June 23, 2008Andrea St. Rose & Associates CAACM - IFRS WORKSHOP Presented by Andrea St. Rose &...

118

June 23, 2008 Andrea St. Rose & Associates CAACM - IFRS WORKSHOP Presented by Andrea St. Rose & Associates Bay Gardens Hotel – June -23, 2008

-

Upload

buddy-shepherd -

Category

Documents

-

view

214 -

download

0

Transcript of June 23, 2008Andrea St. Rose & Associates CAACM - IFRS WORKSHOP Presented by Andrea St. Rose &...

June 23, 2008 Andrea St. Rose & Associates

CAACM - IFRS WORKSHOPPresented by

Andrea St. Rose & Associates

Bay Gardens Hotel – June -23, 2008

9/12/2005

Presenter

Andrea St. Rose – LL.B(Hons),FCIS,CFE, MBA, CGA, CA

9/12/2005

IFRS PRESENTATION

ISSUE OF CREDITS/AcknowledgementsDeloitt’s IAS Plus PricewaterhouseCoopers

Other Sources:Reference is made to the 2008 IFRS

manual issued by the IASB

ECFH Annual Report

9/12/2005

IFRS Workshop

1. Introduction1. Introduction

2. IFRS 7 2. IFRS 7

3. IAS 13. IAS 1

4. IAS 394. IAS 39

Agenda

9/12/2005

IFRS Training Seminar

5. IAS 325. IAS 32

7. Practical Issues 7. Practical Issues

4. Questions and Answers 4. Questions and Answers

Agenda cont’d

6. Overview of IFRS 46. Overview of IFRS 4

9/12/2005

CAACM IFRS Worshop

INTRODUCTION

9/12/2005

Introduction

LEARNING OBJECTIVESHighlight critical aspects of the standards

Enhance general understanding

9/12/2005

Introduction

Quick Recap Why International Financial reporting

Standards?

Status of Application globally

Role of Audit Committee regarding IFRS

9/12/2005

Introduction – Quick Recap

Why IFRS ? Consistency/global

Comparability

High quality /inv

9/12/2005

Introduction Quick Recap

Status of Application GloballyTotal

IFRSs permitted 25

IFRSs required 81 (for all domestic companies)

IFRS required 3(for some domestic companies) ____

109

Source: Sir David Tweedie, IASB Chairman

9/12/2005

Quick Recap

Role of Audit Committee Regarding IFRS

Ensure the accuracy and reliability of financial reporting – implies …..

For this reason – at least on financial expert on committee

9/12/2005

IFRS 7

Financial Instruments : Disclosures

9/12/2005

IFRS 7

History:

July 22, 2004 - Exposure Draft issued

August 18, 2005 - IFRS 7 issued

Jan 1, 2007 - Effective date of application

(source: IASB and Deloittes - IAS Plus )

9/12/2005

IFRS 7

How did it Evolve?

Replaced Disclosures Require by IAS 30 – Disclosure in Financial Statements of Banks and Similar FI’s

Added some new disclosures to those required by IAS 32 – simplified some disclosures about risk – credit etc

Placed all those disclosures in one new standard - IFRS 7 – Financial Instruments : Disclosures.

9/12/2005

IFRS 7

THE END RESULT

IAS 32 now deal only with financial instruments presentation matters – disclosures are now dealt with under IFRS 7.

IFRS 7 now supersedes IAS 30.

9/12/2005

IFRS 7

The Reasons for Isssuing IFRS 7

IASB believes that users of FS need info about an entity’s exposure to risk and how those risks are managed.

info can influence a users assessement of Fin Pos and Performance of entity or the amt, timing and certain of future cah flows

Greater transparancy regarding those risks allows users to make informed judgements about risk and return.

9/12/2005

IFRS 7

SCOPE OF APPLICATION Applies to all financial instruments with certain

exceptions – covered by other stds e.g. rights and obligations for pension – IAS 19.

Applies to all entities – e.g. a manufacturer whose only FI’s are accounts receivable and accounts payable – Financial Institutions most of whose assets and liabilities are FI’s.

9/12/2005

IFRS 7

The two main disclosures required by IFRS7:

Information about the significance of financial instruments. (Many of the requirements previously in IAS 32).

Information about the nature and extent of risks arising from financial instruments – Qualitatve and Quantitative.

9/12/2005

IFRS 7

Risk Management DisclosuresAttempts to “Look at risk through the eyes

of Management”. The extent of disclosures will be depend

to some extent on the way mangement manages financial risks.

It will also depend on the extent to which the entity utilises financial instruments

9/12/2005

IFRS 7

A look at some of the Disclosures

( No Change in Balance Sheet /P&L Presentation)

9/12/2005

IFRS 7

Balance Sheet Categories of Financial Assets and Laibilities Carrying amounts of:

Financial assets measured at fair value through profit and loss, showing separately those held for trading and those designated at initial recognition.

Held-to-maturity investments. Loans and receivables. Available-for-sale assets. Financial liabilities at fair value through profit and loss,

showing separately those held for trading and those designated at initial recognition.

Financial liabilities measured at amortised cost.

9/12/2005

IFRS 7

Balance Sheet – cont’dAdditional disclosures about financial

assets and financial liabilities designated to be measured at fair value through profit and loss, including disclosures about credit risk and market risk and changes in fair values [IFRS 7.9-10]

(source: IASB and Deloittes IAS Plus)

9/12/2005

IFRS 7

FV through Profit and Loss: If an entity has designated a loan or

receivable as at fair value through profit and loss it shall disclose –

the maximum exposure to credit risk of the loan or receivable at the reporting date

The amount by which any related credit derivatives or similar instruments mitigate that maximum exposure to credit risk

9/12/2005

IFRS 7

FV through Profit and Loss: cont’d

The amount of change during the period and cumulatively , in FV of the loan or receivable that is attributable to changes in the credit risk of the financial asset.

9/12/2005

IFRS 7

Balance Sheet – cont’dReclassifications of financial instruments

from fair value to amortised cost or vice versa [IFRS 7.12] – disclose amounts and reasons for that reclassification.

Information about financial assets pledged as collateral and about financial or non-financial assets held as collateral [IFRS 7.14-15] – disclose terms and conditions of the pledge

9/12/2005

IFRS 7

Balance Sheet – cont’dReconciliation of the allowance account

for credit losses (bad debts). [IFRS 7.16] – for each class of financial assets.

If compound financial instruments with multiple embedded derivatives are held [IFRS 7.17] – whose values are interdependent e.g. callable convertible debt instrument. Disclose the existence of those features.

9/12/2005

IFRS 7

Balance Sheet – Cont’dBreaches of terms of loan agreements. [IFRS

7.18-19] – payable at reorting date Details of any defaults during the period of principal,

interest, sinking fund or redemption terms Carrying amount of the loans payable in default at the

end of the reporting period Whether the default terms of the loans were remedied

or the terms of the loans payable renegotiated before the financial statements were authorised for issue.

9/12/2005

IFRS 7

Income Statement and EquityItems of income, expense, gains, and losses,

with separate disclosure of net gains or net losses from: [IFRS 7.20(a)]

Financial assets measured at fair value through profit and loss, showing separately those held for trading and those designated at initial recognition.

Held-to-maturity investments. Loans and receivables. Available-for-sale assets. Financial liabilities measured at fair value through

profit and loss, showing separately those held for trading and those designated at initial recognition.

Financial liabilities measured at amortised cost.

9/12/2005

IFRS 7

Income Statemant and Equity – cont’dTotal interest income and total interest

expense for those financial instruments ( assets and liabilities) that are not measured at fair value through profit and loss [IFRS 7.20(b)] – calculated using the effective interest method

9/12/2005

IFRS 7

Income Statement and Equity – cont’d

Fee income and expense arising from FA and FL that are not at fair value though profit or loss[IFRS 7.20(c)]

Amount of impairment losses for each class of financial assets [IFRS 7.20(e)]

Interest income on impaired financial assets accrued in accordance with IAS 39 [IFRS 7.20(d)] – using interest rate used to discount future cash flows for measuring impairment loss.

9/12/2005

IFRS 7

Other DisclosuresDisclosure of accounting policies as

required by IAS 1Information about hedge accounting,

including: [IFRS 7.22] Description of each hedge, hedging

instrument, and fair values of those instruments, and nature of risks being hedged.

9/12/2005

IFRS 7

Other Disclosures – cont’dInformation about the fair values of each

class of financial asset and financial liability, along with: [IFRS 7.25-30] Comparable carrying amounts. Description of how fair value was determined.

– methods ; if valuation techniques are used, the assumptions applied in determining FV for each class.

Detailed information if fair value cannot be reliably measured.

9/12/2005

IFRS 7

Other Disclosures- Cont’d Disclosures of Fair Value not required when :

the carrying amount is a reasonable approximation of fair value, e.g. short-term trade receivables and payables,

fair value cannot be measured reliably. e.g. equity instruments that do not have a quoted or active market[IFRS 7.29]

9/12/2005

IFRS 7

Nature and Extent of Risks Arising from Financial Instruments

(Qualitative and Quantative)

9/12/2005

IFRS 7

QUALITATIVE DISCLOSURES

The qualitative disclosures describe: The exposures to risk and how they arise -

for each type of financial instrument. Management's objectives, policies, and

processes for managing those risks and the methods used to measure the risk.

Changes ( in the above) from the previous period.

9/12/2005

IFRS 7

QUANTITATIVE DISCLOSURESThe quantitative disclosures provide information

about the extent to which the entity is exposed to risk, based on information provided internally to the entity's key management personnel. These disclosures include: [IFRS 7.34]

Summary quantitative data about exposure to each risk at the reporting period.

Disclosures about credit risk, liquidity risk, and market risk

Concentrations of risk – if not apparent from above.

9/12/2005

IFRS 7

Credit RiskDisclosures about credit risk include: [IFRS 7.36-

38] Maximum amount of exposure at the end of the

period without taking account of value of any collateral held ( on and off balance sheet amounts)

description of collateral, information about credit quality of financial assets that

are neither past due nor impaired, and The carrying amount of financial assets that would

otherwise be past due or impaired whose terms have been renegotiated. [IFRS 7.36]

9/12/2005

IFRS 7

Credit Risk – Cont’dFinancial Assets that are either past due

or impaired:Aging analysis of financial assets that are

past due but not impairedAnalysis of financial assets that are

impaired and impairment factors For the above amounts, a description of

collateral held as security and unless impracticable, an estimate of fair value.

9/12/2005

IFRS 7

CREDIT RISK – Cont’dInformation about collateral or other credit

enhancements obtained or called e.g. guarantees [IFRS 7.38] The nature and carrying amount of the assets

obtained When assets are not readily convertible nto

cash. Its policies for disposing of such assets or for using them in operations.

9/12/2005

IFRS 7

LIQUIDITY RISKDisclosures

Maturity analysis of contractual liabilities that shows the remaning contractual maturities

A description of how the entity manages the liquidity risk inherent in the above.

9/12/2005

IFRS 7

MARKET RISKMarket risk is the risk that the fair value or

future cash flows of a financial instrument will fluctuate due to changes in market prices. Market risk comprises : interest rate risk, currency risk, and other price risks.

9/12/2005

IFRS 7

MARKET RISKDisclosures about market risk include:

A sensitivity analysis of each type of market risk to which the entity is exposed.

IFRS 7 provides that if an entity prepares a sensitivity analysis for management purposes that reflects interdependencies between risk variables – and it uses same to manage those risks (for instance, interest risk and foreign currency risk combined), it may disclose that analysis instead of a separate sensitivity analysis for each type of market risk.

9/12/2005

IFRS 7

SENSITIVITY ANALYSESShow effect on P&L and equity of reasonably

possible changes in the relevant risk variable – e.g. prevailing market interest rates, currency rates, equity prices etc.

Assumes the change occurred at the end of the reporting period and applied to the risk exposure at that date.

Effect of the change applied at the limits of the reasonably possible range , e.g. a 50 basis point increase or decrease in interest rates.

9/12/2005

IFRS 7

MARKET RISKSensitivity Analyses:Sensitivity of profit or loss from instruments

classified at fair value through profit and loss is disclosed separately from the sensitivity of equity, that arises for example from instruments classified as available for sale.

Financial instruments that are classified as equity instruments are not remeasured –nil impact on P& L or equity – hence no sensitivity analysis is required.

For currency risk - disclose for each currency to which an entity has a significant exposure.

9/12/2005

IFRS 7

What are the application issues?

9/12/2005

IAS 1

9/12/2005

IAS 1

HISTORY OF IAS 1 Exposure draft first issued 1974 IAS 1 (1997) issued 1997 Sept Effective date of IAS 1(1997) 1998 July 1 Revised IAS 1 issued 2003 Dec Effective date of IAS1( rev 2003) 2005 Jan1 Amend – disclosures about Capital 2005 Aug Effective date of amendments 2007 Jan Revised IAS 1 issued 2007 Sept Effective date of IAS 1 revised 2009 Jan

(Source: Deloittes IAS Plus)

9/12/2005

IAS 1 Presentation of financial Statements

The application of IFRS is presumed to result in fair presentation of financial statements.

Financial statements shall not be described as being in compliance with IFRS unless they comply with all the requirements.

9/12/2005

IAS 1

IAS 1 amendments (relating to IFRS 7 - Aug 2005)

the entity's objectives, policies and processes for managing capital;

quantitative data about what the entity regards as capital;

whether the entity has complied with any capital requirements; and

if it has not complied, the consequences of such non-compliance.

9/12/2005

IAS 1

Objectives of Revising IAS 1 ( Effective 2009)

To present all owner changes in equity separately from non –owner changes in equity

To improve and reorder sections of IAS 1 to make it easier to read

9/12/2005

IAS 1

Main Changes from Previous version of IAS 1: ( effective 2009)

Balance Sheet - Statement of Financial Position

Cash Flow statement – Statement of Cash Flows

An increase in the number of statements included in a set of financial statements

9/12/2005

IAS 1

Main changes effective 2009

Present at a minimum 2 statements of financial position

Two of each of the other statements and related notes

9/12/2005

IAS 1

Main Changes Effecive 2009 cont’dIf a change in accounting policy is applied

retrospectively or when items are reclassified Present at least 3 statements of financial

position and two of the other related statements

9/12/2005

IAS 1

Main Changes cont’d effective 2009Hence an entity presents statements of

financial position as at: The end of the current period The end of the previous period ( same as

beginning of current period) The beginning of earliest comparative period.

9/12/2005

IAS 1

Main Changes Cont’d (effective 2009)

The Concept of a “Statement of Comprehensive Income” is Introduced

All non-owner changes in Equity

9/12/2005

IAS 1

Main Changes Cont’d (effective 2009) Present all non-owner changes in equity

(that is, 'comprehensive income') either in one statement of comprehensive income or

in two statements (a separate income statement and a statement of comprehensive income).

9/12/2005

IAS 1

Statement of Compehensive Income

Statement of comprehensive income begins with profit or loss and adds other components of comprehensive income

9/12/2005

IAS 1 cont’d

Main Changes cont’d effective 2009

Components of comprehensive income may not be presented in the statement of changes in equity. Shown in total

9/12/2005

IAS 1

Main Changes effective 2009 cont’d

Examples of other comprehensive income: Gain on property revaluation Gains on available-for-sale financial assets Actuarial gains or losses on defined benefit

pension plans Exchange differences on translating foreign

operations

9/12/2005

IAS 1

Main Changes cont’d effective 2009Other disclosures:

Income tax relating to each component of other comprehensive income ( in statement or notes)

May be presented Net of related tax or before related tax with amount shown of aggregate of income tax.

9/12/2005

IAS 1

ANY APPLICATION ISSUES?

9/12/2005

IAS 32

Financial Instruments : Presentation

9/12/2005

IAS 32

Where are we?

Sept 1991 - Exposure draft

Jan 1996 - Effective date of IAS 32

Dec 1998 - IAS 32 revised by IAS 39

Dec 2003 - Revised IAS 32 issued

Jan 2005 - Effectve date of IAS 32 (Revised 2003)

Aug 2005 - Disclosure provisions replaced by IFRS 7 effective

2007 – title change

9/12/2005

IAS 32

Financial Statements : Presentation

9/12/2005

IAS 32

IASB - IAS 32 Financial Instruments: Disclosure and Presentation was issued in December 2003 and is applicable for annual periods beginning on or after 1 January 2005.

IAS 32 is intended to enhance financial statement users’ understanding of the significance of financial instruments to an entity’s financial position, performance and cash flows.

The disclosure requirements of this standard were superceded by IFRS 7- issued on the 18th August 2005

9/12/2005

IAS 32 – KEY FEATURES

The following are outside the scope of IAS 32 Insurance contracts (IFRS 4) Employee benefits (IAS 19) Share based payments (IFRS 2) Contracts for contingent consideration in a

business combination (IFRS 3) Financial guarantee contracts & weather

derivatives (if specific IFRS 4) Interests in subsidiaries, associates and joint

ventures covered under IAS 27, 28 & 31

9/12/2005

IAS 32 – KEY FEATURES

Presentation of Financial Instruments

“A financial instrument is any contract that gives rise to a financial asset of one entity and a financial liability or equity instrument of another entity” They include:

Financial assetsFinancial LiabilitiesEquity

9/12/2005

IAS 32 KEY FEATURES

Definition

A financial asset is any asset that is:CashA contractual right to receive cash or another

financial asset from another enterpriseA contractual right to exchange financial

instruments with another enterprise under conditions that are potentially favorable; or

An equity instrument of another enterprise

9/12/2005

IAS 32 KEY FEATURES

Definition

A financial liability is any liability that is a contractual obligation:

• To deliver cash or another financial asset to another enterprise; or

• To exchange financial instruments with another enterprise under conditions that are potentially unfavorable

9/12/2005

IAS 32

Definition

Equity is any contract that evidences a residual interest in the assets of an

entity after deducting all of its liabilities

9/12/2005

IAS 32

Presentation of Financial Instruments

Classification as Liability or Equity

Compound Financial Instruments Interest, dividends, losses and gainsOffsetting a financial asset and a

financial liability

9/12/2005

IAS 32

IFRS 7 replaces all the disclosure requirements of IAS 32 and puts all financial instrument disclosure under one standard

IFRS 7 provides information about significant financial instruments for an entity’s financial position and performance

New disclosures for financial instruments

9/12/2005

IAS 39 – Financial Instruments Recognition and Measurement

What is the standard about

Key featuresDisclosure

requirements

9/12/2005

IAS 39

Where are we?Many revisions – however main changes

are: Oct 1984 - Exposure draft issued Jan 2005 - Effective date of IAS 39

(Revised 2004) June 2005 - Amendment for Fair Value

option Aug 2005 - Amendment for Financial

Guaratee Contracts

9/12/2005

IAS 39 – Financial Instruments Recognition and Measurement

IASB - IAS 39 Financial Instruments: Recognition and Measurement was issued in December 2003 and is applicable for annual periods beginning on or after 1 January 2005

IAS 39 prescribes principles for recognizing and measuring all types of financial instruments with some exceptions

9/12/2005

IAS 39

The following are outside the scope of IAS 39

Rights and obligations under leases (IAS 17)*

Financial guarantee contracts & weather derivatives (if specific IFRS 4)

Financial instruments that meet the definition of own equity under IAS 32

Share based payments (IFRS 2)

9/12/2005

IAS 39

The following are outside the scope of IAS 39 Interests in subsidiaries, associates and joint

ventures covered under IAS 27, 28 & 31 Employee benefits (IAS 19) Insurance contracts (IFRS 4)* Contracts for contingent consideration in a

business combination (IFRS 3) Certain loan commitments

9/12/2005

IAS 39

IAS 39 – Financial Instruments coverRecognition and derecognition

Measurement and impairment

Hedging

9/12/2005

IAS 39

Recognition of financial instrumentsFinancial assets

Financial Liabilities

Derivatives

9/12/2005

IAS 39

Derivatives“its value changes in response to the change

specified interest rate, financial instrument price, commodity price, foreign exchange rate, price index, or other variables;

requires no initial investment, or one that is smaller than would be required for a contract with similar response to changes in market factors; and

That is settled at a future date.

9/12/2005

IAS 39

Initial Recognition:“Recognize a financial asset or liability

when and only when the entity becomes a party to the contractual provisions of the instrument.” Any examples?

9/12/2005

IAS 39 – Key Features

Classification of financial assets

Available-for-sale financial assets

(AFS)C

Financial assets at fair value through profit or loss

Loans and receivables

Held-to-maturity investments

9/12/2005

IAS 39 – Key Features

Financial assets at fair value through profit or loss

Held for trading

Held for trading

Designated at inception

Designated at inception

9/12/2005

IAS 39 – key Features

Loans and receivables

Non-derivative financial assetsNot quotedNot intention of trading

Non-derivative financial assetsNot quotedNot intention of trading

9/12/2005

IAS 39 – Key Features

Held-to-maturity investments

Non-derivative financial assetsFixed or determinable payments & fixed maturityNo intention of trading Able to hold to maturity

Non-derivative financial assetsFixed or determinable payments & fixed maturityNo intention of trading Able to hold to maturity

Special Tainting Rules

9/12/2005

IAS 39 – Key Features

Available-for-sale financial assets

(AFS)

All financial assets that

are not classified in

another category are

classified as available-for-sale.

All financial assets that

are not classified in

another category are

classified as available-for-sale.

9/12/2005

IAS 39 – Key Features

Financial Liability Classification

At fair value through profit or loss

Other financial liabilities

Held for tradingDesignated at

inception

9/12/2005

IAS 39 – key FeaturesDerecognition

Financial Assets Has the entity

transferred the rights to receive cash flow from the asset

Has the entity transferred substantially all the risks and rewards from the asset

Does the entity retain control over the asset

Financial Liabilities Has the liability been

discharged, cancelled or expired

9/12/2005

IAS 39 – Key Features

Measurement

Financial assets/

liabilities at fair value through profit or loss

Loans and receivables

Other liabilities

Held-to-maturity investments

Available-for-sale financial assets

(AFS)C

At FV through profit or loss

At amortised cost

At FV through equity

9/12/2005

IAS 39 – Key Features

Measurement

Fair Value – the amount for which an asset could be exchanged or a liability settled between knowledgeable, willing parties in an arm’s length transaction

Amortized Cost – the amount at which the financial asset or liability is measured at initial recognition minus principal repayments, plus or minus the cumulative amortization using the effective interest rate method of any differences between the initial amount and the maturity amount adjusted for impairment

9/12/2005

IAS 39 – Key Features

Impairment

“An entity shall assess at each balance sheet date whether there is any objective evidence that a financial asset is impaired.”

9/12/2005

IAS 39 – key Features

Objective evidence

Disappearanceof an active market because of financial

difficulties

High probabilityof bankruptcy

Adverse change inpayment status or national

or local economic factor

Granting of a concession to the

borrower

Breach of contract, such as default or

delinquency ininterest or principal

Significant financialdifficulty of the issuer

or obligator

9/12/2005

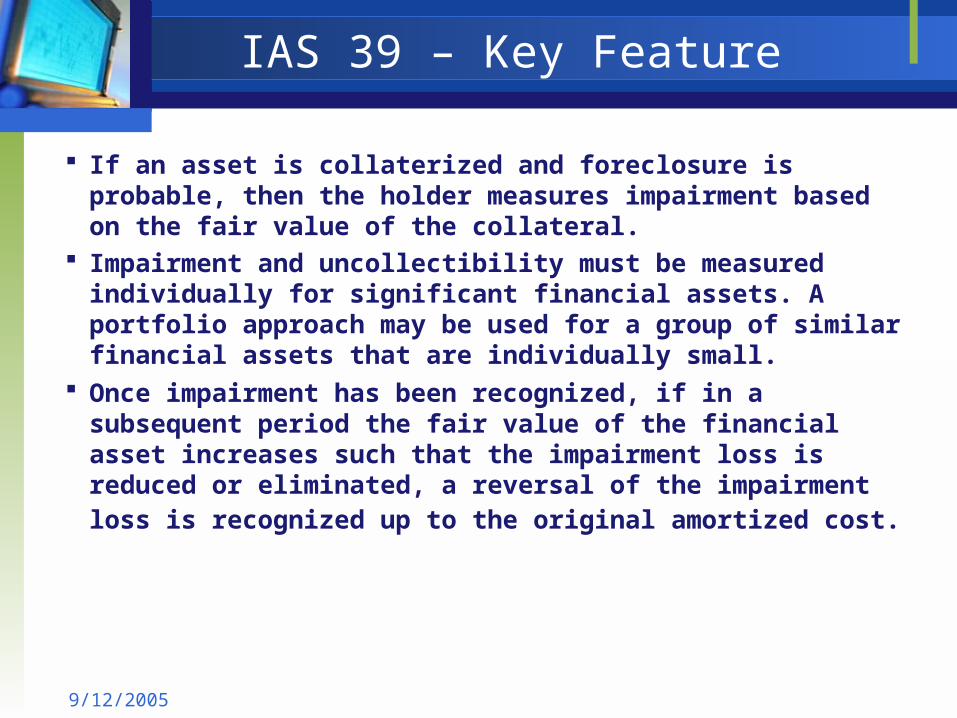

IAS 39 – Key Feature

If an asset is collaterized and foreclosure is probable, then the holder measures impairment based on the fair value of the collateral.

Impairment and uncollectibility must be measured individually for significant financial assets. A portfolio approach may be used for a group of similar financial assets that are individually small.

Once impairment has been recognized, if in a subsequent period the fair value of the financial asset increases such that the impairment loss is reduced or eliminated, a reversal of the impairment loss is recognized up to the original amortized cost.

9/12/2005

IAS 39 – Key Features

Larger Loans Identify individually significant loans and review them

for impairment separately (need to estimate future cash flows)

If these loans impaired, measure and record a separate impairment loss. Do not recognise any further losses.

If they are not impaired, should include them into group of similar loans for further impairment assessment

All remaining (small) loans should be assessed on a portfolio basis

9/12/2005

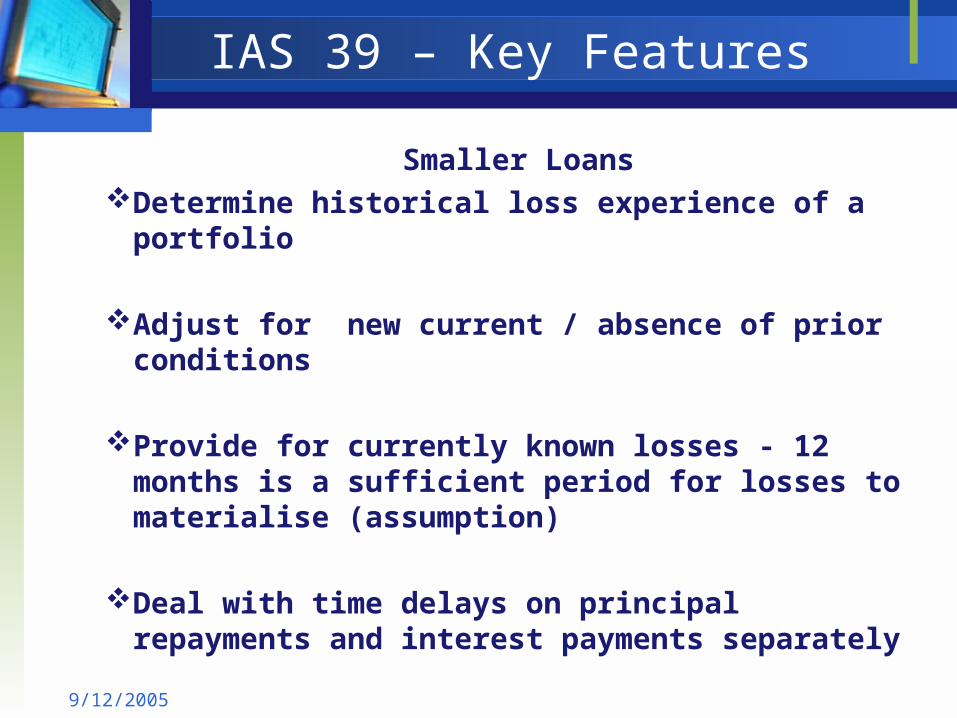

IAS 39 – Key Features

Smaller LoansDetermine historical loss experience of a portfolio

Adjust for new current / absence of prior conditions

Provide for currently known losses - 12 months is a sufficient period for losses to materialise (assumption)

Deal with time delays on principal repayments and interest payments separately

9/12/2005

IAS 39 – Key Features

ImpairmentAFS - Impairment loss recognized directly

in equityFinancial assets carried at cost –

difference between the carrying amount of the asset and present value of estimated future cash flows discounted at the current market rate for similar assets.

9/12/2005

IAS 39 – Key FeaturesLoan impairment testing

Loan 1

Collateral PVPrincipal

balance O/SIAS

InterestIAS

(P+I)IAS 39

ProvisionEntity’s

Provision

Proposed Write

(down)/up

Loan 2

2,616

4,412

1,420

3,270

730

3,700

49

0

779

3,700

0

430

73

400

(73)

30

Example 2 - collaterized loans

IAS 39 interest = Principal Balances o/s * (original interest rate)

IAS 39 provision = Difference between IAS 39 (P+I) and the present value

Proposed write down = Difference between IAS39 provision and entity’s provision

9/12/2005

IAS 39 – Key FeaturesLoan impairment testing

Original Loan amount - $20,000

loan is impaired in T2 – amortized cost is $16K

effective interest rate – 10% - fixed rate

Cash flows expected – T1 T2 T3 T4$7K $7K $5K* $4K*

Example 1 – non collateralized loans

PVIFA 10%, 2 years 0.909 .826

PV of future cash flows $4.5K + $3.3K = $7.8K

Loss = $16K-$7.8K = $8.2K

* - based on the bank’s determination of the monies they expected to collect from the customer

9/12/2005

IAS 39 – Key Features

The loss is the difference between carrying amount and expected future cash flows discounted at the original effective interest rate. (non variable rate loans)

Reduce carrying amount to its recoverable amount directly or through allowance account.

Include loss in net profit/loss for the period.

Steps in determining the loan loss provisions

9/12/2005

IAS 39 – Key FeaturesPractical implications

No “general provisions just in case”

Both timing and amount of loan losses are important

Larger loans: discounted cash flow model should be

used

Smaller loans: need to have sufficient statistical data

of historical losses

Collateral – at fair value

9/12/2005

IAS 39 – Key Features

The calculation of the loss is the difference between the assets carrying amount and the present value of the expected future cash flows.

The financial instrument’s original effective interest rate is the rate to be used for discounting.

If a loan receivable, has a variable interest rate the discount rate for measuring a recoverable amount is the current effective rate. [IAS 39.111]

Any impairment loss is charged to net profit or loss for the period.

9/12/2005

IAS 39 – Key Features

HTM portfolio is tainted if management sold or

reclassified as AFS, before maturity, during the current

or two preceding years more than an insignificant

amount of HTM assets (Vs total HTM category)

There are three exceptions to the rule: The sale is close to maturity; Collected substantially all of original principal through

schedule payments; Isolated event beyond entity’s control may not invoke

tainting.

9/12/2005

IAS 39

What application Issues have you experienced?

9/12/2005

IFRS 4 – INSURANCE CONTRACTS

AN OVERVIEW

9/12/2005

IFRS 4

Where are we ?

March 2004 - IFRS 4 issuedJan 2005 - Effective Date of IFRS 4Aug 2005 - Amendment to IFRS 4 for

financial guarantee contracts

9/12/2005

IFRS 4

First Guidance – not the Last

Driven by urgent need to provide guidance for adoption in Europe in 2005

Phase II to be issued later

9/12/2005

IFRS 4

Definition of an Insurance Contract :

An insurance contract is a "contract under which one party (the insurer) accepts significant insurance risk from another party (the policyholder) by agreeing to compensate the policyholder if a specified uncertain future event (the insured event) adversely affects the policyholder."

( IASB)

9/12/2005

IFRS 4

Significant Insurance Risk If the insured event could cause an insurer to

pay significant additional benefits

The additional benefit refers to amounts that exceed those that would be payable if no insured event occurred – includes claim handling and claims assessment costs.

9/12/2005

IFRS 4

TEMPORARY EXEMPTION FROM OTHER IFRS’s

Exemption applying the criteria IAS 8 (10-12) in developing an accounting policy where no IFRS specially applies.

IFRS 7 exempts an insurer from applying those criteria for insurance contracts that it issues and Re-insurance contracts that it holds.

9/12/2005

IFRS 4

The IFRS however Prohibits provisions for possible claims under contracts

that are not in existence at the reporting date (such as catastrophe and equalisation provisions).

Requires a test for the adequacy of recognised insurance liabilities and an impairment test for reinsurance assets.

Requires an insurer to keep insurance liabilities in its balance sheet until they are discharged or cancelled, or expire, and prohibits offsetting insurance liabilities against related reinsurance assets.

(Source: Deloittes’s IAS plus)

9/12/2005

IFRS 4

Liability Adequacy TestRequired to assess at the end of each

period the adequacy of its recognised insurance liabilities using current estimates of future cash flows under its insurance contracts.

Any shortfalls are recognised immediately in profit or loss.

(suggested that an actuary be used).

9/12/2005

IFRS 4

Unbundling of Deposit Components

Some insurance contracts contain both an insurance component and a deposit component . In some cases, the insurer is required or permitted to unbundle those components

9/12/2005

IFRS 4

UNBUNDLINGRequired if:

The insurer can measure the deposit component separately without considering the insurance component and

The insurers accounting policies do not otherwise require it to recognise all obligations and rights arising from the deposit component

9/12/2005

IFRS 4

Unbundling permitted but not required : If the depost liabilities can be measured separately as

above but its accounting policies requires it to recognise all obligations and rights arising from the deposit component

Unbundling is prohibited : If an insurer cannot measure the deposit component

separately.

IAS 39 is applied to the deposit component

9/12/2005

IFRS 4

Other Disclosures RequiredNature and extent of risks arising from

insurance contracts Objectives, policies and processes for

managing riks rising from insurance contracts

Sensitivity to insurance risk Concentrations of insurance risk Actual claims compared to previous

estimates

9/12/2005

IFRS 4

Other Disclosures Required Credit risk, liquidity risk, and market risk as

under IFRS 7

9/12/2005

IFRS 7

What are the application Issues?

9/12/2005

Closing Remarks