J.C. Penney Offers Big Upside Potential

14

J.C. Penney Offers Big Upside Potential

-

Upload

the-motley-fool -

Category

Business

-

view

6.506 -

download

1

Transcript of J.C. Penney Offers Big Upside Potential

J.C. Penney Offers Big Upside Potential

The thesis

J.C Penney (NYSE: JCP) has suffered from declining sales and compressing profit margins over the last several years.

However, performance is clearly improving in recent quarters.

When compared to more profitable competitors such as Macy's(NYSE: M) and Kohl's (NYSE: KSS), J.C. Penney still has plenty of room for improvement.

J.C. Penney will merit a considerably higher valuation if it continues on the right track.

The turnaround

“We completed the first two phases of our turnaround by strengthening our team, stabilizing the company operationally and financially, and by rebuilding parts of the business that were key to our long-term success. This year we have begun progressing through the go-forward phase and I am pleased to report we are making excellent progress. And I believe the results we announced today demonstrate that case.

During this phase, we are focused on refining our merchandising and marketing strategies and are to steadily grow sales and significantly improve gross margins while continuing to tighten and manage our expenses, all with an eye toward returning to profitable growth.”

--Mike Ullman, CEO

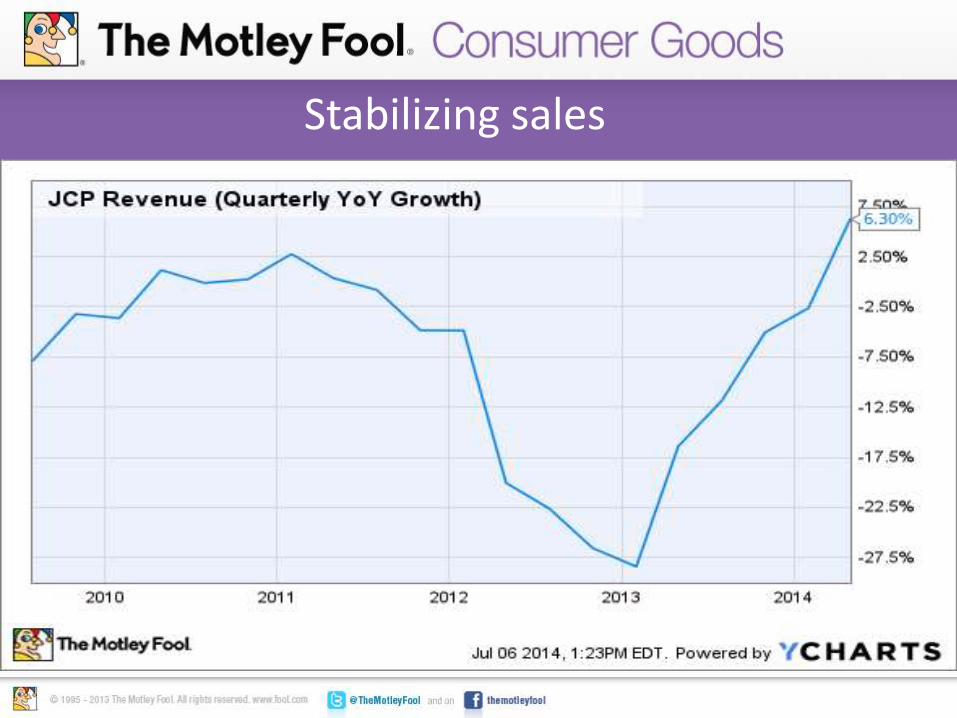

Stabilizing sales

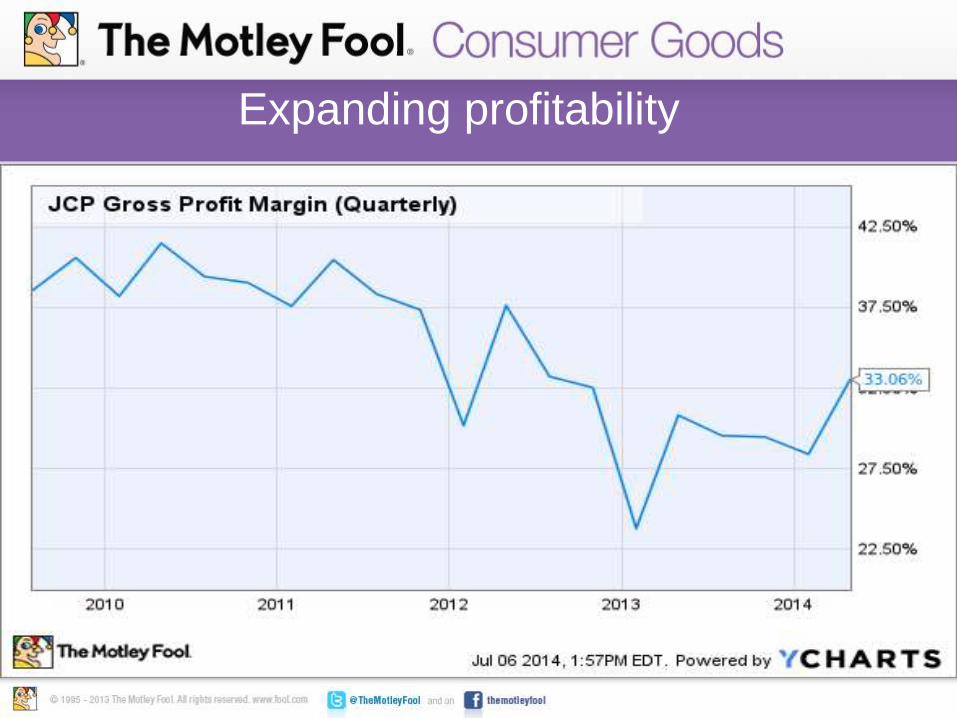

Expanding profitability

Optimistic guidance

Management expects comparable-store sales to increase in the mid-single digits during both the coming quarter and the full year in 2014.

Gross margin is forecast to “improve significantly” in 2014 versus 2013.

J.C. Penney expects to produce breakeven free cash flow in 2014.

Upside potential

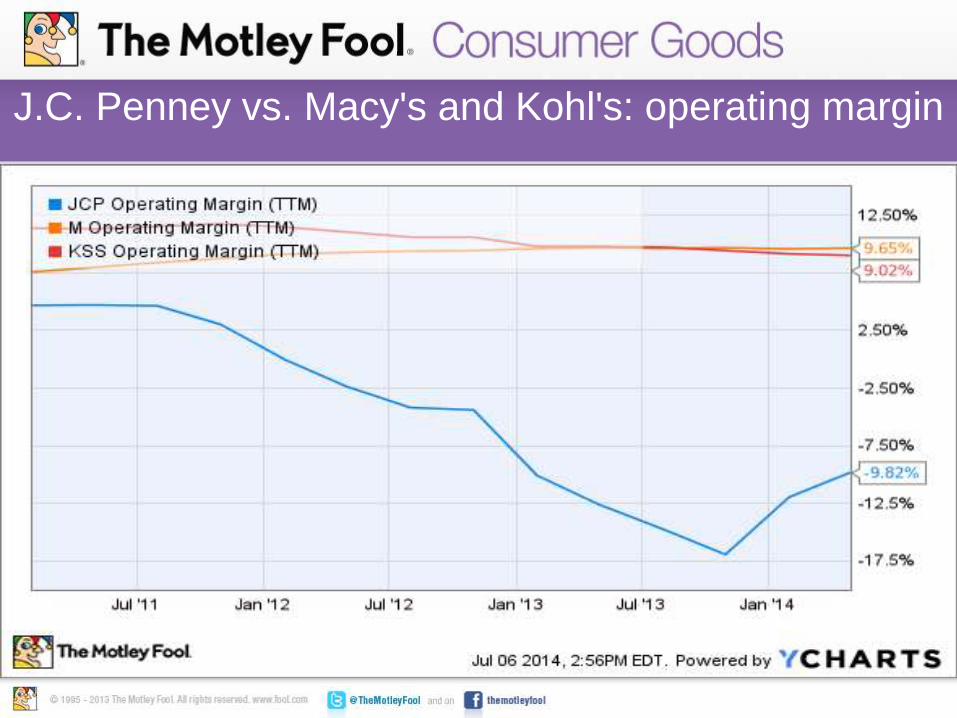

When compared to peers Macy's and Kohl's, J.C. Penney still has ample room for improving profitability.

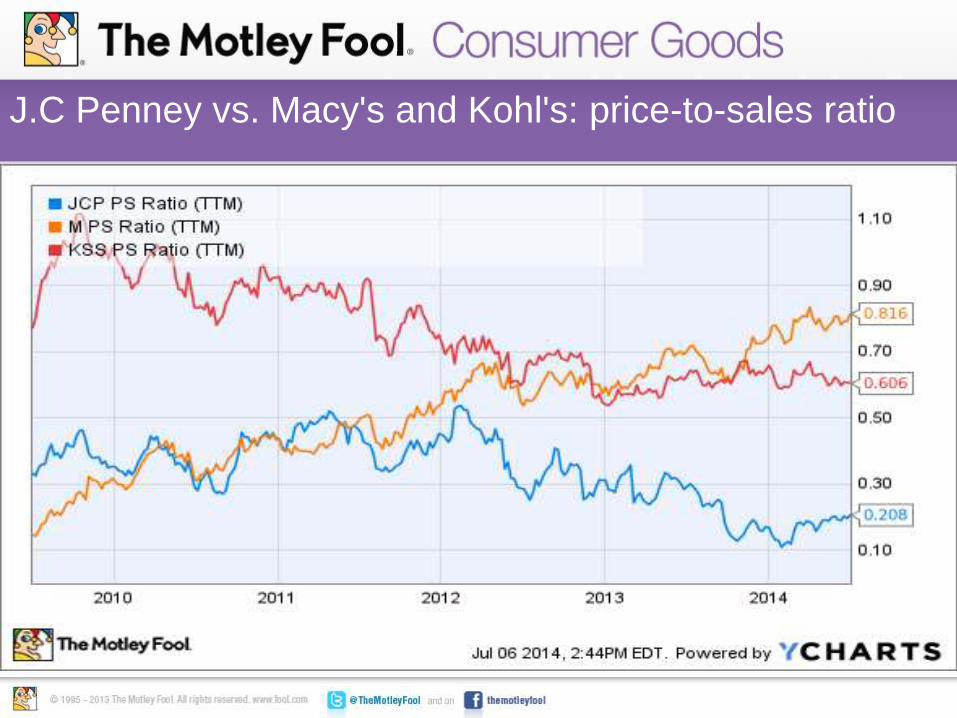

J.C. Penney is considerably cheaper than Macy's and Kohl's based on price-to-sales ratios.

Higher profit margins would deserve a considerably higher valuation for J.C. Penney.

Margin expansion opportunities

Better product selection should mean higher pricing power and reduced inventory clearance.Growing sales allow the company to leverage fixed costs on

a growing revenue base, generating opportunities for margin expansion beyond cost-cutting. Private brands such as St. John's Bay, Worthington,

Stafford, J. Ferrar, and Xersion are outperforming in terms of both sales and margins. A stronger financial position could mean lower financing

costs in the future. J.C. Penney has recently secured a new $2.35 billion credit facility, providing more flexibility and better terms than previous ones.

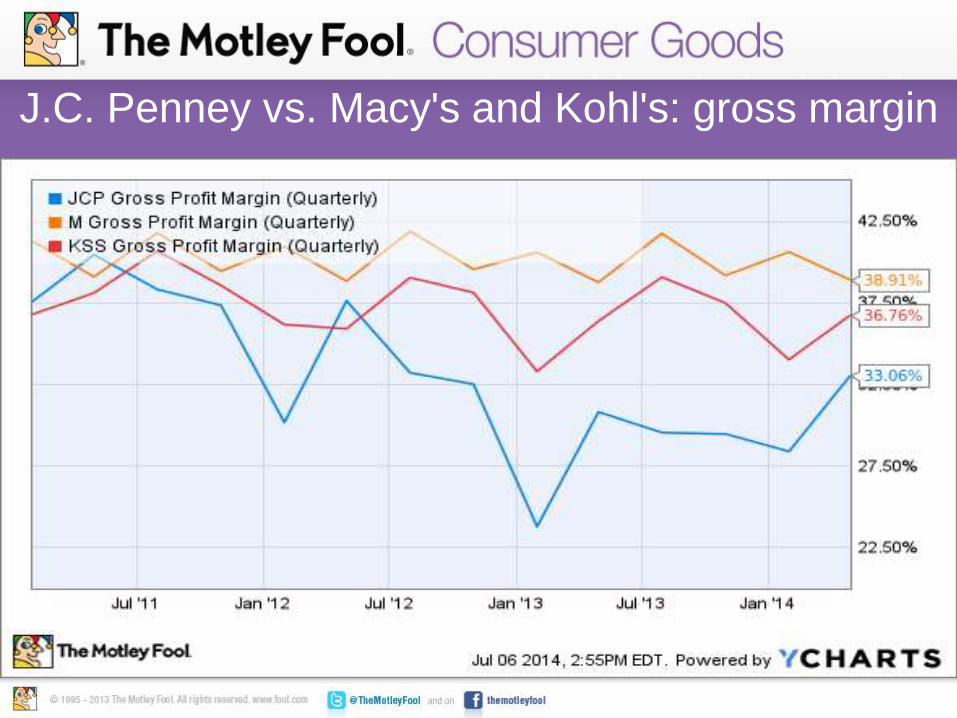

J.C. Penney vs. Macy's and Kohl's: gross margin

J.C. Penney vs. Macy's and Kohl's: operating margin

J.C Penney vs. Macy's and Kohl's: price-to-sales ratio

The risks

Turnarounds are always difficult, especially in such an aggressively competitive business as retail.

J.C. Penney is still losing money. The company is moving in the right direction, but it's not completely out of the woods yet.

A highly leveraged balance sheet leaves little room for mistakes.

Foolish takeaway

J.C. Penney is still a risky proposition for investors.

However, the company is making material improvements, and it offers substantial room for gains from a valuation point of view.

For investors with enough risk tolerance, the potential for gains may outweigh the risks.

This coming consumer device can change your financial futureImagine the multi-billion dollar sales potential behind a product that can revolutionize the way the world shops and interacts with its favorite brands every day. Now picture one small, under-the radar company at the epicenter of this revolution that makes this all possible. And its stock price has nearly an unlimited runway ahead for early, in-the-know investors. To be one of them and hop aboard this stock before it takes off, just access our free report below.