Kal_G_2010 ATM Software Trends_To Launch

39

Developed and published by: A guide from ATMmarketplace.com INSIDE: Our annual look at the current trends and uture expectations o A TM sotware. Sponsored by: 2010 ATM Software Trends and Analysis

-

Upload

sibtain-jiwani -

Category

Documents

-

view

227 -

download

0

Transcript of Kal_G_2010 ATM Software Trends_To Launch

8/8/2019 Kal_G_2010 ATM Software Trends_To Launch

http://slidepdf.com/reader/full/kalg2010-atm-software-trendsto-launch 1/38

Developed and published by:

A guide from ATMmarketplace.com

INSIDE: Our annual look at the current trends and utureexpectations o ATM sotware.

Sponsored by:

2010 ATM SoftwareTrends and Analysis

8/8/2019 Kal_G_2010 ATM Software Trends_To Launch

http://slidepdf.com/reader/full/kalg2010-atm-software-trendsto-launch 2/38

© 2010 NetWorld Alliance LLC | Sponsored by KAL 2

Contents

Page 3 About the sponsors

Page 4 Introduction | FIs seek multivendor sotware or cost eciency and channel integrationCost control and eciency

Page 7 Chapter 1 | AM survey analysis: A general overview

Page 14 Chapter 2 | A regional ocus: Te Americas

Cost control and new unctionality present competing priorities in mature markets

Page 22 Chapter 3 | A regional ocus: Europe, the Middle East and AricaFast-growing EMEA markets present challenges or FIs

Page 30 Chapter 4 | A regional ocus: Asia-PacifcAsia-Pacifc leads in innovation

Page 38 Conclusion | ake back control o the AM

8/8/2019 Kal_G_2010 ATM Software Trends_To Launch

http://slidepdf.com/reader/full/kalg2010-atm-software-trendsto-launch 3/38

© 2010 NetWorld Alliance LLC | Sponsored by KAL 3

About the sponsors

Published by NetWorld Alliance LLC© 2010 NetWorld AllianceWritten by Gary Wollenhaupt, contributor, ATMmarketplace.com.

Dick Good, CEOom Harper, presidentAndrew Davis, executive vice presidentJoseph Grove, executive editor

KAL, the world’s premier independent AM sotware company, bringstogether ultra-high quality and reliable sotware, unparalleled exper-tise and experience combined with quality o support that is second tonone. And the result? AM, kiosk and bank branch sotware solutionsthat reduce operating costs and set the standard or next-generationretail banking operation. Unparalleled unctionality, fexibility, mis-

sion-critical robustness and the highest levels o security make KAL’sadvanced, multivendor AM sotware systems unrivaled, worldwide.

AM Marketplace, owned and operated by Louisville, Ky.-based NetWorld Alliance, is the world’s largest online provider o inormationabout and or the AM industry. Te content, which is updated everybusiness day and read by business and industry proessionals through-out the world, is ree.

8/8/2019 Kal_G_2010 ATM Software Trends_To Launch

http://slidepdf.com/reader/full/kalg2010-atm-software-trendsto-launch 4/38

© 2010 NetWorld Alliance LLC | Sponsored by KAL 4

IntroductionFIs seek multivendor sotware or cost eciency and channel integration

S ince ATMmarketplace.com beganpublishing “ATM Sotware Trendsand Analysis” in 2007, the view o

multivendor sotware within the industry has changed. Aided in large part by themigration o ATM sotware platorms toMicrosot Windows, awareness and accep-tance o platorm-independent ATM sot-ware has grown, as indicated in the survey results shown in this guide.

Another indication is the Retail Banking

Research Ltd. “Multivendor Sotware 2010”study that ound approximately 450,000ATMs globally run multivendor sotware,a nearly 60 percent increase over the pasttwo years. According to the report, NCR isthe world’s largest supplier o ATM middle-ware and applications.

A news release issued by NCR Corp. aboutthe RBR indings states that the majority o inancial institutions in North Americarely on NCR’s APTRA ATM sotware

suite, when compared with similar sot-ware suites provided by NCR competitorsDiebold Inc. and Wincor Nixdor AG.NCR says RBR also ound that NCR holdsthe majority o the ATM market share inWestern Europe and Latin America.

The RBR study ound that KAL is one o the top three vendors in the multivendorATM sotware market, with 21 percento the ATM multivendor sotware share.

Outside o the top three companies, theother companies listed in the research eachaccount or 7 percent or less o the total

market. KAL says it is the only company among leading ATM sotware competi-tors to ocus solely on ATM sotware.

Regionally, the report ound that WesternEurope, Asia-Paciic and North Americaaccounted or 80 percent o the multivendorsotware installations, with Western Europehaving the largest number o ATMs by region. Additionally, the number o ATMsrunning multivendor sotware in LatinAmerica has doubled in the past two years.

It’s clear that inancial institutions under-stand the value o a hardware-independentATM sotware application, regardless o whether it’s provided by an ATM manuac-turer or an independent sotware vendorsuch as KAL. Now, FIs are looking ormore than technological eiciency romtheir ATM sotware and they want toleverage their ATM networks or a muchgreater competitive advantage.

“We’re seeing a more mature view o it,”said Joe Gallagher, general manager o inan-cial sotware solutions or NCR Corp. “It’smoved beyond the question o whether your application runs on other hardware.”

The spread o Windows has aided thewidespread use o XFS, a global sotwarestandard that enables multivendor sot-ware. Aravinda Korala, chie executive o-icer o KAL, compared XFS to the TCP/IP

protocol that makes the Internet possible.Most current ATMs are XFS compatible.Even FIs that don’t use multivendor sot-

By Gary Wollenhaupt

Contributing writer,

ATMmarketplace.com

Financial institutions understand the value o a hardware-independent ATMsotware application, regardless o whether it’s provided by an ATM

manuacturer or an independent sotware vendor.

8/8/2019 Kal_G_2010 ATM Software Trends_To Launch

http://slidepdf.com/reader/full/kalg2010-atm-software-trendsto-launch 5/38

© 2010 NetWorld Alliance LLC | Sponsored by KAL 5

INRODUCION FIs seek multivendor sotware or cost eciency and channel integration

FIs consider multivendor solutions or avariety o reasons, but the most common

is to reduce cost and improve eciency

or the ATM network.

ware speciy that capability in the ATMsthey purchase.

“Even i the FI is not going to use multiven-dor sotware immediately, they want theirATMs to be XFS compliant or the uture,”Korala said.

Certainly, the repercussions o the inan-cial crisis that swept the industry in 2009still inluence spending and marketingdecisions by FIs. In the United States, as

well as other countries, instability andeven ailures among FIs has led to new corporate entities that have resulted rommerged operations.

“However, the inancial crisis doesn’t seemto have slowed things down or stoppedpeople rom doing the things they want todo with ATM sotware,” Korala said. “Costreduction or the ATM network is evenmore important than it ever was.”

These abrupt changes in the industry may also negatively impact customer relation-ships, making the ATM a vital servicedelivery channel or FIs.

“The extent to which an FI can improvethe customer experience at the ATM, aswell as other delivery channels, helps buildbetter relationships,” said Robert Usner,senior director o global markets strategy and planning or Diebold. “That’s impor-

tant or most FIs because deposits areincreasingly important.”

Cost control and eciency

FIs consider multivendor solutions or a variety o reasons, but the most commonis to reduce cost and improve eiciency or the ATM network. That’s especially

true i an FI operates ATMs rom multiplemanuacturers.

I each type o machine operates proprie-tary sotware, then sotware updates,security upgrades and new eatures mustbe managed or each variant o the sot-ware. On the other hand, XFS-capablemachines running multivendor sotwareacross all hardware types can be managedwith a single sotware application.

“In the past, you had dierent sotware ordierent ATM types, and that was just un-tenable or a big bank,” Korala said. “Thereare so many things FIs need to do; they

want to be able to do it all just once.”

Managing a complex, perhaps international,ATM network presents myriad challengesor an FI. From a simple inormation tech-nology perspective, the task is dauntingand expensive.

“Just by virtue o dierent geographies,invariably there will be dierent hardware vendors, but with a multivendor ATM ap-plication they can reduce operational costs

and keep consistent consumer experience,”said Gallagher.

Any way to reduce that complexity has aguaranteed return on investment.

“Having a single application or ATMsreduces eort internally within a bank roma development, testing and certiication

8/8/2019 Kal_G_2010 ATM Software Trends_To Launch

http://slidepdf.com/reader/full/kalg2010-atm-software-trendsto-launch 6/38

© 2010 NetWorld Alliance LLC | Sponsored by KAL 6

process,” said Alan Walsh, executive vicepresident o banking or Wincor Nixdor.“It also makes FIs more independent,which means they can buy any vendor’shardware rom a cost-control perspective.”

In just a ew years, the multivendor con-cept has transormed rom a technology solution to one that supports an FI’s overallstrategic approach. FIs look or sotwarethat supports new unctions at the ATMand integrates with other channels such as

online and mobile banking.

A multivendor approach makes it easier tointegrate customer-acing enhancementsthroughout a network.

“I an FI wants to do one-to-one marketing,it becomes easier to embed that in a singlesotware application across dierent hard-ware vendors,” Gallagher said. “They cantie it into the branch system or online pres-ence as well.”

For FIs aced with rising costs, increasingly strict regulatory environments and on-going security concerns, multivendorsotware gives them the opportunity totake back control o their ATM networks.Multivendor sotware allows FIs to managethe ATM network with ewer technology resources than using proprietary sotwareor each ATM type.

“An FI can do what makes business senseor them to do and not yield control to vendors unless they choose to,” said SteveHensley, executive vice president o globalsales or KAL. “Banks can take control o their networks and exercise as much con-

trol as they want.”

With greater control provided via multi- vendor sotware, an FI can add transactions,enhance unctions and conduct marketingcampaigns much more eiciently.

“An FI can use the ATM channel as acompetitive edge, as opposed to it beinga commodity,” Hensley said.

For 2010, ATMmarketplace.com has onceagain surveyed key individuals to updatethe “ATM Sotware Trends and Analysis”guide to highlight trends in major globalmarkets. The purpose o the guide is tobuild a comprehensive, global view o ATM sotware and the role it plays in theinancial services industry, assisting FIs indeveloping their own sotware strategies.

INRODUCION FIs seek multivendor sotware or cost eciency and channel integration

A multivendor approach makes it easier tointegrate customer-acing enhancements

throughout a network.

8/8/2019 Kal_G_2010 ATM Software Trends_To Launch

http://slidepdf.com/reader/full/kalg2010-atm-software-trendsto-launch 7/38

© 2010 NetWorld Alliance LLC | Sponsored by KAL 7

I n 2010, ATMmarketplace.com repeatedits survey o global ATM executives tolearn about companies’ current sot-

ware unctionality and uture plans. Theserespondents, representing some o theworld’s top inancial institutions, sharedtheir thoughts and strategies or ATM sot-ware. Given the situation in many o theworld’s inancial markets, the responseshave been tempered by a diicult climateand uncertainty about what might lie ahead.

This year’s survey repeated the questionsrom 2009 regarding inancial institutions’understanding o multivendor ATM sot-ware and motivations or sotware deci-sions, as well as the ATM unctions that

FIs would most like to see in uture sot-ware implementation. See where you stackup in comparison — is your organizationtaking ull advantage o the possibilities o multivendor ATM sotware?

We thank the industry leaders, literally rom around the globe, who shared their

insights via this survey. Here’s an overview o their responses, as well as comparisonswith the 2009 survey, where data is avail-able. Subsequent chapters will delve intothe responses on a regional basis.

Chapter 1 AM survey analysis: A general overview

Total survey respondentsFor 2010: 243 For 2009: 206

2010 2009

ATM manuacturer/vendor 27% 34%

Financial institution — global top 100 by assets 15% 8%

Financial institution — other 24% 18%

ISO/IAD 9% 20%

Processor or EFT network 1% 7%

Other 15% 15%

1. Respondent breakdown by industry

The largest group represented comes romNorth America, which perhaps is ittingdue to the ubiquity o the ATM in theUnited States and Canada. Other largermarkets are well represented and Australiahas a presence, too.

2. Respondent breakdown by region

Australia2%

Latin America8%

Middle East/Africa12%

Asia19%

Europe23%

United Statesand Canada

36%

8/8/2019 Kal_G_2010 ATM Software Trends_To Launch

http://slidepdf.com/reader/full/kalg2010-atm-software-trendsto-launch 8/38

© 2010 NetWorld Alliance LLC | Sponsored by KAL 8

CHAPER 1 AM survey analysis: A general overview

2010 2009

Executive/management 32% 39%

Finance or procurement 1% 2%

IT 23% 18%

Operations 9% 21%

Sales/marketing 24% 18%

Other 11% 13%

3. Respondent breakdown by job responsibility

The survey respondents included a mix o executives rom FIs, independent sales organi-zations and independent ATM deployers, transaction processors, electronic-und-transernetworks, ATM manuacturers and ATM vendors.

2010 2009

100% 36% 33%

50% - 99% 37% 34%

Less than 50% 4% 18%

Don’t know 3% 7%

Not applicable 10% 10%

4. What percentage o your organization’s AMs or your customers’ AMs run onMicrosot Windows today?

The number o respondents running at least hal o their ATMs on Microsot Windowsgrew rom about 67 percent last year to nearly 73 percent or 2010. Although other plat-orms such as Linux and IBM’s legacy OS/2 survive on the ringe, none o them will beable to make much headway against the Microsot product. Those who choose to orsakeWindows ace an uphill battle or hardware and sotware support rom the ATM manuac-turers.

8/8/2019 Kal_G_2010 ATM Software Trends_To Launch

http://slidepdf.com/reader/full/kalg2010-atm-software-trendsto-launch 9/38

© 2010 NetWorld Alliance LLC | Sponsored by KAL 9

CHAPER 1 AM survey analysis: A general overview

2010 2009

Yes, planned and budgeted or this year 17% 19%

Yes, planning or next year or the ollowing year 26% 20%

No, we recently replaced it 11% 9%

No, there are no plans to replace the existing ATM sotware 27% 33%

Not applicable 19% 18%

5. Are there plans to replace your organization’s current AM sotware or yourcustomers’ current AM sotware?

About 3 percent more respondents plan to replace their sotware within the next three years than planned to do so in last year’s survey. In last year’s responses, 20 percentplanned or the next year or the ollowing year, compared with 26 percent with similarplans rom the 2010 survey. That response relects both the desire to take advantage o multivendor sotware and uncertainty on spending due to the economy.

2010 2009

ATMs rom multiple vendors, single sotware application on all 29.1% 24%

ATMs rom multiple vendors, considering multivendor sotwarein the uture

33.6% 30%

ATMs rom a single vendor, understand the benets o multivendorATM sotware

11.7% 10%

ATMs rom a single vendor, see no need or multivendor ATM sotware 8.1% 9%

Not a consideration 14.2% 19%

Not sure what this means 3.2% 8%

6. Which statement best identiies your organization’s multivendor AM strategy, orthe multivendor AM strategy o your customers?

The number o respondents running multivendor sotware on ATMs rom multiple vendors grew rom 24 percent to nearly 30 percent, an indication that more institutionsseek the cost-saving and marketing beneits o multivendor applications. The number o respondents considering multivendor sotware also grew, relecting the desire to holisti-cally operate multivendor networks. These increases are ueled by a growing awarenesso the multivendor concept, as seen in the signiicant drop in the number o respondentswho did not understand the concept.

8/8/2019 Kal_G_2010 ATM Software Trends_To Launch

http://slidepdf.com/reader/full/kalg2010-atm-software-trendsto-launch 10/38

© 2010 NetWorld Alliance LLC | Sponsored by KAL 10

CHAPER 1 AM survey analysis: A general overview

Even institutions with ATMs rom a single vendor increasingly understand that they canuse multivendor sotware to add new unctionality and upgrade security across a networkcomposed o hardware models rom one manuacturer that may vary in age. Addition-ally, having multivendor sotware reduces the cost o purchasing new ATMs and reducesthe cost o maintaining them since the FI is ree to buy rom any provider, thereby puttingsigniicant pricing pressure on the vendors.

2010 2009

Increased security (such as EMV, 3DES, remote key, biometrics) 57% 51%

Increased productivity and efciency 50% N/A

Added unctionality (such as new transactions) 49% 49%

Cost reduction o the ATM network 49% 35%

Providing an enhanced user experience(such as transaction personalization)

44% 45%

Support or new technology 41% 47%

Ease o changing sotware when needed 26% 28%

Need or better customer relationships 26% N/A

Improved ATM reliability 26% 37%

Improved support 22% 28%

None o the above 7% 13%

7. What is the primary driver (or drivers) or changing AM sotware?

Increased security once again tops the list o reasons or FIs to change their ATM sot-ware. Increasing sophistication on the part o criminals and increasing pressure romregulators combine to make security a top priority or any entity involved in inancial

services. FIs are looking or sotware that supports the latest in security enhancements,such as EMV, Triple DES (Data Encryption Standard), remote key loading, biometrics andother eatures. Close behind are support or other new technologies and cost reduction inoperating the ATM network. FIs also value the beneits rom multivendor sotware thatallow them to operate more eiciently and oer more to their customer base.

8/8/2019 Kal_G_2010 ATM Software Trends_To Launch

http://slidepdf.com/reader/full/kalg2010-atm-software-trendsto-launch 11/38

© 2010 NetWorld Alliance LLC | Sponsored by KAL 11

CHAPER 1 AM survey analysis: A general overview

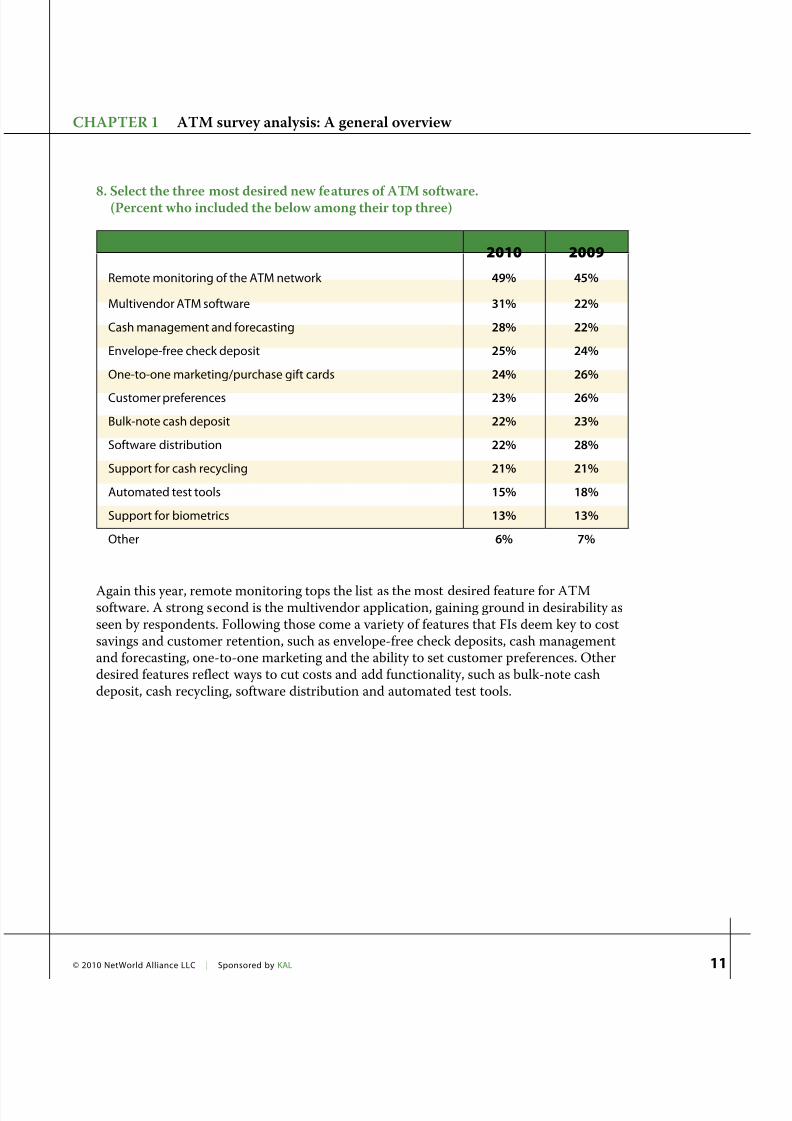

2010 2009

Remote monitoring o the ATM network 49% 45%

Multivendor ATM sotware 31% 22%

Cash management and orecasting 28% 22%

Envelope-ree check deposit 25% 24%

One-to-one marketing/purchase git cards 24% 26%

Customer preerences 23% 26%

Bulk-note cash deposit 22% 23%

Sotware distribution 22% 28%

Support or cash recycling 21% 21%

Automated test tools 15% 18%

Support or biometrics 13% 13%

Other 6% 7%

8. Select the three most desired new eatures o AM sotware.(Percent who included the below among their top three)

Again this year, remote monitoring tops the list as the most desired eature or ATMsotware. A strong second is the multivendor application, gaining ground in desirability asseen by respondents. Following those come a variety o eatures that FIs deem key to costsavings and customer retention, such as envelope-ree check deposits, cash managementand orecasting, one-to-one marketing and the ability to set customer preerences. Otherdesired eatures relect ways to cut costs and add unctionality, such as bulk-note cashdeposit, cash recycling, sotware distribution and automated test tools.

8/8/2019 Kal_G_2010 ATM Software Trends_To Launch

http://slidepdf.com/reader/full/kalg2010-atm-software-trendsto-launch 12/38

© 2010 NetWorld Alliance LLC | Sponsored by KAL 12

CHAPER 1 AM survey analysis: A general overview

2010 2009

Reduce operational costs 31% 38%

Create a better ATM customer experience 18% N/A

Improve the ability to remotely manage the ATM network 16% 19%

Adopt enhanced security technologies 13% 11%

Improve customer unctionality 13% 20%

Improve the User Interace 3% 4%No changes needed 5% 8%

9. What is the most critical change your organization or your customers’ organizationneeds to make to its AM network in 2010?

Although the economic pressures on FIs have not subsided, the ocus has shited some-what to customer-acing enhancements. Retaining existing customer relationships andbuilding deposits become higher priorities. Security remains a priority o many, as doescreating a better ATM customer experience. Even the small number o respondents whothought no changes were needed has lowered. FI executives seemingly understand how vital customer and member relations are when it comes to retention. Customers havemany choices — in many cases the relationship comes down to the experience the cus-tomer has in transacting business.

10. Given customers have increasingly ewer reasons to visit bank branches, how important a delivery channel do you see your AM network as a customer touch-point that allows you to compete eectively with other banks?

In a new question or 2010, theseanswers relect the ongoingimportance o ATMs to an FI’scustomer interactions. For many customers, it may be the most common

interaction with an institution.

The responses to this question varied by region. For the United States and Canada,48 percent thought the ATM was the mostimportant customer touchpoint. In con-trast, 70 percent o the respondents romMiddle East/Arica indicated the ATMwas most important. For Asia, it was 63

percent; Latin America, 53 percent; andEurope, 50 percent.

Not applicable7.3%

Same as before8.1%

Not important at all1.6%

Becoming

less important2.4%

Becomingmore important

25.9%

Very important54.7%

8/8/2019 Kal_G_2010 ATM Software Trends_To Launch

http://slidepdf.com/reader/full/kalg2010-atm-software-trendsto-launch 13/38

© 2010 NetWorld Alliance LLC | Sponsored by KAL 13

CHAPER 1 AM survey analysis: A general overview

11. Rate the ollowing bank service delivery channels in order o importance as acustomer touchpoint.

0 10 20 30 40 50 60 70

33%

7%

2%

16%

43%

Most Important

2nd Most Important

3rd Most Important

4th Most Important

5th Most Important

ATM

0 10 20 30 40 50 60 70

40%

14%

14%

14%

18%

Most Important

2nd Most Important

3rd Most Important

4th Most Important

5th Most Important

Branch

While the largest number o respondents viewed the ATMas the second-most importantcustomer touchpoint, it rankeda close second overall aterthe branch as the most impor-tant. The mobile phone spacewas solidly ranked as the leastimportant. The branch is still

clearly the top touchpoint,despite advances in customer-acing technologies.

0 10 20 30 40 50 60 70

3%

25%

36%

26%

10%

Most Important

2nd Most Important

3rd Most Important

4th Most Important

5th Most Important

Call center

0 10 20 30 40 50 60 70

19%

34%

20%

3%

23%

Most Important

2nd Most Important

3rd Most Important

4th Most Important

5th Most Important

Internet

0 10 20 30 40 50 60 70

4%

11%

24%

55%

7%

Most Important

2nd Most Important

3rd Most Important

4th Most Important

5th Most Important

Mobile phone

8/8/2019 Kal_G_2010 ATM Software Trends_To Launch

http://slidepdf.com/reader/full/kalg2010-atm-software-trendsto-launch 14/38

© 2010 NetWorld Alliance LLC | Sponsored by KAL 14

Chapter 2 A regional ocus: Te Americas

2010 2009

100% 24% 20%

50% - 99% 39% 32%

Less than 50% 22% 31%

Don’t know 5% 6%

Not applicable 10% 11%

12. What percentage o your organization’s AMs or your customers’ AMs run Mi-crosot Windows today?

Microsot Windows continues to be the dominant player in the Americas. It’s especially strong in South America, where ATMs are a more recent market development and wherethere are ewer older machines with other OSs than there are in North America. Those FIsusing other operating systems ace ongoing compatibility problems with the demands o the most current sotware and security saeguards.

Total survey respondents rom the Americas:For 2010: 109 | For 2009: 94

Includes North America, Mexico, Latin America, South America and the Caribbean

2010 2009

Yes, planned and budgeted or this year 16% 15%

Yes, planning or next year or the ollowing year 20% 21%

No, we recently replaced it 6% 11%

No, there are no plans to replace the existing ATM sotware 30% 30%

Not applicable 19% 23%

13. Are there plans to replace your organization’s current AM sotware or your

customers’ current AM sotware?

Almost a third o the respondents don’t plan to replace existing sotware, perhaps a relec-tion o the newer-vintage machines deployed in South America. Those planning to replacesotware this year, next year or the ollowing year are about the same, 36 percent or 2010and 2009. Due to ongoing inancial pressures, FIs still see a strong business case or chang-ing their sotware to improve eiciency.

8/8/2019 Kal_G_2010 ATM Software Trends_To Launch

http://slidepdf.com/reader/full/kalg2010-atm-software-trendsto-launch 15/38

© 2010 NetWorld Alliance LLC | Sponsored by KAL 15

CHAPER 2 A regional ocus: Te Americas

2010 2009

Increased security (such as EMV, 3DES, remote key, biometrics) 51% 39%

Added unctionality (such as new transactions) 44% 46%

Increase in productivity and efciency 44% N/A

Providing an enhanced user experience(such as transaction personalization)

44% 37%

Cost reduction o the ATM network 37% 29%

Support or new technology 37% 47%

Ease o changing sotware when needed 26% 30%

Need or better customer relationships 19% N/A

Improved ATM reliability 18% 31%

Improved support 17% 24%

None o the above 12% 16%

14. What is the primary driver (or drivers) or changing AM sotware?

Increased security and increased eiciency tallied as two o the highest priorities orrespondents. Interestingly, support or new technology ell as a primary driver, as costreductions gain importance or FIs’ survival. However, customer-acing enhancements,such as added unctionality or new transactions, indicate an awareness o the importanceo the ATM in an FI’s marketing strategy.

2010 2009

ATMs rom multiple vendors, single sotware application on all 24% 19%

ATMs rom multiple vendors, considering multivendor sotwarein the uture

32% 34%

ATMs rom a single vendor, understand the benets o multivendorATM sotware

15% 10%

ATMs rom a single vendor, see no need or multivendor ATM sotware 10% 9%

Not a consideration 15% 21%

Not sure what this means 4% 7%

15. Which statement best identiies your organization’s multivendor AM strategy, orthe multivendor AM strategy o your customers?

More than hal the respondents said they operated ATMs rom multiple vendors in their leet,but only about a quarter take advantage o the beneits o multivendor sotware. Awarenesslevels o the beneits o multivendor ATM sotware seem to be rising, as the percentage o respondents who understand the beneits but don’t use it rose rom 10 percent to 15 percent.

8/8/2019 Kal_G_2010 ATM Software Trends_To Launch

http://slidepdf.com/reader/full/kalg2010-atm-software-trendsto-launch 16/38

© 2010 NetWorld Alliance LLC | Sponsored by KAL 16

CHAPER 2 A regional ocus: Te Americas

2010 2009

Remote monitoring o the ATM network 46% 43%

Envelope-ree check deposit 41% 33%

Customer preerences 25% 34%

One-to-one marketing / purchase git cards 25% 24%

Bulk-note cash deposit 24% 2%

Multivendor ATM sotware 24% 22%

Sotware distribution 24% 24%

Cash management and orecasting 21% 21%

Support or cash recycling 21% 12%

Automated test tools 13% 18%

Support or biometrics 7% 7%

Other 6% 7%

16. Select the three most desired new eatures o AM sotware.(Percent who included the below among their top three)

Remote management o ATM sotware again tops the list o most desired new eatures

or the Americas region. That relects the eiciency gains that come with remote man-agement, underscoring the cost-cutting value o robust multivendor sotware. Interest inenvelope-ree check deposit has grown, based on the promise o the Check 21 legislationin the United States that allows or non-envelope-based check deposits. Other areas o the region are less reliant on checks, so that eature may be less o a priority. Several othereatures hold a roughly similar level o attraction, including support or cash recycling,bulk-note cash deposit, one-to-one marketing and sotware distribution.

8/8/2019 Kal_G_2010 ATM Software Trends_To Launch

http://slidepdf.com/reader/full/kalg2010-atm-software-trendsto-launch 17/38

© 2010 NetWorld Alliance LLC | Sponsored by KAL 17

CHAPER 2 A regional ocus: Te Americas

2010 2009

Reduce operational costs 36% 44%

Create a better ATM customer experience 22% N/A

Improve the ability to remotely manage the ATM network 16% 16%

Improve customer unctionality 14% 17%

Adopt enhanced security technologies 10% 6%

Improve the user interace 4% 4%

No changes needed 9% 13%

17. What is the most critical change your organization or your customers’ organizationneeds to make to its AM network in 2010?

The trend toward eiciency continues here, with operational cost reductions a high prior-ity or ATM networks. O course, security continues to be a concern. Better use o theATM as a customer touchpoint is seen as a critical change as well.

For respondents in theAmericas, the ATM isconsidered an increasingly important critical delivery channel as sel-servicebecomes a larger part o

daily lie.

18. Given customers have increasingly ewer reasons to visit bank branches, how im-portant a delivery channel do you see your AM network as a customer touchpointthat allows you to compete eectively with other banks?

Not applicable12% Same as before

4%

Not important at all2%

Becoming less important2%

Becomingmore important

30%

Very important50%

8/8/2019 Kal_G_2010 ATM Software Trends_To Launch

http://slidepdf.com/reader/full/kalg2010-atm-software-trendsto-launch 18/38

© 2010 NetWorld Alliance LLC | Sponsored by KAL 18

CHAPER 2 A regional ocus: Te Americas

19. Rate the ollowing bank service delivery channels in order o importance as acustomer touchpoint.

0 10 20 30 40 50 60 70

29%

7%

1%

21%

42%

Most Important

2nd Most Important

3rd Most Important

4th Most Important

5th Most Important

ATM

0 10 20 30 40 50 60 70

45%

13%

16%

11%

15%

Most Important

2nd Most Important

3rd Most Important

4th Most Important

5th Most Important

Branch

0 10 20 30 40 50 60 70

0%

22%

39%

30%

13%

Most Important

2nd Most Important

3rd Most Important

4th Most Important

5th Most Important

Call center

0 10 20 30 40 50 60 70

25%

38%

17%

0%

21%

Most Important

2nd Most Important

3rd Most Important

4th Most Important

5th Most Important

Internet

0 10 20 30 40 50 60 70

2%

10%

21%

58%

10%

Most Important

2nd Most Important

3rd Most Important

4th Most Important

5th Most Important

Mobile phone

The traditional bank branchstill reigns supreme as themost important service de-livery channel in the Ameri-cas, but the ATM is strongly considered the second-mostimportant means o customerinteraction.

8/8/2019 Kal_G_2010 ATM Software Trends_To Launch

http://slidepdf.com/reader/full/kalg2010-atm-software-trendsto-launch 19/38

© 2010 NetWorld Alliance LLC | Sponsored by KAL 19

CHAPER 2 A regional ocus: Te Americas

Cost control and new unctionality present competing priorities inmature markets

In mature markets, the desire to lower ATMoperating costs competes with the desireor new unctionality. Throughout theregion, FIs seek ATM sotware that allowsthem to pursue both objectives.

For many FIs, lower costs result rom thelexibility that comes with the ability to

separate sotware rom the purchase o ATM hardware and service. FIs can shopor the best price and service or each com-ponent, or sign up with an independent vendor to service some or all aspects o theoperation.

Some FIs are seeking greater control overtheir ATM operations to reduce operatingcosts.

“We do not have ull control over unction-

ality now, but would like to have it in theuture,” said Pam Hasara, vice president andATM relationship and product manager orBankAtlantic (US $6 billion).

The Fort Lauderdale, Fla.-based institutionhas struggled with the cost o managing itsleet o 305 ATMs, which includes 136 oncruise ships.

“We have put a lot o controls into our

current ATM operation and have reducedlocations because o the cost o equipmentand servicing involved,” Hasara said.

Remote monitoring capability is one sot-ware eature that FIs rely on or cost savings.With a multivendor installation, all ATMsin a network can utilize the same eatureset to save money rom more eicient

management. Beore remote management,service calls might be hit or miss. A techni-cian wouldn’t necessarily know why a unitwas out o service, and what parts might beneeded to return it to service.

“With a state-o-the-art ATM remotemonitoring and management system, an FIcan minimize the number o times some-one has to go out and physically touchthe machine,” said KAL’s Hensley. “Whena technician is dispatched, an FI can be

sure they have the right components andmaterials to ix the problem they’re goingto encounter at the ATM.”

Lower costs result rom the exibility that comeswith the ability to separate sotware rom the

purchase o ATM hardware and service.

ATM sotware can even take care o itsel,in many cases eliminating the need or a

service call.

“The ATM sotware can be sel-diagnos-ing, detecting i there are things wrongwith the ATM and sending detailed statusinormation to the monitoring system,”Hensley said. “With the right sotwaretools, FIs can have better control over ix-ing their ATMs so availability goes up andcosts go down.”

Multivendor sotware can enable a host o new eatures, such as customer relation-ship marketing and automated deposits,that FIs value.

Long on the horizon, no-envelope cashand check deposit transactions at theATM may inally be gaining traction as asought-ater eature that’s supported by

8/8/2019 Kal_G_2010 ATM Software Trends_To Launch

http://slidepdf.com/reader/full/kalg2010-atm-software-trendsto-launch 20/38

© 2010 NetWorld Alliance LLC | Sponsored by KAL 20

CHAPER 2 A regional ocus: Te Americas

many multivendor sotware solutions orthe ATM. In the United States, the move toautomated deposits has been driven by theCheck Clearing or the 21st Century Act,or Check 21, a law that’s been on the bookssince 2004. The act allows check truncationand processing o electronic check images.

“Envelope-ree deposits are gaining popu-larity and it won’t be long beore consumersembrace this convenient eature as wellas others such as advanced check cashing

unctionality,” said KAL’s Korala.

However, in regions where checks makeup a smaller portion o the transaction volume, check imaging is less o a priority.“Outside the United States it’s not such abig deal,” Korala said.

BankAtlantic is one FI weighing the busi-ness case or adding this unction.

“We are reviewing no-envelope depositstrategies at this time,” Hasara said. “Thecost o upgrading the ATMs to bulk depositis a major concern.”

The sotware and hardware inrastructuredeposits also could be used or other appli-cations such as bill payments. But in theUnited States, there are some barriers.

“In the United States, there’s no standardor the bills, which makes it diicult or

sel-service channels to recognize the billand pay it,” said Wincor’s Walsh. In Europe,on the other hand, billing statements tendto be standardized, making sel-service amore viable option at this point.

One trend that’s on the horizon is the inte-gration o ATM and mobile channels. Oneconcept is to view the mobile platorm as

another orm o the card through near-ieldcommunication, or short-range radio waves,essentially.

Even beore NFC becomes widespread, FIscan leverage the power o mobile and ATM

channels through cross-promotion enabledby sotware integration. Take mobile bank-ing, widely available on smartphones. Themost common way or consumers in theUnited States to sign up or mobile bankingis via the online channel.

But FIs don’t ully promote the mobilechannel through their online presence.However, about 70 percent o FI customersuse an ATM, creating a perect opportu-nity to sign up costumers or the mobile

channel.

Security continues to be a high priority orFIs. Compliance with the PCI Data Securi-ty Standard as well as developing technolo-gies such as EMV and remote key loadingare important aspects o ATM sotware.Fighting raudsters remains a concern orFIs, rom both the hardware and sotwareaspects. BankAtlantic, like FIs everywhere,aces security challenges.

“Skimming is our biggest issue, but we arealso concerned with sotware hacking,”Hasara said.

Markets outside the United States haveadopted chip-and-pin technology, alsoknown as EMV (Europay, MasterCardand Visa standard). As its neighbors to the

FIs can leverage the power o mobile and ATMchannels through cross-promotion enabled by

sotware integration.

8/8/2019 Kal_G_2010 ATM Software Trends_To Launch

http://slidepdf.com/reader/full/kalg2010-atm-software-trendsto-launch 21/38

© 2010 NetWorld Alliance LLC | Sponsored by KAL 21

CHAPER 2 A regional ocus: Te Americas

north and south o the United States adoptEMV chip, the security gap may be toomuch or American regulators to ignore.Multivendor sotware enables enterprise-wide delivery o sotware updates andupgrades to improve compliance and cutoperating costs.

“With dierent security requirementsin dierent regions around the world, aglobal sotware provider like KAL has tobe proactive and know the requirements

and regulations in the dierent regions andprovide comprehensive support or them,”Hensley said.

8/8/2019 Kal_G_2010 ATM Software Trends_To Launch

http://slidepdf.com/reader/full/kalg2010-atm-software-trendsto-launch 22/38

© 2010 NetWorld Alliance LLC | Sponsored by KAL 22

Chapter 3 A regional ocus: Europe, the Middle East and Arica

Total survey respondents rom Europe, the Middle East and Arica (EMEA):For 2010: 87 | For 2009: 42

2010 2009

100% 51% 55%

50% - 99% 32% 14%Less than 50% 3% 7%

Don’t know 3% 12%

Not applicable 11% 12%

20. What percentage o your organization’s AMs or your customers’ AMs run Mi-crosot Windows today?

In this region, as well as the others, Microsot Windows reigns. In the developing coun-tries o EMEA, irst-generation ATM deployments are based on the Microsot OS, leap-rogging other options that were previously popular in other regions.

2010 2009

Yes, planned and budgeted or this year 18% 31%

Yes, planning or next year or the ollowing year 21% 17%

No, we recently replaced it 20% 7%

No, there are no plans to replace the existing ATM sotware 22% 29%

Not applicable 20% 17%

21. Are there plans to replace your organization’s current AM sotware or yourcustomers’ current AM sotware?

One-ith o the 2010 respondents replaced their sotware, a relection o the higher num-ber o respondents with plans or replacements in the 2009 survey. The number o respon-dents with no plans to replace it ell compared to the previous year.

8/8/2019 Kal_G_2010 ATM Software Trends_To Launch

http://slidepdf.com/reader/full/kalg2010-atm-software-trendsto-launch 23/38

© 2010 NetWorld Alliance LLC | Sponsored by KAL 23

CHAPER 3 A regional ocus: Europe, the Middle East and Arica

2010 2009

ATMs rom multiple vendors, running a single sotware application on all 39% 36%

ATMs rom multiple vendors, considering multivendor sotware inthe uture

29% 14%

ATMs rom a single vendor, understand the benets o multivendor ATMsotware

9% 12%

ATMs rom a single vendor, see no need or multivendor ATM sotware 10% 10%

Not a consideration 13% 19%

Not sure what this means 5% 10%

22. Which statement best identiies your organization’s multivendor AM strategy, orthe multivendor AM strategy o your customers?

About two-thirds o the EMEA respondents operate multivendor sotware or are consid-ering it, while another 9 percent understand the beneits. Clearly, the value o multivendorsotware is well known in the region.

2010 2009

Increased security (such as EMV, 3DES, remote key, biometrics) 60% 57%

Cost reduction o the ATM network 59% 42%

Added unctionality (such as new transactions) 57% 21%

An increase in productivity and efciency 53% N/A

Support or new technology 45% 31%

Providing an enhanced user experience (such as transaction personalization) 41% 38%

Improved support 38% 52%

Need or better customer relationships 32% N/AImproved ATM reliability 29% 37%

Ease o changing sotware when needed 25% 10%

None o the above 1% 0

23. What is the primary driver (or drivers) or changing AM sotware?

EMEA respondents’ interest in security, highest among the regions, is no surprise in anarea home to many emerging economies susceptible to criminal activity. Cost reductionalso is a high priority, particularly in the more mature European markets.

8/8/2019 Kal_G_2010 ATM Software Trends_To Launch

http://slidepdf.com/reader/full/kalg2010-atm-software-trendsto-launch 24/38

8/8/2019 Kal_G_2010 ATM Software Trends_To Launch

http://slidepdf.com/reader/full/kalg2010-atm-software-trendsto-launch 25/38

© 2010 NetWorld Alliance LLC | Sponsored by KAL 25

CHAPER 3 A regional ocus: Europe, the Middle East and Arica

26. Given customers have increasingly ewer reasons to visit bank branches, how im-portant a delivery channel do you see your AM network as a customer touchpointthat allows you to compete eectively with other banks?

FIs in the region will continueto rely on ATMs as a customertouchpoint, in some casesperhaps the only interactionconsumers may have with theirbank.

Not applicable5%

Same as before14%

Not important at all2%

Becomingless important

3%

Becomingmore important

20%Very important

56%

27. Rate the ollowing bank service delivery channels in order o importance as acustomer touchpoint.

0 10 20 30 40 50 60 70

32%

8%

2%

14%

44%

Most Important

2nd Most Important

3rd Most Important

4th Most Important

5th Most Important

ATM

0 10 20 30 40 50 60 70

39%

16%

11%

13%

21%

Most Important

2nd Most Important

3rd Most Important

4th Most Important

5th Most Important

Branch

8/8/2019 Kal_G_2010 ATM Software Trends_To Launch

http://slidepdf.com/reader/full/kalg2010-atm-software-trendsto-launch 26/38

© 2010 NetWorld Alliance LLC | Sponsored by KAL 26

CHAPER 3 A regional ocus: Europe, the Middle East and Arica

ATMs take on a higher importance in the EMEA as a close second in the most importantcategory than they do in the Americas. Clearly, the mobile channel remains one that ismore promise than reality or the EMEA, as well as the Americas. Call centers have less

relevance in markets where the customer base has embraced online and mobile phoneinteraction.

0 10 20 30 40 50 60 70

3%

25%

34%

26%

9%

Most Important

2nd Most Important

3rd Most Important

4th Most Important

5th Most Important

Call center

0 10 20 30 40 50 60 70

18%

32%

22%

5%

24%

Most Important

2nd Most Important

3rd Most Important

4th Most Important

5th Most Important

Internet

0 10 20 30 40 50 60 70

7%

13%

25%

53%

2%

Most Important

2nd Most Important

3rd Most Important

4th Most Important

5th Most Important

Mobile phone

8/8/2019 Kal_G_2010 ATM Software Trends_To Launch

http://slidepdf.com/reader/full/kalg2010-atm-software-trendsto-launch 27/38

© 2010 NetWorld Alliance LLC | Sponsored by KAL 27

Integration o the ATM with other channels remainsvital or FIs that rely on a traditional branch

presence as well as the technology-based customer interactions.

CHAPER 3 A regional ocus: Europe, the Middle East and Arica

Fast-growing EMEA marketspresent challenges or FIs

FIs in the emerging nations o Europe, theMiddle East and Arica can take advantageo the latest eatures enabled through theirATM sotware. Those FIs in the arguably more mature markets in this region beneitrom the eiciency gains rom multivendorsotware.

As FIs seek sotware to support their stra-

tegic eiciency and marketing programs,there are some regional dierences in theirapproaches. Desired eatures and unctions vary with the markets around the world, asdoes the approach to sotware development.

For example, cash recycling and deposit auto-mation are very important in the Chinesemarket, whereas the ability to depositchecks and cash without an envelope isimportant in the United States. The sot-ware and services an FI will deploy have to

correspond with those capabilities that aregoing orward in those markets.

Fueled in part by higher real estate pricesthat make branches prohibitively expensive,European FIs rely on ATMs to provide moreunctionality than their North Americancounterparts. For instance, consumers inthe Netherlands and other nations routinely pay bills at the ATM, while in Spain oot-ball tickets are a big sel-service business.

In the U.K., ATMs unction essentially as mini branches, oering bill payments,statement printing and automated cashand check deposit.

Even in technologically advanced markets,cash is still king. A Bank o England study ound that ATM withdrawals account orabout 70 percent o cash acquisition in

2009, compared to 25 percent in the 1990s,although the overall number o cash retailtransactions has dropped. In times o eco-nomic turmoil, the public still trusts cash,and its movement is vital to the economy.

Integration o the ATM with other chan-nels remains vital or FIs that rely on atraditional branch presence as well as thetechnology-based customer interactions.For instance, RBR reports that 10 percento European ATMs accept automated de-posits, maintaining customer relationshipsat a lower cost.

Multivendor sotware eiciently enables

the lexibility necessary to meet these chal-lenges.

“With real estate challenges, banks inEurope have to maintain customer satis-action, and the best way to do that is tooer alternative channels,” said Walsh,who worked or Wincor Nixdor in Irelandbeore transerring to the United States.“Financial institutions are trying to reducecosts and oer consistent customer experi-ence, and the best way to do that is to have

one application across all channels.”

FIs understand the need to build a seam-less customer experience.

“We want to integrate the ATM channelwith the other ones in the organization,such as electronic banking, branch, mo-bile and so on,” said Miguel Angel Cámara

8/8/2019 Kal_G_2010 ATM Software Trends_To Launch

http://slidepdf.com/reader/full/kalg2010-atm-software-trendsto-launch 28/38

© 2010 NetWorld Alliance LLC | Sponsored by KAL 28

CHAPER 3 A regional ocus: Europe, the Middle East and Arica

López, project manager o sel-service orCECA, the Spanish Conederation o SavingsBanks, which operates 3,500 ATMs. “Theclient must eel the organization the sameway, regardless o the channel he or shechooses.”

To maintain channel integrity and providea seamless, yet eicient, customer experi-ence, the ATM is a prime opportunity. Atla Caixa (EUR 243,517 million) the leadingsavings bank in Europe and the third-larg-

est inancial entity in Spain, the ATM is away to reduce operating costs and improvethe customer experience.

“The ATM is strategic or us in order to re-duce branch repetitive and time-consumingtransactions and let our employees spendtheir time in commercial tasks,” said PereRàols, ATM and ticketing IT manager orla Caixa.

Instead o expanding branches and ATMlocations, the Spanish bank expects to cutcosts and retain customers with additionalunctions. Its customers enjoy nearly 200unctions at la Caixa’s ATM network o nearly 8,000 ATMs, which is larger than itscompetitors.

“We expect to add more unctionality i necessary to reduce low value-addedtransactions in our branches and do themthrough our ATMs,” Ràols said.

Emerging economies o the Middle Eastand Arica basically skipped the checkphase o inancial instruments, insteadrelying on cash and stored-value cards, aswell as mobile banking.

An executive at a bank in Kenya, whowished to remain anonymous, noted that

his institution is adding services to itsATM leet. These include utility payments,check deposits, money transers and mobile

phone top-ups.

As ATMmarketplace.com reported previ-ously , Diebold ormed a direct sales opera-tion in Turkey to service customers in theregion.

“The ATM market in Turkey is one o theastest-growing in the EMEA region,” saidDanilo Rivalta, vice president and generalmanager o Diebold Europe, Middle Eastand Arica (EMEA) in late 2009. “Thismarket has increased by 20 percent duringthe last year and is expected to grow at thesame level during the coming year.”

Standard Bank o South Arica, through itsUgandan subsidiary Stanbic Bank Uganda,in conjunction with MTN, brought itsmobile payments application to Uganda inearly 2009. Called MTN Mobile Money, theUganda service builds on Standard Bank’sprevious launch in South Arica. Users

registering or the product will be able tosend and receive unds using their mobilehandsets. Additional banking unctionality would be added onto the application aterurther development and testing.

When launching the service in South Arica,Irene Charnley, commercial director o theMTN Group, a Standard Bank subsidiary,

“The ATM is strategic or us in order to reducebranch repetitive and time-consuming

transactions and let our employees spend their time in commercial tasks.”

— Pere Ràfols, ATM and ticketing IT manager, la Caixa

8/8/2019 Kal_G_2010 ATM Software Trends_To Launch

http://slidepdf.com/reader/full/kalg2010-atm-software-trendsto-launch 29/38

© 2010 NetWorld Alliance LLC | Sponsored by KAL 29

CHAPER 3 A regional ocus: Europe, the Middle East and Arica

noted that MTN Banking’s mobile productleveraged cellular telephone technology and inancial services expertise or thebeneit o clients.

“It is a unique oering that creates 24/7banking or the mobile generation,” she said.

The South Arican mobile products arelinked to a cash card that can be upgradedto a MasterCard. The MasterCard enablespurchasing rom merchants who accept

the card, and opens up ATM access toSaswitch ATMs and the Standard Banknetwork. There are no monthly ees and nominimum balances.

The product enables person-to-person pay-ments and transers to other bank accountsand credit cards and bill payments. Clientscan even pay traic ines by phone or loadtheir electricity accounts with prepaid credits.

“This convenient retail environmentrevolutionizes inancial sector marketingand distribution channels while massively simpliying service access,” Charnley said.

ATM usage in the Middle East is expectedto surge in the coming years. A reportrom Retail Banking Research Ltd. estimat-ed that the number o ATMs in the MiddleEast will reach 70,000 by 2013.

That growth is ueled in large part by

recent developments o inancial instru-ments that conorm to Shari’ah, or Islamiclaw. MasterCard Worldwide, along withEonCap Islamic Bank, launched an Islamicdebit MasterCard. It’s a debit card withATM unctions that also incorporates thePayPass system o noncontact payments.

“It’s designed to appeal to both Muslim andnon-Muslim individuals who preer betterinancial control as the card ensures thatpurchases are automatically deducted romthe cardholder’s account and approved only i enough unds exist within the account,”said Fozia Amanulla, chie executive oicero Eoncap Islamic Bank. “It’s acceptedworldwide at more than 26 million loca-tions and can be used at an ATM ore-banking.”

In Bahrain, Al Salam Bank launched aShari’ah-compliant credit card that alsogives holders access to 30 million ATMsand retail shops worldwide. The smart cardalso incorporates a dynamic mechanismor personal data veriication in addition toease o use at all points o sale.

That level o security is vital to consumerconidence around the world, but especially in emerging markets where there may be lessaith in institutions than in more mature

economies.

“Ensuring a secure environment or ATMusers is all the more important or emergingmarkets such as the Middle East, since theextent o market growth is closely linked tothe level o transaction security oered tocustomers,” said Dave Wetzel, vice presi-dent and managing director or Europe,the Middle East and Arica o Diebold, atthe Middle East ATMs 2010 conerence.

FIs ear physical attacks such as skimming,as well as sophisticated sotware hacks.

“We guard against all o them but now ourmain ocus is sotware hacking and sensi-ble data encryption,” said la Caixa’s Ràols.

8/8/2019 Kal_G_2010 ATM Software Trends_To Launch

http://slidepdf.com/reader/full/kalg2010-atm-software-trendsto-launch 30/38

© 2010 NetWorld Alliance LLC | Sponsored by KAL 30

Chapter 4 A regional ocus: Asia-Pacifc

Total respondents rom Asia-Pacifc, including Australia:For 2010: 47 | For 2009: 39

2010 2009

100% 35% 46%

50% - 99% 41% 44%

Less than 50% 15% 0

Don’t know 0% 5%

Not applicable 9% 5%

28. What percentage o your organization’s AMs or your customers’ AMs run Mi-crosot Windows today?

As elsewhere in the world, Microsot Windows dominates the operating system marketor ATMs.

2010 2009

Yes, planned and budgeted or this year 13% 21%

Yes, planning or next year or the ollowing year 28% 18%

No, we recently replaced it 7% 13%

No, there are no plans to replace the existing ATM sotware 33% 41%

Not applicable 20% 8%

29. Are there plans to replace your organization’s current AM sotware or yourcustomers’ current AM sotware?

The drive to change sotware is less in Asia than it is in other regions o the world, al-though more than a quarter o respondents plan to make a change in 2011 or 2012. How-ever, a third have no plans to change their sotware.

8/8/2019 Kal_G_2010 ATM Software Trends_To Launch

http://slidepdf.com/reader/full/kalg2010-atm-software-trendsto-launch 31/38

© 2010 NetWorld Alliance LLC | Sponsored by KAL 31

CHAPER 4 A regional ocus: Asia-Pacifc

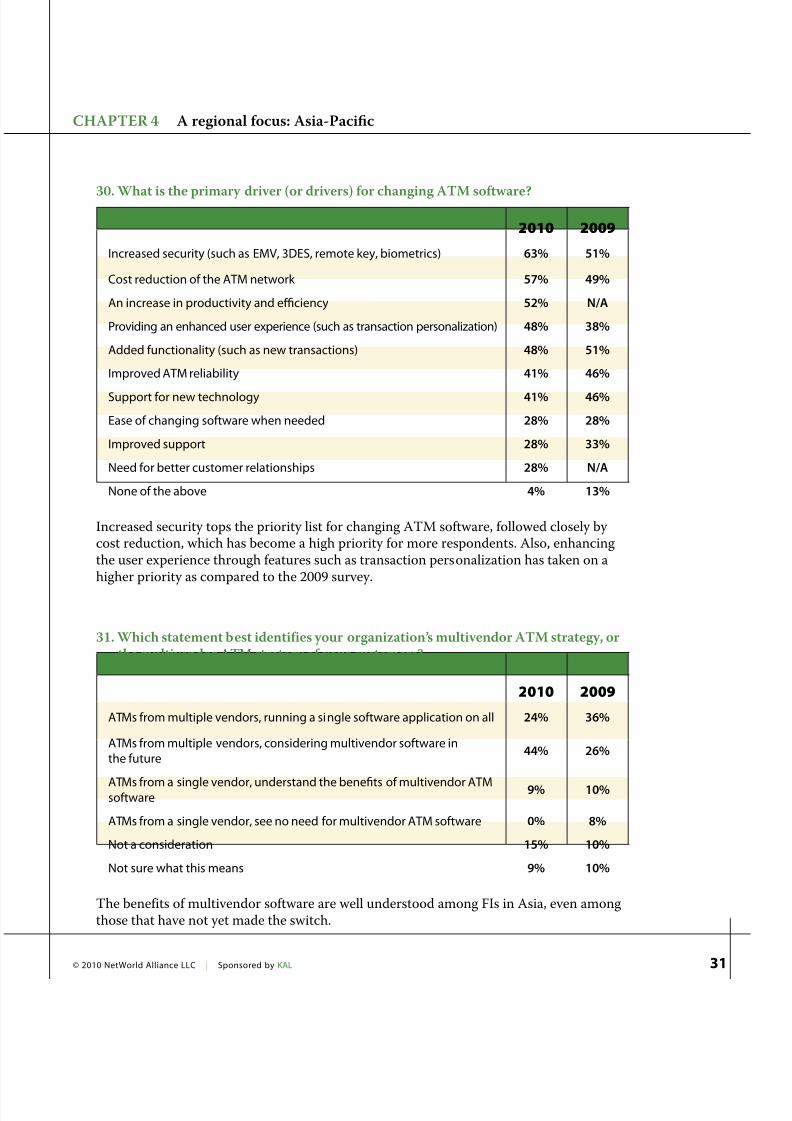

2010 2009

Increased security (such as EMV, 3DES, remote key, biometrics) 63% 51%

Cost reduction o the ATM network 57% 49%

An increase in productivity and efciency 52% N/A

Providing an enhanced user experience (such as transaction personalization) 48% 38%

Added unctionality (such as new transactions) 48% 51%

Improved ATM reliability 41% 46%

Support or new technology 41% 46%

Ease o changing sotware when needed 28% 28%

Improved support 28% 33%

Need or better customer relationships 28% N/A

None o the above 4% 13%

30. What is the primary driver (or drivers) or changing AM sotware?

Increased security tops the priority list or changing ATM sotware, ollowed closely by cost reduction, which has become a high priority or more respondents. Also, enhancingthe user experience through eatures such as transaction personalization has taken on ahigher priority as compared to the 2009 survey.

2010 2009

ATMs rom multiple vendors, running a single sotware application on all 24% 36%

ATMs rom multiple vendors, considering multivendor sotware inthe uture

44% 26%

ATMs rom a single vendor, understand the benets o multivendor ATMsotware 9% 10%

ATMs rom a single vendor, see no need or multivendor ATM sotware 0% 8%

Not a consideration 15% 10%

Not sure what this means 9% 10%

31. Which statement best identiies your organization’s multivendor AM strategy, orthe multivendor AM strategy o your customers?

The beneits o multivendor sotware are well understood among FIs in Asia, even amongthose that have not yet made the switch.

8/8/2019 Kal_G_2010 ATM Software Trends_To Launch

http://slidepdf.com/reader/full/kalg2010-atm-software-trendsto-launch 32/38

© 2010 NetWorld Alliance LLC | Sponsored by KAL 32

CHAPER 4 A regional ocus: Asia-Pacifc

2010 2009

Remote monitoring o the ATM network 60% 51%

Multivendor ATM sotware 40% 28%

Cash management and orecasting 31% 28%

Customer preerences 27% N/A

Sotware distribution 22% 38%

Automated test tools 20% 13%

Support or biometrics 20% 18%

One-to-one marketing / purchase git cards 18% 31%

Support or cash recycling 16% 28%

Bulk-note cash deposit 13% 28%

Envelope-ree check deposit 11% 13%

Other 2% 1%

32. Select the three most desired new eatures o AM sotware.(Percent who included the below among their top three)

Desire or network eiciency ranks highly in Asia-Paciic as 60 percent o the respondentsidentiied remote monitoring as the most desired eature. Cash management and orecast-ing also was a top desire, to aid FIs in being more eicient in managing vault cash. The

desire or multivendor-capable sotware signiicantly increased over the previous year.

2010 2009

Reduce operational costs 33% 23%

Improve the ability to remotely manage the ATM network 17% 23%

Adopt enhanced security technologies 15% 21%Create a better ATM customer experience 15% N/A

Improve customer unctionality 15% 23%

Improve the user interace 4% 5%

No changes needed 0% 5%

33. What is the most critical change your organization or your customers’ organizationneeds to make to its AM network in 2010?

Priorities have shited in the Asia-Paciic market, as the drive to reduce operational coststakes precedence over improvement o the customer experience.

8/8/2019 Kal_G_2010 ATM Software Trends_To Launch

http://slidepdf.com/reader/full/kalg2010-atm-software-trendsto-launch 33/38

© 2010 NetWorld Alliance LLC | Sponsored by KAL 33

0 10 20 30 40 50 60 70

46%

0%

2%

11%

41%

Most Important

2nd Most Important

3rd Most Important

4th Most Important

5th Most Important

ATM

CHAPER 4 A regional ocus: Asia-Pacifc

34. Given customers have increasingly ewer reasons to visit bank branches, how im-portant a delivery channel do you see your AM network as a customer touchpointthat allows you to compete eectively with other banks?

35. Rate the ollowing bank service delivery channels in order o importance as acustomer touchpoint.

Some 82 percent o FIs in Asia-Paciic consider the ATM “very important” and “becoming moreimportant” as a customer touch-point vital to their competitiveadvantage in the marketplace.

Not applicable11%

Same as before3%

Not important at all

2%

Becomingless important

2%

Becomingmore important

31%

Very important51%

0 10 20 30 40 50 60 70

30%

11%

17%

22%

20%

Most Important

2nd Most Important

3rd Most Important

4th Most Important

5th Most Important

Branch

8/8/2019 Kal_G_2010 ATM Software Trends_To Launch

http://slidepdf.com/reader/full/kalg2010-atm-software-trendsto-launch 34/38

© 2010 NetWorld Alliance LLC | Sponsored by KAL 34

CHAPER 4 A regional ocus: Asia-Pacifc

Traditional branches and ATMs rank highly in the Asia-Paciic market as well as otherregions, a surprise considering the growth o mobile transactions that garner headlines.Perhaps the region is more traditional than the mobile hype would indicate.

0 10 20 30 40 50 60 70

11%

40%

33%

13%

4%

Most Important

2nd Most Important

3rd Most Important

4th Most Important

5th Most Important

Call center

0 10 20 30 40 50 60 70

9%

26%

30%

9%

26%

Most Important

2nd Most Important

3rd Most Important

4th Most Important

5th Most Important

Internet

0 10 20 30 40 50 60 70

4%

13%

20%

54%

9%

Most Important

2nd Most Important

3rd Most Important

4th Most Important

5th Most Important

Mobile phone

8/8/2019 Kal_G_2010 ATM Software Trends_To Launch

http://slidepdf.com/reader/full/kalg2010-atm-software-trendsto-launch 35/38

© 2010 NetWorld Alliance LLC | Sponsored by KAL 35

CHAPER 4 A regional ocus: Asia-Pacifc

Asia-Pacifc leads in innovationThe Asia-Paciic region continues to be ahotbed o innovation or ATM sotware, asconsumer demand pressures FIs to keep up.

In mature markets, such as Japan andSouth Korea, consumers rely on a seamlessmix o ATM, online and mobile inancialservices. In emerging markets, rapidly advancing technology means that a multi- vendor solution helps FIs stay current.

For instance, research irm Celent expectsexplosive growth in the ATM markets inChina and India to continue, with morethan 350,000 ATMs in both marketsthrough 2010 and 2011. Both China andIndia are predominately cash-based econo-mies, and customers preer the convenienceo 24/7 neighborhood banking via ATMs.

“Like India, China is experiencing rapidgrowth in ATMs, driven by its largely cash-based society, the low density o bankbranches at a time when demand or inan-cial services is accelerating rapidly, and theneed to more aggressively deploy ATMsbeyond the largest metropolitan centersto midsize and small cities and suburbanregions,” said Wenli Yuan, Celent senioranalyst and co-author o the report “TheDragon and Tiger o the ATM Markets:China and India.”

Mobile transactions have been the hottopic in Asia, with some countries oeringmore than 200 types o transaction romsmart phones. Contactless cards also are agrowing trend, as top-ups or transit cards,tickets and other stored-value transactions.

“Asia is still the leader in this type o activ-ity, although there are pilot projects all

over the world, and the world is becomingsmaller in terms o dierences,” said NCR’sGallagher.

FIs in other regions could learn rom theAsian banks that have made cash automa-

tion and recycling a common service orconsumers.

Zijin Fulcrum Technology, a KAL partnerbased in Guandong, China, operates 20,000ATMs and maintains sotware or nearly 60,000 units. The company is using trans-action personalization as a marketingadvantage to reach its youthul audiencethat relies on ATMs or cash transactions.

“Because cash is very common in China,ATM users are mostly young people andtransaction personalization has greatattractions or young people,” said ZhongCheng, vice president or Zijin.

One-to-one marketing and transactionpersonalization move the customer rela-tionship orward, something that’s otenneglected at the ATM channel. How otendo consumers have to select their preer-ences rom the same one-size-its-all menus,

or view irrelevant advertising? The rightsotware can enable the ATM to eel like amuch more personalized interaction.

“When banks have dierent touchpoints,instead o having multiple applications orthat, they should have one application orall o them,” said Wincor’s Walsh. “FIs aretrying to reduce costs and oer consistent

FIs in other regions could learn rom the Asianbanks that have made cash automation and

recycling a common service or consumers.

8/8/2019 Kal_G_2010 ATM Software Trends_To Launch

http://slidepdf.com/reader/full/kalg2010-atm-software-trendsto-launch 36/38

© 2010 NetWorld Alliance LLC | Sponsored by KAL 36

customer experiences, and the best way todo that is to have one application across allchannels.”

Savvy FIs break down the internal depart-mental silo walls so those marketing eortscross channels to reach consumers withindividualized messages that build rela-tionships. Ideally, the online channel willknow a customer’s ATM preerences and vice versa.

“Quite oten each o these channels iscompletely independent with their owninormation technology groups,” said NCR’sGallagher. “FIs can try to link these chan-nels so they can optimize it and build thesystem only one time.”

O course, cost control plays a role or AsianFIs as it does elsewhere.

“For us the most critical areas are the costo sotware maintenance and consumables,such as journal rolls,” Cheng said.

Asian FIs such as China Construction Bankand China Everbright Bank adopted KAL’sKalignite multivendor sotware across theirportolios o more than 32,000 ATMs and1,500 ATMs, respectively. China EverbrightBank rolled out Kalignite over only eightmonths. The installation allows CEB morelexibility in growing its ATM leet.

“One major advantage or us is a muchgreater choice o ATM hardware now thatwe have the Kalignite multivendor ATMplatorm installed,” said Li Jian, general man-ager o the CEB’s E-banking department.

Tisco Bank o Thailand relied on KAL’ssotware to implement new transactions.The new Tisco banking kiosks include

smartcard and ePurse transactions as wellas payment transactions or utility bills,insurance, mutual unds, loan payments andmore. Tisco’s kiosks running the Kalignitesotware communicate with multiple hosts

simultaneously to perorm the transactions,simpliying the back-end integration whilecarrying the transactional workload on thekiosk itsel.

The kiosk application also doubles as ateller station solution inside Tisco’s bankbranches. The lexibility o the Kalignitekiosk application allowed Tisco to use itat the bank’s teller stations to perorm thesame set o transactions or teller-assistedcustomer transactions with a modiied

transaction low.

With just more than 38,000 ATMs in India,a country with a population o more than1.2 billion, there is a huge demand orATM banking services across India. HCLInosystems, a banking technology integra-tion irm, partnered with Nautilus Hyo-sung to provide complete ATM solutionsor Indian banks, especially those servingrural areas.

Nautilus Hyosung uses its hardware andsotware expertise to customize oer-ings or the Indian market. Nautilus, inconjunction with HCL, designed units todeploy ATMs in rural locations with rela-tively low transaction volumes.

To enhance security, specialized sotware

Savvy FIs break down the internal departmental silo walls so marketing eforts cross channels toreach consumers with individualized messages

that build relationships.

CHAPER 4 A regional ocus: Asia-Pacifc

8/8/2019 Kal_G_2010 ATM Software Trends_To Launch

http://slidepdf.com/reader/full/kalg2010-atm-software-trendsto-launch 37/38

8/8/2019 Kal_G_2010 ATM Software Trends_To Launch

http://slidepdf.com/reader/full/kalg2010-atm-software-trendsto-launch 38/38