Kajaria Ceramics Ltd. · Kajaria Ceramics Limited (Kajaria), promoted by Mr. Ashok Kajaria in 1985,...

8

May 16, 2018 Kajaria Ceramics Ltd. …scaling high CMP INR 544 Target INR: 701 Result Update –Buy SKP Securities Ltd www.skpmoneywise.com Page 1 of 8 Company Background Kajaria Ceramics Limited (Kajaria), promoted by Mr. Ashok Kajaria in 1985, is the largest player in India’s Ceramic Tiles industry, with ~10% market share, under “KAJARIA” brand with a combined manufacturing capacity of 68.4 MSM which includes its own manufacturing facilities in Uttar Pradesh & Rajasthan and its JV manufacturing partners. It also sells tiles outsourced from Morbi, Gujarat. It also manufactures sanitaryware and faucets through JV partners, which provides it strategic product extension opportunities to leverage its channel. Investment Rationale Topline to grow at a CAGR of ~16.5% over FY17-20E During Q4FY18, Kajaria reported consolidated net sales of Rs 7,500.4 mn, registering marginal growth of ~4% y-o-y basis on account of muted volume growth. It witnessed ~5% volume growth to 20.24 MSM vis-a-vis last year and 6% growth during FY18 to 71.96 MSM. The contribution from owned, JVs, and outsourced tiles to the total consolidated revenues were ~60%, ~25 and ~15% respectively, during the quarter. Contributions from sanitaryware & faucet segments were Rs 490.8 mn. Going forward, with Kajaria’s focus on value added products, increasing contribution from GVT and PVT segment, and positive implications of GST, implementation of interstate (w.e.f. April 1, 2018) and intrastate (expected by June 1, 2018) e-way bill, we expect the Company to grow at a CAGR of ~16.5% during FY17-FY20E. EBIDTA Margins to expand: EBIDTA margins during Q4FY18, declined by 210 bps y-o-y to 16%, mainly on account of higher gas prices, decline in GVT realisations and losses in some of the JVs. Power & fuel cost to sales ratio increased to 20.3% during the quarter vis-à-vis 18% corresponding quarter last year. We expect industry to pick-up from FY19 onwards due to structural shift towards organised players post e-waybill implementation, which is expected to generate traction in the industry.With Kajaria’s focus on superior, value-added products, going forward, we expect the product mix to result in increase of margins to ~17.8%by FY20E. Expanding capacity of PVT & GVT tiles by 5.6 MSM and 5 MSM respectively: There is an increased demand for life style consumption products, especially from aspiring mass affluent. To meet the resultant demand of ceramic tiles, Kajaria is expanding the capacity of PVT tiles at existing location at Maluthana, Rajasthan, by 5.6 MSM with the capex of ~Rs 800 mn. Plant is expected to get commissioned by FY19E. With this expansion the total capacity of the company at Maluthana will increase to 12.1 MSM, from the current 6.5 MSM. Apart from the above capacity expansions through organic route, Kajaria is also in the process of acquiring 51% stake in Floera Ceramics Pvt Ltd (a JV), which has plans to setup 5 MSM (earlier 5.7 MSM) PVT tiles facility, at Andhra Pradesh, with an investment of ~Rs 1 bn. This capacity is expected to get on-stream by September 2018. West Bridge Crossover LLC has committed an investment of Rs 645 mn, for 15% equity stake in Kajaria Bathware Pvt Ltd - a subsidiary of Kajaria producing faucets at Gailpur, reposing the confidence in Kajaria. Ventured in plywood business: Kajaria has announced its entry into another building product viz. plywood by acquiring 50% stake in Kajaria Plywood Pvt Ltd., to leverage its customers and channels. Initially, it will trade in this segment for a couple of years to understand market dynamics. Plywood market is pegged at Rs 180 bn of which Rs 140 bn is dominated by unorganized segment, creating huge opportunities for branded players like Kajaria. VALUATION Better economic growth, leaving more disposable income for discretionary life style consumption, rapid urbanisation, changing customer preference towards quality branded products particularly amongst the growing mass affluent, increasing nuclear families and Governments’ thrust on “Housing for All” coupled with strong brand equity and recall and distribution network, augers well for the Company. It has de-risked its growth strategy with an asset light business model, adopting a joint venture route. We have valued the stock on the basis of P/E - method of relative valuation - of 30x of FY20E earnings. In view of the sharp correction in the share price to Rs 544 now, after a stupendous rally to a 52 week high of Rs 768 recently, we recommend a BUY on the stock with a target price of Rs 701/- (~29% upside) in 18 months. Key Share Data Face Value (INR) 1.0 Equity Capital (INR Mn) 158.9 Market Cap (INR mn) 86462.3 52 Week High/Low (INR) 768/503 Avg. Daily Volume (BSE) 66,528 BSE Code 500233 NSE Code KAJARIACER Reuters Code KAJR.NS Bloomberg Code KJC:IN Shareholding Pattern (Mar 31, 2018) 48% 9% 28% 15% Promoters DII FII Public & Others Particulars FY17 FY18 FY19E FY20E Net Sales 25,496.3 27,106.0 31,773.2 36,777.5 Growth (%) 5.6% 6.3% 17.2% 15.7% EBITDA 4,963.3 4,563.5 5,465.0 6,546.4 PAT 2,528.4 2,349.5 3,001.5 3,712.4 Growth (%) 9.3% -7.1% 27.8% 23.7% EPS (INR) 15.9 14.8 18.9 23.4 BVPS (INR) 73.9 85.0 96.7 110.4 Key Financials (INR Million) Particulars FY17 FY18 FY19E FY20E P/E (x) 34.2 36.8 28.8 23.3 P/BVPS (x) 7.4 6.4 5.6 4.9 Mcap/Sales (x) 3.4 3.2 2.7 2.4 EV/EBITDA (x) 17.7 19.1 16.0 13.2 ROCE (%) 30.8% 24.8% 26.4% 29.3% ROE (%) 21.5% 17.4% 19.5% 21.2% EBIDTA Mar (%) 19.5% 16.8% 17.2% 17.8% PAT Mar (%) 9.9% 8.7% 9.4% 10.1% Debt - Equity (x) 0.1 0.1 0.1 0.1 Source: Company, SKP Research Key Financials Ratios Price Performance Kajaria vs BSE 200 -30% -20% -10% 0% 10% 20% May-17 May-17 Jun-17 Jul-17 Aug-17 Aug-17 Sep-17 Oct-17 Oct-17 Nov-17 Dec-17 Dec-17 Jan-18 Feb-18 Feb-18 Mar-18 Apr-18 May-18 Kajaria BSE 200 Analyst: Vineet Agrawal Tel No: +91-22-49226006; Mobile: +91-9819510575 e-mail: [email protected]

Transcript of Kajaria Ceramics Ltd. · Kajaria Ceramics Limited (Kajaria), promoted by Mr. Ashok Kajaria in 1985,...

May 16, 2018

Kajaria Ceramics Ltd.

…scaling high

CMP INR 544 Target INR: 701 Result Update –Buy

SKP Securities Ltd www.skpmoneywise.com Page 1 of 8

Company Background

Kajaria Ceramics Limited (Kajaria), promoted by Mr. Ashok Kajaria in 1985, is the largest player in India’s Ceramic Tiles industry, with ~10% market share, under “KAJARIA” brand with a combined manufacturing capacity of 68.4 MSM which includes its own manufacturing facilities in Uttar Pradesh & Rajasthan and its JV manufacturing partners. It also sells tiles outsourced from Morbi, Gujarat. It also manufactures sanitaryware and faucets through JV partners, which provides it strategic product extension opportunities to leverage its channel.

Investment Rationale

Topline to grow at a CAGR of ~16.5% over FY17-20E During Q4FY18, Kajaria reported consolidated net sales of Rs 7,500.4 mn, registering

marginal growth of ~4% y-o-y basis on account of muted volume growth. It witnessed ~5% volume growth to 20.24 MSM vis-a-vis last year and 6% growth during FY18 to 71.96 MSM.

The contribution from owned, JVs, and outsourced tiles to the total consolidated revenues were ~60%, ~25 and ~15% respectively, during the quarter. Contributions from sanitaryware & faucet segments were Rs 490.8 mn.

Going forward, with Kajaria’s focus on value added products, increasing contribution from GVT and PVT segment, and positive implications of GST, implementation of interstate (w.e.f. April 1, 2018) and intrastate (expected by June 1, 2018) e-way bill, we expect the Company to grow at a CAGR of ~16.5% during FY17-FY20E.

EBIDTA Margins to expand: EBIDTA margins during Q4FY18, declined by 210 bps y-o-y to 16%, mainly on account

of higher gas prices, decline in GVT realisations and losses in some of the JVs. Power & fuel cost to sales ratio increased to 20.3% during the quarter vis-à-vis 18% corresponding quarter last year.

We expect industry to pick-up from FY19 onwards due to structural shift towards organised players post e-waybill implementation, which is expected to generate traction in the industry.With Kajaria’s focus on superior, value-added products, going forward, we expect the product mix to result in increase of margins to ~17.8%by FY20E.

Expanding capacity of PVT & GVT tiles by 5.6 MSM and 5 MSM respectively: There is an increased demand for life style consumption products, especially from

aspiring mass affluent. To meet the resultant demand of ceramic tiles, Kajaria is expanding the capacity of PVT tiles at existing location at Maluthana, Rajasthan, by 5.6 MSM with the capex of ~Rs 800 mn. Plant is expected to get commissioned by FY19E. With this expansion the total capacity of the company at Maluthana will increase to 12.1 MSM, from the current 6.5 MSM.

Apart from the above capacity expansions through organic route, Kajaria is also in the process of acquiring 51% stake in Floera Ceramics Pvt Ltd (a JV), which has plans to setup 5 MSM (earlier 5.7 MSM) PVT tiles facility, at Andhra Pradesh, with an investment of ~Rs 1 bn. This capacity is expected to get on-stream by September 2018.

West Bridge Crossover LLC has committed an investment of Rs 645 mn, for 15% equity stake in Kajaria Bathware Pvt Ltd - a subsidiary of Kajaria producing faucets at Gailpur, reposing the confidence in Kajaria.

Ventured in plywood business: Kajaria has announced its entry into another building product viz. plywood by acquiring

50% stake in Kajaria Plywood Pvt Ltd., to leverage its customers and channels. Initially, it will trade in this segment for a couple of years to understand market dynamics. Plywood market is pegged at Rs 180 bn of which Rs 140 bn is dominated by unorganized segment, creating huge opportunities for branded players like Kajaria.

VALUATION

Better economic growth, leaving more disposable income for discretionary life style consumption, rapid urbanisation, changing customer preference towards quality branded products particularly amongst the growing mass affluent, increasing nuclear families and Governments’ thrust on “Housing for All” coupled with strong brand equity and recall and distribution network, augers well for the Company. It has de-risked its growth strategy with an asset light business model, adopting a joint venture route.

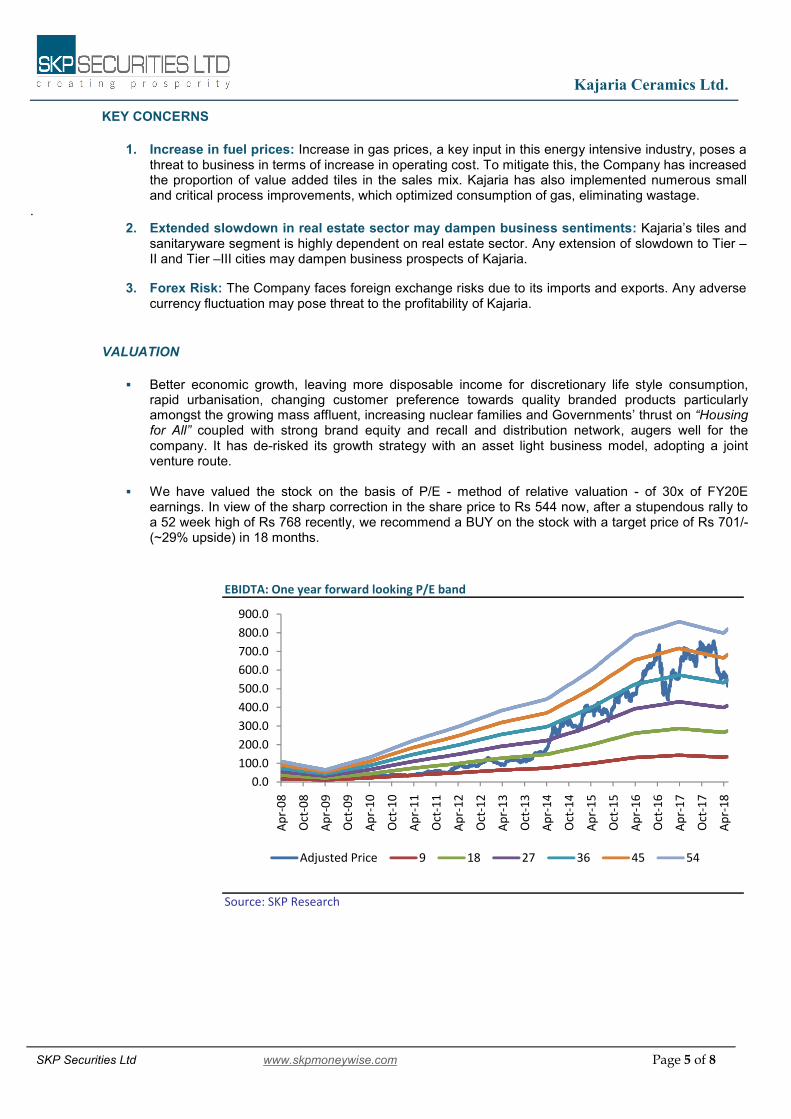

We have valued the stock on the basis of P/E - method of relative valuation - of 30x of FY20E earnings. In view of the sharp correction in the share price to Rs 544 now, after a stupendous rally to a 52 week high of Rs 768 recently, we recommend a BUY on the stock with a target price of Rs 701/- (~29% upside) in 18 months.

Key Share Data

Face Value (INR) 1.0

Equity Capital (INR Mn) 158.9

Market Cap (INR mn) 86462.3

52 Week High/Low (INR) 768/503

Avg. Daily Volume (BSE) 66,528

BSE Code 500233

NSE Code KAJARIACER

Reuters Code KAJR.NS

Bloomberg Code KJC:IN

Shareholding Pattern (Mar 31, 2018)

48%

9%

28%

15%

Promoters

DII

FII

Public & Others

Particulars FY17 FY18 FY19E FY20E

Net Sales 25,496.3 27,106.0 31,773.2 36,777.5

Growth (%) 5.6% 6.3% 17.2% 15.7%

EBITDA 4,963.3 4,563.5 5,465.0 6,546.4

PAT 2,528.4 2,349.5 3,001.5 3,712.4

Growth (%) 9.3% -7.1% 27.8% 23.7%

EPS (INR) 15.9 14.8 18.9 23.4

BVPS (INR) 73.9 85.0 96.7 110.4

Key Financials (INR Million)

Particulars FY17 FY18 FY19E FY20E

P/E (x) 34.2 36.8 28.8 23.3

P/BVPS (x) 7.4 6.4 5.6 4.9

Mcap/Sales (x) 3.4 3.2 2.7 2.4

EV/EBITDA (x) 17.7 19.1 16.0 13.2

ROCE (%) 30.8% 24.8% 26.4% 29.3%

ROE (%) 21.5% 17.4% 19.5% 21.2%

EBIDTA Mar (%) 19.5% 16.8% 17.2% 17.8%

PAT Mar (%) 9.9% 8.7% 9.4% 10.1%

Debt - Equity (x) 0.1 0.1 0.1 0.1

Source: Company, SKP Research

Key Financials Ratios

Price Performance Kajaria vs BSE 200

-30%

-20%

-10%

0%

10%

20%

May

-17

May

-17

Jun

-17

Jul-

17

Au

g-1

7

Au

g-1

7

Sep

-17

Oct

-17

Oct

-17

No

v-1

7

De

c-1

7

De

c-1

7

Jan

-18

Feb

-18

Feb

-18

Mar

-18

Ap

r-1

8

May

-18

Kajaria BSE 200

Analyst: Vineet Agrawal

Tel No: +91-22-49226006; Mobile: +91-9819510575

e-mail: [email protected]

Kajaria Ceramics Ltd.

SKP Securities Ltd www.skpmoneywise.com Page 2 of 8

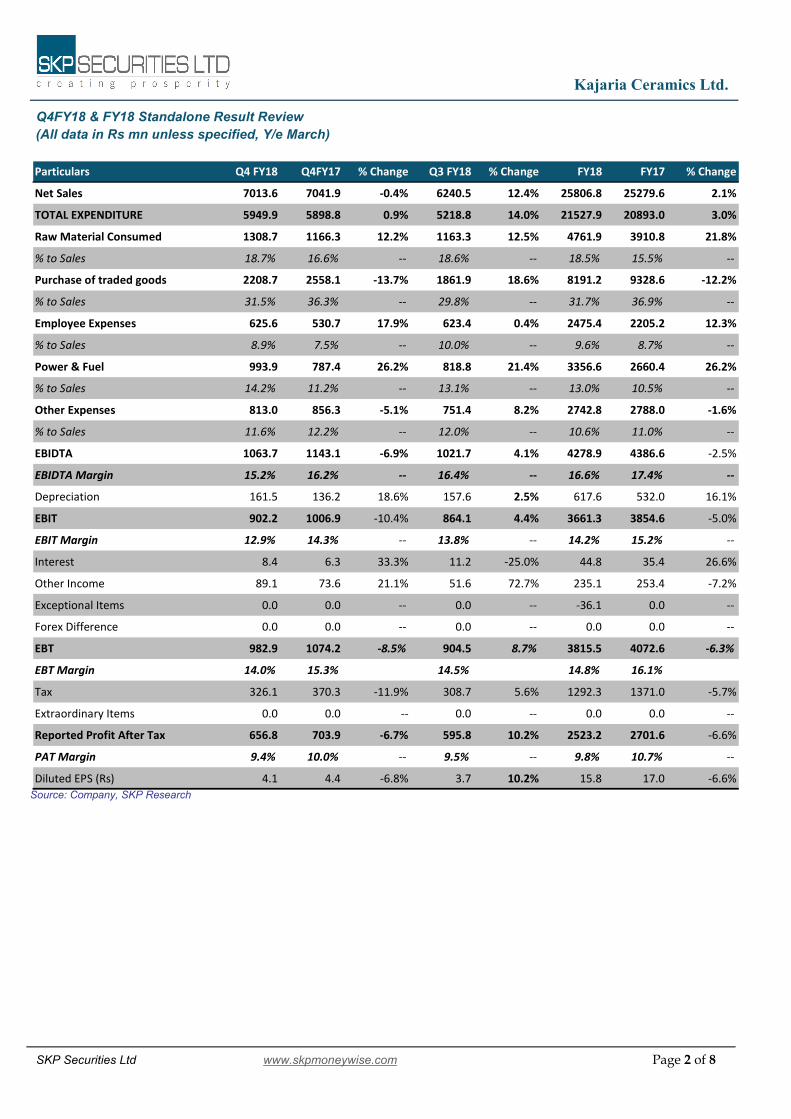

Q4FY18 & FY18 Standalone Result Review

(All data in Rs mn unless specified, Y/e March)

Source: Company, SKP Research

Particulars Q4 FY18 Q4FY17 % Change Q3 FY18 % Change FY18 FY17 % Change

Net Sales 7013.6 7041.9 -0.4% 6240.5 12.4% 25806.8 25279.6 2.1%

TOTAL EXPENDITURE 5949.9 5898.8 0.9% 5218.8 14.0% 21527.9 20893.0 3.0%

Raw Material Consumed 1308.7 1166.3 12.2% 1163.3 12.5% 4761.9 3910.8 21.8%

% to Sales 18.7% 16.6% -- 18.6% -- 18.5% 15.5% --

Purchase of traded goods 2208.7 2558.1 -13.7% 1861.9 18.6% 8191.2 9328.6 -12.2%

% to Sales 31.5% 36.3% -- 29.8% -- 31.7% 36.9% --

Employee Expenses 625.6 530.7 17.9% 623.4 0.4% 2475.4 2205.2 12.3%

% to Sales 8.9% 7.5% -- 10.0% -- 9.6% 8.7% --

Power & Fuel 993.9 787.4 26.2% 818.8 21.4% 3356.6 2660.4 26.2%

% to Sales 14.2% 11.2% -- 13.1% -- 13.0% 10.5% --

Other Expenses 813.0 856.3 -5.1% 751.4 8.2% 2742.8 2788.0 -1.6%

% to Sales 11.6% 12.2% -- 12.0% -- 10.6% 11.0% --

EBIDTA 1063.7 1143.1 -6.9% 1021.7 4.1% 4278.9 4386.6 -2.5%

EBIDTA Margin 15.2% 16.2% -- 16.4% -- 16.6% 17.4% --

Depreciation 161.5 136.2 18.6% 157.6 2.5% 617.6 532.0 16.1%

EBIT 902.2 1006.9 -10.4% 864.1 4.4% 3661.3 3854.6 -5.0%

EBIT Margin 12.9% 14.3% -- 13.8% -- 14.2% 15.2% --

Interest 8.4 6.3 33.3% 11.2 -25.0% 44.8 35.4 26.6%

Other Income 89.1 73.6 21.1% 51.6 72.7% 235.1 253.4 -7.2%

Exceptional Items 0.0 0.0 -- 0.0 -- -36.1 0.0 --

Forex Difference 0.0 0.0 -- 0.0 -- 0.0 0.0 --

EBT 982.9 1074.2 -8.5% 904.5 8.7% 3815.5 4072.6 -6.3%

EBT Margin 14.0% 15.3% 14.5% 14.8% 16.1%

Tax 326.1 370.3 -11.9% 308.7 5.6% 1292.3 1371.0 -5.7%

Extraordinary Items 0.0 0.0 -- 0.0 -- 0.0 0.0 --

Reported Profit After Tax 656.8 703.9 -6.7% 595.8 10.2% 2523.2 2701.6 -6.6%

PAT Margin 9.4% 10.0% -- 9.5% -- 9.8% 10.7% --

Diluted EPS (Rs) 4.1 4.4 -6.8% 3.7 10.2% 15.8 17.0 -6.6%

Kajaria Ceramics Ltd.

SKP Securities Ltd www.skpmoneywise.com Page 3 of 8

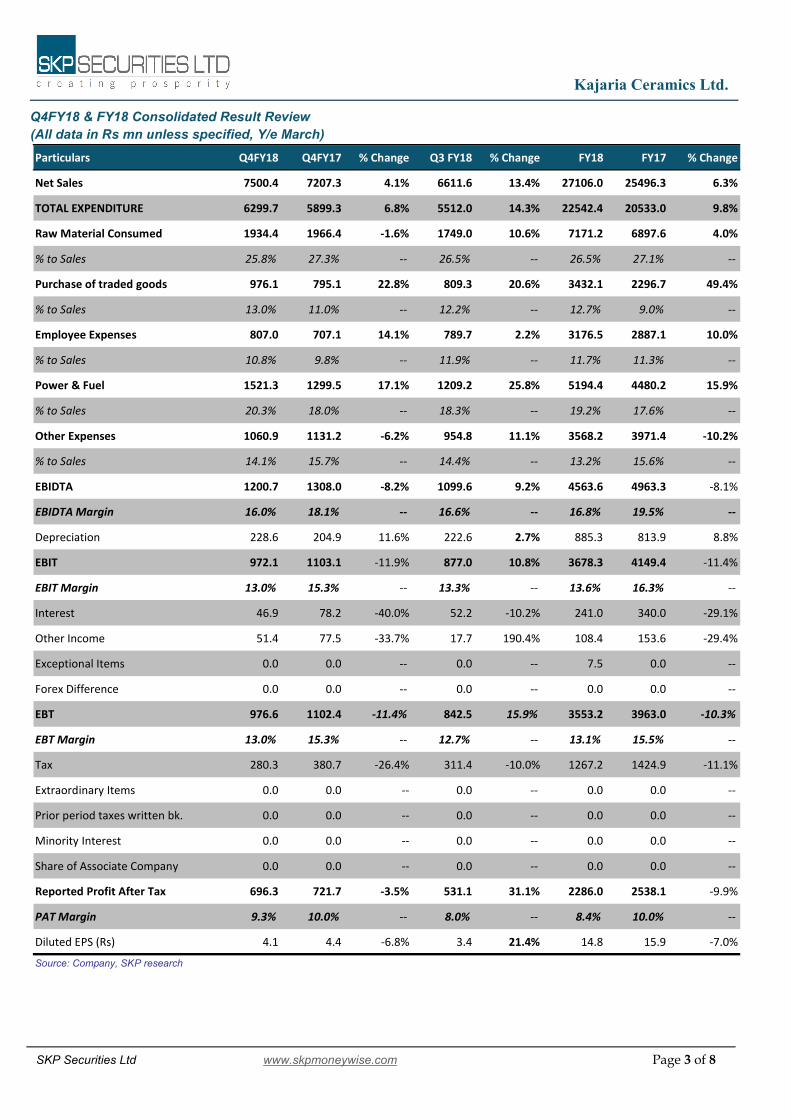

Q4FY18 & FY18 Consolidated Result Review

(All data in Rs mn unless specified, Y/e March)

Particulars Q4FY18 Q4FY17 % Change Q3 FY18 % Change FY18 FY17 % Change

Net Sales 7500.4 7207.3 4.1% 6611.6 13.4% 27106.0 25496.3 6.3%

TOTAL EXPENDITURE 6299.7 5899.3 6.8% 5512.0 14.3% 22542.4 20533.0 9.8%

Raw Material Consumed 1934.4 1966.4 -1.6% 1749.0 10.6% 7171.2 6897.6 4.0%

% to Sales 25.8% 27.3% -- 26.5% -- 26.5% 27.1% --

Purchase of traded goods 976.1 795.1 22.8% 809.3 20.6% 3432.1 2296.7 49.4%

% to Sales 13.0% 11.0% -- 12.2% -- 12.7% 9.0% --

Employee Expenses 807.0 707.1 14.1% 789.7 2.2% 3176.5 2887.1 10.0%

% to Sales 10.8% 9.8% -- 11.9% -- 11.7% 11.3% --

Power & Fuel 1521.3 1299.5 17.1% 1209.2 25.8% 5194.4 4480.2 15.9%

% to Sales 20.3% 18.0% -- 18.3% -- 19.2% 17.6% --

Other Expenses 1060.9 1131.2 -6.2% 954.8 11.1% 3568.2 3971.4 -10.2%

% to Sales 14.1% 15.7% -- 14.4% -- 13.2% 15.6% --

EBIDTA 1200.7 1308.0 -8.2% 1099.6 9.2% 4563.6 4963.3 -8.1%

EBIDTA Margin 16.0% 18.1% -- 16.6% -- 16.8% 19.5% --

Depreciation 228.6 204.9 11.6% 222.6 2.7% 885.3 813.9 8.8%

EBIT 972.1 1103.1 -11.9% 877.0 10.8% 3678.3 4149.4 -11.4%

EBIT Margin 13.0% 15.3% -- 13.3% -- 13.6% 16.3% --

Interest 46.9 78.2 -40.0% 52.2 -10.2% 241.0 340.0 -29.1%

Other Income 51.4 77.5 -33.7% 17.7 190.4% 108.4 153.6 -29.4%

Exceptional Items 0.0 0.0 -- 0.0 -- 7.5 0.0 --

Forex Difference 0.0 0.0 -- 0.0 -- 0.0 0.0 --

EBT 976.6 1102.4 -11.4% 842.5 15.9% 3553.2 3963.0 -10.3%

EBT Margin 13.0% 15.3% -- 12.7% -- 13.1% 15.5% --

Tax 280.3 380.7 -26.4% 311.4 -10.0% 1267.2 1424.9 -11.1%

Extraordinary Items 0.0 0.0 -- 0.0 -- 0.0 0.0 --

Prior period taxes written bk. 0.0 0.0 -- 0.0 -- 0.0 0.0 --

Minority Interest 0.0 0.0 -- 0.0 -- 0.0 0.0 --

Share of Associate Company 0.0 0.0 -- 0.0 -- 0.0 0.0 --

Reported Profit After Tax 696.3 721.7 -3.5% 531.1 31.1% 2286.0 2538.1 -9.9%

PAT Margin 9.3% 10.0% -- 8.0% -- 8.4% 10.0% --

Diluted EPS (Rs) 4.1 4.4 -6.8% 3.4 21.4% 14.8 15.9 -7.0%

Source: Company, SKP research

Kajaria Ceramics Ltd.

SKP Securities Ltd www.skpmoneywise.com Page 4 of 8

Chart 1: Operating Revenues Chart 2: Volume wise tiles Sales (MSM)

Chart 3: Volume Wise Revenue Contribution Chart 4: Value wise tiles sales

Chart 5: Value wise Revenue Contribution Chart 6: EBIDTA & EBIDTAT Margins

Chart 7: PAT & PAT Margin Chart 8: Debt & D/E

Source: SKP Research Desk

13

13

0.3

15

83

2.8

18

36

3.1

21

86

8.9

24

13

4.5

25

49

6.3

27

10

6.0

31

77

3.2

36

77

7.5

0

5000

10000

15000

20000

25000

30000

35000

40000

FY12 FY13 FY14 FY15 FY16 FY17 FY18 FY19E FY20E

Ove

rall

Ne

t R

eve

nu

es

(Rs

mn

)

26.9 27.1 27.6 29.3 32.7 37.4 39.8 43.2 46.52.3

8.214.2

18.524.8

22.2 18.8

26.631.8

10.610.3

10.311.0

7.6 8.1 13.4

11.0

12.0

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

90.0

100.0

FY12 FY13 FY14 FY15 FY16 FY17 FY18 FY19E FY20E

Tiles - Outsourced Tiles - JV Tiles-Own Mfg

68%59%

53% 50% 50% 55% 55% 53% 52%

6% 18% 27% 31%38% 33%

26% 33% 35%

27% 23% 20% 19%12% 12%

19% 14% 13%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

FY12 FY13 FY14 FY15 FY16 FY17 FY18 FY19E FY20E

Outsourced (%) JV (%) Owned Mfg (%)

7.9 8.9 9.5 10.8 11.9 13.7 15.3 17.0 18.80.6

2.94.8

6.89.0

8.1 6.6

9.6

11.8

4.6

4.44.0

4.22.5 2.6 3.8

3.2

3.6

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

FY12 FY13 FY14 FY15 FY16 FY17 FY18 FY19E FY20E

Tiles - Outsourced Tiles - JV Tiles-Own Mfg

60% 55% 52% 50% 51% 56% 59% 57% 55%

5% 18% 27% 31%38% 33% 26% 32% 34%

35%27% 22% 19%

11% 11% 15% 11% 11%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

FY12 FY13 FY14 FY15 FY16 FY17 FY18 FY19E FY20E

Outsourced (%) JV (%) Owned Mfg (%)

80

8.9

10

45

.1

12

42

.2

17

56

.0

23

13

.3

25

28

.4

23

49

.5

30

01

.5

37

12

.4

6.2%6.6% 6.8%

8.0%

9.6% 9.9%

8.7%

9.4%10.1%

0%

2%

4%

6%

8%

10%

12%

0

500

1000

1500

2000

2500

3000

3500

4000

FY12 FY13 FY14 FY15 FY16 FY17 FY18 FY19E FY20E

PA

T M

argi

n (

%)

PA

T (R

s m

n)

20

62

.0

24

46

.5

28

51

.2

35

41

.3

45

74

.6

49

63

.3

45

63

.5

54

65

.0

65

46

.415.7%15.5% 15.5%

16.2%

19.0%19.5%

16.8%17.2%

17.8%

12%

13%

14%

15%

16%

17%

18%

19%

20%

0

1000

2000

3000

4000

5000

6000

7000

FY12 FY13 FY14 FY15 FY16 FY17 FY18 FY19E FY20EEB

IDTA

Mar

gin

(%

)

EB

IDT

A (

Rs m

n)

10

16

.36

91

6.7

5

89

2.6

9

85

1.3

0

96

4.0

0

14

21

.10

11

55

.00

75

6.7

0

11

25

.00

52

5.0

010

66

.83

11

43

.28

17

35

.06

10

86

.80

12

56

.30

11

04

.90

55

0.8

0

59

4.2

0

69

4.2

0

89

4.2

0

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1.0

0

200

400

600

800

1000

1200

1400

1600

1800

2000

FY1

1

FY1

2

FY1

3

FY1

4

FY1

5

FY1

6

FY1

7

FY1

8

FY1

9E

FY2

0E

x

Rs

mn

Long Term Debt (LHS) Short Term Debt (LHS) D/E (RHS)

Kajaria Ceramics Ltd.

SKP Securities Ltd www.skpmoneywise.com Page 5 of 8

KEY CONCERNS

1. Increase in fuel prices: Increase in gas prices, a key input in this energy intensive industry, poses a threat to business in terms of increase in operating cost. To mitigate this, the Company has increased the proportion of value added tiles in the sales mix. Kajaria has also implemented numerous small and critical process improvements, which optimized consumption of gas, eliminating wastage.

.

2. Extended slowdown in real estate sector may dampen business sentiments: Kajaria’s tiles and sanitaryware segment is highly dependent on real estate sector. Any extension of slowdown to Tier – II and Tier –III cities may dampen business prospects of Kajaria.

3. Forex Risk: The Company faces foreign exchange risks due to its imports and exports. Any adverse currency fluctuation may pose threat to the profitability of Kajaria.

VALUATION

Better economic growth, leaving more disposable income for discretionary life style consumption,

rapid urbanisation, changing customer preference towards quality branded products particularly amongst the growing mass affluent, increasing nuclear families and Governments’ thrust on “Housing for All” coupled with strong brand equity and recall and distribution network, augers well for the company. It has de-risked its growth strategy with an asset light business model, adopting a joint venture route.

We have valued the stock on the basis of P/E - method of relative valuation - of 30x of FY20E earnings. In view of the sharp correction in the share price to Rs 544 now, after a stupendous rally to a 52 week high of Rs 768 recently, we recommend a BUY on the stock with a target price of Rs 701/- (~29% upside) in 18 months.

EBIDTA: One year forward looking P/E band

Source: SKP Research

0.0

100.0

200.0

300.0

400.0

500.0

600.0

700.0

800.0

900.0

Ap

r-0

8

Oct

-08

Ap

r-0

9

Oct

-09

Ap

r-1

0

Oct

-10

Ap

r-1

1

Oct

-11

Ap

r-1

2

Oct

-12

Ap

r-1

3

Oct

-13

Ap

r-1

4

Oct

-14

Ap

r-1

5

Oct

-15

Ap

r-1

6

Oct

-16

Ap

r-1

7

Oct

-17

Ap

r-1

8

Adjusted Price 9 18 27 36 45 54

Kajaria Ceramics Ltd.

SKP Securities Ltd www.skpmoneywise.com Page 6 of 8

Consolidated Financials

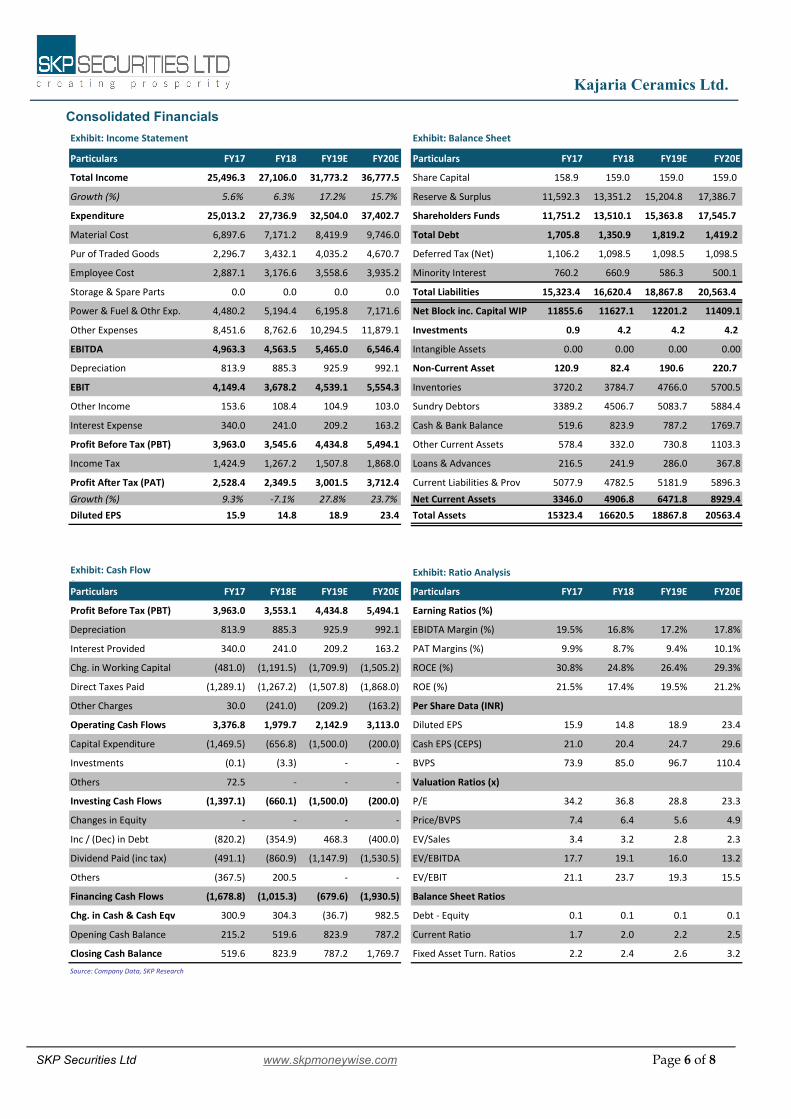

Exhibit: Income Statement Exhibit: Balance Sheet

Particulars FY17 FY18 FY19E FY20E Particulars FY17 FY18 FY19E FY20E

Total Income 25,496.3 27,106.0 31,773.2 36,777.5 Share Capital 158.9 159.0 159.0 159.0

Growth (%) 5.6% 6.3% 17.2% 15.7% Reserve & Surplus 11,592.3 13,351.2 15,204.8 17,386.7

Expenditure 25,013.2 27,736.9 32,504.0 37,402.7 Shareholders Funds 11,751.2 13,510.1 15,363.8 17,545.7

Material Cost 6,897.6 7,171.2 8,419.9 9,746.0 Total Debt 1,705.8 1,350.9 1,819.2 1,419.2

Pur of Traded Goods 2,296.7 3,432.1 4,035.2 4,670.7 Deferred Tax (Net) 1,106.2 1,098.5 1,098.5 1,098.5

Employee Cost 2,887.1 3,176.6 3,558.6 3,935.2 Minority Interest 760.2 660.9 586.3 500.1

Storage & Spare Parts 0.0 0.0 0.0 0.0 Total Liabilities 15,323.4 16,620.4 18,867.8 20,563.4

Power & Fuel & Othr Exp. 4,480.2 5,194.4 6,195.8 7,171.6 Net Block inc. Capital WIP 11855.6 11627.1 12201.2 11409.1

Other Expenses 8,451.6 8,762.6 10,294.5 11,879.1 Investments 0.9 4.2 4.2 4.2

EBITDA 4,963.3 4,563.5 5,465.0 6,546.4 Intangible Assets 0.00 0.00 0.00 0.00

Depreciation 813.9 885.3 925.9 992.1 Non-Current Asset 120.9 82.4 190.6 220.7

EBIT 4,149.4 3,678.2 4,539.1 5,554.3 Inventories 3720.2 3784.7 4766.0 5700.5

Other Income 153.6 108.4 104.9 103.0 Sundry Debtors 3389.2 4506.7 5083.7 5884.4

Interest Expense 340.0 241.0 209.2 163.2 Cash & Bank Balance 519.6 823.9 787.2 1769.7

Profit Before Tax (PBT) 3,963.0 3,545.6 4,434.8 5,494.1 Other Current Assets 578.4 332.0 730.8 1103.3

Income Tax 1,424.9 1,267.2 1,507.8 1,868.0 Loans & Advances 216.5 241.9 286.0 367.8

Profit After Tax (PAT) 2,528.4 2,349.5 3,001.5 3,712.4 Current Liabilities & Prov 5077.9 4782.5 5181.9 5896.3

Growth (%) 9.3% -7.1% 27.8% 23.7% Net Current Assets 3346.0 4906.8 6471.8 8929.4

Diluted EPS 15.9 14.8 18.9 23.4 Total Assets 15323.4 16620.5 18867.8 20563.4

Exhibit: Cash Flow

StatementExhibit: Ratio Analysis

Particulars FY17 FY18E FY19E FY20E Particulars FY17 FY18 FY19E FY20E

Profit Before Tax (PBT) 3,963.0 3,553.1 4,434.8 5,494.1 Earning Ratios (%)

Depreciation 813.9 885.3 925.9 992.1 EBIDTA Margin (%) 19.5% 16.8% 17.2% 17.8%

Interest Provided 340.0 241.0 209.2 163.2 PAT Margins (%) 9.9% 8.7% 9.4% 10.1%

Chg. in Working Capital (481.0) (1,191.5) (1,709.9) (1,505.2) ROCE (%) 30.8% 24.8% 26.4% 29.3%

Direct Taxes Paid (1,289.1) (1,267.2) (1,507.8) (1,868.0) ROE (%) 21.5% 17.4% 19.5% 21.2%

Other Charges 30.0 (241.0) (209.2) (163.2) Per Share Data (INR)

Operating Cash Flows 3,376.8 1,979.7 2,142.9 3,113.0 Diluted EPS 15.9 14.8 18.9 23.4

Capital Expenditure (1,469.5) (656.8) (1,500.0) (200.0) Cash EPS (CEPS) 21.0 20.4 24.7 29.6

Investments (0.1) (3.3) - - BVPS 73.9 85.0 96.7 110.4

Others 72.5 - - - Valuation Ratios (x)

Investing Cash Flows (1,397.1) (660.1) (1,500.0) (200.0) P/E 34.2 36.8 28.8 23.3

Changes in Equity - - - - Price/BVPS 7.4 6.4 5.6 4.9

Inc / (Dec) in Debt (820.2) (354.9) 468.3 (400.0) EV/Sales 3.4 3.2 2.8 2.3

Dividend Paid (inc tax) (491.1) (860.9) (1,147.9) (1,530.5) EV/EBITDA 17.7 19.1 16.0 13.2

Others (367.5) 200.5 - - EV/EBIT 21.1 23.7 19.3 15.5

Financing Cash Flows (1,678.8) (1,015.3) (679.6) (1,930.5) Balance Sheet Ratios

Chg. in Cash & Cash Eqv 300.9 304.3 (36.7) 982.5 Debt - Equity 0.1 0.1 0.1 0.1

Opening Cash Balance 215.2 519.6 823.9 787.2 Current Ratio 1.7 2.0 2.2 2.5

Closing Cash Balance 519.6 823.9 787.2 1,769.7 Fixed Asset Turn. Ratios 2.2 2.4 2.6 3.2

Source: Company Data, SKP Research

Kajaria Ceramics Ltd.

SKP Securities Ltd www.skpmoneywise.com Page 7 of 8

Note:

The above analysis and data are based on last available prices and not official closing rates. SKP Research is also available on Bloomberg and Thomson First Call.

DISCLAIMER:

This document has been prepared by SKP Securities Ltd, hereinafter referred to as SKP to provide information about the company(ies)/sector(s), if any, covered in the report and may be distributed by it and/or its affiliates. SKP Securities Ltd., offers broking and depository participant services and is regulated by Securities and Exchange Board of India (SEBI). It also distributes investment products/services like mutual funds, alternative investment funds, bonds, IPOs, etc., renders corporate advisory services and invests its own funds in securities and investment products. We declare that no material disciplinary action has been taken against SKP by any regulatory authority impacting Equity Research Analysis. As a value addition to its clients, it offers its research services and reports in various formats to its clients and prospects. As such, SKP is making these disclosures under SEBI (Research Analysts) Regulations, 2014.

Terms & Conditions and Other Disclosures:

This research report (“Report”) is for the personal information of the selected recipient(s), does not construe to be any investment, legal or taxation advice, is not for public distribution and should not be copied, reproduced or redistributed to any other person or in any form without SKP’s prior permission. The information provided in the Report is from publicly available data, which we believe, are reliable. While reasonable endeavours have been made to present reliable data in the Report so far as it relates to current and historical information, but SKP does not guarantee the accuracy or completeness of the data in the Report. Accordingly, SKP or its promoters, directors, subsidiaries, associates or employees shall not be in any way responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained and views and opinions expressed in this publication. Past performance mentioned in the Report should not be taken as an indication or guarantee of future performance, and no representation or warranty, express or implied, is made regarding future performance. Information, opinions and estimates contained in this report reflect a judgment of its original date of publication by SKP and are subject to change without notice. The price, value of and income from any of the securities mentioned in this report can rise or fall. The Report includes analysis and views of individual research analysts (which, hereinafter, includes persons reporting to them) covering this Report. The Report is purely for information purposes. Opinions expressed in the Report are SKP’s or its research analysts’ current opinions as of the date of the Report and may be subject to change from time to time without notice. SKP or any person connected with it does not accept any liability arising from the use of this document. Investors should not solely rely on the information contained in this Report and must make investment decisions based on their own investment objectives, judgment, risk profile and financial position. The recipients of this Report may take professional advice before acting on this information. SKP, along with its affiliates, are engaged in various financial services and so might have financial, businesses or other interest in other entities, including the subject company or its affiliates mentioned in this report, for which it might have received any compensation in the past twelve months. SKP does not provide any merchant banking or market making service and does not manage public offers. However, SKP encourages independence in preparation of research reports and strives to minimize conflict in preparation of research reports. SKP and its analysts did not receive any compensation or other benefits from the subject company mentioned in the Report or from a third party in connection with preparation of the Report. Accordingly, SKP and its Research Analyst do not have any material conflict of interest at the time of publication of this Report. SKP’s research analysts may provide

Exhibit: Recommendation -History Table Exhibit: Recommendation -History Chart

03-Nov-15 ACCUMULTE 442 466 6% --

28-Jan-16 BUY 477 589 23% 18

03-May-16 ACCUMULTE 531 565 6% --

09-Aug-16 ACCUMULTE 618 677 10% --

24-Oct-16 HOLD 617 646 5% --

27-Jan-17 BUY 582 703 21% 18

24-May-17 ACCUMULTE 667 734 10% --

17-Aug-17 ACCUMULTE 626 687 10% --

06-Nov-17 NEUTRAL 695 -- -- --

09-Feb-18 BUY 615 750 22% 18

16-May-18 BUY 543 701 29% 18

Source: SKP Research; Price adjusted for stock split Source: BSE, SKP Research; Price adjusted for stock split

Period (months)

Date RatingAdj Issue

PriceAdj Target

PriceUpside

Potential

300

350

400

450

500

550

600

650

700

750

800

03-

No

v-1

5

03-

Jan

-16

03-

Mar

-16

03

-May

-16

03

-Ju

l-1

6

03

-Sep

-16

03-

No

v-1

6

03-

Jan

-17

03-

Mar

-17

03

-May

-17

03

-Ju

l-1

7

03

-Sep

-17

03-

No

v-1

7

03-

Jan

-18

03-

Mar

-18

03

-May

-18

Adj Close Price Adj Target Price

Kajaria Ceramics Ltd.

SKP Securities Ltd www.skpmoneywise.com Page 8 of 8

input into its other business activities. Investors should assume that SKP and/or its affiliates are seeking or will seek business assignments from the company(ies) that are the subject of this material and that the research analysts who are involved in preparing this material may educate investors on investments in such businesses. The research analysts responsible for the preparation of this document may interact with trading desk/sales personnel and other parties for the purpose of gathering, applying and interpreting information. Our research analysts are paid on the profitability of SKP, which may include earnings from business activities for which this Report is being used, but not for the preparation of this report. SKP generally prohibits its analysts, persons reporting to analysts and their relatives from maintaining a financial interest in the securities or derivatives of any company(ies) that the analyst covers. Additionally, SKP generally, prohibits its analysts and persons reporting to analysts from serving as an officer, director or advisory board member of any companies that the analyst cover. The following Disclosure of Interest Statement, clarifies it further: SKP and/or its Directors/or its affiliates or its Research Analyst(s) engaged in preparation of this Report or his/her relative (i) do not own 1% or more of the equity securities of the subject company mentioned in the report as of the last day of the month preceding the publication of the research report (ii) do not have any financial interests in the subject company mentioned in this report (iii) do not have any other material conflict of interest at the time of publication of the research report. The distribution of this document in other jurisdictions may be strictly restricted and/ or prohibited by law, and persons into whose possession this document comes should inform themselves about such restriction and/ or prohibition, and observe any such restrictions and/ or prohibition. The Promoter & Managing Director of SKP is an Independent Director on the Board of Directors of Linc Pen & Plastics Ltd.

SKP Securities Limited is registered as a Research Analyst under SEBI (Research Analyst) Regulations, 2014 having registration no. INH300002902.

Analyst Certification

The views expressed in this research report accurately reflect the personal views of the analyst about the subject securities or issues, which are subject to change without prior notice and does not represent to be an authority on the subject. No part of the compensation of the research analyst was, is, or will be directly or indirectly related to the specific recommendations and views expressed by research analyst in this report. The research analysts, strategists, or research associates principally responsible for preparation of SKP research receive compensation based upon various factors, including quality of research, investor client feedback, stock picking, competitive factors and firm revenues.

Disclosure of Interest Statement

Analyst ownership of the stock NIL

Served as an officer, director or employee NIL

SKP Securities Ltd

Contacts Research Sales

Mumbai Kolkata Mumbai Kolkata

Phone 022 4922 6006 033 4007 7000 022 4922 6000 033 4007 7400

Fax 022 4922 6066 033 4007 7007 022 4922 6066 033 4007 7007

E-mail [email protected] [email protected] [email protected]

Member: NSE BSE NSDL CDSL

INB/INF: 230707532, NSECDS – NSE230707532, BSE INB: 010707538, CDSL DPID: 021800, IN-DP-155-2015, NSDL DP ID: IN302646, IN-DP-NSDL: 222-2001, ARN: 0006

Institutional & Retail Broking Wealth Advisory & Distribution Investment Banking