Jeff Barbacci, Audit Shareholder Thomas Howell Ferguson P ... Barbacci, Audit Shareholder Thomas...

95

Jeff Barbacci, Audit Shareholder Thomas Howell Ferguson P.A. (850) 668-8100 Al Altun, CFO - West Construction, Inc. (561) 588-2027

Transcript of Jeff Barbacci, Audit Shareholder Thomas Howell Ferguson P ... Barbacci, Audit Shareholder Thomas...

Jeff Barbacci, Audit Shareholder

Thomas Howell Ferguson P.A.

(850) 668-8100

Al Altun, CFO - West Construction, Inc.

(561) 588-2027

Presentation Outline� Introductions

� Economic Factors for Florida

� The American Recovery and Reinvestment Act of 2009 (ARRA)

� ARRA Effects on the Single Audit in accordance with OMB circular A-133

� Authoritative Updates

� Recent GASB Pronouncements

� GASB Outlook

� Internal Revenue Code Subsection 3402(t)

� Closing Remarks

2

Economic Factors for Florida� Florida’s Gross Domestic Product, in real growth, has declined

from 2nd in the nation in 2005, to 48th in the nation in 2008.

� Unemployment skyrocketed with 49 of the 67 counties showing double-digit unemployment rates. As of December 2009, the unemployment rate for Florida was 11.8% while the nation’s unemployment rate was 10%.

� Population growth, which is the state’s primary engine of economic growth for fueling both employment and income growth, has slowed.

3

Economic Factors for Florida (continued)

� Home sales were on an upswing due to the homebuyer tax credits, which expired April 30, 2010.

� Sales mix points to lower prices within the economy.

� Sentiment is improving, with Florida’s consumer confidence increasing.

� The job market will take a long time to recover. Of all factors, this is the one that drives the train of the economy. No jobs equals no income, no housing, and no consumer spending; it goes on and on.

� Funds for state and local governments have tightened which has caused the scrutiny over those funds to increase.

� Revenues have decreased for most businesses with net assets taking hits. (Direct effect on shrinking materiality levels).

4

Financial Emergencies

� Failure to pay short term loans or make long-term debt payments due to lack of funds

� Failure to pay uncontested claims within 90 days due to a lack of funds

� Failure to timely transfer withholding taxes or other withholdings

� Failure to pay wages salaries or retirement benefits

� Unreserved/unrestricted fund balance/net assets deficit

� Others as identified by the AG

5

The American Recovery and

Reinvestment Act of 2009 (ARRA)Purpose:

� To preserve and create jobs and promote economic recovery.

� To assist those most impacted by the recession.

� To provide investments needed to increase economic efficiency by spurring technological advances in science and health.

� To invest in transportation, environmental protection, and other infrastructures that will provide long-term economic benefits.

� To stabilize state and local government budgets, in order to minimize and avoid reductions in essential services and counterproductive state and local tax increases.

7

ARRA Reporting RequirementsNo later than 10 days after the end of each calendar quarter, each recipient that received recovery funds from a federal agency shall submit a report to that agency that contains —

1)the total amount of recovery funds received from that agency;

2)the amount of recovery funds received that were expended or obligated to projects or activities; and

8

ARRA Reporting Requirements (continued)

3) A detailed list of all projects or activities for which recovery funds were expended or obligated, including —a) the name of the project or activity;b) a description of the project or activity;c) an evaluation of the completion status of the project or activity;d) an estimate of the number of jobs created and the number of jobs

retained by the project or activity(should be converted to FTE);and

e) for infrastructure investments made by state and local governments, the purpose, total cost, and rationale of the agency for funding the infrastructure investment with funds made available under this Act, and the name of the person to contact at the agency if there are concerns with the infrastructure investment.

4) Detailed information on any subcontracts or subgrants awarded by the recipient are to include the data elements required to comply with the Federal Funding Accountability and Transparency Act of 2006.

9

ARRA Reporting Requirements (continued)

What happens to the reports submitted?

� Reported numbers are aggregated and reported on www.recovery.gov

� Latest Florida figures:

� Total Funds Awarded = $9,117,040.00 (Feb. 17, 2009 – Mar. 31, 2010)

� Total Funds Received = $2,184,530.00 (Feb. 17, 2009 – Mar. 31, 2010)

� Recipient Reported Jobs = 38,496 (Jan. 1, 2010 – Mar. 31, 2010)

� 924 Contracts Awarded (Feb. 17, 2009 – Mar. 31, 2010)

� 5123 Grants Awarded (Feb. 17, 2009 – Mar. 31, 2010)

� 9 Loans Awarded (Feb. 17, 2009 – Mar. 31, 2010)

10

ARRA effects on A-133 Audits� The effects of the ARRA on audits under OMB Circular A-133

will increase significantly as awards and expenditures under ARRA programs increase.

� Due to the inherent risk with the new transparency and accountability requirements over expenditures of ARRA awards, the auditor should consider all federal programs with expenditures of ARRA awards to be programs of higher risk in accordance with §___.525(c)(2) and §___.525(d) of OMB Circular A-133.

� Type A programs with expenditures of ARRA awards should not be considered low-risk except when the auditor determines, and clearly documents the reasons, that the expenditures of ARRA awards is low-risk for the program.

11

ARRA effects on A-133 Audits (continued)

� Any cluster (i.e., Research and Development [R&D], Student Financial Assistance [SFA], or other clusters) to which a federal program with a new ARRA CFDA number has been added should be considered a new program and would not qualify as a low-risk Type A program under §___.520(c)(1) of OMB Circular A-133 (i.e., the cluster will not meet the requirement of having been audited as a major program in at least one of the two most recent audit periods as the federal program funded under the ARRA did not previously exist).

12

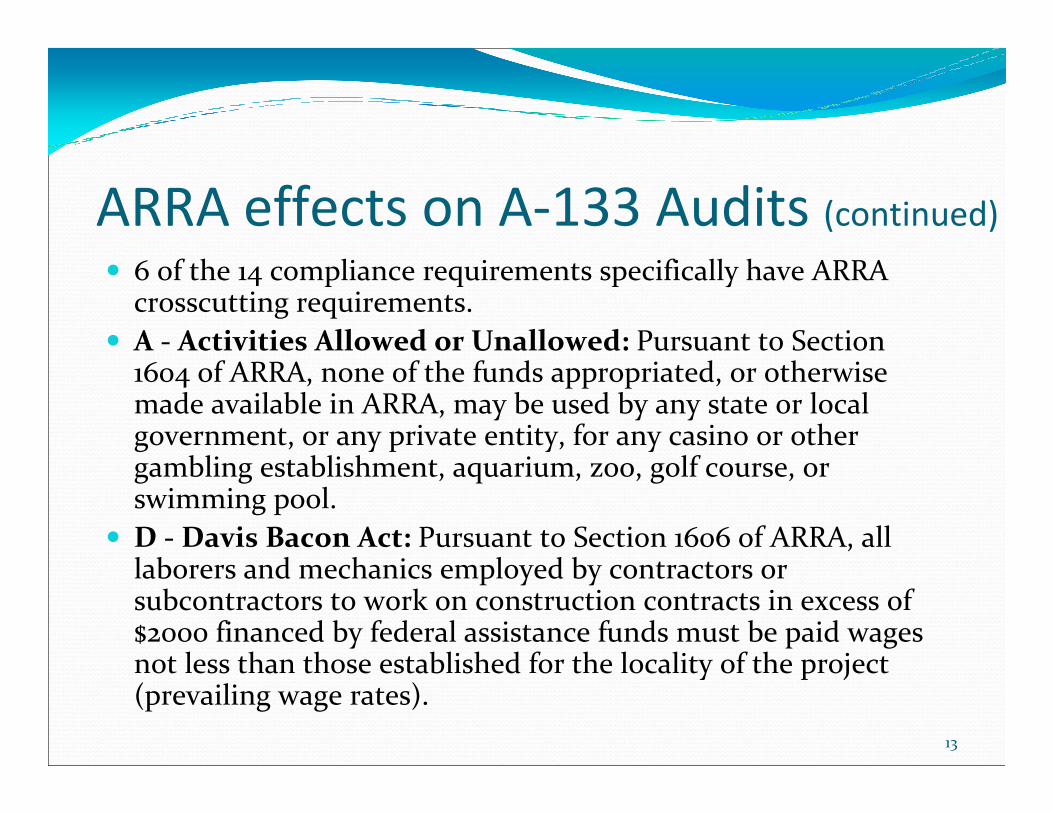

ARRA effects on A-133 Audits (continued)

� 6 of the 14 compliance requirements specifically have ARRA crosscutting requirements.

� A - Activities Allowed or Unallowed: Pursuant to Section 1604 of ARRA, none of the funds appropriated, or otherwise made available in ARRA, may be used by any state or local government, or any private entity, for any casino or other gambling establishment, aquarium, zoo, golf course, or swimming pool.

� D - Davis Bacon Act: Pursuant to Section 1606 of ARRA, all laborers and mechanics employed by contractors or subcontractors to work on construction contracts in excess of $2000 financed by federal assistance funds must be paid wages not less than those established for the locality of the project (prevailing wage rates).

13

� I - Procurement and Suspension and Debarment: ARRA Section 1605 prohibits the use of ARRA funds for a project for the construction, alteration, maintenance, or repair of a public building or work, unless all of the iron, steel, and manufactured goods used in the project are produced in the United States.

� L – Reporting Requirements : Section 1512 of ARRA encompasses the reporting requirements (discussed in previous slides).

� M – Subrecipient Monitoring: Pursuant to Section 1512(h) of ARRA, identifying to first-tier subrecipients the requirement to register in the Central Contractor Registration, including obtaining a Dun and Bradstreet Data Universal Numbering System (DUNS) number, and maintaining the currency of that information .

ARRA effects on A-133 Audits (continued)

14

ARRA effects on A-133 Audits (continued)

� N – Special Tests and Provisions:

� ARRA funds must be accounted for separately.

� The financial management system must permit the preparation of required reports and tracing of funds adequate to establish thatfunds were used for authorized purposes and allowable costs.

� The SEFA must separately identify ARRA awards.

� Separately identify to each subrecipient the document at the time of the sub-award and the disbursement of funds, the federal award number, the CFDA number, and the amount of ARRA funds

15

ARRA – Message Points for Clients

� Need process for accepting Recovery Act funds (should be a conscious management decision) and segregating Recovery Act funds

� Should be aware of Recovery Act compliance requirements and establish internal control over compliance to ensure those requirements met

� Need to be able to meet 1512 reporting requirements and understand that not complying with those requirements could mean sanctions going forward

� Likely to be more federal agency follow-up on findings reported in single audits

16

National Single Audit Sampling

Project

Background

� The Project was conducted under the auspices of the Audit Committee of the President’s Council on Integrity and Efficiency (PCIE), as a collaborative effort involving PCIE member organizations, as well as a member of the Executive Council on Integrity and Efficiency (ECIE) and three State Auditors.

Purpose

� Performed to determine the quality of single audits using statistical methods and to make recommendations to address noted audit quality issues. By agreement with OMB and the other participants, the U.S. Department of Education and the Office of Inspector General coordinated the administration of the Project and prepared the Project report.

18

National Single Audit Sampling Project

(continued)Dates

� The report date for the project was June 21, 2007.

� Population from audits submitted and accepted from the period of April 1, 2003 through March 31, 2004.

Sampling

� 208 audits randomly selected from a universe of over 38,000 audits submitted and accepted.

� Stratum I included audits of entities that expended $50 million or more of federal awards. (852 total Stratum I audits)

� Stratum II included audits of entities that expended at least $500,000 of federal awards, but less than $50 million. (37,671 total Stratum II audits)

19

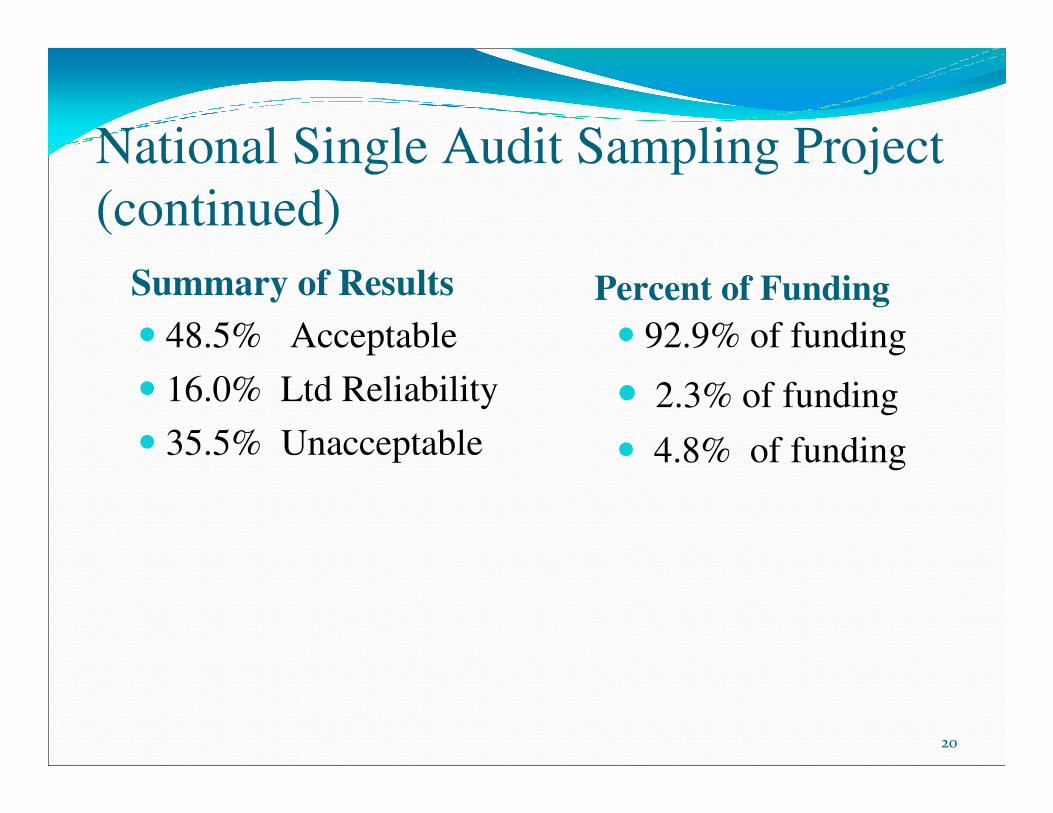

National Single Audit Sampling Project

(continued)

Summary of Results Percent of Funding

� 48.5% Acceptable

� 16.0% Ltd Reliability

� 35.5% Unacceptable

� 92.9% of funding

� 2.3% of funding

� 4.8% of funding

20

National Single Audit Sampling Project

(continued)

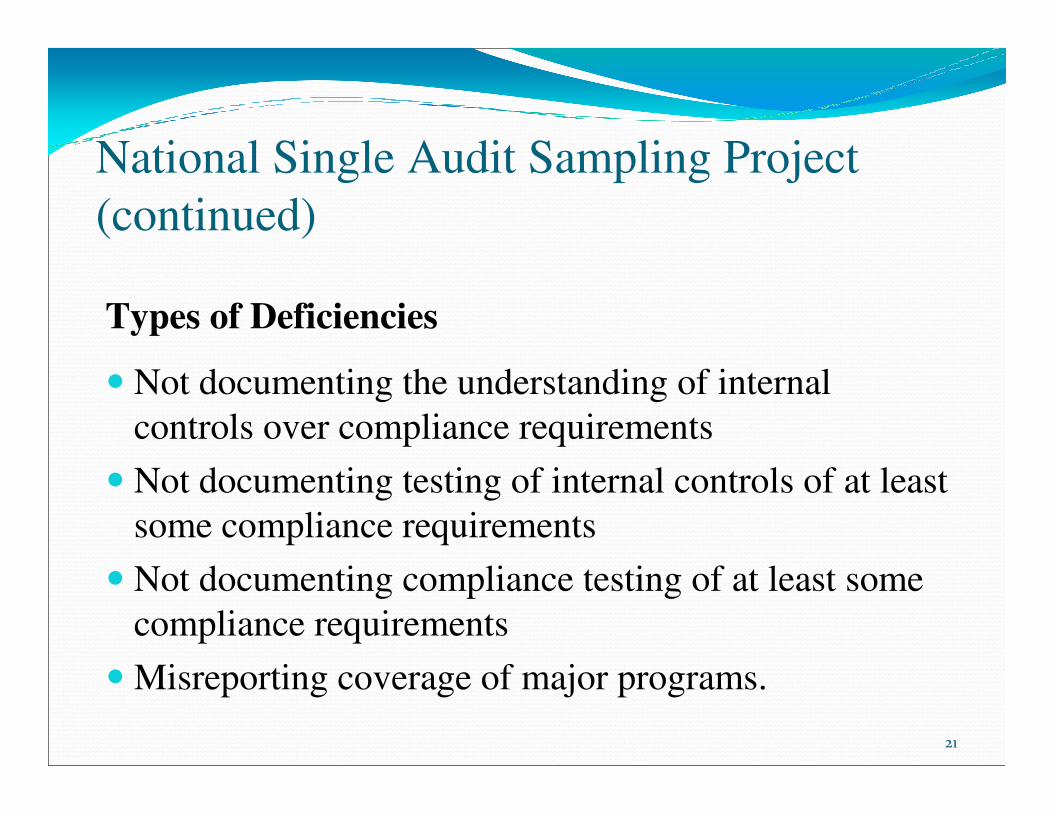

Types of Deficiencies

� Not documenting the understanding of internal

controls over compliance requirements

� Not documenting testing of internal controls of at least

some compliance requirements

� Not documenting compliance testing of at least some

compliance requirements

� Misreporting coverage of major programs.

21

National Single Audit Sampling Project

(continued)Recommendations for the deficiencies

OMB, the AICPA and other parties, as appropriate, work

together to address the deficiencies as follows:

� Revise and improve single audit standards, criteria and

guidance

� Establish minimum requirements for training on

performing single audits

� Review and enhance processes to address unacceptable

single audits

� Develop consistent sampling processes

22

Status of Recommendations

Work Completed� Sampling Issues In A Single Audit Environment � Internal Control And Compliance Responsibilities In A

Single Audit Environment � Schedule Of Expenditures Federal Awards Reporting

Issues � SAS 74 Revisions (SAS 117)

Still Active� Reporting Audit Findings In A Single Audit� Single Audit Training Needs And Continuing

Professional Education Evaluation� Peer Review

23

Technical Update – F.A.C.

Data Collection Form being updated for 2010 – 2012 audits

� Federal Register notice posted March 30, 2010 proposing a new form and instructions; comments due April 29, 2010

� The proposed revised Form SF-SAC will replace the current form for audit periods ending 2010 and will also be used for audit periods ending in 2011 and 2012

� The proposed change is to add a new data element on Part III of the SF-SAC Form to identify ARRA expenditures

� The new 2010 Form will allow FAC to collect and store "Y" or "N" to identify ARRA awards to allow for direct searching

25

Technical Update - GAO

26

Technical Update - AICPA Governmental

and A-133 Audit Guide

� Added Chapter 11 on sampling

� Changes to reflect FASB codifications

� Numerous paragraphs revised to define professional requirements.

� Appendix B added to paragraph 4.52,containing sample reports based on SAS N0. 115.

� Numerous paragraphs revised addressing electronic submission of the data collection form

27

Technical Update – Sampling

� New chapter included in the 2010 AICPA Audit Guide, Government Auditing Standards and Circular A-133 (GAS-A133 Guide)

� You should be considering this guidance as you design your test work this year

28

Technical Update – Sampling

29

Importance / Significance of

Control Being Tested

Minimum Sample Size

0 deviations tolerated

Very Significant and High Risk of Deviation 60

Very Significant and Low Risk or Deviation

Or Moderate Significant and High

Risk of Deviation

40

Moderately Significant and Low Risk of Deviation 25

30

Minimum samples for populations >250 - CONTROLS

Technical Update – Sampling

Compliance Testing for each Direct and Material Compliance Requirement in relation to:

� Other evidence obtained

� Risk assessment procedures

� Important item testing

� Determine the risk of material noncompliance

� Inherent risk assessment

� Controls testing results—control risk assessment

31

Technical Update – Sampling

Minimum samples for populations >250 – COMPLIANCE

Desired Level of Assurance

(Remaining Risk of Material

Noncompliance)

Minimum Sample Size

High 60

Moderate 40

Low 25

Technical Update – Sampling

32

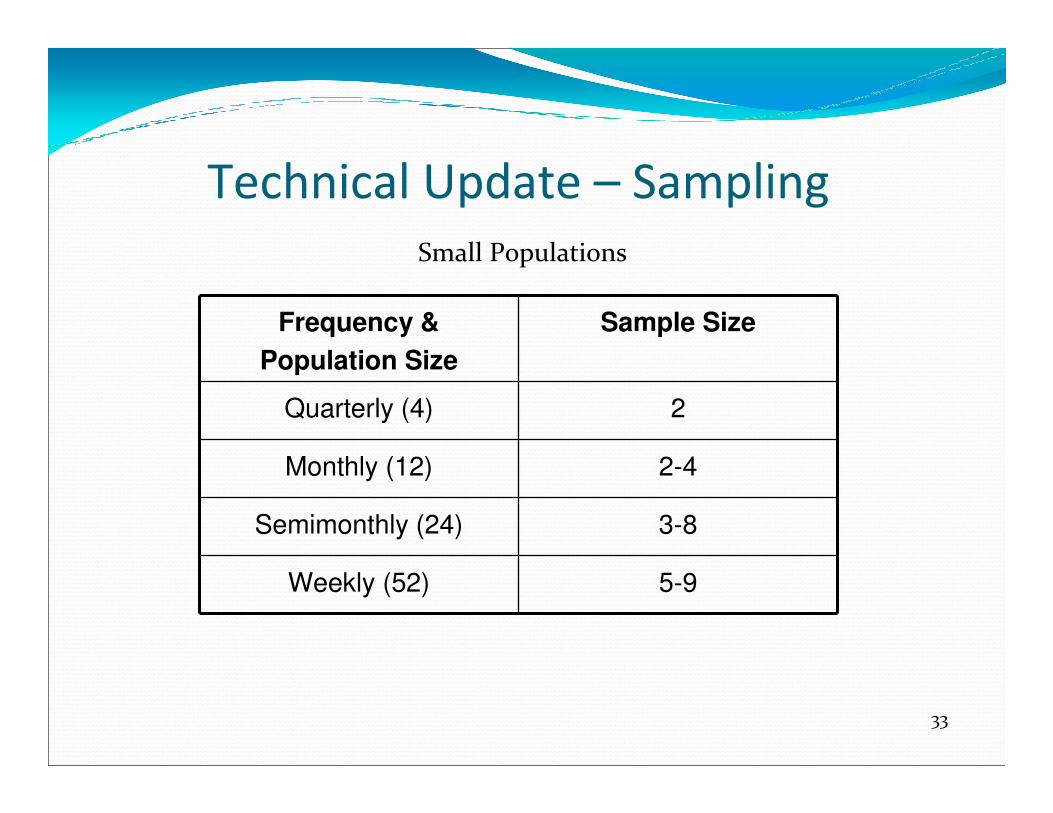

Small Populations

Frequency &

Population Size

Sample Size

Quarterly (4) 2

Monthly (12) 2-4

Semimonthly (24) 3-8

Weekly (52) 5-9

Technical Update – Sampling

33

Technical Update – AICPA

SAS 117 – Compliance Auditing

� Background� GAQC/ASB TF charged with reviewing SAS No. 74 and making

appropriate changes/enhancements needed in response to federal study on single audit quality

� New SAS issued in December in new clarity format

� Clarifies auditor’s responsibilities in a compliance audit performed under GAAS

� States that all other auditing standards apply to compliance audits unless otherwise noted in the revised SAS

� Effective date June 30, 2010, year-ends

� Related GAS/A133 Guide revisions currently in process

34

Technical Update – AICPA

SAS 117Responsibilities:

1. Management is responsible for compliance

2. Auditor responsible for obtaining sufficient audit evidence to form an opinion over applicable compliance requirements

35

Technical Update – AICPA

SAS 117Process

1. Identify applicable programs and compliance requirements

2. Perform risk assessment procedures

3. Assess risk of material noncompliance due to error or fraud for each applicable compliance requirement

4. Perform appropriate testing

5. Perform procedures through date of auditor’s report

6. Obtain tailored client representations

7. Evaluate audit evidence and form an opinion

36

Technical Update – AICPA

SAS 117Documentation:

1. Risk assessment procedures performed including those to understand I/C over compliance

2. Responses to assessments of risk of material noncompliance, testing procedures performed and the results of those tests

3. Materiality levels and the basis on which they were determined

4. How the auditor complied with other supplementary audit requirements

37

Technical Update - AICPA

� SAS 115 - Communicating Internal Control Related Matters Identified in an Audit� Effective for audits of financial statements for periods ending on or after December

15, 2009

� New definitions:� A material weakness is a deficiency, or combination of

deficiencies, in internal control, such that there is a reasonable possibility that a material misstatement of the entity's financial statements will not be prevented, or detected and corrected on atimely basis.

� A significant deficiency is a deficiency, or a combination of deficiencies, in internal control that is less severe than a material weakness, yet important enough to merit attention by those charged with governance.

38

Technical Update - AICPA

39

Three new audit standards on Supplementary information:

1.SAS 118 (AU section 550)2.SAS 119 (AU section 551)3.SAS 120 (AU section 558)

Effective for periods beginning on or after 12/25/10; early application is permitted

Technical Update – AICPA A&A Guides

2010 GAS/A133 Guide issued May 2010� Chapter 11 – audit sampling considerations

� Incorporates SAS 115, 117, 119 and OMB guidance� Other standards applicable to compliance audit – guide

provides some guidance (e.g., fraud, internal auditors, etc.

� Recovery Act guidance only appears at end of each chapter

State and Local A&A Guide

� Updates through March 2010

� New GASB standards that become effective this year

� Footnotes to identify places where GASB standards issued but not yet effective

40

Recent GASB Pronouncements� Statement 54 - Fund Balance Reporting and Governmental

Fund Type Definitions

� Statement 55 - The Hierarchy of Generally Accepted Accounting Principles for State and Local Governments

� Statement 56 - Codification of Accounting and Financial Reporting Guidance Contained in the AICPA Statements on Auditing Standards

� Statement 57 - OPEB Measurements by Agent Employers and Agent Multiple-Employer Plans

� Statement 58 - Chapter 9 Bankruptcies

� Concepts Statement No. 5 - Amendment of Concepts Statement No. 2 – SEA Reporting

� Comprehensive Implementation Guide

42

Statement No. 54� Title: Fund Balance Reporting and Governmental Fund Type

Definitions

� Issue date: March 2009

� Implementation Date: Effective for dates beginning after June 15, 2010, early implementation is encouraged.

� Summary: New fund balance presentation hierarchy is based primarily on the degree of spending constraints placed upon use of resources for specific purposes versus availability for appropriation. Five new fund balance classifications.

43

Statement No. 54 (continued)

� What is Gone ?

� Reserved and unreserved classifications.

� Designation classifications.

� What are the five new classifications ?

1) Nonspendable Fund Balance

2) Restricted Fund Balance

3) Committed Fund Balance

4)Assigned Fund Balance

5) Unassigned Fund Balance

44

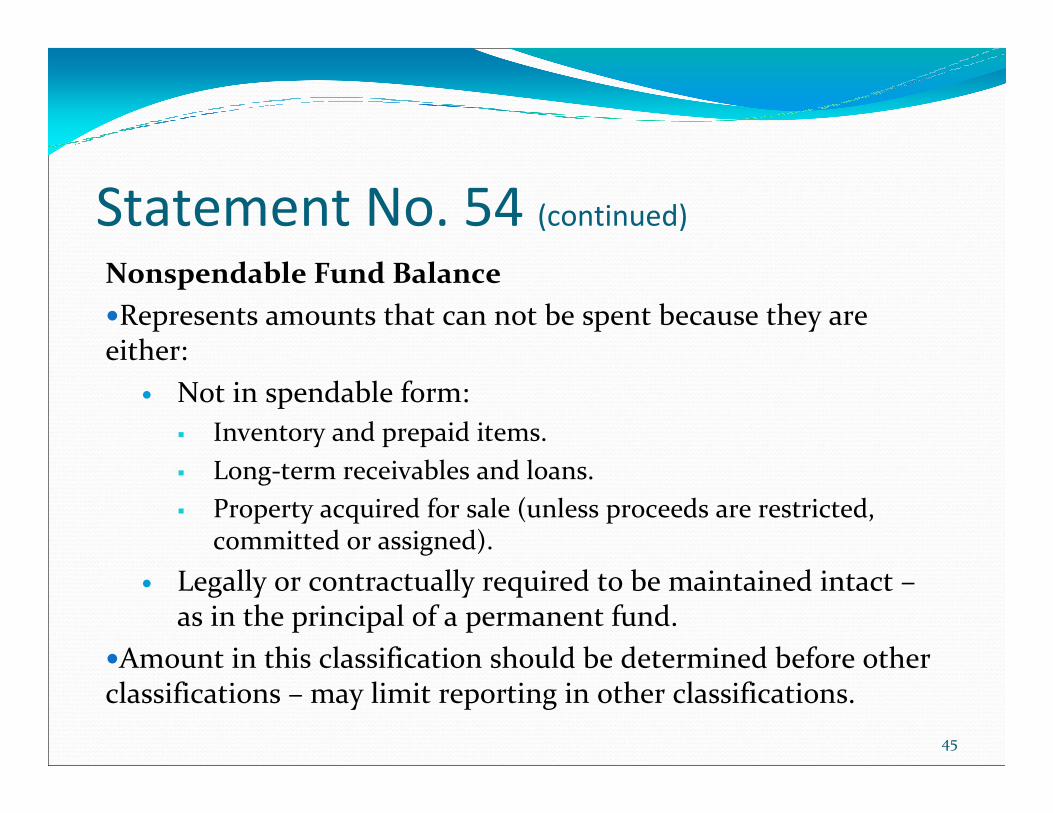

Statement No. 54 (continued)

Nonspendable Fund Balance

�Represents amounts that can not be spent because they are either:

� Not in spendable form:

� Inventory and prepaid items.

� Long-term receivables and loans.

� Property acquired for sale (unless proceeds are restricted, committed or assigned).

� Legally or contractually required to be maintained intact –as in the principal of a permanent fund.

�Amount in this classification should be determined before other classifications – may limit reporting in other classifications.

45

Statement No. 54 (continued)

Restricted Fund Balance

�Constraints placed on the use of amounts are either:

� Externally imposed by creditors (such as through debt covenants), grantors, contributors, or laws or regulations of other government

� Imposed by law through constitutional provisions or enabling legislation.

46

Statement No. 54 (continued)

Committed Fund Balance

�Amounts that can only be used for specific purposes, pursuant toconstraints imposed by formal action of the government’s highest level of decision-making authority.

�Amounts classified as “committed” are not subject to legal enforceability like restricted resources; however, they cannot be used for any other purpose, unless the government removes or changes the commitment by taking the same action it employed to impose the commitment.

�The authorization specifying the purposes for which amounts can be used should have consent of both the legislative and executive branches of the government, if applicable.

47

Statement No. 54 (continued)

Assigned Fund Balance

�Amounts that are intended by the government to be used for a particular purpose, but are neither restricted nor committed, should be reported as assigned fund balance.

�Intent should be expressed by:� The governing body itself, or

� A subordinate high-level body or official possessing the authority to assign resources to be used for specific purposes, in accordance with policy established by the governing body.

�Residual category of Fund Balance for classification of any governmental fund other than the General Fund.

�Use in the General Funds indicates intent to use resources in manner that is narrower than general purpose of the government – cannot cause a deficit in the Unassigned category.

48

Statement No. 54 (continued)

Unassigned Fund Balance

�Residual classification of the General Fund.

�Positive amounts should only be reported in the General Fund.

�Negative amounts can be reported in other funds, but only after assigned amounts have been eliminated.

49

Statement No. 54 (continued)

What other changes?

� Amended the definition of Special Revenue Funds and Capital Projects Funds to incorporate new fund balance classification changes for consistency purposes.

� Addresses fund balance classifications of “stabilization” or “rainy day amounts.”

� New note disclosures are required.

50

Statement No. 54 (continued)

Stabilization or Rainy Day Arrangements

�For the purposes of reporting fund balance, stabilization is considered a specific purpose.

� If criteria is met:

� Restricted Fund Balance.

� Committed Fund Balance.

� If criteria is not met:

� Unassigned Fund Balance (General Fund).

� If criteria is not met:

� Rarely reported in a Special Revenue Fund.

51

Statement No. 54 (continued)

Note Disclosures

�If the aggregate reporting option is utilized for Restricted, Committed, and Assigned Fund Balances, details must be reported in the notes.

�For Committed Fund Balance disclose:

� Governments highest level of decision-making authority.

� Formal action required to be taken to establish, modify, or rescind a commitment.

�For Assigned Fund Balance disclose:

� Body or official authorized to assign amounts to a specific purpose.

� Policy established by governing body pursuant to which that authority is given.

52

Statement No. 54 (continued)

Note Disclosures (continued)

�Classifying Fund Balances:

� Whether the government considers restricted or unrestricted amounts to have been spent when both are available.

� Whether committed, assigned, or unassigned amounts are considered to have been spent when any of those categories could have been used.

�If the government adopts a minimum fund balance policy, the policy should be described in the notes, including the action taken to adopt the policy.

53

Statement No. 54 (continued)

Note Disclosures (continued)

�Encumbrances

� Amounts that are encumbered should not be displayed separately from the categories of Fund Balance on the face of the balance sheet, instead:

� Significant encumbrance should be reported in the notes by major and non-major funds, in the aggregate, in conjunction with disclosures about any other significant commitments.

� Encumbrance for a specific purpose should be reported as committed or assigned, as appropriate, rather than as unassigned.

54

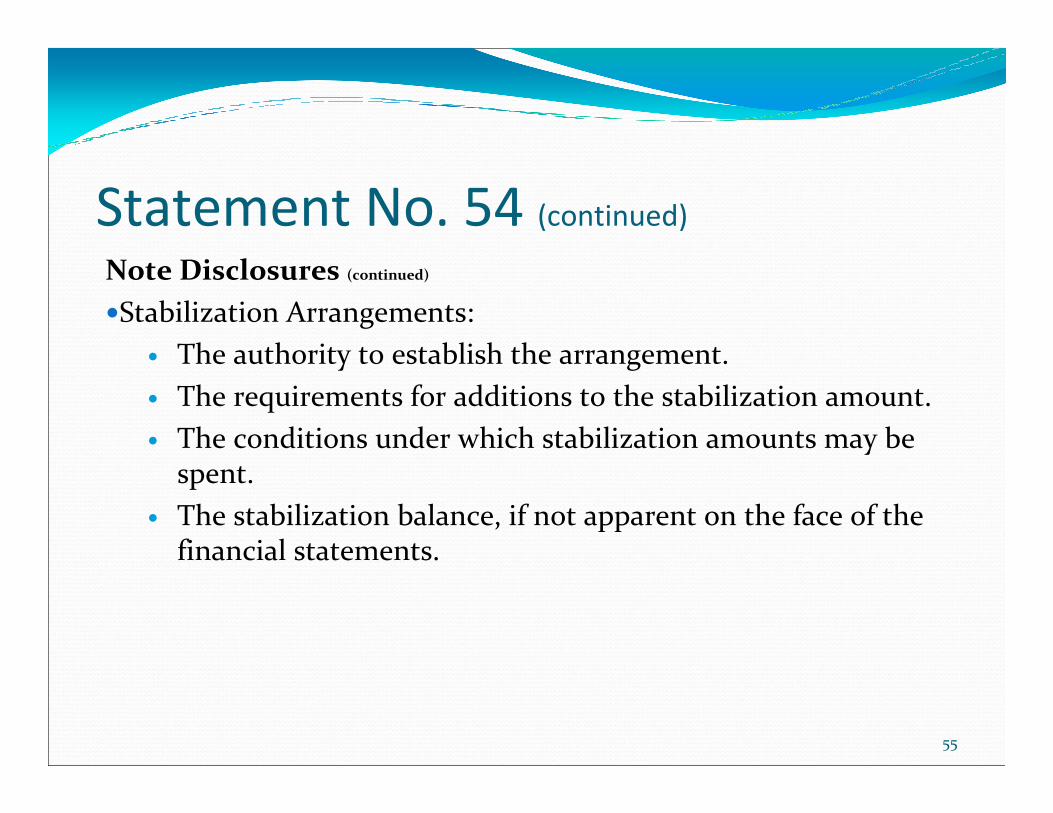

Statement No. 54 (continued)

Note Disclosures (continued)

�Stabilization Arrangements:

� The authority to establish the arrangement.

� The requirements for additions to the stabilization amount.

� The conditions under which stabilization amounts may be spent.

� The stabilization balance, if not apparent on the face of the financial statements.

55

Statement No. 55� Title: The Hierarchy of Generally Accepted Accounting

Principles for State and Local Governments

� Issue date: March 2009

� Implementation Date: Effective immediately.

� Summary: Objective is to incorporate the hierarchy of generally accepted accounting principles (GAAP) for state and local governments into the GASB authoritative literature.

56

Statement No. 55 (continued)The GASB Hierarchy

� Level A – GASB Statements and Interpretations

� Level B – GASB Technical Bulletins and AICPA Industry Audit and Accounting guides, and AICPA Statements of Position (Only if specifically made applicable to SLG entities and cleared by the GASB.

� Level C – AICPA practice bulletins (Specific for SLG’s and cleared by GASB).

� Level D – Implementation guides published by GASB staff, as well as practices that are widely recognized and prevalent to SLG’s.

� Level E – Other literature such as GASB and FASB Concepts statements, audit and accounting textbooks, etc.

57

Statement No. 56� Title: Codification of Accounting and Financial Reporting

Guidance Contained in the AICPA Statements on Auditing Standards

� Issue date: March 2009

� Implementation Date: Effective immediately.

� Summary: Accounting and financial reporting guidance currently found in the AICPA’s Statements on Auditing Standards brought into the GASB literature “as is.” Areas covered are related party transactions, subsequent events, and going concern considerations.

58

Statement No. 57� Title: OPEB Measurements by Agent Employers and Agent

Multiple-Employer Plans

� Issue date: December 2009

� Implementation Date: Effective immediately, except for paragraph 8 (provisions related to the frequency and timing of measurements ), which is effective for periods beginning after June 15, 2011.

� Summary: The objective of this Statement is to address issues related to the use of the alternative measurement method and the frequency and timing of measurements by employers that participate in agent multiple-employer other postemployment benefit (OPEB) plans (that is, agent employers).

59

Statement No. 57 (continued)

What’s New?

� Amends GASB statements 43 and 45.

� Expands option for qualified agent employers that have an individual-employer OPEB plan with less than 100 total plan members to use the alternative measurement method.

� Permits the requirement to be satisfied for an agent multiple-employer OPEB plan by reporting an aggregation of results of actuarial valuations of the individual-employer OPEB plans, or measurements resulting from use of the alternative measurement method for individual-employer OPEB plans that are eligible.

� Clarifies measurement frequency and timing requirements for agent employers (Paragraph 8).

60

Statement No. 58� Title: Accounting and Financial reporting for Chapter 9

Bankruptcies

� Issue date: December 2009

� Implementation Date: Effective for periods beginning after June 15, 2009.

� Summary: The objective of this Statement is to provide accounting and financial reporting guidance for governments that have petitioned for protection from creditors by filing forbankruptcy under Chapter 9 of the United States Bankruptcy Code.

61

Concepts Statement No.5� An amendment of Concepts Statement No. 2, Service Efforts

and Accomplishments Reporting, that updates the conceptual framework by:

� Focusing on voluntary reporting.

� Clarifying the role of GASB.

� Incorporating information from more recent research and reporting experience.

62

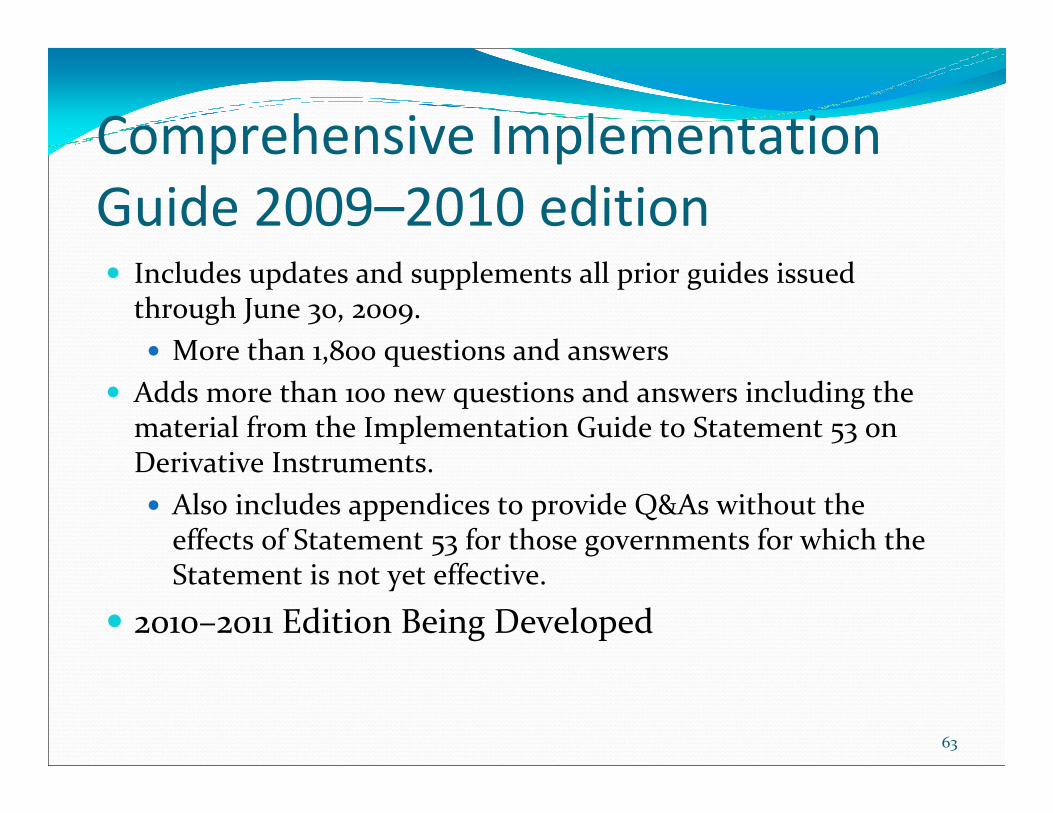

Comprehensive Implementation

Guide 2009–2010 edition� Includes updates and supplements all prior guides issued

through June 30, 2009.

� More than 1,800 questions and answers

� Adds more than 100 new questions and answers including the material from the Implementation Guide to Statement 53 on Derivative Instruments.

� Also includes appendices to provide Q&As without the effects of Statement 53 for those governments for which the Statement is not yet effective.

� 2010–2011 Edition Being Developed

63

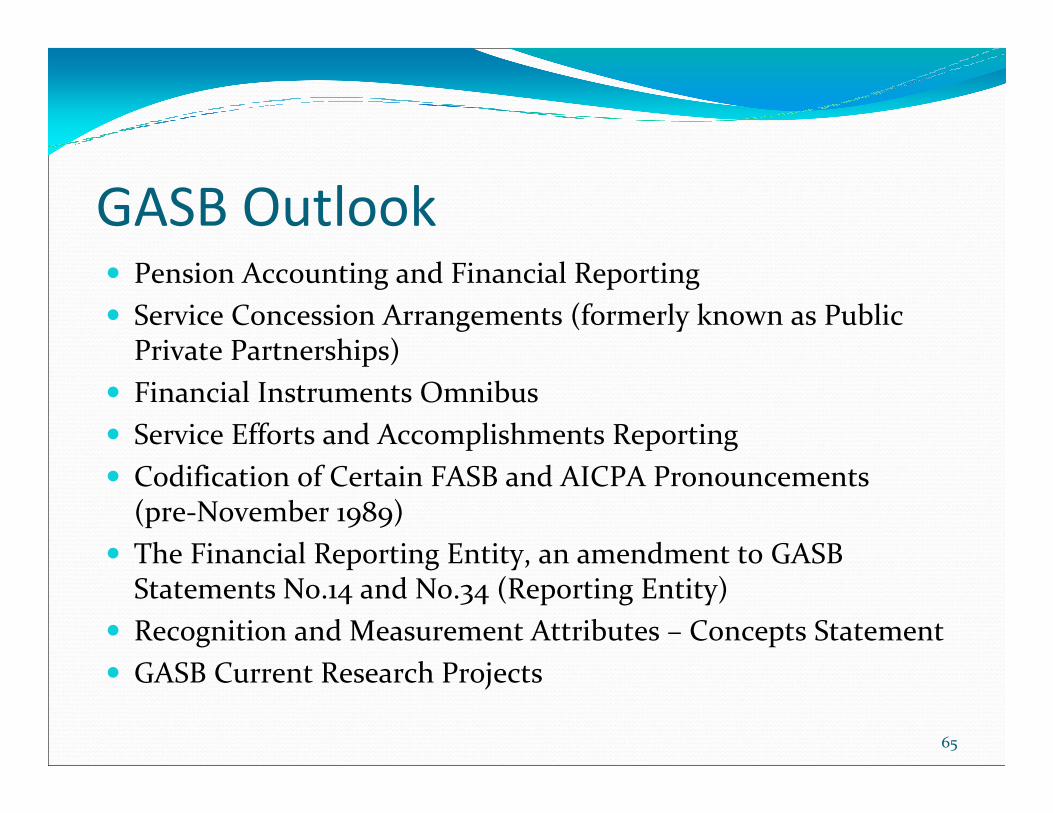

GASB Outlook� Pension Accounting and Financial Reporting

� Service Concession Arrangements (formerly known as Public Private Partnerships)

� Financial Instruments Omnibus

� Service Efforts and Accomplishments Reporting

� Codification of Certain FASB and AICPA Pronouncements (pre-November 1989)

� The Financial Reporting Entity, an amendment to GASB Statements No.14 and No.34 (Reporting Entity)

� Recognition and Measurement Attributes – Concepts Statement

� GASB Current Research Projects

65

GASB Outlook (continued)

Pension Accounting and Financial Reporting

� Invitation for comments issued March 31, 2009; responses were due July 31, 2009. More than 115 responses received. Currently being deliberated by the GASB.

� Included re-examination of Pension Statements No.25 (Plans) and 27 (Employers) to assess effectiveness and consider potential improvements in financial reporting.

� Preliminary Views document scheduled to be issued in June 2010.

66

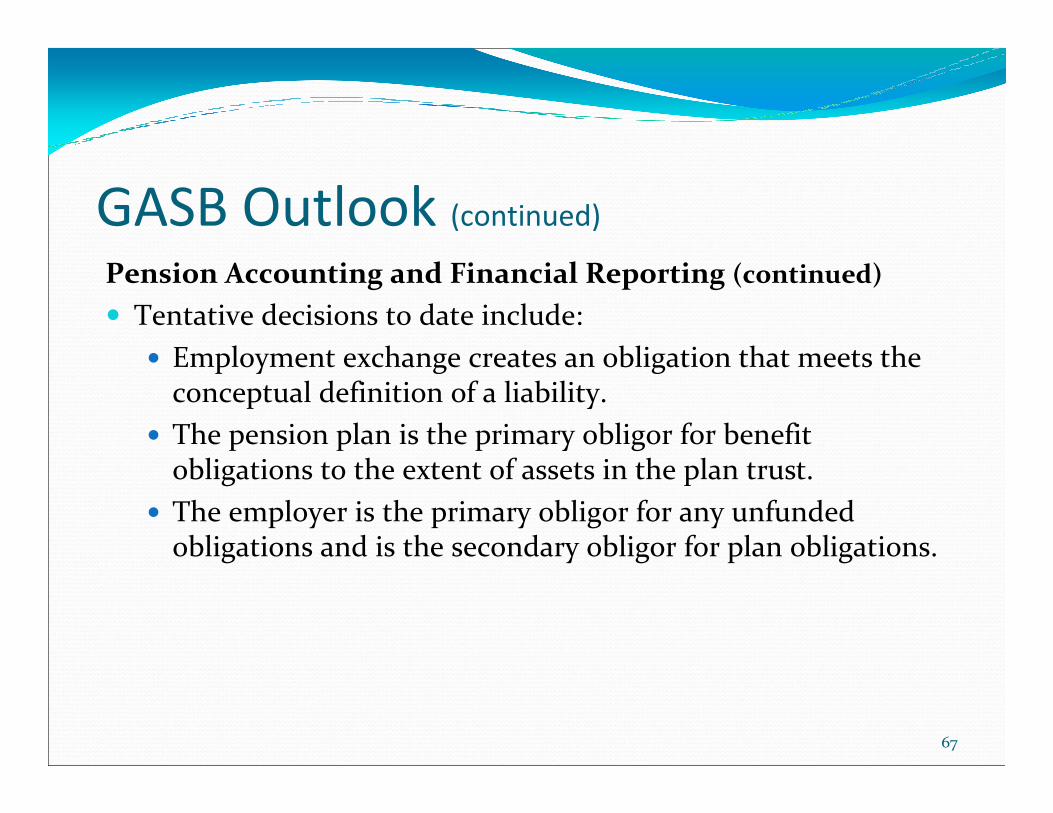

GASB Outlook (continued)

Pension Accounting and Financial Reporting (continued)

� Tentative decisions to date include:

� Employment exchange creates an obligation that meets the conceptual definition of a liability.

� The pension plan is the primary obligor for benefit obligations to the extent of assets in the plan trust.

� The employer is the primary obligor for any unfunded obligations and is the secondary obligor for plan obligations.

67

GASB Outlook (continued)

Service Concession Arrangements

� Formerly – public/private partnerships

� Exposure Draft Issued June 2010

� A Service Concession Arrangement (SCA) is an arrangement between a transferor (government) and an operator (governmental or nongovernmental) in which:

1) The transferor conveys to an operator the right and related obligation to provide services through the use of infrastructure or another public asset (facility) AND

2) the operator collects fees from third parties.

68

GASB Outlook (continued)

Service Concession Arrangements (continued)

Issues being examined/researched:

� Who should report the capital asset in a service concession

arrangement — transferor vs. the operator? Who “controls” the asset?

� The transferor determines or regulates services the operator is

required to provide, to whom the operator is required to provide

them, and the price ranges or rates that can be charged for

services;

� The transferor is entitled - through ownership, beneficial

entitlement, or otherwise – to significant residual interest in the

property at the end of the arrangement.

� When should up-front payments be recognized?

� Generally, over the life of the agreement. 69

GASB Outlook (continued)

Financial Instruments Omnibus

� Exposure Draft issued in June 2009 with a comment deadline of October 30, 2009. Currently being deliberated by the GASB.

� Proposes revisions of existing financial reporting requirements to address issues that have arisen since the release of:

Statement 31 Investments and External Investment Pools

Statement 40 Deposit and Investment Risk Disclosures

Statement 53 Derivative Instruments

70

GASB Outlook (continued)

Service Efforts and Accomplishments (SEA) Reporting

� Proposal issued in June 2009 with a comment deadline of October 30, 2009. Currently being deliberated by the GASB to be issued in June 2010.

� The project:

� Focuses on voluntary reporting.

� Focuses on suggested guidelines.

� The project does not:

� Establish performance measures.

� Establish performance benchmarks.

� Require SEA Reporting.

71

GASB Outlook (continued)

Service Efforts and Accomplishments (SEA) Reporting (continued)

� Proposes four essential components of an effective SAE report:

1) Purpose and scope: Why is the information being reported and what portion of the government does it relate to?

2) Major goals and objectives: Basis for assessing the degree to which a government has achieved the intended results of its programs and services.

3) Key measures of SEA performance: Focus on the measures most important to the reader.

4) Discussion and analysis of results and challenges: An explanation of what has been achieved and what factors affect the level of achievement.

72

GASB Outlook (continued)

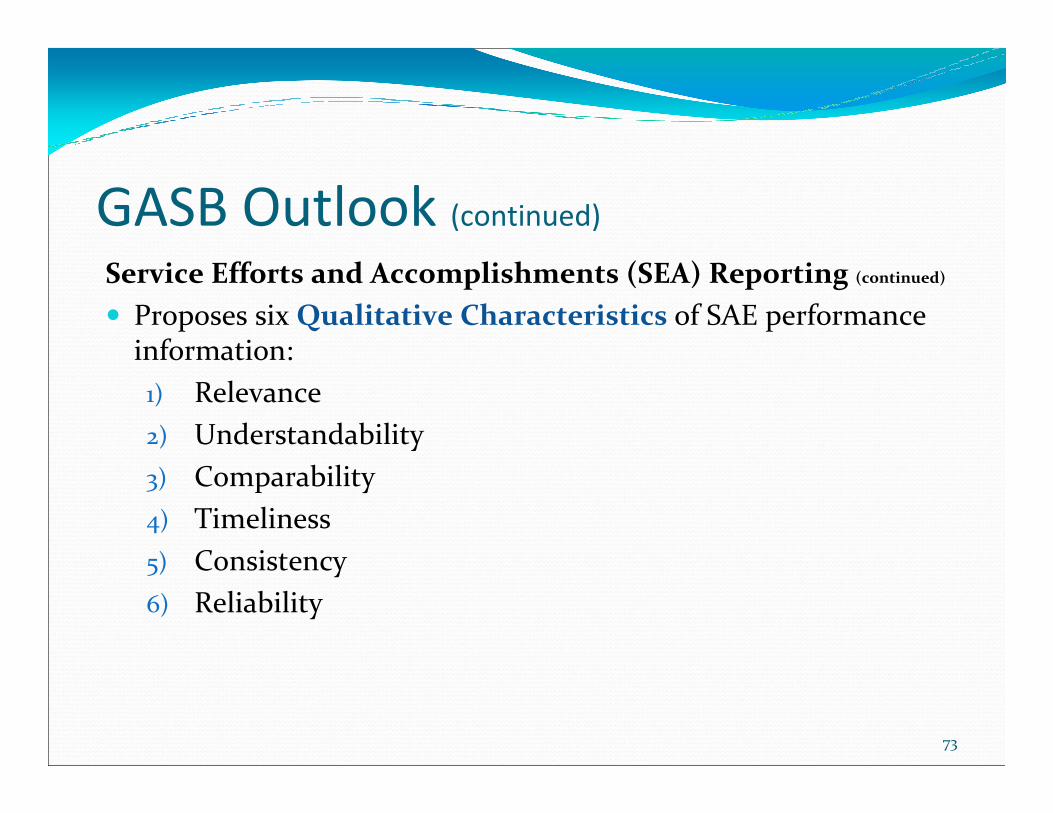

Service Efforts and Accomplishments (SEA) Reporting (continued)

� Proposes six Qualitative Characteristics of SAE performance information:

1) Relevance

2) Understandability

3) Comparability

4) Timeliness

5) Consistency

6) Reliability

73

GASB Outlook (continued)

Service Efforts and Accomplishments (SEA) Reporting (continued)

� Discusses how to effectively communicate SEA performance information.

� Suggested guidelines, although voluntary, will assist governments in improving the quality of their reported SEA performance information.

� Traditional financial statements provide information about fiscal and operational accountability but not the degree to which the government was successful in helping to maintain or improve the well-being of its citizens by providing services.

74

GASB Outlook (continued)

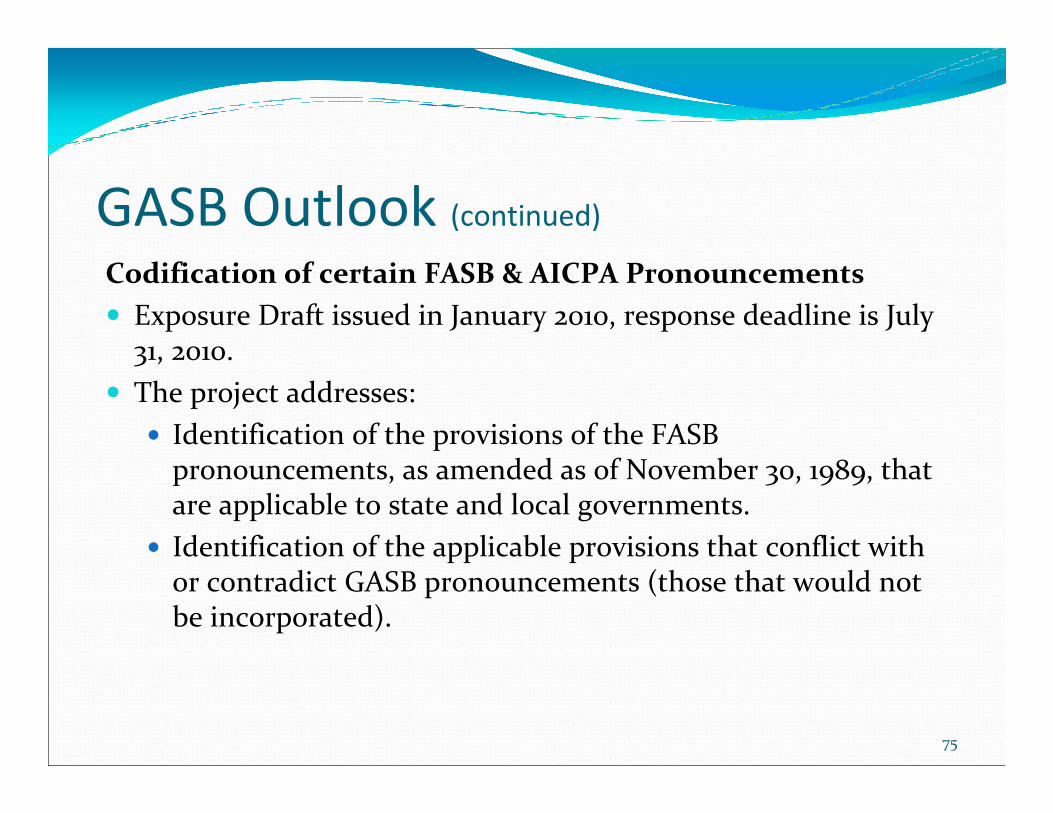

Codification of certain FASB & AICPA Pronouncements

� Exposure Draft issued in January 2010, response deadline is July31, 2010.

� The project addresses:

� Identification of the provisions of the FASB pronouncements, as amended as of November 30, 1989, that are applicable to state and local governments.

� Identification of the applicable provisions that conflict with or contradict GASB pronouncements (those that would not be incorporated).

75

GASB Outlook (continued)

Codification of certain FASB & AICPA Pronouncements (continued)

� The project addresses (continued):

� Which of the applicable provisions (that do not conflict with or contradict GASB pronouncements) should be:

� Adopted and incorporated into GASB pronouncements “as is.”

� Modified and incorporated into GASB pronouncements.

� Omitted from GASB pronouncements (for example, FASB Statement No. 31, Accounting for Tax Benefits Related to U.K. Tax Legislation concerning Stock Relief).

76

GASB Outlook (continued)

The Financial Reporting Entity, an amendment to GASB Statements No.14 and No.34 (Reporting Entity)

�Exposure Draft issued in March 2010, response deadline is July 31, 2010.

�For organizations that were previously included as a component unit based on meeting fiscal dependency criterion, it adds requirements that a financial benefit or burden relationship be present.

�Further defines the manner in which relationships are to be considered when determining to include an entity as component unit and when excluding them will be misleading.

�Also amends the blended presentation requirements.

77

GASB Outlook (continued)

Recognition and Measurement Attributes – Concepts Statement

�Will result in a concept statement and is currently being deliberated by the GASB.

�Develop recognition criteria for whether information should be reported in state and local government financial statements and when that information should be reported.

�Consider the measurement attribute(s)(for example, historical cost or fair value) that conceptually should be used for measurement.

78

Yellow Book Exposure Draft

Why expose the yellow book?

� Promote the modernization of auditing standards

� Streamline with standard setters

� Address issues GAO has observed

80

Summary of Changes

Realigned Chapters 1 and 2 � Along with the introduction, Chapter 1 now includes

the foundation and ethical principles of government

auditing

� The overall discussion on the use and application of

GAGAS is now in Chapter 2

81

Summary of Changes

Chapter 3� Independence

� Professional Judgment

� Continuing education

� Competence

� Quality Control and Assurance

82

Chapter 3 - Independence

The conceptual framework for independence requires that auditors:

1. Identify threats to independence

2. Evaluate the significance of the threats

identified

3. Apply safeguards, when necessary, to

eliminate the threats or reduce them to an

acceptable level

83

84

Assess condition or activity for threats to independence

Is threat significant? Proceed

Identify and apply appropriate safeguard(s)

Is threat eliminated or reduced to an acceptable level?

Potential independence impairment; do not proceed

YES

NO

YES

NO

Assess safeguard effectiveness

Assess threat for significance

Threat identified?NO

YES

Summary of Changes

Chapter 4� The chapters on financial audit performance

and reporting, formerly Chapters 4 and 5 respectively, have been combined into one chapter

Chapter 5� Clarified proper use of attest engagements

Chapters 6 and 7� Clarified obligation for reporting fraud

85

Timeline for the New Yellow Book

� August 2010: • Exposure Draft of 2011 Revision issued

� November 22, 2010:• Comments due on Exposure Draft

� February – March 2011:• Issue 2011 Revision of GAGAS

• Effective date to be determined

86

Internal Revenue Code: Subsection 3402(t)

� New tax code requiring that payments by governmental entities for goods or services after December 31, 2011, are subject to 3% income tax withholding, with some exceptions. Comment deadline June 30, 2010.

� Which Government Entities Are Required To Withhold:

1) The entire U.S. government, including all federal agencies, the executive branch, the legislative branch, and the judicial branch.

2) All states, including the District of Columbia (but not including Indian tribal governments).

3) All political subdivisions of a state government, or every instrumentality of such subdivisions, unless the instrumentalitymakes annual payments for property or services of less than $100million.

87

IRC: Subsection 3402(t) (continued)

� Generally :

Withholding is required on all payments to all persons providing property or services to the government, including individuals, trusts, estates, partnerships, associations, and corporations. Withholding is required at the time of payment, and applies to payment in any form (cash, check, credit card, orpayment card). If the government entity fails to withhold the tax required under section 3402(t), it becomes liable for the payment of the tax

88

IRC: Subsection 3402(t) (continued)

� Exceptions from the 3 % Withholding:

1) Payments otherwise subject to withholding, such as wages.

2) Payments for retirement benefits, unemployment compensation, or social security.

3) Payments subject to backup withholding, if the required backup withholding is actually performed.

4) Payments for real property.

5) Payment of interest.

6) Payments to other government entities, foreign governments, tax-exempt organizations, or Indian tribes.

89

IRC: Subsection 3402(t) (continued)

� Exceptions from the 3 % Withholding (continued):

7) Payments made under confidential or classified contracts, as described in IRC 6050M(e)(3).

8) Payments made by a political subdivision of a state, or instrumentalities of a political subdivision of a state that make annual payments for property of services of less than $100 million.

9) Public assistance payments made on the basis of need or income. However, assistance programs based solely on age, such as Medicare, are subject to the requirements.

90

Internal Revenue Code:

Subsection 3402(t) (continued)� Exceptions from the 3 % Withholding (continued):

10) Payments to employees in connection with service, such as retirement plan contributions, fringe benefits, and expense reimbursements under an accountable plan.

11) Payments received by nonresident aliens and foreign corporations.

12) Payments made by Indian tribal governments.

13) Payments in emergency or disaster situations.

91

IRC: Subsection 3402(t) (continued)

� Exception for small entities:

Subdivisions of a state, or instrumentalities of a subdivision of a state, are exempt from the withholding requirement if its total annual payments for property and services (not including wages) are less than $100 million. The proposed regulations provide a simple rule for determining whether an entity makes annual payments less than $100 million. In general, the entity looks to its accounting year ending with or within the second preceding calendar year. For example, if total payments for theentity’s 2010 accounting year exceed $100 million, the withholding requirement will apply in 2012.

92

GAQC Audit Resources � Archived member events (many of which we referred to in

this presentation) (www.aicpa.org/GAQC/Resources/)

� Archived Webcast - have your staff view at: (www.aicpa.org/GAQC/Resources/)

� Single Audit Practice Aids (www.aicpa.org/GAQC/Resources/)

� Illustrative Report Examples https://gaqc.aicpa.org/Resources/Illustrative+Auditors+Reports/

� Peer Review Checklists

(www.aicpa.org/GAQC/Resources/)

93

GAQC Audit Resources� Member discussion forum

� Links to other key organizations, news items, and documents

� Articles

� Member listing

� Membership Q&A

� Marketing toolkit

� Governmental event and conferences summary

94

Contact Information

Jeff Barbacci, Audit Partner/Director of AuditThomas Howell Ferguson P.A.

Al Altun, CFOWest Construction, Inc.

Address and Phone/Fax Numbers:2615 Centennial Boulevard, Suite 200

Tallahassee, FL 32308Phone: (850) 668-8100

Fax: (850) 668-8199

95