January 11, 2008 Confidential Tsubakimoto Chain Co. Initiatives for 2008 Providing Clarity and...

13

January 11, 2008 Confidential Tsubakimoto Chain Co. Initiatives for 2008 Providing Clarity and Excitement

-

Upload

nathan-oliver -

Category

Documents

-

view

214 -

download

0

Transcript of January 11, 2008 Confidential Tsubakimoto Chain Co. Initiatives for 2008 Providing Clarity and...

January 11, 2008

Confidential

Tsubakimoto Chain Co.Initiatives for 2008Providing Clarity and Excitement

2

Tsubakimoto Chain's Stock Price in 2007

1 2 3 4 5 6 7 8 9 10 11 12

600

650

700

750

800

850

900

950

• 2007 was a volatile year for TC due to various factors

• However, we hope that TC’s fundamentals will continue to remain strong and that 2008 will be a prosperous year for the company

2007 Review and 2008 Prospects2007 Review and 2008 Prospects

What are the reasons for the weak stock price?

May 14: Announced solid FY3/07 results and buyback next day

Aug. 9: “BNP Paribas Shock”*

Source: FactSet *BNP Paribas froze three funds exposed to the stumbling US subprime mortgage market

Nov. 14: Announced H1 FY3/08 results and downgraded full-year sales forecast

Nov. 9: Yen strengthens to 110 yen level

Oct end: Oil price exceeds $90/B

Aug. 17: Yen strengthens to 115 yen level

3

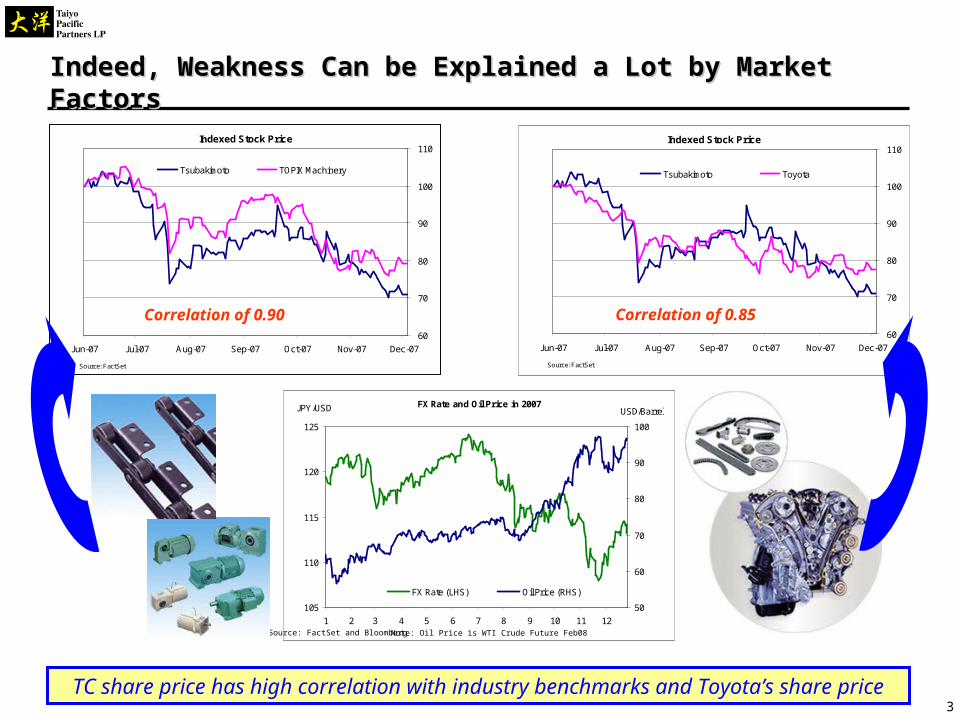

FX Rate and Oil Price in 2007

105

110

115

120

125

1 2 3 4 5 6 7 8 9 10 11 12

JPY/USD

50

60

70

80

90

100

USD/Barrel

FX Rate (LHS) Oil Price (RHS)

Indexed Stock Price

Jun-07 Jul-07 Aug-07 Sep-07 Oct-07 Nov-07 Dec-07

Source: FactSet

60

70

80

90

100

110

Tsubakimoto Toyota

Indexed Stock Price

Jun-07 Jul-07 Aug-07 Sep-07 Oct-07 Nov-07 Dec-07

Source: FactSet

60

70

80

90

100

110

Tsubakimoto TOPIX Machinery

Indeed, Weakness Can be Explained a Lot by Market FactorsIndeed, Weakness Can be Explained a Lot by Market Factors

TC share price has high correlation with industry benchmarks and Toyota’s share price

Correlation of 0.85Correlation of 0.90

Source: FactSet and Bloomberg Note: Oil Price is WTI Crude Future Feb08

4

Jul Aug Sep Oct Nov Dec

70

75

80

85

90

95

100

105Tsubakimoto Chain Co. (6371-JP) 70.9Japan TOPIX 1st Section / Machinery (188378) 79.1Japan TOPIX 1st Section / Transportation Equipment (188380) 82.8Japan TOPIX 1st Section (180460) 83.1

Indexed Price29-Jun-2007 to 28-Dec-2007 (Daily)29-Jun-2007=100; Local

Data Source: Exshare ©FactSet Research Systems 2008

Underperformance

Nevertheless, Overall Market Weakness is Not the Only Factor at PlayNevertheless, Overall Market Weakness is Not the Only Factor at Play

• Since July 2007, TC’s stock price has declined around 30%, which is greater than those of the benchmarks

TOPIX Machinery

TOPIX 1st Section

Tsubakimoto

This decline suggests concerns market participants have on TC and its business environment

TOPIX Transportation

5

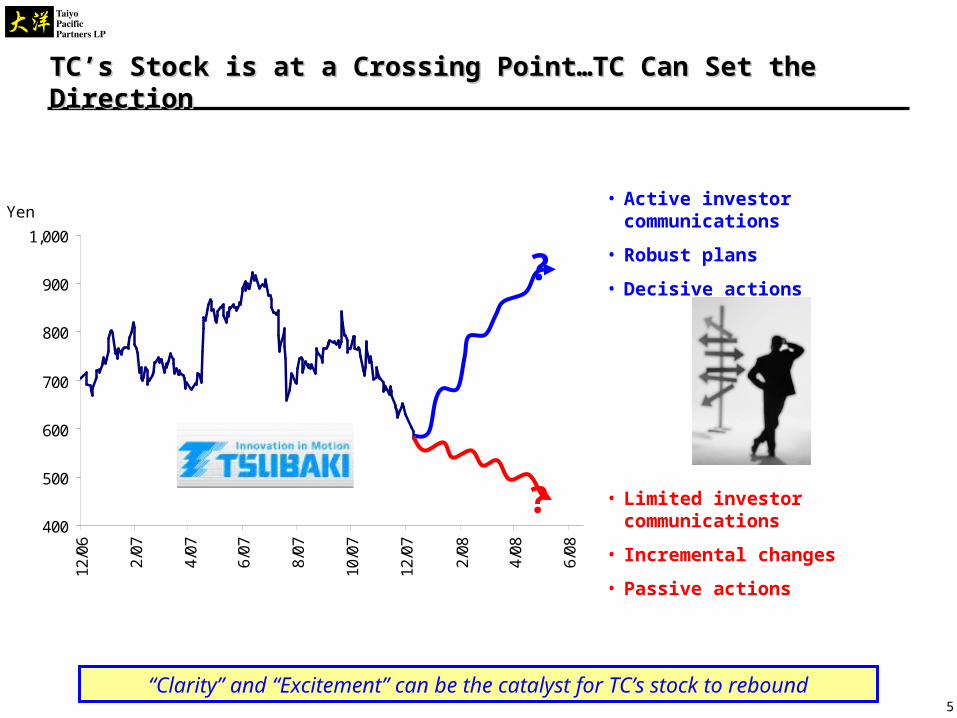

TC’s Stock is at a Crossing Point…TC Can Set the DirectionTC’s Stock is at a Crossing Point…TC Can Set the Direction

“Clarity” and “Excitement” can be the catalyst for TC’s stock to rebound

400

500

600

700

800

900

1,000

12/0

6

2/07

4/07

6/07

8/07

10/0

7

12/0

7

2/08

4/08

6/08

• Active investor communications

• Robust plans

• Decisive actions

• Limited investor communications

• Incremental changes

• Passive actions

?

?

Yen

6

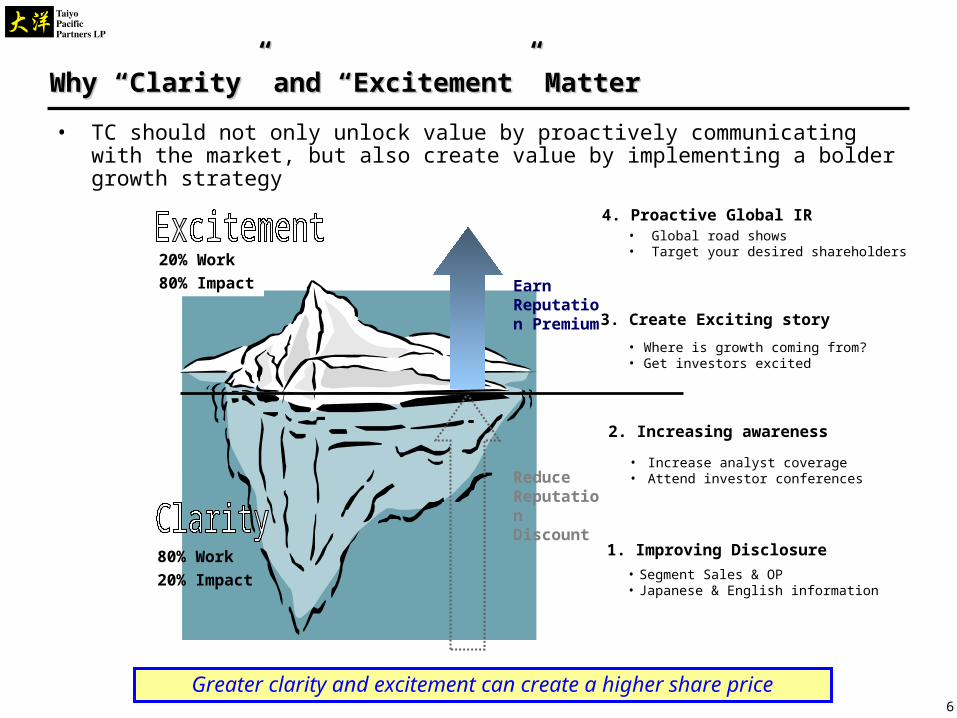

Why “Clarity” and “Excitement” MatterWhy “Clarity” and “Excitement” Matter

Greater clarity and excitement can create a higher share price

Earn Reputation Premium

Reduce Reputation Discount

1. Improving Disclosure

4. Proactive Global IR

• Segment Sales & OP• Japanese & English information

• Increase analyst coverage• Attend investor conferences

• Where is growth coming from?• Get investors excited

3. Create Exciting story

2. Increasing awareness

• Global road shows• Target your desired shareholders

80% Work

20% Impact

20% Work

80% Impact

• TC should not only unlock value by proactively communicating with the market, but also create value by implementing a bolder growth strategy

7

Clarity – Negative “Subprime” PerceptionClarity – Negative “Subprime” Perception

Market Noise

“Subprime”

Hike in

oil price

Yen

appreciation

Investor Perception TC Downgrade (as 1HY result announcement)

Original Forecast

Sales: Y170.0bn OP: Y17.6bn

New Forecast

Sales: Y164.0bn (ΔY6.0bn) OP: Y17.6bn

By Business

Sales Forecast

Current Situation

Chain Δ3.1%Growing as domestic demand stays firm for machine tools, auto, and steel industries

Auto Parts

Δ2.0%Solid growth driven by brisk exports, offsetting slow down in Japan

Precision Δ6.1%Losing competitiveness in products while IT-related demand is sluggish

Materials Handling Δ5.0%

Order of large-scale projects from both auto and IT industries slowing down

TC should emphasize that the downgrade came from ex-”subprime” issues and that the core business remains strong

• Decline in consumer confidence

• Slow down in US auto sales

Source: Company IR material, analysts comments, Taiyo

8

Clarity – Analysts ConcernsClarity – Analysts Concerns

TC should address “Off-The-Record” concerns to rebuild clarity and confidence

UBS

Ms. Yamazaki / Mr. Hoshino

Rating: “Buy” / TP¥1,050

• H1 results better than initially planed by company

• Further expansion likely in chains biz

• Making progress in materials handling biz

KBC

Mr. McDonald

Rating: “Neutral” / No TP

• Some positives backed by global successes of Japanese automakers and growth in some Asian markets

Macquarie

Mr. Hayami

Rating: “Outperform” / TP¥950

• H1 results came in better than expected

• Strong global auto production should drive power transmission biz

Okasan

Mr. Shibata

Rating: “Above Average” / No TP

• Growth rate of auto parts biz likely to top company’ forecast thanks to growth in NA

• Likely benefit significantly from shift to chains from belts in engines

Nikko Citigroup

Mr. Sakurada

Rating: “Hold” / TP¥760

• Benefiting significantly from growth of Japanese automakers

• Profitability in materials handling biz is improving

• Why not disclose monthly and/or quarterly order data?

• Why is full year OP guidance so rigid?

• What is TC-Emerson’s competitive advantage and strategy in speed reducers?

• Can TC dissolve the Emerson relationship and enter the US precision market?

• What is TC’s strategy for its materials handling business?

• Are there any immediate catalysts?

“On-The-Record” “Off-The-Record”

9

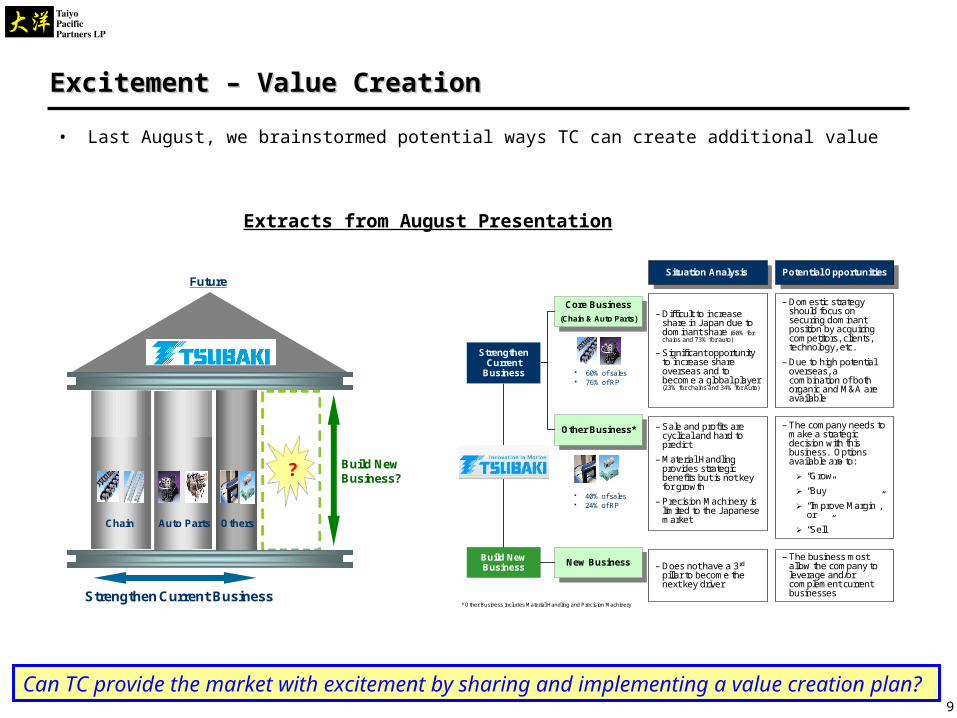

Build New Business?

Future

?

Auto PartsChain Others

Strengthen Current Business

Excitement – Value CreationExcitement – Value Creation

Can TC provide the market with excitement by sharing and implementing a value creation plan?

• Last August, we brainstormed potential ways TC can create additional value

Build New Business

Other Business*Other Business*

Core Business

(Chain & Auto Parts)

Core Business

(Chain & Auto Parts)

Situation Analysis Situation Analysis

New BusinessNew Business

60% of sales 76% of RP

40% of sales 24% of RP

* Other Business includes Material Handling and Precision Machinery

Potential OpportunitiesPotential Opportunities

– Domestic strategy should focus on securing dominant position by acquiring competitors, clients, technology, etc.

– Due to high potential overseas, a combination of both organic and M&A are available

Strengthen Current

Business

– Difficult to increase share in Japan due to dominant share (60% for chains and 73% for auto)

– Significant opportunity to increase share overseas and to become a global player (23% for chains and 34% for Auto)

– The company needs to make a strategic decision with this business. Options available are to:

“Grow”

“Buy”

“Improve Margin”, or

“Sell”

– Sale and profits are cyclical and hard to predict

– Material Handling provides strategic benefits but is not key for growth

– Precision Machinery is limited to the Japanese market

– The business most allow the company to leverage and/or complement current businesses

– Does not have a 3rd

pillar to become the next key driver

Extracts from August Presentation

10

760

900

612 561

468

1,050

1,2001,122

1,374

941

200

400

600

800

1,000

1,200

1,400

1,600

P/En EV/EBITDA P/B DCF AnalystConsensus

TC’s stock price will remain undervalued without any actionTC’s stock price will remain undervalued without any action

TC needs to reduce the 37% undervaluation gap

Current Share Price

Yen

Source: FactSet and Taiyo AnalysisNote: Data as of Jan. 9, 2008. 2-year High and Low data for P/En, EV/EBITDA, and P/B

Historically Cheap

Intrinsically Cheap

“Street” Cheap

Avg. 705

Avg. 993

Avg. 842

Avg. 1,050

Avg. 905

Avg. 846

Avg. Y934

Y586

Fair Value Estimate

Δ37%

11

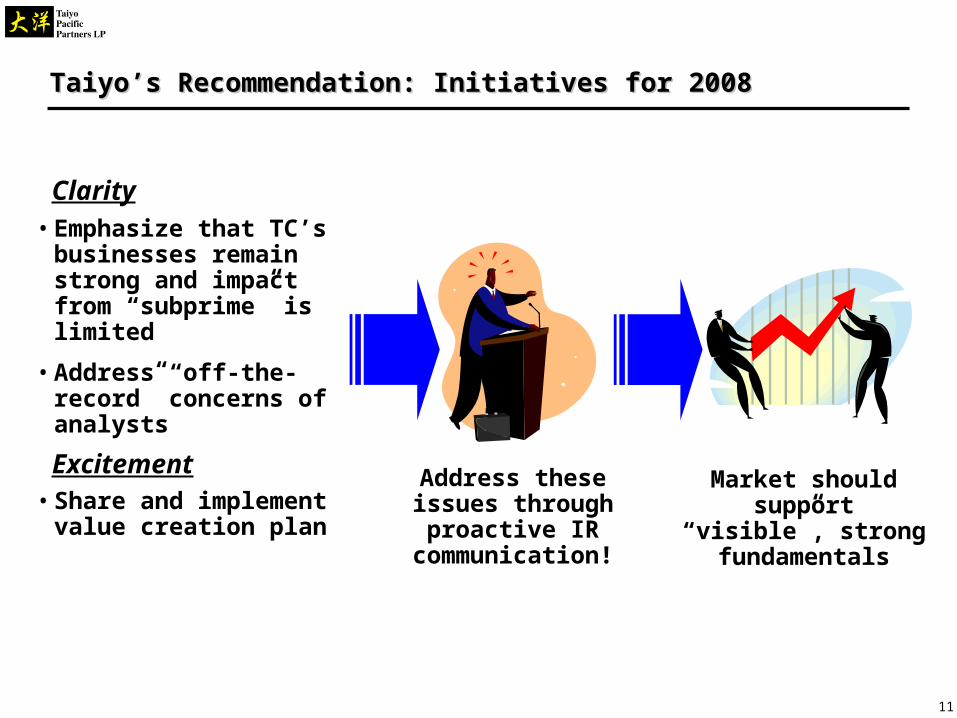

Taiyo’s Recommendation: Initiatives for 2008Taiyo’s Recommendation: Initiatives for 2008

Address these issues through

proactive IR communication!

Market should support “visible”,

strong fundamentals

Clarity

Excitement

• Emphasize that TC’s businesses remain strong and impact from “subprime” is limited

• Address “off-the-record” concerns of analysts

• Share and implement value creation plan

12

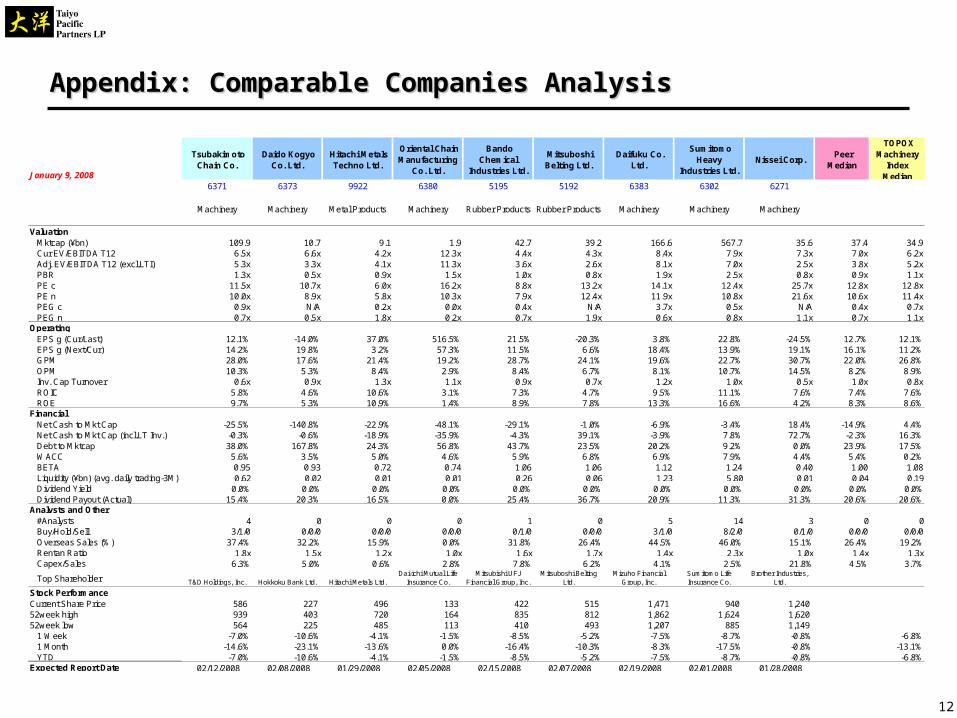

January 9, 2008

Tsubakimoto Chain Co.

Daido Kogyo Co. Ltd.

Hitachi Metals Techno Ltd.

Oriental Chain Manufacturing

Co. Ltd.

Bando Chemical

Industries Ltd.

Mitsuboshi Belting Ltd.

Daifuku Co. Ltd.

Sumitomo Heavy

Industries Ltd. Nissei Corp.

Peer Median

TOPOX Machinery

Index Median

6371 6373 9922 6380 5195 5192 6383 6302 6271

Machinery Machinery Metal Products Machinery Rubber Products Rubber Products Machinery Machinery Machinery

ValuationMktcap (¥bn) 109.9 10.7 9.1 1.9 42.7 39.2 166.6 567.7 35.6 37.4 34.9Cur EV/EBITDA T12 6.5x 6.6x 4.2x 12.3x 4.4x 4.3x 8.4x 7.9x 7.3x 7.0x 6.2xAdj. EV/EBITDA T12 (excl.LTI) 5.3x 3.3x 4.1x 11.3x 3.6x 2.6x 8.1x 7.0x 2.5x 3.8x 5.2xPBR 1.3x 0.5x 0.9x 1.5x 1.0x 0.8x 1.9x 2.5x 0.8x 0.9x 1.1xPE c 11.5x 10.7x 6.0x 16.2x 8.8x 13.2x 14.1x 12.4x 25.7x 12.8x 12.8xPE n 10.0x 8.9x 5.8x 10.3x 7.9x 12.4x 11.9x 10.8x 21.6x 10.6x 11.4xPEG c 0.9x N/A 0.2x 0.0x 0.4x N/A 3.7x 0.5x N/A 0.4x 0.7xPEG n 0.7x 0.5x 1.8x 0.2x 0.7x 1.9x 0.6x 0.8x 1.1x 0.7x 1.1x

OperatingEPS g (Cur/Last) 12.1% -14.0% 37.0% 516.5% 21.5% -20.3% 3.8% 22.8% -24.5% 12.7% 12.1%EPS g (Next/Cur) 14.2% 19.8% 3.2% 57.3% 11.5% 6.6% 18.4% 13.9% 19.1% 16.1% 11.2%GPM 28.0% 17.6% 21.4% 19.2% 28.7% 24.1% 19.6% 22.7% 30.7% 22.0% 26.8%OPM 10.3% 5.3% 8.4% 2.9% 8.4% 6.7% 8.1% 10.7% 14.5% 8.2% 8.9%Inv. Cap Turnover 0.6x 0.9x 1.3x 1.1x 0.9x 0.7x 1.2x 1.0x 0.5x 1.0x 0.8xROIC 5.8% 4.6% 10.6% 3.1% 7.3% 4.7% 9.5% 11.1% 7.6% 7.4% 7.6%ROE 9.7% 5.3% 10.9% 1.4% 8.9% 7.8% 13.3% 16.6% 4.2% 8.3% 8.6%

FinancialNet Cash to Mkt Cap -25.5% -140.8% -22.9% -48.1% -29.1% -1.0% -6.9% -3.4% 18.4% -14.9% 4.4%Net Cash to Mkt Cap (incl.LT Inv.) -0.3% -0.6% -18.9% -35.9% -4.3% 39.1% -3.9% 7.8% 72.7% -2.3% 16.3%Debt to Mktcap 38.0% 167.8% 24.3% 56.8% 43.7% 23.5% 20.2% 9.2% 0.0% 23.9% 17.5%WACC 5.6% 3.5% 5.0% 4.6% 5.9% 6.8% 6.9% 7.9% 4.4% 5.4% 0.2%BETA 0.95 0.93 0.72 0.74 1.06 1.06 1.12 1.24 0.40 1.00 1.08Liquidity (¥bn) (avg. daily trading-3M) 0.62 0.02 0.01 0.01 0.26 0.06 1.23 5.80 0.01 0.04 0.19Dividend Yield 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%Dividend Payout (Actual) 15.4% 20.3% 16.5% 0.0% 25.4% 36.7% 20.9% 11.3% 31.3% 20.6% 20.6%

Analysts and Other#Analysts 4 0 0 0 1 0 5 14 3 0 0Buy/Hold/Sell 3/1/0 0/0/0 0/0/0 0/0/0 0/1/0 0/0/0 3/1/0 8/2/0 0/1/0 0/0/0 0/0/0Overseas Sales (%) 37.4% 32.2% 15.9% 0.0% 31.8% 26.4% 44.5% 46.0% 15.1% 26.4% 19.2%Rentan Ratio 1.8x 1.5x 1.2x 1.0x 1.6x 1.7x 1.4x 2.3x 1.0x 1.4x 1.3xCapex/Sales 6.3% 5.0% 0.6% 2.8% 7.8% 6.2% 4.1% 2.5% 21.8% 4.5% 3.7%

Top Shareholder T&D Holdings, Inc. Hokkoku Bank Ltd. Hitachi Metals Ltd.Dai-ichi Mutual Life

Insurance Co.Mitsubishi UFJ

Financial Group, Inc.Mitsuboshi Belting

Ltd.Mizuho Financial

Group, Inc.Sumitomo Life Insurance Co.

Brother Industries, Ltd.

Stock PerformanceCurrent Share Price 586 227 496 133 422 515 1,471 940 1,240 52week high 939 403 720 164 835 812 1,862 1,624 1,620 52week low 564 225 485 113 410 493 1,207 885 1,149

1 Week -7.0% -10.6% -4.1% -1.5% -8.5% -5.2% -7.5% -8.7% -0.8% -6.8%1 Month -14.6% -23.1% -13.6% 0.0% -16.4% -10.3% -8.3% -17.5% -0.8% -13.1%YTD -7.0% -10.6% -4.1% -1.5% -8.5% -5.2% -7.5% -8.7% -0.8% -6.8%

Expected Report Date 02/12/2008 02/08/2008 01/29/2008 02/05/2008 02/15/2008 02/07/2008 02/19/2008 02/01/2008 01/28/2008

Appendix: Comparable CompaniesAppendix: Comparable Companies AnalysisAnalysis

DisclaimerDisclaimer

Taiyo Pacific Partners LP (“TPP”) does not make any warranty, express or implied a) as to the accuracy or completeness of the contents of this report, or b) as to the results of using any information contained herein.

In no case shall TPP have any liability to any person in respect of any loss, claim, damages, costs or liability arising from reliance on any information contained in this report or use of this report.

This report is indented only for the use of addressee and may contain information that is TPP’s work product, privileged and confidential.

Copyright: This report is protected by U.S., and other copyright laws. Information contained herein may not be reproduced, distributed, transmitted, displayed or broadcasted without the prior written consent of TPP.