Kathuria Rajat

40

Rajat Kathur ia Leased Line Prices in India and Indonesia Comparing the Impact of Decline in Leased Line Prices in India and Indonesia: Lessons for Latin America Prof. Rajat Kathuria ICRIER [email protected] Abstract Telecommunications provide access and backbone services which affect efficiency and growth across a wide range of industries. The quality and price of such key services shape overall economic performance, as they affect the capacity of businesses to compete in foreign and domestic markets. Reflecting the rapid pace of innovation in information and communications t echnologies (IT!, competitive market forces are becoming increasingly important in the provision of t elecommunication and networking services, definitely moving the secto r away from the "" natur al monopo ly# # market model ($or ld %ank, &''&!. Inte rnatio nal evidence suggests that market openness in telecommunications services and the quality of the regulatory regime are drivers of IT sector development ()*, &'''!. This study attempts to assess the impact of declin e of leased line prices in Indones ia. It tries to capture this impact thro ugh qualitat ive as well as quantitative impacts. +ince the decline in prices occurred recently, the period post the decline is not large enough to do a meaningful time ser ies analysis. -owever, qualitative ass essment is made and the impact is compared with India, where decline in leased line pr ices led to substantial be nefits to user industries. f particular significance is the trigger to the price decline in Indonesia. The process was set in moti on by a presentation of research results by IR/)asia in 0akarta in ctober &''1 and culminated with the incumb ent operator 2T Te lkom and others repor ting a 34567 per cent reduc tion in lease d line prices in 8pril &''6 & . 8nne9 I provides a chronology of the sequenc e and section : in the paper draws interesting comparisons with a similar process in India. Keywords: I. IMPACT OF TELECOM ON ECONOMIC DEVELOPMENT %efore dealing with the specific situation in Indonesia it will be useful to briefly e9amine why modern telecommunications is so important for economic development. ;ost studies by economists conclude that a modern telecommunications infrastructure has a substantial impact on economic growth. %ased on samples 1 Press release of No. 32/DJPT1/KOMINFO/ 4/2008 showing e!line in "he "ariff of Ne"wor# $en" "owars "he e!line in "he "ariff of In"erne" %!! ess in Inonesia & a!!esse a" h""'(//www .'os"el.go.i /)'a"e/i/*a!a+info. as',i+info-4 & Op cit

Transcript of Kathuria Rajat

8/11/2019 Kathuria Rajat

http://slidepdf.com/reader/full/kathuria-rajat 1/40

Rajat Kathuria Leased Line Prices in India and Indonesia

Comparing the Impact of Decline in Leased Line Prices

in India and Indonesia: Lessons for Latin America

Prof. Rajat Kathuria

ICRIER

Abstract

Telecommunications provide access and backbone services which affect efficiency and growth across awide range of industries. The quality and price of such key services shape overall economic performance,as they affect the capacity of businesses to compete in foreign and domestic markets. Reflecting the rapid pace of innovation in information and communications technologies (IT!, competitive market forces are becoming increasingly important in the provision of telecommunication and networking services, definitelymoving the sector away from the ""natural monopoly## market model ($orld %ank, &''&!. Internationalevidence suggests that market openness in telecommunications services and the quality of the regulatoryregime are drivers of IT sector development ()*, &'''!. This study attempts to assess the impact of decline of leased line prices in Indonesia. It tries to capture this impact through qualitative as well asquantitative impacts. +ince the decline in prices occurred recently, the period post the decline is not largeenough to do a meaningful time series analysis. -owever, qualitative assessment is made and the impact iscompared with India, where decline in leased line prices led to substantial benefits to user industries. f particular significance is the trigger to the price decline in Indonesia. The process was set in motion by a presentation of research results by IR/)asia in 0akarta in ctober &''1 and culminated with theincumbent operator 2T Telkom and others reporting a 34567 per cent reduction in leased line prices in8pril &''6&. 8nne9 I provides a chronology of the sequence and section : in the paper draws interestingcomparisons with a similar process in India.

Keywords:

I. IMPACT OF TELECOM ON ECONOMIC DEVELOPMENT

%efore dealing with the specific situation in Indonesia it will be useful to briefly e9amine why moderntelecommunications is so important for economic development. ;ost studies by economists conclude that amodern telecommunications infrastructure has a substantial impact on economic growth. %ased on samples

1 Press release of No. 32/DJPT1/KOMINFO/4/2008 showing e!line in "he "ariff of Ne"wor# $en""owars "he e!line in "he "ariff of In"erne" %!!ess in Inonesia & a!!esse a"h""'(//www.'os"el.go.i/)'a"e/i/*a!a+info.as',i+info-4

& Op cit

8/11/2019 Kathuria Rajat

http://slidepdf.com/reader/full/kathuria-rajat 2/40

of :< and &: countries, /orton (44&! concludes that in economic development ""a telecommunicationsinfrastructure must be viewed as at least as important as conventional economic forces such as stablemoney growth, low inflation and an open economy.## Roller and $averman (&''! found that one5third of the economic growth in a group of & )* countries over the &'5year period 4<'=44' could beattributed to the direct and indirect impact of the telecommunications sector. 0ames %urnham has studiedthe ama>ing economic transformation of Ireland in the 44's, which owed much of its momentum to timelyinvestment in a modern telecommunications system (&''7!. The background note of the $T +ecretariatdescribes telecommunications as essential to the facilitation of international trade, economic developmentand the enrichment of citi>en#s life#s ($T446!. Innovation in telecom has also been linked to growth inelectronic commerce and increased accessibility of telecom services are accepted as the foundation of successful national and global society initiatives and the social benefits these initiatives will bestow. 8ndfinally, ?aroudakis, et. al demonstrate that improving the quality and lowering the cost of telecommunications services holds a key role in improving overall economic performance, especially indeveloping countries as a result of

• %etter and low5cost telecom services bolster internal efficiency, competitiveness and

strengthen the links of developing economies with global markets.

• ;ore competitive telecom markets improve the investment climate, and greatly enhance the

attractiveness of liberali>ing countries to A*I.

• 8 low access cost and high5quality telecommunications infrastructure also facilitates the

diffusion of the internet and IT applications. 8nd the spread of the internet holds great promise in helping developing countries catch up more rapidly with the e9panding pool ofglobal knowledge

• *eveloping countries may also be able to successfully position themselves in the global IT

market by nurturing competitive advantage in specific nichesBas suggested, for e9ample, bythe booming e9ports of IT business services and software in countries like India, Israel and;alaysia.

It is well known that telecommunications can create direct as well as indirect benefits. *irect benefitsinclude revenue and employment generation. 8s with any other form of development, the presence andgrowth of industries producing telecommunications goods and services is clearly important to the growth of real C*2. Crowth results in Dobs and revenue. The si>e of the benefits will of course depend upon thecontribution of the sector to C*2 and the speed of sector growth. 8n important indirect benefit throughthe use of telecom user services is the (impact! increase in productivity. Induced changes result in economicgrowth and an increase in productivity for businesses and individuals.

8t a firm level, it would seem that large firms can afford to invest in telecom infrastructure, but it is alsoreasonable to assume that such investment would improve efficiency, reduce cost and increase si>e. This ishowever an empirical question and would therefore require more micro level indicators and data tounderstand the underlying factors. The issue is that telecom infrastructure such as leased circuits are"enabling# or general purpose technologies which implies that their use is ubiquitous yet difficult tomeasure because they are dominantly indirect. In addition it has been argued that it is not Dust deploymentof infrastructure or technology that matter, but how the technology is used to transform organi>ations, processes and behavior that is important (0ohn ?an Reenen et al. &''1!. The push to liberali>e leasedcircuits in the early days of the C8T+ negotiations was based on the conviction that maDor benefits could begenerated through competitive provision of telecommunications infrastructure, especially leased circuits.

These benefits included economic and social and are summari>ed in Aigure below.

Figure 1: Spill!er be"e#its # e$pa"%i"g telecmmu"icati"s ser!ices a"% "et&r's

&

8/11/2019 Kathuria Rajat

http://slidepdf.com/reader/full/kathuria-rajat 3/40

Source: Positive network effects of expanding telecommunications services and networks: economic

opportunity growth and social !enefits accessed at

http:""www#wto#org"english"tratop$e"serv$e"telecom$e"sym$fe!%&$e"sym$fe!%&$e#htm

$hile the government of Indonesia has frequently declared the importance of developing the country#stelecommunications sector, typically in statements by the ;inistry of ommunications and Information(;oI!, the actual priority given to this effort is questionable. 8s will be shown in this paper, many policydecisions have had the effect of limiting competition thereby restricting the possibility of e9ploiting thesector as an engine for economic growth. The study offers an assessment of this unreali>ed potential, andreviews the scope for medium term telecom sector growth. It also offers some estimates of the likely impactof telecommunications liberali>ation on user sectors and on broader economic performance. +ection & givesan overview of the telecom sector in Indonesia, including the changes that have recently occurred in thesector. +ections 7 and : focus on the leased circuit market in Indonesia and India respectively andcompares the two markets especially with regard to pace and sequencing of "liberali>ation# in this category.+ection 1 e9amines the empirical linkages between the market for leased circuits and certain user groupsand estimates the unreali>ed growth potential. +ection 3 evaluates the benefits from inDecting morecompetition into the market. +ection < offers some lessons for atin 8merican telecommunications markets

based on the results for India and Indonesia while +ection 6 concludes and draws the policy implications of the analysis.

II. INDONESIA(S TELECOMM)NICATIONS MA*+ET

Entil &''', telecommunications services in Indonesia were provided by a succession of state ownedenterprises reflecting, in part, the natural monopoly characteristics of the service. In part it also reflected thegovernment#s reluctance to involve private participation fully in a sector that provided it with control andcash. It is also possible that complete appreciation of the benefits of competition had not been understood.Thus, since early 46's, the telecom sector was dominated by two state owned operators, 2T Indosat, thee9clusive provider of international services and 2T 2erumtel which operated fi9ed local and long distanceservices. In 44, the latter was partially privati>ed and reconstituted as 2T Telkom. The governmentcreated 2T +atelindo in 447 to be the second provider of international service. -owever, competition was

limited since 2T Indosat owned <.1 percent of its shares and 2T Telkom &1 percent. Aurthermore, 2T+atelindo and 2T Indosat were required to charge identical tariffs for international service (Coswami,&''3,!. In 44:, 2T +atelindo and 2T Telkomsel were granted a C+; license. )9celcomindo, a companythat the government did not hold shares in, was also given a mobile license in 443.

The financial crisis of 44< provided the impetus to reform the sector. The overall programme of telecomsector deregulation was closely linked to the national economic recovery programme supported by the I;A.The telecom reform policy, contained in the ;oIs "%lueprint# dated 0uly &', 444 sought to

• Increase the sector performance in the era of globali>ation

7

8/11/2019 Kathuria Rajat

http://slidepdf.com/reader/full/kathuria-rajat 4/40

• iberalise the sector with a competitive structure by removing monopolistic controls

• Increase transparency and predictability of the regulatory framework

• reate opportunities for national telecommunications operators to form strategic alliances with

foreign partners

• reate business opportunities for small and medium enterprises

• Aacilitate new Dob opportunities7.

Recent regulatory reforms in Indonesia have their basis in the Telecommunications aw /o. 73 of 444.The law provides key guidelines for industry reforms, including industry liberali>ation, facilitation of newentrants and enhanced transparency and competition (2T Telkom, 8nnual Report &''3, submitted to +),E+8!. Ender the Indonesian regulatory framework, the Telecommunications aw only outlines substantive principles of the subDect matter. *etailed implementation of the law is done, interestingly, by Covernmentregulations, ministerial decrees and decrees of the *C2T. The "independent# regulatory 8uthority(Indonesian Telecommunications Regulatory %ody, %RTI! created on 0uly , &''7, has been given only anadvisory role and is dependent on *C2T for budgetary support, resulting in a confusing, multilayeredregulatory structure, not conducive to efficient decision making. %y the governments own admission Ftodate, it G%RTIH has been largely inactive and the ;inistry of ommunication and Information has beenmore effective in pushing through sector reforms# (Indonesian Trade 2olicy Review &''<, $T!. 2art of the reason for the unreali>ed potential of telecom in Indonesia must squarely be attributed to the confusing

and multilayered regulatory structure. This is discussed later in +ection 1.

The telecommunications law classifies telecommunications providers into three categories (%RTI, &'':!

. Telecommunications /etwork 2roviders&. Telecommunications +ervices 2roviders and7. +pecial Telecommunications providers

Telecommunications /etwork 2roviders are the only ones allowed to put up infrastructure. $ith a /etwork 2rovider license, it is possible to provide services for(a! Ai9ed /etwork local, long distance, international, and closed user network (b! ;obile /etwork terrestrial, cellular, and satellite

8s will be argued later the institutional framework does not promote network development. )9cept mobiletelephony, competition is less than adequate in other segments, including in network roll out anddevelopment creating a situation of substantial unreali>ed benefits. This seems surprising since Indonesiais a late starter in telecommunications reform and therefore had the benefit of both technology and policyoptions to introduce pro competitive regulation in the sector drawing from the e9perience of alreadysuccessful markets.

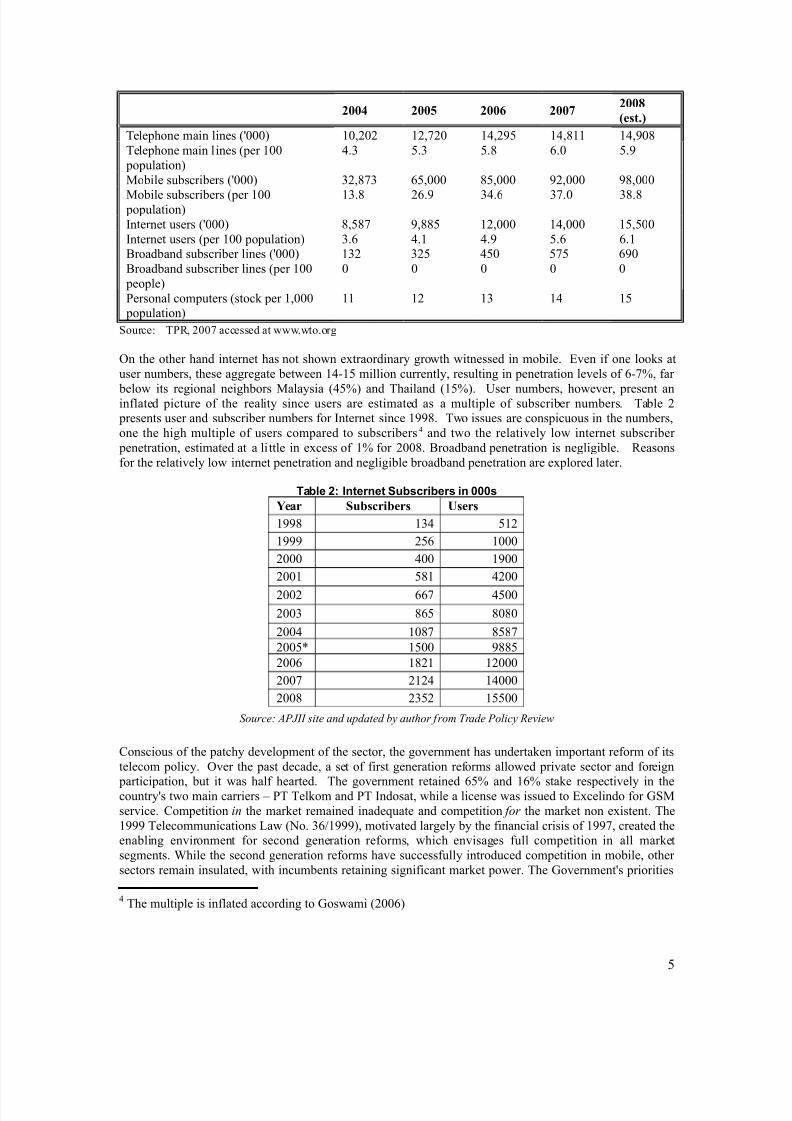

Crowth of the Indonesian Telecom market has been uneven. $hile the mobile market has shownconsiderable e9pansion, fi9ed lines have stagnated in the last two years. It is estimated that fi9ed linesJ''will decline marginally from 3 to 1.4 in &''6. n the other hand, mobile telephony has grown andsurpassed fi9ed5line penetration since it does not need the same substantial investment in infrastructure. 8sa result the number of mobile subscribers has increased strongly, rising from 7&.6 million in &'': to anestimated 4& million in &''<, equivalent to access pathsJ'' of around 7< (Table I!.

Table 1: Telecm sectr, -/0

3 This paper shows that while the policy says the right things, the conditions on the ground even after <

years deviate significantly from the stated obDectives in many respects

:

8/11/2019 Kathuria Rajat

http://slidepdf.com/reader/full/kathuria-rajat 5/40

!!" !!# !!$ !!%!!&

'est.(

Telephone main lines (K'''! ',&'& &,<&' :,&41 :,6 :,4'6Telephone main lines (per '' population!

:.7 1.7 1.6 3.' 1.4

;obile subscribers (K'''! 7&,6<7 31,''' 61,''' 4&,''' 46,'''

;obile subscribers (per '' population!

7.6 &3.4 7:.3 7<.' 76.6

Internet users (K'''! 6,16< 4,661 &,''' :,''' 1,1''Internet users (per '' population! 7.3 :. :.4 1.3 3.%roadband subscriber lines (K'''! 7& 7&1 :1' 1<1 34'%roadband subscriber lines (per '' people!

' ' ' ' '

2ersonal computers (stock per ,''' population!

& 7 : 1

+ource T2R, &''< accessed at www.wto.org

n the other hand internet has not shown e9traordinary growth witnessed in mobile. )ven if one looks atuser numbers, these aggregate between :51 million currently, resulting in penetration levels of 35<L, far

below its regional neighbors ;alaysia (:1L! and Thailand (1L!. Eser numbers, however, present aninflated picture of the reality since users are estimated as a multiple of subscriber numbers. Table & presents user and subscriber numbers for Internet since 446. Two issues are conspicuous in the numbers,one the high multiple of users compared to subscribers : and two the relatively low internet subscriber penetration, estimated at a little in e9cess of L for &''6. %roadband penetration is negligible. Reasonsfor the relatively low internet penetration and negligible broadband penetration are e9plored later.

Table -: I"ter"et Subscribers i" s

)ear *u+scri+ers ,sers

446 7: 1&

444 &13 '''

&''' :'' 4''

&'' 16 :&''

&''& 33< :1''

&''7 631 6'6'

&'': '6< 616<

&''1M 1'' 4661

&''3 6& &'''

&''< &&: :'''

&''6 &71& 11''

Source: 'P(II site and updated !y author from )rade Policy Review

onscious of the patchy development of the sector, the government has undertaken important reform of itstelecom policy. ver the past decade, a set of first generation reforms allowed private sector and foreign

participation, but it was half hearted. The government retained 31L and 3L stake respectively in thecountryKs two main carriers = 2T Telkom and 2T Indosat, while a license was issued to )9celindo for C+;service. ompetition in the market remained inadequate and competition for the market non e9istent. The444 Telecommunications aw (/o. 73J444!, motivated largely by the financial crisis of 44<, created theenabling environment for second generation reforms, which envisages full competition in all marketsegments. $hile the second generation reforms have successfully introduced competition in mobile, other sectors remain insulated, with incumbents retaining significant market power. The CovernmentKs priorities

: The multiple is inflated according to Coswami (&''3!

1

8/11/2019 Kathuria Rajat

http://slidepdf.com/reader/full/kathuria-rajat 6/40

over the ne9t few years include implementing the provisions of the 444 law, in particular the developmentof the regulatory framework that is crucial for the success of the sector liberali>ation programme.

In &''&, the Covernment ended the e9clusive rights of 2T Telkom for domestic long5distance service andlocal fi9ed5line service in 8ugust &''1 and of 2T Indosat and +atelindo for international calling service in&''7. 2T Telkom and 2T Indosat were established as IndonesiaKs only full service providers, a move thatensured 2T TelkomKs survival in the face of increasing competition from ?oice5Internet 2rotocol (?oI2!services. +ince &''&, however, 2T Telkom has focused most investment in the value5added cellular marketand has added few new fi9ed lines. The provisions of IndonesiaKs Telecommunications aw have steeredreforms to end monopolies and open basic telecommunications services to maDority foreign ownership.Thus, TelkomKs and IndosatKs respective monopolies on domestic and international services were ended in&''& as a first step towards introduction of full competition. ompetition in fi9ed5line services has emergedfrom companies using ?oice over Internet 2rotocol (?oI2! technology. -owever, the Covernment haschosen to restrict entry into this new market segment to five companies Telkom, Indosat, +atelindo, andtwo independent operators. In terms of number of operators, competition is well5advanced in the provisionof mobile services. Telkomsel, Dointly owned by 2T Telkom and the +ingaporean carrier +ingTel, is thelargest mobile operator, with a market share of over 1'L. Its two main competitors are +atelindo, fullyowned by Indosat, and )9celcomindo, partly owned by T;I ?eri>on (Table 7!.

The reality as it e9ists today (see Table 7! however does not suggest any degree of success in meeting the

declared obDective of introducing "effective# competition in the sector. In each of the 7 categories (fi9ed,cellular and international!, the -erfindahl -irschman Inde9 (--I! e9ceeds 6'' 3, implying, according tothe E+ applied benchmark that the market is "presumptively anti competitive#. )ven if a lower benchmark is applied, say &1'' (the --I that would obtain with : operators of equal si>e in the relevant market!, itwould still "raise serious doubts# in regard to the e9tent of competition in the market. 8n alternativeanalysis using the R: ratio i.e. the sum of the market shares of the top : firms produces poorer resultswith respect to competition in the Indonesian telecom market. .

Table 2: Telecmmu"icati"s mar'et s3ares i" -4 5Per ce"t6

Type perator +hare --I R:

Ai9ed phone Telkom 4' &-&.%# -!!

Indosat &%akrieTel 1

%% Tel &;obile Telkomsel 1: $#! /$

Indosat &3)9celcom :;obile56 : /T+ N;andara N-utchinson N2rimasel N

International Telkom 1& "-"& /!

Indosat 76

Source: )PR *%%+ and author calculations

1 ,efore *%%* P) )elkom operated as the exclusive provider of fixed-line local long-distance and leased-

line telecommunications services# 't the same time in .//0 )elkom awarded .0-year so-called 1KS21

concessions to private consortia to operate fixed line services on a monopoly !asis in five of seven regional districts 3P) )elkom retained control of 4reater (akarta and 5ast (ava6# )he concessions attracted

su!stantial foreign investment from large international operators including 7rance )elecom 8edia 2ne

)elstra 9)) a!le ; <ireless and Singapore )elecom# Su!se=uently )elkom decided to !uy out two of

the regional operators although disputes still exist with two other regional carriers#3 >>I is the sum of s=uares of market shares of all providers in the relevant market#

3

8/11/2019 Kathuria Rajat

http://slidepdf.com/reader/full/kathuria-rajat 7/40

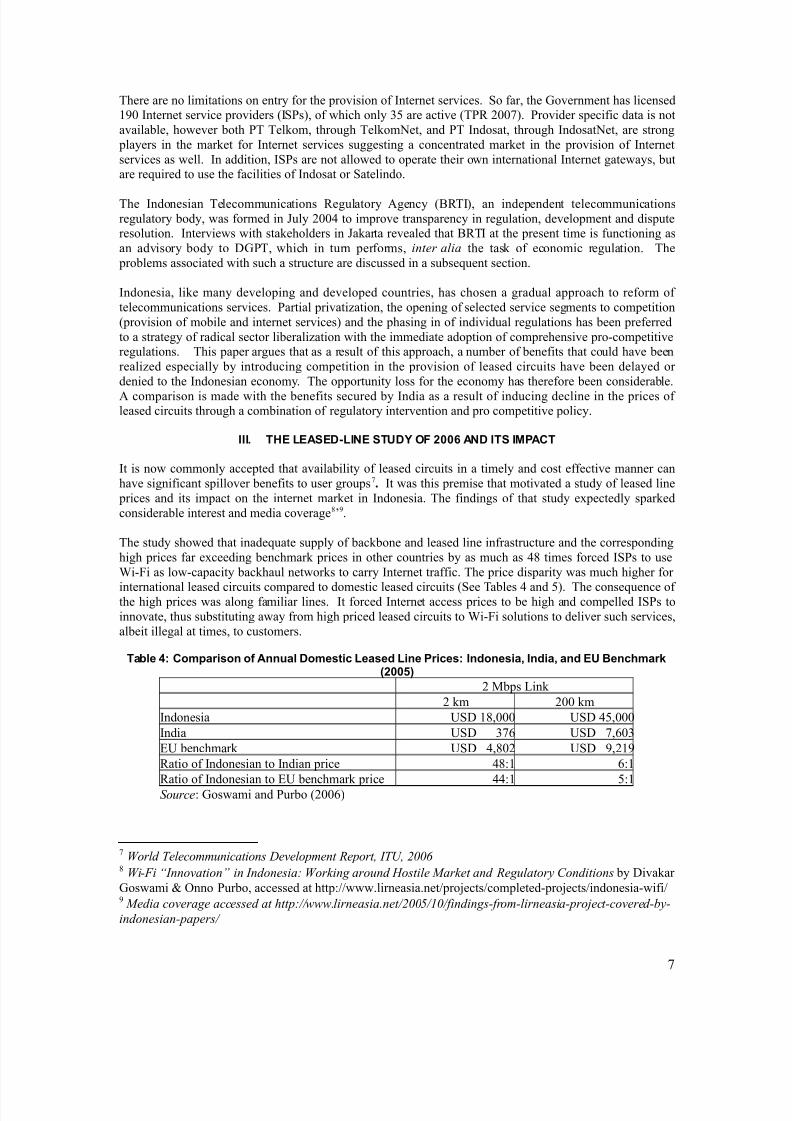

There are no limitations on entry for the provision of Internet services. +o far, the Covernment has licensed4' Internet service providers (I+2s!, of which only 71 are active (T2R &''<!. 2rovider specific data is notavailable, however both 2T Telkom, through Telkom/et, and 2T Indosat, through Indosat/et, are strong players in the market for Internet services suggesting a concentrated market in the provision of Internetservices as well. In addition, I+2s are not allowed to operate their own international Internet gateways, butare required to use the facilities of Indosat or +atelindo.

The Indonesian Telecommunications Regulatory 8gency (%RTI!, an independent telecommunicationsregulatory body, was formed in 0uly &'': to improve transparency in regulation, development and disputeresolution. Interviews with stakeholders in 0akarta revealed that %RTI at the present time is functioning asan advisory body to *C2T, which in turn performs, inter alia the task of economic regulation. The problems associated with such a structure are discussed in a subsequent section.

Indonesia, like many developing and developed countries, has chosen a gradual approach to reform of telecommunications services. 2artial privati>ation, the opening of selected service segments to competition(provision of mobile and internet services! and the phasing in of individual regulations has been preferredto a strategy of radical sector liberali>ation with the immediate adoption of comprehensive pro5competitiveregulations. This paper argues that as a result of this approach, a number of benefits that could have beenreali>ed especially by introducing competition in the provision of leased circuits have been delayed or denied to the Indonesian economy. The opportunity loss for the economy has therefore been considerable.

8 comparison is made with the benefits secured by India as a result of inducing decline in the prices of leased circuits through a combination of regulatory intervention and pro competitive policy.

III. T7E LEASED0LINE ST)D8 OF -4 AND ITS IMPACT

It is now commonly accepted that availability of leased circuits in a timely and cost effective manner canhave significant spillover benefits to user groups<. It was this premise that motivated a study of leased line prices and its impact on the internet market in Indonesia. The findings of that study e9pectedly sparkedconsiderable interest and media coverage6#4.

The study showed that inadequate supply of backbone and leased line infrastructure and the correspondinghigh prices far e9ceeding benchmark prices in other countries by as much as :6 times forced I+2s to use$i5Ai as low5capacity backhaul networks to carry Internet traffic. The price disparity was much higher for

international leased circuits compared to domestic leased circuits (+ee Tables : and 1!. The consequence of the high prices was along familiar lines. It forced Internet access prices to be high and compelled I+2s toinnovate, thus substituting away from high priced leased circuits to $i5Ai solutions to deliver such services,albeit illegal at times, to customers.

Table /: Cmparis" # A""ual Dmestic Lease% Li"e Prices: I"%"esia, I"%ia, a"% E) 9e"c3mar'5-6

& ;bps ink

& km &'' km

Indonesia E+* 6,''' E+* :1,'''

India E+* 7<3 E+* <,3'7

)E benchmark E+* :,6'& E+* 4,&4

Ratio of Indonesian to Indian price :6 3

Ratio of Indonesian to )E benchmark price :: 1Source Coswami and 2urbo (&''3!

< <orld )elecommunications ?evelopment Report I)@ *%%A 6 <i-7i BInnovationC in Indonesia: <orking around >ostile 8arket and Regulatory onditions by *ivakar

Coswami O nno 2urbo, accessed at httpJJwww.lirneasia.netJproDectsJcompleted5proDectsJindonesia5wifiJ4 8edia coverage accessed at http:""www#lirneasia#net"*%%0".%"findings-from-lirneasia-project-covered-!y-

indonesian-papers"

<

8/11/2019 Kathuria Rajat

http://slidepdf.com/reader/full/kathuria-rajat 8/40

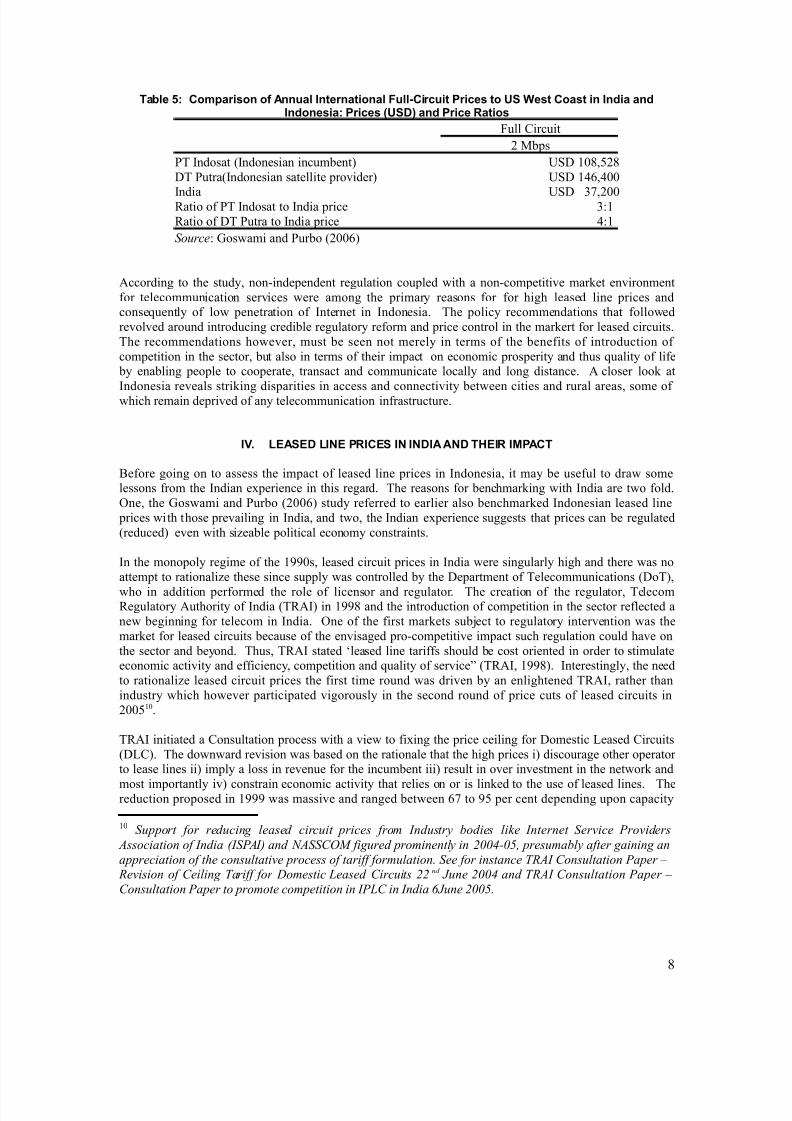

Table : Cmparis" # A""ual I"ter"ati"al Full0Circuit Prices t )S ;est Cast i" I"%ia a"%I"%"esia: Prices 5)SD6 a"% Price *atis

Aull ircuit

& ;bps

2T Indosat (Indonesian incumbent! E+* '6,1&6*T 2utra(Indonesian satellite provider! E+* :3,:''

India E+* 7<,&''Ratio of 2T Indosat to India price 7Ratio of *T 2utra to India price :

Source Coswami and 2urbo (&''3!

8ccording to the study, non5independent regulation coupled with a non5competitive market environmentfor telecommunication services were among the primary reasons for for high leased line prices andconsequently of low penetration of Internet in Indonesia. The policy recommendations that followedrevolved around introducing credible regulatory reform and price control in the markert for leased circuits.The recommendations however, must be seen not merely in terms of the benefits of introduction of competition in the sector, but also in terms of their impact on economic prosperity and thus quality of life by enabling people to cooperate, transact and communicate locally and long distance. 8 closer look atIndonesia reveals striking disparities in access and connectivity between cities and rural areas, some of which remain deprived of any telecommunication infrastructure.

IV. LEASED LINE P*ICES IN INDIA AND T7EI* IMPACT

%efore going on to assess the impact of leased line prices in Indonesia, it may be useful to draw somelessons from the Indian e9perience in this regard. The reasons for benchmarking with India are two fold.ne, the Coswami and 2urbo (&''3! study referred to earlier also benchmarked Indonesian leased line prices with those prevailing in India, and two, the Indian e9perience suggests that prices can be regulated(reduced! even with si>eable political economy constraints.

In the monopoly regime of the 44's, leased circuit prices in India were singularly high and there was noattempt to rationali>e these since supply was controlled by the *epartment of Telecommunications (*oT!,

who in addition performed the role of licensor and regulator. The creation of the regulator, TelecomRegulatory 8uthority of India (TR8I! in 446 and the introduction of competition in the sector reflected anew beginning for telecom in India. ne of the first markets subDect to regulatory intervention was themarket for leased circuits because of the envisaged pro5competitive impact such regulation could have onthe sector and beyond. Thus, TR8I stated "leased line tariffs should be cost oriented in order to stimulateeconomic activity and efficiency, competition and quality of serviceP (TR8I, 446!. Interestingly, the needto rationali>e leased circuit prices the first time round was driven by an enlightened TR8I, rather thanindustry which however participated vigorously in the second round of price cuts of leased circuits in&''1'.

TR8I initiated a onsultation process with a view to fi9ing the price ceiling for *omestic eased ircuits(*!. The downward revision was based on the rationale that the high prices i! discourage other operator to lease lines ii! imply a loss in revenue for the incumbent iii! result in over investment in the network and

most importantly iv! constrain economic activity that relies on or is linked to the use of leased lines. Thereduction proposed in 444 was massive and ranged between 3< to 41 per cent depending upon capacity

' Support for reducing leased circuit prices from Industry !odies like Internet Service Providers

'ssociation of India 3ISP'I6 and 9'SS28 figured prominently in *%%D-%0 presuma!ly after gaining an

appreciation of the consultative process of tariff formulation# See for instance )R'I onsultation Paper E Revision of eiling )ariff for ?omestic Leased ircuits **nd (une *%%D and )R'I onsultation Paper E

onsultation Paper to promote competition in IPL in India A(une *%%0#

6

8/11/2019 Kathuria Rajat

http://slidepdf.com/reader/full/kathuria-rajat 9/40

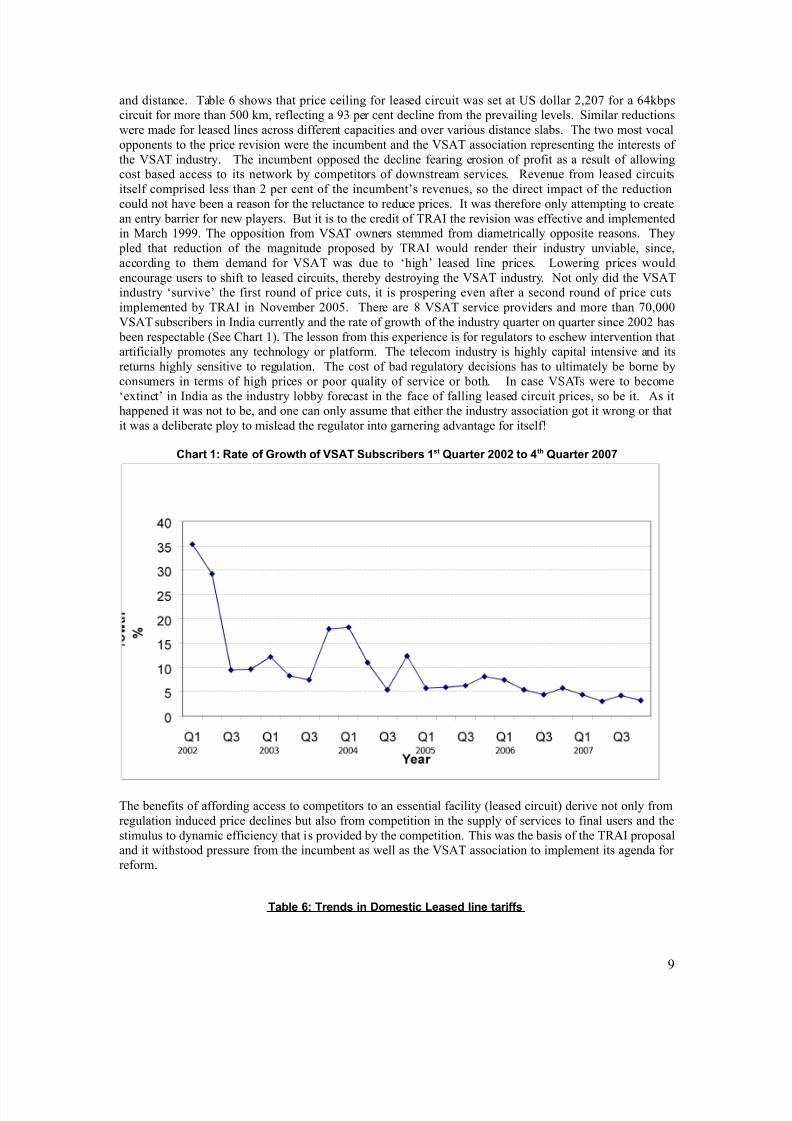

and distance. Table 3 shows that price ceiling for leased circuit was set at E+ dollar &,&'< for a 3:kbpscircuit for more than 1'' km, reflecting a 47 per cent decline from the prevailing levels. +imilar reductionswere made for leased lines across different capacities and over various distance slabs. The two most vocalopponents to the price revision were the incumbent and the ?+8T association representing the interests of the ?+8T industry. The incumbent opposed the decline fearing erosion of profit as a result of allowingcost based access to its network by competitors of downstream services. Revenue from leased circuitsitself comprised less than & per cent of the incumbent#s revenues, so the direct impact of the reductioncould not have been a reason for the reluctance to reduce prices. It was therefore only attempting to createan entry barrier for new players. %ut it is to the credit of TR8I the revision was effective and implementedin ;arch 444. The opposition from ?+8T owners stemmed from diametrically opposite reasons. They pled that reduction of the magnitude proposed by TR8I would render their industry unviable, since,according to them demand for ?+8T was due to "high# leased line prices. owering prices wouldencourage users to shift to leased circuits, thereby destroying the ?+8T industry. /ot only did the ?+8Tindustry "survive# the first round of price cuts, it is prospering even after a second round of price cutsimplemented by TR8I in /ovember &''1. There are 6 ?+8T service providers and more than <','''?+8T subscribers in India currently and the rate of growth of the industry quarter on quarter since &''& has been respectable (+ee hart !. The lesson from this e9perience is for regulators to eschew intervention thatartificially promotes any technology or platform. The telecom industry is highly capital intensive and itsreturns highly sensitive to regulation. The cost of bad regulatory decisions has to ultimately be borne byconsumers in terms of high prices or poor quality of service or both. In case ?+8Ts were to become

"e9tinct# in India as the industry lobby forecast in the face of falling leased circuit prices, so be it. 8s ithappened it was not to be, and one can only assume that either the industry association got it wrong or thatit was a deliberate ploy to mislead the regulator into garnering advantage for itselfQ

C3art 1: *ate # <r&t3 # VSAT Subscribers 1st =uarter -- t /t3 =uarter ->

The benefits of affording access to competitors to an essential facility (leased circuit! derive not only fromregulation induced price declines but also from competition in the supply of services to final users and thestimulus to dynamic efficiency that is provided by the competition. This was the basis of the TR8I proposaland it withstood pressure from the incumbent as well as the ?+8T association to implement its agenda for reform.

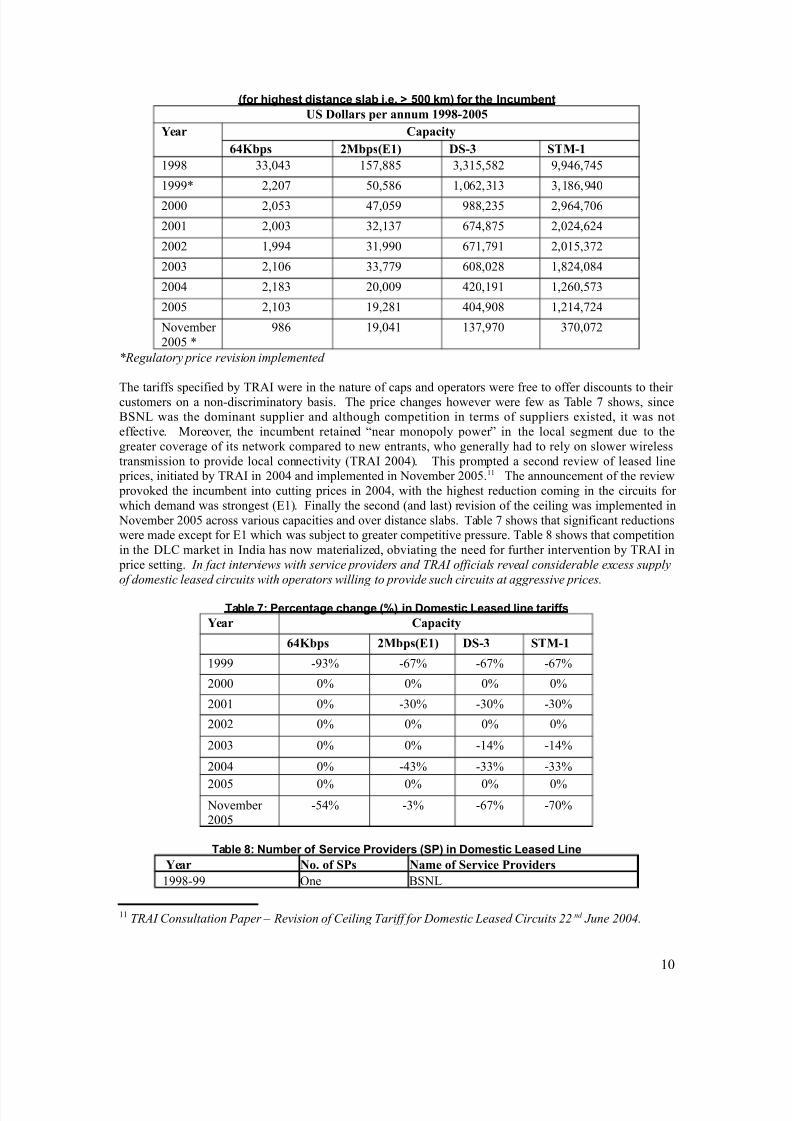

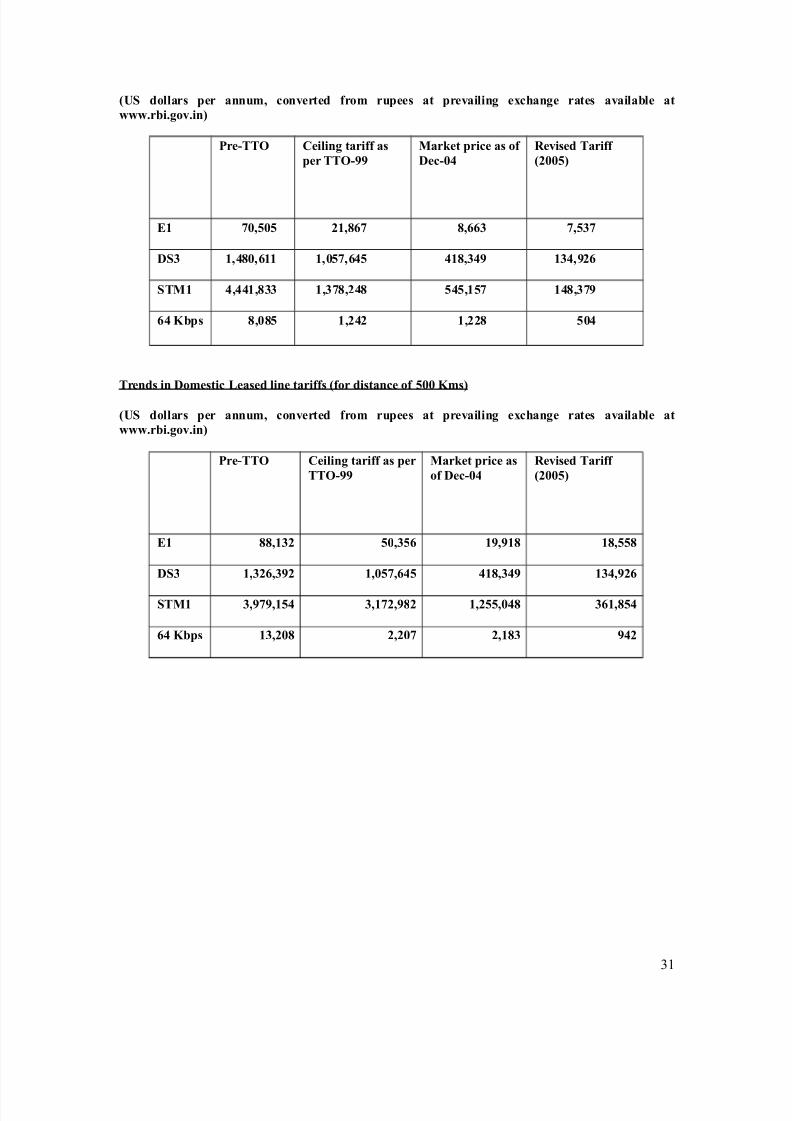

Table 4: Tre"%s i" Dmestic Lease% li"e tari##s

4

8/11/2019 Kathuria Rajat

http://slidepdf.com/reader/full/kathuria-rajat 10/40

5#r 3ig3est %ista"ce slab i.e. ? 'm6 #r t3e I"cumbe"t

,* Dollars per annum -//&0!!#

)ear Capacity

$"K+ps 1+ps'E-( D*0 *210-

446 77,':7 1<,661 7,71,16& 4,4:3,<:1

444M &,&'< 1',163 ,'3&,77 7,63,4:'

&''' &,'17 :<,'14 466,&71 &,43:,<'3

&'' &,''7 7&,7< 3<:,6<1 &,'&:,3&:

&''& ,44: 7,44' 3<,<4 &,'1,7<&

&''7 &,'3 77,<<4 3'6,'&6 ,6&:,'6:

&'': &,67 &',''4 :&',4 ,&3',1<7

&''1 &,'7 4,&6 :':,4'6 ,&:,<&:

/ovember &''1 M

463 4,': 7<,4<' 7<','<&

FRegulatory price revision implemented

The tariffs specified by TR8I were in the nature of caps and operators were free to offer discounts to their customers on a non5discriminatory basis. The price changes however were few as Table < shows, since%+/ was the dominant supplier and although competition in terms of suppliers e9isted, it was noteffective. ;oreover, the incumbent retained Fnear monopoly powerP in the local segment due to thegreater coverage of its network compared to new entrants, who generally had to rely on slower wirelesstransmission to provide local connectivity (TR8I &'':!. This prompted a second review of leased line prices, initiated by TR8I in &'': and implemented in /ovember &''1. The announcement of the review provoked the incumbent into cutting prices in &'':, with the highest reduction coming in the circuits for which demand was strongest ()!. Ainally the second (and last! revision of the ceiling was implemented in /ovember &''1 across various capacities and over distance slabs. Table < shows that significant reductionswere made e9cept for ) which was subDect to greater competitive pressure. Table 6 shows that competitionin the * market in India has now materiali>ed, obviating the need for further intervention by TR8I in price setting. In fact interviews with service providers and )R'I officials reveal considera!le excess supply

of domestic leased circuits with operators willing to provide such circuits at aggressive prices#

Table >: Perce"tage c3a"ge 5@6 i" Dmestic Lease% li"e tari##s

)ear Capacity

$"K+ps 1+ps'E-( D*0 *210-

444 547L 53<L 53<L 53<L

&''' 'L 'L 'L 'L

&'' 'L 57'L 57'L 57'L

&''& 'L 'L 'L 'L

&''7 'L 'L 5:L 5:L

&'': 'L 5:7L 577L 577L

&''1 'L 'L 'L 'L /ovember&''1

51:L 57L 53<L 5<'L

Table : Number # Ser!ice Pr!i%ers 5SP6 i" Dmestic Lease% Li"e

)ear 3o. of *Ps 3ame of *er4ice Pro4iders

446544 ne %+/

)R'I onsultation Paper E Revision of eiling )ariff for ?omestic Leased ircuits **nd (une *%%D#

'

8/11/2019 Kathuria Rajat

http://slidepdf.com/reader/full/kathuria-rajat 11/40

&'''5&''6 )ight2lus I25II

%+/, Tata , %harti, -ughes, Reliance,+hyam Telelink, -A and I25II +ervice2roviders.

IP- Infrastructure Providers such as Railways Power @tilities and 4as @tilities

The other market which is complementary to the * market and has an equally fundamental impact on

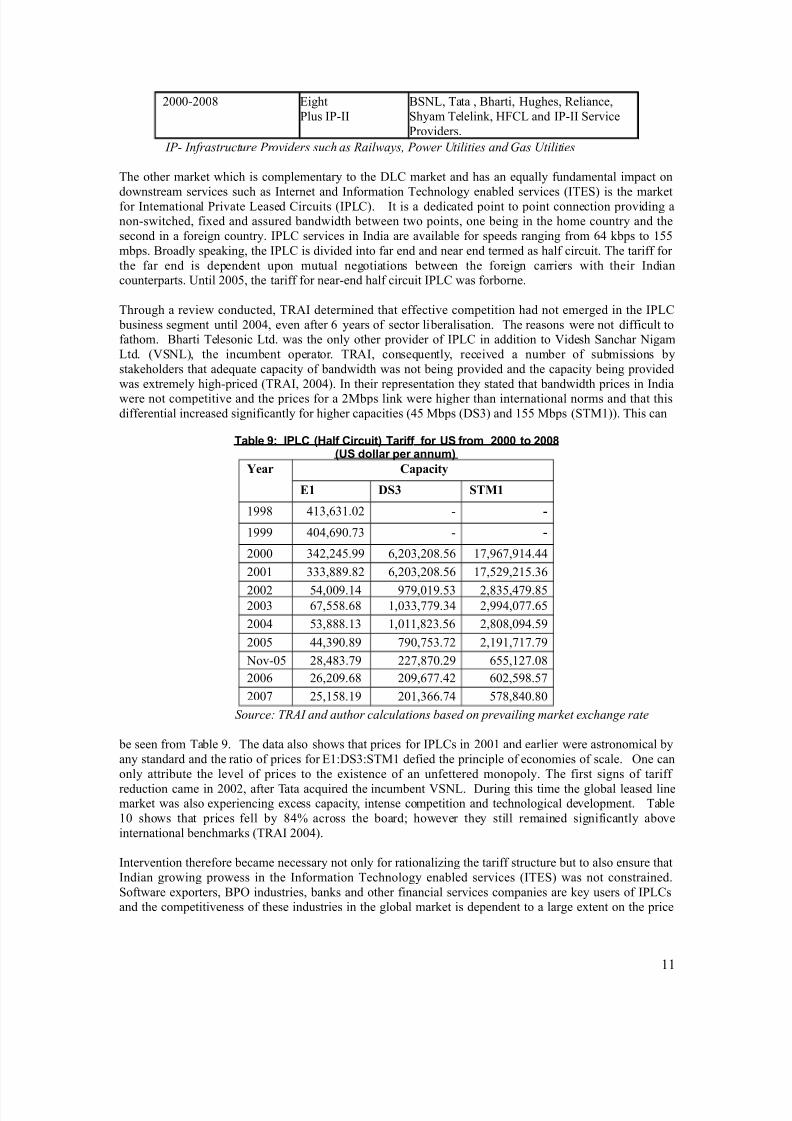

downstream services such as Internet and Information Technology enabled services (IT)+! is the marketfor International 2rivate eased ircuits (I2!. It is a dedicated point to point connection providing anon5switched, fi9ed and assured bandwidth between two points, one being in the home country and thesecond in a foreign country. I2 services in India are available for speeds ranging from 3: kbps to 11mbps. %roadly speaking, the I2 is divided into far end and near end termed as half circuit. The tariff for the far end is dependent upon mutual negotiations between the foreign carriers with their Indiancounterparts. Entil &''1, the tariff for near5end half circuit I2 was forborne.

Through a review conducted, TR8I determined that effective competition had not emerged in the I2 business segment until &'':, even after 3 years of sector liberalisation. The reasons were not difficult tofathom. %harti Telesonic td. was the only other provider of I2 in addition to ?idesh +anchar /igamtd. (?+/!, the incumbent operator. TR8I, consequently, received a number of submissions bystakeholders that adequate capacity of bandwidth was not being provided and the capacity being providedwas e9tremely high5priced (TR8I, &'':!. In their representation they stated that bandwidth prices in Indiawere not competitive and the prices for a &;bps link were higher than international norms and that thisdifferential increased significantly for higher capacities (:1 ;bps (*+7! and 11 ;bps (+T;!!. This can

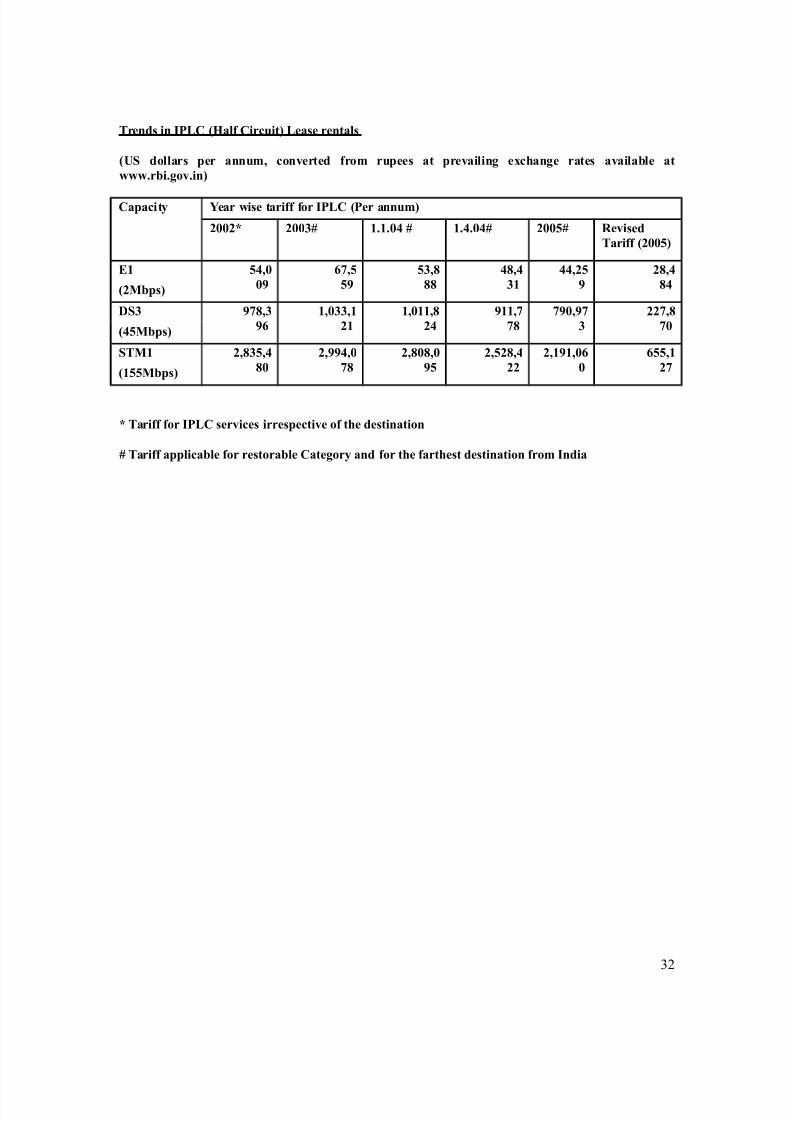

Table : IPLC 57al# Circuit6 Tari## #r )S #rm - t -5)S %llar per a""um6

)ear Capacity

E- D* *21-

446 :7,37.'& 5 0

444 :':,34'.<7 5 0

&''' 7:&,&:1.44 3,&'7,&'6.13 <,43<,4:.::

&'' 777,664.6& 3,&'7,&'6.13 <,1&4,&1.73

&''& 1:,''4.: 4<4,'4.17 &,671,:<4.61&''7 3<,116.36 ,'77,<<4.7: &,44:,'<<.31

&'': 17,666.7 ,',6&7.13 &,6'6,'4:.14

&''1 ::,74'.64 <4',<17.<& &,4,<<.<4

/ov5'1 &6,:67.<4 &&<,6<'.&4 311,&<.'6

&''3 &3,&'4.36 &'4,3<<.:& 3'&,146.1<

&''< &1,16.4 &',733.<: 1<6,6:'.6'

Source: )R'I and author calculations !ased on prevailing market exchange rate

be seen from Table 4. The data also shows that prices for I2s in &'' and earlier were astronomical byany standard and the ratio of prices for )*+7+T; defied the principle of economies of scale. ne canonly attribute the level of prices to the e9istence of an unfettered monopoly. The first signs of tariff

reduction came in &''&, after Tata acquired the incumbent ?+/. *uring this time the global leased linemarket was also e9periencing e9cess capacity, intense competition and technological development. Table' shows that prices fell by 6:L across the board however they still remained significantly aboveinternational benchmarks (TR8I &'':!.

Intervention therefore became necessary not only for rationali>ing the tariff structure but to also ensure thatIndian growing prowess in the Information Technology enabled services (IT)+! was not constrained.+oftware e9porters, %2 industries, banks and other financial services companies are key users of I2sand the competitiveness of these industries in the global market is dependent to a large e9tent on the price

8/11/2019 Kathuria Rajat

http://slidepdf.com/reader/full/kathuria-rajat 12/40

they pay for I2. In addition, Internet +ervice 2roviders (I+2! also use I2 for their upstreamconnectivity abroad and high cost of I2#s get reflected into the Internet access tariff which couldadversely affect Internet growth in the country.

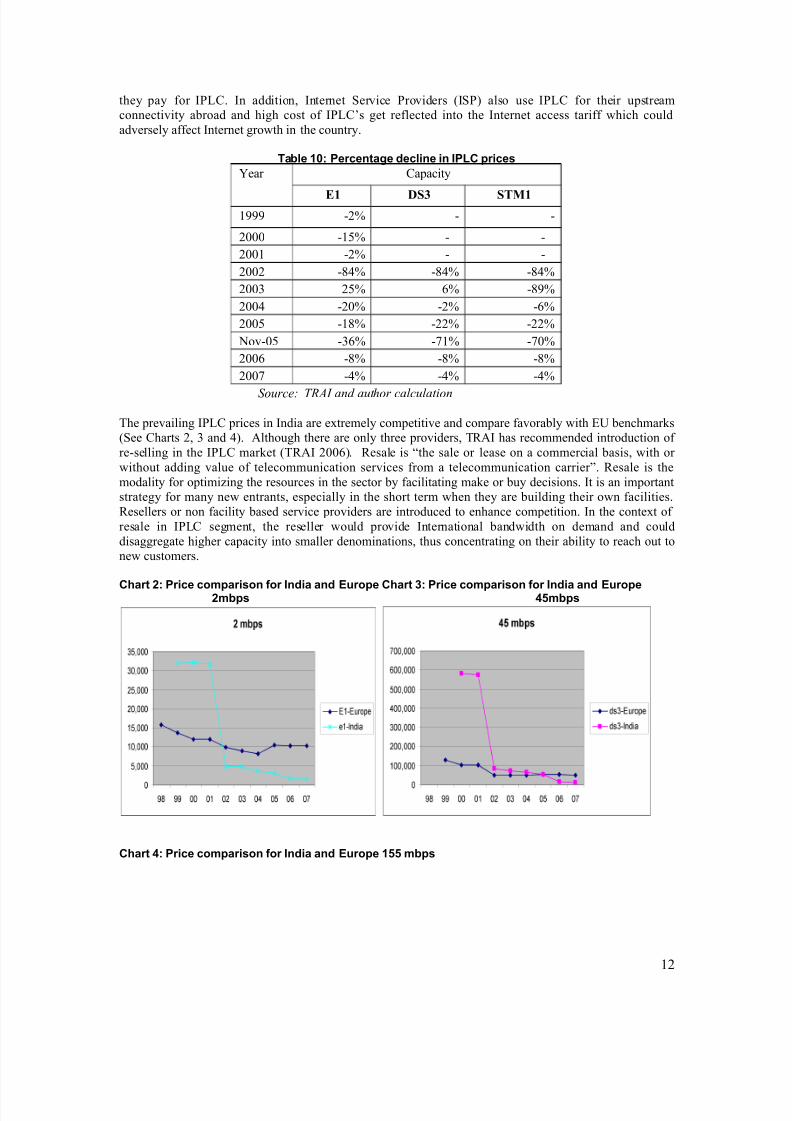

Table 1: Perce"tage %ecli"e i" IPLC prices

ear apacity

E- D* *21-

444 5&L 5 5

&''' 51L 5 5

&'' 5&L 5 5

&''& 56:L 56:L 56:L

&''7 &1L 3L 564L

&'': 5&'L 5&L 53L

&''1 56L 5&&L 5&&L

/ov5'1 573L 5<L 5<'L

&''3 56L 56L 56L

&''< 5:L 5:L 5:L

Source: )R'I and author calculation

The prevailing I2 prices in India are e9tremely competitive and compare favorably with )E benchmarks(+ee harts &, 7 and :!. 8lthough there are only three providers, TR8I has recommended introduction of re5selling in the I2 market (TR8I &''3!. Resale is Fthe sale or lease on a commercial basis, with or without adding value of telecommunication services from a telecommunication carrierP. Resale is themodality for optimi>ing the resources in the sector by facilitating make or buy decisions. It is an importantstrategy for many new entrants, especially in the short term when they are building their own facilities.Resellers or non facility based service providers are introduced to enhance competition. In the conte9t of resale in I2 segment, the reseller would provide International bandwidth on demand and coulddisaggregate higher capacity into smaller denominations, thus concentrating on their ability to reach out tonew customers.

C3art -: Price cmparis" #r I"%ia a"% Eurpe C3art 2: Price cmparis" #r I"%ia a"% Eurpe -mbps /mbps

C3art /: Price cmparis" #r I"%ia a"% Eurpe 1 mbps

&

8/11/2019 Kathuria Rajat

http://slidepdf.com/reader/full/kathuria-rajat 13/40

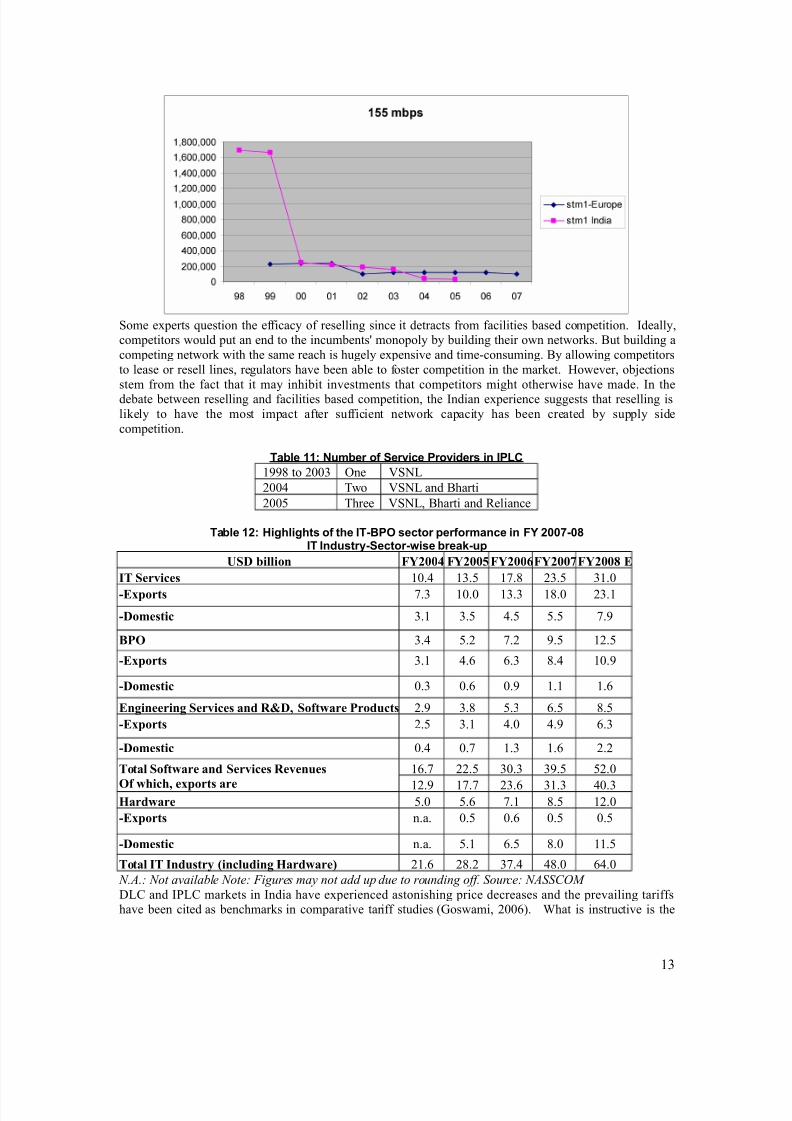

+ome e9perts question the efficacy of reselling since it detracts from facilities based competition. Ideally,competitors would put an end to the incumbentsK monopoly by building their own networks. %ut building acompeting network with the same reach is hugely e9pensive and time5consuming. %y allowing competitorsto lease or resell lines, regulators have been able to foster competition in the market. -owever, obDectionsstem from the fact that it may inhibit investments that competitors might otherwise have made. In thedebate between reselling and facilities based competition, the Indian e9perience suggests that reselling islikely to have the most impact after sufficient network capacity has been created by supply sidecompetition.

Table 11: Number # Ser!ice Pr!i%ers i" IPLC

446 to &''7 ne ?+/

&'': Two ?+/ and %harti

&''1 Three ?+/, %harti and Reliance

Table 1-: 7ig3lig3ts # t3e IT09PO sectr per#rma"ce i" F8 ->0IT I"%ustrB0Sectr0&ise brea'0up

,*D +illion 5)!!" 5)!!#5)!!$5)!!%5)!!& E

I2 *er4ices '.: 7.1 <.6 &7.1 7.'

0E6ports <.7 '.' 7.7 6.' &7.

0Domestic 7. 7.1 :.1 1.1 <.4

7P8 7.: 1.& <.& 4.1 &.1

0E6ports 7. :.3 3.7 6.: '.4

0Domestic '.7 '.3 '.4 . .3

Engineering *er4ices and R9D *oftware Products &.4 7.6 1.7 3.1 6.1

0E6ports &.1 7. :.' :.4 3.7

0Domestic '.: '.< .7 .3 &.&

2otal *oftware and *er4ices Re4enues

8f which e6ports are

3.< &&.1 7'.7 74.1 1&.'

&.4 <.< &7.3 7.7 :'.7;ardware 1.' 1.3 <. 6.1 &.'

0E6ports n.a. '.1 '.3 '.1 '.1

0Domestic n.a. 1. 3.1 6.' .1

2otal I2 Industry 'including ;ardware( &.3 &6.& 7<.: :6.' 3:.'

9#'#: 9ot availa!le 9ote: 7igures may not add up due to rounding off# Source: 9'SS28

* and I2 markets in India have e9perienced astonishing price decreases and the prevailing tariffshave been cited as benchmarks in comparative tariff studies (Coswami, &''3!. $hat is instructive is the

7

8/11/2019 Kathuria Rajat

http://slidepdf.com/reader/full/kathuria-rajat 14/40

manner in which the price decline occurred. In both markets, regulatory intervention was necessary tostart with but competition was as much necessary to ensure that cost reductions through technical progresswere passed on to the customer. TR8I also overcame the incumbents# procedural, legal and technicalreasons for tardiness&. 8 lack of competition5boosting oversight is one reason for the poor record of Indonesia in this regard (see below!. ;ost Indian companies using * and I2s, including I+2+ have achoice of at least three International bandwidth providers and many more domestic leased line providers.ompetition therefore ensures that providers race to offer their customers better and faster access atincreasingly attractive prices.

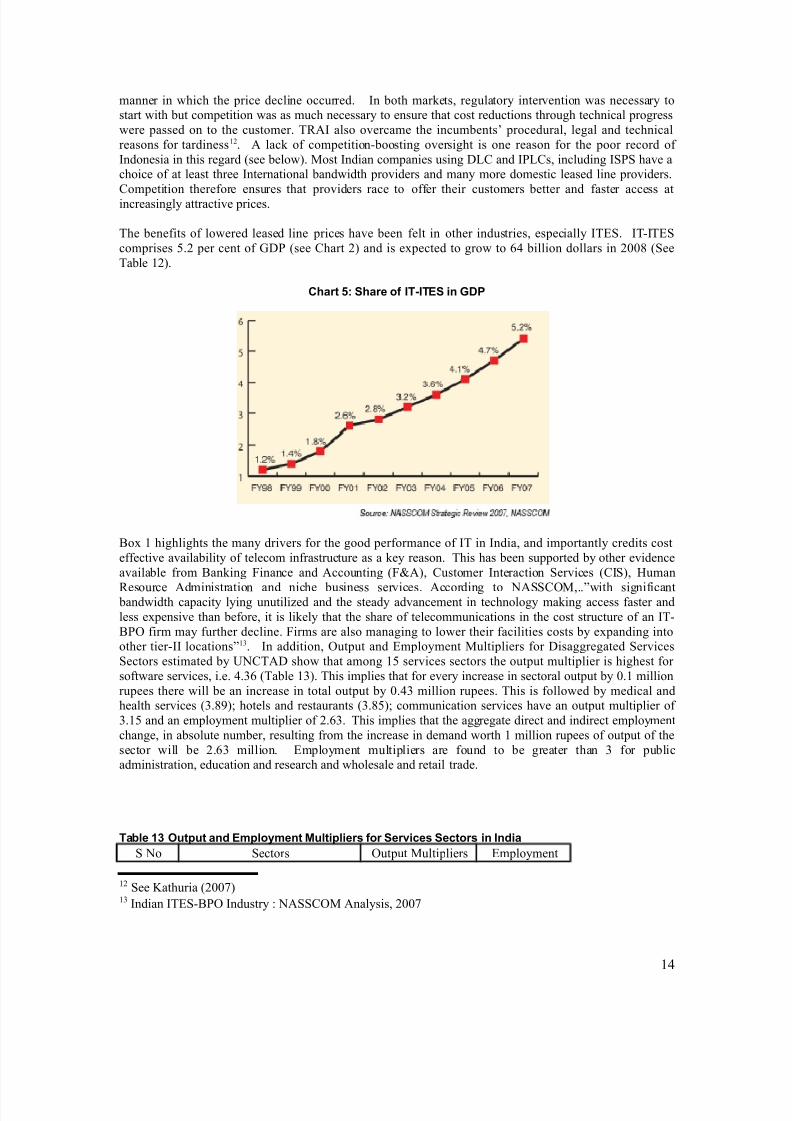

The benefits of lowered leased line prices have been felt in other industries, especially IT)+. IT5IT)+comprises 1.& per cent of C*2 (see hart &! and is e9pected to grow to 3: billion dollars in &''6 (+eeTable &!.

C3art : S3are # IT0ITES i" <DP

%o9 highlights the many drivers for the good performance of IT in India, and importantly credits costeffective availability of telecom infrastructure as a key reason. This has been supported by other evidenceavailable from %anking Ainance and 8ccounting (AO8!, ustomer Interaction +ervices (I+!, -uman

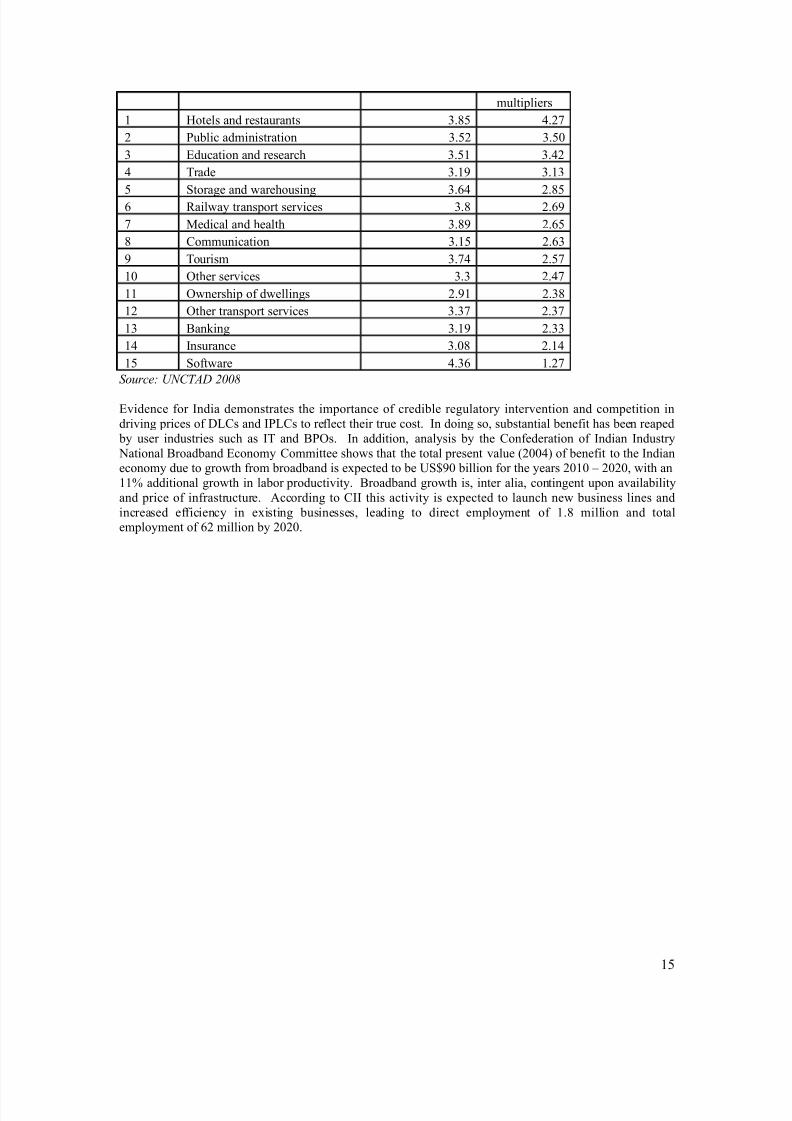

Resource 8dministration and niche business services. 8ccording to /8++;,..Pwith significant bandwidth capacity lying unutili>ed and the steady advancement in technology making access faster andless e9pensive than before, it is likely that the share of telecommunications in the cost structure of an IT5%2 firm may further decline. Airms are also managing to lower their facilities costs by e9panding intoother tier5II locationsP7. In addition, utput and )mployment ;ultipliers for *isaggregated +ervices+ectors estimated by E/T8* show that among 1 services sectors the output multiplier is highest for software services, i.e. :.73 (Table 7!. This implies that for every increase in sectoral output by '. millionrupees there will be an increase in total output by '.:7 million rupees. This is followed by medical andhealth services (7.64! hotels and restaurants (7.61! communication services have an output multiplier of 7.1 and an employment multiplier of &.37. This implies that the aggregate direct and indirect employmentchange, in absolute number, resulting from the increase in demand worth million rupees of output of thesector will be &.37 million. )mployment multipliers are found to be greater than 7 for publicadministration, education and research and wholesale and retail trade.

Table 12 Output a"% EmplBme"t Multipliers #r Ser!ices Sectrs i" I"%ia

+ /o +ectors utput ;ultipliers )mployment

& +ee Sathuria (&''<!7 Indian IT)+5%2 Industry /8++; 8nalysis, &''<

:

8/11/2019 Kathuria Rajat

http://slidepdf.com/reader/full/kathuria-rajat 15/40

multipliers

-otels and restaurants 7.61 :.&<

& 2ublic administration 7.1& 7.1'

7 )ducation and research 7.1 7.:&

: Trade 7.4 7.7

1 +torage and warehousing 7.3: &.613 Railway transport services 7.6 &.34

< ;edical and health 7.64 &.31

6 ommunication 7.1 &.37

4 Tourism 7.<: &.1<

' ther services 7.7 &.:<

wnership of dwellings &.4 &.76

& ther transport services 7.7< &.7<

7 %anking 7.4 &.77

: Insurance 7.'6 &.:

1 +oftware :.73 .&<

Source: @9)'? *%%&

)vidence for India demonstrates the importance of credible regulatory intervention and competition indriving prices of *s and I2s to reflect their true cost. In doing so, substantial benefit has been reaped by user industries such as IT and %2s. In addition, analysis by the onfederation of Indian Industry /ational %roadband )conomy ommittee shows that the total present value (&'':! of benefit to the Indianeconomy due to growth from broadband is e9pected to be E+4' billion for the years &'' = &'&', with anL additional growth in labor productivity. %roadband growth is, inter alia, contingent upon availabilityand price of infrastructure. 8ccording to II this activity is e9pected to launch new business lines andincreased efficiency in e9isting businesses, leading to direct employment of .6 million and totalemployment of 3& million by &'&'.

1

8/11/2019 Kathuria Rajat

http://slidepdf.com/reader/full/kathuria-rajat 16/40

7o6 -: Key <rowth Dri4ers of Indian I2E*07P8 E6ports

=+undant 2alent5 India#s young demographic profile is an inherent advantage complemented by an

academic infrastructure that generates a large pool of )nglish speaking talent. Talent suitabilityconcerns are being addressed through a combination of government, academia and industry ledinitiatives. These initiatives include national rollout of skill certification through /8 (/8++;

8ssessment of ompetence!, setting up finishing schools in association ;-R* to supplementgraduate education with training in specific technology areas and soft skills and ;oE#s with educationagencies like EC and 8IT) to facilitate industry inputs on curriculum and teaching and developfaculty development programme.

*ustained cost competiti4eness5 India has a strong track record of delivering a significant cost

advantage, with clients regularly reporting savings of &151' percent over the original cost base. Theability to achieve such high levels of cost advantage by sourcing services from India is driven primarily by the ability to access highly skilled talent at significantly lower wage costs and theresultant productivity gains derived from having a very competent employee base. )his is further

complemented !y relative advantages in other elements of the cost structure 3e#g# telecom6 that

contri!ute to IndiaGs cost competitiveness E even when compared to other low-cost destinations.

Continued focus on >uality5 *emonstrated process quality and e9pertise in service delivery has been

a key factor driving India#s sustained leadership in global service delivery. +ince the inception of theindustry in India, players within the country have been focusing on quality initiatives, to alignthemselves with international standards. ver the years, the industry has built robust processes and procedures to offer world class IT software and technology related services.

?orld class information security en4ironment5 +takeholders of Indian %2 recognise fool proof

security as an indispensable element of global service delivery. Individual firm level efforts arecomplemented by a comprehensive policy framework established by Indian authorities, which has builta strong foundation for an "info5secure# environment in the country. These include strengthening theregulatory framework through proposed amendments to further strengthen the IT 8ct &''', scaling upthe cyber lab initiative, scaling up the /ational +kills Registry (/+R! and establishing a self regulatoryorganisation.

Rapid growth in @ey +usiness infrastructure5 Rapid growth in key business infrastructure has

ensured unhindered growth and e9pansion of this sector. )he ,P2 sector has !een a key !eneficiarywith the cost of international connectivity declining rapidly and service level improving significantly#

)he growth is taking place not only in existing ur!an centres !ut increasingly in satellite towns and

smaller cities# ritical !usiness infrastructure such as telecom and commercial real estate is well in

placeH improving other supporting infrastructure a key priority for the government# S)PI infrastructureavaila!le across the country and magnitude of investments shows government support to the industry#

Ena+ling 7usiness policy and Regulatory en4ironment5 The enabling policy environment in India

was instrumental in cataly>ing the early phases of growth in this sector. 2olicy makers in India havelaid special emphasis on encouraging foreign participation in most sectors of the economy, recognisingits importance not only as a source of financial capital but also as a facilitator of knowledge andtechnology transfer. The Indian IT)+5%2 sector has benefited from this approach, with participatingfirms enDoying minimal regulatory and policy restrictions along with a broad range of fiscal and procedural incentives.

+ource /asscom &''< Indian ITES-BPO Industry – Fact Sheet ( 5mphases added6

3

8/11/2019 Kathuria Rajat

http://slidepdf.com/reader/full/kathuria-rajat 17/40

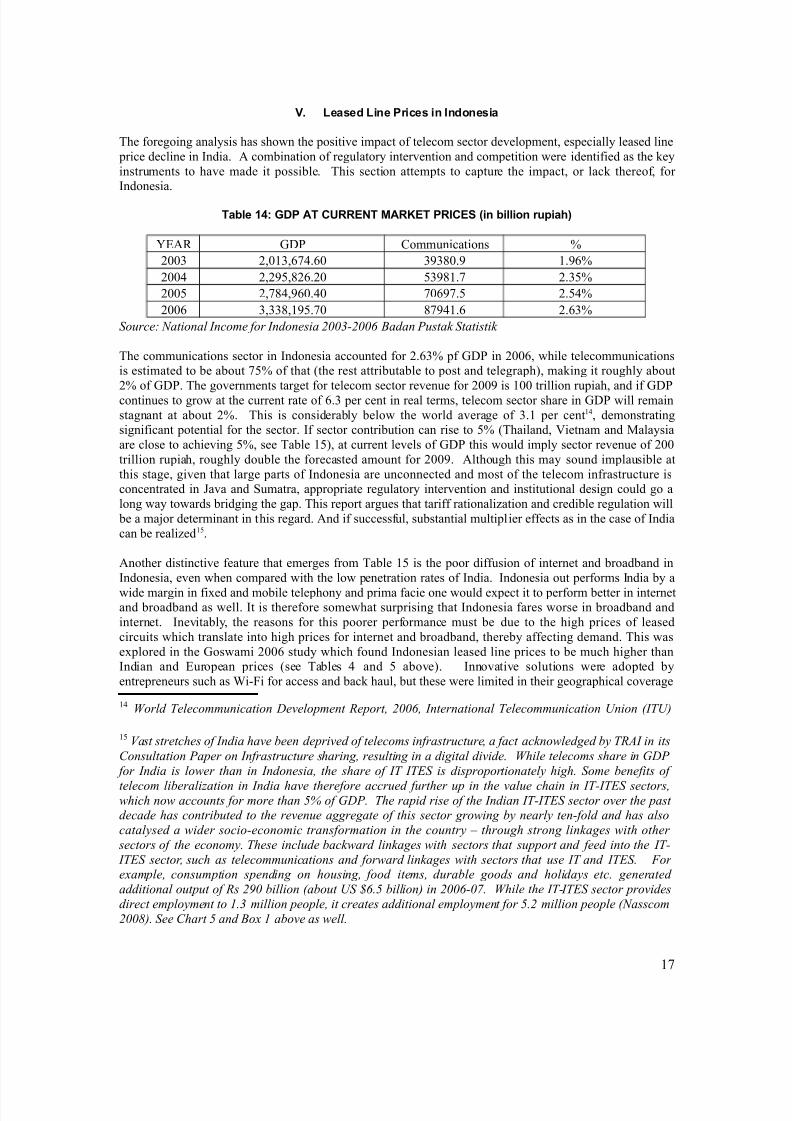

V. Lease% Li"e Prices i" I"%"esia

The foregoing analysis has shown the positive impact of telecom sector development, especially leased line price decline in India. 8 combination of regulatory intervention and competition were identified as the keyinstruments to have made it possible. This section attempts to capture the impact, or lack thereof, for Indonesia.

Table 1/: <DP AT C)**ENT MA*+ET P*ICES 5i" billi" rupia36

)8R C*2 ommunications L

&''7 &,'7,3<:.3' 7476'.4 .43L

&'': &,&41,6&3.&' 1746.< &.71L

&''1 &,<6:,43'.:' <'34<.1 &.1:L

&''3 7,776,41.<' 6<4:.3 &.37L

Source: 9ational Income for Indonesia *%%-*%%A ,adan Pustak Statistik

The communications sector in Indonesia accounted for &.37L pf C*2 in &''3, while telecommunicationsis estimated to be about <1L of that (the rest attributable to post and telegraph!, making it roughly about&L of C*2. The governments target for telecom sector revenue for &''4 is '' trillion rupiah, and if C*2continues to grow at the current rate of 3.7 per cent in real terms, telecom sector share in C*2 will remainstagnant at about &L. This is considerably below the world average of 7. per cent:, demonstratingsignificant potential for the sector. If sector contribution can rise to 1L (Thailand, ?ietnam and ;alaysiaare close to achieving 1L, see Table 1!, at current levels of C*2 this would imply sector revenue of &''trillion rupiah, roughly double the forecasted amount for &''4. 8lthough this may sound implausible atthis stage, given that large parts of Indonesia are unconnected and most of the telecom infrastructure isconcentrated in 0ava and +umatra, appropriate regulatory intervention and institutional design could go along way towards bridging the gap. This report argues that tariff rationali>ation and credible regulation will be a maDor determinant in this regard. 8nd if successful, substantial multiplier effects as in the case of Indiacan be reali>ed1.

8nother distinctive feature that emerges from Table 1 is the poor diffusion of internet and broadband inIndonesia, even when compared with the low penetration rates of India. Indonesia out performs India by a

wide margin in fi9ed and mobile telephony and prima facie one would e9pect it to perform better in internetand broadband as well. It is therefore somewhat surprising that Indonesia fares worse in broadband andinternet. Inevitably, the reasons for this poorer performance must be due to the high prices of leasedcircuits which translate into high prices for internet and broadband, thereby affecting demand. This wase9plored in the Coswami &''3 study which found Indonesian leased line prices to be much higher thanIndian and )uropean prices (see Tables : and 1 above!. Innovative solutions were adopted byentrepreneurs such as $i5Ai for access and back haul, but these were limited in their geographical coverage

: <orld )elecommunication ?evelopment Report *%%A International )elecommunication @nion 3I)@6

1 Jast stretches of India have !een deprived of telecoms infrastructure a fact acknowledged !y )R'I in its

onsultation Paper on Infrastructure sharing resulting in a digital divide# <hile telecoms share in 4?P

for India is lower than in Indonesia the share of I) I)5S is disproportionately high# Some !enefits of

telecom li!eraliation in India have therefore accrued further up in the value chain in I)-I)5S sectorswhich now accounts for more than 0 of 4?P# )he rapid rise of the Indian I)-I)5S sector over the past decade has contri!uted to the revenue aggregate of this sector growing !y nearly ten-fold and has also

catalysed a wider socio-economic transformation in the country E through strong linkages with other

sectors of the economy# )hese include !ackward linkages with sectors that support and feed into the I)-

I)5S sector such as telecommunications and forward linkages with sectors that use I) and I)5S# 7or example consumption spending on housing food items dura!le goods and holidays etc# generated

additional output of Rs */% !illion 3a!out @S MA#0 !illion6 in *%%A-%+# <hile the I)-I)5S sector provides

direct employment to .# million people it creates additional employment for 0#* million people 39asscom

*%%&6# See hart 0 and ,ox . a!ove as well#

<

8/11/2019 Kathuria Rajat

http://slidepdf.com/reader/full/kathuria-rajat 18/40

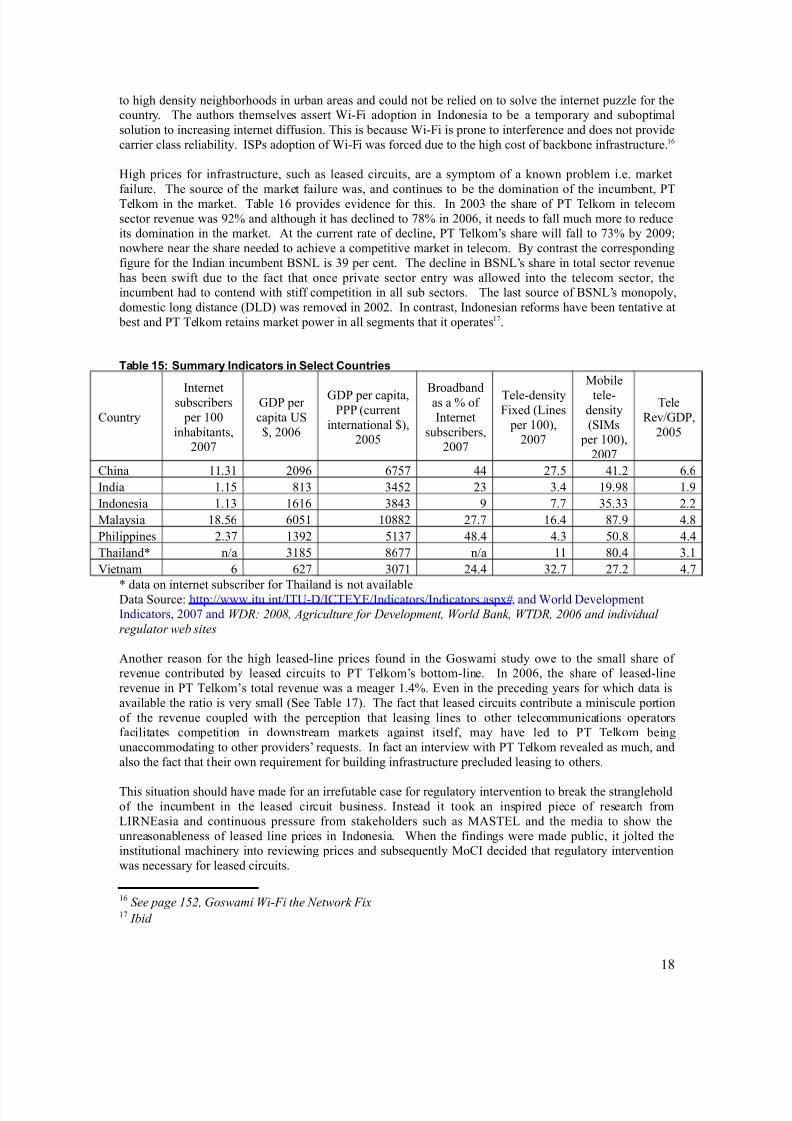

to high density neighborhoods in urban areas and could not be relied on to solve the internet pu>>le for thecountry. The authors themselves assert $i5Ai adoption in Indonesia to be a temporary and suboptimalsolution to increasing internet diffusion. This is because $i5Ai is prone to interference and does not providecarrier class reliability. I+2s adoption of $i5Ai was forced due to the high cost of backbone infrastructure.3

-igh prices for infrastructure, such as leased circuits, are a symptom of a known problem i.e. marketfailure. The source of the market failure was, and continues to be the domination of the incumbent, 2TTelkom in the market. Table 3 provides evidence for this. In &''7 the share of 2T Telkom in telecomsector revenue was 4&L and although it has declined to <6L in &''3, it needs to fall much more to reduceits domination in the market. 8t the current rate of decline, 2T Telkom#s share will fall to <7L by &''4nowhere near the share needed to achieve a competitive market in telecom. %y contrast the correspondingfigure for the Indian incumbent %+/ is 74 per cent. The decline in %+/#s share in total sector revenuehas been swift due to the fact that once private sector entry was allowed into the telecom sector, theincumbent had to contend with stiff competition in all sub sectors. The last source of %+/#s monopoly,domestic long distance (**! was removed in &''&. In contrast, Indonesian reforms have been tentative at best and 2T Telkom retains market power in all segments that it operates<.

Table 1: SummarB I"%icatrs i" Select Cu"tries

ountry

Internetsubscribers per ''

inhabitants,&''<

C*2 per capita E+, &''3

C*2 per capita,222 (current

international !,&''1

%roadbandas a L of Internet

subscribers,&''<

Tele5densityAi9ed (ines per ''!,

&''<

;obile

tele5density(+I;s

per ''!,&''<

TeleRevJC*2,

&''1

hina .7 &'43 3<1< :: &<.1 :.& 3.3

India .1 67 7:1& &7 7.: 4.46 .4

Indonesia .7 33 76:7 4 <.< 71.77 &.&

;alaysia 6.13 3'1 '66& &<.< 3.: 6<.4 :.6

2hilippines &.7< 74& 17< :6.: :.7 1'.6 :.:

ThailandM nJa 761 63<< nJa 6'.: 7.

?ietnam 3 3&< 7'< &:.: 7&.< &<.& :.<

M data on internet subscriber for Thailand is not available*ata +ource httpJJwww.itu.intJITE5*JIT))JIndicatorsJIndicators.asp9U, and $orld *evelopmentIndicators, &''< and <?R: *%%& 'griculture for ?evelopment <orld ,ank <)?R *%%A and individual

regulator we! sites

8nother reason for the high leased5line prices found in the Coswami study owe to the small share of revenue contributed by leased circuits to 2T Telkom#s bottom5line. In &''3, the share of leased5linerevenue in 2T Telkom#s total revenue was a meager .:L. )ven in the preceding years for which data isavailable the ratio is very small (+ee Table <!. The fact that leased circuits contribute a miniscule portionof the revenue coupled with the perception that leasing lines to other telecommunications operatorsfacilitates competition in downstream markets against itself, may have led to 2T Telkom beingunaccommodating to other providers# requests. In fact an interview with 2T Telkom revealed as much, andalso the fact that their own requirement for building infrastructure precluded leasing to others.

This situation should have made for an irrefutable case for regulatory intervention to break the strangleholdof the incumbent in the leased circuit business. Instead it took an inspired piece of research fromIR/)asia and continuous pressure from stakeholders such as ;8+T) and the media to show theunreasonableness of leased line prices in Indonesia. $hen the findings were made public, it Dolted theinstitutional machinery into reviewing prices and subsequently ;oI decided that regulatory interventionwas necessary for leased circuits.

3 See page .0* 4oswami <i-7i the 9etwork 7ix< I!id

6

8/11/2019 Kathuria Rajat

http://slidepdf.com/reader/full/kathuria-rajat 19/40

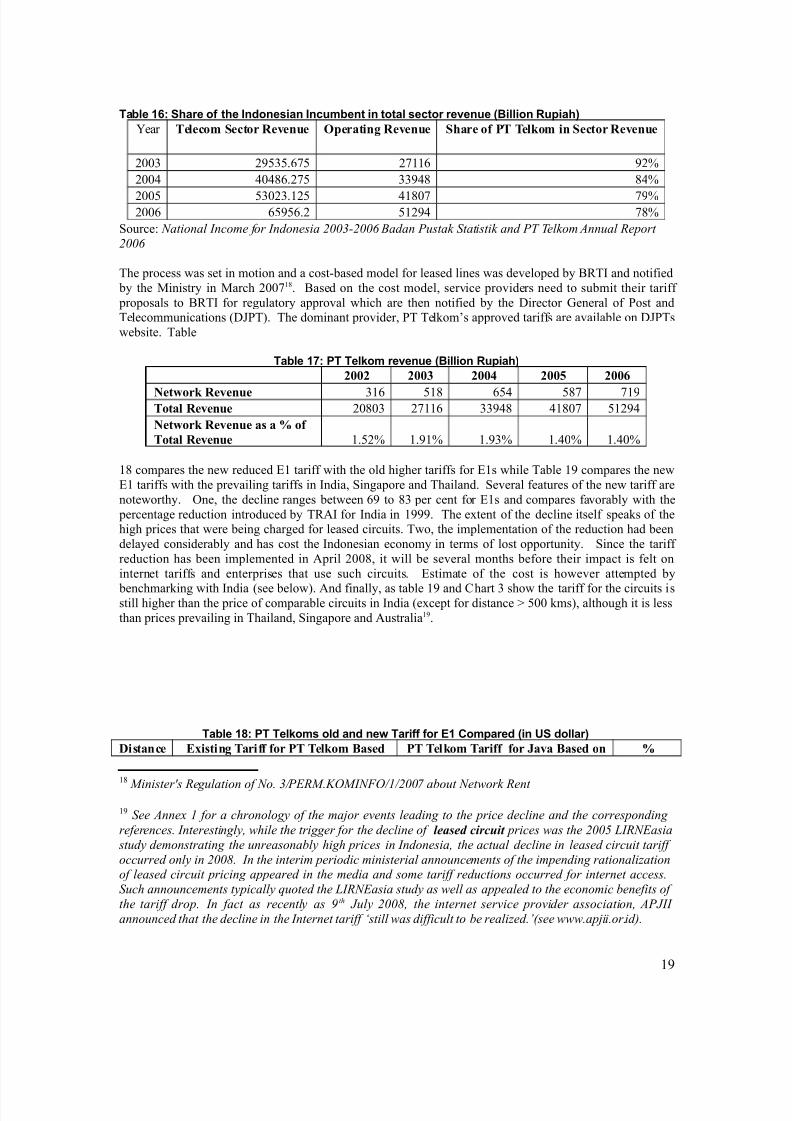

Table 14: S3are # t3e I"%"esia" I"cumbe"t i" ttal sectr re!e"ue 59illi" *upia36

ear 2elecom *ector Re4enue 8perating Re4enue *hare of P2 2el@om in *ector Re4enue

&''7 &4171.3<1 &<3 4&L

&'': :':63.&<1 774:6 6:L

&''1 17'&7.&1 :6'< <4L&''3 31413.& 1&4: <6L

+ource 9ational Income for Indonesia *%%-*%%A ,adan Pustak Statistik and P) )elkom 'nnual Report

*%%A

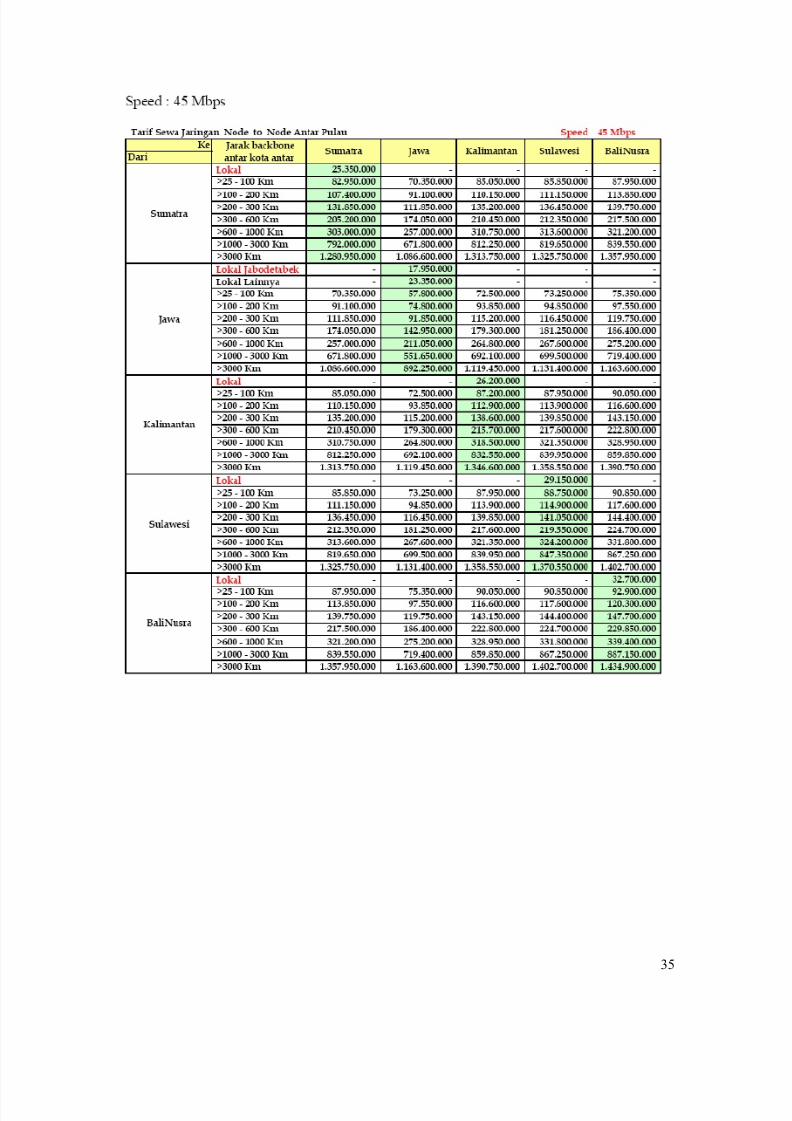

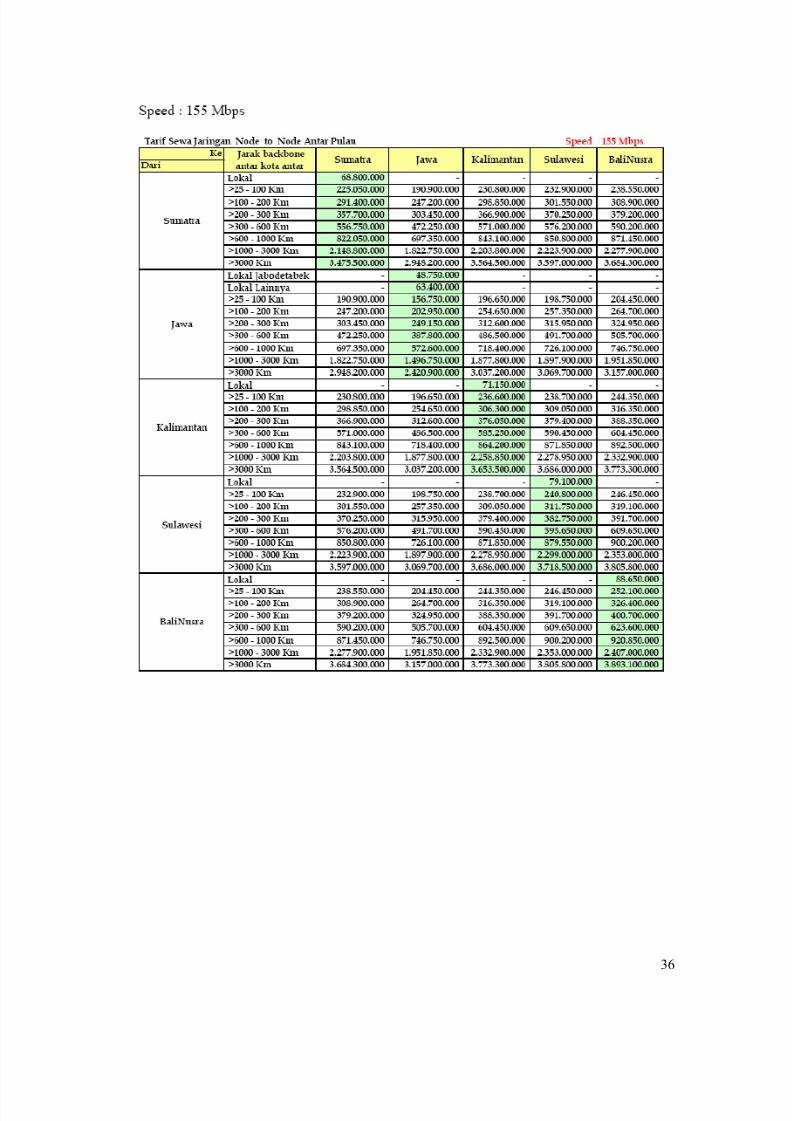

The process was set in motion and a cost5based model for leased lines was developed by %RTI and notified by the ;inistry in ;arch &''<6. %ased on the cost model, service providers need to submit their tariff proposals to %RTI for regulatory approval which are then notified by the *irector Ceneral of 2ost andTelecommunications (*02T!. The dominant provider, 2T Telkom#s approved tariffs are available on *02Tswebsite. Table

Table 1>: PT Tel'm re!e"ue 59illi" *upia36

!! !! !!" !!# !!$

3etwor@ Re4enue 73 16 31: 16< <42otal Re4enue &'6'7 &<3 774:6 :6'< 1&4:

3etwor@ Re4enue as a A of

2otal Re4enue .1&L .4L .47L .:'L .:'L

6 compares the new reduced ) tariff with the old higher tariffs for )s while Table 4 compares the new) tariffs with the prevailing tariffs in India, +ingapore and Thailand. +everal features of the new tariff arenoteworthy. ne, the decline ranges between 34 to 67 per cent for )s and compares favorably with the percentage reduction introduced by TR8I for India in 444. The e9tent of the decline itself speaks of thehigh prices that were being charged for leased circuits. Two, the implementation of the reduction had beendelayed considerably and has cost the Indonesian economy in terms of lost opportunity. +ince the tariff reduction has been implemented in 8pril &''6, it will be several months before their impact is felt oninternet tariffs and enterprises that use such circuits. )stimate of the cost is however attempted by

benchmarking with India (see below!. 8nd finally, as table 4 and hart 7 show the tariff for the circuits isstill higher than the price of comparable circuits in India (e9cept for distance V 1'' kms!, although it is lessthan prices prevailing in Thailand, +ingapore and 8ustralia4.

Table 1: PT Tel'ms l% a"% "e& Tari## #r E1 Cmpare% 5i" )S %llar6

Distance E6isting 2ariff for P2 2el@om 7ased P2 2el@om 2ariff for Ba4a 7ased on A

6

8inister1s Regulation of 9o# "P5R8#K28I972"."*%%+ a!out 9etwork Rent

4 See 'nnex . for a chronology of the major events leading to the price decline and the corresponding

references# Interestingly while the trigger for the decline of leased circuit prices was the *%%0 LIR95asia

study demonstrating the unreasona!ly high prices in Indonesia the actual decline in leased circuit tariff

occurred only in *%%&# In the interim periodic ministerial announcements of the impending rationaliationof leased circuit pricing appeared in the media and some tariff reductions occurred for internet access#

Such announcements typically =uoted the LIR95asia study as well as appealed to the economic !enefits of

the tariff drop# In fact as recently as /th (uly *%%& the internet service provider association 'P(II

announced that the decline in the Internet tariff Nstill was difficult to !e realied#G3see www#apjii#or#id6#

4

8/11/2019 Kathuria Rajat

http://slidepdf.com/reader/full/kathuria-rajat 20/40

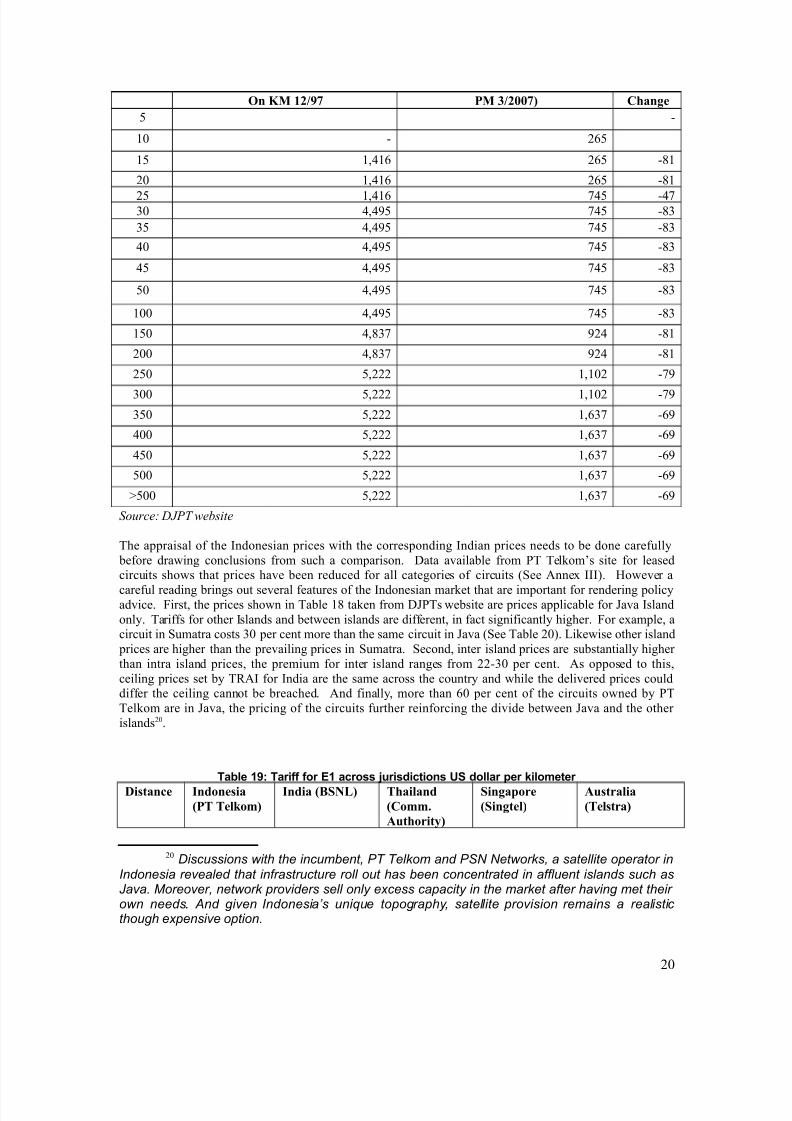

8n K1 -/% P1 !!%( Change

1 5

' 5 &31

1 ,:3 &31 56

&' ,:3 &31 56

&1 ,:3 <:1 5:<7' :,:41 <:1 567

71 :,:41 <:1 567

:' :,:41 <:1 567

:1 :,:41 <:1 567

1' :,:41 <:1 567

'' :,:41 <:1 567

1' :,67< 4&: 56

&'' :,67< 4&: 56

&1' 1,&&& ,'& 5<4

7'' 1,&&& ,'& 5<4

71' 1,&&& ,37< 534

:'' 1,&&& ,37< 534

:1' 1,&&& ,37< 534

1'' 1,&&& ,37< 534

V1'' 1,&&& ,37< 534

Source: ?(P) we!site

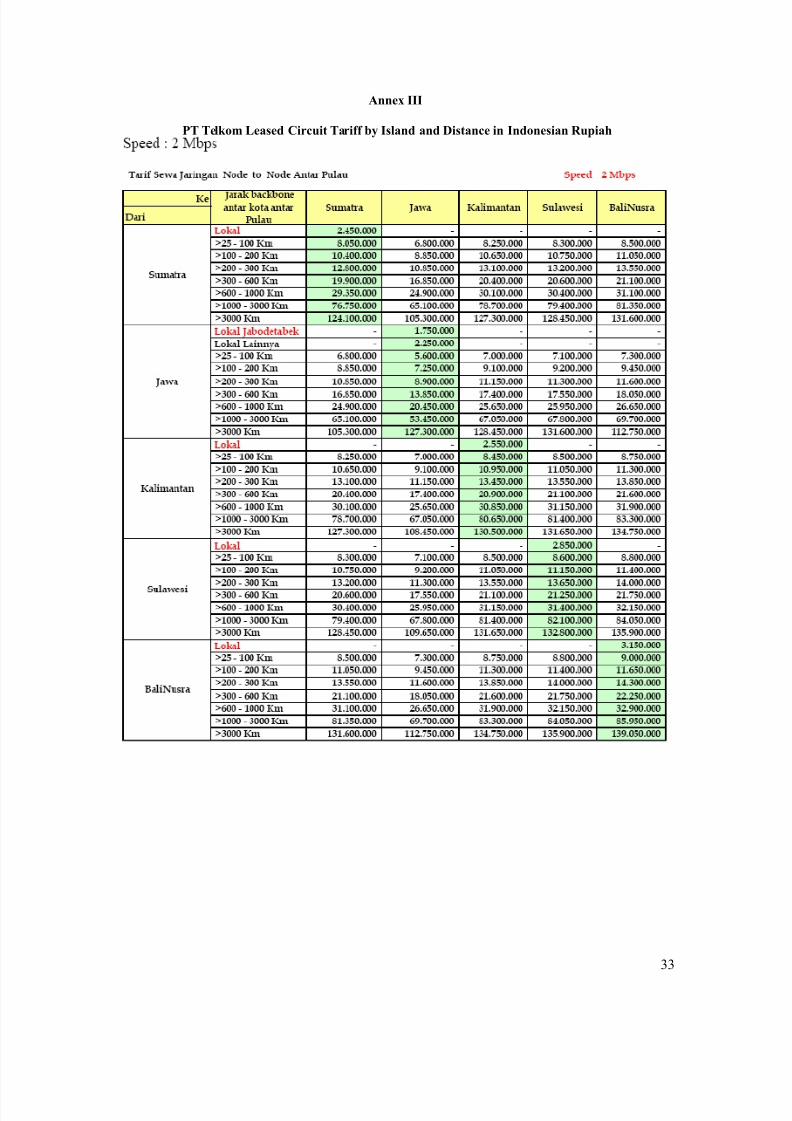

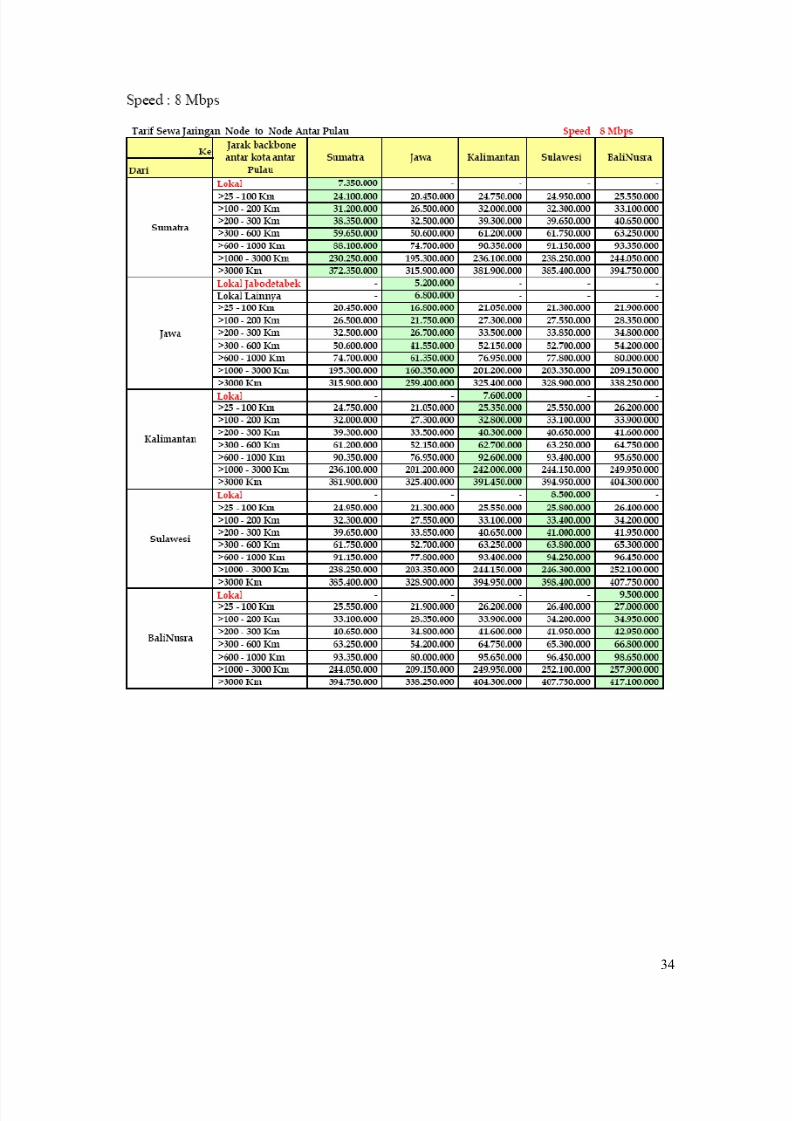

The appraisal of the Indonesian prices with the corresponding Indian prices needs to be done carefully before drawing conclusions from such a comparison. *ata available from 2T Telkom#s site for leasedcircuits shows that prices have been reduced for all categories of circuits (+ee 8nne9 III!. -owever a

careful reading brings out several features of the Indonesian market that are important for rendering policyadvice. Airst, the prices shown in Table 6 taken from *02Ts website are prices applicable for 0ava Islandonly. Tariffs for other Islands and between islands are different, in fact significantly higher. Aor e9ample, acircuit in +umatra costs 7' per cent more than the same circuit in 0ava (+ee Table &'!. ikewise other island prices are higher than the prevailing prices in +umatra. +econd, inter island prices are substantially higher than intra island prices, the premium for inter island ranges from &&57' per cent. 8s opposed to this,ceiling prices set by TR8I for India are the same across the country and while the delivered prices coulddiffer the ceiling cannot be breached. 8nd finally, more than 3' per cent of the circuits owned by 2TTelkom are in 0ava, the pricing of the circuits further reinforcing the divide between 0ava and the other islands&'.

Table 1: Tari## #r E1 acrss uris%icti"s )S %llar per 'ilmeter

Distance Indonesia

'P2 2el@om(

India '7*3L( 2hailand

'Comm.

=uthority(

*ingapore

'*ingtel(

=ustralia

'2elstra(

&' Discussions with the incumbent, PT Telkom and PSN Networks, a satellite operator inIndonesia revealed that infrastructure roll out has been concentrated in affluent islands such asJava. oreover, network providers sell onl! e"cess capacit! in the market after havin# met their own needs. $nd #iven Indonesia%s uni&ue topo#raph!, satellite provision remains a realistic thou#h e"pensive option.

&'

8/11/2019 Kathuria Rajat

http://slidepdf.com/reader/full/kathuria-rajat 21/40

1 &31 73 ,1'7 &,6& ,46&

' &31 17 ,1'7 &,6& &,7:6

1 &31 <' ,1'7 &,6& &,<:

&' &31 6< ,1'7 &,6& &,41&

&1 <:1 '1 ,1'7 &,6& 7,4'

7' <:1 && ,1'7 &,6& 7,:&6

71 <:1 74 ,1'7 &,6& 7,333:' <:1 13 ,1'7 &,6& 7,4':

:1 <:1 <7 ,1'7 &,6& :,:7

1' <:1 41 ,1'7 &,6& :,76

'' <:1 7<& ,1'7 &,6& 1,&&4

1' 4&: 1:6 ,1'7 &,6& 1,&&4

&'' 4&: <&1 &,11 &,6& 3,::

&1' ,'& 4' &,11 &,6& 6,'6

7'' ,'& ,'<6 &,11 &,6& 6,'6

71' ,37< ,&1: 7,6'7 &,6& 6,'6

:'' ,37< ,:7 7,6'7 &,6& 4,111

:1' ,37< ,3'6 7,6'7 &,6& 4,111

1'' ,37< ,<6: 7,6'7 &,6& ,:<V1'' ,37< ,<4' 7,6'7 &,6& ,:<

*ate <58pr5'6 5/ov5'< 5ct544 5/ov5'3 5/ov5'<

+ource Telkom Teligen Teligen Teligen Teligen

Source: 's reported !y ?(P) accessed from www#dgpostel#id

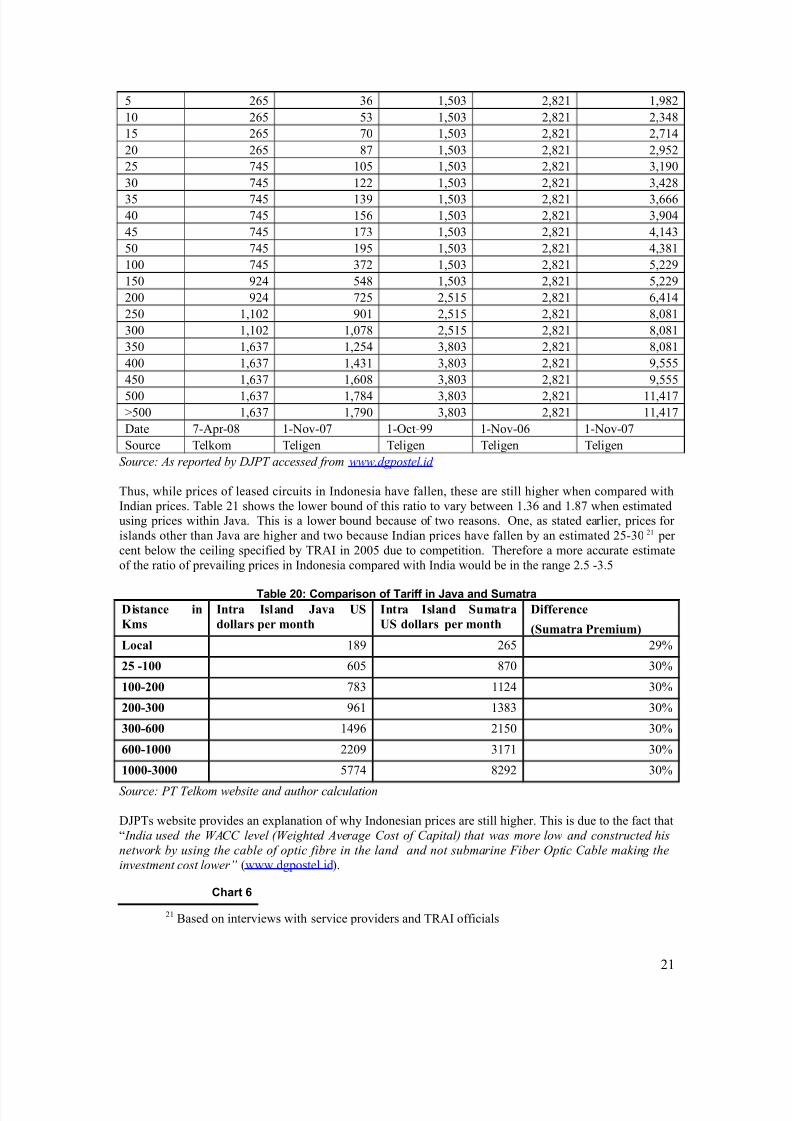

Thus, while prices of leased circuits in Indonesia have fallen, these are still higher when compared withIndian prices. Table & shows the lower bound of this ratio to vary between .73 and .6< when estimatedusing prices within 0ava. This is a lower bound because of two reasons. ne, as stated earlier, prices for islands other than 0ava are higher and two because Indian prices have fallen by an estimated &157' & per cent below the ceiling specified by TR8I in &''1 due to competition. Therefore a more accurate estimateof the ratio of prevailing prices in Indonesia compared with India would be in the range &.1 57.1

Table -: Cmparis" # Tari## i" a!a a"% Sumatra

Distance in

Kms

Intra Island Ba4a ,*

dollars per month

Intra Island *umatra

,* dollars per month

Difference

'*umatra Premium(

Local 64 &31 &4L

# 0-!! 3'1 6<' 7'L

-!!0!! <67 &: 7'L

!!0!! 43 767 7'L

!!0$!! :43 &1' 7'L

$!!0-!!! &&'4 7< 7'L

-!!!0!!! 1<<: 6&4& 7'L

Source: P) )elkom we!site and author calculation

*02Ts website provides an e9planation of why Indonesian prices are still higher. This is due to the fact thatF India used the <' level 3<eighted 'verage ost of apital6 that was more low and constructed his

network !y using the ca!le of optic fi!re in the land and not su!marine 7i!er 2ptic a!le making the

investment cost lowerC (www.dgpostel.id!.

C3art 4

& %ased on interviews with service providers and TR8I officials

&

8/11/2019 Kathuria Rajat

http://slidepdf.com/reader/full/kathuria-rajat 22/40

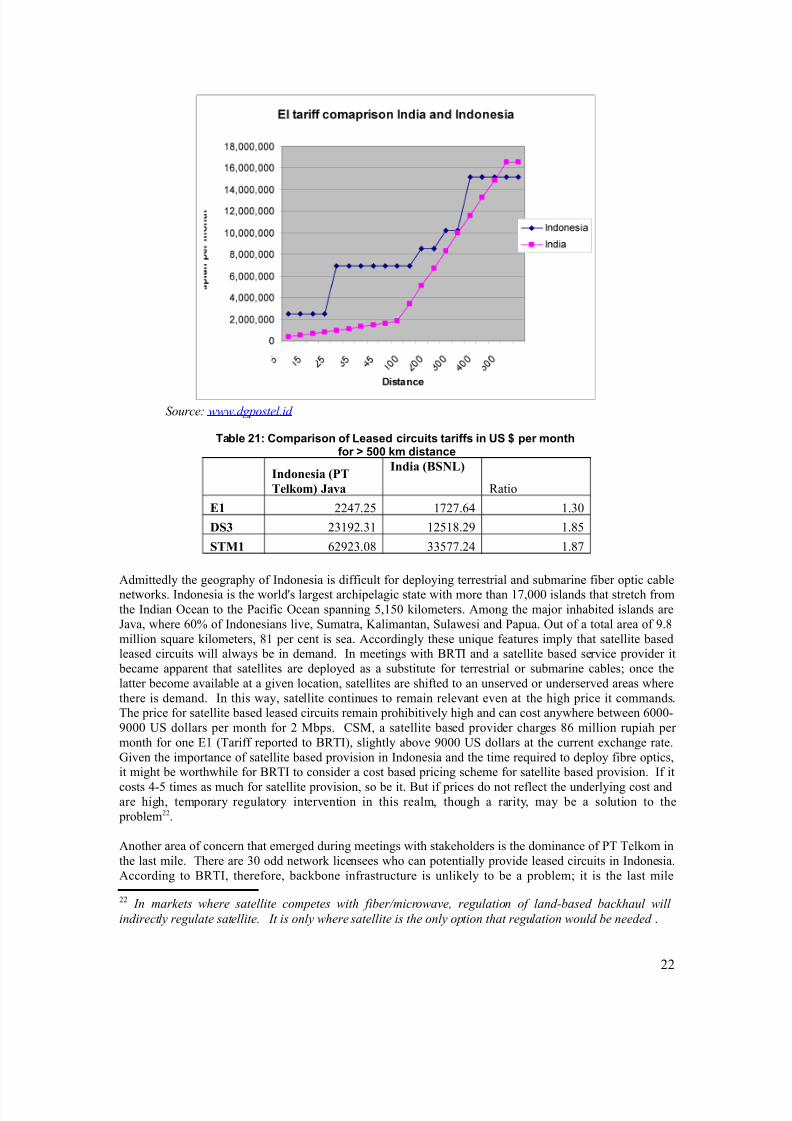

Source: www#dgpostel#id

Table -1: Cmparis" # Lease% circuits tari##s i" )S per m"t3#r ? 'm %ista"ce

Indonesia 'P2

2el@om( Ba4a

India '7*3L(

Ratio

E- &&:<.&1 <&<.3: .7'

D* &74&.7 &16.&4 .61

*21- 3&4&7.'6 771<<.&: .6<

8dmittedly the geography of Indonesia is difficult for deploying terrestrial and submarine fiber optic cablenetworks. Indonesia is the worldKs largest archipelagic state with more than <,''' islands that stretch fromthe Indian cean to the 2acific cean spanning 1,1' kilometers. 8mong the maDor inhabited islands are0ava, where 3'L of Indonesians live, +umatra, Salimantan, +ulawesi and 2apua. ut of a total area of 4.6million square kilometers, 6 per cent is sea. 8ccordingly these unique features imply that satellite basedleased circuits will always be in demand. In meetings with %RTI and a satellite based service provider it became apparent that satellites are deployed as a substitute for terrestrial or submarine cables once thelatter become available at a given location, satellites are shifted to an unserved or underserved areas wherethere is demand. In this way, satellite continues to remain relevant even at the high price it commands.The price for satellite based leased circuits remain prohibitively high and can cost anywhere between 3'''54''' E+ dollars per month for & ;bps. +;, a satellite based provider charges 63 million rupiah per month for one ) (Tariff reported to %RTI!, slightly above 4''' E+ dollars at the current e9change rate.Civen the importance of satellite based provision in Indonesia and the time required to deploy fibre optics,it might be worthwhile for %RTI to consider a cost based pricing scheme for satellite based provision. If it

costs :51 times as much for satellite provision, so be it. %ut if prices do not reflect the underlying cost andare high, temporary regulatory intervention in this realm, though a rarity, may be a solution to the problem&&.

8nother area of concern that emerged during meetings with stakeholders is the dominance of 2T Telkom inthe last mile. There are 7' odd network licensees who can potentially provide leased circuits in Indonesia.8ccording to %RTI, therefore, backbone infrastructure is unlikely to be a problem it is the last mile

&& In markets where satellite competes with fi!er"microwave regulation of land-!ased !ackhaul will

indirectly regulate satellite# It is only where satellite is the only option that regulation would !e needed .

&&

8/11/2019 Kathuria Rajat

http://slidepdf.com/reader/full/kathuria-rajat 23/40

dominance of 2T Telkom that needs to be addressed. -istory of telecom liberali>ation across the world hasdemonstrated the difficulty of making incumbents offer fair terms to potential rivals, unless forced by toughregulatory measures. )vidence from fcom and %ritain may provide a pointer for the ne9t step necessaryin Indonesia in this regard G+ee %o9 &H. There is agreement across the industry that Finfrastructure5basedcompetitionPBin other words, more network providers is the way forward. Indonesia has that part in place.%RTI should now get 2T Telkom to adopt Flocal loop unbundlingP (E! to open up the last mile at fair and reasonable terms. Rival I+2 operators can thereby install or lease equipment for backbone and lease2T Telkom#s lines for the Flast mileP to the subscriber at cost based rates to be determined by theregulator .&7 )9perience across the world however shows conditions for successfully introducing E aree9acting and are unlikely to be met in Indonesia.

7o6 : ?hy 72 has suddenly decided to cut its wholesale prices

-as A;, %ritainKs new communications regulator, won its first victory over %T, by scaring it intomaking huge price cutsW It certainly looks that way. n ;ay <th, %T announced dramatic reductionsBof up to <'LBin the prices it charges rival operators that offer high5speed (broadband! internet links over itsnetwork. The announcement came days after A; unveiled the first of several reports into the state of %ritainKs telecoms market, in which it criticised %TKs high wholesale prices and alluded to the possibility of breaking the company up. Is that what prompted %T to cut its pricesW

ertainly not, sniffs %T. $hile its actions might appear to have been prompted by fear of break5up, it saysit was responding not to A;Ks stick, but to its carrot. 8t the moment, %T shares its network with rival broadband providers in three ways. Airst, it offers them its own broadband services on a wholesale basis,for resale under their own brands. %T makes a good margin, and the rival operator does not have to buildanything. f the &m or so broadband connections delivered over telephone lines in %ritain, %T retailsaround half of them itself, and acts as a wholesaler for the rest in this way. +econd, under a scheme calledFlocal loop unbundlingP (E!, the rival operator can install its own equipment in local e9changes and

&7 @n!undling has !een made to work in a num!er of countries with relatively dense and

well developed traditional copper networks# >owever the conditions have !een exacting re=uiring:

customisation for the national market alternative operators to enter the market medium‐term legal

certainty for those operator the incum!ent operator to !e sufficiently restrained a powerful regulator tomonitor progress and pu!lish statistics a rapid appeals process to avoid lengthy delays and a continuing

refinement of the regulations# )he greatest risk has !een in the nightmare of regulatory gamesmanship

played !y certain incum!ent operators# See @n!undling local loops: glo!al experiences 5wan Sutherland

Link entre *%%+ accessed from http:""link#wits#ac#a"papers"LI9K#pdf

.

&7

8/11/2019 Kathuria Rajat

http://slidepdf.com/reader/full/kathuria-rajat 24/40

lease %TKs lines for the Flast mileP from the e9change to the subscriber. This involves a lot more investment Brival operators need their own high5speed FbackbonesP to link up the e9changesBbut allows them todifferentiate themselves from %T. Eptake of E has, however, been slow fewer than ',''' lines have been unbundled. ast week, %T said it would reduce the prices of unbundled loops by around 71L from0une st, with further cuts to come. %ut while the monthly cost per unbundled loop has fallen, the set5upcharge for each one is still 1'L above the )uropean average, says +erafino 8bate of vum, a consultancy.

+o there is room for more cuts. 8nd while revenue per loop will fall, %T should benefit as the overallmarket grows. %TKs aim is to encourage rival operators to pursue E and not its third broadband service,called *ata+tream. This is a halfway house between the first two options, forced on %T by regulators, inwhich rival operators use %TKs backbone as well as their own infrastructure, providing some scope for differentiation. %T says this is unfair, since it allows its rivals to piggyback on the whi>>y new backbone itis now building. It would much rather its rivals simply resold its broadband products, or built their own backbones and used E. $ith its new E prices, says 8ndrew *arley of I/C, an investment bank, %Thas now made E cheaper than *ata+tream. It has done so because fcom has said that if E takes off,it might rela9 the regulatory requirements around *ata+tream. It is this carrot, rather than the stick of break5up, that has prompted %T to act. $hat is striking is that there is suddenly agreement across theindustry that Finfrastructure5based competitionPBin other words, more EBis the way forward. %T hashistorically been reluctant to push E, but has now decided that doing so is in its best interests.onveniently, many of the rival firms that hoped to e9ploit E have gone bust (thanks, in part, to %TKs previous delaying tactics!.

;ay &'th &'': The 5conomist

I. Impact on Internet

The primary reason for intervention in the leased circuit market by the Indonesian government was to promote usage of internet. The rate of growth of internet subscribers has in fact declined in &''<5'6 to per cent (+ee Table & above!. It is possible that the effect of the decline in leased line prices will be pass5through to internet tariff later and only thereafter affect the subscriber base. 8n announcement by theInternet 8ssociation on its website states that I+2s in Indonesia are likely to reduce tariffs from &' = :'L beginning 0une &''6, following reduction in leased line prices announced by the incumbent 2T Telkom by:3 to 6 per cent in 8pril &''6. &: ther network providers are likely to follow suit, given that new entrants

who provide backbone services will keep leased line prices aligned with 2T Telkom due to pressure fromthe ministry&1. The decline in tariff for leased circuits is based on the *ecision of the *irector Ceneral of post and telecommunications /o.1J&''6 (*02T!. 8ccording to the hairman of 820II +ylvia $.+umarlin, I+2s will reduce the internet tariff when most contracts with network providers are renewed in0une &''6. The association confirmed the decline would be Ffully implemented by ne9t year in view of thefact that all contracts of the memberKs business with the provider of the network will be finished thisyearP&3. $hile tariffs for the internet will fall, these will still remain substantially higher than the Indian prices. )ven if one assumes that tariffs will decline by up to :' L to about E+ 1' per month, these willstill remain about double the Indian price (+ee Table &&!.

Table --: Cmparis" # I"ter"et Tari##, April -

8*+ Enlimited Esage

Indonesia E+* 67

India E+* &1

&: www.apDii.or.id&1 Coswami &''3&3 I!id

&:

8/11/2019 Kathuria Rajat

http://slidepdf.com/reader/full/kathuria-rajat 25/40

Ratio of Indonesian to Indian price 7.7