Jun Bei Liu, FUNDIES’ BEST LONGAND SHORTIDEAS

2

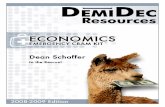

AFRGA1 0018 AFR 5-6 January 2019 The Australian Financial Review | www.afr.com 18 Companies The stocks fund managers are betting against in 2019… Stockland $ Caltex $ JB Hi-Fi $ Seek $ British American Tobacco pence Bright ideas If you are bearish the Australian housing market in 2019 and 2020 then it will be a tough year for Stockland. Preston Hamersley, Indian Pacific The weakest housing market in at least a decade could cripple discretionary spending on items such as electronics. Phil King, Regal Funds With domestic job ads turning negative coupled with a cooling Chinese employment market, Seek will experience further earnings disappointment. Jun Bei Liu, Tribeca The valuation appears to reflect the lowest probability of the eventual decline in the market for cigarettes. Chad Slater, Morphic J18 J F M A M J J A S O N D J18 J F M A M J J A S O N D 23.00 21.00 19.00 17.00 J18 J F M A M J J A S O N D 30.00 28.00 26.00 24.00 22.00 J18 J F M A M J J A S O N D 36.00 32.00 28.00 J18 J F M A M J J A S O N D 4.60 4.20 3.80 5000 4000 3000 Caltex will face on ongoing $80m hit to earnings from renewing their Woolworths contract. Sean Sequeira, Alleron FUNDIE S’ BE S T LONG AND SHORT IDEAS 2019 tips Hedge fund managers are betting against property and backing gaming and insurance to deliver positive returns in what promises to be another wild year in the market. Jonathan Shapiro and Vesna Poljak reveal the stocks fundies are eyeing, feast and famine. Several managers are looking at the real estate investment trust sector and property developers for short ideas as they remain expensive in challenging conditions. PHOTO: STEVENSIEWERT A ustralian hedge fund managers are betting that real estate compan- ies bear the brunt of a property market down- turn while childcare and consumer stocks are also presenting opportunities on the short side. And, as markets face another challenging year, AFR Weekend’s annual survey of the best long and short ideas for the year ahead reveals fund managers are putting their faith in the unloved insurance sector, undis- covered small-cap gems, gaming and min- ing services. For globally focused hedge funds based in Australia, investors are betting that 2019 is the year that Tesla’s Elon Musk unravels, tobacco stocks will run out of puff and that wrestling simply won’t catch on in China. They’re selectively shorting what they believe are overvalued tech stocks and buy- ing the likes of Google and long-forgotten titans such as Nokia and Vivendi. And high-frequency trading may provide a rare opportunity to profit from a violent outbreak of market volatility. ■ Catherine Allfrey and Raaz Bhuyan from WaveStone nominate gaming machine developer Aristocrat Leisure as their long idea. ‘‘If we assume Aristocrat’s historic rate of return on its design and development spend at 11 to 12 per cent of sales (circa $500 million in 2018-19), Aristocrat should organically be able to grow its earnings per share 8 to 10 per cent per annum over the next three to five years. Trading on 15 times P/E we think this too cheap for a global leader.’’ The WaveStone pair are short select ASX- listed technology names. ■ Tribeca’s Jun Bei Liu is also betting on good fortune for Aristocrat Leisure, which is trading at a meaningful discount to the market ‘‘despite strong growth projections over the next few years’’. She is expecting at least a 30 per cent return over 12 months. She continues to bet against online jobs classified site Seek even as the share price has fallen 25 per cent since September. Seek continues to trade at a substantial premium to the market with a limited growth projection taking into account investments. ‘‘With domestic job ads turning negative, coupled with a cooling Chinese employ- ment market, Seek will experience further earnings disappointment.’’ ■ Alleron’s long is QBE Insurance. After years of painful change, Alleron chief investment officer Sean Sequeira believes that ‘‘a simplified, more focused company provides a great back-to-the-future oppor- tunity to improve risk outcomes and returns to shareholders’’. QBE chief executive Pat Regan’s sale of the troubled Latin American business for $100 million above book value in 2017 got the fund manager interested – ‘‘a change in the quality of earnings was taking place’’ – and a new reinsurance program will improve the quality of earnings ‘‘similar to that of the early 2000s’’. With a valuation of 1.1 times book value, Alleron believes there is ‘‘minimal down- side risk but potential for significant gains’’ if management can execute its strategy. Alleron is short Caltex Australia, a stock it previously owned, as it will face an ongo- ing $80 million hit to earnings from renew- ing the Woolworths contract, the fund manager says. ‘‘We also believe management has under- estimated the difficulties and time it would take in transforming the existing retailing business to a fast-food and convenience business, initially at a cost of $100 million to $120 million for buying back the business from its franchisees. This is occurring amidst a backdrop of a significant doubling in net debt to $1 billion in just two years at a time of pressure on refining margins that still comprise 20 per cent of earnings.’’ ■ PWR Holdings is a rare opportunity to buy a quality growth stock that ticks all the boxes for Indian Pacific’s Preston Hamers- ley. The Gold Coast-based manufacturer of high-performance vehicle cooling solutions is a leading player in Formula 1 motor sports, supplying nine of the 10 F1 teams with their coolers. ‘‘They have a pristine balance sheet ($12 million cash and no debt), have a down- to-earth and fiercely-engaged management team with skin in the game (Kees Weel and family founded the company 30 years ago and still own over 30 per cent of stock), the business has a very strong market position with embedded customer relationships and margins are healthy (30 per cent-plus EBITDA margins and 20 per cent net profit margins).’’ Also cashflow conversion is very strong, there are plenty of growth opportun- ities and there is upside risk to 2019-20 fore- casts. Hamersley’s short idea is Stockland, which might appear cheap on headline numbers, but he is cautious about capital- ising current earnings into any yield or mul- tiple analysis. ‘‘Whilst not wanting to single out an otherwise reasonably run company, if you are bearish the Australian housing market in 2019 and 2020 (as I am) then it will be a tough year for Stockland given around 30 per cent of group EBIT comes from their residential land business.’’ ■ Monash Investors’ long stock pick is Nearmap, the aerial surveyor, whose mar- ket it estimates is massive at $US7.4 billion in 2018. ‘‘With a proven organic growth track record, ongoing research and invest- ment into new market-leading products, a very strong balance sheet and its highly attractive operating leverage, Nearmap seems well positioned to climb through these turbulent market times,’’ investment analyst Sebastian Correia says. One of its favourite shorts is Coca-Cola Amatil, which – despite its recent decline – ‘‘remains expensive’’, according to Monash. ‘‘Coca-Cola Amatil has been struggling for years and its market is getting tougher. Con- sumers continue to traverse away from sugar drinks and their water business is struggling,’’ Correia says. Indonesian expan- sion hasn’t worked and, given its 5.5 per cent dividend yield relies on a payout ratio of 85 per cent, and the structural challenges CCL faces, Monash expects further pressure on the share price in 2019. ■ Worley Parsons is the long pick of Firetrail Investments’ James Miller. The oil and gas engineer had a tough end to 2018, but Miller believes it is well positioned to outperform in 2019. Since its peak in September, the stock is down more than 40 per cent because of the fall in the oil price and the market’s apparent scepticism over its large offshore acquisition. ‘‘Worley Parsons is a cheap stock which has diversified its end-market exposures further away from oil with this acquisition. However, what really excites us is the internal rigour that has emerged in the busi- ness over the past three years. ‘‘When oil hit $US28 in 2016, Worley Par- sons did not let a good downturn go to waste, and has significantly improved its cost control and workforce utilisation,’’ Miller says. Firetrail is short the listed property sector. ‘‘Low rates have been driving high valu- ations, but there are signs that this may be turning. Despite most REITs trading at a sig- nificant premium to their net tangible assets, we are seeing transactions being done at close to book value. This is particu-

Transcript of Jun Bei Liu, FUNDIES’ BEST LONGAND SHORTIDEAS

AFRGA1 0018

AFR5-6 January 2019The Australian Financial Review | www.afr.com

18 Companies

The stocks fund managers are betting against in 2019…

Stockland $ Caltex $ JB Hi-Fi $ Seek $ British American Tobacco pence

Bright ideas

If you are bearish the Australian housing market in 2019 and 2020 then it will be a tough year for Stockland.Preston Hamersley, Indian Pacific

The weakest housing market in at least adecade could cripple discretionary spending on items such as electronics.Phil King, Regal Funds

With domestic job ads turning negative coupled with a cooling Chinese employment market, Seek will experience further earnings disappointment.Jun Bei Liu, Tribeca

The valuation appears to reflect the lowest probability of the eventual decline in the market for cigarettes.Chad Slater, Morphic

J18 JF M A M J J A S O N DJ18 JF M A M J J A S O N D

23.00

21.00

19.00

17.00

J18 JF M A M J J A S O N D

30.0028.0026.0024.0022.00

J18 JF M A M J J A S O N D

36.00

32.00

28.00

J18 JF M A M J J A S O N D

4.60

4.20

3.80

5000

4000

3000

Caltex will face on ongoing $80m hit to earnings from renewing their Woolworths contract.Sean Sequeira, Alleron

FUNDIES’ BESTLONG AND

SHORT IDEAS2019 tips Hedge fund managers are betting against

property and backing gaming and insurance to deliverpositive returns in what promises to be another wild year

in the market. Jonathan Shapiro and Vesna Poljakreveal the stocks fundies are eyeing, feast and famine.

Several managers are looking at the real estate investment trust sector and property developers for short ideas asthey remain expensive in challenging conditions. PHOTO: STEVEN SIEWERT

Australian hedge fundmanagers are bettingthat real estate compan-ies bear the brunt of aproperty market down-turn while childcare andconsumer stocks are also

presenting opportunities on the short side.And, as markets face another challenging

year, AFR Weekend’s annual survey of thebest long and short ideas for the year aheadreveals fund managers are putting theirfaith in the unloved insurance sector, undis-covered small-cap gems, gaming and min-ing services.

For globally focused hedge funds based inAustralia, investors are betting that 2019 isthe year that Tesla’s Elon Musk unravels,tobacco stocks will run out of puff and thatwrestling simply won’t catch on in China.

They’re selectively shorting what theybelieve are overvalued tech stocks and buy-ing the likes of Google and long-forgottentitans such as Nokia and Vivendi.

And high-frequency trading may providea rare opportunity to profit from a violentoutbreak of market volatility.

■ Catherine Allfrey and Raaz Bhuyan fromWaveStone nominate gaming machinedeveloper Aristocrat Leisure as their longidea. ‘‘If we assume Aristocrat’s historic rateof return on its design and developmentspend at 11 to 12 per cent of sales (circa$500 million in 2018-19), Aristocrat shouldorganically be able to grow its earnings pershare 8 to 10 per cent per annum over thenext three to five years. Trading on 15 timesP/E we think this too cheap for a globalleader.’’

The WaveStone pair are short select ASX-listed technology names.

■ Tribeca’s Jun Bei Liu is also betting ongood fortune for Aristocrat Leisure, which

is trading at a meaningful discount to themarket ‘‘despite strong growth projectionsover the next few years’’. She is expecting atleast a 30 per cent return over 12 months.

She continues to bet against online jobsclassified site Seek even as the share pricehas fallen 25 per cent since September.

Seek continues to trade at a substantialpremium to the market with a limitedgrowth projection taking into accountinvestments.

‘‘With domestic job ads turning negative,coupled with a cooling Chinese employ-ment market, Seek will experience furtherearnings disappointment.’’

■ Alleron’s long is QBE Insurance. Afteryears of painful change, Alleron chiefinvestment officer Sean Sequeira believesthat ‘‘a simplified, more focused companyprovides a great back-to-the-future oppor-tunity to improve risk outcomes and returnsto shareholders’’.

QBE chief executive Pat Regan’s sale ofthe troubled Latin American business for$100 million above book value in 2017 gotthe fund manager interested – ‘‘a change inthe quality of earnings was taking place’’ –and a new reinsurance program willimprove the quality of earnings ‘‘similar tothat of the early 2000s’’.

With a valuation of 1.1 times book value,Alleron believes there is ‘‘minimal down-side risk but potential for significant gains’’if management can execute its strategy.

Alleron is short Caltex Australia, a stockit previously owned, as it will face an ongo-ing $80 million hit to earnings from renew-ing the Woolworths contract, the fundmanager says.

‘‘We also believe management has under-estimated the difficulties and time it wouldtake in transforming the existing retailingbusiness to a fast-food and conveniencebusiness, initially at a cost of $100 million to$120 million for buying back the businessfrom its franchisees. This is occurringamidst a backdrop of a significant doublingin net debt to $1 billion in just two years at atime of pressure on refining margins thatstill comprise 20 per cent of earnings.’’

■ PWR Holdings is a rare opportunity tobuy a quality growth stock that ticks all theboxes for Indian Pacific’s Preston Hamers-ley. The Gold Coast-based manufacturer ofhigh-performance vehicle cooling solutionsis a leading player in Formula 1 motorsports, supplying nine of the 10 F1 teamswith their coolers.

‘‘They have a pristine balance sheet($12 million cash and no debt), have a down-

to-earth and fiercely-engaged managementteam with skin in the game (Kees Weel andfamily founded the company 30 years agoand still own over 30 per cent of stock), thebusiness has a very strong market positionwith embedded customer relationships andmargins are healthy (30 per cent-plusEBITDA margins and 20 per cent net profitmargins).’’ Also cashflow conversion is verystrong, there are plenty of growth opportun-ities and there is upside risk to 2019-20 fore-casts.

Hamersley’s short idea is Stockland,which might appear cheap on headlinenumbers, but he is cautious about capital-ising current earnings into any yield or mul-tiple analysis. ‘‘Whilst not wanting to singleout an otherwise reasonably run company,if you are bearish the Australian housingmarket in 2019 and 2020 (as I am) then itwill be a tough year for Stockland givenaround 30 per cent of group EBIT comesfrom their residential land business.’’

■ Monash Investors’ long stock pick isNearmap, the aerial surveyor, whose mar-ket it estimates is massive at $US7.4 billionin 2018. ‘‘With a proven organic growthtrack record, ongoing research and invest-ment into new market-leading products, avery strong balance sheet and its highlyattractive operating leverage, Nearmapseems well positioned to climb throughthese turbulent market times,’’ investmentanalyst Sebastian Correia says.

One of its favourite shorts is Coca-ColaAmatil, which – despite its recent decline –‘‘remains expensive’’, according to Monash.

‘‘Coca-Cola Amatil has been struggling foryears and its market is getting tougher. Con-sumers continue to traverse away fromsugar drinks and their water business isstruggling,’’ Correia says. Indonesian expan-sion hasn’t worked and, given its 5.5 percent dividend yield relies on a payout ratioof 85 per cent, and the structural challengesCCL faces, Monash expects further pressureon the share price in 2019.

■ Worley Parsons is the long pick ofFiretrail Investments’ James Miller. The oiland gas engineer had a tough end to 2018,but Miller believes it is well positioned tooutperform in 2019. Since its peak inSeptember, the stock is down more than40 per cent because of the fall in the oil priceand the market’s apparent scepticism overits large offshore acquisition.

‘‘Worley Parsons is a cheap stock whichhas diversified its end-market exposuresfurther away from oil with this acquisition.However, what really excites us is theinternal rigour that has emerged in the busi-ness over the past three years.

‘‘When oil hit $US28 in 2016, Worley Par-sons did not let a good downturn go towaste, and has significantly improved itscost control and workforce utilisation,’’Miller says.

Firetrail is short the listed property sector.‘‘Low rates have been driving high valu-ations, but there are signs that this may beturning. Despite most REITs trading at a sig-nificant premium to their net tangibleassets, we are seeing transactions beingdone at close to book value. This is particu-

AFRGA1 0019

AFR 5-6 January 2019www.afr.com | The Australian Financial Review

19Companies

SOURCE: BLOOMBERG

Aristocrat $

… and the stocks they’re backing

Trading on 15 timesP/E we think Aristocract is too cheap for aglobal leader.Catherine Allfrey, Wavestone

The high level of equity volatility in the fourth quarter of 2018 should also provide for exceptional near-term profit results and cash flow.Andrew Brown, East 72

Two thirds of all music streaming is “back catalogue” with consumers gravitating towards nostalgic tracks versus new releases.Andrew Macken, Montaka

Nokia has been transformed in recent years and is no longer focussed on handsets but critical communications infrastructure.Jacob Mitchell, Antipodes Partners

The business has been caught in the downdraft of the tech selloff despite not having missed a beat on earnings this year.Ben McGarry, Sam Granger, Totus

J18 JF M A M J J A S O N DJ18 JF M A M J J A S O N D

34.00

30.00

26.00

22.00

Virtu Financial $US

40.0035.0030.0025.0020.00

Vivendi €

J18 JF M A M J J A S O N D

25.0024.0023.0022.0021.00

Nokia €

J18 JF M A M J J A S O N D

5.40

5.00

4.60

4.20

Alphabet $US

J18 JF M A M J J A S O N D

1300.00

1200.00

1100.00

1000.00

Phil King, founder RegalFunds Management

larly true for retail property assets, which insome cases have been changing hands at adiscount to book value.’’

Miller says that, when equity marketsbecome volatile, listed property is oftenthought of as a safe sector. ‘‘However, if theeconomic reality of falling property valu-ations hit, this can unwind quickly, and asan investor you don’t want to be caught outin the space,’’ he warns.

■ Regal Funds Management’s Phil King issticking to his guns shorting JB Hi-Fi, theelectronics retailer that continues to dividehedge funds. He says the repercussions ofAmazon’s entry into Australia will continueto mount and will be acute over the next fewyears. ‘‘At the same time, the weakest hous-ing market in at least a decade could cripplediscretionary spending on items such aselectronics,’’ King says.

JB Hi-Fi is ‘‘a classic value trap’’.On the long side, King picked insurance

broker AUB Group as he views rising insur-ance premiums as a huge positive for thesector.

The stock was hurt by dilutive equity rais-ings in 2018, but King says the benefits of aseries of accretive aquisitions hopefully willemerge this year. At a P/E multiple of 16times before factoring in acquisitions, AUBtrades at a ‘‘material discount’’ to Steadfast.

■ Jacob Mitchell of Antipodes Partners haspicked long-discarded Finnish handsetmaker Nokia as a long as the fund sees ‘‘con-nectivity’’ being a theme in 2019. While tele-com operators have cut back spending, 5Ginvestments will get underway, benefitingcompanies such as Nokia.

‘‘Nokia itself has been transformed inrecent years, no longer focused on handsetsbut instead the critical infrastructure thatenables communication systems means it ispoised for accelerating growth at a timewhen growth elsewhere will naturallyslow.’’

On the short side, Mitchell expects aperiod of unprecedented central bankliquidity creating a premium for growthassets, regardless of the underlying businessquality, ‘‘not seen in a generation’’. But asliquidity retreats, the same stocks are com-ing under pressure.

‘‘We see a further shakeout as likely andare focusing our short attention on weakbusinesses and/or weak balance sheet busi-nesses that are excessively valued – span-ning certain technology, industrial, realestate and infrastructure assets across theglobe.’’

■ Clay Smolinski and Andrew Clifford ofPlatinum Asset Management say the sell-offin oil prices presents an excellent entrypoint to Canadian oil and gas companySeven Generations Energy, which has oneof the lowest break-even production costbases in North America.

‘‘Seven Gen is likely to self-fund 10 percent per annum production growth over thenext five years at modest oil prices andshareholders may see dividends orbuybacks.’’

Platinum’s short idea is US-listedMongoDB, which is one of several ‘‘hyper-

priced’’ tech stocks. The company, whichtrades at 20 to 30 times revenue, developeda free, open-source ‘‘NoSQL’’ database andmakes money by selling subscriptions to its‘‘enterprise’’ edition.

‘‘It has never made a profit and looksunlikely to do so in the medium term, withcompetition from Microsoft, Amazon,Google, Oracle and a litany of smaller com-petitors, many of whom can offerdocument-oriented database services forfree as part of overall service offerings.’’

■ Ben McGarry and Sam Granger of TotusCapital believe big tech is offering value andhave picked Alphabet as a long. ‘‘The busi-ness has been caught in the downdraft ofthe tech sell-off despite not having missed abeat on earnings this year. Revenue is stillgrowing at 20 per cent per year, it has$US100 billion of net cash on its balancesheet and in 2019 we should begin to seehow they plan to monetise loss-makingbusinesses like Waymo.’’

On the short side, Totus is betting againstG8 Education despite a strong rally in thestock, anticipating headwinds as it rolls outnew centres in an ‘‘already oversupplied’’market. ‘‘The childcare sector has been agraveyard for listed equity investors and wethink the sector’s reputation as a defensiveis not borne out by the historical facts.’’

Globally, Totus cannot resist shortingElon Musk’s Tesla, which it says has all thehallmarks of its previous successful shorts –Blue Sky and Quintis.

‘‘It has a charismatic founding CEO, cult-

like investor following and a share price thathas completely detached from fundament-als. The company has never posted anannual profit and the stock is trading withina whisker of all-time highs despite intensify-ing competition, the expiry of EV subsidiesin the USA and a stretched balance sheet.We see the risks as asymmetric to the down-side in 2019.’’

■ NSX-listed hedge fund East72’s most obvi-ous short is Tesla given its ‘‘ludicrous’’ valu-ation, but portfolio manager AndrewBrown is also betting against World Wrest-ling Entertainment. Shares in WWE morethan tripled in 2018, before selling off, butBrown says they have further to fall.

‘‘We see WWE as a poor cousin of othertelevised sports – notably UFC – with declin-ing live attendances and a flattening socialmedia following. At 51 times EV/EBITDA theshares reflect exultant hopes for interna-tional growth in a crowded market.’’

On the long side, Brown is betting on USmarket-maker Virtu Financial, which wascast as the villain in Michael Lewis’ high-frequency trading expose Flash Boys.

Brown says the firm’s acquisition of ITGwill diversify its earnings away from a reli-ance on higher market volatility, which isfavourable, and it has a good track record ofintegrating acquisitions. ‘‘The high level ofequity volatility in Q4 2018 should alsoprovide for exceptional near-term profit res-ults and cash flow.’’

The shares trade at 10 times 2020 pro-forma profits and Brown says the company

is ‘‘erecting higher entry barriers to theirbusiness’’.

■ Andrew Macken and Chris Demasi ofMontaka say French-listed Vivendi is thebest way to profit from the accelerated trendtowards music streaming. Vivendi’s Univer-sal Music holds the rights to a third of all theworld’s music and Montaka says its backcatalogue is perfectly positioned to be re-monetised. ‘‘Two thirds of all music stream-ing is back catalogue with consumers grav-itating towards nostalgic tracks versus newreleases. This means that Vivendi is monet-ising an asset (UMG) much more efficientlythan the market has ever seen before andappears to have materially undervalued.’’

■ James Tayler and Chad Slater of MorphicAsset Management are once again puttingtheir faith in Hong Kong-listed China Ever-bright, despite ‘‘an unexpected and badlycommunicated’’ rights issue in 2018.

Everbright has a strong balance sheet andis poised to benefit from the Chinese govern-ment’s environmental policies.

The fund manager has picked London-listed British American Tobacco as its short,even after a terrible 2018 for smoking stocks.They say it’s a mistake to gravitate towardsthe sector for its ‘‘bond-like attributes’’ ifinterest rates decline because it faces mul-tiple threats. ‘‘High barriers to entry are lessrelevant as new entrants provide alterna-tives (vaping and heat-not-burn products)that are rapidly gaining market share at theexpense of incumbents’ revenue growth.’’