July 2014 energy ltd Montney Lightstream Montney Nuvista Montney Paramount Montney RMP Montney 7G...

32

cequence energy ltd July 2014

Transcript of July 2014 energy ltd Montney Lightstream Montney Nuvista Montney Paramount Montney RMP Montney 7G...

cequenceenergy ltd

July 2014

Forward‐Looking Information and Definitions

Summary of Forward‐Looking Statements or InformationCertain information included in this presentation constitutes forward‐looking information under applicable securities legislation. This information relates to future events or future performance of the Company. Investors are cautioned that reliance on such information may not be appropriate for making investment decisions. Many factors could cause the Company’s actual results, performance or achievements to vary from those described herein. The forward‐looking information contained in this presentation is expressly qualified by this and other cautionary statements set forth in the continuous disclosure record of the Company.For a complete description of the forward‐looking statements or information and the definitions used in this presentation, see slide 30 "Forward‐Looking Statements or Information and Definitions."

2

British Columbia Alberta

PEACE RIVER

GRANDE PRAIRIE

Montney Focused Deep Basin Gas

3

USACANADA

Deep Basin

Large operated land position in core Montney trend in Alberta

Strong balance sheet, exit 2014 debt 0.6 times cashflow

Facilities in place Current production 10,400 Boepd Plan to reach 15,000 Boepd in next 9

months

SIMONETTE PROJECT

SIMONETTE PROJECT

Alberta Deep Basin Montney

Cequence owns 89 net sections of Montney land at Simonette in the liquids rich, over‐pressured Montney fairway

4

Approximate TopOver Pressure

XTO

XTOXTO

XTO

XTO

XTO

XTO

XTO XTO

XTO

XTO

XTO

XTO

XTO

XTO

KARR

WAPITI

KAKWA

RESTHAVEN

SIMONETTE

WASKAHIGAN

FIR

ANTE CREEK

Land LegendApache MontneyARC MontneyAthabasca MontneyCIOC MontneyCNRL MontneyCequence MontneyChevron MontneyCPC MontneyDelphi MontneyDonnybrook MontneyEncana MontneyEnerplus MontneyXTO Canada MontneyKelt MontneyLightstream MontneyNuvista MontneyParamount MontneyRMP Montney7G MontneyYoho All Rights

LegendXTO Hzntls Licensed since 2013

R21W5R1W6 R22R23R24R25R26R2R3R4R5R6R7R8R9

T55

T56

T57

T58

T59

T60

T61

T62

T63

T64

T65

T66

T67

T68

T69

Recent Highlights

5

Sold 1,600 Boepd non‐operated asset for $141 million

$135 million senior credit facility undrawn post asset sale

Pad style development drilling now started at Simonette

Increasing 2014 capital program to $170 million (net $23 million after divestitures) and $58 million in Q1 2015

Target exit rate in March 2015 of 15,000 Boepd and $82 million net debt

Production growth to over 40,000 Boepd by year end 2018

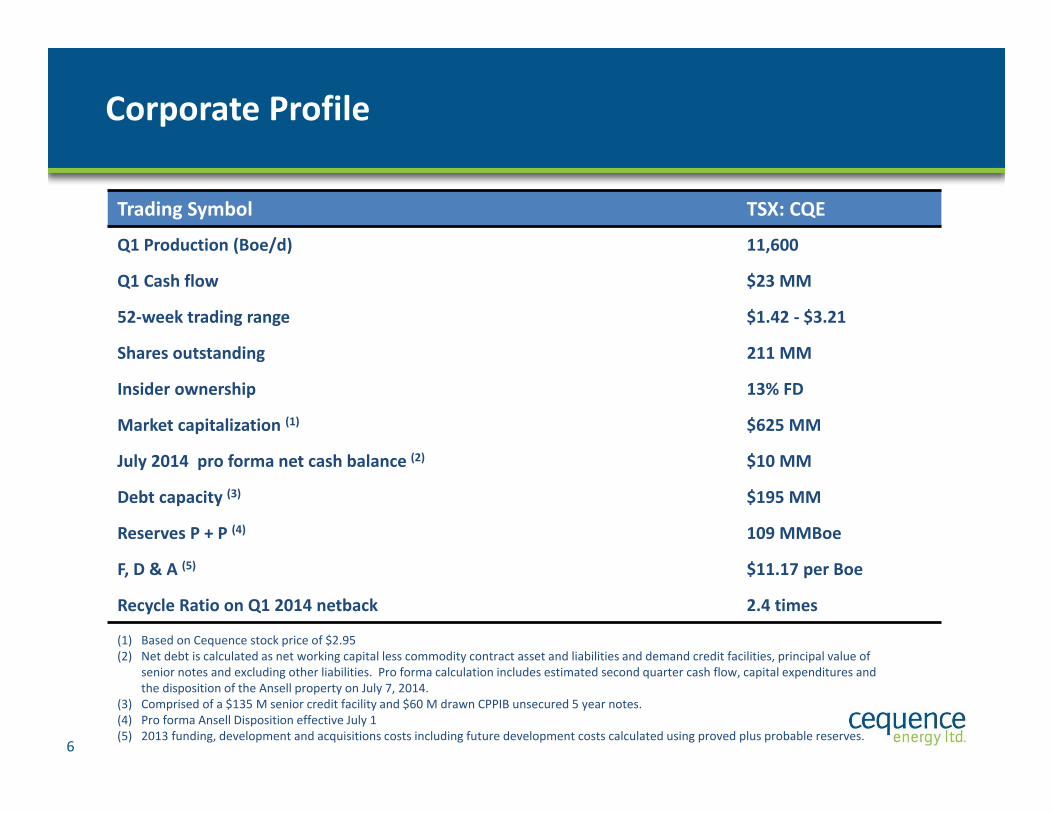

Corporate Profile

6

Trading Symbol TSX: CQE

Q1 Production (Boe/d) 11,600

Q1 Cash flow $23 MM

52‐week trading range $1.42 ‐ $3.21

Shares outstanding 211 MM

Insider ownership 13% FD

Market capitalization (1) $625 MM

July 2014 pro forma net cash balance (2) $10 MM

Debt capacity (3) $195 MM

Reserves P + P (4) 109 MMBoe

F, D & A (5) $11.17 per Boe

Recycle Ratio on Q1 2014 netback 2.4 times

(1) Based on Cequence stock price of $2.95(2) Net debt is calculated as net working capital less commodity contract asset and liabilities and demand credit facilities, principal value of

senior notes and excluding other liabilities. Pro forma calculation includes estimated second quarter cash flow, capital expenditures and the disposition of the Ansell property on July 7, 2014.

(3) Comprised of a $135 M senior credit facility and $60 M drawn CPPIB unsecured 5 year notes.(4) Pro forma Ansell Disposition effective July 1(5) 2013 funding, development and acquisitions costs including future development costs calculated using proved plus probable reserves.

Corporate Guidance

2014 Q1 2015

Average Production (Boe/d) 11,000 13,500

Exit production (Boe/d) 12,000 15,000

Capital expenditures, prior to dispositions (4) $170 MM $58 MM

Capital expenditures, net of dispositions $23 MM $58 MM

Wells drilled 19 (15.2) 6 (6.0)

Operating and transportation costs per Boe $9.00 $8.20

Royalties (% of revenue) 10% 8%

Crude oil – WTI (US$/Bbl) $99.75 $97.00

Natural gas – AECO (Cdn$/GJ) $4.60 $3.85

Funds flow from operations (2) $83 MM $27 MM

Net debt and working capital deficiency (3) $51 MM $82 MM

Basic shares outstanding 211 MM 211 MM

(1) Comprised of 84 percent natural gas and 16% of oil and liquids(2) Funds flow from operations is calculated as cash flow from operating activities before adjustments for decommissioning liabilities(3) Net debt and working capital (deficiency) is calculated as cash and net working capital less commodity contract assets and liabilities,demand credit facilities and the aggregate principal amount of the Notes and excluding other liabilities.(4) Includes an estimated $24.1 million of capital expenditures in 2014 on the Ansell property prior to disposition.7

8

Cequence Simonette 13‐11 Compressor Station

Cequence Simonette 13‐11 Compressor Station

3D SeismicCoverage

Trilogy PlantCQE W.I. = 25%Capacity 10 MMcf/d

9‐10Field Compressor

Keyera ProcessingFacility Capacity 153 MMcf/d

13‐11Compressor Station

To Aux SableDeep Cut PlantChicago, Illinois

CQE GAS To Aux Sable

CQE Land

Alliance PipelineCQE Gathering System3D Seismic Outline

TCPL PipelinePembina Pipeline

R23W5R1W6 R24R25R26R27R2

T60

T61

T62

T63

T64

Simonette Project Infrastructure‐ Ready for full scale development

9

6 miles

13‐11 Facility ‐ Current Capacity 70 MMcf/d

Cequence AllianceMeter StationCapacity 120 MMcf/d

Cequence owns and operates its facilities at Simonette

Phase 6 Facility expansion planned in Q4 to 95 MMcfd

Potential for future additional expansion up to 100 MMcfd to TCPL.

Simonette Area – Q1 operating netback was $35 per Boe prior to hedging

OIL

GAS(Avg 27 Bbls/MMcf Condensate)

100+

Bbls/MMcf

Montney Rights

CQE Montney Oil WellIndustry Montney Oil Well

CQE Montney Gas Well

Industry Montney HZ Well

CQE Wells to Q1 2015

Cequence Land

R25W5R1W6 R26R27

T60

T61

T62

Simonette Montney Drilling Plan through to Q1 2015

10

Currently drilling first pad at 1‐32, second pad at 12‐26 to spud in August

35 pad sites built or approved

Gas condensate yields have increased to 27 Bbls per MMcf, 40 Bbls per MMcf of total NGLs

6 miles

LOWER MONTNEYLOCATION

12‐26 PAD

1‐32PAD

OILGAS

Montney Rights

CQE Montney Oil WellIndustry Montney Oil Well

CQE Montney Gas Well

Industry Montney HZ Well

CQE Planned Wells

Cequence Land

R25W5R1W6 R26R27

T60

T61

T62

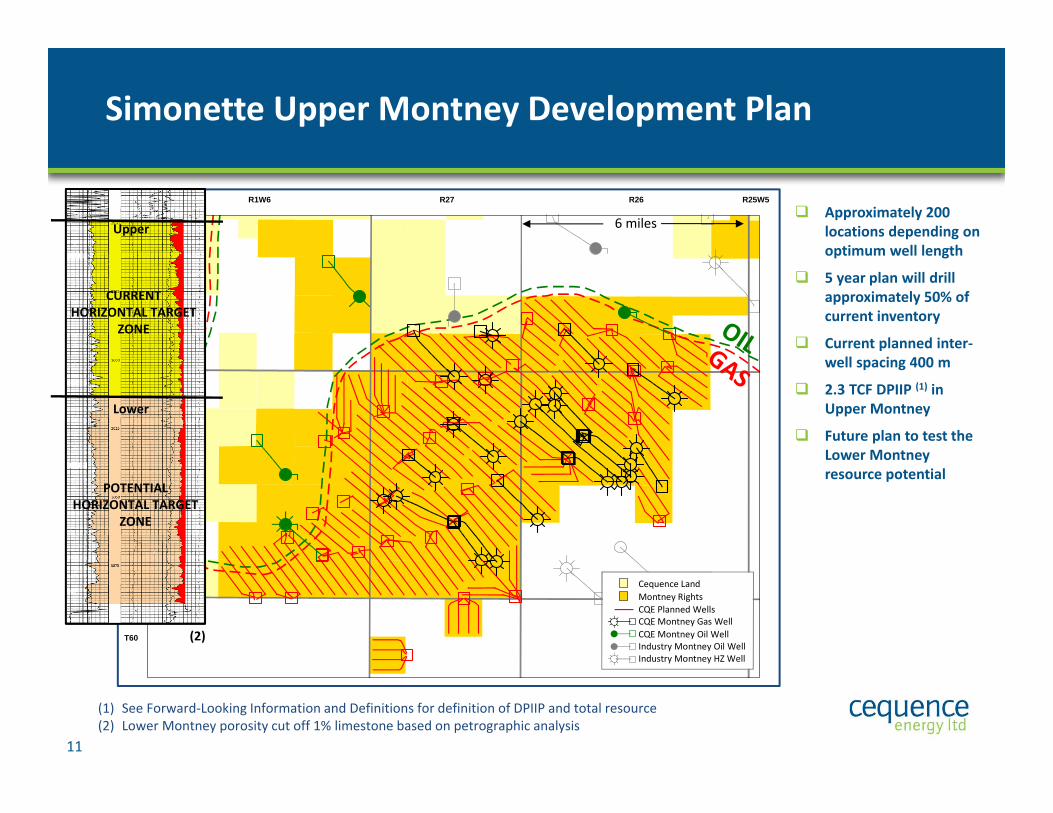

Simonette Upper Montney Development Plan

11

6 miles

(1) See Forward‐Looking Information and Definitions for definition of DPIIP and total resource(2) Lower Montney porosity cut off 1% limestone based on petrographic analysis

Approximately 200 locations depending on optimum well length

5 year plan will drill approximately 50% of current inventory

Current planned inter‐well spacing 400 m

2.3 TCF DPIIP (1) in Upper Montney

Future plan to test the Lower Montneyresource potential

Lower

CURRENT HORIZONTAL TARGET

ZONE

POTENTIAL HORIZONTAL TARGET

ZONE

Upper

(2)

0

1

2

3

4

5

6

7

8

9

10

11

12

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20

Prod

ucing Daily Gas Rate (M

Mcf/d)

Months on Production

CQE 7 BCF High Case

CQE 5 BCF Base Case

Cequence Montney gas producers – 19 wells to date

12

`HALF CYCLE ECONOMICS BASE CASE‐Budget model HIGH CASE

IP (MMcf/d)IP 30 (MMcf/d)EUR (MBoe) Raw Gas (Bcf) Condy (MBbl) NGL (MBbl)

5.54.69255.010050

7.56.91,2907.015065

CAPEX $MM (D,C + TI)ROR BT (%)NPV $MM (10%)PAYOUT (YEARS)CAPITAL EFFICIENCY(1st YEAR, $/Boed)

7.5606.61.6

14,000

7.5135121.0

10,000

Includes 5% GORR, Opex $4.00 per Boe Gas rate does not include liquids

Assumes 30 Bbls/MMcf of NGL’s and condensate Assumes $4.00/GJ AECO, $90 WTI flat *Wells with mechanical complications included

* Mechanical Complications

13

8‐21 costs contain original well combined with re‐drill 9‐21 completion costs 13‐35 was a re‐entry of an existing vertical uphole producer 16‐10 was a strat test with pilot hole and coring program

Montney Drilling and Completion Costs‐Long term target of $7.5 million is achievable

0

10

20

30

40

50

60

70

80

$‐

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

$7,000

$8,000

# of frac

stages

Total $/m

HZ

Total $/m HZ

# of frac stagesTotal $/m HZ includes pilot hole

Dunvegan

Dunvegan

Wilrich

Wilrich

Falhe

r

Dunvegan HZ GasDunvegan HZ OilWilrich HZFalher HZ

Vertical wells in trend

CQE Dunvegan/Falher Rights

R25W5R1W6 R26R27R2

T60

T61

T62

T63

Simonette Dunvegan, Falher and Wilrich plays

Dunvegan Oil and Gas/Condensate play 10‐2 well 90 day IP was 13

MMcf/d 5‐2 well 60 day IP was 9

MMcf/d Cequence has 11 net potential

sections on trend Up to 25 BCF/sec resource

potential

Falher play First two CQE wells – average

90 day IP of 5.5 MMcf/d with 21 bbls/MMcf condensate

Cequence has mapped 28 potential locations on 14 net existing sections

Analog pool produces 60 MMcf/d from 21 existing producers

Wilrich play 20 net sections currently

mapped with 40 potential locations

14

6 miles

Dunvegan Model

15

0

2

4

6

8

10

12

14

16

18

20

22

0 2 4 6 8 10 12 14 16 18 20 22 24

Daily Gas Rate (M

Mcf/d)

Months on Production

10‐02‐61‐02W6

05‐02‐61‐02W6

CQE Working Model

HALF CYCLE ECONOMICS Working Model

IP (MMcf/d)IP 30 (MMcf/d)EUR (MBoe) Raw Gas (Bcf) Condy (MBbl) NGL (MBbl)

10.59.310506.06070

CAPEX $MM (D,C + TI)ROR BT (%)NPV $MM (10%)PAYOUT (YEARS)CAPITAL EFFICIENCY(1st YEAR, $/Boed)

7.51639.90.88,500

Assumes 23 Bbls/MMcf of NGL’s and condensate Assumes $4.00/GJ AECO, $90 WTI flat

Year 1 Opex $2.00 per Boe Gas rate does not include liquids

Falher Model

16

0

2

4

6

8

10

12

14

0 2 4 6 8 10 12 14 16 18 20 22 24

Daily Gas Rate (M

Mcf/d)

Months on Production

16‐18‐61‐01W6

07‐06‐61‐01W6

CQE Working Model

MODEL

HALF CYCLE ECONOMICS Working Model

IP (MMcf/d)IP 30 (MMcf/d)EUR (MBoe) Raw Gas (Bcf) Condy (MBbl) NGL (MBbl)

7.86.08004.011060

CAPEX $MM (D,C + TI)ROR BT (%)NPV $MM (10%)PAYOUT (YEARS)CAPITAL EFFICIENCY(1st YEAR, $/Boed)

8.0535.71.7

15,000

Assumes 45 Bbls/MMcf of NGL’s and condensate Assumes $4.00/GJ AECO, $90 WTI flat

Year 1 Opex $2.00 per Boe Gas rate does not include liquids

Conclusions

17

Simonette Project – start of significant development drilling program to unlock this large resource play

Financial strength ‐ strong balance sheet with $135 million undrawn bank facility through year end 2014

Team has a proven record of capturing large resource opportunities

Highly experienced Board of Directors and Deep Basin Management team with significant ownership

18

Appendix

Cequence Simonette 13‐11 Compressor Station

Management and Board

19

Management Team

Paul Wanklyn ‐ President and CEOPaul Wanklyn ‐ President and CEO

Howard Crone ‐ Executive VP and COOHoward Crone ‐ Executive VP and COO

Steve Stretch ‐ VP Exploration and Chief GeophysicistSteve Stretch ‐ VP Exploration and Chief Geophysicist

Dave Gillis ‐ VP Finance and CFODave Gillis ‐ VP Finance and CFO

Dave Robinson ‐ VP Exploration and Chief GeologistDave Robinson ‐ VP Exploration and Chief Geologist

James Jackson ‐ VP EngineeringJames Jackson ‐ VP Engineering

Chris Soby ‐ VP Land and Corporate DevelopmentChris Soby ‐ VP Land and Corporate Development

Mike Stewart ‐ VP OperationsMike Stewart ‐ VP Operations

Erin Thorson ‐ ControllerErin Thorson ‐ Controller

Board of Directors

Don Archibald ‐ ChairmanDon Archibald ‐ Chairman

Peter BannisterPeter Bannister

Rob CookRob Cook

Howard CroneHoward Crone

Brian FeleskyBrian Felesky

Daryl GilbertDaryl Gilbert

Frank MeleFrank Mele

Paul WanklynPaul Wanklyn

James Gray ‐ Director EmeritusJames Gray ‐ Director Emeritus

Financial Highlights

Q1 2014 Q4 2013 % Change

Average Daily Production (Boe/d) 11,613 10,394 12

Funds flow from operations ($M) (1) $23,082 $14,855 55

Per share, basic and diluted $0.11 $0.07 57

Operating costs per Boe $7.40 $7.33 1

G&A per Boe $2.34 $1.65 42

Capital expenditures, net ($M) $55,318 $51,531 7

Net debt and working capital (deficiency) ($M)(2) ($143,536) ($111,433) 29

Weighted average shares outstanding (diluted) (M) 210,918 210,917 0

20

(1) Funds flow from operations is calculated as cash flow from operating activities before adjustments fordecommissioning liabilities expenditures and net changes in non‐cash working capital(2) Net debt and working capital (deficiency) is calculated as cash and net working capital less commodity contractassets and liabilities and demand credit facilities, long term debt and excluding other liabilities

Production and Cash Costs

21

(1) Operating cost, transportation, G&A and Interest

Simonette will drive 44% growth to exit in 2015

Total cash costs are in the top quartile of Canadian producers

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

2010 2011 2012 2013 2014Est.

Q12015Est.

Boe/d

Production (Boe/d)

Natural Gas Oil & NGL

Merger with Temple Energy

Includes Ansell disposition July 7 close

$0

$2

$4

$6

$8

$10

$12

$14

$16

$18

$20

2010 2011 2012 2013 2014Est.

Q12015Est.

$/Bo

e

Cash Cost ($/Boe)

Cash Cost ($/Boe)

Netback Table – Q1 2014

Simonette Corporate Total

Average daily production (Boe/d) 8,263 11,612Natural gas (MMcf/d) 41.7 59.9

Oil and liquids (Bbls/d) 1,308 1,630

Sales price ($/Boe) $45.76 $44.29

Royalties ($/Boe) ($4.08) ($4.13)

Operating cost ($/Boe) ($5.59) ($7.40)

Transportation cost ($/Boe) ($1.13) ($1.52)

Operating netback $34.96 $31.25

G&A ($/Boe) ($2.34)

Interest ($/Boe) ($1.79)

Cashflow netback ($/Boe) $22.14

22

Note: AECO C spot price of $5.59 CDN$/Mcf and WTI crude oil price of $98.65 US$/Bbl

Hedging

Contract Type Volume GJ/d CAD Price

2014 July 1, 2014 to December 31, 2014 Average GasSwap 30,000 $3.43/GJ AECO or

$3.90/Mcf

2015 January 1, 2015 to March 31, 2015 Average Gas Swap 20,000 $3.79/GJ AECO or

$4.32/Mcf

2015 April 1, 2015 to December 31, 2015 Average Gas Swap 10,000 $3.73/GJ AECO or

$4.25/Mcf

23

(1) Percentage calculated assuming current forecast production net of royalties and an estimated heat content

Reserves and Finding Costs – solid growth per share in reserves and value

$0.00

$2.00

$4.00

$6.00

$8.00

$10.00

$12.00

$14.00

$16.00

2010 2011 2012 2013

FD&A ($/Boe)

Proved + Probable (Incl FDC)

24

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0

20

40

60

80

100

120

140

2010 2011 2012 2013Proved + Probable (2)Total Proved2P per share

49

91

67

3

4

5

6

0

200

400

600

800

1000

1200

2010 2011 2012 2013

2P Reserve Value

Reserve Value 2P per shareProved + Probable GLJ Dec.31, 2013

$1,004(1)

$525

$715$797

Reserves

109

MMBo

e

Boe/share

$MM

$/share

3 year average $11.61 per Boe Reserves increased

122% since 2010

Reserve value has doubled since 2010

(1) NPV10(2) Pro forma Ansell disposition

0

5,000

10,000

15,000

20,000

1.00 2.00 3.00 4.00 5.00 6.00 7.00

NPV

10%

BT ($M)

Flat AECO Gas Price ($/MMBtu)

3.0 BCF + NGL's 5.0 BCF + NGL's 7.0 BCF + NGL's

25

Montney Half Cycle Economics ‐ Sensitivity to Flat Gas Price and Recoverable Gas in Place per Well

Assumptions:Net NGL Yield: 30 Bbl/MMcf C3+Capital: $7.5 MMOil Price: $90/Bbl WTI

Notes: With 5% GORR, Oil $90/Bbl, C3 $31.5/Bbl,C4 $70/Bbl, C5+ $95/Bbl

Simonette Deep Basin Stack

26

Dunvegan

Falher Bluesky / Gething

MontneyWilrich

Simonette Upper

Simonette Lower

CURRENT HORIZONTAL TARGET ZONE

POTENTIAL HORIZONTAL TARGET ZONE

CEQUENCE LAND

27

5‐25 BCF

5‐24 BCF 5‐24 BCF

5‐25 BCF

30‐60 BCF

Dunvegan

FalherWilrich

Gething

UpperMontney

Zone Total ResourcePotential/Sec (1)

2,400m

2,950m

3,100m

2,700m

2,500m

2,800m

(1) See Forward‐Looking Information and Definitions for definition of total resource

6 miles

Multiple Zones with Significant Resource Potential at Simonette

Alberta Deep Basin ‐Montney HZ First 6 month cumulative gas production

28

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

1.8

Cum Gas (B

CF)

Cequence Wells

Average of CQE Wells540 MMcf

Average All Wells390 MMcf

Industry Wells

137 gas wells with production to Dec. 31, 2013, Geoscout data Oil wells excluded.

Alberta Deep Basin Montney HZ Drilling Analysis –CQE among most efficient drillers

29

Includes pilot wells, does not include re‐entries

0

2000

4000

6000

8000

10000

12000

0

50

100

150

200

250

300

2012 and older ‐ 245 wells

Measured Dep

th (m

)

0

2000

4000

6000

8000

10000

12000

0

50

100

150

200

250

300

Meters drilled

per day (m

)

2013 – 63 wells

CQE P50187 m/day

All Wells P50123 m/day

Measured Dep

th (m

)

Competitor WellsCequence Wells

CQE P50137 m/day

All Wells P50107 m/day

Cequence Wells Competitor Wells Measured Depth Measured Depth

Forward‐Looking Statements or Information and Definitions

Certain statements included in this presentation constitute forward‐looking statements or forward‐looking information under applicable securities legislation. Suchforward‐looking statements or information are provided for the purpose of providing information about management's current expectations and plans relating to thefuture. Readers are cautioned that reliance on such information may not be appropriate for other purposes, such as making investment decisions. Forward‐lookingstatements or information typically contain statements with words such as "anticipate", "believe", "expect", "plan", "intend", "estimate", "propose", "project" or similarwords suggesting future outcomes or statements regarding an outlook. Forward‐looking statements or information concerning Cequence in this presentation mayinclude, but are not limited to, statements or information with respect to: guidance, forecasts and related assumptions; expected production growth and cash flowgrowth and the respective timing thereof; use of proceeds from the CPPIB Private Debt Placement; the Company's plan to not issue additional equity until year‐end2018; capital spending; expected resource potential and future reserves; hedging objectives; business strategy and objectives; type curves; drilling, development andexploration plans and the timing, associated costs and results thereof; future net debt and funds flow; commodity pricing and expected royalties; costs associated withoperating in the oil and natural gas business; and future production levels, including the composition thereof. Forward‐looking statements or information are based on anumber of factors and assumptions which have been used to develop such statements and information but which may prove to be incorrect. The Company believes thatthe expectations reflected in such forward‐looking statements or information are reasonable; however, undue reliance should not be placed on forward‐lookingstatements because the Company can give no assurance that such expectations will prove to be correct. In addition to other factors and assumptions which may beidentified in this presentation, assumptions have been made regarding, among other things: the impact of increasing competition; the timely receipt of any requiredregulatory approvals; the ability of the Company to obtain qualified staff, equipment and services in a timely and cost efficient manner; the ability of the operator of theprojects which the Company has an interest in to operate the field in a safe, efficient and effective manner; the ability of the Company to obtain financing on acceptableterms; field production rates and decline rates; the ability to replace and expand oil and natural gas reserves through acquisition, development or exploration; thetiming and costs of operating the Company’s business; the ability of the Company to secure adequate product transportation; future oil and natural gas prices; currency,exchange and interest rates; the regulatory framework regarding royalties, taxes and environmental matters; and the ability of the Company to successfully market itsoil and natural gas products. Readers are cautioned that the foregoing list is not exhaustive of all factors and assumptions which have been used.

Forward‐looking statements or information are based on current expectations, estimates and projections that involve a number of risks and uncertainties which couldcause actual results to differ materially from those anticipated by the Company and described in the forward‐looking statements or information. These risks anduncertainties may cause actual results to differ materially from the forward‐looking statements or information. The material risk factors affecting the Company and itsbusiness are contained in the Company's Annual Information Form which is available at SEDAR at www.sedar.com.The forward‐looking statements or information contained in this presentation are made as of the date hereof and the Company undertakes no obligation to updatepublicly or revise any forward‐looking statements or information, whether as a result of new information, future events or otherwise unless required by applicablesecurities laws. The forward‐looking statements or information contained in this presentation are expressly qualified by this cautionary statement.

30

Forward‐Looking Statements or Information and Definitions

Additional AdvisoriesThis presentation contains references to terms commonly used in the oil and gas industry. Netback is not defined by IFRS in Canada and is referred to as a non‐GAAPmeasure. Netbacks equal total revenue less royalties, operating costs and transportation costs. Management utilizes this measure to analyze operating performance.Funds flow from operations is a non‐GAAP term that represents cash flow from operating activities before adjustments for decommissioning liability expenditures andchanges in working capital. The Company evaluates its performance based on earnings and funds flow from operations. The Company considers funds flow fromoperations to be a key measure as it demonstrates the Company's ability to generate the cash flow necessary to fund future growth through capital investment and torepay debt. The Company's calculation of funds flow from operations may not be comparable to that reported by other companies. Funds flow from operations per shareis calculated using the same weighted average number of shares outstanding used in the calculation of income (loss) per share."Total resources" are that quantity of petroleum that is estimated to exist originally in naturally occurring accumulations. Total resources include that quantity ofpetroleum that is internally estimated, at a given date, to be contained in known accumulations, prior to production, plus those quantities in accumulations yet to bediscovered.Discovered Petroleum in Place ("DPIIP") and "Contingent Resources": DPIIP is equivalent to discovered resources and is defined in the Canadian Oil and Gas EvaluationHandbook ("COGEH") as that quantity of petroleum that is estimated, as of a given date, to be contained in known accumulations prior to production. The recoverableportion of discovered petroleum initially‐in‐place includes production, reserves and contingent resources; the remainder is unrecoverable. "Contingent Resources" aredefined in COGEH as those quantities of petroleum estimated to be potentially recoverable from known accumulations using established technology or technology underdevelopment, but which are not currently considered to be economically recoverable due to one or more contingencies. Contingencies may include factors such aseconomic, legal, environmental, political, and regulatory matters, or a lack of markets. It is also appropriate to classify as contingent resources the estimated discoveredrecoverable quantities associated with a project in the early evaluation stage. The Contingent Resources estimates and the DPIIP estimates are estimates only and theactual results may be greater or less than the estimates provided herein. There is no certainty that it will be commercially viable to produce any portion of the resourcesexcept to the extent identified as proved or probable reserves."Best estimate" is defined in COGEH with respect to entity level estimates, as the value derived by an evaluator using deterministic methods that best represent theexpected outcome with no optimism or conservatism. If probabilistic methods are used, there should be at least a 50 percent probability (P50) that the quantities actuallyrecovered will equal or exceed the best estimate.The foregoing outlook and guidance has been provided to assist investors in analyzing the Company’s anticipated development strategies and prospects and it may not beappropriate for other purposes and actual results could differ from the guidance provided above. Cequence refers to initial production rates which may not be indicativeof long term well performance.BOEs are presented on the basis of one BOE for six Mcf of natural gas. Disclosure provided herein in respect of BOEs may be misleading, particularly if used in isolation. ABOE conversion ratio of 6 Mcf:1 Bbl is based on an energy equivalency conversion method primarily applicable at the burner tip and does not represent a valueequivalency at the wellhead.For the three months ended March 31, 2014, the ratio between the average price of West Texas Intermediate (“WTI”) crude oil at Cushing and NYMEX natural gas wasapproximately 21:1 (“Value Ratio”). The Value Ratio is obtained using the first quarter 2014 WTI average price of $98.65 (US$/Bbl) for crude oil and the first quarter 2014NYMEX average price of $4.72 (US$/MMbtu) for natural gas. This Value Ratio is significantly different from the energy equivalency ratio of 6:1 and using a 6:1 ratio wouldbe misleading as an indication of value.

31

Contacts:Paul WanklynPresident & CEO pwanklyn@cequence‐energy.com

www.cequence-energy.com3100, 525 - 8th Avenue SW Calgary AB T2P 1G1Phone: 403-229-3050 Fax: 403-229-0603

David GillisVice President, Finance & CFOdgillis@cequence‐energy.com