Key Areas for Clerks’ Offices to Focus When it Comes …c.ymcdn.com/sites/ Areas for Clerks’...

80

Key Areas for Clerks’ Offices to Focus When it Comes to Fraud Hector Collazo Jr. Inspector General/Chief Audit Executive 727-464-8371 [email protected]

-

Upload

phungtuong -

Category

Documents

-

view

218 -

download

1

Transcript of Key Areas for Clerks’ Offices to Focus When it Comes …c.ymcdn.com/sites/ Areas for Clerks’...

Key Areas for Clerks’ Offices

to Focus When it Comes to Fraud Hector Collazo Jr.

Inspector General/Chief Audit Executive 727-464-8371

Questions

2

3

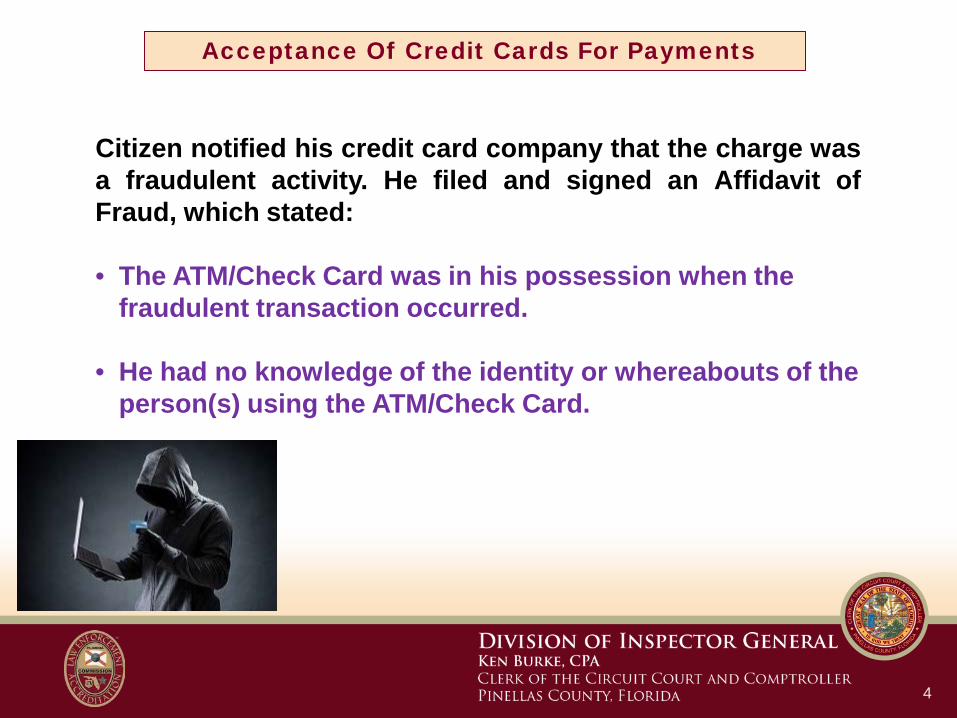

Acceptance Of Credit Cards For Payments

4

Acceptance Of Credit Cards For Payments

Citizen notified his credit card company that the charge was a fraudulent activity. He filed and signed an Affidavit of Fraud, which stated: • The ATM/Check Card was in his possession when the

fraudulent transaction occurred. • He had no knowledge of the identity or whereabouts of the

person(s) using the ATM/Check Card.

5

Acceptance Of Credit Cards For Payments

Department received a Chargeback Sales Request notice from the credit card company because there was a “Fraudulent Transaction – Card Absent Environment” based on the Citizen’s signed and submitted Fraud Statement. The notice stated that the department had 14 days to reply and provide the requested information, or a debit could result to their account.

6

Acceptance Of Credit Cards For Payments

•Pinellas Records Justice Information – Charge, Disposition, Sentence Record

•Pick Up and Receipt from original transaction •Citizen's pet License and Microchip Information •Receipt Print Page from original transaction •Administrative Support Specialist’s Statement •Senior Animal Care Assistant’s Statement •Office Specialist’s Statement •Animal Services Walk-Through Form •Dispute of Chargeback, Department’s responses to Bank •Enforcement Officer’s dispatch information •Statement from Citizen’s former property manager •Sheriff’s Office e-mail providing signature samples •Sheriff’s Inmate Release Form

7

Acceptance Of Credit Cards For Payments

The credit card company authorized the chargeback solely based on the Respondent’s signed Fraud Statement (affidavit) that he did not authorize this transaction.

8

Acceptance Of Credit Cards For Payments

What can Internal Audit or the Inspector General do?

9

Acceptance Of Credit Cards For Payments

10

Acceptance Of Credit Cards For Payments

Solid Waste

11

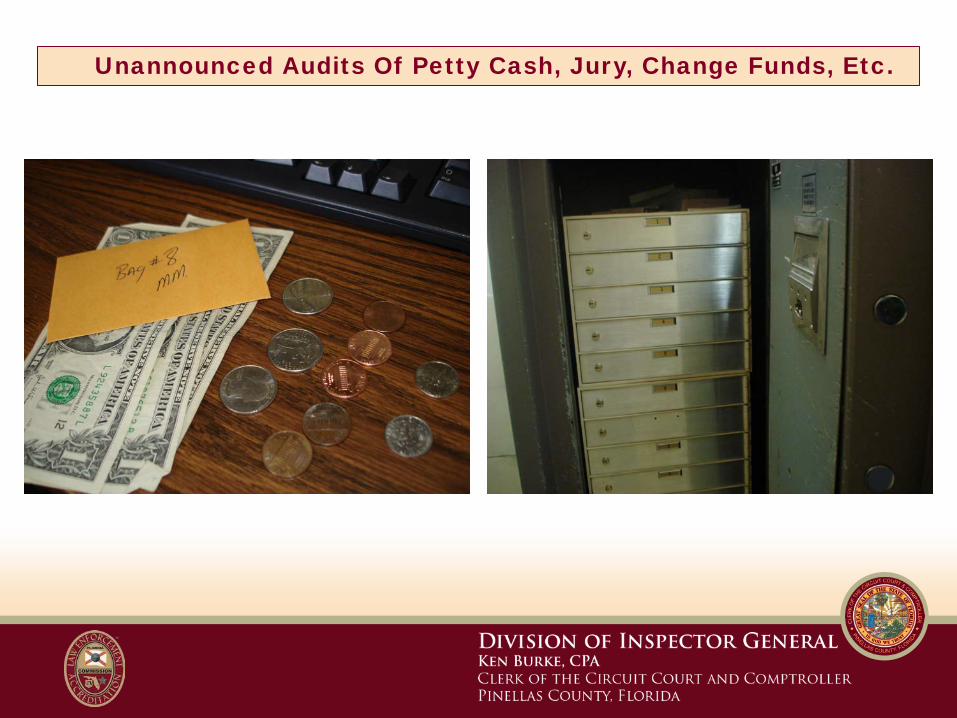

Unannounced Audits Of Petty Cash, Jury, Change

Funds, Etc.

I know what you’re thinking!

What a Waste of Time of Staff Resources!

12

Unannounced Audits Of Petty Cash, Jury, Change Funds, Etc.

Is it a waste of time? What happens when

you are surrounded by tons of cash and have eight hours a day to

figure a way to borrow it?

13

Unannounced Audits Of Petty Cash, Jury, Change Funds, Etc.

14

Unannounced Audits Of Petty Cash, Jury, Change Funds, Etc.

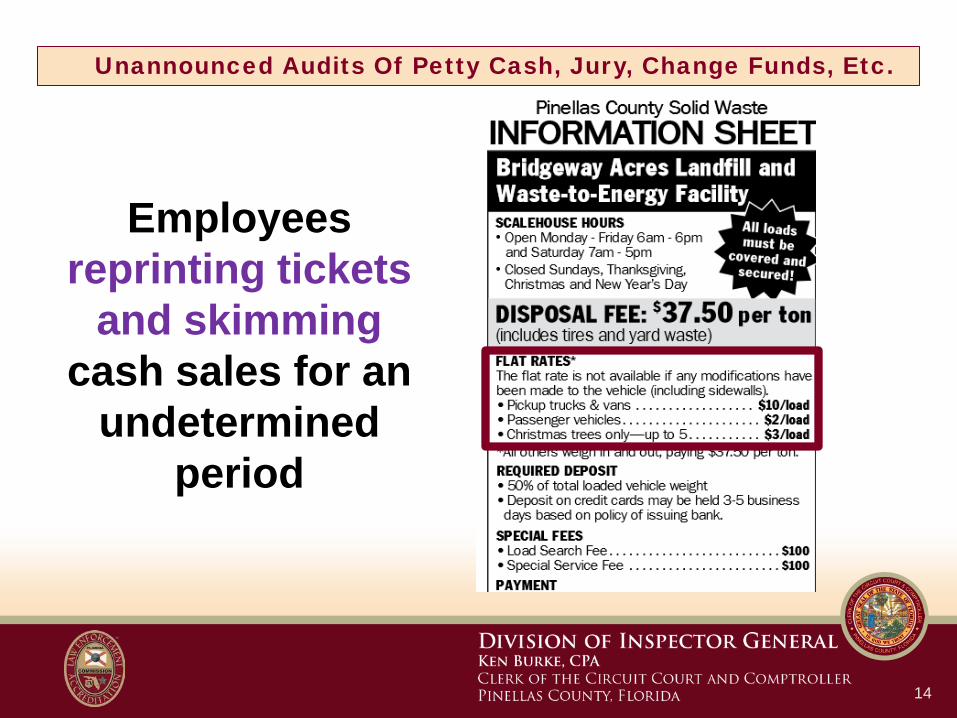

Employees reprinting tickets

and skimming cash sales for an

undetermined period

15

Unannounced Audits Of Petty Cash, Jury, Change Funds, Etc.

Unannounced Audits Of Petty Cash, Jury, Change Funds, Etc.

17

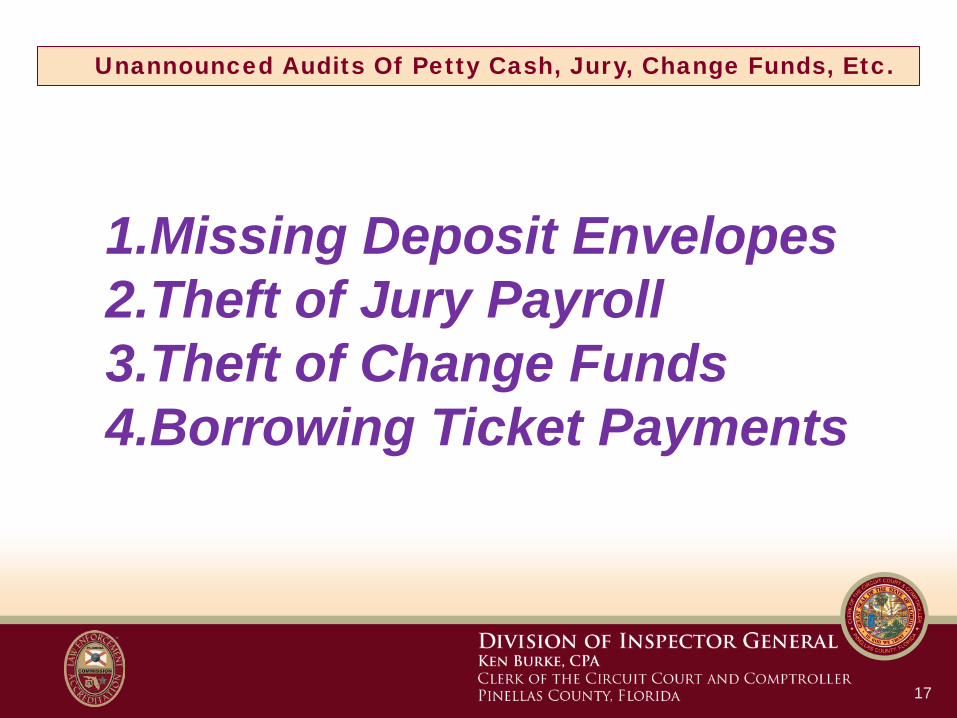

Unannounced Audits Of Petty Cash, Jury, Change Funds, Etc.

1.Missing Deposit Envelopes 2.Theft of Jury Payroll 3.Theft of Change Funds 4.Borrowing Ticket Payments

18

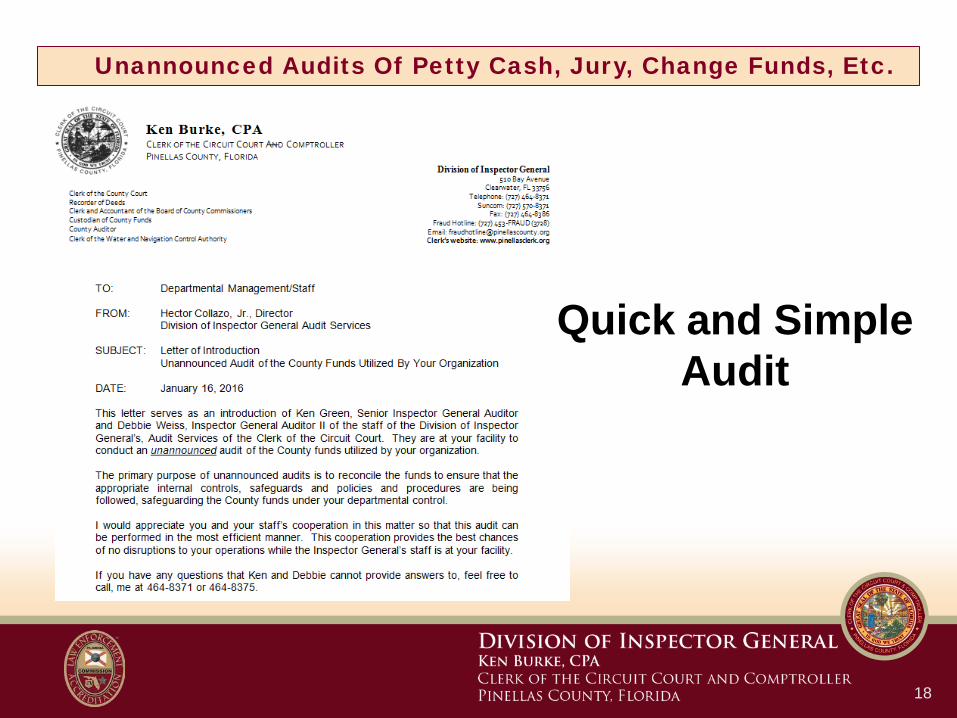

Unannounced Audits Of Petty Cash, Jury, Change Funds, Etc.

Quick and Simple Audit

19

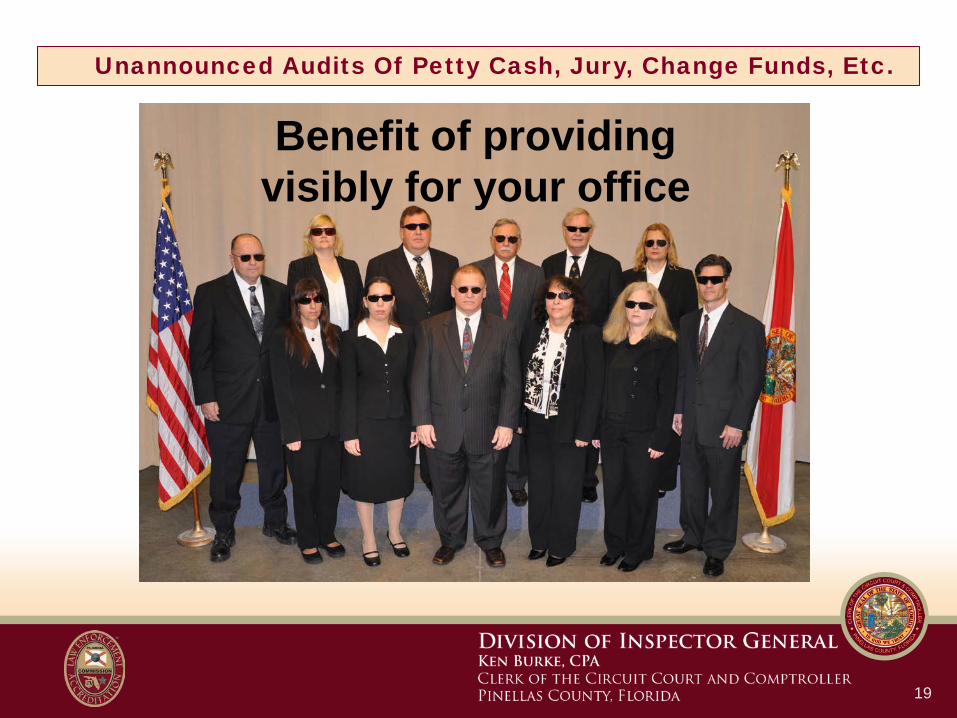

Unannounced Audits Of Petty Cash, Jury, Change Funds, Etc.

Benefit of providing visibly for your office

20

County’s Purchasing Card (P-Card)

Typical concerns: Claims that County’s Purchasing Card (P-Card) holders use the P-Cards to buy personal items or items for non-County related use.

21

County’s Purchasing Card (P-Card)

What can Internal Audit or the Inspector General do?

22

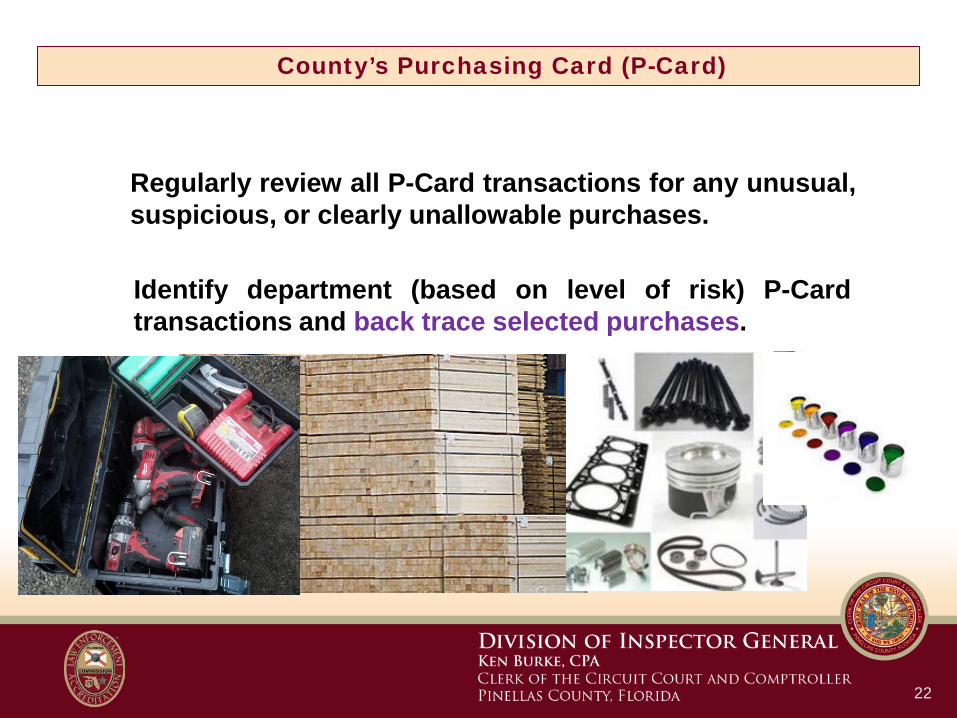

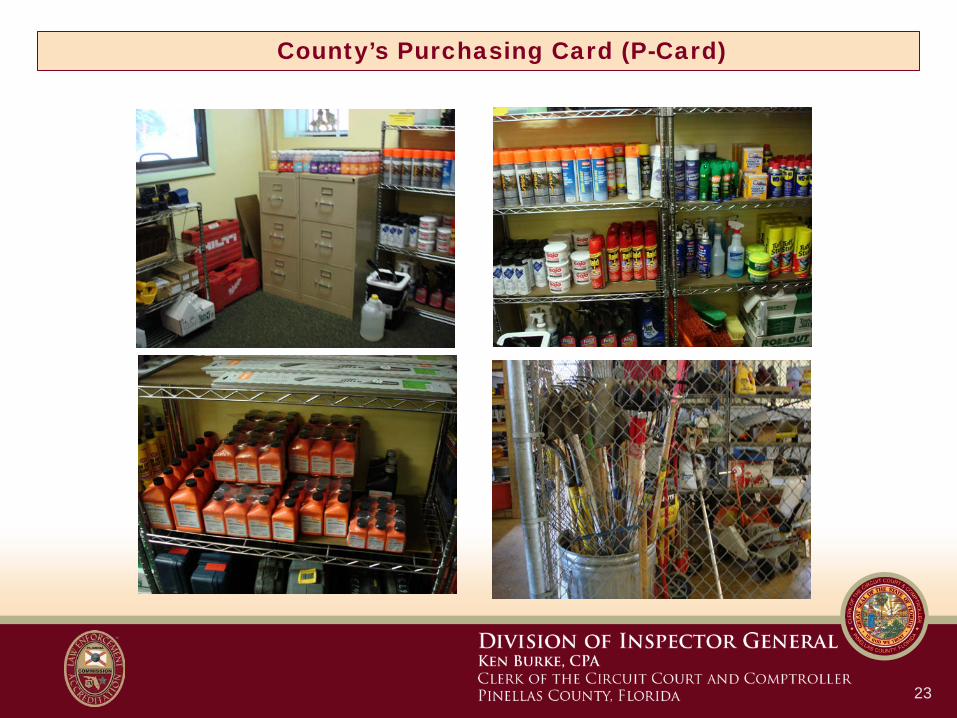

County’s Purchasing Card (P-Card)

Regularly review all P-Card transactions for any unusual, suspicious, or clearly unallowable purchases.

Identify department (based on level of risk) P-Card transactions and back trace selected purchases.

23

County’s Purchasing Card (P-Card)

24

County’s Purchasing Card (P-Card)

Annually - Departments Should Review

• Per transaction limits (i.e., up to $1,000) unless the P-Card holder often purchases big ticket items or services.

• P-Card monthly limits adequate with the purchasing needs of the P-Card holder.

• Ensure accounts are closed when an employee is terminated.

25

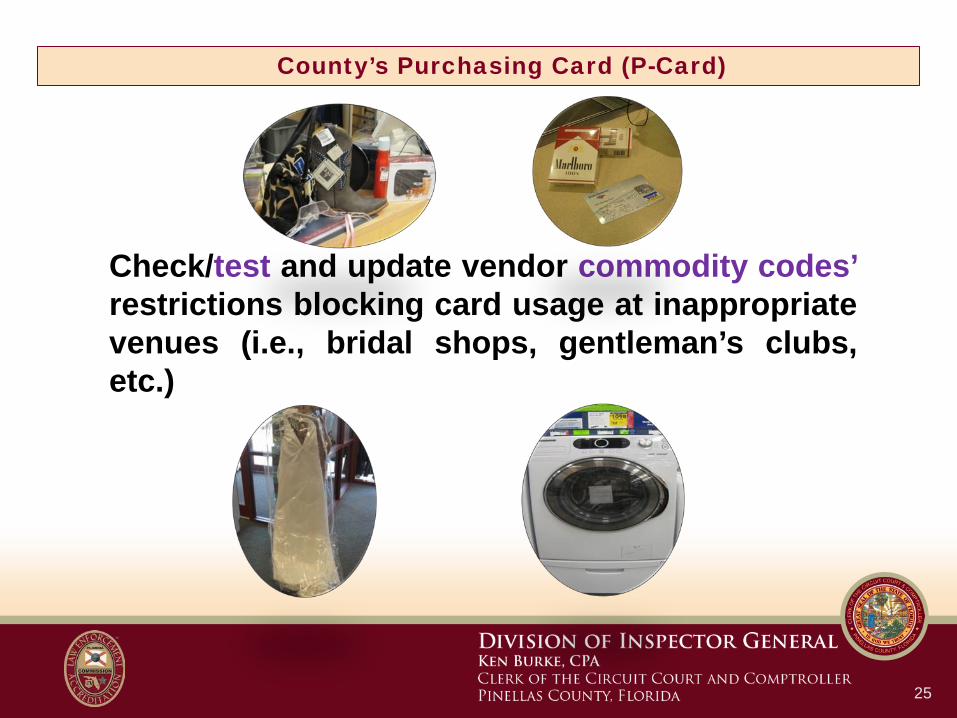

County’s Purchasing Card (P-Card)

Check/test and update vendor commodity codes’ restrictions blocking card usage at inappropriate venues (i.e., bridal shops, gentleman’s clubs, etc.)

26

Audits of Selected County Service &

Maintenance Contracts

27

Audits Of Selected County Service & Maintenance Contracts

Millions of dollars of project work are being awarded annually to engineering consulting firms under continuing contracts’ pools with Public Works.

Management stated they do not document and retain reasons for why a particular engineering firm was selected over others from the pool for a project.

28

Audits Of Selected County Service & Maintenance Contracts

Update and improve the clarity of the written Consultant Selection procedures for the process to include detailed steps and forms for Public Works Engineering management to document and retain with two levels of management approvals for each selection decision for a consultant from the pool for a project.

Consultant Selection

29

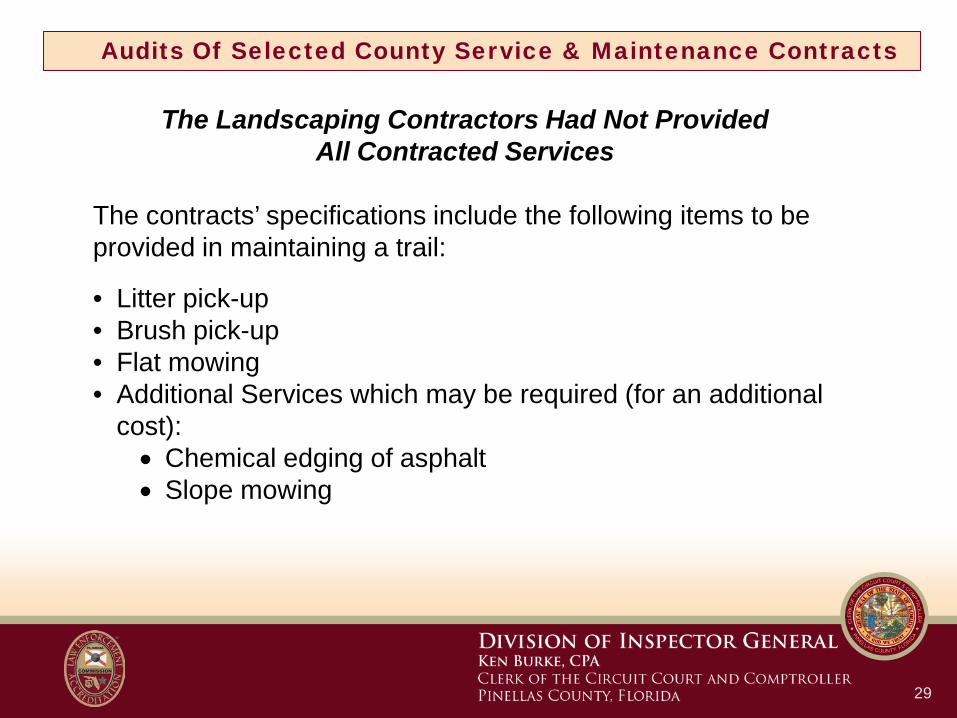

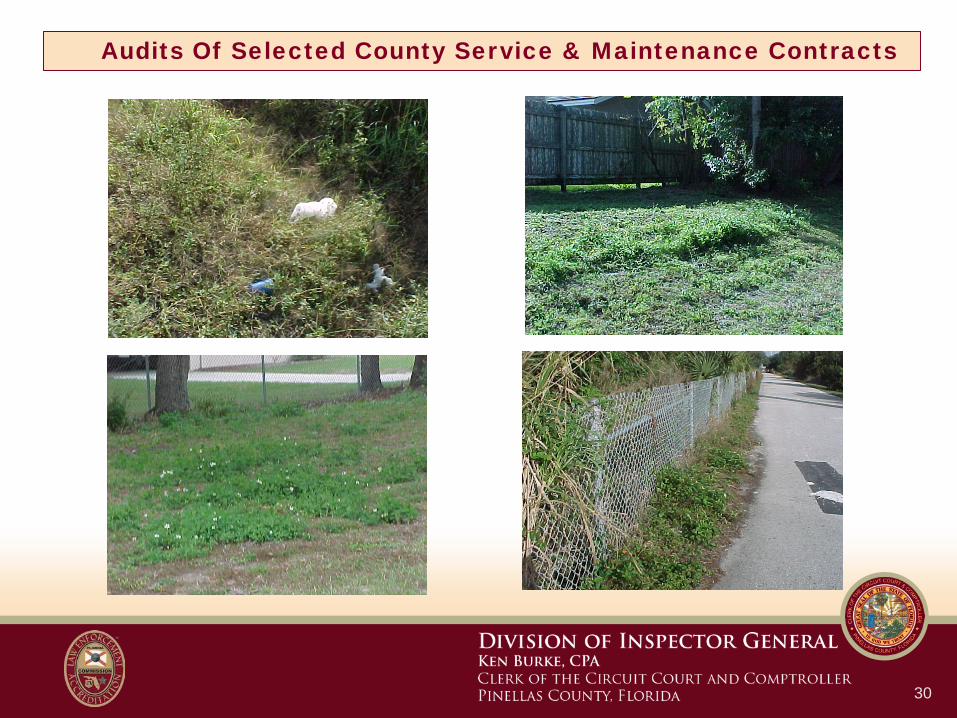

Audits Of Selected County Service & Maintenance Contracts

The Landscaping Contractors Had Not Provided All Contracted Services

The contracts’ specifications include the following items to be provided in maintaining a trail:

• Litter pick-up • Brush pick-up • Flat mowing • Additional Services which may be required (for an additional

cost): • Chemical edging of asphalt • Slope mowing

30

Audits Of Selected County Service & Maintenance Contracts

31

Audits Of Selected County Service & Maintenance Contracts

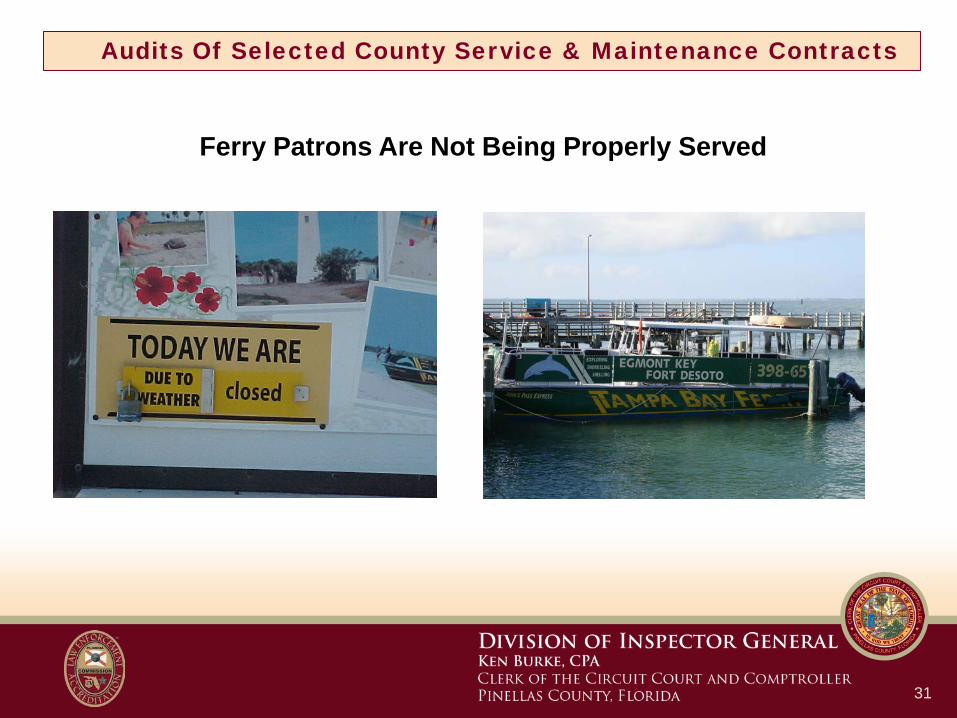

Ferry Patrons Are Not Being Properly Served

32

Audits Of Selected County Service & Maintenance Contracts

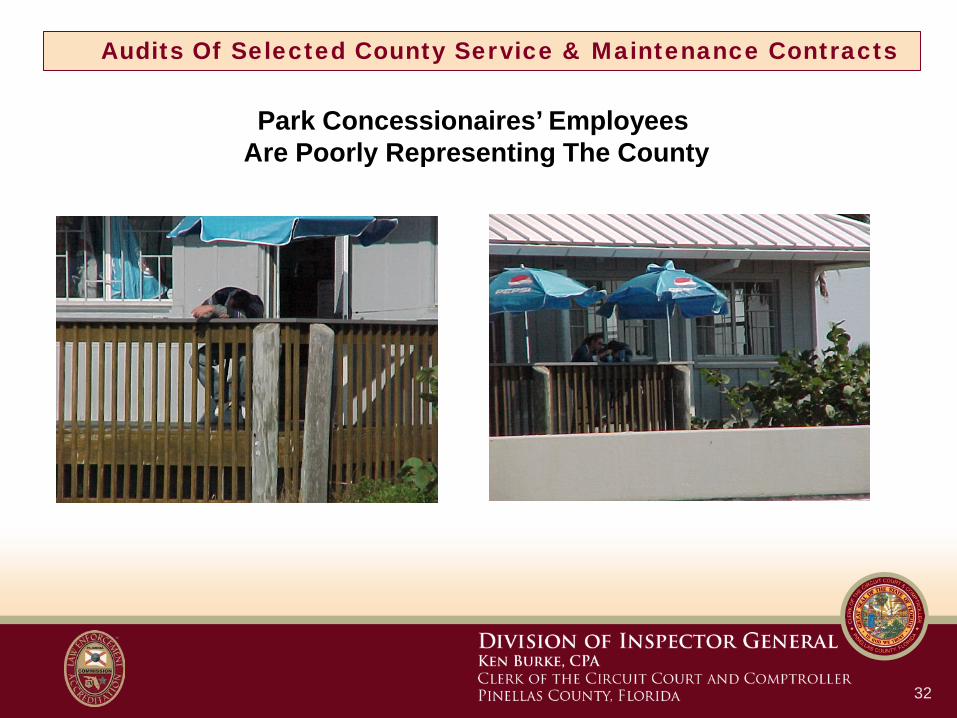

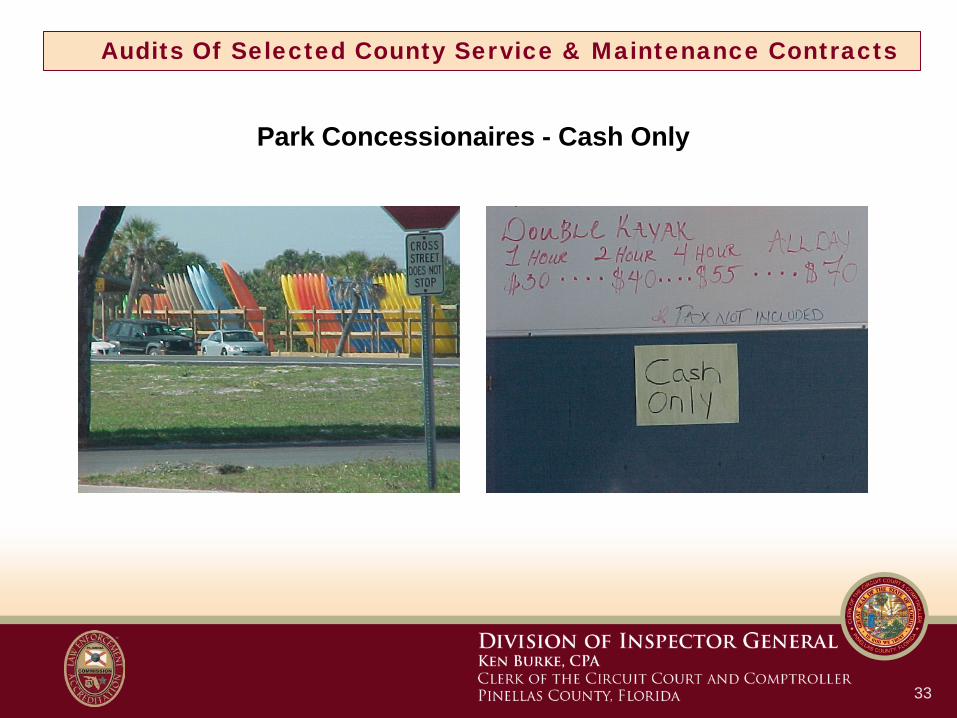

Park Concessionaires’ Employees Are Poorly Representing The County

33

Audits Of Selected County Service & Maintenance Contracts

Park Concessionaires - Cash Only

34

Audits Of Selected County Service & Maintenance Contracts

Educational Activities At The Ranch Are A Major Cost, Create Risks, And Do Not Directly Benefit Pinellas County Citizens.

35

Audits Of Selected County Service & Maintenance Contracts

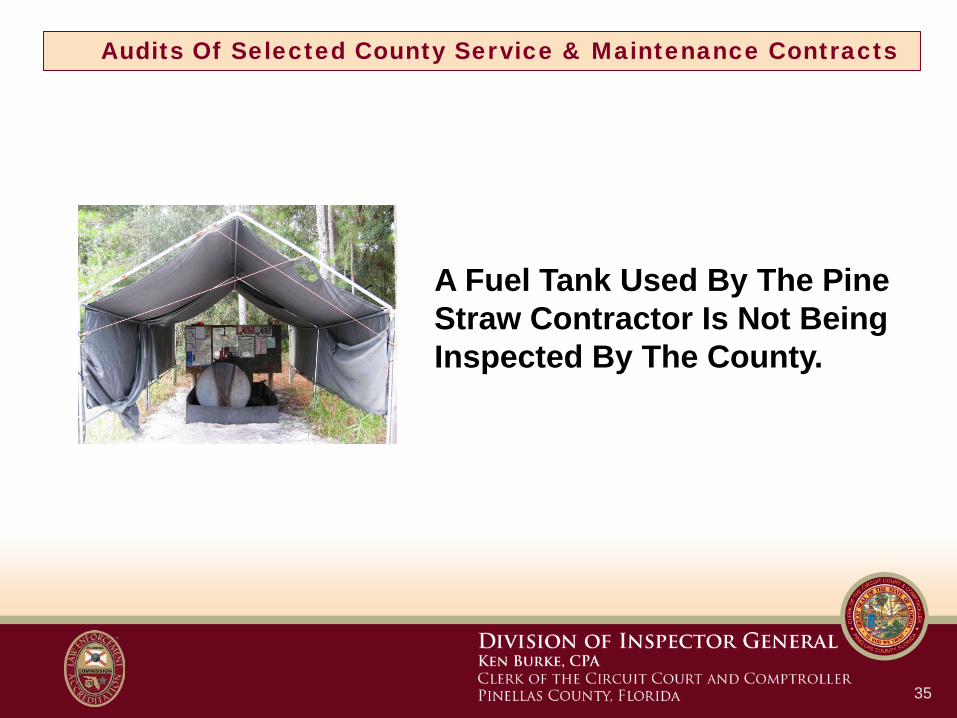

A Fuel Tank Used By The Pine Straw Contractor Is Not Being Inspected By The County.

36

Audits Of Selected County Service & Maintenance Contracts

Biggest Concern is the Lack of

Contract Compliance Administrators

37

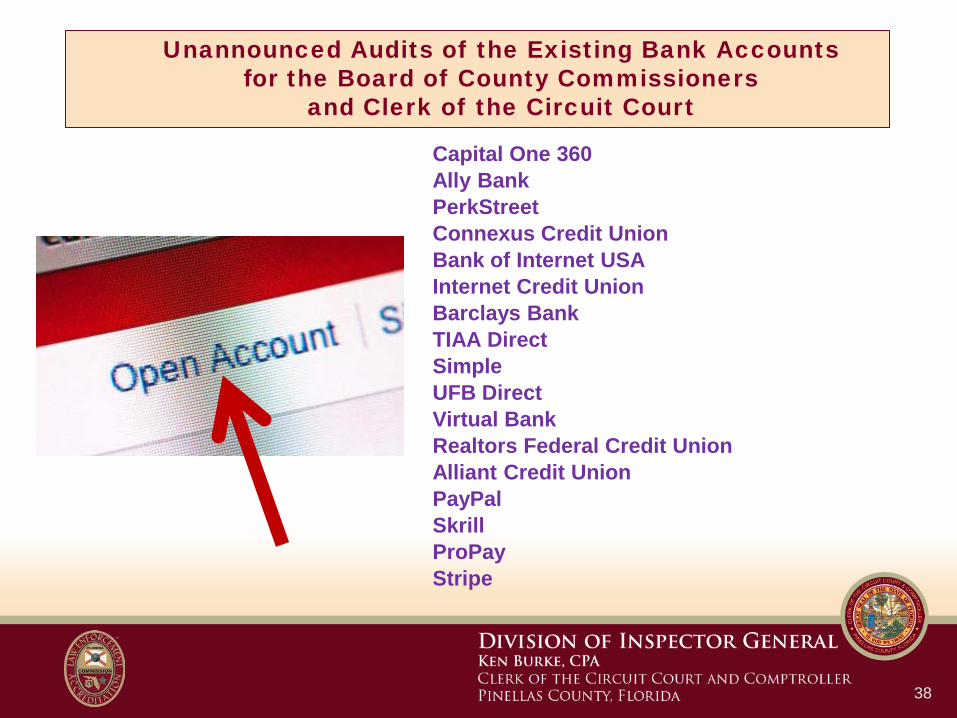

Unannounced Audits of the Existing Bank Accounts

for the Board of County Commissioners

and Clerk of the Circuit Court

38

Unannounced Audits of the Existing Bank Accounts for the Board of County Commissioners

and Clerk of the Circuit Court

Capital One 360 Ally Bank PerkStreet Connexus Credit Union Bank of Internet USA Internet Credit Union Barclays Bank TIAA Direct Simple UFB Direct Virtual Bank Realtors Federal Credit Union Alliant Credit Union PayPal Skrill ProPay Stripe

39

Unannounced Audits of the Existing Bank Accounts for the Board of County Commissioners

and Clerk of the Circuit Court

Virtual banks and payment services from an audit perspective are businesses that offer services for accepting and holding funds. For example, PayPal allows persons and businesses to establish accounts that accept online, mobile, and credit card payments. PayPal then holds the payments in an account for you. These funds on account can be transferred and withdrawn through the banking system. This is an acceptable business practice for the private sector, but is not allowed for government collections. The virtual banks and payment service entities increase the County’s exposure for unauthorized accounts and identity theft. There is also a risk that employees that are not familiar with the legal requirements for qualified public depositories may also establish such accounts.

40

Observations of Annual Physical

Inventory of Fixed Assets

41

Observations of Annual Physical Inventory of Fixed Assets

42

Observations of Annual Physical Inventory of Fixed Assets

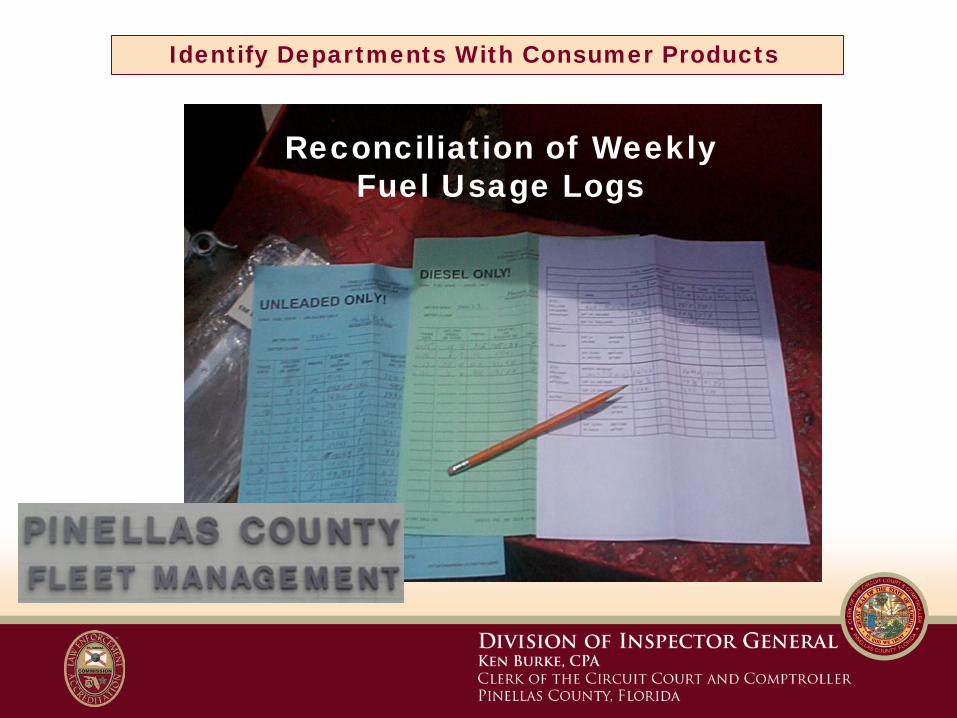

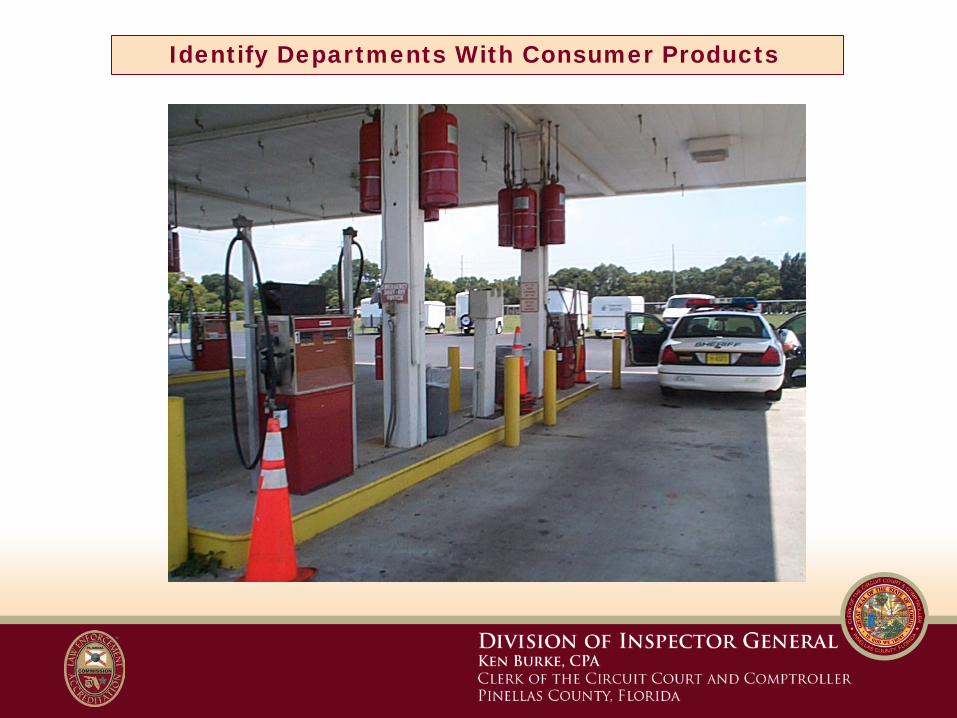

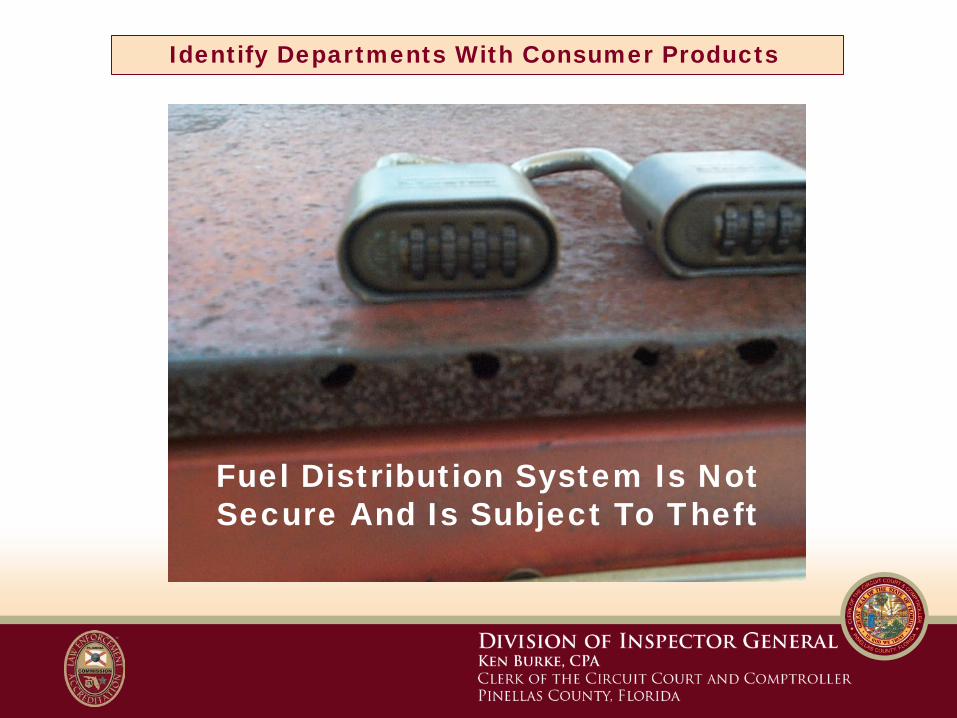

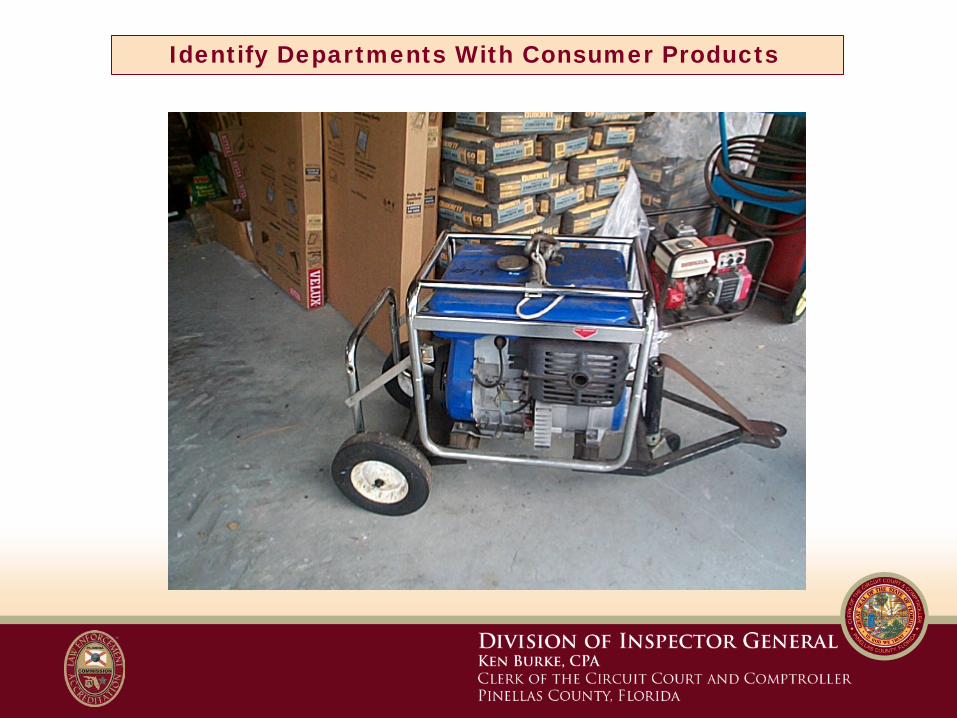

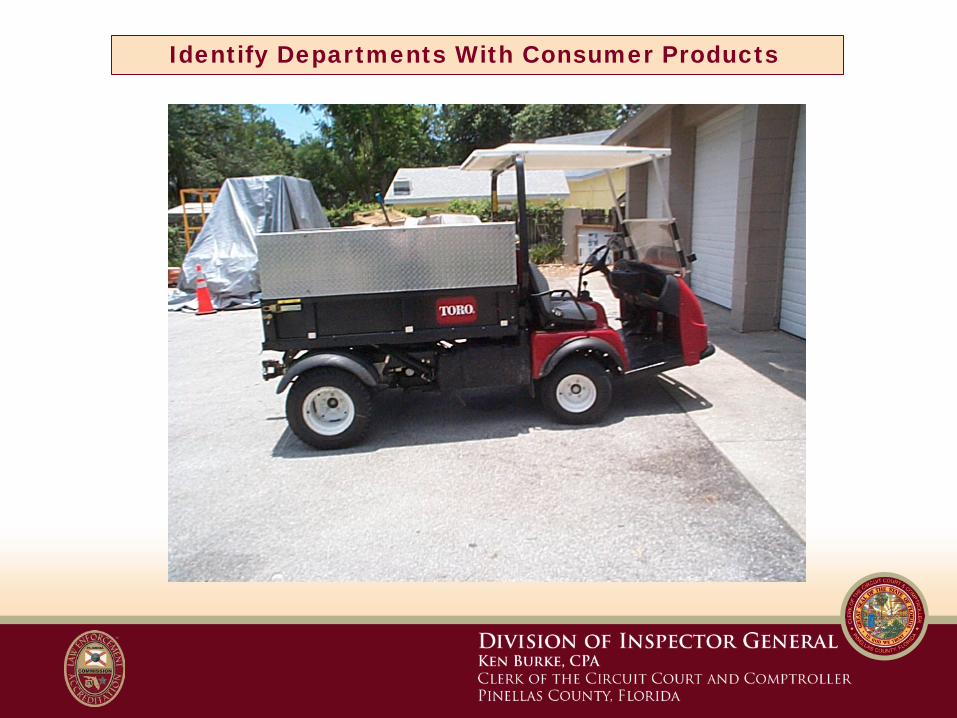

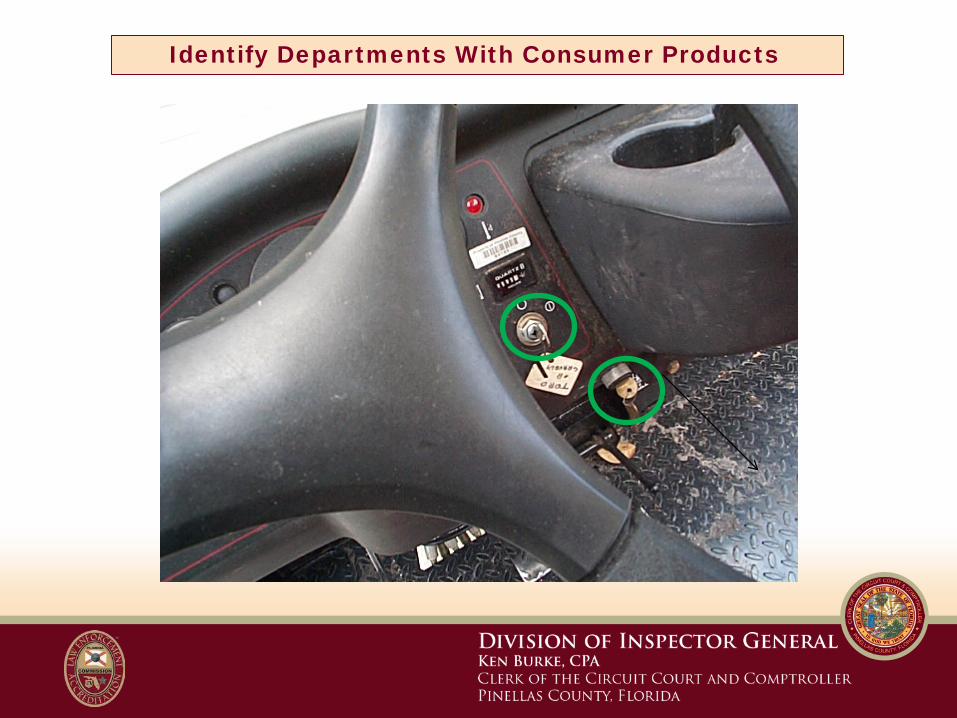

Identify Departments With Consumer

Products

44

The importance of observational skills!

Reconciliation of Weekly Fuel Usage Logs

Identify Departments With Consumer Products

Identify Departments With Consumer Products

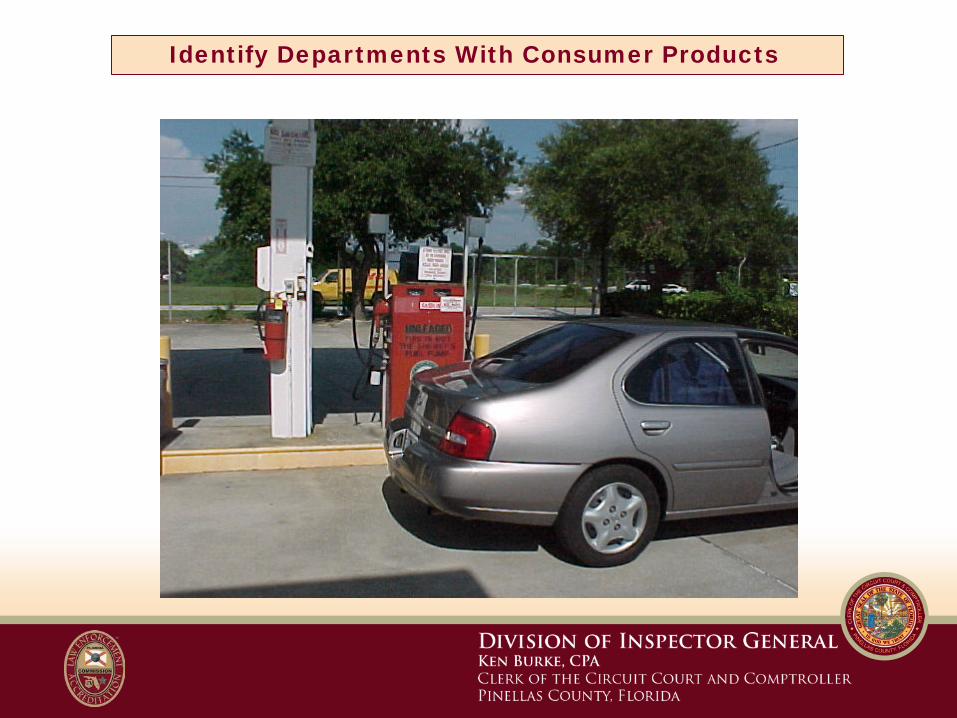

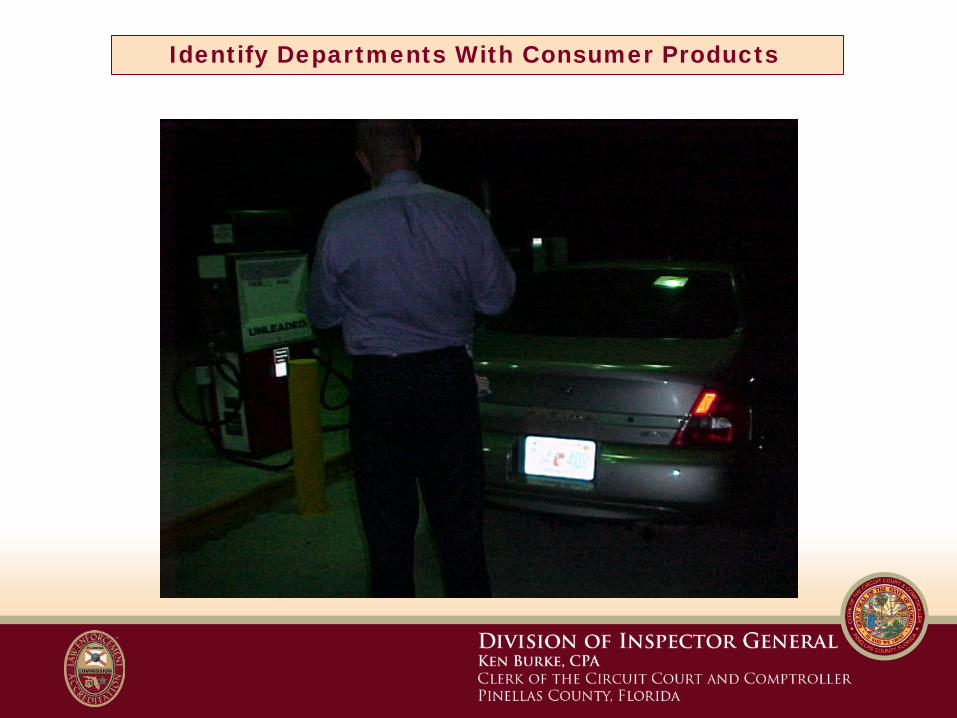

Fuel Distribution System Is Not Secure And Is Subject To Theft

Identify Departments With Consumer Products

Identify Departments With Consumer Products

Identify Departments With Consumer Products

50

Identify Departments With Consumer Products

51

Identify Departments With Consumer Products

Identify Departments With Consumer Products

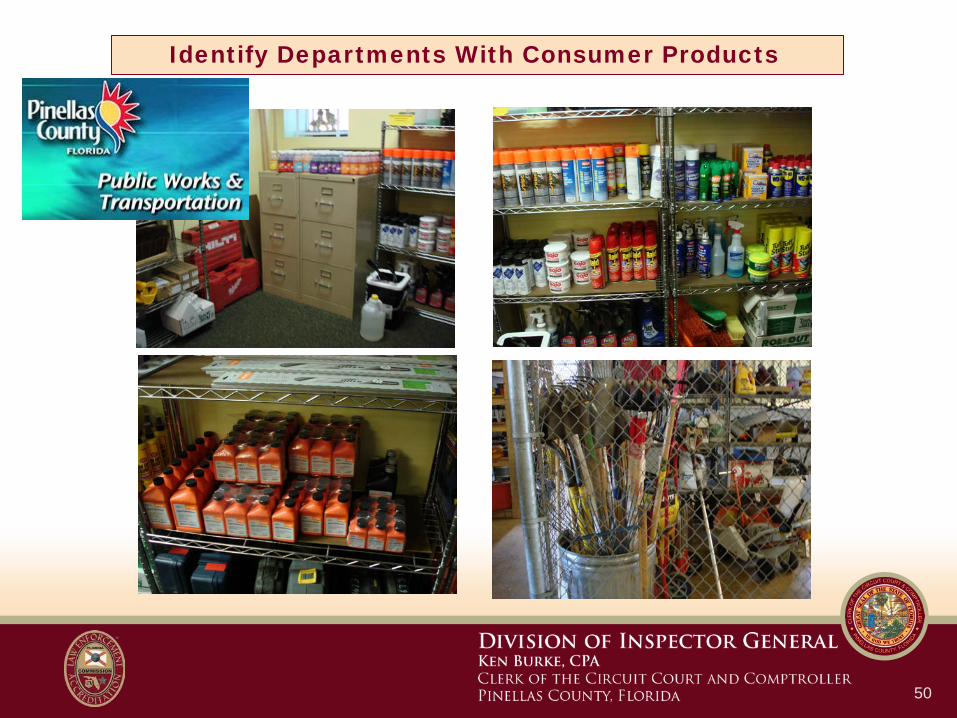

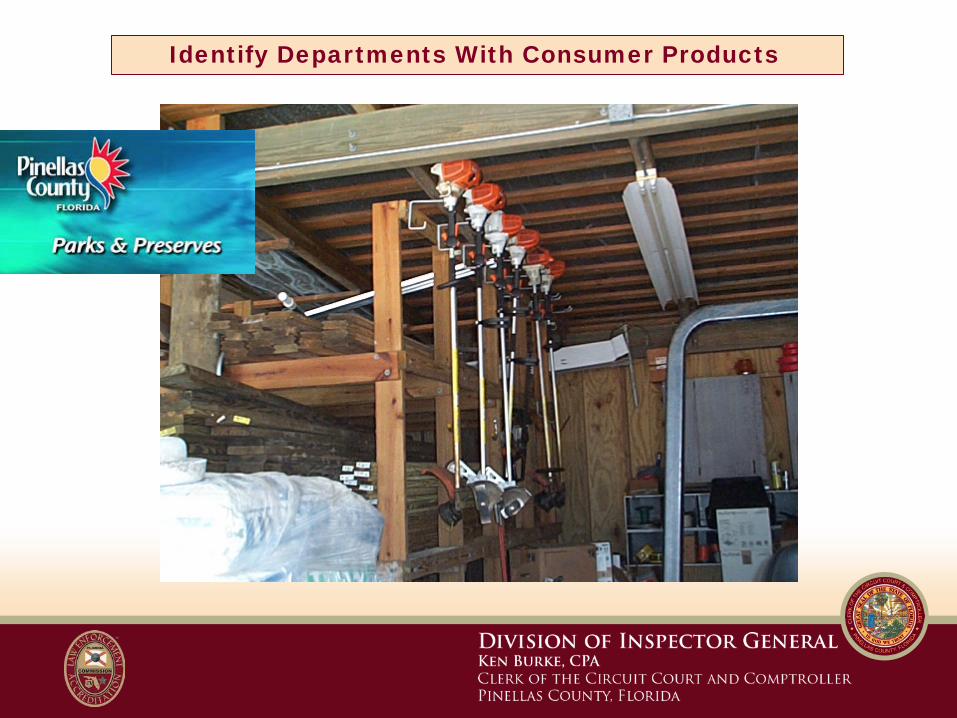

Inventory Not Secure And Is Subject To Theft

Identify Departments With Consumer Products

Identify Departments With Consumer Products

Identify Departments With Consumer Products

Identify Departments With Consumer Products

57

Continuous Audits of Driver and Vehicle Information Database (DAVID)

58

Continuous Audits of Driver and Vehicle Information Database (DAVID)

To fulfill each of the above areas’ responsibilities, the Clerk has entered into a Memorandum of Understanding (MOU) with the Florida Department of Highway Safety and Motor Vehicles (DHSMV), to access the Driver and Vehicle Information Database (DAVID) system. DAVID is a multifaceted database that affords retrieval of driver information, such as information about driver licenses, driver records, and vehicle title and registration data. Clerk’s staff access DAVID to fulfill their duties, such as looking up vehicle registration information when processing indigent determination forms and assisting customers with traffic citation questions. DAVID contains confidential personal information protected by Chapter 119 of the Florida Statutes and the Driver Privacy Protection Act.

59

Continuous Audits of Driver and Vehicle Information Database (DAVID)

1. Formalized Policies And Procedures Addressing DAVID.

2. DAVID User Access Is Not Updated Timely.

3. Required Quarterly Quality Control Reviews Are Not Conducted.

4. DAVID Confidentiality And Criminal Sanctions Acknowledgements Were Not Completed.

60

Audits of Selected Construction Contracts

Public Safety Facilities and Centralized Communications

Center

Description Estimated Costs Preliminary planning $ 2,000,000 Design Professional’s services $ 4,000,000 Construction Manager’s services $ 3,600,000 County’s costs* $ 3,400,000 Subcontractors’ costs $68,400,000

Total $81,400,000

Landfill Tipping Fees

The Abuse Of The $10 Single Axle Flat Rate Fee By Commercial Haulers Is Costing Solid Waste An Estimated

$1 Million Annually In Lost Revenues.

No Modifications

Allowed

Landfill Tipping Fees

Standard Single Axle

Tandem (double) Axle

Landfill Tipping Fees

No Modifications

Allowed

Landfill Tipping Fees

Specialized Modifications

by Local Manufacturer

Landfill Tipping Fees

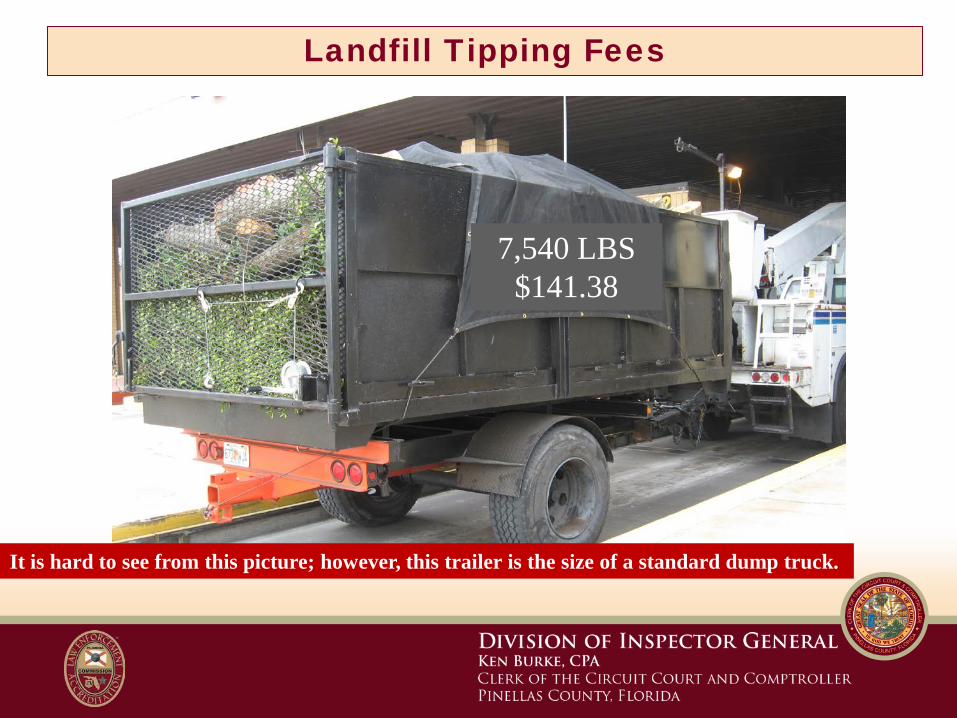

It is hard to see from this picture; however, this trailer is the size of a standard dump truck.

7,540 LBS $141.38

Landfill Tipping Fees

Net Tons Net Lbs Amount Collected Per Ton Charge 0.57 1,140 $ 10.00 $ 21.38 3.44 6,880 10.00 129.00 1.78 3,560 10.00 66.75 1.06 2,120 10.00 39.75 0.55 1,100 10.00 20.63 3.73 7,460 10.00 139.88 0.53 1,060 10.00 19.88 0.78 1,560 10.00 29.25 1.00 2,000 10.00 37.50 0.98 1,960 10.00 36.75 0.97 1,940 10.00 36.38 2.26 4,520 10.00 84.75 1.13 2,260 10.00 42.38 3.57 7,140 10.00 133.88 1.32 2,640 10.00 49.50 1.95 3,900 10.00 73.13 3.77 7,540 10.00 141.38 1.60 3,200 10.00 60.00 1.47 2,940 10.00 55.13 3.52 7,040 10.00 132.00 0.72 1,440 10.00 27.00 4.13 8,260 10.00 154.88 1.35 2,700 10.00 50.63 0.55 1,100 10.00 20.63 1.95 3,900 10.00 73.13 0.79 1,580 10.00 29.63 0.92 1,840 10.00 34.50 2.19 4,380 10.00 82.13 0.71 1,420 10.00 26.63 2.63 5,260 10.00 98.63 0.97 1,940 10.00 36.38 1.61 3,220 10.00 60.38 2.75 5,500 10.00 103.13 0.81 1,620 10.00 30.38 2.77 5,540 10.00 103.88 1.27 2,540 10.00 47.63 0.46 920 10.00 17.25 1.22 2,440 10.00 45.75

$380.00 $2,391.75

ONE DAY SINGLE AXLE

TRAILER SURVEY RESULTS

Net Dollar Range

$17.50 – $141.38

Net Pounds Range

920 – 7,540

Landfill Tipping Fees

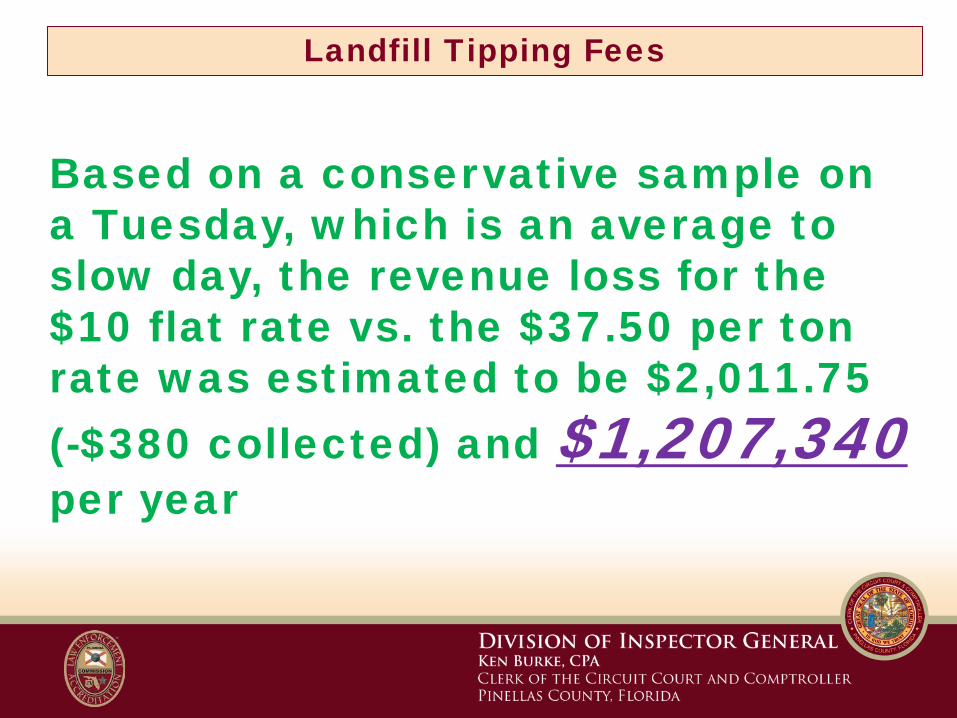

Based on a conservative sample on a Tuesday, which is an average to slow day, the revenue loss for the $10 flat rate vs. the $37.50 per ton rate was estimated to be $2,011.75 (-$380 collected) and $1,207,340 per year

Landfill Tipping Fees

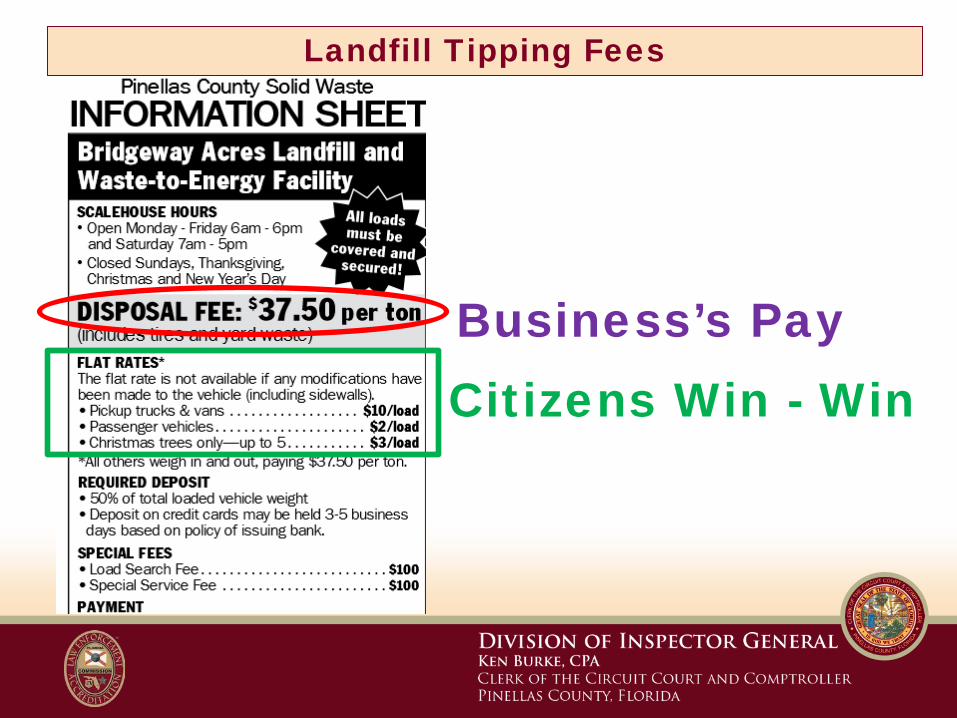

Business’s Pay Citizens Win - Win

Landfill Tipping Fees

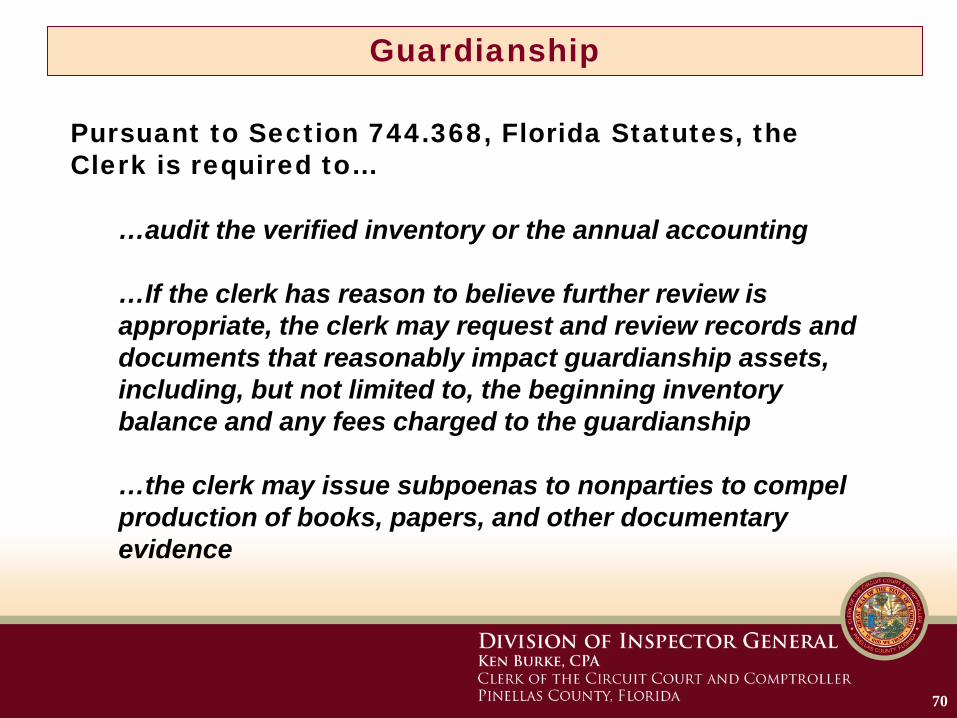

Pursuant to Section 744.368, Florida Statutes, the Clerk is required to…

…audit the verified inventory or the annual accounting …If the clerk has reason to believe further review is appropriate, the clerk may request and review records and documents that reasonably impact guardianship assets, including, but not limited to, the beginning inventory balance and any fees charged to the guardianship …the clerk may issue subpoenas to nonparties to compel production of books, papers, and other documentary evidence

70

Guardianship

INITIAL VERIFIED INVENTORY ANNUAL ACCOUNTINGS

ANNUAL GUARDIANSHIP PLAN

TRUST ACCOUNTINGS INITIAL GUARDIANSHIP PLAN

FINAL ACCOUNTINGS

Guardianship

MOTIVE PRESSURE + OPPORTUNITY + JUSTIFICATION

RATIONALIZATION

= FRAUD

Why Use The Audit Process? Because it is in the best interest of the ward!

Guardianship

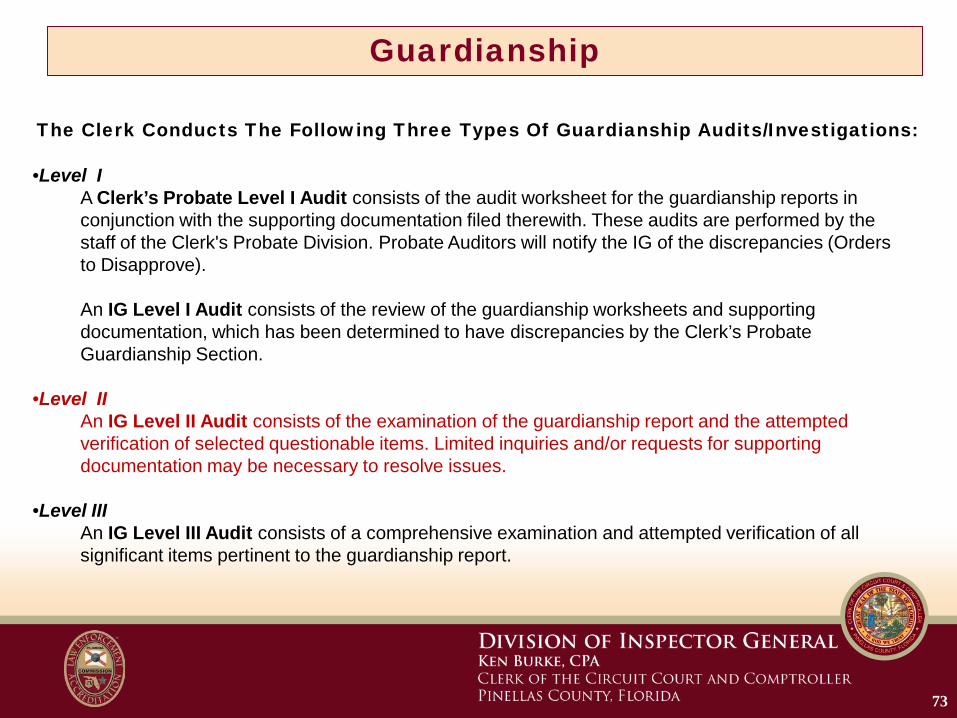

The Clerk Conducts The Following Three Types Of Guardianship Audits/Investigations: •Level I

A Clerk’s Probate Level I Audit consists of the audit worksheet for the guardianship reports in conjunction with the supporting documentation filed therewith. These audits are performed by the staff of the Clerk's Probate Division. Probate Auditors will notify the IG of the discrepancies (Orders to Disapprove).

An IG Level I Audit consists of the review of the guardianship worksheets and supporting documentation, which has been determined to have discrepancies by the Clerk’s Probate Guardianship Section.

•Level II An IG Level II Audit consists of the examination of the guardianship report and the attempted verification of selected questionable items. Limited inquiries and/or requests for supporting documentation may be necessary to resolve issues.

•Level III An IG Level III Audit consists of a comprehensive examination and attempted verification of all significant items pertinent to the guardianship report.

73

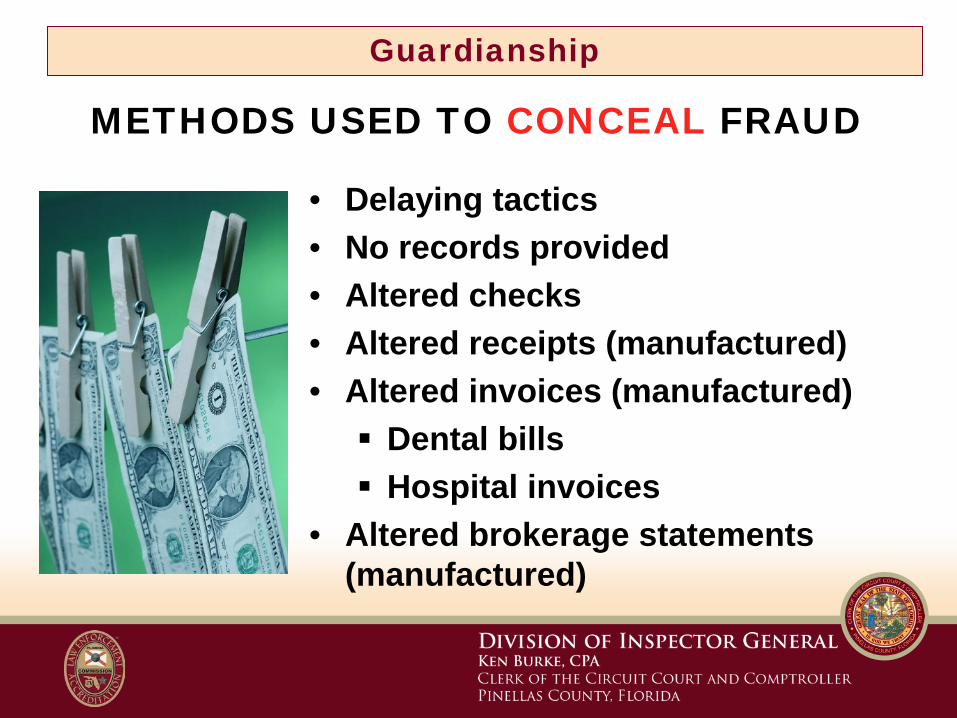

Guardianship

METHODS USED TO CONCEAL FRAUD

• Delaying tactics • No records provided • Altered checks • Altered receipts (manufactured) • Altered invoices (manufactured) Dental bills Hospital invoices

• Altered brokerage statements (manufactured)

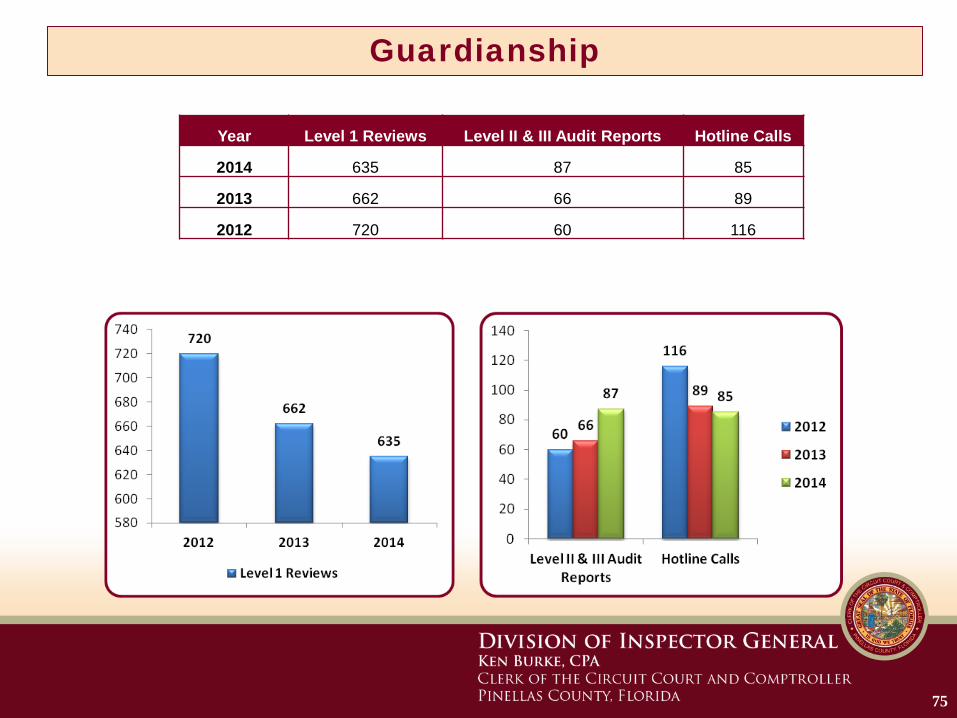

Guardianship

Year Level 1 Reviews Level II & III Audit Reports Hotline Calls

2014 635 87 85

2013 662 66 89

2012 720 60 116

75

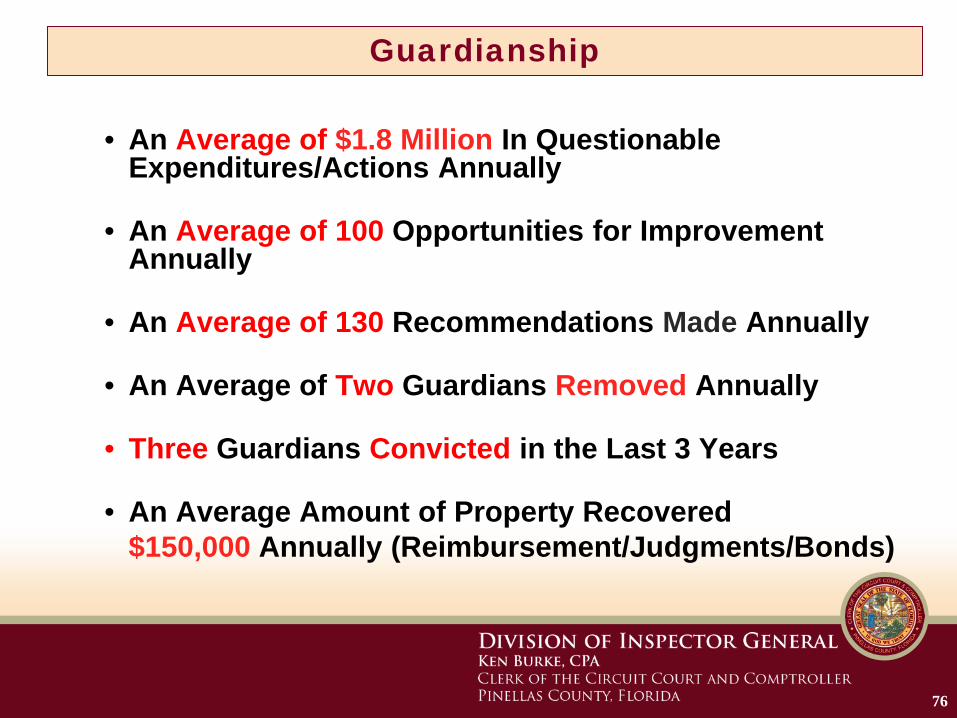

Guardianship

• An Average of $1.8 Million In Questionable Expenditures/Actions Annually

• An Average of 100 Opportunities for Improvement Annually

• An Average of 130 Recommendations Made Annually

• An Average of Two Guardians Removed Annually

• Three Guardians Convicted in the Last 3 Years

• An Average Amount of Property Recovered $150,000 Annually (Reimbursement/Judgments/Bonds)

76

Guardianship

77

Investigations

78

CLERK’S FRAUD, WASTE AND ABUSE POLICY

& BCC ADMINISTRATIVE

DIRECTIVE 19-1

–Posters –Newsletters –Business Cards –Check Stubs (direct deposit)

–County TV –Brochures –Fraud Video

79

Actively Market The Hotline