Jacintha Trading and Profit and Loss Account for the year ... · PDF...

18

1 .1. Jacintha Trading and Profit and Loss Account for the year ended 31 December 2010 $ $ $ Opening stock 60000 Sales 63000 Purchases 26500 Less sales returns 550 Less purchases returns 475 62450 26025 Add: Carriage inwards 900 26925 Cost of goods available for sale 86925 Less closing stock 46500 Cost of goods sold 40425 Gross profit c/d 22025 62450 62450 Carriage outwards 1350 Gross profit b/d 22025 Insurance expense 3000 Commission received 15000 Rent expense 1100 37025 Salaries 5225 Utilities 2400 Motor expenses 1700 Interest expense 750 Total expenses 15525 Net profit to Capital 21500 37025 37025 1 mark each Jacintha Balance Sheet as at 31 December 2010 Fixed asset $ $ Owner equity $ Motor vehicle 163225 Capital 81000 Add net profit 21500 Current asset 102500 Closing stock 46500 Less drawings 9000 Debtors 18000 93500 Bank 8750 Long term liability 73250 Loan from bank 132500 Current liability Creditors 10475 236475 236475 1 mark each

Transcript of Jacintha Trading and Profit and Loss Account for the year ... · PDF...

1

.1.

Jacintha

Trading and Profit and Loss Account for the year ended 31 December 2010

$ $ $

Opening stock 60000 Sales 63000

Purchases 26500 Less sales returns 550

Less purchases returns 475 62450

26025

Add: Carriage inwards 900

26925

Cost of goods available for sale 86925

Less closing stock 46500

Cost of goods sold 40425

Gross profit c/d 22025

62450 62450

Carriage outwards 1350 Gross profit b/d 22025

Insurance expense 3000 Commission received 15000

Rent expense 1100 37025

Salaries 5225

Utilities 2400

Motor expenses 1700

Interest expense 750

Total expenses 15525

Net profit to Capital 21500

37025 37025

1 mark each

Jacintha

Balance Sheet as at 31 December 2010

Fixed asset $ $ Owner equity $

Motor vehicle 163225 Capital 81000

Add net profit 21500

Current asset 102500

Closing stock 46500 Less drawings 9000

Debtors 18000 93500

Bank 8750 Long term liability

73250 Loan from bank 132500

Current liability

Creditors 10475

236475 236475

1 mark each

2

2.

Tom

[0.5] $ $ $ $

Stock as at 1 May 2010 [0.5] 7,500 Sales 80,000 [0.5] Add Purchases [0.5] 63,000 Less Returns Inwards 5,000 [0.5] Less Returns Outwards [0.5] 8,000 Net sales 75,000

55,000 Add Custom duty [0.5] 1,500

Carriage inwards [0.5] 4,500 [0.5] (9000X1/3) Salaries & wages [0.5] 3,000

Net purchases 64,000 Cost of goods available for sale 71,500 Less: Stock as at 30 Apr 2011 [0.5] 10,000 Cost of goods sold 61,500 Gross profit c/d 13,500

75,000 75,000 Carriage outwards [0.5] 5,500 Gross profit b/d 13,500 [0.5] OF General expenses [0.5] 850 Rent received 3,000 [0.5] Interest [0.5] 300 Discount received 750 [0.5] Stationery [0.5] 900 Salaries and wages (9000X2/3) [0.5] [0.5] 6,000 Discount allowed [0.5] 200 Insurance [0.5] 4,500

Net loss 1,000 18,250 18,250

(Total: 11 marks)

Tom

[0.5] Fixed Assets [0.5] $ $ Owner's Equity [0.5] $ $ Premises [0.5] 140,000 Capital as at 1 May 2010 156,000 [0.5] Motor vehicles [0.5] 70,000 Less: Net loss 1,000 [0.5] OF Furniture [0.5] 30,000 155,000

240,000 Less: Drawings 1,000 [0.5] Current Assets [0.5] 154,000 Stock [0.5] 10,000 Long-Term Liabilities [0.5] Debtors [0.5] 15,000 Mortgage on premises 90,000 [0.5] Cash in hand [0.5] 5,000 Current Liabilities [0.5]

30,000 Creditors 20,000 [0.5] Bank overdraft 6,000 [0.5]

26,000 270,000 270,000 0

(Total: 9 marks)

Trading, Profit & Loss Accounts for the year ended 30 April 2011

Balance Sheet as at 30 April 2011

3

3.

Bryan Co

Trading, Profit and Loss Account for the year ended 31 December 2010

$ $ $ $

Opening stock 8000 Sales 55000

Purchases(36200-200) 36000 Less: Sales returns

500

Add: Carriage inwards 700 54500

Duty on purchases 300

37000

Less: Purchases returns 400 36600

Cost of goods available for sale 44600

Less: Closing stock 7200

Cost of goods sold 37400

Gross Profit 17100

54500 54500

Rent 6000 Gross Profit 17100

Utilities 2200 Discount received

800

Wages 2800 Commission received

1200

Discount allowed 1000

Interest expense 450

Carriage outwards 750

Net Profit 5900

19100 19100

4

Bryan Co

Balance Sheet as at 31 December 2010

Fixed Assets $ $ $ Owner's Equity $ $

Office Equipment 3,000 Balance 1.7.09 21300

Motor Vehicle 21,500 24,500 Add:Net Profit 5900 OF

27200

Less:Drawings 1000

Balance 30.6.10 26200

Current assets

Stock 7200 Long Term Liabilities

Debtors 5200 12400 Loan from bank 5000

Current Liabilities

Creditors 4500

Bank overdraft 1200 5700

36,900 36,900

4

5

$ $ Opening Stock [0.5] 8700 Sales [0.5] 87500 Purchases (51250-350) 50900 [1] Less: Returns Inwards [1] 200 Add: Carriage on Purchases 600 [0.5] 87300 Repackaging Wages 2100 [1]

53600 Less Returns Outwards 450 [1]

53150 Cost of Goods Available for Sale 61850 Less Closing Stock [1] 7250 Cost of Goods Sold 54600 Gross Profit c/d 32700

87300 87300

Salaries (3/4x8400) [1] 6300 Gross Profit b/d [1] 32700 Carriage on Sales [0.5] 1270 Commission Received [0.5] 770 Rental Expense [0.5] 3800 General Expense (910-210) [1] 700 Discount Allowed [0.5] 720 Interest Expense (5%x5000) [1] 250 Advertising [0.5] 2200

15240 Net Profit [1] 18230

33470 33470

[14]

$ $ Fixed Assets Owner's Equity Premises [0.5] 20000 Capital, 1 May 2010 [0.5] 15000 Motor Vehicles [0.5] 15000 Add Net Profit [0.5] 18230

35000 Additional Capital [1] 5000 38230

Current Assets Less Drawings [1.5] 2140 Stock [1] 7250 Capital, 30 Apr 2011 [0.5] 36090 Debtors [1] 6570 Cash [0.5] 860 Long-term Liabilities

Bank Loan [1] 5000 14680

Current Liabilities Creditors [0.5] 5840 Bank Overdraft [1] 2750 (2500+250) 8590

49680 49680

[10]

(c) Net Realisable Value of the stock is the market value [1] of the stock after deducting any expenses that may be incurred in the selling process. [1]

(d) Stock are valued based on the lower amount between the Cost and the Net Realizable Value. [1] This is in compliance with the Prudence Concept, which states that businesses should not over-state its profits or assets. [1]

(e)(i) NO, I disagree. Computer purchased for the office staff to use should be recorded as fixed assets since they are can benefit the business for more than 1 acounting period and not meant for resale. [1]

(e)(ii) Profit will decrease. [1] [Total: 30]

Balance Sheet as at 30 April 2011

Trading and Profit and Loss Account for the year ended 30 April 2011 Dean

Dean

6

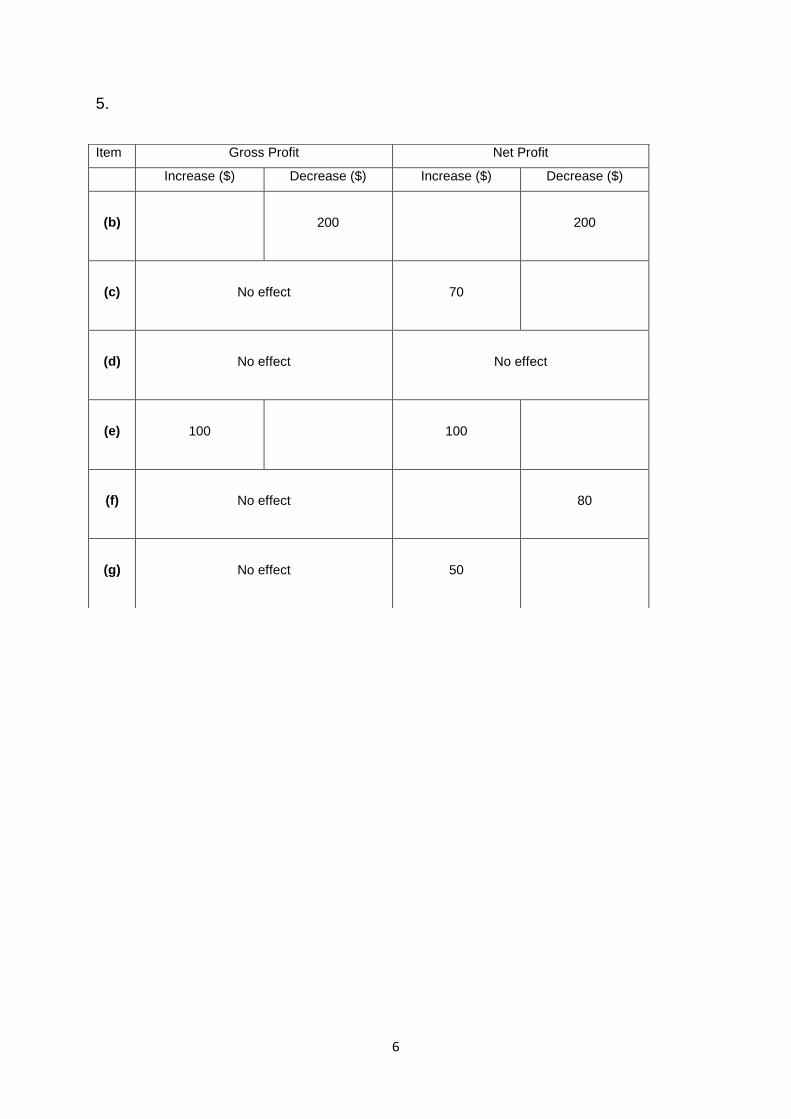

5.

Item Gross Profit Net Profit

Increase ($) Decrease ($) Increase ($) Decrease ($)

(b)

200

200

(c)

No effect

70

(d)

No effect

No effect

(e)

100

100

(f)

No effect

80

(g)

No effect

50

7

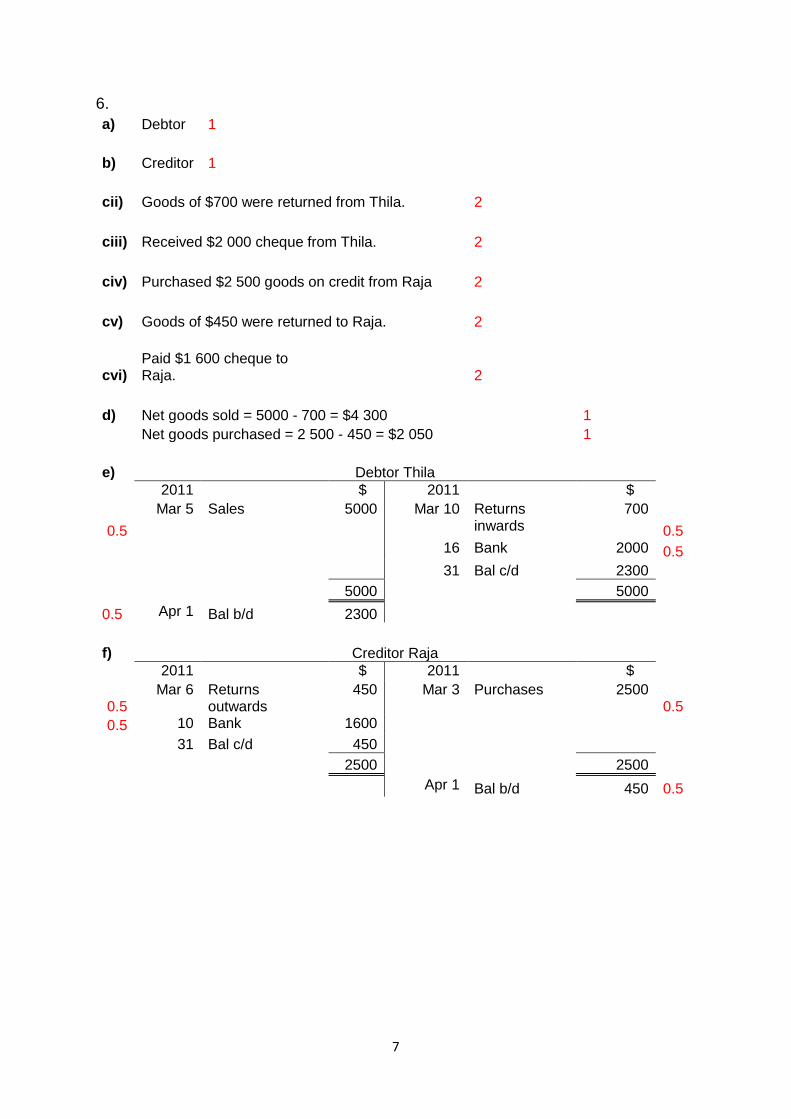

6.

a) Debtor 1

b) Creditor 1

cii) Goods of $700 were returned from Thila. 2

ciii) Received $2 000 cheque from Thila.

2

civ) Purchased $2 500 goods on credit from Raja 2

cv) Goods of $450 were returned to Raja. 2

cvi)

Paid $1 600 cheque to Raja.

2

d) Net goods sold = 5000 - 700 = $4 300

1

Net goods purchased = 2 500 - 450 = $2 050

1

e) Debtor Thila

2011 $ 2011 $

0.5

Mar 5 Sales 5000 Mar 10 Returns inwards

700

0.5

16 Bank 2000 0.5

31 Bal c/d 2300

5000

5000

0.5 Apr 1 Bal b/d 2300

f) Creditor Raja

2011 $ 2011 $

0.5

Mar 6 Returns outwards

450 Mar 3 Purchases 2500 0.5

0.5 10 Bank 1600

31 Bal c/d 450

2500

2500

Apr 1 Bal b/d 450 0.5

8

Updated Cash Book (Bank Columns only)

$ $

2011

Mar 31

Apr 1

Bal b/d

Interest Rec’d

Bal b/d

1,320

50

2011

Mar 31

Insurance

Melvin (Dishonoured

cheque)

Bal c/d

150

120

1,100

1,370 1,370

1,100

Question 5(b):

Bank Reconciliation Statement as at 31 Mar 2011

Adjusted cash Book Balance

Add Unpresented Cheques: Joseph

Less Uncredited Deposits: Liqing

Bank Statement Balance

$

1 100

280

1 380

350

1 030

(a) To reconcile the difference between the Cash Book and the Bank Statement.

Q3 2011 2011 Oct 31 Balance b/d 9,000 [1] Oct 31 Insurance expense 200 [1]

31 Credit Transfer - Matthew 400 [1] 31 Bank charges 20 [1] 31 Interest revenue 100 [1] 31 Balance c/d 9,280

9,500 9,500

Nov 1 Balance b/d 9,280 [1] [6]

Bank Reconciliation Statement as at 31 October 2011 [1]

Balance as per updated cashbook 9,280 [1] Less : Uncredited cheques / deposits

Paul (1,500) [1] Keith (2,500) [1] John (2,000) [1]

3,280 Add : Unpresented cheques / deposits

Meck Supplies 4,200 [1] Tom 1,200 [1]

8,680 [1] [8]

Updated Cashbook

9

Q2a

[0.5]

Date Particulars DA Cash Date Particulars DR Cash [0.5]

2011 2011

[1] Apr 1 Balance b/d 3,540 Apr 5 Cash [0.5]

[0.5] 3 Sales 2,990 15 Rent 6,000 [0.5]

[0.5] 5 Bank 1,020 17 Drawings 3,200 [0.5]

[1] 10 Debtor: Mars Trading 100 23 Debtor: Mars Trading [0.5]

[0.5] 12 Commission revenue 800 25 Bank 1,100 [0.5]

[0.5] 19 Interest revenue 27 Advertising expense [0.5]

[1] 22 Debtor: Venus Trading 250 4,750 29 Wages expense 500 [0.5]

[0.5] 25 Cash 30 Bank 2,000 [0.5]

[0.5] 30 Cash 30 Balance c/d 300

13,100 13,100

[1] May 1 Balance b/d 300

[12]

Q2b A cash discount is given to encourage prompt payment. [1]

Q2c There was insufficient funds in Mars Trading's bank account. [1]

2,000 6,800

Cash book

1,100

1,500

240

Bank

7,080

1,500

Bank

1,020

6,800

2,600

11,92011,920

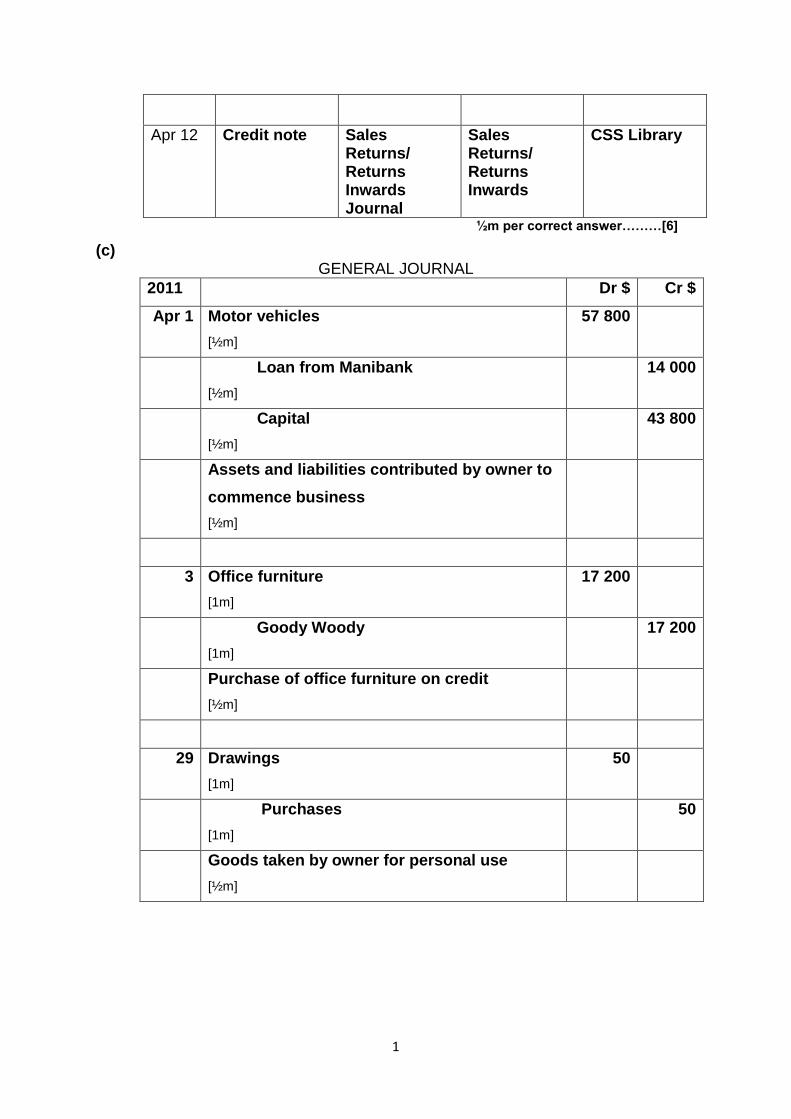

2 (a) Explain what is meant by the double-entry principle. The double-entry principle states that every transaction has a debit and credit entry [1m] of an equal amount [1m]. (b) .

Date Source document

Book of prime entry

Account debited

Account credited

Apr 4 Invoice Purchases Journal

Purchases JJ Publishing

Apr 10 Invoice Sales Journal CSS Library Sales

1

0

Apr 12 Credit note Sales Returns/ Returns Inwards Journal

Sales Returns/ Returns Inwards

CSS Library

½m per correct answer………[6]

(c) GENERAL JOURNAL

2011 Dr $ Cr $

Apr 1 Motor vehicles

[½m]

57 800

Loan from Manibank

[½m]

14 000

Capital

[½m]

43 800

Assets and liabilities contributed by owner to

commence business

[½m]

3 Office furniture

[1m]

17 200

Goody Woody

[1m]

17 200

Purchase of office furniture on credit

[½m]

29 Drawings

[1m]

50

Purchases

[1m]

50

Goods taken by owner for personal use

[½m]

1

1

[7]

(d) Distinguish between cash and credit transactions. A cash transaction is one where immediate payment is made.

[1]

A credit transaction is one where payment is delayed to a later date.

[1] [Total: 17]

a)

General Journal

Debit Credit

2010

$ $

(i) June 5

Dr Motor Vehicle

Cr Capital

4,000 [1]

4,000 [1]

(ii) June 19

Dr Bank

Dr Discount Allowed

Cr Debtor Robin

1,800 [1]

200 [1]

2,000 [1]

(iii) June 23

Dr Utilities

Cr Bank

200 [1]

200 [1]

(iv)

June 30 Dr Bank / Cash at Bank

Cr Cash / Cash on Hand

1,000 [1]

1,000 [1]

b)

1

2

Date Particulars Debit Credit

2010

$ $

a) May 23 Dr Debtor Betty

Cr Office Equipment

Being surplus office equipment sold to Betty on

credit

800 [1]

800 [1]

b) Aug 5

Dr Drawings

Cr Cash

Being cash withdrawn for personal use

300 [1]

300 [1]

c) Oct 17

Dr Bank

Cr Capital

Being proceeds from the sales of personal stocks

banked in

1,500 [1]

1,500 [1]

a) A cash transaction involves the exchange of goods and cash at the same time

(at the point of transaction)[1] but a credit transaction involves only the goods

given or received at the point of transaction, with the cash paid or received on

a later date. [1]

b)

Transaction

Effect on

Asset Liability Owner’s Equity

1

3

(i) Bought furniture worth $5,000 using cheque

Office Furniture +$5,000

Bank - $5,000

(ii)

Sold goods to Jenny at $1,200 and received cash

Cash +$1,200

[1]

Sales +$1,200

[1]

(iii)

Bought goods at $2,000 from Roger on credit

*Stock +$2,000

[1]

Creditor Roger +$2,000

[1]

(iv)

Withdrew goods worth $600 for his wife

*Stock -$600

[1]

Drawings -$600

[1]

(v) Accepted debt settlement from Cass - a computer worth $500 and the remaining $700 received in cash

Office Equipment +$500

[1] Cash +$700

[1] Debtor Cass

-$1,200 [1]

[Total:11 marks]

12. Transactions Books of Original Entry Source Documents

(a)

Credit Sales $2 000 Sales Journal Sales Invoice

Invoice issued

(b)

Purchases Returns $500 Purchases Returns Journal

Credit note received

(c)

Purchase of furniture

$3 000 on credit General Journal Invoice received

1

4

(d) $1 000 cheque received

from debtor Cash Book Receipt issued

(e) Payment of postage $3 Petty Cash Book Petty Cash Voucher

(f) Cash Purchases $650 Cash Book Receipt received

13a) General Journal

Error Particulars Debit ($) Credit($)

(i) Repair 1200

Motor Vehicle 1200

(ii) Rent 500

Bank 500

(iii) Bank 860

Interest Received 860

(iv) Returns Outwards 180

Mavis 180

(v) Mitchel 200

Purchases 200 Michelle 200

Sales 200

13(b) (i) Error of Principle (ii) Error of Omission (iii) Error of Reversal of Entries (iv) Error of Original Entry

1

5

14 (a)

Jenny Cash Book (Bank columns)

2006 $ 2006 $

Sep 30

Bal b/d (unadjusted) 270 Sep 30 Error in cheque 9011 1000

Cash 1800 Insurance 108

Dividends 400 Bank charges 9

Bal c/d (adjusted) 1353

2470 2470

Oct 1 Bal b/d (adjusted) 1353

4B (b)

Jenny Bank Reconciliation Statement as at 30 Sep 2006

$

Bal as per Bank Statement 803

Add Uncredited deposits 100

590 690

1493

Less Unpresented cheque 140

Bal as per Cash Book (adjusted) 1353

4B (c) Current Assets: Cash at Bank $1353

1

6

15(a) & (b) Book of Michael

Trading and Profit & Loss Accounts

Dr. for the half year ended 30 June 2005 [½] Cr.

$ $ $ $

Opening Stock [½] 7000 Sales [½] 64500

Purchases [½] 41800 Less: Returns Inwards [½] 300

add: Duty on Purchases [½] 400 64200

42200 Cost of goods available for sale[½] 49200

less: Closing Stock [½] 9000 Cost of goods sold [½] 40200 Gross Profit c/d [½] 24000

64200 64200

Carriage Outwards [½] 1400 Gross Profit b/d [½] 24000

Office Expenses [½] 2000 Interest Received [½] 1500

Stationery [½] 700 Commission Received [½] 1800

Wages [½] 4200 Net Profit [½] 19000 27300 27300 ST: [ 9m ]

Balance Sheet as at 30 June 2005 [½]

Fixed Assets [½] $ $ Owner's Equity [½] $ $

Premises [½] 50000 Capital, 1 Jan '05 [½] 44200

Motor Vehicles [½] 14000 Add: Net Profit [½] 19000

Fixtures and Fittings [½] 8000 63200

72000 Less: Drawings [½] 1000

Capital, 30 Jun '05 62200

Current Assets [½]

Stock [½] 9000 Long Term Liability [½]

Debtors [½] 5100 Mortgage on Premises [½]

15000

Cash [½] 300

14400 Current Liabilities [½]

Creditors [½] 6900

Bank overdraft [½] 2300

9200

86400 86400 ST of BS : 9

BS Total : 1

Sub-Heading Total :4 items @ ½ m each = 2

Total of (c) = [12m]

1

7

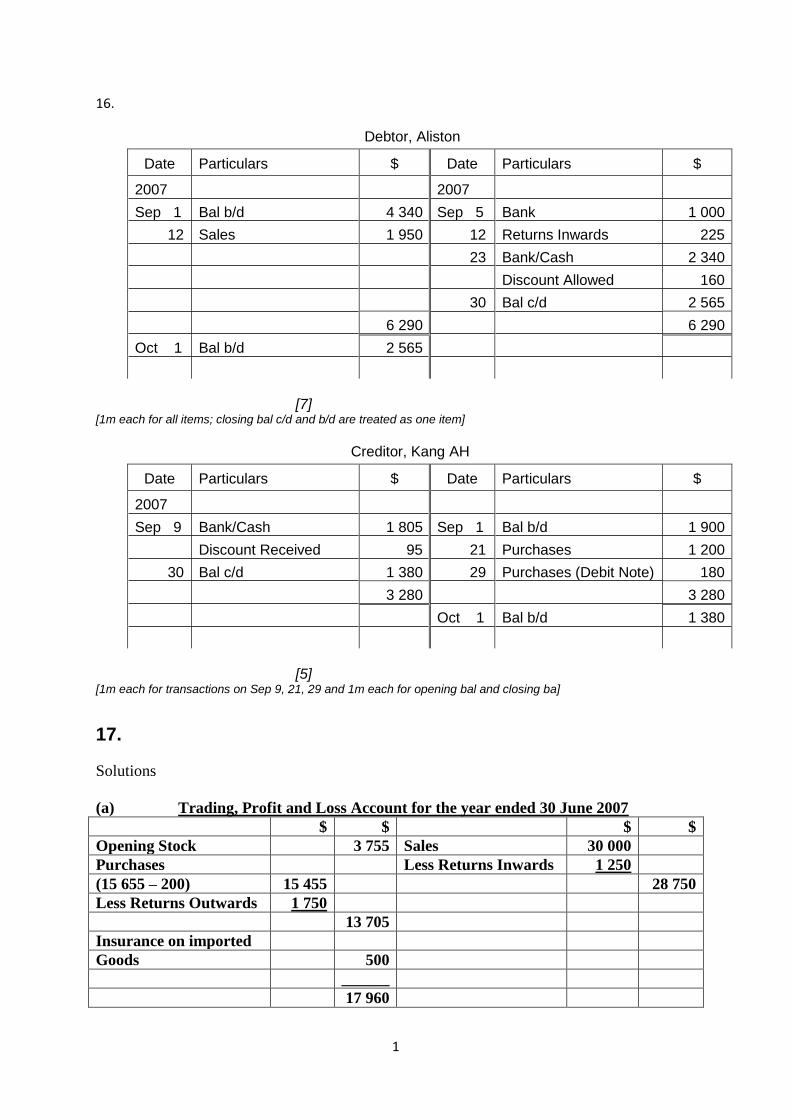

16.

Debtor, Aliston

Date Particulars $ Date Particulars $

2007 2007

Sep 1 Bal b/d 4 340 Sep 5 Bank 1 000

12 Sales 1 950 12 Returns Inwards 225

23 Bank/Cash 2 340

Discount Allowed 160

30 Bal c/d 2 565

6 290 6 290

Oct 1 Bal b/d 2 565

[7] [1m each for all items; closing bal c/d and b/d are treated as one item]

Creditor, Kang AH

Date Particulars $ Date Particulars $

2007

Sep 9 Bank/Cash 1 805 Sep 1 Bal b/d 1 900

Discount Received 95 21 Purchases 1 200

30 Bal c/d 1 380 29 Purchases (Debit Note) 180

3 280 3 280

Oct 1 Bal b/d 1 380

[5] [1m each for transactions on Sep 9, 21, 29 and 1m each for opening bal and closing ba]

17.

Solutions

(a) Trading, Profit and Loss Account for the year ended 30 June 2007

$ $ $ $

Opening Stock 3 755 Sales 30 000

Purchases Less Returns Inwards 1 250

(15 655 – 200) 15 455 28 750

Less Returns Outwards 1 750

13 705

Insurance on imported

Goods 500

______

17 960

1

8

Less Closing Stock 4 000

Cost of Goods Sold 13 960

Gross Profit 14 790 ______

28 750 28 750

Discounts Allowed 103 Gross Profit 14 790

Carriage Outwards 460 Discounts Received 110

Insurance (2755 – 500) 2 255 Interest on Fixed

Sundry Expenses 790 Deposit 315

Wages 6 000

Net Profit 5 607 ______

15 215 15 215

(b) Balance Sheet as at 30 June 2007

$ $ $ $

Fixed Assets Owner’s Equity

Fixtures and Fittings 15 940 Capital 15 430

Add Net Profit 5 607

Current Assets 21 037

Stock 4 000 Less Drawings 3 100

Debtors 8 700 17 937

Fixed Deposit 5 000

Cash 2 057 Long-term Liabilities

19 757 Bank Loan 10 000

Current Liabilities

Bank Overdraft 260

Creditors 7 500

_____ 7 760

35 697 35 697

(c) A trial balance is prepared to check the mathematical accuracy of the debits and

credits in the ledger.

It also facilitates the preparation of final accounts and balance sheet as it is a

complete listing of all account balances.