KCB GROUP PLC INVESTOR PRESENTATION. · Beauty and Personal Care –945 Building and Construction...

30

KCB GROUP PLC INVESTOR PRESENTATION. FY17 FINANCIAL RESULTS JOSHUA OIGARA GROUP CEO & MD LAWRENCE KIMATHI GROUP CFO

Transcript of KCB GROUP PLC INVESTOR PRESENTATION. · Beauty and Personal Care –945 Building and Construction...

KCB GROUP PLC INVESTOR

PRESENTATION.

FY17 FINANCIAL RESULTS

JOSHUA OIGARA GROUP CEO & MD

LAWRENCE KIMATHI GROUP CFO

KCB Group at a glance

2

6,483 staff

15.7M Customers

153,431 shareholders

Market Capitalization $1.5B

Our Purpose, Values and Strategic Objectives

3

Excellence in Customer experience:

NPS target of 60%

Digital financial services / AI:

NFI contribution 40%

Excellent operations performance:

CIR 45%

Outstanding employee engagement:

85% satisfaction levelStrong shareholder value:

ROE >21%,

Growth in Youth and Women enterprises

2017 Group Awards

Re

cogn

itio

n o

f K

CB

G

rou

p:

• The Banker Awards 2017

• Bank of the Year Kenya

• Sustainable Finance Catalyst

• Best Bank in Sustainable Finance (Tier 1 Banks)

• Euro Money Awards

• Best Bank in Kenya

• Best Bank for Corporate Social Responsibility in Africa

• Africa Investor

• Best Performing Company

• Best Ai 40 CEO

4

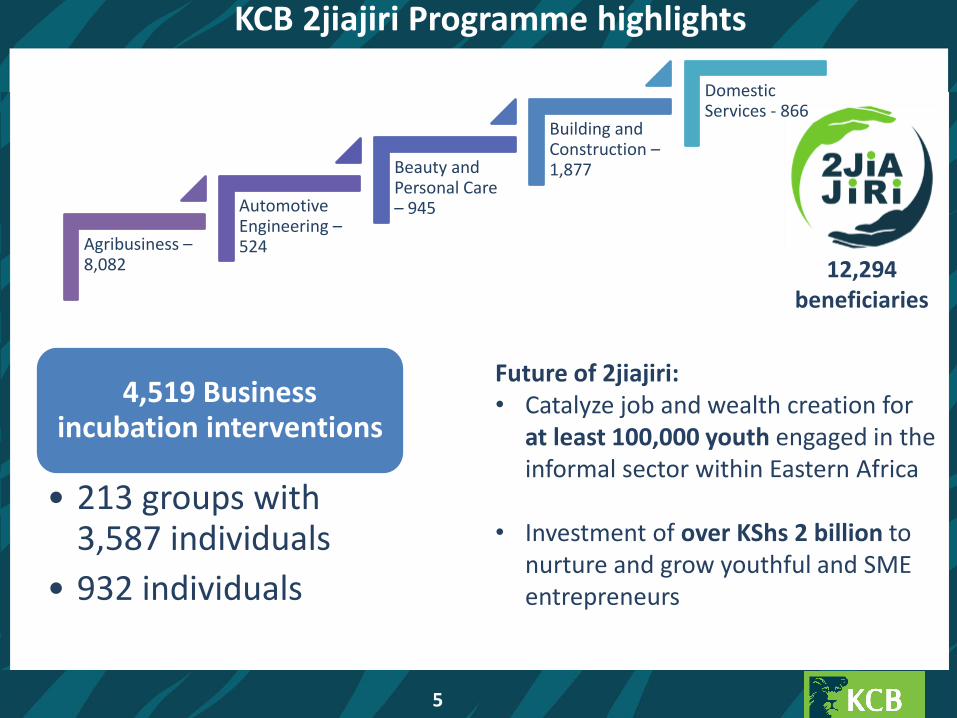

KCB 2jiajiri Programme highlights

5

12,294 beneficiaries

Agribusiness –8,082

Automotive Engineering –524

Beauty and Personal Care – 945

Building and Construction –1,877

Domestic Services - 866

4,519 Business incubation interventions

• 213 groups with 3,587 individuals

• 932 individuals

Future of 2jiajiri:• Catalyze job and wealth creation for

at least 100,000 youth engaged in the informal sector within Eastern Africa

• Investment of over KShs 2 billion to nurture and grow youthful and SMEentrepreneurs

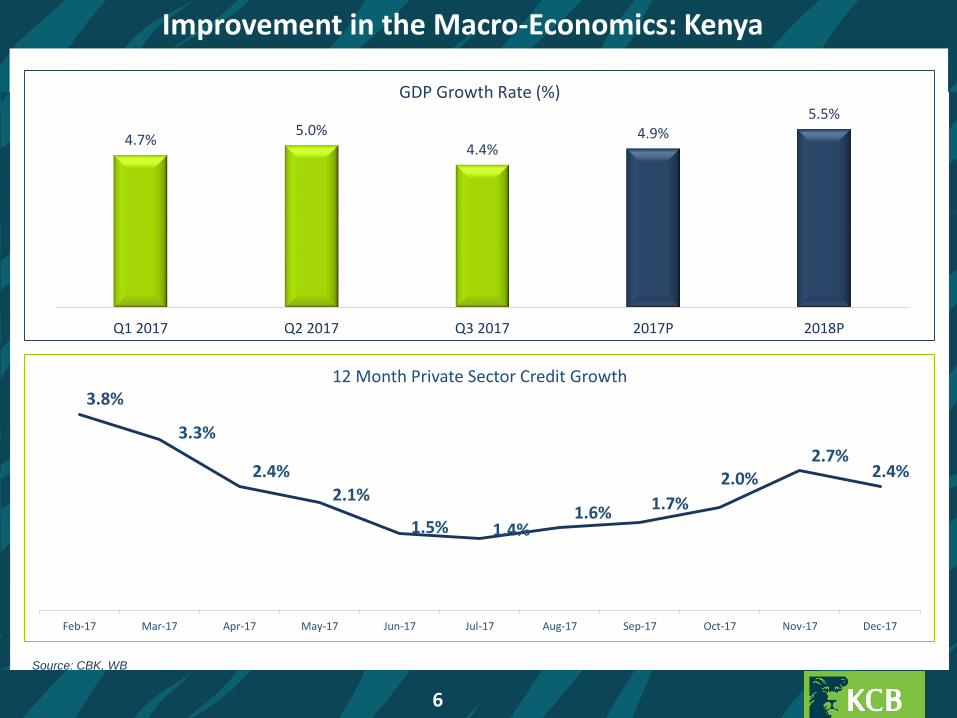

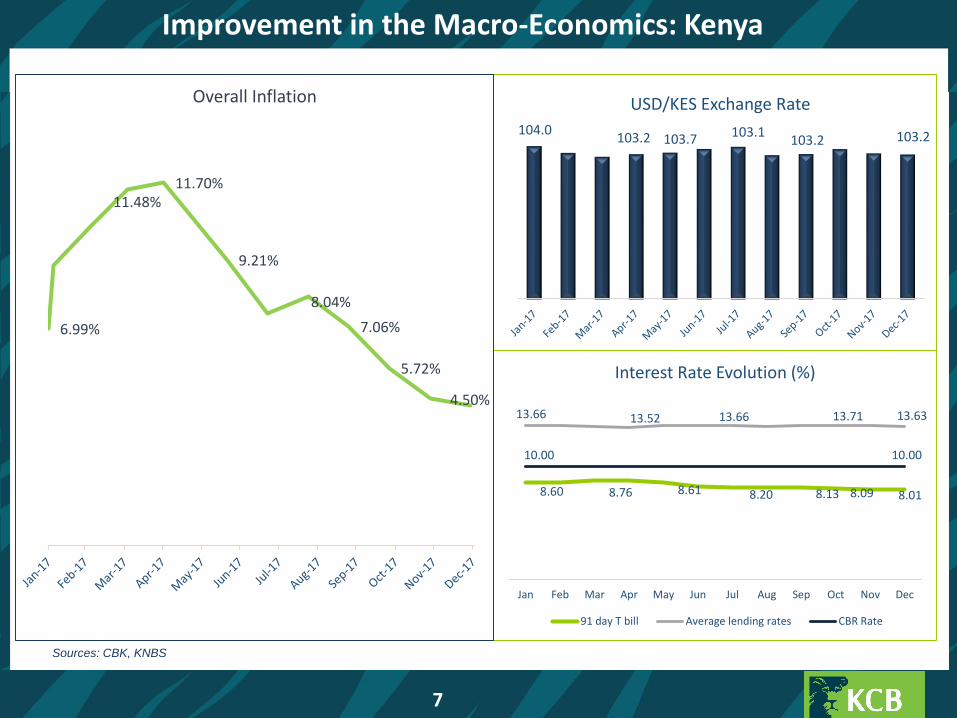

Improvement in the Macro-Economics: Kenya

6

Source: CBK, WB

4.7%5.0%

4.4%4.9%

5.5%

Q1 2017 Q2 2017 Q3 2017 2017P 2018P

GDP Growth Rate (%)

3.8%

3.3%

2.4%

2.1%

1.5% 1.4%1.6% 1.7%

2.0%2.7%

2.4%

Feb-17 Mar-17 Apr-17 May-17 Jun-17 Jul-17 Aug-17 Sep-17 Oct-17 Nov-17 Dec-17

12 Month Private Sector Credit Growth

Sources: CBK, KNBS

104.0 103.2 103.7 103.1

103.2 103.2

USD/KES Exchange Rate

8.60 8.76 8.61 8.20 8.13 8.09 8.01

13.66 13.52 13.66 13.71 13.63

10.00 10.00

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Interest Rate Evolution (%)

91 day T bill Average lending rates CBR Rate

7

6.99%

11.48%11.70%

9.21%

8.04%

7.06%

5.72%

4.50%

Overall Inflation

Improvement in the Macro-Economics: Kenya

Sources: IMF, Bloomberg

Macro-Economic Highlights: Regional

4.9

7.07.0

(3.7)

10.3

5.4

7.0 6.9

(7.1)

9.6

4.4

6.86.0

0.5

5.44.4

6.5 6.2

0.1

8.5

Uganda Tanzania Rwanda Burundi Ethiopia

GDP (%)

2014 2015 2016 2017

13.6%11.8%

4.4%

9.8%

3.0%

9.2%

20.0%

6.0%

8.8%7.0%7.1%

14.0%

9.0%

15.0%

3.8%

8.6%6.4%

4.0%

15.0%

Tanzania Uganda Rwanda Burundi South Sudan

91 Day T-Bills

2014 2015 2016 2017

6.1%

3.1%

1.8%

7.9% 8.1%

5.4% 5.8%

7.1%

18.0%

8.1%

Tanzania Uganda Rwanda Burundi Ethiopia

Inflation

2014 2015 2016 2017

1.7%

52.8%

480.0%

182.2%

South Sudan

8

2,186

3,484

785.6

1,629

22.40 44.3

2,207

3,491

827.9

1,643

27.58 111.4

Tanzania Uganda Rwanda Burundi Ethiopia South Sudan

Exchange rates to USD

2016 2017

9

87% of Transactions outside the Branch

Source: KCB data

Mobile, 53%Branch Teller, 23%

ATMs, 13%

Agency & POS, 11%

2016

Mobile57%Branch

Teller13%

ATMs10%

Agency & POS20%

2017

10

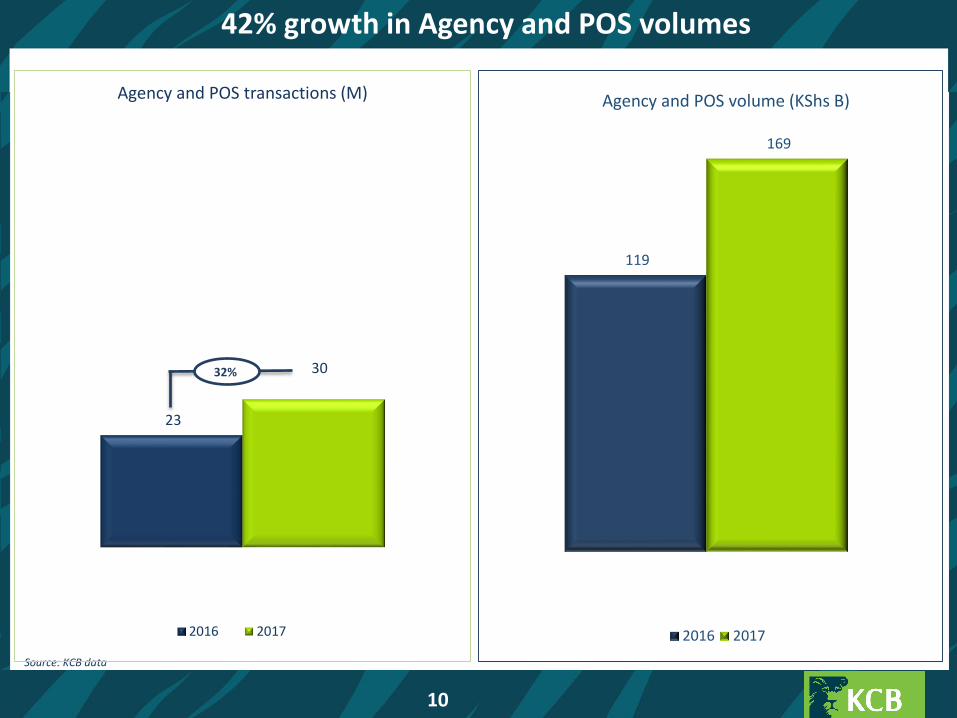

42% growth in Agency and POS volumes

Source: KCB data

23

30

Agency and POS transactions (M)

2016 2017

119

169

Agency and POS volume (KShs B)

2016 2017

32%

11

Marginal change in ATM volumes

Source: KCB data

14 15

ATMs

ATM transactions (M)

2016 2017

153 152

ATMs

ATM volume (KShs B)

2016 2017

Source: KCB data

Sustained Growth on Mobile

14.1

29.6

2016 2017

Mobile Loan Disbursement (KShs B)

12

6.5

17

53.1

88.8

2016 2017

Mobile transactions (M)

KCB App Total transactions

67%

Source: KCB data

Over 500% growth on the KCB App

13

1.43

8.72

0.81

3.34

-

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00

-

1.00

2.00

3.00

4.00

5.00

6.00

7.00

8.00

9.00

10.00

2016 2017

KCB Mobile App Volumes

Value Transacted (B) Transaction No. (M)

35

1,2

59

76

3,0

84

11,289.96

25,243.46

-

5,000.00

10,000.00

15,000.00

20,000.00

25,000.00

30,000.00

-

100,000

200,000

300,000

400,000

500,000

600,000

700,000

800,000

900,000

2016 2017

Customer Utilization

Total Downloads Av value per customer

117%

124%

% ∆

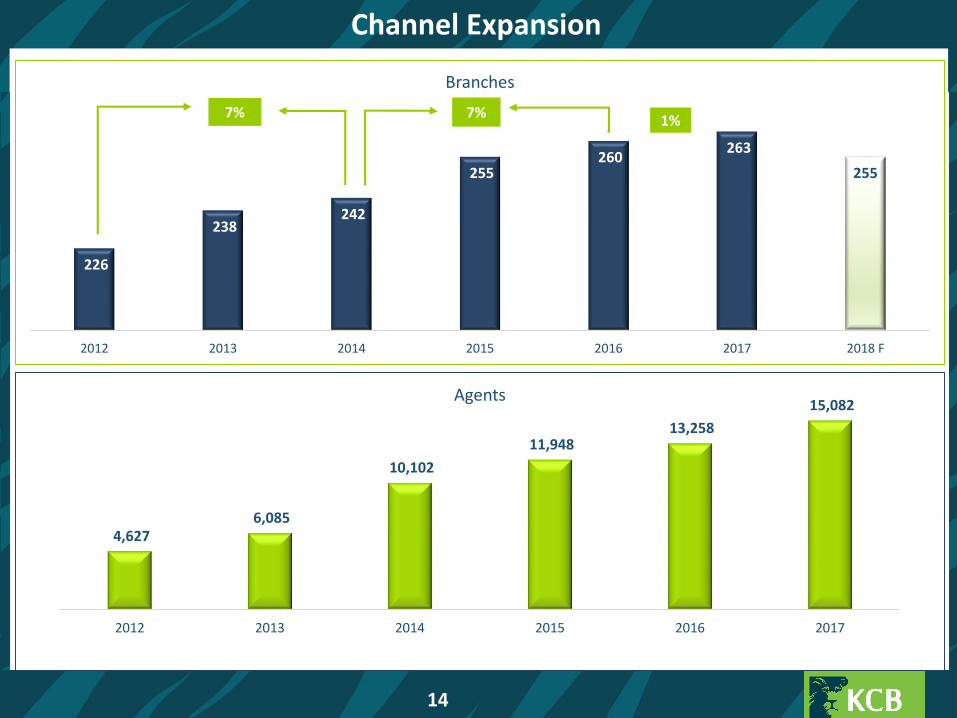

Channel Expansion

14

226

238 242

255 260

263

255

2012 2013 2014 2015 2016 2017 2018 F

Branches

7%1%

7%

4,627 6,085

10,102

11,948 13,258

15,082

2012 2013 2014 2015 2016 2017

Agents

2017 Staff Rationalization programme

15

Average age: 45 years

Staff Released: 316

35% 65%

249

67

KCB Bank Kenya KCB Subsidiaries

Distribution

0.186

2.016

2016 2017

Total Spend (Kshs B)

The key drivers of the programme

• Right sizing of the company’s resource requirements

• Alignment to advancements and changes of technology and todays’ business operating models

OUR PERFORMANCE TO DATE

Group Asset Portfolio up

9%

KShs: 647B

Net Loans and advances

up 10%

KShs: 423B Investment in Govt.

Securities up 7%

KShs: 110B

Cash and Balances with Central Bank

and other Financial

Institutions

0%

KShs:73BFixed and

other Assets up 21%

KShs: 41B

KCB Bank Kenya Asset Portfolio up

10%

KShs: 556B

Net Loans and advances

up 10%

KShs: 388B Investment in Govt.

Securities up 4%

KShs: 95B

Cash and Balances with Central Bank

and other Financial

Institutions up 21%

KShs:39BFixed and

other Assets up 23%

KShs: 34B

9% Total Assets growth driven by Net Loans & Advances

17

KCB Group KCB Bank Kenya

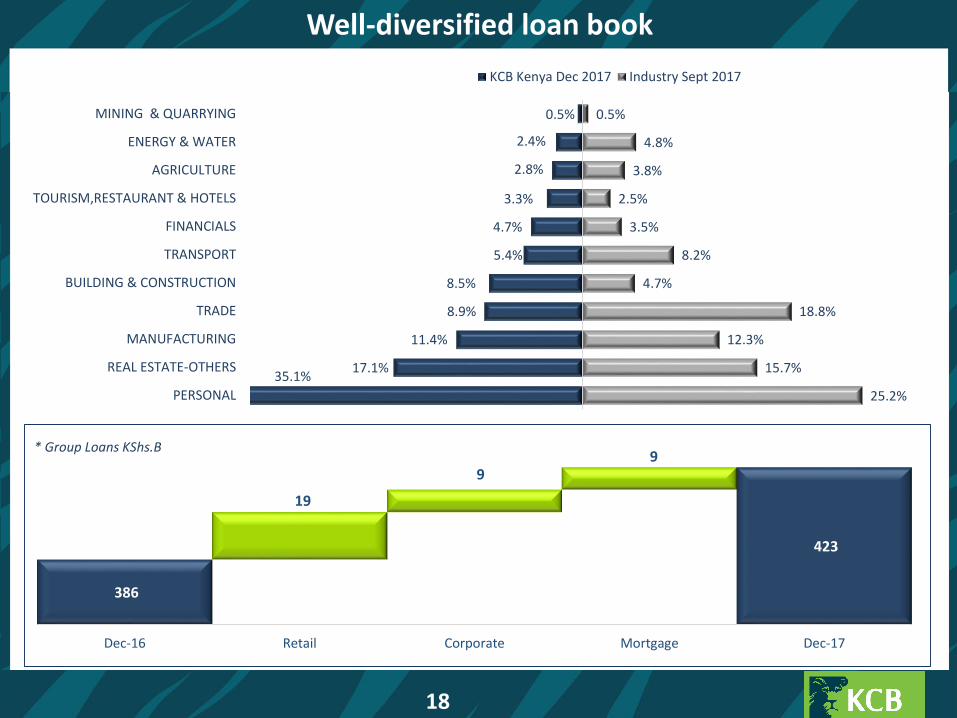

Well-diversified loan book

18

386

423

19

9 9

Dec-16 Retail Corporate Mortgage Dec-17

* Group Loans KShs.B

35.1%17.1%

11.4%

8.9%

8.5%

5.4%

4.7%

3.3%

2.8%

2.4%

0.5%

25.2%

15.7%

12.3%

18.8%

4.7%

8.2%

3.5%

2.5%

3.8%

4.8%

0.5%

PERSONAL

REAL ESTATE-OTHERS

MANUFACTURING

TRADE

BUILDING & CONSTRUCTION

TRANSPORT

FINANCIALS

TOURISM,RESTAURANT & HOTELS

AGRICULTURE

ENERGY & WATER

MINING & QUARRYING

KCB Kenya Dec 2017 Industry Sept 2017

2017 NPL Movement

19

1.0% 1.0% 1.0%1.5%

7.9% 7.9% 8.0%8.5%

Q1 2017 Q2 2017 Q3 2017 2017

CoR NPL Group

3.7%

6.2%

10.4%

13.1%

3.6%

6.5%

10.4%

12.3%

3.2%

7.3%

10.4%

15.5%

3.3%

7.8%

11.0%

16.4%

CHECK OFF MORTGAGE CORPORATE SME & MICRO

Q1 2017 Q2 2017 Q3 2017 Q4 2017

Steady Coverage Position

20

43.6%

48.7%

69.5%

74.4%

2016 2017

IFRS CBK

2017 industry position as at September

37.70%

34.5%

2016 2017

INDUSTRY

GroupLiabilities and Equity up 9%

KShs: 647B

Deposits up 11%

KShs: 500BBalances to banks and Debt down

28%

KShs: 26B

Equity up 10%

KShs:106B

Other Liabilities up

6%

KShs: 15B

KCB Bank Kenya

Liabilities and Equity up

10%

KShs: 556B

Deposits up 14%

KShs: 440BBalances to banks and Debt down

40%

KShs: 16B

Equity up 10%

KShs:89B

Other Liabilities down 3%

KShs: 11B

79% of Funding from Deposits

21

KCB Group KCB Bank Kenya

Well-funded and Diverse Portfolio

Deposits by Type FY 16

65%5%

24%

6%

Demand Savings Term Call

65%4%

26%

5%

Deposits by Type FY 17

42% 50% 51%

55% 47% 46%

2% 3% 3%

2015 2016 2017

Corporate Retail Other

22

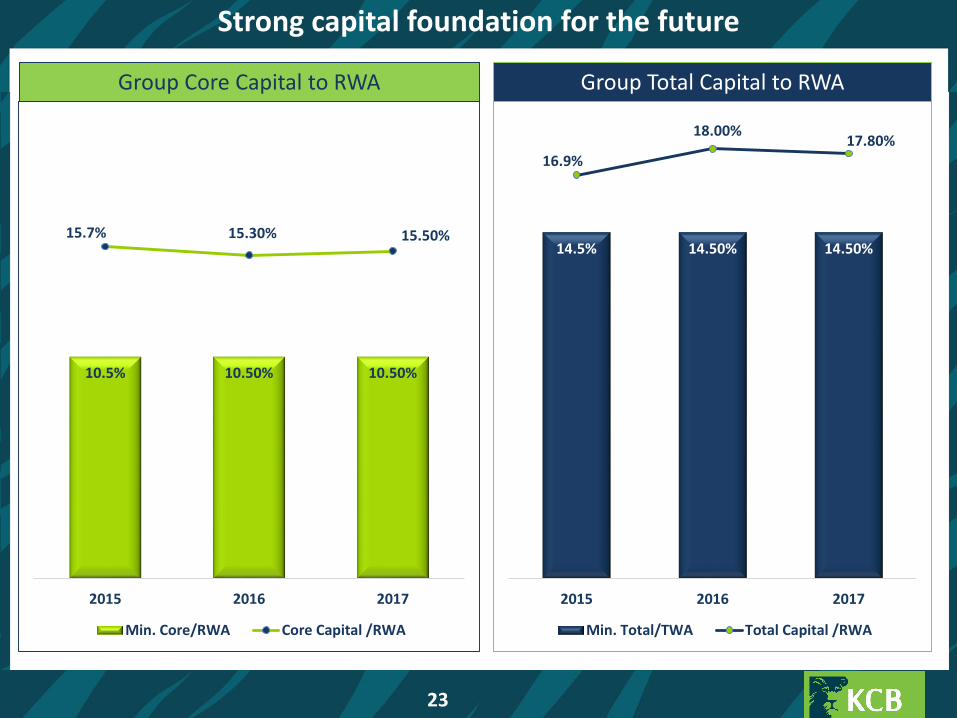

Strong capital foundation for the future

Group Core Capital to RWA Group Total Capital to RWA

10.5% 10.50% 10.50%

15.7% 15.30% 15.50%

2015 2016 2017

Min. Core/RWA Core Capital /RWA

14.5% 14.50% 14.50%

16.9%

18.00%17.80%

2015 2016 2017

Min. Total/TWA Total Capital /RWA

23

Resolute strategy delivers 9% balance sheet growth

KShs Billions

KCB Group KCB Bank Kenya

Actual 2016

Actual2017

Y-O-Y Change

Actual 2016

Actual2017

Y-O-Y Change

Cash and balances with central bank 29.4 29.1 (1%) 26.1 26.0 (1%)

Balances with other institutions 43.7 43.9 0% 6.1 13.1 115%

Investments in Government & Other securities

102.5 110.0 7% 91.0 94.6 4%

Net loans and advances 385.7 422.7 10% 353.9 387.9 10%

Fixed assets 12.7 14.0 10% 9.2 9.5 3%

Other assets 21.2 27.1 28% 18.4 24.5 33%

Total Assets 595.2 646.7 9% 504.8 555.6 10%

Customer Deposits 448.2 499.5 11% 386.6 440.2 14%

Balances due to other banks 13.1 11.0 (16%) 5.6 5.2 (7%)

Other liabilities 14.4 15.2 6% 11.0 10.7 (3%)

Long-term debt 23.0 14.9 (35%) 20.6 10.6 (49%)

Total Liabilities 498.7 540.7 8% 423.8 466.6 10%

Shareholders’ Equity 96.6 106.0 10% 81.0 89.0 10%

Total Liabilities and Equity 595.2 646.7 9% 504.8 555.6 10%

24

Stable profitability despite interest rate pressure

KShs Billions

KCB Group KCB Bank Kenya

Actual 2016

Actual2017

Y-O-Y Change

Actual 2016

Actual2017

Y-O-Y Change

Interest Income 62.8 63.7 1% 56.2 56.9 1%

Interest Expense (15.8) (15.3) (3%) (13.3) (12.8) (3%)

Net interest income 47.0 48.4 3% 42.9 44.1 3%

Foreign exchange income 5.5 4.7 (15%) 2.2 2.9 33%

Net fees and commissions 12.6 14.7 16% 9.1 10.7 18%

Other income 4.3 3.6 (16%) 4.0 3.3 (18%)

Total other operating income 22.5 23.0 2% 15.3 16.9 11%

Total other operating expenses (32.9) (34.9) (6%) (25.9) (28.6) (9%)

Net provisions for bad debts (3.8) (5.9) 55% (3.8) (5.0) 32%

Profit Before Loss on Monetary Position

32.7 30.5 (7%) 28.5 27.5 (4%)

Loss on Monetary Position (3.6) (1.4) (61%) 0.0 0.0 -

Profit before tax 29.1 29.1 0% 28.5 27.5 (4%)

Tax (9.4) (9.4) 0% (8.7) (8.2) (5%)

Profit after tax 19.7 19.7 0% 19.8 19.2 (3%)

25

Income Distribution

83%82% 80%

16%

17% 19%1%

1% 1%

2015 2016 2017

Interest Income & Growth

Loans and advances Govt. Securities Placements & Money Markets

% ∆

26

47%42%

46%

13%

14%

18%

17%24%

20%

22%19%

16%

2015 2016 2017

NFI Mix & Growth

Fees and Commission Lending Fees Fx Income Other Income

14%

-

(18%)

(15%)

29%

13%

% ∆

Overview of Key Financial Ratios

Return on Average Equity

Cost to Income*

Gross NPL to Gross Loans

NPL Coverage

Debt to Equity

Non funded income to total income

Cost of funds

Net Interest Margin

Cost of risk

Loan to Deposit Ratio

Growth of Net Loans and Advances

Growth of Customer Deposits

23.6% 20.1%

47.4% 51.9%

7.8% 8.0%

84.6% 85.6%

14.5% 14.0%

28.3% 32.9%

2.8% 2.9%

9.2% 9.1%

0.9% 1.0%

90.7% 87.4%

19% 15%

16% 16%

19.5%

46.2%

8.5%

74.4%

14.0%

32.2%

3.0%

8.9%

1.5%

85.1%

10%

11%

Q1 17 Q217 Q3 17 KENYA GROUP

20.3%

52.5%

7.9%

79.6%

23.3%

35.0%

3.1%

7.9%

1.0%

86.6%

14%

8%

22.6%

46.8%

8.5%

75.9%

11.9%

27.7%

2.9%

9.1%

1.4%

88.7%

10%

14%

27

*excluding one off restructuring costs

2017 Dividend

28

KCB Group paid an interim dividend in October 2017 of KShs. 1.00 per share.

At the AGM to be held on 27 April 2018, at SafaricomKasarani Indoor Stadium, we shall propose a final dividend of KShs. 2.00 per share.

Based on the 2017 performance of the Group, the proposed dividend is maintained at the same payout level as 2016.

Taking into consideration business performance during the current year, the Group anticipates it shall be able to pay an interim dividend to shareholders.

Outlook 2018

Return on Average Equity

Cost to Income Ratio*

Gross NPL to Gross Loans

Non funded income ratio

Cost of Funds

Net Interest Margin

Cost of Risk

Cost of Funds

Customer Deposit Growth

2018

21.1%

46.0%

3.3%

8.7%

3.3%

7.0%

30.9%

1.3%

11%

29

Strategic Initiatives:

• Excellence in Customer experience: NPS 60%

• Digital financial services / AI: NFI 40%

• Strong shareholder value: ROE >21%

• Growth in Youth and Women enterprises

• Excellent operations performance: CIR 45%

• Outstanding employee engagement: 85% satisfaction level

Net Loans Growth 8%

Targets:

• Continue to improve efficiency

• Increase shareholder value

• Manage asset quality

• Full digital transformation

• Relentless drive for excellence in customer experience

*excluding one off restructuring costs