June 11, 2021 S tock TALES

9

Stock Tales are concise, holistic stock reports across wider spectrum of sectors. Updates will not be periodical but based on significant events or change in price. Stock _____ TALES June 11, 2021

Transcript of June 11, 2021 S tock TALES

Stock Tales are concise, holistic stock reports across wider spectrum of sectors. Updates will not be periodical but based on significant events or change in price.

Stock_____

TALES

June 11, 2021

ICIC

I S

ecurit

ies –

Retail E

quit

y R

esearch

Stock T

ale

s

June 11, 2021

CMP: | 967 Target: | 1200 (24%) Target Period: 12 months

Just Dial Ltd (JUSDIA)

BUY

Key beneficiary of changing digital trend…

Just Dial (JDL) began operations in 1996 by offering local search services

under the Justdial brand. The company generates revenues from advertisers

who list themselves with JDL on various subscription and fee-based

packages. They pay fixed monthly or annual fees and can select from

premium and non-premium packages. We believe the company will be a key

beneficiary of a shift of advertising to the digital medium. This, coupled with

the company’s launch of B2B platform will be a key revenue driver for JDL

in the long run. This is expected to make the company a formidable player

in the B2B, B2C segments leading to revenue, PAT CAGR of 22%, 21%,

respectively, in FY21-23E.

B2B next growth engine

India’s MSME segment is digitally under penetrated. However, we expect

this scenario to change led by Covid-19. There is now increased need for a

digital medium to boost business growth. Further, although the B2B online

market has seen an influx of players, the paid subscribers as a percentage

of total MSME is just 1.3%. This represents tremendous scope for existing

and new players to grow. We believe JDL’s B2B platform JD Mart has

potential to become a significant player in this segment, going forward. The

company has shown a strong commitment to the new platform, by

committing to spend | 100-110 crore for branding & awareness, free leads

and hiring leaders. JDL also plans to provide end-to-end solutions like

logistics, financing, insurance & payment facilities to improve customer

stickiness. This will also enable the company to have two revenue streams

in the long run viz. subscription revenues and transaction-linked revenues.

Apart from these initiatives, JDL currently has 7-8 million listings in the B2B

segment. We believe the company can leverage this for cross sell and upsell.

This, coupled with the JDL’s large sales force (~8000) makes it well poised

to capture the burgeoning B2B market and become a significant player in

this segment.

B2C to improve with easing of lockdowns

We expect revenues to improve with easing of lockdowns and increase in

digital penetration. In addition, the company is also promoting download of

the JD app by providing JD cash against download & referrals. We believe

these initiatives, coupled with an improvement in realisation & increase in

digitisation will drive B2C business in the longer run.

Valuation & Outlook

Covid and changing consumer behaviour have led to increase in

virtualisation of business. Enterprises now have an omni channel presence

(in physical & digital world). JDL’s B2B and B2C platforms are well placed to

capture this burgeoning demand. Hence, we have a BUY recommendation

on the stock with a target price of | 1,200 (24x FY23E EPS).

Key Financial Summary s

Key Financials FY19 FY20 FY21 FY22E FY23E CAGR (FY21-23E)

Net Sales 892 953 675 773 997 21.5%

EBITDA 229 273 155 124 279 34.3%

EBITDA Margins (%) 25.7 28.6 22.9 16.0 28.0

Net Profit 207 272 214 175 311 20.5%

EPS (|) 31.9 42.0 33.0 28.3 50.3

P/E 30.3 23.0 29.3 34.2 19.2

RoNW (%) 20.7 21.1 16.9 12.9 20.6

RoCE (%) 27.4 25.7 19.0 14.9 24.2

Source: Company, ICICI Direct Research

Particulars

Particular Amount

Market Cap (| Crore) 5,981.9

Total Debt (| Crore) -

Cash and Invests (| Crore) 1,572.8

EV (| Crore) 4,409.0

52 week H/L 1063/33

Equity capital 61.9

Face value 10.0

Price Performance

0

500

1,000

1,500

5,000

7,000

9,000

11,000

13,000

15,000

17,000

19,000

Jun-18

Sep-1

8

Dec-18

Mar-19

Jun-19

Sep-1

9

Dec-19

Mar-20

Jun-20

Sep-2

0

Dec-20

Mar-21

Jun-21

Nifty (L.H.S) Price (R.H.S)

Key Risk

Inability of the company to make

significant inroads into B2B market

will adversely impact its growth

prospects

Inability to improve margins will

impact its profitability

Research Analyst

Devang Bhatt

ICICI Securities | Retail Research 2

ICICI Direct Research

Stock Tales | Just Dial Ltd

Company Background

Just Dial began its operations in 1996 by offering local search services under

the Just Dial brand. The website was launched in 2007. The main revenue

generation for JD comes from the advertisers who list themselves with the

company on various subscription and fee-based packages. They pay fixed

monthly or annual fees and can select from premium and non-premium

packages. Based on the package, the customer gets priority listing. The

pricing varies as per location, city and listing placement.

Apart from listing services, the company provides, search plus (which helps

in booking tickets, flight tickets, hotel booking, etc), website service (it helps

SMES in developing websites, mobile ready app & payment capability), JD

pay (which helps in payment transaction), ratings (helping SMEs get rating

& reviews) and JD social (a social media platform with social media type

content & helping in boosting visibility for SMEs). Revenue wise, 95% of

revenues is from listing (| 909 crore), 2% from website development (| 21

crore), 2% from review & rating certification and 1% from transaction fees

and commission income on search plus services. Apart from these

businesses, the company is foraying into the B2B business with JD Mart.

Exhibit 1: Revenue break-up

Search related revenues,

95%

Software and

website …

Review and

rating services,

2%

Search plus

services, 0

Source: company, ICICI Direct Research

Exhibit 2: Paid campaign trend

368.8

435 445

501

536

457

2

18

2

13

7

-15

-20

-15

-10

-5

0

5

10

15

20

0

100

200

300

400

500

600

FY16 FY17 FY18 FY19 FY20 FY21

in %

in 000

Paid campaigns (in 000) YoY growth

Source: company, ICICI Direct Research

ICICI Securities | Retail Research 3

ICICI Direct Research

Stock Tales | Just Dial Ltd

Exhibit 3: Deferred revenue trend

211

274

332

405

336 330

0.5

30

21 22

-17

-2

-20

-10

0

10

20

30

40

0

50

100

150

200

250

300

350

400

450

FY16 FY17 FY18 FY19 FY20 FY21

in %

in | crore

Deffered revenues YoY growth

Source: company, ICICI Direct Research

Exhibit 4: Employee strength

3464

1298

3531

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

FY21

Tele Sales Feet on street (marketing) Feet on street (JDA)

Source: company, ICICI Direct Research

Exhibit 5: Unique visit split (in %)

Mobile, 82%

Web, 13%

Voice, 5%

Source: company, ICICI Direct Research

ICICI Securities | Retail Research 4

ICICI Direct Research

Stock Tales | Just Dial Ltd

Investment Rationale

B2B platform long term growth driver

Out of the ~20 million MSMEs in India, just 32% were digitally connected in

2017 and 17% used the internet for business purposes. On the other hand,

54% of small businesses in the US used e-mail for business in 2017 while

51% had their own website. However, we expect this scenario to change

with growth in internet penetration throughout India along with increased

accessibility and affordability of smartphones. In addition, Covid 19 is

expected to further boost digitisation of MSMEs. In addition, a B2B digital

platform not only helps buyer & sellers with more opportunities but also

helps them in reducing cost like distributor margins and other commissions.

This represents tremendous scope for an online B2B player like JD Mart.

Although IndiaMart is a leader in the B2B segment with ~1,52,000 paid

subscribers, the overall market of paid subscribers as a percentage of total

MSME is just ~1.3%. This represents tremendous scope for existing and

new players to grow.

JDL, currently, is in its initial phase of branding and making JD Mart

remunerative. Hence, the company is planning to spend ~ | 100-110 crore

(of which ~| 50 crore was spent on IPL) on JD Mart. The aim is to push for

higher downloads and brand awareness. Once the download is done (either

proactively or via salesforce), the company plans to give free leads worth

~| 20,000-30,000 for 30-60 days and free catalogues to boost the network

effect.

Further, in order to make the app monetisable the company is planning to

provide logistics service (with 10-11 logistic players), payment facility,

working capital financing and insurance services. This will help in providing

end-to-end solution to customers and also help in increasing stickiness of

customers. In addition, JDL will have two revenue streams in the long run

viz. subscription revenues and transaction-linked revenues.

Apart from advertisement, the company currently has 7-8 million listings

(out of 30 million listings) in the B2B segment. We believe the company can

leverage this for cross sell as well as upsell. This, coupled with the

company’s large sales force (~8000) will further help drive new sales in JD

Mart. In addition, JDL has on-boarded a sales & marketing head for its B2B

business and identified a 500-600 member dedicated sales team for B2B with

focus on metros and tier-1 cities like Delhi NCR, Mumbai, Ahmedabad, Surat,

Rajkot, Jaipur, Pune. We expect JD Mart to generate revenues from FY23E

onwards. However, meaningful contribution to topline is expected to be

seen in subsequent years.

B2C business to improve in H2FY22E

In the near term, we expect revenues to be impacted due to a decline in new

sales (led by lockdown). In addition, we expect margins to be impacted by

increase in advertising expenses (| 50 crore to promote JD Mart). However,

we expect revenues to improve with easing of lockdown and increase in

digital penetration. In addition, JDL is also promoting download of JD app

by providing JD cash against download & referrals. JD Cash is like virtual

cash, which can be used for buying online tickets and against restaurants,

spas & various other establishments once lockdown eases. We believe these

initiatives, coupled with improvement in realisation & improvement in

digitisation will drive the B2C business in the longer run.

ICICI Securities | Retail Research 5

ICICI Direct Research

Stock Tales | Just Dial Ltd

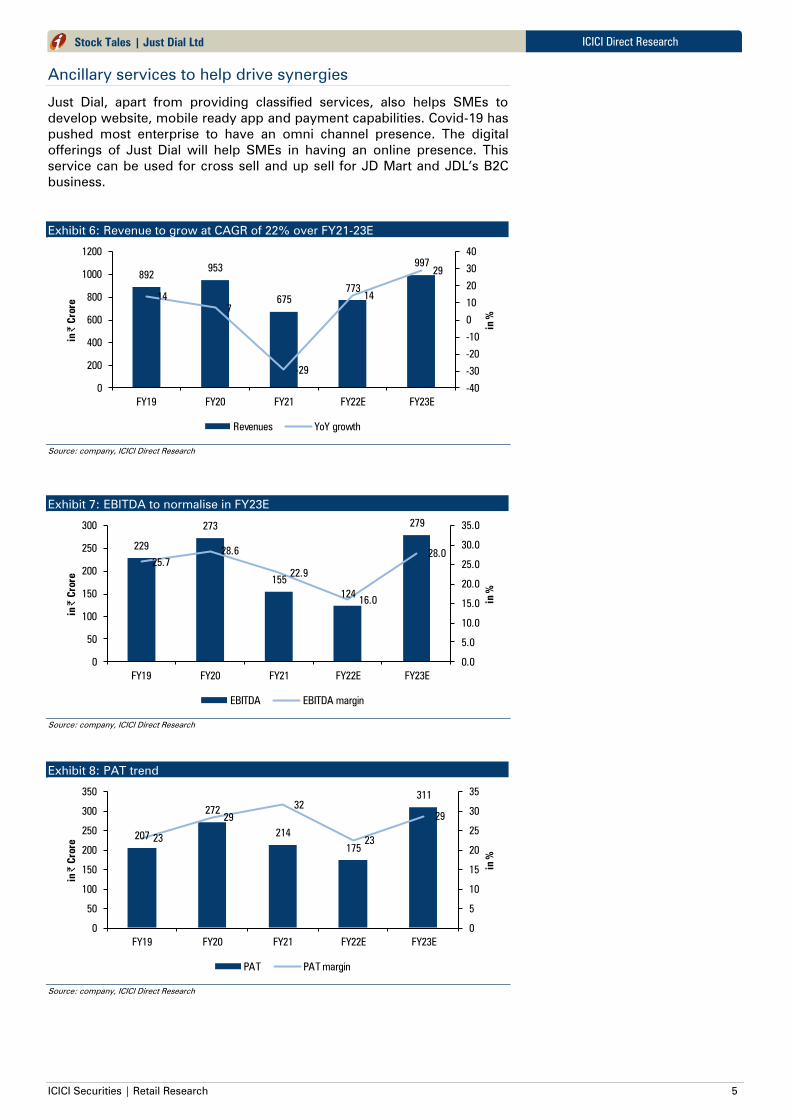

Ancillary services to help drive synergies

Just Dial, apart from providing classified services, also helps SMEs to

develop website, mobile ready app and payment capabilities. Covid-19 has

pushed most enterprise to have an omni channel presence. The digital

offerings of Just Dial will help SMEs in having an online presence. This

service can be used for cross sell and up sell for JD Mart and JDL’s B2C

business.

Exhibit 6: Revenue to grow at CAGR of 22% over FY21-23E

892953

675

773

997

14

7

-29

14

29

-40

-30

-20

-10

0

10

20

30

40

0

200

400

600

800

1000

1200

FY19 FY20 FY21 FY22E FY23E

in %

in |

C

rore

Revenues YoY growth

Source: company, ICICI Direct Research

Exhibit 7: EBITDA to normalise in FY23E

229

273

155

124

279

25.7

28.6

22.9

16.0

28.0

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

0

50

100

150

200

250

300

FY19 FY20 FY21 FY22E FY23E

in %

in |

C

rore

EBITDA EBITDA margin

Source: company, ICICI Direct Research

Exhibit 8: PAT trend

207

272

214

175

311

23

29

32

23

29

0

5

10

15

20

25

30

35

0

50

100

150

200

250

300

350

FY19 FY20 FY21 FY22E FY23E

in %

in |

C

rore

PAT PAT margin

Source: company, ICICI Direct Research

ICICI Securities | Retail Research 6

ICICI Direct Research

Stock Tales | Just Dial Ltd

Financial Summary

Exhibit 9: Profit & loss statement (| crore)

FY20 FY21 FY22E FY23E

Total Revenues 953 675 773 997

Growth (%) 6.9 (29.2) 14.5 29.1

COGS 533 443 479 588

Other Expenses 147 77 170 130

EBITDA 273 155 124 279

Growth (%) 19.2 (43.3) (20.2) 125.9

Depreciation 52 42 42 42

Other Income 140 150 140 170

Interest paid 9 7 8 8

PBT 352 255 213 399

Growth (%) 22.0 (27.6) (16.2) 87.0

Total Tax 79 40 38 88

PAT 272 214 175 311

Adjusted PAT 272 214 175 311

PAT 31.6 (21.4) (18.3) 77.9

EPS - diluted 42.0 33.0 28.3 50.3

EPS (Growth %) 31.6 (21.4) (14.5) 77.9

Source: Company, ICICI Direct Research,

Exhibit 10: Cash flow statement (| crore)

FY20 FY21 FY22E FY23E

Net profit before Tax 352 255 213 399

Depreciation 52 42 42 42

(inc)/dec in Current Assets 15 (2) (11) (25)

(inc)/dec in current Liabilities (85) (1) 73 169

CF from operations 153 139 148 336

Other Investments (125) 178 140 170

(Purchase)/Sale of Fixed Assets (2) (4) (5) (6)

CF from investing Activities (127) 174 135 164

Inc / (Dec) in Equity Capital 4 1 - -

Othes (30) (19) (19) (19)

Dividend & Buyback - (273) (87) (156)

Interest Paid on Loans (0) - (8) (8)

CF from Financial Activities (27) (291) (114) (182)

Cash generating during the year (1) 22 169 317

Opening cash balance 41 40 61 230

Closing cash 40 61 230 548

Source: Company, ICICI Direct Research

Exhibit 11: Balance Sheet (| crore)

FY20 FY21 FY22E FY23E

Equity 65 62 62 62

Reserves & Surplus 1,223 1,202 1,290 1,445

Networth 1,288 1,264 1,352 1,507

Minority Interest - - - -

Total Debt - - - -

Other long term liabilities 117 116 133 171

Source of funds 1,404 1,380 1,485 1,679

Net Block 63 46 32 19

CWIP - - - -

Other intangible assets&Goodwill 1 1 0 (0)

Other long term assets 1,662 1,625 1,623 1,626

Current investments 17 - - -

Other financial assets 10 11 12 16

Cash & Cash equivalents 40 62 231 548

Loans and advances 3 2 2 2

Other Current Assets(OCA) 37 41 47 61

Trade payables 25 15 17 22

Other Current liabilities 394 378 432 558

Provisions 9 14 14 14

Application of funds 1,404 1,380 1,485 1,679

Source: Company, ICICI Direct Research

Exhibit 12: Key ratios

(Year-end March) FY20 FY21 FY22E FY23E

Per share data (|)

Adjusted EPS (Diluted) 42.0 33.0 28.3 50.3

BV per share 198.7 195.1 218.5 243.7

DPS - - 14.1 25.1

Cash per Share 6.1 9.5 37.3 88.6

Operating Ratios

EBITDA Margin (%) 28.6 22.9 16.0 28.0

EBIT Margin (%) 23.2 16.7 10.5 23.8

PAT Margin (%) 28.6 31.7 22.6 31.2

Creditor days 9 8 8 8

Return Ratios (%)

RoE 21.1 16.9 12.9 20.6

RoCE 25.7 19.0 14.9 24.2

Valuation Ratios (x)

P/E 23.0 29.3 34.2 19.2

EV / EBITDA 16.1 28.5 34.3 14.0

Price to Book Value 4.9 5.0 4.4 4.0

EV / Net Sales 4.6 6.5 5.5 3.9

Market Cap / Sales 6.3 8.9 7.7 6.0

Solvency Ratios

Debt/EBITDA - - - -

Debt / Equity - - - -

Current Ratio 0.1 0.1 0.1 0.1

Quick Ratio 0.1 0.1 0.1 0.1

Source: Company, ICICI Direct Research

ICICI Securities | Retail Research 7

ICICI Direct Research

Stock Tales | Just Dial Ltd

RATING RATIONALE

ICICI Direct endeavors to provide objective opinions and recommendations. ICICI Direct assigns ratings to its

stocks according to their notional target price vs. current market price and then categorizes them as Buy, Hold,

Reduce and Sell. The performance horizon is two years unless specified and the notional target price is defined

as the analysts' valuation for a stock

Buy: >15%

Hold: -5% to 15%;

Reduce: -15% to -5%;

Sell: <-15%

Pankaj Pandey Head – Research [email protected]

ICICI Direct Research Desk,

ICICI Securities Limited,

1st Floor, Akruti Trade Centre,

Road No 7, MIDC,

Andheri (East)

Mumbai – 400 093

ICICI Securities | Retail Research 8

ICICI Direct Research

Stock Tales | Just Dial Ltd

ANALYST CERTIFICATION

I/We, Devang Bhatt, PGDBM, authors and the names subscribed to this report, hereby certify that all of the views expressed in this research report accurately reflect our views about the subject issuer(s) or securities. We also certify

that no part of our compensation was, is, or will be directly or indirectly related to the specific recommendation(s) or view(s) in this report. It is also confirmed that above mentioned Analysts of this report have not received any

compensation from the companies mentioned in the report in the preceding twelve months and do not serve as an officer, director or employee of the companies mentioned in the report.

Terms & conditions and other disclosures:

ICICI Securities Limited (ICICI Securities) is a full-service, integrated investment banking and is, inter alia, engaged in the business of stock brokering and distribution of financial products.

ICICI Securities is Sebi registered stock broker, merchant banker, investment adviser, portfolio manager and Research Analyst. ICICI Securities is registered with Insurance Regulatory Development Authority of India Limited (IRDAI)

as a composite corporate agent and with PFRDA as a Point of Presence. ICICI Securities Limited Research Analyst SEBI Registration Number – INH000000990. ICICI Securities Limited SEBI Registration is INZ000183631 for stock

broker. ICICI Securities is a subsidiary of ICICI Bank which is India’s largest private sector bank and has its various subsidiaries engaged in businesses of housing finance, asset management, life insurance, general insurance, venture

capital fund management, etc. (“associates”), the details in respect of which are available on www.icicibank.com.

ICICI Securities is one of the leading merchant bankers/ underwriters of securities and participate in virtually all securities trading markets in India. We and our associates might have investment banking and other business relationship

with a significant percentage of companies covered by our Investment Research Department. ICICI Securities and its analysts, persons reporting to analysts and their relatives are generally prohibited from maintaining a financial

interest in the securities or derivatives of any companies that the analysts cover.

Recommendation in reports based on technical and derivative analysis centre on studying charts of a stock's price movement, outstanding positions, trading volume etc as opposed to focusing on a company's fundamentals and, as

such, may not match with the recommendation in fundamental reports. Investors may visit icicidirect.com to view the Fundamental and Technical Research Reports.

Our proprietary trading and investment businesses may make investment decisions that are inconsistent with the recommendations expressed herein.

ICICI Securities Limited has two independent equity research groups: Institutional Research and Retail Research. This report has been prepared by the Retail Research. The views and opinions expressed in this document may or may

not match or may be contrary with the views, estimates, rating, and target price of the Institutional Research.

The information and opinions in this report have been prepared by ICICI Securities and are subject to change without any notice. The report and information contained herein is strictly confidential and meant solely for the selected

recipient and may not be altered in any way, transmitted to, copied or distributed, in part or in whole, to any other person or to the media or reproduced in any form, without prior written consent of ICICI Securities. While we would

endeavour to update the information herein on a reasonable basis, ICICI Securities is under no obligation to update or keep the information current. Also, there may be regulatory, compliance or other reasons that may prevent ICICI

Securities from doing so. Non-rated securities indicate that rating on a particular security has been suspended temporarily and such suspension is in compliance with applicable regulations and/or ICICI Securities policies, in

circumstances where ICICI Securities might be acting in an advisory capacity to this company, or in certain other circumstances.

This report is based on information obtained from public sources and sources believed to be reliable, but no independent verification has been made nor is its accuracy or completeness guaranteed. This report and information herein

is solely for informational purpose and shall not be used or considered as an offer document or solicitation of offer to buy or sell or subscribe for securities or other financial instruments. Though disseminated to all the customers

simultaneously, not all customers may receive this report at the same time. ICICI Securities will not treat recipients as customers by virtue of their receiving this report. Nothing in this report constitutes investment, legal, accounting

and tax advice or a representation that any investment or strategy is suitable or appropriate to your specific circumstances. The securities discussed and opinions expressed in this report may not be suitable for all investors, who

must make their own investment decisions, based on their own investment objectives, financial positions and needs of specific recipient. This may not be taken in substitution for the exercise of independent judgment by any recipient.

The recipient should independently evaluate the investment risks. The value and return on investment may vary because of changes in interest rates, foreign exchange rates or any other reason. ICICI Securities accepts no liabilities

whatsoever for any loss or damage of any kind arising out of the use of this report. Past performance is not necessarily a guide to future performance. Investors are advised to see Risk Disclosure Document to understand the risks

associated before investing in the securities markets. Actual results may differ materially from those set forth in projections. Forward-looking statements are not predictions and may be subject to change without notice.

ICICI Securities or its associates might have managed or co-managed public offering of securities for the subject company or might have been mandated by the subject company for any other assignment in the past twelve months.

ICICI Securities or its associates might have received any compensation from the companies mentioned in the report during the period preceding twelve months from the date of this report for services in respect of managing or co-

managing public offerings, corporate finance, investment banking or merchant banking, brokerage services or other advisory service in a merger or specific transaction.

ICICI Securities encourages independence in research report preparation and strives to minimize conflict in preparation of research report. ICICI Securities or its associates or its analysts did not receive any compensation or other

benefits from the companies mentioned in the report or third party in connection with preparation of the research report. Accordingly, neither ICICI Securities nor Research Analysts and their relatives have any material conflict of

interest at the time of publication of this report.

Compensation of our Research Analysts is not based on any specific merchant banking, investment banking or brokerage service transactions.

ICICI Securities or its subsidiaries collectively or Research Analysts or their relatives do not own 1% or more of the equity securities of the Company mentioned in the report as of the last day of the month preceding the publication of

the research report.

Since associates of ICICI Securities and ICICI Securities as a entity are engaged in various financial service businesses, they might have financial interests or beneficial ownership in various companies including the subject

company/companies mentioned in this report.

ICICI Securities may have issued other reports that are inconsistent with and reach different conclusion from the information presented in this report.

Neither the Research Analysts nor ICICI Securities have been engaged in market making activity for the companies mentioned in the report.

We submit that no material disciplinary action has been taken on ICICI Securities by any Regulatory Authority impacting Equity Research Analysis activities.

This report is not directed or intended for distribution to, or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction, where such distribution, publication, availability or

use would be contrary to law, regulation or which would subject ICICI Securities and affiliates to any registration or licensing requirement within such jurisdiction. The securities described herein may or may not be eligible for sale in

all jurisdictions or to certain category of investors. Persons in whose possession this document may come are required to inform themselves of and to observe such restriction.