Journal of Technical Analysis (JOTA). Issue 54 (2000, Summer)

37

SM A Publication of Summer-Fall 2000 ● Issue 54 MARKET TECHNICIANS ASSOCIATION, INC. One World Trade Center ● Suite 4447 ● New York, NY 10048 ● 212/912-0995 ● Fax: 212/912-1064 ● e-mail: [email protected] ● www.mta.org A Not-For-Profit Professional Organization ● Incorporated 1973 MTA JOURNAL

-

Upload

beniamin-paylevanyan -

Category

Economy & Finance

-

view

153 -

download

7

Transcript of Journal of Technical Analysis (JOTA). Issue 54 (2000, Summer)

SM

A Publication of

Summer-Fall 2000 ● Issue 54

MARKET TECHNICIANS ASSOCIATION, INC.One World Trade Center ● Suite 4447 ● New York, NY 10048 ● 212/912-0995 ● Fax: 212/912-1064 ● e-mail: [email protected] ● www.mta.org

A Not-For-Profit Professional Organization ● Incorporated 1973

MTAJOURNAL

MTA JOURNAL • Summer-Fall 2000 2

THE MTA JOURNAL – TABLE OF CONTENTS

SUMMER - FALL 2000 • ISSUE 54

12345

MTA JOURNAL EDITORIAL STAFF 3

ABOUT THE MTA JOURNAL 4

MTA MEMBER AND AFFILIATE INFORMATION 5

1999-2000 BOARD OF DIRECTORS AND MANAGEMENT COMMITTEE 6

EDITORIAL COMMENTARYADDRESS TO MTA 25TH ANNIVERSARY SEMINAR – MAY 2000 – “LIVING LEGENDS” PANEL 7

Robert J. Farrell

EXPLOITING VOLATILITY TO ACHIEVE A TRADING EDGE: MARKET-NEUTRAL/DELTA-NEUTRALTRADING USING THE PRISM TRADING SYSTEMS 9

Jeff Morton, M.D., CMT

MECHANICAL TRADING SYSTEM VS. THE SP 100 INDEX: CAN A MECHANICAL TRADING SYSTEMBASED ON THE FOUR WEEK RULE BEAT THE SP 100 INDEX? 13

Art Ruszkowski, CMT, M.Sc.

SCIENCE IS REVEALING THE MECHANISM OF THE WAVE PRINCIPLE 19

Robert R. Prechter, Jr., CMT

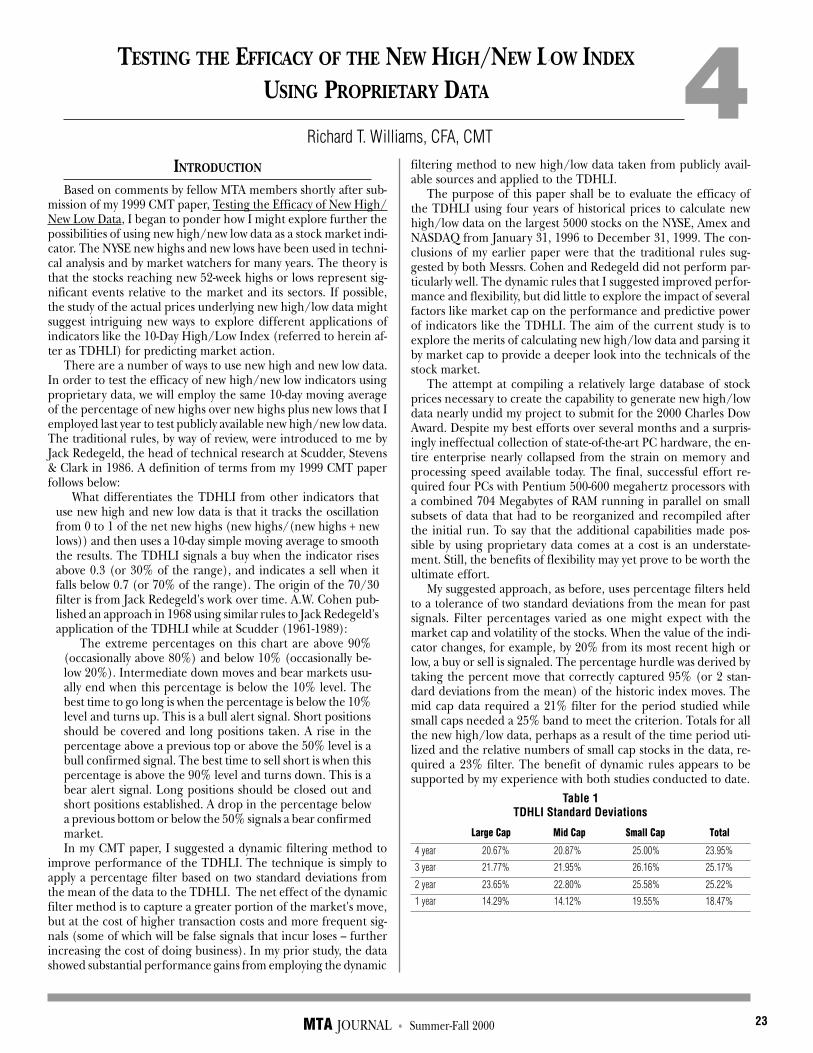

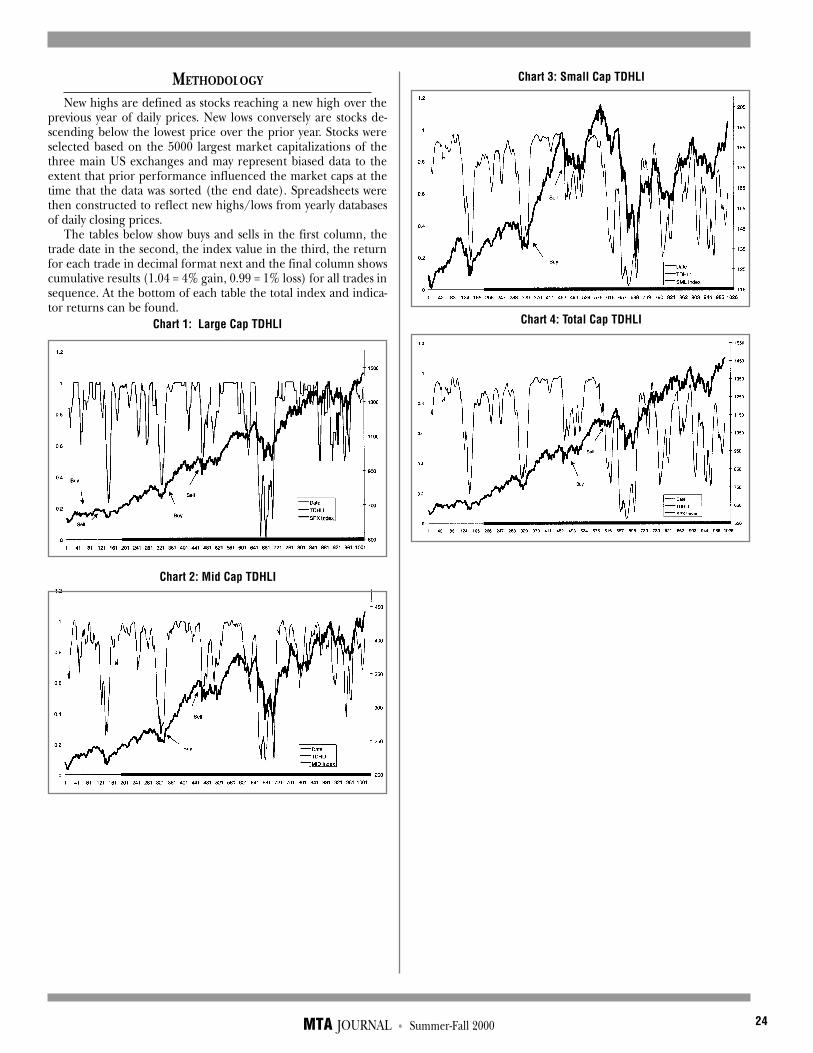

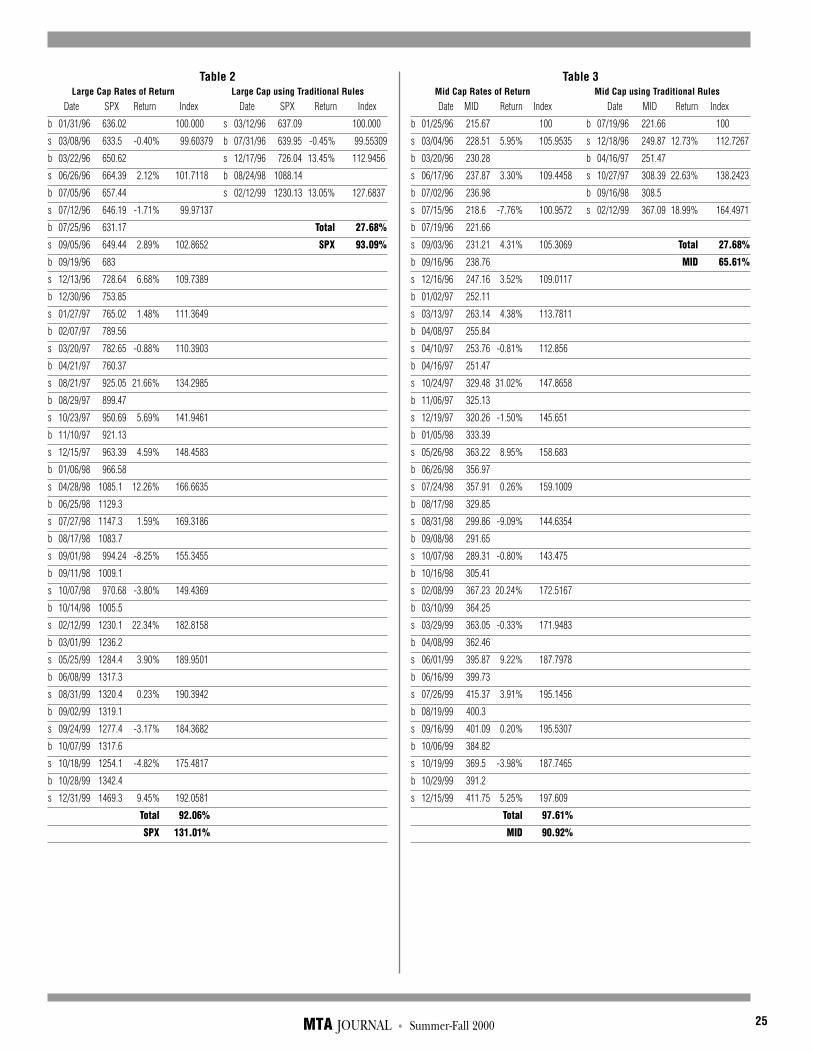

TESTING THE EFFICACY OF THE NEW HIGH/NEW LOW INDEX USING PROPRIETARY DATA 25

Richard T. Williams, CFA, CMT

BIRTH OF A CANDLESTICK - USING GENETIC ALGORITHM TO IDENTIFY USEFUL 31CANDLESTICK REVERSAL PATTERNS

Jonathan T. Lin, CMT

MTA JOURNAL • Summer-Fall 2000 3

EDITOR

Henry O. Pruden, Ph.D.Golden Gate University

San Francisco, California

ASSOCIATE EDITORS

David L. Upshaw, CFA, CMT Jeffrey Morton, M.D.Lake Quivira, Kansas PRISM Trading Advisors

Missouri City, Texas

Connie Brown, CMTAerodynamic Investments Inc.

Pawley's Island, South Carolina

John A. Carder, CMTTopline Investment Graphics

Boulder, Colorado

Ann F. Cody, CFAHilliard Lyons

Louisville, Kentucky

Robert B. PeirceCookson, Peirce & Co., Inc.Pittsburgh, Pennsylvania

Charles D. Kirkpatrick, II, CMTKirkpatrick and Company, Inc.

Chatham, Massachusetts

John McGinley, CMTTechnical Trends

Wilton, Connecticut

Cornelius LucaBridge Information Systems

New York, New York

Theodore �E. Loud, CMTTel Advisor Inc. of Virginia

Charlottesville, Virginia

Michael J. Moody, CMTDorsey, Wright & Associates

Pasadena, California

Richard C. Orr, Ph.D.ROME Partners

Marblehead, Massachusetts

Kenneth G. Tower, CMTUST Securities

Princeton, New Jersey

J. Adrian Trezise, M. App. Sc. (II)Consultant to J.P. Morgan

London, England

PRODUCTION COORDINATOR

Barbara I. GompertsFinancial & Investment Graphic Design

Marblehead, Massachusetts

PUBLISHER

Market Technicians Association, Inc.One World Trade Center, Suite 4447

New York, New York 10048

MANUSCRIPT REVIEWERS

THE MTA JOURNAL

SUMMER - FALL 2000 • ISSUE 54

MTA JOURNAL • Summer-Fall 2000 4

A NOTE TO AUTHORS ABOUT STYLE

You want your article to be published. The staff of the MTA Journal wants to help you. Our commongoal can be achieved efficiently if you will observe the following conventions. You'll also earn thethanks of our reviewers, editors, and production people.

1. Send your article on a disk. When you send typewritten work, please use 8-1/2" x 11" paper. DOUBLE-SPACE YOUR TEXT. If you use both sides of the paper, take care that it is heavy enough to avoidreverse-side images. Footnotes and references should appear at the end of your article.

2. Submit two copies of your article.3. All charts should be provided in camera-ready form and be properly labeled for text reference. Try

to avoid using the words "above" or "below," but rather, Chart A, Table II, etc. when referring to yourgraphics.

4. Greek characters should be avoided in the text and in all formulae.5. Include a short (one paragraph) biography. We will place this at the end of your article upon

publication. Your name will appear beneath the title of your article.We will consider any article you send us, regardless of style, but upon acceptance, we will ask you to

make your article conform to the above conventions.For a more detailed style sheet, please contact the MTA Office, One World Trade Center, Suite 4447,

New York, NY 10048.

Mail your manuscripts to:Dr. Henry O. Pruden

Golden Gate University536 Mission Street

San Francisco, CA 94105-2968

The Market Technicians Association Journal is pub-

lished by the Market Technicians Association, Inc.,

(MTA) One World Trade Center, Suite 4447, New

York, NY 10048. Its purpose is to promote the inves-

tigation and analysis of the price and volume activi-

ties of the world's financial markets. The MTA Jour-

nal is distributed to individuals (both academic and

practitioner) and libraries in the United States,

Canada, Europe and several other countries. The

MTA Journal is copyrighted by the Market Technicians

Association and registered with the Library of Con-

gress. All rights are reserved.

ABOUT THE MTA JOURNAL

DESCRIPTION OF THE MTA JOURNAL

MTA JOURNAL • Summer-Fall 2000 5

Members Affiliates■ Invitation to MTA educational meetings ■■ ■■

■ Receive monthly MTA newsletter ■■ ■■

■ Receive MTA Journal ■■ ■■

■ Use of MTA library ■■ ■■

■ Participate on various committees ■■ ■■

■ Colleague of IFTA ■■ ■■

■ Eligible to chair a committee ■■

■ Eligible to vote ■■

Annual subscription to the MTA Journal for nonmembers: $50 (minimum two issues).

Single issue of the MTA Journal (including back issues): $20 each for members and affiliates and

$30 for nonmembers.

✔ ✔

✔ ✔

✔ ✔

✔ ✔

✔ ✔

✔ ✔

✔ ■■

✔ ■■

MARKET TECHNICIANS ASSOCIATION, INC.MEMBER AND AFFILIATE INFORMATION

MEMBER

Member category is available to those "whose professional efforts are spent practicing financial technicalanalysis that is either made available to the investing public or becomes a primary input into an activeportfolio management process or for whom technical analysis is a primary basis of their investment decision-making process." Applicants for Member must be engaged in the above capacity for five years and must besponsored by three MTA Members familiar with the applicant's work.

AFFILIATE

Affiliate status is available to individuals who are interested in technical analysis, but who do not fullymeet the requirements for Member, as stated above; or who currently do not know three MTA members forsponsorship. Privileges are noted below.

DUES

Dues for Members and Affiliates are $200 per year and are payable when joining the MTA and thereafterupon receipt of annual dues notice mailed on July 1. College students may join at a reduced rate of $50 withthe endorsement of a professor.

APPLICATION FEES

Applicants for Member will be charged a onetime, nonrefundable application fee of $25; no fee forAffiliates.

BENEFITS OF THE MTA

MTA JOURNAL • Summer-Fall 2000 6

Director: PresidentPhilip B. Erlanger, CMT

Phil Erlanger Research Co. Inc.978/263-2536

Fax: 978/266-1104E-mail: [email protected]: Vice President

Richard A. DicksonScott & Stringfellow Inc.

804/780-3292Fax: 804/643-9327

E-mail: [email protected]: Secretary

Bruno DiGiorgiLowry's Reports Inc.

561/842-3514Fax: 561/842-1523

E-mail: [email protected]: Treasurer

Andrew BekoffBloomberg Financial Markets

212/495-0558Fax: 212/809-9143

E-mail: [email protected]: Past President

Dodge Dorland, CMTLANDOR Investment Management

212/737-1254Fax: 212/861-0027

E-mail: [email protected]

Bruce M. Kamich, CMTwallstreetREALITY.com, Inc.

732/463-8438Fax: 732/463-2078

e-mail: [email protected]

Charles Kirkpatrick II, CMTKirkpatrick & Co.

508/945-3222Fax: 508/945-8064

E-mail: [email protected]

Philip J. Roth, CMTMorgan Stanley Dean Witter

212/761-6603Fax: 212/761-0471

E-mail: [email protected]

Kenneth G. Tower, CMTUST Securities Corp.

609/734-7747Fax: 609/520-1635

E-mail: [email protected]

2000-2001 BOARD OF DIRECTORS AND MANAGEMENT COMMITTEEOF THE MARKET TECHNICIANS ASSOCIATION, INC.

Management Committee(4 Officers, Past President and Committee Chairs)

AccreditationDavid L. Upshaw, CFA, CMT

913/268-4708Fax: 913/268-7675

E-mail: [email protected]

Neal Genda, CMTCity National Bank

310/888-6416Fax: 310/888-6388

E-mail: [email protected] of Knowledge

John C. Brooks, CMTYelton Fiscal Inc.

770/645-0095Fax: 770/645-0098

E-mail: [email protected]

TBADistance LearningRichard A. Dickson

Scott & Stringfellow Inc.804/780-3292, Fax: 804/643-9327

E-mail: [email protected]

Philip J. Roth, CMTMorgan Stanley Dean Witter

212/761-6603Fax: 212/761-0471

E-mail: [email protected] & StandardsLisa M. Kinne, CMT

Salomon Smith Barney212/816-3796

Fax: 212/816-3590E-mail: [email protected]

FoundationBruce M. Kamich, CMT

732/463-8438Fax: 732/463-2078

e-mail: [email protected] LiaisonMike Epstein

NDB Capital Markets Corp.617/753-9910

Fax: 617/753-9914E-mail: [email protected]

Internship CommitteeJohn Kosar, CMT

Bridge Information Services312/930-1511

Fax: 312-454-3465E-mail: [email protected]

Board of Directors(4 Officers, 4 Directors & Past President)

Journal�Henry (Hank) O. PrudenGolden Gate University

415/442-6583Fax: 415/442-6579

E-mail: [email protected]

Daniel L. Chesler, CTA, CMT561/793-6867

Fax: 561/791-3379E-mail: [email protected]

MembershipLarry Katz

Market Summary & Forecast805/370-1919

Fax 805/777-0044E-mail: [email protected]

NewsletterMichael N. Kahn

Bridge Information Systems212/372-7541

E-mail: [email protected]

Rick BensignorMorgan Stanley Dean Witter

212/761-6148Fax: 212/761-0471

E-mail: [email protected] (NY)Bernard Prebor

MCM MoneyWatch212/908-4323

Fax: 212/908-4331E-mail: [email protected]

RegionsM. Frederick Meissner

404/875-3733E-mail: [email protected]

RulesGeorge A. Schade, Jr., CMT

602/542-9841Fax: 602/542-9827

E-mail: [email protected]

Nina G. CooperPendragon Research, Inc.

815/244-4451Fax: 815/244-4452

E-mail: [email protected]

MTA JOURNAL • Summer-Fall 2000 7

ADDRESS TO MTA 25TH ANNIVERSARY SEMINAR – MAY 2000“LIVING LEGENDS” PANEL

Robert J. Farrell

[Editor's Note: At the 25th Anniversary Seminar in May 2000 inAtlanta, Georgia, Bob Farrell was a member of a panel called The LivingLegends: A tribute to, and remarks by, the eight winners of the MTA An-nual Award. The winners were: Art Merrill, Hiroshi Okamoto, RalphAcampora, Bob Farrell, Don Worden, Dick Arms, Alan Shaw, and JohnBrooks and all were in attendance. The panel was hosted by your editor,Henry Pruden. The following is the text from Bob Farrell's presentation:]

I appreciate being included in this 25th anniversary year forMTA Seminars. I also appreciate being one of the living recipients

of the annualaward. I remem-ber participatingin the first semi-nar as part of whatwas called the 1-2-3 panel for thefirst time. Institu-tional Investormagazine had in-cluded a markettiming category inits annual All-American Re-search Team polland Don Hahn,

Stan Berge and I were those chosen. That was an indication ofgreater institutional recognition of market analysis and timing. Be-fore the great Bear Market of 1972-74, technical analysis was mostlyregarded with suspicion by professionals. Institutional portfoliomanagers generally denigrated its importance even though in ev-ery meeting I had with them, they all carried chart books. The bigbreakthrough came, however, after so many of them got hurt inthe 1972-74 Bear Market. They started asking how could we haveanticipated the collapse of the nifty-fifty and most other stocks. Theythen began to notice that many market analysts and technicianshad issued warnings about the coming debacle. From then on,they started paying more attention. But just as they did not careabout technical timing at the top of the bull market in the late1960s, by the mid-1970s they wanted to hear more about how toavoid the next bear market. In fact, the Financial Analysts Federa-tion asked me to speak at their annual conference in New York in1975 on using technical tools to avoid the next bear market. WhatI chose to speak about was how to use market timing tools to helpidentify where to be invested for the coming long-term bull mar-ket. It seemed clear to me bear markets of the 1974 intensity didnot come along often and set the stage for new long bull runs.They wanted to me to talk about the past instead of the future.

When I chose to be a market analyst instead of a security analystin the early 1960s, I soon realized that what I needed as a goal wasprofessional recognition. I also realized that it could only comefrom institutions as their dominance was growing in the market.But I knew most portfolio manager's eyes glazed over when I spokeof technical indicators or they were outright hostile to technicians.

So, I came up with a plan. I incorporated more long-term trendand cycle work in my analysis so portfolio managers could look atmy analysis as something beyond short-term trading. I also real-ized I could get their attention by giving them fundamental rea-sons for the conclusions I had arrived at using market indicators.Then I figured out that if I wanted to have impact, effective com-munication was everything. Of course, I had to be right a goodpercentage of the time and make sense, but the ability to write andspeak in a common sense style without arrogance was crucial togetting their attention.

I also realized, as I am sure many of you have figured out, thatmost professional money managers have strong views that you arenot going to change in a single meeting or with a single report.When I got a conviction about a sector or a market change, I knewit had to offer more than a conclusion or opinion. We had to sup-ply information and present it logically to prove a point. Today,there is more information available more quickly than ever beforebut, interestingly, results of most managers are still worse than apassive index. Most want and need to be told which information isimportant. One of the things I capitalized on was the idea that Ihad information not available elsewhere, i.e., Merrill Lynch inter-nal transaction figures. We, in fact, applied the term sentimentanalysis to our figures back in the mid 1960s and used them toadvantage as contrary indicators. Even though they were only onetool, they gave us an edge in supplying unique information to cli-ents. Today, of course, many firms have such data and it is lessunique.

I don't believe in us versus them when it comes to technical analysisand fundamental analysis. The goal is to come up with profitableideas, not whose tools are best. Nevertheless, I had one chance toturn the tables on fundamental security analysts which I enjoyedimmensely. When I went to Columbia Business School in 1955 toget a Master's in Investment Finance, I had both Ben Graham andDavid Dodd as professors. As you know, they were the originalvalue investors who wrote the bible of fundamental analysis called,"Security Analysis." Published in 1934, there was a 50th anniver-sary seminar in 1984 at Columbia to which I was invited as a speaker.When the Dean first invited me, I asked him incredulously, "Doyou know what I do?" Even though he understood that most tech-nical analysis was poles apart from the fundamental value trainingof Graham & Dodd, he said, "Just tell us how they influenced you."I was the last speaker on the all-day program which included War-ren Buffet, Mario Gabelli and others, and I felt very intimidated.But I decided to try a different approach and gave a speech en-titled, Why Ben Graham Was A Closet Technician. Surprisingly, it waswell received. I cited many references he made to the characteris-tics of a market top and his references to measures of speculation.

The fact that I was rated number one in 16 of the 17 years Icompeted in the Institutional Investor All-Star Research poll as ChiefMarket Analyst was not because I was more right than anybody else.I did have a good platform at Merrill Lynch but not everybody atMerrill was ranked #1 either. I think it was my ability to communi-cate what was happening or changing in the markets with an his-

MTA JOURNAL • Summer-Fall 2000 8

torical perspective in a form that mostly fundamental clients couldunderstand. I never talked down to them and always had a sectoropinion that I emphasized where my conviction level was high. Ithought they usually took away something useful from my presen-tation even if they disagreed with some of the general conclusions.

As a result of the integration of fundamental reasoning to backup technical conclusions, I became less regarded as a technicianand more as a market strategist who used historical precedent andtechnical tools. I have never liked the term technician because it istoo limiting and am very much in favor of finding another way todescribe what we do. We study so many things such as price trends,momentum, money flows, cycles and waves, investor behavior andsentiment, supply-demand changes, volume relationships, insideractivity, monetary policy and historical precedent. We have a broadfield of study that has grown more inclusive with time and the com-puter age. It is just not adequately summed up in the term techni-cian. At Merrill Lynch, we use the broader term of market analystto avoid the limiting label of technician. Despite all the attemptsat upgrading and professionalizing our craft by our association, westill have the press calling technicians sorcerers, elves, entrail read-ers and other denigrating terms. We have come a long way, but wehave not shaken the negative image of the past that goes with theterm technician, particularly with the press. You may disagree oreven not care, but experience tells me to emphasize our broaderrange of skills.

I am impressed with the advanced techniques being used to ana-lyze the market data and the progress made in working with theFinancial Analysts Federation and the academic community. Thereis much more substance in our craft as a result of your efforts. Nev-ertheless, the world at large needs to be educated. Investor's Busi-ness Daily does an excellent job of explaining how to use technicaltools and integrate technical and fundamental information on anongoing, real-time basis. We should use this model as an organiza-tion and have our members publish regular educational articles inthe mainstream press or on a net website. We have created excel-lent professional credentials over the years. Now we need to mar-ket our profession – if not as technicians, perhaps as market behav-ioral strategists or market timing and behavioral strategists. Youdeserve recognition for your broader range of skills as well as yourability to provide profitable market and stock conclusions.

Thank you for inviting me.

ROBERT J. FARRELL

Bob Farrell is Senior Investment Advisor of Merrill Lynch,Pierce, Fenner & Smith, Inc., the nation’s largest securitiesfirm, and one of Wall Street’s most highly respected stock mar-ket analysts.

He had been named Number One in the Market Timingcategory of Institutional Investor’s annual “All-American Re-search Team” poll for 16 years prior to assuming his new role.

Bob has spent his entire business career with Merrill Lynch.As Manager of Market Analysis, he pioneered the use of senti-ment figures using Merrill Lynch internal data. His “WeeklyMarket Commentary,” published since 1970, was followed bythousands of professional money managers in this country andabroad.

In his current role as Senior Investment Advisor, he hasbeen writing quarterly on longer-term theme changes in themarket. He will continue advising clients on market strategiesimplementing themes.

Bob was a charter member of the Market Technicians Asso-ciation and its first president from 1972-1974. Bob was alsothe recipient of the MTA Annual Award in 1988. In 1993 hewas inducted into the Wall Street Week Hall of Fame.

He was graduated from Manhattan College in 1954 with aBBA in Economics & Finance, and received an MS in invest-ment finance from the Columbia Graduate School of Busi-ness in 1955.

MTA JOURNAL • Summer-Fall 2000 9

PurposeThis study was designed to evaluate the theoretical returns for a

simple non-directional option strategy initiated after a sudden andsignificant volatility implosion of an underlying stock.

Methods and MaterialsThe 30 Dow Jones Industrial stocks from November 1, 1993,

through May 30, 1998, were chosen for this study. Delta neutral/gamma positive straddle positions were initiated on the openingprice of the stock after the near-term historical volatility of the stockhad significantly imploded relative to its longer-term historical vola-tility. Any signals generated in the same stock before the 6- weektermination date of a prior trade were ignored. On the date ofcalculation, the options prices were determined with the actualimplied volatility using the Black-Scholes model, assuming moder-ate slippage. All trades were equally weighted. The value of theoptions’ positions were calculated based on the closing stock priceat the 2-, 4-, and 6- week periods respectively. Two trading systemswere evaluated. In the first system (time-based system), time wasthe sole determinant used to determine when the option positionswould be closed out. In the second trading system (money man-agement system), simple money management rules were added toreduce draw-downs and to “lock-in” profits in profitable trades.Given the wide variability of brokerage fees, the results are pre-sented without commission costs deducted.

ResultsA total of 280 trades were generated between November 1, 1993,

and May 30, 1998. For the time-based trading system (trading system1), the 2-week, 4-week, and 6-week cumulative return was -191.9%,+334.7%, and -84.3% and the average return per trade was -0.69%,+1.20%, and -0.30% respectively. For the money managementtrading system (trading system 2), the 4-week and 6-week cumulativereturns were +993.4%, and +1188.6% and the average return pertrade was +3.55% and +4.25% respectively. The use of a simplemoney management system significantly reduced the draw-downsof the system.

ConclusionsThe simple time-based volatility trading strategy produced a

positive return holding the options for four weeks. This simplestraddle-based options strategy had significant draw-downs thatpreclude it as a viable trading strategy without modifications. Theaddition of some very simple money management rules significantlyimproved the returns while simultaneously decreasing the draw-downs. This volatility-based, market-neutral, delta-neutral (gammapositive) trading strategy yielded a very substantial positive returnacross a large number of large-cap stocks and across a broad fiveyear period. These results demonstrate the potential positive re-turns that can be obtained from a market-neutral/delta-neutralstrategy. The benefit of a market-neutral strategy as demonstratedhere is of significant importance to institutional portfolio manag-ers in search of non-correlated asset classes.

INTRODUCTION

For options-based trading, the price action of any freely-tradedasset (e.g., stocks, futures, index futures, etc.) can be grouped intothree generic categories (however defined by the trader): (a) bull-ish price action; (b) bearish price action; (c) congestion/tradingrange price action. Specific options-based strategies can be imple-mented which result in profits if any two out of the three outcomesunfold. For example, the purchase of both call and put options onthe same underlying asset for the same strike price and same expi-ration date is termed a “straddle” position (e.g., buying XYZ $100strike March 1999 call and put options = XYZ $100 March 1999straddle). This straddle position can be profitable if either (a) or(b) quickly occur with significant magnitude (i.e., price volatility)prior to option expiration. In this sense, a straddle trade is non-directional since it can profit in both bull and bear moves.

Price volatility can be described by several common technicalindicators including ADX, average-true-range, standard deviation,and statistical volatility (also called historical volatility). Volatilityhas been observed to be “mean-reverting.” Periods of abnormallyhigh or low short-term price volatility are followed by price volatil-ity that is closer to the long-term price volatility of the underlyingasset.(1,3) A short-term drop in price volatility (volatility implosion)can be reliably expected to be followed by a sudden volatility in-crease (volatility explosion). Connors, et. al. have shown that mul-tiple days of short-term volatility implosion is a predictor of a strongprice move.(1,2)

The volatility implosion does not predict the direction of theimpending price move, but only that there is a high probabilitythat the underlying asset is going to move away from its currentprice and by a significant amount. In addition, the volatility implo-sion does not predict when (how quickly) the explosion price movewill develop. We can predict which direction the price of the stock,commodity, or market is not going to move with a high degree ofprobability. It most likely will not move side-ways indefinitely. Know-ing this, one can devise a trading strategy that is able to profit, or atleast not lose money, if the stock moves quickly higher or lowersuch as the straddle strategy earlier described above.

In the option straddle strategy described above (e.g., XYZ $100March 1999 straddle), as the price of the underlying asset movesaway from the option's strike price in either direction, the optionthat is gaining in value will increase at a greater rate than the op-posing option that is losing value. The position is said to be gammapositive in both directions. The straddle will lose if the price of theasset stays at or near the strike prices of the options, i.e. the stockmoves side-ways. The straddle position deteriorates because ofcontinued decrease in the volatility of the underlying asset, plusthe time-decay value of the option as it approaches expiration.

This study was designed to explore the potential investment re-turns that could be obtained using the basic option straddle strat-egy. At PRISM Trading Advisors, Inc., this strategy has been suc-cessfully implemented to generate superior returns at lower riskthan traditional investment portfolio benchmarks.

EXPLOITING VOLATILITY TO ACHIEVE A TRADING EDGE:Market-Neutral/Delta-Neutral Trading Using

the PRISM Trading Systems

Jeff Morton, MD, CMT

1

MTA JOURNAL • Summer-Fall 2000 10

METHODS AND MATERIALS

System 1 (Time-Based Strategy)To test the robustness of this trading strategy, the Dow 30 Indus-

trial stocks from November, 1, 1993, through May 31, 1998, werechosen for this study. They were chosen because they are a well-known group of stocks that have been designed to represent themarket at large. Volatility is defined by the price statistical volatil-ity formula: s.v. = s.d.{log(c/c[1]),n} * square-root (365). Statisti-cal (or historical) price volatility can be descriptively defined asthe standard deviation of day-to-day price change using a log-nor-mal distribution and stated as an annualized percentage. Detailedinformation on statistical volatility is available from the refer-ences.(1,2,3)

■ Rule 1: 6-day s.v. is 50% or less than the 90-day s.v.■ Rule 2: 10-day s.v. is 50% or less than the 90-day s.v.■ Rule 3: Both rule #1 and rule #2 must be satisfied to

initiate the trade. Thus in this study, a volatility implosion was defined as when

the 6-day and 10-day historical volatilities were 50% or less thanthe 90-day historical volatility. When this condition is met, a signalto initiate a straddle position was taken the following trading day.The Black-Scholes model was used to calculate the options pricesthat were used to establish the straddle positions. The openingprice of the stock, the actual implied volatility, and the yield of the90-day U.S. Treasury Bill were used to calculate the price of theoptions. The professional software package OpVue 5 version 1.12(OpVue Systems International) was used to calculate the prices ofthe options assuming a moderate amount of slippage. For the pur-poses of this analysis, it was assumed that each trade was equallyweighted and that an equal dollar amount was invested into eachtrade. Based on the closing stock price, the value of the optionstraddle positions were then calculated using the same methoddescribed above after 2 weeks, 4 weeks, and 6 weeks respectively.Any trading signals generated in a stock with a current open op-tion straddle position before the end of the 6-week open trade pe-riod were ignored. To minimize the effect of time decay and vola-tility, options with greater than 75 days to expiration were used toestablish the straddle positions. The positions were closed out atthe end of the 6-week time period with more than 30 days left untilexpiration. To further minimize the effect of volatility, options werepurchased “at or near the money.” Given the current large vari-ability of brokerage fees, the results were calculated without de-ducting commission costs.

System 2 (Money Management Strategy)A second trading strategy was explored. It was identical to the

first trading strategy except a set of simple money managementrules were added. The rules were designed to 1) cut losses short,2) allow profits to run, and 3) lock in profits.■ Rule #1: A position was closed immediately if a 10% loss oc-

curred.■ Rule #2: If a 5% profit (or greater) was generated, then a trail-

ing stop of one-half (50%) of the maximum open profit achievedby the position was placed and the position closed if the 50%trailing stop was violated.

■ Rule #3: If neither rule #1 or #2 was violated then the positionwas closed out after either 4 weeks or 6 weeks.

RESULTS

System 1 (Time-Based Strategy)A total of 280 trades were generated between November 1, 1993

and May 30, 1998. Numerous parameters of the 280 trades wereanalyzed. The results are summarized in Table 1. The 2-week, 4-week, and 6-week cumulative returns were +191.9%, +334.7%, and-84.3% respectively and are shown in Figure 1. The return of theDJIA over the same time period was +241.8% (3,680.59 to 8,899.95).The maximum draw-downs for the 2-week, 4-week, and 6-week se-ries were, -424.3%, (November 12, 1993 - April 28, 1995), -450.8%(November 8, 1993 - May 17, 1995), and -763.3% (December 6,1993 - May 19, 1995). The maximum draw-ups for the 2-week, 4-week, and 6-week series were, +373.9% (April 7, 1995 - July 1, 1997),+933.2% (April 18, 1995 - November 11, 1997), and +948.2% (April7, 1995 - November 17, 1997).

System 2 (Money Management Strategy)A total of 280 trades were generated between November 1, 1993

and May 30, 1998. Numerous parameters of the 280 trades wereanalyzed. The results are summarized in Table 2. The 4-week, and6-week cumulative returns were +993.4%, and +1188.6% respec-tively, and are shown in Figure 2. The return of the DJIA over thesame time period was +241.8% (3,680.59 to 8,899.95). The maxi-mum draw-downs for the 4-week and 6-week series were -188.1%,(August 5, 1994 - February 23, 1995) and -246.2% (August 5, 1994- February 23, 1995). The maximum draw-ups for the 4-week and6-week series were +641.4% (September 20, 1996 - October 20, 1997)and +704.1% (September 20, 1996 - October 20, 1997).

DISCUSSION

It has been observed that short-term volatility will have a ten-dency to revert back to its longer-term mean.(1,3) Connors et.al.(1)

have published the Connors-Hayward Historical Volatility Systemand showed that when the ratio of the 10-day versus the 100-dayhistorical volatilities was 0.5 or less, there was a tendency for strongstock price moves to follow.

In this study, PRISM Trading Advisors, Inc., have confirmed thephenomenon of volatility mean reversion by presenting the firstlarge scale option-based analysis while maintaining a strict market-neutral/delta-neutral (gamma positive) trading program. We haveshown that a significant price move occurs 75% of the time follow-ing a short-term volatility implosion (as defined in the Methodsand Materials section).

For this analysis we chose a relatively straightforward strategy:to purchase a straddle. A straddle is the proper balance of put andcall options that produce a trade with no directional bias. A straddleis said to be “delta neutral” and will generate the same profit whetherthe underlying asset’s price moves higher or lower. As the assetprice moves away from its initial price one option will increase invalue while the other opposing option will decrease in value. Aprofit is generated because the option that is increasing in valuewill increase in value at a faster rate than the opposing option isdecreasing in value. The straddle is said to be “gamma positive” inboth directions.

This option strategy has a defined maximum risk of the tradethat is known at the initiation of the trade. This maximum risk ofloss is limited to the initial purchase costs of the straddle (premiumcosts of both put and call options). There is no margin call withthis straddle strategy. There is an additional way that this strategycan profit. Since the options are purchased at the time there has

MTA JOURNAL • Summer-Fall 2000 11

(Over)

been an acute rapid decrease in volatility, one should theoreticallybe purchasing “undervalued” options. As the price of the assetsubsequently experiences a sharp price move, there will be an asso-ciated increase in volatility which will increase the value of all theoptions that make-up the straddle position. The side of the straddlewhich is increasing in value will increase at an even faster rate, whilethe opposite side of the straddle which is decreasing in value willdecrease in value at a slower rate. So as to not further complicatethe analysis, the exit strategy for the first system (time-based strat-egy) for this study was even more basic using a time-stop exit crite-ria.

Prior to the study, it was our impression that a 4-week time pe-riod would be the most optimal of the three. This is what was seen.The 4-week exit produced a positive return over the study period(334.7%). However, the use of a 2-week time-stop was frequentlynot sufficient time to allow for the anticipated price move. Notethat in Figure 1, the 2-week maximum open-profit draw-up was sig-nificantly less than the draw-ups for both the 4-week and 6-weektime-stops (373.9% vs. 933.2% and 948.2% respectively). The 6-weeks strategy was too long, allowing for substantially greater maxi-mum draw-down secondary to the adverse effects of time decay,volatility, and price regression back toward the stock’s initial start-ing price that eroded the value to the straddle position when com-pared to the 2-week and 4-week strategies. All other aspects of thetrades of the three exit strategies were similar. There were no sig-nificant differences in the percentage of wining/losing trades ornumber of consecutive winning or losing trades.

A second system using a simple set of money management ruleswas tested (money management system). These rules were designedto close-out non-performing trades early before they could turninto large losses and kept performing positions open as long asthey continued to generate profits. These goals were accomplishedby closing out any position if its value decreased to 90% of its ini-tial value (10% loss). A position with open profits had a 50% trail-ing stop of the maximum open profit achieved by the position atanytime open profits exceeded 5%. If neither of these two condi-tions occurred, the position was closed out at the end of six weeks.

As predicted, the 6-week money management strategy producedboth a greater total return (+993.4% versus 1,188.6%) and a slightlygreater maximum draw-down than the 4-week money managementstrategy. By closing positions when a loss of 10% had occurred, wewere able to significantly decrease the amount of losses incurred.This is evidenced by the maximum draw-down for the 6-weekpositions being decreased significantly from (-763.3%) to (-246.2%) employing no money management versus implementingthe above money management rules. Also the total returns weremarkedly improved with the total return increasing from (-84.3%)to (+1188.6%).

While the first trading system (time-based strategy) study dem-onstrated that this trading strategy with a 4-week time-stop exit pro-duced a positive return, it is not sufficient as a stand-alone systemfor real-time trading. It does, however, indicate that this strategycan be used as the foundation to design a viable trading systemthat can capture the majority of the gains while simultaneously elimi-nating the majority of the loses. There are almost an infinite num-ber of possibilities one could explore to achieve this goal.

The second method, and the one explored in this paper, wasthe application of a simple set of money management rules. Asdiscussed above, this dramatically improved the overall returns whilesimultaneously decreasing the draw-downs experienced in the firststrategy (time-based strategy). Other possibilities include the ad-dition of a second entry filter such as a momentum indicator like

the RSI, ROC or MACD indicator. One could design a more so-phisticated exit strategy such as exiting the position if the stockprice exceeds a predetermined price objective as defined by pricechannels, parabolic functions, etc. An additional possibility wouldbe to re-establish a nondirectional option’s position at a predeter-mined price objective, thereby “locking in” all the profits gener-ated up to that point. The myriad of options-based strategies avail-able to adjust back to a delta neutral position based on technicalindicators and predetermined price objectives are beyond the scopeof this paper.

Although both systems had positive expectations based on 280trades, there are several limitations of the study design. Althoughmoderate slippage was used in all the calculations, the robustnessof this study might have been improved if access to real-time stockoption bid-ask prices were available for all of the trades investi-gated. Unfortunately, such a large, detailed database is not readilyavailable. Given that the real-time bid-ask prices were not avail-able, the use of the Black-Scholes formula with the known histori-cal inputs (stock price, implied volatility, 90-day T-Bill yield) is anacceptable alternative thereby minimizing any pricing differencesbetween the actual and theoretical option prices systematicallythroughout the time period used in the study.

The current study revealed that a simple straddle options-basedstrategy designed to exploit a sudden implosion of a stock’s volatil-ity with time as the only existing criteria produced draw-downs thatpreclude it as a viable trading strategy in its own right. However,this simple strategy had a positive expectation of generating supe-rior returns, and therefore can be used as the basis to develop trad-ing strategies capable of producing superior returns without theneed to correctly predict the direction of a given stock, commod-ity, or market being traded. The addition of some simple moneymanagement rules dramatically improved the overall returns whilesimultaneously decreasing the excessive draw-downs that plaguedthe original trading strategy, thereby transforming it into a appli-cable trading system for every day use. This volatility-based, delta-neutral strategy also is independent of market direction. A mar-ket-neutral strategy and portfolio may be considered as a separateasset class by portfolio managers in the efficient allocation of theirclients’ investment portfolios to boost returns while simultaneouslydecreasing their clients risk exposure.

In conclusion, this is the first large-scale trading research studyto be shared with the trading public that clearly demonstrated howthe phenomenon of price volatility mean-reversion can be exploitedby using an options-based delta-neutral approach. Price, time andvolatility factors using options-based strategies to further maximizepositive expectancy represent active areas of real-time trading re-search at PRISM Trading Advisors, Inc. These results will be thesubject of future articles.

REFERENCES

1. Connors, L. A., and Hayward, B.E., Investment Secrets of a HedgeFund Manager, Probus Publishing, 1995.

2. Connors, L. A: Professional Traders Journal, Oceanview FinancialResearch, Malibu, CA. March 1996, Volume 1, Issue 1.

3. Natenberg, S., Option Volatility and Pricing. Advanced Trading Strat-egies and Techniques, McGraw Hill, 1994.

MTA JOURNAL • Summer-Fall 2000 12

TABLE 1

System 1 (Time-Based System)

2 Week 4 Week 6 Week

Total Return -191.9% +334.7% -84.3%

Average Return per Trade -0.69% +1.20% -0.30%

Maximum Draw-Up +373.9% +933.2% +948.2%

Maximum Draw-Down -424.3% -450.8% -763.3%

Total # Winning Trades 91 106 100

Total # Break Even Trades 4 0 3

Total # Losing Trades 185 174 177

Max. # of Consecutive Wins 7 5 5

Max. # of Consecutive Loses 14 9 13

Greatest Gain in One Trade +87.8% +132.1% +109.0%

Greatest Loss in One Trade -48.0% -51.8% -59.0%

Figure 1

System 1 (Time-Based System)

TABLE 2

System 2 (Money Management System)

4 Week 6 Week

Total Return +993.4% +1188.6%

Average Return per Trade +3.55% +4.25%

Maximum Draw-up +641.4% +704.1%

Maximum Draw-Down -188.1% -246.2%

Total # Winning Trades 120 117

Total # Break Even Trades 0 2

Total # Losing Trades 160 161

Max. # Consecutive Wins 6 7

Max. # Consecutive Loses 8 9

Greatest Gain in One Trade +132.1% +109.0%

Greatest Loss in One Trade -10.0% -10.0%

Figure 2

System 2 (Money Management System)

JEFF MORTON, MD, CMT

Jeff Morton is Chief Technical Analyst & Executive VicePresident at PRISM Trading Advisors (Electronic SignatureOnly). He received his bachelor’s degree from Stanford Uni-versity Medical School in 1981 and his Medical Degree fromthe Yale School of Medicine in 1985. He began his career as atechnical analysts in 1992 as a consultant for Schea CapitalManagement. In 1995, he helped start PRISM Trading Advi-sors, Inc. a Houston, Texas based proprietary trading firm.His major areas of expertise include options strategies, volatil-ity trading, and trading strategies based on ADX, ATR, point& figure charting. His other duties at PRISM Trading Advi-sors, Inc. include compliance/due diligence, trader education,and journal publications. Dr. Morton is very active in theMTA. He currently is serving as an associate editor of the MTAJournal, and on the accreditation committee.

MTA JOURNAL • Summer-Fall 2000 13

PREFACE

In their quest to outperform the Index, equity fund managersmust solve a four-piece puzzle: which stocks should they buy, whenshould they buy them, when should they sell them and how much capitalshould they allocate to each stock. The performance of different fundmanagers varies greatly. Some are able to outperform the Index,and others cannot. This paper investigates the question of whethertechnical analysis in its most simplistic form along with simplemoney management can be used to outperform the Index.

THE FOUR-WEEK RULE

Most market technicians will agree that the simplest technicalmarket analysis rule is the Four-Week Rule. The Four-Week Rule(4WR) was originally developed for application to futures marketsby Richard Donchian, and can be expressed as follows:

Cover shorts and go long when the price exceeds the highs of thefour preceding full calendar weeks and conversely liquidate longsand go short when the price falls below the lows of the four preced-ing full calendar weeks.

The rationale behind this rule is that the four-week or 20-daytrading cycle is a dominant cycle that influences all markets.

For the purpose of further discussion, let’s modify the Four-Week Rule system as follows:

Buy if the price exceeds the highs of the four preceding full calendarweeks and liquidate open positions when the price falls below thelows of the four preceding full calendar weeks.

With this modification, the 4WR – (no shorts) system can beeasily applied by many equity fund managers because very few ofthem can go short.

Let us formally define our modified mechanical system:

System Code: NS-20BS-EQ (No Shorts, 20 days for Buy andSell Rules, Equally Allocate Capital)

1. Money management rule - Equal allocation ruleUse $100,000 of capital into one hundred S&P 100 Index stocks,allocating an equal amount of money into each stock ($1000).

2. Technical analysis rule - BuyBuy a stock if its closing price is higher than the high of last 20trading days.

3. Technical analysis rule - SellSell a stock if its close price is lower than the low of last 20 trad-ing days

4. Money management rule - Redistribute profits equallyIf the profit from the sale of a stock is greater than the initialallocation of capital to this stock, then that profit is equally dis-tributed among all stocks which are in a potential Buy position.

5. Money management rule - Earn interest on cashAll cash on hand earns fix rate interest @ 5% per annum.

6. Money management rule - Transaction costsA fixed transaction cost of $50 is applied to each transaction(this cost represents a fair average of commissions and slippage).

A custom computer software was designed and created to testthis system in the time frame from January 1, 1984 to January 1,1989. During this time frame the following performance statisticswere calculated for NS-20BS-EQ system and were compared to theperformance statistics of the Index (S&P 100) with a “Buy-and-HoldStrategy.”

Performance Statistics MeasuredThe following performance statistics were measured for each

case (definitions are included in Appendix 1):■ Average Annual Compounded Return (R)■ Sharpe Ratio (SR)■ Return Retracement Ratio (RRR)■ Maximum Loss (ML)

ResultsDays used for

System� Time Frame� Money Allocation� Buy and Sell rules�

NS-20BS-EQ� 01/01/1984 - 01/01/1989 Equal 20�

System� IndexAverage Annual Compounded Return 7.58% 9.00%��

Sharpe Ratio� 4.15% 3.85%��

Return Retracement Ratio� 0.45 0.34��

Maximum Loss� 0.36� 0.58��

It is clear that the above system is performing less than the “Buy-and-Hold Strategy” of S&P 100 Index.

There are several choices to improve performance of the sys-tem by modifying system parameters. The most natural change isto search for better performance by modifying the number daysused for the Buy and Sell rules. The performance of the NS-xBS-EQ system where x is the number of days for Buy and Sell rules wastested for x between 10 days and 90 days. Results of the test areprovided in the Appendix 2.1.

Testing proved that the best performing system was the one with50 days used for the Buy and Sell rules.

ResultsDays used for

System� Time Frame� Money Allocation� Buy and Sell rules�

NS-50BS-EQ 01/01/1984 - 01/01/1989 Equal� 50��

System IndexAverage Annual Compounded Return� 7.70%� 9.00%��

Sharpe Ratio 4.49% 3.85%��

Return Retracement Ratio 0.42 0.34��

Maximum Loss� 0.40� 0.58��

Still the performance of the above system is not very impres-sive, so let’s consider further research. Let’s modify Rule 1 fromthe system definition and replace it by following rule:1A. Money management rule - Proportional allocation rule

Use $100,000 of capital into one hundred S&P 100 Index stocks,allocating money into each stock according to its percentageparticipation in the index at the starting date of the testing pe-riod (January 1, 1984).

MECHANICAL TRADING SYSTEM VS. THE S&P 100 INDEXCan a Mechanical Trading System Based on the

Four-Week Rule Beat the S&P 100 Index?

Art Ruszkowski, CMT, M.Sc.

2

MTA JOURNAL • Summer-Fall 2000 14

So we consider the new system:

System Code: NS-xBS-P (No Shorts, x Days for Buy and SellRules, Proportionally Allocate Capital)

The new system consists of Rule 1A and Rules 2-6.The performance of the NS-xBS-P system where x is the num-

ber of days for Buy and Sell rules was tested for x between 10 daysand 90 days. Results of the test are provided in the Appendix 2.2.

Testing proved that the best-performing system was one with 50days used for Buy and Sell rules.

ResultsDays used for

System� Time Frame� Money Allocation� Buy and Sell rules�

NS-50BS-P� 01/01/1984 - 01/01/1989 Proportional� 50��

System� IndexAverage Annual Compounded Return� 10.57%� 9.00%��

Sharpe Ratio� 4.44% 3.85%��

Return Retracement Ratio� 0.51 0.34��

Maximum Loss� 0.48 0.58��

The last system outperforms the S&P100 “Buy-and-Hold Strat-egy” but let’s consider further research. So far modifications werelimited to systems with different number of days for the Buy andSell rule and for using different initial allocations of the capital –equal and proportional. Let’s consider the following hybrid of theoriginal NS-20BS-EQ system – by replacing Rule 3 with followingnew rule:3B. Money management Stop Loss Rule - Sell losing positions

Sell a stock if it is losing more than y% of its buy price, where yis a system parameter

Let’s name this system:

System Code: NS-xB-P-Sy (No Shorts, x Days for Buy Rule,Proportionally Allocate Capital, – Sell When Drops y%)

Only systems with proportionally allocated capital are analyzeddue to the fact that they perform better than equally allocated onesin a considered period of time. The performance of the NS-xB-P-Sy system where x is the number of days for Buy rule was tested forx between 10 days and 90 days and for y between 10% and 70%.Results of the test are provided in the Appendix 3.

Testing of systems NS-xB-P-Sy proved that the best performingsystem was one with 50 days used for Buy rule and 25% moneymanagement stop loss rule.

ResultsMoney Days used % Loss used

System� Time Frame� Allocation� for Buy in Rule 3B

NS-50B-P-S25� 01/01/1984 - 01/01/1989 Proportional� 50� 25%��

System� IndexAverage Annual Compounded Return� 14.78%� 9.00%��

Sharpe Ratio� 4.48%� 3.85%��

Return Retracement Ratio� 0.52� 0.34��

Maximum Loss� 0.64� 0.58��

The last system which is the result of several cycles of modifica-tions to the initial 4WR outperforms the S&P100 “Buy-and-HoldStrategy” by a good margin. To find out how time-stable the abovesystem was, a blind test was conducted.

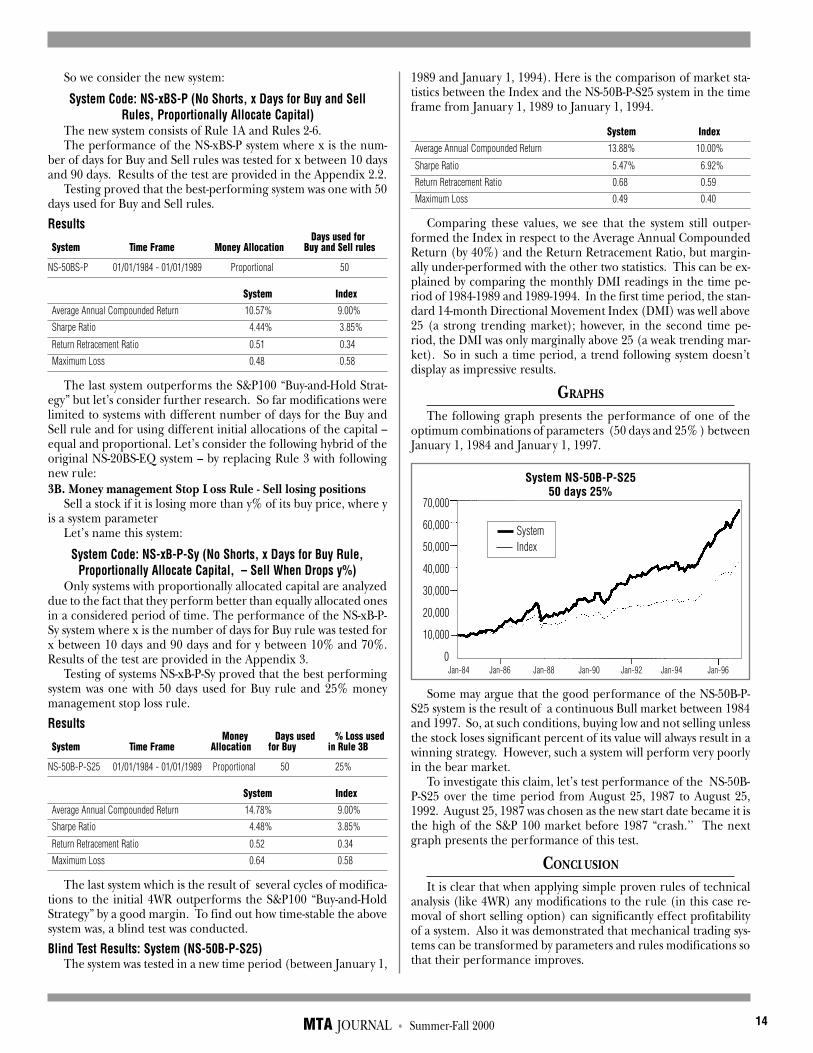

Blind Test Results: System (NS-50B-P-S25)The system was tested in a new time period (between January 1,

1989 and January 1, 1994). Here is the comparison of market sta-tistics between the Index and the NS-50B-P-S25 system in the timeframe from January 1, 1989 to January 1, 1994.

System� IndexAverage Annual Compounded Return� 13.88%� 10.00%��

Sharpe Ratio� 5.47%� 6.92%��

Return Retracement Ratio� 0.68� 0.59��

Maximum Loss� 0.49� 0.40��

Comparing these values, we see that the system still outper-formed the Index in respect to the Average Annual CompoundedReturn (by 40%) and the Return Retracement Ratio, but margin-ally under-performed with the other two statistics. This can be ex-plained by comparing the monthly DMI readings in the time pe-riod of 1984-1989 and 1989-1994. In the first time period, the stan-dard 14-month Directional Movement Index (DMI) was well above25 (a strong trending market); however, in the second time pe-riod, the DMI was only marginally above 25 (a weak trending mar-ket). So in such a time period, a trend following system doesn’tdisplay as impressive results.

GRAPHS

The following graph presents the performance of one of theoptimum combinations of parameters (50 days and 25% ) betweenJanuary 1, 1984 and January 1, 1997.

Some may argue that the good performance of the NS-50B-P-S25 system is the result of a continuous Bull market between 1984and 1997. So, at such conditions, buying low and not selling unlessthe stock loses significant percent of its value will always result in awinning strategy. However, such a system will perform very poorlyin the bear market.

To investigate this claim, let’s test performance of the NS-50B-P-S25 over the time period from August 25, 1987 to August 25,1992. August 25, 1987 was chosen as the new start date became it isthe high of the S&P 100 market before 1987 “crash.’’ The nextgraph presents the performance of this test.

CONCLUSION

It is clear that when applying simple proven rules of technicalanalysis (like 4WR) any modifications to the rule (in this case re-moval of short selling option) can significantly effect profitabilityof a system. Also it was demonstrated that mechanical trading sys-tems can be transformed by parameters and rules modifications sothat their performance improves.

System NS-50B-P-S2550 days 25%

70,000

60,000

50,000

40,000

30,000

20,000

10,000

0

SystemIndex

Jan-84 Jan-86 Jan-88 Jan-90 Jan-92 Jan-94 Jan-96

MTA JOURNAL • Summer-Fall 2000 15

One very interesting observation worth further study is the factthat the large difference in performance was affected by the amountof money allocated into each stock. This is due to fact that the S&P100 Index is a capitalization-weighted index of 100 stocks. Thecomponent stocks are weighted according to the total market valueof their outstanding shares. The impact of the component’s pricechange is proportional to the stock’s total market value, which isthe share price times the number of shares outstanding. In otherwords, the S&P 100 Index can be considered as a relative-strengthbased index. An index-based capital allocation system (NS-50B-P-S25) performs best and gives an objective measure of the validityof its trading rules as well as its money management rules when itsperformance is compared to the performance of the Index. Sys-tems with sound trading and money management rules, as well ascapital-allocation based on relative strength should, in general,outperform both the index and equally-allocated systems.

It is worth observing that the proportionally-allocated systemoutperformed the equally-allocated system and the Index duringthe tested time periods regardless whether during those periodsthe Large Cap outperformed the Small Cap or vice versa.

BIBLIOGRAPHY

i John. J. Murphy, Technical Analysis of the Futures Markets, NewYork Institute of Finance,1986.

ii Jack D. Schwager, Schwager on Futures - Technical Analysis, JohnWiley & Sons, Inc., 1996.

iii Carla Cavaletti, Trading Style Wars, Futures, July 1997.�

APPENDIX 1

Glossary of Terms:Mechanical Trading System: A set of rules that can be used to gen-erate trade signals and trading performed according to the rulesof mechanical system. Primary benefits of mechanical trading sys-tems are elimination of emotions from trading, and consistency ofapproach and risk management. Mechanical trading systems canbe classified as Trend-Following (initiating a position with thetrend), and Counter-Trend (initiating a position in the oppositedirection to the trend). Trend following systems can be dividedinto fast and slow. Fast – a more sensitive system responds quicklyto signs of trend reversal and will tend to maximize profit on validsignals, but also generate far more false signals. A good trend fol-lowing system should not be too fast or too slow. ii �

Trading according to signals generated by mechanical tradingsystem is called systematic trading which is opposite to discretion-ary trading. Discretionary traders claim that emotions, which areexcluded from systems trading, offer an edge. On the contrary,

systematic traders favor backtesting, analyzing patterns and elimi-nating emotions. According to Barclay Trading Group Ltd., overthe last ten years systematic traders have yielded higher annual re-turns than discretionary traders six times. iii �Optimization of the trading system: The process of finding thebest performing parameter set for a given system. The underlyingpremise of optimization is that the parameter set must work notonly in its initial time frame but any time frame. Almost any me-chanical system can be optimized in a way that it will show positiveresults in any given period of time. ii

Parameter: A value that can be freely assigned in the trading sys-tem in order to vary the timing of signals. iiParameter Set: Any combination of parameter values. ii

Parameter Stability: The goal of optimization is to find broad re-gions of parameter values with good system performance, insteadonly one parameter which can represent an isolated set of marketconditions. ii

Time Stability: In the case of positive performance of the mechani-cal system in a specific time frame, it should be analyzed in differ-ent time frames to make sure the good performance is not depen-dent only on the initial time frame. ii

Blind Simulation: This is the test of an optimized parameter set ina different time frame to see if the good results reoccur.Average Parameter Set Performance: The complete universe ofparameter sets is defined before any simulation. Simulations arethen run for all the selected parameter sets, and the average ofthese is used as an indication of the system’s potential performance.ii

Average Annual Compounded Return: R = exp(1/N(ln(E) - ln(S)) - 1S - starting equityE - ending equityN - number of years ii

Return Retracement Ratio: (RRR) = R/AMRR - average annual compounded returnAMR - average maximum retracement for each data point. Using

drawdowns (the worst at each given point in time) to measurerisk, the risk component of RRR (AMR) comes closer to de-scribing risk than standard deviation. n

AMR=1/n(Σ MRi) i=1MRi=max(MRPPi,MRSLi)

MRPPi=(PEi - Ei)/PeiMRSLi=(Ei - MEi)/Ei-1Ei - equity at the end of month i,PEi - peak equity on or prior to month i,Ei-1 - equity at the end of month prior to month i,MEi - minimum equity on or subsequent to month i.

RRR represents better return/risk measure than Sharpe ratio.ii

Sharpe Ratio: SR=E/sdvE - expected returnSdv - standard deviation of returns.ii

Expected Net Profit Per Trade: ENPPT= P*AP - L*AL,P - percent of total trades that are profitableL - percent of total trades that are in net lossAP - average net profit of profitable tradesAL - average net loss of losing trade.ii

Maximum Loss: ML= max(MRSLi)i<=n, this represent worse-casepossibilityii

Trade-Based Profit/Loss Ratio: TBPLR= P*AP/L*ALii

4WR_NS_B50_P_M2550 days 25%

20,000

15,000

10,000

5,000

0

SystemIndex

Aug-87 Aug-88 Aug-89 Aug-90 Aug-91

MTA JOURNAL • Summer-Fall 2000 16

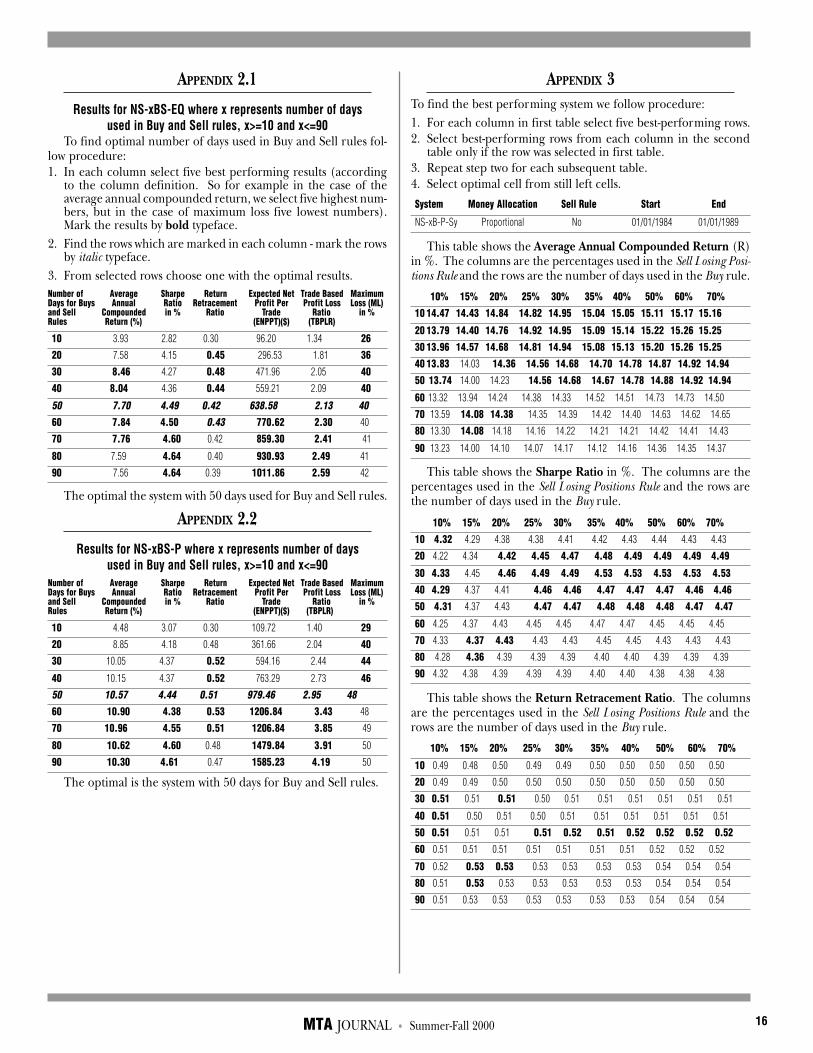

APPENDIX 3To find the best performing system we follow procedure:1. For each column in first table select five best-performing rows.2. Select best-performing rows from each column in the second

table only if the row was selected in first table.3. Repeat step two for each subsequent table.4. Select optimal cell from still left cells.

System Money Allocation Sell Rule Start End��

NS-xB-P-Sy Proportional No 01/01/1984 01/01/1989��

This table shows the Average Annual Compounded Return (R)in %. The columns are the percentages used in the Sell Losing Posi-tions Rule and the rows are the number of days used in the Buy rule.

� 10%� 15%� 20%� 25%� 30%� 35%� 40%� 50%� 60%� 70%10� 14.47� 14.43� 14.84� 14.82� 14.95� 15.04� 15.05� 15.11� 15.17� 15.16��

20� 13.79� 14.40� 14.76� 14.92� 14.95� 15.09� 15.14� 15.22� 15.26� 15.25��30� 13.96� 14.57� 14.68� 14.81� 14.94� 15.08� 15.13� 15.20� 15.26� 15.25��40� 13.83 � 14.03� 14.36� 14.56� 14.68� 14.70� 14.78� 14.87� 14.92� 14.94� �

50 � 13.74� 14.00� 14.23� 14.56� 14.68� 14.67� 14.78� 14.88� 14.92� 14.94��

60 � 13.32� 13.94� 14.24� 14.38� 14.33� 14.52� 14.51� 14.73� 14.73� 14.50��

70� 13.59� 14.08� 14.38 � 14.35� 14.39� 14.42� 14.40� 14.63� 14.62� 14.65��

80 13.30� 14.08� 14.18� 14.16� 14.22� 14.21� 14.21� 14.42� 14.41� 14.43

90 13.23� 14.00� 14.10� 14.07� 14.17� 14.12� 14.16� 14.36� 14.35� 14.37��

This table shows the Sharpe Ratio in %. The columns are thepercentages used in the Sell Losing Positions Rule and the rows arethe number of days used in the Buy rule.

10%� 15%� 20%� 25%� 30%� 35%� 40%� 50%� 60%� 70%��10 4.32� 4.29� 4.38� 4.38� 4.41� 4.42� 4.43� 4.44� 4.43� 4.43

20 � 4.22� 4.34� 4.42� 4.45� 4.47� 4.48� 4.49� 4.49� 4.49� 4.49� �

30� 4.33 � 4.45� 4.46� 4.49� 4.49� 4.53� 4.53� 4.53� 4.53� 4.5340� 4.29 � 4.37� 4.41� 4.46� 4.46� 4.47� 4.47� 4.47� 4.46� 4.46� �

50 � 4.31� 4.37� 4.43� 4.47� 4.47� 4.48� 4.48� 4.48� 4.47� 4.47

60 � 4.25� 4.37� 4.43� 4.45� 4.45� 4.47� 4.47� 4.45� 4.45� 4.45��

70 � 4.33� 4.37� 4.43 � 4.43� 4.43� 4.45� 4.45� 4.43� 4.43� 4.43��

80� 4.28� 4.36� 4.39� 4.39� 4.39� 4.40� 4.40� 4.39� 4.39� 4.39

90 � 4.32� 4.38� 4.39� 4.39� 4.39� 4.40� 4.40� 4.38� 4.38� 4.38��

This table shows the Return Retracement Ratio. The columnsare the percentages used in the Sell Losing Positions Rule and therows are the number of days used in the Buy rule.

� 10%� 15%� 20%� 25% 30% 35% 40% 50% 60% 70%��

10 � 0.49� 0.48� 0.50� 0.49� 0.49� 0.50� 0.50� 0.50� 0.50� 0.50

20 � 0.49� 0.49� 0.50� 0.50� 0.50� 0.50� 0.50� 0.50� 0.50� 0.50

30� 0.51 � 0.51� 0.51� 0.50� 0.51 �0.51� 0.51� 0.51� 0.51� 0.51

40� 0.51� 0.50� 0.51� 0.50� 0.51� 0.51� 0.51� 0.51� 0.51� 0.51

50� 0.51 � 0.51� 0.51� 0.51� 0.52� 0.51� 0.52� 0.52� 0.52� 0.5260 � 0.51� 0.51� 0.51� 0.51� 0.51� 0.51� 0.51� 0.52� 0.52� 0.52

70 � 0.52� 0.53� 0.53 � 0.53� 0.53� 0.53� 0.53� 0.54� 0.54� 0.54

80 � 0.51� 0.53� 0.53� 0.53� 0.53� 0.53� 0.53� 0.54� 0.54� 0.54

90 � 0.51� 0.53� 0.53� 0.53� 0.53� 0.53� 0.53� 0.54� 0.54� 0.54

APPENDIX 2.1

Results for NS-xBS-EQ where x represents number of daysused in Buy and Sell rules, x>=10 and x<=90

To find optimal number of days used in Buy and Sell rules fol-low procedure:1. In each column select five best performing results (according

to the column definition. So for example in the case of theaverage annual compounded return, we select five highest num-bers, but in the case of maximum loss five lowest numbers).Mark the results by bold typeface.

2. Find the rows which are marked in each column - mark the rowsby italic typeface.

3. From selected rows choose one with the optimal results.Number of Average Sharpe Return Expected Net Trade Based MaximumDays for Buys Annual Ratio Retracement Profit Per Profit Loss Loss (ML)and Sell Compounded in % Ratio Trade Ratio in %Rules Return (%) (ENPPT)($) (TBPLR)

10 3.93� 2.82� 0.30� 96.20� 1.34� 2620� 7.58� 4.15� 0.45� 296.53� 1.81� 36� �30 � 8.46� 4.27� 0.48� 471.96� 2.05� 40� �40� 8.04 � 4.36� 0.44� 559.21� 2.09� 40 �

50 � 7.70� 4.49� 0.42� 638.58 � 2.13� 40� �60 � 7.84� 4.50� 0.43� 770.62� 2.30� 40��

70 � 7.76 4.60 0.42 859.30 2.41 41

80 � 7.59� 4.64� 0.40� 930.93� 2.49 � 41�

90� 7.56� 4.64� 0.39� 1011.86� 2.59 � 42��

The optimal the system with 50 days used for Buy and Sell rules.

APPENDIX 2.2

Results for NS-xBS-P where x represents number of daysused in Buy and Sell rules, x>=10 and x<=90

Number of Average Sharpe Return Expected Net Trade Based MaximumDays for Buys Annual Ratio Retracement Profit Per Profit Loss Loss (ML)and Sell Compounded in % Ratio Trade Ratio in %Rules Return (%) (ENPPT)($) (TBPLR)��

10 4.48� 3.07� 0.30� 109.72� 1.40� 29 �

20� 8.85� 4.18� 0.48� 361.66� 2.04� 40 � �

30 � 10.05� 4.37� 0.52� 594.16� 2.44� 44

40 � 10.15� 4.37� 0.52� 763.29� 2.73� 4650� 10.57� 4.44� 0.51� 979.46� 2.95� 48 ��60 � 10.90� 4.38� 0.53� 1206.84 � 3.43� 48��

70� 10.96 � 4.55� 0.51� 1206.84� 3.85� 49��

80 � 10.62� 4.60� 0.48� 1479.84� 3.91� 50��

90 10.30� 4.61� 0.47� 1585.23� 4.19� 50��

The optimal is the system with 50 days for Buy and Sell rules.

MTA JOURNAL • Summer-Fall 2000 17

This table shows the Expected Net Profit Per Trade (ENPPT)in $. The columns are the percentages used in the Sell Losing Posi-tions Rule and the rows are the number of days used in the Buy rule.

10%� 15%� 20%� 25%� 30%� 35%� 40%� 50%� 60%� 70%��10 3511.64� 4507.22� 5905.14� 6597.08� 7739.21� 8520.50� 8823.50� 9802.04� 10245.87 10447.28

20 3385.28� 4695.31� 5949.73� 7252.84 7716.12 8677.11 9264.20 9869.52 10502.81 10498.79

30 � 3709.77 5067.45 5923.62 7009.01 7807.08 8492.72 9224.62 9817.10 10472.16 10465.79

40 � 3805.97 4834.92 5955.58 7140.84 7725.92 8265.74 8924.55 9607.69 10041.16 10156.11

50� 3925.73 � 5107.18� 6188.47� 7345.42� 7969.82� 8372.83� 9164.75� 9608.21�10030.17�10149.77

60 � 3710.81� 5241.00� 6428.99� 7492.27� 7966.95� 8540.02� 8931.42� 9557.56� 9840.63� 9961.49

70 � 4053.34� 5541.77� 6717.81 � 7384.87� 8043.70� 8427.56� 8805.56� 9528.22� 9711.08� 9830.62

80 � 4078.14� 5771.52� 6622.01� 7355.29� 8109.93� 8316.63� 8708.21� 9420.13� 9502.17� 9619.90

90 � 4020.47 5821.46 6611.41 7275.61 8127.05 8230.48 8736.40 9347.20 9432.68 9544.71

This table shows the Maximum Loss (ML) in %. The columnsare the percentages used in the Sell Losing Positions Rule and therows are the number of days used in the Buy rule.

� 10%� 15%� 20% �25%� 30%� 35%� 40%� 50%� 60%� 70%��10� 0.65� 0.66� 0.66� 0.66� 0.66� 0.66� 0.67� 0.67� 0.67� 0.67��

20 � 0.63� 0.65� 0.65� 0.66� 0.66� 0.66� 0.66� 0.66� 0.67� 0.67��

30 � 0.62� 0.64� 0.64� 0.65� 0.65� 0.65� 0.66� 0.66� 0.66� 0.66��

40� 0.61� 0.62� 0.63� 0.64� 0.64� 0.64� 0.65� 0.65� 0.65� 0.65��

50� 0.61� 0.62� 0.63� 0.63� 0.64� 0.64� 0.64� 0.64� 0.64� 0.6460 � 0.60� 0.61� 0.62� 0.63� 0.63� 0.63� 0.63� 0.64� 0.64� 0.64��

70 � 0.60� 0.61� 0.61 � 0.62� 0.62� 0.62� 0.62� 0.62� 0.62� 0.62

80 � 0.59� 0.61� 0.61� 0.61� 0.61� 0.61� 0.61� 0.61� 0.61� 0.61

90 � 0.59� 0.60� 0.61� 0.61� 0.61� 0.61� 0.61� 0.61� 0.61� 0.61�

This table shows the Trade-Based Profit/Loss Ratio (TBPLR).The columns are the percentages used in the Sell Losing PositionsRule and the rows are the number of days used in the Buy rule.

� 10%� 15%� 20%� 25%� 30%� 35%� 40%� 50%� 60% 70%10 9.76 10.04 14.62 16.25 19.87 25.01 27.07 39.85 62.18 81.81

20 � 8.95� 11.17� 15.42� 21.44� 22.65� 26.89� 32.67� 41.55� 95.37� 93.95

30 � 10.31� 13.94� 15.41� 19.61� 22.47� 26.39� 32.00� 40.02� 93.59� 92.20

40 � 10.24� 12.44� 15.63� 20.79� 23.31� 25.28� 31.02� 37.71� 60.18� 90.27

50 10.15� 12.93� 16.78� 21.31� 24.21 � 24.91� 33.52� 38.51 61.27 93.06

60 9.11� 13.88� 19.17� 24.92� 25.00� 30.36� 33.32� 63.53� 64.58� 102.15

70 � 11.45� 16.57� 23.84 � 24.46� 27.89� 29.73� 30.79 �64.39� 63.26� 99.61

80 � 11.08� 19.83� 23.73� 24.85� 29.52� 29.36� 31.24� 66.51� 64.05� 102.01

90 � 11.36� 20.05� 24.62� 24.23� 31.79 �29.51� 33.90� 71.46� 69.73 111.06

The best performing is the system with 50 days used for Buyrule and 25% Sell Losing Position rule.�

ART RUSZKOWSKI, CMT, M.SC.Art Ruszkowski combines his strong scientific background

with knowledge and practice of technical analysis specializingin quantitive analysis, and mechanical trading system designand testing. He is currently a partner in a private investmentfund, and is responsible for development of models, studies,portfolio selections and money management strategies.

Art is a member of the MTA and the CSTA.

MTA JOURNAL • Summer-Fall 2000 18

It is one thing to say that the Wave Principle makes sense in thecontext of nature and its growth forms. It is another to postulate ahypothesis about its mechanism. The biological and behavioral sci-ences have produced enough relevant work to make a case thatunconscious paleomentational processes produce a herding im-pulse with Fibonacci-related tendencies in both individuals andcollectives. Man’s unconscious mind, in conjunction with others, isthus disposed toward producing a pattern having the properties ofthe Wave Principle.

THE PALEOMENTATIONAL HERDING IMPULSE

Over a lifetime of work, Paul MacLean, former head of the Labo-ratory for Brain Evolution at the National Institute of Mental Health,has developed a mass of evidence supporting the concept of a“triune” brain, i.e., one that is divided into three basic parts. Theprimitive brain stem, called the basal ganglia, which we share withanimal forms as low as reptiles, controls impulses essential to sur-vival. The limbic system, which we share with mammals, controlsemotions. The neocortex, which is significantly developed only inhumans, is the seat of reason. Thus, we actually have three con-nected minds: primal, emotional and rational. Figure 1, fromMacLean’s book, The Triune Brain in Evolution,1 roughly shows theirphysical locations.

The neocortex is involved in the preservation of the individualby processing ideas using reason. It derives its information fromthe external world, and its convictions are malleable thereby. Incontrast, the styles of mentation outside the cerebral cortex areunreasoning, impulsive and very rigid. The “thinking” done by thebrain stem and limbic system is primitive and pre-rational, exactlyas in animals that rely upon them.

The basal ganglia control brain functions that are often termedinstinctive: the desire for security, the reaction to fear, the desire toacquire, the desire for pleasure, fighting, fleeing, territorialism,migration, hoarding, grooming, choosing a mate, breeding, theestablishment of social hierarchy and the selection of leaders. Morepertinent to our discussion, this bunch of nerves also controls co-ordinated behavior such as flocking, schooling and herding. All

these brain functions insure lifesaving or life-enhancing actionunder most circumstances and are fundamental to animal motiva-tion. Due to our evolutionary background, they are integral tohuman motivation as well. In effect, then, portions of the brain are“hardwired for certain emotional and physical patterns of reaction”2

to insure survival of the species. Presumably, herding behavior, whichderives from the same primitive portion of the brain, is similarlyhardwired and impulsive. As one of its primitive tools of survival,then, emotional impulses from the limbic system impel a desireamong individuals to seek signals from others in matters of knowl-edge and behavior, and therefore to align their feelings and con-victions with those of the group.

There is not only a physical distinction between the neocortexand the primitive brain but a functional dissociation between them.The intellect of the neocortex and the emotional mentation of thelimbic system are so independent that “the limbic system has thecapacity to generate out-of-context, affective feelings of convictionthat we attach to our beliefs regardless of whether they are true or false.”3

Feelings of certainty can be so overwhelming that they stand fast inthe face of logic and contradiction. They can attach themselves toa political doctrine, a social plan, the verity of a religion, the suretyof winning on the next spin of the roulette wheel, the presumedpath of a financial market or any other idea.4 This tendency is sopowerful that Robert Thatcher, a neuroscientist at the Universityof South Florida College of Medicine in Tampa, says, “The limbicsystem is where we live, and the cortex is basically a slave to that.”5

While this may be an overstatement, a soft version of that depic-tion, which appears to be a minimum statement of the facts, is thatmost people live in the limbic system with respect to fields of knowl-edge and activity about which they lack either expertise or wisdom.

This tendency is marked in financial markets, where most peoplefeel lost and buffeted by forces that they cannot control or foresee.In the 1920s, Cambridge economist A.C. Pigou connected coop-erative social dynamics to booms and despression.6 His idea is thatindividuals rountinely correct their own errors of thought whenoperating alone but abidicate their responsibility to do so in mat-ters that have strong social agreement, regardless of the egregious-ness of the ideational error. In Pigou's words,

Apart altogether from the financial ties by which different busi-nessmen are bound together, there exists among them a certain mea-sure of psychological interdependence. A change of tone in one partof the business world diffuses itself, in a quite unreasoning man-ner, over other and wholly disconnected parts.7

“Wall Street” certainly shares aspects of a crowd, and there isabundant evidence that herding behavior exists among stock mar-ket participants. Myriad measures of market optimism and pessi-mism8 show that in the aggregate, such sentiments among both thepublic and financial professionals wax and wane concurrently withthe trend and level of the market. This tendency is not simply fairlycommon; it is ubiquitous. Most people get virtually all of their ideasabout financial markets from other people, through newspapers,television, tipsters and analysts, without checking a thing. Theythink, “Who am I to check? These other people are supposed to beexperts.” The unconscious mind says: You have too little basis uponwhich to exercise reason; your only alternative is to assume that theherd knows where it is going.

SCIENCE IS REVEALING THE MECHANISM OF THEWAVE PRINCIPLE

Robert R. Prechter, Jr., CMT3

Figure 1The Three Sections of the Triune Brain

Source: The Triune Brain in Evolution

MTA JOURNAL • Summer-Fall 2000 19

In 1987, three researchers from the University of Arizona andIndiana University conducted 60 laboratory market simulations us-ing as few as a dozen volunteers, typically economics students butalso, in some experiments, professional businessmen. Despite giv-ing all the participants the same perfect knowledge of coming divi-dend prospects and then an actual declared dividend at the end ofthe simulated trading day, which could vary more or less randomlybut which would average a certain amount, the subjects in these ex-periments repeatedly created a boom-and-bust market profile. The extrem-ity of that profile was a function of the participants’ lack of experi-ence in the speculative arena. Head research economist Vernon L.Smith came to this conclusion: “We find that inexperienced trad-ers never trade consistently near fundamental value, and most com-monly generate a boom followed by a crash....” Groups that haveexperienced one crash “continue to bubble and crash, but at re-duced volume. Groups brought back for a third trading sessiontend to trade near fundamental dividend value.” In the real world,“these bubbles and crashes would be a lot less likely if the sametraders were in the market all the time,” but novices are alwaysentering the market.9

While these experiments were conducted as if participants couldactually possess true knowledge of coming events and so-called fun-damental value, no such knowledge is available in the real world.The fact that participants create a boom-bust pattern anyway is over-whelming evidence of the power of the herding impulse.

It is not only novices who fall in line. It is a lesser-known factthat the vast majority of professionals herd just like the naïve ma-jority. Figure 2 shows the percentage of cash held at institutions asit relates to the level of the S&P 500 Composite Index. As you cansee, the two data series move roughly together, showing that pro-fessional fund managers herd right along with the market just asthe public does.

Apparent expressions of cold reason by professionals followherding patterns as well. Finance professor Robert Olsen recentlyconducted a study of 4,000 corporate earnings estimates by com-pany analysts and reached this conclusion:

Experts’ earnings predictions exhibit positive bias and disappoint-ing accuracy. These shortcomings are usually attributed to somecombination of incomplete knowledge, incompetence, and/or mis-representation. This article suggests that the human desire for con-

sensus leads to herding behavior among earnings forecasters.10

Olsen’s study shows that the more analysts are wrong, which isanother source of stress, the more their herding behavior increases.11

How can seemingly rational professionals be so utterly seducedby the opinion of their peers that they will not only hold, but changeopinions collectively? Recall that the neocortex is to a significantdegree functionally disassociated from the limbic system. Thismeans not only that feelings of conviction may attach to utterlycontradictory ideas in different people, but that they can do so inthe same person at different times. In other words, the same brain cansupport opposite views with equally intense emotion, depending uponthe demands of survival perceived by the limbic system. This factrelates directly to the behavior of financial market participants, whocan be flushed with confidence one day and in a state of utter panicthe next. As Yale economist Robert Schiller puts it, “You wouldthink enlightened people would not have firm opinions” about mar-kets, “but they do, and it changes all the time.”12 Throughout the herd-ing process, whether the markets are real or simulated, and whetherthe participants are novices or professionals, the general convic-tion of the rightness of stock valuation at each price level is power-ful, emotional and impervious to argument.