June 2011 Investor Presentation - TransAlta MWh until 2020 13 2000 2001 2002 2003 2004 2005 2006...

28

1 June 2011 Investor Presentation.

Transcript of June 2011 Investor Presentation - TransAlta MWh until 2020 13 2000 2001 2002 2003 2004 2005 2006...

1

June 2011 Investor Presentation.

2

This presentation may contain forward looking statements, including statements

regarding the business and anticipated financial performance of TransAlta Corporation.

All forward looking statements are based on our beliefs and assumptions based on

information available at the time the assumption was made. These statements are not

guarantees of our future performance and are subject to a number of risks and

uncertainties that may cause actual results to differ materially from those contemplated

by the forward looking statements. Some of the factors that could cause such

differences include cost of fuels to produce electricity, legislative or regulatory

developments, competition, global capital markets activity, changes in prevailing interest

rates, currency exchange rates, inflation levels, unanticipated accounting or audit issues

with respect to our financial statements or our internal control over financial reporting,

plant availability, and general economic conditions in geographic areas where TransAlta

Corporation operates. Given these uncertainties, the reader should not place undue

reliance on this forward looking information, which is given as of this date. The material

assumptions in making these forward looking statements are disclosed in our 2010

Annual Report to shareholders and other disclosure documents filed with securities

regulators.

Unless otherwise specified, all dollar amounts are expressed in Canadian dollars.

Forward looking statements

3

TransAlta at a glance

Canada’s largest publicly traded wholesale power

generator & marketer with over 100 years of

operating experience

Over 8,000 MW strategically positioned in

Canada, Western U.S. and Australia

2,100 MW of renewable energy

3,100 MW of new assets added during last ten

years

Revenues of ~$3 billion generated from an asset

base of over $9 billion

Enterprise value of ~ $10 billion with a market cap

of ~$5 billion

Investment grade credit ratings

Listed on Toronto and New York stock exchanges

Coal:

4,317 MW

Gas:

1,813 MW

Hydro:

912 MW

Wind:

1,064 MW

Geothermal:

164 MW

4

Why TransAlta

Diversified generation portfolio located in growing markets Diversified portfolio with over 75 facilities spanning multiple fuels and geographies

High quality resource base supporting low cost operations and future growth

Well positioned in markets with strong market fundamentals

Attractive yield supported by significant cash flow 5.5% dividend yield

$800 - $900 million in funds from operations with ~$200 million of free cash

Highly contracted with upside potential to rising power prices

Significant incremental EBITDA post 2020 when Power Purchase Arrangements roll-off

Proven track record for growth with significant upside potential

3,100 MW added in the last 10 years with 50% increase in gross margins per MWh

Significant growth pipeline across multiple fuels and geographies

Environmental leadership mitigates risk and provides growth optionality

Financial strength to deliver Investment grade ratings

$2 billion of committed credit facilities

Significant cash flow and favourable access to capital

Delivering shareholder value through yield and growth

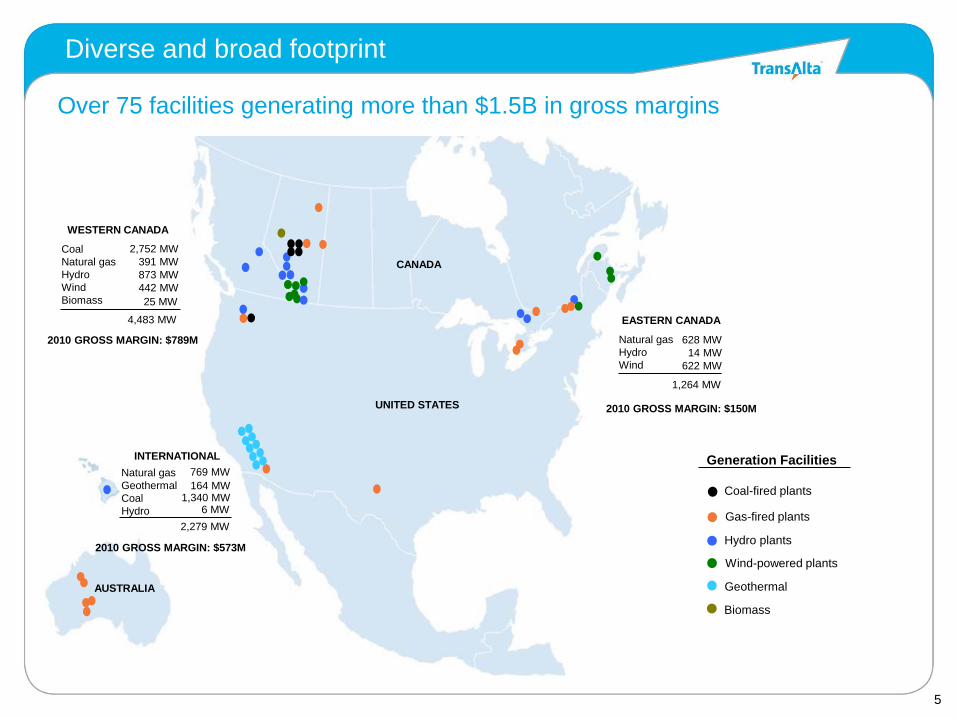

5

INTERNATIONAL

14 MW

AUSTRALIA

UNITED STATES

CANADA

Over 75 facilities generating more than $1.5B in gross margins

Diverse and broad footprint

WESTERN CANADA

Coal

Natural gas

Hydro

Wind

Biomass

2,752 MW

391 MW

25 MW

442 MW

873 MW

4,483 MW EASTERN CANADA

Natural gas

Hydro

Wind

628 MW

622 MW

1,264 MW

Natural gas

Geothermal

Coal

Hydro

769 MW

164 MW 1,340 MW

6 MW

2,279 MW

Hydro under development

Generation Facilities

Coal-fired under construction

Coal-fired plants

Gas-fired plants

Hydro plants

Wind-powered plants

Geothermal

Biomass

Wind under development

2010 GROSS MARGIN: $789M

2010 GROSS MARGIN: $150M

2010 GROSS MARGIN: $573M

6

Western U.S.

Strategically well positioned for growth

Alberta

Sources: AESO; NERC

Rest of Canada Australia

Growing at 2% - 4% per year; requiring 200 – 400

MW of new capacity each year

Tightening reserve margins driving higher power prices

TransAlta is largest player with 35% of the market capacity

Significant development opportunities in gas and renewables

Long-term investment opportunities of $9+ billion

Well positioned with more than 1,500 MW of coal

and geothermal

High quality geothermal resource supporting significant development opportunities

Opportunities to grow renewable and gas-fired generation through development and acquisitions

Recent Washington State bill allows for long-term contracting

Renewable and gas-fired assets located in B.C.,

Ontario, Quebec and New Brunswick

Well positioned for additional development and acquisitions

Highly reliable supplier of electricity to the mining

industry

Significant growth potential as mining industry and general economy expands

7

5%

10%

15%

20%

25%

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

$30

$40

$50

$60

$70

$80

$90

$100

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Actual Forecast

Reserve Margins2 3

1% load growth

2% load growth

3% load growth

2 Figures as of May 4, 2011

Alberta Power Prices2

Actuals Current Market

+$1 / GJ = ~$8 - $10 / MWh

Incumbent generator in AB where demand is growing at 2 - 4% per year

3 Includes transmission; does not include assumptions around announced

facilities, only facilities under construction

Alberta: Strong market fundamentals

$/MWh

Oil sands recovery driving load growth; >$2 trillion to

be invested in the oil sands between now and 20353

0

1,000

2,000

3,000

4,000

5,000

6,000

2011 2013 2015 2017 2019 2021 2023 2025 2027 2029 2031

Canada’s 45 year plan provides significant future

investment opportunities in Alberta alone

Alberta Long-term Investment

Opportunities

(TransAlta Fleet Only)

TransAlta AB Portfolio Growth

Replacement Opportunity TransAlta Coal

MW Total growth opportunity: 4,800 MW

Total investment opportunity1: $9 - $13 B

1 Based on 45 year coal-life and $1,800 - $2,800 per KW

8

0%

50%

100%

150%

200%

250%

300%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

0%

5%

10%

15%

20%

Cumulative TSR Dividend Yield

Yield2

Strong cash flow and stable yield and has created significant shareholder value

throughout market cycles

Attractive yield and value

155% cumulative TSR

9% compound annual growth rate

3.0% - 5.8% dividend yield

TSR1

1 Based on a $100 investment made at Dec. 31, 1999 and assumes the reinvestment of dividends 2 Based on the closing share price on the first day of each year

Total Shareholder Return & Dividend Yield

2000 - 2010

9

Eastern Canada Western Canada

United States Australia

Multiple

Geographies Fuel

Diversification

We maintain a low-to-moderate risk profile through fuel diversification, multiple

geographies, and a solid contractual base

= Low-to-moderate risk profile

Highly

Contracted

+ + Long-term

& PPAs

70%

Merchant

Short &

medium

term

Low-to-moderate risk

24%

58%

14% 4%

2011e

MW by

region

10

$-

$250

$500

$750

$1,000

2002

2003

2004

2005

2006

2007

2008

2009

2010

Dividends

2011e

Base operations have generated strong cash flow and excellent

dividend coverage

Targeting $800 - 900 million of FFO in 2011

Solid cash flow growth

FFO

$M

Funds from Operations (FFO)

25 – 35% Payout

Ratio

Sustaining

Capex

Free cash

flow

$800 - $900M

11

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

2011 2012 2013 2014

Contracted Open

$0

$50

$100

$150

$200

$250

1 2 3 4 5

Total Portfolio Contractedness Avg. Incremental EBITDA From Higher

Prices (2011 – 2014)1

$MM

1 Relative to a base of $50/MWh in Alberta and $35/MWh in the PacNW 2 Based on a 10% ROCE, $1,500 – $3,000 per KW and a 30 year depreciation

$55

$40

$60

$45

$65

$50

$70

$55

$75

$60

Alberta:

PacNW:

MWs

At a 10% ROCE, 200 MW

growth can add another

$40 - $80 million in

additional EBITDA2

Highly contracted with upside potential

Contracting strategy provides solid downside protection while maintaining

leverage to power price recovery

2013 2014 2012 2011

Contracted

91% 75% 84% 70%

Open

70% base Upside potential

12

-

500

1,000

1,500

2,000

2,500

3,000

3,500

1

$-

$250

$500

$750

$1,000

$1,250

$1,500

$1,750

$60 $70 $80 $90 $100 $110 $120

Est.

EBIT

$MM

Estimated Incremental EBITDA in 2021

$750 - $1,250 M1

$750

$1,000

$1,250

Alberta Power Prices 2021 ($/MWh)

1 Includes Sundance units 3 – 6, Keephills, Sheerness, and Alberta Hydro facilities

End of PPAs will provide significant EBITDA upside as production reverts

back to TransAlta

2 Minimum power prices required for new NGCC facility

2

Significant long-term upside potential post 2020

Facility MWs

under PPAs1

MW

2011 - 2020

Over 3,000 MWs under PPAs

currently priced at $30 - $35

per MWh until 2020

13

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011e

$31.53

$20.96

Coal Gas Renewables

Generation gross margin

per MWh produced

We have diversified our fuel mix and more than doubled our renewable portfolio;

diversified growth & optimization have driven a 50% increase in gross margins

Significant growth track record

73%

15%

12% 26%

52%

22%

Total Portfolio Fuel Mix (MW)

6,870 MW

8,270 MW

1,900 MW replaced

+ 1,400 MW pure growth =

3,300 MW total growth

14

2000 2005 2010

Hydro Wind Geothermal

800 MW

1,117 MW

2,121 MW

Growth in renewables

We have significantly diversified and increased our renewable portfolio

Renewable Portfolio Capacity

High quality resource with

significant development potential

Canada’s largest generator of

wind power

Alberta’s largest generator of

hydro power

15

Bone Creek Keephills 3 Keephills 1 &

2 Uprates

Sundance 3

Uprate

New

Richmond

Location British Columbia Alberta Alberta Alberta Quebec

Type Hydro Supercritical Coal Efficiency

Uprates

Efficiency Uprate Wind

Size 19 MW 225 MW 1 46 MW

(23 MW each)

15 MW 66 MW

Total Project Cost $48 MM 2 ~$1,015 MM 3 $68 MM $27 MM $205 MM

Unlevered after tax IRR 10%+ 10%+ 15%+ 15%+ 2 – 4% above

Cost of Capital

Commercial Operations

Date

Q2 2011 Q3 2011 Q4 2012 4 Q4 2012 Q4 2012

Contract Status LTC Merchant Merchant Merchant Quebec PPA

On time / On budget Tracking Tracking Tracking Tracking Tracking

1 450 MW gross size 2 Bone Creek’s capital spend prior to the acquisition was $23 MM which does not form part of our total project cost 3 Keephills 3 capital spend increased from $988 MM to $1,015 MM and its COD was revised from Q2 2011 to Q3 2011 due to testing 4 Keephills unit 1 uprate has been moved to 2012

TransAlta’s growth investments deliver long-term sustainable cash flow and

earnings growth

Current growth projects

16

0

1,000

2,000

3,000

4,000

5,000

Alb

ert

a

Oth

er

Canada

Unite

d

Sta

tes

Austr

alia

Geothermal

Wind

Gas Fired

Hydro

Significant future growth opportunity

Replacement Opportunity

MW

Significant near, medium and long-term development opportunities

Development opportunities

Gas fired

Hydro

Geothermal

Wind

17

We have many options for growth

Strong competitive advantages in multiple fuels and technologies

Permitted generation

sites with access to

water & transmission

100 years experience in hydro,

20+ years in natural-gas fired

generation

We are not dependent on a single fuel source or a single region

Carbon Capture and Storage supports the future of coal and provides

the opportunity to utilize massive economic coal reserves in Alberta

Canada

U.S.

18

TransAlta is recognized for outstanding environmental stewardship;

competitively positioned to mitigate emission costs

Cost pass through

under change-in-law

provisions

Continuous

improvement at

existing facilities

Active acquisition of

lower cost offsets

(with Technology Fund

as backstop)

Pursuit of clean

combustion technology &

renewables

Emissions

Management

Environmental leadership

Named to the Jantzi list of Canada’s 50 most responsible corporations

Named as one in 15 Carbon Disclosure Leaders in Canada

2010 Achievements

19

$-

$0.5

$1.0

$1.5

$2.0

$2.5

Q1 2011

Credit Lines Utilized Credit Lines Available

Investment Grade Credit Ratios

Financial strength to grow

$B

Dec. 31

2010

Mar. 31

2011

Target

Range

Cash flow to debt

19.6%

20.7%

20 – 25%

Cash flow to interest

4.6x

4.7x

4 – 5x

Debt to capital

53.1%

52.8%

55 – 60%

Committed Credit Lines

Investment grade credit ratings and significant liquidity provided through $2B of

committed credit lines

20

Financial strength

Optimal balance between debt, dividends, and growth

Balance sheet

enhancement

Growth

Dividends

Balanced capital allocation and disciplined investment decisions supports value

creation through market cycles

Provide shareholders with strong, sustainable dividend

Remain disciplined in how we manage our balance sheet

Disciplined growth targeting unlevered after-tax IRRs of 2 – 4% above

cost of capital

Divest or improve non-core and underperforming assets:

Meridian - sold in 2010

Sarnia - renegotiated new LTC in 2009

Mexico - sold in 2008

Portfolio

Optimization

21

Strategically positioned in markets with strong growth opportunities

Strong and stable cash flow growth

Highly contracted with leverage to power price recovery

Significant upside when Alberta PPAs roll off in 2020

Financial strength and stability

Near and long-term value driven by our unwavering commitment to provide strong

yield and growth

Why invest?

22

Additional information

23

Event:

Late in 2010, TransAlta removed from service

its Sundance units 1 & 2 due to boiler

conditions and declared force majeure.

Subsequently, in early 2011 TransAlta issued a

notice of termination for economic destruction.

The PPA Buyer has disputed the notice of FM

and termination for destruction.

Current status:

An arbitration panel has been set and currently

the arbitrators are dealing with procedural

issues. The time frame to complete the

arbitration is still unclear at this time.

TransAlta continues to work with the PPA

Buyer and the Balancing Pool under the

processes established within the PPA.

Sundance Units 1 and 2, 560 MW of coal-fired generation, removed from

TransAlta’s portfolio and the Alberta market

Sundance Units 1 and 2 facts

Impact to TransAlta:

TransAlta is entitled to recover the net book value as

specified in the PPA if these matters are resolved in its

favour

24

Benefits to TransAlta:

Ability to enter into long-term contracts

• Utilities incented to enter into contracts

• Process for approving contracts streamlined

• Centralia is one of the lowest cost providers of

electricity in the region

Protected from any future State GHG

requirements and more stringent NOx/SOx

requirements

Provides date certainty to allow TransAlta to

optimize operation and capex

Expedited permitting for a replacement gas plant

Future gas plant exempt from future State GHG

regulations

Washington State’s bill regarding Centralia poses many benefits to TransAlta

Centralia facts

25

0

250

500

750

1,000

1,250

1,500

1,750

2009 2010

88.9

85.1

80

82

84

86

88

90

2009 2010

Availability (%)

2010 Operational performance and fuel mix

4%

Increase

Gas Renewables Coal

18%

30%

52% 48%

28%

24%

$M Comparable Generation Gross

Margins by Fuel Type

*Excludes the impact of mark-to-market movements

*

26

$888

$965

2009 2010

$0.90

$0.98

$0.84

$0.88

$0.92

$0.96

$1.00

2009 2010

$729

$783

650

700

750

800

2009 2010

M

M

2010 Financial performance

Comparable EBITDA

Funds from Operations Comparable EPS

9%

Increase

7%

Increase

9%

Increase

M

M

27

0

75

150

225

300

375

450

Q1 2010 Q1 2011

92.7

91.4

86

88

90

92

94

Q1 2010 Q1 2011

Q1 2011 Operational performance and fuel mix

Availability (%) Comparable Generation Gross

Margins by Fuel Type

Gas Renewables Coal

25%

21%

54%

25%

25%

50%

**

$M

*Excludes the impact of Sundance Units 1 and 2

*

**Includes comparable gross margin from finance

lease and equity investment assets

28

$0.27

$0.34

Q1 2010 Q1 2011

$249

$287

Q1 2010 Q1 2011

$194

$226

Q1 2010 Q1 2011

Q1 2011 Financial performance

Comparable EBITDA

Funds from Operations Comparable EPS

17%

Increase

15%

Increase

26%

Increase

M

M

M

M