Infrastructure Solutions for Commercial Properties and Developers

January 2016

2

think about theENVIRONMENT

3

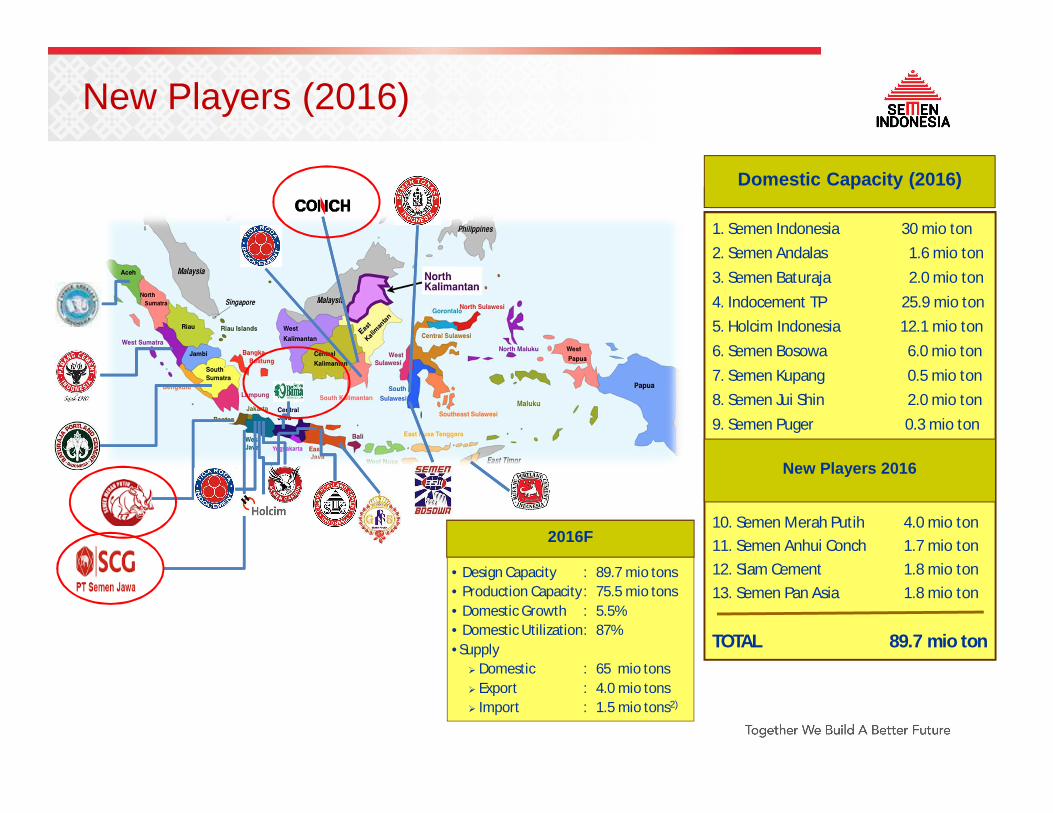

• Design Capacity : 89.7 mio tons• Production Capacity : 75.5 mio tons• Domestic Growth : 5.5%• Domestic Utilization: 87%•Supply Domestic : 65 mio tons Export : 4.0 mio tons Import : 1.5 mio tons2)

Domestic Capacity (2016)

2016F

New Players (2016)

1. Semen Indonesia 30 mio ton2. Semen Andalas 1.6 mio ton3. Semen Baturaja 2.0 mio ton4. Indocement TP 25.9 mio ton5. Holcim Indonesia 12.1 mio ton6. Semen Bosowa 6.0 mio ton7. Semen Kupang 0.5 mio ton8. Semen Jui Shin 2.0 mio ton9. Semen Puger 0.3 mio ton

10. Semen Merah Putih 4.0 mio ton11. Semen Anhui Conch 1.7 mio ton12. Siam Cement 1.8 mio ton13. Semen Pan Asia 1.8 mio ton

TOTAL 89.7 mio ton

New Players 2016

4

Supply and demand of Cement in the next 5 years

Ton

0

20

40

60

80

100

120

2014 2015 2016 2017 2018 2019

Gap Supply & Demand

Installed Capacity Production Capacity Growth 4% Growth 6% Growth 8%

5

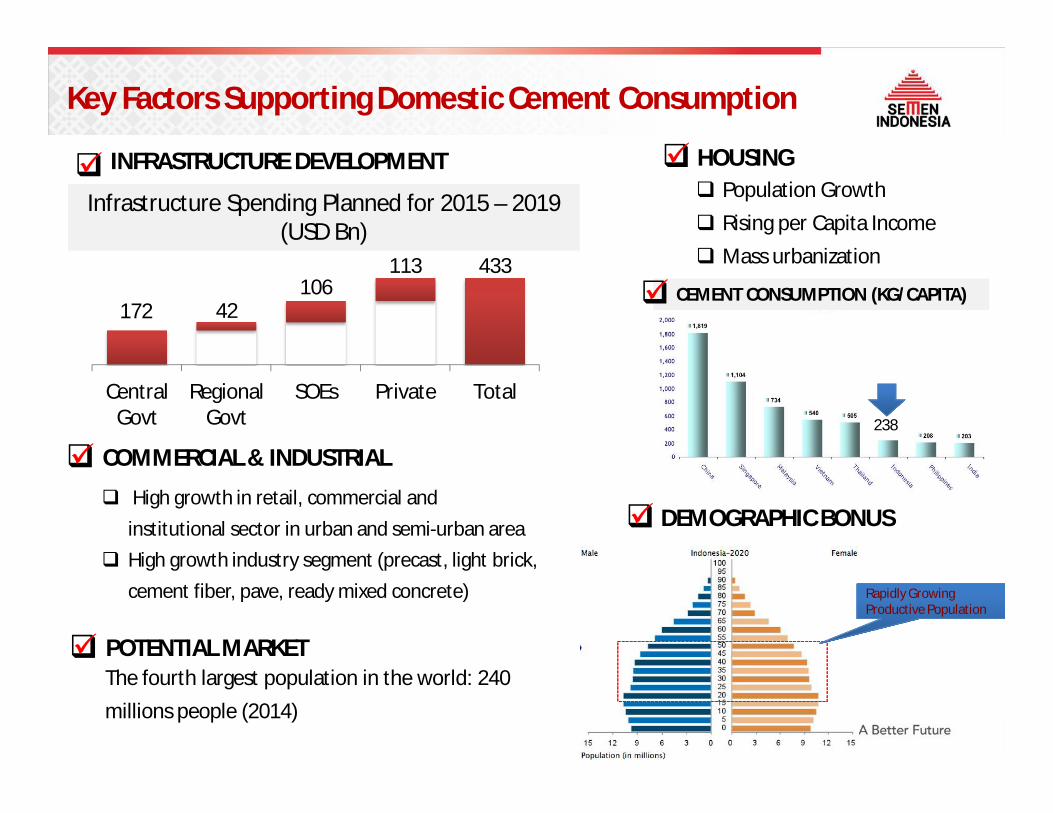

Infrastructure Spending Planned for 2015 – 2019 (USD Bn)

INFRASTRUCTURE DEVELOPMENT

COMMERCIAL & INDUSTRIAL High growth in retail, commercial and

institutional sector in urban and semi-urban area High growth industry segment (precast, light brick,

cement fiber, pave, ready mixed concrete)

HOUSING Population Growth Rising per Capita Income Mass urbanization

CEMENT CONSUMPTION (KG/CAPITA)

Rapidly Growing Productive Population

Key Factors Supporting Domestic Cement Consumption

172 42106

113 433

CentralGovt

RegionalGovt

SOEs Private Total238

POTENTIAL MARKETThe fourth largest population in the world: 240 millions people (2014)

DEMOGRAPHIC BONUS

6

Strategic Projects

These strategic projects are to ensure the Company’ position as the market leader.

Strategic Projects Capacity Investment(US$mn)

Construction

Start Completion

Indarung VI-Sumatera Barat

3.0 Mt

352 Q2-2013 Q3-2016

Rembang –Jawa Tengah

3.0Mt

403 Q2-2013 Q3-2016

Grinding millJawa Barat

2.0Mt

61.1 Q2-2015 Q3-2016

Waste Heat Recovery Power Generation

30.6 MW 49.3 Q4-2014 Q4-2016

MAIN STORAGE

PREHEATER AREA

INDARUNG PROJECT REMBANG PROJECT

MAIN STORAGE

PREHEATER AREA

RAW MILL AREARAW MILL AREA

Projects completed in 2015:• Packing Plant Pontianak

• Packing Plant Balikpapan

• Packing Plant Lampung

• Grinding Plant Dumai

• New Coal Mill Tonasa

7

Source: Company data, Indonesia Cement Association

Market update – recovery of demandSMGR sales volume (million tons)

11M15 11M14 Change (%)DomesticSemen Indonesia 12.8 12.8 (0.2) Semen Padang 5.8 6.1 (5.0) Semen Tonasa 4.9 4.9 0.1 Total domestic 23.5 23.9 (1.4) Export 0.45 0.20 128.4 Total volume 24.0 24.1 (0.3)

Domestic consumption (million tons)Area 11M15 11M14 Change (%)Jakarta 4.9 5.2 (7.3) Banten 3.0 2.9 3.4 West Java 8.2 8.1 0.8 Central Java 6.5 6.3 2.8 Yogyakarta 0.9 0.9 (5.1) East Java 7.4 7.3 1.6 Total Java 30.8 30.8 0.1 Sumatera 11.8 11.4 3.6 Kalimantan 3.7 4.1 (9.5) Sulawesi 4.3 4.1 5.1 Nusa Tenggara 3.2 3.1 4.0 Maluku & Papua 1.2 1.1 5.5 Total outside Java 24.2 23.7 1.8 Total Indonesia 55.0 54.5 0.8 Export Cement 0.53 0.22 140.8 Clinker 0.45 0.04 893.2 Total export 0.97 0.26 268.5 Grand total 56.0 54.8 2.1

SMGR sales type

mt mtBag 17.8 76% 18.1 76% -1.8% -0.6%Bulk 5.7 24% 5.6 24% 0.5% 0.6%

Industry sales type

mt mtBag 41.9 76% 42.7 78% -1.9% -2.2%Bulk 13.0 24% 11.7 22% 10.9% 2.2%

11M15 11M14 Change (%)

11M15 11M14 Change (%)

8

Source: Indonesian Cement Association & BPS Statistic

Long-term demand growth 7% pa

9

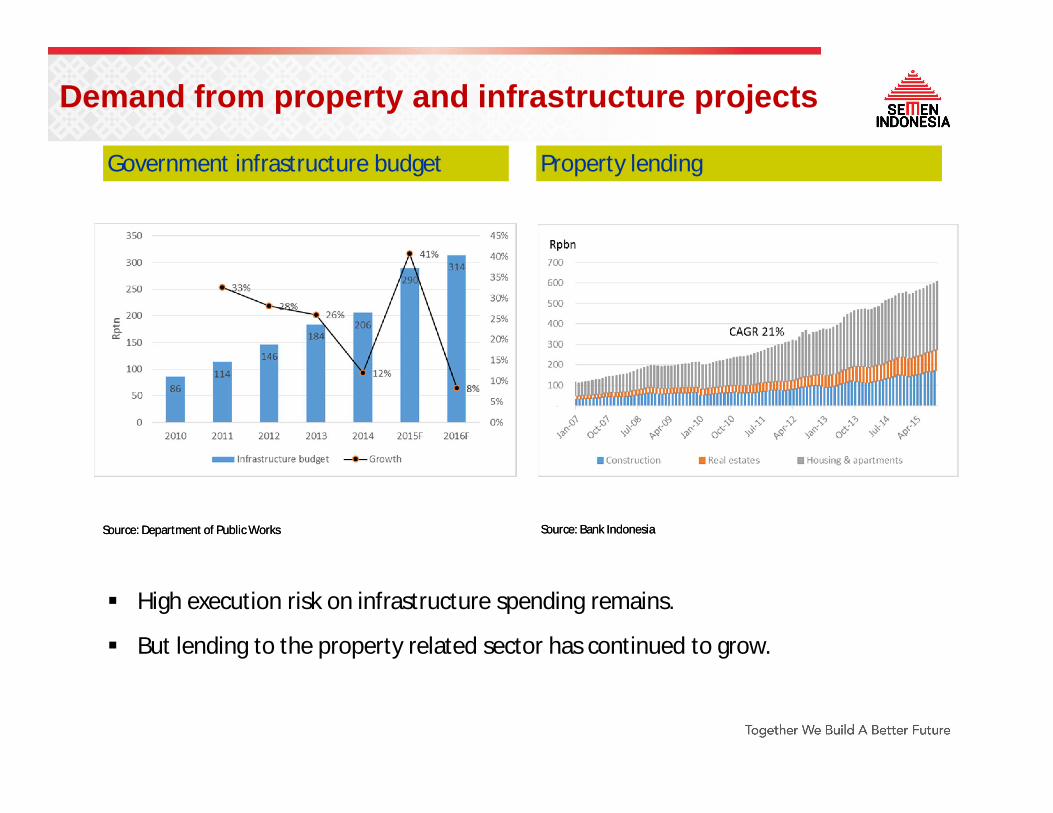

Demand from property and infrastructure projects

Source: Department of Public WorksSource: Department of Public Works

Government infrastructure budget Property lending

Source: Bank IndonesiaSource: Bank Indonesia

High execution risk on infrastructure spending remains.

But lending to the property related sector has continued to grow.

10

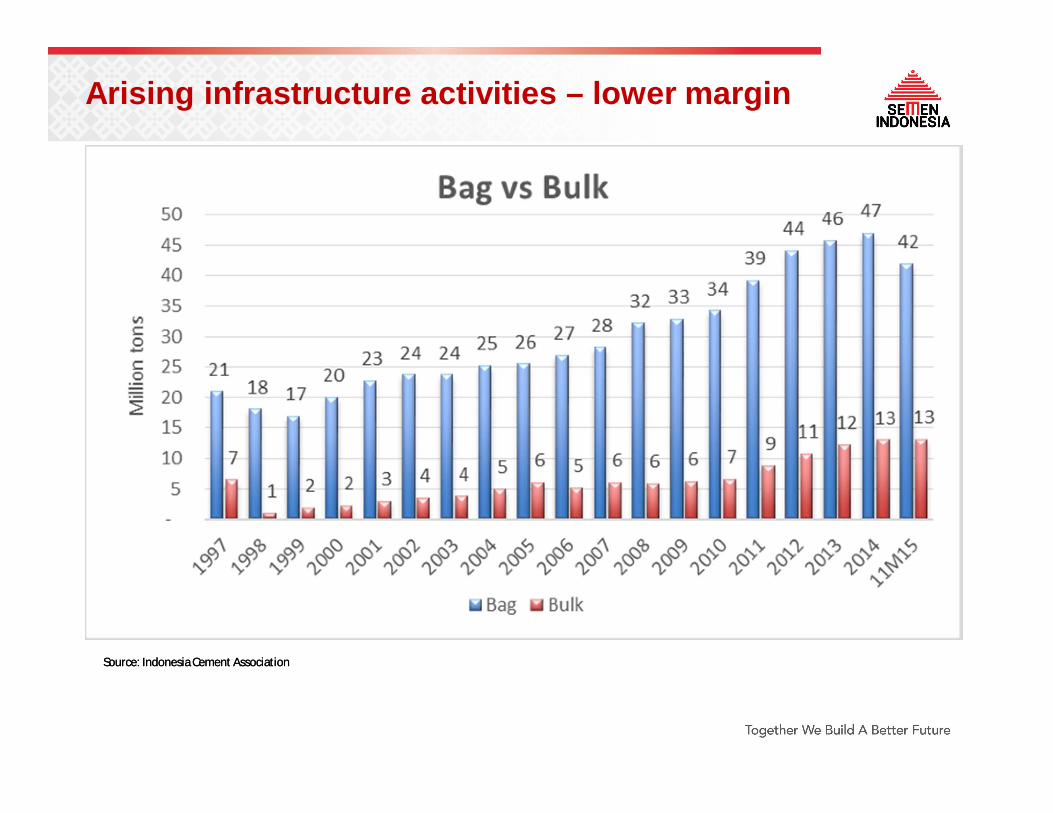

Arising infrastructure activities – lower margin

Source: Indonesia Cement AssociationSource: Indonesia Cement Association

11

Retail (residential) sector is the largest consumer of cement in Indonesia

Bag76.7%

Bulk23.3%

• Ready-mix (infrastructure):± 60%

• Fabricator (pre-cast, fiber cement, cement based industry):± 35%

• Projects (mortar, render):± 5%

• Ready-mix (infrastructure):± 60%

• Fabricator (pre-cast, fiber cement, cement based industry):± 35%

• Projects (mortar, render):± 5%

• Housing:± 90%

• Cement based industry:± 10%

• Housing:± 90%

• Cement based industry:± 10%

±

±

Source: Internal Research

Domestic market consumption

12

Papua

Bali & N T

Sulawesi

Kalimantan

Population Distribution (FY14)Population Distribution (FY14)

Sumatera21.3% Java

57.5.%

8.4%

5.8%

5.5% 1.5%

20.9%

6.6%9.1%

5.9% 2.2%

Java55.4%

Sumatera

Cement DistributionCement Distribution

Domestic Market Share

Market by Geography

SMGR INTP SMCB SMBR Bosowa Andalas Kupang MP JC

Java 40% 36% 18% - 2% - - 3% 2%

Sumatra 43% 11% 15% 12% 3% 14% - 2% 0%

Kalimantan 52% 28% 10% - 7% - - 3% 0%

Sulawesi 50% 10% 1% - 21% - - 17% -

Nusa Tenggara 37% 32% 6% - 14% - 7% 4% -

East Indonesia 57% 18% 1% - 24% - - - -

Total Indonesia 42% 27% 14% 3% 5% 3% 0% 4% 1%

Market share

13

We are the market leader

Source: Indonesia Cement AssociationSource: Indonesia Cement Association

Target markets Market share

Source: Indonesia Cement AssociationSource: Indonesia Cement Association

14

Export market opportunity

15

Financial Summary: 9M15 Results

*) Total debt calculated from interest bearing debt

In Rpbn 9M15 9M14 ChangeRevenue 19,115 19,349 -1.2%Cost revenue 11,602 10,898 6.5%Gross profit 7,513 8,451 -11.1%Operating expenses 3,352 3,242 3.4%Operating income 4,160 5,209 -20.1%EBITDA 5,211 6,138 -15.1%Pre-tax profit 4,102 5,193 -21.0%Net profit 3,198 4,077 -21.6%EPS (Rp) 539 687 -21.6%RatioEBITDA margin 27% 32% -4%Interest coverage - x 19 25 (6)Cost ratio 78% 73% 5%Net debt to equity 5% h2% 4%Debt to equity 16% 18% -2%Receivable turnover - days 52 45 7

16

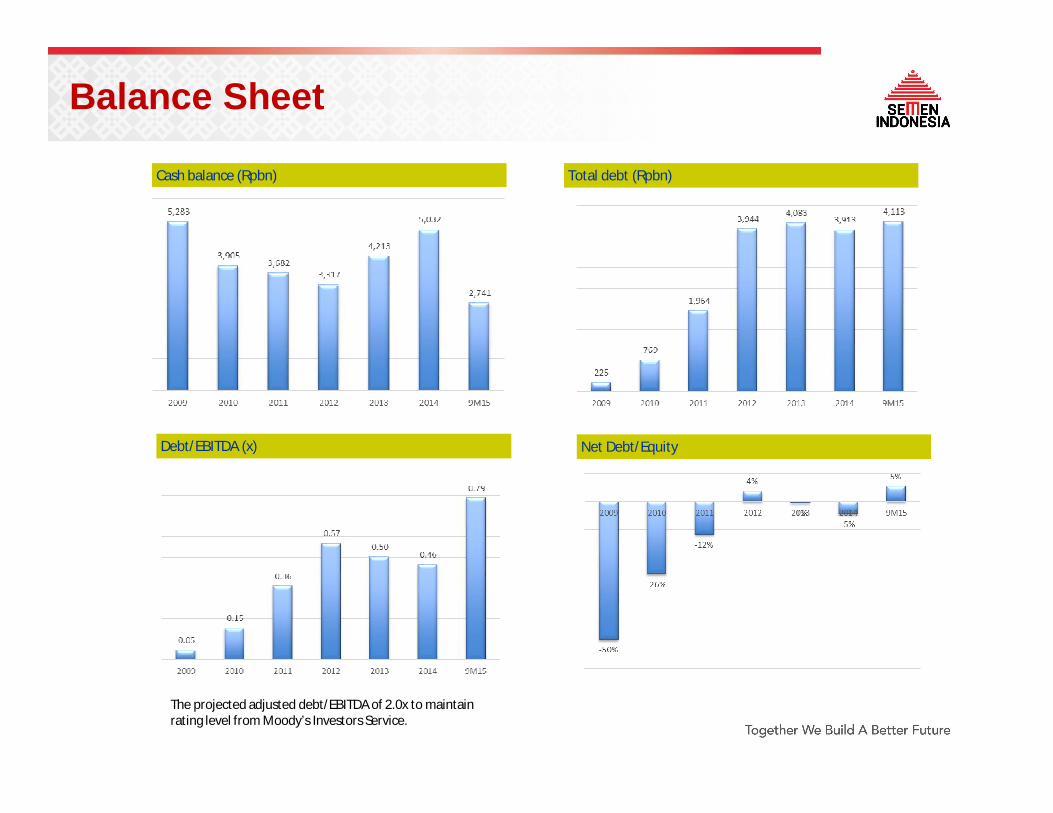

Balance Sheet

Cash balance (Rpbn) Total debt (Rpbn)

Debt/EBITDA (x) Net Debt/Equity

The projected adjusted debt/EBITDA of 2.0x to maintain rating level from Moody’s Investors Service.

17

Margin & Returns

Return on Equity (%) Return on Assets (%)

EBITDA/t (US$/t) Receivables Turnover (days)

The projected adjusted debt/EBITDA of 2.0x to maintain rating level from Moody’s Investors Service.

18

Cost structureRp000/t 9M15 9M14 ChangeRaw materials 37 30 22%Fuel 110 117 -6%Electricity 103 85 22%Labor 52 51 4%Maintenance 54 49 10%Packaging 27 36 -23%Trading 85 89 -5%Others 52 35 52%Cost of goods sold 523 491 6%Selling expense 93 96 -4%G&A 75 68 11%Total cost 591 550 7%Unit cost (US$/t)Cash COGS 39 40 -4%Total cash cost 51 53 -5%

Cash COGS in Rp000/t

Energy prices in US$/unit

19

think about theENVIRONMENT

20

Development New Industrial Estates is a catalyst for cement demand

Semen Indonesia Packing PlantNew Industrial Estate Area

21

Funding for the Government Infrastructure Development (2015 – 2019)

If 1% from total project value for roads, MRT, airport, seaport, housing ($206bn) spent to cement consumption, estimated cement consumption in the next 5 years around 26.8 Mio ton or 5.4 Mio ton per year)

22

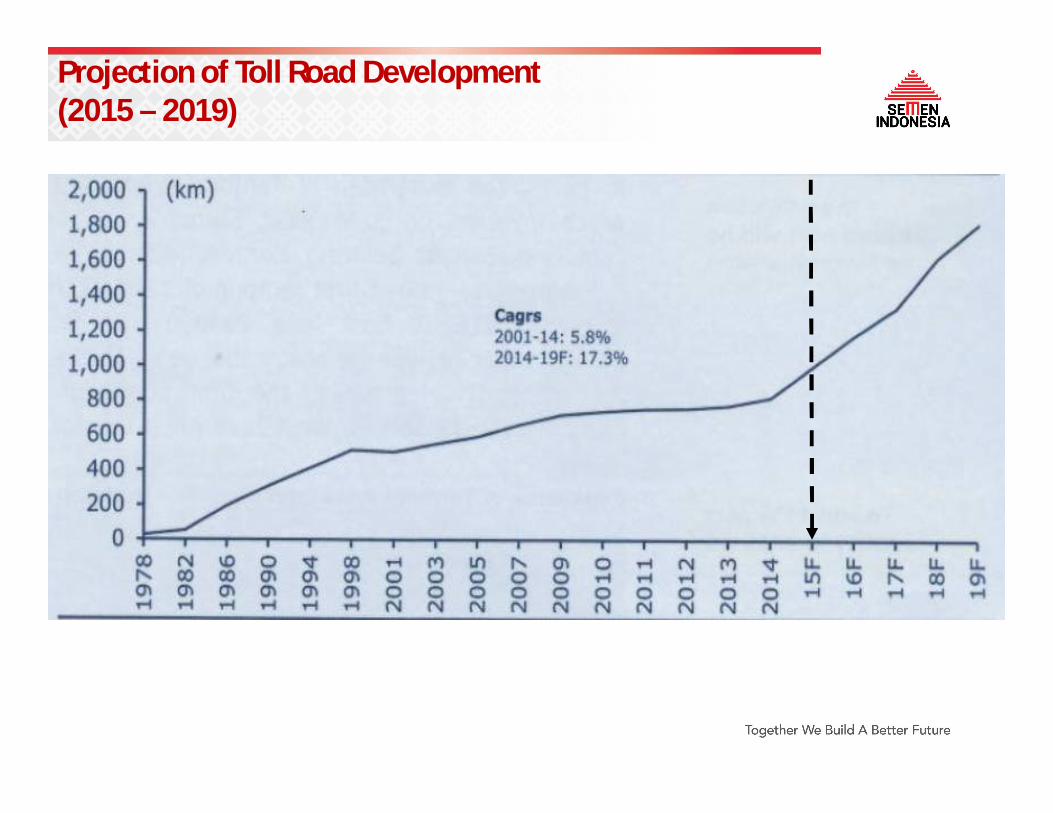

Projection of Toll Road Development (2015 – 2019)

23

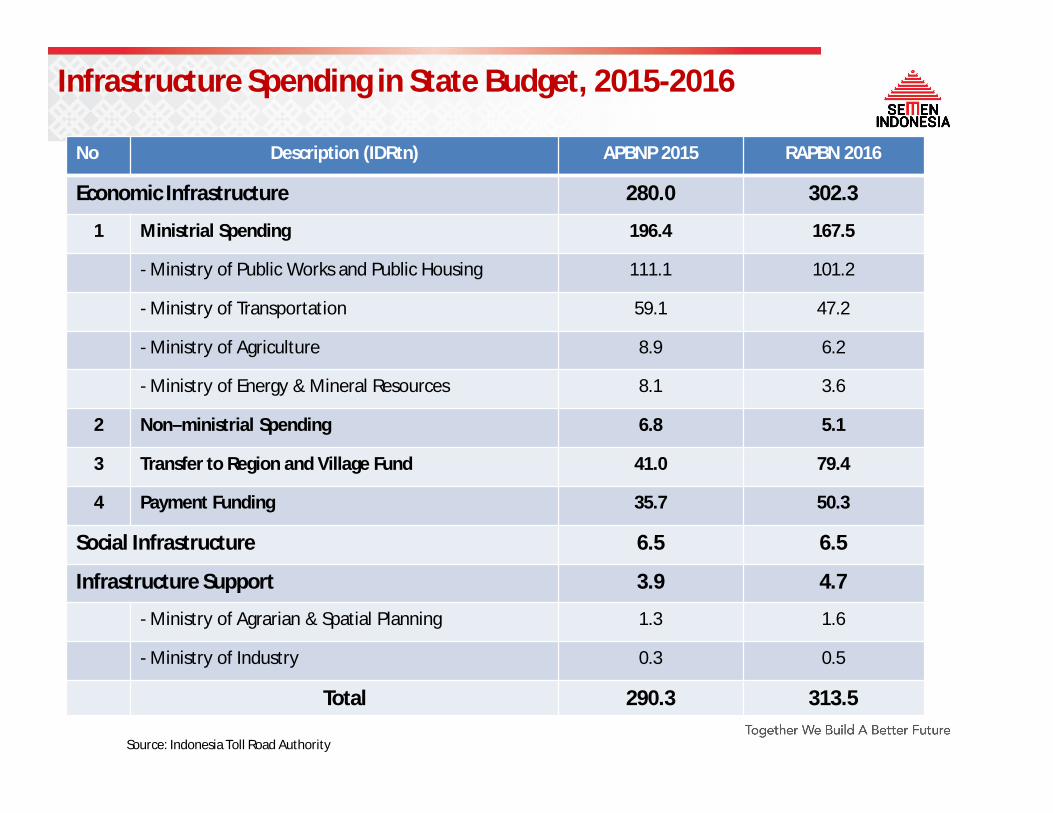

Infrastructure Spending in State Budget, 2015-2016

No Description (IDRtn) APBNP 2015 RAPBN 2016

Economic Infrastructure 280.0 302.3

1 Ministrial Spending 196.4 167.5

- Ministry of Public Works and Public Housing 111.1 101.2

- Ministry of Transportation 59.1 47.2

- Ministry of Agriculture 8.9 6.2

- Ministry of Energy & Mineral Resources 8.1 3.6

2 Non–ministrial Spending 6.8 5.1

3 Transfer to Region and Village Fund 41.0 79.4

4 Payment Funding 35.7 50.3

Social Infrastructure 6.5 6.5

Infrastructure Support 3.9 4.7

- Ministry of Agrarian & Spatial Planning 1.3 1.6

- Ministry of Industry 0.3 0.5

Total 290.3 313.5

Source: Indonesia Toll Road Authority

24

think about theENVIRONMENT

25

BRIEF HISTORYBRIEF HISTORY SMGR CAPACITY BUILD-OUT (MM TONS)SMGR CAPACITY BUILD-OUT (MM TONS)31,8 mn tons

Semen Indonesia highlights

1957 : Inauguration of Gresik I, installed capacity of250,000 ton cement per annum

1991 : Initial Public Offering, Market Cap.: IDR0.63tn,resulting shareholding structure post IPO:

●Government of Republic of Indonesia: 73%●Public: 27%

1995 : Acquisition of PT Semen Padang (Persero) andPT Semen Tonasa (Persero)

1998 : Cemex became a strategic partner, Market Cap.:IDR4.9tn

2006 : Blue Valley Holdings bought Cemex’s 24.9%stake in SMGR, Market Cap.: IDR21.5tn

2010 : In March 31, Blue Valley Holdings sold all of itsstake ownership in SMGR, Market Cap per April 30,2010: IDR72.1tn

2011 : Total installed capacity of 20.00mm tons, MarketCap per June 29, 2012: IDR67.0tn

2012 : Acquisition of Thang Long Cement Vietnam, Totalinstalled capacity of 2.3mm tons, Market Cap Dec 19th,2012: IDR91.9tn

2013: Transformed to PT Semen Indonesia (Persero)Tbk as strategic holding co.

0,0

5,0

10,0

15,0

20,0

25,0

30,0

35,0

1957

1970

1980

1984

1985

1986

1990

1995

1997

1998

2006

2007

2008

2009

2010

2011

2012

2013

2014

26

Semen Indonesia as strategic holding company

99,9% 99,9% 70,0%55,0%

SP ST TLCCPT United Tractors Semen Gresik

97,0%PT SGG Energi Prima

60,0% PT Industri KemasanSemen Gresik

65,0% PT Kawasan IndustriGresik

99,99% PT SGG Prima Beton

24,95% PT Varia Usaha

25% PT Swadaya Graha

17,6%

99,9%

SG

NO

N C

EMEN

T CO

MPA

NY

50,0%PT Krakatau SemenIndonesia

CEMENT COMPANY

Komposisi Pemegang Saham Per 31 Desember 2014

85%

PT Eternit Gresik

PT SISI

No Shareholders %

1 Government RI 51.01

2 Foreign Institution 38.59

3 Foreign Individual 0.01

4 Domestic Institution 9.73

5 Domestic Individual 0.67

27

Regional market

Kiln 1 unit

Cement Mill 1 unit

Kiln 4 unit

Cement Mill 9 unit

Grinding Plant

1 unit Cement Mill

Kiln 4 unit

Cement Mill 6 unit

Grinding Plant

3 unit Cement Mill

Kiln 4 unit

Cement Mill 6 unit

25 lokasi

28

Main Office:Main Building of Semen Gresik

Jln. Veteran Gresik 61122 – IndonesiaPhone: (62-31) 3981731 -2, 3981745

Fax: (62-31) 3983209, 3972264

Representative Office:The East Building, 18 floorJl. Lingkar Mega Kuningan Blok E 3.2 No. 1,JAKARTA – 12950Telp.: 021 – 5261174, 5261175; Faks : 021 – 5261176

www.semenindonesia.com