JPMorgan Diversified Alternatives ETF - J.P. Morgan …. MORGAN DIVERSIFIED ALTERNATIVES ETF EMPLOYS...

22

FOR INSTITUTIONAL USE ONLY | NOT FOR PUBLIC DISTRIBUTION JPMorgan Diversified Alternatives ETF J.P. Morgan Asset Management | 2016

-

Upload

truongcong -

Category

Documents

-

view

220 -

download

1

Transcript of JPMorgan Diversified Alternatives ETF - J.P. Morgan …. MORGAN DIVERSIFIED ALTERNATIVES ETF EMPLOYS...

FOR INSTITUTIONAL USE ONLY | NOT FOR PUBLIC DISTRIBUTION

JPMorgan Diversified Alternatives ETF

J.P. Morgan Asset Management | 2016

1 | FOR INSTITUTIONAL USE ONLY | NOT FOR PUBLIC DISTRIBUTION

GUIDE TO THE MARKETS – PAGES 32,36 2

(NOMINAL 10-YEAR TREASURY YIELD)

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

'62 '67 '72 '77 '82 '87 '92 '97 '02 '07 '12

GUIDE TO THE MARKETS – PAGE 4 1

(S&P 500 INDEX AT INFLECTION POINTS)

600

800

1,000

1,200

1,400

1,600

1,800

2,000

2,200

'97 '98 '99 '00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '14 '15 '16

Current equity market levels and the prospect of rising rates may mean lower returns

and higher volatility in traditional portfolios

1 Source: J.P. Morgan Asset Management Guide to the Market 3Q 2016, Standard & Poor’s, Compustat, FactSet. Dividend yield is calculated as the annualized dividend rate divided by price, as provided

by Compustat. Forward Price to Earnings Ratio is a bottom-up calculation based on the most recent S&P500 Index Price, divided by consensus estimates for earnings in the next 12 months (NTM), and is

provided by FactSet Market Aggregates. Returns are cumulative and based on S&P500 Index price movement only, and do not include the reinvestment of dividends.

2 Source: J.P. Morgan Asset Management Guide to the Market 3Q 2016, Federal Reserve, BLS, Barclays Capital, U.S. Treasury. Change in bond prices is calculated using both duration and convexity

according to the following formula: New Price = (Price + (Price * -Duration * Change in Interest Rates)) + (0.5 * Price * Convexity * (Change in Interest Rates)^2).

Shown for illustrative purposes only. Past performance is not indicative of future results.

S&P 500 INDEX AT INFLECTION POINTS… …AND U.S. INTEREST RATE CYCLE IN TRANSITION

-19.2%

-8.7%

-4.7%

-4.9%

-2.0%

-25% -20% -15% -10% -5% 0%

30y UST

10y UST

5y UST

TIPS

2y UST

PRICE IMPACT OF A 1% RISE IN

INTEREST RATES Characteristic Mar-2000 Oct-2007 Mar-2016

Index Level 1,527 1,565 2,099

P/E Ratio (fwd.) 27.2x 15.7x 16.6x

Dividend Yield 1.1% 1.8% 2.3%

Dec. 31, 1996

P/E (fwd.) = 16.0x

741

+106%

Mar. 24, 2000

P/E (fwd.) = 27.2x

1,527

-49%

Oct. 9, 2002

P/E (fwd.) = 14.1x

777

+101%

Oct. 9, 2007

P/E (fwd.) = 15.7x

1,565

-57%

Mar. 9, 2009

P/E (fwd.) = 10.3x

677

+210%

Jun. 30, 2016

P/E (fwd.) = 16.6x

2,099

Sep. 30, 1981:

15.84%

Jun. 30, 2016:

1.49%

2 | FOR INSTITUTIONAL USE ONLY | NOT FOR PUBLIC DISTRIBUTION

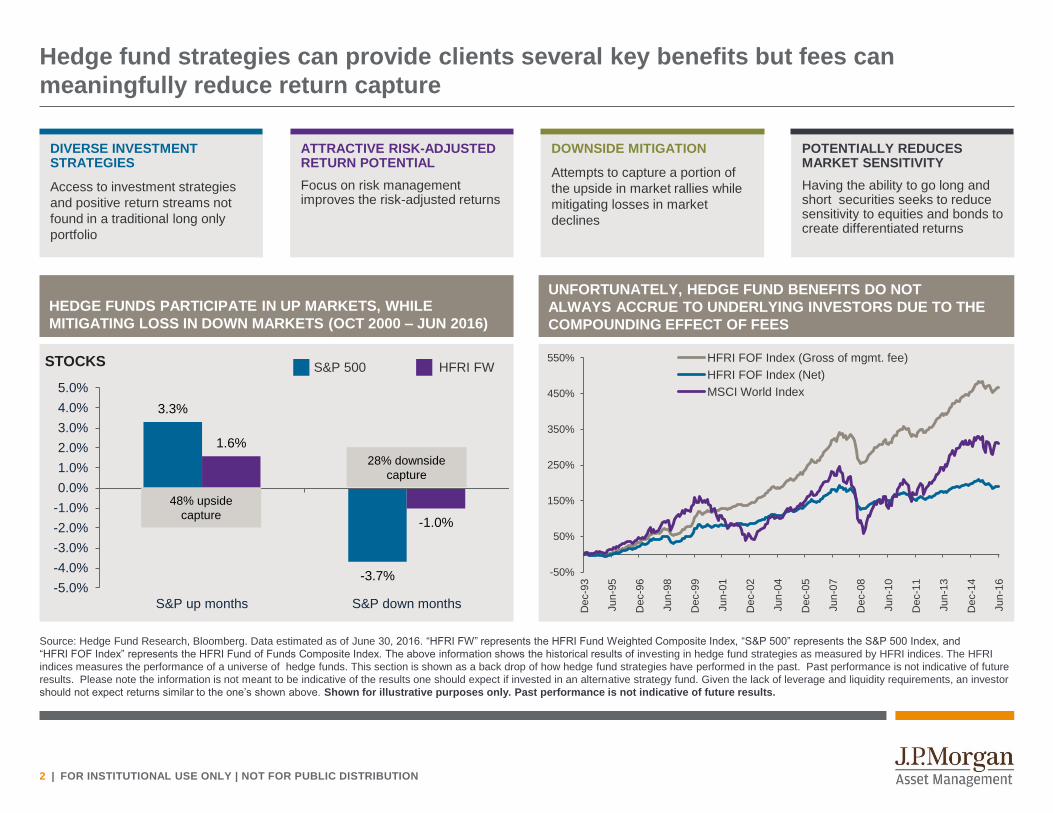

Hedge fund strategies can provide clients several key benefits but fees can

meaningfully reduce return capture

Source: Hedge Fund Research, Bloomberg. Data estimated as of June 30, 2016. “HFRI FW” represents the HFRI Fund Weighted Composite Index, “S&P 500” represents the S&P 500 Index, and

“HFRI FOF Index” represents the HFRI Fund of Funds Composite Index. The above information shows the historical results of investing in hedge fund strategies as measured by HFRI indices. The HFRI

indices measures the performance of a universe of hedge funds. This section is shown as a back drop of how hedge fund strategies have performed in the past. Past performance is not indicative of future

results. Please note the information is not meant to be indicative of the results one should expect if invested in an alternative strategy fund. Given the lack of leverage and liquidity requirements, an investor

should not expect returns similar to the one’s shown above. Shown for illustrative purposes only. Past performance is not indicative of future results.

HEDGE FUNDS PARTICIPATE IN UP MARKETS, WHILE

MITIGATING LOSS IN DOWN MARKETS (OCT 2000 – JUN 2016)

3.3%

-3.7%

1.6%

-1.0%

-5.0%

-4.0%

-3.0%

-2.0%

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

S&P up months S&P down months

48% upside

capture

28% downside

capture

S&P 500 HFRI FW STOCKS

-50%

50%

150%

250%

350%

450%

550%

Dec-9

3

Jun

-95

Dec-9

6

Jun

-98

Dec-9

9

Jun

-01

Dec-0

2

Jun

-04

Dec-0

5

Jun

-07

Dec-0

8

Jun

-10

Dec-1

1

Jun

-13

Dec-1

4

Jun

-16

HFRI FOF Index (Gross of mgmt. fee)

HFRI FOF Index (Net)

MSCI World Index

UNFORTUNATELY, HEDGE FUND BENEFITS DO NOT

ALWAYS ACCRUE TO UNDERLYING INVESTORS DUE TO THE

COMPOUNDING EFFECT OF FEES

DIVERSE INVESTMENT STRATEGIES

Access to investment strategies

and positive return streams not

found in a traditional long only

portfolio

ATTRACTIVE RISK-ADJUSTED RETURN POTENTIAL

Focus on risk management improves the risk-adjusted returns

DOWNSIDE MITIGATION

Attempts to capture a portion of

the upside in market rallies while

mitigating losses in market

declines

POTENTIALLY REDUCES MARKET SENSITIVITY

Having the ability to go long and short securities seeks to reduce sensitivity to equities and bonds to create differentiated returns

3 | FOR INSTITUTIONAL USE ONLY | NOT FOR PUBLIC DISTRIBUTION

Hedge fund strategies, once offered only to institutional clients, are now offered to

retail clients

COMMON MISCONCEPTIONS ABOUT HEDGE FUND STRATEGIES

Only institutional or accredited investors can access high quality hedge fund strategies

Individual investors can access hedge fund strategies through an array of Alternative ETFs and Mutual Funds which have been created in recent years

Investing in one hedge fund strategy will diversify my portfolio

Investing in only one hedge fund strategy may provide some diversification benefits but can also concentrate risk exposures; diversifying across strategies may create a more optimal portfolio

Alternative strategies are too risky for individual investors

Prudent allocations to hedge fund strategies in a diversified portfolio can help reduce volatility and help your clients stay invested

Hedge fund returns are solely attributed to manager skill

As sources of return are better understood, a significant portion of hedge fund returns can be systematically captured

For discussion and illustrative purposes only. Diversification does not guarantee investment returns and does not eliminate the risk of loss.

4 | FOR INSTITUTIONAL USE ONLY | NOT FOR PUBLIC DISTRIBUTION

Diversified Alternatives ETF is designed to capture key exposures and benefits of

hedge fund strategies

Exposure to 80% of

hedge fund universe

AUM through

systematic bottoms-up

approach

Broad

Core Solution to diversify

investors’ portfolio

Positive Return

THE FUND IS DESIGNED TO DELIVER FUND SEEKS TO PROVIDE

Diversification

Long/Short Exposure +

-

JPM Insights

For discussion and illustrative purposes only. Diversification does not guarantee investment returns and does not eliminate the risk of loss.

There are additional risks related to short exposure and active management. Please refer to the disclosure page for additional information.

5 | FOR INSTITUTIONAL USE ONLY | NOT FOR PUBLIC DISTRIBUTION

Fund is managed by an experienced team and pioneer in hedge fund beta investing

1 Years of Experience: Industry / JPM

As of March 31, 2016. There can be no assurance that the professionals currently employed by J.P. Morgan Asset Management will continue to be employed by J.P. Morgan Asset Management or that the

past performance or success of any such professional serves as an indicator of such professional's future performance or success.

Sources: Financial News ‘40 under 40’ (2015), Pensions & Investments (November 2012), Financial Times (April 2012), Nordic Region Pensions and Investments News (April 2012)

YAZANN ROMAHI, PHD, CFA

Managing Director

Global Head of Quantitative Research

Years of Experience: 17/131

LEAD PORTFOLIO MANAGER

Supported by team of 17 investment specialists on Multi-

Asset Solutions Quantitative Strategies and Research team

– 5 dedicated technologists

Researching and developing alternative beta philosophy

since 2005

Recognized as thought leaders in the space authoring many

papers and articles

Investing in alternative beta strategies since July 2009, with

>$3.6 billion in assets under management

PORTFOLIO MANAGEMENT TEAM HIGHLIGHTS

RECOGNITION

Dr. Romahi named in the Financial News ‘40 under 40’ Rising

Hedge Fund Stars List

6 | FOR INSTITUTIONAL USE ONLY | NOT FOR PUBLIC DISTRIBUTION

GLOBAL MACRO

EQUITY LONG SHORT

EVENT-DRIVEN STRATEGIES

Sub strategies

Merger arbitrage

Spinoff announcements

Activist following

Share buybacks

Post reorganization

Index reconstitution arbitrage

Diversified Alternatives ETF is uniquely positioned in the alternatives space

Source: JP Morgan Asset Management, as of June 30, 2016. Target Equity Beta in reference to MSCI World Index

For discussion and illustrative purposes only.

HEDGE FUND INDEX REPLICATION ALTERNATIVE BETA MULTI-MANAGER

Top-down approach that seeks to replicate the

historical performance of broad hedge fund

universe

Bottom-up approach to systematically build the

exposures to beta of various hedge fund styles

(80% of universe by AUM)

Allocates to a diversified set of hedge fund styles

through highly specialized sub advisors

More Quantitative More Qualitative

J.P. MORGAN DIVERSIFIED ALTERNATIVES ETF EMPLOYS A RULES BASED, BOTTOM UP SECURITY SELECTION PROCESS

J.P. MORGAN DIVERSIFIED ALTERNATIVES ETF

Sub strategies

Carry

Momentum

Sub strategies

Value Premium

Momentum

Quality

Size Premium

Target Equity Beta: 0.3

7 | FOR INSTITUTIONAL USE ONLY | NOT FOR PUBLIC DISTRIBUTION

Employs a multi-strategy construct to access different alternative strategy styles

The manger seeks to achieve the stated objectives. There can be no guarantee the objectives will be met.

EVENT-DRIVEN

Traditionally a core hedge fund style that

seeks to exploit mispricing related to

companies that are undergoing

significant corporate change

We focus on six sub-strategies: merger

arbitrage, spinoff announcements,

activist following, share buybacks, post

reorg and index reconstitution arbitrage

We seek to capture a significant portion

of the event-driven hedge fund style

using this systematic process

Alternative Beta Sub-Strategies

EQUITY LONG / SHORT

Attempts to capture four risk factors:

Momentum, Value, Size and Quality.

These factors form the backbone of

many quantitative and qualitative equity

products and drive many equity

investment philosophies

Portfolio constructed to have a beta of

0.3, across developed markets and be

sector neutral

Broad developed market universe (S&P

Developed BMI), with a portfolio of

approximately 350 long and 300 short

positions

GLOBAL MACRO BASED STRATEGIES

Seeks to capture exposure to carry and

momentum across fixed income, currency,

commodity and equity markets

Carry trades are across 6 developed bond

markets, G10 and 20 EM currencies, and

17 commodities (roll yield)

Time series momentum trades are across

6 developed bond markets, 11 developed

market equity indices and 17 commodities

Relative value momentum trades are made

in G10 currencies and 17 commodities

8 | FOR INSTITUTIONAL USE ONLY | NOT FOR PUBLIC DISTRIBUTION

How to allocate to alternatives

For discussion and illustrative purposes only . All investment decisions should be based on prevailing market conditions as well as individual investors’ facts and financial circumstances.

Diversification does not guarantee investment returns and does not eliminate the risk of loss.

2. REALLOCATE BASED ON DESIRED OUTCOME 1. TARGET 10-20% ALLOCATION

REDUCE EQUITY BETA

INCREASE DIVERSIFICATION

REDUCE INTEREST RATE RISK

75% from Equities

25% from Fixed Income

50% from Equities

50% from Fixed Income

25% from Equities

75% from Fixed Income

3. CREATE A MIX OF ALTERNATIVES

EQUITIES

40-60%

FIXED INCOME

40-60%

ALTERNATIVES

10-20%

EQUITY

ALTERNATIVES

Diversify long-only

equity holdings by

investing in equity

alternative strategies

CORE

DIVERSIFIERS

Diversify the overall

portfolio by investing in

diversified alternative

strategies

JPMORGAN

DIVERSIFIED

ALTERNATIVES ETF

FIXED INCOME

ALTERNATIVES

Diversify long-only fixed

income holdings by

investing in fixed

income alternative

strategies

9 | FOR INSTITUTIONAL USE ONLY | NOT FOR PUBLIC DISTRIBUTION

Appendix 1: Diversified Alternatives ETF Sub-Strategies

10 | FOR INSTITUTIONAL USE ONLY | NOT FOR PUBLIC DISTRIBUTION

Approximately 15% of all activist targets turn into merger transactions

Uses 13-D filings to track activist campaigns in an effort to capture abnormal returns unrelated to classical equity risk premia

SHAREHOLDER

ACTIVISM

Attempts to capture positive performance of parent company as value is unlocked through spinoff announcement. The source of the premium is the additional information released to the markets, which typically leads to a revaluation of the company

Long positions in all parent companies post-announcement to capture post-announcement price drift, closing just prior to record date

PARENTS AND

SPINOFFS

Attempts to capture the deal risk premium inherent in merger transactions

Invests in the target company of all merger deals globally, subject to a number of size and liquidity filters, while shorting the acquirer

MERGER

ARBITRAGE

Attempts to exploit outperformance of a company engaged in a share buyback program, which is generally driven by market underreaction in the reduction in the cost of capital

Long positions in stocks whose outstanding shares have been declining while hedging the beta using equity futures

SHARE

REPURCHASES

Index changes typically pre-announced to avoid market dislocation on effective date due to price pressure from beta trackers

Buy index additions at announcement and sell on effective date; compensation for liquidity provision to the market

EQUITY INDEX

ARBITRAGE

Companies emerging from bankruptcy exhibit risk of failure, low analyst coverage, unusual shareholder composition, and have the stigma of the former bankrupt entity despite often being restructured into a different company

Buy companies that have emerged from the Chapter 11 bankruptcy process to capture this set of unique risks

POST-

REORGANIZATION

EQUITY

EVENT DRIVEN Event-driven investing: systematic capture of underlying strategies

Source: J.P. Morgan Asset Management. For illustrative purposes only.

11 | FOR INSTITUTIONAL USE ONLY | NOT FOR PUBLIC DISTRIBUTION

Event-driven

Source: Factset, Bloomberg, J.P. Morgan Asset Management, January 31, 1993 through June 30, 2016.

For illustrative purposes only.

INDEX PERFORMANCE ANALYSIS RISK-RETURN PROFILE

Periods to June 30,

2016

HFRI Event-

Driven Index

MSCI World

Index

Total return 9.7% 6.2%

Risk 6.6% 14.8%

Maximum drawdown 24.8% 55.4%

Information ratio 1.47 0.42

Beta 0.34 0%

100%

200%

300%

400%

500%

600%

700%

800%

900%

1000%

Jan-93Jan-95Jan-97Jan-99Jan-01Jan-03Jan-05Jan-07Jan-09Jan-11Jan-13Jan-15

HFRI Event Driven Index

MSCI World Index

EVENT DRIVEN

12 | FOR INSTITUTIONAL USE ONLY | NOT FOR PUBLIC DISTRIBUTION

Equity long / short – diversified, systematic capture of risk premia

Source: J.P. Morgan Asset Management. For illustrative purposes only.

Return Driver: Behavioral bias

Strategy: (1) Long positions with decreasing accruals, short stocks with growing accruals (2) Long positions with low beta, shorts stocks with high beta

QUALITY

Return Driver: Behavioral bias

Strategy: (1) Long positive earnings revision stocks, short negative revision stocks (2) Buy stocks whose momentum is in the top decile while shorting those in the bottom decile

MOMENTUM

Return Driver: Risk premium

Strategy: Long “cheap” stocks, short “expensive” stocks (as measured by P/E, Div Yld etc)

These factors form the backbone of many quantitative and qualitative equity products and drive many equity investment philosophies

VALUE PREMIUM

Return Driver: Risk premium

Strategy: Buy small cap stocks, short large cap stocks SIZE PREMIUM

EQUITY LONG/SHORT

CAPTURING THE RISK PREMIA IN OUR EQUITY LONG / SHORT STRATEGY

Equity Long/Short strategies –low correlation to equity markets

Beta profile of 0.3 similar to the beta found across different equity long short strategies

8,500 companies in universe (S&P Broad Market Index), around 300-350 long and short companies in portfolio

Diversify idiosyncratic risk, includes mid and small cap exposure

Equally weighted minimum market cap USD 500m; Liquidity: Minimum 3mth average daily volume above USD 2m

Capital efficient investment, low turnover

13 | FOR INSTITUTIONAL USE ONLY | NOT FOR PUBLIC DISTRIBUTION

Equity long / short

Source: Factset, Bloomberg, J.P. Morgan Asset Management, January 31, 1993 through June 30, 2016.

For illustrative purposes only.

INDEX PERFORMANCE ANALYSIS

0%

100%

200%

300%

400%

500%

600%

700%

800%

900%

1000%

Jan-93Jan-95Jan-97Jan-99Jan-01Jan-03Jan-05Jan-07Jan-09Jan-11Jan-13Jan-15

HFRI Equity Hedge Index

MSCI World Index

RISK-RETURN PROFILE

Periods to June 30,

2016

HFRI Equity

Hedge Index

MSCI World

Index

Total return 9.8% 6.2%

Risk 8.9% 14.8%

Maximum drawdown 30.6% 55.4%

Information ratio 1.11 0.42

Beta 0.48

EQUITY LONG/SHORT

14 | FOR INSTITUTIONAL USE ONLY | NOT FOR PUBLIC DISTRIBUTION

Time Series Momentum - across fixed income, equity indices and commodities

– Momentum measured over 3, 6, and 12 months

– Universe of 10 developed market equity indices; 6 developed market bond indices and 17 commodities

Relative Value Momentum - across currency and commodities

– Developed market FX strategy

– Commodity momentum over 17 commodities using 12 month momentum

MOMENTUM

Fixed income – compensation for uncertainty around future interest rate paths and realized inflation

– Long the long end of steepest curves and short the long end of the flattest curves

– Long the highest carry bond markets and short the lowest carry bond markets

Currency – compensation for potential exchange rate devaluation / forward rate bias

– Long the highest yielding currencies and short the lowest yielding currencies across 10 developed and 20 emerging market currencies

Commodities – compensation for price risk transfer between hedgers (producers and consumers) and speculators

– Relative Roll Yield – long backwardated commodities and short those in contango across 17 commodities

CARRY

Capturing macro risk premia

Source: J.P. Morgan Asset Management. For illustrative purposes only.

CAPTURING THE MACRO RISK PREMIA IN OUR GLOBAL MACRO STRATEGY

Carry and momentum strategies across asset classes are uncorrelated

Within carry and within momentum, the strategies are also generally uncorrelated

The two fixed income carry strategies are negatively correlated

FX strategies exhibit the highest correlation within an asset class but are still diversifying to one another

Use both time series momentum and relative value momentum

GLOBAL MACRO

15 | FOR INSTITUTIONAL USE ONLY | NOT FOR PUBLIC DISTRIBUTION

Global macro

Source: Factset, Bloomberg, J.P. Morgan Asset Management, January 31, 1993 through June 30, 2016.

For illustrative purposes only.

INDEX PERFORMANCE ANALYSIS RISK-RETURN PROFILE

Periods to June 30,

2016

HFRI Macro

Index

MSCI World

Index

Total return 8.6% 6.2%

Risk 6.8% 14.8%

Maximum drawdown 10.7% 55.4%

Information ratio 1.27 0.42

Beta 0.16 0%

100%

200%

300%

400%

500%

600%

700%

800%

900%

1000%

Jan-93 Jan-95 Jan-97 Jan-99 Jan-01 Jan-03 Jan-05 Jan-07 Jan-09 Jan-11 Jan-13 Jan-15

HFRI Macro Index

MSCI World Index

GLOBAL MACRO

FOR INSTITUTIONAL USE ONLY | NOT FOR PUBLIC DISTRIBUTION

Appendix 2: Team Overview

17 | FOR INSTITUTIONAL USE ONLY | NOT FOR PUBLIC DISTRIBUTION

Quantitative strategies and research team

Source: J.P. Morgan Asset Management. As of March 31st 2016. There can be no assurance that the professionals currently employed by J.P. Morgan Asset Management will continue to be employed by

J.P. Morgan Asset Management or that the past performance or success of any such professional serves as an indicator of such professional's future performance or success.

JAMES ELLIOT

MULTI-ASSET SOLUTIONS, CIO INTERNATIONAL

Investment Director Review

Model Risk and Development

INDEPENDENT FUNCTIONS

JPMAM Risk Management

GIM SOLUTIONS - MASCOO

GIMS – MAS MIDDLE OFFICE

Katherine

Santiago

Kartik

Aiyar

Victor

Li

Jonathan

Msika

Joe

Staines

Albert

Chuang

YAZANN ROMAHI

GLOBAL HEAD OF ALTERNATIVE BETA AND QUANTITATIVE RESEARCH

QUANTITATIVE STRATEGIES AND RESEARCH

Steven

Wu

Yann

Vestring

Grace

Koo

Abdullah

Sheikh

Livia

Wu

David

Lu

GLOBAL RESEARCH TECHNOLOGY

Kai

Shen

Rafael

Forte

Kent

Zheng

Erkut

Gokan

Oleg

Mihailik

KEY INVESTMENT PARTNERS

John Bilton,

Head of Global

Multi-Asset Strategy

Antony Vallee,

Head of Convertible

Bond and Capital

Structure Team

Shrenick Shah,

Total Return

Portfolio Manager

Talib Sheikh,

Total Return

Portfolio Manager

18 | FOR INSTITUTIONAL USE ONLY | NOT FOR PUBLIC DISTRIBUTION

Key personnel

There can be no assurances that the professionals currently employed by JPMAM will continue to be employed by JPMAM or that the past performance or success of any such professional serves as an

indicator of such professional’s future performance or success.

YAZANN ROMAHI

Yazann Romahi, PhD, CFA, managing director, is the Head of Research and Quantitative Strategies in GIM - Multi Asset

Solutions. The Research and Quantitative Strategies Team is responsible for the quantitative models that help establish the

broad asset allocation reflected across Multi-Asset Solutions portfolios globally. In addition, Yazann and his team are

responsible for the design and portfolio management of the Alternative Beta suite of products. An employee since 2003, prior

to joining J.P.Morgan, Yazann worked as a research analyst at the Centre for Financial Research at the University of

Cambridge and undertook consulting assignments for a number of financial institutions including Pioneer Asset

Management, PricewaterhouseCoopers and HSBC. Yazann holds a PhD in Applied Mathematics from the University of

Cambridge and is a CFA charterholder.

VICTOR LI

Victor Li, PhD, CFA, vice president, is a portfolio manager for the Alternative Beta suite of products in the Quantitative

Portfolio Strategies team within Global Investment Management-Multi Asset Solutions based in London. He is a member of

the quantitative research team focused on quantitative asset allocation and global Multi-strategy. An employee since July

2010, Victor joined the firm after completing a PhD in Communications and Signal Processing at Imperial College London,

where he was also employed as a full time research assistant. Victor also obtained an MSc with Distinction in

Communications Engineering from the University of Manchester and a BEng in Information Engineering from the Beijing

Institute of Technology. He is a CFA charterholder.

19 | FOR INSTITUTIONAL USE ONLY | NOT FOR PUBLIC DISTRIBUTION

Glossary of terms

Normal backwardation is when the futures price is below the expected future spot price. This is desirable for speculators who are net long in their

positions; they want the futures price to increase. Thus, normal backwardation is when the futures price is increasing

Contango is when the futures price is above the expected future spot price. Because the futures price must converge on the expected future spot

price, contango implies that future prices are falling over time as new information brings them into line with the expected future spot price

Spot price is the current price at which a particular commodity, security or currency can be bought or sold at a specified time and place

The maximum drawdown is the largest percentage drawdown that has occurred in any investment data record from peak to trough

Beta is a measure of the volatility, or systematic risk, of a security or a portfolio in comparison to the market as a whole. Beta is calculated using

regression. A beta of one indicates that the security’s price will move in line with the market. A beta less than one means that the security will be

less volatile than the market. A beta greater than one indicates that the security’s price will be more volatile than the market

Alpha is the portion of an investment return arising from a specific (non-market) risk. It is an estimate of the amount of return expected from an

investment’s inherent values and is distinct from the amount of return caused by volatility, which is measured by beta

Volatility is the characteristic of a security, commodity or market to rise or fall sharply in price within a short-term period. A measure of the relative

volatility of a stock to the overall market is its beta

Carry refers to return obtained from an asset (if positive) or cost of holding an asset (if negative). Carry is usually associated with a currency carry

trade where an investor sells a certain low-yielding currency and uses the funds to buy a different currency yielding a higher interest rate. The

strategy attempts to capture the difference between the rates

Forward rate bias refers to tendency of currency markets to over-estimate changes in exchange rates, whereby actual movements tend to be

smaller than those implied by forward rates

Momentum investing is a strategy that aims to capture the continuation of existing trends in the market. Two different forms of momentum investing

include: 1) time series momentum, and 2) relative value momentum. Time series momentum refers to the potential asset pricing anomaly whereby

past returns of an investment instrument may be a positive predictor of its future return Relative value momentum refers to the potential asset

pricing anomaly whereby an investment instrument’s relative or cross-sectional returns may be a positive predictor of its future return

Information ratio is a ratio of excess portfolio returns (relative to benchmark) divided by the volatility of excess returns (relative to benchmark)

For illustrative and discussion purposes only.

20 | FOR INSTITUTIONAL USE ONLY | NOT FOR PUBLIC DISTRIBUTION

J.P. Morgan Asset Management

RISKS ASSOCIATED WITH INVESTING

Investing involves risk, including possible loss of principal. The price of equity securities may rise or fall because of changes in the broad market or changes in a company’s financial condition, sometimes

rapidly or unpredictably. These price movements may result from factors affecting individual companies, sectors or industries selected for the portfolio or the securities market as a whole, such as changes in

economic or political conditions. Investments in smaller companies may be riskier, more volatile and more vulnerable to economic, market and industry changes.

There is no guarantee that the use of long and short positions will succeed in limiting the Fund's exposure to domestic stock market movements, capitalization, sector-swings or other risk factors. Investment

in a portfolio involved in long and short selling may have higher portfolio turnover rates. This will likely result in additional tax consequences. Short selling involves certain risks, including additional costs

associated with covering short positions and a possibility of unlimited loss on certain short sale positions. The Securities and Exchange Commission (SEC) and financial industry regulatory authorities in

other countries may impose prohibitions, restrictions or other regulatory requirements on short sales, which could inhibit the ability of the adviser to enter into short sale transactions on behalf of the Fund.

Investments in bonds and other debt securities will change in value based on changes in interest rates. If rates rise, the value of these investments generally drops. Securities with greater interest rate

sensitivity and longer are subject to greater fluctuations in value. Credit risk is the risk of loss of principal or loss of a financial reward stemming from a borrower’s failure to repay a loan or otherwise meet a

contractual obligation.

International investing involves a greater degree of risk and increased volatility. Changes in currency exchange rates and differences in accounting and taxation policies outside the U.S. can raise or lower

returns. Also, some overseas markets may not be as politically and economically stable as the United States and other nations. Investments that are concentrated in a single country or region are subject to

the additional risk associated with a smaller number of issuers. International investing bears greater risk due to social, economic, regulatory and political instability in countries in "emerging markets." This

makes emerging market securities more volatile and less liquid developed market securities. Changes in exchange rates and differences in accounting and taxation policies outside the U.S. can also affect

returns.

Investing in alternative assets involves higher risks than traditional investments and is suitable only for sophisticated investors. Alternative investments involve greater risks than traditional investments and

should not be deemed a complete investment program. They are not tax efficient and an investor should consult with his/her tax advisor prior to investing. Alternative investments have higher fees than

traditional investments and they may also be highly leveraged and engage in speculative investment techniques, which can magnify the potential for investment loss or gain. The value of the investment may

fall as well as rise and investors may get back less than they invested.

The Fund will also employ various alternative investment strategies that involve the use of complicated investment techniques. There is no guarantee that these strategies will succeed and their use may

subject the Fund to greater volatility and loss. Alternative strategies involve complex securities transactions that involve risks in addition to those risks with direct investments in securities.

The Fund will invest in derivatives, including swaps, futures, options, and forward contracts, which may be riskier than other types of investments and may increase the volatility of the Fund. Derivatives may

be sensitive to changes in economic and market conditions and may create leverage, which could result in significant losses. Derivatives expose the Fund to counterparty risk, which is the risk that the

derivative counterparty will not fulfill its contractual obligations (and includes credit risk associated with the counterparty). Under normal market conditions, the adviser currently expects that a significant

portion of the Fund’s exposure will be attained through the use of derivatives. Investing in derivatives will result in a form of leverage, which may be significant. Leverage involves special risks. Derivatives

may not perform as expected, so the Fund may not realize the intended benefits. When used for hedging, the change in value of a derivative may not correlate as expected with the currency, security or

other risk being hedged. In addition, given their complexity, derivatives expose the Fund to risks of mispricing or improper valuation. The Fund may be more volatile than if the Fund had not been leveraged

because leverage tends to exaggerate the effect of any increase or decrease in the value of the Fund’s portfolio securities. The Fund cannot assure that the use of leverage will result in higher returns, and

using leverage could result in a net loss.

The Fund will likely engage in active and frequent trading leading to increased portfolio turnover, higher transaction costs, and the possibility of increased capital gains.

The Fund is actively managed and may not achieve its objective.

Diversification does not guarantee investment returns and does not eliminate the risk of loss.

ETF shares are bought and sold throughout the day on an exchange at market price (not NAV) through a brokerage account, and are not individually redeemed from the fund.

21 | FOR INSTITUTIONAL USE ONLY | NOT FOR PUBLIC DISTRIBUTION

J.P. Morgan Asset Management

Investors should carefully consider the investment objectives and risks as well as charges and expenses of the JPMorgan ETF before

investing. The prospectus contains this and other information about the ETF. Read the prospectus carefully before investing. Call

1-844-4JPM-ETF or visit www.jpmorganETFs.com to obtain a prospectus.

Opinions, estimates, forecasts, and statements of financial market trends that are based on current market conditions constitute our judgment and are

subject to change without notice. We believe the information provided here is reliable. These views and strategies described may not be suitable for all

investors. References to specific securities, asset classes and financial markets are for illustrative purposes only and are not intended to be, and

should not be interpreted as, recommendations. Past performance is no guarantee of future results.

There can be no assurance that the professionals currently employed by JPMAM will continue to be employed by JPMAM or that the past performance

or success of any such professional serves as an indicator of such professional’s future performance or success.

Any securities/portfolio holdings mentioned throughout the presentation are shown for illustrative purposes only and should not be interpreted as

recommendations to buy or sell. A full list of firm recommendations for the past year are available upon request.

Past performance does not guarantee future results. Total returns assumes reinvestment of any income. The deduction of an advisory fee reduces an

investor’s return. Actual account performance will vary on individual portfolio security selection and the applicable fee schedule. Fees are available

upon request.

Securities may be sold through J.P. Morgan Institutional Investments Inc., member FINRA/SIPC.

J.P. Morgan Asset Management is the marketing name for the asset management businesses of JPMorgan Chase & Co. Those businesses include,

but are not limited to, JPMorgan Chase Bank N.A., J.P. Morgan Investment Management Inc., Security Capital Research & Management Incorporated,

J.P. Morgan Alternative Asset Management, Inc., and J.P. Morgan Asset Management (Canada), Inc.

J.P. Morgan Funds ETF products are distributed by SEI Investments Distribution Co., which is not affiliated with J.P. Morgan Chase & Co. or any of its

affiliates.

Copyright 2016 JPMorgan Chase & Co. All rights reserved.