Key Concept Excerise Week 8

6

_ October 1, 2015 KEY CONCEPT EXCERISE WEEK 8 Introduction BSC is a management system and has “emerged as a decision support tool at the strategic management level” (Martinsons, Davison and Tse, 1999). Nowadays, manages evaluate their organization performance through “linking the operational and non-financial corporate activities with causal chains to the firm’s long-term strategy” (Figge et al., 2002) . The BSC is “a tool which provides both hard and soft performance measures for both non-profit and business organizations” (Ahmad and Hasnu, 2013) Implementation of BSC A BSC starts with identifying strategies derived from organization’s vision and mission. Then, these themes are developed by evaluating the vision and mission statement from four dimensions which is shown in the below diagram as below;

-

Upload

aizer-mogahed -

Category

Documents

-

view

213 -

download

1

description

assignement

Transcript of Key Concept Excerise Week 8

_October 1, 2015

KEY CONCEPT EXCERISE WEEK 8

Introduction

BSC is a management system and has “emerged as a decision support tool at the

strategic management level” (Martinsons, Davison and Tse, 1999). Nowadays,

manages evaluate their organization performance through “linking the

operational and non-financial corporate activities with causal chains

to the firm’s long-term strategy” (Figge et al., 2002)

. The BSC is “a tool which provides both hard and soft performance

measures for both non-profit and business organizations” (Ahmad and

Hasnu, 2013)

Implementation of BSC

A BSC starts with identifying strategies derived from organization’s

vision and mission. Then, these themes are developed by evaluating

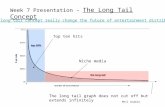

the vision and mission statement from four dimensions which is shown

in the below diagram as below;

_October 1, 2015

Adopted from Robert S. Kaplan and David P. Norton, “Using the balanced scorecard

as strategic management” Harvard Business Review (Kaplan and Norton, 1996)

From the above diagram, four perspectives are highlighted as below;

Financial ; supports the strategy of business explanations,

profitability and the risk for the owner of shareholders and

owners. This perspective can be measured by considering

measures; operating profit, revenue growth and revenues from

the new or modified products etc. (Martinsons, Davison and

Tse, 1999).

Customers ; it trace customers satisfaction on the company

performance through what it delivers to them. This can be

measured through the market shares, customer retention

percentage and time taken to meet customer’s request.

Internal business process ; it derives the operation or process

needed to meet customer satisfaction on delivering products or

servicing

Learning and growth ; concerns on how organization train its

employees, gain knowledge and maintain its competitive

advantage taking in consideration the dynamicity of the market

environment (Ronchetti, 2006).

Accordingly, each perspective should be considered in regards to the

following factors.

In regards to define and evaluate the four perspectives, following

factors are considered

Objectives; it represents an organization objectives such as

market growth and profitability

_October 1, 2015

Measures; in regards to the objectives, measures will be chosen

to asses an organization’s progress to achieve its objectives

Targets; this can be defined as the targets have been placed in

order to achieve measures.

Initiative; Actions that should be taken to achieve the objectives

Advantages of BSC

The implementation of BSC has increased due its rational process and

clarity . Therefore it has become a management strategy, which can

be used across various sectors within an organization.

The BSC approach is a performance measure, which combines the financial and

nonfinancial measures to provide the managers with a comprehensive report about

the activities that they are managing. Accordingly BSC approach adds a value to an

organization due to the followings;

1. It combines the financial and non-financial measures.

2. Concentrates on the process not metrics like most companies hold most of

their capital in intangible assets as training and motivating the employees

3. It translates an organization’s vision and mission in to measurable goals

through which it can measure the performance against these goals

4. It helps in raising the consciousness, and knowledge about the operation

process in which it can help to tackle the bottleneck process and improve it.

In conclusion, I do encourage for the implementation of BSC across different

organization due to its effectiveness in providing the full picture of the current

status of an organization and taking actions on the lag activities where improvement

_October 1, 2015

should be done. Therefore, implementing BSC in my organization will assist the

management to mainly concentrate on the four perspectives and narrow its strategy

in order to be adjusted to BSC perspectives. Accordingly, the implementation of BSC

will be effective based on how successful an organization can relate its strategy to

BSC perspective. The ability of BSC to combine an organization financial and non-

financial factors enable an organization to achieve competitive advantage and to be

adapted to the dynamicity of today’s business environment

Bibliography

Ahmad, S. T. and Hasnu, S. A. F. (2013) 'Balanced Scorecard Implementation: Case

Study of COMSATS Abbottabad, Pakistan', google. Available from:

http://www.sciencepub.net/researcher Department of Management Sciences,

COMSATS Institute of Information Technology, Abbottabad, Pakistan.: (Accessed: 4

october 2015). pp.88-91.

Figge, F., Hahn, T., Schaltegger, S. and Wagner, M. (2002) 'The sustainability

balanced scorecard–linking sustainability management to business strategy',

Business strategy and the Environment, 11 (5), (Accessed: 4 October 2015). pp.269-

84.

Kaplan, R. S. and Norton, D. P. (1996) 'Using the Balanced Scorecard as a Strategic

Management System', Harv.Bus.Rev., 74 (1), (Accessed: 4 October 2015). pp.75-85.

_October 1, 2015

Martinsons, M., Davison, R. and Tse, D. (1999) 'The balanced scorecard: a foundation

for the strategic management of information systems', Decis.Support Syst., 25 (1),

(Accessed: 4 October 2015). pp.71-88.

Ronchetti, J. L. (2006) 'An integrated Balanced Scorecard strategic planning model

for nonprofit organizations', Journal of practical consulting, 1 (1), scholar google

[Online]. (Accessed: 4 October 2015). pp.25-35.