Kaolin Concept Study 20210712 Final

149

Page 1 of 149 Concept Study – July 2021 Surprise Kaolin Project

Transcript of Kaolin Concept Study 20210712 Final

Page 1 of 149

Concept Study – July 2021

Surprise Kaolin Project

Page 2 of 149

Table of Contents 1. Executive Summary ........................................................................................................ 11

a) Context ........................................................................................................................ 11

b) Kaolin & Metakaolin .................................................................................................... 11

c) Business Configuration ................................................................................................ 12

d) Preliminary Economic Assessment .............................................................................. 15

e) Project Development Pathway .................................................................................... 20

f) Environmental and Permitting Considerations ........................................................... 21

g) Risks and Opportunities ............................................................................................... 22

2. Introduction .................................................................................................................... 22

a) InterGroup Mining ....................................................................................................... 22

b) The Surprise Project .................................................................................................... 22

c) Project Outline ............................................................................................................. 23

d) Kaolin Market .............................................................................................................. 24

e) Metakaolin Market and Use ........................................................................................ 24

f) Report Objective .......................................................................................................... 25

g) Use of This Report ....................................................................................................... 25

3. Reliance on Experts ........................................................................................................ 25

4. Property Description and Location ................................................................................. 27

5. Accessibility, Climate, Local Resources, Infrastructure and Physiography ..................... 28

a) Accessibility ................................................................................................................. 28

b) Climate ........................................................................................................................ 29

c) Land Use ...................................................................................................................... 29

d) Local Infrastructure ..................................................................................................... 29

6. History ............................................................................................................................ 29

a) History of Cement Development ................................................................................. 29

b) Modern Cement Chemistry ......................................................................................... 30

c) Cement Additions ........................................................................................................ 30

d) Cement Chemistry and Pozzolan Reactions ................................................................ 32

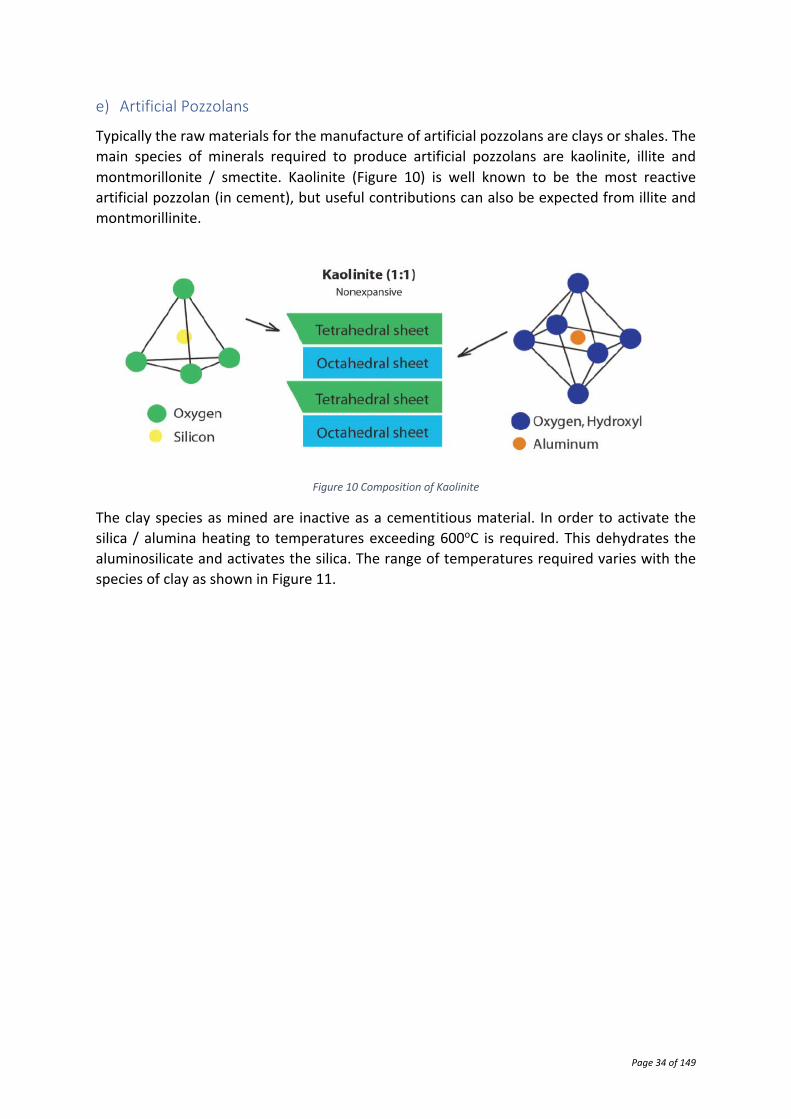

e) Artificial Pozzolans ....................................................................................................... 34

f) Metakaolin in Cement ................................................................................................. 36

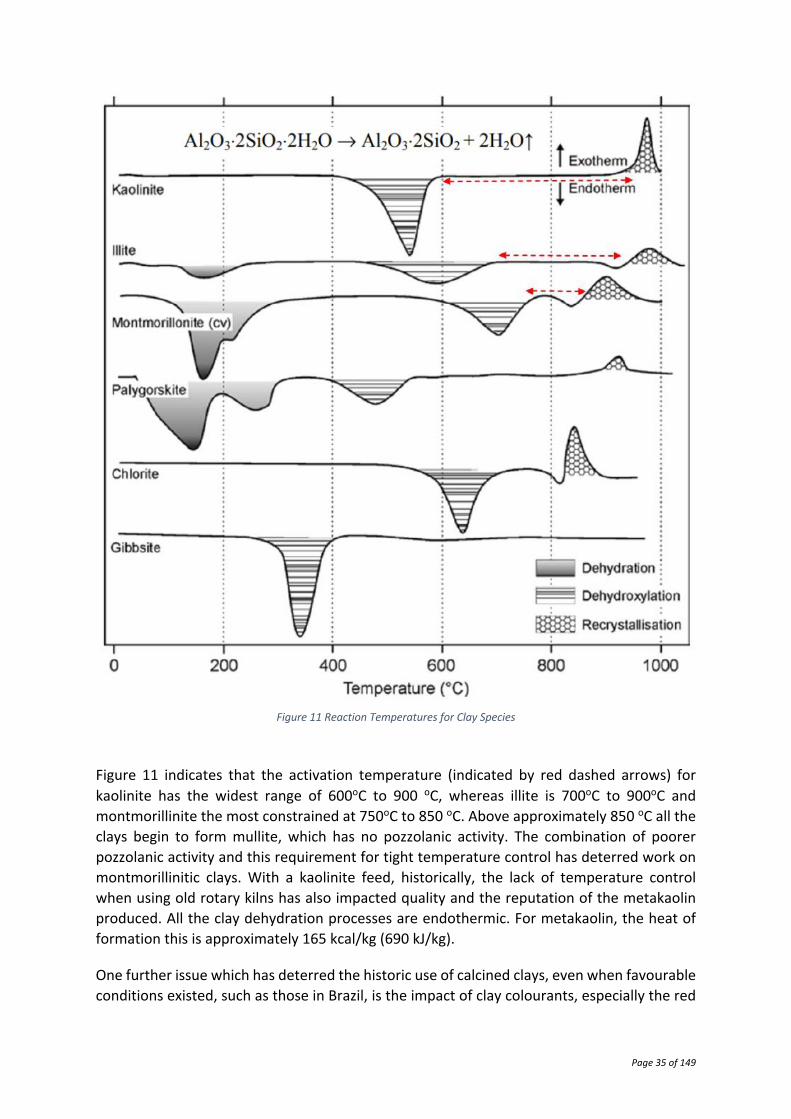

7. Geological Setting and Mineralization of the Kaolin Deposits ....................................... 37

Page 3 of 149

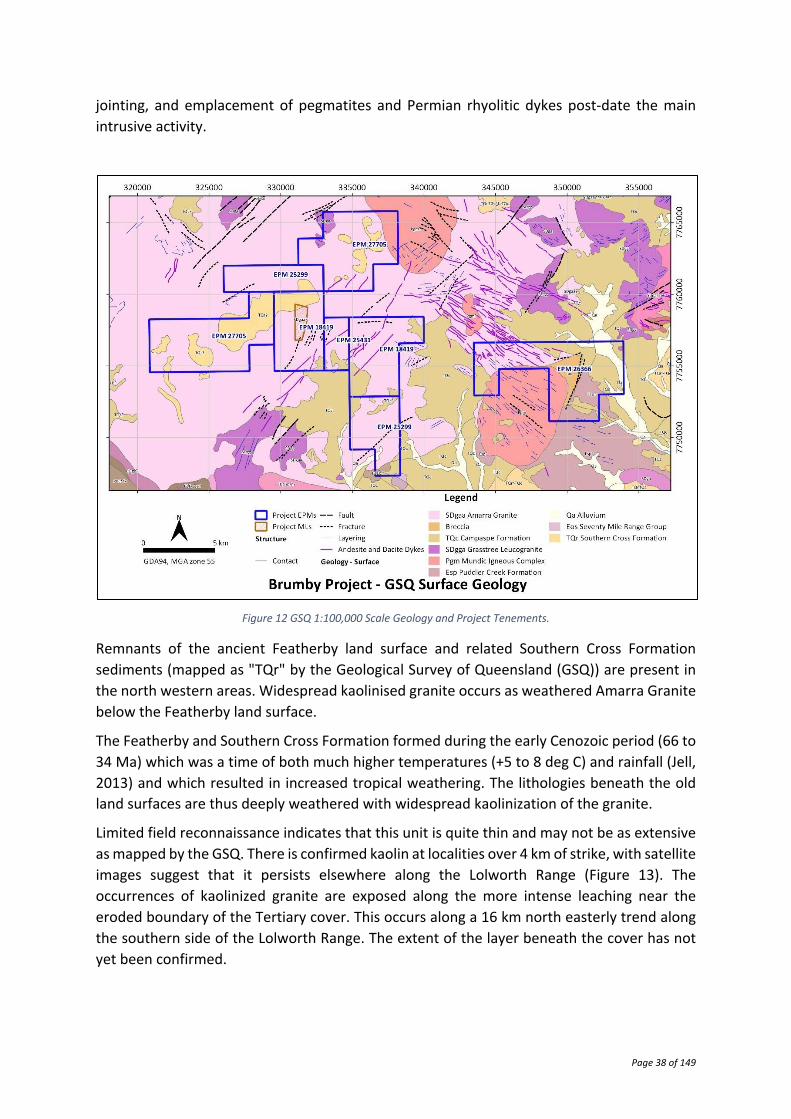

a) Geological Setting ........................................................................................................ 37

b) Kaolin Mineralisation ................................................................................................... 39

8. Deposit Types ................................................................................................................. 39

a) Kaolin Mineralisation ................................................................................................... 39

b) Gold Mineralisation ..................................................................................................... 40

9. Exploration ..................................................................................................................... 40

a) Kaolin Exploration Targets ........................................................................................... 40

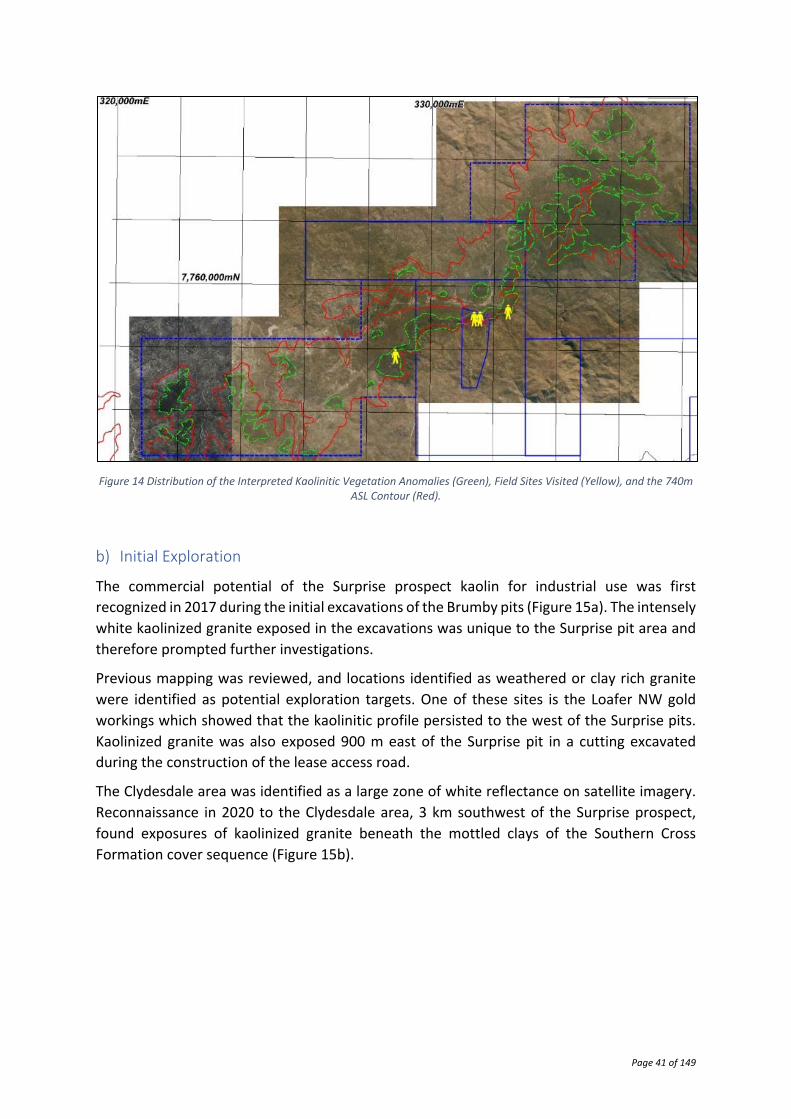

b) Initial Exploration ........................................................................................................ 41

10. Drilling ......................................................................................................................... 45

a) Drilling Evaluation ........................................................................................................ 45

b) Future Drilling .............................................................................................................. 48

c) Kaolin Exploration Targets Estimation ......................................................................... 50

a. Surprise Project Target Estimation .............................................................................. 50

d) Surprise Pit Area Target Estimation ............................................................................. 52

11. Sample Preparation, Analyses and Security ................................................................ 53

a) Drilling Procedures ...................................................................................................... 53

12. Data Verification .......................................................................................................... 57

13. Mineral Processing and Metallurgical Testing ............................................................. 57

a) Pozzolanic Material Specifications and Testing ........................................................... 57

b) Test Work Completed to Date ..................................................................................... 58

14. Mineral Resource Estimates ........................................................................................ 69

15. Mineral Reserve Estimates .......................................................................................... 69

16. Mining Methods .......................................................................................................... 69

a) Preamble ..................................................................................................................... 69

b) Works Preparatory to Mining ...................................................................................... 69

c) Mining for the Demonstration Plant ........................................................................... 70

d) Mining for the Bulk Processing Plant ........................................................................... 72

17. Process Plant Requirements ........................................................................................ 72

a) Overview ...................................................................................................................... 72

b) Quartz Rejection .......................................................................................................... 72

a. Wet processing ............................................................................................................ 72

b. Dry processing ............................................................................................................. 74

Page 4 of 149

c) Metakaolin Production ................................................................................................ 75

18. Project Infrastructure .................................................................................................. 82

a) Mine Site Infrastructure .............................................................................................. 82

b) Townsville Site Infrastructure ...................................................................................... 84

c) Geotechnical Scope ..................................................................................................... 84

d) Hydrology .................................................................................................................... 84

e) Tailings Storage Facilities ............................................................................................. 84

19. Market Studies and Contracts ..................................................................................... 84

a) Market Summary ......................................................................................................... 84

b) Growth Forecast .......................................................................................................... 87

c) Growing Use of Metakaolin in High Strength Concretes ............................................. 88

d) Australian Metakaolin Market ..................................................................................... 88

20. Environmental Studies, Permitting and Social or Community Impact ........................ 90

a) Mine Site ...................................................................................................................... 90

a. Landholdings ............................................................................................................... 90

b. Native title and cultural heritage ................................................................................. 90

c. Social and heritage impacts ......................................................................................... 91

d. Assessment of obstacles .............................................................................................. 91

e. Environment ................................................................................................................ 91

i. Environmental authorities held ................................................................................... 91

ii. Environmental closure liabilities ................................................................................. 92

f. Social and Facilities ...................................................................................................... 92

i. Planning Permission and Reclamation Liability ........................................................... 92

ii. Third Party Obligations ................................................................................................ 92

Obligations of the Landowner ............................................................................................ 92

Obligations of IGM.............................................................................................................. 93

b) Townsville Site ............................................................................................................. 93

a. Metakaolin production ................................................................................................ 93

b. Potential process locations .......................................................................................... 94

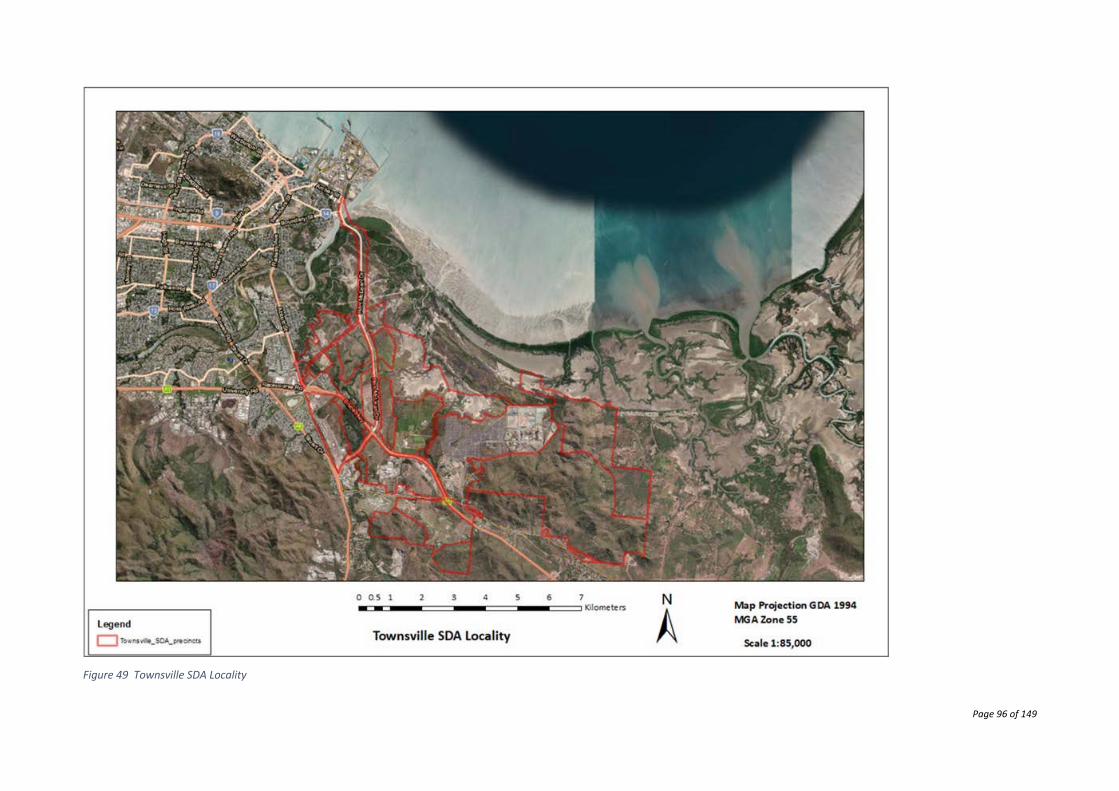

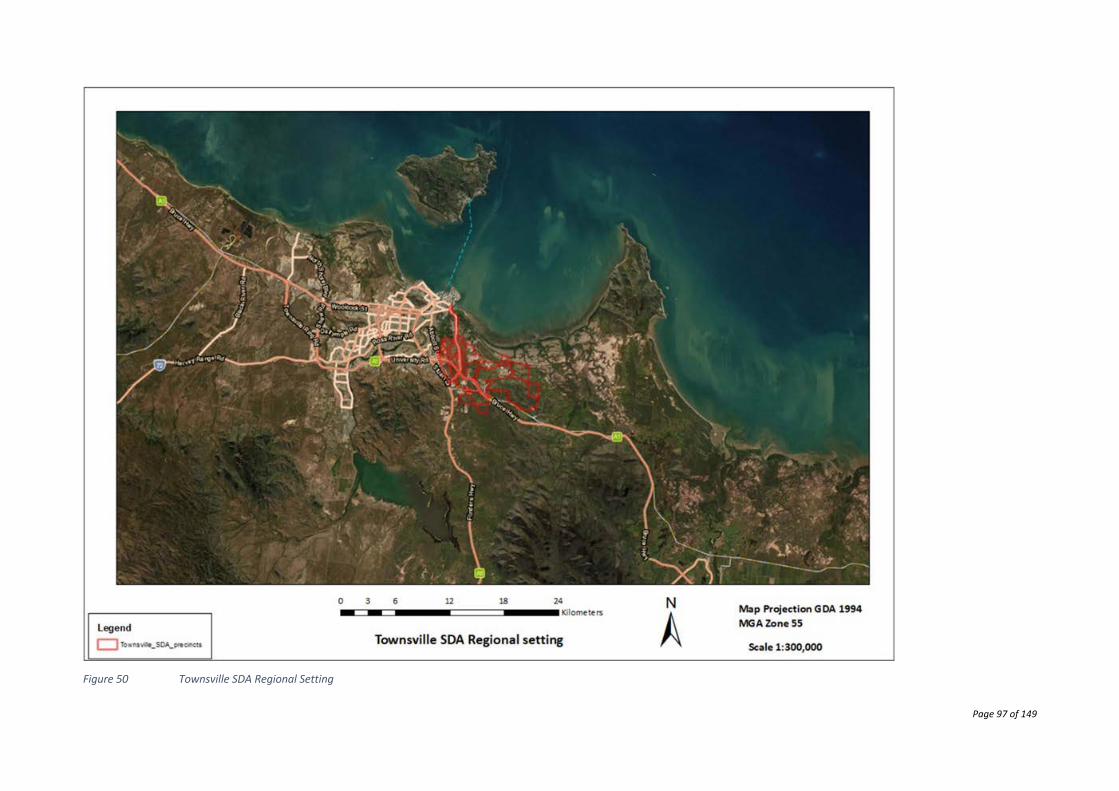

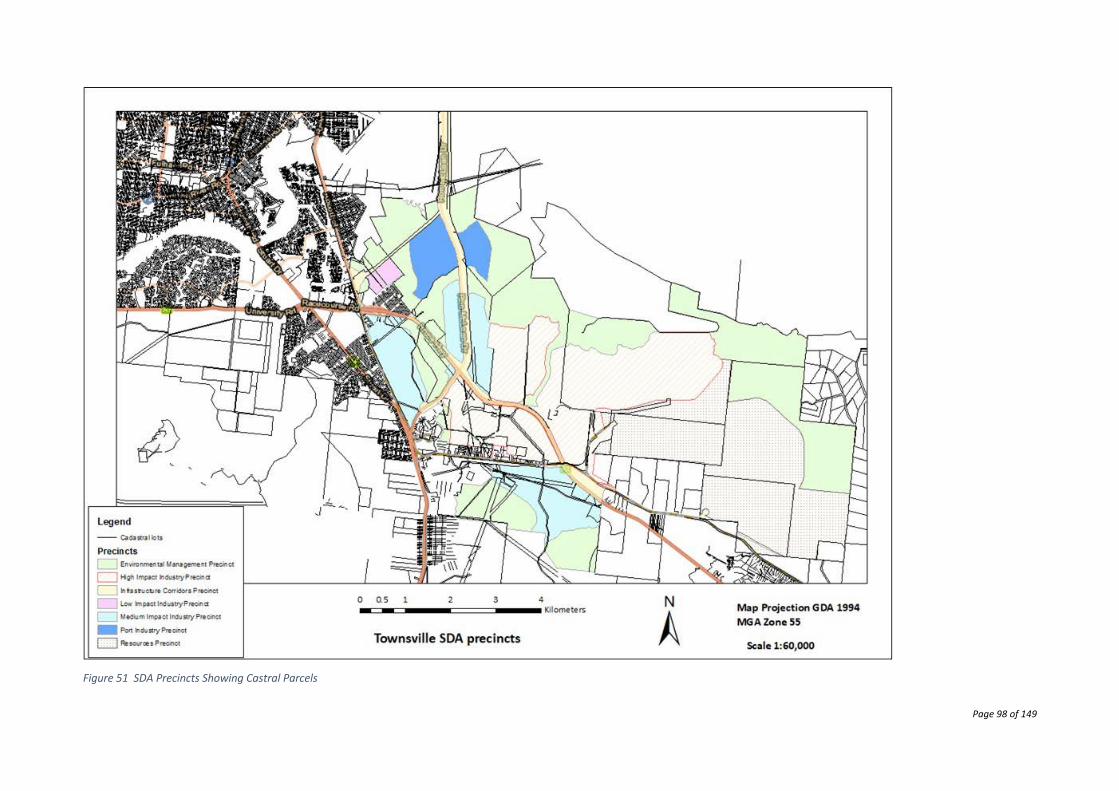

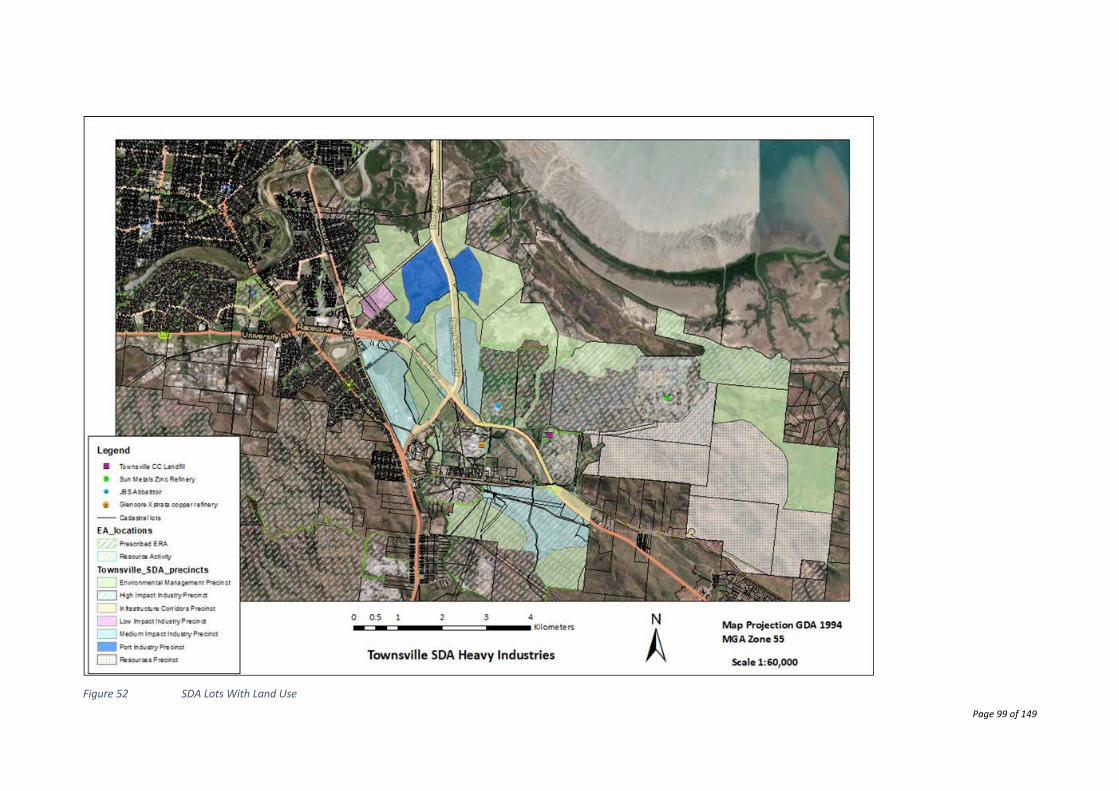

i. Townsville State Development Area ........................................................................... 94

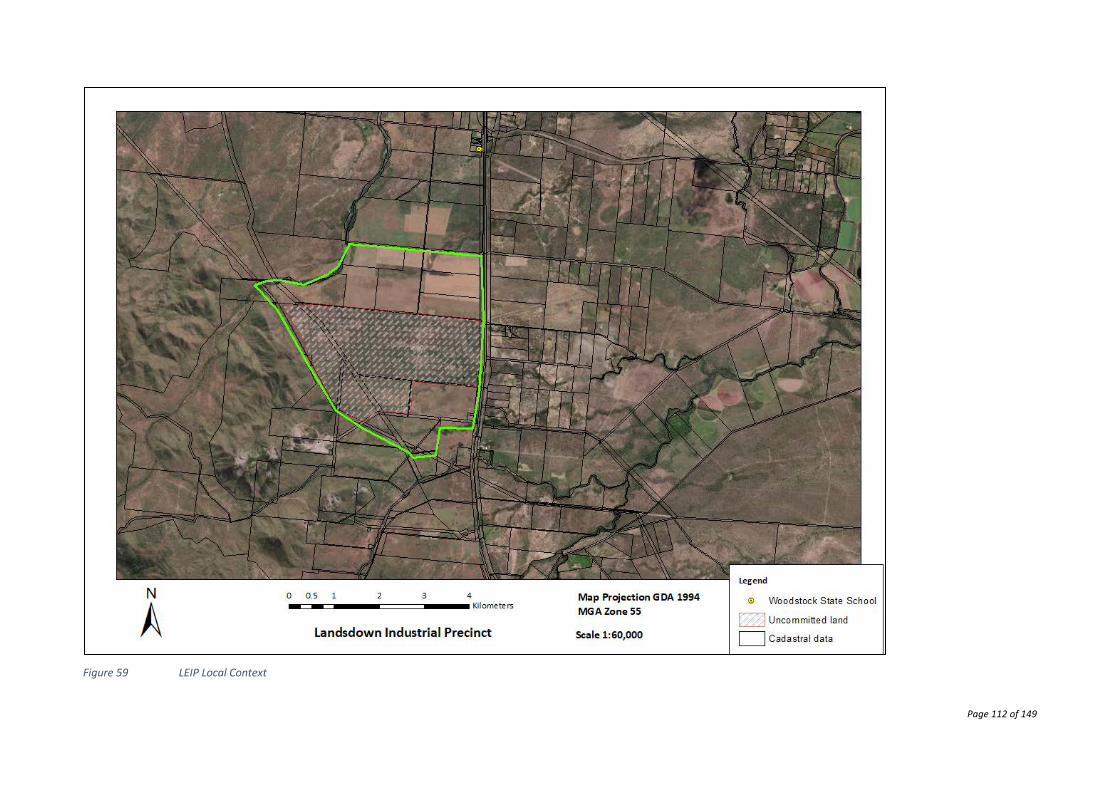

ii. Landsdown Eco Precinct ............................................................................................ 109

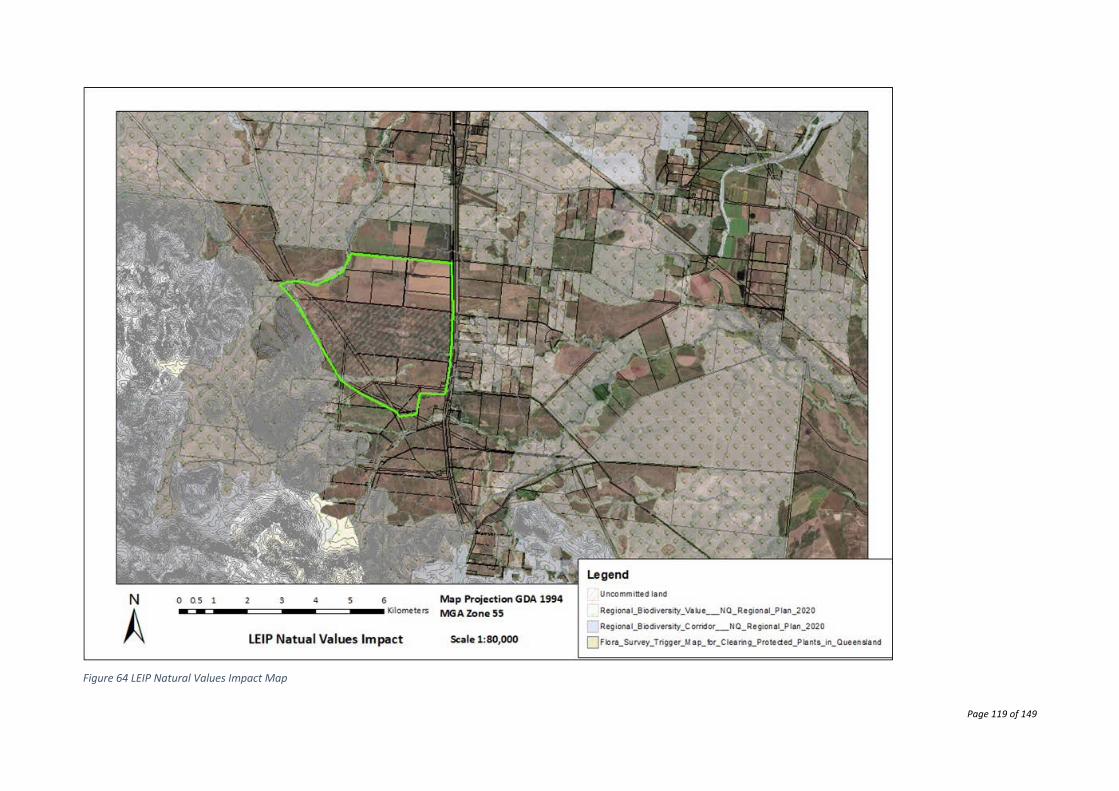

Impacts on natural values ............................................................................................ 122

Page 5 of 149

21. Capital and Operating Costs ...................................................................................... 125

a) Capital Costs .............................................................................................................. 125

a. Basis of Estimate ........................................................................................................ 126

b. Proposed Short Term Programs and Expenditure ..................................................... 127

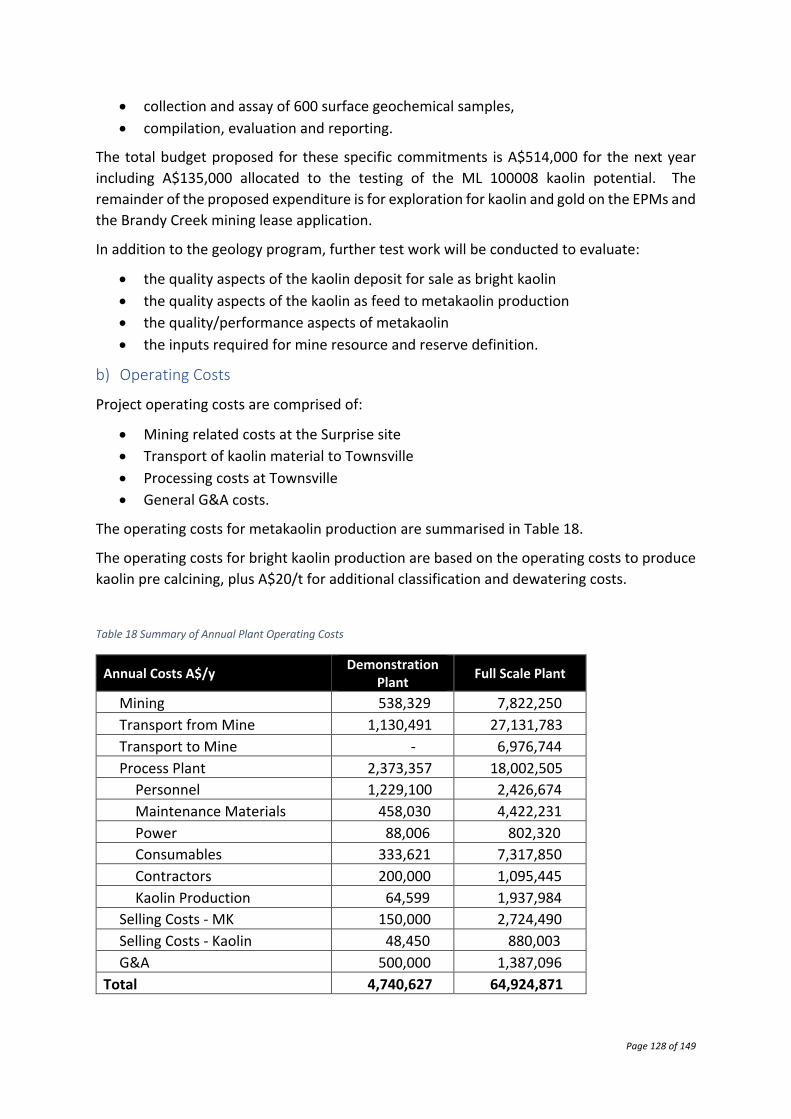

b) Operating Costs ......................................................................................................... 128

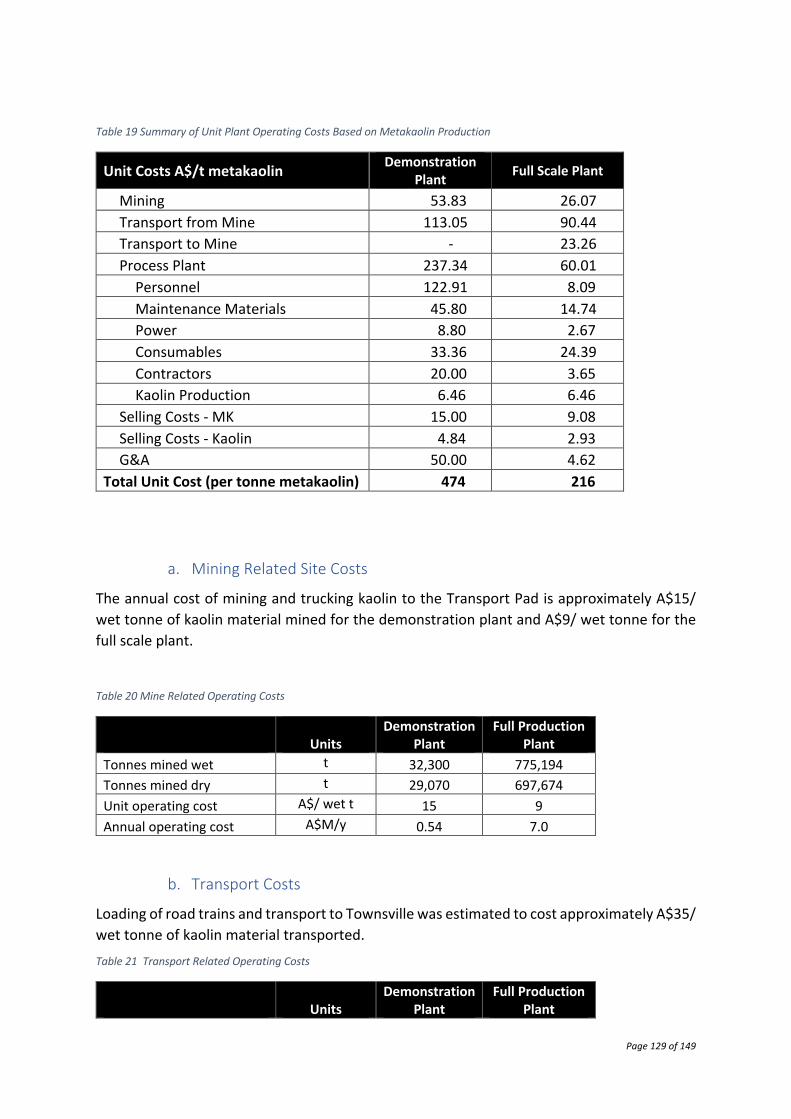

a. Mining Related Site Costs .......................................................................................... 129

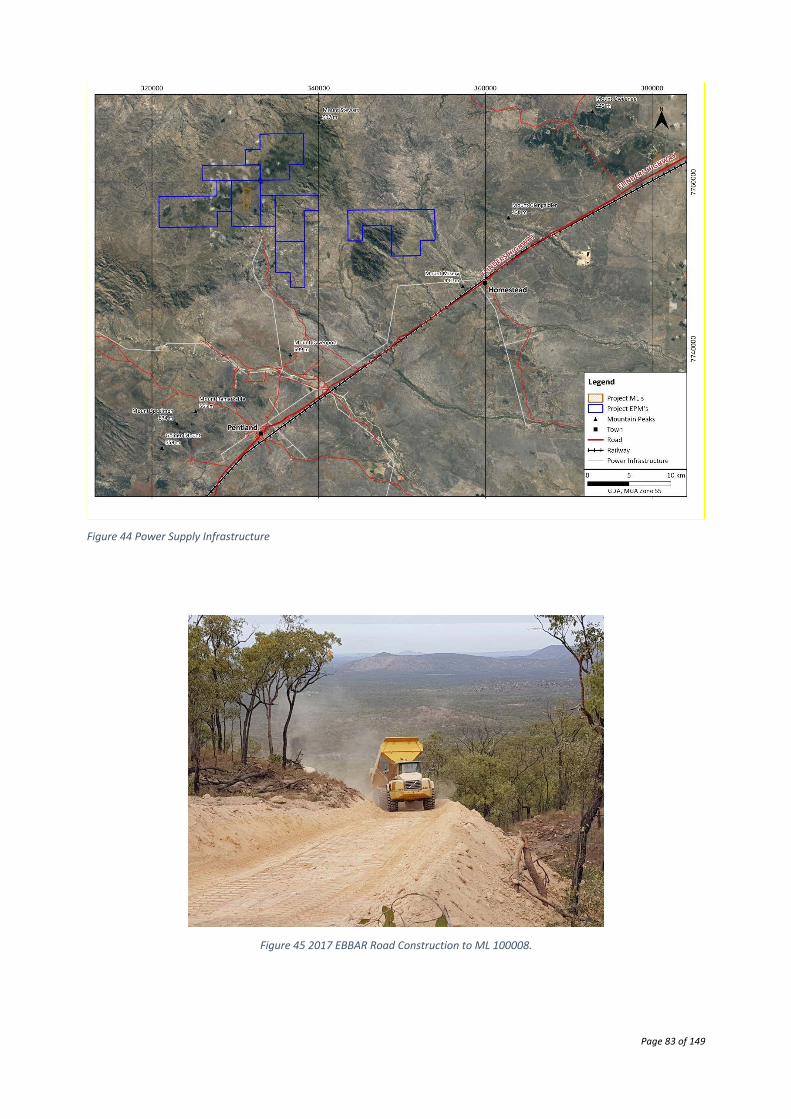

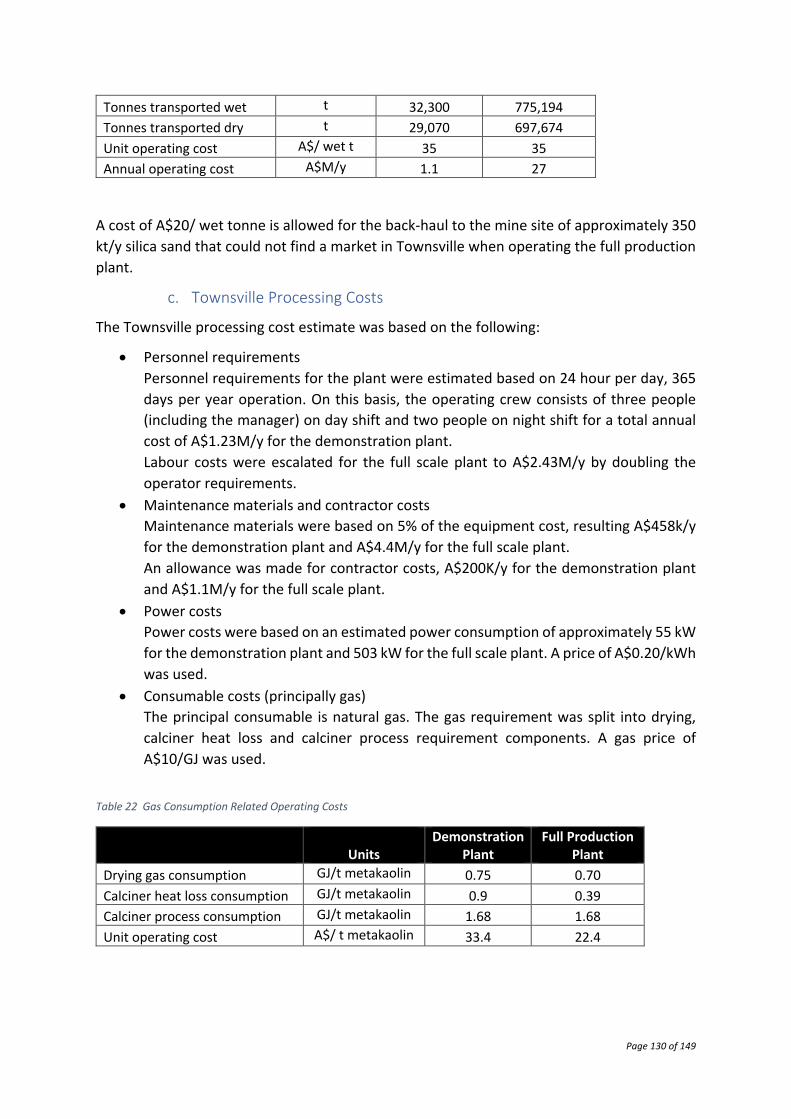

b. Transport Costs .......................................................................................................... 129

c. Townsville Processing Costs ...................................................................................... 130

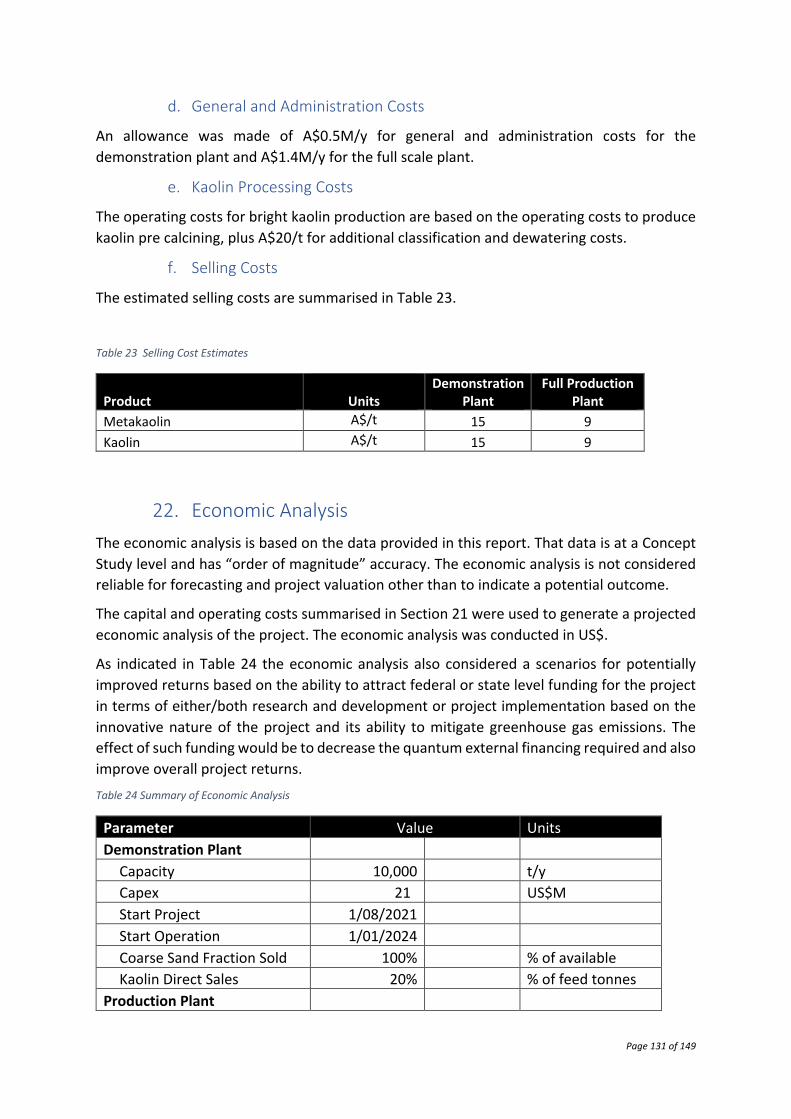

d. General and Administration Costs ............................................................................. 131

e. Kaolin Processing Costs ............................................................................................. 131

f. Selling Costs ............................................................................................................... 131

22. Economic Analysis ..................................................................................................... 131

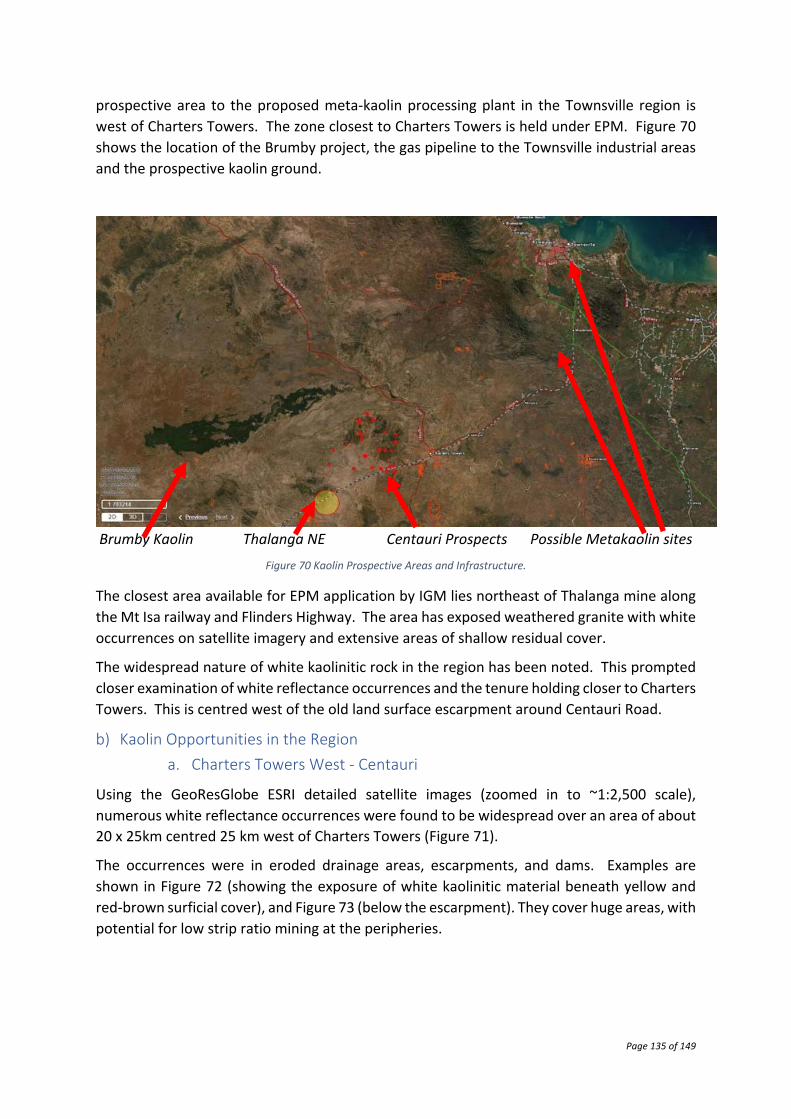

23. Adjacent Properties ................................................................................................... 134

a) Nearby Properties ..................................................................................................... 134

b) Kaolin Opportunities in the Region ........................................................................... 135

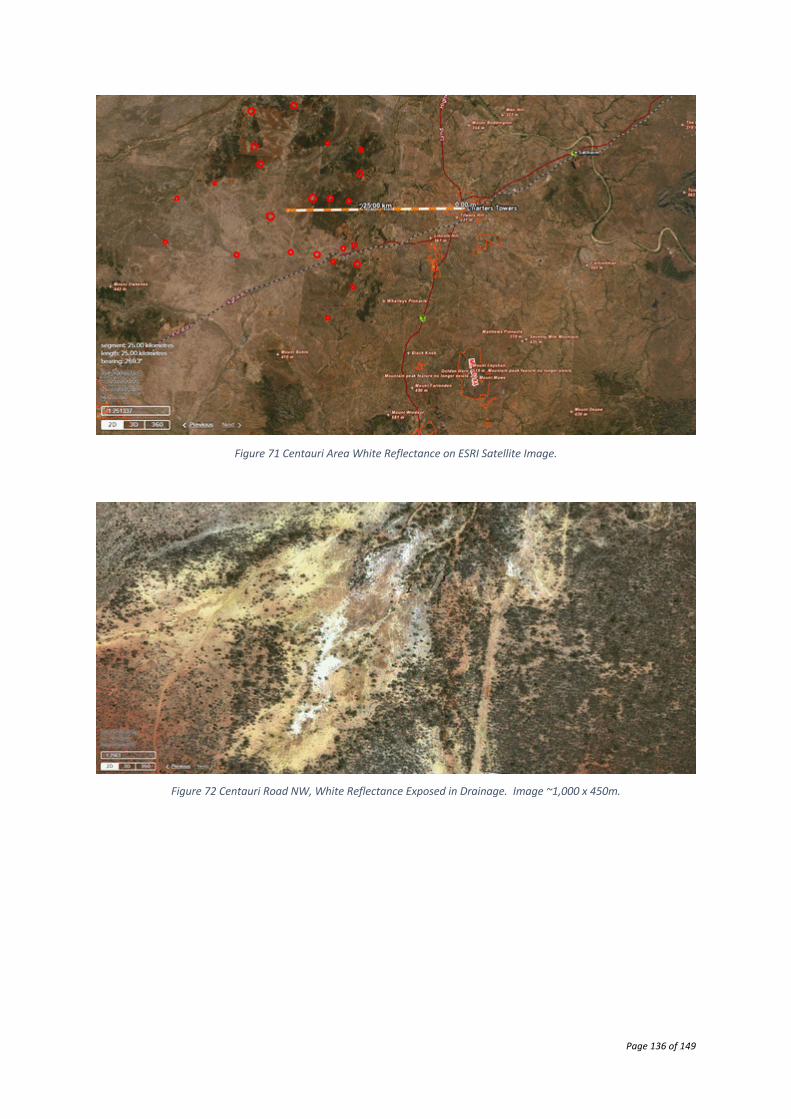

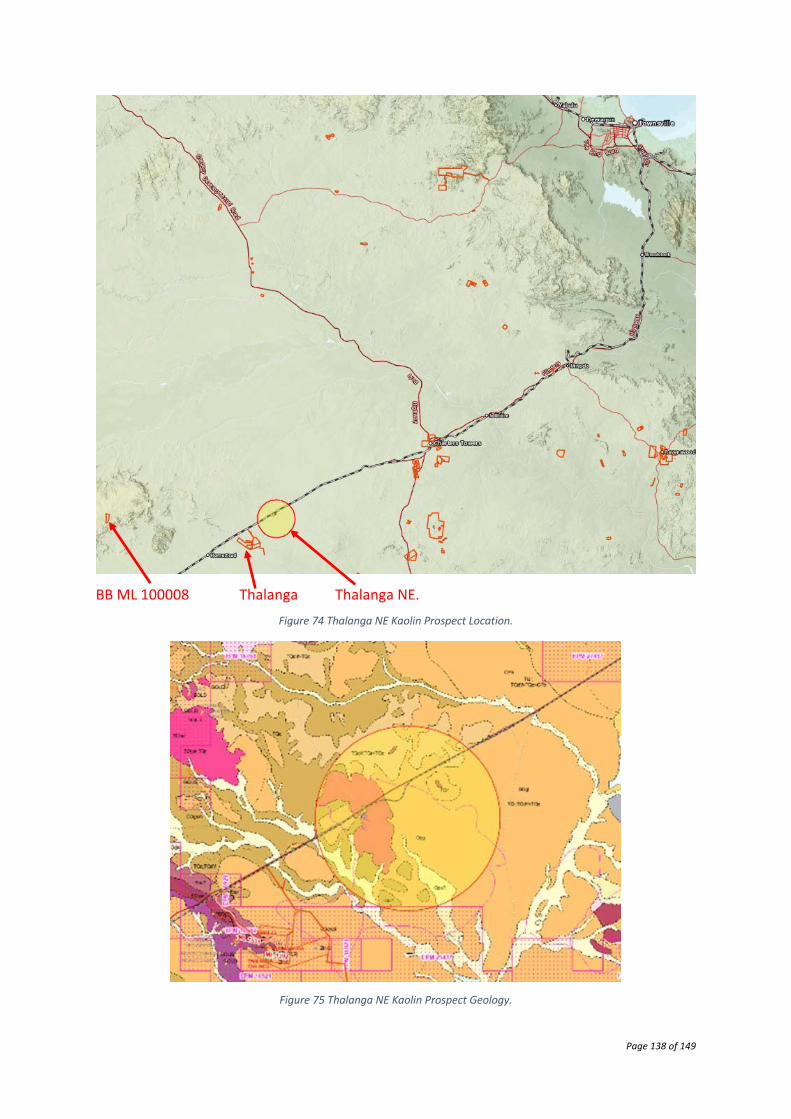

a. Charters Towers West - Centauri .............................................................................. 135

b. Thalanga Northeast ................................................................................................... 137

c. Drummond Basin ....................................................................................................... 139

24. Other Relevant Data and Information ....................................................................... 141

a) Key Technical Risks and Opportunities ...................................................................... 141

a. Risks ........................................................................................................................... 141

b. Opportunities ............................................................................................................ 142

25. Interpretation and Conclusions ................................................................................. 142

a) Kaolin Assets Review ................................................................................................. 142

b) Potential Project Value .............................................................................................. 143

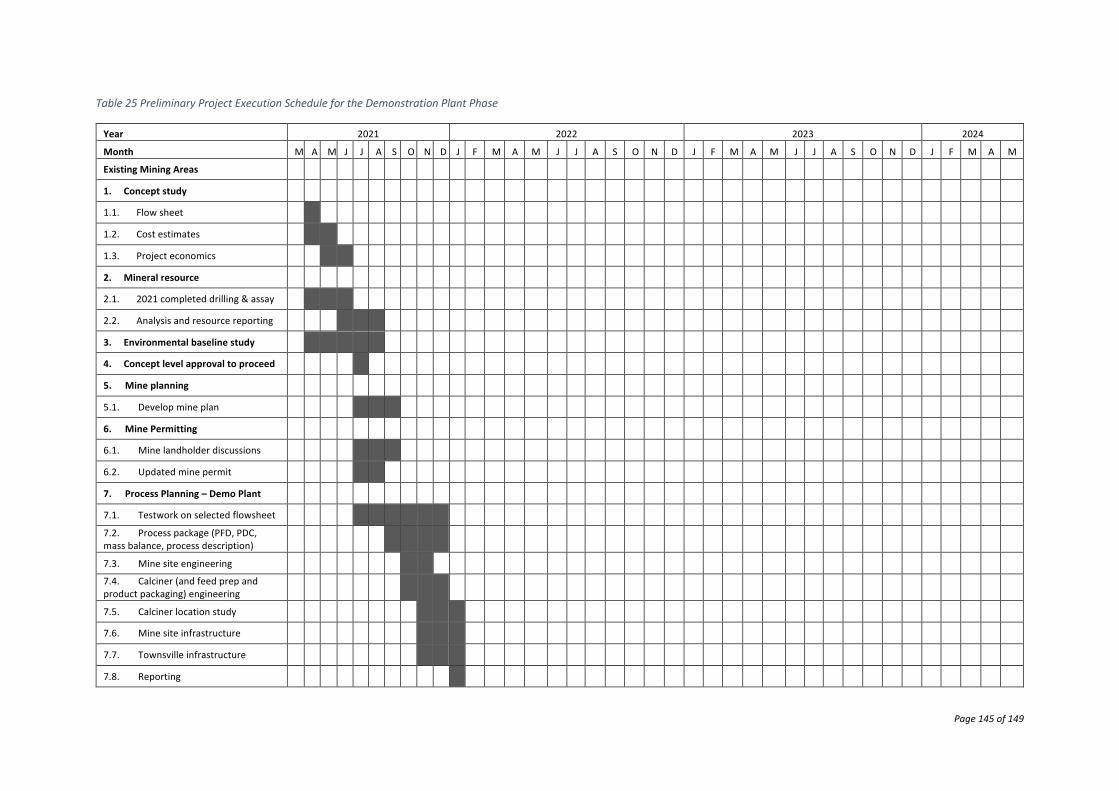

26. Recommendations and Further Work ....................................................................... 143

27. References ................................................................................................................. 147

List of Tables Table 1 Summary of Economic Analysis ................................................................................ 15

Page 6 of 149

Table 2 Summary of Project Capital Costs for the Metakaolin Demonstration and Full Scale Plants ...................................................................................................................................... 19

Table 3 Summary of Unit Plant Operating Costs Based on Metakaolin Production ............... 20

Table 4 Potential Resource Estimate Tonnages ..................................................................... 53

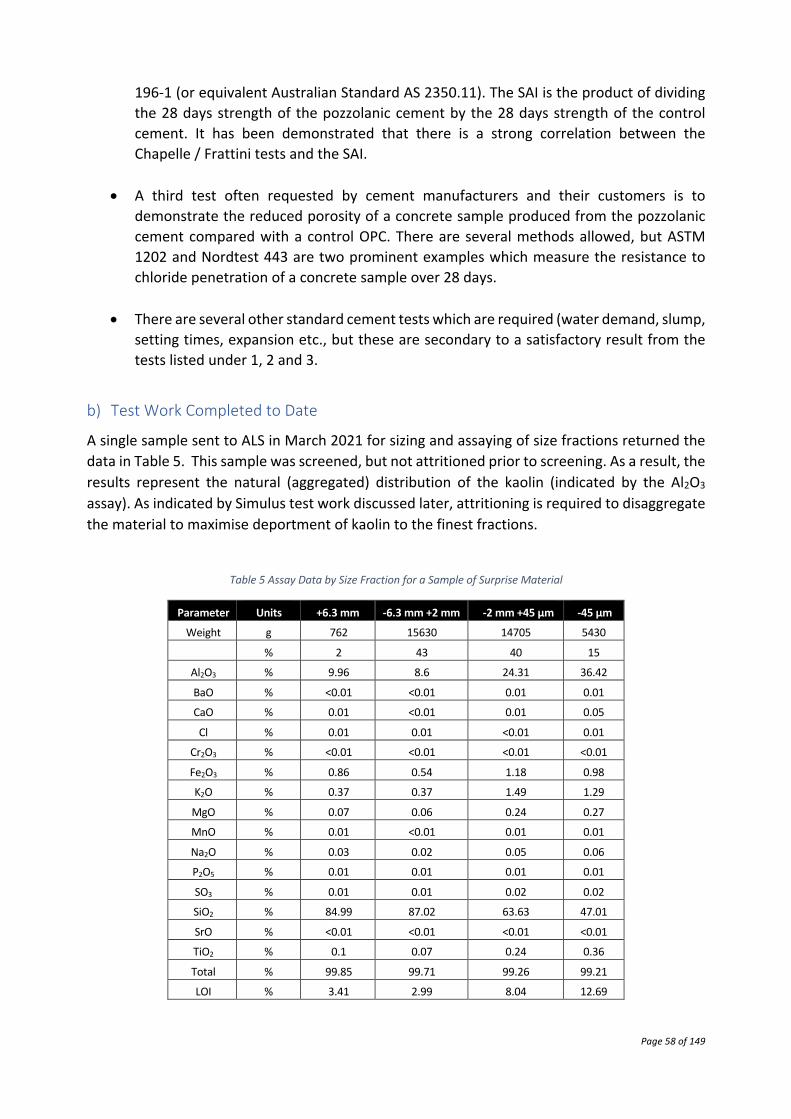

Table 5 Assay Data by Size Fraction for a Sample of Surprise Material .................................. 58

Table 6 Feedstock Characterisation .................................................................................. 62

Table 7 Surprise Kaolin Sample Elemental Analysis ........................................................... 63

Table 8 Surprise Kaolin Sample XRD analysis ..................................................................... 63

Table 9 Impact of Scrubbing on Elemental Deportment (Source: Simulus BRIL-947-TBR-001 Rev A - Lab Testwork Report) ................................................................................................. 63

Table 10 Clay Fraction XRD Assay ........................................................................................... 64

Table 11 Comparative Kaolin Composition (White Spot 11 is a sample from the Clydesdale prospect). ............................................................................................................................... 66

Table 12 Chemical Analyses of World Metakaolin Products Compared With Clydesdale derived Metakaolin ............................................................................................................................. 66

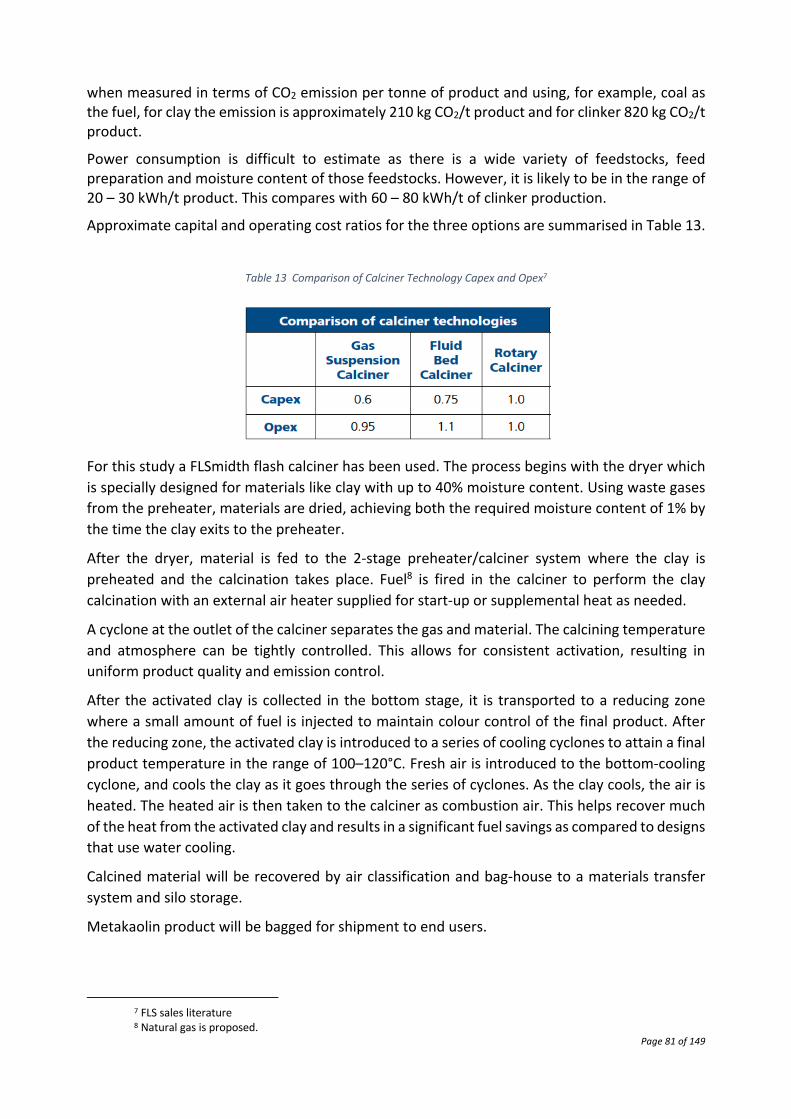

Table 13 Comparison of Calciner Technology Capex and Opex ............................................. 81

Table 14 Implied Demand for Metakaolin Based on Substitution for Portland Cement ........ 90

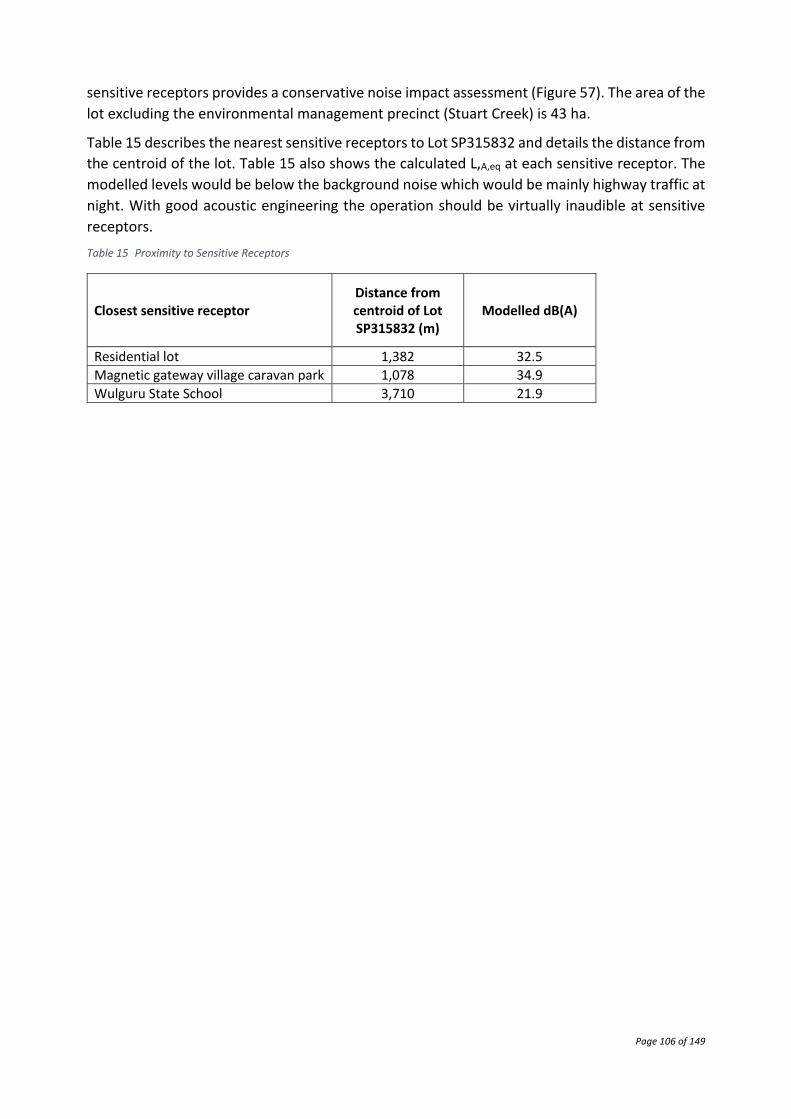

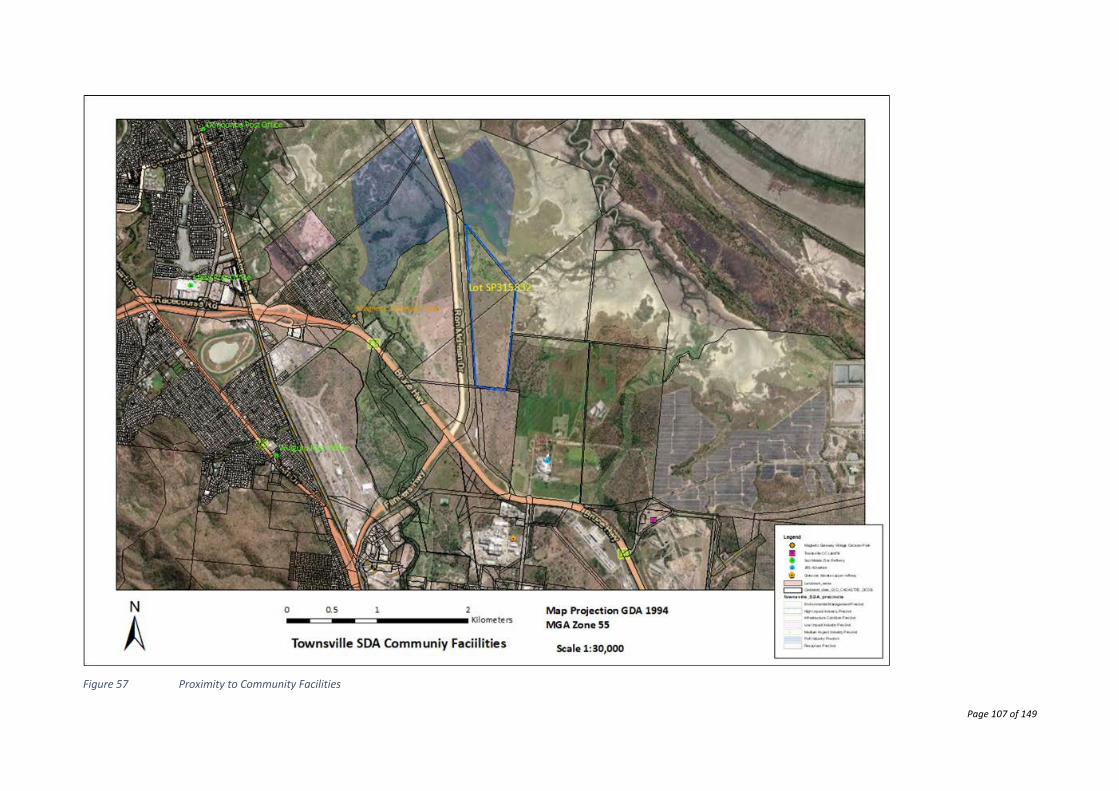

Table 15 Proximity to Sensitive Receptors ........................................................................ 106

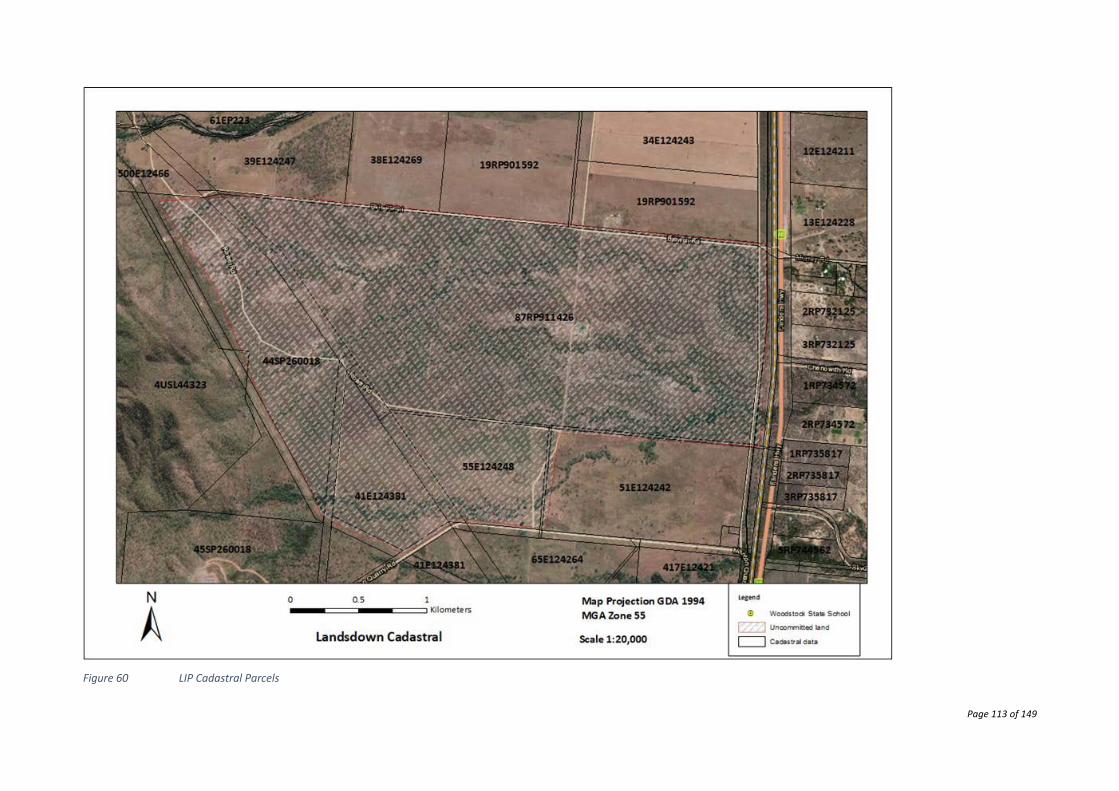

Table 16 LEIP Available Land Parcels ................................................................................ 114

Table 17 Summary of Project Capital Costs for the Metakaolin Demonstration and Full Scale Plants .................................................................................................................................... 126

Table 18 Summary of Annual Plant Operating Costs ............................................................ 128

Table 19 Summary of Unit Plant Operating Costs Based on Metakaolin Production ........... 129

Table 20 Mine Related Operating Costs ............................................................................... 129

Table 21 Transport Related Operating Costs ....................................................................... 129

Table 22 Gas Consumption Related Operating Costs .......................................................... 130

Table 23 Selling Cost Estimates ........................................................................................... 131

Table 24 Summary of Economic Analysis ............................................................................. 131

Table 25 Preliminary Project Execution Schedule for the Demonstration Plant Phase ....... 145

List of Figures Figure 1 Process Schematic Showing Dry and Wet Screening Options at the Surprise Site ... 15

Page 7 of 149

Figure 2 Project Revenues Based on Metakaolin (MK), Kaolin and Aggregate (Sand) ........... 17

Figure 3 Projected Project Cash Flow ..................................................................................... 17

Figure 4 Project Returns ......................................................................................................... 18

Figure 5 Project Cash Flow Showing Impact of Grants ........................................................... 18

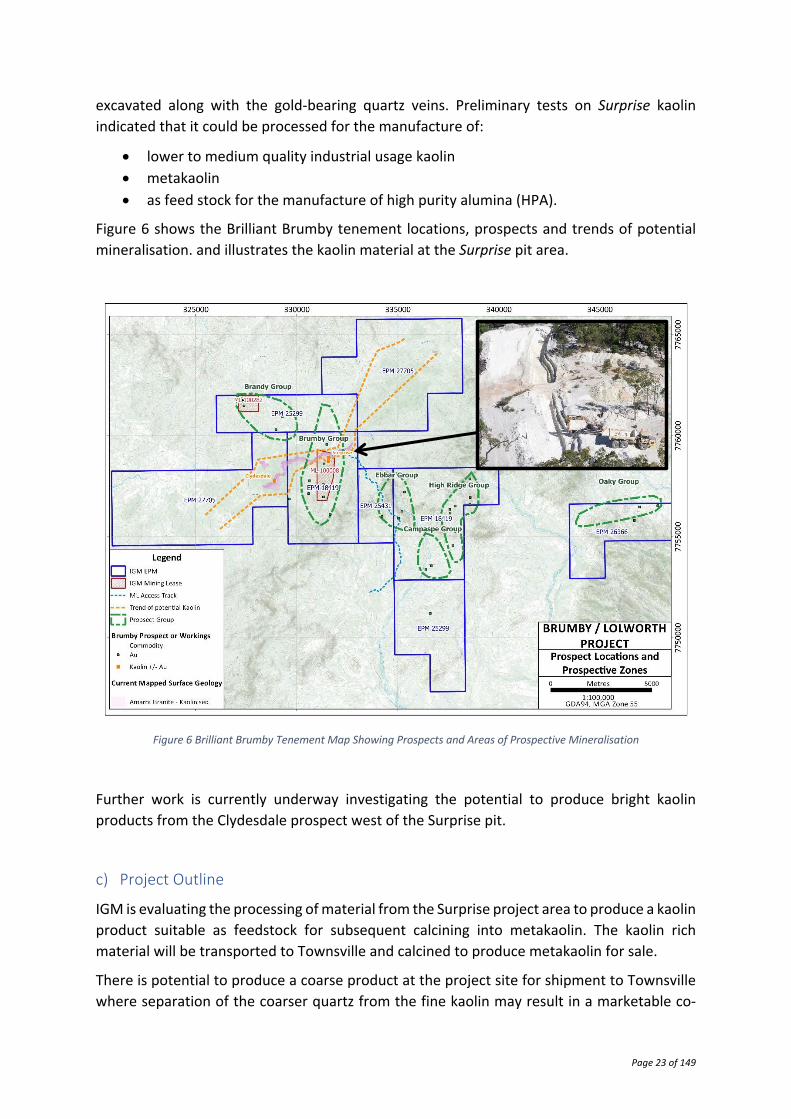

Figure 6 Brilliant Brumby Tenement Map Showing Prospects and Areas of Prospective Mineralisation ........................................................................................................................ 23

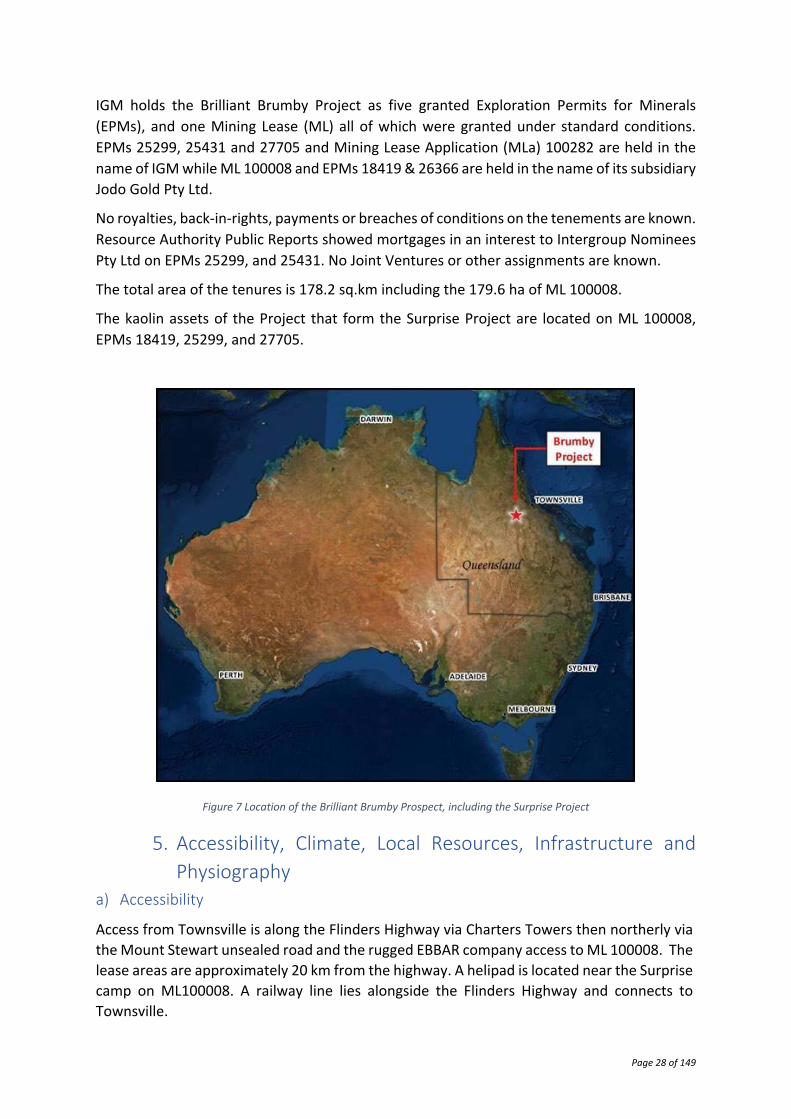

Figure 7 Location of the Brilliant Brumby Prospect, including the Surprise Project ............... 28

Figure 8 Initial Hydration of Cement Particles to form Hydrates (CBA internal data) ............ 33

Figure 9 Hydration of Individual Species to form Initial Hydrated Products (CBA Internal data) ................................................................................................................................................ 33

Figure 10 Composition of Kaolinite ........................................................................................ 34

Figure 11 Reaction Temperatures for Clay Species ................................................................ 35

Figure 12 GSQ 1:100,000 Scale Geology and Project Tenements. ......................................... 38

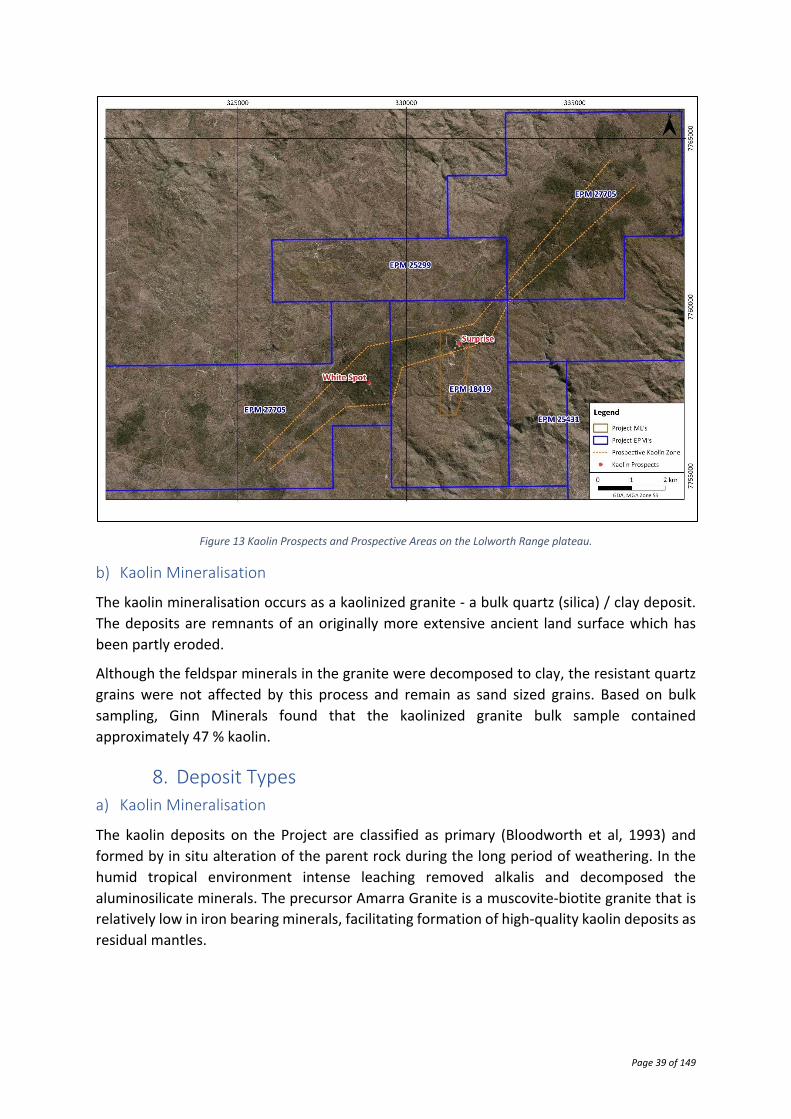

Figure 13 Kaolin Prospects and Prospective Areas on the Lolworth Range plateau. ............. 39

Figure 14 Distribution of the Interpreted Kaolinitic Vegetation Anomalies (Green), Field Sites Visited (Yellow), and the 740m ASL Contour (Red). ............................................................... 41

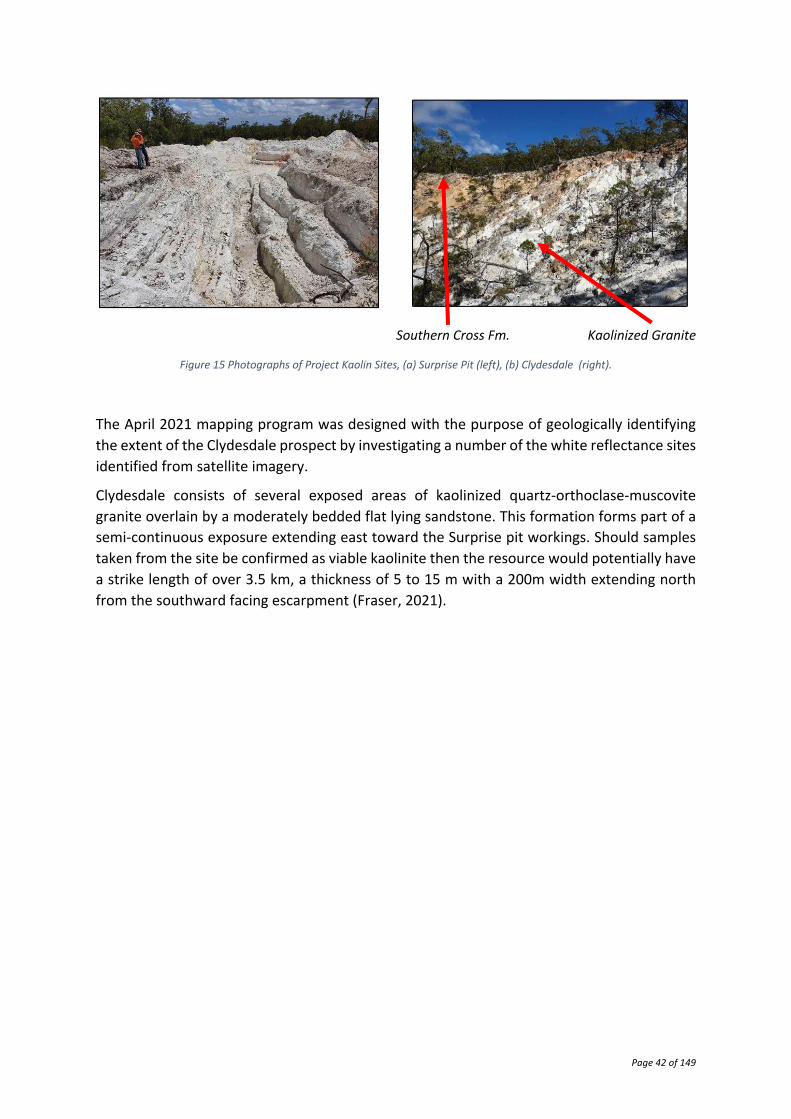

Figure 17 Photographs of Project Kaolin Sites, (a) Surprise Pit (left), (b) Clydesdale (right). 42

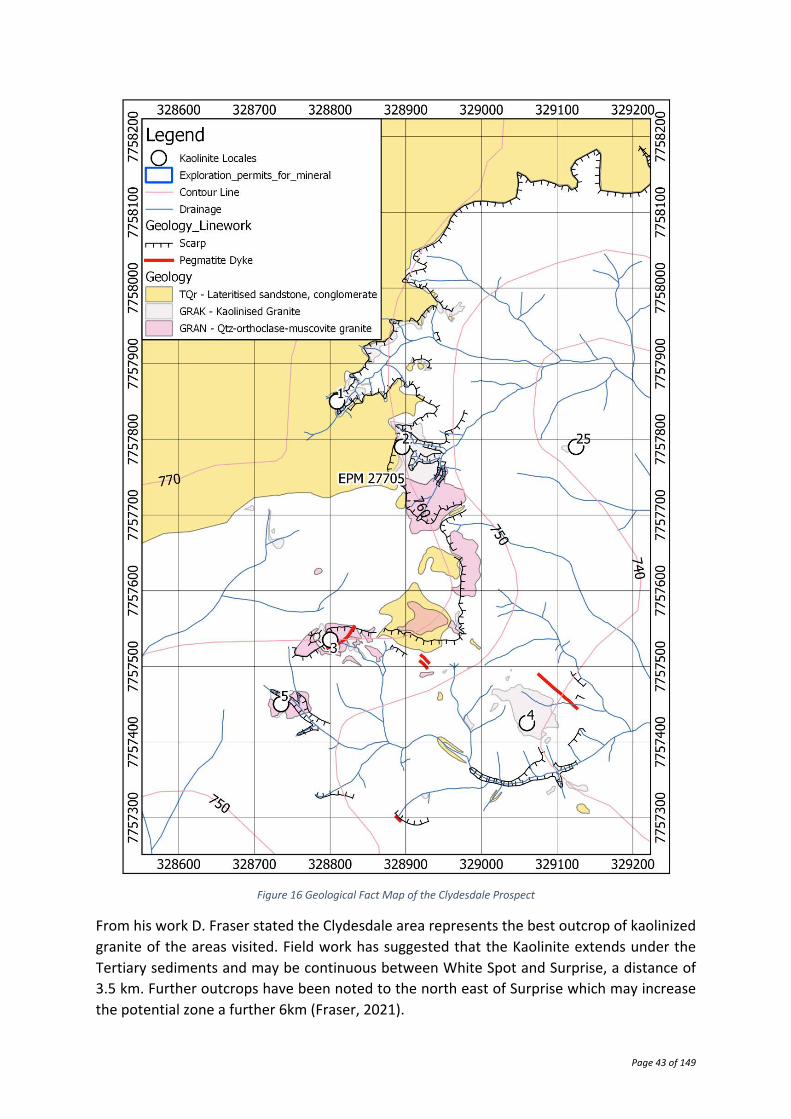

Figure 16 Geological Fact Map of the Clydesdale Prospect ................................................... 43

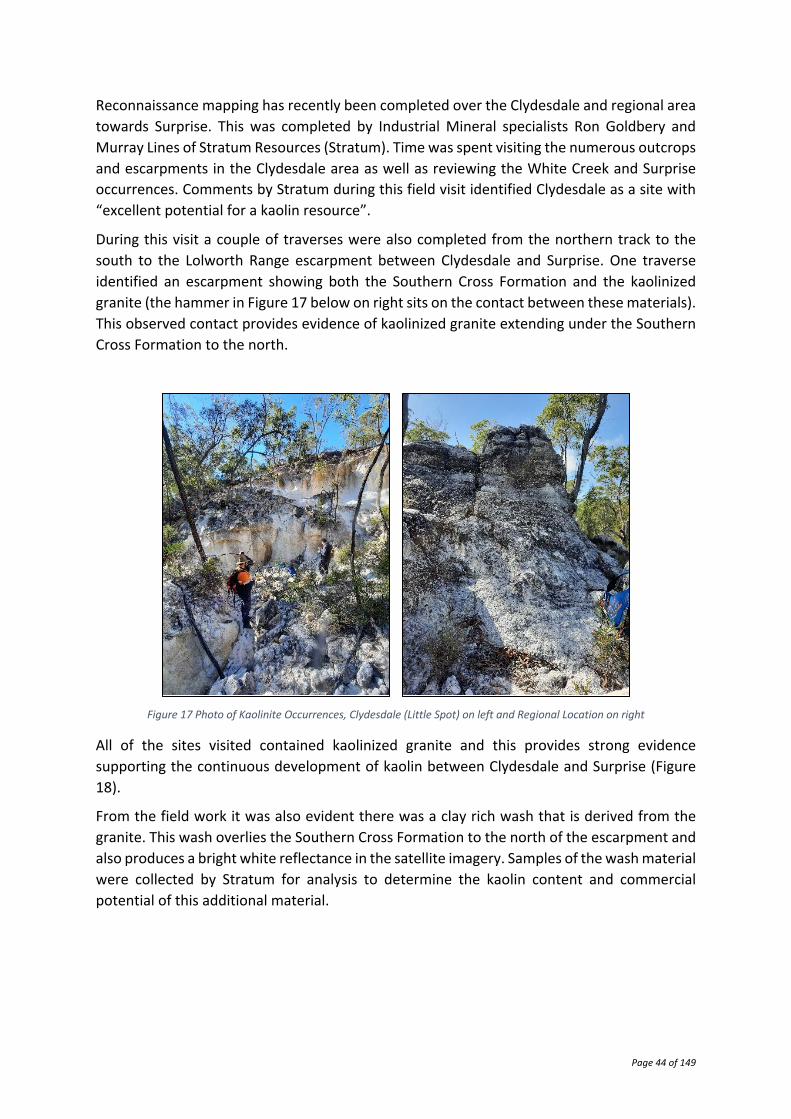

Figure 17 Photo of Kaolinite Occurrences, Clydesdale (Little Spot) on left and Regional Location on right .................................................................................................................... 44

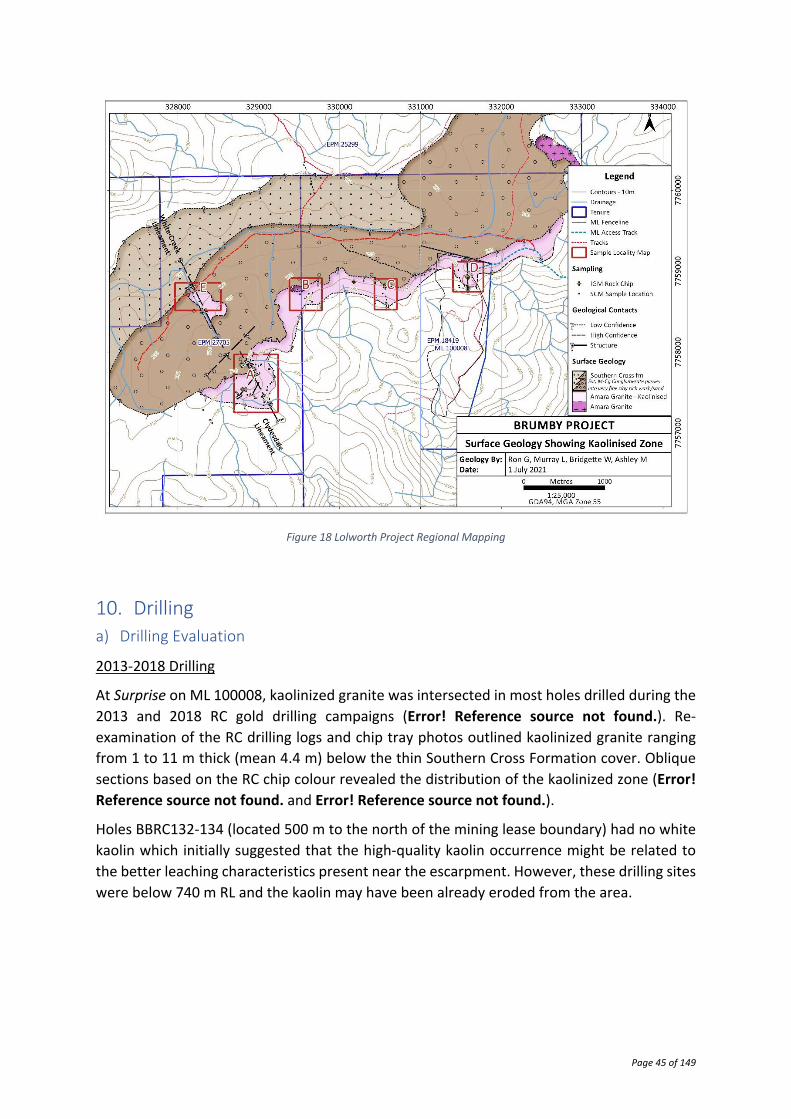

Figure 18 Lolworth Project Regional Mapping ....................................................................... 45

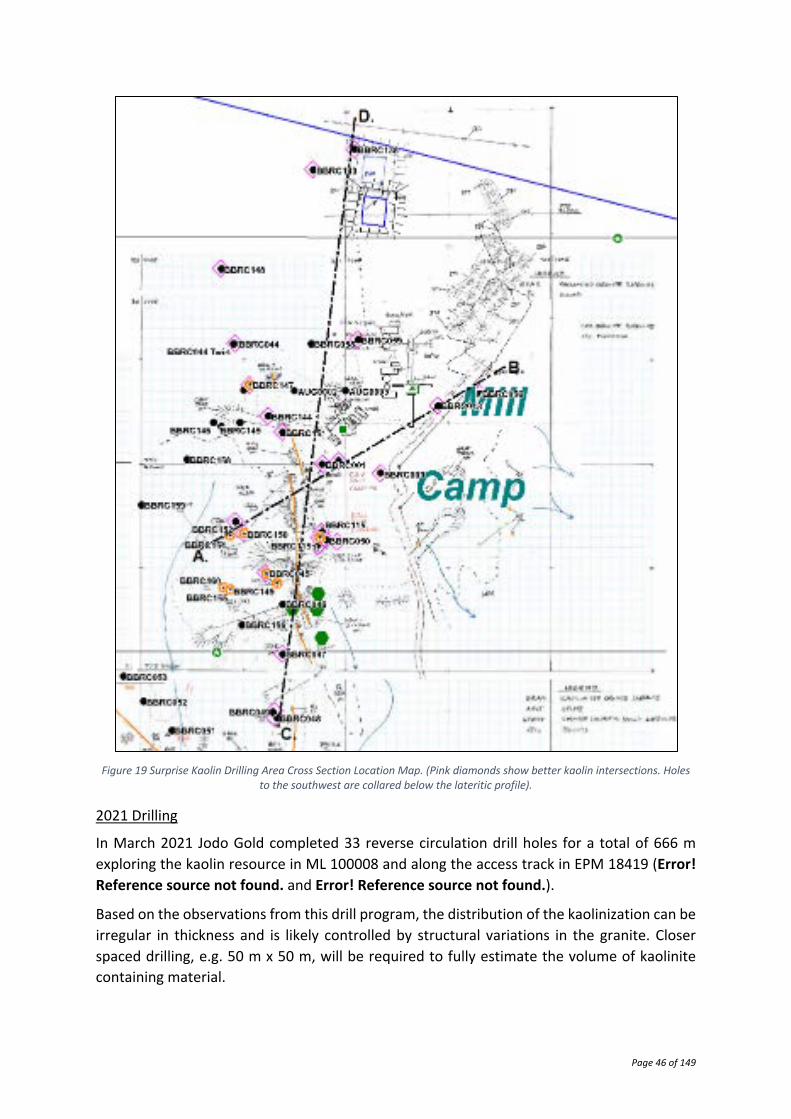

Figure 18 Surprise Kaolin Drilling Area Cross Section Location Map. (Pink diamonds show better kaolin intersections. Holes to the southwest are collared below the lateritic profile). ................................................................................................................................................ 46

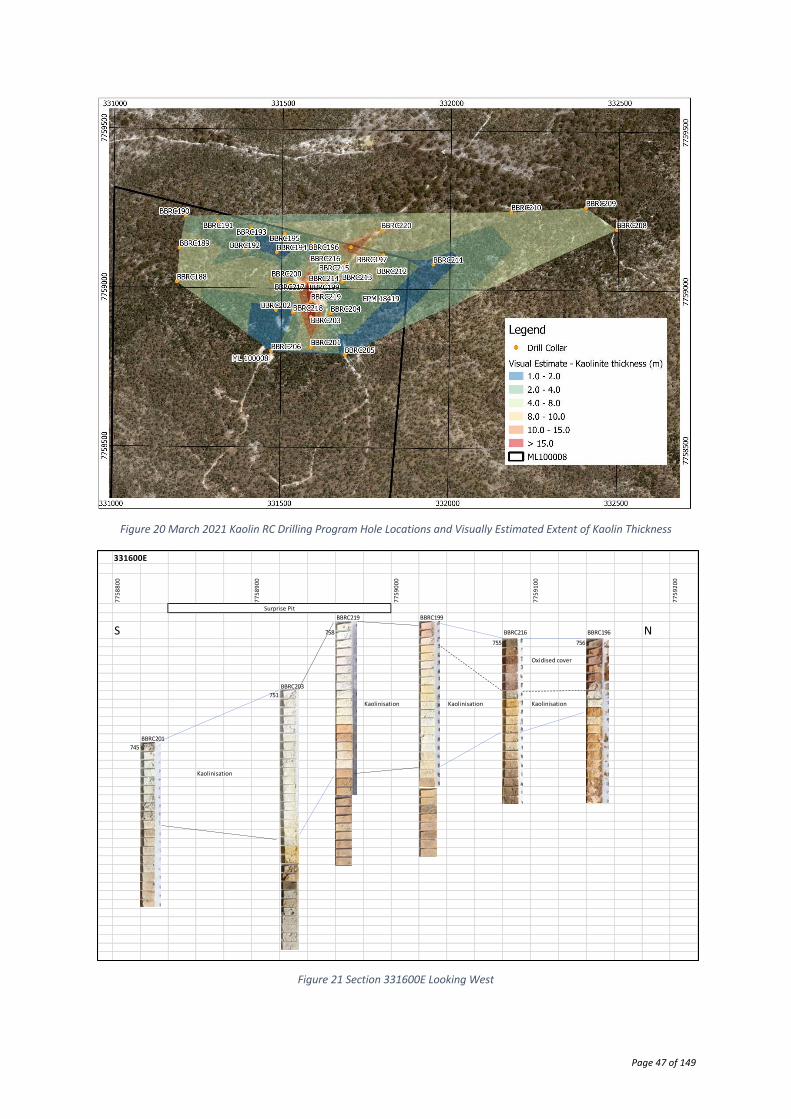

Figure 19 March 2021 Kaolin RC Drilling Program Hole Locations and Visually Estimated Extent of Kaolin Thickness ................................................................................................................. 47

Figure 20 Section 331600E Looking West .............................................................................. 47

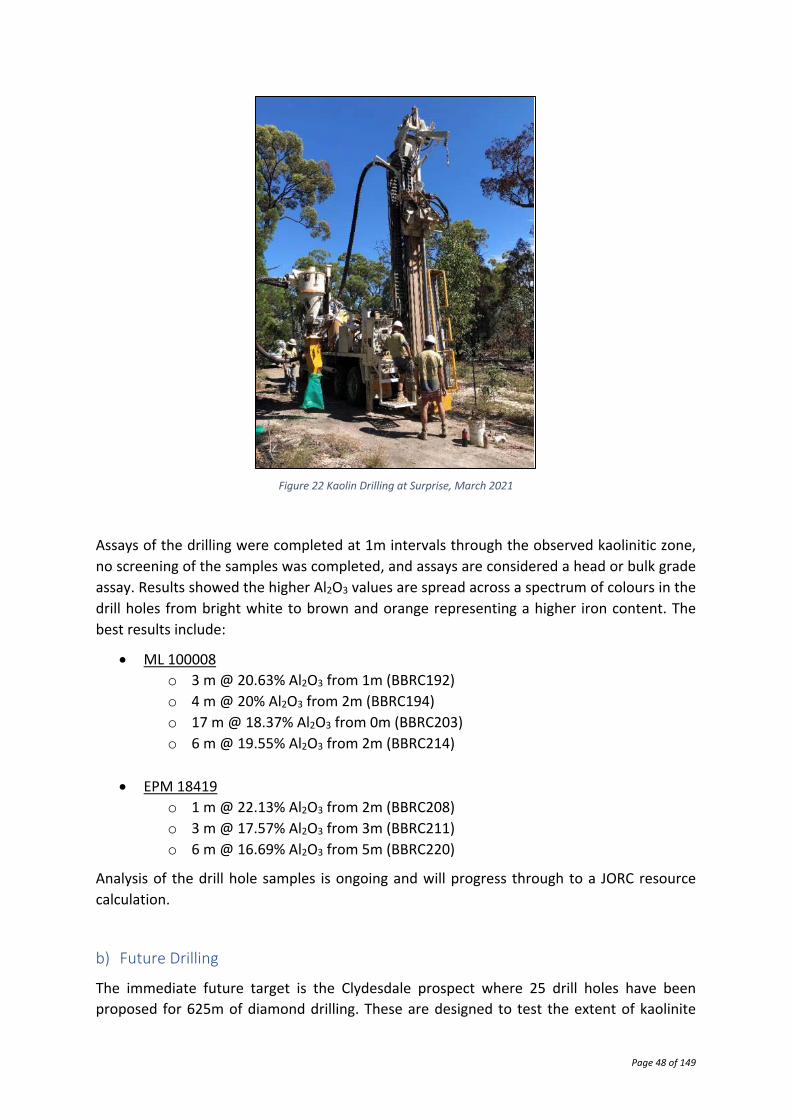

Figure 21 Kaolin Drilling at Surprise, March 2021 .................................................................. 48

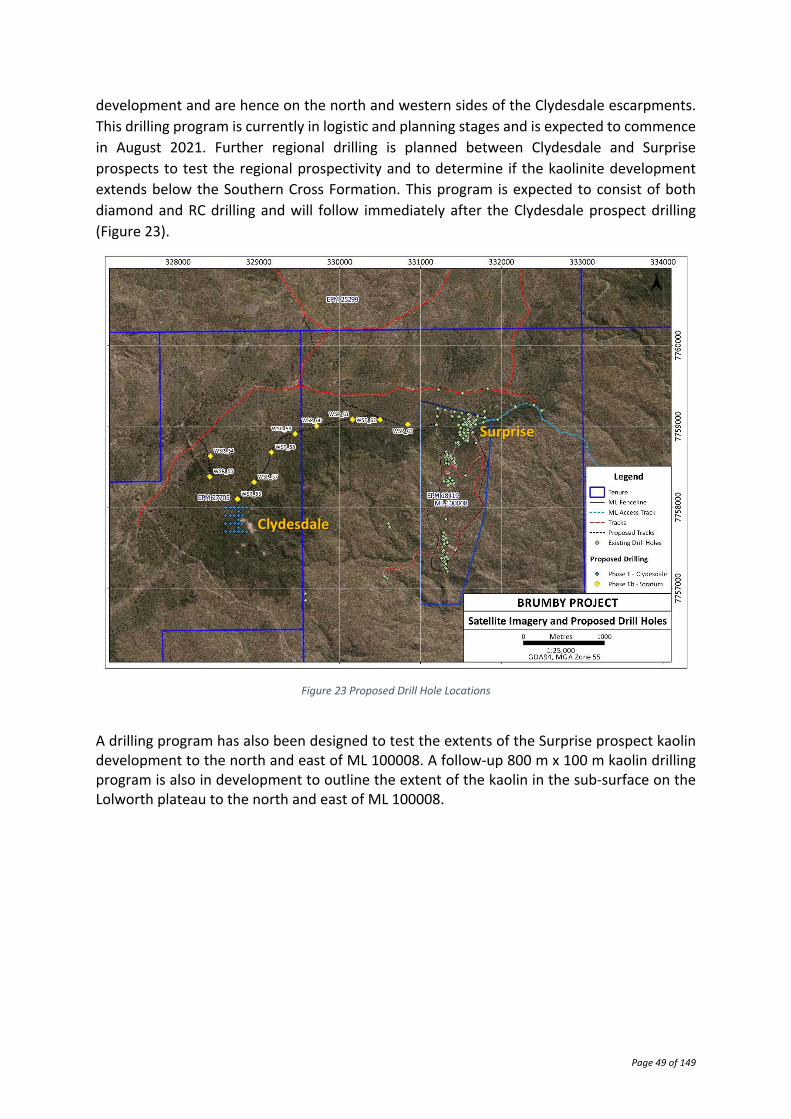

Figure 23 Proposed Drill Hole Locations ................................................................................. 49

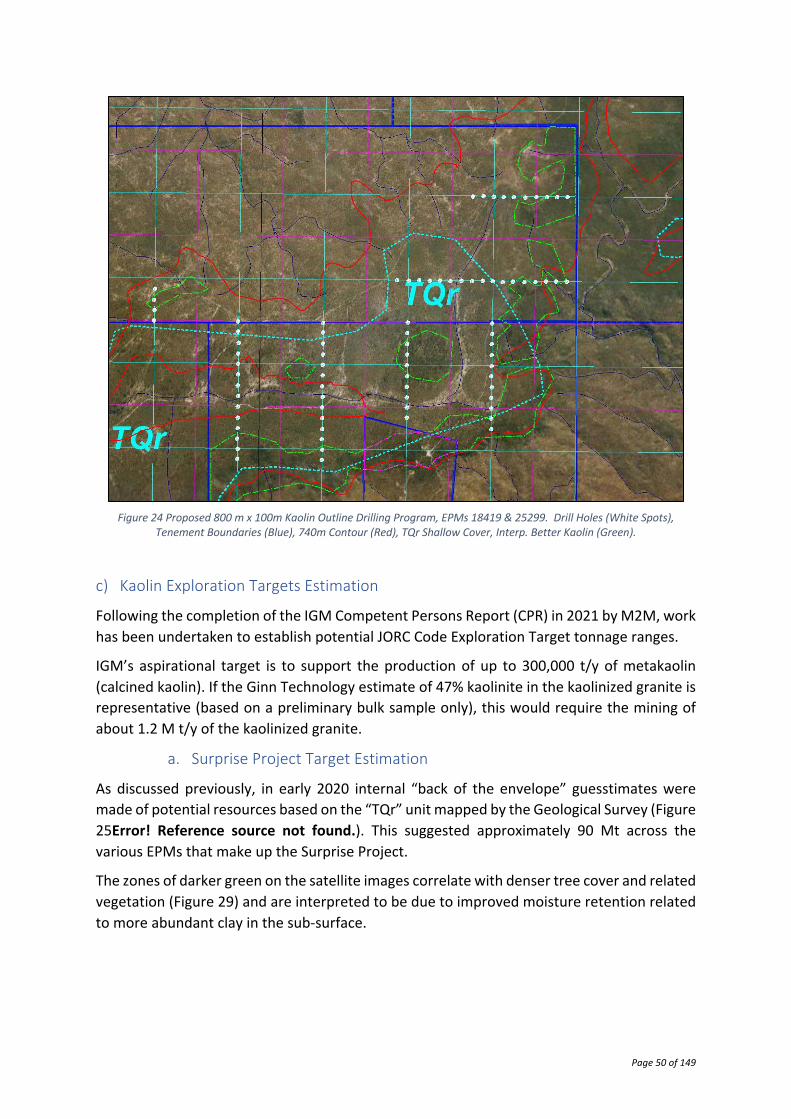

Figure 22 Proposed 800 m x 100m Kaolin Outline Drilling Program, EPMs 18419 & 25299. Drill Holes (White Spots), Tenement Boundaries (Blue), 740m Contour (Red), TQr Shallow Cover, Interp. Better Kaolin (Green). ................................................................................................. 50

Figure 25 Distribution of the GSQ’s “TQr” Unit (Pale Blue) and the 740m ASL Contour (Red). ................................................................................................................................................ 51

Page 8 of 149

Figure 16 Distribution of White Reflectance Occurrences and the 740m ASL Contour (Red). ................................................................................................................................................ 52

Figure 22 Surprise Pit Area 2021 Drilling Voronoi Polygons for Internal Resource Calculation ................................................................................................................................................ 53

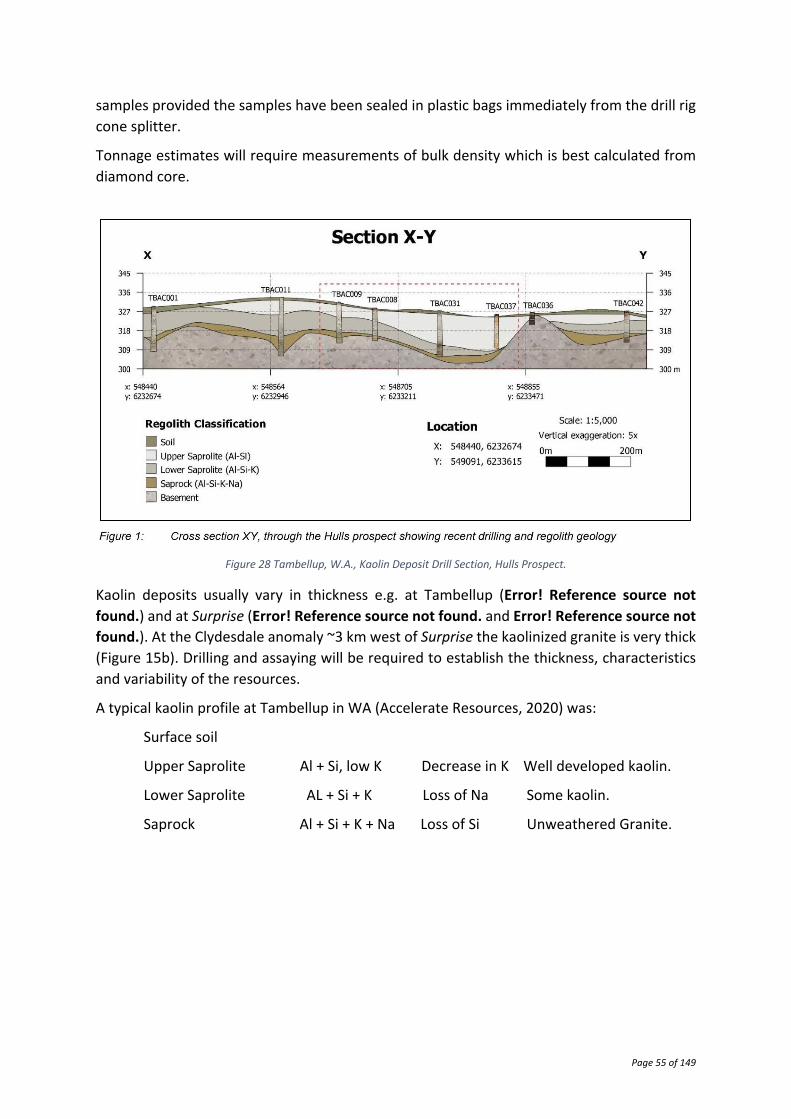

Figure 24 Tambellup, W.A., Kaolin Deposit Drill Section, Hulls Prospect. .............................. 55

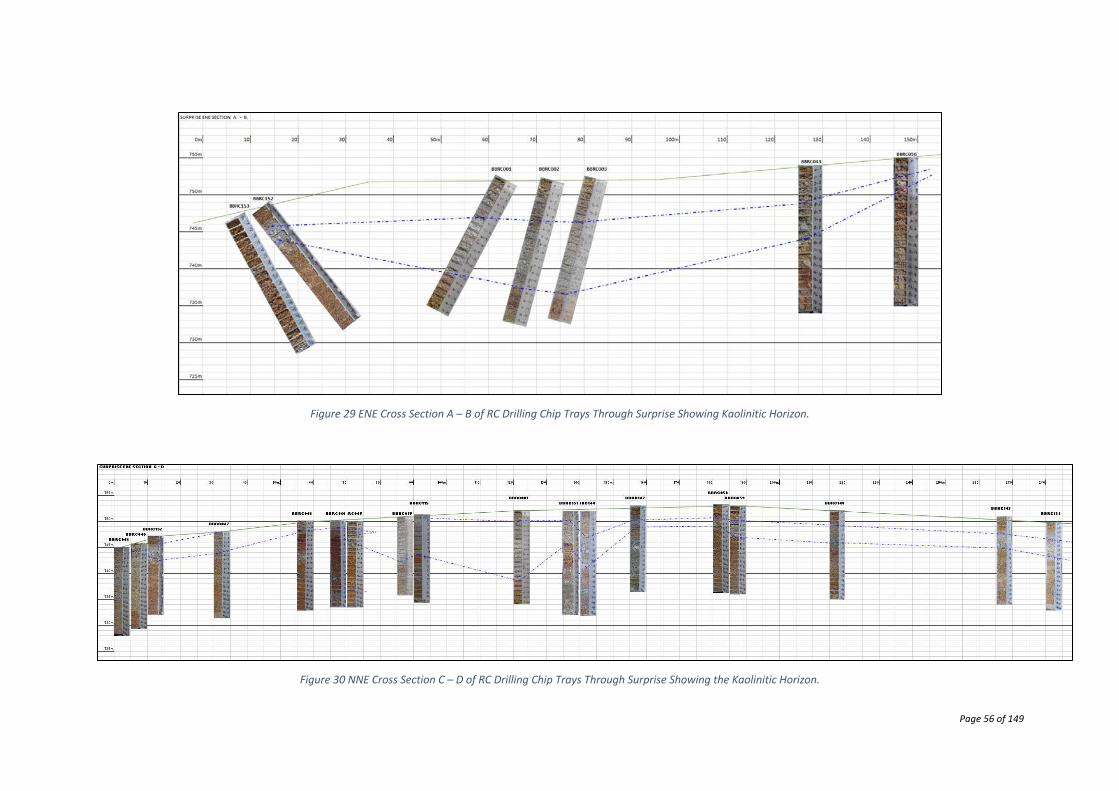

Figure 25 ENE Cross Section A – B of RC Drilling Chip Trays Through Surprise Showing Kaolinitic Horizon. .................................................................................................................................. 56

Figure 26 NNE Cross Section C – D of RC Drilling Chip Trays Through Surprise Showing the Kaolinitic Horizon. .................................................................................................................. 56

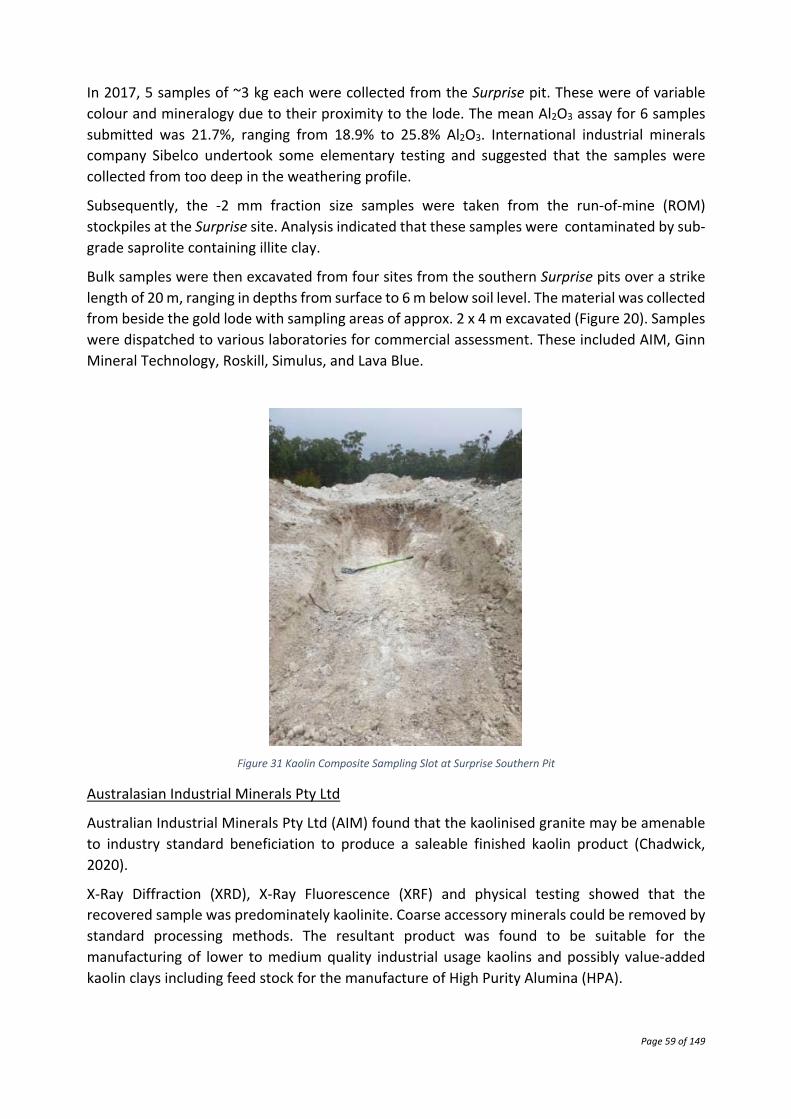

Figure 27 Kaolin Composite Sampling Slot at Surprise Southern Pit ...................................... 59

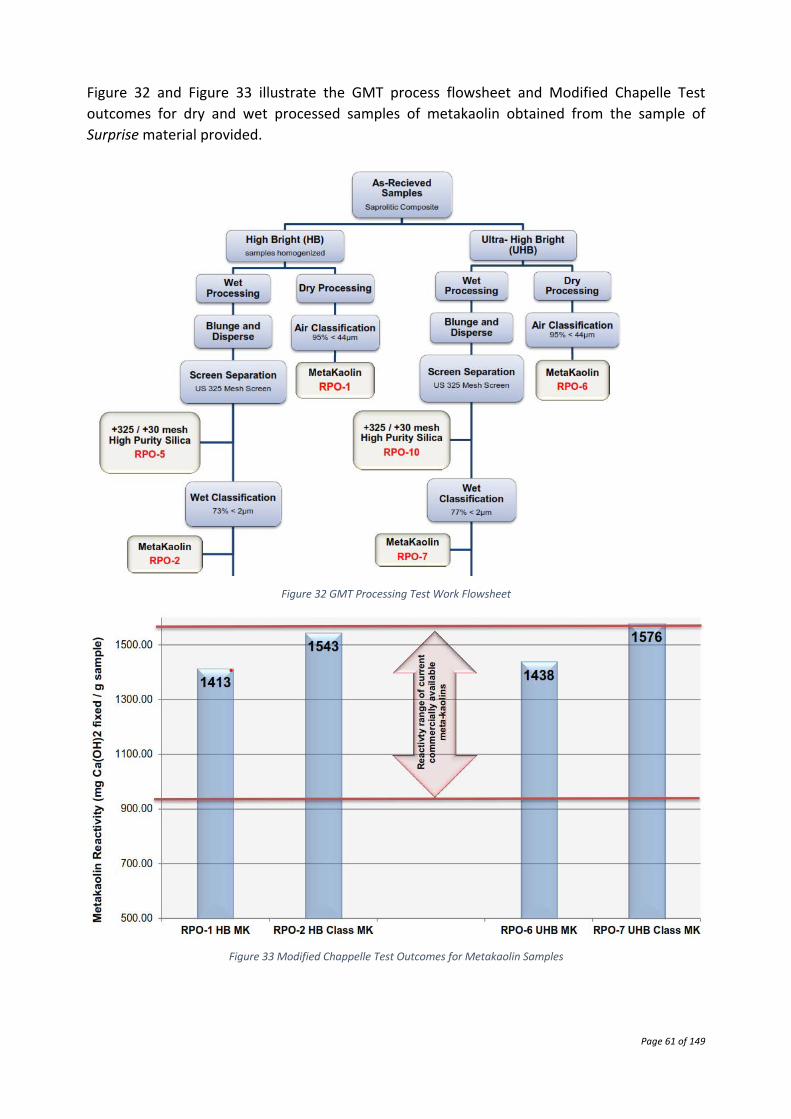

Figure 28 GMT Processing Test Work Flowsheet ................................................................... 61

Figure 29 Modified Chappelle Test Outcomes for Metakaolin Samples ................................ 61

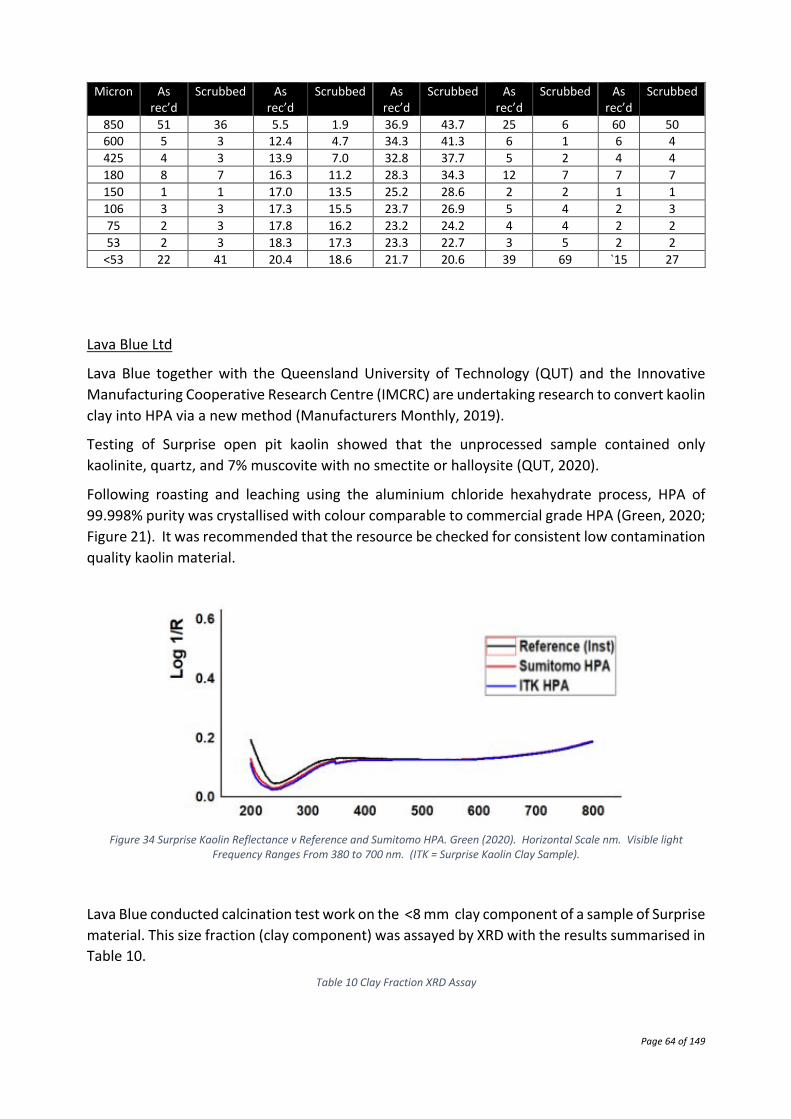

Figure 30 Surprise Kaolin Reflectance v Reference and Sumitomo HPA. Green (2020). Horizontal Scale nm. Visible light Frequency Ranges From 380 to 700 nm. (ITK = Surprise Kaolin Clay Sample). ............................................................................................................... 64

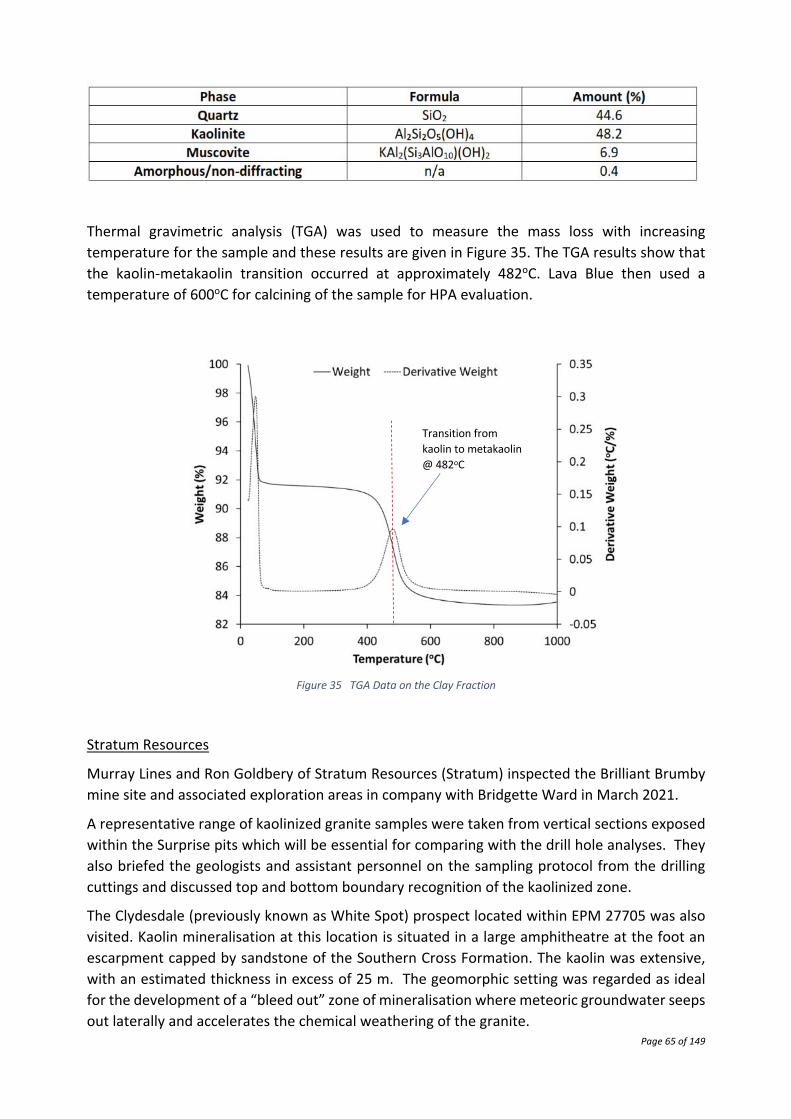

Figure 35 TGA Data on the Clay Fraction .............................................................................. 65

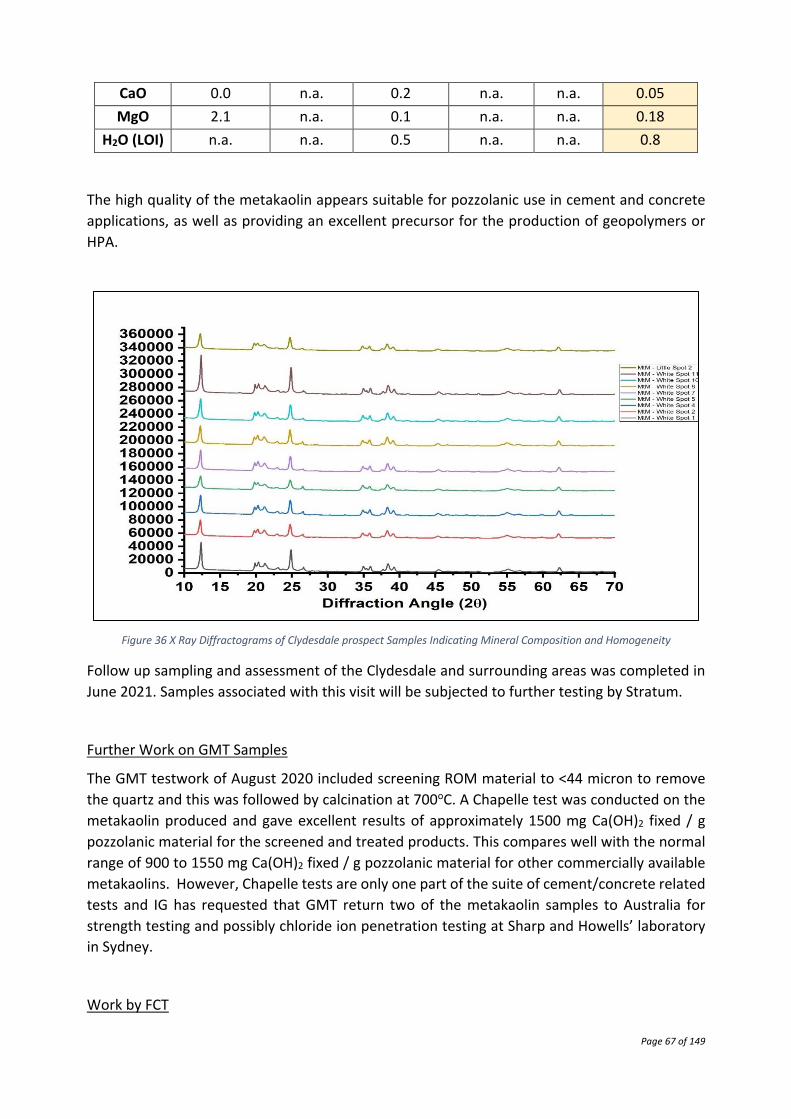

Figure 36 X Ray Diffractograms of Clydesdale prospect Samples Indicating Mineral Composition and Homogeneity .............................................................................................. 67

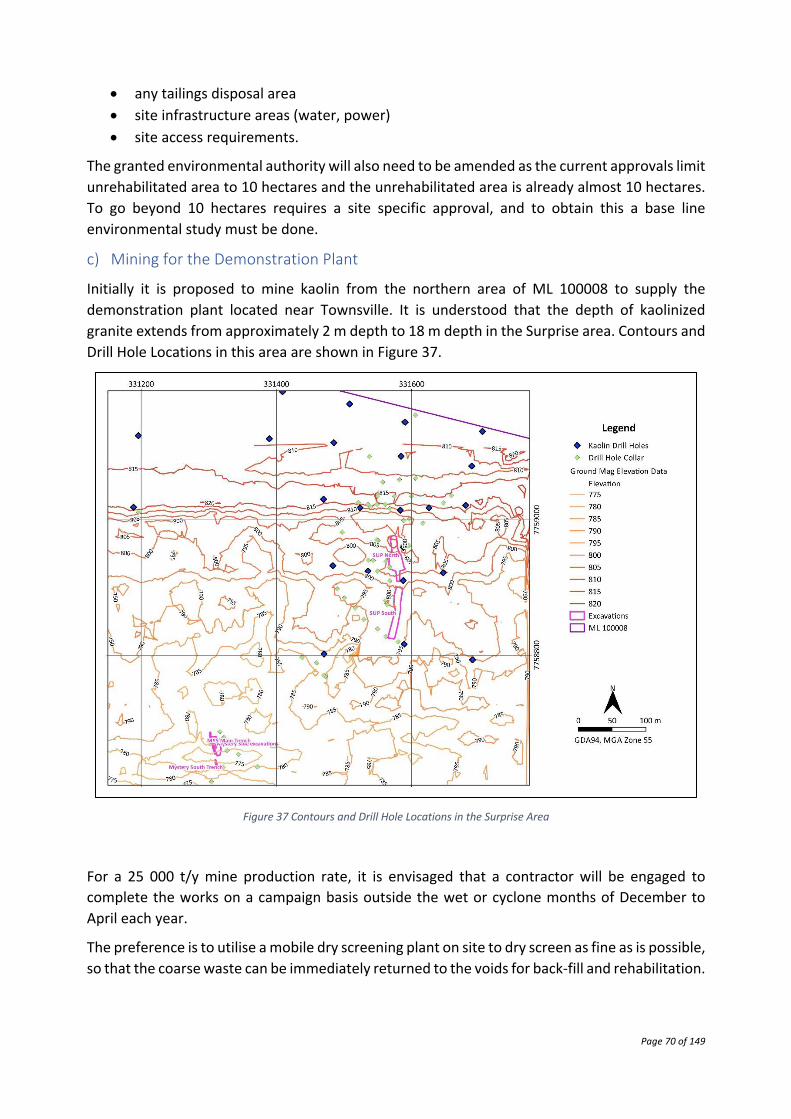

Figure 37 Contours and Drill Hole Locations in the Surprise Area .......................................... 70

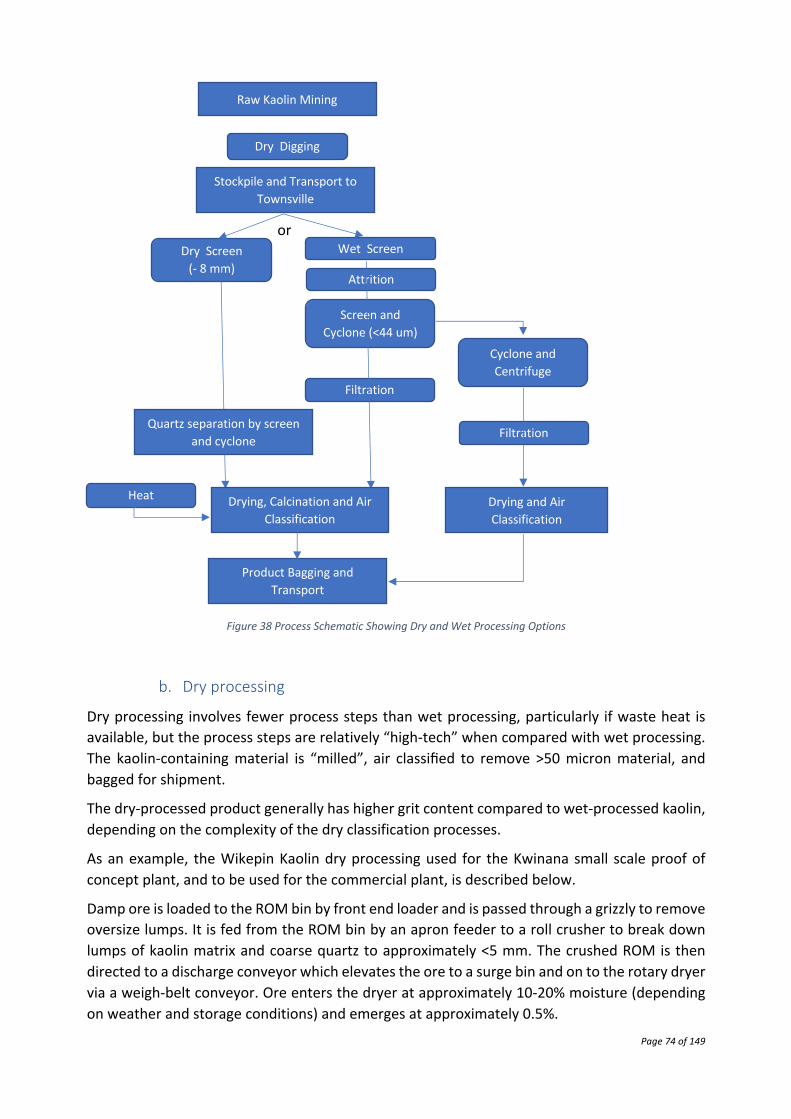

Figure 32 Process Schematic Showing Dry and Wet Processing Options ............................... 74

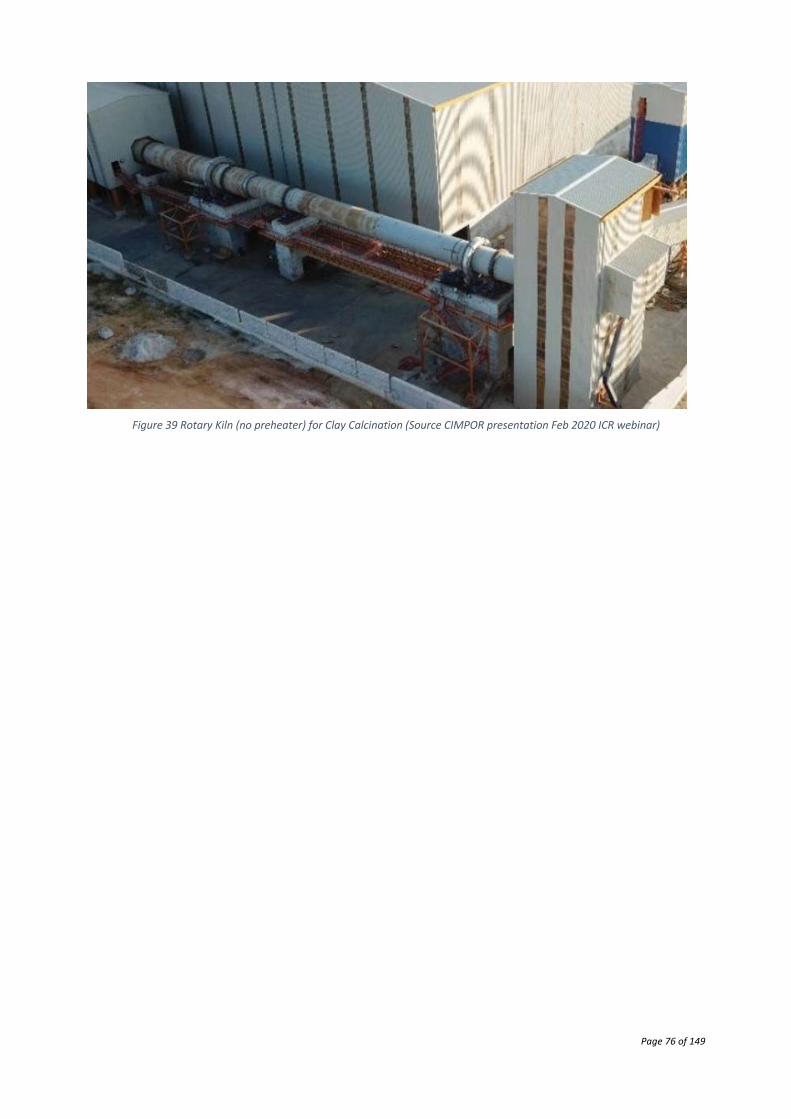

Figure 34 Rotary Kiln (no preheater) for Clay Calcination (Source CIMPOR presentation Feb 2020 ICR webinar) .................................................................................................................. 76

Figure 35 Rotary Kiln with Preheater for Clay Calcination (Source: Dynamis Presentation Feb 2020 ICR webinar) .................................................................................................................. 77

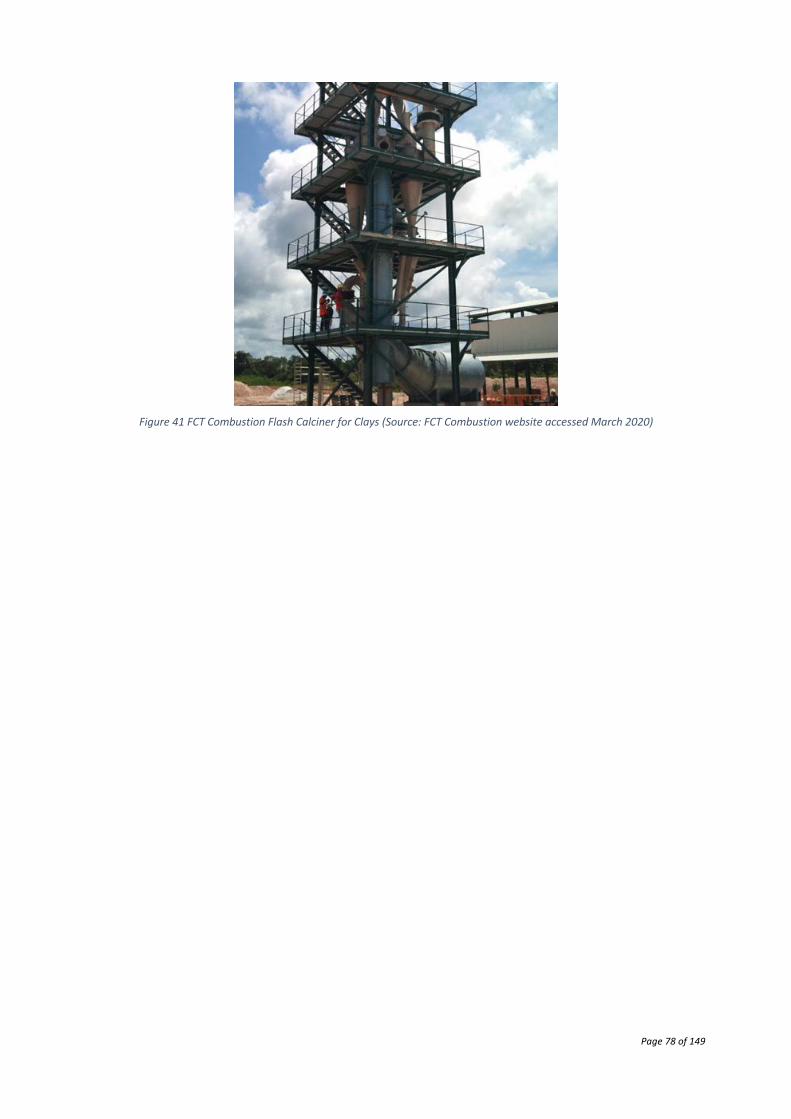

Figure 36 FCT Combustion Flash Calciner for Clays (Source: FCT Combustion website accessed March 2020) ........................................................................................................................... 78

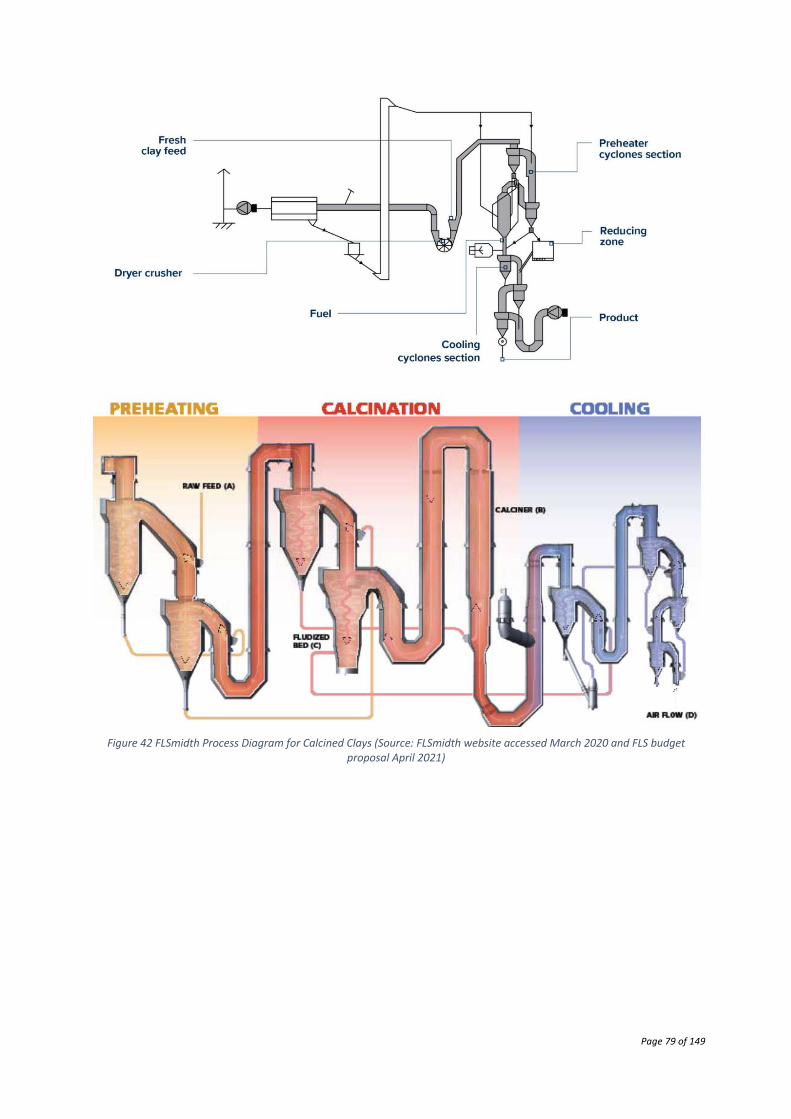

Figure 37 FLSmidth Process Diagram for Calcined Clays (Source: FLSmidth website accessed March 2020 and FLS budget proposal April 2021) ................................................................. 79

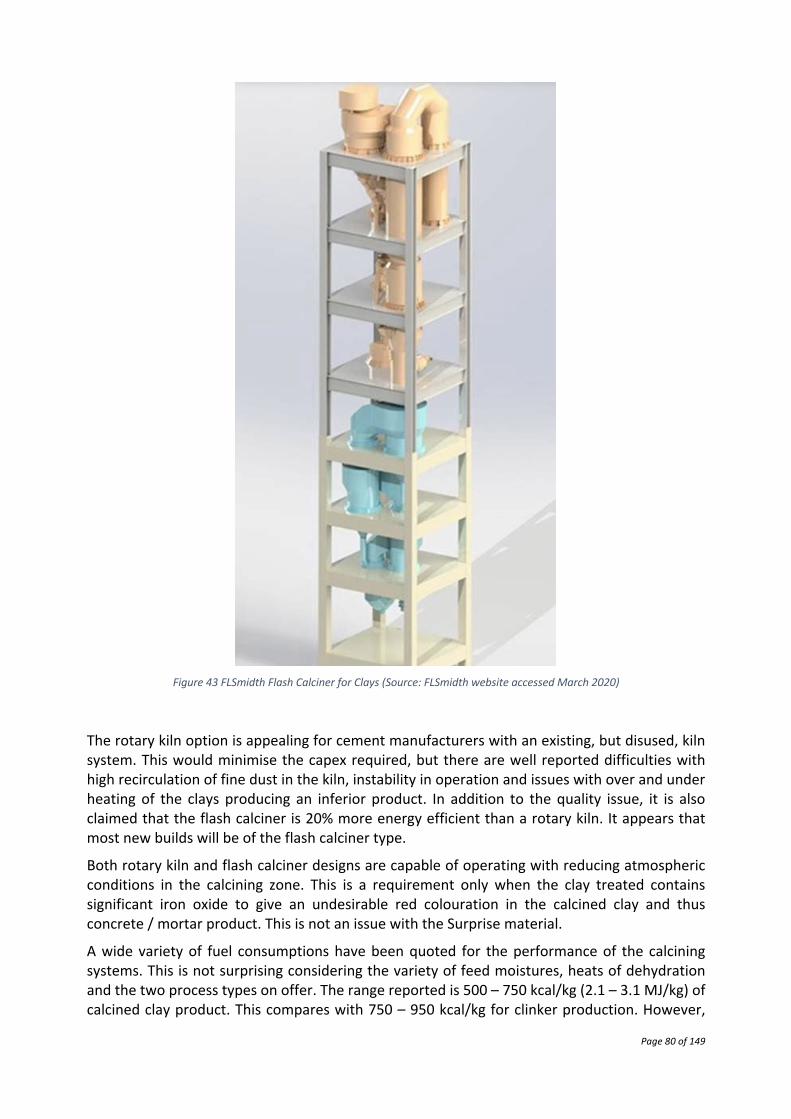

Figure 38 FLSmidth Flash Calciner for Clays (Source: FLSmidth website accessed March 2020) ................................................................................................................................................ 80

Figure 39 Power Supply Infrastructure ................................................................................... 83

Figure 40 2017 EBBAR Road Construction to ML 100008. ..................................................... 83

Figure 41 Global Construction Industry Spending 2014-19 With Forecasts for 2020-35 (US$ trillions) (Source: Statista) ...................................................................................................... 85

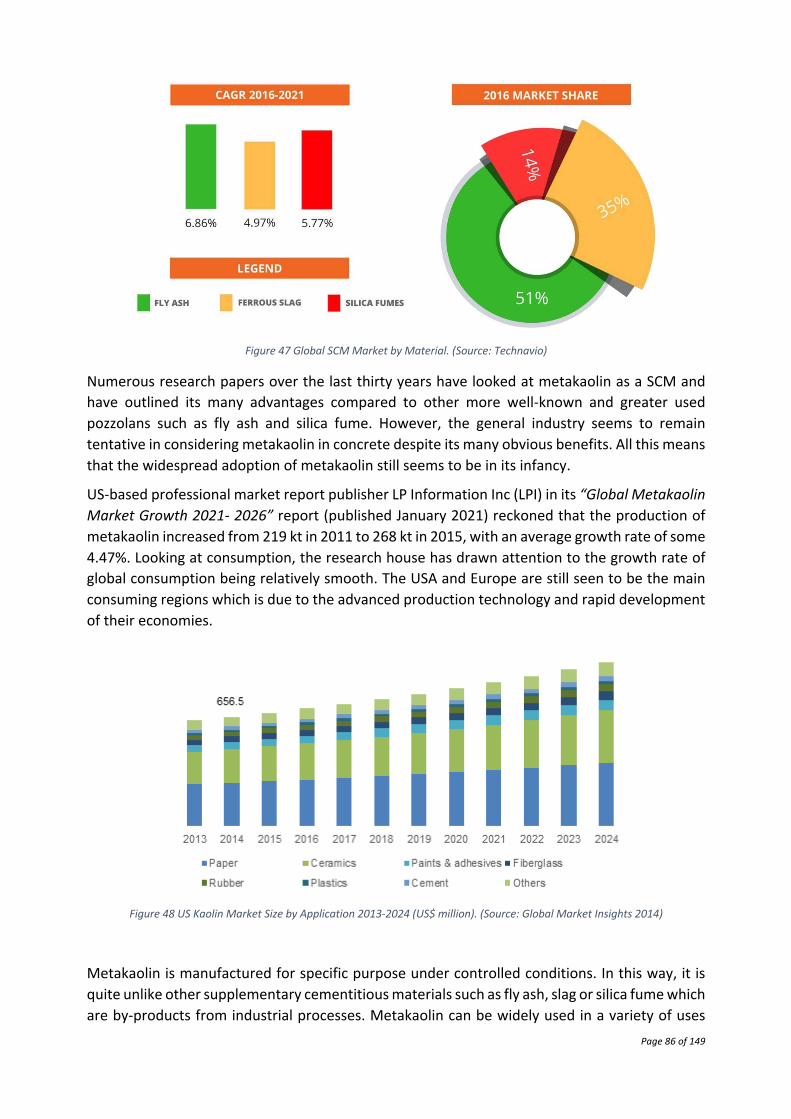

Figure 42 Global SCM Market by Material. (Source: Technavio) ............................................ 86

Page 9 of 149

Figure 43 US Kaolin Market Size by Application 2013-2024 (US$ million). (Source: Global Market Insights 2014) ............................................................................................................. 86

Figure 44 Townsville SDA Locality ......................................................................................... 96

Figure 45 Townsville SDA Regional Setting ....................................................................... 97

Figure 46 SDA Precincts Showing Castral Parcels ............................................................ 98

Figure 47 SDA Lots With Land Use ................................................................................... 99

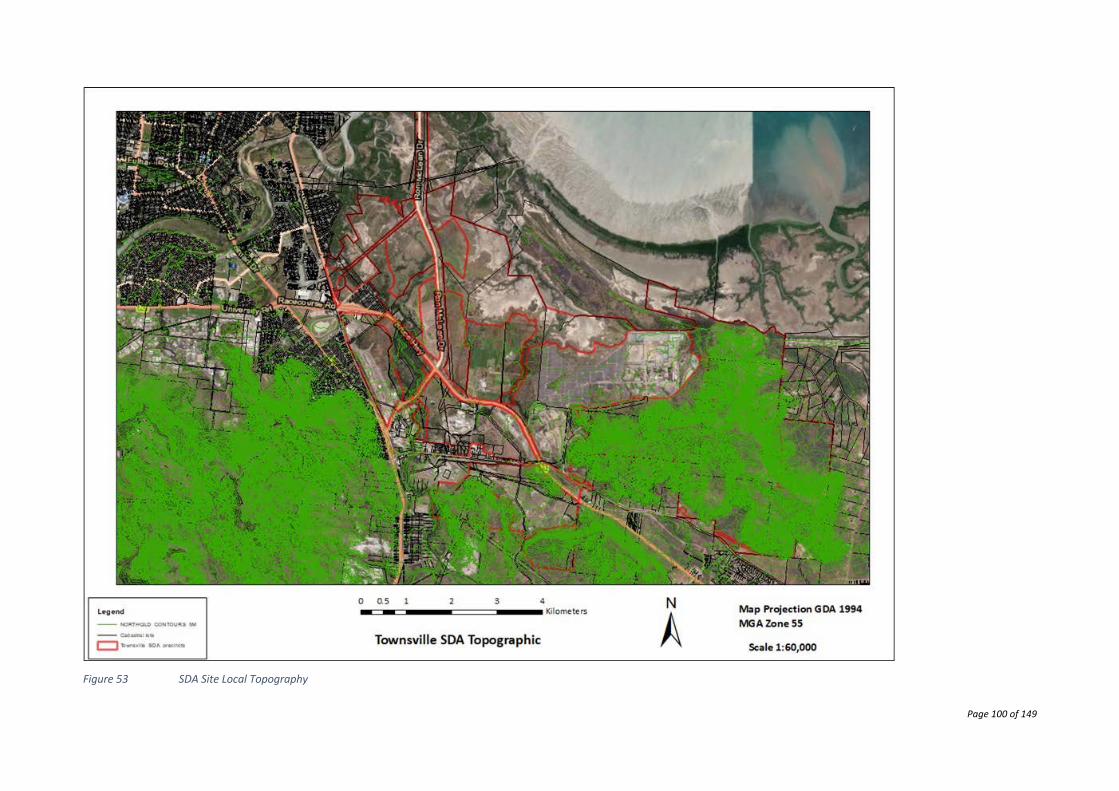

Figure 48 SDA Site Local Topography ............................................................................. 100

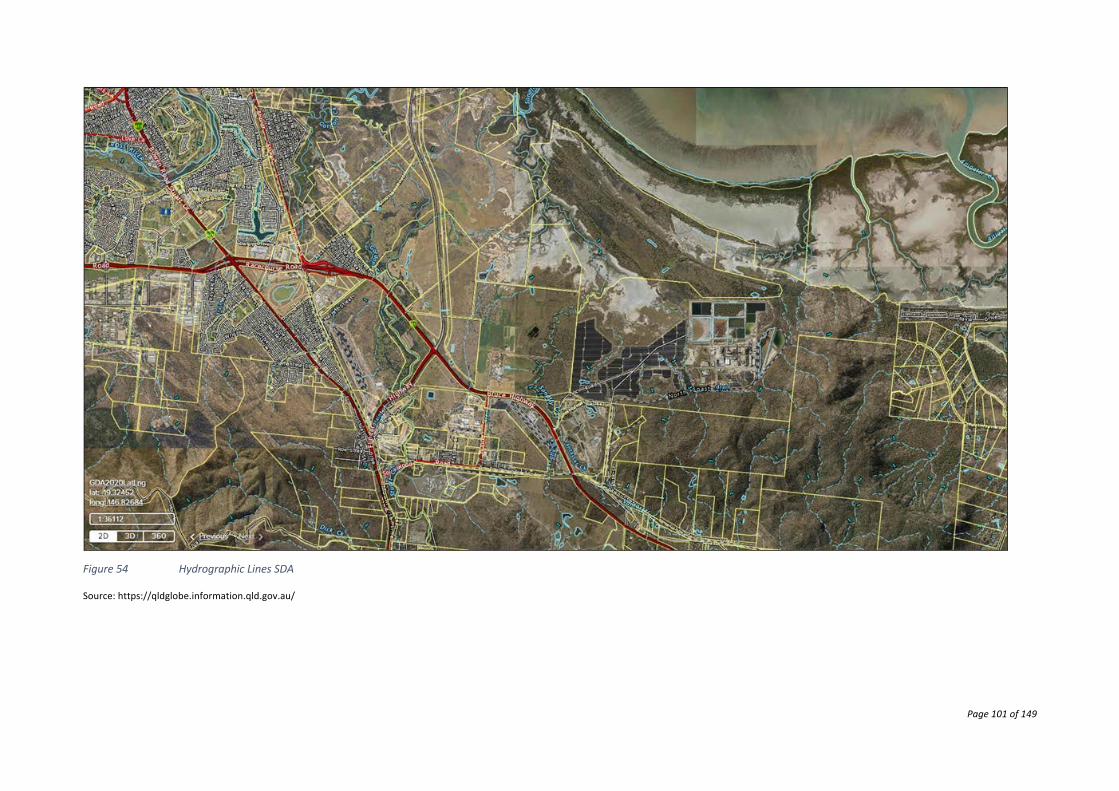

Figure 49 Hydrographic Lines SDA .................................................................................. 101

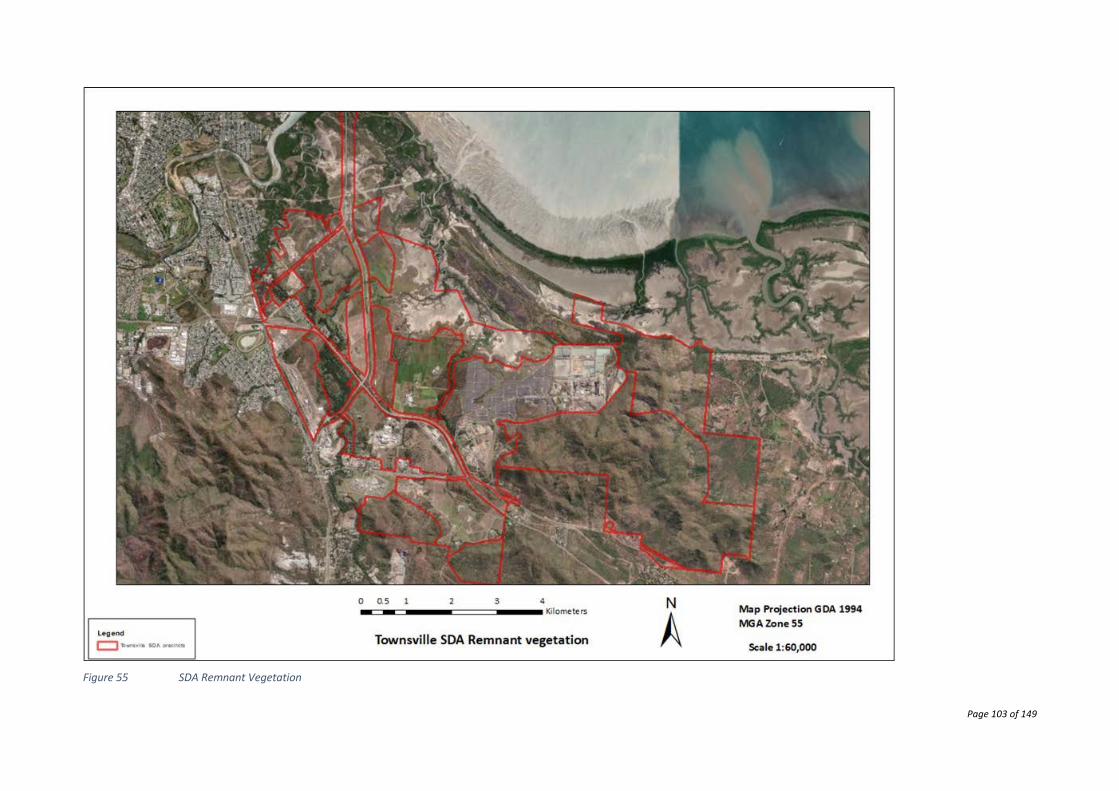

Figure 50 SDA Remnant Vegetation ............................................................................... 103

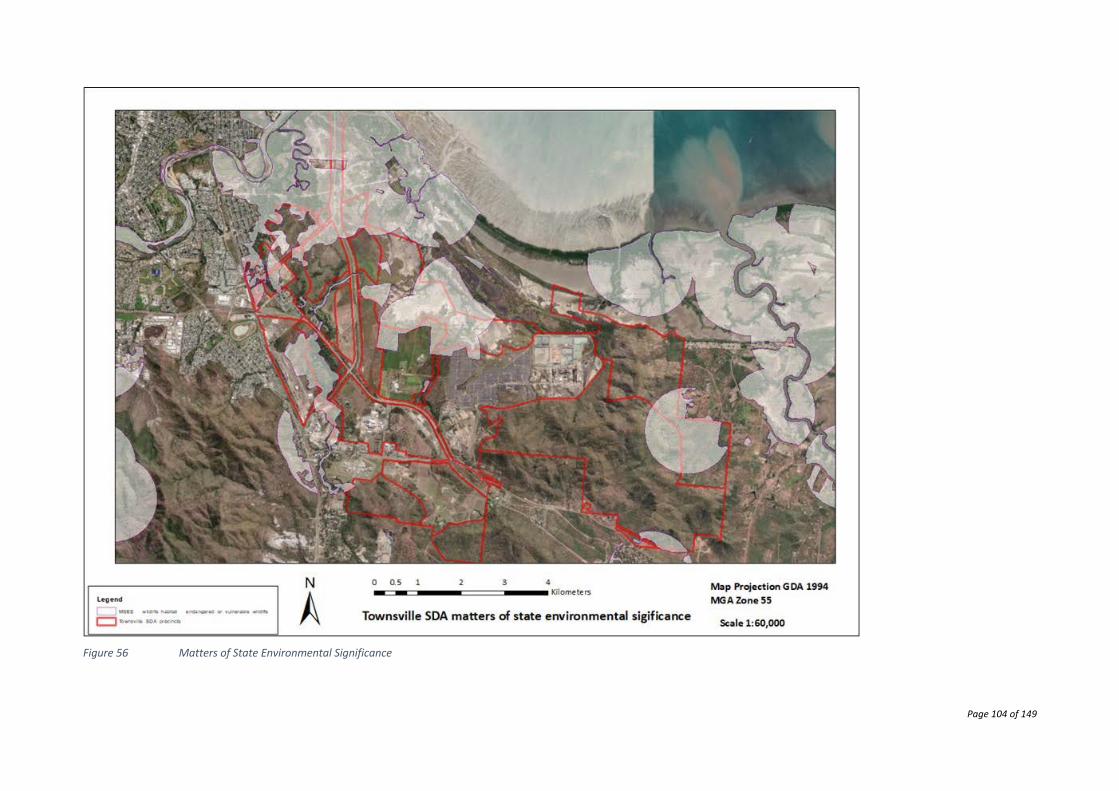

Figure 51 Matters of State Environmental Significance ................................................. 104

Figure 52 Proximity to Community Facilities .................................................................. 107

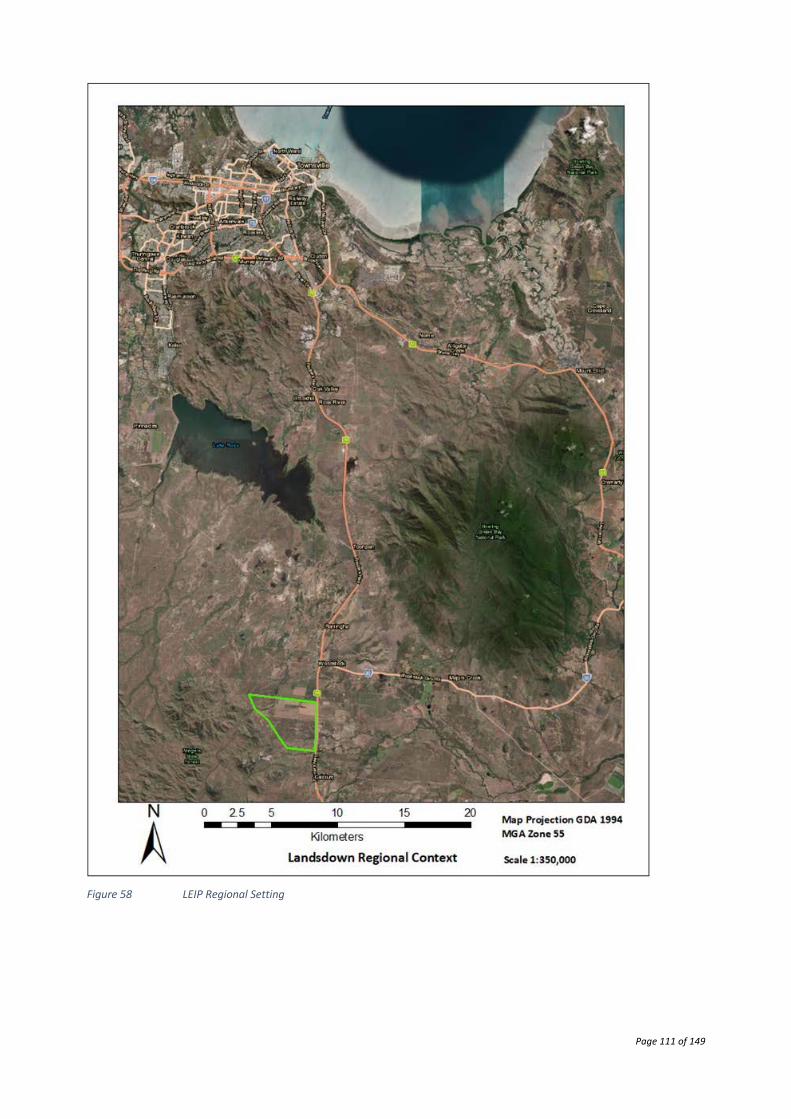

Figure 53 LEIP Regional Setting ...................................................................................... 111

Figure 54 LEIP Local Context ........................................................................................... 112

Figure 55 LIP Cadastral Parcels ....................................................................................... 113

Figure 56 LEIP Topography and Hydrology ..................................................................... 115

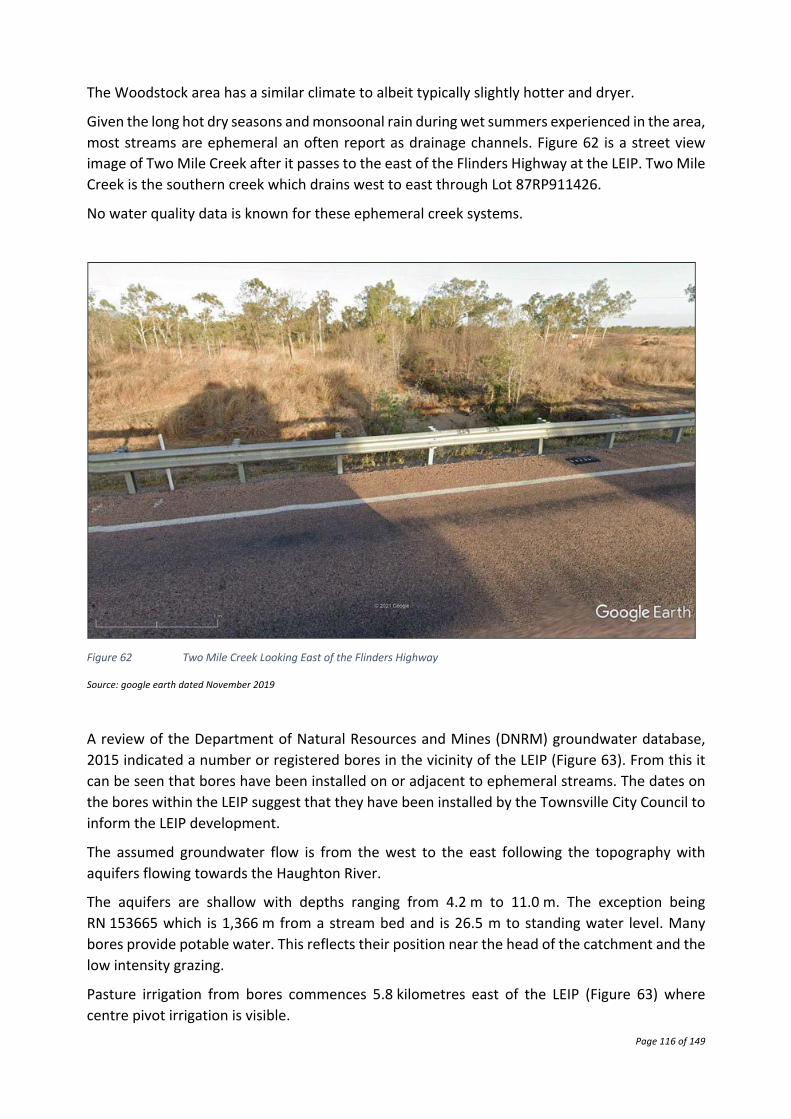

Figure 57 Two Mile Creek Looking East of the Flinders Highway ................................... 116

Figure 58 Registered Bores ............................................................................................. 118

Figure 59 LEIP Natural Values Impact Map .................................................................... 119

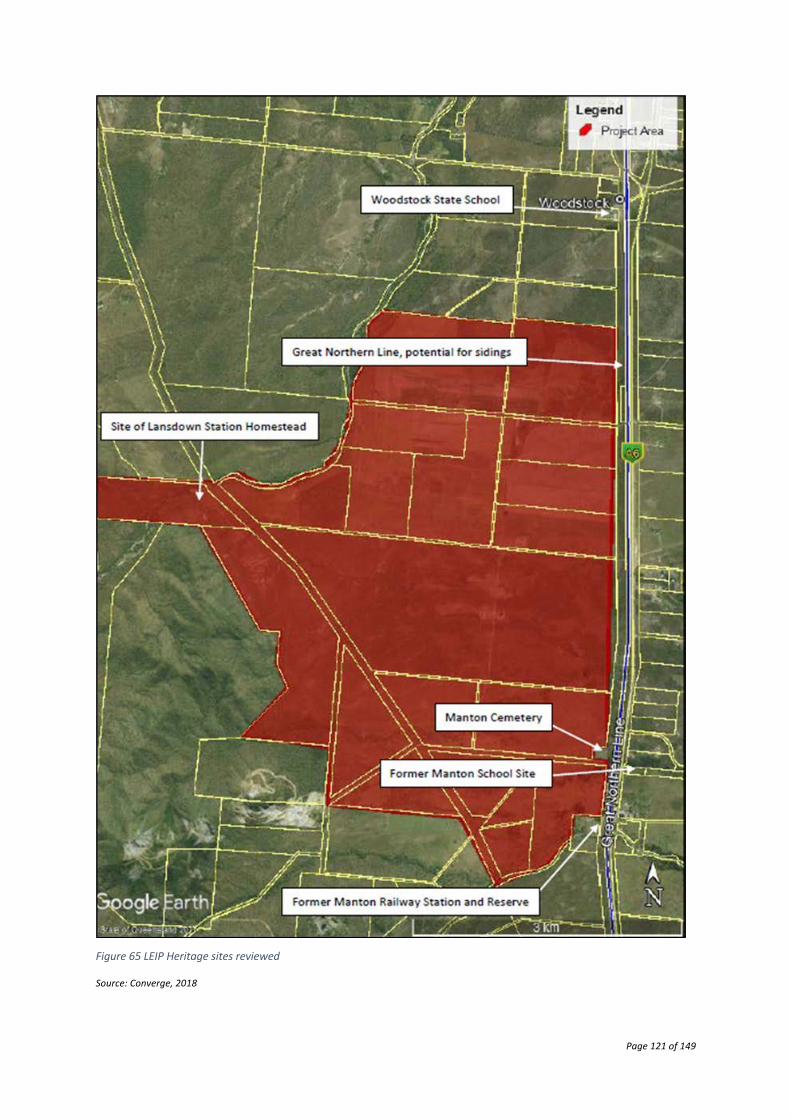

Figure 60 LEIP Heritage sites reviewed ........................................................................... 121

Figure 61 Project Revenues Based on Metakaolin (MK), Kaolin and Aggregate (Sand) ....... 133

Figure 62 Projected Project Cash Flow ................................................................................. 133

Figure 63 Project Returns ..................................................................................................... 134

Figure 64 Project Cash Flow Showing Impact of Grants ....................................................... 134

Figure 65 Kaolin Prospective Areas and Infrastructure. ....................................................... 135

Figure 66 Centauri Area White Reflectance on ESRI Satellite Image. ................................... 136

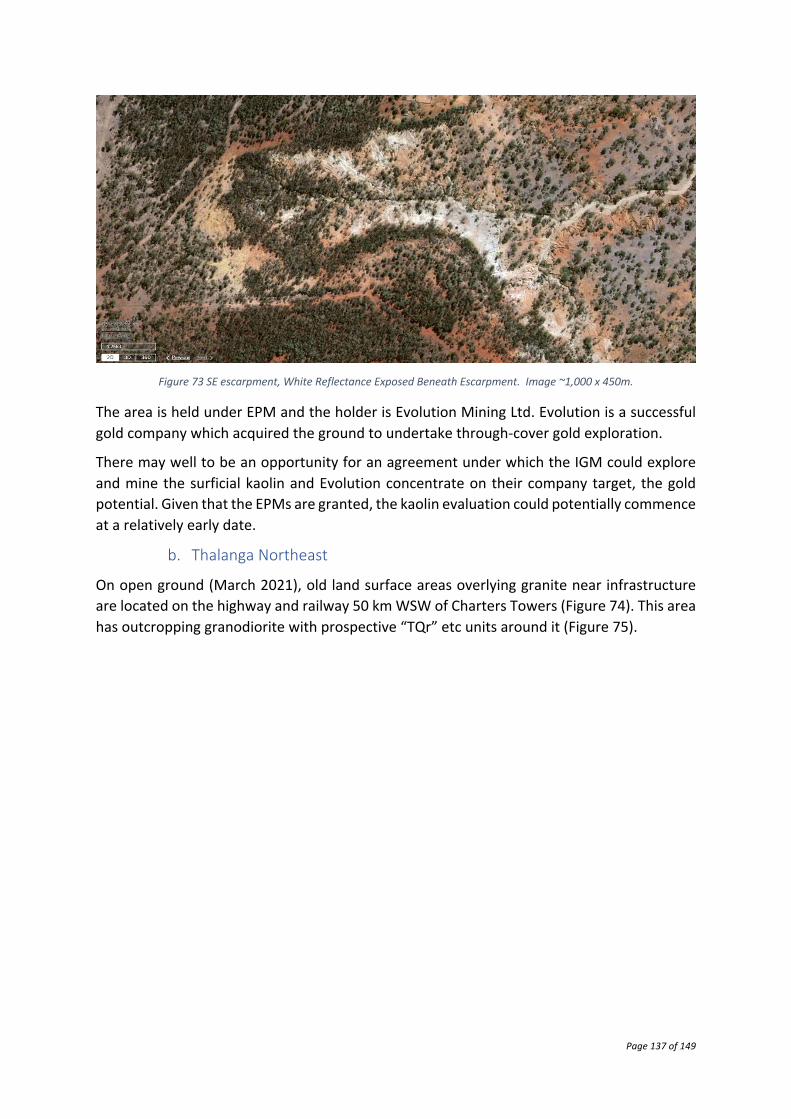

Figure 67 Centauri Road NW, White Reflectance Exposed in Drainage. Image ~1,000 x 450m. .............................................................................................................................................. 136

Figure 68 SE escarpment, White Reflectance Exposed Beneath Escarpment. Image ~1,000 x 450m. ................................................................................................................................... 137

Figure 69 Thalanga NE Kaolin Prospect Location. ................................................................ 138

Figure 70 Thalanga NE Kaolin Prospect Geology. ................................................................. 138

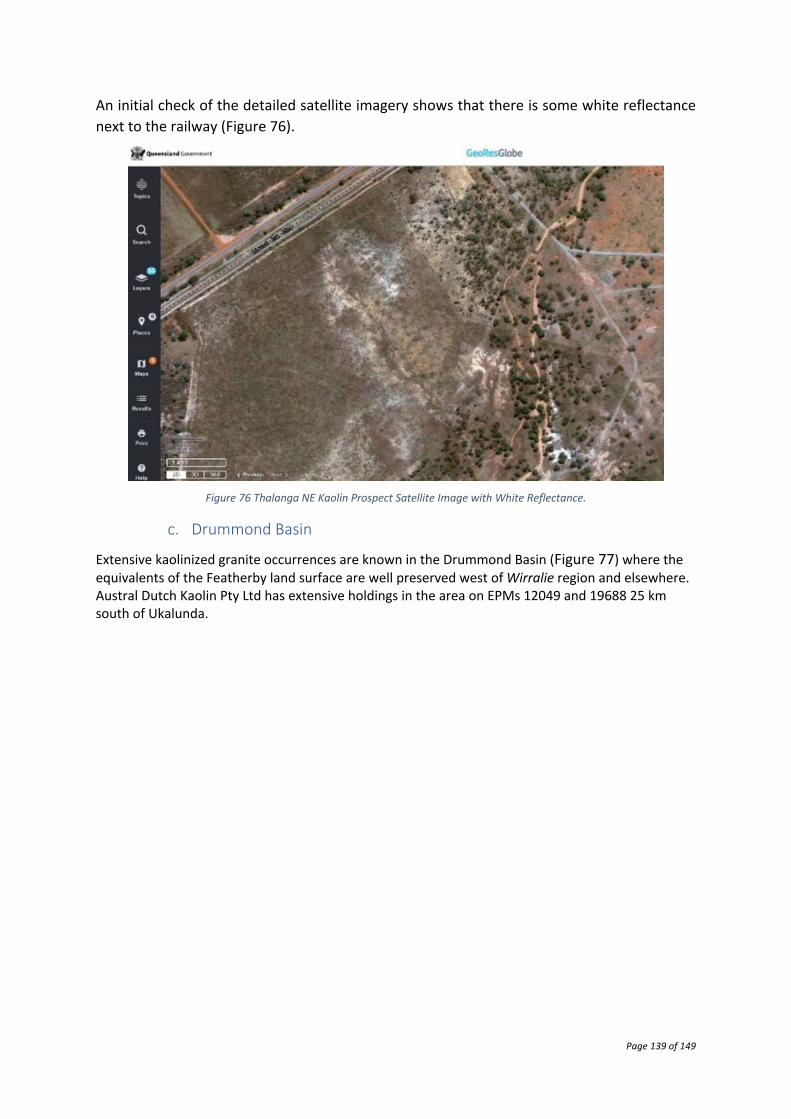

Figure 71 Thalanga NE Kaolin Prospect Satellite Image with White Reflectance. ................ 139

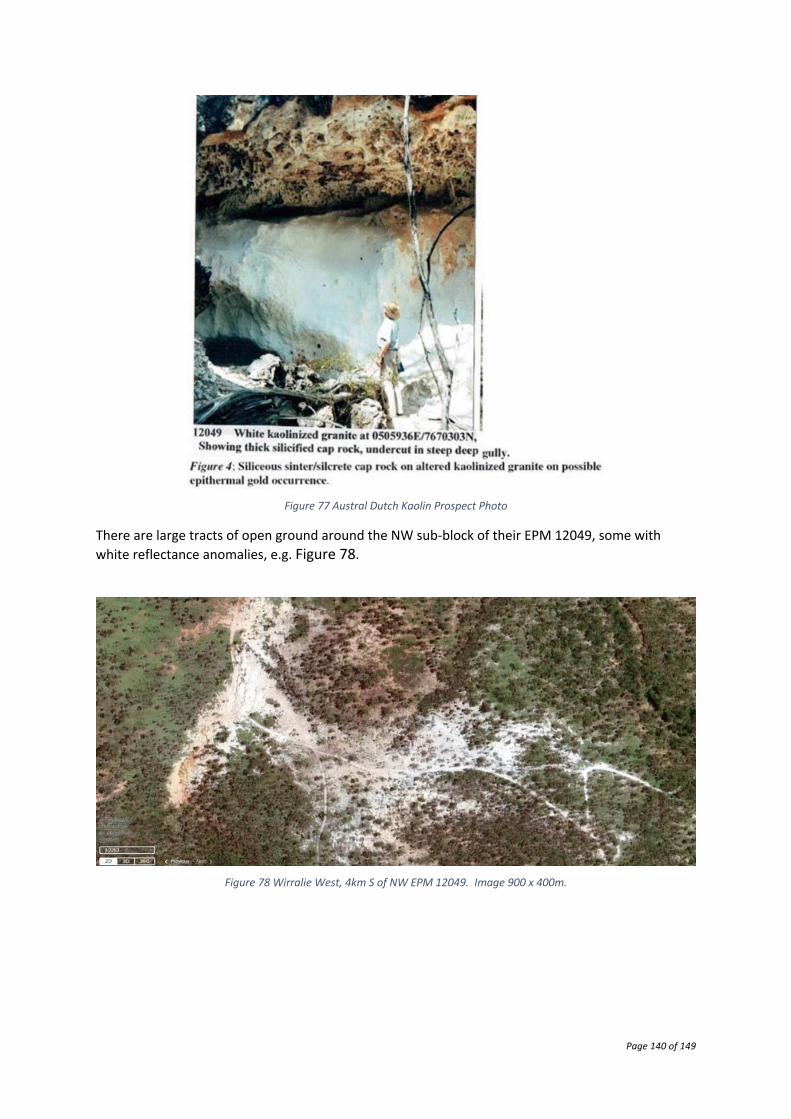

Figure 72 Austral Dutch Kaolin Prospect Photo .................................................................... 140

Page 10 of 149

Figure 73 Wirralie West, 4km S of NW EPM 12049. Image 900 x 400m. ............................ 140

Page 11 of 149

1. Executive Summary a) Context

InterGroup Mining Limited (IGM) is an Australian based exploration and project development company. The company’s activities are focused in North Queensland with a current focus on developing exploration and mining lease areas in the Lolworth Range.

The Brumby/Surprise leases in the Lolworth Range were initially explored and developed with a view to exploit their gold prospects and pilot scale mining activities on the mining lease commenced in 2018. The gold is hosted in quartz veins that are derived from hydrothermal fluids transported through the fractures and weak zones in the Amarra granite.

Over time the near surface granite was weathered and in parts of the project the granite outcrops at surface in the form of quartz grains and clay with minor detrital minerals. Closer examination of the clay component identified kaolinite and drilling at the Surprise prospect indicated a kaolinite rich zone with thicknesses ranging from 1 to 17m.

In 2020, IGM commenced an assessment of whether there was any potential for the commercialisation of the kaolin component.

IGM is evaluating a project based on staged development that includes:

• An initial 1 t/h metakaolin demonstration plant • Followed by a 300 000 t/y metakaolin production plant.

Both project stages would also produce a small quantity of kaolin for industrial uses. The demonstration plant will be used to refine the production process and match the products to the market.

The Surprise Project comprises all kaolin-rich areas across IGM’s exploration properties in the Lolworth Range. This includes the Surprise pit, originally developed for trial mining of gold in this location and the source of initial kaolin-based investigations, and other locations as outlined in this report.

This Surprise Project Concept Study Report was compiled to consolidate the work completed on the Project to June 2021. The work has focussed on the evaluation of the geology and the opportunities to commercialise the mining, processing and marketing of the kaolin material.

This report was compiled for internal IGM purposes only.

b) Kaolin & Metakaolin

Kaolin is a mineral with a long history of use in multiple applications. In many of these applications from paper to ceramics it is used as a filler. For the higher value applications, the whiteness of the kaolin, which in turn affects the whiteness of the end product, is the primary determinant of value. High whiteness material achieves substantial price premiums whereas the lower value products are priced at close to the cost of supply. In this regard, the kaolin initially found on the Surprise lease did not achieve the highest brightness, principally due the level of iron content in its chemistry. However, the nearby Clydesdale area appears to contain kaolin that may achieve high brightness specifications.

Page 12 of 149

There are other applications for kaolin within the building sector that rely more on its mineralogical and chemical characteristics than is colour. At the basic level, it can be used as part of the raw material feed for clinker production (the calcination process that converts limestone into Ordinary Portland Cement (OPC)) where it is used to make up chemical shortfalls in the feed mix. While Surprise material would be relevant to these applications it is unlikely that the material would achieve more than a marginal return over cost.

An alternative and growing market for kaolin in the construction sector does offer an attractive option for the commercialisation of the Surprise kaolin, notably in the production of metakaolin (a highly reactive pozzolanic material) and its subsequent use as a Supplementary Cementitious Material (SCM). Metakaolin has be used in the construction industry for many years because its addition to OPC improves the engineering properties, the workability and finishing, and the durability of the resulting concrete. Traditionally, metakaolin based cements have been applied in more niche applications where architectural or performance needs result in its specification.

However, the use of metakaolin as a partial substitute for OPC also results in concrete with lower carbon emissions. Currently, cement production is the biggest global emitter of CO2 at about 8% of global industrial production. In this context, a range of SCMs have historically be used to extend clinker usage in the production of cement and then concrete. These SCMs are variously cementitious materials that were by-products of other processes such as iron slag, fly ash or silica fume dust. As by-products of, or waste from, other processes they were typically cheap to procure and their usage as SCMs reduced the cost of the resulting cement.

Typically cement production results in 925 kg of CO2 per tonne of cement. Around half (52.5%) these emissions (479 CO2 kg/t cement) are the direct result of calcining limestone CaCO3 to form CaO. The next largest source (approximately 35%) of emissions relate to the energy used for calcination, requiring a temperature of approximately 1,400oC, with the residual emissions (12.5%) relating to mining, ancillary processing and transportation activities1.

c) Business Configuration

Kaolin was observed in, and adjacent to, the Surprise trial mining pit that was initially mined for quartz bearing gold. Subsequently, the Surprise Project has been used as the project name for the kaolin commercialisation in the wider area, which includes a notable occurrence at Clydesdale and, more generally, mineralisation along at least a 16 km strike length.

Following the completion of the IGM Competent Persons Report (CPR) by Map to Mine Pty Ltd (M2M), work has been undertaken to establish JORC Code exploration target tonnage ranges.

In early 2020 internal “back of the envelope” guesstimates were made of potential resources. These suggested potential for commercial kaolin containing material across the various EPMs that then made up the Brilliant Brumby Project. In the Surprise pit area, the kaolin layer occurs above the 740 m RL contour with the deposits associated with more abundant tree cover. The Queensland Government’s GeoResGlobe high-resolution satellite imagery has now

1 Czigler, T., Reiter, S., Schulze, P., Some, K., Laying the foundation for zero-carbon cement, McKinsey & Company, May, 2020

Page 13 of 149

been used to better delineate prospective areas. Darker green vegetation areas correlate with denser tree cover and are interpreted to be due to improved moisture retention related to more abundant clay in the sub-surface.

Assuming the Featherby surface is preserving the kaolinized granite below surface there is a total of 1,209 ha with interpreted full kaolinitic profiles on the Surprise Project tenements (12 sq.km.) including 17.5 ha on ML 100008.

Based on these areas, tonnage estimations were made using an inferred density of 1.7 t/cubic metre for kaolinized granite (FYI Resources, 2018). For the total Project the kaolin material would range from 41 Mt to 165 Mt depending on the thickness of the kaolinization (estimate range is based on a thickness of between 2 and 8 m). These values will remain speculative until the geology is confirmed on the ground. Drilling in March 2021 was focused on the Surprise prospect on ML 100008 and was designed to provide data for a resource estimate. While test work is still ongoing on the drill hole samples, an internal calculation was completed and indicated a potential resource of 1.8 Mt kaolinized granite at a 17.6 % Al2O3. This is not a JORC compliant resource and further resource calculations are being completed on the Surprise prospect to update the confidence of these figures.

IGM’s aspirational target is for the production of up to 300,000 t/y of metakaolin (calcined kaolin). Preliminary estimates indicate that the mineable material is about 47% kaolinite and this would require the mining of about 1.2 M t/y of the kaolinized granite.

Metallurgical test work is progressing on material taken from bulk samples in both the Surprise pit and Clydesdale areas. As highlighted earlier, test work on Surprise pit samples has focussed on the suitability of the material for the production of metakaolin for use in cement/concrete. In addition, work is underway to assess the quality of Clydesdale kaolin for industrial uses due to its potential high purity and brightness qualities.

The current focus is predominantly on revenue from metakaolin production. Metallurgical testwork has included the calcination of kaolin to produce metakaolin. The quality of the metakaolin for use in cement/concrete has been checked using Chapelle tests and strength tests will be conducted to validate the expected improvement in concrete quality when Portland cement is substituted (by up to 25%) by metakaolin.

Mining of the kaolin material is expected to result in a relatively low strip ratio and principally be conducted using an excavator and small truck fleet. Initially, it is proposed to mine the kaolin from the northern area of ML 100008 to supply the demonstration plant located near Townsville. It is understood that the depth of kaolinized granite extends from 0 m to 30 m in the Surprise area. For a 25 000 t/y mine production rate, it is envisaged that a contractor will be engaged to complete the works on a campaign basis outside the wet or cyclone months of December to April each year.

Mining operations will initially be completed in daylight hours only to allow for grade control and the observation of quartz veins.

Once the agreements and approvals are obtained it is envisaged that the following activities will be undertaken:

Page 14 of 149

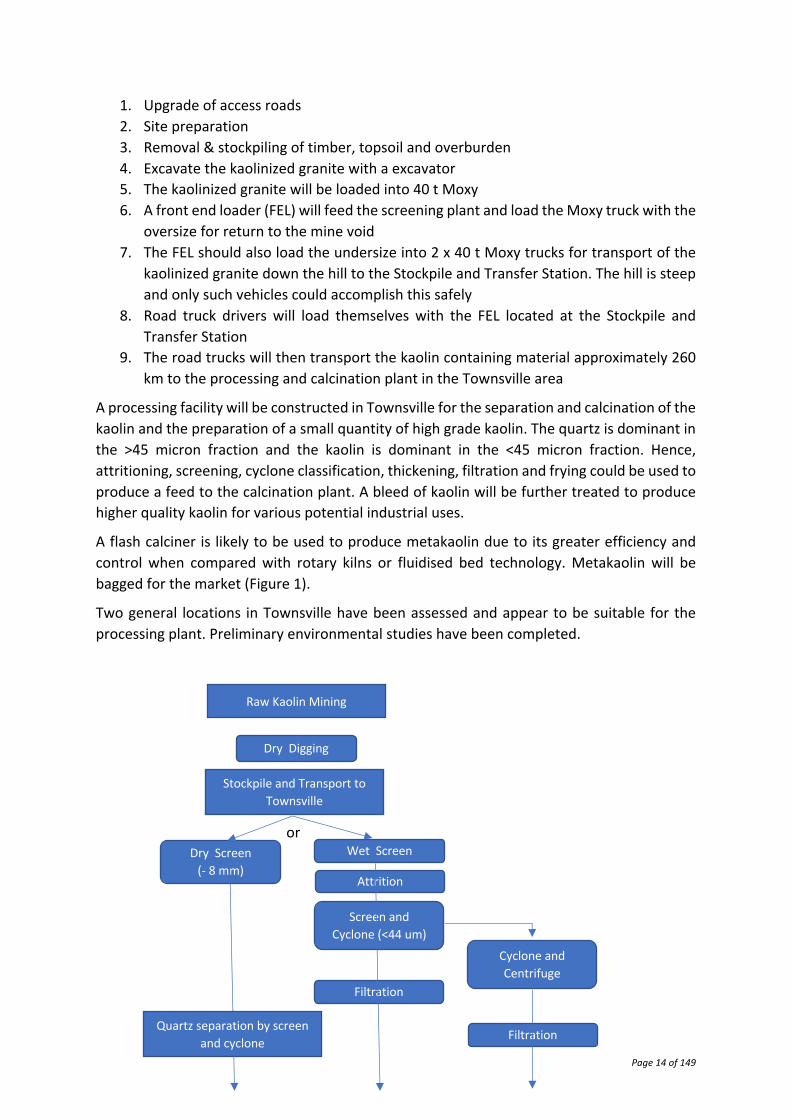

1. Upgrade of access roads 2. Site preparation 3. Removal & stockpiling of timber, topsoil and overburden 4. Excavate the kaolinized granite with a excavator 5. The kaolinized granite will be loaded into 40 t Moxy 6. A front end loader (FEL) will feed the screening plant and load the Moxy truck with the

oversize for return to the mine void 7. The FEL should also load the undersize into 2 x 40 t Moxy trucks for transport of the

kaolinized granite down the hill to the Stockpile and Transfer Station. The hill is steep and only such vehicles could accomplish this safely

8. Road truck drivers will load themselves with the FEL located at the Stockpile and Transfer Station

9. The road trucks will then transport the kaolin containing material approximately 260 km to the processing and calcination plant in the Townsville area

A processing facility will be constructed in Townsville for the separation and calcination of the kaolin and the preparation of a small quantity of high grade kaolin. The quartz is dominant in the >45 micron fraction and the kaolin is dominant in the <45 micron fraction. Hence, attritioning, screening, cyclone classification, thickening, filtration and frying could be used to produce a feed to the calcination plant. A bleed of kaolin will be further treated to produce higher quality kaolin for various potential industrial uses.

A flash calciner is likely to be used to produce metakaolin due to its greater efficiency and control when compared with rotary kilns or fluidised bed technology. Metakaolin will be bagged for the market (Figure 1).

Two general locations in Townsville have been assessed and appear to be suitable for the processing plant. Preliminary environmental studies have been completed.

Raw Kaolin Mining

Dry Digging

Dry Screen (- 8 mm)

Wet Screen

Attrition

Screen and Cyclone (<44 um)

Stockpile and Transport to Townsville

Filtration

Quartz separation by screen and cyclone

or

Cyclone and Centrifuge

Filtration

Page 15 of 149

Figure 1 Process Schematic Showing Dry and Wet Screening Options at the Surprise Site

IGM anticipates that a major source of growth in the demand for metakaolin will be derived from its use as a SCM. This will be driven by the ongoing requirement to reduce construction related CO2 emissions. Metakaolin will either replace fly ash or slag as their availability declines or be used in preference to fly ash and slag to achieve high performance concretes. Market and technical experience indicates that metakaolin can replace clinker cement in concrete by up to 25% and under these circumstances, depending on the rate of market evolution, the demand for metakaolin in Australia alone could reach and exceed 1 million tonnes per year. The current Australian market for cement is approximately 11 million tonnes. For IGM, local Australian demand could be supplemented by exports to nearby pacific countries.

Additionally, Cement Business Advisory estimated that in 2019 Australia imported almost 3 Mt of clinker and 0.9 Mt of cement. The clinker goes to the 12 grinding plants in Australia. Hence, there is a deficit in indigenous clinker in Australia and in theory a good clinker substitute should be of interest to the industry.

The market for bright kaolin is very specific to kaolin product size, assay impurities, colour and brightness. IGM will carefully assess market options when test work on kaolin quantity is further developed.

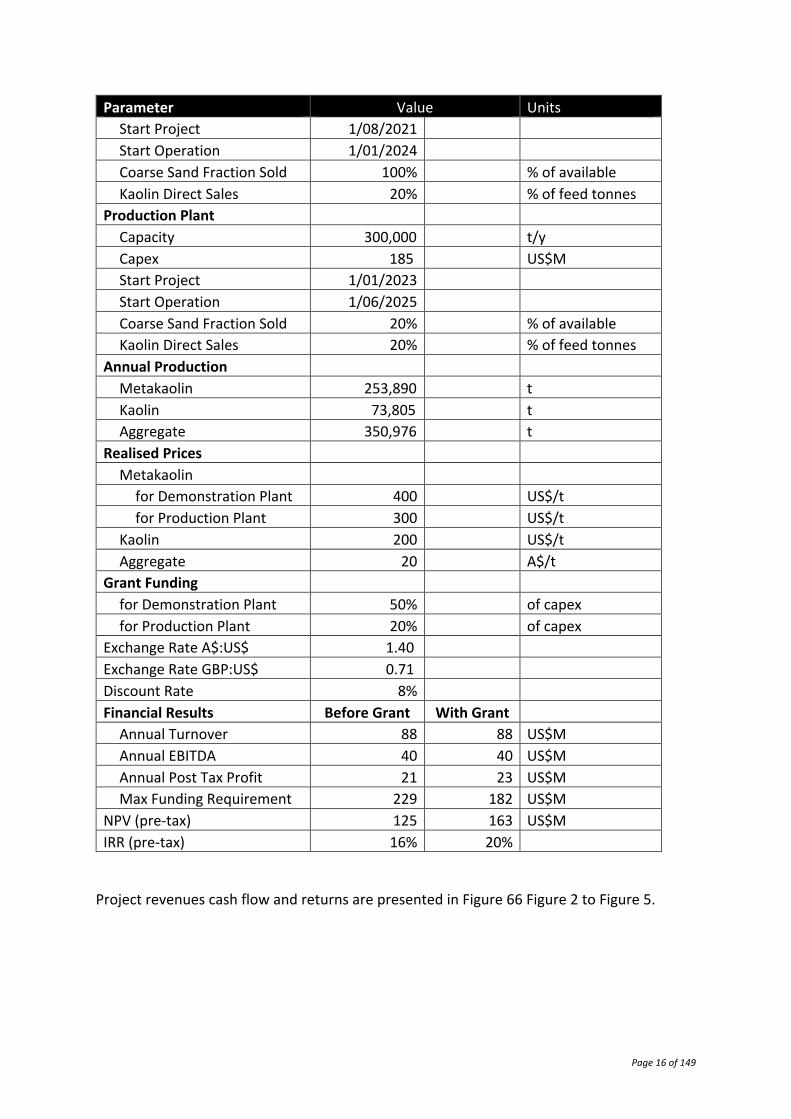

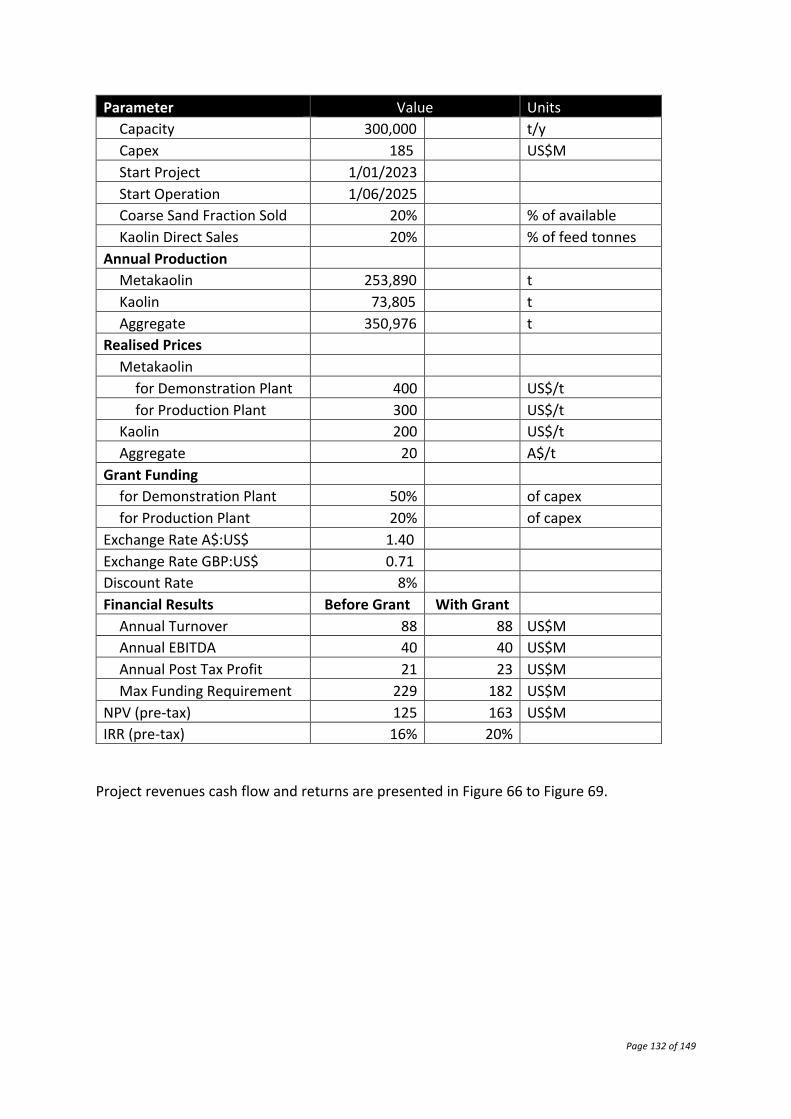

d) Preliminary Economic Assessment

Order of magnitude accuracy capital and operating costs were developed for the project to enable an assessment of project viability, risk and opportunities.

The economic analysis (Table 1) was based on the data provided in this report. The economic analysis is not considered reliable for forecasting and project valuation other than to indicate a potential outcome. The economic analysis was conducted in US$.

Table 1 Summary of Economic Analysis

Parameter Value Units Demonstration Plant

Capacity 10,000 t/y Capex 21 US$M

Drying, Calcination and Air Classification

Heat

Product Bagging and Transport

Drying and Air Classification

Page 16 of 149

Parameter Value Units Start Project 1/08/2021 Start Operation 1/01/2024 Coarse Sand Fraction Sold 100% % of available Kaolin Direct Sales 20% % of feed tonnes

Production Plant Capacity 300,000 t/y Capex 185 US$M Start Project 1/01/2023 Start Operation 1/06/2025 Coarse Sand Fraction Sold 20% % of available Kaolin Direct Sales 20% % of feed tonnes

Annual Production Metakaolin 253,890 t Kaolin 73,805 t Aggregate 350,976 t

Realised Prices Metakaolin

for Demonstration Plant 400 US$/t for Production Plant 300 US$/t

Kaolin 200 US$/t Aggregate 20 A$/t

Grant Funding for Demonstration Plant 50% of capex for Production Plant 20% of capex

Exchange Rate A$:US$ 1.40 Exchange Rate GBP:US$ 0.71 Discount Rate 8% Financial Results Before Grant With Grant

Annual Turnover 88 88 US$M Annual EBITDA 40 40 US$M Annual Post Tax Profit 21 23 US$M Max Funding Requirement 229 182 US$M

NPV (pre-tax) 125 163 US$M IRR (pre-tax) 16% 20%

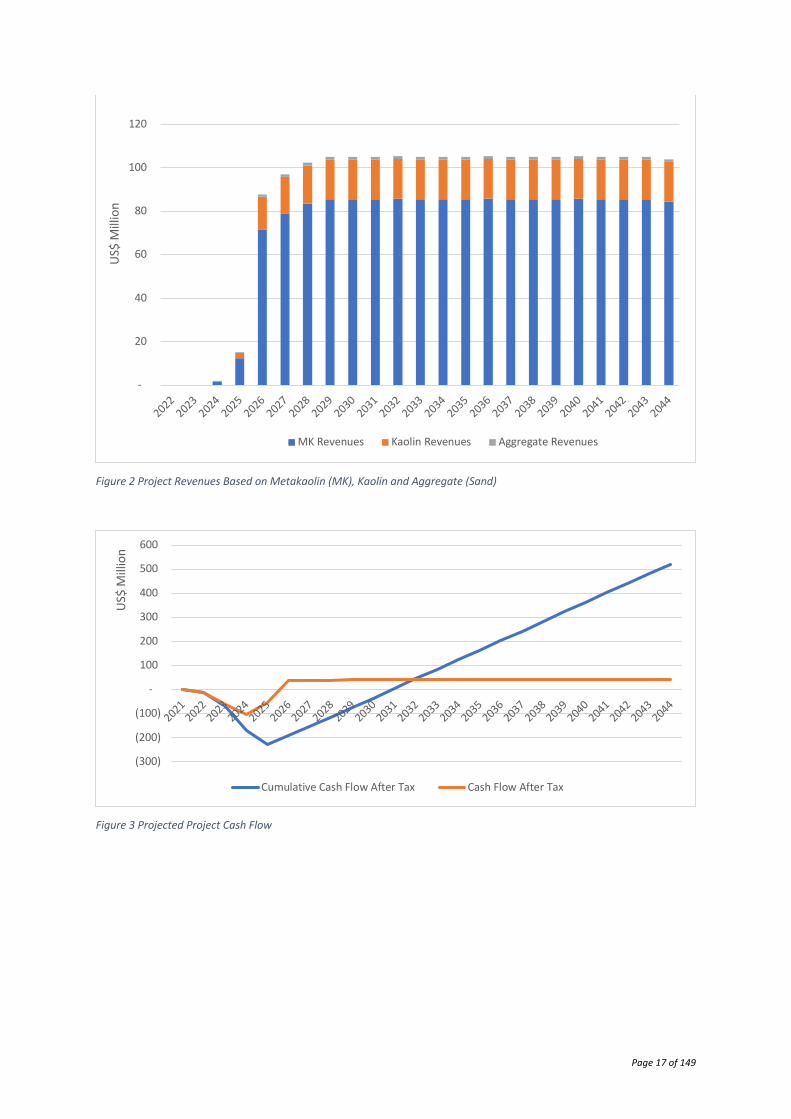

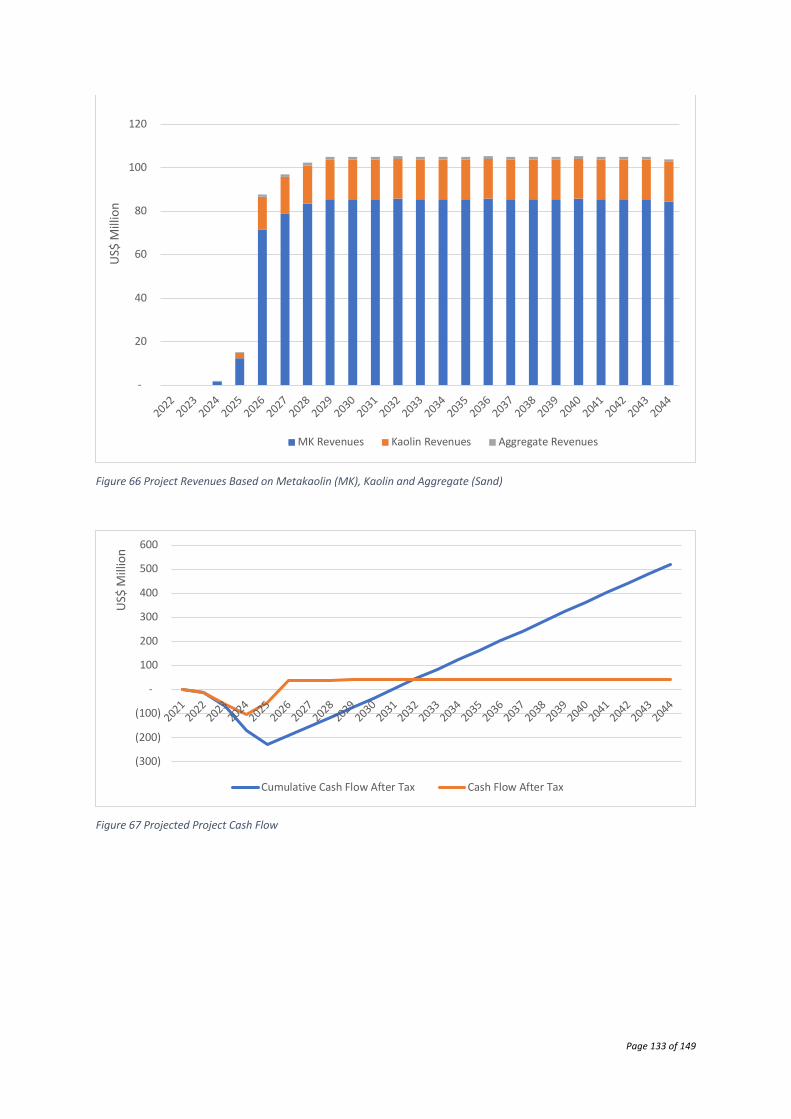

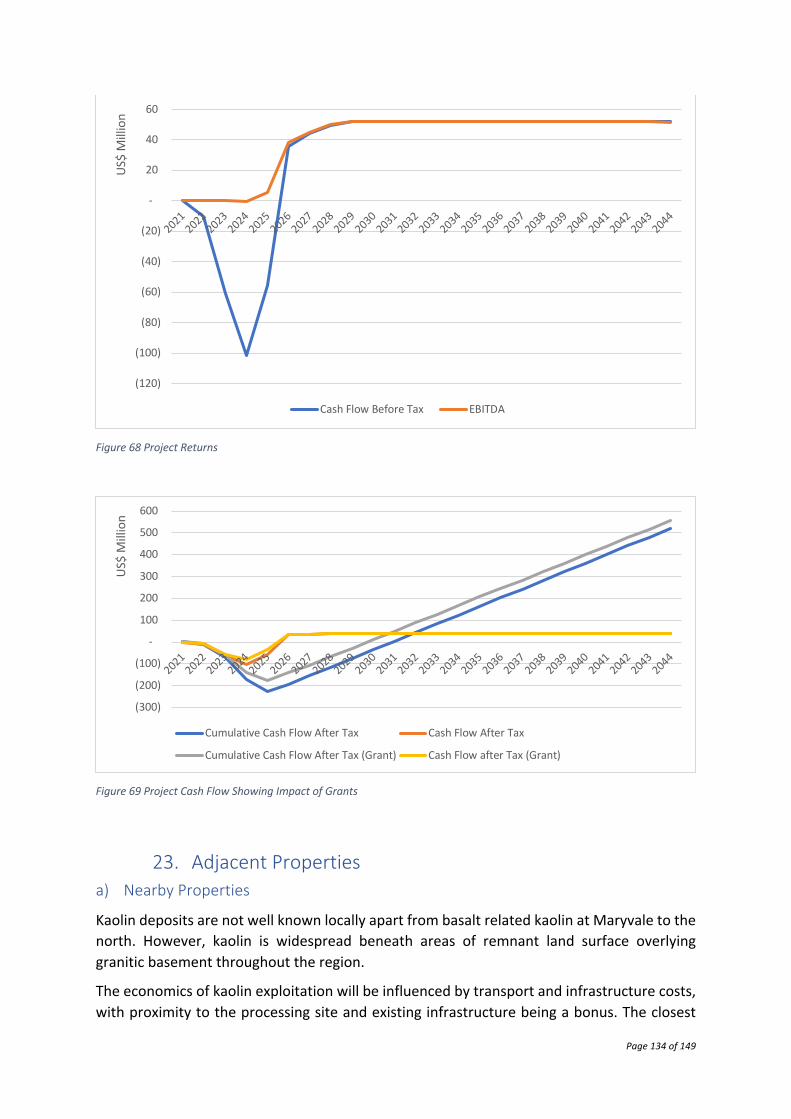

Project revenues cash flow and returns are presented in Figure 66 Figure 2 to Figure 5.

Page 17 of 149

Figure 2 Project Revenues Based on Metakaolin (MK), Kaolin and Aggregate (Sand)

Figure 3 Projected Project Cash Flow

-

20

40

60

80

100

120

20222023

20242025

20262027

20282029

20302031

20322033

20342035

20362037

20382039

20402041

20422043

2044

US$

Mill

ion

MK Revenues Kaolin Revenues Aggregate Revenues

(300)

(200)

(100)

-

100

200

300

400

500

600

20212022

20232024

20252026

20272028

20292030

20312032

20332034

20352036

20372038

20392040

20412042

20432044

US$

Mill

ion

Cumulative Cash Flow After Tax Cash Flow After Tax

Page 18 of 149

Figure 4 Project Returns

Figure 5 Project Cash Flow Showing Impact of Grants

The demonstration plant capital costs were based on mining of the kaolin material at Surprise and coarse dry screening at site to minimise site-related costs. The product transported to the Townsville site for processing would typically be 50% silica and 50% kaolin with a high separation efficiency at 45 microns due to the very fine nature of the kaolinite clays.

As a result, mine site capital costs are limited to infrastructure as all site works will be conducted on a contract basis.

Key elements of the Townsville demonstration plant are:

(120)

(100)

(80)

(60)

(40)

(20)

-

20

40

60

20212022

20232024

20252026

20272028

20292030

20312032

20332034

20352036

20372038

20392040

20412042

20432044

US$

Mill

ion

Cash Flow Before Tax EBITDA

(300)

(200)

(100)

-

100

200

300

400

500

600

20212022

20232024

20252026

20272028

20292030

20312032

20332034

20352036

20372038

20392040

20412042

20432044

US$

Mill

ion

Cumulative Cash Flow After Tax Cash Flow After Tax

Cumulative Cash Flow After Tax (Grant) Cash Flow after Tax (Grant)

Page 19 of 149

• Material receival and storage • Attritioning • Screening • Cycloning • Kaolin dewatering (thickening and filtration) • Kaolin drying • Kaolin packaging (for kaolin sales) • Kaolin calcination • Kaolin product handling • Silica sand product handling • Plant infrastructure (water and power) • Warehouse, offices and maintenance facilities will be located in a common building

(shed)

In addition, allowance is made for owner’s project costs (including exploration and geology and project management), contingency and indirect costs.

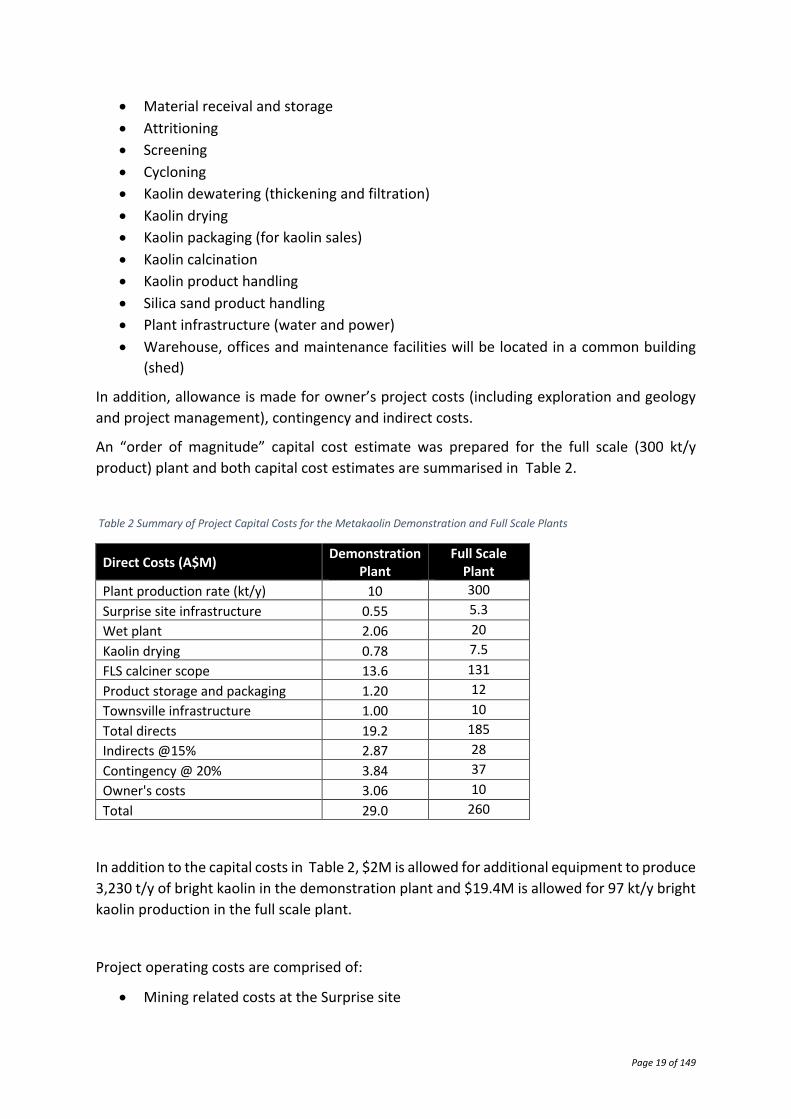

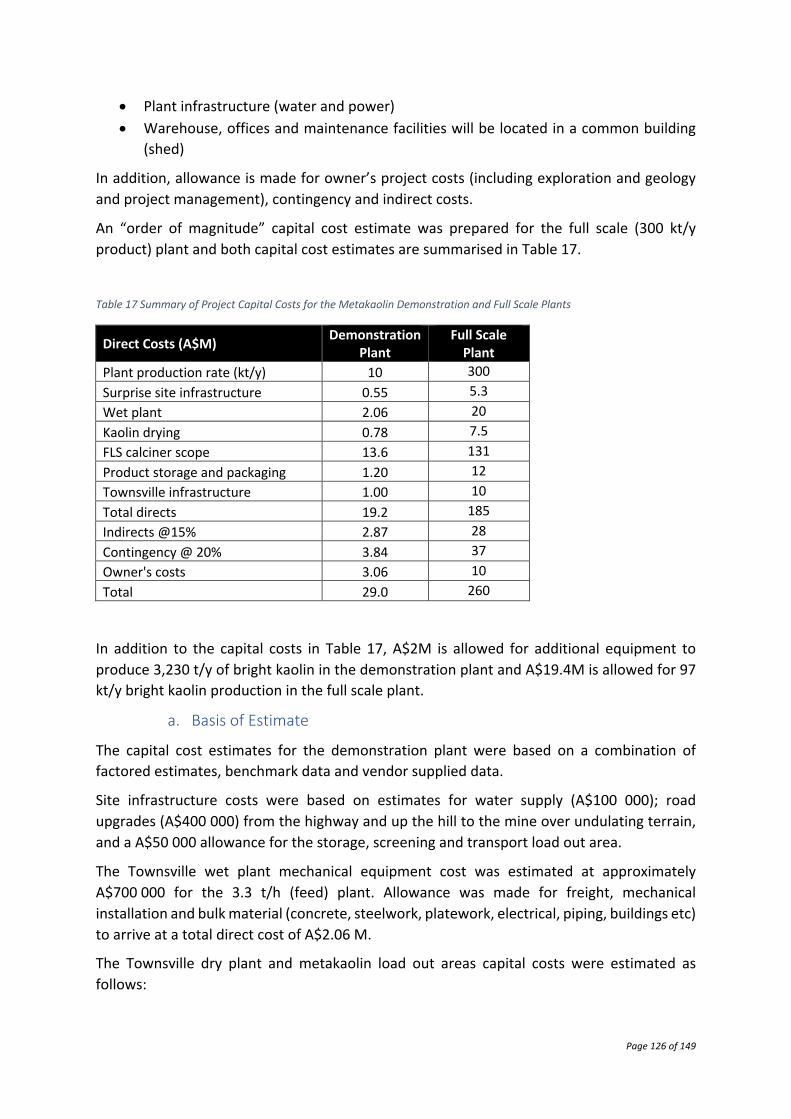

An “order of magnitude” capital cost estimate was prepared for the full scale (300 kt/y product) plant and both capital cost estimates are summarised in Table 2.

Table 2 Summary of Project Capital Costs for the Metakaolin Demonstration and Full Scale Plants

Direct Costs (A$M) Demonstration Plant

Full Scale Plant

Plant production rate (kt/y) 10 300 Surprise site infrastructure 0.55 5.3 Wet plant 2.06 20 Kaolin drying 0.78 7.5 FLS calciner scope 13.6 131 Product storage and packaging 1.20 12 Townsville infrastructure 1.00 10 Total directs 19.2 185 Indirects @15% 2.87 28 Contingency @ 20% 3.84 37 Owner's costs 3.06 10 Total 29.0 260

In addition to the capital costs in Table 2, $2M is allowed for additional equipment to produce 3,230 t/y of bright kaolin in the demonstration plant and $19.4M is allowed for 97 kt/y bright kaolin production in the full scale plant.

Project operating costs are comprised of:

• Mining related costs at the Surprise site

Page 20 of 149

• Transport of kaolin material to Townsville • Processing costs at Townsville • General G&A costs.

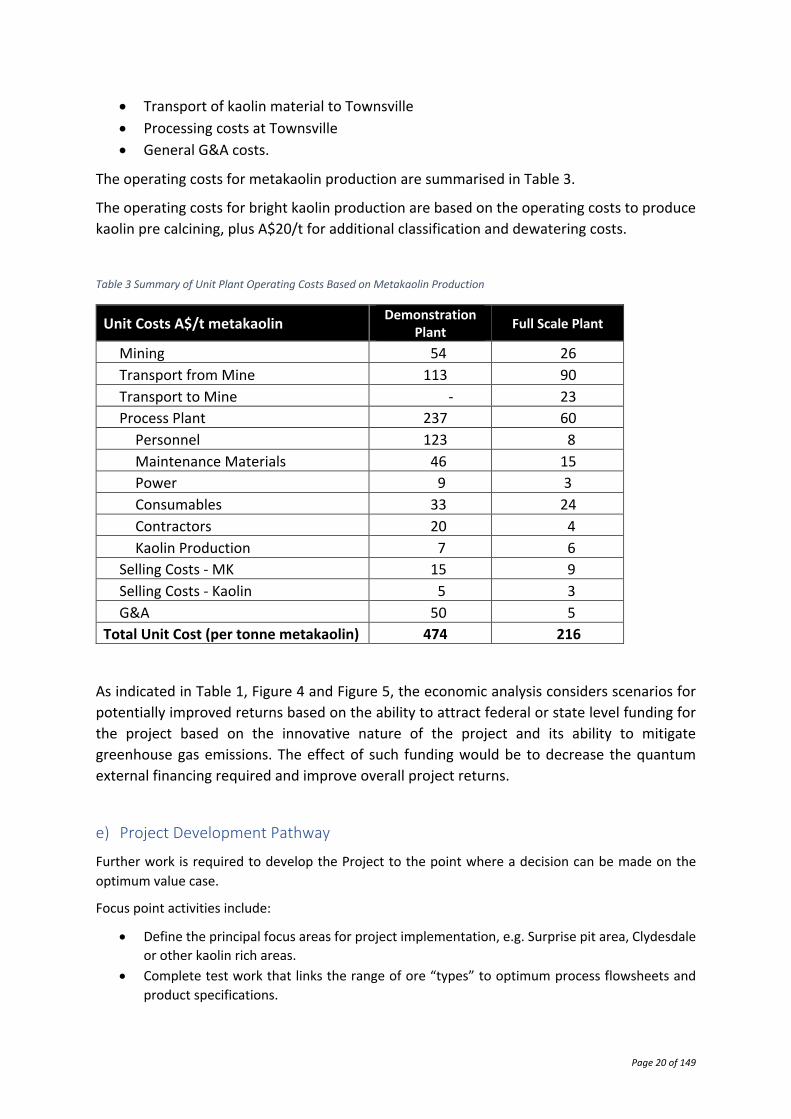

The operating costs for metakaolin production are summarised in Table 3.

The operating costs for bright kaolin production are based on the operating costs to produce kaolin pre calcining, plus A$20/t for additional classification and dewatering costs.

Table 3 Summary of Unit Plant Operating Costs Based on Metakaolin Production

Unit Costs A$/t metakaolin Demonstration Plant Full Scale Plant

Mining 54 26 Transport from Mine 113 90 Transport to Mine - 23 Process Plant 237 60

Personnel 123 8 Maintenance Materials 46 15 Power 9 3 Consumables 33 24 Contractors 20 4 Kaolin Production 7 6

Selling Costs - MK 15 9 Selling Costs - Kaolin 5 3 G&A 50 5

Total Unit Cost (per tonne metakaolin) 474 216

As indicated in Table 1, Figure 4 and Figure 5, the economic analysis considers scenarios for potentially improved returns based on the ability to attract federal or state level funding for the project based on the innovative nature of the project and its ability to mitigate greenhouse gas emissions. The effect of such funding would be to decrease the quantum external financing required and improve overall project returns.

e) Project Development Pathway

Further work is required to develop the Project to the point where a decision can be made on the optimum value case.

Focus point activities include:

• Define the principal focus areas for project implementation, e.g. Surprise pit area, Clydesdale or other kaolin rich areas.

• Complete test work that links the range of ore “types” to optimum process flowsheets and product specifications.

Page 21 of 149

• Relate the mineralogy within and across the kaolin rich areas with product value and a viable mine plan. Future resource and project modelling will endeavour to derive a JORC mineral resource and then mineral reserve.

• Define location options for the Townsville process plant. • Complete baseline environmental studies. • Conduct discussions with landowners and other stakeholders in the mine area. • Conduct marketing studies to determine the range of potential product values and market

options.

The Demonstration Plant project has the following major milestones, providing funding is available:

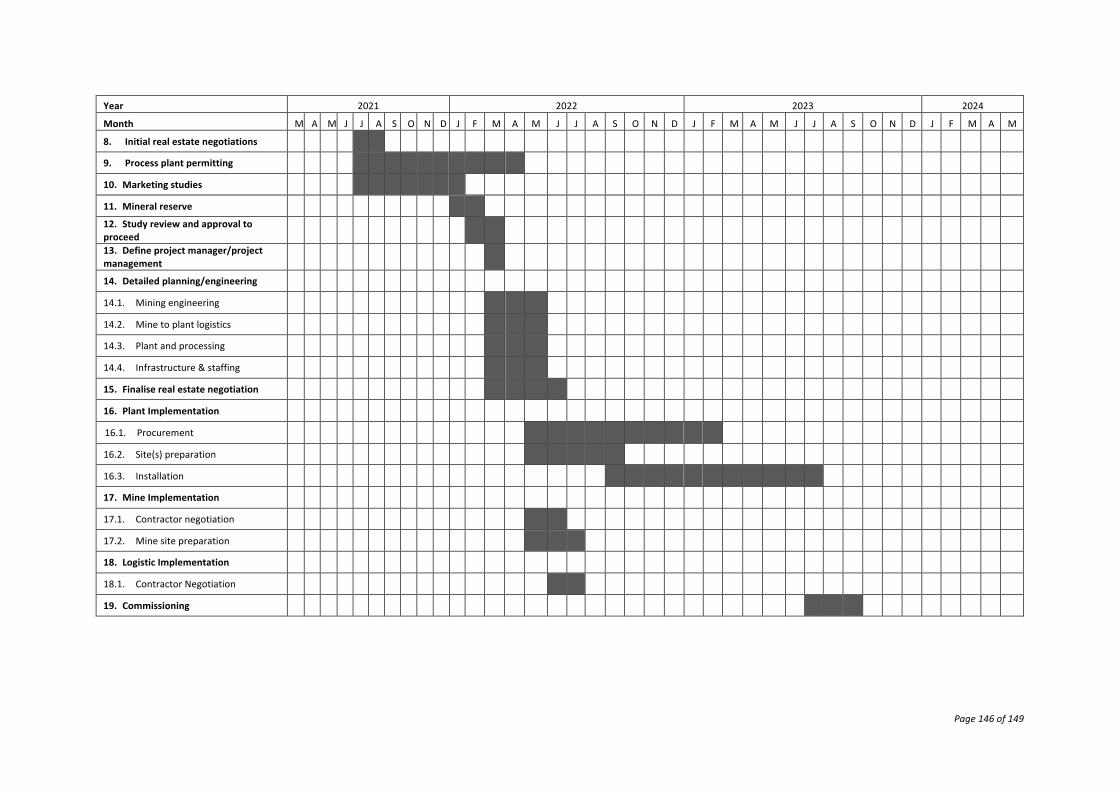

• Concept Study acceptance and approval to proceed, set for July 2021 • Mineral resource declared August 2021 • Mineral reserve declared February 2022 • Definition Phase completion, set for February 2022 • Partial notice to proceed and commencement of detailed planning in March 2022 • Full notice to proceed and commencement of project implementation phase in May 2022 • Commissioning in July 2023.

Study expenditure for the execution of the Demonstration Plant project phase includes:

• Environmental, social and government • Geology and mineral resources • Mining and mineral reserve • Metallurgical test work • Engineering studies • Property purchases • Logistics studies • Marketing studies • Project definition and EPCM • Project commissioning

The cost for this work is included in the capital estimate.

f) Environmental and Permitting Considerations

Preliminary assessments of the project environmental, social and government (ESG) interfaces has been reported herein to frame the potential project.

Discussions with landholders and stakeholders are either yet to commence or are in the very early stages.

A key focus of the next stage of project development will be ensuring that the project is on a firm ESG footing.

Small scale mining for gold recovery has been undertaken recently by IGM at the Surprise mine site and the locality has a long history of exploration and small scale mining. Townsville has a long history of mining-related industry and generally supports sound, environmentally conscious minerals processing project development.

Page 22 of 149

g) Risks and Opportunities

At a Concept Study level there are many risks and opportunities that present during project assessment. The Surprise Project appears to be potentially viable, albeit with a modest IRR (in mining project terms).

Significant work is required on all aspects of the project from exploration to marketing to finalise the optimum business case. A key focus will be determining whether locations like Clydesdale can produce high grade bright kaolin for ceramics, or similar higher value and lower input cost uses.

Work is still in progress to confirm the net value of metakaolin that may be produced by the project for the cement/concrete industry.

2. Introduction a) InterGroup Mining

InterGroup Mining Limited (IGM), an Australian company, together with its wholly owned subsidiary Jodo Gold Pty Ltd (Jodo), has a major kaolin and gold exploration project located in North Queensland, Australia, immediately north of the gold bearing district of Pentland. For this report the Surprise Project comprises the kaolin component of the development project and the Brumby Project refers to the gold component. Jointly, the project area is known as Brilliant Brumby.

b) The Surprise Project

The kaolin prospects cover more than 100 km² of highly prospective ground in an underexplored gold district of the Charters Towers Gold Province where more than 20 million ounces (Moz) of gold has previously been mined. Detailed exploration and drilling continue to highlight the growing potential of the Surprise Project. IGM began its initial gold mining activity at ML 100008 in 2018 and good progress has been made since then including bulk sampling and trial processing.

IGMs interest in kaolin dates back to 2017 when the first kaolin assays were taken from the Surprise prospect on ML 100008. More recent interest in the kaolin potential has resulted from a review of the detailed drilling logs of 36 of the RC holes from the 2018 drilling programme in the Surprise pit area. Analysis of the results demonstrated that 30% of the holes were logged as having grey or white cuttings. An additional 16% of the holes which were drilled in or near the gold bearing quartz lodes showed pale cuttings with sericite alteration caused by hydrothermal activity typically associated with gold deposition.

In early 2020, internal “back of the envelope” guesstimates were made of potential resources based on regional Geological Survey mapping. This suggested the possibility of approximately 90 Mt of kaolin containing material across available area, with a range from 41 Mt to 165 Mt.

Testing has been conducted on selected kaolin samples to ascertain purity and brightness in order to determine whether a potential saleable product can be mined. This material was

Page 23 of 149

excavated along with the gold-bearing quartz veins. Preliminary tests on Surprise kaolin indicated that it could be processed for the manufacture of:

• lower to medium quality industrial usage kaolin • metakaolin • as feed stock for the manufacture of high purity alumina (HPA).

Figure 6 shows the Brilliant Brumby tenement locations, prospects and trends of potential mineralisation. and illustrates the kaolin material at the Surprise pit area.

Figure 6 Brilliant Brumby Tenement Map Showing Prospects and Areas of Prospective Mineralisation

Further work is currently underway investigating the potential to produce bright kaolin products from the Clydesdale prospect west of the Surprise pit.

c) Project Outline

IGM is evaluating the processing of material from the Surprise project area to produce a kaolin product suitable as feedstock for subsequent calcining into metakaolin. The kaolin rich material will be transported to Townsville and calcined to produce metakaolin for sale.

There is potential to produce a coarse product at the project site for shipment to Townsville where separation of the coarser quartz from the fine kaolin may result in a marketable co-

Page 24 of 149

product (quartz) as well as a kaolin-based products. Processing is likely to include attritioning, screening, hydrocyclone classification, thickening of the fine cyclone overflow and filtration or centrifuging to produce a moist kaolin rich material.

It is expected that some kaolin product (approximately 20% of kaolin based production) will also be produced that achieves the bright kaolin product specifications of grade, fineness and brightness. This processing stream will require additional classification and separate drying and bagging systems.

Residual kaolin rich material will be dried, calcined and bagged as metakaolin product.

d) Kaolin Market

There is a 29 Mt/y international market for kaolin which has a range of industrial applications led by paper, ceramics and other speciality uses. Demand is dominated by the paper industry which accounts for more than 40% of market share in terms of volume where kaolin acts as both as a filler to reduce costs as well as improving printing characteristics which is important in the manufacturing of high-quality paper for promotional material. Lightweight coated papers can contain up to 35-40% kaolin. The second biggest market is for use in the manufacture of whiteware ceramics where kaolin makes ceramics whiter in anything from vitreous-china sanitaryware to tableware and wall tiles. Specialty applications include the use of kaolin as a filler in paint as well as being used in rubber, plastics, adhesives, sealants, pharmaceuticals, animal feed, white cement and glass fibre.

The minerals associated with a kaolin product determine its suitability for a particular use. However, there is a growing use by a myriad of new-age industries. Kaolin is now being heralded as “white gold” as it can be transformed into high purity alumina (HPA) which is a key ingredient of the modern world. HPA is a highly versatile material with many uses including LEDs, coating cathode and anode electrode separator sheets in the lithium-ion battery for electric vehicles and energy storage. HPA produced from kaolin may be more cost effective as it is less energy intensive than the traditional processing route which uses bauxite (via aluminium metal) as the feedstock material.

India and US based market researcher Grand View Research2 believes that the global kaolin market was worth US$4.36 billion in 2019 and expects it to grow at a compound annual growth rate (CAGR) of 3.3% from 2020 – 27. The key driving factor is expected to continue to be the increasing demand for ceramics in the construction industry as kaolin is the major raw material used in manufacturing ceramic tiles. Grand View has also pointed out that increasing construction activities in developing economies (China, Brazil and India), resulting from rapid urbanization and industrialisation, is projected to drive the demand for new housing units resulting in a positive influence on ceramic tile demand.

e) Metakaolin Market and Use

IGM’s current major target market is metakaolin for the cement industry. Metakaolin is one of the most effective pozzolanic materials for use in concrete. It is manufactured by heating kaolin, to a temperature between 600 and 800oC. Its quality can be controlled during

2 https://www.grandviewresearch.com/industry-analysis/kaolin-market, accessed 12 April 2021

Page 25 of 149

manufacture, resulting in a much less variable material than industrial pozzolans that are by-products. First used in the 1960s for the construction of a number of large dams in Brazil, metakaolin was successfully incorporated into the concrete with the original intention of suppressing any damage due to alkali-silica reaction1.

When used to replace cement at levels of 5 to 10% by weight, the concrete produced is generally more cohesive and less likely to bleed. As a result, pumping and finishing processes require less effort. The compressive strength of hardened concrete is also increased at this level of replacement.

Slightly higher replacement levels (up to 20%) produce a cement matrix that has low porosity and permeability. This results in improvements to resistance of the hardened concrete to attack by sulfates, chloride ions and other aggressive substances, such as mineral and organic acids. Freeze/ thaw resistance is improved and the risk of damage resulting from the effects of impact or abrasion is reduced for metakaolin concrete that has been finished and cured properly1.

f) Report Objective

The objective of this Concept Study is to present the status of the Surprise Project for internal IGM use. The report structure is similar to that of Technical Reports for the TSX. This structure was used for convenience and clarity.

g) Use of This Report

Use of this report for purposes other than those associated with internal IGM project development are at the reader’s risk. The authors accept no liability for any loss or damage arising as a result of any person or entity, other than IGM, acting in reliance on any information, opinion or advice contained in this document.

3. Reliance on Experts This report was co-ordinated and compiled by Lane Project Services (LPS) based on input from the following experts:

• R J Morrison. Jim Morrison is a geologist with MSc, DIC, FRMIT qualifications and is a Fellow and Chartered Professional (Geology) of the Australasian Institute of Mining and Metallurgy (“AusIMM”), a Member of the Australian Institute of Geoscientists (“AIG”) and of the Advisory Board of the Economic Geology Research Centre (EGRU) of James Cook University, Townsville. He has over 50 years of experience in the Australian mining and exploration industry with various mining companies and for the Geological Survey of WA. For the past 30 years he has worked in northern Queensland holding a number of senior geological positions including significant periods at the Charters Towers, Mount Leyshon and Pajingo gold operations. Since 2014, employed by MTM as a Senior Geologist, he has mapped or inspected most of the main prospects on the Brilliant Brumby Project, and was involved with the planning and supervision of the drilling programs.

Page 26 of 149

• B P Ward. Bridgette Ward has a BSc qualification in Geology and is a Member of the Australian Institute of Geoscientists. Her 13 years of mineral exploration experience in Queensland, includes the assessment of gold, base metal, phosphate and other mineral deposits in northern Queensland. She is Geology Manager for MTM having extensive experience in project management, GIS software and tenement administration as well as a high level of expertise in data compilation, management and database administration. She has inspected many of the prospects and supervised the mining operations on the lease as well as the ground penetrating radar surveys during 2018.

• G S Lane. Greg Lane (BAppSc, MSc, RPEQ, FAusIMM) has over 35 years of experience in minerals processing and has managed, reported and reviewed numerous feasibility studies in Australia, South East Asia, Africa, North America, South America and Europe. He has worked as a subject matter expert for engineering and operating companies across a wide range of commodities, including gold, lithium, copper, iron ore, base metals and industrial minerals.

• M Green. Dr Michael Green is an independent analyst who specialising in growth companies and resources companies. He gained a BSc Honours degree in Mining Engineering from Nottingham University, UK and PhD for a thesis that looked at the economic analysis of mining projects. Having been involved in consultancy work, Michael began working in London in the 1980s as a Mining Analyst with stockbrokers Buckmaster & Moore and then HSBC-owned Greenwell Montagu Securities. Subsequently, he was involved in analysing a wide range of growth companies and became Head of Research at stockbroker Everett Financial which specialised in the small cap market. Since 2006 Michael has been an independent analyst. He has specialised in analysing companies in the resources sector providing research for mining companies, stockbrokers, corporate finance houses, advisers and independent research firms. Between 2008 – 2011, he was a Non-Executive Director of Ascot Mining PLC, a quoted Central American gold mining company. In addition, he has worked closely with resources companies assisting in IR.

• T Pavlopoulos. Terry Pavlopoulos is the managing partner of Cement Business Advisory, a consulting boutique in the global cement sector, and a senior advisor at CemBR, an intelligence and data provider in the global cement sector. Terry has been an independent consultant in the global cement sector since 2008. During this time, he has advised senior managers in several cement producers in Europe, MENA, India, Africa, and Latin America along with some very well-established financial institutions. Previously, he had a successful career with a global cement company (Blue Circle Industries plc) where he was initially a member of the Group Strategy team and subsequently a senior manager of a vertically integrated cement subsidiary. Before embarking on his independent career, Terry spent eight years at Credit Suisse Asset Management as a Buy Side analyst/fund manager, investing in the global cement and building materials sector. Terry’s client list includes the EBRD (European Bank for Reconstruction and Development), and a global development finance institution, where he has an external advisor role, contributing to all of the Bank’s cement related projects.

Page 27 of 149

• L P Evans. Lawrie Evans is a chemical engineer with almost 50 years of experience in the cement industry. He is currently an independent consultant focusing on business improvement by operational, strategic and commercial optimisation mainly, but not exclusively, in the cement industry. He is also engaged in several research projects for novel methods of producing cement with a lower CO2 footprint. He gained a BSc Honours degree in Chemical Engineering from Leeds University. Lawrie joined Blue Circle Industries (BCI), then one of the leading global cement producers, direct from University and progressed through the Technical Centre support group to become Chief Chemical Engineer of BCI in 1991. One responsibility of this position was to manage the technical due diligences for BCI cement acquisitions and following its acquisition by BCI in 1999 Lawrie moved to Heracles Cement in Greece as Operations Director. Following BCIs acquisition by Lafarge in 2002, Lawrie moved to Italcementi, initially as General Manager of a cement plant in Puerto Rico. In 2007, he moved to Italy as Performance Director of Italcementi and remained in this position until retirement in 2014.

• M Barden. Mike Barden is an engineer with over 40 years of experience in the mining industry. After an initial career designing, manufacturing and servicing mining equipment he has then spent the balance of his career in advisory roles. These advisory roles have spanned the full range of activities across the mining value chain from operational to strategic perspectives. Over this period he has been a partner at the Monitor Company, a Director at KPMG and CEO of the CRU group of companies. Mike has consulted to companies across the size horizon and worked in each of the major mining geographies with experience in precious and base metals, bulk commodities and industrial minerals. He currently leads Commodity and Mining Insight, an advisory firm focused on the integration of practical engineering in the mining sector, and the economics and the enabling funding.

• R Garling. Ross Garling has over 50 years of experience in the mining industry. He has a B.E.(Mining)(UNSW), M.B.A.(Macg.), 1st Cl. Cert. as a Mine Mgr.(Qld), and is a Fellow of The Australasian Institute of Mining and Metallurgy. He has held senior positions in a number of mining companies in Australasia and has worked in a diverse range of commodities including zinc (Century Zinc), tin, coal, gold, silver, iron ore, nickel, fly ash, beach sands, etc. Over the last 30 years he has done extensive works in the planning, evaluation, re-mining, re-processing and rehabilitation of mine tailings and mine waste as a consultant and contractor.

4. Property Description and Location The Brilliant Brumby Project is situated in north east Queensland at approximately 20°15’ 30” S latitude and 145°23’ E longitude, 250 km by road south west of Townsville. Charters Towers lies 95 km to the east northeast, and the Thalanga base metal mine is located 40 km to the ESE.

Page 28 of 149

IGM holds the Brilliant Brumby Project as five granted Exploration Permits for Minerals (EPMs), and one Mining Lease (ML) all of which were granted under standard conditions. EPMs 25299, 25431 and 27705 and Mining Lease Application (MLa) 100282 are held in the name of IGM while ML 100008 and EPMs 18419 & 26366 are held in the name of its subsidiary Jodo Gold Pty Ltd.

No royalties, back-in-rights, payments or breaches of conditions on the tenements are known. Resource Authority Public Reports showed mortgages in an interest to Intergroup Nominees Pty Ltd on EPMs 25299, and 25431. No Joint Ventures or other assignments are known.

The total area of the tenures is 178.2 sq.km including the 179.6 ha of ML 100008.

The kaolin assets of the Project that form the Surprise Project are located on ML 100008, EPMs 18419, 25299, and 27705.

Figure 7 Location of the Brilliant Brumby Prospect, including the Surprise Project

5. Accessibility, Climate, Local Resources, Infrastructure and Physiography

a) Accessibility

Access from Townsville is along the Flinders Highway via Charters Towers then northerly via the Mount Stewart unsealed road and the rugged EBBAR company access to ML 100008. The lease areas are approximately 20 km from the highway. A helipad is located near the Surprise camp on ML100008. A railway line lies alongside the Flinders Highway and connects to Townsville.

Page 29 of 149

There are no sealed public or private roads within the Project area. However, a network of station tracks link many of the old mines and prospects. Most roads and tracks are 4-wheel drive only due to the steep slopes accessing the top of the Lolworth Range, and to the numerous ephemeral creek crossings. Roads and tracks sometimes become impassable after heavy rain events. Some of the more remote prospects are only accessible on foot or all-terrain vehicle.

b) Climate

The project has a hot semi-arid climate. In nearby Charters Towers, there is little rainfall throughout the year. The Köppen-Geiger climate classification is BSh. The average annual temperature is 23.1 °C in Charters Towers with about 585 mm of rain annually.

Average maximum temperatures are 35 °C in summer and 25 °C in winter. Corresponding average minimum temperatures are 22 °C to 11 °C.

Rainfall is predominantly in summer with an average of 145 mm in January and 15 to 20 mm in June through September.

c) Land Use

The current land use on the Project is cattle grazing. The landholders are mostly familiar with mineral exploration activities and of the presence of mining leases and small-scale operations on their holdings.

d) Local Infrastructure

The Surprise pit site is remote and has limited access by tracks, no power supply and limited availability of water.

The initial project plans to provide a dirt access road. Power supply will initially be by diesel generator for the mining and on-site processing activities required for demonstration plant operation. The larger production plant will likely be supplied by a combination of diesel, solar and battery power and road access across the properties will be upgraded.

A local water supply will be developed to supply raw water and potable water for mine use.

The potential locations of the kaolin/metakaolin process plant, potentially a fluid bed or flash calciner and dry classification circuit, are in the Townsville surrounds and will be accessed by sealed roads, have grid power and scheme water.

6. History a) History of Cement Development

The first cementitious materials used were lime mortars, some of which have been dated back to 6500 BC. Limestone was burned to manufacture the lime and when mixed with water and sand a lime mortar was produced which could be used for jointing etc. However, the strength of this mortar was low and very slow to develop as it required the absorption of carbon dioxide back into the mortar. The Romans made the next advance in cements with the addition of a pozzolanic volcanic ash to the lime mortar. The active silica in the pozzolan

Page 30 of 149

combined with the hydrated lime to form calcium silicate hydrate which crystallised and interlocked to form a rigid structure. The longevity and strength of this mortar can be seen in the 2000-year-old Pantheon building in Rome. The roof used pumice as a lightweight aggregate to reduce the mass of the structure.

The formation of natural pozzolans is associated with geothermal activity. It was not until the 1820s when Joseph Aspdin heated a poor-quality marl in an attempt to make lime and accidentally made the first Portland cement. This occurred when the lime and silica combined at high temperature to produce calcium silicates and when water and sand was added it replicated the Roman reaction to form calcium silicate hydrate crystals, producing a rigid structure. The reaction was rapid and the addition of gypsum was subsequently used to control the hydration rate / setting time.

b) Modern Cement Chemistry

For modern pure Portland cement, in its most basic form, the raw materials comprise a mix of a limestone / chalk component for calcium carbonate and a clay or shale for silica, alumina, and iron. In the kiln process the calcium carbonate is decarbonated at temperatures of 700 to 900oC before it combines with the silica, alumina, and iron oxides in the rotary kiln at temperatures of 1400 to 1500oC.

The main four components of Portland cement clinker are, in cement industry shorthand, C3S, C2S, C3A and C4AF. In full form these are tricalcium silicate, dicalcium silicate, tricalcium aluminate and tetracalcium aluminoferrite. Most of the final strength in concrete is due to hydration of the C3S and C2S components with a lesser contribution from C3A and a negligible contribution from C4AF.

The main reason for including the iron oxide in the mix is that it forms most of the high temperature liquid phase in the kiln and facilitates the combination of the calcium and silica compounds.

Pure Portland cement containing only ground clinker, with some 5% gypsum to control setting time, remained the dominant cementitious material used globally until the middle of the 20th century, when the role of additions to cement began to be developed. Due to the conservatism of the construction industry, recognition and acceptance of technological change is slow and changes in the enabling Cement Standards to allow, for example cement additions, are commensurately slow. As an example, Australian Standards as recently as 1982 had no standard permitting pozzolan addition (either natural or artificial) or more than a few percentage points of limestone.

c) Cement Additions

The main additions to cement which have become accepted globally, and their impact on cement characteristics, are as follows.

• Limestone is generally used as an inert filler, although studies have shown that up to approximately 5% addition there is a slightly beneficial impact on strengths due to

Page 31 of 149

activation of the C3A component. Above this level strengths are simply diluted at all stages by limestone addition. The acceptance of limestone cements varies around the world, but even as recently as 25 years ago a few major countries (Australia included) had no limestone cement standard other than for masonry cement types. Limestone cements are almost only offered direct from integrated cement or grinding plants.