January, 2014 frá Avrit - Kringvarp Føroya

23

1 Samherji hf. Transfer Pricing Report Headquarter Services January, 2014 Strictly Private and Confidential This draft is for factual confirmation and discussion purposes only This document contains commercially sensitive information and is strictly for the use of Samherji hf. and readers nominated by them Avrit frá kvf.fo

Transcript of January, 2014 frá Avrit - Kringvarp Føroya

1

Samherji hf.

Transfer Pricing Report

Headquarter Services

January, 2014

Strictly Private and Confidential

This draft is for factual confirmation

and discussion purposes only

This document contains commercially

sensitive information and is strictly for

the use of Samherji hf. and

readers nominated by them

Avrit

frá k

vf.fo

2

Contents

Index

1 Objective and scope ____________________________________________4

2 Glossary _____________________________________________________5

3 Introduction __________________________________________________6

3.1 Corporate background ______________________________________________ 6

3.2 Summary supply chain _____________________________________________ 7

3.3 Contractual terms _________________________________________________ 7

4 Functional Analysis _____________________________________________7

4.1 CEO ____________________________________________________________ 8

4.2 Legal advisor ____________________________________________________ 10

4.3 CFO ___________________________________________________________ 10

4.4 CAO ___________________________________________________________ 11

4.5 Business development _____________________________________________ 11

4.6 Risks __________________________________________________________ 12

4.7 Analysis of assets used ____________________________________________ 12

4.8 Characterization of Samherji hf. ___________________________________ 1312

5 Selection of transfer pricing method _______________________________ 14

6 OECD Transfer Pricing Guidelines for Services ________________________ 15

6.1 Introduction ____________________________________________________ 15

6.2 Benefit test _____________________________________________________ 15

6.3 Shareholder activities and costs _____________________________________ 15

6.4 Duplication _____________________________________________________ 16

6.5 Determine the level of the service charge ______________________________ 16

7 Service charge models ________________________________________ 1617

7.1 Direct charge model ______________________________________________ 17

7.2 Indirect charge model _____________________________________________ 17

7.3 Mixed model ____________________________________________________ 17

8 Transfer Pricing Policy __________________________________________ 18

8.1 Key characteristics _______________________________________________ 18

8.2 Considerations in relation to the cost base _____________________________ 18

8.3 Service charge model _____________________________________________ 18

Avrit

frá k

vf.fo

3

8.4 Allocation keys __________________________________________________ 19

8.5 Group Benefits __________________________________________________ 19

8.6 Transfer Pricing Model _____________________________________________ 21

9 Appendices (Service agreements) _________________________________ 23

Avrit

frá k

vf.fo

4

1 Objective and scope

Samherji hf. engaged KPMG ehf. and KPMG Meijburg & Co (hereafter jointly referred to as: “KPMG”) to assist in documenting its transfer pricing policies for intragroup services rendered by Samherji hf. to group companies.

This transfer pricing memorandum pertains to the following:

Objective Transfer pricing documentation file for Samherji hf. substantiating the transfer pricing methodology in relation to the intercompany transaction specified below

Scope Transaction subject to documentation: service relationship between Samherji hf. and group members

Regulations considered OECD Transfer Pricing Guidelines and guidance issues by EU Joint Transfer Pricing Forum (EJTPF)

Information considered This document is based on the facts and circumstances as provided by Samherji hf. in the period November-December 2013

KPMG’s conclusions are based on the completeness and accuracy of the information supplied by Samherji Group and on the assumptions stated in this memorandum. KPMG has relied on information supplied by and obtained through interviews with Samherji Group without audit or verification. Should any of the facts or assumptions be inaccurate of incomplete, it is imperative that KPMG will be informed immediately as inaccurate or incomplete information could materially affect the conclusion presented herein.

Avrit

frá k

vf.fo

5

2 Glossary

The table below includes information on abbreviations used in this report.

CUP Comparable Uncontrolled Price Method

CPLM Cost Plus Method

ERP Enterprise Resource Planning

EUR Euro

FTE Full Time Equivalent

HSE Health, Safety & Environment

ISK Icelandic Krona

OECD Guidelines Transfer Pricing Guidelines of the Organization for Economic Co-operation and Development, 22 July 2010

PSM Transactional Profit Split Method

RPM Resale Price Method

TNMM Transactional Net Margin Method

Avrit

frá k

vf.fo

6

3 Introduction

3.1 Corporate background

The Samherji Group (hereinafter referred to as: “Samherji”) is one of the largest companies in the Icelandic fish industry. The company engages in operating freezer trawlers, purse seiners as well as land based factories in Iceland for white fish and farmed fish. Samherji’s value chain is vertically integrated and Samherji exports its own produce under the "Ice Fresh Seafood" brand. The turnover of Samherji is almost equally divided between fishing and processing. Samherji holds shares in several Icelandic Companies in the seafood industry.

Operating in a system of resource management where the aim is sustainable fishing, Samherji, founded in 1983, is a leading seafood company in Iceland. Outside Iceland, Samherji has or takes part in operations in Germany, Poland, U.K., the Faroe Islands, Africa, Canada, France and Spain. Samherji is a vertically integrated seafood company, controlling a significant volume of fishing quota, operating a powerful fleet of fishing vessels; freezer and fresh fish trawlers, as well as multipurpose vessels, white fish factories and fish farming. Samherji also runs extensive sales and marketing operations which are coordinated at the company´s head office.

Samherji’s success is primarily based on the fact that as a food producer the company itself takes care of the entire process from the catch to the market. Samherji employs qualified and enterprising personnel and management, has a powerful fleet, large fishing quotas and highly advanced onshore plants. Equipped in this manner, the company aims at a continuing leading position in the fishing industry, both in Iceland and at international level.

The strong position of Samherji together with knowledge, experience and strong quota ownership in all species ensures that the company can minimize risks and ensure stability. The quota is owned by a Samherji group companies and not by Samherji hf.

Samherji group runs two large and very advanced whitefish plants, one in Dalvik and Útgerdarfelag Akureyringa in Akureyri (Iceland). The plants produce wide variety of fresh and frozen fish products as well as dried fish.

Segments

It can be said that the group is divided into the following five geographical segments:

1. Iceland (Faroe Island)

2. U.K.

3. Germany (Poland)

4. Cyprus (Africa)

5. Canada (independent)

An overview of the Samherji Group's legal structure as per December, 1, 2013 is attached to this report in appendix A.

Kommenterede [F1]: Er Samherjasamstæðan eitt stærsta

fyrirtækið?

Kommenterede [F2]: Kýpur? Lettland?

Kommenterede [F3]: Er vinna Seagold, Mercury, Icefresh Ltd.

O.fl. öll ákveðin í höfuðstöðvum Samherja á Akureyri???

Kommenterede [F4]: Athugasemdir í hinu skjal

Avrit

frá k

vf.fo

7

3.2 Summary supply chain

3.3 Contractual terms

See annex.

4 Functional Analysis

This section discusses a functional overview and description of most of the activities performed by Samherji hf. The organizational structure of the Samherji Group as per December 2013 is depicted below:

Transactions under review:

Fishing company

Fish processing / Sales Company

Sales Company

Customers:Carrefour

Marks & Spencer Sainsburys

3d party Fishing company

Samherji hf. Head office

Quota

Service

Fish

FishProcessed

Fish

ProcessedFish

Kommenterede [F5]: Alrangt

-Guadalupe og Brynjar ekki hluti

-SÓ hættur – en hefur AH í raun ekki tekið við hans hlutverki sem

BD?

-AB vantar

-IJ er ekki undir Samherja og er ekki CAO

-Er Gústaf í vinnu hjá Grúppunni en ekki Kristján Vilhelms?

Avrit

frá k

vf.fo

8

The following persons employed by Samherji hf. are rendering services to group companies: - ); - Sigursteinn Ingvarsson (CFO); - Sigurður Ólafsson (Business Development Director); - Ingvar Juliusson (CAO); - Arna Bryndís (legal).

The other persons showed on the organizational structure are not employed by the head office directly and are not rendering management services to group companies.

4.1 CEO

4.1.1 Functional overview

The Chief Executive Officer (CEO) of Samherji hf. is ultimately responsible for the strategy and results of the Samherji Group. The CEO formally reports to the shareholders of the Group. The CEO is the only Managing Director of the Samherji Group. There is no formal Management Team within Samherji hf., however the CEO is supported by the CFO, CAO, CC, a business development officer and a personal assistant. 4.1.2 Description of the activities of the CEO

The CEO is involved in a broad range of general management activities and deals with several strategic and operational issues (fishing strategy / selecting key management / key decisions regarding business operations). The CEO determines the Group's direction regarding entering new markets and business developments. He also makes the decisions regarding significant investments. Furthermore, the CEO is

Þorsteinn Már Baldvinsson

CEO

Canada

only shareholder interest

Kristján Vilhelmsson

(Fishery officer)

Gestur Geirsson (CEO landvinnsla)

Jón Kjartan (farmed fish)

Iceland

Aðalsteinn Helgson (CEO)

Brynjar Þórsson (CFO)

Guadalupe Bengoechea (Spanish)

Cyprus

SpainAfrica

Haralduur Grétarsson (CEO)

Germany and Onward FC

Support functions:

Sigursteinn (CFO)

Sigurður Óli (BD)

Ingvar Júlíusson (CAO)

Gústaf Baldvinsson

Marketing and Sale UK/Iceland

Sigmundur Andrésson (CEO)

Icefresh GmbH

Kommenterede [F6]: Þessi setning er rugl!

Kommenterede [F9]: Hér þarf að vera alveg á hreinu skilin milli

erlendu dótturfélaganna og Íslands. Erfitt að pikka út annars.

Kommenterede [F10]: Á þetta við um samstæðuna alla?

Kommenterede [F11]: Í lagi erlendis

Kommenterede [F12]: Ekki í lagi erlendis

Kommenterede [F13]: Vafasamt ef þetta á líka við um

erlendu dótturfélögin (þetta fellur líklega allt undir operational

issues og er því ekki í lagi)

Avrit

frá k

vf.fo

9

involved in negotiations with third parties in case of acquisitions and potential strategic partnerships and handles certain press related matters. In brief, the activities performed by the CEO of the Samherji Group can be summarized as follows:

• General management (stakeholder management / corporate communication / business reviews) ;

• Strategy management / development ( major investment decisions);

• Fishing strategy;

• Selecting key persons (management / captains).

The CEO performs the general management of the Samherji Group and meets with shareholders as well as the most important customers. All strategic decisions need to be approved and are usually initiated by the CEO himself, for example: acquisitions, investments in new vessels, investments in new plants etc. Setting up activities in other counties is also been done upon the initiative or at least the approval of the CEO. The local companies deal with quotas themselves, due to the characteristics of quota it can only be dealt with beneficially on company level. Furthermore the CEO is board member of a number of group companies. The CEO manages on a day-to-day basis the so-called fishing strategy. He stays in contact with the market and sales company that provides input on market prices and market developments. Based on this information, the CEO sets out the fishing strategy and instructs the management of the fishing companies as well as the plant managers. This is among others the approval of the fishing-plans (financial budget including fish plan), as well as the management of the vessels strategy (where and how to fish) and the fishing strategy in combination with the relevant fishing plants. As the whole group owns a significant amount of quota in different fishing companies, the fishing strategy (where to fish and how to fish) is a key value driver of the Group. The CEO stays in contact with the marketing and sales companies and sets out the fishing strategy in order to sell the fish for the best price while making and making efficient use of the different vessels, quota as well as plants.

For example it can be decided to close down a specific production operation for a certain period and use a fishing vessel that is also capable of processing at sea. Or a decision not to use a certain quota up to the moment the market price is the highest, but use the relevant vessel in other areas at that time or even not using the vessel. The available quota, fishing vessels, plants etc. is therefore used in the most efficient way. This reduces operating cost and avoids idle time of the vessels.

Furthermore, in order to be successful as a fishing company this size of key management is important as decisions can be taken quickly. Even more, the CEO stays in contact with the key management on a day to day basis to determine the fishing strategy. Key management includes the captains of the fishing vessels, which are very important for being a successful fishing company. Every captain and key manager is selected by the CEO himself. It should be noted that the head office does not manage other HR activities, this is taken care of on a company level. The CEO provides:

• talent scouting and talent management;

• strengthen compliance (developing code of conduct; arranging rollout & training);

• advisory in the field of HR.

Finally, the CEO is supported directly by its own personal assistant / secretary.

4.2 Legal advisor

The legal advisor started at Samherji hf. in 2013. The legal advisor formally reports to the Group's CEO depending on the activities the Legal Advisor will also work closely with

Kommenterede [F14]: Vafasamt ef þetta á líka við um

dótturfélögin, mjög spes varðandi skipstjórana.

Kommenterede [F15]: ATH

Kommenterede [F16]: ATH

Kommenterede [F17]: Er það ekki óþarfi?

Kommenterede [F18]: ATH

Kommenterede [F19]: ATH

Kommenterede [F20]: Á kvóta í mismunandi skúffum og ÞMB

velur svo og ákveður hvað skal gera??

Kommenterede [F21]: Taka út

Kommenterede [F22]: Hvaða key management??? Ekki talað

um það fyrir ofan?

Kommenterede [F23]: Gengur ekki. Velur ÞMB skipstjórana

sem gera svo samning við fyrirtæki sem aðrir eiga að stjórna? Jafnvel

fyrirtæki mjög neðarlega í strúktúrnum?!

Kommenterede [F24]: Er ÞMB

mannauðsstjóri/starfsmannastjóri eða er Anna María það? Avrit

frá k

vf.fo

10

other key management persons within the group. The legal advisor will be engaged in in-house legal advice, legal control matters and coordination of legal services and board meetings within the Samherji Group. Most of the activities conducted by the legal advisor will be performed on an ad-hoc basis. The activities can be summarized as follows:

• Board Coordinator in board meetings in Samherji Group companies;

• Legal control activities;

• Legal aspects regarding the fishing vessels and its crew of the group companies;

• Legal assistance to Samherji Group companies.

• Identify, analyses and advise on law developments;

• Responsible for ensuring global and regional compliance with (inter)national laws, rules and legislations;

• Ensure compliance with national standards, laws and regulations

• Provide support in case of disputes, claims and arbitrations;

• Ensure legal risks are identified and an appropriate course of action is taken;

• Review legal contracts and assess legal implications requiring attention.

• Investigate and monitor accidents and severe incidents with recommendations and action plans;

•

4.3 CFO

4.3.1 Functional overview

The chief financial officer (CFO) manages the financial aspects on a group level as well on a day to day financial management of Icelandic operations of the Samherji Group. As a result of the decentralized organization of the Samherji Group, every group company has its own manager that deals with controlling and accounting, except for treasury management. Every local finance manager however reports budgets as well as the financial results of the group companies for consolidation purposes to the CFO. The CFO subsequently reports to the CEO.

4.3.2 Description of activities of the CFO

The activities performed by the CFO of Samherji hf. can be summarized as:

• Board meetings and other shareholder related issues;

• Controlling and Reporting;

• Financing and cash management;

• Business reviews and budget process;

• Financial aspects of special projects. The CFO manages on a day-to-day basis all finance matters of the Icelandic operations. The foreign group companies report to the CFO for financial reporting and consolidation purposes. An active role of the CFO for these foreign group companies relates to the review of the financial budgets and finance management. Besides that the CFO provides the relevant finance managers of group companies with advice upon request. The CFO performs among others the following services:

• Arrange bank guarantee facility and related negotiations;

• Review requests for bank guarantees by local group members;

• Review forecasts (e.g. cash flow planning; currency forecast (in development); guarantee forecast);

Kommenterede [F25]: Ath. er í lagi að SI sjái um fjárstýringu

einstakra dótturfélaga?

Avrit

frá k

vf.fo

11

• Negotiation of financial facilities with relevant financial institutions;

• Concluding financial facilities with relevant financial institutions;

• Managing guarantees and securities for financial facilities;

• Review requests for funding by group members, analyze funding needs, assess creditworthiness;

• Advising on funding position;

• Advising on adequate liquidity management (e.g. redemption).

4.4 CAO

4.4.1 Functional overview

The chief accounting officer (CAO) reports directly to the CEO of Samherji hf. He is responsible for overseeing the group´s accounting operations and tax planning and . He works closely with the CFO on developing financial strategies. He is accountable to auditors and financial regulators along with the CFO. Maintaining accurate and detailed financial records is a critical part of his responsibilities. . 4.4.2 Description of the activities of the CAO

The CAO is involved in all the tax aspects of the group, whether it is relates to withholding tax, intercompany The CAO is involved in all the tax aspects of the group, whether it is relates to withholding tax, intercompany The CAO is involved in all the tax aspects of the group, whether it is relates to withholding tax, intercompany The CAO is involved in all the tax aspects of the group, whether it is relates to withholding tax, intercompany

• developing and implementing tax planning strategies for group companies to minimize the effective tax rate whilst being compliant and to limit risks;

• ensure global and regional compliance with (inter)national tax laws, rules and legislations;

• drive and conduct proper risk-management from a tax perspective across the organization; and

• Business development

Business development The Group Business Development Director (Business Analyst) reports directly to the CEO. The Director analyses geographic extending of Samherji’s operations in every business aspect of the group (fishing, farms, processing factories, cold storage etc.). The approval of such an extension/investments is taken by the CEO and local board of directors in close operation with the Business Development Director. The local directors are subsequently responsible for operations etc. within a specific country, however the Business Development Director will assist them in further the development of specific aspects. The purpose of the Business Development Director is:

• to develop and maintain business relationships of identified Strategic Global Clients in order to maintain business and to support new business development in pre-targeted areas.

• to set and guide the strategic direction for the group and regional activities based on strategic business plans.

Kommenterede [F26]: Taka þetta allt út eða ráða CAO

Avrit

frá k

vf.fo

12

• to maintain up to date market/business intelligence on current developments across the core business sectors; and

• develop and establish strategies for new business and/or market entry as defined in strategic business plans;

•

4.84.6 Risks

4.8.14.6.1 Credit risk

Samherji hf. faces credit risk in relation to service fees charged depending on the creditworthiness and liquidity of the local group member receiving the services.

4.8.24.6.2 Foreign exchange risk

Samherji hf. invoices in Euro currency, while it incurs most of its costs in ISK. As a result, the company does not bear any significant currency risk. Particularly, service recipients outside the Euro zone bear currency risk in relation to the service transaction.

4.8.34.6.3 Liability risk

The service contract generally excludes liability risk. As Samherji hf. partly manages liability risk due to approval processes, service providers have a derivate liability in this respect. This risk is considered moderate.

4.8.44.6.4 Market risk

Key personnel employed by local group companies include Regional Managing Directors, Regional Finance Directors, Managing Directors and the Captains of the vessels (including crew). Local group members act as profit centers and perform important functions in the value chain as specified in the group master file. These functions contribute significantly to the group’s value drivers. As a result, local group member bear most of the related risks, market risk incurred at the level of Samherji hf. is considered minor.

4.94.7 Analysis of assets used

Samherji hf.’s primarily assets used for rendering the services include office buildings, office equipment as well as IT equipment (computers). Vessels and other crucial assets for the business are owned by the individual group companies.

Samherji hf. owns the brand names Samherji, IceFresh and IceFresh salmon these brand names are not part of the management services.

4.104.8 Characterization of Samherji hf.

When assessing and documenting any transfer pricing method, particular attention should be paid to the structure and organization of the Group1. Based on the analysis of functions, risks and assets, Samherji hf. can, in general, be characterized as service provider to the operating Samherji Group companies. Samherji is a vertically integrated seafood company, controlling a significant volume of fishing quota, employs qualified and enterprising personnel and management, operating a powerful fleet of fishing vessels; freezer and fresh fish trawlers, as well as multipurpose vessels, and highly advanced onshore plants. Samherji itself takes care of the entire process from the catch to the market, this concept is the main

1 OECD Transfer Pricing Guidelines for Multinational Enterprises and Tax Administrations (OECD Guidelines), Section 1.42.

Avrit

frá k

vf.fo

13

value driver. Samherji hf. has a significant role in linking the different companies and activities together in order to maintain this concept as well as to further develop it. Hence, Samherji hf. plays an important role in assisting its group companies via its CEO, CFO, CC, CAO and Business Development Director on tax, financing, financial advice, cash management, human resource (captains / key management), fishing budgets, fishing strategy, strategy aspects as well as special projects and assistance via the Business Development Director.

Avrit

frá k

vf.fo

14

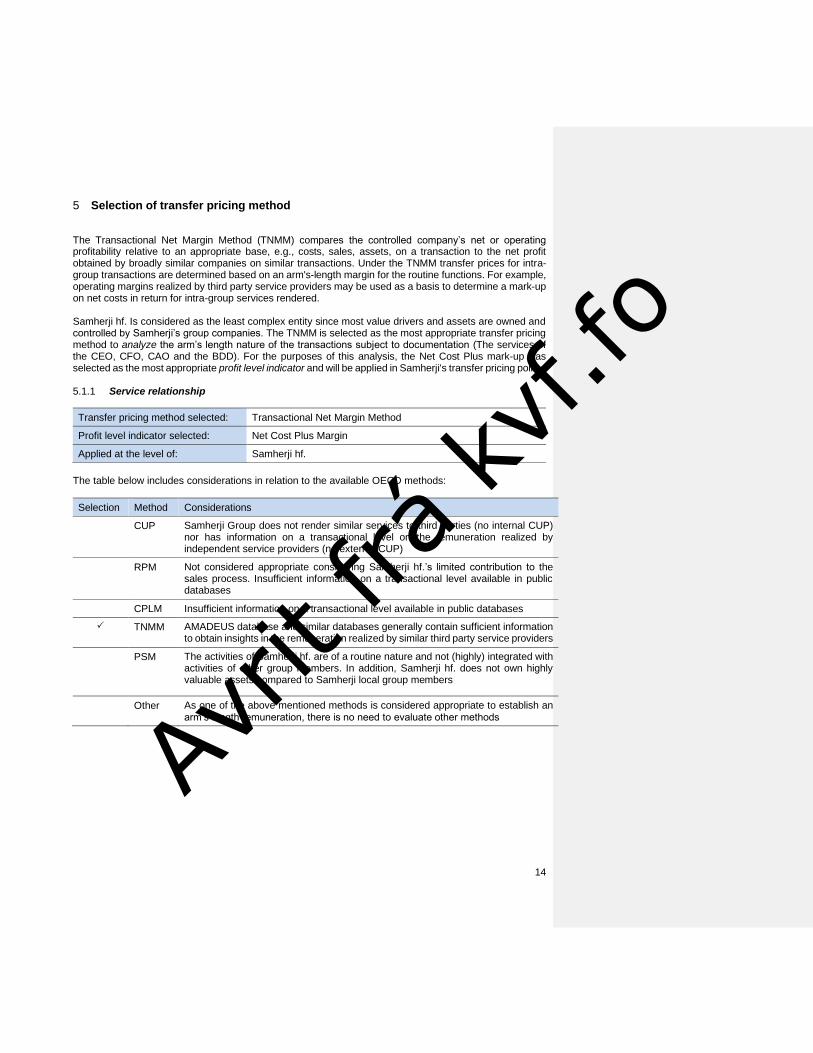

5 Selection of transfer pricing method

The Transactional Net Margin Method (TNMM) compares the controlled company’s net or operating profitability relative to an appropriate base, e.g., costs, sales, assets, on a transaction to the net profit obtained by broadly similar companies on similar transactions. Under the TNMM transfer prices for intra-group transactions are determined based on an arm's-length margin for the routine functions. For example, operating margins realized by third party service providers may be used as a basis to determine a mark-up on net costs in return for intra-group services rendered. Samherji hf. Is considered as the least complex entity since most value drivers and assets are owned and controlled by Samherji’s group companies. The TNMM is selected as the most appropriate transfer pricing method to analyze the arm’s length nature of the transactions subject to documentation (The services of the CEO, CFO, CAO and the BDD). For the purposes of this analysis, the Net Cost Plus mark-up was selected as the most appropriate profit level indicator and will be applied in Samherji's transfer pricing policy. 5.1.1 Service relationship

Transfer pricing method selected: Transactional Net Margin Method

Profit level indicator selected: Net Cost Plus Margin

Applied at the level of: Samherji hf.

The table below includes considerations in relation to the available OECD methods:

Selection Method Considerations

CUP Samherji Group does not render similar services to third parties (no internal CUP) nor has information on a transactional level on the remuneration realized by independent service providers (no external CUP)

RPM Not considered appropriate considering Samherji hf.’s limited contribution to the sales process. Insufficient information on a transactional level available in public databases

CPLM Insufficient information on a transactional level available in public databases

TNMM AMADEUS database and similar databases generally contain sufficient information to obtain insights in the remuneration realized by similar third party service providers

PSM The activities of Samherji hf. are of a routine nature and not (highly) integrated with activities of other group members. In addition, Samherji hf. does not own highly valuable assets compared to Samherji local group members

Other As one of the above mentioned methods is considered appropriate to establish an arm’s length remuneration, there is no need to evaluate other methods

Avrit

frá k

vf.fo

15

6 OECD Transfer Pricing Guidelines for Services

6.1 Introduction

The OECD Guidelines specify a three stage procedure when determining the level of charges for services to an affiliate, which is also followed in our report.

a. Only those service that provide a commercial benefit to affiliates should be charged for (this implies that functional analysis and cost allocation should be made).

b. An approved method should be chosen from the OECD Guidelines. The OECD Guidelines provide detailed descriptions of methods that are used to apply the arm’s length principle. These methods fall into two categories: “traditional transaction methods” and “transactional profit methods”.

c. The actual level of the charge must be determined.

6.2 Benefit test

• Under the OECD Guidelines, a charge should only be made if the service provides a commercial benefit to the service recipient.

• It should be determined ''whether an independent enterprise in comparable circumstances would have been willing to pay for the activity performed for it by an independent enterprise or would have performed the activity in-house itself. ‘’

• In order to determine whether the costs incurred by a group company were in the interest of another group company (or more group companies), a benefit test should be executed. The appropriate information needed for the benefit test can be acquired by conducting functional interviews.

• In determining the allocation of service fees, the OECD Guidelines note that whilst it is preferable to charge directly for a particular service, it may be administratively burdensome to do this.

• In cases where it is not possible to identify the costs related to a particular service, the OECD Guidelines allow the use of allocation keys, which approximate the relevant costs of providing a particular service.

• When determining which allocation key to use, the Guidelines note that the allocation key ''should be sensitive to the commercial features of the individual case, contain safe guards against manipulation and follow sound accounting principles, and be capable of providing charges or allocation of costs that are commensurate with the actual or reasonably expected benefits to the recipient of the services''.

6.3 Shareholder activities and costs

In order to determine whether an intra-group service is rendered, it needs to be assessed whether an independent enterprise in comparable circumstances would have been willing to pay for the activity, either performed by an independent enterprise or in-house. An intra-group service is not rendered when a group member (usually the parent company or a regional holding company) performs the activity solely because of its ownership interest in one or more other group members, i.e. in its capacity as a shareholder.

The costs related to such shareholder activities may not be allocated to a group company as such activities are not considered to be an intra-group service under the arm's length principle. These costs should therefore be excluded from the ''pool'' of costs that will be charged out.

The following examples constitute shareholder activities according to the OECD Transfer Pricing Guidelines:

Avrit

frá k

vf.fo

16

• Costs of activities relating to the juridical structure of the parent company itself, such as meetings of shareholders of the parent, issuing of shares in the parent company and costs of the supervisory board;

• Costs relating to reporting requirements of the parent company including the consolidation of reports;

• Costs of raising funds for the acquisition of its participations.

6.4 Duplication

In general, no intra-group service should be found for activities undertaken by one group member that merely duplicate a service that another group member is performing for itself, or that is being performed for such other group member by a third party.

Similarly, an associated enterprise should not be considered to receive an intra-group service when it obtains incidental benefits attributable solely to its being part of a larger concern, and not to any specific activity being performed.

6.5 Determine the level of the service charge

6.5.1 Introduction

When using a cost plus model, a proper cost base should be determined considering direct costs and indirect costs attributable to the service operations.

6.5.2 Direct costs

• All directly attributable service costs must be considered.

• These costs relate to a service that has been provided to an individual recipient where the cost relating to the provision of the service can be identified.

• These costs should be charged to the individual subsidiary that has received and benefited from this specific service.

6.5.3 Indirect costs

• In addition, indirectly attributable service costs have to be considered. These costs relate to services that are provided to a number of subsidiaries, where separate recording and analysis of services provided to each company is not possible or would be very burdensome. These costs should be charged to the subsidiaries that benefited from these services based on an appropriate allocation key. This allocation key should ensure that the costs charged to each of the subsidiaries are in accordance with the benefits received.

• In order to determine whether the costs incurred by a group company were in the interest of another (one or more) group company, a benefit test should be executed. The appropriate information needed for the benefit test can be acquired by conducting functional interviews.

7 Service charge models

Various models could be considered for charging service fees to group members

Avrit

frá k

vf.fo

17

7.1 Direct charge model

A direct charge model is generally considered more robust, although not always possible for many head office functions.

7.2 Indirect charge model

The OECD Transfer Pricing Guidelines allow the use of indirect charges, especially if various group members benefit from the services and the administrative burden of applying direct charges is considered disproportionate.

7.3 Mixed model

A mixed model is a service model which combines direct charge mechanisms (e.g. for a major project performed for a specific group member) and indirect charge mechanisms. Considering the above, Samherji hf. aims to establish a model of charging relevant service fees to group members via indirect allocation keys combined with a direct charge for the specific projects of the Business Development Director.

Avrit

frá k

vf.fo

18

8 Transfer Pricing Policy

8.1 Key characteristics

This section summarized the transfer pricing policy in relation to service charges

Type of cost plus model Net Cost Plus Model

Mark-up: 7%-10%

For low-value added services, the EU Joint Transfer Pricing Forum2 generally observes modest mark-ups typically falling within a range of 3% and 10%, often around 5%. Considering the different nature of the services rendered by Samherji hf. and the value added functions performed by local group members a different mark-up per service is considered.

Samherji hf. notes that the so-called fishing strategy service and HR service of the CEO and the service of the Business Development Director regarding specific projects is not a low-value. Therefore these services require a higher mark-up (10% instead of 7%) in order to meet the arm’s length principle.

8.2 Considerations in relation to the cost base

Costs base Relevant costs of Samherji hf. for rendering the services. Costs particularly consist of salary costs, office costs and advisory costs.

Costs excluded from cost base: • Costs related to other activities (i.e. shareholder activities)

• Costs of duplicative activities (if any)

• Tax costs (corporate income tax)

• Interest costs

Disbursements3 Key disbursements include:

• Purchase of fishing gear

• Certain logistic cost

Cost relating to the personal assistant are allocated to the CEO, the same applies to the cost of the Business Development Director (BDD) except for the cost that can be allocated to specific projects and are directly charged. Cost regarding the legal advisor are no taken into account, as the legal advisor performed only activities for the head office.

8.3 Service charge model

Samherji hf. has a lean head office. As applying direct charges is considered disproportional considering the limited cost base, Samherji hf. applies an indirect charge model for most of the activities. Due to the nature of the specific project services of the BDD an indirect charge for these services is not at arm’s length, therefore the direct method is used for specific projects.

Service charge model Mixed Model

2 EU Joint Transfer Pricing Forum / January 2011 3 Disbursements pertain to third party costs which are incurred on behalf of another group member. These include costs that are

initially paid by the service provider, but which are generally passed on separately to the client, for example, legal dues, court registry charges and costs charged for third party services. As service provider does not add any value to these costs when

rendering the services, these external charges do not warrant any additional remuneration.

Avrit

frá k

vf.fo

19

8.4 Allocation keys

As the nature of the services differs, Samherji hf. allocates the relevant cost base to various functional persons (CEO, CFO, CAO, BDD) to establish an arm’s length allocation of the service charge to various group members. Per department, Samherji hf. selected suitable allocation keys. Allocation keys should lead to charges reflecting the benefit of the services for the relevant group members (i.e. service recipients), taking into account the cost driver of the services. Samherji hf. applies the following allocation keys to allocate the service fee towards relevant group members:

- Quota; - Key management (includes captains and managing directors); - Number of foreign group companies (which is pro rata method).

Samherji hf. considers quota based allocation keys appropriate as these take into account the size of the local entity, which is considered an important cost driver for operational management services of the head office by the CEO. In addition, it is considered to reflect the benefits. The same applies for the CEO services with respect to key management.

With respect to the other services Samherji hf. considers the number of foreign group companies an appropriate allocation key. Due to the type of services it affects every company.

We note that the direct charge regarding specific projects of the BDD will be charged to the service recipient directly.

8.5 Group Benefits

8.5.1 CEO

The following specific benefits were identified, that are provided by Management, Business Development and Human Resources, for the Samherji group companies:

• Is involved in negotiations with third parties in case of acquisitions and potential strategic

• All strategic decisions for the group.

• Handles certain press related matters;

• Determines the direction when entering new markets;

• Makes the decision regarding significant investment of the group;

• Meets with the most important customers and negotiates terms with them;

• Execute recruitment and appointment of staff;

• Participate and mediate in disputes and disciplinary actions;

• Negotiate and conclude contracts with key managers;

• Makes decisions effecting the group based on recommendation set by Business development such as the geographic extension of the Samherji group and new business aspects;

• Analyses and implements synergies in association with business development;

8.5.2 CFO

• The following specific benefits were identified, that are provided by Treasury, Guarantees, Financing, Control and budgeting for the Samherji group companies:

• Financial budgeting for the group;

• Finance and cash management for the group;

• Negotiates financial facilities with financial institutions;

• Manages guarantees for the group companies;

• Advices upon request on funding of the group companies;

• Provide recommendations and maintain solutions to business and financial problems;

Avrit

frá k

vf.fo

20

• Conduct risk assessments to identify and resolve potential business and financial risks;

• Arrange financing for various projects;

• Provide advice and analysis on investment decisions;

• Compose financial forecasts and track performance;

• Monitor compliance with statutory obligations and advise accordingly;

• Advising on adequate liquidity management (e.g. redemption).

8.5.3 CAO

• The following specific benefits were identified, that are provided by for the Legal, Tax, Compliance group companies:

•

• Responsible for all tax aspects of the group, such as withholding tax optimization and transfer pricing;

• Identify tax risks and opportunities, including general tax strategies but also on specific contracts and other proposed transactions;

• Manage corporate tax audits;

• Responsible for ensuring global and regional compliance with (inter)national tax laws, rules and legislations;

• Drives and conduct proper risk-management from a tax perspective across the organization

•

•

Avrit

frá k

vf.fo

21

8.6 Transfer Pricing Model

Services Share

Share of

total Service recipients Benefit of the service Allocable cost Direct Allocation Key

CEO

Group management

& Shareholder

relations

20% 10%Holding Company and

shareholders -

No (shareholder

cost) - -

Operational

Management

(strategic, HR)

20% 10% Samherji GroupGroup-w ide know -how

and functional competence

Yes (indirect

allocation key)No Key management

Operational

Management

(f ishing strategy)

60% 30% Samherji Group

Fishing know -how , optimal

use of f ishing vessels

plants and quota

Yes (indirect

allocation key)No Quota

CFO

Icelandic companies

& consolidation

activities

25% 13%

Group companies

Iceland and head

off ice

- No - -

Cash management 25% 13% Samherji Group

Cash and heding

management as w ell as

know -how of the CFO

Yes (indirect

allocation key)No

Number of

foreign

companies

Financing / hedging

group companies10% 5%

Head off iice / Iceland

companies - No - -

Financing / hedging

group companies40% 20% Samherji Group

Financial management and

know -of CFO

Yes (indirect

allocation key)No

Number of

foreign

companies

CAO

Management

Spanish Group70% Spanish Group - No - -

Tax, structuring,

f inancinal reporting

and financial

assistance

30% Samherji Group

Tax, f inance and legal

know -how , service and

cost savings

Yes (indirect

allocation key)No

Number of

foreign

companies

Avrit

frá k

vf.fo

22

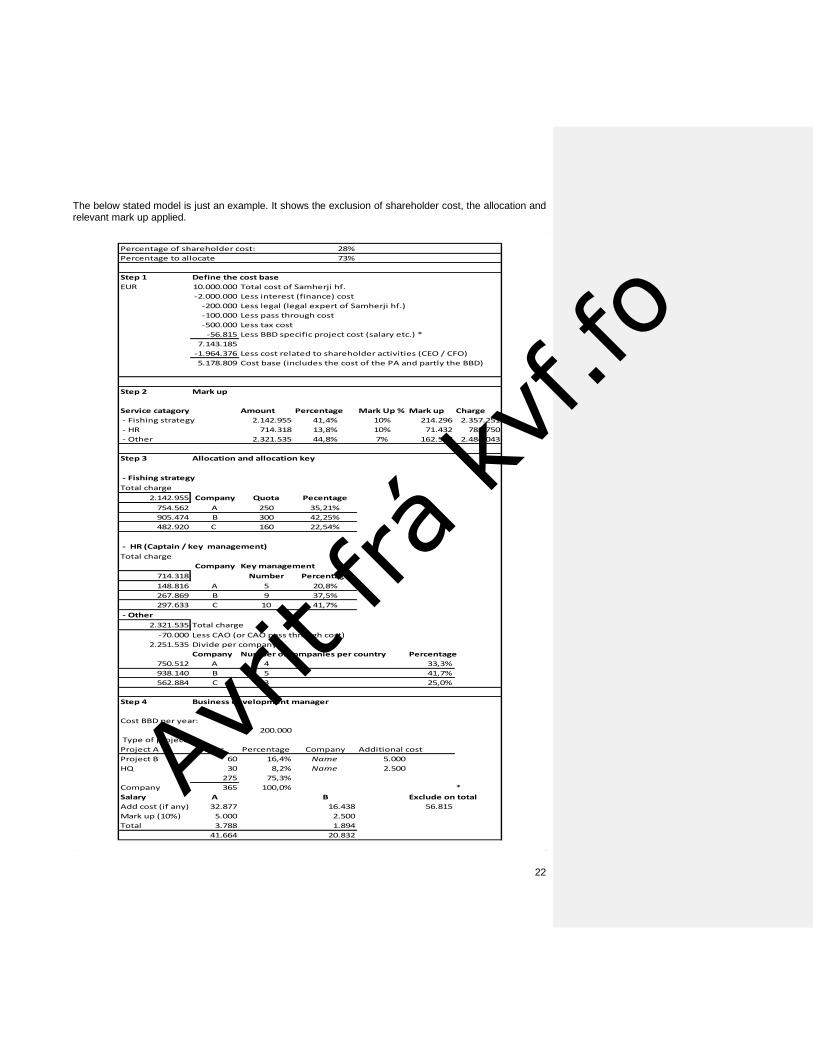

The below stated model is just an example. It shows the exclusion of shareholder cost, the allocation and relevant mark up applied.

Percentage of shareholder cost: 28%

Percentage to allocate 73%

Step 1 Define the cost base

EUR 10.000.000 Total cost of Samherji hf.

-2.000.000 Less interest (finance) cost

-200.000 Less legal (legal expert of Samherji hf.)

-100.000 Less pass through cost

-500.000 Less tax cost

-56.815 Less BBD specific project cost (salary etc.) *

7.143.185

-1.964.376 Less cost related to shareholder activities (CEO / CFO)

5.178.809 Cost base (includes the cost of the PA and partly the BBD)

Step 2 Mark up

Service catagory Amount Percentage Mark Up % Mark up Charge

- Fishing strategy 2.142.955 41,4% 10% 214.296 2.357.251

- HR 714.318 13,8% 10% 71.432 785.750

- Other 2.321.535 44,8% 7% 162.507 2.484.043

Step 3 Allocation and allocation key

- Fishing strategy

Total charge

2.142.955 Company Quota Pecentage

754.562 A 250 35,21%

905.474 B 300 42,25%

482.920 C 160 22,54%

- HR (Captain / key management)

Total charge

Company Key management

714.318 Number Percentage

148.816 A 5 20,8%

267.869 B 9 37,5%

297.633 C 10 41,7%

- Other

2.321.535 Total charge

-70.000 Less CAO (or CAO pass through cost)

2.251.535 Divide per company

Company Number of companies per country Percentage

750.512 A 4 33,3%

938.140 B 5 41,7%

562.884 C 3 25,0%

Step 4 Business development manager

Cost BBD per year:

200.000

Type of project

Project A Days Percentage Company Additional cost

Project B 60 16,4% Name 5.000

HQ 30 8,2% Name 2.500

275 75,3%

Company 365 100,0% *

Salary A B Exclude on total

Add cost (if any) 32.877 16.438 56.815

Mark up (10%) 5.000 2.500

Total 3.788 1.894

41.664 20.832

Avrit

frá k

vf.fo

23

9 Appendices (Service agreements)

Avrit

frá k

vf.fo