Kd skladi part 2

13

15 Description: Naftna industrija Srbije is a vertically integrated oil and gas company incorporated in Serbia. Sector: Energy Market Cap: €1.3bn (RSD 145bn) Current Price: RSD 890 Upside: 23% Strengths: A vertically integrated oil&gas company which is highly profitable as oil prices are liberalised and royalty taxes are very low Privatised in 2009 when GazpromNeft became a majority shareholder GPN brought industry know-how and started an investment cycle after which operational efficiency increased significantly One of the lowest valuations among regional peers at 2.8 2013 EV/EBITDA Stock story: NIS (Serbia) Current overweight 5.5% 500 550 600 650 700 750 800 850 900 950 30.06.2011 31.07.2011 31.08.2011 30.09.2011 31.10.2011 30.11.2011 31.12.2011 31.01.2012 29.02.2012 31.03.2012 30.04.2012 31.05.2012 30.06.2012 31.07.2012 31.08.2012 30.09.2012 31.10.2012 30.11.2012 31.12.2012 31.01.2013 28.02.2013 Profit taking Buy Buy Recommendation: Buy

-

Upload

citywirewebsite -

Category

Documents

-

view

314 -

download

2

Transcript of Kd skladi part 2

15

Description: Naftna industrija Srbije is a

vertically integrated oil and gas company

incorporated in Serbia.

Sector: Energy

Market Cap: €1.3bn (RSD 145bn)

Current Price: RSD 890

Upside: 23%

Strengths:

A vertically integrated oil&gas company

which is highly profitable as oil prices are

liberalised and royalty taxes are very low

Privatised in 2009 when GazpromNeft

became a majority shareholder

GPN brought industry know-how and started

an investment cycle after which operational

efficiency increased significantly

One of the lowest valuations among regional

peers at 2.8 2013 EV/EBITDA

Stock story: NIS (Serbia) Current overweight 5.5%

500

550

600

650

700

750

800

850

900

950

30.06.2011

31.07.2011

31.08.2011

30.09.2011

31.10.2011

30.11.2011

31.12.2011

31.01.2012

29.02.2012

31.03.2012

30.04.2012

31.05.2012

30.06.2012

31.07.2012

31.08.2012

30.09.2012

31.10.2012

30.11.2012

31.12.2012

31.01.2013

28.02.2013

Profit taking

Buy Buy

Recommendation: Buy

16

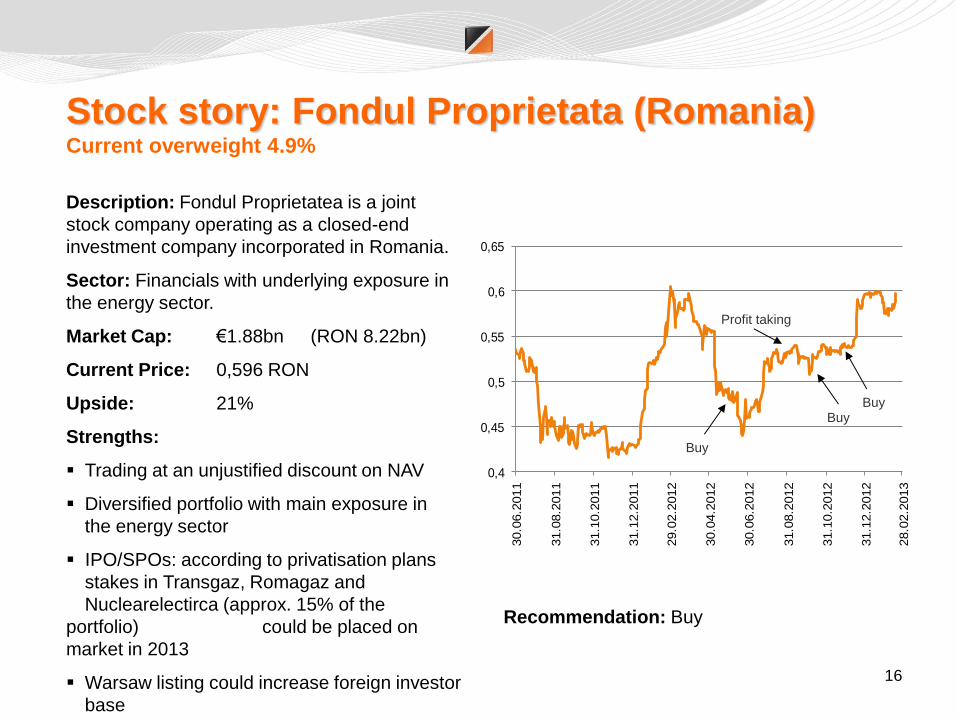

Description: Fondul Proprietatea is a joint

stock company operating as a closed-end

investment company incorporated in Romania.

Sector: Financials with underlying exposure in

the energy sector.

Market Cap: €1.88bn (RON 8.22bn)

Current Price: 0,596 RON

Upside: 21%

Strengths:

Trading at an unjustified discount on NAV

Diversified portfolio with main exposure in

the energy sector

IPO/SPOs: according to privatisation plans

stakes in Transgaz, Romagaz and

Nuclearelectirca (approx. 15% of the

portfolio) could be placed on

market in 2013

Warsaw listing could increase foreign investor

base

Recommendation: Buy

Stock story: Fondul Proprietata (Romania) Current overweight 4.9%

0,4

0,45

0,5

0,55

0,6

0,65

30.0

6.2

011

31.0

8.2

011

31.1

0.2

011

31.1

2.2

011

29.0

2.2

012

30.0

4.2

012

30.0

6.2

012

31.0

8.2

012

31.1

0.2

012

31.1

2.2

012

28.0

2.2

013

Buy

Buy

Profit taking

Buy

17

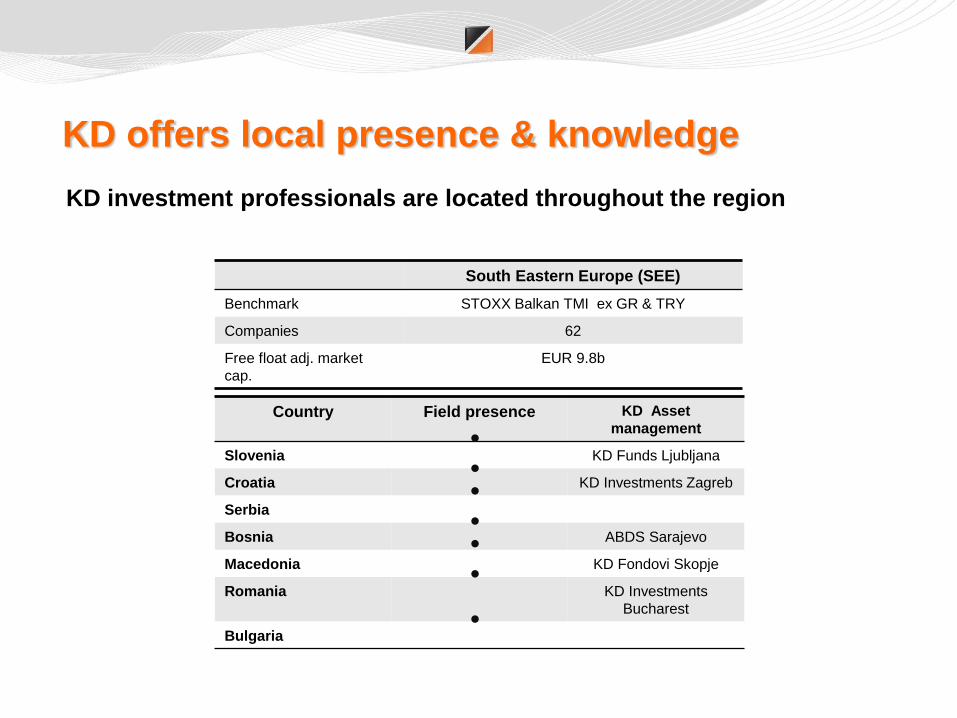

KD, the Asset Manager for the region

The privatisation process in many Balkan countries has not been finalised. Privatisation, even partial, is making companies more efficient and better managed. KD has deep experience and understanding of the way governments behave in privatisation processes

KD investment professionals have an extensive information network which is

imperative when dealing in these relationship-based markets

KD investment professionals speak the local language and understand the market

dynamics

One trigger to increase shareholder value in regional companies is to improve corporate governance and transparency. KD actively works to improve the corporate governance of the companies we own and we convey our views about specific corporate governance issues through formal and informal communication with the management of companies in which we invest

KD has extensive knowledge of the regulatory environment in each Balkan

country

KD can access tightly held/concentrated shareholdings

KD has been investing in the region for over 15 years

Appendix

Country Field presence KD Asset

management

Slovenia KD Funds Ljubljana

Croatia KD Investments Zagreb

Serbia

Bosnia ABDS Sarajevo

Macedonia KD Fondovi Skopje

Romania

KD Investments

Bucharest

Bulgaria

South Eastern Europe (SEE)

Benchmark STOXX Balkan TMI ex GR & TRY

Companies 62

Free float adj. market

cap.

EUR 9.8b

KD offers local presence & knowledge

KD investment professionals are located throughout the region

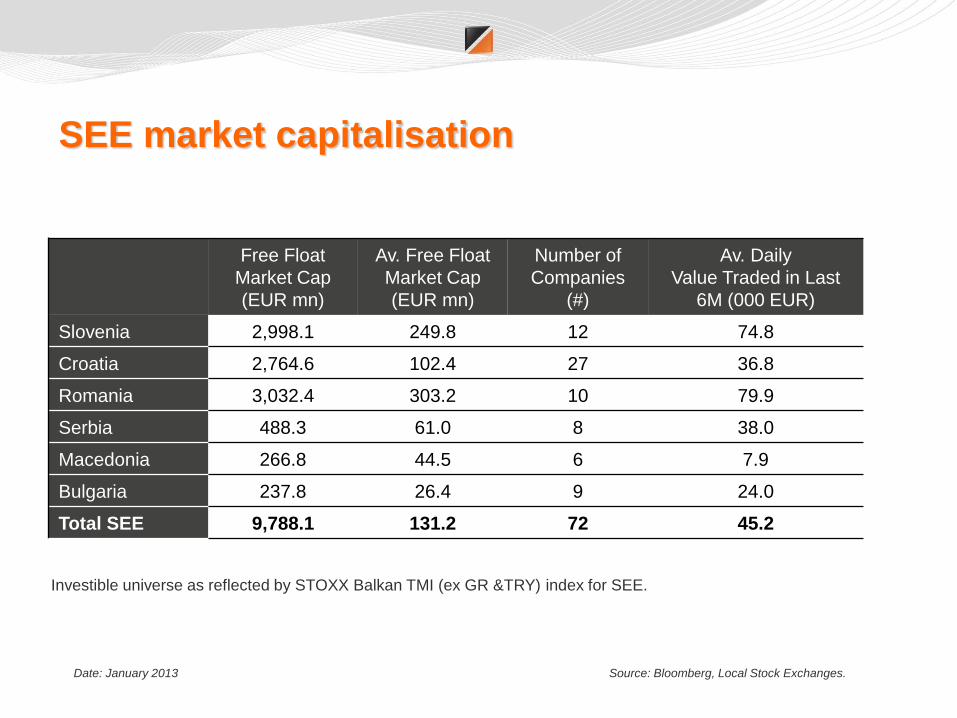

SEE market capitalisation

Free Float

Market Cap

(EUR mn)

Av. Free Float

Market Cap

(EUR mn)

Number of

Companies

(#)

Av. Daily

Value Traded in Last

6M (000 EUR)

Slovenia 2,998.1 249.8 12 74.8

Croatia 2,764.6 102.4 27 36.8

Romania 3,032.4 303.2 10 79.9

Serbia 488.3 61.0 8 38.0

Macedonia 266.8 44.5 6 7.9

Bulgaria 237.8 26.4 9 24.0

Total SEE 9,788.1 131.2 72 45.2

Source: Bloomberg, Local Stock Exchanges. Date: January 2013

Investible universe as reflected by STOXX Balkan TMI (ex GR &TRY) index for SEE.

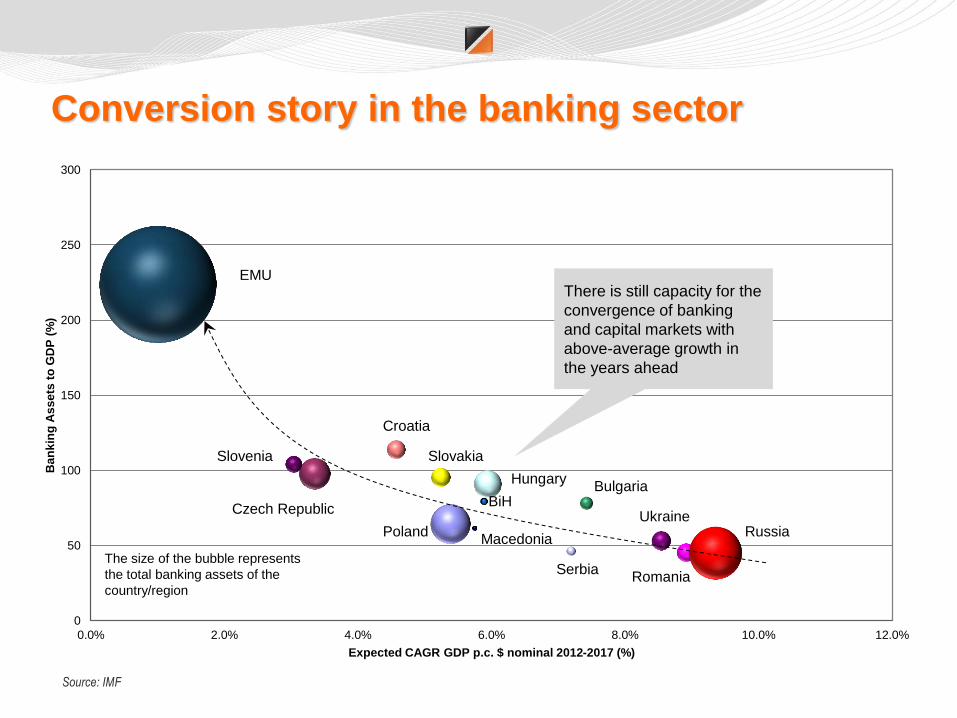

Conversion story in the banking sector

Source: IMF

0

50

100

150

200

250

300

0.0% 2.0% 4.0% 6.0% 8.0% 10.0% 12.0%

Ban

kin

g A

ss

ets

to

GD

P (

%)

Expected CAGR GDP p.c. $ nominal 2012-2017 (%)

The size of the bubble represents

the total banking assets of the

country/region

There is still capacity for the

convergence of banking

and capital markets with

above-average growth in

the years ahead

EMU

Slovenia

Czech Republic

Croatia

Slovakia

Poland

Hungary

BiH

Macedonia

Serbia

Bulgaria

Ukraine Russia

Romania

Convergence in the consumer sector suffered a

setback Slovenia looks to be at the end of convergence

0.0%

20.0%

40.0%

60.0%

80.0%

100.0%

120.0%

140.0%

160.0%

0.0% 2.0% 4.0% 6.0% 8.0% 10.0% 12.0% 14.0%

% o

f EU

per

son

al c

on

sum

pti

on

per

cap

ita

aver

age

Nominal growth in personal consumption per capita 2001 - 2011 (% CAGR)

Austria

Poland

Romania Bulgaria

Czech Rep.

Slovenia

Macedonia

Slovakia Croatia

EU 27

Hungary

Austria was a major beneficiary of

CEE and SEE convergence

Slovenia was the first SEE

country to adopt the euro and a

successful example of

convergence

Countries where the most

notable medium-term

purchasing power

convergence effect is expected

Countries where the strong

long-term effect of purchasing

power convergence is

expected

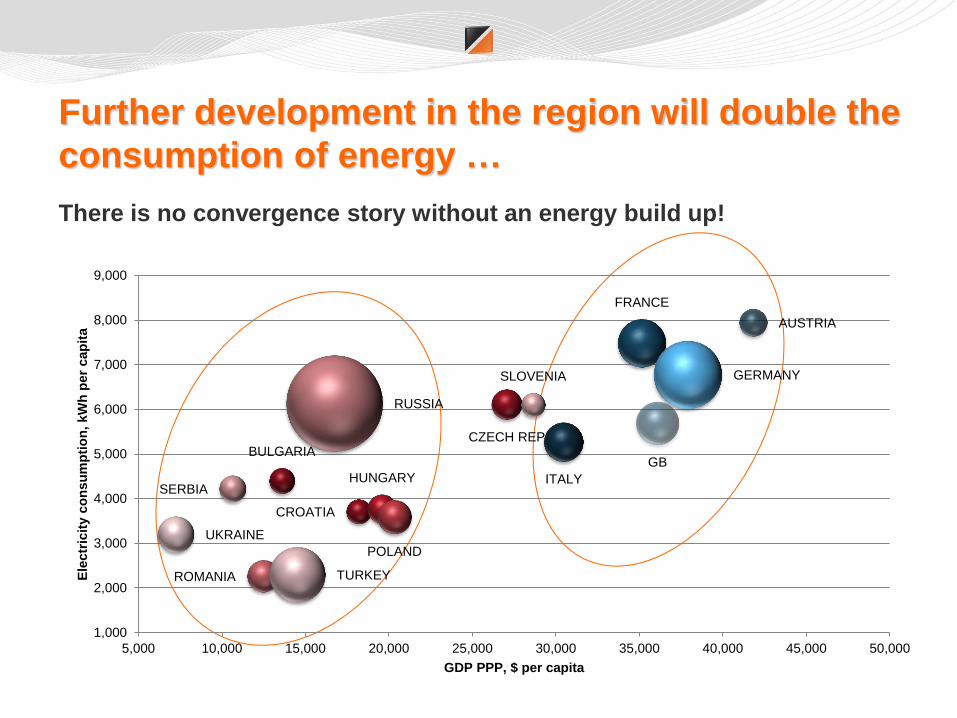

Further development in the region will double the

consumption of energy …

There is no convergence story without an energy build up!

AUSTRIA

BULGARIA

CROATIA

CZECH REP

FRANCE

GERMANY

HUNGARY ITALY

POLAND

ROMANIA

RUSSIA

SERBIA

SLOVENIA

TURKEY

UKRAINE

GB

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

5,000 10,000 15,000 20,000 25,000 30,000 35,000 40,000 45,000 50,000

Ele

ctr

icit

y c

on

su

mp

tio

n,

kW

h p

er

cap

ita

GDP PPP, $ per capita

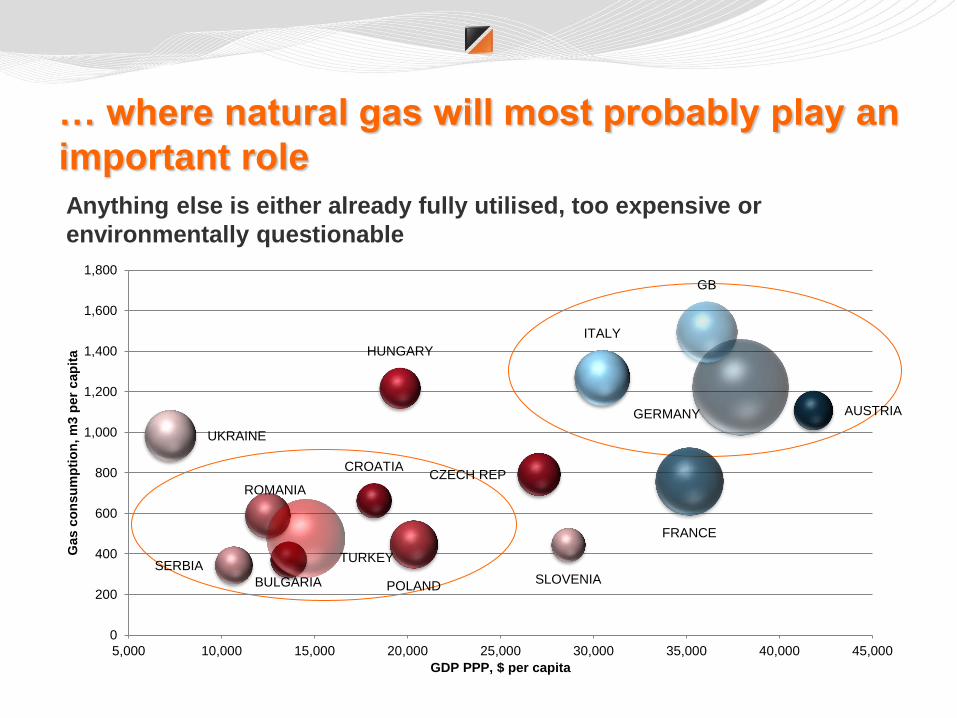

… where natural gas will most probably play an

important role

Anything else is either already fully utilised, too expensive or

environmentally questionable

AUSTRIA

BULGARIA

CROATIA CZECH REP

FRANCE

GERMANY

HUNGARY

ITALY

POLAND

ROMANIA

SERBIA SLOVENIA

TURKEY

UKRAINE

GB

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

5,000 10,000 15,000 20,000 25,000 30,000 35,000 40,000 45,000

Gas c

on

su

mp

tio

n, m

3 p

er

cap

ita

GDP PPP, $ per capita

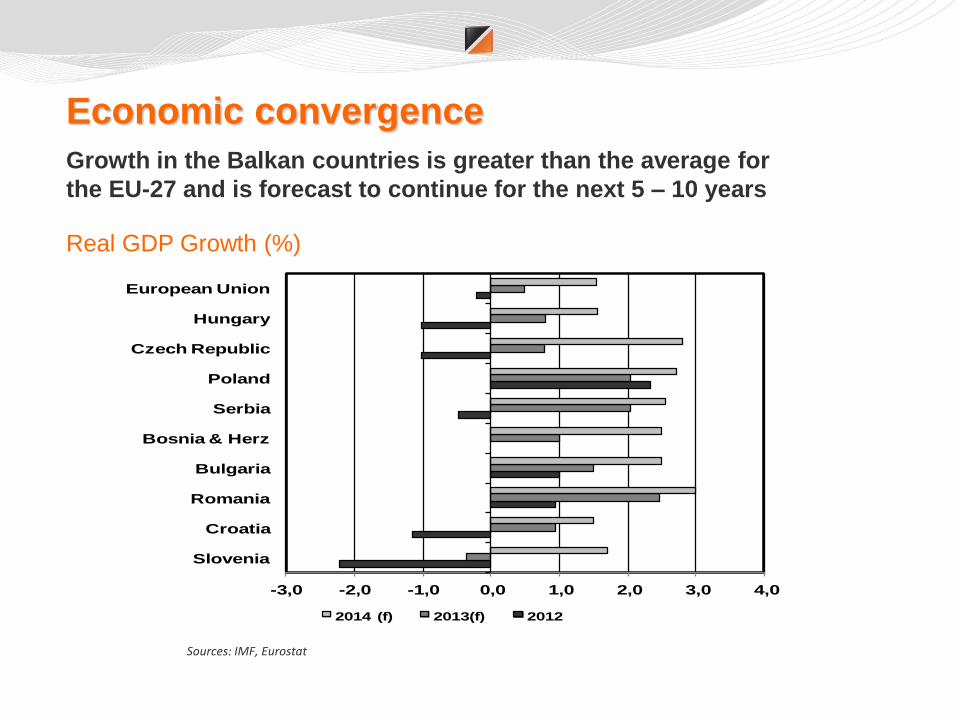

Economic convergence

Growth in the Balkan countries is greater than the average for

the EU-27 and is forecast to continue for the next 5 – 10 years

Real GDP Growth (%)

Sources: IMF, Eurostat

-3,0 -2,0 -1,0 0,0 1,0 2,0 3,0 4,0

Slovenia

Croatia

Romania

Bulgaria

Bosnia & Herz

Serbia

Poland

Czech Republic

Hungary

European Union

2014 (f) 2013(f) 2012

So there is a reason to invest

• TThe

The Balkans:

A unique journey,

millions of people

and countless

emotions

Disclaimer

This presentation is provided for information purposes only and does not constitute financial or investment advice or form part of an

offer, subscription, recommendation or solicitation to buy or sell any financial instrument, nor should it be relied on in connection

with any contract or commitment. Returns are not guaranteed and investment returns tend to fluctuate. Past performance does not

guarantee future results.

KD Funds – Management Company LLC (KD Skladi, družba za upravljanje, d. o. o.), Dunajska cesta 63, Ljubljana, Slovenia,

manages the KD Umbrella Fund and its subfunds KD Galileo, Mixed Flexible Fund; KD Rastko, Europe Equity Fund; KD Bond –

EUR; KD MM, Money Market - EUR; KD First Selection, Fund of Equity Funds; KD Balkan, Equity; KD New Markets, Equity; KD

Raw Materials and Energy, Equity; KD Technology, Equity; KD Vitality, Equity; KD India – China, Equity; KD Latin America, Equity;

KD Eastern Europe, Equity; and KD Dividend, Equity. Hard copies of the prospectus including the fund rules, the Key Investor

Information Document (KIID), and the latest published annual and semi-annual reports in the Slovenian language are available to

investors free of charge at the company's headquarters and subscription offices, and in e-format on the website www.kd-skladi.si.

KD Funds is registered in Slovenia.

![KD-R975BTS / KD-R970BTS / KD-R97MBS / KD … Size: B6L (182 mm x 128 mm) Book Size: B6L (182 mm x 128 mm) ENGLISH FRANÇAIS ESPAÑOL B5A-0813-10 [K] KD-R975BTS / KD-R970BTS / KD-R97MBS](https://static.fdocuments.in/doc/165x107/5aaf5da87f8b9a25088d67a8/kd-r975bts-kd-r970bts-kd-r97mbs-kd-size-b6l-182-mm-x-128-mm-book-size.jpg)

![KD-R981BT / KD-R889BT / KD-R881BT / KD-R784BT / KD ...Data Size: B6L (182 mm x 128 mm) Book Size: B6L (182 mm x 128 mm) ENGLISH FRANÇAIS DEUTSCH РУCCKИЙ B5A-1353-00 [E] KD-R981BT](https://static.fdocuments.in/doc/165x107/60f8a461e650da6d260a5f67/kd-r981bt-kd-r889bt-kd-r881bt-kd-r784bt-kd-data-size-b6l-182-mm-x.jpg)