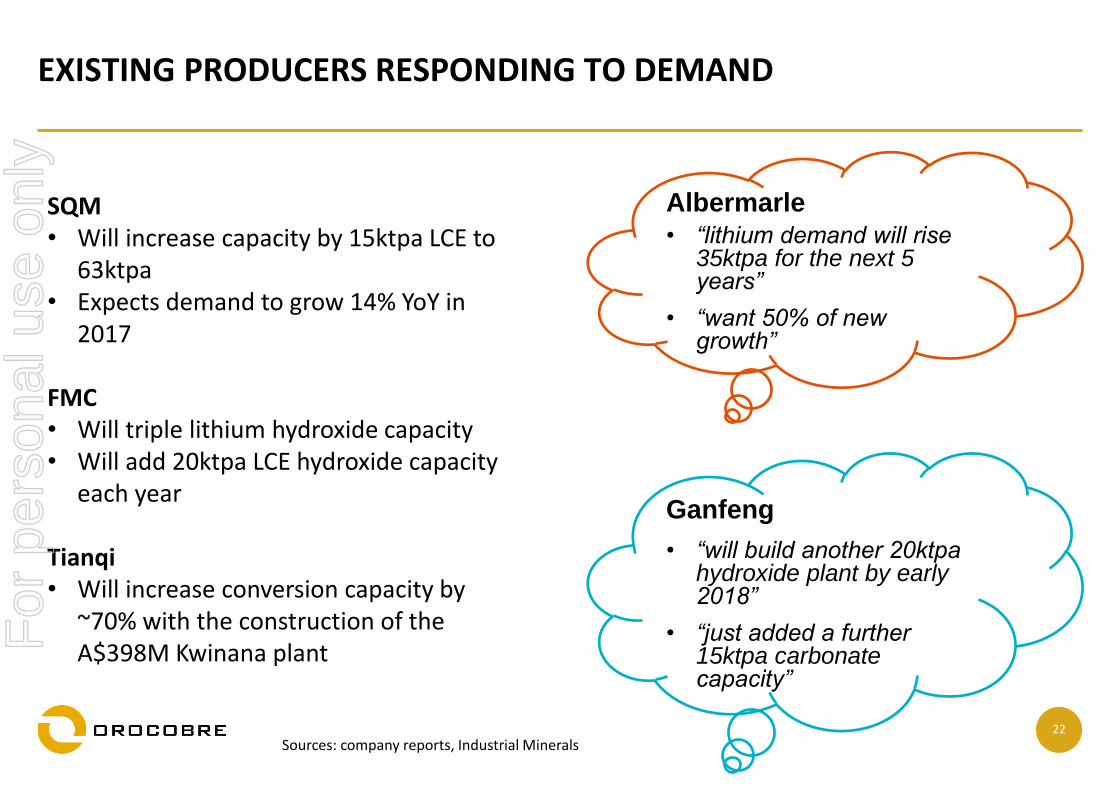

EXISTING PRODUCERS RESPONDING TO DEMAND

SQM• Will increase capacity by 15ktpa LCE to

63ktpa• Expects demand to grow 14% YoY in

2017

FMC• Will triple lithium hydroxide capacity • Will add 20ktpa LCE hydroxide capacity

each year

Tianqi• Will increase conversion capacity by

~70% with the construction of the A$398M Kwinana plant

Sources: company reports, Industrial Minerals

Albermarle

• “lithium demand will rise 35ktpa for the next 5 years”

• “want 50% of new growth”

Ganfeng

• “will build another 20ktpa hydroxide plant by early 2018”

• “just added a further 15ktpa carbonate capacity”

For

per

sona

l use

onl

y

23

INCUMBENTS HAVE SIGNIFICANT ADVANTAGES

• Lower capital intensity

• Existing operations with knowledge of production processes and understanding of technology

• Production scale to protect unit costs

• Existing infrastructure, workforce and supply chains

• A relationship with regulators and familiarity with local laws

• Established markets

• Lower capital intensity

• Shorter time to delivery

• Access to finance

For

per

sona

l use

onl

y

24

CONCLUSIONS

For

per

sona

l use

onl

y

25

SUMMARY

• Strong growth in demand but uncertainty on how strong

• New developments are needed to meet >2.5% EV penetration in 2020

• There are projects in the pipeline but supply response will be slower than

desired

• Financing projects is challenging and juniors need partners

• Established producers rising to the challenge but response will take time

• Market conditions to stay tight, if not undersupplied, to 2020

For

per

sona

l use

onl

y

26

KEY CONCERNS FOR THE LITHIUM INDUSTRY TO THE END OF THE DECADELITHIUM SUPPLY & MARKETS CONFERENCE MONTREAL, CANADA

31 MAY 2017

For

per

sona

l use

onl

y