Just-In-Time Cost Accounting System and Social … 1...Just-In-Time Cost Accounting System and...

13

© 2014 Research Academy of Social Sciences http://www.rassweb.com 116 Journal of Empirical Economics Vol. 2, No. 3, 2014, 116-128 Just-In-Time Cost Accounting System and Social Economic Factors Affecting Its Adoption by Nigerian Firms Emmanuel Amaps Loveday Ibanichuka 1 , Oyadonghan Kereotu James 2 Abstract Just in time costing in inventory, purchase and production and accounting for such transactions are considered to be much better for record keeping and financial information disclosure as compared with the traditional method of accounting for stock keeping. The advantages in most times seems to be unknown by firms in the developing world. A critical review of various literatures shows that most managers of manufacturing firms known. This gives rise to the desire of the researchers to find out the factors affecting its adoption in developing countries like Nigeria and others. To achieve this objective, the researchers used a well structured questionnaire to collect primary data from top management staff of selected manufacturing firms that are equally quoted in the Nigerian Stock market. The data generated was analysed with simple regression statistical tool, using E-View soft ware version3.1. The findings revealed that level of technological advancement, culture, management commitment, awareness and other factors are responsible for its adoption. Therefore, the researchers recommended that effective training programmes for managers and staff should be regularly organised. Also Government should engage in more infrastructural development activities and provide a high capital allowance for firms for adopting just-in-time system of accounting and production. Key Words: Just-in-time, Accounting, Cost, System, Factors and Nigeria. 1. Introduction Just-in-time as the name implies is to produce goods just-in-time for sale or use. According to Omoregie, (2002) Just-in-time manufacturing is best described as a philosophy of management dedicated to the elimination of waste. It’s intended to avoid situations in which inventory exceeds demand which places increased burden on business to manage such extra inventory. Colin (2008) identified two cardinal objectives of just-in-time which are, Elimination of all activities that do not add value to a product or service. The emphasis is on simplification and increased visibility to identify activities that do not add value to a product. Similar to this is Akbar et al (2013), view that Just-in-Time objective is to reduce the amount tied up in inventories of raw materials and finished goods. Just-in-time system had its origin in Japan in the 1970s. It was introduced by Taichi Ohno, vice president of Toyota manufacturing cooperation. Japan after World War II had a devastating economy which affected their manufacturing sector? Enormous defects, such as rising cost of production, production delays existed in their manufacturing sector. Most of the Japanese manufacturers wanted to develop a good manufacturing technique aimed at revamping their manufacturing sector and developing the economy. They also wanted to gain the most efficient use of their limited resources as well as meeting customers demand (Colin, 2008)), (Ohno 1997). Ohno and his associate started by examining the American Industry involve in the production of cars and found out that it was based on the traditional idea where several parts in assembling a car are being 1 Department Of Accounting, Faculty Of Management Sciences, University Of Port-Harcourt, Port-Harcourt 2 Department Of Accounting And Finance Niger Delta University, Wilberforce Island, Pmb 071, Yenagoa, Bayelsa State,Nigeria

Transcript of Just-In-Time Cost Accounting System and Social … 1...Just-In-Time Cost Accounting System and...

© 2014 Research Academy of Social Sciences

http://www.rassweb.com 116

Journal of Empirical Economics

Vol. 2, No. 3, 2014, 116-128

Just-In-Time Cost Accounting System and Social Economic Factors

Affecting Its Adoption by Nigerian Firms

Emmanuel Amaps Loveday Ibanichuka1, Oyadonghan Kereotu James

2

Abstract

Just in time costing in inventory, purchase and production and accounting for such transactions are

considered to be much better for record keeping and financial information disclosure as compared with the

traditional method of accounting for stock keeping. The advantages in most times seems to be unknown by

firms in the developing world. A critical review of various literatures shows that most managers of

manufacturing firms known. This gives rise to the desire of the researchers to find out the factors affecting its

adoption in developing countries like Nigeria and others. To achieve this objective, the researchers used a

well structured questionnaire to collect primary data from top management staff of selected manufacturing

firms that are equally quoted in the Nigerian Stock market. The data generated was analysed with simple

regression statistical tool, using E-View soft ware version3.1. The findings revealed that level of

technological advancement, culture, management commitment, awareness and other factors are responsible

for its adoption. Therefore, the researchers recommended that effective training programmes for managers

and staff should be regularly organised. Also Government should engage in more infrastructural

development activities and provide a high capital allowance for firms for adopting just-in-time system of

accounting and production.

Key Words: Just-in-time, Accounting, Cost, System, Factors and Nigeria.

1. Introduction

Just-in-time as the name implies is to produce goods just-in-time for sale or use. According to

Omoregie, (2002) Just-in-time manufacturing is best described as a philosophy of management dedicated to

the elimination of waste. It’s intended to avoid situations in which inventory exceeds demand which places

increased burden on business to manage such extra inventory. Colin (2008) identified two cardinal objectives

of just-in-time which are, Elimination of all activities that do not add value to a product or service. The

emphasis is on simplification and increased visibility to identify activities that do not add value to a product.

Similar to this is Akbar et al (2013), view that Just-in-Time objective is to reduce the amount tied up in

inventories of raw materials and finished goods.

Just-in-time system had its origin in Japan in the 1970s. It was introduced by Taichi Ohno, vice

president of Toyota manufacturing cooperation. Japan after World War II had a devastating economy which

affected their manufacturing sector? Enormous defects, such as rising cost of production, production delays

existed in their manufacturing sector. Most of the Japanese manufacturers wanted to develop a good

manufacturing technique aimed at revamping their manufacturing sector and developing the economy. They

also wanted to gain the most efficient use of their limited resources as well as meeting customers demand

(Colin, 2008)), (Ohno 1997).

Ohno and his associate started by examining the American Industry involve in the production of cars

and found out that it was based on the traditional idea where several parts in assembling a car are being

1Department Of Accounting, Faculty Of Management Sciences, University Of Port-Harcourt, Port-Harcourt

2Department Of Accounting And Finance Niger Delta University, Wilberforce Island, Pmb 071, Yenagoa, Bayelsa

State,Nigeria

Journal of Empirical Economics

117

stored till demand is made. For Ohno adopting such idea in Japan would not be effective due to low demand

for products. Research however have it that Ohno examined the American supermarket which practiced the

Kanban (pull) system. In this system, inventory level is aligned with actual consumption that is, super

markets stock only what it expects to sell within a given time frame and customers obtain the required

component. Also a signal is sent to produce and deliver new shipment when stock is completely consumed

which in turn causes the store to restock.

Ohno applied this idea by devising a system based on the elimination of waste, producing more than

what is needed is termed as waste hence production should be based on quantity demanded by customers.

This led to the emergence of just-in-time system. This concept spread throughout Japanese industries. From

Japan, it spread to other industrialized nations including England, Germany and Canada. Companies such as

General Motor, Wresting Honk, Ford Motor Company, Hodges Aircraft, Dell Computer have employed just-

in-time system with great success (Ray et al, 2003).

Adoption of just-in-time system results in efficient and effective management of inventory material. It

contrasts with the traditional system where manufacturers simply produced and store many goods as possible

which often results to higher cost in storing, obsolescence cost etc. Companies that have implemented this

system claimed to have substantially reduced their investment on storage of raw materials and work-in-

process inventory. It has also helped in accurate valuation of stock for financial statements (McDonough,

2013). Seeing the advantages of just-in-time costing should ordinarily impel manufacturing firms to

implement it. However most manufacturing firms still make use of the traditional manufacturing system

which often leads to increase cost in inventory management, occurrence of obsolescence cost and wastages

due to impairment of assets. The problem therefore is the inability of such companies to properly evaluate

asset or stock impairment as well as accounting for them as stipulated in IFRS 2 and 36, in the financial

statement thereby resulting in wrong asset valuation and misrepresentation of financial statements in

published accounts.

However, factors such as organizational culture, lack of awareness, supplier’s factors, technology, lack

of resources are seen as possible hindrances to just-in-time costing and production system implementation in

most manufacturing firms. This research therefore focuses on the importance of just-in-time in relation to

accurate valuation of stock as well as to determine the effect of just-in-time costing system on financial

statement representation, and investigate the relationship between the social and economic factors and the

implementation of just-in-time costing system in manufacturing firms in Nigeria.

2. Theoretical Framework and Literature Review

Today, just-in-time has evolved into an effective inventory management system encompassing a body of

knowledge and set of manufacturing principles and techniques. Most literature has indicated that its ideas

come from different disciplines, (Omoregie, 2002) including production management, industrial engineering,

economics etc. Manufacturers operating just-in-time, purchase only those materials required to meet daily

production needs. After production, goods are shipped immediately to customers thus eliminating work in

process and goods sitting idle at the end of each day, McDonough (2013). This is in line with the market

equilibrium theory which states that quantity demanded equals quantity supplied. Colin (2008) stated that

when supply and demand are equal, it is said to be at equilibrium and at this point the allocation of goods is

at its most efficient use because the amount of goods demanded is same with the amount of goods supplied.

Just-in-time is thus based on this concept.

It applies primarily to repetitive manufacturing process in which the same products are produced over

and over again. For McDonough (2013). just in time is a cluster of lean manufacturing system designed to

manufacture products to meet customers demand. It however goes hand in hand with concepts such as total

quality management; continuous improvement etc. Colin (2008) sited that total quality management boast

significant cost reduction, eliminating duplication of work in process and optimal operation. For Colin

E. A. L. Ibanichuka & O. K. James

118

(2008) companies operating just-in-time must develop total quantity management. The goal is to ensure

smooth production and prevention of defect materials from suppliers.

Nature of Just-In-Time

Just-in-time is seen as an inventory control system aimed at minimizing on hand inventory and

increasing inventory returns. Implementing a just-in-time system is a mechanism for reducing non value

added cost and long run cost in manufacturing (Akbar et al 2013). Waste from producing more than what is

needed and keeping stock may also be avoided. According to McDonough (2013) just-in-time aims at

producing the right part at the right time only when they are needed and at the quantity needed. For Roger et

al (1998), production does not begin on an item until order is received from customers with just-in-time

system. Adeniyi (2012) identified the aim of just-in-time system as follows:

Zero inventory

Elimination of non value adding activities.

Zero defects

100% on time delivery service.

Demand pull manufacturing

When applied to purchase, just-in-time tend to match the usage of material according to customers

demand. Implementation of just-in-time purchase techniques reduces investment in raw materials and work-

in-process stock. It also save factory space, generate quantity large discounts, savings in time from

negotiating with fewer supplier (ICAN 2012). Just-in-time is an attempt to change the manufacturing process

by eliminating non value added activities in production in order to avoid high inventory cost.

Plant Layout

Just-in-time is totally pulled oriented. The pull system of production is where materials are pulled by

next level of production only when is signaled or required by the next stage of production. McDonough

(2013), asserted that just-in-time is a production system which is driven by demand for finished products

where by each component on a production line is produced only when needed. Just-in-time requires a

production layout with continuous flow, one without delay once production starts (Akbar et al 2013). All

machines used at different stages are located in close proximity to each other in order to ensure smooth and

rapid production without delay. This allows workers to focus all of their effort from start to finish during

production process without interruption and also to provide high quality products at the required time. This

differs from the traditional push system. The push system of production pushes materials to the next stage of

production irrespective of whether time and resources are needed at the next level of production thus creating

lots of inventories at each level of production floor (Akbar et al 2013). Companies operating traditional

system design their plant floor such that similar machines are grouped together (Ray et al 2003). This

approach of plant layout requires that product move from a group of machines to another frequently across

plant in the process of production. This had resulted in extensive material handling cost, delay in production

and sometimes damage in work-in-process inventory which move frequently over long distances during

production process.

Though just-in-time aims at minimizing on hand inventory, a side effect of having fever inventories in

the factory is risk to coordinate production much better in order to avoid inventory short fall. However,

factors in ensuring successful operation of just-in-time manufacturing include the following:-

Improving plant layout through pull method of coordinating production.

Creating lasting relationship with reliable suppliers.

Management and employee commitment.

Reduction in set up time in production.( Adeniyi 2012)

Journal of Empirical Economics

119

Just-In-Time Accounting

Just-in-time is a simplified costing method used in manufacturing firms. Adopting just-in-time results in

substantial reduction of inventories thus making inventory valuation less relevant. One of the reasons for

assigning cost on products as it passes through production process is to know the value of work-in-process

inventories at the end of an accounting period (Nurus et al, 2012) ). With just-in-time system, accountants do

not have to compute the work-in-process inventory since there are no such inventories. This simplifies record

keeping and also saves time.

Similarly, the use of just-in-time has resulted in narrowing the difference in unit cost between Fifo and

weighted average method (Ray et al 2003). The distinction between fifo and weighted average method

centers on how cost is handled in work in process inventories. In just-in-time system, work-in-process

inventories is either eliminated or reduced to minimal level. The elimination of these inventories totally

eliminates the difference between the two costing method thus leaving the unit cost of both method

equivalent. According to Charles (2005) just-in-time wait until the units are completed to record cost of

production. Detailed tracking of cost is eliminated as production cost is calculated once goods are produced.

It however follows the back flushing system.

Back flushing is a product costing method whereby accountants delay costing and journal entries until

products are produced (Akbar et al 2013)). Cost transactions such as accounts for raw materials, during

work-in-process may be eliminated. Journal entries to inventory account may also be delayed until the time

production is completion or even the time of sale. According to Nurus et al (2012)). Back flush costing aims

to eliminate detailed accounting transactions. For him, rather than tracking the movement of material through

the production process, a black flush costing system focuses first on the output of an organization and then

works backward when allocating cost between cost of goods sold and inventory with no separate account for

work-in-process. Both materials and work-in-process inventory are combined into Raw and In Process (RIP)

account. The overhead accounts are replaced by a single account known as conversion account. The other

accounts Include the cost of goods sold and finished goods account. It does not maintain separate account for

work-in-process inventory (Adeniyi 2012). Cost is usually charged backward after production. The concept,

economic order quantity (EOQ) helps in determining the economic production at the long-run. Just-in-time in

relation to EOQ strives to push down all cost on continual basis. Through reduction in ordering cost a firm is

able to reduce its total cost.

McDonough .(2013), stated that economic order quantity method is used to determine what level would

be economical for just-in-time operation. However Fanzine (1997) in his mathematical model compared the

economic order quantity with just-in-time purchasing order. For him, it is better to choose just-in-time over

EOQ because it results in reduction in purchase price, holding and ordering cost. The concept of just-in-time

costing system offer many benefits to manufacturing firms: They include:-

Reduction in risk that most of the output cannot be sold.

Reduction in unit cost of items through elimination of non-value adding activities.

Inventory exceeding demand may be avoided.

Investment of funds in other business opportunity resulting from funds tied up in inventory.

Better customer satisfaction through production of high quality products.

Enhancement of better competitive environment.

Traditional Versus Just-In-Time System

Management of inventory is usually a difficult task carried out by management in manufacturing

industries. Traditionally, manufacturers keep large inventories of raw materials, work-in-process as well as

finished goods in order to meet customers demand and also to ensure smooth operation of business.

According to Ray (1994), the reason for excessive inventory is usually attributed to the following:-

E. A. L. Ibanichuka & O. K. James

120

To guard against being out of stock.

Prevention of errors made in production resulting in stock piles of raw materials or finished

goods.

Production in large batches with the believe that, large batches are more economical to

produce than small batches.

While these inventories act as buffers against unforeseen circumstances, they however incur higher cost.

Experts argue that the presence of inventories encourages inefficient sloppy work and geometrically increase

the amount of time required to complete a product (Eric 2003). It also leads to higher inventory cost such as

product obsolescence, defect rates, pilferage etc. In just-in-time, production of goods is usually driven by

demand,. goods are not produced until demand is made by customers. This results in little or no inventory in

warehouse thus reducing cost on inventory. Many companies regard just-in-time as a general philosophy for

waste elimination (Charles 2005).

The Impact of Just-In-Time Costing System on Financial Statement.

Valuation of inventory has an impacts on financial statements, be it balance sheet and profit and loss

account. Without accurate stock valuation, net profit may be under or over stated. Inventory may exist in

warehouse in order to make it accessible to customers. When demand for such stock is low, it often times

results in stock pilling of stock at the end of a period.

However, a side effect of these is that it results in defect rate of stock, obsolescence stock, pilferage etc.

all of these factors hinder the fair and accurate presentation of actual stock value in the financial statement of

a firm. According to Ronald (2005) “just-in-time intends to avoid situations whereby inventory exceeds

demand. Here, goods are produced only when customer’s places order which leads to little or no inventory in

the warehouse thus resulting in real valuation of cost of sales in the trading account, and stock in the balance

sheet statement showing a true and fair value. The objective of inventory control is to minimize total

inventory cost (Adeniyi 2012). Just-in-time aims at reducing inventory costs. When there is low cost on

products, demand increases and when customers’ buys inventory, the value of inventory account is reduced

by the cost of goods sold. All of these factors increases the profit of a firm and results in more attractive

financial statement to end users. Just-in-time costing is thus based on these concepts.

Social and Economic Factors Affecting the Implementation of Just-In-Time System

Despite the immense benefits just-in-time system offers, its adoption by most manufacturing firms is

quite limited. Several factors have been seen as possible hindrances to just-in-time adoption. These factors

are seen as possible impediments to implementing a just-in-time system successfully. They include:-

Organizational Culture: The success of implementation of any particular practice frequently depends upon

organizational characteristics and not all organizations can implement the same set of practices.

Organizational Culture varies from firm to firm. There are some manufacturing industries that are tied to

other systems of operation hence it becomes difficult to change its culture to a just-in-time system within a

short time. Manufacturing firms operating the traditional technique may find it difficult in switching over to a

just-in-time system. This is because they depend greatly on safety stock, (Ofurum and Ogbonna, 2008).

Suppliers Factor: One of the key elements of a successful just-in-time system is having reliable suppliers as

they influence production process greatly. Akbar et al (2013) sited that Toyota the developer of just-in-time

had to close down all of its Japanese assemble lines when they found out that their main supplier of plant

known as Aisin Seiki company plant was gutted with fire. By the time the supply of plants had been restored.

Toyota had lost an estimated fifteen billion in sales. Without reliable suppliers, just-in-time implementation

becomes difficult.

Cost Factor: The task of converting the manufacturing system to one that uses the just-in-time system

cannot be achieved overnight. Just-in-time is not a simple method that any company can buy into as it

involves complete overhaul of the entire manufacturing process (Ronald 2005). To achieve this, it requires

high initial investment which most manufacturing firms cannot afford.

Journal of Empirical Economics

121

Technological Advances: Emerging technologies have provided some new growth in advance

manufacturing system (Nurus et al 2012). Highly advanced technological support facilities provide the

necessary backup that just in time system requires. To completely operate a just in time system, resources

must be made available to obtain technologically advance system and facilities so as to facilitate production.

When such facilities cannot be afforded or it lack competent workers that can actually operate these facilities,

then it becomes difficult to implement just-in-time successfully.

Personnel Factor: The success of just in time lies heavily in the hands of employees and management.

According to Ray et al (2003) just in time requires workers that are multi skilled. Cross training of

employees in order to gain better understanding of the whole system is an important one. Based on research,

employees training helped Toyota to cut its set up time during production from several hours to a few

minutes. This in turn increases the flexibility in meeting customers demand.

Just in time requires nothing less than a new way of thinking. It is a cultural change that must be led by

management. Management and employees need to be committed and experienced in operating just in time

system. When all of these factors are lacking in any manufacturing industry wishing to operate just in time

system then its implementation becomes difficult.

Risk: Just-in-time comes with some form of risk and little guarantee of success. According to Akbar et al

(2013), just in time manufacturing is simple in theory but hard to achieve in practice.

Defective units create a big problem in just in time environment. If vital parts ordered by a manufacturer

contain a defective unit, it can halt production process and this might cause delay in meeting customers

demand at the required time. Also, since just in time costing system aims at eliminating work in process

inventory, most manufacturing industries find it difficult to implement this system because with no work-in-

process inventory, a problem anywhere in the factory cell can halt production process which might lead to

delay in delivering goods to customers at the appropriate time.

Lack of Awareness: Promotion of just-in-time in terms of implementation is not effective due to ignorance

about the system (Adeyemi 2010). Many manufacturing firms, especially smaller ones are still unaware of its

existence much less the working of just-in-time system. Firms that have successfully implemented this

system and are getting tremendous benefit may not wish to publicize it because they do not want to share a

competitive advantage.

3. Empirical Studies

Various research works had been carried out in the area of just in time manufacturing and few of the

studies have however spelt out its importance as well as basis for implementation.

McDonough .(2013) indicated that a just in time inventory system helps manufacturing firms to become

more efficient and competitive in the way they handle their supply chains and response to customers. Based

on his findings, companies that had used just-in-time system have a greater level of control over the entire

manufacturing process thus making it easy for such firms to respond quickly when the need of customer

preference changes.

For Omorigie (2002), elimination of waste in just-in-time manufacturing can be achieved by adopting

practices such as total quality management, focused factory, reduced set up times, pull production system

and effective use of technology. Similar to this is Bulfin and Inman , (1991) who suggested that key

obstacles such as high variable production process, large container size, several production processes, long

lead time should be removed from the manufacturing process before the implementation of just in time

system.

Nurus et al (2012) spelt out that success of just in time implementation in manufacturing is largely

dependent on organizational support. Different from other studies conducted identified critical factors that

can lead to a successful just in time implementation which include smooth production flow and suppliers

efforts.

E. A. L. Ibanichuka & O. K. James

122

From Hung and Cheng (2010) perspective, material quality, firm size, proximity of suppliers is

important factors in a firm’s decision to adopt just-in-time system. Based on their findings a major limitation

of just in time implementation is attributable to ignorance about the system.

However, Akbar et al (2013) stated that implementation of just-in-time requires government support to

manufacturing firms by extending financial incentives. This will enable firms to become innovative as it

bears some of the financial burden associated with it. In light of the above arguments, it can be seen that

though just-in-time technique comes with enormous benefits in manufacturing, its implementation therefore

requires organizational commitment as well as supplies involvement.

4. Materials and Methods

This study attempts to find out the social and economic factors hindering the implementation of just-in-

time system in most manufacturing firms in Nigeria. The researchers used a survey method in carrying out

his research work. The sample size is selected based on judgmental sampling. The researchers choose this

method as a result of convenience in selection of industries. The sample covers ten (10) manufacturing firms

from variety of industries situated within the Niger Delta Region of Nigeria. A questionnaire was carefully

structured in closed and open ended form. The closed ended form consists of nine (9) items. Each item is

ranked from lowest to highest and is thus as follows:

1. Representing no extent

2. Representing considerably extent

3. Representing great extent

4. Representing very great extent

This is to enable respondents rate each statement according to the extent of agreement. The open ended

form consists of provisions for experienced information and viewpoints of management staff. This is also to

enable respondents give their personal view on the subject matter. Copies of the questionnaires were issued

to companies. It was distributed to mangers, accountants, store supervisors and production engineers to

provide the needed information. Since the study was about relationships and effects of different independent

factors on the implementation of just-in-time costing system, the statistical model preferred for the study was

the least square regression analysis using Econometric view soft ware (E-view) version 3.1

Model Specification

The primary data for the study were generated through the administration of questionnaires conducted to

evaluate the factors influencing the implementation of just-in-time costing system in Nigeria. Two hundred

and fifty respondents from ten (10) companies were given questionnaires. The study was conducted between

August - October 2013. The study used instruments developed by Brooks, (2008), Adamu and Olotu (2010) ,

but modified by the authors. The Yaro Yemen model was used for the purpose of sample size determination.

A total of sixty three (63) usable questionnaires were completed and used for the analysis representing sixty

five percent (65%). The modified questionnaire was pre-tested using two (2) firms in the study. A reliability

and internal consistency test was done on the collected data using Cronbach Alpha and Pearson Product

Moment Correlation Coefficient model, to explore the consistency of the questionnaire. The result of the

reliability test shows that the questionnaire design was reliable and consistent at 0.732 and 0.781. Excel

software helped the researchers to transform the variables into a format suitable for analysis, after which the

econometric view (e-view) was utilized for data analysis. The ordinary least square regression, granger

causality, unit root and diagnostic tests are adopted for the purpose of data analysis. Asterious and Hall

(2007), document that the ordinary least square regression analysis shows the direction of causing/affecting

between the dependent and independent variable. Gujarati and Porter (2009), suggested that unit root test

such as Dickey-Fuller, Augmented Dickey-Fuller, Philips-Perron and Kwiatkowski, are used to determine

the stationarity and non-stationarity of variables. Granger Causality test refers to the ability of one variable to

predict (and therefore cause) the other. Diagnostic tests were also conducted to determine the assumptions of

Journal of Empirical Economics

123

the classical near regression model of multicollinearity, heteroskedasticity, autocorrelation, normality of

disturbance. The ordinary least square was guided by the following linear model:

Y=f(X) …………………………………………………………………… (1)

Where X are the factors that determines JIT adoption

Y=f(X1, X2, X3, X4, X5, X6 ,X7, X8)………. …………………………..(2)

Where X1 = suppliers factor, X2 = technology, X3 = organizational culture, X4 = cost factor, X5 = risk,

X6 = lack of awareness, X7= employee commitment and Y = Just-in-time costing..

JIT=α+β1SUPL+β2TECH+β3ORGC+β4COST+β5RISK+β6LACKW+β57EMPL+ε ………(3)

The a priori expectation of the linear model is presented below

∂SUPL/∂JIT> 0; ∂TECH/∂JIT >0; ∂ORGC/∂JIT >0; ∂COST/∂JIT >0; LACKW/∂JIT >0; ∂EMPL/∂JIT

>0 and ∂RISK/∂JIT >0

Where: JIT=just-in-time costing; SUPL=suppliers factor; TECH= technology; ORGC=organizational

culture; COST=cost of implementation; LACK= lack of awareness; RISK=risk of implementation β1, β2, β3,

β4, β5, β6; β7 are the coefficients of the regression, α is the intercept of the regression and ε is the error term

capturing other explanatory variables not explicitly included in the model.

5. Data Analysis And Presentation

Table 4.1 Regression analysis of variables

Source: E-View result with primary data generated by researchers, 2013.

The result in table 4.1 above shows that a one 1% increase in the efficiency of the performance of

TRADITIONAL COSTING (TRD), will result to a 0.135032 increase in better financial statement

representation by firms (FSR) in Nigeria, with a t-statistics of 1.001452. Again, with a 1% increase in the use

of just-in-time costing system (JIT) will increase fair representation of financial statements by 0.347%. With

a t-Statistics of 2.7964 which is greater than the t critical value of 1.96, at 0.0162 probabilities which is less

than 0.5%, the null hypothesis is rejected and the alternative accepted that there is a significant relation

between just-in-time costing system and efficient representation of financial statements with a probability of

0.3364 which is greater than 0.5%.

Dependent Variable: FSR

Method: Least Squares

Date:11/23/13 Time: 17:22

Sample: 63

Included observations: 63

Variable Coefficient Std. Error t-Statistic Prob.

C 6.154906 26.06844 0.236106 0.8173

TRD 0.135032 0.134837 1.001452 0.3364

JIT 0.347626 0.124311 2.796424 0.0162

R-squared 0.603691 Mean dependent var 72.68750

Adjusted R-squared 0.504613 S.D. dependent var 15.37409

S.E. of regression 10.82085 Akaike info criterion 7.813145

Sum squared resid 1405.090 Schwarz criterion 8.006292

Log likelihood -58.50516 F-statistic 6.093122

Durbin-Watson stat 2.441970 Prob(F-statistic) 0.009227

E. A. L. Ibanichuka & O. K. James

124

The probability of F-statistics is 0.009227, indicating the overall fitness of the variables in the research

model. With the Durbin-Watson text of 2.4419, there is no evidence of existence of positive first order auto

correlation in the model. Meaning that the result from this model can be used for long-run forecasting.

Finally the R-Square of 0.60 and the adjusted R-Square of 0.50 means that the variables, TRD and JIT

explains at least 50% of the behavior of fair representation of financial statements by firms in Nigeria.

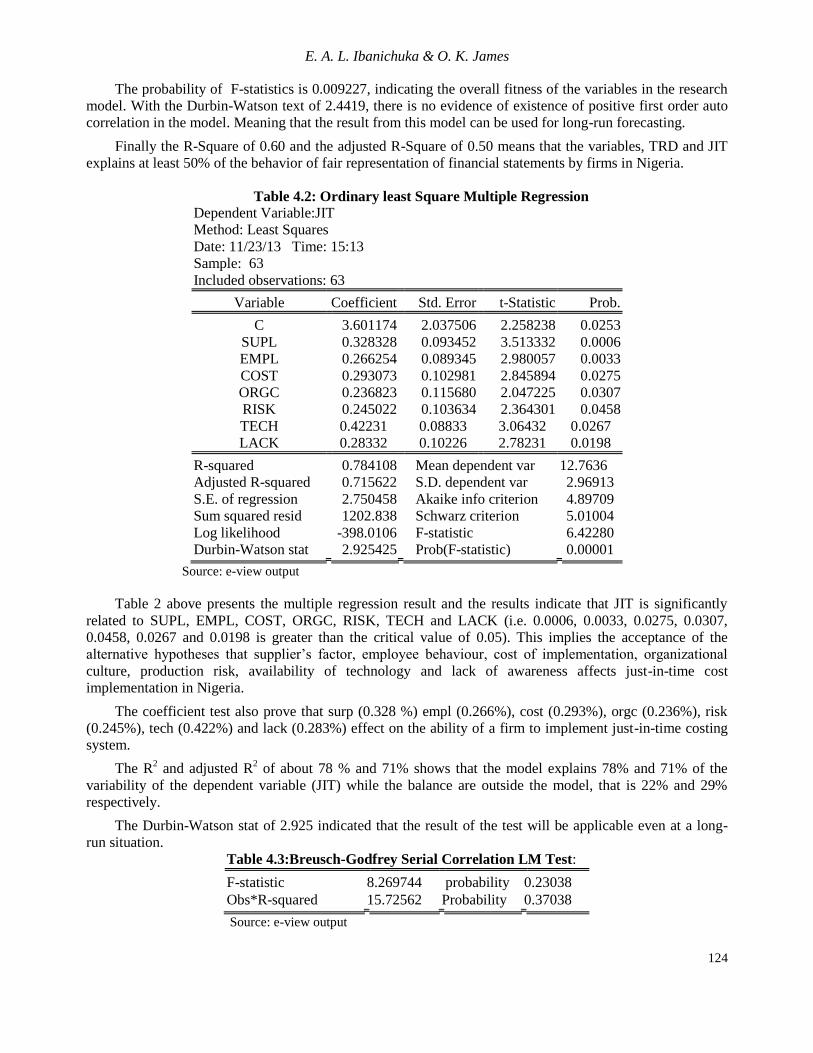

Table 4.2: Ordinary least Square Multiple Regression

Dependent Variable:JIT

Method: Least Squares

Date: 11/23/13 Time: 15:13

Sample: 63

Included observations: 63

Variable Coefficient Std. Error t-Statistic Prob.

C 3.601174 2.037506 2.258238 0.0253

SUPL 0.328328 0.093452 3.513332 0.0006

EMPL 0.266254 0.089345 2.980057 0.0033

COST 0.293073 0.102981 2.845894 0.0275

ORGC 0.236823 0.115680 2.047225 0.0307

RISK

TECH

LACK

0.245022

0.42231

0.28332

0.103634

0.08833

0.10226

2.364301

3.06432

2.78231

0.0458

0.0267

0.0198

R-squared 0.784108 Mean dependent var 12.7636

Adjusted R-squared 0.715622 S.D. dependent var 2.96913

S.E. of regression 2.750458 Akaike info criterion 4.89709

Sum squared resid 1202.838 Schwarz criterion 5.01004

Log likelihood -398.0106 F-statistic 6.42280

Durbin-Watson stat 2.925425 Prob(F-statistic) 0.00001

Source: e-view output

Table 2 above presents the multiple regression result and the results indicate that JIT is significantly

related to SUPL, EMPL, COST, ORGC, RISK, TECH and LACK (i.e. 0.0006, 0.0033, 0.0275, 0.0307,

0.0458, 0.0267 and 0.0198 is greater than the critical value of 0.05). This implies the acceptance of the

alternative hypotheses that supplier’s factor, employee behaviour, cost of implementation, organizational

culture, production risk, availability of technology and lack of awareness affects just-in-time cost

implementation in Nigeria.

The coefficient test also prove that surp (0.328 %) empl (0.266%), cost (0.293%), orgc (0.236%), risk

(0.245%), tech (0.422%) and lack (0.283%) effect on the ability of a firm to implement just-in-time costing

system.

The R2 and adjusted R

2 of about 78 % and 71% shows that the model explains 78% and 71% of the

variability of the dependent variable (JIT) while the balance are outside the model, that is 22% and 29%

respectively.

The Durbin-Watson stat of 2.925 indicated that the result of the test will be applicable even at a long-

run situation.

Table 4.3:Breusch-Godfrey Serial Correlation LM Test:

F-statistic 8.269744 probability 0.23038

Obs*R-squared 15.72562 Probability 0.37038

Source: e-view output

Journal of Empirical Economics

125

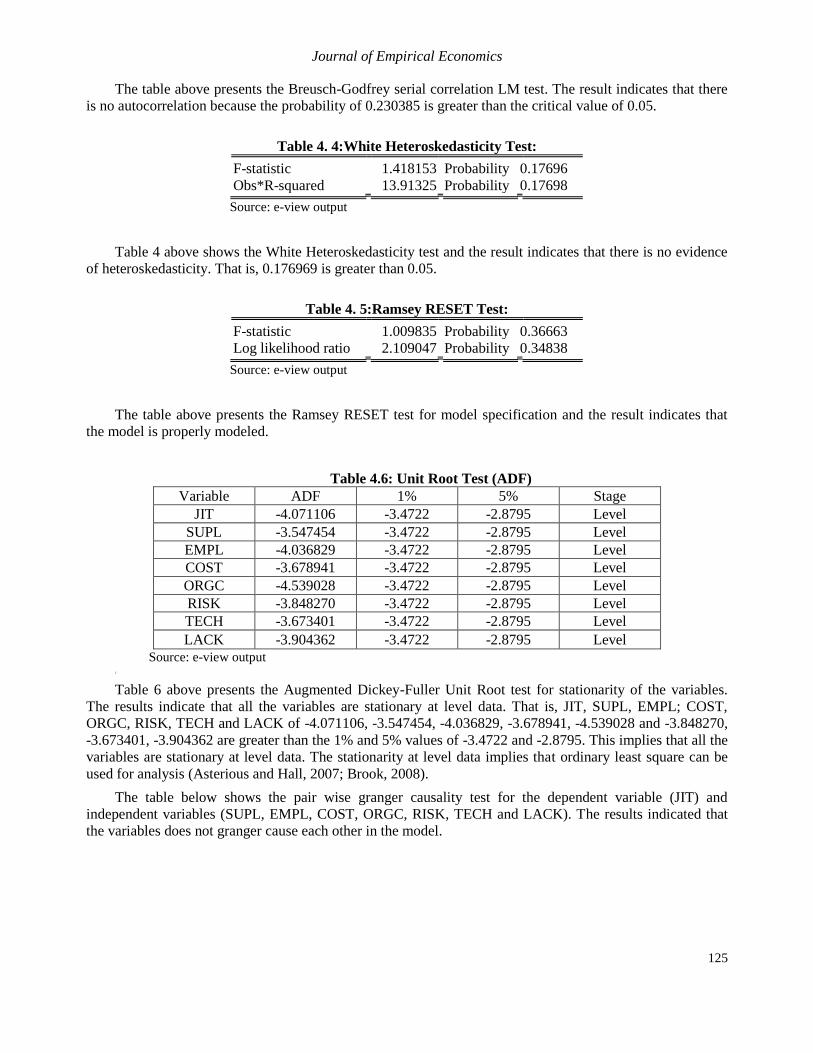

The table above presents the Breusch-Godfrey serial correlation LM test. The result indicates that there

is no autocorrelation because the probability of 0.230385 is greater than the critical value of 0.05.

Table 4. 4:White Heteroskedasticity Test:

F-statistic 1.418153 Probability 0.17696

Obs*R-squared 13.91325 Probability 0.17698

Source: e-view output

Table 4 above shows the White Heteroskedasticity test and the result indicates that there is no evidence

of heteroskedasticity. That is, 0.176969 is greater than 0.05.

Table 4. 5:Ramsey RESET Test:

F-statistic 1.009835 Probability 0.36663

Log likelihood ratio 2.109047 Probability 0.34838

Source: e-view output

The table above presents the Ramsey RESET test for model specification and the result indicates that

the model is properly modeled.

Table 4.6: Unit Root Test (ADF)

Variable ADF 1% 5% Stage

JIT -4.071106 -3.4722 -2.8795 Level

SUPL -3.547454 -3.4722 -2.8795 Level

EMPL -4.036829 -3.4722 -2.8795 Level

COST -3.678941 -3.4722 -2.8795 Level

ORGC -4.539028 -3.4722 -2.8795 Level

RISK -3.848270 -3.4722 -2.8795 Level

TECH -3.673401 -3.4722 -2.8795 Level

LACK -3.904362 -3.4722 -2.8795 Level

Source: e-view output 2

Table 6 above presents the Augmented Dickey-Fuller Unit Root test for stationarity of the variables.

The results indicate that all the variables are stationary at level data. That is, JIT, SUPL, EMPL; COST,

ORGC, RISK, TECH and LACK of -4.071106, -3.547454, -4.036829, -3.678941, -4.539028 and -3.848270,

-3.673401, -3.904362 are greater than the 1% and 5% values of -3.4722 and -2.8795. This implies that all the

variables are stationary at level data. The stationarity at level data implies that ordinary least square can be

used for analysis (Asterious and Hall, 2007; Brook, 2008).

The table below shows the pair wise granger causality test for the dependent variable (JIT) and

independent variables (SUPL, EMPL, COST, ORGC, RISK, TECH and LACK). The results indicated that

the variables does not granger cause each other in the model.

E. A. L. Ibanichuka & O. K. James

126

Table 4.7: Pairwise Granger Causality Tests

Date: 12/13/11 Time: 14:57

Sample: 1 165

Lags: 2

Null Hypothesis: Obs F-Statistic Probability

SUPL does not Granger Cause JIT 63 1.54590 0.02633

JIT does not Granger Cause SUPL 2.54603 0.08160

EMPL does not Granger Cause JIT 63 1.45180 0.01725

JIT does not Granger Cause EMPL 1.68234 0.18925

COST does not Granger Cause JIT 63 0.38804 0.04903

JIT does not Granger Cause COST 1.55125 0.21519

ORGC does not Granger Cause JIT 63 0.21019 0.03065

JIT does not Granger Cause ORGC 4.20803 0.01658

RISK does not Granger Cause JIT 63 0.04156 0.04930

JIT does not Granger Cause RISK 1.69897 0.18620

TECH does not Granger Cause JIT 63 0.05256 0.14930

JIT does not Granger Cause TECH 1.59897 0.18620

LACK does not Granger Cause JIT 63 0.54156 0.02930

JIT does not Granger Cause LACK 2.69897 0.18620

Source: e-view output

6. Discussion of Findings

The results from the tables above proved that just-in-time costing system has a greater positive impact

on the fair presentation of stock and net profit in the financial statements as compared with the use of the

traditional method with an impact difference of 0.212% ( 0.135 - 0.347). This provides the reason for just-in-

time being better off to the traditional method.

With regard to the low level of the implementation of this system, the study also revealed that socio-

economic factors such as suppliers’ commitment, employees’ value for change, cost of implementation,

availability of advance technology, risk of failure, lack of awareness are some factors responsible for it. They

jointly accounted for 71% of the reason for non implementation of JIT by firms in Nigeria. The aim of this

research was to examine the effect of just-in-time costing system on financial statement representation. It is

also geared at finding out the socio -economic factors hindering the implementation of just-in-time system

within manufacturing firms in Nigeria these results agreed with the findings of Ronald (2005), and Eric

(2003) and McDonough .(2013) .

7. Conclusion

Every successful business relies on many factors to survive in its competitive environment one of which

is reliable inventory control system. Just-in-time costing system have been proven to be an effective and

efficient technique used by most manufacturing firms when it comes to inventory control as it results in

minimizing high inventory cost. It has been discovered in the study also that valuation of inventory using

just-in-time costing system results in fair and accurate presentation of stock in the financial statements as

compared with the traditional method.

Journal of Empirical Economics

127

However, despite the benefits associated with just-in-time technique, most firms still find it difficult to

implement it. The result reveals therefore that most firms are still unable to implement this system due to the

following:

- Lack of awareness about the system

- Firms organizational culture

- Lack of technological skills and advance technological facilities

- Lack of reliable suppliers

- Low level of commitment by employees and management towards an effective just-in-time system.

- High cost in implementing the system.

8. Recommendations

Based on the above findings the following recommendations are made:

- Awareness should be created through the establishment of effective training programs in form of

seminars/workshops in order to sensitize management and employees on the need and usefulness of just-

in-time costing system implementation as well as to gain more knowledge on how just-in-time system

operates.

- Motivation of suppliers through negotiation of fair price so as to enhance delivery of quality materials

with a reduced lead time.

- Government can support companies wishing to implement just-in-time system by extending financial

incentives and reducing tax on firms’ income. By this, companies can bear some of the financial burden

associated with the cost of implementing just-in-time system.

Also, government needs to ensure that the award of contract to contractors on infrastructural projects

such as roads had to be executed effectively. This will help to reduce the cost of transporting goods and

production output from one location to another.

- Self inspection should be made by employees and management wishing to implement just-in-time

system. This is to ensure that production inputs supplies are of high quality and it adds value to the

goods produced.

- Motivation of employees through employee empowerment programs such as reward and compensation

scheme. This will enable employees to become more committed and innovative on the adoption of just-

in-time system. It also leads to significant expansion of workers skills.

References

Adamu, A. and Olotu, A.I. (2010). “The Practicability of Activity-Based Costing System in Hospitality

Industry”, Journal of Finance and Accounting Research, Nasarawa State University, Keffi, 1(10: 36-

49.

Adeniyi A. Adeniyi (2012). An Insight into Management Accounting. 6th Edition. Mushin, Lagos El-toda

ventures limited.

Akbar J. K, Shahab G. K, and Zahra AS (2013) Just–in–time Manufacturing System, Revolution in

Management Accounting from Concept to Implementation. International Review of Management

and Business Research Journal. Vol. 2 issues 1. Pg. 53 - 67

Asterious, D. and Hall, S.G. (2007). Applied Econometrics: A Modern Approach, London: Palgrave and

Macmillan.

Brooks, C. (2008). Introductory Econometrics for Finance (2nd), New York: Cambridge University Press.

Bulfin R. L and Inman A (1991) Sequencing of just – in – time Mixed Model Assembly lines. Management

Science, Vol 37. Pg 901 – 904. www.jstor.org. (Retrieved Oct 20th 2013).

E. A. L. Ibanichuka & O. K. James

128

Charles T. H (2005) Accounting 6th Edition. New Jersey, Pearson Prentice Hall Inc,

Colin Drury (2008) management and cost accounting. 6th Edition. Bed Ford Row, London Book Power

Thompson Learning Publishers.

Eric W. N (2003) Management Accounting. 10th Edition, New York, USA. Von Hoffmann Press.

Fanzine Faze (1997) A Comparative Analysis of Inventory Cost of Just – in –Time and Economic Order

Quantity Purchasing. International Journal of Physical Distribution and Logistics Management, vol

27 no 8. Pp. 23-41.

Gujarati, D.N. and Porter, D.C. (2009). Basic Econometrics (5th ed.), New York: McGraw-Hill.

Hung M and Cheng N (2010). An empirical Study of just – in – time in queen land Manufacturing Industry.

PHd thesis the library of Queen land, Queen Land University, Pg 47- 52.

ICAN (2012) Management Accounting professional examination study pack. Lagos Nigeria, Value analysis

publisher.

Kozhan, R. (2010). Financial Econometrics with E-views.Roman Kozhan and Ventus Publishing.

www.bookboon.com Malaysia May 19–20. www. prcentre.org. (Retrieved July 12-24.

McDonough M.(2013) Real-Life Examples of Successful JIT Systems.

http://www.brighthubpm.com/methods-strategies/71540-real-life-examples-of-successful-jit-

systems/) retrieved August 26, 2013

Nurus A. A, M. Y. Nafrizuan, Y. A. Razlan (2012). Review on Elements of Just–in–time Implementation.

International Conference of Auto motive, Mechanical and Material Engineering Penang (ICAMME

2012)

Ofurum, C.O. and Ogbonna, G.N. (2008). Accounting Information Systems: A Functional Approach,

Owerri: Bon Publications.

Ohno T (1997) Toyota to Recalibrate just-in–time. “International Herald Tribune, February 8th, 1997 Pg 9.”

Omoregie, N.V. (2002). Effective Cost Management: An Introductory Text, Lagos: Novgie Press

Publication.

Ray H. and Gamson D. B. A. (1994) Management Accounting Concept for Planning Control and Decision

Making. 7th Edition. New York, Von Hoffmann Press.

Roger H. and Hermansion N, (1998) Accounting for Business Perspective. 7th Edition. New York, Mc Graw-

Hilirwin companies Inc.

Ronald W. H (2005) Management Accounting Creating Value in a Dynamic Business Environment. 6th

Edition, New York. Mc Graw-Hilirwin.