Village Roadshow Limited Hong Kong May 27 th Singapore May 29 th

4-6 October 2010

J. P. Morgan Asia Roadshow

Singapore & Hong Kong

© Contact Energy Limited 22

Important Notice

This presentation may contain projections or forward looking statements regarding a variety of items. Such forward-

looking statements are based upon current expectations and involve risks and uncertainties.

Actual results may differ materially from those stated in any forward-looking statement based on a number of important

factors and risks.

Although management may indicate and believe that the assumptions underlying the forward-looking statements are

reasonable, any of the assumptions could prove inaccurate or incorrect and, therefore, there can be no assurance that

the results contemplated in the forward-looking statements will be realised.

Furthermore, while all reasonable care has been taken in compiling this presentation, Contact accepts no responsibility

for any errors or omissions.

This presentation does not constitute investment advice.

© Contact Energy Limited

Outline

1. Business and market overview

2. Performance

3. Strategy and growth

4. Financial results overview

5. Sector information

3

© Contact Energy Limited

1. Business and market overview

4

© Contact Energy Limited

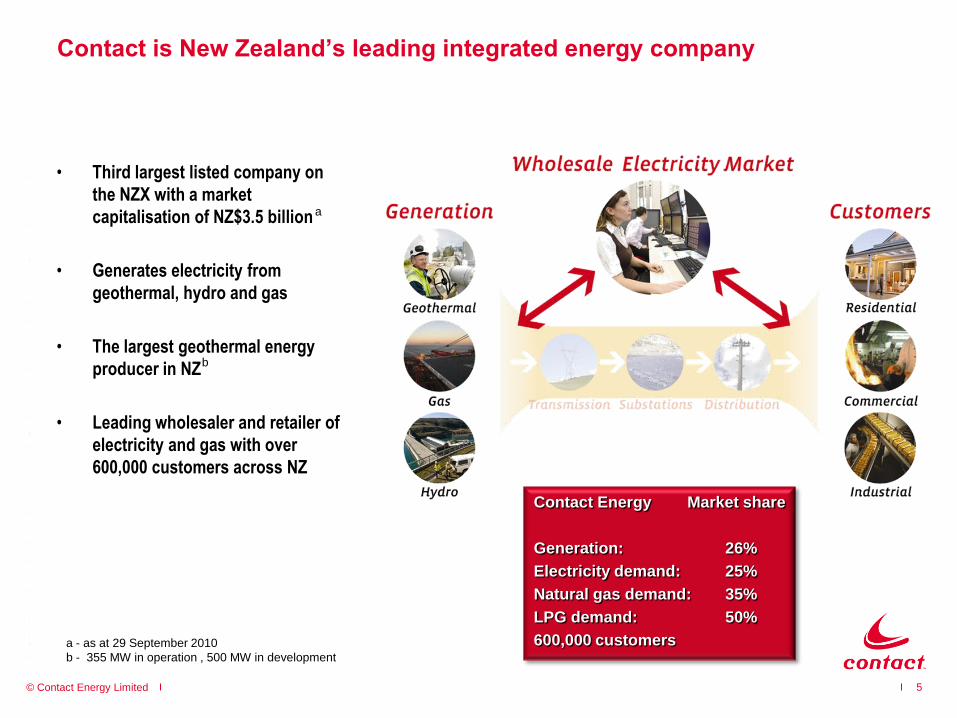

Contact Energy Market share

Generation: 26%

Electricity demand: 25%

Natural gas demand: 35%

LPG demand: 50%

600,000 customers

Contact is New Zealand’s leading integrated energy company

5

• Third largest listed company on

the NZX with a market

capitalisation of NZ$3.5 billion

• Generates electricity from

geothermal, hydro and gas

• The largest geothermal energy

producer in NZ

• Leading wholesaler and retailer of

electricity and gas with over

600,000 customers across NZ

a

a - as at 29 September 2010

b - 355 MW in operation , 500 MW in development

b

© Contact Energy Limited

New Zealand produces the majority of its generation from hydro

6

Generation by hydro sequence - FY12

25,000

30,000

35,000

40,000

45,000

19

95

19

88

19

83

19

98

19

80

19

81

19

84

19

86

19

92

19

82

19

74

20

02

19

85

20

00

19

91

20

01

19

87

19

76

19

73

19

77

GWh

Renewable

(Hydro, Geothermal, Wind)

Thermal balancing requirement

12 TWh

5 TWh

• Weather-dependent renewable generation requires

thermal generation to balance supply

– Thermal capacity is required to balance hydro and

wind volatility

• NZ has ~3,000 MW of installed thermal capacity

– 1,000 MW coal-fired (Genesis)

– 3 x 400 MW CCGT (Contact, Genesis)

– 2 x 100 MW OCGT (Contact ) (currently commissioning)

– 95 MW OCGT (MRP, Genesis)

– 440 MW cogen (Contact, others) (~50% sold to industrial users)

– 155 MW diesel-fired OCGT (Government)

• All thermal capacity is valuable during dry periods

– Peaking and firming thermal generation is valuable

in wet periods

NZ’s electricity supply and demand

…Thermal generation (in red) balances renewables

(predominately hydro). The chart is ordered by

decreasing renewables from left to right

(a wet year on the left and a dry year on the right)

Energ

y

TW

h/

year

The years represent the actual

amount of hydro generation

generated

700 MW of wind and geothermal has

been added in the last decade

© Contact Energy Limited

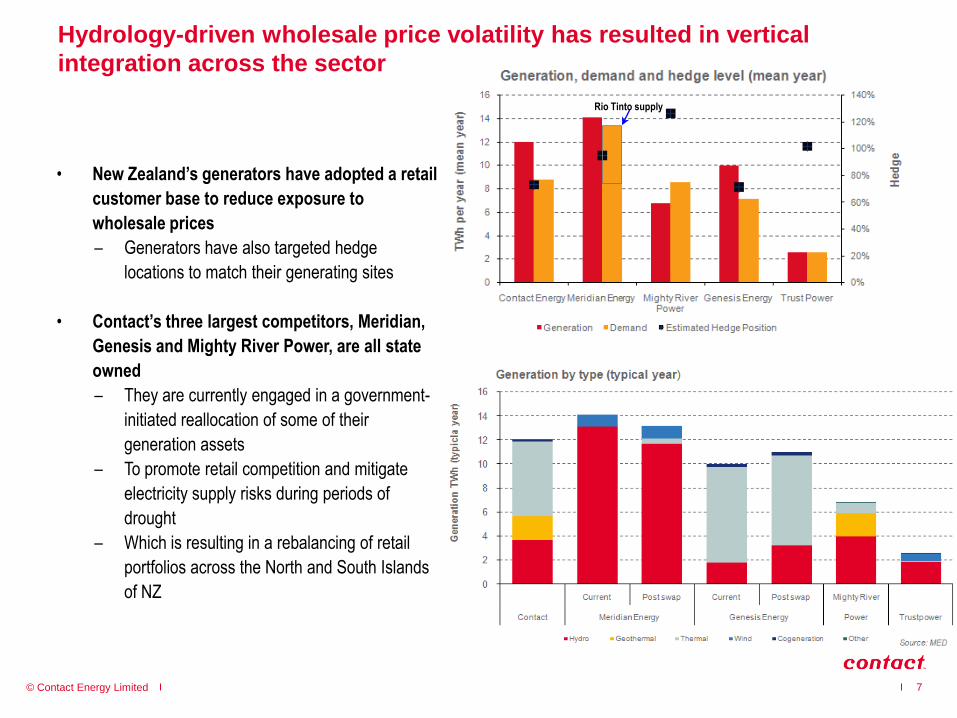

Hydrology-driven wholesale price volatility has resulted in vertical

integration across the sector

• New Zealand’s generators have adopted a retail

customer base to reduce exposure to

wholesale prices

– Generators have also targeted hedge

locations to match their generating sites

• Contact’s three largest competitors, Meridian,

Genesis and Mighty River Power, are all state

owned

– They are currently engaged in a government-

initiated reallocation of some of their

generation assets

– To promote retail competition and mitigate

electricity supply risks during periods of

drought

– Which is resulting in a rebalancing of retail

portfolios across the North and South Islands

of NZ

7

Rio Tinto supply

© Contact Energy Limited

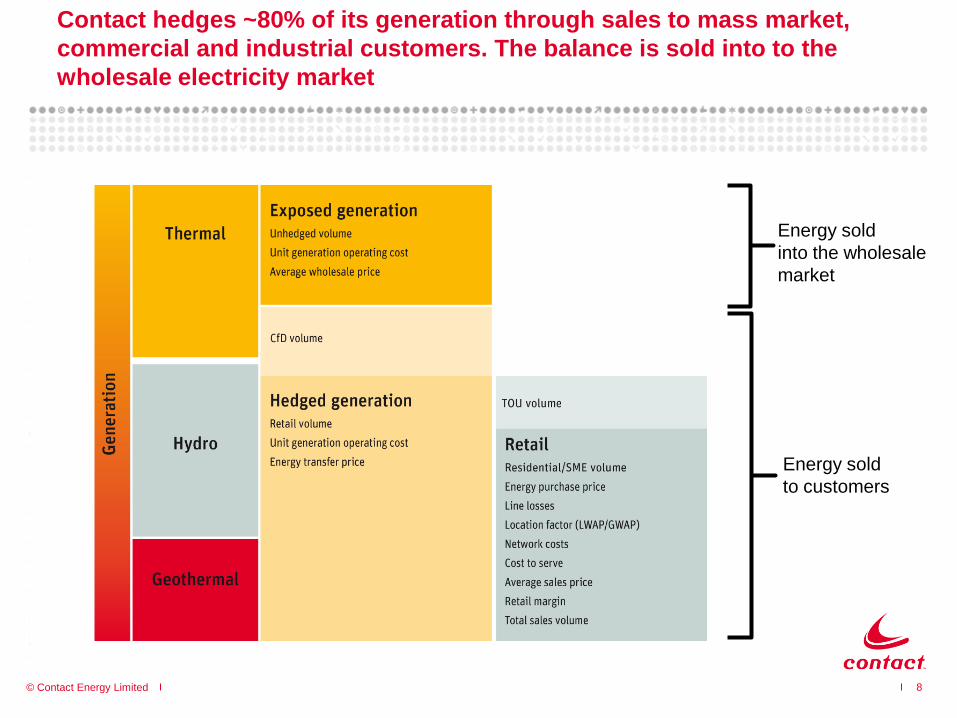

Contact hedges ~80% of its generation through sales to mass market,

commercial and industrial customers. The balance is sold into to the

wholesale electricity market

8

Energy sold

into the wholesale

market

Energy sold

to customers

© Contact Energy Limited

2. Performance

9

© Contact Energy Limited

-

20

40

60

80

100

120

-

100

200

300

400

500

600

2002 2003 2004 2005 2006

$/M

Wh

NZ

$ M

illio

ns

Financial Year

EBITDAF and wholesale electricity prices

EBITDAF Average wholesale price

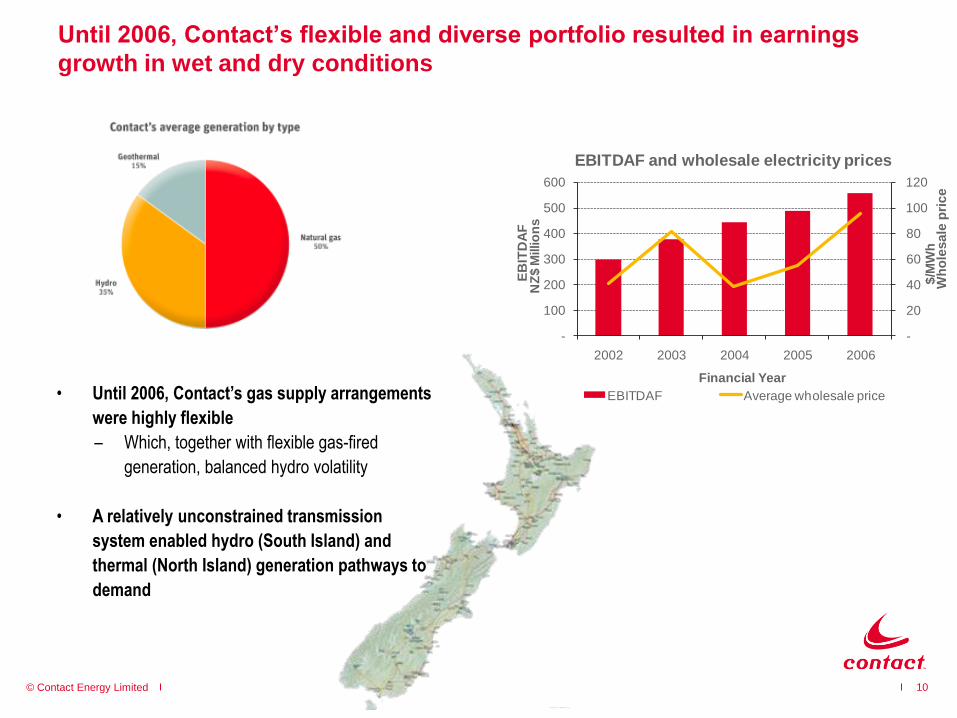

Until 2006, Contact’s flexible and diverse portfolio resulted in earnings

growth in wet and dry conditions

10

EB

ITD

AF

Wh

ole

sale

pri

ce

• Until 2006, Contact’s gas supply arrangements

were highly flexible

– Which, together with flexible gas-fired

generation, balanced hydro volatility

• A relatively unconstrained transmission

system enabled hydro (South Island) and

thermal (North Island) generation pathways to

demand

© Contact Energy Limited

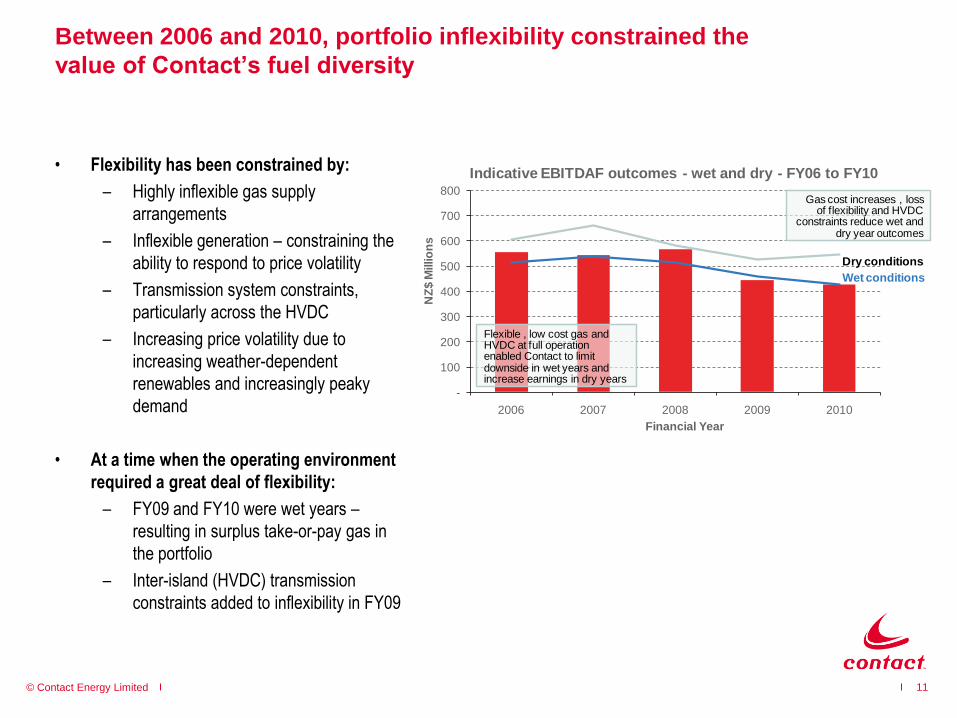

Between 2006 and 2010, portfolio inflexibility constrained the

value of Contact’s fuel diversity

• Flexibility has been constrained by:

– Highly inflexible gas supply

arrangements

– Inflexible generation – constraining the

ability to respond to price volatility

– Transmission system constraints,

particularly across the HVDC

– Increasing price volatility due to

increasing weather-dependent

renewables and increasingly peaky

demand

• At a time when the operating environment

required a great deal of flexibility:

– FY09 and FY10 were wet years –

resulting in surplus take-or-pay gas in

the portfolio

– Inter-island (HVDC) transmission

constraints added to inflexibility in FY09

11

Wet conditions

Dry conditions

-

100

200

300

400

500

600

700

800

2006 2007 2008 2009 2010

NZ

$ M

illio

ns

Financial Year

Indicative EBITDAF outcomes - wet and dry - FY06 to FY10

Flexible , low cost gas and HVDC at full operation enabled Contact to limit downside in wet years and increase earnings in dry years

Gas cost increases , loss of flexibility and HVDC

constraints reduce wet and dry year outcomes

© Contact Energy Limited

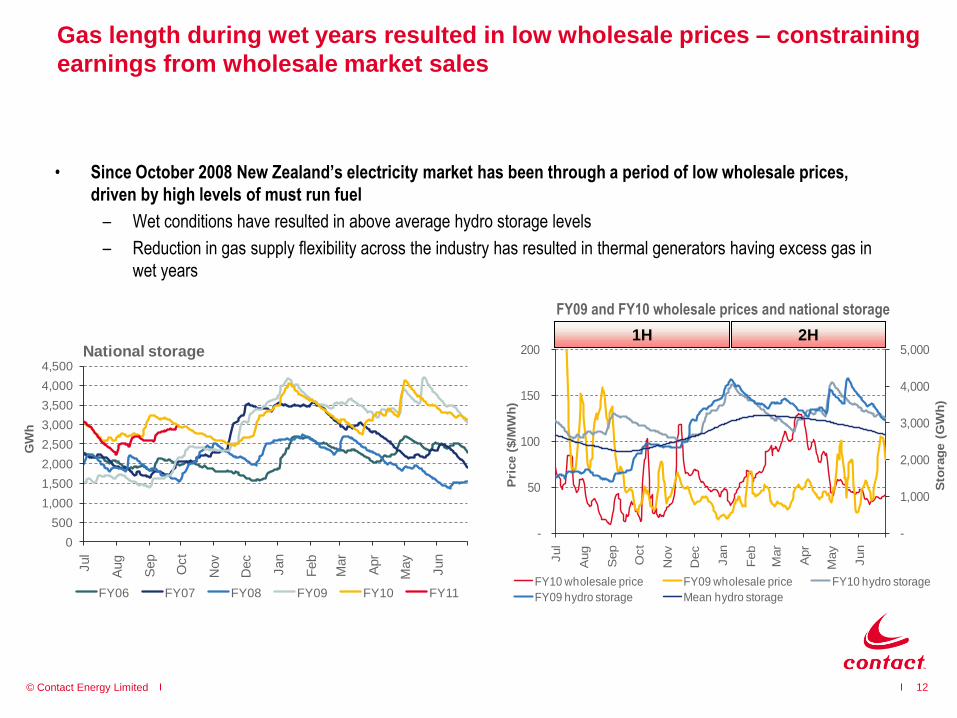

Gas length during wet years resulted in low wholesale prices – constraining

earnings from wholesale market sales

12

• Since October 2008 New Zealand’s electricity market has been through a period of low wholesale prices,

driven by high levels of must run fuel

– Wet conditions have resulted in above average hydro storage levels

– Reduction in gas supply flexibility across the industry has resulted in thermal generators having excess gas in

wet years

-

1,000

2,000

3,000

4,000

5,000

-

50

100

150

200

Jul

Aug

Sep

Oct

Nov

Dec

Jan

Feb

Mar

Apr

May

Jun

Sto

rag

e (

GW

h)

Pri

ce (

$/M

Wh

)

FY10 wholesale price FY09 wholesale price FY10 hydro storage

FY09 hydro storage Mean hydro storage

1H 2H

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

Jul

Aug

Sep

Oct

Nov

Dec

Jan

Feb

Mar

Apr

May

Jun

GW

h

National storage

FY06 FY07 FY08 FY09 FY10 FY11

FY09 and FY10 wholesale prices and national storage

© Contact Energy Limited

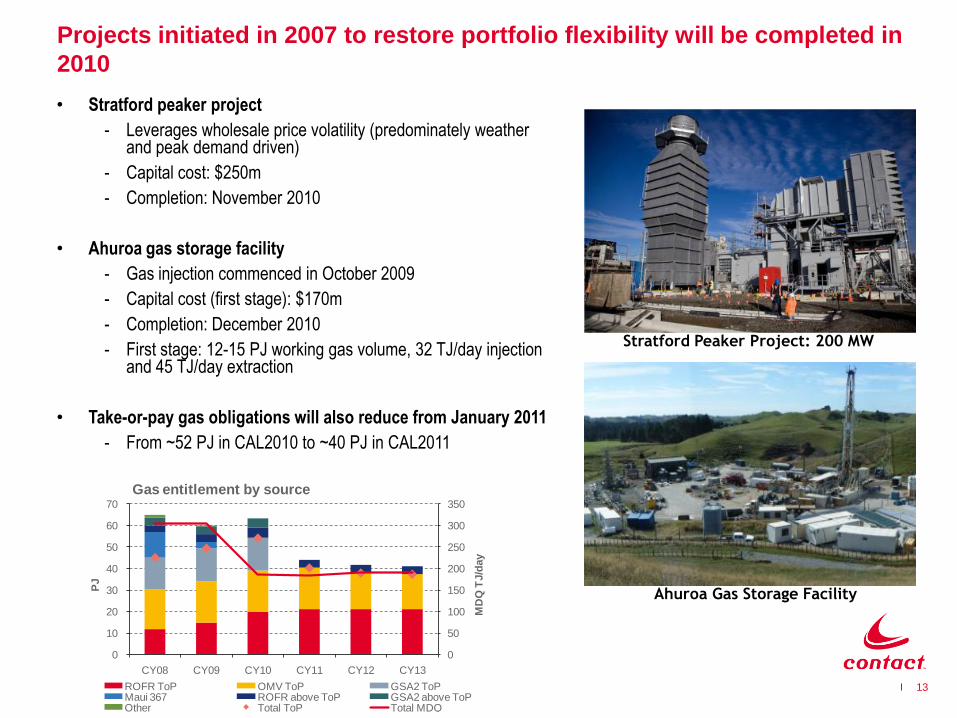

Projects initiated in 2007 to restore portfolio flexibility will be completed in

2010

13

Stratford Peaker Project: 200 MW

Ahuroa Gas Storage Facility

• Stratford peaker project

- Leverages wholesale price volatility (predominately weather and peak demand driven)

- Capital cost: $250m

- Completion: November 2010

• Ahuroa gas storage facility

- Gas injection commenced in October 2009

- Capital cost (first stage): $170m

- Completion: December 2010

- First stage: 12-15 PJ working gas volume, 32 TJ/day injection and 45 TJ/day extraction

• Take-or-pay gas obligations will also reduce from January 2011

- From ~52 PJ in CAL2010 to ~40 PJ in CAL2011

0

50

100

150

200

250

300

350

0

10

20

30

40

50

60

70

CY08 CY09 CY10 CY11 CY12 CY13

MD

Q T

J/d

ay

PJ

Gas entitlement by source

ROFR ToP OMV ToP GSA2 ToPMaui 367 ROFR above ToP GSA2 above ToPOther Total ToP Total MDQ

© Contact Energy Limited

The restoration of portfolio flexibility is expected to lift

performance in both wet and dry years – enabling Contact’s fuel

diversity to be leveraged

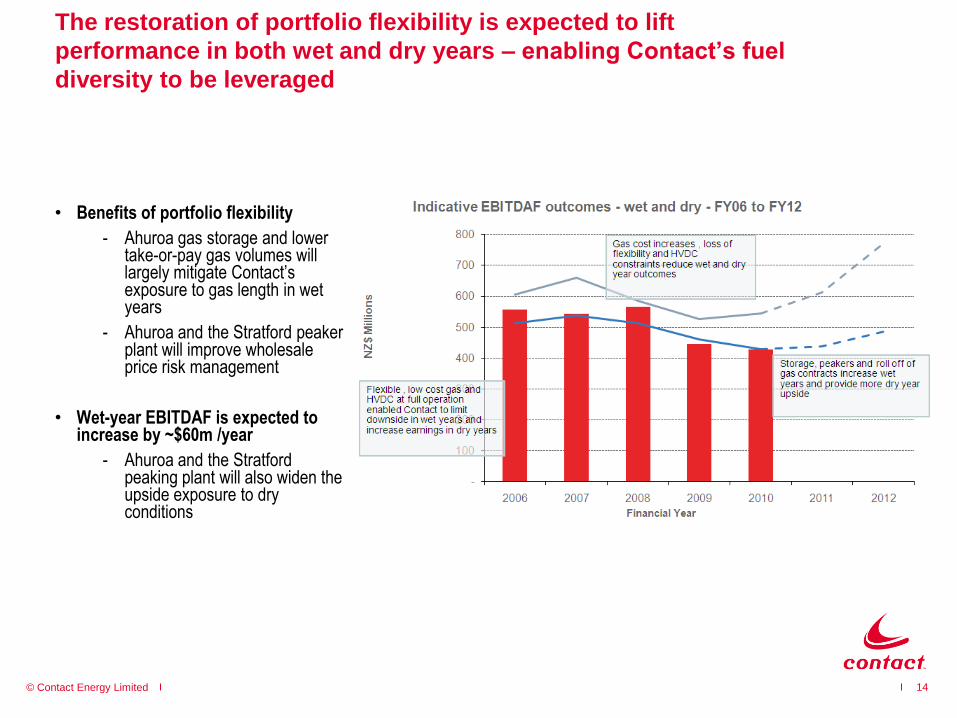

• Benefits of portfolio flexibility

- Ahuroa gas storage and lower take-or-pay gas volumes will largely mitigate Contact’s exposure to gas length in wet years

- Ahuroa and the Stratford peakerplant will improve wholesale price risk management

• Wet-year EBITDAF is expected to increase by ~$60m /year

- Ahuroa and the Stratford peaking plant will also widen the upside exposure to dry conditions

14

© Contact Energy Limited

3. Strategy and growth

15

© Contact Energy Limited

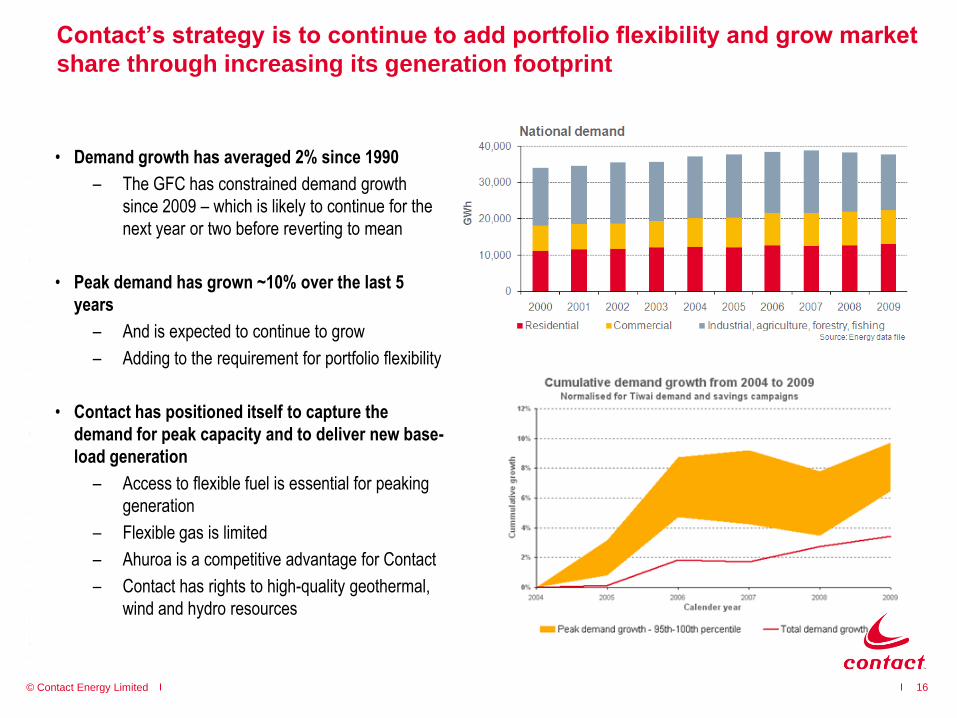

• Demand growth has averaged 2% since 1990

– The GFC has constrained demand growth

since 2009 – which is likely to continue for the

next year or two before reverting to mean

• Peak demand has grown ~10% over the last 5

years

– And is expected to continue to grow

– Adding to the requirement for portfolio flexibility

• Contact has positioned itself to capture the

demand for peak capacity and to deliver new base-

load generation

– Access to flexible fuel is essential for peaking

generation

– Flexible gas is limited

– Ahuroa is a competitive advantage for Contact

– Contact has rights to high-quality geothermal,

wind and hydro resources

16

Contact’s strategy is to continue to add portfolio flexibility and grow market

share through increasing its generation footprint

© Contact Energy Limited

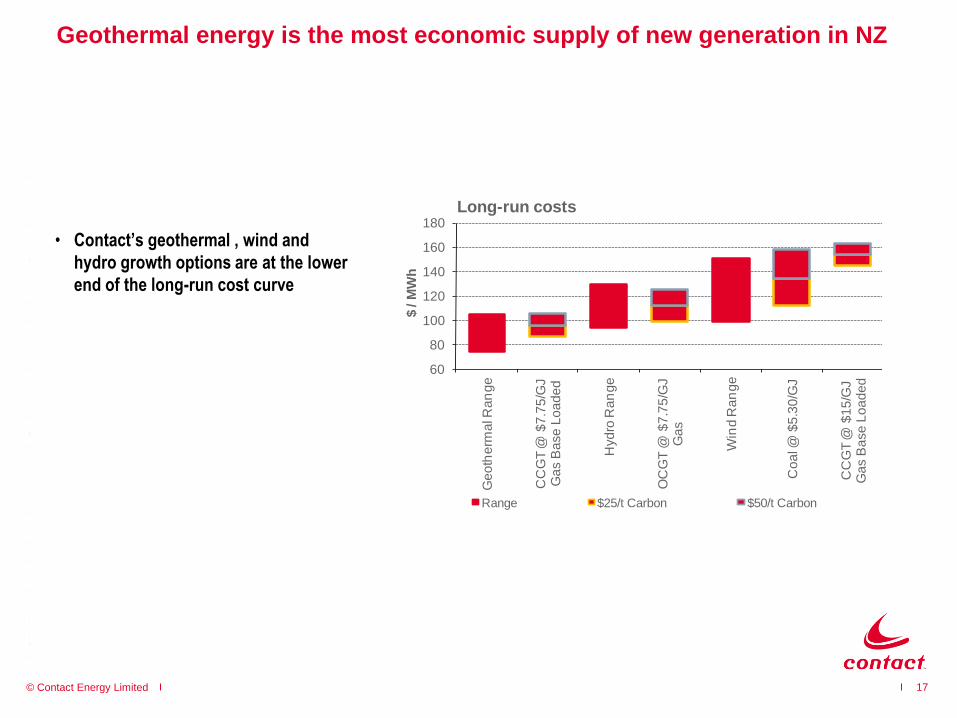

Geothermal energy is the most economic supply of new generation in NZ

17

60

80

100

120

140

160

180

Ge

oth

erm

al R

an

ge

CC

GT

@ $

7.7

5/G

J

Ga

s B

ase

Lo

ad

ed

Hyd

ro R

an

ge

OC

GT

@ $

7.7

5/G

J

Ga

s

Win

d R

an

ge

Co

al @

$5

.30

/GJ

CC

GT

@ $

15

/GJ

Ga

s B

ase

Lo

ad

ed

$ /

MW

h

Long-run costs

Range $25/t Carbon $50/t Carbon

• Contact’s geothermal , wind and

hydro growth options are at the lower

end of the long-run cost curve

© Contact Energy Limited 18

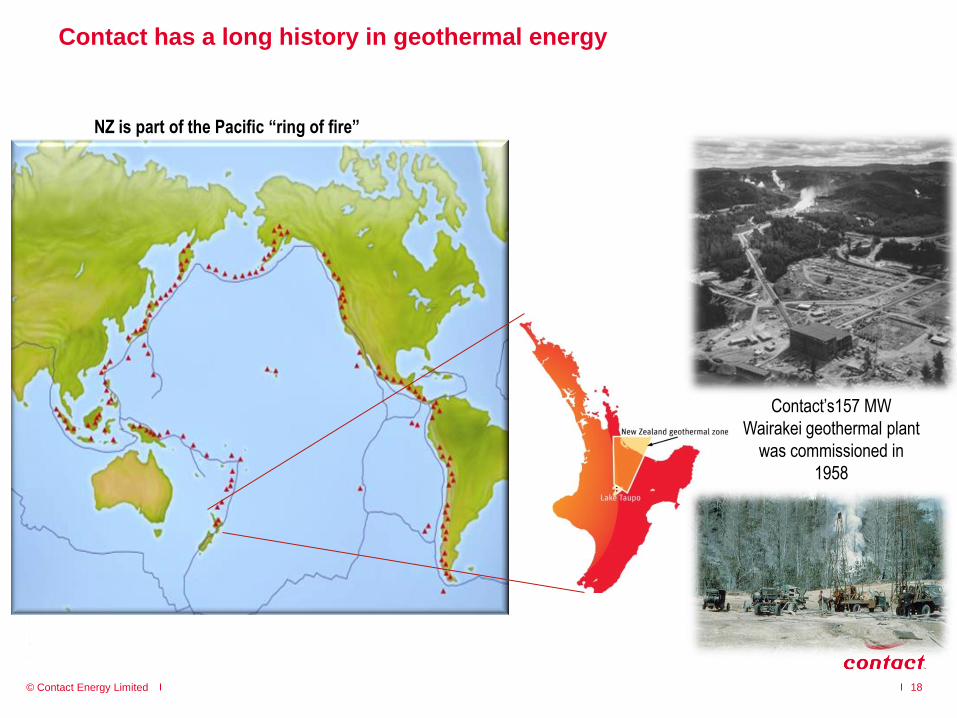

Contact has a long history in geothermal energy

NZ is part of the Pacific “ring of fire”

Contact’s157 MW

Wairakei geothermal plant

was commissioned in

1958

© Contact Energy Limited 19

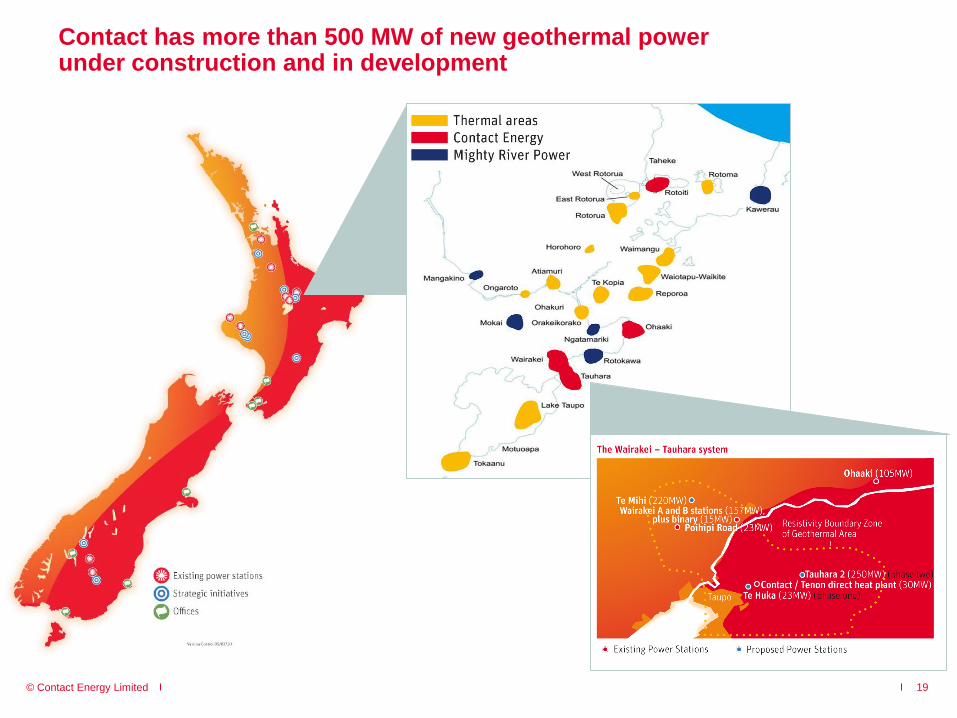

Contact has more than 500 MW of new geothermal power under construction and in development

© Contact Energy Limited

Gas, wind and hydro growth options

Gas

• Contact is currently seeking to consent an

option for a new set of 200 MW peakers

• 900 MW of consented development sites

Wind

• HMR (500 MW) – in development (consenting)

• Waitahora (156 MW) – in development (consenting)

Hydro

• Conceptual design and community engagement

underway for hydro options on the Upper and Lower

Clutha

• Development potential: 150 – 350 MW

20

© Contact Energy Limited 21

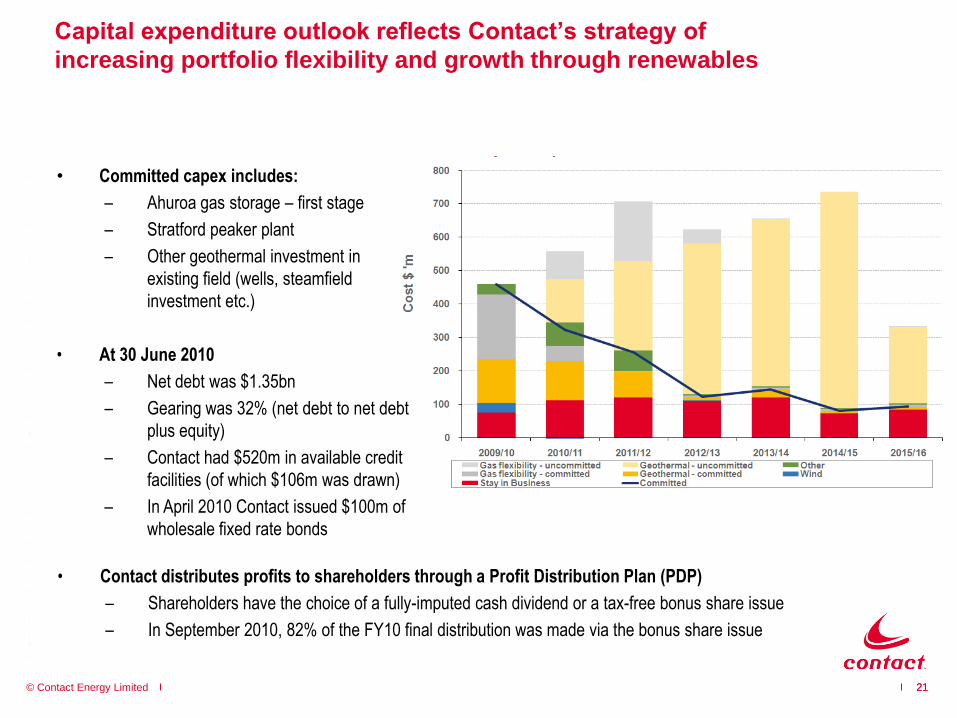

Capital expenditure outlook reflects Contact’s strategy of

increasing portfolio flexibility and growth through renewables

• Committed capex includes:

– Ahuroa gas storage – first stage

– Stratford peaker plant

– Other geothermal investment in

existing field (wells, steamfield

investment etc.)

• At 30 June 2010

– Net debt was $1.35bn

– Gearing was 32% (net debt to net debt

plus equity)

– Contact had $520m in available credit

facilities (of which $106m was drawn)

– In April 2010 Contact issued $100m of

wholesale fixed rate bonds

• Contact distributes profits to shareholders through a Profit Distribution Plan (PDP)

– Shareholders have the choice of a fully-imputed cash dividend or a tax-free bonus share issue

– In September 2010, 82% of the FY10 final distribution was made via the bonus share issue

21

© Contact Energy Limited

4. Financial Results Overview

22

© Contact Energy Limited 23

EBITDAF down $18m (4%) from FY09

Wet conditions for most of the year; retail competition intensified

• Retail electricity margins contracted from 5% to 2%

– Volumes and customer numbers maintained

– Sales revenue up $18m (2%)

– Network, energy and retail costs up $48m (4%)

• Unit generation costs up 5%

– 7% increase in underlying unit gas costs to $8.16/GJ

– High hydro inflows, increased renewables

– Gas storage helped mitigate consequential gas length

– Residual take-or-pay gas costs: $24m (added a further

0.84/GJ to effective gas costs)

– Contribution from exposed generation up $7m (higher

volume, lower average price)

• Other (wholesale and retail gas/LPG) contribution up

$7m

– Retail gas margins improved during the year

© Contact Energy Limited 24

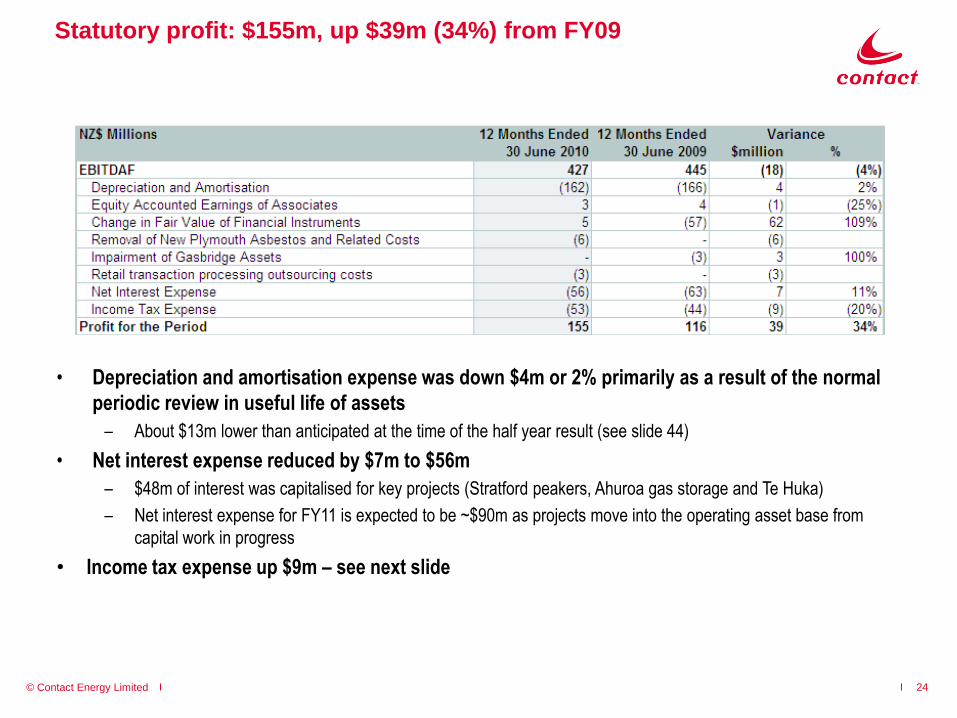

• Depreciation and amortisation expense was down $4m or 2% primarily as a result of the normal

periodic review in useful life of assets

– About $13m lower than anticipated at the time of the half year result (see slide 44)

• Net interest expense reduced by $7m to $56m

– $48m of interest was capitalised for key projects (Stratford peakers, Ahuroa gas storage and Te Huka)

– Net interest expense for FY11 is expected to be ~$90m as projects move into the operating asset base from

capital work in progress

• Income tax expense up $9m – see next slide

Statutory profit: $155m, up $39m (34%) from FY09

© Contact Energy Limited

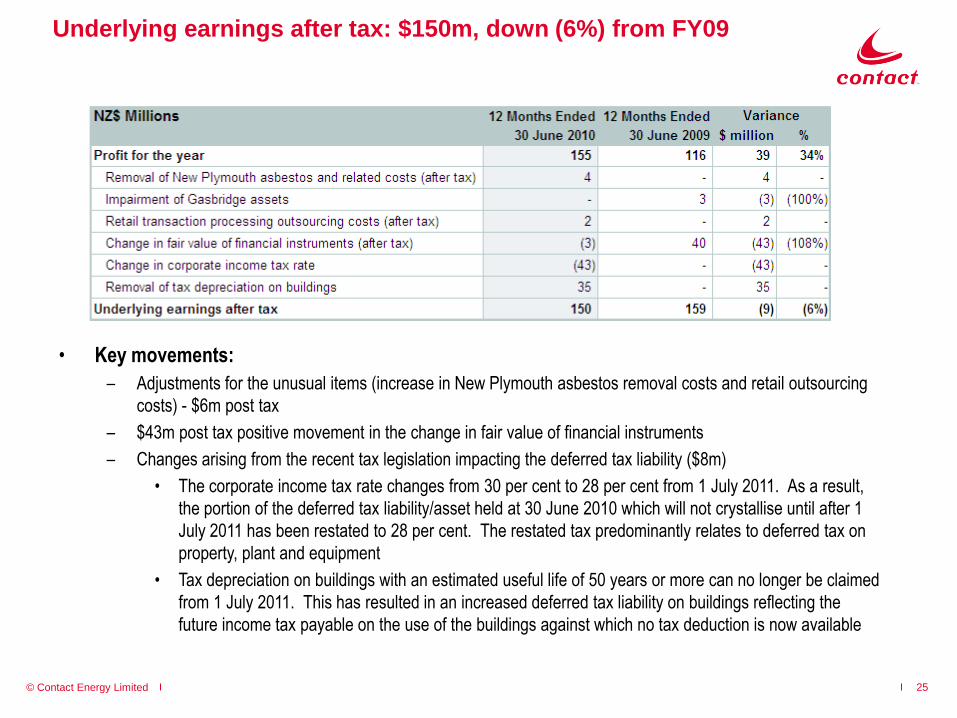

• Key movements:

– Adjustments for the unusual items (increase in New Plymouth asbestos removal costs and retail outsourcing

costs) - $6m post tax

– $43m post tax positive movement in the change in fair value of financial instruments

– Changes arising from the recent tax legislation impacting the deferred tax liability ($8m)

• The corporate income tax rate changes from 30 per cent to 28 per cent from 1 July 2011. As a result,

the portion of the deferred tax liability/asset held at 30 June 2010 which will not crystallise until after 1

July 2011 has been restated to 28 per cent. The restated tax predominantly relates to deferred tax on

property, plant and equipment

• Tax depreciation on buildings with an estimated useful life of 50 years or more can no longer be claimed

from 1 July 2011. This has resulted in an increased deferred tax liability on buildings reflecting the

future income tax payable on the use of the buildings against which no tax deduction is now available

25

Underlying earnings after tax: $150m, down (6%) from FY09

© Contact Energy Limited

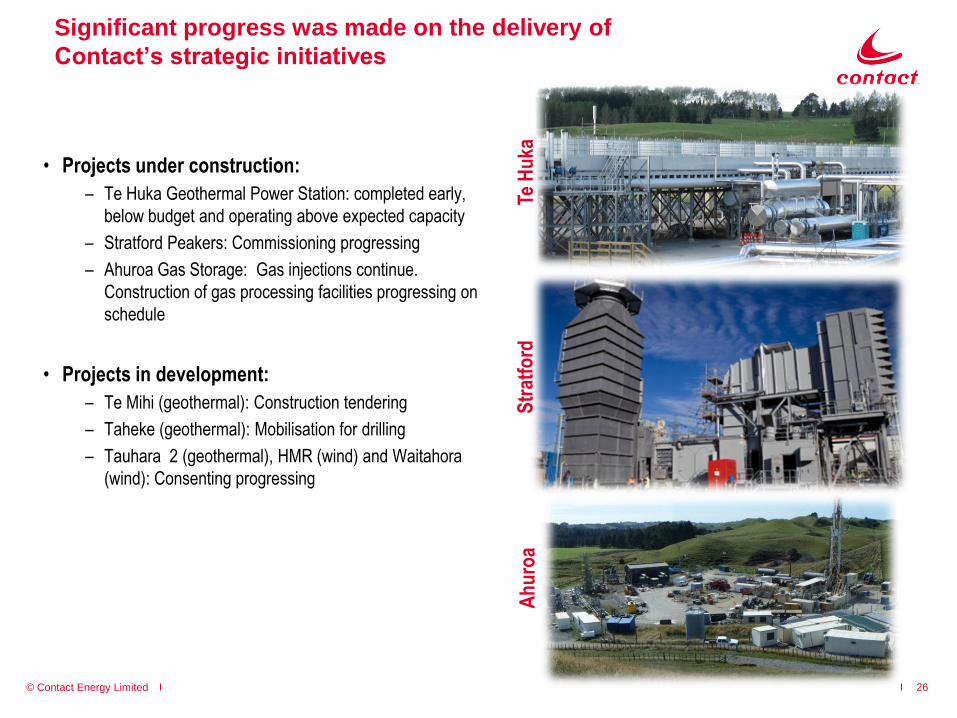

Significant progress was made on the delivery of

Contact’s strategic initiatives

• Projects under construction:

– Te Huka Geothermal Power Station: completed early,

below budget and operating above expected capacity

– Stratford Peakers: Commissioning progressing

– Ahuroa Gas Storage: Gas injections continue.

Construction of gas processing facilities progressing on

schedule

• Projects in development:

– Te Mihi (geothermal): Construction tendering

– Taheke (geothermal): Mobilisation for drilling

– Tauhara 2 (geothermal), HMR (wind) and Waitahora

(wind): Consenting progressing

Te H

uka

Str

atfo

rdA

hu

roa

26

© Contact Energy Limited

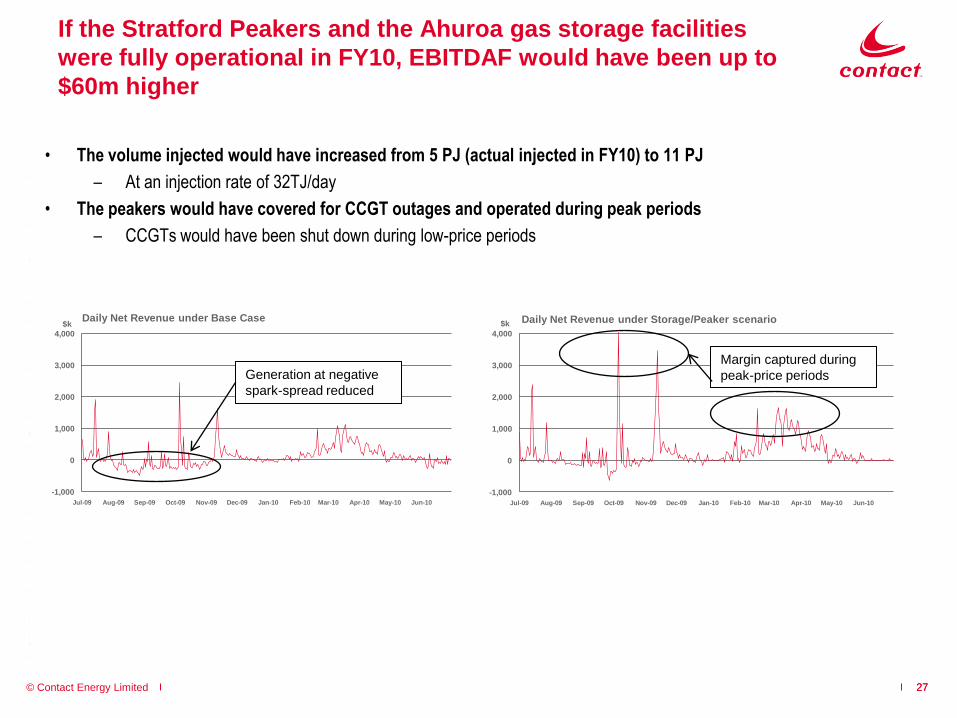

If the Stratford Peakers and the Ahuroa gas storage facilities

were fully operational in FY10, EBITDAF would have been up to

$60m higher

• The volume injected would have increased from 5 PJ (actual injected in FY10) to 11 PJ

– At an injection rate of 32TJ/day

• The peakers would have covered for CCGT outages and operated during peak periods

– CCGTs would have been shut down during low-price periods

-1,000

0

1,000

2,000

3,000

4,000

Jul-09 Aug-09 Sep-09 Oct-09 Nov-09 Dec-09 Jan-10 Feb-10 Mar-10 Apr-10 May-10 Jun-10

$kDaily Net Revenue under Base Case

Generation at negative

spark-spread reduced

-1,000

0

1,000

2,000

3,000

4,000

Jul-09 Aug-09 Sep-09 Oct-09 Nov-09 Dec-09 Jan-10 Feb-10 Mar-10 Apr-10 May-10 Jun-10

$k Daily Net Revenue under Storage/Peaker scenario

Margin captured during

peak-price periods

2727

© Contact Energy Limited

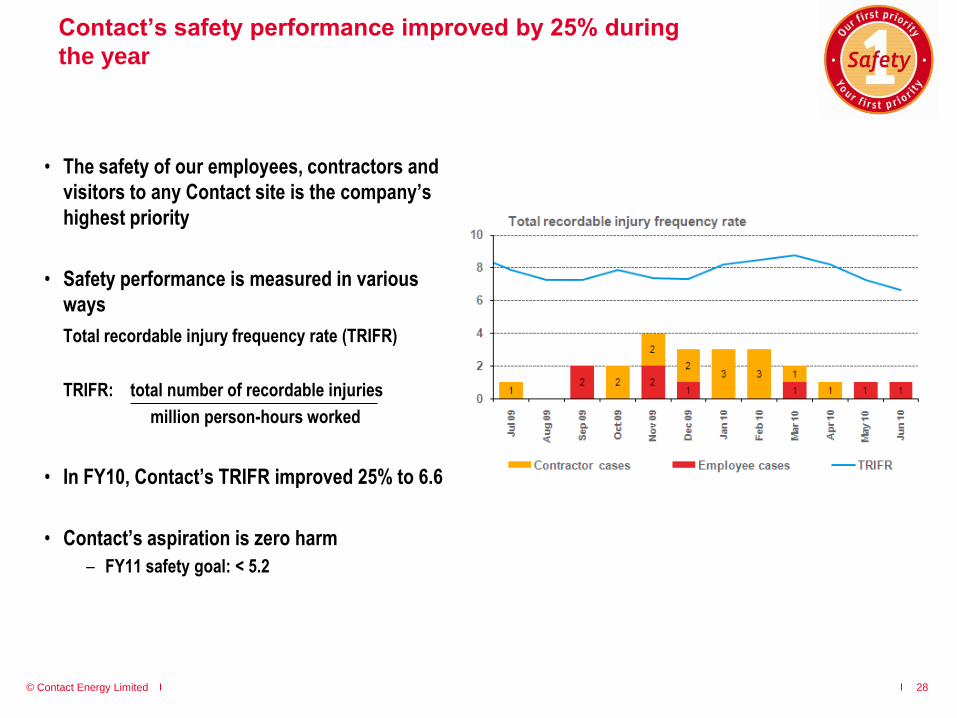

Contact’s safety performance improved by 25% during

the year

• The safety of our employees, contractors and

visitors to any Contact site is the company’s

highest priority

• Safety performance is measured in various

ways

Total recordable injury frequency rate (TRIFR)

TRIFR: total number of recordable injuries

million person-hours worked

• In FY10, Contact’s TRIFR improved 25% to 6.6

• Contact’s aspiration is zero harm

– FY11 safety goal: < 5.2

28

© Contact Energy Limited

5. Sector Information

29

© Contact Energy Limited

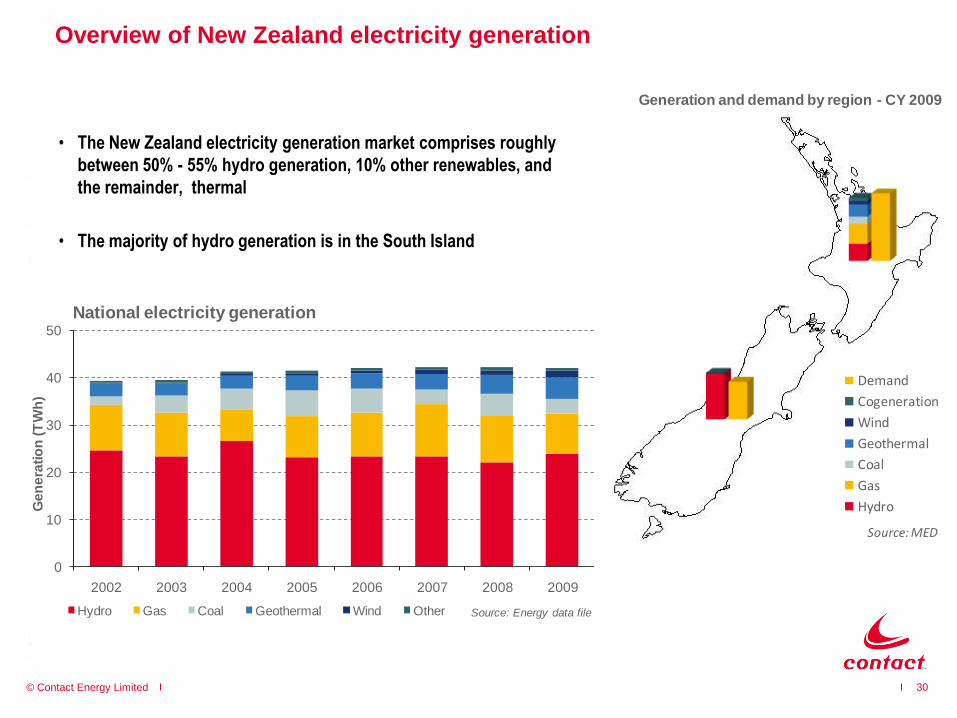

Overview of New Zealand electricity generation

• The New Zealand electricity generation market comprises roughly

between 50% - 55% hydro generation, 10% other renewables, and

the remainder, thermal

• The majority of hydro generation is in the South Island

30

0

10

20

30

40

50

2002 2003 2004 2005 2006 2007 2008 2009

Ge

ne

rati

on

(T

Wh

)

Source: Energy data file

National electricity generation

Hydro Gas Coal Geothermal Wind Other

Generation and demand by region - CY 2009

Demand

Cogeneration

Wind

Geothermal

Coal

Gas

Hydro

Source:MED

© Contact Energy Limited

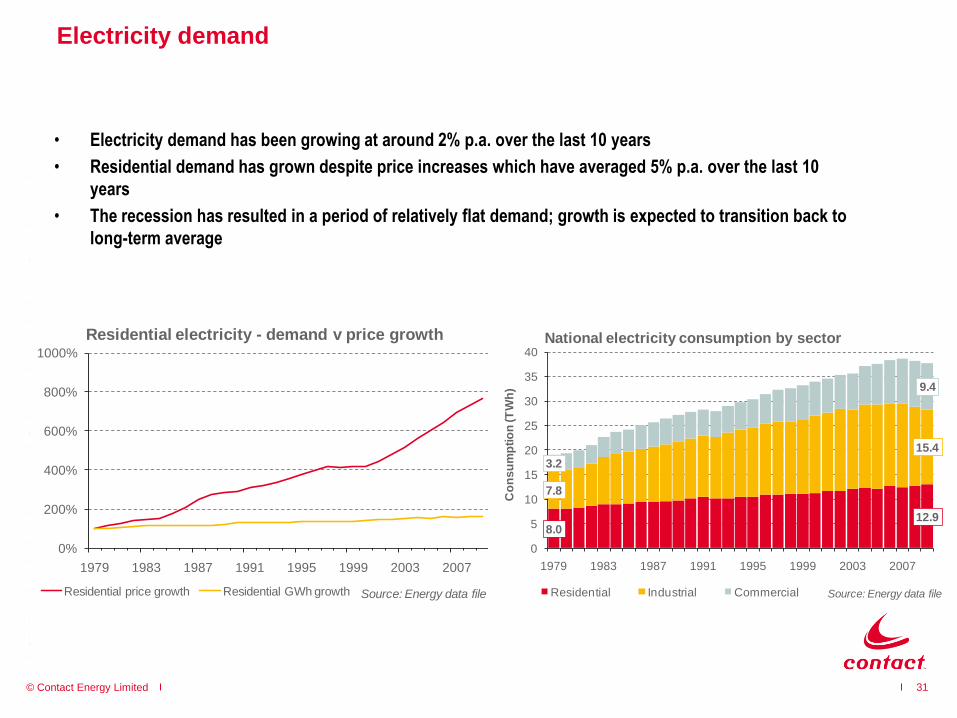

Electricity demand

• Electricity demand has been growing at around 2% p.a. over the last 10 years

• Residential demand has grown despite price increases which have averaged 5% p.a. over the last 10

years

• The recession has resulted in a period of relatively flat demand; growth is expected to transition back to

long-term average

31

8.0 12.9

7.8

15.4

3.2

9.4

0

5

10

15

20

25

30

35

40

1979 1983 1987 1991 1995 1999 2003 2007

Co

ns

um

pti

on

(T

Wh

)

Source: Energy data file

National electricity consumption by sector

Residential Industrial Commercial

0%

200%

400%

600%

800%

1000%

1979 1983 1987 1991 1995 1999 2003 2007

Source: Energy data file

Residential electricity - demand v price growth

Residential price growth Residential GWh growth

© Contact Energy Limited

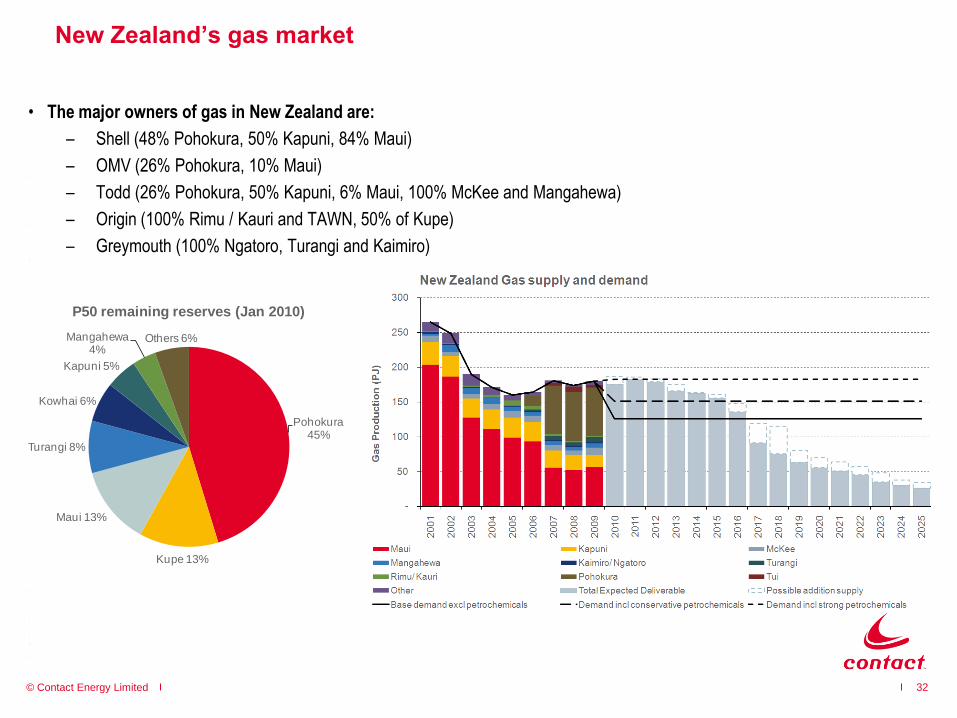

New Zealand’s gas market

• The major owners of gas in New Zealand are:

– Shell (48% Pohokura, 50% Kapuni, 84% Maui)

– OMV (26% Pohokura, 10% Maui)

– Todd (26% Pohokura, 50% Kapuni, 6% Maui, 100% McKee and Mangahewa)

– Origin (100% Rimu / Kauri and TAWN, 50% of Kupe)

– Greymouth (100% Ngatoro, Turangi and Kaimiro)

Source: Energy Data file, July 2010

32

Pohokura 45%

Kupe 13%

Maui 13%

Turangi 8%

Kowhai 6%

Kapuni 5%

Mangahewa 4%

Others 6%

P50 remaining reserves (Jan 2010)