Kedco PLC Annual Report 2012

76

Kedco plc ANNUAL REPORT AND ACCOUNTS 2012

-

Upload

charlie-neville -

Category

Documents

-

view

217 -

download

1

description

Annual Report 2012

Transcript of Kedco PLC Annual Report 2012

Kedcoplc

ANNUAL REPORT AND ACCOUNTS

2012

Contents -

Our Business 01

Chairman’s Statement 06

Chief Executive’s Report 07

Board of Directors 10

Directors’ Report 11

Statement of Directors’ Responsibilities 14

Corporate Governance Report 15

Independent Auditors’ Report 16

Consolidated Statement of Comprehensive Income 18

Consolidated Statement of Other Comprehensive Income 19

Consolidated Statement of Financial Position 20

Consolidated Statement of Changes in Equity 21

Consolidated Statement of Cash Flows 22

Company Statement of Financial Position 23

Company Statement of Changes in Equity 24

Company Statement of Cash Flows 25

Notes to the Consolidated Financial Statements 26

Advisers and Other Information 73

Our Business - Who We AreOur stated aim is to be one of the UK and Ireland’s largest

independent renewable energy companies, with a diverse

portfolio of operating and developing assets across various

renewable energy technologies.

Our business strategy is to identify, develop, build, own and

operate renewable power plants in the UK and Ireland.

We identify seven stages in the development of a renewable

power generation project. These are; initial evaluation, sign

letter of intent, secure site, obtain planning and permitting,

secure financial closure, construction and finally operation.

Value is created as we move from one stage of a renewable

power project to the next. When we secure a site, value is

created; when we secure planning and permitting further

value is created. Moving to financial close on projects and

actual construction and operation in our view increases

project value substantially.

Why Renewable Energy?� The UK and Irish Governments view the Renewable

Energy Sector as an opportunity for economic rejuvenation,

driving industry growth and job creation

� The Renewable Energy Sector in the UK and Ireland is

driven by clear economic and political factors such as rising

energy costs, growing concerns over climate change and

increasingly supportive Government policy and regulation.

� Bound by targets under the EU Renewable Energy

Directive both Governments must ensure that 15% of

energy consumption is from renewables by 2020.

� The Renewable Energy market in the UK is estimated to

be worth £120 billion, making it the world’s sixth largest low

carbon economy. By 2014/15 this growing sector is

expected to be worth £150 billion.

Kedco PLC - Annual Report and Accounts 2012

KKeeddccoo ppllcc’’ss rreenneewwaabbllee eenneerrggyyppoorrttffoolliioo iinncclluuddeess iinntteerreessttss iinn tthhee UUnniitteedd KKiinnggddoomm aanndd IIrreellaanndd

Kedco plc’s 4MW biomass electricity and heat generatingplant, Newry, Northern Ireland

p1

Operational Highlights -

The company achieved its objective of transitioning from a

clean energy project developer to an operational project

owner with the commencement of generation of electricity

at the 4MW Newry Biomass project in Northern Ireland.

�

Significant progress has been made in relation to the ready

to construct 12MW Enfield Biomass project in London which

has included detailed discussions with EPC contractors and

with potential debt and equity partners.

�

Pre planning consultation phase for the Clay Cross Biomass

project is now complete with a full planning application to be

submitted by the end of Q1 2013.

�

Successfully negotiated the proposed acquisition of Reforce

Energy Limited a project developer with 60 active projects

with a capacity in excess of 40MW at various stages of

development in the UK and Ireland which will be completed

shortly

p2

Financial Highlights – Year ended 30th June 2012

�

� Revenue from continuing operations of e10.1m (FY 2011

restated: e0.9m)

�

� Administrative costs reduced to e0.9m (FY 2011 restated:

e3.6m)

� Loss before tax from continuing operations for the period

reduced to e1.6m (FY 2011 restated: Loss before tax

e5.3m)

�

� Total loss for the period reduced to e2.5m (FY 2011

restated: Loss for period e4.5m) includes one-off

impairment cost of e1.4m arising on the revaluation of the

Group’s Latvian subsidiary, SIA Vudlande

� 0.6 cent loss per share for continuing operations (FY 2011

restated: loss per share 2.3 cent)

Kedco PLC - Annual Report and Accounts 2012

p3

Debt Restructuring – � Successfully negotiated balance sheet restructuring with

various lenders, resulting in the conversion of debt to equity

and a reduction of balance sheet debt by approximately

e10.8m.

�

� Material reduction in ongoing annual interest of

approximately e1.5m.

p4

Asset Disposal -� Completed the disposal of a further non-core asset being

the entire interest in Latvian subsidiary for e3m, as part of

debt restructuring.

Share Placing / Funding -� Successful placings of shares to new investors in February

2012, May 2012 and November 2012 raising approximately

e1.5m.

�

� Negotiated and agreed term sheet for the provision of

£1.5m in VCT funding for the Newry Biomass project.

Kedco PLC - Annual Report and Accounts 2012

p5

I am pleased to present the 2012Annual Report, which provides anupdate on a year which has beenone of significant development forthe Company. This financial year haswithout doubt been the mostimportant in the Group’s history.

In September 2012 the Companyannounced that its biomasselectricity and heat generation plantin Newry, Northern Ireland,commenced the exportation ofpower to the grid. This marked theCompany’s transition from a puredevelopment company to anoperator of renewable energy assets.

Operationally the Companycompleted the refocusing of thebusiness portfolio towards its core,renewable energy power generationactivities. Cost savings have beendelivered through the exit from non-core and non-profitable businesssegments, creating a leaner, moreefficient business structure with thefocus purely on the renewableenergy power generation business.

Since 30th June 2012, the Company has carried out arestructuring process, with the objectives of stabilising theCompany’s financial affairs, positioning the Company in amanner which will enable it to raise further capital, andenabling the Company to adopt a more appropriate capitalstructure. This will facilitate the advancement of itsdevelopment project line through the planning andpermitting process. At the Extraordinary General Meetingheld on 5th October 2012, shareholders approvedresolutions regarding the restructuring process. The Board ishappy to report that this process in now complete.

The Board took the opportunity to reposition the Companyas a ‘technology neutral’ renewable energy business with acore focus on developing and delivering operationalelectricity and heat generation projects. The Company willfocus on both large and small-scale projects, providingflexibility to maximise existing land positions whilstdiversifying development and technology risks. This flexiblebusiness model will deploy capital where it can achieve thebest return for shareholders whilst still keeping the focus onthe generation of clean energy from either electricity or heat.

With this in mind the Company entered into negotiations toacquire Reforce Energy Limited (‘Reforce’), a renewableenergy development company focused on small-scalerenewable projects across various technologies. Reforce’skey markets are the UK, Ireland and Northern Ireland whereit already has an active pipeline of over 60 projects with acapacity of in excess of 40MW at various stages ofdevelopment. We expect to complete the acquisition shortly.

The Company’s ultimate aim is to be one of the UK andIreland’s largest independent renewable energy companies,with a diverse portfolio of operating and development assetsacross various renewable energy technologies. To this end,the Company will focus on developing its existing portfolioas well as considering strategic bolt-on acquisitionopportunities that add generating potential to its projectportfolio.

On behalf of my colleagues on the Board, we wish toexpress our thanks to the management and staff who haveworked so diligently over the past year. I look forward toupdating shareholders further on the Company’s progress atour Annual General Meeting in December.

Dermot O’ConnellNon-Executive Chairman

Chairman’s Statement -

‘NNeewwrryy pprroojjeeccttmmaarrkkss tthheeCCoommppaannyy’’ssttrraannssiittiioonn ttoo aannooppeerraattoorr ooffrreenneewwaabbllee eenneerrggyyaasssseettss ffrroomm aa ppuurreeddeevveellooppmmeennttccoommppaannyy

p6

Operational ReviewThe Company’s stated aim is to beone of the UK and Ireland’s largestindependent renewable energycompanies, with a diverse portfolioof operating and development assetsacross various renewable energytechnologies.

The Company currently has 67MWof potential power at various stagesof development as set out below:

Newry Biomass – 4MW Biomasscombined heat and power (‘CHP’)The Company recently announcedthat its plant in Newry, NorthernIreland, commenced the exportationof power to the grid. This marks theCompany’s transition to an operatorof renewable energy assets from apure development company. Theelectricity generated by the plant isbeing sold to Bord Gáis Eireann

under a Power Purchase Agreement (‘PPA’). The Companynow intends to move towards the completion of the next2MW phase of the project, which is expected to come onlinein Q4 2013. The civil and on-site works for this additional2MW have already been completed and a deposit has beenpaid to secure the expansion of the grid infrastructure forthe project. Kedco has invested £6m through a combinationof equity and loan notes in the project corporate entity andowns 50 per cent of the ordinary equity and 92 per cent ofthe economic return from the project. Our majorshareholder, Farmer Business Developments plc, owns theremaining 50 per cent of the ordinary equity but is onlyentitled to eight per cent of the economic return from theproject. The balance of the project funding was arrangedthrough a financing deal with RBS Ulster Bank, whichcommitted project finance facilities of up to £8m. Furtherupdates will be provided in the near future as the projectmoves towards full commissioning of the first phase.

We intend to complete the planning process for a further4MW extension to the Newry Biomass project, bringing thecapacity up to 8MW in the coming year.

Enfield Biomass – 12MW Biomass CHPThe Company’s other key asset is the 12MW EnfieldBiomass project located in Enfield, London. This project hasfull planning and permitting to convert 60,000 tonnes perannum of waste wood and has entered into advanceddiscussions in relation to an offer to connect to the nationalgrid. The Company has already entered into a 20 year leasein relation to the site. The Company has various optionsavailable in relation to feedstock sourced locally for theplant. The Directors believe that this project is one of themost advanced biomass development projects located in theLondon region and the Company intends to progress theproject towards financial close and commencement ofconstruction. Advanced discussions are currently takingplace with potential debt and equity partners in relation tothe project. We intend to complete the financing andstarting construction of the 12MW Enfield Biomass projectin the coming year. A further update will be provided asappropriate.

Cork and Kerry Anaerobic Digestion (‘AD’) projects The Company has full planning and permitting for two siteslocated in the South of Ireland which could convert 40,000tonnes of agricultural and food waste per annum into up to1.5MW of electricity and 1.4MW of heat. These projects willqualify for the Irish Government support scheme forrenewable energy under REFIT III, which covers biomasstechnologies for the period 2010 to 2015. This schemeprovides for a fixed feed in tariff rate of between e0.10-e0.13 per kilowatt hour (‘kWh’) produced, depending onthe use of heat generated from the plant. A strategicdecision regarding the development of these two projects iscurrently being undertaken.

Clay Cross Biomass CHP and AD and Rutland ADThe Company has also invested heavily in planning andpermitting over the last 18 months and it is currentlyengaged in the consenting process for an 8MW site inDerbyshire and 1.3MW AD site in East Anglia, both in theUK.

Chief Executive’s Report -

Kedco PLC - Annual Report and Accounts 2012

‘TThhee ccoonnssttrraaiinniinnggffaaccttoorrss ooff tthhee ppaassttaarree nnooww bbeehhiinndd

p7

Pluckanes Wind FarmReforce recently made an announcement that it hascompleted the purchase of Pluckanes Windfarm Limited(‘Pluckanes’), which has developed a fully consented 800kwsingle wind turbine project located in Cork, Ireland. Thepurchase of the Pluckanes project has added a constructionready asset to the portfolio, which is targeted to becomeoperational during 2013. Once the Acquisition is finalisedand with the commissioning of the project next year, theCompany’s operational capacity will increase by 40 per cent.

Project PortfolioThe Company is currently in discussion with a number of siteowners in the UK and Ireland regarding future sites for thedevelopment of renewable energy projects. The intention isto secure sites that will increase the development pipeline toa minimum 300MW within the next three years.

Reforce whose acquisition will be completed shortly has apipeline of over 60 projects with a capacity of in excess of40MW across various technologies located in the UK,Ireland and Northern Ireland.

Financial ReviewRevenue in the period amounted to e10.1m and was in linewith expectations (FY 2011 restated: e0.9m). The Groupreported a loss for the period of e2.5m, a decrease on theprior year loss of e4.5m for FY 2011. Included in the loss ofe2.5m is a one-off impairment cost of e1.4m arising on therevaluation of the group’s Latvian subsidiary, SIA Vudlandebefore disposal post year end. The decrease in losses isattributable to a significant reduction in administrative costsduring the year and a decrease in financing costs arisingfrom the restructuring of debt.

At 30th June 2012, the Group had net debt of e11.9m(30th June 2011: e11.8m) including cash balances ofe144,764 (30th June 2010: e616,285).

The Group has carried out a restructuring process since theyear end which has significantly strengthened the Group’sbalance sheet through the reduction of approximatelye10.8m of debt obligations of the Group, as well as areduction of its annual interest charge by approximatelye1.5m. The reduction of e10.8m was achieved through theconversion of debt into equity and the sale of its Latviansubsidiary, SIA Vudlande.

OutlookIn the 2011 preliminary announcement the Board promisedshareholders that we would aggressively pursue otheropportunities in our project pipeline. I am pleased to reportthat we have made substantial progress in adding furtherprojects to the pipeline, which I believe will add shareholdervalue in the short to medium term.

Against this positive backdrop, we have further refined andrefocused the Company’s strategy with a clear aim of beingone of the largest independent renewable energy companiesin the UK and Ireland. The successful completion of thebalance sheet restructure further solidifies this strategy andprovides a springboard for the Company to accelerate itsproject pipeline. In light of the Company’s expandingpipeline of development and acquisition opportunities, theDirectors anticipate undertaking a further equity fundraisingin 2013.

I was also delighted to announce the impending acquisitionof Reforce which is expected to close imminently. I feel thatthe transaction provides a key endorsement of our strategy.In addition to a strong pipeline of renewable energy projects,Reforce has an experienced management team with over 10years’ experience across 500MW+ of renewable energyprojects. The Reforce management team and shareholders,by agreeing to the acquisition, believe there is an attractivevalue creation story for the combined Group.

Chief Executive’s Report - continued

p8

The Board has identified the following objectives for thecoming 12 months:� To complete the financing and starting construction of the12MW Enfield Biomass project. � To complete the financing and start installation of thesecond stage of the 4MW Newry Biomass which will be fullycommissioned by end of the 2013.� To complete the planning process for a further 4MWextension to the Newry Biomass project, thereby bringingthe capacity up to 8MW. � Once the Reforce Acquisition is finalised, complete thefinancing and commissioning the 800kw PluckanesWindfarm project.� To obtain planning permission for the 8MW Clay CrossBiomass project.� Once the Acquisition is finalised bring the Altilow 800kwwind project to a fully consented and ready-to-constructstage.� To obtain at least another six planning permissions forsmall scale renewable energy projects� To double the size of the Company’s current developmentpipeline.

We believe the constraining factors of the past are nowbehind the Company. With the restructuring, pipelineprogress and proposed acquisition of Reforce, we are moreconfident than ever of being able to deliver real shareholdervalue in the short to medium term.

We will continue to focus the Company’s resources onbringing projects to construction ready and financial closestages and in managing the operations of these projects.Projects will sit in their own individual special purposeentities and project funding will take place in those entities.The Company intends to retain an equity interest in all futureprojects to the benefit of shareholders in the listed Company.

Gerry MaddenCEO

Chief Executive’s Report - continued

Kedco PLC - Annual Report and Accounts 2012

p9

Kedco PLC Board of Directors -

�� Dermot O’ConnellNon-Executive ChairmanDermot O’Connell, who isChairman of Cork CooperativeMarts and a director of theCompany’s largest shareholder,Farmer Business Developmentsplc, joined the Board as a Non-Executive Director in March2011 and was appointed asNon – Executive Chairman inOctober 2011. Dermot's other directorships compriseFairfield Estates Limited, Fairfield Developments Limited,CCM House Limited, Corrin Event Centre Limited, MarketGreen Developments Limited, Market Green Estates Limitedand CCM Dovea Genetics Limited.

�� Gerry Madden CEO and Interim Finance DirectorGerry Madden joined Kedco plc in May 2007 as FinanceDirector. He has more than two decades of experience inbusiness in the UK and Ireland. Prior to joining Kedco, Gerryoperated his own consulting practice between 1998 and2007, advising companies on corporate finance and businessstrategy. Before that Gerry worked for 16 years with theinternational accountants KPMG and was auditor andadviser to listed companies, multinationals and privatecompanies operating in Ireland and internationally. Gerry hasacted as Non-Executive Director for a variety of companiesin different business sectors in Ireland. Gerry is a Fellow ofthe Institute of Chartered Accountants in Ireland havingqualified as an accountant with KPMG in 1987. Gerry holdsa degree in Commerce from University College Cork.

�� Brendan Halpin Executive DirectorBrendan Halpin joined Kedco plc in February 2006 asFinancial Controller and joined the Board as ExecutiveDirector in March 2011. Brendan is a Fellow of the Instituteof Chartered Accountants in Ireland, having qualified as anaccountant with PricewaterhouseCoopers in 1998. Hiscurrent responsibilities include inter alia, financemanagement, project management and treasury functions.

�� Edward Barrett Non-Executive DirectorEddie Barrett is one of the original founders of Kedco plc.He established International Livestock Genetics Ltd, an Irishimporter and distributor of bovine genetics based in Co.Cork and has been Managing Director since 1993. Inaddition, Eddie is a Director of Platinum Asset ManagementLtd, an investment company specialising in the renewableenergy sector.

�� William Kingston Non-Executive DirectorWilliam Kingston is one of the original founders of Kedcoplc, joining the Board in January 2005 as Chairman. He isalso a past president of the Irish Grassland Association, abody focused on research and dissemination of informationto the Irish agricultural industry. William was a boardmember of the Food Safety Authority of Ireland from 2002to 2006 and the West Cork Leader (an EU-backed bodyinvolved in rural development) from 2005 to 2007.

�� Diarmuid Lynch Non-Executive DirectorDiarmuid Lynch is one of the original founders of Kedco plc.He operates one of the largest dairy farms in Ireland basedin Co. Cork. From 1998 to 2000, he served on the board ofthe Blackwater Trading Company, a group involved in theprocurement of agricultural inputs, services and feedstockin the Blackwater region of Ireland.

�� Donal O’Sullivan Non-Executive DirectorDonal O’Sullivan joined the board in August 2007. He wasthe Chairman and Executive Director of Esso Ireland Limitedbetween 1986 and 2001. He was also a Director of the IrishPetroleum Industry Association, the representative body ofcompanies in Ireland who import, distribute and marketpetroleum products. Donal held the position of ManagingDirector of HOYER Ireland Ltd and was a board member ofHOYER in the UK from 2001 to 2006. HOYER Ireland is asubsidiary of HOYER GmbH, a company involved in theprovision of specialist logistics services to the petroleum,chemical, gas and foodstuff sector.

Kedco plc Board of Directors (l-r): Edward Barrett, Donal O'Sullivan, Diarmuid Lynch, Dermot O'Connell, Brendan Halpin, Gerry Madden and William Kingston.

p10

Directors’ Report -

The Directors present their annual report and the audited financial statements of the company and its subsidiaries collectively known as‘the Group’ for the year ended 30th June 2012.

Principal ActivitiesThe principal activities of the Group are to identify, develop, build, own and operate power plants in the UK and Ireland using renewableenergy technologies. The Group focuses on both large and small scale projects, providing flexibility to maximize existing land positions whilediversifying development and technology risks. The Group’s ultimate aim is to be one of the UK and Ireland’s largest independent renewableenergy companies, with a diverse portfolio of operating and development assets across various renewable technologies. To this end, theGroup will focus on developing its existing portfolio as well as considering strategic bolt-on acquisition opportunities that add generatingpotential to its project portfolio.

Review of Business and Future Developments and Key Performance Indicators

A review of the Group’s business and future developments and key performance indicators is contained in the Chairman’s Statement andthe Chief Executive’s Report on pages 6 to 9. Below is a summary.

Operational HighlightsThe Company achieved its objective of transitioning from a clean energy project developer to an operational project owner with thecommencement of generation of electricity at the 4MW Newry Biomass project in Northern Ireland.●Significant progress has been made in relation to the ready-to-construct 12MW Enfield Biomass project in London, including detaileddiscussions with EPC contractors and with potential debt and equity partners.●Pre-planning consultation phase for the Clay Cross Biomass project is now complete with a full planning application to be submitted bythe end of Q1 2013.●Successfully negotiated the proposed acquisition of Reforce Energy Limited (‘Reforce’), a project developer with 60 active projects and acapacity in excess of 40MW at various stages of development in the UK and Ireland. It is anticipated that the acquisition will be completedshortly.

Financial Highlights Revenue from continuing operations of e10.1m (FY 2011 restated: e0.9m).●Administrative costs reduced to e0.95million (FY 2011 restated: e3.6m).●Loss before tax from continuing operations for the period reduced to e1.6m (FY 2011 restated: Loss before tax e5.3m). ●Total loss for the period reduced to e2.5m (FY 2011 restated: Loss for period e4.5m) includes one-off impairment cost of e1.4m arisingon the revaluation of the Group’s Latvian subsidiary, SIA Vudlande.●0.6 cent loss per share for continuing operations (FY 2011 restated: loss per share 2.3 cent).

Debt RestructuringSuccessfully negotiated balance sheet restructuring with various lenders, resulting in the conversion of debt to equity and a reduction ofbalance sheet debt by approximately e10.8m.●Material reduction in ongoing annual interest of approximately e1.5m.

Asset DisposalCompleted the disposal of a further non-core asset being the entire interest in Latvian subsidiary for e3m, as part of debt restructuring.

Share Placing / Funding Successful placings of shares to new investors in February 2012, May 2012 and November 2012 raising approximately e1.5m.●Negotiated and agreed term sheet for the provision of £1.5m in VCT funding for the Newry Biomass project.

Results and DividendsThe results for the year are set out on page 18. No dividends have been proposed by the Directors (2011: eNil).

Kedco PLC - Annual Report and Accounts 2012

p11

Directors’ Report - (continued)

Principal Risks and UncertaintiesThe Group has a risk management structure in place, which is designed to identify, manage and mitigate business risk. Risk assessmentand evaluation is an essential part of the Group’s internal control system.

Information about the financial risk management objectives and policies of the Group, along with exposure of the group to credit risk,liquidity risk and market risk, are disclosed in Note 4 of the notes to the consolidated financial statements.

The Group is exposed to a number of other risks and uncertainties. These break into two categories:1 General risks impacting the business.2 Project development related risk.

GGeenneerraall RRiisskkss

Electricity marketThe Group’s plans are exposed to electricity market price risk through variations in the wholesale price of electricity. The Group managesthis risk by entering into long term power purchase agreements.

Legislative riskThe Group is exposed to adverse changes in legislation that may impact the income for renewable energy power plants. The directorsmonitor possible changes to legislation and where possible engage in the consultation process to safeguard the Group’s interests.Projected project revenues could be affected by changes to the renewable legislation including for example; the number of RenewableObligation Certificates awarded per MWh of generation under the Renewable Obligation. Any negative changes to these projectedrevenues could impact the ability of the group to secure debt and equity for projects.

PPrroojjeecctt ddeevveellooppmmeenntt rriisskkss

Site evaluation and procurementSecuring sites for the development of renewable energy power plants is a key requirement in further developing the business. This reliesupon the ability of the Group to locate, evaluate, select, develop and realise appropriate opportunities, and to be able to negotiate andcomplete land agreements and related access/connection agreements at a cost that allows profitable projects to be developed.

The Group manages these risks by continually reviewing a large number of sites in the UK and Ireland such that it is not focused onany one particular landowner or location.

Planning and development consentOnce a site is secured a planning and development consent is sought, together with any other necessary permits to allow a renewableenergy power plant to be constructed and operated. During this stage of the process the Group is exposed to the following specificrisks:�

�

�

�

The Group manages these risks through securing sites on which it believes it can secure planning and development consent, employingsuitably qualified and significantly experienced staff to manage the consenting process and ensure compliance with the latest legislation,as well as ensuring maximum engagement of local authorities and interested stakeholders from a very early stage.

The Group has significant experience of securing planning consents for renewable energy power plants and knowledge of the importantcriteria involved. The Group uses this experience when selecting sites for development.

consents may be subjected to delays beyond the Group’s control, which may subsequently cause the project to be delayed or aborted.There are no guarantees that any or all of the necessary consents will be granted;consents granted may be subject to conditions that affect the economic or operational viability of the proposed project. These couldin turn impact the Group’s ability to raise project finance, or reduce the value of a project in the case of a sale;delays or onerous planning conditions may lead to unforeseen costs which the Group may need to raise finance for;legislative changes may influence the acceptability of the site or the economic viability of the project.

p12

Directors’ Report - (continued)

Principal Risks and Uncertainties (continued)PPrroojjeecctt ddeevveellooppmmeenntt rriisskkss (continued)Contract NegotiationThis stage of the development process involves the negotiation of contracts for the construction of the renewable energy plant, thesale of electricity and related products produced by the plant, the procurement of fuel for the plant and the operation of the plant. Thisstage begins during the early stages of the planning and development and concludes at the point of financial close. During this stagethe Group is exposed to the following specific risks in addition to those outlined above:�

�

The Group manages these risks through soliciting bids from a number of different suppliers for the equipment required to constructthe plant and any other materials or equipment required to ensure the plant can operate profitably.

Financial closeThis stage relates to the crystallisation of the project into the construction stage. This may involve either the sale of the project, in wholeor part, or securing project finance enabling the project to be constructed. During this stage the Group is exposed to the additionalrisks:�

�

�

�

It is the Boards view that once the project has planning and development consent, these risks are mitigated by the potential to sell aproject for at least its book value.

The Group has experience in negotiating financial arrangements for power plants and understands the contract structures required tosecure project finance. Additionally the Group has relationships with a number of project finance banks, utility and large industrialcompanies allowing project finance or sale discussions to be initiated.

ConstructionThis stage is reached once financing, both debt and equity, is secure and all project contracts are entered into.

During this stage the Group is exposed to the following specific risks:�

�

�

�

The Group seeks to mitigate these risks through the negotiation of fixed price contracts with reputable contractors and by ensuringthe financial plans include adequate levels of contingency to accommodate cost overruns. Additionally, the Group seeks to appoint anowner’s engineer with significant experience to oversee the project programme once construction commences.

Going ConcernThe directors have assessed going concern. See Note 3 for further details.

DirectorsThe present Directors are listed on page 10.

Mr Alf Smiddy resigned as director of the company on 13th February, 2012.

In accordance with the Articles of Association, Diarmuid Lynch and Donal O’Sullivan retire by rotation and, being eligible, offerthemselves for re-election.

The board recommends the re-election of Diarmuid Lynch and Donal O’Sullivan as directors.

the ability to secure fixed price contracts for the construction of each power plant with the required level of guarantees that allowproject finance to be secured;significant changes to inflation impacting the costs of building and operating renewable energy power plants and therefore theprofitability of renewable energy power plants; and

the general availability of finance to fund the construction of power plants, and the level of lending that can be secured;changes to interest rates which may impact the cost of financing power projects;the ability to secure equity on acceptable terms for the construction of projects once debt is in place; anddepressed market for the sale of projects, leading to low prices or no willing buyers.

cost overruns by contractors or claims made may result in a need for additional equity or debt funding;delays to the construction programme leading to higher than planned interest charges during the construction programme and maydelay the commencement of operating cash flows to fund the Company’s ongoing activities;failure of the completed plant to operate as planned; andsupplier insolvency.

Kedco PLC - Annual Report and Accounts 2012

p13

Directors’ Report - (continued)

Directors’ and Secretary’s Interests in SharesThe Directors and Secretary of Kedco plc who held office at 30th June 2012 had the following interests in the shares of the Company:

� Diarmuid Lynch 21,294,186 5,021,880 21,294,186 5,021,880� William Kingston 16,639,734 4,094,100 16,559,734 4,094,100� Edward Barret 13,571,666 3,080,000 13,486,666 3,080,000� Brendan Halpin 8,271,120 3,261,873 8,271,120 3,261,873� Gerry Madden 76,667 14,926,161 76,667 14,926,161� Donal O’Sullivan 66,667 2,238,924 66,667 2,238,924� Dermot O’Connell - - - -

Remuneration Committee ReportThe Group’s policy on senior executive remuneration is designed to attract and retain people of the highest calibre who can bring theirexperience and independent views to the policy, strategic decisions and governance of the Group.

In setting remuneration levels the Remuneration Committee takes into consideration the remuneration practices of other companies ofsimilar size and scope. A key philosophy is that staff must be properly rewarded and motivated to perform in the best interests of theshareholders. Details of Directors remuneration are included in Note 36 of the notes to the consolidated financial statements.

Books of AccountTo ensure that proper books and accounting records are kept in accordance with Section 202 of the Companies Act, 1990, the Directorshave employed appropriately qualified accounting personnel and have maintained appropriate computerised accounting systems. Thebooks of account are located at 4600 Airport Business Park, Cork, Ireland.

Subsequent EventsDetails of events occurring since 30th June 2012 which impact on the Group are included in Note 41.

AuditorsThe auditors, Deloitte & Touche, Chartered Accountants, continue in office in accordance with Section 160(2) of the Companies Act 1963.

Approved by the Board on 30th November 2012.

Dermot O’Connell Gerard Madden Chairman Director

Number of Ordinary Sharesat 30th June 2012

Number of ‘A’ Ordinary Sharesat 30th June 2012

Number of Ordinary Sharesat 1st July 2011

(or at date ofappointment if earlier)

Number of ‘A’ Ordinary Sharesat 1st July 2011

(or at date ofappointment if earlier)

Statement of Directors’ Responsibilities -

Irish company law requires the Directors to prepare financial statements for each financial year, which gives a true and fair view of the stateof affairs of the Company and the Group, and of the profit or loss of the Group for that period.

In preparing the financial statements, the Directors are required to:� Select suitable accounting policies and then apply them consistently;� Make judgements and estimates that are reasonable and prudent; and� Prepare the financial statements on the going concern basis unless it is inappropriate to presume that the Company will continue in

business.

The Directors are responsible for keeping proper books of account which disclose with reasonable accuracy at any time the financial positionof the Company and to enable them to ensure that the financial statements are prepared in accordance with accounting standards generallyaccepted in Ireland and comply with Irish statute comprising the Companies Acts, 1963 to 2012. They are also responsible for safeguardingthe assets of the Company and hence for taking reasonable steps for the prevention and detection of fraud and other irregularities. TheDirectors are responsible for the maintenance and integrity of the corporate and financial information included on the Company’s website.

Corporate Governance Report -

The Company is not subject to the Combined UK Corporate Governance Code, applicable to companies with full listing on the LondonStock Exchange. The Company does however intend, so far as is practicable and desirable, given the size and nature of the business, tofollow the recommendations on corporate governance for AIM companies (the ‘QCA Guidelines’) issued by the Quoted CompaniesAlliance (‘QCA’).

The BoardThe board of directors of the Company is responsible to shareholders for leadership in all aspects of the business. The board comprises sevenmembers. Five independent Non-Executive directors, contribute individual experience from diverse backgrounds. Two Executive Directorsare responsible for the implementation of all board decisions and oversee the management of the Group on a day-to-day basis.

In accordance with the articles of association, one-third of directors retire by rotation each year. Each director must be subject to re-electionat least every three years.

Role of the BoardThe Company has adopted a schedule of matters reserved for consideration by the whole board, including, for example: approval of theGroup’s long-term objectives and commercial strategy; approval of the annual operating and capital expenditure budgets of the Group (andany material changes thereto); changes relating to the Group’s structure; major changes to the Group’s corporate structure; approval ofthe Group’s annual report and accounts; approval of the dividend policy; major capital projects; changes to the structure, size andcomposition of the board; determination of the remuneration for the directors, the Company Secretary and executive management; divisionof responsibilities between the Chairman, the Chief Executive and other executives of the board; and the making of political donations orpolitical expenditure.

The Board is also responsible for ensuring maintenance of sound systems of internal control and risk management and the directors confirmthat they continually review the effectiveness of the system of internal control, covering all material controls including financial, operationaland compliance controls and risk management.

In accordance with QCA Guidelines, the board has established audit, nomination and remuneration committees, as described below, andutilises other committees as necessary in order to ensure effective governance.

Audit CommitteeThe Company’s Audit Committee comprises William Kingston as the Chairman, Donal O’Sullivan and Diarmuid Lynch. The Audit Committeemeet at least three times a year at appropriate times in the reporting and audit cycle and otherwise as required. The Finance Directornormally attends meetings of the Committee and the Chief Executive Officer attends as necessary. The external auditors are invited toattend meetings of the Audit Committee on a regular basis.

The terms of reference for the Audit Committee include the following responsibilities:� Monitoring the integrity of the reported financial performance of the Group, including its preliminary results announcement, annual reportand interim report;

� Reviewing the effectiveness of the Group’s internal financial controls;� Making recommendations to the board on the appointment and removal of the external auditors and the audit fee;� Monitoring the objectivity and independence of the external auditors.

Nomination CommitteeThe Company’s Nomination Committee comprises Donal O’Sullivan as the Chairman, Diarmuid Lynch and William Kingston. TheNomination Committee meets at such times required by the Chairman of the Committee. The Nomination Committee is responsible formaking recommendations on all new board appointments.

Remuneration CommitteeThe Company’s Remuneration Committee comprises Edward Barrett as the Chairman, Diarmuid Lynch and William Kingston. The role ofthe Remuneration Committee is to review the performance of the Executive Directors and other senior executives and to set the scale andstructure of their remuneration, including the implementation of any bonus arrangements, with due regard to the interests of OrdinaryShareholders. The Remuneration Committee also administers and establishes performance targets for share incentive schemes anddetermines the allocation of share incentives to employees.

The Board has adopted a code for dealings in the Company’s securities by directors and applicable employees, which conforms to therequirement of the AIM Rules (Share Dealing Code). The Company will be responsible for taking all proper and reasonable steps to ensurecompliance by the directors and applicable employees with the Share Dealing Code and the AIM Rules. The Company complies with thecorporate governance obligations applicable to Irish registered public companies whose shares are quoted on the AIM market of theLondon Stock Exchange.

Kedco PLC - Annual Report and Accounts 2012

p15

Independent Auditor’s Report to the members of Kedco plc -

We have audited the financial statements of Kedco plc for the year ended 30th June 2012 which comprise the Group Financial Statements:the Consolidated Statement of Comprehensive Income, the Consolidated Statement of Other Comprehensive Income, the ConsolidatedStatement of Financial Position, the Consolidated Statement of Changes in Equity, the Consolidated Statement of Cashflows and theCompany Financial Statements: the Company Statement of Financial Position, the Company Statement of Changes in Equity and CompanyStatement of Cashflows and the related Notes 1 to 42. These financial statements have been prepared under the accounting policies setout therein.

This report is made solely to the company's members, as a body, in accordance with Section 193 the Companies Act, 1990. Our auditwork has been undertaken so that we might state to the company’s members those matters we are required to state to them in an auditors’report and for no other purpose. To the fullest extent permitted by law, we do not accept or assume responsibility to anyone other thanthe company and the company’s members as a body, for our audit work, for this report, or for the opinions we have formed.

Respective responsibilities of directors and auditorsThe directors are responsible for preparing the Annual Report, including the preparation of the Group Financial Statements in accordancewith applicable law and International Financial Reporting Standards (IFRSs) as adopted by the European Union and the Parent CompanyFinancial Statements in accordance with applicable law and accounting standards issued by the Accounting Standards Board and publishedby the Institute of Chartered Accountants in Ireland (Generally Accepted Accounting Practice in Ireland).

Our responsibility, as independent auditor, is to audit the financial statements in accordance with relevant legal and regulatory requirementsand International Standards on Auditing (UK and Ireland).

We report to you our opinion as to whether the Group Financial Statements give a true and fair view, in accordance with IFRSs as adoptedby the European Union and the Parent Company Financial Statements give a true and fair view, in accordance with Generally AcceptedAccounting Practice in Ireland, and are properly prepared in accordance with Irish statute comprising the Companies Acts, 1963 to 2012.We also report to you whether in our opinion: proper books of account have been kept by the company; whether, at the balance sheetdate, there exists a financial situation requiring the convening of an extraordinary general meeting of the company; and whether theinformation given in the Directors' Report is consistent with the financial statements. In addition, we state whether we have obtained allthe information and explanations necessary for the purpose of our audit and whether the company's balance sheet is in agreement withthe books of account.

We also report to you if, in our opinion, any information specified by law or the Listing Rules of the Alternative Investment Market of theLondon Stock Exchange regarding directors’ remuneration and directors’ transactions is not disclosed and, where practicable, include suchinformation in our report.

We read the other information contained in the Annual Report and consider the implications for our report if we become aware of anyapparent misstatement or material inconsistencies with the financial statements. The other information comprises only the Chairman’sStatement, Chief Executive’s Report, Director’s Report and the Corporate Governance Statement. Our responsibilities do not extend to otherinformation.

Basis of audit opinionWe conducted our audit in accordance with International Standards on Auditing (UK and Ireland) issued by the Auditing Practices Board.An audit includes examination, on a test basis, of evidence relevant to the amounts and disclosures in the financial statements. It alsoincludes an assessment of the significant estimates and judgements made by the directors in the preparation of the financial statementsand of whether the accounting policies are appropriate to the company’s and the group’s circumstances, consistently applied and adequatelydisclosed.

We planned and performed our audit so as to obtain all the information and explanations which we considered necessary in order toprovide us with sufficient evidence to give reasonable assurance that the financial statements are free from material misstatement, whethercaused by fraud or other irregularity or error. In forming our opinion we evaluated the overall adequacy of the presentation of informationin the financial statements.

p16

Independent Auditor’s Report to the members of Kedco plc (continued)

OpinionIn our opinion: • the Group Financial Statements give a true and fair view, in accordance with IFRSs as adopted by the European Union, of thestate of the affairs of the group as at 30 June 2011 and of its loss for the year then ended; • the Group Financial Statements have been properly prepared in accordance with the Companies Acts, 196to 2009 • the Parent Company Financial Statements give a true and fair view, in accordance with Generally Accepted AccountingPractice in Ireland as applied in accordance with the provisions of the Companies Acts 1963 to 2009, of the state of the parentcompany affairs as at 30 June 2011; and • the Parent Company financial statements have been properly prepared in accordance with the Companies Acts, 1963 to2009.

Emphasis of Matter – Going Concern Without qualifying our opinion, we draw your attention to Note 3 to the financial statements which indicates that the Groupincurred a loss for the year of e2,481,358 and had net current liabilities and net liabilities of e6,258,722 and e827,330 respectivelyat the balance sheet date. These conditions indicate the existence of a material uncertainty which may cast significant doubt aboutthe Group’s ability to continue as a going concern. The directors believe progress towards securing finance is being made and thatmeasures have been taken to strengthen the Group’s financial position. The directors have a reasonable expectation that the Groupwill have adequate resources to continue in operational existence for the foreseeable future. The directors have prepared thefinancial statements of the company and the group on a going concern basis. The financial statements do not include theadjustments that would result if the Group was unable to continue as a going concern.

We have obtained all the information and explanations we considered necessary for the purpose of our audit. In our opinionproper books of account have been kept by the company. The company’s balance sheet is in agreement with the books of account.

In our opinion the information given in the Directors' Report is consistent with the financial statements.

The net assets of the company, as stated in the Company Statement of Financial Position are more than half the amount of its called-up share capital and, in our opinion, on that basis there did not exist at 30th June 2012 a financial situation which, under Section40(1) of the Companies (Amendment) Act, 1983, would require the convening of an extraordinary general meeting of theCompany.

Brian Murphy For and on behalf of Deloitte & Touche Chartered Accountants and Registered Auditors Cork

Date: 10th December 2012

The Group Financial Statements give a true and fair view, in accordance with IFRSs as adopted by the European Union, of thestate of the affairs of the group as at 30th June 2012 and of its loss for the year then ended; The Group Financial Statements have been properly prepared in accordance with the Companies Acts, 1963 to 2012;The Parent Company Financial Statements give a true and fair view, in accordance with Generally Accepted Accounting Practicein Ireland as applied in accordance with the provisions of the Companies Acts, 1963 to 2012, of the state of the parent companyaffairs as at 30th June 2012; and The Parent Company financial statements have been properly prepared in accordance with the Companies Acts, 1963 to 2012.

Kedco PLC - Annual Report and Accounts 2012

p17

Consolidated Statement of Comprehensive Income -for the year ended 30th June 2012

(Restated)Notes 2012 2011

h h

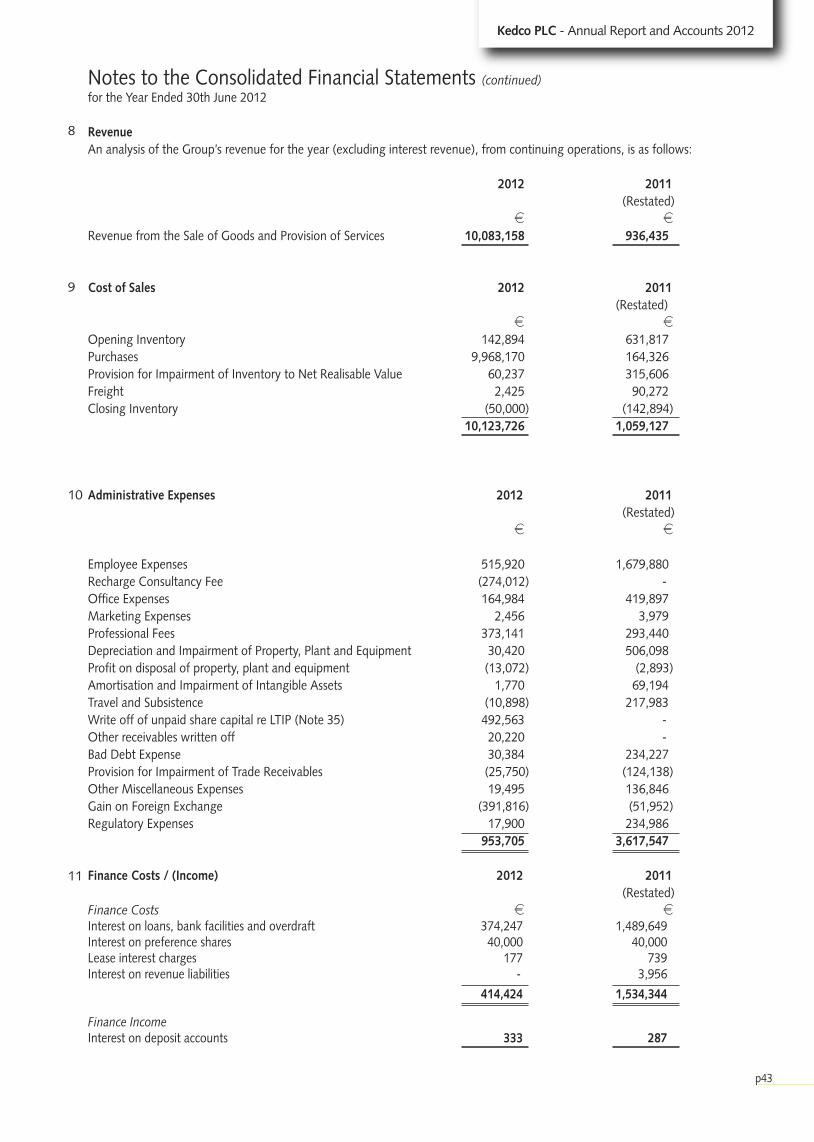

Revenue 8 10,083,158 9,936,435

Cost of Sales 9 (10,123,726) (1,059,127)

Gross Loss (40,568) (122,692)

Operating ExpensesAdministrative Expenses 10 (953,705) (3,617,547)Other Operating Income 11,100 7,605

Operating Loss (983,173) (3,732,634)

Finance Costs 11 (414,424) (1,534,344)Share of Losses on Joint Ventures after Tax 23 (213,923) (356,228)Profit on Disposal of Share in Joint Venture 23 - 9,285,379Finance Income 11 333 287

Loss Before Taxation 13 (1,611,187) (5,337,540)

Income Tax Expense 14 - -

Loss for the Year from Continuing Operations (1,611,187) (5,337,540)

Profit for the year from discounted operations 15 493,911 9,802,677Losses arising on the remeasurement of assets held for sale 15 (1,364,082) -

Net loss for the year from discontinued operations 15 (870,171) 9,802,677

Loss for the year - total (2,481,358) (4,534,863)

Loss Attributable To:Owners of the Company (2,580,140) (4,698,241)Non-Controlling Interest 98,782 163,378

(2,481,358) (4,534,863)

Euro Per Share Euro Per ShareBasic Loss Per Share:From Continuing Operations 17 (0.006) (0.023)From Continuing and Discontinued Operations 17 (0.009) (0.020)

Diluted Loss Per Share:From Continuing Operations 17 (0.006) (0.023)From Continuing and Discontinued Operations 17 (0.009) (0.020)

p18

Consolidated Statement of Other Comprehensive Income -for the year ended 30th June 2012

2012 2011h h

Loss for the Financial Year (2,481,358) (4,534,863)

Other Comprehensive IncomeExchange differences arising on retranslation of foreign operations (310,844) 21,063

Total comprehensive income and expense for the year (2,792,202) (4,513,800)

Attributable to:Owners of the company (2,890,984) (4,677,178)Non-controlling interests 98,782 163,378

(2,792,202) (4,513,800)

Kedco PLC - Annual Report and Accounts 2012

p19

Consolidated Statement of Financial Position -At ended 30th June 2012

Notes 2012 2011ASSETS h h

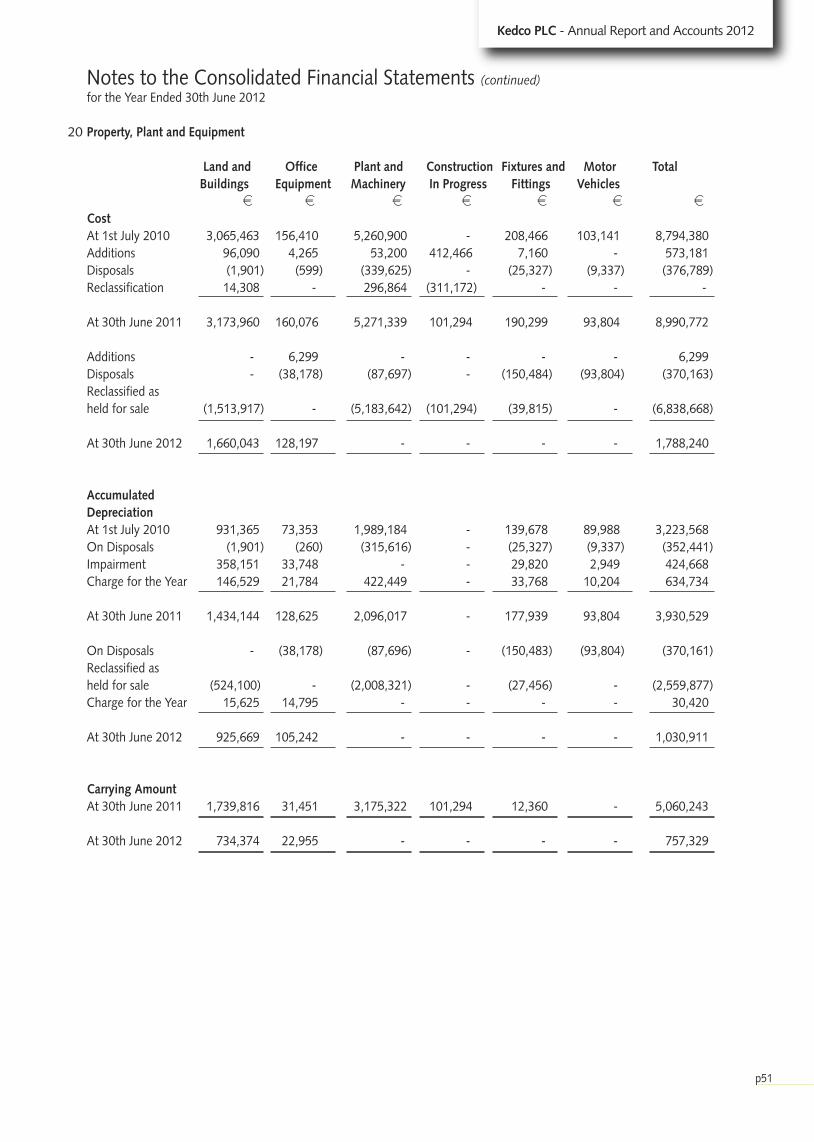

Non-Current AssetsGoodwill 18 - 549,451Intangible assets 19 - 505Property, plant and equipment 20 757,329 5,060,243Financial assets 21 7,608,687 990,000Total Non-Current Assets 8,366,016 6,600,199

Current AssetsInventories 24 50,000 1,613,026Amounts due from customers under construction contracts 25 1,355,212 9,425,279Trade and other receivables 26 1,605,518 2,848,088Cash and cash equivalents 37 144,764 616,285

3,155,494 14,502,678Assets classified as held for sale 16 6,584,239 -

Total Current Assets 9,739,733 14,502,678

TOTAL ASSETS 18,105,749 21,102,877

EQUITY AND LIABILITIESEquityShare capital 27 4,106,808 3,543,999Share premium 27 19,375,525 19,038,300Shared based payment reserves 28 - 492,580Retained earnings – deficit (25,207,673) (22,316,689)

(Deficit) /Equity attributable to equity holders of the parent (1,725,340) 758,190Non-controlling interest 898,010 799,228Total (Deficit) /Equity (827,330) 1,557,418

Non-Current LiabilitiesBorrowings 29 2,425,025 7,958,393Deferred income – government grants 30 - 36,915Finance lease liabilities 31 - 373Share of net liabilities of jointly controlled entities 23 509,599 18,867Deferred tax liability 33 - 268,062Total Non-Current Liabilities 2,934,624 8,282,610

Current LiabilitiesAmounts due to customers under construction contracts 25 1,110,090 1,272,735Trade and other payables 32 2,595,766 5,481,674Borrowings 29 9,661,645 4,494,676Deferred income – government grants 30 - 9,444Finance lease liabilities 31 373 4,320

13,367,874 11,262,849Liabilities associated with assets held for sale 16 2,630,581 -Total Current Liabilities 15,998,455 11,262,849

TOTAL EQUITY AND LIABILITIES 18,105,749 21,102,877

p20

Consolidated Statement of Changes in Equity -for the year ended 30th June 2012

Share Share Retained Share Based Attributable to Non TotalCapital Premium Earnings Payment Equity Holders Controlling

Reserve of the Parent Interesti i i i i i i

Balance at 1st July 2010 3,239,407 17,410,077 (17,639,511) 328,383 3,338,356 635,850 3,974,206

Issue of ordinary shares in Kedco plc 304,592 1,628,223 - - 1,932,815 - 1,932,815

Loss for the financial year - - (4,698,241) - (4,698,241) 163,378 (4,534,863)

Unrealised foreign exchange gain - - 21,063 - 21,063 - 21,063

Share based payments - - - 164,197 164,197 - 164,197

Balance at 30th June 2011 3,543,999 19,038,300 (22,316,689) 492,580 758,190 799,228 1,557,418

Issue of ordinary sharesin Kedco plc 562,809 337,225 - - 900,034 - 900,034

Loss for the financial year - - (2,580,140) - (2,580,140) 98,782 (2,481,358)

Unrealised foreign - - (310,844) - (310,844) - (310,844)exchange gain

Share based payments - - (492,580) (492,580) - (492,580)

Balance at 30th June 2012 4,106,808 19,375,525 (25,207,673) - (1,725,340) 898,010 (827,330)

Kedco PLC - Annual Report and Accounts 2012

p21

Consolidated Statement of Cash Flows -for the year ended 30th June 2012

Notes 2012 2011Cash Flows from Operating Activities h h

Loss for the financial year (2,481,358) (4,394,977)Adjustments for:Income Tax 69,731 -Share based payments (492,580) 164,197Depreciation of property, plant and equipment 596,418 634,734Amortisation of intangible assets 2,275 71,396Profit on disposal of property, plant and equipment (67,236) (88,881)Impairment of property, plant and equipment - 424,668Impairment of intangible assets - 94Impairment of assets held for sale 1,364,082 -Write off of unpaid share capital 492,563 -Unrealised foreign exchange gain 163,677 6,941Share of losses of jointly controlled entities after tax 213,923 356,228Decrease in provision for impairment of trade receivables (71,924) (166,014)(Decrease) /Increase in impairment of inventories (294,715) 281,921Decrease in deferred income (10,302) (10,303)Interest expense 506,754 1,627,690Profit on disposal of share in joint venture - (285,379)Interest income (338) (364)

Operating cash flows before working capital changes (9,030) (1,378,049)Decrease/(Increase) in:Amounts due from customers under construction contracts 8,070,067 (133,368)Trade and other receivables 4,336 (174,720)Inventories 276,377 (284,932)

(Decrease)/increase in:Amounts due to customers under construction contracts (162,645) (29,622)Trade and other payables (2,476,219) (717,781)

Cash From /(Used in) Operations 5,702,886 (2,718,472)Income taxes paid (9,108) (55,968)Net Cash From /(Used in) Operating Activities 5,693,778 (2,774,440)

Cash Flows from Investing ActivitiesAdditions to property, plant and equipment (644,737) (573,181)Proceeds from sale of property, plant and equipment 126,951 113,229Additions to intangible assets (1,770) -Additions to investments in jointly controlled entities (6,660,010) -Proceeds from disposal of interest in jointly controlled entities - 134,840Interest received 338 364Net Cash Used in Investing Activities (7,179,228) (324,748)

Cash Flows from Financing ActivitiesProceeds from borrowings 2,896,483 4,142,687Repayments of borrowings (2,293,628) (1,583,381)Proceeds from issuance of ordinary shares 644,250 1,932,815Payments of finance leases (58,496) (36,803)Interest paid (255,842) (590,526)Net Cash from Financing Activities 932,767 3,864,792

Net (Decrease) /Increase in Cash and Cash Equivalents (552,683) 765,604Cash and cash equivalents at the beginning of the financial year 208,587 (557,017)Cash and cash equivalents at the end of the financial year 37 (344,096) 208,587

p22

Company Statement of Financial Position -At 30th June 2012

Notes 2012 2011h h

ASSETSNon-Current AssetsIntangible Assets 19 - -Investment in Subsidiary Undertakings 21 24,941,463 24,941,463

Total Non-Current Assets 24,941,463 24,941,463

Current AssetsTrade and other receivables 26 18,336,014 10,850,094Cash and bank balances 37 14,331 402,718

Total Current Assets 18,350,345 11,252,812

TOTAL ASSETS 43,291,808 36,194,275

EQUITY AND LIABILITIESEquityShare Capital 27 4,106,808 3,543,999Share Premium 27 38,309,604 37,972,379Share based payment reserve 28 - 492,580Retained earnings - deficit (11,835,887) (11,550,529)

Equity attributable to equity holders of the parent 38 30,580,525 30,458,429

Non-Current LiabilitiesBorrowings 29 - 3,435,580

Total Non-Current Liabilities - 3,435,580

Current LiabilitiesBorrowings 29 6,680,402 1,827,070Trade and other payables 32 6,030,881 473,196

Total Current Liabilities 12,711,283 2,300,266

TOTAL EQUITY AND LIABILITIES 43,291,808 36,194,275

Kedco PLC - Annual Report and Accounts 2012

p23

Company Statement of Changes in Equity -for the Year Ended 30th June 2012

Share Share Retained Share-Based TOTALCapital Premium Earnings Payment

Reserveh h h h h

Balance at 1st July 2010 3,239,407 36,344,157 (401,254) 328,383 39,510,693

Issue of ordinary sharesin Kedco plc 304,592 1,628,222 - - 1,932,814

Loss for the financial year - - (11,149,275) - (11,149,275)

Share based payments - - - 164,197 164,197

Balance at 30th June 2011 3,543,999 37,972,379 (11,550,529) 492,580 30,458,429

Issue of ordinary sharesin Kedco plc 562,809 337,225 - - 900,034

Loss for the financial year - - (285,358) - (285,358)

Share based payments - - - (492,580) (492,580)

Balance at 30th June 2012 4,106,808 38,309,604 (11,835,887) - 30,580,525

p24

Company Statement of Cash Flows -for the Year Ended 30th June 2012

Year Ended Year EndedNotes 30th June 2012 30th June 2011

u u

Cash Flows from Operating ActivitiesLoss before taxation (285,358) (11,149,275)Adjustments for:Share based payments (492,580) 164,197Interest expense 160,926 1,148,881Interest income (333) (265)Amortisation of intangible assets 1,770 -Foreign currency losses arising from retranslation of borrowings 430,401 -Provision for impairment of investment in subsidiaries - 10,460,290

Operating cash flows before working capital changes (185,174) 623,828

Increase in:Trade and other receivables (7,485,824) (5,326,037)

Increase in:Trade and other payables 5,551,138 287,286

Cash used in operations (2,119,860) (4,414,923)Income taxes paid (695) (5,390)

Net Cash Used in Operating Activities (2,120,555) (4,420,313)

Cash Flows from Investing ActivitiesAdditions to investments in subsidiaries - (1)Additions to intangible assets (1,770) -Interest received 333 265

Net Cash (used in) / from Investing Activities (1,437) 264

Cash Flows from Financing ActivitiesProceeds from borrowings 1,200,000 4,117,732Repayments of borrowings (95,979) (1,073,411)Proceeds from issuance of ordinary shares 644,250 1,932,814Interest paid (14,666) (182,091)

Net Cash from Financing Activities 1,733,605 4,795,044

Net (Decrease) / Increase in Cash and Cash Equivalents (388,387) 374,995

Cash and cash equivalents at the beginning of the Financial Year 402,718 27,723

Cash and Cash Equivalents at the end of the Financial Year 37 14,331 402,718

Kedco PLC - Annual Report and Accounts 2012

p25

Notes to the Consolidated Financial Statements -for the Year Ended 30th June 2012

General InformationKedco plc (‘the Company’) was incorporated in Ireland on 2nd October 2008. The address of its registered office and principal placeof business is Building 4600, Cork Airport Business Park, Kinsale Road, Cork.

On 13th October 2008 the Group, previously headed by Kedco Block Holdings Limited, underwent a re-organisation by virtue ofwhich Kedco Block Holdings Limited’s shareholders, in their entirety, exchanged their shares for shares in Kedco plc, a newly-formedcompany. Kedco plc then became the ultimate parent company of the Group.

These financial statements for the year ended 30th June 2012 consolidate the individual financial statements of the Company and itssubsidiaries (together referred to as ‘the Group’).

On 20th October 2008 the Company’s shares were admitted to trading on the London Stock Exchange’s AIM market.

The principal activity of the Group is as follows:

� Identify, develop, build, own and operate power plants in the UK and Ireland using renewable energy technologies. The Groupfocuses on both large and small scale projects, providing flexibility to maximise existing land positions while diversifying developmentand technology risks.

Application of New and Revised International Financial Reporting Standards (IFRSs)The following new and revised Standards and Interpretations have been adopted by the Group with no significant impact on itsconsolidated results or financial position, but may impact the accounting for future transactions or arrangements:

AS 24 Related Party Disclosures (2009) clarifies the definition of a related party and provides a partial exemption from related partydisclosures for government-related entities.

Amendment to IFRIC 14 Prepayments of a minimum funding requirement remedies an unintended consequence of IFRIC 14 whereentities are in some circumstances not permitted to recognise as an asset prepayments of minimum funding contributions.

Improvements to IFRSs (2010). These amendments concerned the following Standards:

� IFRS1 First Time Adoption of International Financial Reporting Standards clarifies the requirement to explain changes in accountingpolicy in the year of adoption and amends the usage of deemed cost in certain circumstances.

� IFRS7 Financial Instruments: Disclosures encourages the use of qualitative disclosures to enable users to understand the nature andextent of risks arising from financial instruments and clarifies the required level of disclosure around credit risk and collateral held.

� IAS1 Presentation of Financial Statements clarifies that an entity may present the analysis of other comprehensive income by itemeither in the statement of changes in equity or in the notes to the financial statements.

� IAS 34 Interim Financial Reporting emphasises the principle in IAS34 that the disclosure of significant events and transactions in interim periods should update the relevant information presented in the most recent annual report.

� IFRIC 13 Customer Loyalty Programmes clarifies what should be accounted for in determining the fair value of award credits.

Disclosures – Transfers of Financial Assets (Amendments to IFRS 7 Financial Instruments: Disclosures) increases the disclosurerequirements for transactions involving the transfer of financial assets, enhances the existing disclosures under IFRS7 where an assetis transferred but not derecognised and introduces new disclosures for assets that are derecognised but the entity continues to have acontinuing exposure to the asset after the sale.

The following new and revised Standards and Interpretations have not been adopted by the Group, whether endorsed by the EuropeanUnion or not. The Group is currently analysing the practical consequences of the new Standards and the effects of applying them tothe financial statements. The related standards and interpretations are:

� IFRS 9 Financial Instruments and subsequent amendments (effective for annual periods beginning on or after 1st January 2015, notyet endorsed by the European Union);

� IFRS 10 Consolidated Financial Statements (effective for annual periods beginning on or after 1st January 2013; not yet endorsedby the European Union).

1

2

p26

Notes to the Consolidated Financial Statements - (continued)for the Year Ended 30th June 2012

Application of New and Revised International Financial Reporting Standards (IFRSs) (continued)� IFRS 11 Joint Arrangements (effective for annual periods beginning on or after 1st January 2013; not yet endorsed by the EuropeanUnion).

� IFRS 12 Disclosure of Interest in Other Entities (effective for annual periods beginning on or after 1st January 2013; not yet endorsedby the European Union).

� IFRS 13 Fair Value Measurement (effective for annual periods beginning on or after 1st January 2013; not yet endorsed by theEuropean Union).

� IAS 27 Separate Financial Statements (Amended 2011) (effective for annual periods beginning on or after 1st January 2013; not yetendorsed by the European Union).

� IAS 28 Investments in Associates and Joint Ventures (Amended 2011) (effective for annual periods beginning on or after 1st January2013; not yet endorsed by the European Union).

� Amendments to IFRS 1 First Time Adoption of International Financial Reporting Standards (effective for annual periods beginningon or after 1st January 2013; not yet endorsed by the European Union).

� Amendments to IFRS 7 Financial Instruments: Disclosures (effective for annual periods beginning on or after 1st January 2013; notyet endorsed by the European Union).

� Amendments to IAS 1 Presentation of Financial Statements (effective for annual periods beginning on or after 1st July 2012; endorsedby the European Union 5th June 2012).

� Amendments to IAS 12 Income Taxes (effective for annual periods beginning on or after 1st January 2012; not yet endorsed by theEuropean Union).

� Amendments to IAS 19 Employee Benefits (effective for annual periods beginning on or after 1st January 2013; endorsed by the European Union 5th June 2012).

� Amendments to IAS 32 Financial Instruments: Presentation (effective for annual periods beginning on or after 1st January 2014; notyet endorsed by the European Union).

� Annual Improvements to IFRSs: 2009-2011 Cycle (effective for annual periods beginning on or after 1st January 2013; not yet endorsed by the European Union)

� Consolidated Financial Statements, Joint Arrangements and Disclosure of Interests in Other Entities: Transitional Guidance (effectivefor annual periods beginning on or after 1st January 2013; not yet endorsed by the European Union)

Statement of Accounting Policies

Basis of PreparationThe Group’s consolidated financial statements have been prepared in accordance with International Financial Reporting Standards(IFRS) effective at 30th June 2012 for all periods presented as issued by the International Accounting Standards Board. The consolidatedfinancial statements are also prepared in accordance with IFRS as adopted by the European Union (‘EU’).

The consolidated financial statements are prepared under the historical cost convention except for certain financial assets and financialliabilities which are measured ar fair value. The principal accounting policies set out below have been applied consistently by the parentcompany and by all of the Company’s subsidiaries to all periods presented in these consolidated financial statements.

The financial statements of the parent company, Kedco plc have been prepared in accordance with accounting standards generallyaccepted in Ireland and Irish statute comprising the Companies Acts, 1963 to 2012.

2

3

Kedco PLC - Annual Report and Accounts 2012

p27

Notes to the Consolidated Financial Statements - (continued)for the Year Ended 30th June 2012

Statement of Accounting Policies (continued)Basis of Preparation (continued)As described in the Chief Executive’s Report, the Company continues to invest capital in developing customer and partner relationshipsin the UK and Ireland. The Company has also continued to develop and expand its pipeline of projects. These activities resulted in theCompany continuing to report reduced losses for the year to 30th June 2012.

The group incurred a loss of e2,481,358 (2011: e4,534,863) during the year, and it had net current liabilities of e6,258,722 (2011:net current assets e3,239,829) and net liabilities of e827,330 (2011: net assets e1,557,418) at 30th June 2012. Since 30th June 2012,the Company has carried out a restructuring process, with the objective of stabilising the Company’s financial affairs, position theCompany in a manner which will enable it to raise further capital, and enable the Company to adopt a more appropriate capitalstructure, which will facilitate the advancement of its development project line through the planning and permitting process. Resolutionsapproving the restructuring process were agreed by the members of the Company at an Extraordinary General Meeting of the Companyheld on 5th October 2012.

The restructuring has significantly strengthened the Group’s balance sheet through the reduction of approximately e10.8m of DebtObligations from the group and a reduction of its annual interest charge by approximately e1.5m. The reduction in e10.8m wasachieved through the conversion of debt into equity (e5.8m) and the sale of its Latvian subsidiary SIA Vudlande, which has the affectof removing debt (e1.4m) from the balance sheet and paying down zero loan note holders (e3m).

In conjunction with the above restructuring, the Company raised approximately e0.95m in an equity placing in November 2012. Theproceeds of the Fundraising will be used by the Company to meet its on-going working capital requirements including the continueddevelopment of its project pipeline. The Company also announced in November 2012 that it had secured a conditional offer of furtherfinancing of £1.5m for the further development of its Newry Power Plant.

The financial statements have been prepared on a going concern basis. The Directors have given careful consideration to theappropriateness of the going concern concept in the preparation of the financial statements. The validity of the going concern conceptis dependent upon finance being available for the Group’s working capital requirements and for the continued investment in theGroup’s strategy of identifying, developing, building and operating power generating plants so that the Group can continue to realiseits assets and discharge its liabilities in the normal course of business. The financial statements do not include any adjustments that wouldresult should the above conditions not be met.

After making enquiries and considering the matters referred to above, the Directors believe that progress towards securing finance hasbeen and is being made. The Directors have a reasonable expectation that the Group will have adequate resources to continue inoperational existence for the foreseeable future. For these reasons the Directors continue to adopt the going concern basis of accountingin preparing the financial statements.

3

p28

Notes to the Consolidated Financial Statements - (continued)for the Year Ended 30th June 2012

Statement of Accounting Policies (continued)Basis of ConsolidationThe consolidated financial statements incorporate the financial information of the Company and its subsidiaries. The financial year-endsof all entities in the Group are coterminous.

The financial statements of subsidiaries are included in the consolidated financial statements from the date on which control over theoperating and financial decisions is obtained and cease to be consolidated from the date on which control is transferred out of theGroup. Control exists where the Company has the power, directly or indirectly, to govern the financial and operating policies of theentity so as to obtain economic benefits from its activities.

The results of subsidiaries acquired or disposed of during the year are included in the consolidated income statement from the effectivedate of acquisition or up to the effective date of disposal, as appropriate.

Where necessary, adjustments are made to the financial statements of subsidiaries to bring their accounting policies in line with thoseused by other members of the Group.

The results and assets and liabilities of subsidiaries are incorporated in these financial statements using equity method of accounting,except when the subsidiary is classified as held for sale, in which case it is accounted for in accordance with IFRS 5 Non-current AssetsHeld for Sale and Discontinued Operations.

On 13th October 2008 the Group, previously headed by Kedco Block Holdings Limited, underwent a re-organisation by virtue ofwhich Kedco Block Holdings Limited’s shareholders, in their entirety, exchanged their shares for shares in Kedco plc, a newly formedCompany. Kedco plc then became the ultimate parent company of the Group. Notwithstanding the change in the legal parent of theGroup, this transaction has been accounted for as a reverse acquisition under IFRS 3 Business Combinations and these consolidatedfinancial statements are prepared on the basis of the new legal parent, Kedco plc, having been acquired by the existing Group. As aresult of applying reverse acquisition accounting, the consolidated financial statements are a continuation of the financial statementsof Kedco Block Holdings Limited and its subsidiaries.

All intra-group transactions, balances, income and expenses are eliminated in full on consolidation.

Non-controlling interests in the net assets (excluding goodwill) of consolidated subsidiaries are identified separately from the Group’sequity therein. Non-controlling interests consist of the amount of those interests at the date of the original business combination andthe non-controlling share of changes in equity since the date of the combination. Losses applicable to the non-controlling interest inexcess of its interest in the subsidiary’s equity are allocated against the interests of the Group except to the extent that the non-controlling interest has a binding obligation and is able to make an additional investment to cover the losses.

Business CombinationsAcquisitions of subsidiaries and businesses from third parties are accounted for using the purchase method. The cost of the businesscombination is measured at the aggregate of the fair values (at the date of exchange) of assets given, liabilities incurred or assumed,and equity instruments issued by the Group in exchange for control of the acquiree, plus any costs directly attributable to the businesscombination. The acquiree’s identifiable assets, liabilities and contingent liabilities that meet the conditions for recognition under IFRS 3,Business Combinations, are recognised at their fair values at the acquisition date, except for non-current assets that are classified asheld for sale in accordance with IFRS 5, Non-Current Assets Held for Sale and Discontinued Operations, which are recognised andmeasured at fair value less costs to sell.

Goodwill arising on acquisition is recognised as an asset and initially measured at cost, being the excess of the cost of the businesscombination over the Group’s interest in the net fair value of the identifiable assets, liabilities and contingent liabilities recognised. If,after reassessment, the Group’s interest in the net fair value of the acquiree’s identifiable assets, liabilities and contingent liabilitiesexceeds the cost of the business combination, the excess is recognised immediately in profit or loss.

The interest of non-controlling shareholders in the acquiree is measured at the non-controlling interest’s proportion of the net fairvalue of the assets, liabilities and contingent liabilities recognised.

GoodwillFor the purpose of impairment testing, goodwill is allocated to each of the Group’s cash-generating units expected to benefit from thesynergies of the combination. Cash-generating units to which goodwill has been allocated are tested for impairment annually, or morefrequently when there is an indication that the unit may be impaired. If the recoverable amount of the cash-generating unit is less thanthe carrying amount of the unit, the impairment loss is allocated first to reduce the carrying amount of any goodwill allocated to theunit and then to the other assets of the unit pro-rata on the basis of the carrying amount of each asset in the unit.

3

Kedco PLC - Annual Report and Accounts 2012

p29

Notes to the Consolidated Financial Statements - (continued)for the Year Ended 30th June 2012

Statement of Accounting Policies (continued)Goodwill (continued)An impairment loss for goodwill is immediately recognised in profit or loss and not reversed in a subsequent year.

On disposal of a subsidiary or a jointly controlled entity, the attributable amount of goodwill is included in the determination of theprofit or loss on disposal.