J. K. Dietrich - FBE 524 - Fall, 2005 Measuring and Managing Interest Rate Risk Week 9 – October...

33

. Dietrich - FBE 524 - Fall, 2005 Measuring and Managing Interest Rate Risk Week 9 – October 19, 2005

-

date post

21-Dec-2015 -

Category

Documents

-

view

216 -

download

0

Transcript of J. K. Dietrich - FBE 524 - Fall, 2005 Measuring and Managing Interest Rate Risk Week 9 – October...

J. K. Dietrich - FBE 524 - Fall, 2005

Measuring and Managing Interest Rate Risk

Week 9 – October 19, 2005

J. K. Dietrich - FBE 524 - Fall, 2005

Interest rate risk

Future interest rates will affect value of all assets and liabilities, both real and financial assets and financial liabilities

No one knows future interest rates– Predictions of econometric models and the Lucas

critique– Supply and demand factors (e.g. bond calendar)

reflect expectations used in planning– Rational expectations and market rates

J. K. Dietrich - FBE 524 - Fall, 2005

Interest Rate Risk

Interest rates change constantly– Each element of rates change: real rate,

inflation premium, term premium, and risk premium

– Market participants have varying degrees of sensitivity to changes in components of rates

One way to view interest-rate risk is in terms of balance sheet risk

J. K. Dietrich - FBE 524 - Fall, 2005

Balance Sheet Risk

Real AssetsInventoriesEquipmentPlant Land

Financial AssetsReceivablesMoneyBondsStock

Financial LiabilitiesPayablesShort-term notesMortgagesBondsPreferred stock

Common Stock

Assets Liabilities and Equity

Incr

easi

ng

dura

tion

Incr

easi

ng

dura

tion

J. K. Dietrich - FBE 524 - Fall, 2005

Hedging Balance Sheet Risk

Hedging on balance sheet– Matching duration of assets and liabilities:

– Changing duration of assets and/or liabilities through swaps

– Floating rate securities with short re-pricing intervals have short durations

Hedging off balance sheet– Futures, forward contracts, and options

Weighted average asset duration = Weighted average liability duration

J. K. Dietrich - FBE 524 - Fall, 2005

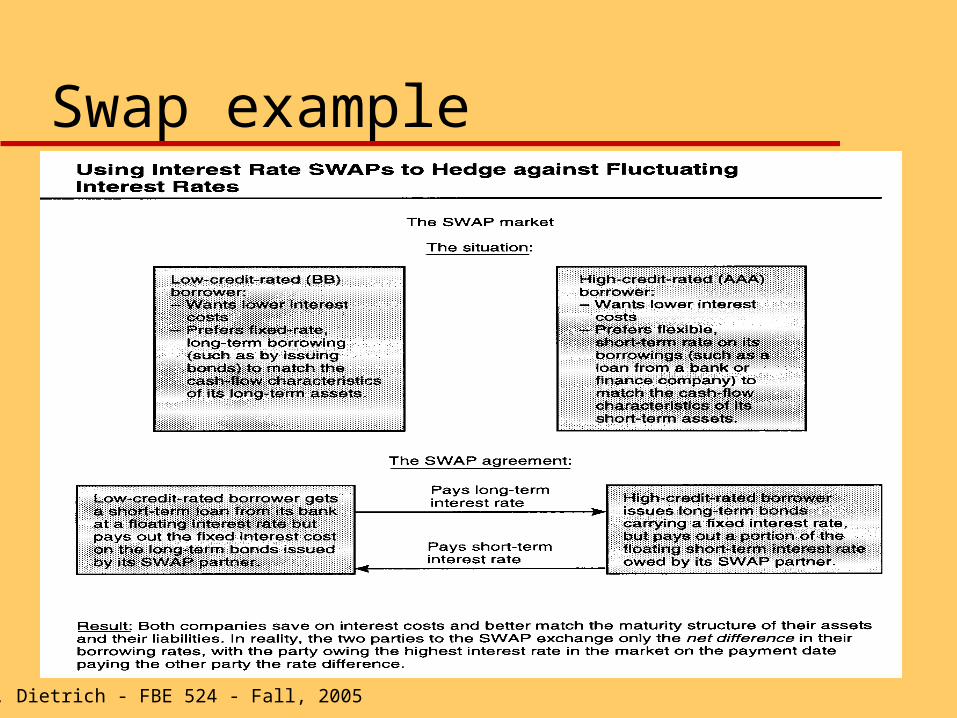

Swaps

Exchange of future cash flows based on movement of some asset or price– Interest rates– Exchange rates– Commodity prices or other contingencies

Swaps are all over-the-counter contracts Two contracting entities are called counter-parties Financial institution can take both sides

J. K. Dietrich - FBE 524 - Fall, 2005

Swap example

J. K. Dietrich - FBE 524 - Fall, 2005

Interest Rate Swap:Plain vanilla, [email protected]%

Company A(receive floating)

Company B(receive fixed)

Notional Amount$100 mm

$2.5mm$2.75mm

1/2 5% fixed

1/2 6-month LIBOR

J. K. Dietrich - FBE 524 - Fall, 2005

Definition of Derivatives Derivatives are contracts

– Commit parties to certain actions/payments in the future

– The payment/action depends on outcomes of pre-specified events in the future

In most cases, the major cash flow or costly action will or may occur in the future, not in the present

Contracts can be standardized or negotiated

J. K. Dietrich - FBE 524 - Fall, 2005

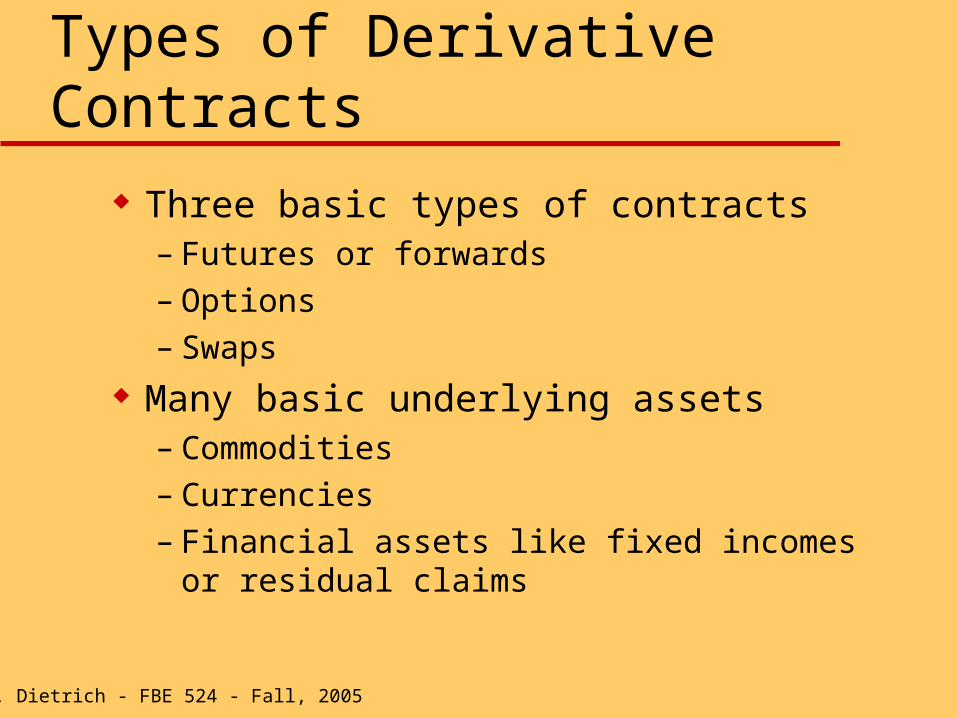

Types of Derivative Contracts

Three basic types of contracts– Futures or forwards– Options– Swaps

Many basic underlying assets– Commodities– Currencies– Financial assets like fixed incomes or residual claims

J. K. Dietrich - FBE 524 - Fall, 2005

Derivatives = Value Derived from Prices of Other Assets

Stock market or equity price, commodity price, exchange and interest rate derivatives

Swaps, forwards and futures, options, and swap-options (or swaptions)

Traded and over-the-counter derivatives Derivative are a zero-sum game Credit risk in derivatives is performance

risk, not notional value risk

J. K. Dietrich - FBE 524 - Fall, 2005

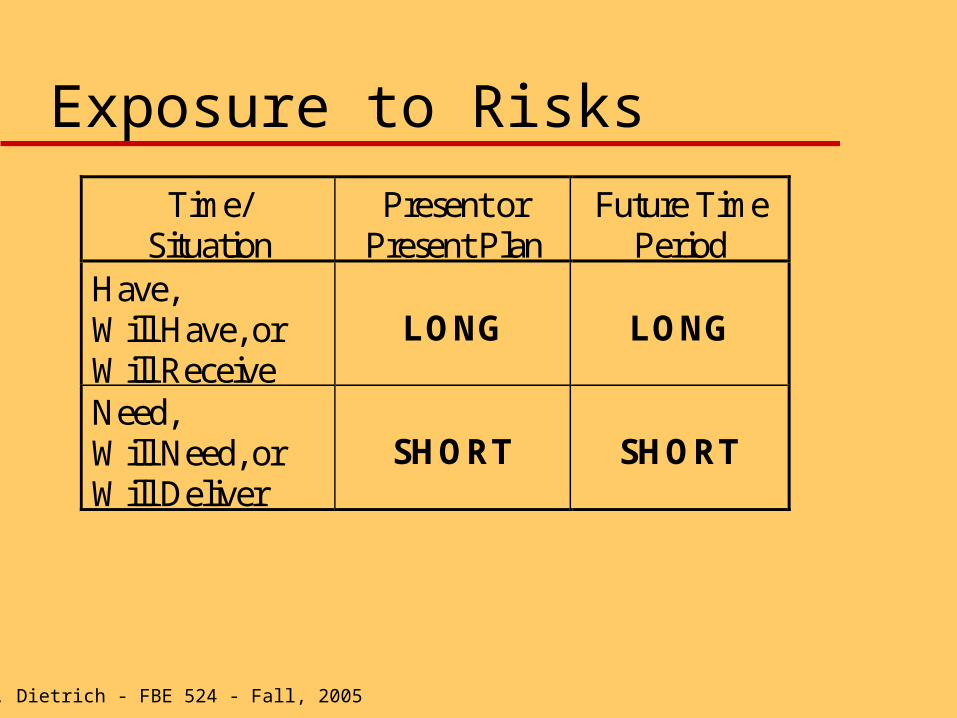

Exposure to Risk

A general term to describe a firm’s exposure to a particular risk (e.g. a commodity price) is to classify the exposure as long or short

Long exposure means that the firm will benefit from increases in prices or values

Short exposure means that the firm will benefit from decreases in prices or values

J. K. Dietrich - FBE 524 - Fall, 2005

Long Exposure

A firm (or individual) is long if at the time of the risk assessment if it has or will have an asset or commodity. As examples– The firm owns assets, as in inventories of raw

materials or finished goods– The firm produces a commodity or product, as

in an agribusiness raising wheat or livestock– The firm will take possession in the future or a

commodity or an asset– The firm has bought a commodity or asset

J. K. Dietrich - FBE 524 - Fall, 2005

Short Exposure A firm (or individual) is short if at the time

of the risk assessment if it needs or will need an asset or commodity. As examples– The firm is planning or has promised to deliver

raw materials or finished goods – The firm uses a commodity or product in

production as inputs, like steel or lumber– The firm will have possession in the future or a

commodity or an asset it does not need or needs to sell

– The firm has sold a commodity or asset and must deliver

J. K. Dietrich - FBE 524 - Fall, 2005

Exposure to Risks

Time/Situation

Present orPresent Plan

Future TimePeriod

Have,Will Have, orWill Receive

LONG LONG

Need,Will Need, orWill Deliver

SHORT SHORT

J. K. Dietrich - FBE 524 - Fall, 2005

Examples of Exposure

Farmer with wheat is long wheat Honey Baked Ham is short pork before

Easter selling season Treasurer with excess cash in three months is

short investments Company needing cash in nine months is

long financial assets (its liabilities are others’ assets) to sell

J. K. Dietrich - FBE 524 - Fall, 2005

Price Exposure in a Diagram

P0 P0

Long

Short

Profit

Loss

0 0

Profit

Loss

J. K. Dietrich - FBE 524 - Fall, 2005

Futures Contracts

Wall Street Journal tables Standardized contracts

– Quantity and quality– Delivery date– Last trading date– Deliverables

Clearing house is counter-party Margin requirements, mark to market

J. K. Dietrich - FBE 524 - Fall, 2005

Forward vs. Futures Contracts

Bilateral contract (usually with a financial firm as counter-party)

Terms are tailor made to needs of client, not standardized

No exchange of cash until maturity of contract

Over-the-counter market not as liquid as organized exchange

J. K. Dietrich - FBE 524 - Fall, 2005

Managing Risk with Futures

Offset price or interest rate risk with contract which moves in opposite direction

“Cross diagonally in the box” Identify contract with price or interest rate

which moves as close as possible with the price or interest rate exposure

Imperfect correlation is basis risk Not using futures or forwards can be speculation

J. K. Dietrich - FBE 524 - Fall, 2005

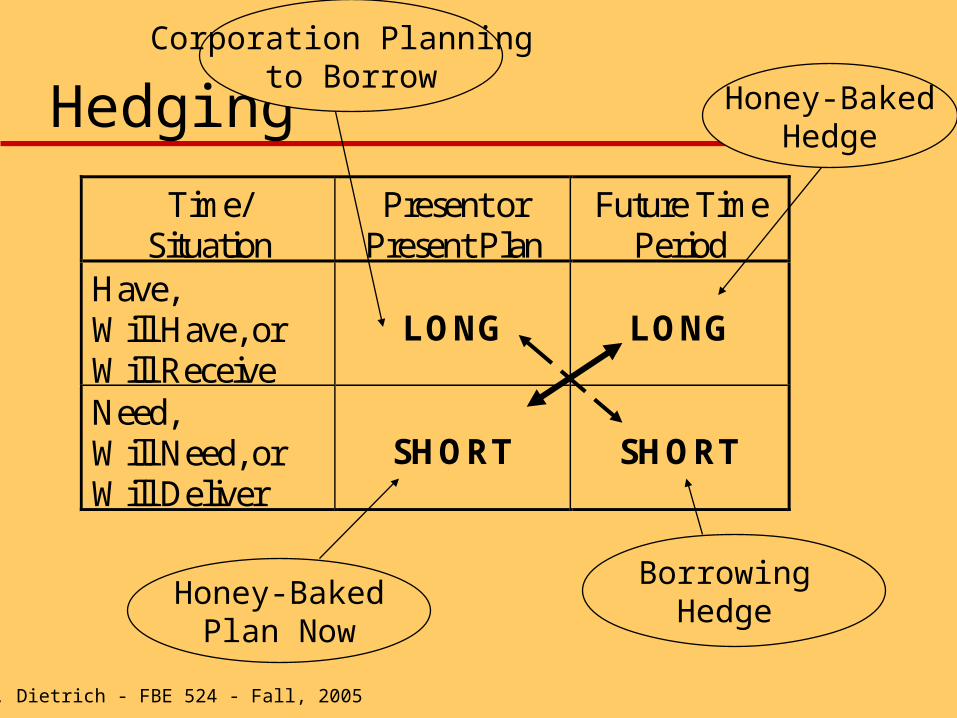

Hedging

Time/Situation

Present orPresent Plan

Future TimePeriod

Have,Will Have, orWill Receive

LONG LONG

Need,Will Need, orWill Deliver

SHORT SHORT

Honey-BakedPlan Now

Honey-BakedHedge

Corporation Planning to Borrow

Borrowing Hedge

J. K. Dietrich - FBE 524 - Fall, 2005

Options (Definition)

An option is the right (not the obligation) to buy or sell an asset at a fixed price before a given date– call is right to buy, put is right to sell– strike or exercise price is a fixed price which

determines conversion value– expiration date

Options on stocks, commodities, real estate, and future contracts

J. K. Dietrich - FBE 524 - Fall, 2005

Interpreting Option Quotationsin the Wall Street Journal

Listed option quotations versus “over-the-counter” options

Stock versus commodity Futures options versus asset options Strike/Expiration of Call/Put Volume, last, and open interest LEAPs and index options

J. K. Dietrich - FBE 524 - Fall, 2005

Call Options Profits at Maturity

0Strike Price

Profit

Asset Value

Payoffto Buyer

J. K. Dietrich - FBE 524 - Fall, 2005

Call Writer’s (Seller’s) Profits

0Strike Price

Profit

Loss

Asset Value

Possible Cost to Writer

J. K. Dietrich - FBE 524 - Fall, 2005

Option Value Sensitivityto Price Changes in Assets

Write Put Write Call

Buy Put Buy Call

S S

J. K. Dietrich - FBE 524 - Fall, 2005

Option Values

Conversion value = asset value - strike price Option premium = Option value - conversion

value Factors determining option premiums

» Time to maturity

» Asset value

» Strike price

» Volatility

» Interest rate

J. K. Dietrich - FBE 524 - Fall, 2005

Value of Call Options

0

Profit

Asset Value

OptionPremium

Strike Price

“Out of the Money”“At the Money”

“In the Money”

J. K. Dietrich - FBE 524 - Fall, 2005

Caps, floors, and collars

If a borrower has a loan commitment with a cap (maximum rate), this is the same as a put option on a note

If at the same time, a borrower commits to pay a floor or minimum rate, this is the same as writing a call

A collar is a cap and a floor

J. K. Dietrich - FBE 524 - Fall, 2005

Collars: Cap 6%, floor 4%

Profit

0

Loss

9400 9500 9600

J. K. Dietrich - FBE 524 - Fall, 2005

Replication Futures with Options

P0 P0

LongProfit

Loss

0 0

Profit

Loss

Buy Call

Write Put

J. K. Dietrich - FBE 524 - Fall, 2005

Other option developments

Credit risk options Casualty risk options Requirements for developing an option

– Interest– Calculable payoffs– Enforceable

J. K. Dietrich - FBE 524 - Fall, 2005

Next week: Oct. 26, 2005 Provide me with one-page description of

group project, including (1) problem to be addressed, (2) analytical framework to be used, and (3) data analysis and sources to be employed to address problem in (1)

Read Chapters 10 and 11 and review contents of Instruments of the Money Market