Jagannath Institute of Management Sciences Lajpat Nagar · 2016-02-29 · Jagannath Institute of...

74

Jagannath Institute of Management Sciences Lajpat Nagar BBA VI Sem INDIAN FINANCIAL SERVICES

Transcript of Jagannath Institute of Management Sciences Lajpat Nagar · 2016-02-29 · Jagannath Institute of...

Jagannath Institute of Management Sciences

Lajpat Nagar

BBA VI Sem

INDIAN FINANCIAL SERVICES

UNIT-1

DEFINITION of 'Financial System'

A financial system can be defined at the global, regional or firm specific level. The firm's

financial system is the set of implemented procedures that track the financial activities of the

company. On a regional scale, the financial system is the system that enables lenders and

borrowers to exchange funds. The global financial system is basically a broader regional

system that encompasses all financial institutions, borrowers and lenders within the global

economy.

A financial system is a network of financial institutions, financial markets, financial

instruments and financial services to facilitate the transfer of funds. The system consists of

savers, intermediaries, instruments and the ultimate user of funds. The level of economic

growth largely depends upon and is facilitated by the state of financial system prevailing in

the economy. Efficient financial system and sustainable economic growth are corollary. The

financial system mobilises the savings and channelizes them into the productive activity and

thus influences the pace of economic development. Economic growth is hampered for want

of effective financial system. Broadly speaking, financial system deals with three inter-

related and interdependent variables, i.e., money, credit and finance.

The functions of financial system can be enumerated as follows:

Financial system works as an effective conduit for optimum allocation of financial

resources in an economy.

It helps in establishing a link between the savers and the investors.

Financial system allows ‘asset-liability transformation’. Banks create claims (liabilities)

against themselves when they accept deposits from customers but also create assets when

they provide loans to clients.

Economic resources (i.e., funds) are transferred from one party to another through

financial system.

The financial system ensures the efficient functioning of the payment mechanism in an

economy. All transactions between the buyers and sellers of goods and services are

effected smoothly because of financial system.

Financial system helps in risk transformation by diversification, as in case of mutual

funds.

Financial system enhances liquidity of financial claims.

Financial system helps price discovery of financial assets resulting from the interaction

of buyers and sellers. For example, the prices of securities are determined by demand and

supply forces in the capital market.

Financial system helps reducing the cost of transactions.

Structure and Function of of Indian Financial System!

Financial System is a set of institutional arrangements through which financial surpluses in the economy

are mobilised from surplus units and transferred to deficit spenders.

The institutional arrangements include all conditions and mechanisms governing the production,

distribution, exchange and holding of financial assets or instruments of all kinds and the

organisations as well as the manner of operations of financial markets and institutions of all

descriptions.

Thus, there are three main constituents of financial system:

(a) Financial Assets

(b) Financial Markets, and

(c) Financial Institutions.

Financial assets are subdivided under two heads:

Primary securities and secondary securities. The former are financial claims against real-sector units, for

example, bills, bonds, equities etc. They are created by real-sector units as ultimate borrowers

for raising funds to finance their deficit spending. The secondary securities are financial claims

issued by financial institutions or intermediaries against themselves to raise funds from public.

For examples, bank deposits, life insurance policies, UTI units, IDBI bonds etc.

Functions of Financial System:

The financial system helps production, capital accumulation, and growth by (i) encouraging savings, (ii)

mobilising them, and (iii) allocating them among alternative uses and users. Each of these

functions is important and the efficiency of a given financial system depends on how well it

performs each of these functions.

(i) Encourage Savings:

Financial system promotes savings by providing a wide array of financial assets as stores of value aided

by the services of financial markets and intermediaries of various kinds. For wealth holders, all

this offers ample choice of portfolios with attractive combinations of income, safety and yield.

With financial progress and innovations in financial technology, the scope of portfolio choice has also

improved. Therefore, it is widely held that the savings-income ratio is directly related to both

financial assets and financial institutions. That is, financial progress generally insures larger

savings out of the same level of real income.

As stores of value, financial assets command certain advantages over tangible assets (physical capital,

inventories of goods, etc.) they are convenient to hold, or easily storable, more liquid, that is

more easily encashable, more easily divisible, and less risky.

A very important property of financial assets is that they do not require regular management of the kind

most tangible assets do. The financial assets have made possible the separation of ultimate

ownership and management of tangible assets. The separation of savings from management has

encouraged savings greatly.

Savings are done by households, businesses, and government. Following the official classification

adopted by the Central Statistical Organization (CSO), Government of India, we reclassify savers

into— household sector, domestic private corporate sector, and the public sector.

The household sector is defined to comprise individuals, non-Government, non-corporate entities in

agriculture, trade and industry, and non-profit making organisations like trusts and charitable

and religious institutions.

The public sector comprises Central and state governments, departmental and non departmental

undertakings, the RBI, etc. The domestic private corporate sector comprises non-government

public and private limited companies (whether financial or non-financial) and corrective

institutions.

Of these three sectors, the dominant saver is the household sector, followed by the domestic private

corporate sector. The contribution of the public sector to total net domestic savings is relatively

small.

(ii) Mobilisation of Savings:

Financial system is a highly efficient mechanism for mobilising savings. In a fully-monetised economy

this is done automatically when, in the first instance, the public holds its savings in the form of

money. However, this is not the only way of instantaneous mobilisation of savings.

Other financial methods used are deductions at source of the contributions to provident fund and other

savings schemes. More generally, mobilisation of savings taken place when savers move into

financial assets, whether currency, bank deposits, post office savings deposits, life insurance

policies, bill, bonds, equity shares, etc.

(iii) Allocation of Funds:

Another important function of a financial system is to arrange smooth, efficient, and socially equitable

allocation of credit. With modem financial development and new financial assets, institutions

and markets have come to be organised, which are replaying an increasingly important role in

the provision of credit.

In the allocative functions of financial institutions lies their main source of power. By granting easy and

cheap credit to particular firms, they can shift outward the resource constraint of these firms

and make them grow faster.

Structure of Indian Financial System:

Financial system operates through financial markets and institutions.

The Indian Financial system (financial markets) is broadly divided under two heads:

(i) Indian Money Market

(ii) Indian Capital Market

The Indian money market is the market in which short-term funds are borrowed and lent. The money

market does not deal in cash, or money but in bills of exchange, grade bills and treasury bills and

other instruments. The capital market in India on the other hand is the market for the medium

term and long term funds.

The role of financial systems in the economy

This section discusses the main functions of financial intermediaries and financial markets, and their

comparative roles. Financial systems, i.e. financial intermediaries and financial markets, channel

funds from those who have savings to those who have more productive uses for them. They

perform two main types of financial service that reduce the costs of moving funds between

borrowers and lenders, leading to a more efficient allocation of resources and faster economic

growth. These are the provision of liquidity and the transformation of the risk characteristics of

assets.

Provision of liquidity

The link between liquidity and economic performance arises because many high return investment

projects require long-term commitments of capital, but risk adverse lenders (savers) are

generally unwilling to delegate control over their savings to borrowers (investors) for long

periods. Financial systems mobilise savings by agglomerating and pooling funds from disparate

sources and creating small denomination instruments. These instruments provide opportunities

for individuals to hold diversified portfolios. Without pooling individuals and households would

have to buy and sell entire firms (Levine 1997).

Financial markets can also transform illiquid assets (long-term capital investments in illiquid production

processes) into liquid liabilities (financial instrument). With liquid financial markets

savers/lenders can hold assets like equity or bonds, which can be quickly and easily converted

into purchasing power, if they need to access their savings.

For lenders, the services performed by financial markets and intermediaries are substitutable around

the desired risk, return and liquidity provided by particular investments. Financial intermediaries

and markets make longer-term investments more attractive and facilitate investment in higher

return, longer gestation investment and technologies. They provide different forms of finance to

borrowers. Financial markets provide arms length debt or equity finance (to those firms able to

access markets), often at a lower cost than finance from financial intermediaries.

Transformation of the risk characteristics of assets

The second main service financial intermediaries and markets provide is the transformation of the risk

characteristics of assets. Financial systems perform this function in at least two ways. First, they

can enhance risk diversification and second, they resolve an information asymmetry problem

that may otherwise prevent the exchange of goods and services, in this case the provision of

capital (Akerlof 1970).

Financial systems facilitate risk-sharing by reducing information and transactions costs. If there are costs

associated with the channelling of funds between borrowers and lenders, financial systems can

reduce the costs of holding a diversified portfolio of assets. Intermediaries perform this role by

taking advantage of economies of scale, markets do so by facilitating the broad offer and trade

of assets comprising investors’ portfolios.

Financial systems can reduce information and transaction costs that arise from an information

asymmetry between borrowers and lenders. In credit markets an information asymmetry arises

because borrowers generally know more about their investment projects than lenders. A

borrower may have an entrepreneurial “gut feeling” that can not be communicated to lenders,

or more simply, may have information about a looming financial risk to their firm that they may

not wish to share with past or potential lenders. An information asymmetry can occur ex ante or

ex post. An ex ante information asymmetry arises when lenders can not differentiate between

borrowers with different credit risks before providing a loan and leads to an adverse selection

problem. Adverse selection problems arise when lenders are more likely to make a loan to high-

risk borrowers, because those who are willing to pay high interest rates will, on average, be

worse risks.

The problem with imperfect information is that information is a “public good”. If costly privately-

produced information can subsequently be used at less cost by other agents, there will be

inadequate motivation to invest in the publicly optimal quantity of information (Hirshleifer and

Riley 1979). The implication for financial intermediaries is as follows. Once financial

intermediaries obtain information they must be able to obtain a market return on that

information before any signalling of that information advantage results in it being bid away. If

they can not prevent information from being revealed prior to obtaining that return, they will

not commit the resources necessary to obtain it. One reason financial intermediaries can obtain

information at a lower cost than individual lenders is that financial intermediation avoids

duplication of the production of information faced by multiple individual lenders. Moreover,

financial intermediaries develop special skills in evaluating prospective borrowers and

investment projects. They can also exploit cross- customer information and re-use information

over time. Financial intermediaries thus improve the screening of potential borrowers and

investment projects before finance is committed and enforce monitoring and corporate control

after investment projects have been funded. Financial intermediation thus leads to a more

efficient allocation of capital. The information acquisition cost may be lowered further as

financial intermediaries and borrowers develop long-run relationships (Petersen and Rajan 1994

and Faulkender and Petersen 2003).

Financial markets create their own incentives to acquire and process information for listed firms. The

larger and more liquid financial markets become the more incentive market participants have to

collect information about these firms. However, because information is quickly revealed in

financial markets through posted prices, there may be less of an incentive to use private

resources to acquire information. In financial markets information is aggregated and

disseminated through published prices, which means that agents who do not undertake the

costly process of ex ante screening and ex post monitoring, can freely observe the information

obtained by other investors as reflected in financial prices. Rules and regulation, such as

continuous disclosure requirements, can help encourage the production of information.

Financial intermediaries and financial markets resolve ex post information asymmetries and the

resulting moral hazard problem by improving the ability of investors to directly evaluate the

returns to projects by monitoring, by increasing the ability of investors to influence

management decisions and by facilitating the takeover of poorly managed firms. When these

issues are not well managed, investors will not be willing to delegate control of their savings to

borrowers. Diamond (1984), for example, develops a model in which the returns from firms’

investment projects are not known ex post to external investors, unless information is gathered

to assess the outcome, i.e. there is “costly state verification” (Townsend 1979). This leads to a

moral hazard problem. Moral hazard arises when a borrower engages in activities that reduce

the likelihood of a loan being repaid. For example, when firms’ owners “siphon off” funds

(legally or illegally) to themselves or their associates through loss-making contracts signed with

associated firms.

Fund Based Services

● WORKING CAPITAL FINANCING:

A firm's working capital is the money available to meet current obligations (those due in less

than a year) and to acquire earning assets. Chinatrust Commercial Bank offers corporations

Working Capital Finance to meet their operating expenses, purchasing inventory, receivables

financing, either by direct funding or by issuing letter of credit.

Key Benefits

Funded facilities, i.e. the bank provides funding and assistance to actually purchase business

assets or to meet business expenses.

Non-Funded facilities, i.e. the bank can issue letters of credit or can give a guarantee on behalf

of the customer to the suppliers, Government Departments for the procurement of goods and

services on credit.

Available in both Indian as well as Foreign currency.

● SHORT TERM FINANCING

The bank can structure low cost credit programmes and cash flow financing to meet your

specific short-term cash requirements. The loans are structured to enhance your profitability by

scheduling the repayment to match the cash flow available to repay the debt.

● BILL DISCOUNTING

Bill discounting is a short tenure financing instrument for companies willing to discount their

purchase / sales bills to get funds for the short run and as for the investors in them. These are

customized to suit your requirement for short-term finance, from the date of sale to the date of

receipt of payment there on.

We consider two types of bills facility viz. where documents are delivered on payment, i.e. D/P

Bills and where the documents are delivered against acceptance i.e. D/A Bills.

● EXPORT CREDIT

We offer short-term working capital finance both at the pre-shipment and post-shipment stages

Pre-shipment finance facility provides liquidity for procuring raw materials, processing, packing,

transporting, meant for export.

Post-shipment finance is a credit facility extended from the date of shipment of goods till the

realization of the export proceeds. The different types of post-shipment advances include:

Export bills purchased/discounted

Export bills negotiated (against letter of credit)

Advances against bills sent on collection basis

Advances against exports on consignment basis

Exporters have the option of availing Post-Shipment finance either in rupees or in foreign currency.

● STRUCTURED FINANCE

Structured Finance describes any "non-standard" way of raising money. These tailor-made

securities go beyond "standard" securities like conventional loans, debentures, debt, and equity.

The reason to structure a more advanced security may be that conventional securities may be

unattractive, unavailable or too expensive. These products are structured for both long and

short tenor with exit options at intervals for both parties.

● TERM LENDING

CTCB offers very competitive rates for term financing. We also provide advisory services to

companies for syndication of the term loans to a wide spectrum of financial institutions.

Under Term Finance, Chinatrust Commercial Bank, offers the following:

Fund Based Finance for capital expenditure acquisition of fixed assets towards starting or

expanding a business to swap with high cost existing debt from other bank / financial institution

Non-Fund Based Finance in the form of Deferred Payment Guarantee for acquisition of fixed

assets towards starting / expanding a business or industrial unit.

A financial system refers to a system which enables the transfer of money between investors and borrowers.

A financial system could be defined at an international, regional or organization level. The term “system” in

“Financial System” indicates a group of complex and closely linked institutions, agents, procedures, markets,

transactions, claims and liabilities within a economy.

Five Basic Components of Financial System

Financial Institutions

Financial Markets

Financial Instruments (Assets or Securities)

Financial Services

Money

Financial Institutions

Financial institutions facilitate smooth working of the financial system by making investors and borrowers meet.

They mobilize the savings of investors either directly or indirectly via financial markets, by making use of

different financial instruments as well as in the process using the services of numerous financial services

providers. They could be categorized into Regulatory, Intermediaries, Non-intermediaries and Others. They

offer services to organizations looking for advises on different problems including restructuring to diversification

strategies. They offer complete array of services to the organizations who want to raise funds from the markets

and take care of financial assets for example deposits, securities, loans, etc.

Figure 1: Five Basic Components of Financial System

Financial Markets

A financial market is the place where financial assets are created or transferred. It can be broadly categorized

into money markets and capital markets. Money market handles short-term financial assets (less than a year)

whereas capital markets take care of those financial assets that have maturity period of more than a year. The

key functions are:

1. Assist in creation and allocation of credit and liquidity.

2. Serve as intermediaries for mobilization of savings.

3. Help achieve balanced economic growth.

4. Offer financial convenience.

One more classification is possible: primary markets and secondary markets. Primary markets handles new

issue of securities in contrast secondary markets take care of securities that are presently available in the stock

market.

Financial markets catch the attention of investors and make it possible for companies to finance their

operations and attain growth. Money markets make it possible for businesses to gain access to funds on a

short term basis, while capital markets allow businesses to gain long-term funding to aid expansion. Without

financial markets, borrowers would have problems finding lenders. Intermediaries like banks assist in this

procedure. Banks take deposits from investors and lend money from this pool of deposited money to people

who need loan. Banks commonly provide money in the form of loans.

Financial Instruments

This is an important component of financial system. The products which are traded in a financial market are

financial assets, securities or other type of financial instruments. There is a wide range of securities in the

markets since the needs of investors and credit seekers are different. They indicate a claim on the settlement

of principal down the road or payment of a regular amount by means of interest or dividend. Equity shares,

debentures, bonds, etc are some examples.

Financial Services

Financial services consist of services provided by Asset Management and Liability Management Companies.

They help to get the necessary funds and also make sure that they are efficiently deployed. They assist to

determine the financing combination and extend their professional services upto the stage of servicing of

lenders. They help with borrowing, selling and purchasing securities, lending and investing, making and

allowing payments and settlements and taking care of risk exposures in financial markets. These range from

the leasing companies, mutual fund houses, merchant bankers, portfolio managers, bill discounting and

acceptance houses. The financial services sector offers a number of professional services like credit rating,

venture capital financing, mutual funds, merchant banking, depository services, book building, etc. Financial

institutions and financial markets help in the working of the financial system by means of financial instruments.

To be able to carry out the jobs given, they need several services of financial nature. Therefore, Financial

services are considered as the 4th major component of the financial system.

Money

Money is understood to be anything that is accepted for payment of products and services or for the repayment

of debt. It is a medium of exchange and acts as a store of value.

Characteristics of financial service firms

There are many dimensions on which financial service firms differ from other firms in

the market. In this section, we will focus on four key differences and look at why these

differences can create estimation issues in valuation. The first is that many categories (albeit not

all) of financial service firms operate under strict regulatory constraints on how they run their

businesses and how much capital they need to set aside to keep operating. The second is that

accounting rules for recording earnings and asset value at financial service firms are at variance

with accounting rules for the rest of the market. The third is that debt for a financial service firm

is more akin to raw material than to a source of capital; the notion of cost of capital and

enterprise value may be meaningless as a consequence. The final factor is that the defining

reinvestment (net capital expenditures and working capital) for a bank or insurance company

may be not just difficult, but impossible, and cash flows cannot be computed.

The Regulatory Overlay

Financial service firms are heavily regulated all over the world, though the extent of the

regulation varies from country to country. In general, these regulations take three forms. First,

banks and insurance companies are required to maintain regulatory capital ratios, computed

based upon the book value of equity and their operations, to ensure that they do not expand

beyond their means and put their claimholders or depositors at risk. Second, financial service

firms are often constrained in terms of where they can invest their funds. For instance, until a

decade ago, the Glass-Steagall Act in the United States restricted commercial banks from

investment banking activities as well as from taking active equity positions in non-financial

service firms. Third, the entry of new firms into the business is often controlled by the

regulatory authorities, as are mergers between existing firms.

Differences in Accounting Rules

The accounting rules used to measure earnings and record book value are different for

financial service firms than the rest of the market, for two reasons. The first is that the assets of

financial service firms tend to be financial instruments (bonds, securitized obligations) that often

have an active market place. Not surprisingly, marking assets to market value has been an

established practice in financial service firms, well before other firms even started talking about

fair value accounting. The second is that the nature of operations for a financial service firm is

such that long periods of profitability are interspersed with short periods of large losses;

accounting standard have been developed to counter this tendency and create smoother earnings.

a. Mark to Market: If the new trend in accounting is towards recording assets at fair value

(rather than original costs), financial service firms operate as a laboratory for this experiment.

After all, accounting rules for banks, insurance companies and investment banks have

required that assets be recorded at fair value for more than a decade, based upon the

argument that most of a bank�s assets are traded, have market prices and therefore do not

require too many subjective judgments. In general, the assets of banks and insurance

companies tend to be securities, many of which are publicly traded. Since the market price is

observable for many of these investments, accounting rules have tilted towards using market

value (actual of estimated) for these assets. To the extent that some or a significant portion

of the assets of a financial service firms are marked to market, and the assets of most non-

financial service firms are not, we fact two problems. The first is in comparing ratios based

upon book value (both market to book ratios like price to book and accounting ratios like

return on equity) across financial and non-financial service firms. The second is in

interpreting these ratios, once computed. While the return on equity for a non-financial

service firm can be considered a measure of return earned on equity invested originally in

assets, the same cannot be said about return on equity at financial service firms, where the

book equity measures not what was originally invested in assets but an updated market value.

b. Loss Provisions and smoothing out earnings: Consider a bank that makes money the old

fashioned way – by taking in funds from depositors and lending these funds out to

individuals and corporations at higher rates. While the rate charged to lenders will be higher

than that promised to depositors, the risk that the bank faces is that lenders may default, and

the rate at which they default will vary widely over time – low during good economic times

and high during economic downturns. Rather than write off the bad loans, as they occur,

banks usually create provisions for losses that average out losses over time and charge this

amount against earnings every year. Though this practice is logical, there is a catch, insofar

as the bank is given the responsibility of making the loan loss assessment. A conservative

bank will set aside more for loan losses, given a loan portfolio, than a more aggressive bank,

and this will lead to the latter reporting higher profits during good times.

Debt and Equity

In the financial balance sheet that we used to describe firms, there are only two ways to

raise funds to finance a business – debt and equity. While this is true for both all firms, financial

service firms differ from non-financial service firms on three dimensions:

a. Debt is raw material, not capital: When we talk about capital for non-financial service firms,

we tend to talk about both debt and equity. A firm raises funds from both equity investor and

bondholders (and banks) and uses these funds to make its investments. When we value the firm,

we value the value of the assets owned by the firm, rather than just the value of its equity. With a

financial service firm, debt has a different connotation. Rather than view debt as a source of

capital, most financial service firms seem to view it as a raw material. In other words, debt is to a

bank what steel is to a manufacturing company, something to be molded into other products

which can then be sold at a higher price and yield a profit. Consequently, capital at financial

service firms seems to be narrowly defined as including only equity capital. This definition of

capital is reinforced by the regulatory authorities, who evaluate the equity capital ratios of banks

and insurance firms.

b. Defining Debt: The definition of what comprises debt also is murkier with a financial service

firm than it is with a non-financial service firm. For instance, should deposits made by customers

into their checking accounts at a bank be treated as debt by that bank? Especially on interest-

bearing checking accounts, there is little distinction between a deposit and debt issued by the

bank. If we do categorize this as debt, the operating income for a bank should be measured prior

to interest paid to depositors, which would be problematic since interest expenses are usually the

biggest single expense item for a bank.

c. Degree of financial leverage: Even if we can define debt as a source of capital and can

measure it precisely, there is a final dimension on which financial service firms differ from other

firms. They tend to use more debt in funding their businesses and thus have higher financial

leverage than most other firms. While there are good reasons that can be offered for why they

have been able to do this historically - more predictable earnings and the regulatory framework

are two that are commonly cited – there are consequences for valuation. Since equity is a sliver

of the overall value of a financial service firm, small changes in the value of the firm�s assets

can translate into big swings in equity value.

Changes have been taken place in the Indian financial system since independencs

The role of financial system in economic development has been a much discussed topic among economists. Is

it possible to influence the level of national income, employment, standard of living, and social welfare through

variations in the supply of fiancé?

Following section provides a brief history of India's shift from financial repression to financial liberalization.

Seven interrelated challenges that India faces in its second wave of financial sector reforms:

1. reducing the fiscal deficit, to reduce the risk of macroeconomic instability and to increase the

availability of finance to the private sector;

2. improving the legal, regulatory and supervisory frameworks, in order to improve banks' credit and risk

management;

3. improving systems for dealing with weak banks;

4. developing capital markets further,

5. developing pensions and insurance to increase finance for long term investments, including

infrastructure;

6. improving financial services to improve the welfare of customers and meet the challenge of

globalization of financial services; and

7. managing links to external capital markets;

and possible approaches to meeting these challenges.

The organization of the Indian financial system before 1951 had a close resemblance with the theoretical model

of a financial organization in a traditional economy. A traditional economy, according to R. L. Bennett, “is one in

which the per capital output is low and constant.”

The main elements of the financial organization in planned economic development could be categorized into

four broad groups:

a. Public /Government ownership of financial institutions.

b. Fortification of the institutional structure.

c. Protection to investors and

d. Participation of financial institutions in corporate management.

The organization of the Indian financial system, since the mid-eighties in general, and the launching of the new

economic policy in 1991 in particular, has been characterized by profound transformation.

Needs for economic reforms or new economic policy was felt mainly because of the following reasons:

Increasing in fiscal deficit was main reason to bring new economic policy. It was 5.4% of gross domestic

product in 1981-82 and rose up to 8.4 % of GDP in 1990-91.

Disequilibrium in balance of payment is occurred when total imports exceed the total exports. In 1980-81 it was

adverse with the Rs. 2,214 Crores and rose up to 17,367 Crores in 1990-91.

Petrol priceswere at high at the time of Iran war in 1990-91 and during that time India did not get any

remittances from gulf countries and which lead to adverse balance of payment. It was called Gulf Crisis.

Diminishing foreign reserves were not sufficient even to pay two weeks' imports in 1990-91. Reserves were Rs

8151 crores in 1986-87, declined up to 6252 crores in 1989-90.

Increasing pressure of inflation due to rise in prices. Cost of production is high due to high rate of inflation

which affects the domestic and foreign demand.

Lack of sufficient gain form public sector in recent years due to poor performance of some of the public sector

enterprises and suffered loss.

On view of above reasons it was inevitable for the government to adopt new economic policy.

The notable developments in the organization of the Indian financial system during this phase are briefly

outlined below with reference to (i) privatization of financial institutions (ii) reorganization of institutional

structure and (iii) investor protection. The phase III organization of the Indian financial system is portrayed in

the figure 1:-

Post -1991 phase organization of the Indian Financial System

Main Features of economic reforms

Privatization

Globalization

Liberalization

In the context of economic reforms, Privatizationmeans allowing the private sector to setup more and more of

such industries as were previously reserved for public sector. Under it existing enterprises of the public sector

are either wholly or partially sold to private sector.

Privatization was brought due to less output of public sector. It was just due to lack of decision making of

managers in public sector enterprises who always took decisions over a long time. Consequently productivity of

the public sector was to go down. In view of these reasons privatization was brought into existence so that

there would be more competition, quality of production and customer may be benefited.

Following measures were adopted in respect of privatization under economic reforms:

Sale of Public sector securities

Disinvestment in public sector

Number of industries exclusively reserved for public sector was reduced from 17 to 4

Investment in private sector was at maximum

Globalizationmeans integrating the economy of a country with the economies of other countries under condition

of freer flow of trade and capital and movement of persons across borders.

In the globalization policy it was assumed that Indian economy should have linked with the rest of world so that

there may be mutual cooperation of Indian economy with the rest of the world. Following measures were

adopted under the globalization of Indian economy are as under:

Foreign investment limit raised i.e. 40 percent to 51percent.

Devaluationwas taken place in 1991 to the extent of 20 percent on an average to promote export, import

substitution and foreign capital.

Before 1991 government had imposed many controls like restrictions on big house investment,

licensing policy, foreign exchange controls etc. but these controls spread over the economy only

corruption, long time process, political interference, and inefficiency. The rate of growth was fallen

down and reserves of foreign exchange were just sufficient to cater the needs of two weeks' import

only. There was political instability, inflation, gulf crisis, rising deficit in balance of payments etc. To

bring the economic stability and put the economy into the path of consistent growth it was must to

remove the curb rising pricing, correct adverse balance of payments etc.

UNIT-2

Bank

An establishment authorized by a government to accept deposits, pay interest, clear checks, make loans, act

as an intermediary in financial transactions, and provide other financial services to its customers.

In simple words, Banking can be defined as the business activity of accepting and safeguarding money owned

by other individuals and entities, and then lending out this money in order to earn a profit.

Banking systems can be defined as a mechanism through which the money supply of the country is created

and controlled.

In 1839, some Indian merchants in Calcutta established India's first bank known as "Union Bank", but it could

not survive for long and failed in 1848 due to economic crisis of 1848-49. Similarly, in 1863, "Bank of Upper

India" was formed but it failed in 1913.

In 1865, "Allahabad Bank" was established as a joint stock bank. This bank has survived till date and is now

considered as the oldest surviving bank in India.

What are the Functions of Banks? Diagram

The functions of banks are briefly highlighted in following Diagram or Chart.

These functions of banks are explained in following paragraphs of this article.

A. Primary Functions of Banks

The primary functions of a bank are also known as banking functions. They are the main functions of a bank.

These primary functions of banks are explained below.

1. Accepting Deposits

The bank collects deposits from the public. These deposits can be of different types, such as :-

a. Saving Deposits

b. Fixed Deposits

c. Current Deposits

d. Recurring Deposits

a. Saving Deposits

This type of deposits encourages saving habit among the public. The rate of interest is low. At present it is

about 4% p.a. Withdrawals of deposits are allowed subject to certain restrictions. This account is suitable to

salary and wage earners. This account can be opened in single name or in joint names.

b. Fixed Deposits

Lump sum amount is deposited at one time for a specific period. Higher rate of interest is paid, which varies

with the period of deposit. Withdrawals are not allowed before the expiry of the period. Those who have

surplus funds go for fixed deposit.

c. Current Deposits

This type of account is operated by businessmen. Withdrawals are freely allowed. No interest is paid. In fact,

there are service charges. The account holders can get the benefit of overdraft facility.

d. Recurring Deposits

This type of account is operated by salaried persons and petty traders. A certain sum of money is periodically

deposited into the bank. Withdrawals are permitted only after the expiry of certain period. A higher rate of

interest is paid.

2. Granting of Loans and Advances

The bank advances loans to the business community and other members of the public. The rate charged is

higher than what it pays on deposits. The difference in the interest rates (lending rate and the deposit rate) is

its profit.

The types of bank loans and advances are :-

a. Overdraft

b. Cash Credits

c. Loans

d. Discounting of Bill of Exchange

a. Overdraft

This type of advances are given to current account holders. No separate account is maintained. All entries are

made in the current account. A certain amount is sanctioned as overdraft which can be withdrawn within a

certain period of time say three months or so. Interest is charged on actual amount withdrawn. An overdraft

facility is granted against a collateral security. It is sanctioned to businessman and firms.

b. Cash Credits

The client is allowed cash credit upto a specific limit fixed in advance. It can be given to current account

holders as well as to others who do not have an account with bank. Separate cash credit account is

maintained. Interest is charged on the amount withdrawn in excess of limit. The cash credit is given against

the security of tangible assets and / or guarantees. The advance is given for a longer period and a larger

amount of loan is sanctioned than that of overdraft.

c. Loans

It is normally for short term say a period of one year or medium term say a period of five years. Now-a-days,

banks do lend money for long term. Repayment of money can be in the form of installments spread over a

period of time or in a lumpsum amount. Interest is charged on the actual amount sanctioned, whether

withdrawn or not. The rate of interest may be slightly lower than what is charged on overdrafts and cash

credits. Loans are normally secured against tangible assets of the company.

d. Discounting of Bill of Exchange

The bank can advance money by discounting or by purchasing bills of exchange both domestic and foreign

bills. The bank pays the bill amount to the drawer or the beneficiary of the bill by deducting usual discount

charges. On maturity, the bill is presented to the drawee or acceptor of the bill and the amount is collected.

B. Secondary Functions of Banks

The bank performs a number of secondary functions, also called as non-banking functions.

These important secondary functions of banks are explained below.

1. Agency Functions

The bank acts as an agent of its customers. The bank performs a number of agency functions which includes :-

a. Transfer of Funds

b. Collection of Cheques

c. Periodic Payments

d. Portfolio Management

e. Periodic Collections

f. Other Agency Functions

a. Transfer of Funds

The bank transfer funds from one branch to another or from one place to another.

b. Collection of Cheques

The bank collects the money of the cheques through clearing section of its customers. The bank also collects

money of the bills of exchange.

c. Periodic Payments

On standing instructions of the client, the bank makes periodic payments in respect of electricity bills, rent,

etc.

d. Portfolio Management

The banks also undertakes to purchase and sell the shares and debentures on behalf of the clients and

accordingly debits or credits the account. This facility is called portfolio management.

e. Periodic Collections

The bank collects salary, pension, dividend and such other periodic collections on behalf of the client.

f. Other Agency Functions

They act as trustees, executors, advisers and administrators on behalf of its clients. They act as

representatives of clients to deal with other banks and institutions.

2. General Utility Functions

The bank also performs general utility functions, such as :-

a. Issue of Drafts, Letter of Credits, etc.

b. Locker Facility

c. Underwriting of Shares

d. Dealing in Foreign Exchange

e. Project Reports

f. Social Welfare Programmes

g. Other Utility Functions

a. Issue of Drafts and Letter of Credits

Banks issue drafts for transferring money from one place to another. It also issues letter of credit, especially

in case of, import trade. It also issues travellers' cheques.

b. Locker Facility

The bank provides a locker facility for the safe custody of valuable documents, gold ornaments and other

valuables.

c. Underwriting of Shares

The bank underwrites shares and debentures through its merchant banking division.

d. Dealing in Foreign Exchange

The commercial banks are allowed by RBI to deal in foreign exchange.

e. Project Reports

The bank may also undertake to prepare project reports on behalf of its clients.

f. Social Welfare Programmes

It undertakes social welfare programmes, such as adult literacy programmes, public welfare campaigns, etc.

g. Other Utility Functions

It acts as a referee to financial standing of customers. It collects creditworthiness information about clients of

its customers. It provides market information to its customers, etc. It provides travellers' cheque facility.

Banks are those institutions which conduct the business purely on profit motive. Banks receive surplus

money from the people who are not using it and lend to those who need it for productive purpose. When we

speak of abank, we generally mean a commercial bank. Commercial banks are those institutions which

conduct the business purely on profit motive. Commercial banks receive surplus money from the people who

are not using it and lend to those who need it for productive purpose.

A commercial bank is a dealer in short and medium-term credit. It borrows money from a group of people at a

lower rate of interest and lends to the other group of people at some higher rate of interest. The difference

between the two rates of interest is the profit of the bank.

1. Definition Of A Commercial Bank:

Some important definitions of commercial bank are given below.

"A bank is a firm which collects money from those who have it spare. It lends to those who require it."

1.2. Professor Parking:

"A bank is a firm that takes deposits from households and firms and makes loans to other household and

firms.

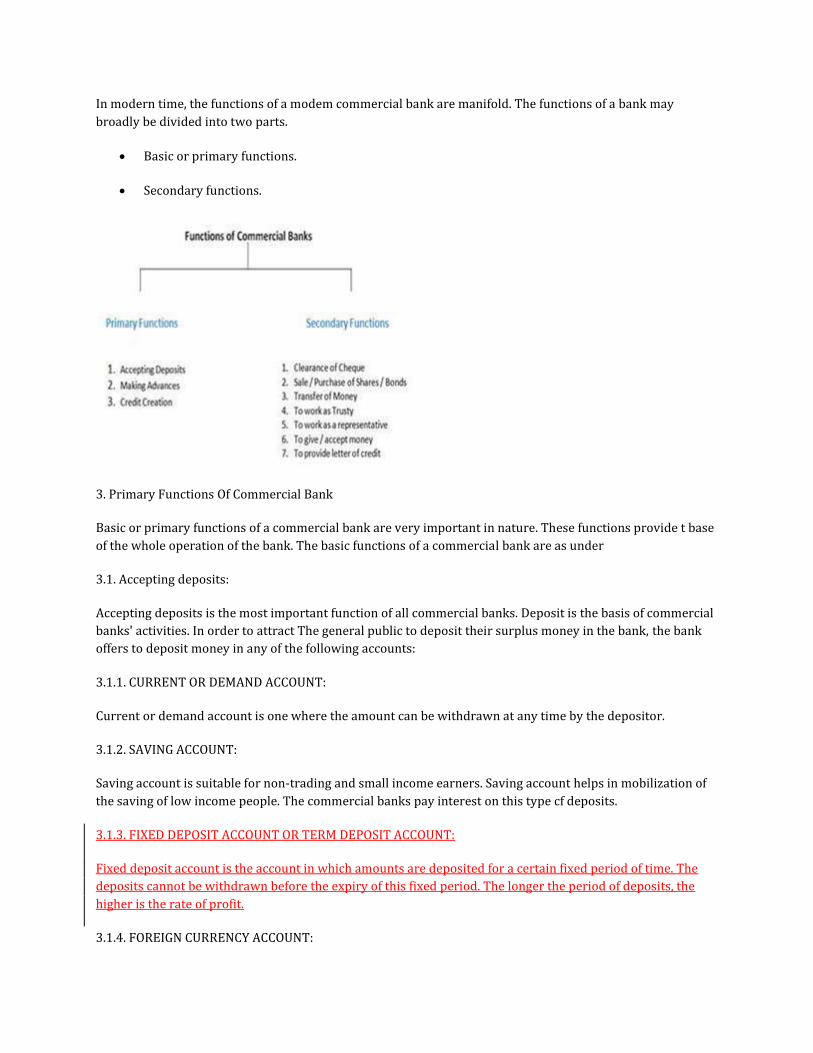

2. Functions Of Commercial Bank:

In modern time, the functions of a modem commercial bank are manifold. The functions of a bank may

broadly be divided into two parts.

Basic or primary functions.

Secondary functions.

3. Primary Functions Of Commercial Bank

Basic or primary functions of a commercial bank are very important in nature. These functions provide t base

of the whole operation of the bank. The basic functions of a commercial bank are as under

3.1. Accepting deposits:

Accepting deposits is the most important function of all commercial banks. Deposit is the basis of commercial

banks' activities. In order to attract The general public to deposit their surplus money in the bank, the bank

offers to deposit money in any of the following accounts:

3.1.1. CURRENT OR DEMAND ACCOUNT:

Current or demand account is one where the amount can be withdrawn at any time by the depositor.

3.1.2. SAVING ACCOUNT:

Saving account is suitable for non-trading and small income earners. Saving account helps in mobilization of

the saving of low income people. The commercial banks pay interest on this type cf deposits.

3.1.3. FIXED DEPOSIT ACCOUNT OR TERM DEPOSIT ACCOUNT:

Fixed deposit account is the account in which amounts are deposited for a certain fixed period of time. The

deposits cannot be withdrawn before the expiry of this fixed period. The longer the period of deposits, the

higher is the rate of profit.

3.1.4. FOREIGN CURRENCY ACCOUNT:

Foreign currency account is opened only in authorized branches. A foreign currency account may be a foreign

currency saving account or foreign currency term deposit account. Foreign currency account in Pakistan can

be opened in USA Dollar, UK Pound, German Mark, Japanese Yen, etc. This account is exempted from all taxes

and deduction. No income tax or Zakat is deducted from this account.

3.2. Advancing Loans:

The second important function of commercial bank is advancing loans to the individuals, businessmen and

government bodies. The loans are granted out of deposited money. Generally, a commercial bank grants

short-term loans.

Banks grant loan in any of the following forms:

3.2.1. OVERDRAFT:

Overdraft is a short-term loan granted by commercial banks to their account holders. Under this type of loan,

the customers are allowed to draw more than what they have in their current accountup to a certain limit.

The excess amount overdrawn is called overdraft.

3.2.2. CASH CREDIT:

Cash credit is a very common form of loan granted by commercial banks to businessmen and industrial units

against the security of goods. The loan granted under this head is credited tocurrent account opened in the

name of borrower. The borrower can withdraw money throughcheques according to his requirement. The

interest is charged on the amount actually withdrawn by the borrower.

3.2.3. LOANS:

Commercial banks grant loans for short and medium-term to individuals and traders against the security of

movable and immovable property. The amount of loan is credited to the borrower's account. Interest is

charged on the entire loan sanctioned.

3.2.4. DISCOUNTING BILLS OF EXCHANGE:

Banks provide short term lean to the businessmen by discounting bills of exchange. Discounting the bills of

exchange means the arrangements of making payments before maturity of bills of exchange. The payment

made by the bank to the holder of bill of exchange before its maturity is the amount of loan. The discount

charged is the earning of the bank.

4. Secondary Functions Of A Commercial Bank:

The secondary functions of commercial bank can be classified under the following heads.

1. Agency functions

2. General utility functions

3. Miscellaneous functions

4.1. Agency Functions:

The banks render important services as agent on behalf of their customers in return for a small commission.

When banks act as agent, law of agency applies. The agency functions or services of bank are as follows:

4.1.1. COLLECTION OF CHEQUES:

Commercial banks collect the cheques, bills of exchange, etc, on behalf of their customers. Banks collect local

and outstation cheques and bills of exchange through clearing house facilities provided by the central bank,

4.1.2. COLLECTION OF INCOME:

The commercial banks collect dividends, interest on investment, pension and rent of property due to the

customers. When any income is collected by the bank, a credit voucher is sent to the customer for

information.

4.1.3. PAYMENT OF EXPENSES:

The banks make payment of insurance premiums, rent, trade subscription, school fee and other obligation of

the customers. When any expense is paid by the bank, a debit voucher is sent to the customer for information.

4.1.4. DEALER IN SECURITIES:

The banks carry out purchase and sale of securities on behalf of their customers. Banks do it well because

they are aware of the market conditions.

4.1.5. ACTS AS TRUSTEE:

The banks act as trustee to manage trust property as per instructions of property owners. Banks are required

to follow the terms and conditions of trust deed.

4.1.6. ACTS AS AN AGENT:

Commercial bank sometimes acts as an agent on behalf of its customers at home or abroad in dealing with

other banks or financial institutions.

4.1.7. OBEYS STANDING INSTRUCTIONS:

Sometimes, customer may order his bank to do something on his behalf regarding the conduct of his account.

This written order is called standing instruction. The bank being the agent of its customer obeys the standing

instructions.

4.1.8. ACTS AS TAX CONSULTANT:

Commercial bank acts as tax consultant to its client. The commercial bank prepares general sales tax return,

income tax return, etc. Tiles the same with tax authorities.

4.2. General Utility Functions:

Commercial bank performs different utility functions for their customers. When bank performs utility

functions, it does not act as an agent of the customers. The general utility functions are as follows:

4.2.1. PROVIDES LOCKERS FACILITIES:

Commercial banks provide lockers facilities to its customers for safe custody of Jewelery, shares, securities

and other valuables. This has minimized the risk of losing due to theft.

4.2.2. ISSUE OF TRAVELER'S CHEQUE:

Bank issues traveler's cheques to the customers for traveling in and outside the country.

4.2.3. FOREIGN EXCHANGE:

Commercial banks deal in foreign exchange. This enables the individuals and businessmen to obtain foreign

currency in exchange of their home currency. For dealing in foreign exchange, commercial banks have to

obtain permission from the central bank.

4.2.4. TRANSFER OF MONEY:

Commercial banks provide facilities for the transfer of money to any place within and outside the country.

The funds are transferred by means of draft, telephonic transfer, electronic transfer etc.

4.2.5. FINANCES FOREIGN TRADE:

A commercial bank finances foreign trade by accepting foreign bills of exchange. Bank also issues letter of

credit on behalf of its customers to facilitate foreign trade. According to Sir John Poget:

"The issuing of letters of credit is the basic function of a bank."

The focus of banking is varied, the needs diverse and methods different. Thus, we need distinctive

kinds of banks to cater to the above-mentioned complexities. Deposit-taking institutions take the form of

commercial banks, which accept deposits and make commercial, real estate, and other loans. There are also

mutual savings banks, which accept deposits and make mortgage and other types of loans. Another type is

credit unions, which are cooperative organizations that issue share certificates and make member (consumer)

and other loans.

The banking industry can be divided into following sectors, based on the clientele served and products and

services offered:

1. Retail Banks

2. Commercial banks

3. Cooperative banks

4. Investment Banks

5. Specialized banks

6. Central banks

Retail Banks:

Retail banks provide basic banking services to individual consumers. Examples include savings banks, savings

and loan associations, and recurring and fixed deposits. Products and services include safe deposit boxes,

checking and savings accounting, certificates of deposit (CDs), mortgages, personal, consumer and car loans.

Commercial Banks:

Banking means accepting deposits of money from the public for the purpose of lending or investment.

Commercial Banks provide financial services to businesses, including credit and debit cards, bank accounts,

deposits and loans, and secured and unsecured loans. Due to deregulation, commercial banks are also

competing more with investment banks in money market operations, bond underwriting, and financial advisory

work. Commercial banks in modern capitalist societies act as financial intermediaries, raising funds from

depositors and lending the same funds to borrowers. The depositors’ claims against the bank, their deposits,

are liquid, meaning banks are expected to redeem deposits on demand, instantly.

Banks’ claims against their borrowers are much less liquid, giving borrowers a much longer span of time to

repay money owed banks. Because a bank cannot immediately reclaim money lent to borrowers, it may face

bankruptcy if all its depositors show up on a given day to withdraw all their money.

There are two types of commercial banks, public sector and private sector banks.

Public Sector Banks:

Public sectors banks are those in which the government has a major stake and they usually need to emphasize

on social objectives than on profitability.

Private sector banks:

Private sector banks are owned, managed and controlled by private promoters and they are free to operate as

per market forces.

Investment Banks:

An investment bank is a financial institution that assists individuals, corporations and governments in raising

capital by underwriting and/or acting as the client's agent in the issuance of securities. An investment bank may

also assist companies involved in mergers and acquisitions, and provide ancillary services such as market

making, trading of derivatives, fixed income instruments, foreign exchange, commodities, and equity securities.

Investment banks aid companies in acquiring funds and they provide advice for a wide range of transactions.

These banks also offer financial consulting services to companies and give advice on mergers and acquisitions

and management of public assets.

Cooperative Banks:

Cooperative Banks are governed by the provisions of State Cooperative Societies Act and meant essentially for

providing cheap credit to their members. It is an important source of rural credit i.e., agricultural financing in

India.

Specialized Banks:

Specialized banks are foreign exchange banks, industrial banks, development banks, export-import banks

catering to specific needs of these unique activities. These banks provide financial aid to industries, heavy

turnkey projects and foreign trade.

Central Banks:

Central banks are bankers’ banks, and these banks trace their history from the Bank of England. They

guarantee stable monetary and financial policy from country to country and play an important role in the

economy of the country. Typical functions include implementing monetary policy, managing foreign exchange

and gold reserves, making decisions regarding official interest rates, acting as banker to the government and

other banks, and regulating and supervising the banking industry.

These banks buy government debt, have a monopoly on the issuance of paper money, and often act as a

lender of last resort to commercial banks. The term bank nowadays refers to these commercial banks. The

Central bank of any country supervises controls and regulates the activities of all the commercial banks of that

country. It also acts as a government banker. It controls and coordinates currency and credit policies of any

country. The Reserve Bank of India is the central bank of India.- Learn more at www.technofunc.com. Your

online source for free professional tutorials.

Banking sector has witnessed enormous growth in the past decades. The banks have transformed themselves

from traditional deposit and borrowing institutes to large organizations offering a variety of services. Discussion

about various classifications of banks.

The banking industry can be divided into two categories commercial banking and investment banking.

Commercial Banking:

This category represents consumer and business banking and includes commercial and foreign banks, savings

and loan associations, credit unions, thrifts, and other savings banks. Commercial banks in modern capitalist

societies act as financial intermediaries, raising funds from depositors and lending the same funds to

borrowers. The depositors’ claims against the bank, their deposits, are liquid, meaning banks are expected to

redeem deposits on demand, instantly. Banks’ claims against their borrowers are much less liquid, giving

borrowers a much longer span of time to repay money owed banks. Because a bank cannot immediately

reclaim money lent to borrowers, it may face bankruptcy if all its depositors show up on a given day to withdraw

all their money.

Products and services include consumer and commercial deposits, consumer loans, mortgage and real estate

loans, overseas operations, investment in high-grade securities, and commercial and industrial loans.

Investment Banking:

The products and services of this category include managing portfolios of financial assets, trading in securities,

fixed income, commodity and currency, corporate advisory services for mergers and acquisitions, corporate

finance, and debt and equity underwriting. Trading activities include trading both on behalf of clients or on the

banks own account.

Other Classifications:

Banking products can be further classified as Retail Banking, Corporate Banking and Risk and Capital

Management. In modern world banks perform and manage all the following functions and different

classifications exist based on the need:

Retail Banking

Corporate Banking

Banking Operations

Risk Management

Asset Management

Wealth Management

Treasury Management

Cards Issuance and Management

Trading Intermediary acting as Depository Participant, Registry, Exchanges, Trading or Broker Dealer

Banking Functions:

The banking industry is growing rapidly. It's estimated that the assets of the 1,000 largest banks are worth

almost $100 trillion USD. With the growth in the industry banks manages a diverse portfolio of functions. Apart

from the segments discussed above banks also need to manage following functions and can also be classified

based on functions:

Banking Technology

Internal and External Reconciliations

Internal and External Clearing

Surveillance

Human Resources

Finance

Legal and Compliance

Sales and Trading

Transaction Banking

Banking sector in India has witnessed unparalled growth in the last decade.- Learn more at

www.technofunc.com. Your online source for free professional tutorials.

Commercial banks: These banks function to help the entrepreneurs and businesses. They

give financial services to these businessmen like debit cards, banks accounts, short term

deposits, etc. with the money people deposit in such banks. They also lend money to

businessmen in the form of overdrafts, credit cards, secured loans, unsecured loans and

mortgage loans to businessmen. The commercial banks in the country were nationalized in

1969. So the various policies regarding the loans, rates of interest and loans etc are

controlled by the Reserve Bank. These days, the commercialized banks provide some

services given by investment banks to their clients.

The commercial banks can be further classifies as: public sector bank, private sector banks,

foreign banks and regional banks.

1. The public sector banks are owned and operated by the government, who has a

major share in them. The major focus of these banks is to serve the people rather

earn profits. Some examples of these banks include State Bank of India, Punjab

National Bank, Bank of Maharashtra, etc.

2. The private sector banks are owned and operated by private institutes. They are

free to operate and are controlled by market forces. A greater share is held by

private players and not the government. For example, Axis Bank, Kotak Mahindra

Bank etc.

3. The foreign banks are those that are based in a foreign country but have several

branches in India. Some examples of these banks include; HSBC, Standard Chartered

Bank etc.

4. The regional rural banks were brought into operation with the objective of

providing credit to the rural and agricultural regions and were brought into effect in

1975 by RRB Act. These banks are restricted to operate only in the areas specified by

government of India. These banks are owned by State Government and a sponsor

bank. This sponsorship was to be done by a nationalized bank and a State

Cooperative bank. Prathama Bank is one such example, which is located in

Moradabad in U.P.

Cooperative banks: These banks are controlled, owned, managed and operated by cooperative

societies and came into existence under the Cooperative Societies Act in 1912. these banks are

located in the urban as well in the rural areas. Although these banks have the same functions as the

commercial banks, they provide finance to farmers, salaried people, small scale industries, etc. and

their rates of interest of interest are lower as compared to other banks.

There are three types of cooperative banks in India, namely:

1. Primary credit societies: These are formed in small locality like a small town or a

village. The members using this bank usually know each other and the chances of

committing fraud is minimal.

2. Central cooperative banks: These banks have their members who belong to the

same district. They function as other commercial banks and provide loans to their

members. They act as a link between the state cooperative banks and the primary

credit societies.

3. State cooperative banks: these banks have a presence in all the states of the

country and have their presence throughout the state.

Various Types of Banks and Their Functions – Banking Study Material & Notes

Broadly, banks are classified either into commercial banks or as central bank. they are also classified as

Scheduled and Non-scheduled Banks.

Scheduled banks have been included in the second schedule of the Reserve Bank, and fulfils the following

three criteria:

1. It must have a paid up capital of at least Rs. 5 lakhs.

2. It must fulfil the RBI norms about no activity that may be detrimental to the depositors interests.

3. It must be a Corporation(not a partnership or a single ownership firm).

Non-Scheduled Banks are excluded from the Second schedule of RBI. The Reserve Bank does not exercise

much control over them, but they report monthly to RBI.

I. Public Sector Banks – Majority stake is held by Government

State Bank of India and its associate banks: These associate banks are State Bank of Bikaner &

Jaipur, State Bank of Hyderabad, State Bank of Mysore, State Bank of Patiala, and State Bank of

Travancore.

Nationalised Banks– These are those commercial banks that have been nationalized for fulfilling the

social objectives of the government. There are 20 Nationalised banks in India. These are – Allahabad

Bank, Andhra Bank, Bank of Maharashtra, Bank of Baroda, Canara Bank, Central Bank of India, Bank

of India, , Corporation Bank, Dena Bank, Indian Overseas Bank, IDBI Bank Ltd., Oriental Bank of

Commerce, Indian Bank, Punjab & Sind Bank, Punjab National Bank, Union Bank of India, Syndicate

Bank, United Bank of India,UCO Bank, and Vijaya Bank.

Regional Rural Banks(RRB)– These banks have been established to strengthen the rural economy.

They facilitate the credit and deposit flow for farmers, artisans, labourers in their limited local area.

These banks are jointly owned by the central and state government along with a sponsor commercial

bank.

II. Private Sector Banks – Majority share capital is with private individuals & corporates

Old Private Banks – There are fourteen old private banks operating in India. These banks were not

nationalised when other banks were nationalised in 1969 and 1980. These are- Catholic Syrian Bank

Ltd., Dhanalakshmi Bank Ltd., City Union Bank Ltd., Federal Bank Ltd., Lakshmi Vilas Bank Ltd., ING

Vysya Bank Ltd., Karur Vysya Bank Ltd., Karnataka Bank Ltd., , Nainital Bank Ltd., Ratnakar Bank

Ltd., Jammu & Kashmir Bank Ltd., South Indian Bank Ltd., SBI Commercial & International Bank Ltd,

and Tamilnad Mercantile Bank Ltd.

New Private Banks- There are seven new private banks functioning in the Indian economy. These

are- Axis Bank Ltd., Development Credit Bank Ltd, ICICI Bank Ltd., IndusInd Bank Ltd., Kotak

Mahindra Bank Ltd., HDFC Bank Ltd., and Yes Bank Ltd.

Foreign Banks- These banks have their registered head offices in a foreign country, while they

operate their branches in India. They can operate in India either through wholly-owned subsidiaries or

through branches. There are 32 foreign banks operating their various branches in India.

Co-operative Banks – Cooperative banks are those scheduled banks that are regulated by RBI,

under a cooperative structure to provide credit to all actegories of businesses. Their ownership

structure is unique where like minded individuals and companies pool in money together to support

credit facilities to businesses. These can operate in either Urban or Rural setting. That is another

criteria to differentiate these co-operative banks.

The types of banks in India can be understood from the following table, which explains what kind of

customer base different types of banks have.

.

Indian Banking System: Structure and other Details!

Bank is an institution that accepts deposits of money from the public.

Anybody who has account in the bank can withdraw money. Bank also lends money.

Indigenous Banking:

The exact date of existence of indigenous bank is not known. But, it is certain that the old banking

system has been functioning for centuries. Some people trace the presence of indigenous banks to the

Vedic times of 2000-1400 BC. It has admirably fulfilled the needs of the country in the past.

However, with the coming of the British, its decline started. Despite the fast growth of modern

commercial banks, however, the indigenous banks continue to hold a prominent position in the Indian

money market even in the present times. It includes shroffs, seths, mahajans, chettis, etc. The

indigenous bankers lend money; act as money changers and finance internal trade of India by means

of hundis or internal bills of exchange.

Defects:

The main defects of indigenous banking are:

(i) They are unorganised and do not have any contact with other sections of the banking world.

(ii) They combine banking with trading and commission business and thus have introduced trade risks

into their banking business.

(iii) They do not distinguish between short term and long term finance and also between the purpose

of finance.

(iv) They follow vernacular methods of keeping accounts. They do not give receipts in most cases and

interest which they charge is out of proportion to the rate of interest charged by other banking

institutions in the country.

Suggestions for Improvements:

(i) The banking practices need to be upgraded.

(ii) Encouraging them to avail of certain facilities from the banking system, including the RBI.

(iii) These banks should be linked with commercial banks on the basis of certain understanding in the

respect of interest charged from the borrowers, the verification of the same by the commercial banks

and the passing of the concessions to the priority sectors etc.

(iv) These banks should be encouraged to become corporate bodies rather than continuing as family

based enterprises.

Structure of Organised Indian Banking System:

The organised banking system in India can be classified as given below:

Reserve Bank of India (RBI):

The country had no central bank prior to the establishment of the RBI. The RBI is the supreme

monetary and banking authority in the country and controls the banking system in India. It is called

the Reserve Bank’ as it keeps the reserves of all commercial banks.

Commercial Banks:

Commercial banks mobilise savings of general public and make them available to large and small

industrial and trading units mainly for working capital requirements.

Commercial banks in India are largely Indian-public sector and private sector with a few foreign

banks. The public sector banks account for more than 92 percent of the entire banking business in

India—occupying a dominant position in the commercial banking. The State Bank of India and its 7

associate banks along with another 19 banks are the public sector banks.

Scheduled and Non-Scheduled Banks:

The scheduled banks are those which are enshrined in the second schedule of the RBI Act, 1934.

These banks have a paid-up capital and reserves of an aggregate value of not less than Rs. 5 lakhs,

hey have to satisfy the RBI that their affairs are carried out in the interest of their depositors.

All commercial banks (Indian and foreign), regional rural banks, and state cooperative banks are

scheduled banks. Non- scheduled banks are those which are not included in the second schedule of

the RBI Act, 1934. At present these are only three such banks in the country.

Regional Rural Banks:

The Regional Rural Banks (RRBs) the newest form of banks, came into existence in the middle of

1970s (sponsored by individual nationalised commercial banks) with the objective of developing rural

economy by providing credit and deposit facilities for agriculture and other productive activities of al

kinds in rural areas.

The emphasis is on providing such facilities to small and marginal farmers, agricultural labourers, rural

artisans and other small entrepreneurs in rural areas.

Other special features of these banks are:

(i) their area of operation is limited to a specified region, comprising one or more districts in any

state; (ii) their lending rates cannot be higher than the prevailing lending rates of cooperative credit

societies in any particular state; (iii) the paid-up capital of each rural bank is Rs. 25 lakh, 50 percent

of which has been contributed by the Central Government, 15 percent by State Government and 35

percent by sponsoring public sector commercial banks which are also responsible for actual setting up

of the RRBs.

These banks are helped by higher-level agencies: the sponsoring banks lend them funds and advise

and train their senior staff, the NABARD (National Bank for Agriculture and Rural Development) gives

them short-term and medium, term loans: the RBI has kept CRR (Cash Reserve Requirements) of

them at 3% and SLR (Statutory Liquidity Requirement) at 25% of their total net liabilities, whereas for

other commercial banks the required minimum ratios have been varied over time.

Cooperative Banks:

Cooperative banks are so-called because they are organised under the provisions of the Cooperative

Credit Societies Act of the states. The major beneficiary of the Cooperative Banking is the agricultural

sector in particular and the rural sector in general.

The cooperative credit institutions operating in the country are mainly of two kinds: agricultural

(dominant) and non-agricultural. There are two separate cooperative agencies for the provision of

agricultural credit: one for short and medium-term credit, and the other for long-term credit. The

former has three tier and federal structure.

At the apex is the State Co-operative Bank (SCB) (cooperation being a state subject in India), at the